fostering competition in the brazilian financial sector · fostering competition in the brazilian...

TRANSCRIPT

Fostering competition in theBrazilian Financial Sector

Cleofas Salviano Junior

Central Bank of Brazil

April 2008Cemla-Banco de México Seminar

Financial Inclusion and Modernization in LA

Agenda

Overview of competition in Brazilian bankingResults of empirical researchRegulatory approach

Number of financial institutions -september 2007

134 multiple banks20 commercial banks17 investment banks289 broker/dealers53 finance companies1465 credit unions234 other financial institutions

80

120

160

200

240

280

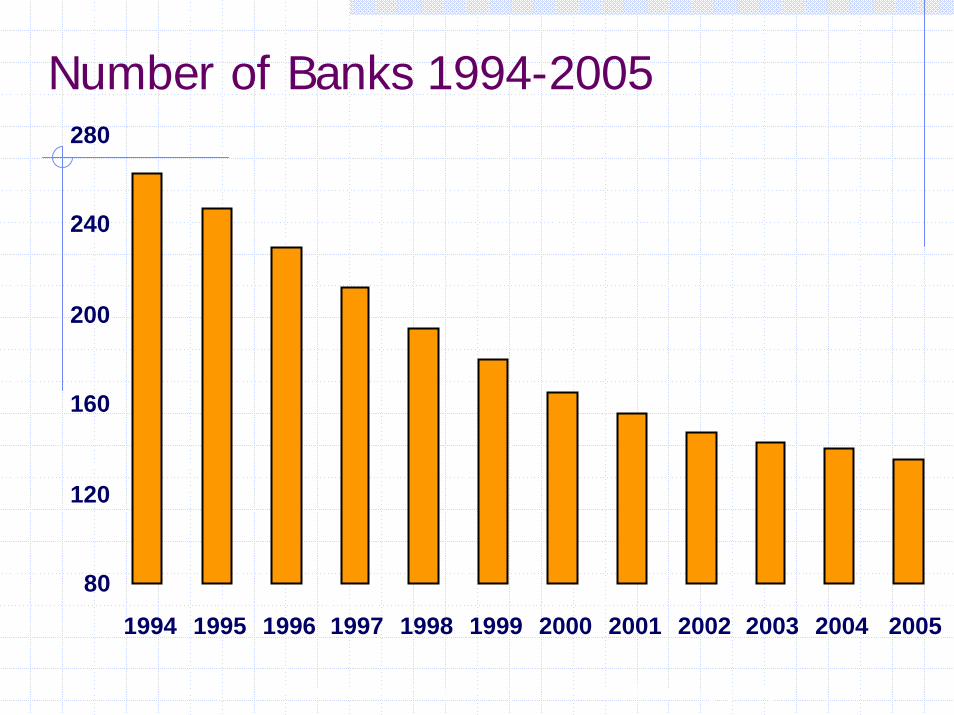

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Number of Banks 1994-2005

* Includes different banks of same banking group

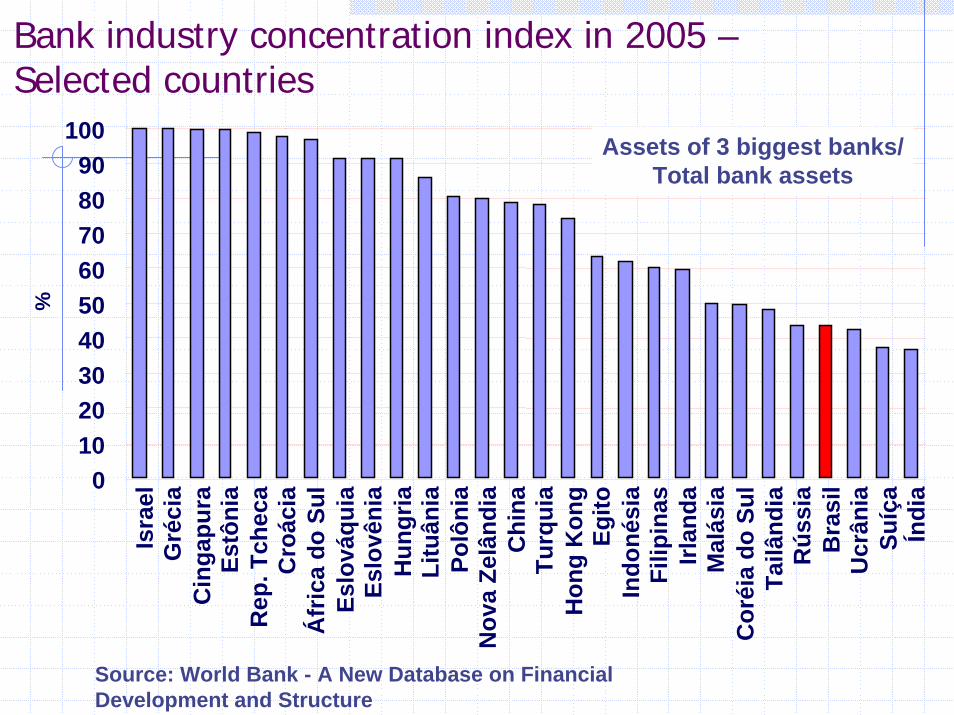

Bank industry concentration index in 2005 –Selected countries

%

0 10 20 30 40 50 60 70 80 90

100 Is

rael

Gré

cia

Cin

gapu

raEs

tôni

aR

ep. T

chec

aC

roác

iaÁ

fric

a do

Sul

Eslo

váqu

iaEs

lovê

nia

Hun

gria

Litu

ânia

Polô

nia

Nov

a Ze

lând

iaC

hina

Turq

uia

Hon

gK

ong

Egito

Indo

nési

aFi

lipin

asIrl

anda

Mal

ásia

Cor

éia

do S

ulTa

ilând

iaR

ússi

aB

rasi

lU

crân

iaSu

íça

Índi

a

Source: World Bank - A New Database on Financial Development and Structure

Assets of 3 biggest banks/Total bank assets

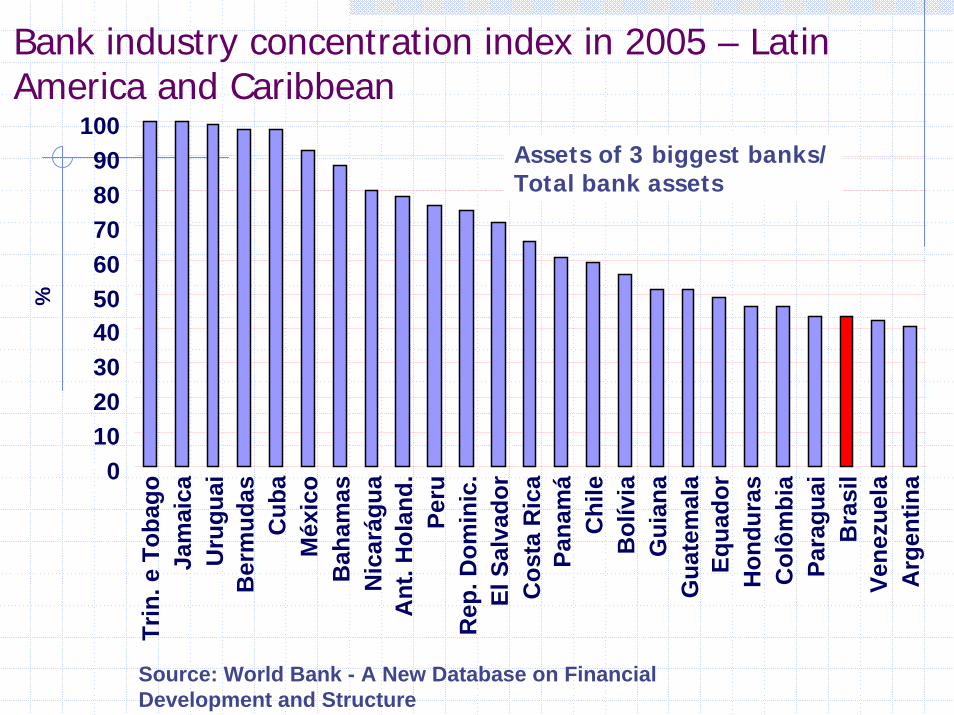

Bank industry concentration index in 2005 – LatinAmerica and Caribbean

%

0102030405060708090

100Tr

in. e

Tob

ago

Jam

aica

Uru

guai

Ber

mud

asC

uba

Méx

ico

Bah

amas

Nic

arág

uaA

nt. H

olan

d.Pe

ruR

ep. D

omin

ic.

El S

alva

dor

Cos

ta R

ica

Pana

má

Chi

leB

olív

iaG

uian

aG

uate

mal

aEq

uado

rH

ondu

ras

Col

ômbi

aPa

ragu

aiB

rasi

lVe

nezu

ela

Arg

entin

a

Source: World Bank - A New Database on Financial Development and Structure

Assets of 3 biggest banks/Total bank assets

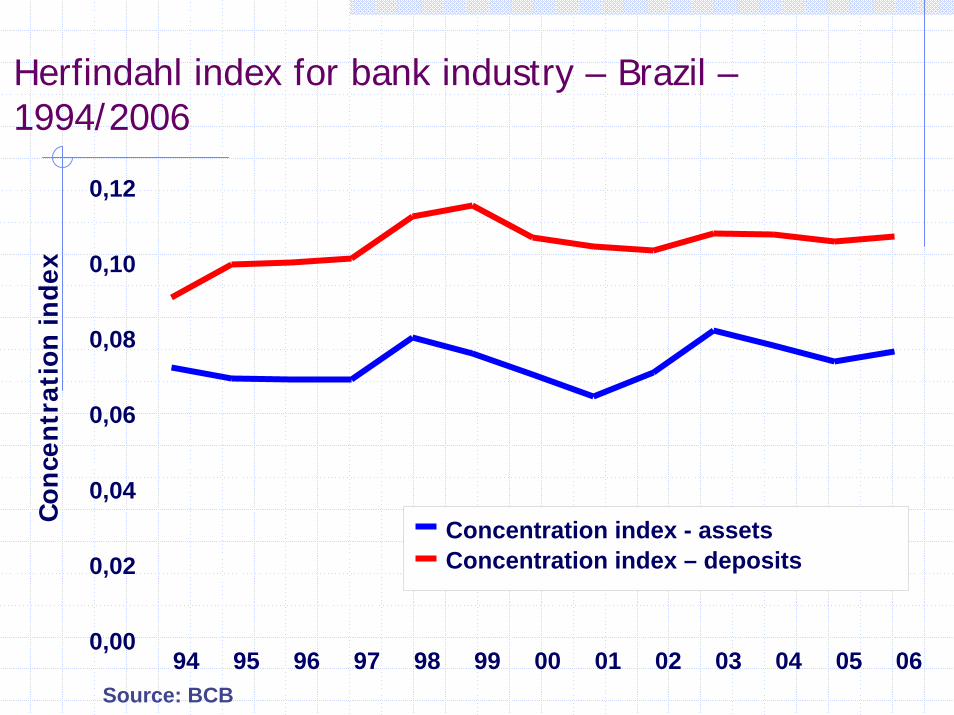

Herfindahl index for bank industry – Brazil –1994/2006

0,0094 95

0,02

0,04

0,06

0,08

0,10

0,12

96 97 98 99 00 01 02 03 04 05 06

Con

cen

trat

ion

inde

x

Concentration index - assetsConcentration index – deposits

Source: BCB

Spreads on non-directed loans – 2003-2008

Source: BCB

Companies

Natural persons

p.p.

p.p.

12

13

14

15

16

17

jan03

jan04

jan05

jan06

jan07

Feb08

30

36

42

48

54

60

Tests of market power

Traditional IO: without assimetry ofinformation.

Nakane (2002)Belaisch (2003)Petterini & Jorge Neto (2003)Nakane, Alencar & Kanczuk (2006)

Tests of market power

Conclusions:Cartel-colusion always rejectedPerfect competition almost alwaysrejectedMarket structure is imperfect but thereis a high degree of competition

Market failures

So market power is irrelevant in thebank sector? How to account for high spreads?Special features of financial sector:

Assimetric information/ InformationalRents;Service bundling;Switching costs;Moral hazard and adverse selection.

Consequences for regulation

Evidence suggests high spreads are notcaused by colusive behavior, but ratherto high switching costs and adverseselectionTherefore, measures like portability andcredit bureaux might be important

1 – Credit information system (SCR)

Created in 1997Explosures to each client above R$ 5,000

have to be informedAll financial institutions (except the very

small ones) should send informationAccess of banks to information on a

particular client must be authorized by theclientClient has direct access to her owninformation

2 - Portability

Portability of personal file information(Res. 2.835, of 30/5/2001)Loan portability (Res. 3.401, of6/9/2006)

3 - Increasing transparency

Banks required to disclose monthly interestrates and all other costs in loan contracts(Circular 2.936, of 14/10/1999)Banks required to disclose total effective costof loans (Res. 3.517, of 6/12/2007)Central Bank site on the internet: Rates, bankfees, ranking of complaintsRegulation of bank fees (Res. 3.518, of6/12/2007)Bank fees: standardized table of basic servicesfor natural persons (Circ. 3.371, of 6/12/2007)

4 - Stimulating competitors

Reduced restrictions to creationand operation of credit unions(Res. 3.442, de 28/2/2007)Entry of foreign banksIPOs of middle sized banks

4 - Geographic dimension of competition

Bank correspondents (Res. 3.110, of 31/7/2003)96.000 points of sale, compared to17.000 branchesAllows bank system to reach allmunicipalities

5 - Increasing asset liquidity

Loan sales and securitization:Res. 2.836/2001: Loan salesRes. 2907/2001: Loan investmentfunds (FDICs)Law 10.931/2004: “Loan bonds”(CCB)

6 - Licencing procedures for mergersand acquisitions

Definition of relevant marketsImpact on concentration indexesContestabilityEconomies of scale and scope

Conclusions

Research is still neededComplex problem Multiple approachRoom for improvementEspecially important for SMEs and the underbanked

Muchas gracias

Cleofas Salviano [email protected] advisorFinancial System Regulation DepartmentCentral Bank of Brazil