form 990 vs audited financials

DESCRIPTION

Presentation from Tate & Tyron - Washington DC CPA Firm - discussing the differences between the IRS Form 990 and the Audited Financial Statements.TRANSCRIPT

Presented by: Doug Boedeker, CPA, CMA, Partner Fred Longwood, CPA, Tax Manager

Form 990 vs. Audited Financials, Explaining Differences to the Board of Directors

Wednesday, August 29, 2012

Agenda

Why are we here?

What are the major differences between Form 990 and Audited Financial Statements (AFS) reporting?

How are the Form 990 and AFS similar?

Tips on presenting to Boards 1 www.tatetryon.com

Why are we here?

2 www.tatetryon.com

Boards are often confused because…

Many do not know that a 990 is even filed (& readily available to the public @ Guidestar.org)

Audited Financial Statements (AFS) and the 990 are viewed as part of the same process.

990 is just similar enough to the AFS to appear “the same.”

3 www.tatetryon.com

The point of the AFS

Primary audience is Audit Committee, Board, and third-party users.

Attempts to present an entity’s economic reality at a point in time.

Complete managerial transparency is not really the goal.

Uses GAAP as the reporting framework.

4 www.tatetryon.com

The point of the 990

Primary audience is third-party users – even those without any economic interest in the entity!

Serves as a tax-compliance check-up to alert the IRS to potential problems.

Transparency regarding basic governance practices and transactions with interested parties is a key focus.

Uses a unique blend of GAAP and tax-basis accounting as the reporting framework.

5 www.tatetryon.com

Major Reporting Differences

6 www.tatetryon.com

Investment Reporting – the big one!

GAAP mandates that investments be reported at fair value with the corresponding unrealized gain/loss reflected in “net income.”

990 follows basic tax accounting – unrealized investment gains/losses are not reflected in “net income.”

However, total net assets per AFS and 990 generally agree. This causes confusion at first glance.

7 www.tatetryon.com

Investment Reporting – the big one!

Example of the resulting confusion:

Notice how the “Revenue less expenses” on line 19 does not equal the actual “Change in net assets” on line 22.

8 www.tatetryon.com

In-kind Services – a common hassle!

Fundamental difference between GAAP accounting and tax accounting.

Under GAAP’s economic reality presentation, in-kind services are no different from any other type of contribution. (Subject to certain criteria.)

Tax accounting precludes including in-kind services in an entity’s revenue and expense.

Well-designed Charts of Accounts are helpful. 9 www.tatetryon.com

In-kind Services – a common hassle!

A quick refresher on GAAP’s recording criteria:

Contributions of services shall be recognized if the services received meet any of the following criteria: a. They create or enhance nonfinancial assets. b. They require specialized skills, are provided by individuals possessing

those skills, and would typically need to be purchased if not provided by donation. (Services requiring specialized skills are provided by accountants, architects, carpenters, doctors, electricians, lawyers, nurses, plumbers, teachers, and other professionals and craftsmen.)

Contributed services and promises to give services that do not meet these criteria shall not be recognized.

(FASB ASC 958-605-25-16)

10 www.tatetryon.com

In-kind Services – a common hassle!

Why does the IRS exclude contributed services? Concern over valuation?

Could contributed services skew program vs. supporting

service expense ratios?

Would contributed services muddy the calculation of “gross receipts”?

Would contributed services make the tedious Schedule A support tests even more painful?

11 www.tatetryon.com

When is “Grant” revenue recognized?

This causes headaches for support test calculations and also for fund raising ratios.

Auditors often look at grants differently from tax accountants.

A wonderfully gray area leading to scintillating debates!

12 www.tatetryon.com

When is “Grant” revenue recognized?

GAAP states that “unconditional” promises to give should be recognized as temporarily restricted revenue during the period the promise is made.

However, many auditors take the position that a grant agreement containing performance milestones is not a truly “unconditional” promise to give.

As a result, grant revenue may actually be recognized over time as benchmarks are met.

13 www.tatetryon.com

When is “Grant” revenue recognized?

To cause further confusion, there may be some debate as to which line of Form 990, Part VIII should be used to record the grant revenue.

This comes up most commonly with Government awards even though GAAP explicitly says the analysis should be the same

Is it a “Contribution” or an “Exchange” transaction? When is benefit “reciprocal” vs. primarily to charitable

beneficiary? 14 www.tatetryon.com

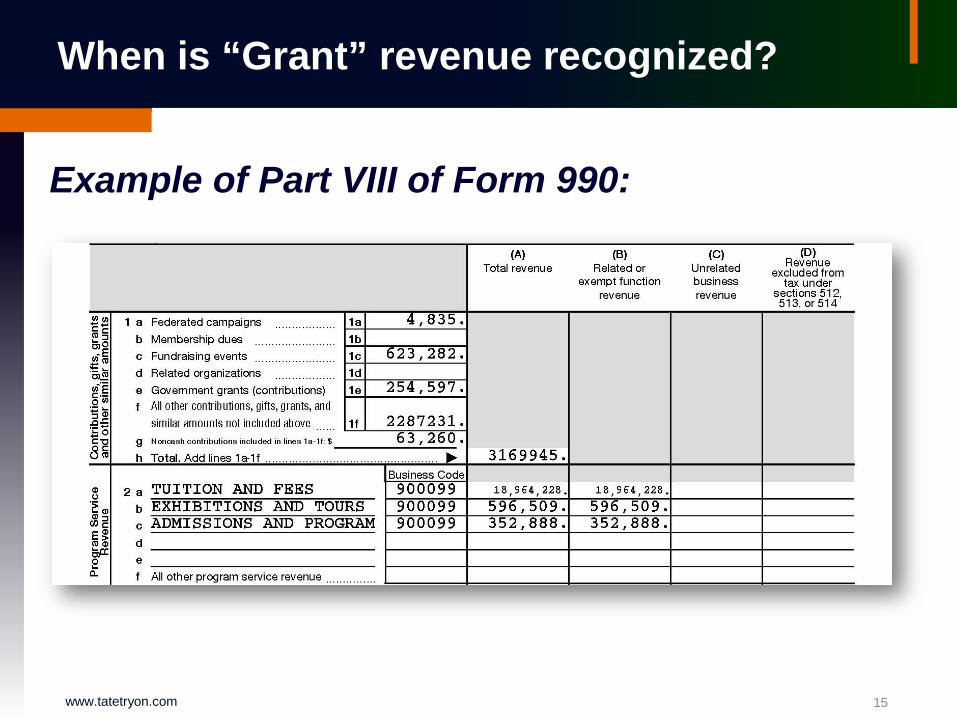

When is “Grant” revenue recognized?

Example of Part VIII of Form 990:

15 www.tatetryon.com

When is “Grant” revenue recognized?

Form 990 instructions state that a “contribution”:

“….includes donations, gifts, bequests, grants,

and other transfers of money or property to the extent that adequate consideration is not provided in exchange and that the contributor intends to make a gift, whether or not made for charitable purposes. A transaction can be partly a sale and partly a contribution.”

16 www.tatetryon.com

When is “Grant” revenue recognized?

The revenue recognition and classification is important for Schedule A and donor perceptions.

“Exchange” transactions have a different, usually less favorable, impact on a charity’s public support test.

Fund raising expenses incurred to obtain the grant may be recognized by AFS in a different period from the revenue – this can make fund raising costs appear high. (990 provides some wiggle room.)

17 www.tatetryon.com

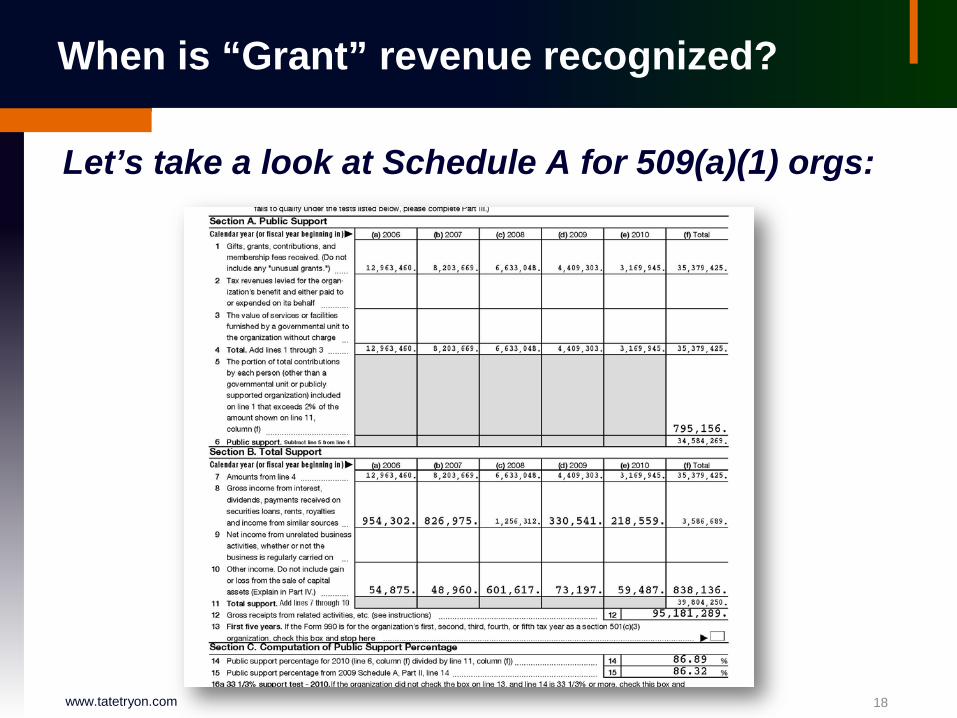

When is “Grant” revenue recognized?

Let’s take a look at Schedule A for 509(a)(1) orgs:

18 www.tatetryon.com

When is “Grant” revenue recognized?

Let’s take a look at Schedule A for 509(a)(2) orgs:

19 www.tatetryon.com

“Gross” vs. “Net” Reporting – Ugh!

GAAP generally takes a very dim view of reporting revenues and expenses at net.

The 990 stipulates that certain items should be presented at net.

As a result, total revenue and expense shown on the 990 and the AFS will often be different.

20 www.tatetryon.com

“Gross” vs. “Net” Reporting – Ugh!

The reporting of fund raising events seems to be the most painful.

First, the 990 wants the “contribution” component of the funds generated shown separately from the event’s “earned” revenue.

Second, the 990 wants direct expenses related to the event netted against the direct revenues.

Most AFS don’t show things this way!

21 www.tatetryon.com

“Gross” vs. “Net” Reporting – Ugh!

Other items for which the 990 mandates “net” reporting are:

Rental income & expense

Sales of securities & “other” assets

Sales of inventory

Gaming revenue

22 www.tatetryon.com

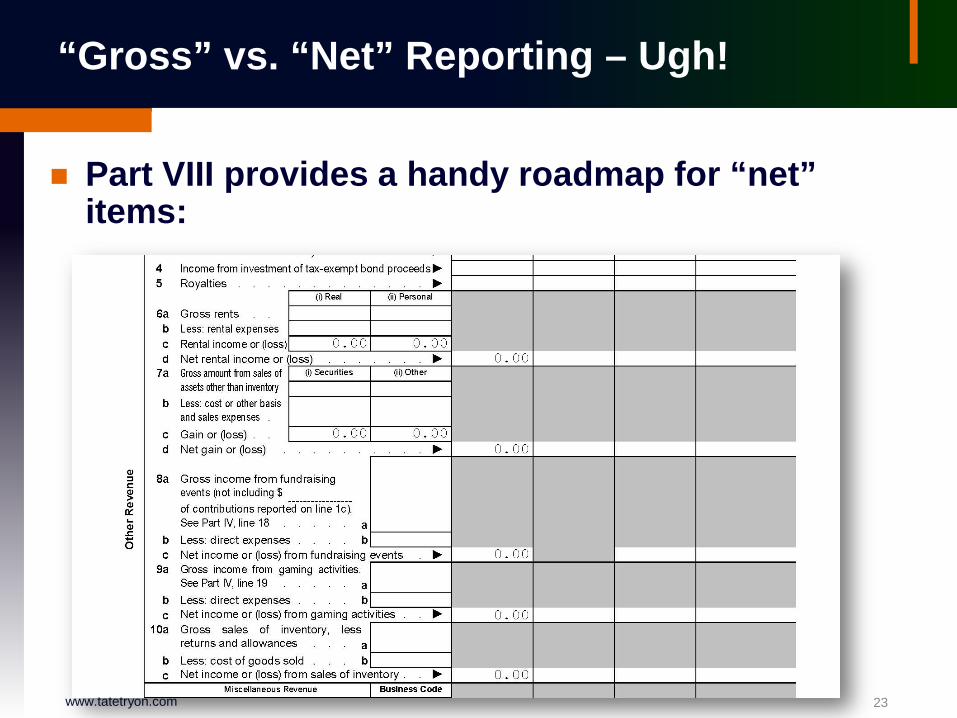

“Gross” vs. “Net” Reporting – Ugh!

Part VIII provides a handy roadmap for “net” items:

23 www.tatetryon.com

“Gross” vs. “Net” Reporting – Ugh!

Investment management fees – the exception that proves the rule!

For audit purposes, many entities show investment income net of management fees.

However, the 990 mandates the reporting of investment management fees as an expense and reporting investment income at “gross.”

24 www.tatetryon.com

Compensation Reporting – the juicy stuff!

Problem #1 – compensation details reported on a calendar year basis. Big-time confusion for fiscal year-end entities!

Same deal as #1 above for reporting independent contractor payments.

The Form 990’s definition of “compensation” may not be intuitive to all Board members.

25 www.tatetryon.com

Compensation Reporting – the juicy stuff!

Lines 5 and 6 of Part IX can be a big headache….

26 www.tatetryon.com

Compensation Reporting – the juicy stuff!

Explaining the reporting of deferred compensation plans is a real treat.

990 requires reporting deferred compensation “earned” during the period as a component of an individual’s total compensation package. (This includes increases or decreases in the actuarial value of defined benefit plans.)

For AFS purposes, the accrual of deferred compensation plan expenses can be a gray area and lead to differences with the 990. 27 www.tatetryon.com

Compensation Reporting – the juicy stuff!

Quote from Schedule J instructions….

“Enter in column (F) any payment reported in this year’s column (B) to the extent such payment was already reported as deferred compensation to the listed person in a prior Form 990.., for this purpose, the amount must have been reported as compensation specifically for the listed person on the prior form.”

Surprising that Board members get confused?

28 www.tatetryon.com

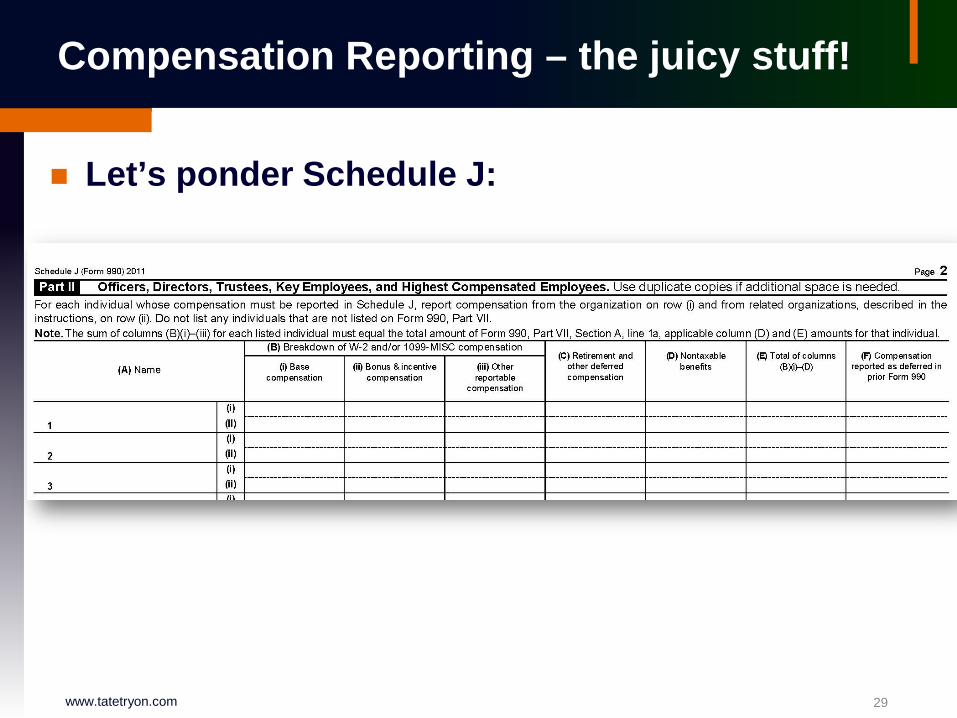

Compensation Reporting – the juicy stuff!

Let’s ponder Schedule J:

29 www.tatetryon.com

Other Bits and Pieces

The 990 reporting for financial statement restatements was quite clunky – it has gotten better with the introduction of Part XI to the core form:

30 www.tatetryon.com

Other Bits and Pieces

Consolidated vs. Separate Entity reporting for AFS and 990 causes more confusion than you’d think.

Schedule R is a good memory jogger for Board members regarding what entities exist and how they relate to each other.

31 www.tatetryon.com

Other Bits and Pieces

Here’s page one of Schedule R

32 www.tatetryon.com

There’s hope - Schedule D is our friend!

33 www.tatetryon.com

How are the documents similar?

34 www.tatetryon.com

How are the documents similar?

The 990 uses a mix of GAAP & tax accounting, so GAAP is the fundamental building block for the 990.

Functional expense allocations for joint activities (the standard formerly known as SOP 98-2) are usually the same between the AFS and 990.

Endowment reporting required on Schedule D usually mirrors the data from the AFS footnote.

The balance sheet usually ties nicely between AFS

and 990. 35 www.tatetryon.com

Presenting the 990 and AFS to a Board.

36 www.tatetryon.com

(Handy tip – be sure the Board gets these documents before the meeting!)

37 www.tatetryon.com

Presenting the AFS

Start with the “Required Communications Letter” (RCL) first. This often takes the suspense out of the room. Covers major changes in accounting principles Covers highly subjective or “soft” financial statement

values Covers major footnotes to the AFS

Move next to the “Management Letter” (ML). Internal control is what Boards really want to talk about! 38 www.tatetryon.com

Presenting the AFS

After the RCL and ML, most of the big issues should be dealt with.

Cover the auditor’s opinion.

Make sure Board understands the flow of restricted activities on the Statement of Financial Position and Statement of Activities.

Hit any other truly odd recording/presentational items.

39 www.tatetryon.com

Presenting the 990

Most Boards are interested in a 30,000 foot overview of the Form 990 – not necessarily a page by page review of the Form

Make certain the pages of the Form 990 are numbered!

Generally, it is best to cover the highlights of the Form, which include the following: Governance, Management, and Disclosure – Part VI Compensation – Part VII (and Schedule J, if applicable) Schedule O –Supplemental Information Schedule L – Transactions with Interested Persons (if

applicable)

40 www.tatetryon.com

Presenting the 990

Section 501 (c)(3) organizations are mostly interested in: Statement of Program Services – Part III Statement of Functional Expenses – Part IX Schedule A – Public Charity Status and Public Support Schedule D Part V – Endowment Funds

Section 501 (c)(6) organizations are mostly

interested in: Schedule C – Political Campaign and Lobbying Activities Schedule R – Related Organizations

41 www.tatetryon.com

Presenting the 990

If there are any heartburn-inducing answers to tax compliance questions on Part V, or Governance disclosures in Part VI, be ready to talk about them!

Plan ahead to explain differences in total income and total expense: Provide a tailored overview of how Part XI of

Schedule D navigates from the 990 to the AFS.

42 www.tatetryon.com

Thank you for your time!

43 www.tatetryon.com

Speaker Biography

Douglas Boedeker, is a partner within Tate & Tryon’s Audit and Assurance Services unit and is also actively involved in the Firm's exempt organization tax services group. He has 20 years of experience providing an array of audit, tax, and consulting services to a variety of nonprofit organizations and employee benefit plans. He takes particular pride that his family has contained at least one CPA every year since 1923. Doug graduated summa cum laude from Susquehanna University in Selinsgrove, Pennsylvania with a Bachelor of Science degree in accounting while simultaneously completing the coursework for a second major in arts administration. Doug is a frequent speaker on a variety of exempt organization tax issues and the Form 990. He recently presented a session on easing the 990 preparation process for CFOs and auditors at the 2011 AICPA Not for Profit Industry Conference. Doug is a coauthor to Guide to the Newest IRS Form 990: Interpreting and Complying with the New Tax Reporting Requirements for Transparency and Accountability, (published by ASAE).

Doug Boedeker, CPA, CMA Audit Partner Tate & Tryon Direct: 202-419-5106 [email protected]

44 www.tatetryon.com

Speaker Biography

Fred Longwood is a manager in the Firm's Exempt Organization Tax Department with over 15 years of experience working with a broad range of tax-exempt organizations including research and educational organizations, public charities, civic leagues, membership organizations, and private foundations. Mr. Longwood has advised exempt organizations on a variety of issues including Taxation of employee benefit plans, intermediate sanctions, unrelated business income tax, and taxable subsidiaries. In addition to his exempt organization advisory and compliance experience, Mr. Longwood participated in the "Preparing for the new Form 990," Tate & Tryon client seminar series held October 2008 and March 2009 highlighting the changes to the Form 990 and was also a coauthor of the "Guide to the Newest IRS Form 990: Interpreting and Complying with the New Tax Reporting Requirements for Transparency and Accountability," (published by ASAE). Fred is a member of the American Institute of CPAs (AICPA) and the Greater Washington Society of CPAs (GWSCPA).

Fred Longwood, CPA Tax Manager Tate & Tryon Direct: 202-419-5116 [email protected]

45 www.tatetryon.com