foreign account tax compliance act (fatca) workshop ... · foreign account tax compliance act...

TRANSCRIPT

Foreign Account Tax

Compliance Act

(FATCA) Workshop,

Bucharest

László Winkler - Director, Deloitte Hungary

Enikő Takács - Manager, Deloitte Hungary

March 11, 2014

The path forward

Foreign Account Tax Compliance Act (FATCA) Workshop

General introduction and overview of FATCA

• Aim and general concept of FATCA

• Latest legislative developments and current status of FATCA in Europe and

Central Europe

• Intergovernmental Agreement (IGA) – issues, practical considerations

• OECD’s Model of Competent Authority Agreement and Common Reporting

Standard Model

FATCA requirements and practical issues

• Requirements for financial institutions regarding FATCA compliance

• Challenges and practical experiences with FATCA impact assessment/

implementation

Agenda

© 2014 Deloitte Hungary

Aim and general

concept of FATCA

3 Foreign Account Tax Compliance Act (FATCA) Workshop © 2014 Deloitte Hungary

What does FATCA involve?

• Foreign Financial Institutions (FFIs) are required to enter agreements with U.S.

Treasury to identify and report U.S. accounts annually

• Unless otherwise provided, an account shall be treated as a US account

• Sanction: U.S. withholding agents are required to withhold 30% of withholdable

payments made to recalcitrant account holders, non-participating FFIs or their clients

• Foreign Financial Institutions (FFI)

• US Withholding Agents

• US individuals

• US entities

• Non-US Financial Entities with substantial US ownership

Who must meet the FATCA requirements?

Who are the targets?

FATCA aims to identify US persons trying to avoid

US tax obligations by holding assets in non-US

structures and products

© 2014 Deloitte Hungary 4 Foreign Account Tax Compliance Act (FATCA) Workshop

• Proposed regulations were released in February 2012

• Final regulations were released on January 17, 2013

• The IRS has released Notice 2013-43 extending most of the FATCA deadlines by 6

months

• FFI Registration Portal opened on August 19, 2013

• Notice 2013-69 (FFI Agreement) in October, 2013

• The U.S. Department of Treasury and the Internal Revenue Service released temporary

regulations that revise and clarify the final FATCA regulations on February 20, 2014

• The U.S. Department of Treasury and the Internal Revenue Service released

Coordination Regulations on the FATCA on February 20, 2014

FATCA – Regulatory update

© 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop 5

Evolution of internal FATCA Regulations

• In July 2012 the Model 1 Intergovernmental Agreement (IGA) was released, in

November 2012 the Model 2 IGA was released

• Over 60 countries around the globe are negotiating Model 1 and Model 2 IGAs with the

U.S. government

• The U.S. has now entered into a Model 1 IGA with Denmark, Ireland, United Kingdom,

Germany, Norway, Spain, France, Jersey, Guernsey, Isle of Man, Netherlands, Malta,

Italy, Hungary and Finland, and into Model 2 IGA with Switzerland

• Annex 2 of Model 1 IGA released on May 9, 2013

• Announcement regarding the registration deadline for Model1 FFIs was issued on

January, 2014

FATCA – Regulatory update

Development of IGA framework

6 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Intergovernmental Agreement (IGA)

7 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

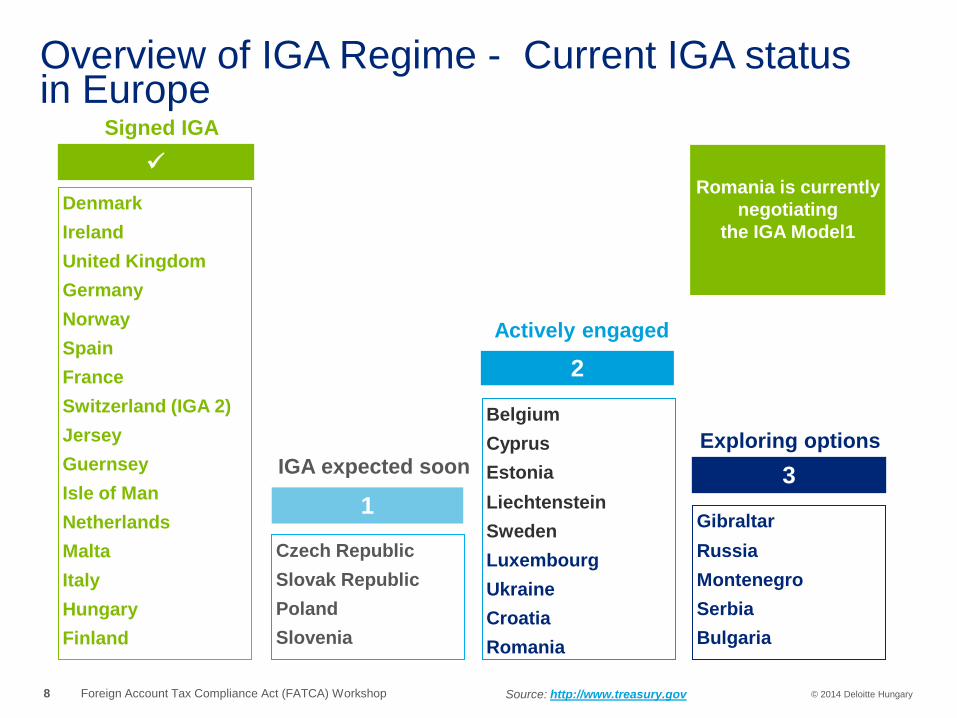

Overview of IGA Regime - Current IGA status in Europe

Source: http://www.treasury.gov

Gibraltar

Russia

Montenegro

Serbia

Bulgaria

1

2

3

Denmark

Ireland

United Kingdom

Germany

Norway

Spain

France

Switzerland (IGA 2)

Jersey

Guernsey

Isle of Man

Netherlands

Malta

Italy

Hungary

Finland

Czech Republic

Slovak Republic

Poland

Slovenia

Belgium

Cyprus

Estonia

Liechtenstein

Sweden

Luxembourg

Ukraine

Croatia

Romania

Signed IGA

IGA expected soon

Actively engaged

Exploring options

© 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Romania is currently

negotiating

the IGA Model1

8

Romania – The IGA is currently under negotiation.

Bulgaria - US Treasury has decided not to conclude the Model 1A IGA (reciprocal) with

Bulgaria. They offered Bulgaria to join FATCA under the IGA Model 1B or IGA Model 2.

Czech Republic – IGA is expected to be signed soon.

Croatia - Convention on Mutual Administrative Assistance in Tax Matters was signed in

October 2013, they are in the negations process.

Hungary - IGA was signed in February, 2014.

Montenegro - they intend to enter into an IGA latest by June 2014.

Poland - IGA is expected to be signed in the coming months.

Slovakia - IGA is expected to be signed in the coming weeks.

Slovenia - The U.S. and Slovenia initialed the IGA in January, 2014.

Serbia - the Ministry of Finance intends to enter into an IGA latest by June 2014.

9 © 2014 Deloitte Hungary

Overview of IGA Status in Central Europe

Foreign Account Tax Compliance Act (FATCA) Workshop

Overview of IGA Regime Conceptual differences in IGA 1A vs. FATCA Regulations

IGA FATCA Regulations

Countries enter into inter-governmental

agreements

FFIs have to enter into FFI

agreements

FATCA provisions need to be

implemented into local law

FFIs apply the FATCA regulations

directly

FATCA reporting to local authorities which

report to the IRS FATCA reporting directly to IRS

US reciprocity No reciprocity

10 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Overview of IGA Regime – IGA 1 in general Benefits

• Government will facilitate compliance -

removing local legal obstacles

• Group level compliance may become

easier

• It maybe possible to negotiate

exemptions for certain entities

and products

• Exceptions for withholding

• No requirement to close recalcitrant

accounts

Implications

• All FFIs will need to be in compliance

• Local Government will enforce

11 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Overview of IGA Regime – IGA 1 in general (cont.)

Depth

• IGA is not as detailed as the FATCA Regulations

•Some of the countries already published their own guidelines on the

interpretation issues (Memorandum of Understanding – MOU)

“Most favored nation” clause

•Entitles FATCA Partner to apply more favorable terms negotiated in other

IGAs

•These provisions won’t have direct effect for local Financial Institutions

•New IGAs are negotiated on the basis of the latest signed IGA

Negative consequences of non-compliance

•Domestic penalties are applicable

•Withholding is applicable for US source withholdable payments

(significant non-compliance rule)

© 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop 12

Overview of IGA Regime – Structure of the IGA

Structure of the IGA

(1) Main part

Scope of the IGA and definitions (foreign financial institution, financial

account definition, account holder, related entity, etc.)

Details (content and deadlines) of reporting obligation for FFIs

(2) Annex 1

Detailed rules of the client due diligence

(3) Annex 2

Exempted entities, products, and deemed compliant statuses

© 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop 13

Overview of IGA Regime - Scope of the IGA

Effected institutions

(foreign financial institution

categories):

(1) Depositary institution - accepts deposits

in the ordinary course of a banking or

similar business.

Interpretation question: is the

definition for banking or similar

business in the FATCA Regulations

applicable under IGA?

(2) Custodial institution - holds, as a

substantial portion of its business,

financial assets for the account of others.

14 Foreign Account Tax Compliance Act (FATCA) Workshop © 2014 Deloitte Hungary

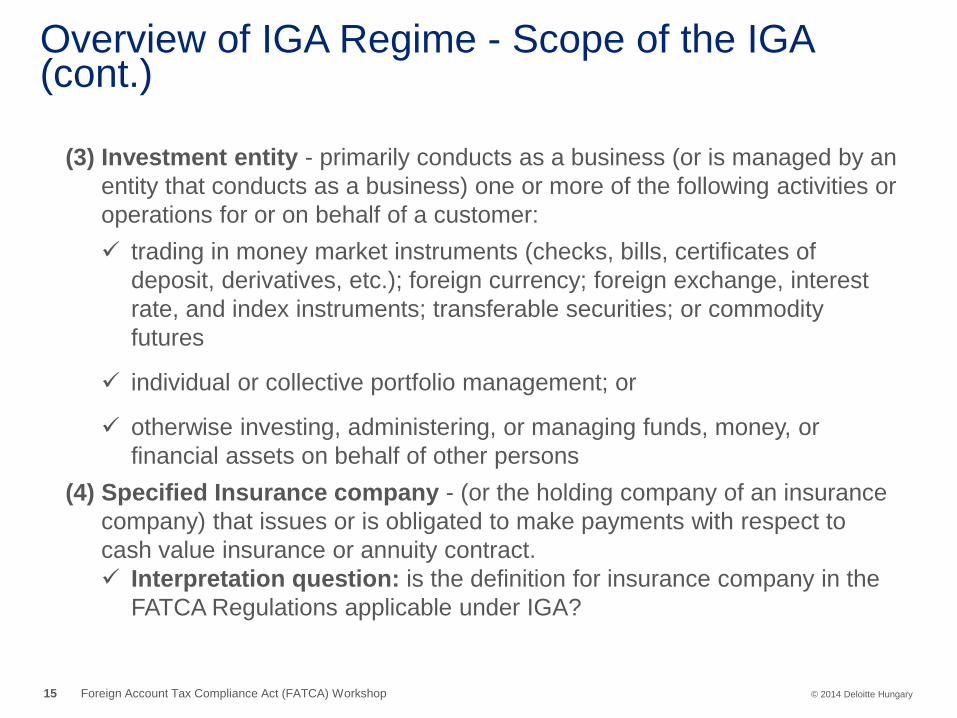

Overview of IGA Regime - Scope of the IGA (cont.)

(3) Investment entity - primarily conducts as a business (or is managed by an

entity that conducts as a business) one or more of the following activities or

operations for or on behalf of a customer:

trading in money market instruments (checks, bills, certificates of

deposit, derivatives, etc.); foreign currency; foreign exchange, interest

rate, and index instruments; transferable securities; or commodity

futures

individual or collective portfolio management; or

otherwise investing, administering, or managing funds, money, or

financial assets on behalf of other persons

(4) Specified Insurance company - (or the holding company of an insurance

company) that issues or is obligated to make payments with respect to

cash value insurance or annuity contract.

Interpretation question: is the definition for insurance company in the

FATCA Regulations applicable under IGA?

15 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

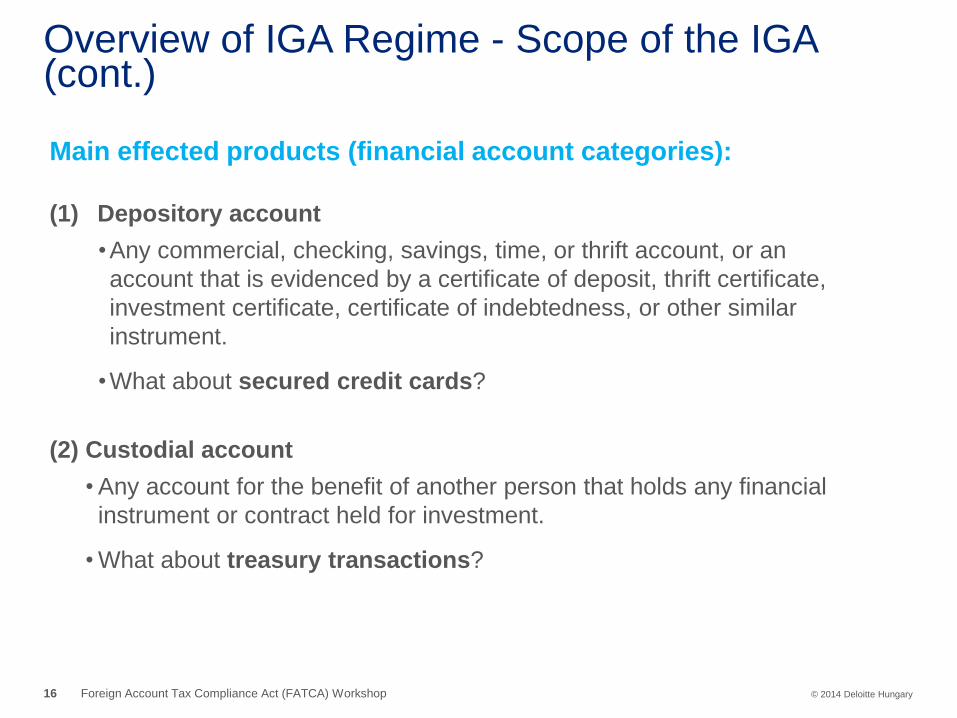

Overview of IGA Regime - Scope of the IGA (cont.)

Main effected products (financial account categories):

(1) Depository account

•Any commercial, checking, savings, time, or thrift account, or an

account that is evidenced by a certificate of deposit, thrift certificate,

investment certificate, certificate of indebtedness, or other similar

instrument.

•What about secured credit cards?

(2) Custodial account

• Any account for the benefit of another person that holds any financial

instrument or contract held for investment.

• What about treasury transactions?

16 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Overview of IGA Regime - Scope of the IGA (cont.)

(3) Equity, or debt interest in an investment entity

• Any equity or debt interest (other than interests that are regularly traded

on an established securities market) in an investment entity

• What about interest in fund management entities?

(4) Cash value insurance contract, annuity contract

•Cash value insurance in an insurance contract (other than an indemnity

reinsurance contract between two insurance companies) that has a

Cash Value greater than $50,000

•Annuity Contract is a contract under which the issuer agrees to make

payments for a period of time determined in whole or in part by reference

to the life expectancy of one or more individuals

17 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Overview of IGA Regime - IGA Annex 1 Annex 1

General rules of due diligence

•FFIs may use the rules of the Regulations instead of the rules of the IGA

provided that Romania permits the use of this rule

•The election can be made separately for each section, and separately to any

clearly identified group of accounts

Rules of the client due diligence

•Due diligence of preexisting accounts (accounts opened prior to 1 July, 2014) is

required

•The procedure of client due diligence is different in the case of individual and

corporate, existing and new clients

18 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Overview of IGA Regime - IGA Annex 1 (cont.)

Annex 1 (continued)

Special rules and definitions

•Active/ passive NFFE definition

•Account balance aggregation rules

•Currency translation rules

•Documentary evidence rules

19 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Overview of IGA Regime - IGA Annex 2

Annex 2

•According to the version released on May 9, 2013 the exempted entities and

products can not be listed country by country.

• It contains general terms, which are very similar to the categories in the

FATCA Regulations.

•This part is the most flexible part of the IGA.

• In the course of the negotiations the requirements can slightly be modified in

order to cover country specific institution and products.

20 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Overview of IGA Regime - IGA Annex 2 (cont.)

Annex 2 - Exempt beneficial owners

Main categories of exempted institutions

•Governmental entity

• International organization

•Central bank

•Retirement funds:

There are three type of the retirement funds: (1) treaty qualified retirement

fund, (2) broad participation retirement fund, (3) narrow participation

retirement fund

Private retirement funds, mutual funds can be treated as exempted entities if

they are covered by the DTT, or fulfill the requirements of the other 2

categories

In the Hungarian version of the IGA the definition of the broad participation

retirement fund was modified in order to be able to treat these entities as

exempted beneficial owner

21 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Overview of IGA Regime - IGA Annex 2

Annex 2 - Deemed-compliant FFIs

•Purpose of the deemed-compliant category is to ease the compliance of small

local market players that do not present a high risk of being used to evade tax

•The fulfillment of the FATCA requirements is easier for these categories

•As a general rule they do not have to register, and they have no reporting

obligation

•Main categories:

Financial institution with local client base

Local bank

Financial institution with only low-value accounts

Qualified credit card issuer

Certain investment entities

22 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Overview of IGA Regime - IGA Annex 2

Annex 2 - Deemed-compliant FFIs (cont.)

Sponsoring, sponsored FFI categories

• Special status for investment funds, trusts

• Sponsoring entity (e.g. fund management entity) and sponsored entity (e.g.

investment fund) have to agree that the sponsoring entity fulfills the FATCA

requirements on behalf of the sponsored entity.

• Main categories:

Sponsored investment entity

Sponsored, closely held investment vehicle

23 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Overview of IGA Regime - IGA Annex 2

Annex 2 - Exemptions from the financial account definition

• Exempted accounts are products which present a low risk for being used for

avoiding tax.

1) Two types of savings accounts: retirement and pension accounts

and certain tax-favored products.

2) Certain term life insurance contracts which are not appropriate for

investment purposes.

3) Accounts held by an estate

4) Escrow account

• In the Hungarian version of the IGA, the definition for saving accounts was

modified in order to be able to treat products as exempted where there is no

limit set by law for the annual contribution.

24 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Hungarian IGA

25

• The main part and Annex 1 were not modified

• There are minor modifications in Annex 2

Modifications in Hungarian Annex 2:

Broad Participation Retirement Fund:

• Based on Model IGA fund members should be current or former employees, in

the Hungarian IGA there is no such limitation

• Annual reporting requirement about the fund members is modified as in

Hungary retirement funds report to the supervisory authorities

© 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Hungarian IGA – cont

26

Non-Retirement Savings

Accounts:

• State-subsidized products are also

included

• Withdrawals can be made for

residential and social purposes as

well

• Requirement for the annual

contribution limit was modified – if the

annual contribution does not exceed

$50,000 the requirement is fulfilled

Foreign Account Tax Compliance Act (FATCA) Workshop © 2014 Deloitte Hungary

Steps of the development of the legal

environment for FATCA compliance through

Hungary’s example • Signing IGA with the US and incorporation of the signed IGA into domestic law

• Prepare and adopt the amendments in the relevant regulations to enable the

FATCA compliance and to eliminate the potential conflicts

• Acts to be amended in Hungary:

o Act on the Capital Market

o Act on Insurance Institutions and the Insurance Business

o Act on Investment Firms and Commodity Dealers, and on the Regulations

Governing their Activities

o Act on Credit Institutions and Financial Companies

o Act on Certain Rules of International Public Administration Cooperation in

Tax and Other Social Contributions

• Determine the additional roles and task of the Hungarian Tax Authority (e.g.:

preparation of the forms and detailed instructions for the reporting)

27 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

OECD’s Model of Competent Authority Agreement and Common Reporting Standard Model

28 Foreign Account Tax Compliance Act (FATCA) Workshop © 2014 Deloitte Hungary

OECD’s Model of Competent Authority Agreement and Common Reporting Standard Model

• On February 13, 2014 OECD released global standard for automatic exchange

of financial account information

• Purpose of the OECD standard: co-operation between tax administrations to

fight against tax evasion

• Two components:

The Model CAA (Competent Authority Agreement) contains detailed rules

on the exchange of information

The Model of CRS (Common Reporting Standard) contains the reporting

and due diligence rules to be imposed to financial institutions

• The CAA can be executed within existing legal frameworks, the CRS will need

to be translated into domestic law

29 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

The main aspects of CRS:

• Reportable accounts are defined as

accounts held by residents in the Reportable Jurisdiction; and

by Passive Non-Financial Entities with controlling reportable persons

(looking through passive entities to report on the individuals that ultimately

control these entities is required)

• The financial information to be reported with respect to Reportable Accounts

includes

all types of investment income

account balances; and

sales proceeds from financial assets

30 © 2014 Deloitte Hungary

OECD’s Model of Competent Authority Agreement and Common Reporting Standard Model

Foreign Account Tax Compliance Act (FATCA) Workshop

Next steps:

• The standard will be complemented by detailed commentary and technical

solutions to implement the actual information exchange

• It is planned that the commentary and the technical solutions will be delivered

for the September G20 Finance Minister Meetings

• Countries will need to change their domestic legislation to adopt the CRS and

conclude CAAs with other participating countries based on the model CAA

• Financial institutions will need to introduce necessary changes to IT systems

and client on-boarding procedures for implementing CRS

31 © 2014 Deloitte Hungary

OECD’s Model of Competent Authority Agreement and Common Reporting Standard Model

Foreign Account Tax Compliance Act (FATCA) Workshop

FATCA

requirements and

practical issues

32 Foreign Account Tax Compliance Act (FATCA) Workshop © 2014 Deloitte Hungary

FATCA requirements

for FFIs

33 Foreign Account Tax Compliance Act (FATCA) Workshop © 2014 Deloitte Hungary

Overview of the FATCA requirements

Registration

Due diligence of clients

Reporting

Withholding

FATCA classification of group entities

34 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Company

group

Registration

FFI NFFE

Pre-existing accounts

(Entity / Individual)

New accounts

(Entity / Individual)

Accounts held

by a Non-

participating FFI

US accounts

30%

withholding tax

Non-US

accounts

Deadlines for

FATCA

requirements

35 Foreign Account Tax Compliance Act (FATCA) Workshop © 2014 Deloitte Hungary

FATCA requirements have been pushed back by 6 months by the IRS (Notice 2013-43), July, 2013

Registration

• New registration deadline is April 25, 2014

Due diligence of clients

• Due diligence of preexisting accounts (accounts opened prior to July 1, 2014) July 1, 2014 - June 30, 2016

• New client identification process from July 1, 2014

Reporting

• 9th month following the given year is the deadline for the data exchange between the Countries

• No reporting is required for 2013

• First reporting is due by 2015 related to 2014 (year end balance)

Withholding

• U.S. source FDAP income from July 1, 2014

• Gross proceed and foreign passthru payments from January 1, 2017

Deadlines for FATCA requirements

36 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

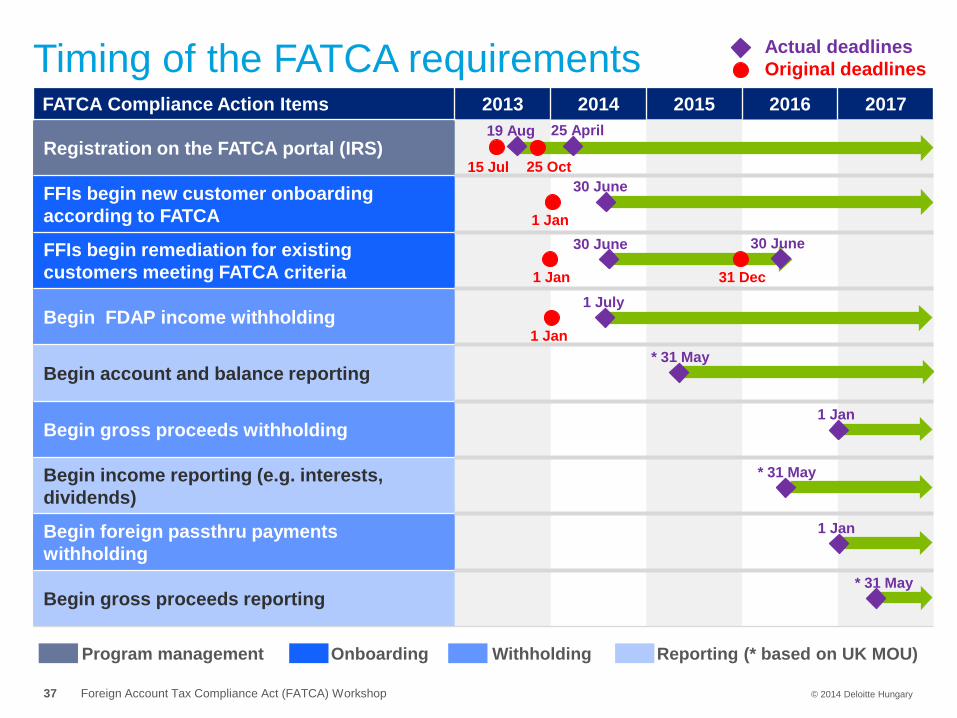

FATCA Compliance Action Items 2013 2014 2015 2016 2017

Registration on the FATCA portal (IRS)

FFIs begin new customer onboarding

according to FATCA

FFIs begin remediation for existing

customers meeting FATCA criteria

Begin FDAP income withholding

Begin account and balance reporting

Begin gross proceeds withholding

Begin income reporting (e.g. interests,

dividends)

Begin foreign passthru payments

withholding

Begin gross proceeds reporting

Timing of the FATCA requirements

37

25 April 19 Aug

15 Jul 25 Oct

1 Jan

30 June

1 Jan

30 June 30 June

31 Dec

1 Jan

1 July

* 31 May

1 Jan

* 31 May

1 Jan

* 31 May

Actual deadlines

Original deadlines

Reporting (* based on UK MOU) Withholding Onboarding Program management

© 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Determination of

FATCA impact

38 Foreign Account Tax Compliance Act (FATCA) Workshop © 2014 Deloitte Hungary

Overview of the FATCA requirements

Registration

Due diligence of clients

Reporting

Withholding

© 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

FATCA classification of group entities

39

Company

group

Registration

FFI NFFE

Pre-existing accounts

(Entity / Individual)

New accounts

(Entity / Individual)

Accounts held

by a Non-

participating FFI

US accounts

30%

withholding tax

Non-US

accounts

Determination of FATCA impact

• As FATCA requires group level

compliance, FATCA impact must be

determined with respect to each members

of the group.

• Group members must be classified as FFI

or NFFE

• Foreign Financial Institutions, FFI

The four main FATCA specified financial

institution categories are applicable.

• Non-financial Foreign Entities, NFFE

Any other foreign (non-US) entity that is

not a financial institution.

40 Foreign Account Tax Compliance Act (FATCA) Workshop © 2014 Deloitte Hungary

Group level compliance

• Any member of an expanded affiliated group identified as an FFI must be participating

FFIs, deemed-compliant FFIs, or limited FFIs.

• Each FFI that is a member of an expanded affiliated group must register with the IRS

(except for certified-deemed compliant FFIs), and

• agree to all the requirements for the status for which it applies with respect to all of the

accounts it maintains.

• If a group member is non compliant with FATCA, then this makes the entire group non-

participating, unless, the respective group member has a limited FFI status.

Practical issue

• Is this rule applicable under the IGA?

Expanded Affiliated Group for FATCA purposes

© 2014 Deloitte Hungary 41 Foreign Account Tax Compliance Act (FATCA) Workshop

Effect of FATCA for entities which are not group members for FATCA

purposes

• FATCA compliance of entities outside the expanded affiliated group does not influence

the FATCA compliance of the group.

• Based on the Regulations, in the case of entities which are not part of the expanded

affiliated group, however qualify as FFIs under FATCA (e.g. funds, insurance entities) the

advantages/ disadvantages of becoming a participating FFI should be considered on a

single entity level under the Regulations.

Practical issue

• Is this rule applicable under the IGA?

© 2014 Deloitte Hungary 42 Foreign Account Tax Compliance Act (FATCA) Workshop

Expanded Affiliated Group for FATCA purposes

Registration

43 Foreign Account Tax Compliance Act (FATCA) Workshop © 2014 Deloitte Hungary

Overview of the FATCA requirements

Registration

Due diligence of clients

Reporting

Withholding

FATCA classification of group entities

Company

group

Registration

FFI NFFE

Pre-existing accounts

(Entity / Individual)

New accounts

(Entity / Individual)

Accounts held

by a Non-

participating FFI

US accounts

30%

withholding tax

Non-US

accounts

44 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Registration Process – general rules 1/2

• FFIs are required to register

• The registration can be done by filling out a paper form ('Form 8957') or

electronically through IRS’s portal

• FFIs must nominate a Responsible Officer ('RO'), who will be the

representative/contact person of the FFI with respect to the FATCA

requirements. The RO may designate five Point of Contacts ('POCs')

• IRS will issue Global Intermediary Identification Numbers ('GIIN') to

registered FFIs

• IRS will continuously (monthly) release an IRS FFI list containing GIINs of

registered FFIs (first list will be released in June, 2014)

45 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Registration Process - general rules 2/2

• The deadline for FFIs to register to appear on first IRS FFI list is

April 25, 2014

• FFIs operating in a country which signed a Model 1 IGA should not be

negatively discriminated until January 1, 2015 due to the lack of GIIN.

GIIN. According to Announcement issued in January 2014 – the registration

deadline is December 22, 2014

• FATCA classification of FFIs should be also indicated (e.g. participating FFI,

registered deemed compliant FFI, limited FFI)

• FIs resident in a Model 1 IGA country should register as registered deemed

compliant FFI

46 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Registration electronically through IRS’s portal

• The FATCA registration portal is available as of August 2013

• Detailed user guide is available for the registration on the website of the IRS

• From January 1, 2014 the registration can be submitted as final

• As first step of the registration, account should be created, for this (1) access

code should be chosen, (2) after that the system will assign a FATCA ID

• FATCA ID and access code is needed for entering the registration portal

47 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Registration of an FFI group

• In case of a group with more FFI members, Lead FFI should be designated

• It is possible to designate more than one Lead FFI, and to create

subgroups under different Lead FFIs

• Lead FI has to create an online FATCA account for its Members

1) Lead FFI obtains own FATCA ID

2) A Lead FI generates FATCA ID for Member FIs by providing identifying

information about its Member FIs (legal name, country of residence,

FATCA classification)

• Reporting FI under a Model 1 IGA must register prior to July 1, 2014 if it

intends to be a Lead FI for one or more Member FIs in countries which are not

covered by Model 1 IGA jurisdictions

48 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Registration of an FFI group

49 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Registration of a branch of an FFI

• The FFI can obtain GIIN for its

branches

• There is no need for separate

registration

• Deadline of the registration: If the

FFI has a branch in a country with

no Model1 IGA, the FFI should

obtain for GIIN prior to July 1,

2014 in order to avoid any

negative effect

50 Foreign Account Tax Compliance Act (FATCA) Workshop © 2014 Deloitte Hungary

Registration of a branch of an FFI

51 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Due diligence of clients

52 Foreign Account Tax Compliance Act (FATCA) Workshop © 2014 Deloitte Hungary

Overview of the FATCA requirements

Registration

Due diligence of clients

Reporting

Withholding

FATCA classification of group entities

Company

group

Registration

FFI NFFE

Pre-existing accounts

(Entity / Individual)

New accounts

(Entity / Individual)

Accounts held

by a Non-

participating FFI

US accounts

30%

withholding tax

Non-US

accounts

53 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Client identification

General rules

• Purpose of the client due diligence process is the identification of

1) US Reportable Accounts

Accounts of Specified US persons,

Passive NFFEs with Specified US controlling persons

2) Accounts held by Nonparticipating Financial Institutions

• The account identification process is different for pre-existing accounts

(exists on June 30, 2014.) and for the new accounts (opened on or after

July 1,2014).

• The IGA sets different identification processes for entity and

individual clients.

54 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

• Specified US persons:

1) a US citizen or tax resident individual

2) entity clients organized in the United States or under the laws of the United Stated

which do not fall into the exempted US person category (e.g. publicly traded US

entities, US governmental entities, US financial institutions, US nonprofit entities).

• Passive NFFEs

• At least 50% of the NFFE’s gross income is passive income or at least 50% of the

assets held by the NFFE are assets that produce or are held for the production of

passive income.

• Controlling person

• The natural persons who exercise control over an Entity.

• The term “Controlling Persons” shall be interpreted in a manner consistent with the

Financial Action Task Force Recommendations

55 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Client identification

General rules

Individual clients

56 Foreign Account Tax Compliance Act (FATCA) Workshop © 2014 Deloitte Hungary

Due diligence of pre-existing individual clients

• Pre-existing account: accounts opened prior July 1, 2014

• Exemption from due diligence

Accounts with an aggregated balance not exceeding $50,000 on June 30,

2014 do not need to be reviewed, identified or reported

The threshold is $250,000 in case of cash value insurance and

annuity contracts

The exemption rule can be applied to all accounts, or to clearly identified

group of accounts

Yearly remediation is required – if the balance of the exempted account

exceeds $1,000,000 at 31 December of any subsequent year are subject

to high value account due diligence

First yearly remediation has to be done in 2015

57 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Practical challenge - Aggregation rules

• The aggregation is driven by the IT system, aggregation is required if the

computerized system link accounts by reference to a data element

such as client number, or tax number

• If the IT system is able to link the accounts of the client held by

different members of the affiliated group aggregation is a must

• If due to domestic rules such „transfer of data” (i.e. account balance) is

not possible de minimis rules cannot be applied and all preexisting

individual accounts should be deemed to qualify as high-value account

subject to enhanced review

• Other group members using separate systems may apply de minimis

rules irrespective of the above (provided that there is no unique data

element based on which they can link accounts)

58 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Steps of the due diligence

1) Electronic or paper-based search

(depending on the account balance)

for US indicia.

2) If US indicia is found, further information

must be requested (self-certification and/ or

documentary evidence).

3) Flagging the accounts as 'reportable US

account' or as

'non-reportable account'.

59 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Due diligence of pre-existing

individual clients

© 2014 Deloitte Hungary

• US citizenship, US tax residency

• US place of birth

• US address

• US phone number

• Sole address on record with FFI is U.S. 'in-care-of ' or ' hold

• Power of Attorney granted to person with US address

• Standing instructions to transfer funds to account maintained

in the USA

© 2014 Deloitte Hungary 60 Foreign Account Tax Compliance Act (FATCA) Workshop

US Indicia

Due diligence process of lower value accounts

• Lower value accounts: accounts with an aggregated balance exceeding $50,000

but not exceeding $1,000,000 as of June 30, 2014

• FFI must review its electronically searchable data for US indicia

• The review of such accounts must be completed by June 30, 2016

• Yearly remediation – if the balance exceeds $1,000,000 at 31 December of any

subsequent year are subject to high value account due diligence

• Change in circumstances should be monitored

61 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Due diligence – lower value accounts

Due diligence – high value accounts

Due diligence process of high value accounts

• Accounts with an aggregated balance exceeding $1,000,000 June 30, 2014

• In addition to the electronic search, FFI must perform a paper search for US

indicia, and relationship manager inquiry

• The review of such accounts must be completed by June 30, 2015.

• No yearly remediation is required

• Change in circumstances should be monitored, in the monitoring process the

relationship manager should be involved

62 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

New accounts: accounts opened on or after July 1, 2014

• Exemption from due diligence

• Depository accounts not exceeding $50,000 at the end of any calendar

year

• Case value insurance contracts not exceeding $50,000 at the end of any

calendar year

63 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Client identification of new individuals

Steps of the client identification

1) The client has to provide self-certification to prove the US / non US

status.

2) FFI should confirm the reasonableness of the self-certification.

3) If the account holder is US resident, US TIN must be obtained.

4) If no valid self-certification is obtained, the client should be treated as

US reportable account.

5) Change in circumstances should be monitored.

Practical questions

• What should be the form and content of the self-certification?

• How should we check the reasonableness of the self-certification?

• How should we treat the new account of preexisting clients?

64 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Due diligence of individual clients

Entity clients

65 Foreign Account Tax Compliance Act (FATCA) Workshop © 2014 Deloitte Hungary

Passive NFFEs

Entity clients – FATCA statuses

Overview

Entity clients

US person Non-US person

FFI (foreign financial

institution)

Passive NFFE Active NFFE

NFFE (non-financial

foreign entity)

Non-specified US

person (exempted

from reporting)

Passive NFFE – no

US controlling

person

Specified US

person

Passive NFFE –

with US controlling

person

Participating

FFI

Nonpartici-

pating FFI

Deemed

compliant FFI

Exempt

beneficial

owner

66 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Due diligence of pre-existing entity clients

• Pre-existing account: accounts opened prior July 1, 2014

• Exemption from due diligence: accounts with a balance of $250,000 or less,

until account balance exceeds $1,000,000

• Steps of the due diligence

1) Determine whether the clients is a Specified US person based on the place of

incorporation/ organization, or address

2) Determine whether the non-US clients are financial institutions and the FATCA

status of the FFI clients (i.e. participating, nonparticipating, exempt beneficial

owner, deemed compliant)

3) Determine whether the non-financial foreign entities are active/ or passive

NFFEs

Practical questions

How should be determined the passive/ active NFFE status?

67 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Due diligence of pre-existing entity clients

4) Determine whether the passive NFFEs have US/ non-US controlling person

In case accounts below $1,000,000, FFI may rely on information collected

for AML/KYC due diligence to identify the status of the controlling person

Above $1,000,000 self-certification should be obtained

• The review of such accounts must be completed by June 30, 2016

68 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Client identification of new entity clients

• New accounts: accounts opened on or after July 1, 2014

• Exemption from due diligence

Credit card account or a revolving credit if the Financial Institution

maintaining such account implements policies and procedures to prevent

an account balance owed to the Account Holder that exceeds $50,000

Steps of the due diligence

1) Obtain self certification to determine whether the clients is a Specified

US person

2) Determine whether the non-US clients are financial institutions and the

FATCA status of the FFI clients (i.e. participating, nonparticipating, exempt

beneficial owner, deemed compliant)

3) Determine whether the non-financial foreign entities are active or passive

NFFEs

4) Determine whether the passive NFFEs have US/ non-US controlling person

69 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Reporting

70 Foreign Account Tax Compliance Act (FATCA) Workshop © 2014 Deloitte Hungary

Overview of the FATCA requirements

Registration

Due diligence of clients

Reporting

Withholding

FATCA classification of group entities

Company

group

Registration

FFI NFFE

Pre-existing accounts

(Entity / Individual)

New accounts

(Entity / Individual)

Accounts held

by a Non-

participating FFI

US accounts

30%

withholding tax

Non-US

accounts

71 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

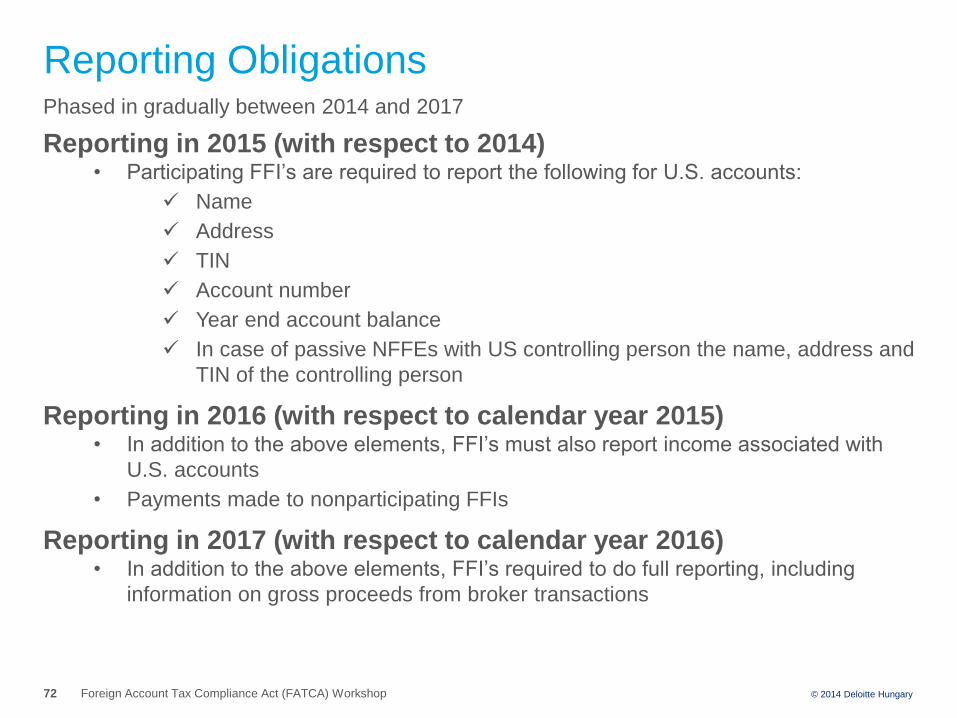

Phased in gradually between 2014 and 2017

Reporting in 2015 (with respect to 2014) • Participating FFI’s are required to report the following for U.S. accounts:

Name

Address

TIN

Account number

Year end account balance

In case of passive NFFEs with US controlling person the name, address and

TIN of the controlling person

Reporting in 2016 (with respect to calendar year 2015) • In addition to the above elements, FFI’s must also report income associated with

U.S. accounts

• Payments made to nonparticipating FFIs

Reporting in 2017 (with respect to calendar year 2016) • In addition to the above elements, FFI’s required to do full reporting, including

information on gross proceeds from broker transactions

Reporting Obligations

72 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Withholding

73 Foreign Account Tax Compliance Act (FATCA) Workshop © 2014 Deloitte Hungary

Overview of the FATCA requirements

Registration

Due diligence of clients

Reporting

Withholding

FATCA classification of group entities

Company

group

Registration

FFI NFFE

Pre-existing accounts

(Entity / Individual)

New accounts

(Entity / Individual)

Accounts held

by a Non-

participating FFI

US accounts

30%

withholding tax

Non-US

accounts

74 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

• Not complying with the FATCA regulations may result 30% withholding from the

US source payments

• Withholding – The FFIs not complying with the FATCA will be affected

• Withholding may apply to payments made as of or after July 1, 2014. Transition

rules are in force between 2014 and 2017. The final system will be working

from 2017

• Withholding before 2017 concerns only the US payees

• The FFIs in IGA countries are not obliged to withhold. However, they need to

provide information for the US payees in respect to the FATCA status of the

entitled of the payments

Withholding General rules

© 2014 Deloitte Hungary 75 Foreign Account Tax Compliance Act (FATCA) Workshop

US Source FDAP: Fixed, determinable, annual and periodic income

• Includes any payment of interest, dividends, rents, salaries, wages, premiums,

annuities, compensations, remunerations, emoluments, and other fixed or

determinable annual or periodical gains, profits, and income

Gross proceeds:

• Sale, exchange, or disposition of property that produces or can produce

interest or dividend payments that would be subject to U.S. source FDAP

income

• Includes sales of securities; stock redemptions; retirement and redemptions of

indebtedness; entering into short sale; closing a forward contract, option, or

other instrument that is otherwise a sale; corporate distribution consisting of

capital gains, etc.

Withholdable Payments

© 2014 Deloitte Hungary 76 Foreign Account Tax Compliance Act (FATCA) Workshop

Phased in gradually between 2014 and 2017

July 1, 2014

• Withholding starts on income payments

• FDAP (Fixed, Determinable, Annual, and Periodic): Includes U.S. sourced

interest, dividends, OID, rents, royalties

January 1, 2017

• Withholding will be expanded to include gross proceeds as well as income

payments

• Gross proceeds from the sale of property that generates U.S. sourced

interest or dividends

January 1, 2017

• Earliest date required to apply withholding on Foreign passthru payments

(pending further guidance)

Withholding

77 © 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Deloitte Hungary contacts

78

Takács Enikő

Manager

Phone: +36 1 428 6491

Mobile: +36 (30) 311 6945

E-mail: [email protected]

Winkler László

Director

Phone: +36 1 428 6683

Mobile: +36 (20) 582 1301

E-mail: [email protected]

© 2014 Deloitte Hungary Foreign Account Tax Compliance Act (FATCA) Workshop

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited

by guarantee, and its network of member firms, each of which is a legally separate and

independent entity. Please see www.deloitte.hu/about for a detailed description of the legal

structure of Deloitte Touche Tohmatsu Limited and its member firms.

© 2014 Deloitte Hungary.