forefront - india hedge fund 2012

DESCRIPTION

Study of Hedge Fund Industry in India 2012TRANSCRIPT

India Hedge Fund 2012 Global Ideas. Local Opportunities.

CAPITAL MANAGEMENT

2 | P a g e

Table of Contents

CAPITAL MANAGEMENT

Introduction About India Hedge Fund 2012

Globally hedge funds are an important pillar of the alternative asset management industry and a key

component of a sophisticated investor’s asset allocation. In India however, this asset class has been

virtually absent, partially because of the focus on long only investing and partially because of the lack of a

clean regulated hedge fund structure. SEBI’s proposed AIF regulations however are poised to change this

and give the hedge fund industry a real chance to provide something new to investors and wealth

managers.

No financial asset class can grow without support from the entire ecosystem – regulators, wealth

managers and investors – and meaningful guidance on how to understand, evaluate and participate in this

asset class. India Hedge Fund 2012: Global Ideas, Local Opportunities is Forefront’s small contribution

towards investor education on alternative investments. A focal point of this report is a detailed

breakdown of global hedge fund strategies that will find their way into the Indian markets. We hope this

makes for valuable reference material and great reading!

About Forefront Capital Management

Forefront Capital Management is a SEBI registered portfolio management firm focused on alternative

investing in the Indian public markets. Forefront was founded in 2009 by three Wharton graduates who

were hedge fund managers at two of the largest global funds – Goldman Sachs Asset Management (New

York) and AQR Capital Management (Greenwich). Forefront was founded with the goal of bringing

innovative and best in class global investment strategies to the Indian market. The firm has focused on

providing investment innovation in scalable and transparent products that fit into India’s regulatory

framework. Since 2009 Forefront has created a range of unique strategies for the Indian markets and has a

diverse pan-India client base of high net worth individuals, family offices and institutions.

3 | P a g e

Table of Contents

CAPITAL MANAGEMENT

Hedge Fund Strategy Basics .................................................. 4

Evaluating a Hedge Fund ........................................................ 7

Strategy Drilldown .............................................................. 10

Equity Futures ...................................................................................... 11

Equity Options ..................................................................................... 17

Arbitrage .............................................................................................. 21

Commodities and Currencies ............................................................... 26

Multi Asset Class .................................................................................. 28

Multi Strategy Funds ............................................................ 29

References and Disclosures................................................... 30

4 | P a g e

Hedge Fund Strategy Basics

CAPITAL MANAGEMENT

Demystifying Hedge Fund Strategies

Hedge funds have always had something exotic about them. But in reality their goals are very simple:

positive annual returns, low volatility and capital preservation. Hedge funds achieve this by trading a range

of strategies across available asset classes – equities, commodities, currencies, debt and a range of

financial instruments – futures, options, swaps, forwards and other derivatives. Different hedge funds

have different investment styles (fundamental, systematic, quantitative) and run different investment

strategies, some of which we cover in this publication. Globally the number of hedge funds has grown from

under 3,000 in 1995 to more than 9,000 today, and the hedge fund industry manages over USD 1 trillion in

assets.

What’s Different?

Because of India’s regulatory structure domestic investors have typically seen only long only equities either

through a mutual fund, direct equity or PMS route. These strategies hold only cash equities typically for

the long term. Regardless of the investment process which can vary from bottom up stock picking to

purely system driven, these strategies are long only relative return strategies. Over the long term they

have done very well, and in general buy and hold strategies do well particularly in a growing equity market.

The issue, as many investors are discovering is, is the length of time and starting point. Market timing –

when you buy – is critical. Investors who bought in December 2007 at the peak of the markets vs.

investors who bought in October 2008 at the absolute low, will have a very different 5 year return on their

portfolios. Standing in December 2011, the annualized five year return on the NIFTY was 3.1%, a

depressing number for long term investors. As for the manager, the best they can do in a long only setting

is outperform the index – if the fund declines, their portfolios will decline less than the benchmark.

Contrary to long only managers, hedge fund managers focus on risk adjusted absolute returns – the

objective is to increase capital value rather than to beat a benchmark. Globally as a result hedge fund

managers charge performance fees on the absolute returns generated, whereas long only managers

charge only fixed fees. The heavy performance fee component keeps hedge fund manager incentives

aligned to investor incentives.

Hedging and leverage are two key tools used by hedge fund managers to generate positive absolute

returns. Hedging focuses on protecting the portfolio against sharp movements in markets. On the long

side the manager will buy assets that have good long term prospects and on the short side sell assets with

poor prospects. The latter can be implemented with futures and options in the Indian market. Hedging is

essential to keep the absolute return characteristics of the portfolio intact and generate absolute returns in

poor markets.

Since a hedge fund manager focuses on hedged opportunities that are immune to market returns, these

opportunities involve small trading margins. In themselves the small trading margins do not generate

5 | P a g e

Hedge Fund Strategy Basics

CAPITAL MANAGEMENT

meaningful absolute returns, but when leveraged they do. Leverage is essentially taking on positions

larger than the capital deployed. For instance, a typically mutual fund manager takes Rs. 1 crore of

positions for every Rs. 1 crore of capital he is given. A hedge fund manager on the other hand may take Rs.

2 crores of positions, resulting in two times the leverage. Higher positions or leverage comes with higher

risk and risk management is the hallmark of a good hedge fund manager. In fact risk adjusted returns are

the most meaningful metric of hedge fund manager performance.

Do hedge funds create negative externalities?

While hedge funds have always been cited as a cause for market crashes and associated with negative

externalities, much of this is myth. The U.S. Securities and Exchange Commission (SEC) recently determined

that there is little evidence that hedge funds can move markets, and several research studies have found

no evidence that hedge funds were a cause of the Asian crisis or other world economic turmoil.

A counterpoint is that hedge fund activity makes financial markets more efficient and, in many cases, more

liquid. Not only do hedge funds contribute to the adjustments of markets when they overshoot, they also

help banks and other creditors unbundle risks related to real economic activity by actively participating in

the market of securitized financial instruments. And because hedge fund returns in many cases are less

correlated with broader debt and equity markets, hedge funds offer more traditional investment

institutions a way to reduce risk by providing portfolio diversification.

Where do these strategies fit into my asset allocation?

A natural question to ask with a new investment class is where does this fit into my or my client’s asset

allocation. For many strategies, the answer is it is a new category of absolute return strategies that falls in

the alternatives bucket. These strategies cannot be classified as fixed income because they are risk taking

strategies (with the exception of arbitrage). Nor do they fall into the equity category even if the risk is

comparable because they have no correlation to equities (with the exception of strategies such as 130/30

Equity and Buy-Write Equity which explicitly have equity beta). In fact, bucketing them with equities will

confuse clients because they will compare the returns to the market and wonder why they are down in a

month when the market is up 10%!

How do such strategies make a difference to my portfolio?

While each hedge fund strategy has a different risk / return / beta profile as discussed in the strategy

drilldown, adding a hedge fund strategy to your portfolio can improve diversification, reduce portfolio risk

and increase the risk adjusted return of your portfolio. The basic portfolio example below illustrates this.

6 | P a g e

Hedge Fund Strategy Basics

CAPITAL MANAGEMENT

Assume a client has a basic portfolio of equities (NIFTY) and debt (one year fixed deposits), with a 70% and

30% allocation respectively. The return, risk and risk adjusted return of the individual assets as well as the

portfolio is below (assuming asset returns since 1998).

Equities Debt Portfolio

Weight 70% 30% 100% Return 18% 8% 15%

Risk 27% 1% 19%

Sharpe Ratio 0.66 12.80 0.79

Equities and debt are uncorrelated assets so combining them together in a portfolio yields a portfolio with

lower risk than equities, and higher risk adjusted return than equities. Now assume the client shifts 25% of

his portfolio to two hedge fund strategies – for the sake of argument Strategy 1 (Long Short Equities) and

Strategy 2 (Long Short Commodities). Both these strategies deliver a risk adjusted return of 1.0 in the long

term, are uncorrelated to each other as well as to other asset classes like debt, equity and gold. The new

portfolio characteristics are as below.

Equities Debt Strategy 1 Strategy 2 Portfolio

Weight 52% 22% 12.5% 12.5% 100% Return 18% 8% 14% 16% 15%

Risk 27% 1% 14% 16% 14%

Sharpe Ratio 0.66 12.80 1.00 1.00 1.04

By adding two new uncorrelated sources of risk, the overall portfolio risk has fallen from 19% to 14%, and

risk adjusted return has gone up from 0.79 to 1.04. Globally institutions enhance this simple example by

building a portfolio of many uncorrelated strategies, thereby maximizing risk adjusted returns.

7 | P a g e

CAPITAL MANAGEMENT

Evaluating A Hedge Fund

Why is hedge fund evaluation important?

Since hedge funds are a new investment class trading both asset classes and instruments that clients,

wealth managers, and sometimes even managers may not completely understand, evaluating hedge funds

thoroughly is important. The metrics for evaluating a hedge fund are different from those for a long only

investment, with manager skill and risk management being a much bigger part of the evaluation process.

The guide below lists the basic parameters that should be understood in any hedge fund like product.

Target returns

Clients invest for absolute returns so returns are one of the first parameters that should be evaluated. It’s

important to understand the level of absolute return the strategy can generate and whether it is

meaningful to you as an investor. Because hedge fund strategies involve small trading margins they can

generate positive absolute returns, but the level of those returns may not be meaningful (for instance,

some arbitrage strategies consistently generate positive absolute returns but often in line with fixed

income rates). It’s also important to understand the investment period over which those returns can be

expected because hedge fund strategies vary from very high frequency to much longer term. A poor

understanding of the time horizon only leads to frustration among investors and wealth managers. Finally

it’s important to understand what the returns will look like in different markets – when the strategy will

perform and when it will not. No risk taking strategy is always up, and a prior understanding of when the

strategy doesn’t work will make for a much more peaceful experience.

Risk

The importance of understanding risk in hedge fund strategies cannot be overemphasized enough. Risk is

best measured by the annualized standard deviation of the realized returns. As an example, a fixed

deposit has a risk of nearly zero and the NIFTY over 15 years has a realized risk of over 25%. By comparing

the risk of your strategy to asset classes like NIFTY, gold, as well as balance funds / monthly income plans,

you will have a good sense of what to expect as far as monthly and annual returns and drawdown

expectations. Quantitative or systematic managers will be able to give you an assessment of risk from

their backtest and fundamental managers should also be able to give you a target risk number. Hedge

funds often make investments with asymmetric payoffs, hence analyzing worst case drawdowns, value-at-

risk and higher moments such as skewness and kurtosis are also important.

Leverage

Leverage and risk go hand in hand but they are not the same thing. A strategy can be very risky but involve

no leverage and vice-versa. Leverage is important to understand because in a leveraged strategy, one can

lose more capital than initially deployed. This will result in margin calls, which if not met can lead to

8 | P a g e

CAPITAL MANAGEMENT

Evaluating A Hedge Fund

positions being shut down. In hedge fund strategies, there is a great temptation to keep scaling up

leverage to scale up returns, but a good hedge fund manager will push back and maintain a reasonable

level of leverage. One way to evaluate leverage is to ask a manager what kind of loss on a daily or monthly

basis it would take to get a margin call, and then see if there is enough of a safety margin built in.

In our analysis of different hedge fund strategies we look at the gross leverage of each strategy. For our

purpose, every instrument contributes to gross leverage regardless of how similar other instruments in the

portfolio are. So for example, a long position in Reliance and a corresponding short position in Reliance

Futures would have a gross leverage of 200% even though the position is perfectly hedged.

Leverage is also a robust risk metric because it is easy to calculate and does not make any assumptions on

the distribution of returns.

Risk adjusted returns

Risk adjusted returns or Sharpe ratio (the average annual return divided by the average annual risk) is a

good measure of manager skill and performance in a hedge fund context. The risk adjusted returns

measure the value a manager has added for each unit of risk taken. Sharpe ratios can vary from 0.5 to 1

for low frequency strategies to much higher for higher frequency strategies. Two managers can generate

15% returns but if one is taking half the risk of the other, he has done a far superior job. While a backtest

can give you an idea of the Sharpe ratio a strategy can generate, the proof here is really in the pudding.

When working with a manager it’s very important to a sanity check on the expectedly Sharpe ratio to see if

they are reasonable. For low frequency funds for instance, a range between 0.6 to 1 is what a manager

can reasonably deliver over the long term.

Given the asymmetric nature of some hedge fund strategies, alternative measures of risk adjusted returns

should also be used. These include the Sortino ratio (return per unit of downside volatility) and the Sterling

ratio (average return / maximum drawdown).

Beta and correlation to existing asset classes

Both beta and correlation measure the strategy’s sensitivity to existing asset classes such as equities, debt,

commodities and currencies. Since hedge funds are at least partially (if not fully) hedged strategies to

respective asset classes, they should have low betas / correlations to other asset classes. For instance long

short equity funds depending on whether they are pure market neutral or slightly long biased funds should

have a very low beta to equities. It’s important to measure beta relative to the right asset class. For a

commodity long short fund for instance, the beta to gold, crude and copper as well as a major commodity

index should be low. Measuring beta gives you a sense of whether a manager is sticking to the hedge fund

mandate and what kind of hidden risks there are. For instance, an equity market neutral fund with a beta

9 | P a g e

CAPITAL MANAGEMENT

Evaluating A Hedge Fund

of 0.7 to the NIFTY is doing something deeply wrong. Again a back test can give you an idea of what to

expect here and realized returns can do a check on whether the manager is following the strategy.

Liquidity and trading implementation

Since hedge fund strategies trade exotic asset classes and instruments understanding the liquidity and

trading costs of these instruments is important. Ideally for an open ended fund asset classes and

instruments should be liquid enough that the portfolio can be exited in 3-5 days without impacting the

portfolio adversely. Hedge funds are often not locked in vehicles and can see redemptions, and

redemptions from one investor should not hurt existing investors because of liquidity.

Tail risk

Tail risk was an alien concept to investors until the financial crisis of 2008 when strategies with heavy tail

risks cost clients a fortune. Tail risk is the risk of a strategy losing large amounts of money when an

extremely unexpected event happens. The probability of the loss is very low but the magnitude is usually

very high. A number of strategies for instance appear innocuous but have large hidden tail risks. For

instance, options writing is a strategy that generates a very innocuous constant return but loses large

amounts of money when the market has a significant directional move. A manager should be asked if

strategies are insulated for tail risk.

Experience

While every strategy can be evaluated on quantitative and qualitative parameters, ultimately a strategy is

run by a manager. More so than other fields, genuine asset management experience in running the

strategy and trading it with client money will distinguish a manager in the long run. Experience will help a

manager focus on measuring risks correctly, giving realistic return expectations, protecting tail risk, and

picking up after a drawdown, which is inevitable in every strategy. Hedge fund experience is also very

different from long only experience because of the important role of risk management and the exotic and

complex nature of the instruments used. Similarly buy side experience will outperform sell side

experience because hedge fund asset management raises complex issues that are difficult to see on a

brokerage desk.

10 | P a g e

Strategy Drilldown

CAPITAL MANAGEMENT

Overview

The list of existing hedge fund strategies are countless and one edition of this publication cannot do justice

to them. What we have attempted to do is to look at the major global hedge fund strategies that could be

applied to the Indian markets in light of the new Alternative Investment Fund regulations. Given the

regulations are yet to take complete shape, we have not attempted to answer what is regulatory

permissible and what is not.

Our goal is to give investors and wealth managers a flavour of what can and may be done. We have also

evaluated these strategies on the basic hedge fund evaluation parameters so that clients and wealth

managers know what to look out for. The classes of strategies covered are:

Strategy Risk Asset Allocation

Category Beta Leverage

Time

Horizon

Equity Futures

130-30 Equities High Equities 0.9 – 1.0 1.6 x 3 yrs.

Long Short Equities Med – High Absolute Return 0.0 – 0.6 1x – 2.5x 18 mo.

Short Biased Equities High Equities -1.0 – 0.0 Max: 2x 3 yrs.

Directional Equities High Absolute Return 0.0 Max: 1x 1-2 yrs.

Pairs Trading Med Absolute Return 0.0 Depends 18 mo.

Managed Futures High Absolute Return 0.0 1x – 2.5x 18 mo.

Equity Options

Buy-Write Equities Med – High Equities 0.6 – 1.0 1x - 2x 3 yrs.

Volatility Trading High Absolute Return 0.0 1x – 1.5x 18 mo.

Correlation Trading High Absolute Return 0.0 1x – 1.5x 18 mo.

Black Swan Protection Limited Insurance Negative Max: 1x 3 yrs.

Arbitrage

Cash Futures Arbitrage Low Fixed Income 0.0 Max: 2x 3-6 mo.

Pure Arbitrage Low Fixed Income 0.0 Depends 3-6 mo.

Commodity Arbitrage Low Fixed Income 0.0 Max: 2x 3-6 mo.

Statistical Arbitrage Med – High Absolute Return 0.0 Depends 18 mo.

Event Arbitrage Med – High Absolute Return 0.0 Max: 1x 18 mo.

Commodities and Currencies

Long Short Commodities Med – High Absolute Return 0.0 1x – 1.5x 18 mo.

Long Short Currencies Med – High Absolute Return 0.0 2x – 5x 18 mo.

Multi Class

Tactical Asset Allocation Med Absolute Return 0.0 – 0.5 1x – 2x 18 mo.

11 | P a g e

Equity Futures

CAPITAL MANAGEMENT

130-30 Equities

Characteristic Description

Strategy

Description

A mutual fund is limited to holding no more than 10% in a single stock and not taking

net short positions in stocks. 130/30 Equity relaxes these constraints by allowing

managers to invest more than 10% in high conviction ideas and create additional

alpha by shorting stocks that they are bearish on.

Economic

Rationale

If a long-only manager has skill in beating his benchmark, then giving him more

freedom to express his views on high conviction ideas and short side ideas should

lead to higher outperformance.

Assets Held Long: Single stock futures or cash equities

Short: Single stock futures

Sample

Position

Long a diversified portfolio of fundamentally strong stocks, short stocks that are

overvalued or that have weak fundamentals.

Target Beta 0.9 – 1.0

Unique Risks Cash management is important especially if a large portion of the portfolio’s long

positions are held in cash equities.

Performs

Well In...

Rising equity markets (in absolute terms) and when the manager’s stock and sector

picks are correct (relative to the benchmark).

Performs

Poorly In...

Falling equity markets (in absolute terms) and when the manager’s stock and sector

picks go wrong (relative to the benchmark).

Client Profile Equity like product for moderate to aggressive clients.

Asset

Allocation

Fits into the equity portion of a client’s asset allocation along with mutual funds.

Trading

Frequency

Portfolios are rebalanced at least once a month to coincide with the futures roll.

Since the portfolio views are of an intermediate term, portfolios will be similar

month-to-month.

Is the strategy

opportunistic?

No

Leverage

Taken

Gross Leverage = 1.6x

Risk / Return

Profile

Has a similar risk / return profile to the NIFTY or a traditional diversified equity

mutual fund. Should aim to outperform the benchmark over long periods.

Investment

Horizon

3 Years

Points to

consider

The manager’s stock picking ability and cash management are important.

Strategy Drilldown

Strategy Drilldown

Strategy Drilldown

12 | P a g e

Equity Futures

CAPITAL MANAGEMENT

Long Short Equities / Equity Market Neutral

Characteristic Description

Strategy

Description

Long a portfolio of stocks that are undervalued and/or have strong fundamentals and

short a portfolio of stocks that are overvalued and/or have weak fundamentals.

Focuses purely on a manager’s stock selection and sector rotation abilities rather

than mixing it with market beta like in a long-only mutual fund.

Economic

Rationale

Undervalued stocks with strong fundamentals will outperform overvalued stocks

with weak fundamentals over a market cycle.

Assets Held Long: Single stock futures or cash equities.

Short side: Single stock futures or index futures/options to hedge the equity beta.

Sample

Position

Rank PSU Banks based on their Price / Book ratios. Take long positions in banks with

low Price / Book values and short positions in banks with high Price / Book values.

Target Beta Long-Short Equity portfolios are often run with a long-equity bias (i.e. Beta between

0 and 0.6). Equity market neutral is a special case of Long-Short Equities where the

manager targets a beta of 0 at all times.

Unique Risks The strategy presents operational risks because managing a book of 40+ futures

positions can be challenging if the manager’s systems are not up to par.

Performs

Well In...

In fundamental driven markets, when there are flights to quality stocks and during

earnings if the positions are related to fundamental factors.

Performs

Poorly In...

In speculative or junk led rallies. The strategy will also do poorly if there is a rapid

shift in a company’s fundamental prospects.

Client Profile Moderate (low-leverage) to aggressive (high-leverage) clients

Asset

Allocation

Absolute return allocation.

Trading

Frequency

Portfolios are rebalanced at least once a month to coincide with the futures roll.

Since the views are intermediate term, portfolios are similar month-to-month.

Is the strategy

opportunistic?

No.

Leverage

Taken

Leverage can be varied based on a client’s risk profile. A long-short portfolio with

gross leverage of 1x has an annualized risk of 5% (similar to an aggressive monthly

income plan). A portfolio with gross leverage of 2.5x has an annualized risk of 12.5%

(similar to a balanced fund).

Risk / Return

Profile

Should deliver 15%-20% with leverage over an 18 month period regardless of what

the NIFTY does. The strategy could be down in a given month or quarter.

Investment

Horizon

18 months.

Points to

consider

Investment process, portfolio construction and implementation are very important

points to consider when evaluating an equity long-short manager.

Strategy Drilldown

Strategy Drilldown

Strategy Drilldown

13 | P a g e

Equity Futures

CAPITAL MANAGEMENT

Short Biased Equities

Characteristic Description

Strategy

Description

Short overvalued and fundamentally weak companies.

Economic

Rationale

The market is structurally biased to be long equities. The strategy attempts to profit

from companies that are overvalued, highly levered, have large pledged promoter

holdings, faulty accounting, weak management or unsound business models.

Assets Held Single stock options and futures, index futures.

Sample

Position

Short a diversified portfolio of stocks, long NIFTY futures.

Target Beta -1.0 to 0.

Unique Risks Cash management is important because futures positions could suffer mark-to-

market losses if stocks remain irrationally priced longer than expected. Stocks could

also be propped up by unscrupulous management.

Performs

Well In...

Bear markets, rising interest rate environments and when liquidity is tight.

Performs

Poorly In...

Bull markets and speculative rallies.

Client Profile Aggressive clients.

Asset

Allocation

Equity allocation.

Trading

Frequency

Monthly or whenever there are market opportunities.

Is the strategy

opportunistic?

Partially – Segments of the market are always overvalued but stock specific

opportunities appear from time to time.

Leverage

Taken

Max Gross Leverage = 2x

Risk / Return

Profile

Similar to a short NIFTY position.

Investment

Horizon

3 years.

Points to

consider

The manager’s forensic accounting, stock picking ability and cash management are

important.

14 | P a g e

Equity Futures

CAPITAL MANAGEMENT

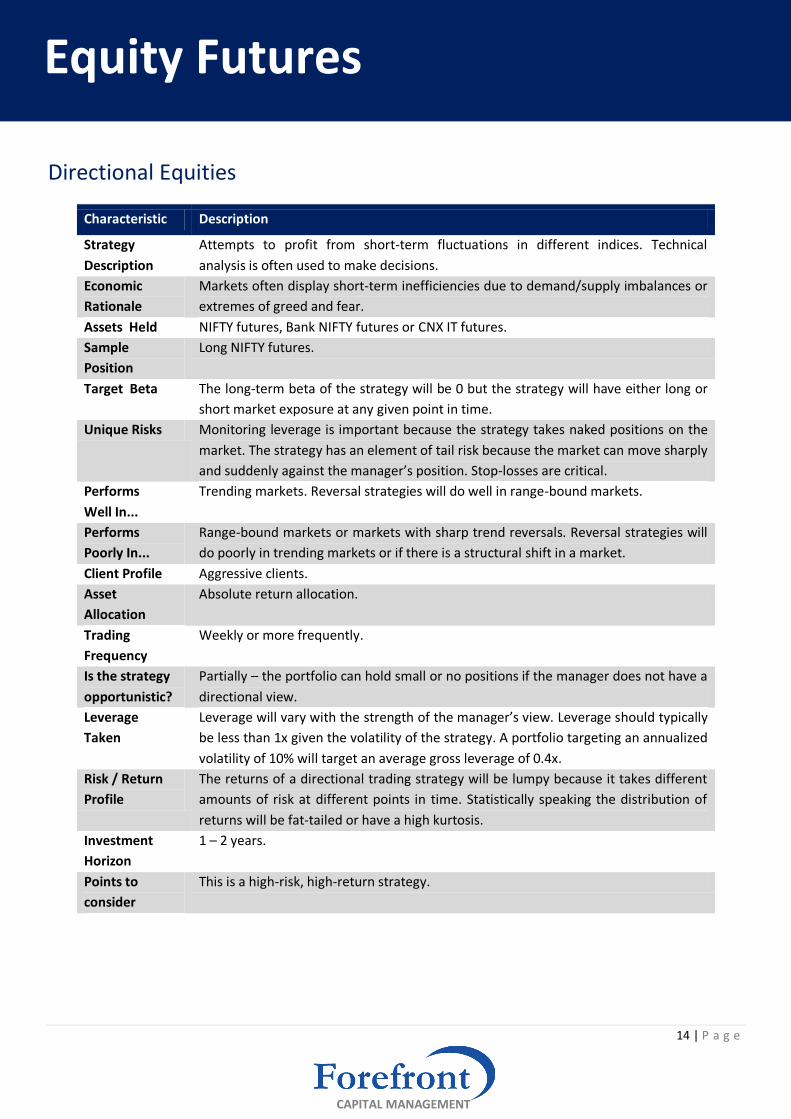

Directional Equities

Characteristic Description

Strategy

Description

Attempts to profit from short-term fluctuations in different indices. Technical

analysis is often used to make decisions.

Economic

Rationale

Markets often display short-term inefficiencies due to demand/supply imbalances or

extremes of greed and fear.

Assets Held NIFTY futures, Bank NIFTY futures or CNX IT futures.

Sample

Position

Long NIFTY futures.

Target Beta The long-term beta of the strategy will be 0 but the strategy will have either long or

short market exposure at any given point in time.

Unique Risks Monitoring leverage is important because the strategy takes naked positions on the

market. The strategy has an element of tail risk because the market can move sharply

and suddenly against the manager’s position. Stop-losses are critical.

Performs

Well In...

Trending markets. Reversal strategies will do well in range-bound markets.

Performs

Poorly In...

Range-bound markets or markets with sharp trend reversals. Reversal strategies will

do poorly in trending markets or if there is a structural shift in a market.

Client Profile Aggressive clients.

Asset

Allocation

Absolute return allocation.

Trading

Frequency

Weekly or more frequently.

Is the strategy

opportunistic?

Partially – the portfolio can hold small or no positions if the manager does not have a

directional view.

Leverage

Taken

Leverage will vary with the strength of the manager’s view. Leverage should typically

be less than 1x given the volatility of the strategy. A portfolio targeting an annualized

volatility of 10% will target an average gross leverage of 0.4x.

Risk / Return

Profile

The returns of a directional trading strategy will be lumpy because it takes different

amounts of risk at different points in time. Statistically speaking the distribution of

returns will be fat-tailed or have a high kurtosis.

Investment

Horizon

1 – 2 years.

Points to

consider

This is a high-risk, high-return strategy.

15 | P a g e

Equity Futures

CAPITAL MANAGEMENT

Pairs Trading

Characteristic Description

Strategy

Description

When the prices of two highly correlated stocks diverge, a pairs trading strategy

attempts to profit from their convergence.

Economic

Rationale

Highly correlated stocks that are in the same sector and have similar businesses must

move together. Prices can diverge temporarily because of demand/supply

imbalances but they must converge back eventually.

Assets Held Single stock futures.

Sample

Position

Long HEROMOTOCO and Short BAJAJ-AUTO in the ratio of 1.3:1

Target Beta Zero.

Unique Risks Pairs Trading is exposed to event risk because the correlation between two stocks

can breakdown if one of them undergoes a structural change due to a change in

business, management or regulation.

Performs

Well In...

Benign markets and when the correlations between stocks are stable.

Performs

Poorly In...

Periods when there is stock specific news, event risk and when correlations break

down.

Client Profile Moderate risk clients.

Asset

Allocation

Absolute return allocation.

Trading

Frequency

As and when opportunities arise. Positions are rolled monthly.

Is the strategy

opportunistic?

Yes.

Leverage

Taken

Depends on the number of pairs.

Risk / Return

Profile

A single pair trade position can have 75% of the volatility of the equity market. But a

portfolio of 5 pairs will have an annualized standard deviation of 8%-10% (similar to

the volatility of a portfolio of 1/3rd equities, 1/3rd gold and 1/3rd debt).

Investment

Horizon

18 months.

Points to

consider

Risk management including stop-losses and a qualitative filter to identify structural

breaks are important. How the hedge ratios are determined whether on a value-

neutral, beta-neutral or volatility-neutral basis are also important.

16 | P a g e

Equity Futures

CAPITAL MANAGEMENT

Managed Futures

Characteristic Description

Strategy

Description

Long stocks with positive price momentum, short stocks with negative price

momentum. The strategy can also be applied to commodities and currencies.

Economic

Rationale

Individual stocks display price momentum because of sustained buying or selling, a

tendency for investors to hold on to losers and sell winners too early and the

tendency for market participants to under react to market news.

Assets Held Single stock futures.

Sample

Position

Long stocks that have risen in the last 3 months, short stocks that have fallen in the

last 3 months.

Target Beta Zero. The strategy could have positive or negative market exposure at any point in

time.

Unique Risks In India, managed futures runs the risk of being the last man holding if a stock is

being manipulated.

Performs

Well In...

Trending markets and in periods of volatility.

Performs

Poorly In...

Range bound markets and tranquil periods.

Client Profile Aggressive clients.

Asset

Allocation

Absolute return allocation.

Trading

Frequency

Weekly or more frequently.

Is the strategy

opportunistic?

No.

Leverage

Taken

Leverage can be varied based on a client’s risk profile. A managed futures book with

gross leverage of 1x has an annualized risk of 5% (similar to an aggressive monthly

income plan). A portfolio with gross leverage of 2.5x has an annualized risk of 12.5%

(similar to a balanced fund).

Risk / Return

Profile

Should return 15%-20% over a 12-18 month period with leverage regardless of what

the NIFTY does. The strategy could be down in a given month or quarter.

Investment

Horizon

18 months.

Points to

consider

Risk management including position sizing and stop losses are important for a

managed futures book.

17 | P a g e

Equity Options

CAPITAL MANAGEMENT

Buy-Write Equities

Characteristic Description

Strategy

Description

Buy a portfolio of stocks and sell out-of-the-money NIFTY call options.

Economic

Rationale

Selling out-of-the-money index call options generates income that helps a long-only manager outperform his benchmark.

Assets Held Cash Equities, Index Call Options.

Sample

Position

Long a diversified portfolio of stocks, short NIFTY call options.

Target Beta 0.6 – 1.0.

Unique Risks Cash management is important because short call option positions could suffer mark-to-market losses.

Performs

Well In...

Moderate bull markets and when implied volatilities are high.

Performs

Poorly In...

Falling equity markets (in absolute terms), in sudden market rallies (relative to the benchmark) and when the manager’s stock and sector picks go wrong (relative to the benchmark).

Client Profile Moderate to aggressive clients.

Asset

Allocation

Equity portion of a client’s asset allocation along with traditional mutual funds.

Trading

Frequency

The cash equity portion of the portfolio is rebalanced whenever there is a change in the manager’s view. The index options are rolled monthly.

Is the strategy

opportunistic?

No.

Leverage

Taken

Max Gross Leverage = 2x but lower levels of leverage can also be taken.

Risk / Return

Profile

Buy-Write Equity has a similar risk / return profile to the NIFTY or a traditional diversified equity mutual fund.

Investment

Horizon

3 years.

Points to

consider

The manager’s stock picking ability and cash management are important.

18 | P a g e

Equity Options

CAPITAL MANAGEMENT

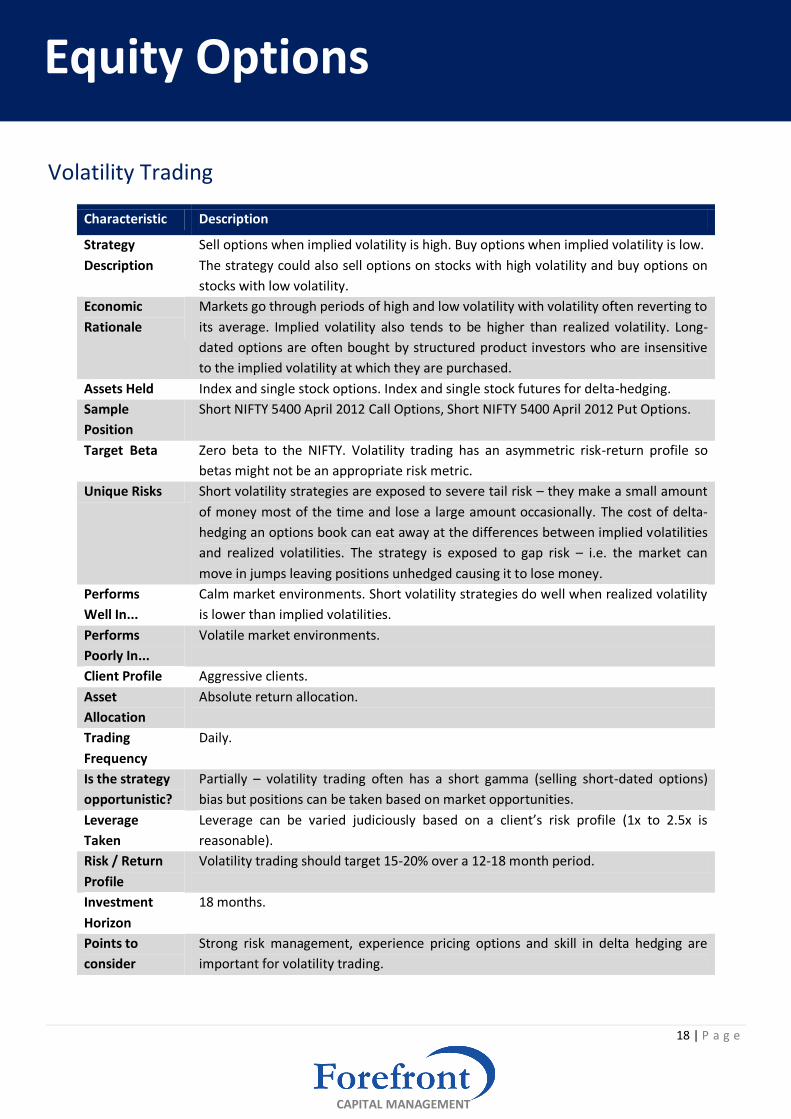

Volatility Trading

Characteristic Description

Strategy

Description

Sell options when implied volatility is high. Buy options when implied volatility is low.

The strategy could also sell options on stocks with high volatility and buy options on

stocks with low volatility.

Economic

Rationale

Markets go through periods of high and low volatility with volatility often reverting to

its average. Implied volatility also tends to be higher than realized volatility. Long-

dated options are often bought by structured product investors who are insensitive

to the implied volatility at which they are purchased.

Assets Held Index and single stock options. Index and single stock futures for delta-hedging.

Sample

Position

Short NIFTY 5400 April 2012 Call Options, Short NIFTY 5400 April 2012 Put Options.

Target Beta Zero beta to the NIFTY. Volatility trading has an asymmetric risk-return profile so

betas might not be an appropriate risk metric.

Unique Risks Short volatility strategies are exposed to severe tail risk – they make a small amount

of money most of the time and lose a large amount occasionally. The cost of delta-

hedging an options book can eat away at the differences between implied volatilities

and realized volatilities. The strategy is exposed to gap risk – i.e. the market can

move in jumps leaving positions unhedged causing it to lose money.

Performs

Well In...

Calm market environments. Short volatility strategies do well when realized volatility

is lower than implied volatilities.

Performs

Poorly In...

Volatile market environments.

Client Profile Aggressive clients.

Asset

Allocation

Absolute return allocation.

Trading

Frequency

Daily.

Is the strategy

opportunistic?

Partially – volatility trading often has a short gamma (selling short-dated options)

bias but positions can be taken based on market opportunities.

Leverage

Taken

Leverage can be varied judiciously based on a client’s risk profile (1x to 2.5x is

reasonable).

Risk / Return

Profile

Volatility trading should target 15-20% over a 12-18 month period.

Investment

Horizon

18 months.

Points to

consider

Strong risk management, experience pricing options and skill in delta hedging are

important for volatility trading.

19 | P a g e

Equity Options

CAPITAL MANAGEMENT

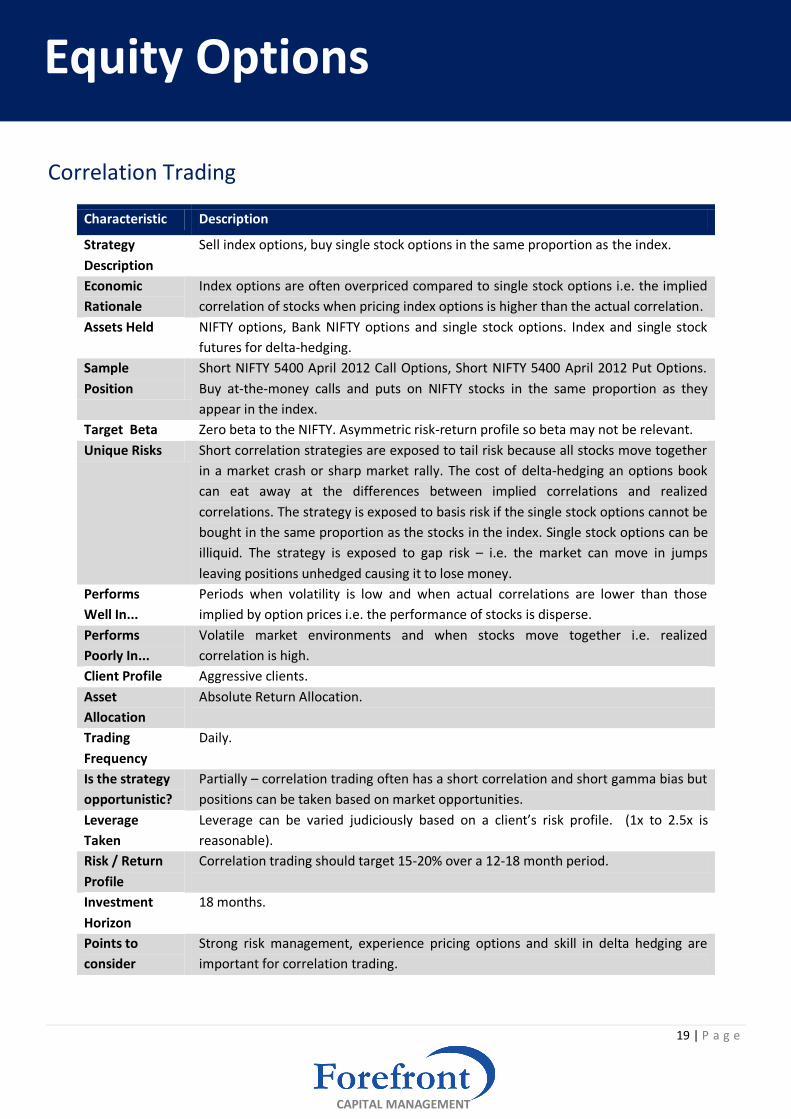

Correlation Trading

Characteristic Description

Strategy

Description

Sell index options, buy single stock options in the same proportion as the index.

Economic

Rationale

Index options are often overpriced compared to single stock options i.e. the implied

correlation of stocks when pricing index options is higher than the actual correlation.

Assets Held NIFTY options, Bank NIFTY options and single stock options. Index and single stock

futures for delta-hedging.

Sample

Position

Short NIFTY 5400 April 2012 Call Options, Short NIFTY 5400 April 2012 Put Options.

Buy at-the-money calls and puts on NIFTY stocks in the same proportion as they

appear in the index.

Target Beta Zero beta to the NIFTY. Asymmetric risk-return profile so beta may not be relevant.

Unique Risks Short correlation strategies are exposed to tail risk because all stocks move together

in a market crash or sharp market rally. The cost of delta-hedging an options book

can eat away at the differences between implied correlations and realized

correlations. The strategy is exposed to basis risk if the single stock options cannot be

bought in the same proportion as the stocks in the index. Single stock options can be

illiquid. The strategy is exposed to gap risk – i.e. the market can move in jumps

leaving positions unhedged causing it to lose money.

Performs

Well In...

Periods when volatility is low and when actual correlations are lower than those

implied by option prices i.e. the performance of stocks is disperse.

Performs

Poorly In...

Volatile market environments and when stocks move together i.e. realized

correlation is high.

Client Profile Aggressive clients.

Asset

Allocation

Absolute Return Allocation.

Trading

Frequency

Daily.

Is the strategy

opportunistic?

Partially – correlation trading often has a short correlation and short gamma bias but

positions can be taken based on market opportunities.

Leverage

Taken

Leverage can be varied judiciously based on a client’s risk profile. (1x to 2.5x is

reasonable).

Risk / Return

Profile

Correlation trading should target 15-20% over a 12-18 month period.

Investment

Horizon

18 months.

Points to

consider

Strong risk management, experience pricing options and skill in delta hedging are

important for correlation trading.

20 | P a g e

Equity Options

CAPITAL MANAGEMENT

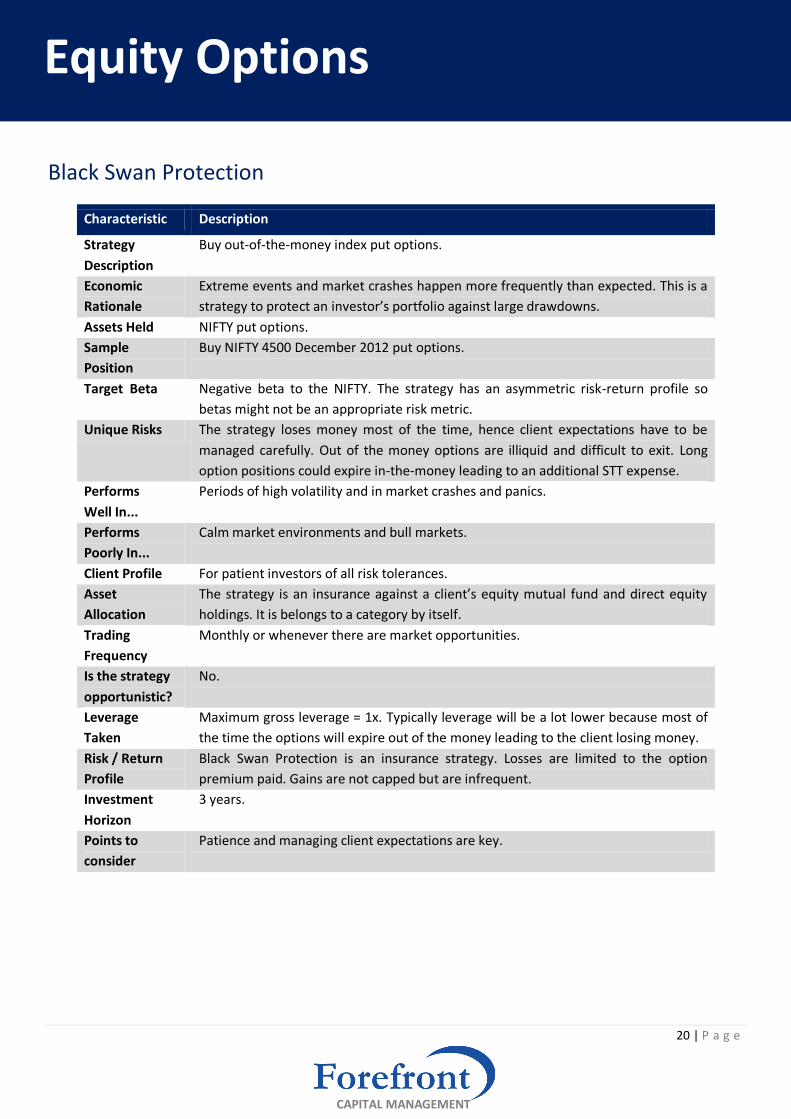

Black Swan Protection

Characteristic Description

Strategy

Description

Buy out-of-the-money index put options.

Economic

Rationale

Extreme events and market crashes happen more frequently than expected. This is a

strategy to protect an investor’s portfolio against large drawdowns.

Assets Held NIFTY put options.

Sample

Position

Buy NIFTY 4500 December 2012 put options.

Target Beta Negative beta to the NIFTY. The strategy has an asymmetric risk-return profile so

betas might not be an appropriate risk metric.

Unique Risks The strategy loses money most of the time, hence client expectations have to be

managed carefully. Out of the money options are illiquid and difficult to exit. Long

option positions could expire in-the-money leading to an additional STT expense.

Performs

Well In...

Periods of high volatility and in market crashes and panics.

Performs

Poorly In...

Calm market environments and bull markets.

Client Profile For patient investors of all risk tolerances.

Asset

Allocation

The strategy is an insurance against a client’s equity mutual fund and direct equity

holdings. It is belongs to a category by itself.

Trading

Frequency

Monthly or whenever there are market opportunities.

Is the strategy

opportunistic?

No.

Leverage

Taken

Maximum gross leverage = 1x. Typically leverage will be a lot lower because most of

the time the options will expire out of the money leading to the client losing money.

Risk / Return

Profile

Black Swan Protection is an insurance strategy. Losses are limited to the option

premium paid. Gains are not capped but are infrequent.

Investment

Horizon

3 years.

Points to

consider

Patience and managing client expectations are key.

21 | P a g e

Arbitrage

CAPITAL MANAGEMENT

Cash Futures Arbitrage

Characteristic Description

Strategy

Description

Profiting from differences between the cash and futures prices of the same security.

Economic

Rationale

Typically: Future Price = Cash Price x (1 + Short Term Interest Rate). However, the

futures price can occasionally trade at a premium to the price implied by short term

interest rates because of demand/supply imbalances.

Assets Held Long: Cash Equities. Short: Single Stock Futures.

Sample

Position

Buy Pantaloon in the cash market, Sell Pantaloon April 2012 futures.

Target Beta Zero.

Unique Risks In a sharp rally the portfolio might run out of cash due to mark-to-market losses on

futures. This might force the manager to unwind positions before arbitrage spreads

have converged. If the futures position cannot be rolled over and the cash positions

cannot be exited, portfolio can be left with a directional exposure to a given stock.

Performs

Well In...

Periods when rates on non-deliverable currency forwards are high because the cost

of FII’s hedging their arbitrage books becomes expensive. The strategy also does well

when stocks hit their FII ownership limits or when short term interest rates are high.

Performs

Poorly In...

Periods when NDF spreads are low, when there are no frictions between the cash

and futures market or when short term interest rates are low.

Client Profile Conservative clients.

Asset

Allocation

Fixed income allocation.

Trading

Frequency

Monthly or whenever there are opportunities.

Is the strategy

opportunistic?

Partially – positions taken whenever there are arbitrage opportunities available.

Futures positions can be rolled monthly to continue to generate debt like returns.

Leverage

Taken

Maximum possible gross leverage (Cash + Futures)= 2x. Gross leverage will likely be

lower because a cash buffer has to be maintained for initial margin and mark-to-

market losses on the futures positions.

Risk / Return

Profile

Cash-futures arbitrage is an interest generating strategy that has the risk / return

profile of a liquid fund.

Investment

Horizon

3-6 months.

Points to

consider

Cash management, portfolio concentration and trading implementation is important.

22 | P a g e

Arbitrage

CAPITAL MANAGEMENT

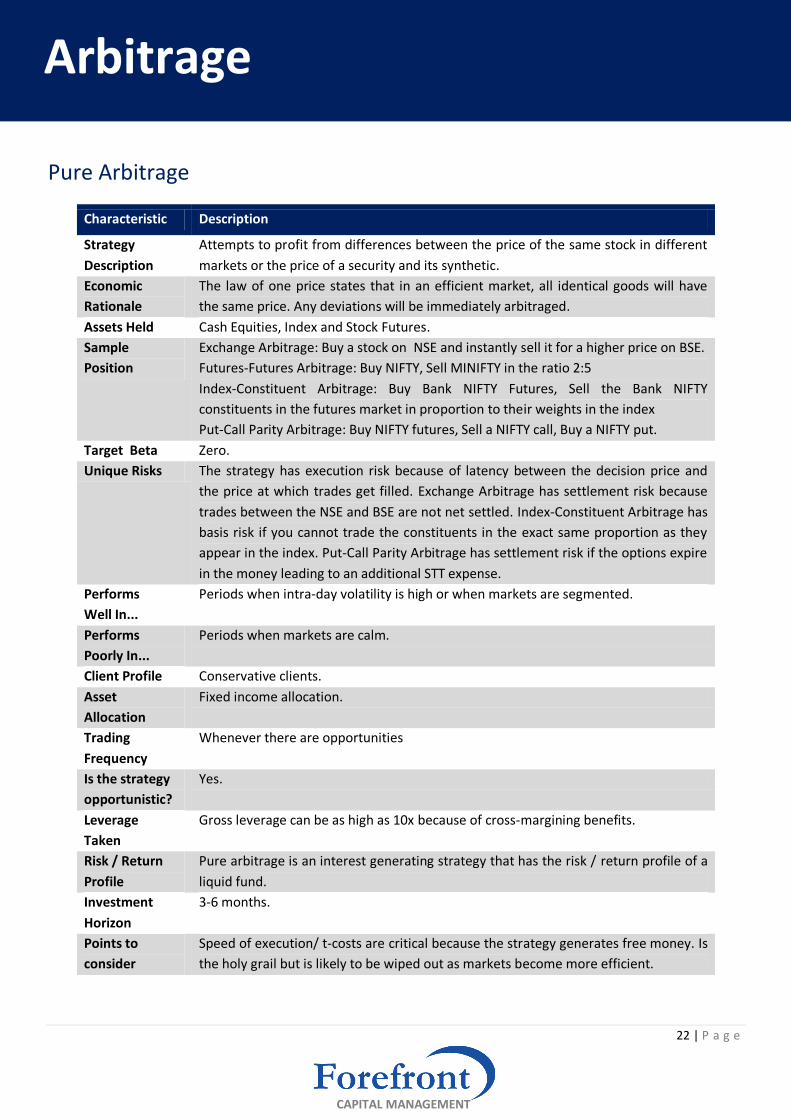

Pure Arbitrage

Characteristic Description

Strategy

Description

Attempts to profit from differences between the price of the same stock in different

markets or the price of a security and its synthetic.

Economic

Rationale

The law of one price states that in an efficient market, all identical goods will have

the same price. Any deviations will be immediately arbitraged.

Assets Held Cash Equities, Index and Stock Futures.

Sample

Position

Exchange Arbitrage: Buy a stock on NSE and instantly sell it for a higher price on BSE.

Futures-Futures Arbitrage: Buy NIFTY, Sell MINIFTY in the ratio 2:5

Index-Constituent Arbitrage: Buy Bank NIFTY Futures, Sell the Bank NIFTY

constituents in the futures market in proportion to their weights in the index

Put-Call Parity Arbitrage: Buy NIFTY futures, Sell a NIFTY call, Buy a NIFTY put.

Target Beta Zero.

Unique Risks The strategy has execution risk because of latency between the decision price and

the price at which trades get filled. Exchange Arbitrage has settlement risk because

trades between the NSE and BSE are not net settled. Index-Constituent Arbitrage has

basis risk if you cannot trade the constituents in the exact same proportion as they

appear in the index. Put-Call Parity Arbitrage has settlement risk if the options expire

in the money leading to an additional STT expense.

Performs

Well In...

Periods when intra-day volatility is high or when markets are segmented.

Performs

Poorly In...

Periods when markets are calm.

Client Profile Conservative clients.

Asset

Allocation

Fixed income allocation.

Trading

Frequency

Whenever there are opportunities

Is the strategy

opportunistic?

Yes.

Leverage

Taken

Gross leverage can be as high as 10x because of cross-margining benefits.

Risk / Return

Profile

Pure arbitrage is an interest generating strategy that has the risk / return profile of a

liquid fund.

Investment

Horizon

3-6 months.

Points to

consider

Speed of execution/ t-costs are critical because the strategy generates free money. Is

the holy grail but is likely to be wiped out as markets become more efficient.

23 | P a g e

Arbitrage

CAPITAL MANAGEMENT

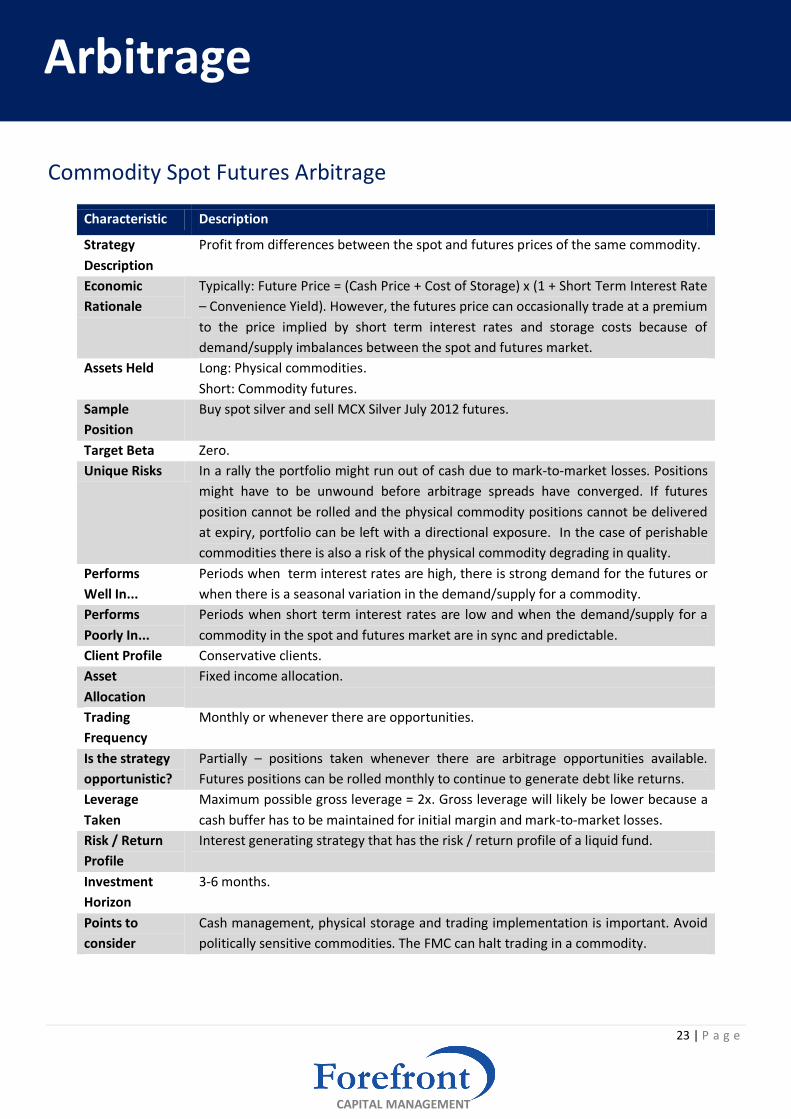

Commodity Spot Futures Arbitrage

Characteristic Description

Strategy

Description

Profit from differences between the spot and futures prices of the same commodity.

Economic

Rationale

Typically: Future Price = (Cash Price + Cost of Storage) x (1 + Short Term Interest Rate

– Convenience Yield). However, the futures price can occasionally trade at a premium

to the price implied by short term interest rates and storage costs because of

demand/supply imbalances between the spot and futures market.

Assets Held Long: Physical commodities.

Short: Commodity futures.

Sample

Position

Buy spot silver and sell MCX Silver July 2012 futures.

Target Beta Zero.

Unique Risks In a rally the portfolio might run out of cash due to mark-to-market losses. Positions

might have to be unwound before arbitrage spreads have converged. If futures

position cannot be rolled and the physical commodity positions cannot be delivered

at expiry, portfolio can be left with a directional exposure. In the case of perishable

commodities there is also a risk of the physical commodity degrading in quality.

Performs

Well In...

Periods when term interest rates are high, there is strong demand for the futures or

when there is a seasonal variation in the demand/supply for a commodity.

Performs

Poorly In...

Periods when short term interest rates are low and when the demand/supply for a

commodity in the spot and futures market are in sync and predictable.

Client Profile Conservative clients.

Asset

Allocation

Fixed income allocation.

Trading

Frequency

Monthly or whenever there are opportunities.

Is the strategy

opportunistic?

Partially – positions taken whenever there are arbitrage opportunities available.

Futures positions can be rolled monthly to continue to generate debt like returns.

Leverage

Taken

Maximum possible gross leverage = 2x. Gross leverage will likely be lower because a

cash buffer has to be maintained for initial margin and mark-to-market losses.

Risk / Return

Profile

Interest generating strategy that has the risk / return profile of a liquid fund.

Investment

Horizon

3-6 months.

Points to

consider

Cash management, physical storage and trading implementation is important. Avoid

politically sensitive commodities. The FMC can halt trading in a commodity.

24 | P a g e

Arbitrage

CAPITAL MANAGEMENT

Statistical Arbitrage / High Frequency Trading

Characteristic Description

Strategy

Description

Attempt to profit from intra-day patterns in market microstructure and high

frequency technical patterns.

Economic

Rationale

Market participants are pre-disposed to certain patterns e.g. buying according to a

volume weighted average price (VWAP) pattern or selling in the last half hour to

target the close price. This leads to intra-day efficiencies.

Assets Held Single stock futures, Index futures, Cash Equities

Sample

Position

Buy NIFTY futures because the market has gapped up, unwind position at the end of

the day.

Target Beta Zero.

Unique Risks Positions might not be able to be unwound at the end of the day leading to overnight

risk. There could be slippage between decision prices and executed prices.

Performs

Well In...

Periods when there are large price-insensitive players in the market. For example, if

all ETFs have to buy the same stock on the close to match their index. The strategy

also does well when intra-day volatility is high.

Performs

Poorly In...

Periods when markets are illiquid or when intra-day volatility is low.

Client Profile Moderate to Aggressive clients.

Asset

Allocation

Absolute return allocation.

Trading

Frequency

Intra-day. Portfolio turnover is high.

Is the strategy

opportunistic?

Can be. Strategies can be event driven i.e. take advantage of ETF trading around an

index reconstitution or always on: Buy the NIFTY if it opens up / Short the NIFTY if it

opens down.

Leverage

Taken

Gross leverage depends on the strength of the manager’s view. Leverage should be

moderate if the manager is taking directional positions intra-day.

Risk / Return

Profile

At 1x gross leverage, the strategy has the risk / return profile of an aggressive

monthly income plan. Individual months or quarters could be negative.

Investment

Horizon

18 months.

Points to

consider

Trading costs and quality of execution are critical for intra-day strategies. Wealth

managers’ reporting systems might misestimate these strategies because end-of-day

reports do not capture the risks of strategies that end each day without any

positions.

25 | P a g e

Arbitrage

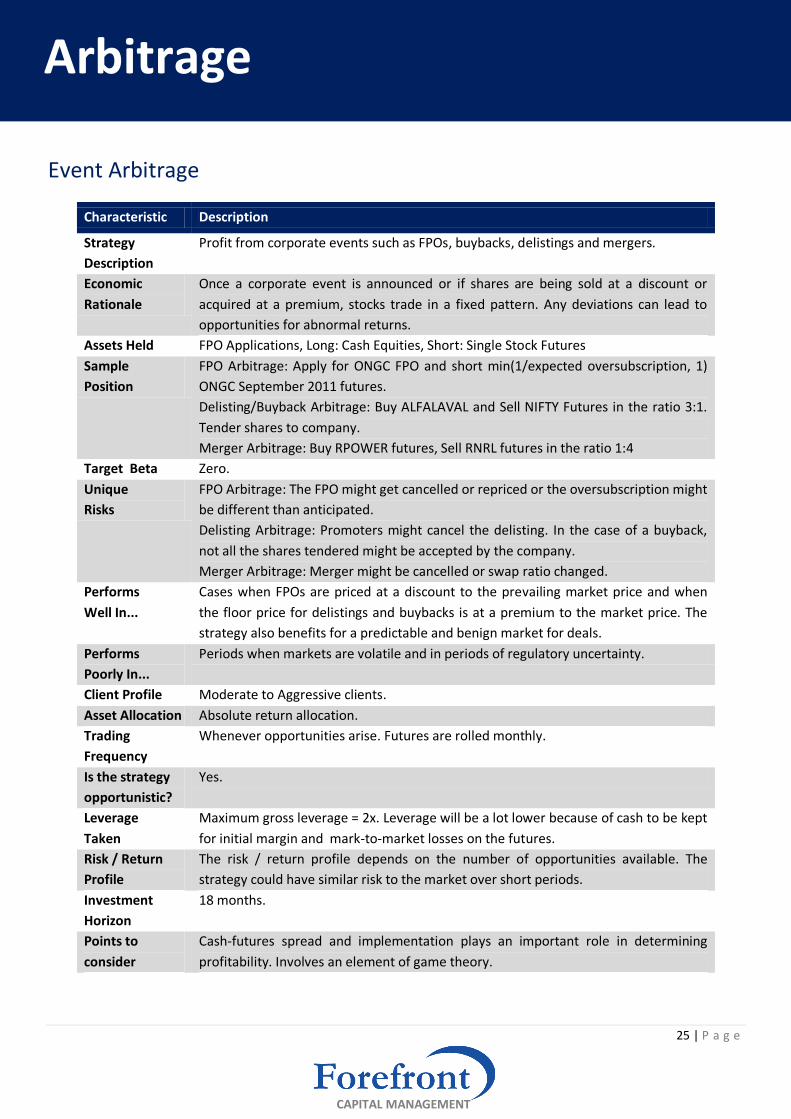

CAPITAL MANAGEMENT

Event Arbitrage

Characteristic Description

Strategy

Description

Profit from corporate events such as FPOs, buybacks, delistings and mergers.

Economic

Rationale

Once a corporate event is announced or if shares are being sold at a discount or

acquired at a premium, stocks trade in a fixed pattern. Any deviations can lead to

opportunities for abnormal returns.

Assets Held FPO Applications, Long: Cash Equities, Short: Single Stock Futures

Sample

Position

FPO Arbitrage: Apply for ONGC FPO and short min(1/expected oversubscription, 1)

ONGC September 2011 futures.

Delisting/Buyback Arbitrage: Buy ALFALAVAL and Sell NIFTY Futures in the ratio 3:1.

Tender shares to company.

Merger Arbitrage: Buy RPOWER futures, Sell RNRL futures in the ratio 1:4

Target Beta Zero.

Unique

Risks

FPO Arbitrage: The FPO might get cancelled or repriced or the oversubscription might

be different than anticipated.

Delisting Arbitrage: Promoters might cancel the delisting. In the case of a buyback,

not all the shares tendered might be accepted by the company.

Merger Arbitrage: Merger might be cancelled or swap ratio changed.

Performs

Well In...

Cases when FPOs are priced at a discount to the prevailing market price and when

the floor price for delistings and buybacks is at a premium to the market price. The

strategy also benefits for a predictable and benign market for deals.

Performs

Poorly In...

Periods when markets are volatile and in periods of regulatory uncertainty.

Client Profile Moderate to Aggressive clients.

Asset Allocation Absolute return allocation.

Trading

Frequency

Whenever opportunities arise. Futures are rolled monthly.

Is the strategy

opportunistic?

Yes.

Leverage

Taken

Maximum gross leverage = 2x. Leverage will be a lot lower because of cash to be kept

for initial margin and mark-to-market losses on the futures.

Risk / Return

Profile

The risk / return profile depends on the number of opportunities available. The

strategy could have similar risk to the market over short periods.

Investment

Horizon

18 months.

Points to

consider

Cash-futures spread and implementation plays an important role in determining

profitability. Involves an element of game theory.

26 | P a g e

CAPITAL MANAGEMENT

Commodities and Currencies

Long Short Commodities

Characteristic Description

Strategy

Description

Long commodities that have are undervalued and/or have strong fundamentals and

short commodities that are overvalued and/or have weak fundamentals.

Economic

Rationale

Commodities for which demand is strong or supply is scarce will outperform

commodities for which demand is weak or supply is abundant.

Assets Held MCX Futures, NCDEX Futures.

Sample

Position

Rank commodities based on their inventory levels. Long commodities that have

falling inventories and short commodities that have rising inventories.

Target Beta Zero beta to the NIFTY, Gold, Oil, Copper or any individual commodity. Portfolios

could have directional exposure to commodities at a given point in time.

Unique

Risks

Agricultural commodities can be politically sensitive. Illiquid markets could be frozen

in an upper or lower circuit for a number of days. The FMC or exchanges could raise

margins forcing levered positions to be cut. Futures positions might not be able to be

rolled over leading to delivery of physical commodities. The cost of carry can be very

high due to commodities being in extreme contango. Net Rupee Exposure can leave

the portfolio exposed to fluctuations in the USD-INR exchange rate because the

prices of many commodities are determined in US Dollars.

Performs

Well In...

Fundamental driven markets.

Performs

Poorly In...

Periods when there is a structural change in a commodity market’s fundamentals.

Client Profile Moderate (low-leverage) to aggressive (high-leverage) clients.

Asset

Allocation

Absolute return allocation. Long Short Commodities cannot be bucketed with gold in

a client’s asset allocation.

Trading

Frequency

Weekly.

Is the strategy

opportunistic?

No.

Leverage

Taken

Leverage can be varied judiciously based on a client’s risk profile. A long-short

portfolio with gross leverage = 1x has an annualized standard deviation of 10%.

Risk / Return

Profile

Should look to deliver 15%-20% with leverage over a 12-18 month period regardless

of what the NIFTY, Gold or any other commodity does. Could be down in a given

month or quarter.

Investment

Horizon

18 months.

Points to

consider

Past experience trading commodities, risk management and implementation are very

important points to consider when evaluating a commodity manager.

27 | P a g e

CAPITAL MANAGEMENT

Commodities and Currencies

Long Short Currencies

Characteristic Description

Strategy

Description

Invest in undervalued currencies, countries with strong macro-economic

fundamentals and those with high interest rates.

Economic

Rationale

Currencies which are undervalued on a purchasing power parity (PPP) basis will

appreciate. Countries with high interest rates and strong economic fundamentals will

attract capital flows leading to an appreciation of their currencies.

Assets Held NSE Currency Futures, MCX Currency Futures.

Sample

Position

Long USD-INR and JPY-INR futures and Short EUR-INR and GBP-INR futures.

Target Beta Zero beta to the NIFTY. Can be managed with a net INR exposure or INR-neutral.

Unique Risks Portfolios with a net INR exposure will be exposed to flows between emerging and

developed markets and sudden flights to safety. Central banks could intervene in

currency markets. Currencies could deviate from PPP for a long periods of time.

Performs

Well In...

Calm market environments for carry based strategies (long high rate currencies, short low rate currencies). Macro/momentum strategies do well in volatile markets.

Performs

Poorly In...

Carry strategies do poorly when volatility is high. Momentum strategies do poorly in

range bound markets.

Client Profile Moderate (low-leverage) to Aggressive (high-leverage) clients.

Asset

Allocation

Absolute return allocation.

Trading

Frequency

Weekly.

Is the strategy

opportunistic?

No.

Leverage

Taken

Leverage can be varied judiciously based on a client’s risk profile. A long-short

currency portfolio with gross leverage = 2x has an annualized standard deviation of

10%.

Risk / Return

Profile

Should look to deliver 15%-20% with leverage over a 12-18 month period regardless

of what the NIFTY does. Could be down in a given month or quarter.

Investment

Horizon

18 months.

Points to

consider

Past experience trading currencies, an understanding of fixed income and risk

management are important for a currency strategy.

28 | P a g e

Multi Asset Class

CAPITAL MANAGEMENT

Tactical Asset Allocation

Characteristic Description

Strategy

Description

Build a long-only portfolio of uncorrelated sources of beta and allocate more to

undervalued asset classes with stronger fundamentals.

Economic

Rationale

Different asset classes perform at different points in time. Combining multiple

uncorrelated asset classes leads to lower risk and more consistent returns.

Assets Held Equities: NIFTY ETFs, NIFTY futures and Mid Cap ETFs.

Global Markets: International Equity funds.

Commodities: Gold ETFs and futures, eSilver and Silver futures, eCopper and Copper

futures, Crude Oil futures

Debt: Liquid funds, Income funds.

Currencies: Currency futures.

Sample

Position

Long 60% NIFTY futures, long 60% gold futures.

Target Beta NIFTY beta: 0 – 0.5.

Unique Risks Cash management is important for levered positions.

Performs

Well In...

Periods when the underlying asset classes do well. Depends on the managers

judgement of asset class performance.

Performs

Poorly In...

Periods when the underlying asset classes do poorly. Depends on the managers

judgement of asset class performance.

Client Profile Moderate risk taking clients.

Asset

Allocation

Absolute return allocation.

Trading

Frequency

Monthly.

Is the strategy

opportunistic?

No.

Leverage

Taken

Gross leverage ranges between 1x and 2x.

Risk / Return

Profile

A diversified portfolio with gross leverage of 1x will have an annualized risk of about

10%. Returns depend on the performance of underlying asset classes but without

leverage such a strategy can generate 12-15% over the long term.

Investment

Horizon

18 months.

Points to

consider

Comparisons between asset classes can be difficult to make. A manager should have

an understanding of asset management issues across asset classes.

29 | P a g e

Multi Strategy Funds

CAPITAL MANAGEMENT

Combining Multiple Strategies

While hedge fund strategies are interesting in themselves, they can be packaged into a more robust and

diversified investment in the form of a multi strategy fund. A multi strategy fund is a combination of two

or more unrelated strategies packaged as a single investment fund. When such a fund combines multiple

absolute return strategies which are uncorrelated (as many of the strategies presented are), the net

outcome is a fund with lower risk than the individual strategies and superior risk adjusted returns. From a

clients and wealth manager’s perspective, since strategies perform differently at different times, this

means more consistent monthly and quarterly performance patterns.

Strategies can be combined into theme based groups such as a collective arbitrage strategy or a collective

long short strategy, or strategies can be combined in a single asset class (a multi strategy equity futures

fund). The focus should be on combining uncorrelated strategies but ones with a similar client profile. For

instance combining a 130-30 equities strategy with a tactical asset allocation strategy is not a great idea

because both have long only equity exposure which overlaps. Of the range of options available, Forefront

has identified a few multi strategy fund examples that sensibly combine the above strategies.

Fund Summary Sub Strategies

Equity Futures Fund

A combination of absolute return oriented

equity futures strategies

1. Long Short Equities

2. Directional Equities

3. Pairs Trading

4. Managed Futures

5. Statistical Arbitrage

6. Event Arbitrage

Equity Options Fund

A combination of absolute return oriented

options trading strategies

1. Volatility Trading

2. Correlation Trading

3. Black Swan Protection

Arbitrage Fund

A combination of low risk arbitrage oriented

strategies with a fixed income profile

1. Cash Futures Arbitrage

2. Pure Arbitrage

3. Commodity Spot Futures Arbitrage

Commodities Fund

A combination of absolute return oriented

commodities strategies

1. Long Short Commodities

2. Commodity Spot Futures Arbitrage

Multi Asset Class Long Short Fund

A combination of absolute return long short

strategies across asset classes

1. Long Short Equities

2. Long Short Commodities

3. Long Short Currencies

30 | P a g e

CAPITAL MANAGEMENT

References and Disclosures

References

Allen S., Financial Risk Management – A Practioner’s Guide to Managing Market and Credit Risk, John

Wiley 2003

Andrade S., di Pietro V. and Seasholes M. “Understanding the Profitability of Pairs Trading”, Working

Paper, University of California, Berkeley and Northwestern University.

Asness C., Krail R. and Liew J. “Do Hedge Funds Hedge?”, AQR Capital Management LLC

Baillie R. and Bollerslev T., 2000, “The Forward Premium Anomaly is Not as Bad as You Think”, Journal of

International Money and Finance, 19(4), 471-488.

Bakshi G. and Kapadia N., 2003, “Delta-Hedged Gains and the Negative Market Volatility Risk Premium”,

Review of Financial Studies, 16(2), 527-566.

Bakshi G., Kapadia N. and Madan D., 2003, “Stock Return Characteristics, Skew Laws and the Differential

Pricing of Individual Equity Options”, Review of Financial Studies, 16(1), 101-143.

Balassa B., 1964, “The Purchasing-Power-Parity Doctrine: A Reappraisal”, Journal of Political Economy, Vol.

72. No 6., December, 584-596.

Bansal R. and Dahlquist M., 2000, “The Forward Premium Puzzle: Different Tales from Developed and

Emerging Economies”, Journal of International Economics, 51, 115-144.

Bhansali V., 2007, “Volatility and the Carry Trade”, The Journal of Fixed Income, 72-84.

Britten-Jones M. and Neuberger A., 2000, “Option Prices, Implied Price Processes, and Stochastic

Volatility”, Journal of Finance, 55, 839-866.

Brown S. and Goetzmann W. “Hedge Funds with Style”, Yale ICF Working Paper No. 00-29

Brown S., Fraser T. And Liang B., “Hedge Fund Due Diligence: A Source of Alpha in a Hedge Fund Portfolio

Strategy”, Working Paper

Burnside C., Eichenbaum M., Kleshchelski I. and Rebelo S., 2006, “The Returns to Currency Speculation”,

NBER working paper.

Carhart M., 1997, “On Persistence in Mutual Fund Performance”, Journal of Finance, vol. 52, no. 1 (March):

57-82

Chan N., Getmansky M., Haas S. and Lo A., “Systemic Risk and Hedge Funds”, MIT Sloan Research Paper No.

4535-05

31 | P a g e

CAPITAL MANAGEMENT

References and Disclosures

References

Chinn M., 2006, “The (Partial) Rehabilitation of Interest Rate Parity: Longer Horizons, Alternative

Expectations and Emerging Markets”, Journal of International Money and Finance, 25(1), 7-21.

Clark K., “Managing a Portfolio of Hedge Funds”, Modern Investment Management – An Equilibrium

Approach, Chapter 27

Connor G. and Korajczyk R., 1993, “A Test for the Number of Factors in an Approximate Factor Model”,

Journal of Finance, Volume 48, 1263-1291.

Conrad J. and Kaul G., 1989, “Mean Reversion in Short-horizon Expected Returns”, Review of Financial

Studies, 2, 225-240.

Daniel K., Hirshleifer D. and Subrahmanyam A. 1998 “Investor Psychology and Security Market Under and

Overreactions”, Journal of Finance, Volume 53, Issue 6, 1839–1885.

Dash M., Kodagi M., Babu N. and Vivekanand B.Y., 2008, “An Empirical Study of FOREX Risk Management

Strategies”, Indian Journal of Finance, Vol.2, No. 8

De Long J., Shleifer A., Summers L. and Waldmann R. 1990, “Noise Trader Risk in Financial Markets”,

Journal of Political Economy, vol. 98, no. 4 (August):703-738

Erb C. and Harvey C., 2006, “The Strategic and Tactical Value of Commodity Futures”, Financial Analysts

Journal, vol 62, no. 2 March / April: 69-97

Engelberg J., Gao P. and Jagannathan R. 2009, “An Anatomy of Pairs Trading: The Role of Idiosyncratic

News, Common Information and Liquidity”, Working paper, University of North Carolina at Chapel Hill,

University of Notre Dame and Northwestern University.

Fama E., 1984, “Forward and Spot Exchange Rates”, Journal of Monetary Economics, 14, 319-338.

Fama E., “The Behavior of Stock-Market Prices”, Journal of Business, vol. 38, no. 1 (January): 34-105.

Fama E. and French K., 1993, “Common Risk Factors in the Returns on Stocks and Bonds”, Journal of

Financial Economics, vol. 33, no. 1 (February): 3-56

Fama E. and French K., 1996, “Multifactor Explanations of Asset Pricing Anomalies,” Journal of Finance, 51,

131-155.

32 | P a g e

CAPITAL MANAGEMENT

References and Disclosures

References

Froot K. A. and Rogoff K., 1995, “Perspectives on PPP and Long-Run Real Exchange Rates”, NBER Working

Paper No. 4952, December, Cambridge, Massachusetts

Fung W. and Hsieh D., “Empirical Characteristics of Dynamic Trading Strategies: The Case of Hedge Funds”,

The Review of Financial Studies Summer 1997 Vol. 10, No. 2, 275–302.

Fung W., Hsieh D., Ramadorai T. and Naik N. 2008 “Hedge Funds: Performance, Risk, and Capital

Formation”, The Journal of Finance, Vol. 63, No. 4.

Gatev E., Goetzmann, W. and Rouwenhorst K., 2006, “Pairs Trading: Performance of Relative Value Rule”,

Yale ICF Working Paper No. 08-03.

Gorton G. and Rouwenhorst K., 2006, “Facts and Fantasies about Commodity Futures”, Financial Analysts

Journal, vol. 62, no. 2 (March/April): 47-68

Graham B., The Intelligent Investor, edited by Jason Zweig, Harper Collins 2003

Graham B. and Dodd D., Security Analysis, 6th edition, McGraw-Hill 2009

Greenblatt J., You Can Be a Stock Market Genius, Simon & Schuster 1997

Klarman S., Margin of Safety: Risk-Averse Value Investing Strategies for the Thoughtful Investor.

HarperCollins 1991

Hansell S., 1989, “Inside Morgan Stanley's Black Box”, Institutional Investor, (May) 204-216

Harvey C., Liechty J., Liecthy M. and Muller P. “Portfolio Selection with Higher Moments”, Quantitative

Finance, vol. 10, no. 5 (May): 469-485.

Hautsch N. and Inkmann, J., 2003, “Optimal Hedging of the Currency Exchange Risk Exposure of

Dynamically Balanced Strategic Asset Allocations”, Journal of Asset Management, 4(3).

Hogan S., Jarrow R., Teo M. and Warachka M., 2004. “Testing Market Efficiency Using Statistical Arbitrage

with Applications to Momentum and Value Strategies” Journal of Financial Economics, vol. 73, no. 3

(September): 525-565

Hong H. and Stein J., 1999, “A Unified Theory of Underreaction, Momentum Trading, and Overreaction in

Asset Markets”, Journal of Finance, Volume 54, Issue 6, 2143–2184

Ibbotson R. and Chen P. “The A,B,Cs of Hedge Funds: Alphas, Betas, and Costs”, Yale ICF Working Paper No.

06-10

33 | P a g e

CAPITAL MANAGEMENT

References and Disclosures

References

Idzorek T., 2006, “Strategic Asset Allocation and Commodities”, Ibbotson Associates.

Jegadeesh N. and Titman S., 1993, “Returns to Buying Winners and Selling Losers: Implications for Stock

Market Efficiency”, Journal of Finance, 48, 65-91.

Jegadeesh N. and Titman S., 1995, “Overreaction, Delayed Reaction, and Contrarian Profits”, Review of

Financial Studies, 8, 973-93.

Liang B., “On the Performance of Hedge Funds”, University of Massachusetts at Amherst Working Paper

Lioui A. and Poncet P., 2005, Dynamic Asset Allocation with Forwards and Futures, Springer

Lo, A., “Risk Management for Hedge Funds: Introduction and Overview”, MIT Working Paper Series.

Lopez de Prado M. and Peijan A., 2004, “Measuring Loss Potential of Hedge Fund Strategies”, Journal of

Alternative Investments, Vol. 7, No. 1, pp. 7-31.

Lustig H., Roussanov N. and Verdelhan A., 2008, “Common Risk Factors in Currency Markets”, working

paper.

Mitchell M., Pulvino T. And Stafford E., 2002, “Limited Arbitrage in Equity Markets”, Journal of Finance, vol.

57, no. 2 (April): 551-584.

Obstfeld M. and Rogoff K., Foundations of International Macroeconomics, Cambridge, Massachusetts: MIT

Press 1998

Patton A., 2004, “On the Out-of-Sample Importance of Skewness and Asymmetric Dependence for Asset

Allocation”, Journal of Financial Econometrics, vol. 2, no. 1 (January):130-168.

Rogoff K., 1996, “The Purchasing Power Parity Puzzle”, Journal of Economic Literature, Vol. 34, No. 2, June,

647-668

Still G., 2009, “Crowd Dynamics in the Foreign Exchange Market,” Working Paper

Swensen, D. Unconventional Success: A Fundamental Approach to Personal Investment. New York: Free

Press 2005

Taleb N. The Black Swan: The Impact of the Highly Improbable, Penguin 2007

34 | P a g e

CAPITAL MANAGEMENT

References and Disclosures

References

Taleb N. Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets, Penguin 2001.

Ubide A., 2006, “Back to Basics”, Finance and Development, Volume 43, Number 2

Walmsley J., International Money and Foreign Exchange Markets: An Introduction, John Wiley and Sons

1996.

Winkelmann K., Clark K., Rosengarten J. and Tyagi T., “Strategic Asset Allocation and Hedge Funds”,

Modern Investment Management – An Equilibrium Approach, Chapter 26

35 | P a g e

CAPITAL MANAGEMENT

References and Disclosures

Disclosures