for personal use only - asx.com.au · 4 phoenix copper limited | annual report 2011 3 tenements...

TRANSCRIPT

ANNUAL REPORT 2011

For

per

sona

l use

onl

y

Share RegistryComputershareLevel 5, 115 Grenfell StreetAdelaide SA 5000

Telephone (within Australia) 1300 305 232

Telephone (outside Australia) +61 (3) 9415 4657

AuditorsDeloitte Touche Tohmatsu11 Waymouth StreetAdelaide SA 5000

LawyersWatsons Lawyers60 Hindmarsh SquareAdelaideSA 5000

ASXThe Company’s fully paid ordinary shares are quoted on ASX. The ASX code is PNX.

Corporate directory

Australian Business Number 67 127 446 271

Country of Incorporation Australia

Board of DirectorsGraham Spurling ChairmanPaul Dowd Managing Director and CEOPeter Watson Non-executive DirectorDavid Hillier Non-executive Director

Company SecretaryPeta Marshman

Principal Administrative OfficeLevel 1, 135 Fullarton RdRose ParkSA 5067

Telephone +61 (8) 8364 3188

Facsimile +61 (8) 8364 4288

Registered OfficeLevel 1135 Fullarton RdRose ParkSA 5067

Telephone +61 (8) 8364 3188

Facsimile +61 (8) 8364 4288

Contact [email protected]

Website www.phoenixcopper.com.au

For

per

sona

l use

onl

y

1PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

Chairman’s Letter 2

Overview 3

Operations and Exploration Report 7

Mineral resources and ore reserves 15

Directors’ Report 16

Remuneration Report 22

Corporate Governance Statement 29

Auditor’s Independence Declaration 33

Financial Statements 34

Directors’ Declaration 61

Independent Audit Report to Members 62

Additional Shareholder Information 64

Contents

For

per

sona

l use

onl

y

2 PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

Chairman’s Letter

Dear Shareholder,

I would like to report on the events of this past year.

The operations at our Mountain of Light mine at Leigh Creek proved to be far more challenging than we considered at the time of purchase. The technical and economic assumptions based on previous existing geological data proved to be inaccurate. We have persevered with the operation for a sufficient period to truly test its potential and to build a realistic data base for utilisation at this and other potential sites.

We are disappointed that we have been unable to establish a viable operation that would partly fund exploration. However with our new operational history based on actual experience, it is now appropriate that we complete a thorough feasibility study to determine whether the application of our new parameters will result in an economically sound mining venture. This study, to be completed early in 2012, will be verified by an on site testwork program.

It continues to be our belief that the corporate model that we have developed can distinguish us from many of our peers. Our model consists of a mix of assets that will establish us as a producer, a developer and an explorer for copper, gold, and copper/ gold—not simply just another junior explorer. Our modelling and testwork of the Leigh Creek ore types is aimed at verifying the economics of the project.

Other copper assets, wholly owned by Phoenix Copper, are at advanced stages of exploration and Lorna Doone is available for development. Their development will be subjected to rigorous assessment based on our experience at Mountain of Light.

Regarding the Burra region, the significant IP anomaly along strike to the north west of the Monster Mine (Burra North Prospect) is an exciting exploration opportunity and, together with the prospect at Yorke Peninsula, will be the primary areas of exploration focus in the coming year. As an explorer, Phoenix Copper is fortunate to hold some extremely prospective land under 100% controlled Exploration Licences from Burra to Kapunda and on the Yorke Peninsula. Since the discovery of the Hillside deposit by Rex Minerals Limited (Rex), the Yorke Peninsula has attracted a great deal of excitement and investment. On 27 July 2011 Rex announced a resource of 1.5Mt Copper and 1.4Moz Gold. Phoenix Copper and Wellington Exploration Pty Ltd (a wholly owned subsidiary of Phoenix Copper) own Exploration Licences immediately adjacent to the Rex tenements. The tenements encompassed by our Exploration Licences display similar characteristics to Moonta-style mineralisation and the mineralisation at Hillside, Prominent Hill and Carapateena.

This highly prospective area of Yorke Peninsula will be the primary focus of our exploration efforts. The potential outcomes could be transformational for the Company.

Thank you for your support so far. Your Board and management maintain confidence in Phoenix Copper’s exciting future.

Yours sincerely

Graham SpurlingC H A I R M A N

26 September 2011

For

per

sona

l use

onl

y

3PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

1 GENERALThe nature of the business of Phoenix Copper Limited (Phoenix Copper or the Company) includes mining and processing operations within granted mining leases, held by its wholly-owned subsidiary Leigh Creek Copper Mine Pty Ltd (LCCM) and exploration within its granted mining leases and exploration licenses, all within South Australia.

2 LEIGH CREEK OPERATIONSCompletion of the acquisition of LCCM was achieved on 23 July 2010.

The operation is a heap leach process and involves preparing the mined ore by crushing, and removing the “fines” through screening. The resultant “coarse” material is then stacked onto prepared compacted and lined “pads” where the ore is then irrigated with a dilute acid solution to leach the contained copper into solution.

The product produced is a copper cement and is subject to an off-take agreement with Adchem (Australia) Pty Ltd, (Adchem), a company based in Burra and adjacent to Phoenix Copper’s exploration base for its Spalding/Burra tenements. Mining is by conventional open pit methods and was conducted by mining contractor personnel, under Phoenix Copper management and direction. Two pits, Rosmann East and Paltridge South, were mined during the period of operations.

Production of copper cement began at the end of August 2010 and the first product sale was on 15 September 2010.

Overview

Figure 1 Phoenix Copper Limited tenure July 2011.

For

per

sona

l use

onl

y

4 PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

3 TENEMENTSPhoenix Copper (and through Wellington Exploration Pty Ltd – its wholly owned subsidiary), holds 20 ELs (Exploration Licenses), covering 4,405km2 and three MLs (Mining Leases), covering 572Ha, a total area of tenements in excess of 4,411km2 in the historically significant and highly prospective Burra, Kapunda, Leigh Creek and Yorke Peninsula regions of South Australia as shown in the following table and Figure 1.

4 PERMITTING

Lorna Doone Mining Lease ML5498, was renewed during the period and now has an expiry date of 17 January 2016.

Exploration Licence No Exploration Licence name Area (sq km) Grant date Registered holder

BURRA GROUP 2,3374226 Burra Central 86 24/02/2009 Phoenix Copper 100%3604 Burra West 69 25/07/2006 Phoenix Copper 100%3716 Burra North 300 6/03/2007 Phoenix Copper 100%4233 Mongolata 283 10/03/2009 Phoenix Copper 100%4032 Mount Bryan 116 21/01/2008 Wellington Exploration 100%3549 Princess Royal 314 1/05/2006 Phoenix Copper 100%4419 Red Banks 396 21/01/2010 Phoenix Copper 100%4476 Hallett Hill 80 27/04/2010 Phoenix Copper 100%4504 The Gums 160 31/05/2010 Phoenix Copper 100%3971 Anabama 465 5/11/2007 Phoenix Copper 100%4711 Burra Creek Plain 68 29/03/2011 Phoenix Copper 100%

YORKE PENINSULA GROUP 8024031 Minlaton 547 21/01/2008 Wellington Exploration 100%4312 Koolywurtie 255 30/09/2009 Phoenix Copper 100%

SPALDING GROUP 489 3686 Spalding 157 2/01/2007 Phoenix Copper 100%4362 Mt Tinline 123 4/11/2009 Phoenix Copper 100%4370 Washpool 209 10/11/2009 Phoenix Copper 100%

EUDUNDA GROUP 7774291 Bagot Well 71 5/08/2009 Phoenix Copper 100%4503 Australia Plains 222 31/05/2010 Phoenix Copper 100%3451 Bagot Well North 142 15/11/2005 Phoenix Copper 100%3972 Tarnma 342 5/11/2007 Phoenix Copper 100%

Total ELs 4,405

Mining Lease No Mining Lease Name Area (Ha) Grant date Registered holder

LEIGH CREEK GROUP 572ML 5467 Mountain of Light 250 16/10/1987 LCCM 100%ML 5741 Mount Coffin 200 3/06/1991 LCCM 100%ML 5498 Lorna Doone 122 18/01/19881 LCCM 100%

Total all tenements 4,411 sq km

1 Mining Lease ML5498 was renewed during the period and now has an expiry date of 17 January 2016.

For

per

sona

l use

onl

y

5PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

5 DISCOVERIES DURING THE PERIOD

Yorke Peninsula Project(see Figures 1, 2 and 3 and Operations and Exploration Report section 2.2)

Thirteen broad exploration target zones defined from construction of a 3D unconstrained inversion model of the regional aeromagnetic data.

Burra Project(see Figures 1 and 4 and Operations and Exploration Report section 2.3)

Significant copper and gold mineralisation in Reverse Circulation (RC) drilling at Princess Royal including:

Copper PCRC007 – 6.8m @ 3.7% Cu from 0.84m and

Gold PCRC021 – 7.0m @ 2.5g/t Au from 4.0m

Mongolata Project(see Figures 1 and 9 and Operations and Exploration Report section 2.6)

Zones of high copper anomalism were found in Field Portable X-Ray Fluorescence Analysis (FPXRF) around the rim of a strong magnetic high in central EL3971.

Spalding Project(see Figures 1, 6 and 7 and Operations and Exploration Report section 2.4)

A Rotary Air Blast (RAB) drilling program around the old Wheal Sarah copper mine 10km north west of Spalding. Encouraging results included; PCRB0070 – 5m @ 0.61%Cu.

Eudunda Project(see Figures 1, 8 and 9 and Operations and Exploration Report section 2.5)

FPXRF analysis continued and zones of most interest found in sampling to date are at Tarnma in the south west of EL3972 and in the north west of EL4626, and at Bagot Well in central EL4291.

Leigh Creek Project(see Figures 1, 10 and 11 and Operations and Exploration Report section 2.7)

Lorna Doone -ML5498

A program of close spaced FPXRF analysis was undertaken over ML5498. Significant anomalism was detected away from the planned pits.

Mount Coffin -ML5741

A program of close spaced FPXRF analysis confirmed the presence of copper around the historic workings, extended this into areas along strike and also identified new areas of interest.

6 SUMMARY OF EXPLORATION UNDERTAKEN ON PHOENIX COPPER TENEMENTS DURING THE PERIOD969m of reverse circulation drilling was completed.

3,811m of RAB drilling was completed.

38,619 FPXRF analyses taken of soils.

3,811 FPXRF analyses taken on RAB samples with checks and standards.

Bud Norris, Field Assistant at the Burra office.

For

per

sona

l use

onl

y

6 PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

507 RAB drill samples sent to the laboratory for copper assay.

969 RC drill samples sent to the laboratory for copper and gold assay.

7 CASH AT HANDCash at Hand as at 30 June 2011 was approximately $1.1 million.

8 ACQUISITIONS DURING THE PERIODApart from LCCM which is reported below, there were no mining leases acquired during the year. Exploration license EL4711 “Burra Creek Plain” was applied for and granted during the year.

LCCMCompletion of the acquisition of LCCM was achieved on 23 July 2010 and the assets subject to the purchase included:

ML 5467 Mountain of Light 250Ha

ML 5741 Mount Coffin 200Ha

ML 5498 Lorna Doone 122Ha

9 CAPITAL RAISEDDuring the financial year Phoenix Copper raised a total of $7,078,930 as follows:

Share purchase plan issuing 2,400,000 ordinary shares at 16c per share on 7 July 2010

Placement issuing 11,875,000 ordinary shares at 16c per share on 23 July 2010

Placement issuing 2,000,000 ordinary shares at 16c per share on 30 July 2010

Placement issuing 6,896,552 ordinary shares at 29c per share on 15 October 2010

Placement issuing 1,724,138 ordinary shares at 29c per share on 1 December 2010

Placement issuing 7,053,320 ordinary shares at 28c per share on 11 March 2011

For

per

sona

l use

onl

y

7PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

Operations and Exploration Report

1 OPERATIONS – LEIGH CREEKCompletion of the acquisition of LCCM was achieved on 23 July 2010, when ownership and control of LCCM passed to Phoenix Copper.

The product produced by LCCM is a copper cement and is subject to an off-take agreement with Adchem (Australia) Pty Ltd, (Adchem), a company based in Burra and adjacent to Phoenix Copper’s exploration base for its Spalding/Burra tenements.

Production of copper cement began at the end of August 2010 and the first product sale was on 15 September 2010.

All mining, crushing and stacking operations at Mountain of Light (MoL) were completed. The leaching of copper continues and it is estimated that all production will cease by November 2011.

1.1 MiningMining for the 11 month period since completion of the acquisition of LCCM was confined to Rosmann East and Paltridge South. Oxide copper ore remains in the Rosmann East pit with sulphide copper beneath the remaining oxide copper resource.

Paltridge South pit was developed and mined to remove all available copper ore down to the level of the water table, where mining ceased.

All mining and crushing/screening activities have been curtailed and modest revenue continues to be generated from existing heap leach pads, which are likely to be depleted of available copper by end-November 2011.

1.2 ProcessingAfter purchase completion, the operation was released from “care-and-maintenance” and the leach pad area and the plant extensively refurbished, with a previously-owned filter press installed. Mined ore was placed onto a Run-of-Mine (ROM) stockpile, reclaimed from the ROM and presented for crushing and screening to reject “fines” material, considered unsuitable for leaching. The remaining coarse ore was stacked onto heaps on specially prepared pads for leaching by dilute acid solution. During the period a new leach pad was constructed, ore stacked on all three pads and placed under irrigation for leaching of copper product.

Copper dissolved in the acid solution was then recovered into a copper cement product produced through an iron exchange process, with thin section, high quality scrap steel, in a Kennecott Cone reactor.

A wet analytical laboratory has been operating at MoL since late 2010 and provided pH, acid concentrations, copper and other analyses for the heap leach operations.

A sample preparation laboratory to prepare all samples, including drill cuttings, ore blast holes, and rock samples was completed during the period.

Additionally, the on-site facility provides an analytical service for MoL and most of Phoenix Copper’s future exploration sampling.

1.3 Production Annual

Copper cement product produced

Wet weight

Dry weight

Contained Cu t

% H2O Cu% wet

Cu% dry

Total to 30 June 2011

508.1 378.2 300.62 25.6% 59.2% 79.5%

2 Sales during the period were 293.97 tonnes of copper contained in product.

2 EXPLORATION

2.1 OverviewWith the purchase of LCCM, Phoenix Copper’s exploration activities were broken into six projects (see Figure 1).

significant primary copper or copper/gold resource similar to Moonta or Hillside was the main focus of activity.

concentrated on exploring for and proving up near surface copper carbonate and oxide resources to feed a potential second treatment facility at Burra.

exploring for and proving up gold and uranium resources

areas, exploring for and proving up near surface copper carbonate and oxide resources to feed the Mountain of Light treatment facility and exploring for deep large tonnage copper resources.

For

per

sona

l use

onl

y

8 PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

2.2 Yorke Peninsula Project(Figures 1 and 2)

2.2.1 Highlights

Completion of a 3D unconstrained inversion model of the regional aeromagnetic data.

Exploration target zones defined.

Deep seated anomalies seen to persist through all rock to a depth of 800m present the highest priority targets.

Evaluation of the geological settings and geophysical techniques used by others to find, target and delineate known Iron-Oxide-Copper-Gold-Uranium (IOCGU) deposits completed.

Most prospective targets are for “Hillside” or “Moonta” style mineralisation.

Planned a “VTEM,” (Versatile Time-Domain Electro-Magnetics), airborne electromagnetic survey using a helicopter platform to map possible mineralisation associated with inferred geological structures.

Applied for “PACE Targeting 2011” funding for the planned “VTEM” air-borne geophysical survey.

2.2.2 Strategy and Prospectivity

Phoenix Copper’s Minlaton (EL4031) and Koolywurtie (EL4312) tenements which cover an area ~802km2 on the west coast of the Yorke Peninsula remain almost unexplored. These tenements overly metasomatised Hiltaba suite rocks, disrupted by major faults, less than 30km from, and neighbouring, the Hillside deposit,

Phoenix Copper is greatly encouraged by the developments in geological, geophysical and structural understanding and modelling by Rex Minerals Limited (Rex) on the Yorke Peninsula and its subsequent exploration successes and resource discoveries, recently announced.

Phoenix Copper has recently completed a review of its data on both exploration licenses (EL4031 and EL4312) that adjoin and partly surround the tenements owned by Rex and determined striking similarities (including trace levels of nickel and copper sulphides in historic drillholes at the Balgowan Prospect) to those areas that host both the Hillside deposit and the Moonta Copper field.

Structure(Figure 3)

Rex’s Hillside Deposit is hosted in the Pine Point Fault. Mineralisation at Moonta is mainly hosted in north east trending faults and shears.

After extensive review of the available geophysical data by Phoenix Copper and a consultant geophysicist it has been concluded that Phoenix Copper’s Yorke Peninsula tenements host:

Structures that appear contemporaneous and splay off the Pine Point Fault.

A structure that is interpreted as the south western extension of the Pine Point Fault.

North east trending and other significant structures that disrupt the Hiltaba Suite in Phoenix Copper’s exploration licenses.

2.2.3 Exploration during the year on Phoenix Copper’s Yorke Peninsula tenure

3D Model of Aeromagnetic Data

A 3D unconstrained inversion model of the regional aeromagnetic data over Phoenix Copper’s project was completed during the period. The data was modelled in 200m cubes identifying targets with good strike and depth extent, estimates of depth to the magnetic anomalies, and providing data to re-evaluate the geological setting (See Figure 3). Thirteen broad targets (T1-T13) were identified for drill testing in the northern tenement block, four of these T9-11 and T13 are deep targets but the remainder occur within 50-100m of the surface.

Targets of the highest priority are those deep seated anomalies that are seen to persist through all 800m of the data e.g. T12 in Figure 3. These are considered the most prospective for “Hillside” or “Moonta” style mineralisation.

Figure 2 Phoenix Copper tenure relative to Olympic Domain IOCGU deposits.

AUSTRA L IA

SOUTHAUSTRALIA

Prospective area forIOCGU depositsCariewerloo Basin

IOCGU mines & major prospects

Adelaide Geosyncline

Torrens Hinge Zone

Phoenix Copper Tenements

For

per

sona

l use

onl

y

9PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

The 3D modelling of the regional aeromagnetics has provided a greater degree of targeting confidence and, combined with a planned airborne electro-magnetics survey, will allow drill collars to be precisely located. It is notable that Rex defined high priority drill targets based on coincident magnetic and electro-magnetic data3. The planned airborne electro-magnetics survey will map massive sulphides associated with inferred structures to depths of 200m targeted using the regional magnetics.

2.2.4 Yorke Peninsula and the Olympic Domain(Figure 2)

An outstanding exploration opportunity is presented (if the Company’s current rights issue is successful), in what has become a new copper/gold province within the Olympic Domain (see Figure 2), with the discoveries of Prominent Hill, Carapateena, and now, Hillside, to complement Olympic Dam – one of the world’s most prominent orebodies. The recent discovery of the Hillside deposit by Rex has confirmed that the Olympic Domain extends south from Prominent Hill, Olympic Dam and Carapateena to the Yorke Peninsula. The style of these deposits is known as Iron Oxide-Copper-Gold-Uranium (IOCGU). Exploration success in these types of geological environments can transform a junior explorer to a significant mining company.

The giant Olympic Dam, deposit contains over 78 million tonnes of copper and 90 million ounces of gold4 – amongst the richest orebodies in the world.

At June 2009 Oz Mineral’s Prominent Hill was reported as containing a total of 2.5 million tonnes of copper and over 3 million ounces of gold in the copper mineral resource.5

Rex recently announced a mineral resource containing 1.5 million tonnes of copper and 1.4 million ounces of gold.6

The Company’s Yorke Peninsula tenements, Minlaton (EL4031) and Koolywurtie (EL4312) are contiguous, and Koolywurtie bounds, the tenements held by Rex. In the north they are in close proximity to the Moonta-Wallaroo region, generally known as the “Copper Triangle” which is an historic mining region that produced >355,000 tonnes of copper and 64,000 ounces of gold.7

3 Rex - ASX and Media Release: 17 September, 2009

4 (9080 Mt at 0.87% Cu, 0.28 kg/tU3O8, 0.31 g/t Au, 1.5 g/t Ag) - Resource data from PIRSA, July 2011, South Australia’s Major Operating Mines and Mineral Development Projects Resource Estimates and Production Statistics.

5 Prominent Hill Mineral Resource Statement - 30 June 2009, (189.7 Mt at 1.32% Cu, 0.5 g/t Au, 3.1 g/t Ag).

6 Rex Minerals Limited Hillside Resource Upgrade (217 Mt at 0.7% Cu and 0.2g/t Au) - Resource data from PIRSA, July 2011, South Australia’s Major Operating Mines and Mineral Development Projects Resource Estimates and Production Statistics.

7 Keeling,J.L. and Hartley,K.L. Poona and Wheal Hughes Cu Deposits, Moonta, South Australia, CRC/LME PIRSA SA.

Phoenix Copper has therefore carefully modelled exploration target types similar to Moonta-Wallaroo and IOCGU style deposits, not simply because of the close proximity of these deposits, but because the “signatures” for these deposits (structure, geology, magnetics and gravity) (see Table 1), generally persist at Minlaton (EL4031) and Koolywurtie (EL4312)tenements. In the two northern blocks the cover sequence is generally thin and will allow relatively shallow and low-cost drilling. Table 1 provides a comparison of the prospectivity for IOCG/IOCGU (Hillside) and Moonta-Wallaroo style deposits within Minlaton (EL4031) and Koolywurtie (EL4312).

A 3D unconstrained inversion model of the regional aeromagnetic data over Phoenix Copper’s project was completed during the period to end-June 2011. The data identified targets with strong magnetic signatures; good strike and depth extent.

Thirteen broad exploration target areas (T1-T13) have been defined from modelling the regional geophysical data, historic geochemical sampling and recent Field Portable X-Ray R Fluorescence (FPXRF) analyses. Four of these T9-11 and T13 are deep targets but the remainder are interpreted to occur within 50-100m of the surface.

The 3D modelling of magnetics has given broad exploration targets and combined with a planned airborne EM survey, will provide sufficient information to precisely locate drill collars on Phoenix Copper’s Yorke Peninsula tenements.

Figure 3 3D model of regional aeromagnetic data with drill targets in white T1-T13.

3D model of anomaly T2

3D model of anomaly T13

For

per

sona

l use

onl

y

10 PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

Table 1: Prospectivity Comparison

Feature Hillside –Moonta Phoenix

Structure Rex’s Hillside Deposit is hosted in the Pine Point Fault.

Mineralisation at Moonta is mainly hosted in north east trending faults and shears.

After review of geophysical data it has been concluded that EL4031 and EL4312 host:

North East trending structures that appear to splay off the Pine Point Fault,

A structure that is interpreted as the south western extension of the Pine Point Fault, and

Other significant structures that disrupt the Hiltaba Suite.

Geology Rex’s Hillside Deposit is hosted in sheared “Skarn” amongst granitic and gabbroic rocks(3rd March 2010 REX Minerals Update Hillside 4400N section).

At Moonta mineralisation is hosted in faulted sheared porphyry.

The northern block of EL4031 hosts magnetite rich meta-somatite at Balgowan, (possibly similar to the Skarns at Hillside)and EL4031 and EL4312 host Hiltaba suite granitic and gabbroic rocks (hosts to mineralisation at Olympic Dam, Carapateena and Prominent Hill) in both the northern and southern parts of the tenements.

Circular magnetic features interpreted to be granites and porphyries similar to those found at Moonta and Wallaroo occur in EL4031 and EL4312.

Magnetics Rex uses this as an important exploration tool and Hillside has a very strong magnetic signature.

EL4031 and EL4312 have many high intensity magnetic anomalies. Priority will be given to anomalies interpreted to be deep seated from 3D Modelling (See Figure 3).

Gravity Rex has undertaken systematic gravity surveying over areas of interest and initially gave high priority to those areas with coincident gravity and magnetic anomalies.

Phoenix Copper has only broad spaced gravity data but once magnetic targets are better prioritised with airborne EM, ground gravity surveys may ensue.

Target type Iron Oxide-Copper-Gold-Uranium (IOCGU). IOCGU deposits such as Olympic Dam, Prominent Hill, Carapateena and Hillside; and Moonta and Wallaroo copper gold deposits which are situated in the Olympic IOCGU Domain (see Figure 2) and display magnetic signatures similar to those seen in Phoenix Copper’s Yorke Peninsula tenements.

Conclusion Exploration success in these tenements could be potentially transformational for the Company as evidenced by Hillside 1.5Mt Cu and 1.4Moz Au (see above) and Moonta-Wallaroo with recorded production of 0.36Mt Cu and 62Koz Au (see footnote 5). The programme is aimed at discovery of repetitions of these occurrences.

2.2.5 Planned Airborne EM Survey – VTEM Survey

Phoenix Copper considers that an airborne EM survey is required to assist in drill target definition.

Phoenix Copper plans to undertake a helicopter–borne Versatile Time-domain Electromagnetic (VTEM) geophysical survey to test for significant Cu-Au mineralisation in Hiltaba suite rocks – considered by Phoenix Copper to be the ideal geological environment.

VTEM is a cost effective technique to cover large areas. EM techniques have assisted in the discovery of mineralisation comprising the Poona and Wheal Hughes deposits.8 An airborne electromagnetic survey over the northern tenements is therefore considered an effective geophysical exploration technique.

Phoenix Copper has applied for “PACE Targeting 2011” funding to assist in undertaking this survey.

2.2.6 Drill Target Identification

Drill targets will be defined from both a revised 3D magnetic model, and the VTEM survey. Targets with coincident 3D magnetic and VTEM anomalism will be considered the highest priority for drilling.

It is anticipated that once crops have been harvested in December 2011, drill locations would be available for drilling in February/March 2012, subject to arranging access with landholders and the satisfactory completion of the current rights issue.

8 Keeling,J.L. and Hartley,K.L. Poona and Wheal Hughes Cu Deposits, Moonta, South Australia, CRC/LME PIRSA SA.

For

per

sona

l use

onl

y

11PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

2.3 Burra Project(Figures 1 and 4)

2.3.1 Burra North Prospect – EL4226

A program of diamond drilling has been planned to test the historic IP anomaly generated in the 1960s by the precursor to PIRSA’s Geological Survey9 (see Figure 4). The Monster Mine is within an area reserved from the operation of the Mining Act 1971 (SA) (Mining Act) and is excluded from EL4226 (see yellow outlined area in figure 4), but is important as it is an indicator of the potential of the Burra North Prospect.

Malachite, Azurite and Chalcocite occur in gossanous/quartz/breccia hydrothermal veins and on joint surfaces and fracture planes in and between the veins and host dolomite.

Excellent copper and significant gold assay results were returned including:

Copper PCRC007 - 6.8m@ 3.7% Cu from 0.84m

PCRC028 - 12.0m@ 2.1% Cu from 12.0m, and

Gold PCRC021 - 7.0m @ 2.5g/t Au from 4.0m,

PCRC043 - 24.0m@ 1.4g/t Au from 0.0m.

Figure 4 SA Dept of Mines IP Anomalies generated 1963-67

Figure 5 Drillhole location plan Princess Royal. Previous diamond drillholes (green), RC holes (red).

Metallurgical leach test work that was to be undertaken at AMMTEC in Perth to confirm whether the deposit is amenable to low cost heap leach will now be conducted at the MoL mine site at Leigh Creek. The material will undergo relevant metallurgical test work that will simulate a range of beneficiation and leaching processes likely to be relevant to the ores, if mined. The aim of this work is to devise a process that optimises the recovery of copper from this copper carbonate ore body that can be used in resource estimation modelling.

A resource estimate is being undertaken.

2.3.3 Drill Program Statement

Holes were all drilled with a RC drill rig and drilled dipping at -60 degrees. Holes collars were surveyed. Rock chip and soil from the drillholes was collected in plastic bags at one metre intervals through a sample splitter and placed in calico bags for analysis. Analysis of 4kg samples was carried out by a commercial Laboratory for acid soluble copper and gold. Data aggregation for this report was generally based on laboratory assays of intersections over 0.3% Cu.

2.3.2 Princess Royal Prospect – EL3459

A program of RC drilling was undertaken at Princess Royal 10km south east of Burra to assist in producing a Resource Statement by infilling existing RAB and diamond drilling near the surface. Forty-four holes for 969m were completed (PCRC001 – PCRC044) on seventeen cross sections, see Figure 5.

9 PIRSA – Report Book - RB6300130 Taylor Dec 1966

Hay Bales

3

-60 degress toward 240400m deep

1Sum

p 1

-60 degress toward 240360m deep

2

-60 degress toward 240200m deep

308,000 mE

6,271,000 mN

6,273,000 mN 307,000 mE

6,272,000 mN

MonsterMine

1960s IP Anomalies

BURRA NORTHPROSPECT

ProposedDrillSection

BURRA

For

per

sona

l use

onl

y

12 PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

Table 2 FPXRF Copper Results for selected holes with significant (>0.3%Cu) intersections

Hole Id GDA94N-‐Z54 GDA94E-‐Z54 Azi mag Azi grid Dip Depth From Width Grade % Cu

Inc. from Width Grade % Cu

LAB %Cu

PCRB0066 6296500 271270 83 90 -60 48 0 1.0 0.40

PCRB0070 6296450 271283 100 107 -60 30 2.0 9.0 0.50 3.0 1.0 1.10 0.95

PCRB0075 6296425 271260 20 27 -60 30 13.0 3.0 0.31 14.0 1.0 0.44 0.34

PCRB0076 6296410 271258 20 27 -60 70 22 3.0 0.56 23.0 1.0 1.54 1.65

PCRB0097 6296700 271320 93 100 -60 42 29.0 4.0 0.45 30.0 1.0 1.10 0.84

PCRB0115 6297015 271410 83 90 -60 39 29 3.0 0.30

Future work will concentrate on defining where major structures disrupt the dolerite then drill testing stratigraphic parallel and cross cutting trends.

2.4 Spalding Project(Figures 1, 6 and 7)

2.4.1 Washpool Prospect

A RAB drilling program designed to test widespread copper anomalism reported in FPXRF analyses to the east and north of the historic Wheal Sarah workings was completed at Washpool on EL4370, nine kilometres NW of Spalding, (see Figures 6 and 7). FPXRF analyses confirmed with lab assays of drill cuttings report widespread, low grade enrichment of Cu, with zones of higher grade mineralisation encountered in some holes.

Significant copper has been identified in analyses of RAB chips from Washpool drilling program.

PCRB0070 - 9m @ 0.50% Cu including 1m @ 1.10% Cu (Lab acid soluble 5m @ 0.61% Cu including 1m @ 0.95% Cu)

PCRB0076 - 3m @ 0.56% Cu including 1m @ 1.54% Cu (Lab acid soluble 3m @ 0.60% Cu including 1m @ 1.65% Cu)

PCRB0097 - 4 m @ 0.45% Cu including 1m @ 1.10% Cu (Lab acid soluble 4m @ 0.34% Cu including 1m @ 0.84% Cu)

One hundred and one holes (PCRB0061-161) for a total of 3811 metres were completed in this program mainly concentrated along the eastern edge and northern arcuate hinge zone of a folded doleritic unit with overlying associated elevated surface FPXRF Cu analyses(See Figure 7).

Four holes were drilled near the Wheal Sarah workings to test for along strike extensions of previously mined east west trending mineralisation seen in the historic workings.

The program was designed to provide information on the grade of copper underlying surface FPXRF anomalies. These holes represent the first exploration drilling conducted in the

area since the South Australian Department of Mines drilled three diamond holes in 1967. This drilling provides important lithological and assay information for further exploration in the area.

The results are encouraging with visible malachite and primary sulphides seen in a number of drillholes in and adjacent to doleritic units (see Table 2).

2.4.2 Drill Program Statement

These were the first holes in the Wheal Sarah area and the first since 1967 in the northern Spalding Inlier. Collar locations were based on surface geochemical sampling using FPXRF. Holes were drilled with a Rotary Air Blast rig and were collared with PVC. Holes dipped at -60 degrees and were not surveyed. Rock chip and soil from the drillholes was collected in plastic bags at 1 metre intervals with ~4kg samples being collected by PVC spear and placed in calico bags for analysis. Analysis of 4kg samples was initially carried out by Field Portable X-Ray Fluorescence, with samples of prospective strata then being assayed in the Laboratory for acid soluble copper. Data aggregation for this report was generally based on FPXRF assays of intersections over 0.3 % Cu.

Figure 6 Rotary air blast drilling at Washpool.

Figure 7 RAB collars and contoured FPXRF Cu assays Washpool.

273,000mE

6,296,000 mN

272,000mE

6,299,000 mN

6,297,000 mN

6,298,000 mN

271,000mE

COSTEAN

WHEAL SARAH

PCRB061PCRB075

PCRB078

PCRB085 PCRB094

PCRB103PCRB117

PCRB118PCRB135

PCRB137

PCRB140

PCRB147PCRB156

PCRB161

For

per

sona

l use

onl

y

13PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

2.5 Eudunda Project(Figures 1, 8 and 9)

2.5.1 Tarnma EL3972, Bagot Well EL4291, Bagot Well North EL4626 and Australia Plains EL4503

2304 FPXRF analyses were taken on the Eudunda tenements Tarnma EL3972, Bagot Well EL4291, Bagot Well North EL4626 and Australia Plains EL4503 during the period. The bulk of these analyses were taken over the interpreted north trending fault in central EL4291 Bagot Well (See Figures 8 and 9).

Previous exploration (by others) in this area had concentrated on geochemical sampling and drilling of the stratigraphic unit hosting the Kapunda ore body to the south. This work had proven unsuccessful and in this recent program of FPXRF analyses Phoenix Copper’s aim was to test the northern extension of the structure that is adjacent to mineralisation at Kapunda for near surface copper carbonate ore and deeper copper sulphide mineralisation that may have been transported in this structural conduit. A copper anomaly over 1km in length was identified between 6204000N and 6206000N (See Figure 9).

This represents a drill target to test for both near surface copper carbonate ore and/or deeper copper sulphide mineralisation. It is intended that this target would be tested with RAB drilling across the strike of known anomalism.

Figure 8 Geochemical analyses Cu over magnetic intensity Bagot Well Prospect EL4291.

2.6 Mongolata Project(Figures 1 and 9)

2.6.1 Redbanks EL4419, Anabama EL3971 and The Gums EL4504

FPXRF analysis continued on the five tenements east of the range at Mongolata. 2864 analyses were taken during the period, taking the total to 27,064. Areas targeted this period included magnetic anomalies defined by Normandy Mining Limited in the late 1990s to early 2000s and geophysical uranium anomalies defined from Radiometrics (See Figure 9).

The results of recent FPXRF surveys in Anabama (EL 3971) have shown subtle geochemical anomalism (Cu, Fe) associated with a major north north-east trending magnetic high visible in TMI imagery (Tropical Rainfall Measuring Mission (TRMM) Microwave Imager [TMI]). Current sampling is providing additional cross-strike lines of FPXRF assays to test the coherence of the subtle geochemical response and provide information for further exploration in the area. The results of FPXRF surveys in The Gums (EL 4504) are less encouraging with no coherent zones of elevated Cu reported in the areas surveyed to date. Whilst extensive FPXRF sampling has been carried out in the northern and eastern portions of Redbanks (EL 4419), to date limited sampling has occurred in the western portion closest to the range front. The assay data collected to date along the Eastern Road highlights some zones with elevated Cu.

Figure 9 Targets generated from the FPXRF analysis and geophysical interpretation of magnetic, radiometric and gravity data sets on the Burra, Spalding, Eudunda and Mongolata Projects.

MongolataProject

EudundaProject

BurraProject

SpaldingProject

MongolataProspect

ArdincapleProspect

Princess RoyalProspect

Burra NorthProspect

Burra Creek PlainProspect

RedbanksProspect

Black HillProspect

ApoingaProspect

KarkultoProspect

TarnmaProspect

Bagot WellProspect

WashpoolProspect

EL3971S

EL4370e

EL4233w

300,000mE

350,000mE

6,200,000 mN

6,250,000 mN

6,300,000 mN

BURRA

SPALDING

EL4233e

EL4419

EL4370w

EL4362 EL4226

EL3604

EL4476

EL3716

EL4626

EL4291

EL4504

EL4711

EL3686

EL4032

EL3549

EL4503

EL3972

EL3971

Copper ppm

>160 80-160 40-80 20-40 <20

Uranium targets

Gold targets

Copper Targets

For

per

sona

l use

onl

y

14 PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

2.7 Leigh Creek Project

(Figures 1, 10 and 11)

2.7.1 ML5467 – Mountain of Light

Mining commenced during the year.

2.7.2 ML5498 – Lorna Doone

During the period Phoenix Copper undertook a program of close spaced FPXRF analysis over the full extent of ML5498, see Figure 10. The program aimed to determine whether additional surface copper anomalism existed outside the planned open pit areas. Significant anomalism was detected away from the immediate planned pits which will need to be drill tested in the future.

Geological mapping of surface outcropping mineralisation at Lynda and Lorna Doone was carried out to better determine the likely dip of the orebodies. This is to assist in the geological “wire-framing” of the ore zone in Vulcan software to allow ore block modelling to be completed as part of the feasibility study for Lynda and Lorna Doone.

Results of exploration undertaken by Zurich Resources Pty Ltd (co-funded by Phoenix Copper), over Phoenix Copper’s ML5498 (host to the Lynda and Lorna Doone prospects), returned encouraging results and support a model for intrusion of copper rich mafic-intermediate magmas.

Figure 10 ML5498 FPXRF sampling contoured for Cu over satellite image with previously planned (by others) pit outlines in RED.

Figure 11 Mt Coffin FPXRF data.

2.7.3 Mount Coffin – ML5741

A program of close spaced FPXRF analysis over the full extent of ML5741 (See Figure 11) confirmed the presence of copper around the historic workings and extended into areas along strike now identified as new areas of interest.

264,000mE

264,500mE

265,000mE

6,621,500 mN

6,620,000 mN

6,620,500 mN

6,621,000 mN

262,500mE

263,000mE

263,500mE

ELSIEADAIR

WESTJUBILEE

MOUNTCOFFIN

SOUTH ADAIR

Copper ppm

>160 80-160 40-80 20-40 <20

For

per

sona

l use

onl

y

15PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

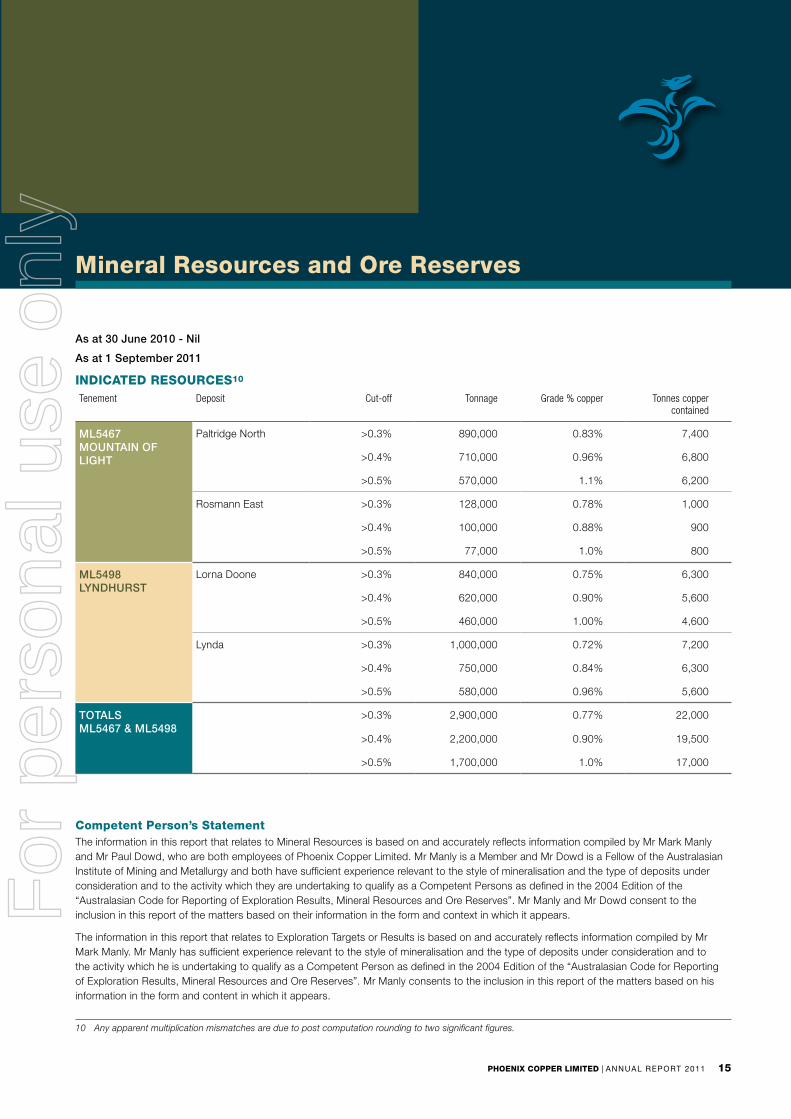

Mineral Resources and Ore Reserves

As at 30 June 2010 - Nil

As at 1 September 2011

INDICATED RESOURCES10

Tenement Deposit Cut-‐off Tonnage Grade % copper Tonnes copper contained

ML5467 MOUNTAIN OF LIGHT

Paltridge North >0.3% 890,000 0.83% 7,400

>0.4% 710,000 0.96% 6,800

>0.5% 570,000 1.1% 6,200

Rosmann East >0.3% 128,000 0.78% 1,000

>0.4% 100,000 0.88% 900

>0.5% 77,000 1.0% 800

ML5498 LYNDHURST

Lorna Doone >0.3% 840,000 0.75% 6,300

>0.4% 620,000 0.90% 5,600

>0.5% 460,000 1.00% 4,600

Lynda >0.3% 1,000,000 0.72% 7,200

>0.4% 750,000 0.84% 6,300

>0.5% 580,000 0.96% 5,600

TOTALS ML5467 & ML5498

>0.3% 2,900,000 0.77% 22,000

>0.4% 2,200,000 0.90% 19,500

>0.5% 1,700,000 1.0% 17,000

Competent Person’s StatementThe information in this report that relates to Mineral Resources is based on and accurately reflects information compiled by Mr Mark Manly and Mr Paul Dowd, who are both employees of Phoenix Copper Limited. Mr Manly is a Member and Mr Dowd is a Fellow of the Australasian Institute of Mining and Metallurgy and both have sufficient experience relevant to the style of mineralisation and the type of deposits under consideration and to the activity which they are undertaking to qualify as a Competent Persons as defined in the 2004 Edition of the “Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves”. Mr Manly and Mr Dowd consent to the inclusion in this report of the matters based on their information in the form and context in which it appears.

The information in this report that relates to Exploration Targets or Results is based on and accurately reflects information compiled by Mr Mark Manly. Mr Manly has sufficient experience relevant to the style of mineralisation and the type of deposits under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2004 Edition of the “Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves”. Mr Manly consents to the inclusion in this report of the matters based on his information in the form and content in which it appears.

10 Any apparent multiplication mismatches are due to post computation rounding to two significant figures.

For

per

sona

l use

onl

y

Directors’ Report

THE DIRECTORS OF PHOENIX COPPER PRESENT THEIR REPORT FOR THE FINANCIAL YEAR ENDED 30 JUNE 2011 (THE FINANCIAL YEAR).

16 PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

For

per

sona

l use

onl

y

17PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

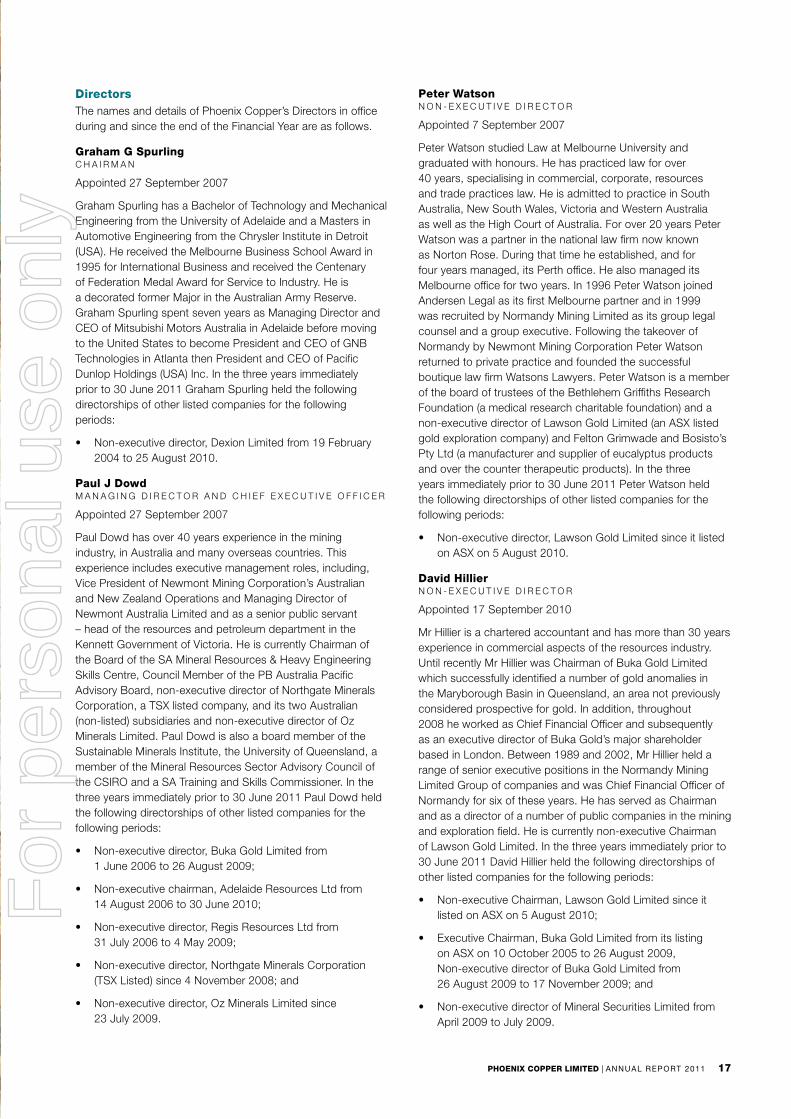

DirectorsThe names and details of Phoenix Copper’s Directors in office during and since the end of the Financial Year are as follows.

Graham G SpurlingC H A I R M A N

Appointed 27 September 2007

Graham Spurling has a Bachelor of Technology and Mechanical Engineering from the University of Adelaide and a Masters in Automotive Engineering from the Chrysler Institute in Detroit (USA). He received the Melbourne Business School Award in 1995 for International Business and received the Centenary of Federation Medal Award for Service to Industry. He is a decorated former Major in the Australian Army Reserve. Graham Spurling spent seven years as Managing Director and CEO of Mitsubishi Motors Australia in Adelaide before moving to the United States to become President and CEO of GNB Technologies in Atlanta then President and CEO of Pacific Dunlop Holdings (USA) Inc. In the three years immediately prior to 30 June 2011 Graham Spurling held the following directorships of other listed companies for the following periods:

Non-executive director, Dexion Limited from 19 February 2004 to 25 August 2010.

Paul J DowdM A N A G I N G D I R E C T O R A N D C H I E F E X E C U T I V E O F F I C E R

Appointed 27 September 2007

Paul Dowd has over 40 years experience in the mining industry, in Australia and many overseas countries. This experience includes executive management roles, including, Vice President of Newmont Mining Corporation’s Australian and New Zealand Operations and Managing Director of Newmont Australia Limited and as a senior public servant – head of the resources and petroleum department in the Kennett Government of Victoria. He is currently Chairman of the Board of the SA Mineral Resources & Heavy Engineering Skills Centre, Council Member of the PB Australia Pacific Advisory Board, non-executive director of Northgate Minerals Corporation, a TSX listed company, and its two Australian (non-listed) subsidiaries and non-executive director of Oz Minerals Limited. Paul Dowd is also a board member of the Sustainable Minerals Institute, the University of Queensland, a member of the Mineral Resources Sector Advisory Council of the CSIRO and a SA Training and Skills Commissioner. In the three years immediately prior to 30 June 2011 Paul Dowd held the following directorships of other listed companies for the following periods:

Non-executive director, Buka Gold Limited from 1 June 2006 to 26 August 2009;

Non-executive chairman, Adelaide Resources Ltd from 14 August 2006 to 30 June 2010;

Non-executive director, Regis Resources Ltd from 31 July 2006 to 4 May 2009;

Non-executive director, Northgate Minerals Corporation (TSX Listed) since 4 November 2008; and

Non-executive director, Oz Minerals Limited since 23 July 2009.

Peter WatsonN O N - E X E C U T I V E D I R E C T O R

Appointed 7 September 2007

Peter Watson studied Law at Melbourne University and graduated with honours. He has practiced law for over 40 years, specialising in commercial, corporate, resources and trade practices law. He is admitted to practice in South Australia, New South Wales, Victoria and Western Australia as well as the High Court of Australia. For over 20 years Peter Watson was a partner in the national law firm now known as Norton Rose. During that time he established, and for four years managed, its Perth office. He also managed its Melbourne office for two years. In 1996 Peter Watson joined Andersen Legal as its first Melbourne partner and in 1999 was recruited by Normandy Mining Limited as its group legal counsel and a group executive. Following the takeover of Normandy by Newmont Mining Corporation Peter Watson returned to private practice and founded the successful boutique law firm Watsons Lawyers. Peter Watson is a member of the board of trustees of the Bethlehem Griffiths Research Foundation (a medical research charitable foundation) and a non-executive director of Lawson Gold Limited (an ASX listed gold exploration company) and Felton Grimwade and Bosisto’s Pty Ltd (a manufacturer and supplier of eucalyptus products and over the counter therapeutic products). In the three years immediately prior to 30 June 2011 Peter Watson held the following directorships of other listed companies for the following periods:

Non-executive director, Lawson Gold Limited since it listed on ASX on 5 August 2010.

David HillierN O N - E X E C U T I V E D I R E C T O R

Appointed 17 September 2010

Mr Hillier is a chartered accountant and has more than 30 years experience in commercial aspects of the resources industry. Until recently Mr Hillier was Chairman of Buka Gold Limited which successfully identified a number of gold anomalies in the Maryborough Basin in Queensland, an area not previously considered prospective for gold. In addition, throughout 2008 he worked as Chief Financial Officer and subsequently as an executive director of Buka Gold’s major shareholder based in London. Between 1989 and 2002, Mr Hillier held a range of senior executive positions in the Normandy Mining Limited Group of companies and was Chief Financial Officer of Normandy for six of these years. He has served as Chairman and as a director of a number of public companies in the mining and exploration field. He is currently non-executive Chairman of Lawson Gold Limited. In the three years immediately prior to 30 June 2011 David Hillier held the following directorships of other listed companies for the following periods:

Non-executive Chairman, Lawson Gold Limited since it listed on ASX on 5 August 2010;

Executive Chairman, Buka Gold Limited from its listing on ASX on 10 October 2005 to 26 August 2009, Non-executive director of Buka Gold Limited from 26 August 2009 to 17 November 2009; and

Non-executive director of Mineral Securities Limited from April 2009 to July 2009.

For

per

sona

l use

onl

y

18 PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

Company Secretary

Peta Marshman

Peta Marshman is a qualified lawyer and also has a Bachelor of Economics.

Interests in the Shares and Options of the CompanyAs at the date of this Report, the interests of the Directors in the shares and options of Phoenix Copper are as follows:

Graham Spurling, Chairman

Graham Spurling has a direct interest in 500,000 unlisted Options exercisable at $0.25 any time on or before 11 February 2013 and an indirect interest in 710,084 Shares.

Paul Dowd, Managing Director and Chief Executive Officer

Paul Dowd has a direct interest in one million Performance Rights under Phoenix Copper’s Employee Performance Rights Plan. Subject to the satisfaction of certain vesting conditions these Performance Rights will result in the issue to Paul Dowd (or his nominee), for no consideration, of one million Shares. Paul Dowd also has an indirect interest in:

543,750 Shares;

500,000 unlisted Options exercisable at $0.25 any time on or before 11 February 2013; and

1,500,000 Performance Shares, the terms of which are set out in the Remuneration Report.

Peter Watson, Non-executive Director

Peter Watson has a direct interest in:

623,750 Shares; and

500,000 unlisted Options exercisable at $0.25 any time on or before 11 February 2013

and an indirect interest in 4,000,000 Shares.

David Hillier, Non-executive Director

David Hillier has an indirect interest in 150,000 Shares.

Dividends and DistributionsNo dividends or distributions were paid to members during the Financial Year and none were recommended or declared for payment.

Principal Activities The principal activities of the Group during the Financial Year comprised mineral exploration and copper cement production.

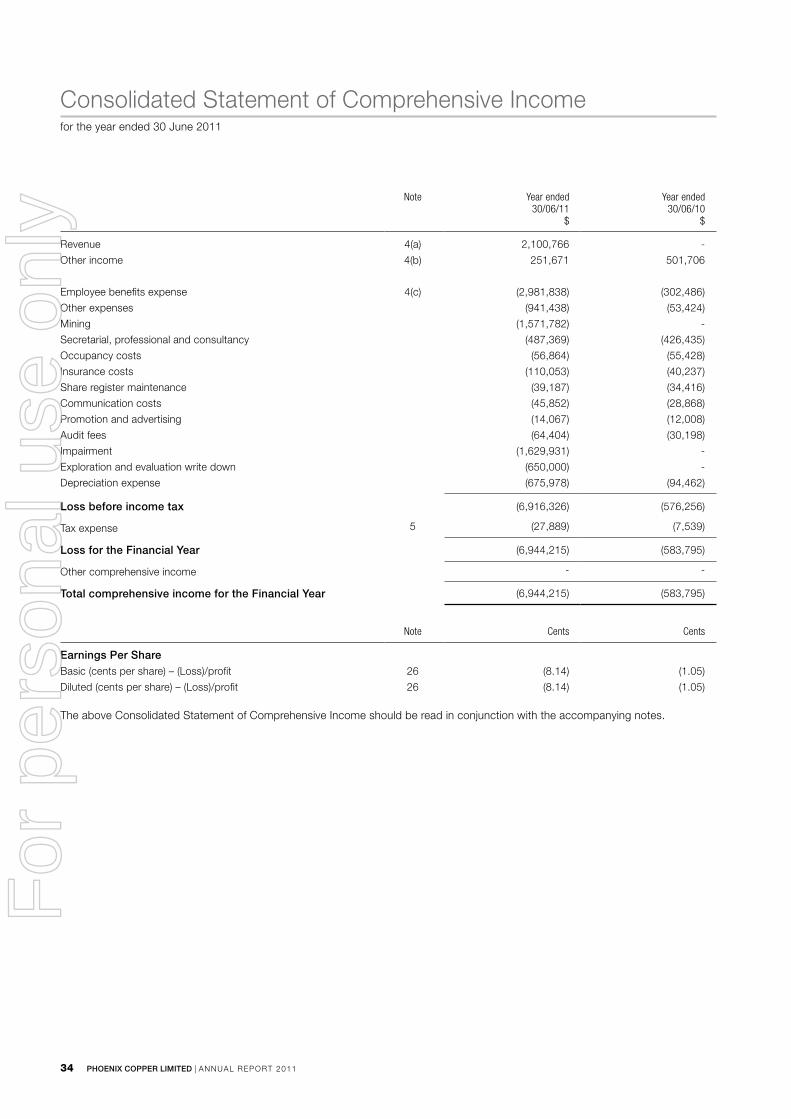

Review of OperationsThe net result of operations for the group for the year was a loss after income tax of $6,944,215 (2010: $583,795).

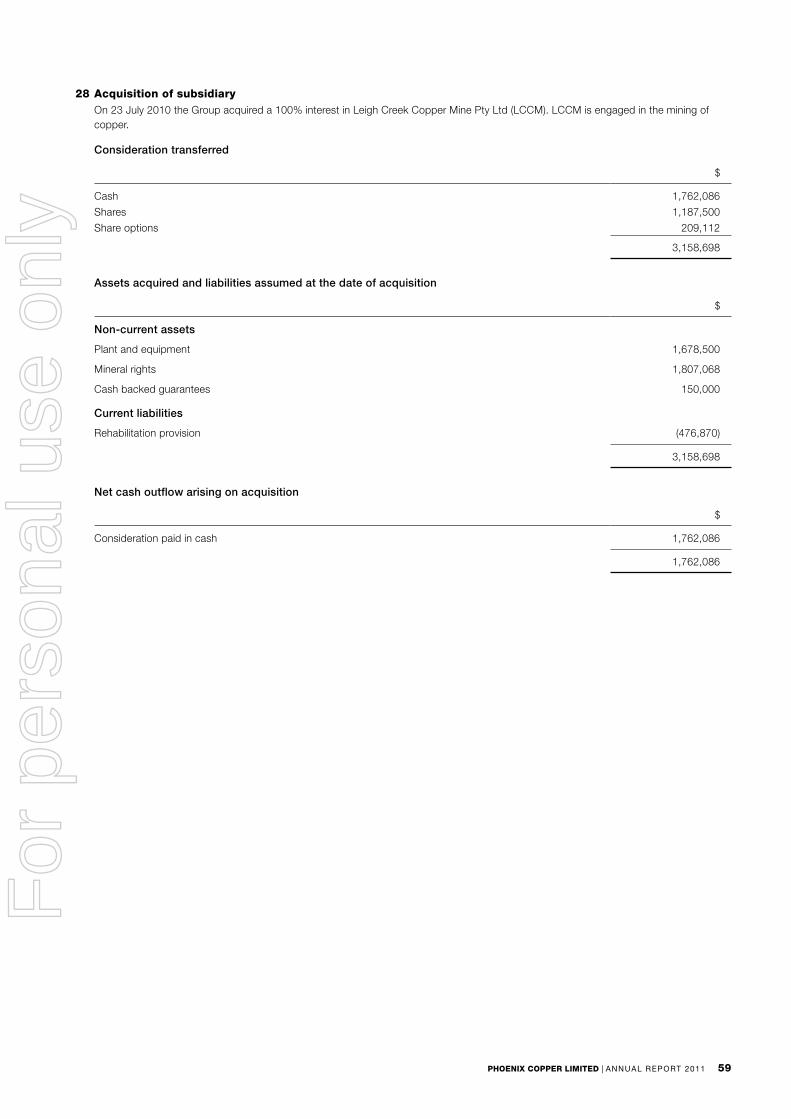

The Company completed the acquisition of Leigh Creek Copper Mine Pty Ltd (LCCM) on 23 July 2010 with ownership and control of LCCM, along with the associated Mountain of Light copper heap leaching operations and three Mining Leases transferring to Phoenix Copper Limited (PNX). After purchase completion, the operation was released from care and maintenance with PNX undertaking refurbishment of the existing leach pads and plant. Mining operations were recommenced at the Rosmann East pit, with newly mined

material being crushed and screened to present the resultant classified course ore for stacking onto leach pads and placement under irrigation for leaching of copper product. In addition to mining of the Rosmann East pit, additional ore was sourced from the Paltridge South pit which was developed and mined during the year. To support the recommenced operations, a new leach pad was constructed during the year.

All mining, crushing and stacking operations at Mountain of Light were completed prior to the end of the year with the leaching of stacked ore continuing through the first half of 2011/12.

Total sales of copper cement product for the year under an off-take agreement with Adchem (Australia) Pty Ltd was approximately 294t contained copper, generating revenues of $2.1M.

With the acquisition of LCCM, the Company now has exploration activities directed to six projects:

the Yorke Peninsula project; where exploration for a significant primary copper or copper/gold resource similar to Moonta or Hillside is the main focus of activity,

the Burra, Spalding and Eudunda projects; where work is concentrated on exploring for and proving up near surface copper carbonate and oxide resources to feed a potential second treatment facility at Burra,

the Mongolata project; where work is concentrated on exploring for and proving up gold and uranium resources,

the Leigh Creek project; where work is concentrated on two areas, exploring for and proving up near surface copper carbonate and oxide resources to feed the Mountain of Light treatment facility and exploring for deep large tonnage copper resources.

During the year a 3D unconstrained inversion model of the regional aeromagnetic data for the Yorke Peninsula project was completed with exploration targets subsequently defined. Deep seated anomalies that were seen to persist at depth are the highest priority targets. A planned “VTEM” (Versatile Time-Domain Electro-Magnetics) airborne electromagnetic survey using a helicopter platform to map possible mineralisation associated with inferred geological structures, which is the subject of a PACE funding application, is scheduled to occur during 2011/12.

At Burra, a program of Reverse Circulation (RC) drilling was undertaken at Princess Royal EL3459 to assist in producing a Resource Statement by infilling existing Rotary Air Blast (RAB) and diamond drilling near the surface. Forty four holes for 969m were completed with significant copper and gold mineralisation encountered including 6.8m @ 3.7% Cu from 0.84m, and 7.0m @ 2.5g/t Au from 4.0m.

Zones of high copper anomalism were found in Field Portable X-Ray Fluorescence Analysis (FPXRF) around the rim of a strong magnetic high in central EL3971 at the Mongolata project.

At the Spalding project a RAB drilling program around the old Wheal Sarah copper mine 10km north west of Spalding was undertaken with encouraging acid soluble results including 5m @ 0.61% Cu.

For

per

sona

l use

onl

y

19PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

FPXRF analysis continued during the year at the Eudunda project with zones of most interest found in sampling performed at Tarnma in the south west of EL3972, in the north west of EL4626 and at Bagot Well in central EL4291.

At the Leigh Creek project, a program of close spaced FPXRF analysis was conducted with significant anomalism detected away from the current planned pits at Lorna Doone ML5498, and the confirmation of the presence of copper around the historic workings at Mount Coffin ML5741 which extended into areas along strike along with the identification of new areas of interest.

On 9 June 2011, PNX provided a market update to the Australian Securities Exchange in respect of issues encountered in ramping up production activities at the Mountain of Light operation. These included:

at least three significant rain events causing major operating disruption,

the mining contractors’ basis of pricing proving to be uneconomic,

a lack of reliable historical process data to assist with process diagnostics and improvements,

a leach cycle of nearer to 120 days than the previously estimated 90 days,

delays in the receipt of laboratory assays resulting in more recently stacked material generally proving to be low grade in comparison with the grade estimated from historical drill data and visual ore spotting,

high acid conditioning of newly stacked material failing to produce sustained increases in the pregnant liquor grade as a result of the low copper grade stacked.

As a consequence, the Company has recorded a net operating loss from its Mountain of Light operations of $2.85M for the financial year, which when aggregated with normal corporate expenditures to support the business has resulted in an operating loss of $4.67M for the Group. Directors also took the decision to raise a charge for impairment against the Mountain of Light assets of $1.63M and to write-down the carrying value of exploration expenditure on a number of tenements by $0.65M, thereby resulting in an overall recorded loss for the financial year of $6.944M.

Significant Changes in the State Of AffairsThe significant changes in the state of affairs of the Group during the Financial Year were as follows:

the raising of $704,000, and issue of 4,400,000 Shares, under a non-renounceable share purchase plan and additional share subscriptions from three investors;

the acquisition of all of the shares in the capital of Leigh Creek Copper Mine Pty Ltd (LCCM), the holder of Mining Leases ML5467, ML5741 and ML5498;

the placement of 11,875,000 Shares to Long Fortune Limited for $1,900,000 to fund recommencement of the mining and production operations at Leigh Creek;

the issue of 6,250,002 Shares and 1,250,000 unlisted Options to creditors of LCCM to settle and discharge the debt owed by LCCM to those creditors (in connection with Phoenix Copper’s acquisition of all of the issued shares in the capital of LCCM);

the acquisition of EL3451, EL3971 and EL3972;

the commencement of copper cement production on 31 August 2010;

the appointment of Nick Harding as chief financial officer on 1 September 2010 and of David Hillier as non-executive Director on 17 September 2010;

Paul Dowd’s employment (as Managing Director and chief executive officer) becoming full time as from 1 September 2010;

the adoption by the Board of an Employee Performance Rights Plan (in place of the Employee Share Option Plan) on 17 September 2010;

the placement of a total of 8,620,690 Shares and 2,873,563 unlisted Options in two tranches (on 15 October 2010 and 1 December 2010 respectively) to strategic New Zealand investors to raise a total of $2,500,000 (before issue costs);

the issue and allotment of 750,000 unlisted Options exercisable at $0.28 and expiring on 31 October 2011 to a contractor of the Company as part consideration for their services

the placement of 7,053,320 Shares and 2,351,102 unlisted Options on 11 March 2011, to raise up to $1,974,930 before expenses;

the issue of 500,000 unsecured Convertible Notes to Talis SA, a Company registered with the Registry of Commerce and Companies of Paris under No. 404 387 748 on 23 June 2011, for $500,000 in subscription monies;

the issue of 202,000 Shares on exercise of 202,000 employee Options; and

the release from voluntary escrow of 500,000 Shares.

Other than the above, there was no significant change in the state of affairs of the consolidated entity during the financial year.

Significant Events Subsequent to Balance DateThe matters or circumstances that have arisen since 30 June 2011 which have significantly affected or may significantly affect:

the Group’s operations in future financial years;

the results of those operations in future financial years; or

the Group’s state of affairs in future financial years,

are as follows:

the cessation on 13 June 2011 of mining activities and on 24 June 2011 of crushing, screening and ore stacking activities at the Mountain of Light (MoL) project and the commencement of a financial and technical review in connection with the future mining of the Paltridge North orebody;

For

per

sona

l use

onl

y

20 PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

the issue of a further 250,000 unsecured Convertible Notes to Talis SA on 7 September 2011, for $250,000 in subscription monies;

the release from voluntary escrow of 15,000,001 Shares; and

the conversion of 750,000 unsecured Convertible Notes by Talis SA resulting in the issue of 8,392,693 Shares on 23 September 2011.

Other than the above, there has not been any matter or circumstance that has occurred subsequent to the end of the financial year that has significantly affected, or may significantly affect, the operations of the consolidated entity, the results of those operations, or the state of affairs of the consolidated entity in future financial years.

Likely Developments The Group expects to continue to produce copper cement from its Mountain of Light project and to deliver that project into its Supply Agreement with Adchem (Australia) Pty Ltd from the existing stockpiled ore in heap leach pads, although this source of copper will be exhausted some time toward the end of 2011.

Mining activities were suspended from 13 June 2011 and crushing, screening and stacking of ore onto heap leach pads was suspended 24 June 2011. Resumption of mining, crushing, screening and stacking of ores is dependent upon the satisfactory results of an internal financial and technical review of the Paltridge North orebody. Independent laboratories will also be utilised for some of the test work.

Two other mining leases are owned by LCCM and ML5498 is the subject of a previously advised Indicated Resource. A Mining and Rehabilitation Plan (MARP) is required before development work can commence at the Lorna Doone and Lynda deposits within ML5498. Work has commenced on the preparation of this draft MARP to allow development of these deposits, once the studies regarding Paltridge North at MoL are concluded and the results are proven to be satisfactory. All deposits within the Leigh Creek/Lyndhurst area are planned to be developed as satellite deposits and will be subject to beneficiation at the “pit rim” to produce a higher grade ore for campaigned trucking to the central “hub” of processing at MoL.

The Group also expects to continue a comprehensive and systematic exploration programme within its existing tenements. All the tenements are in South Australia and it is not contemplated at this time to consider opportunities elsewhere.

Environment Regulation and PerformanceThe Group continues to meet all environmental obligations across its tenements. Despite a number of significant rain events, no reportable incidents occurred during the Financial Year.

Options, Performance Shares, Performance Rights and Convertible NotesDuring the Financial Year and to the date of this Directors’ Report, the Company issued and allotted the following Options:

1,250,000 unlisted Options exercisable at $0.275 and expiring on 29 July 2015;

2,873,563 unlisted Options exercisable at $0.35 and expiring on 15 April 2012;

750,000 unlisted Options exercisable at $0.28 and expiring on 31 October 2011; and

2,351,102 unlisted Options exercisable at $0.35 and expiring on 11 March 2013.

As at the date of this Report, the Company has the following Options on issue:

1,500,000 unlisted Options exercisable at $0.25 and expiring on 11 February 2013;

5,500,000 unlisted Options exercisable at $0.25 and expiring on 25 January 2013;

250,000 unlisted Options exercisable at $0.25 and expiring on 18 June 2013;

500,000 unlisted Options exercisable at $0.25 and expiring on 11 September 2013;

750,000 unlisted Options exercisable at $0.10 and expiring on 15 March 2014;

23,000 unlisted Options exercisable at $0.086 and expiring on 10 June 2014;

62,000 unlisted Options exercisable at $0.073 and expiring on 21 June 2014;

1,250,000 unlisted Options exercisable at $0.275 and expiring on 29 July 2015;

2,873,563 unlisted Options exercisable at $0.35 and expiring on 15 April 2012;

750,000 unlisted Options exercisable at $0.28 and expiring on 31 October 2011; and

2,351,102 unlisted Options exercisable at $0.35 and expiring on 11 March 2013.

202,000 Shares were issued during the Financial Year as a result of the exercise of 202,000 Options.

As at the date of this Report, the Company also has on issue:

1,500,000 unlisted Performance Shares which automatically convert (in tranches of 500,000 shares each) to ordinary shares, when Shares trade for five consecutive ASX trading days at or above 40 cents, 60 cents and 80 cents respectively; F

or p

erso

nal u

se o

nly

21PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

1,100,000 Performance Rights under Phoenix Copper’s Employee Performance Rights Plan which, subject to the satisfaction of certain vesting conditions, will result in the issue for no consideration 1,100,000 Shares; and

500,000 unsecured Convertible Notes, each of which:

»

»quarterly in arrears, by either cash or the number of Shares equal to the accrued but unpaid interest divided by 80% of the volume weighted average closing price on ASX over the preceding 30 trading days, at the option of the Company);

»

»

»

»to participate in the future issues of securities or the distribution of dividends by the Company to its Shareholders prior to conversion;

»(unless redeemed or converted earlier in accordance with the terms of issue);

»of Shares equal to the face value of the Convertible Note divided by 80% of the volume weighted average closing price on ASX over the 30 trading days immediately preceding (but not including) the conversion date; and

»end of each calendar quarter at the face value of the Convertible Note, subject to the following interest premiums for early redemption:

¬ if redeemed on 30 September 2011, additional interest calculated on the face value of the Convertible Note at 4.0% per annum, accrued daily from the issue date to the redemption date;

¬ if redeemed on 31 December 2011, additional interest calculated on the face value of the Convertible Note at 3.0% per annum, accrued daily from the issue date to the redemption date; and

¬ if redeemed on 31 March 2012, additional interest calculated on the face value of the Convertible Note at 2.0% per annum, accrued daily from the issue date to the redemption date.

Option holders, Performance Share holders, Performance Rights holders and convertible note holders do not have any right, by virtue of Options, Performance Shares, Performance Rights or Convertible Notes, to participate in new issues of Shares offered to Shareholders.

Indemnification and Insurance of Directors and OfficersPhoenix Copper entered into a Deed of Access, Insurance and Indemnity with each of the Directors on 12 November 2007 or, in the case of David Hillier, 22 September 2010. Under the terms of these Deeds, the Company has undertaken, subject to restrictions in the Corporations Act, to:

indemnify each Director in certain circumstances;

advance money to a Director for the payment of any legal costs incurred by a Director in defending legal proceedings before the outcome of those proceedings is known (subject to an obligation by the Director to repay any money advanced if the costs become costs in respect of which the Director is not entitled to be indemnified under the Deed);

maintain Directors’ and Officers’ insurance cover (if available) in favour of each Director whilst they remain a director of Phoenix Copper and for a run out period after ceasing to be such a director; and

provide each Director with access to Board papers and other documents provided or available to the Director as an officer of Phoenix Copper.

Throughout the Financial Year Phoenix Copper has had in place and paid premiums for insurance policies, with a limit of liability of $10 million, indemnifying Directors and officers of the Company against certain liabilities incurred in the conduct of business or in the discharge of their duties as Directors or officers. The contracts of insurance contain confidentiality provisions that preclude disclosure of the premium paid.

Directors’ attendance at MeetingsThirteen Board meetings were held during the Financial Year. Graham Spurling and Peter Watson attended all of those meetings. David Hillier was appointed a Director on 17 September 2010 and attended all Board meetings held on and from that date. Paul Dowd attended twelve of the thirteen Board meetings.

Two Audit Committee meetings were held during the Financial Year. All of the Directors attended both of these meetings, Paul Dowd attending by invitation.

Auditors’ Independence DeclarationThe auditor’s independence declaration is included on page 33.

Non-Audit ServicesThe following non-audit services were provided to the Group by the Group’s auditor, Deloitte Touche Tohmatsu, during the Financial Year:

Assistance in the preparation of annual tax return and associated tax advice of $14,576.

The directors are satisfied that the provision of non-audit services, during the year, by the auditor (or by another person or firm on the auditor’s behalf) is compatible with the general standard of independence for auditors imposed by the Corporations Act 2001.

For

per

sona

l use

onl

y

22 PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

This Report outlines the remuneration arrangements in place for the Directors, Company Secretary and senior management of the Group.

Where this report refers to the ‘Grant Date’ of Shares, Options or Performance Rights, the date mentioned is the date on which those Shares, Options or Performance Rights were agreed to be issued (whether conditionally or otherwise) or, if later, the date on which key terms of the Shares, Options or Performance Rights (e.g. subscription or exercise price) were determined.

Director and senior management details

The following persons acted as Directors of the Company during or since the end of the Financial Year:

Graham Spurling (Chairman)

Paul Dowd (Managing Director and Chief Executive Officer)

Peter Watson (Non-executive Director)

David Hillier (Non-executive Director)

The person acting as Company Secretary is Peta Marshman.

The following persons acted as “senior management” of the Company during or since the end of the Financial Year:

Mark Manly (Chief Geologist)

Nick Harding (Chief Financial Officer)

James Fox (General Manager – Mountain of Light Copper Mine)

Relationship between the remuneration policy and Company performance

The table below sets out summary information about the consolidated entity’s earnings and movements in shareholder wealth for the four years to 30 June 2011.

30 June 2011 30 June 2010 30 June 2009 30 June 2008

Revenue $2,100,766 - - -

Net loss before tax $6,916,327 $576,256 $578,272 $406,350

Net loss after tax $6,944,215 $583,795 $785,701 $518,354

Share price on listing on ASX - - - $0.20

Share price at start of the Financial Year $0.16 $0.07 $0.12 -

Share price at end of the Financial Year $0.10 $0.16 $0.07 $0.12

Basic earnings per share ($0.0814) ($0.0105) $(0.0143) $(0.017)

Diluted earnings per share ($0.0814) ($0.0105) $(0.0143) $(0.017)

No dividends have been declared during the Financial Year and the Directors do not recommend the payment of a dividend in respect of the Financial Year.

There is no link between the Company’s performance and the setting of remuneration except as discussed below in relation to the Managing Director’s Performance Shares and Performance Rights and Options for Directors and certain employees.

Remuneration Report

For

per

sona

l use

onl

y

23PHOENIX COPPER LIMITED | ANNUAL REPORT 2011

Remuneration Philosophy

The performance of the Group depends on the quality of its Directors and employees and therefore the Group must attract, motivate and retain appropriately qualified industry personnel. The Group embodies the following principles in its remuneration framework:

provide competitive rewards to attract and retain high calibre executives, Directors and employees;

link executive rewards to Shareholder value (by the granting of Performance Shares or Options);

link reward with the strategic goals and performance of the Company; and

ensure total remuneration is competitive by market standards.

The Company does not currently have a policy on trading in derivatives that limit exposure to losses resulting from Share price decreases applicable to Directors and employees who receive part of their remuneration in securities of the Company.

Remuneration Policy

The Company does not have a separately established remuneration committee. The full Board acts as the Company’s remuneration committee. The Board is responsible for determining and reviewing remuneration arrangements for the non-executive Directors, the Managing Director, Company Secretary and senior management. The Board assesses the appropriateness of the nature and amount of remuneration of such persons on a periodic basis by reference to relevant employment market conditions with the overall objective of ensuring maximum stakeholder benefit from retention of a high quality Board and executive team. External advice on remuneration matters is sought whenever the Board deems it necessary.

The remuneration of the non-executive Directors and Company Secretary is not dependent on the satisfaction of a performance condition. The Managing Director has a direct or indirect interest in Performance Shares, Options and Performance Rights, the terms of which are set out below. The non-executive Directors and the Chief Geologist have interests in Options and Shares, the terms of which are set out below. The General Manager – Mountain of Light Copper Mine has a direct interest in Performance Rights.

Non-Executive Director Remuneration

The Board seeks to set remuneration of non-executive Directors at a level which provides the Company with the ability to attract and retain Directors of the highest calibre, whilst incurring a cost which is appropriate at this stage of the Company’s development.

As Chairman, Graham Spurling is entitled to receive $75,000 per annum inclusive of superannuation and Peter Watson and David Hillier are each entitled to receive $30,000 and $40,000 per annum respectively inclusive of superannuation. Non-executive Directors are entitled to be paid reasonable travelling, accommodation and other expenses incurred as a consequence of their attendance at meetings of Directors and otherwise in the execution of their duties as Directors. Non-executive Directors are also entitled to additional remuneration

for extra services or special exertions, in accordance with the Company’s Constitution. There are no schemes for retirement benefits other than superannuation for non-executive Directors.

Summary details of remuneration for non-executive Directors are given in the table below. Their remuneration is not dependent on the satisfaction of a performance condition. The maximum aggregate remuneration of non-executive Directors, other than for extra services or special exertions, is presently set at $500,000 per annum.

Managing Director Remuneration

The Company aims to reward the Managing Director with a level and mix of remuneration commensurate with his position and responsibilities within the Company to:

align the interests of the Managing Director with those of Shareholders;

link reward with the strategic goals and performance of the Company; and

ensure total remuneration is competitive by market standards.

Paul Dowd joined Phoenix Copper in 2007 as its inaugural Managing Director. He was originally employed on a part-time basis. Until 1 June 2010 Paul Dowd was contracted to devote 2.5 days per week on average to his role as Managing Director of Phoenix Copper. This was increased to 3.5 days per week on average on 1 June 2010. With Phoenix Copper’s transition to producer and explorer resulting from the acquisition of LCCM, Paul Dowd was engaged as Managing Director and Chief Executive Officer on a full time basis with effect from 1 September 2010. Paul Dowd is now employed on a part-time basis at four days per week from 1 July 2011.

Until 1 September 2010, Paul Dowd was entitled to be paid $2,000 per day worked (exclusive of GST but inclusive of superannuation), pro-rata for part days of less than eight hours. He was also entitled to reimbursement of expenses and additional remuneration for extra services or special exertions, in accordance with the Company’s Constitution. Paul Dowd was entitled to 20 days unpaid annual leave and 10 days unpaid sick leave per annum.

The term of Paul Dowd’s employment as Managing Director and Chief Executive Officer is from 1 September 2010 until 30 June 2012 (Initial Term). During the Initial Term Paul Dowd must find, appoint and develop a person, satisfactory to the Board, as his replacement. This person must have commenced employment by 31 March 2012 to ensure an efficient handover. If Paul Dowd’s replacement is not appointment before 30 June 2012 he and the Board will discuss alternative arrangements regarding shortening or extending the Initial Term (as appropriate in the circumstances).

Paul Dowd’s employment with the Company may be terminated on three months written notice, or on summary notice if he: