for econ 103c ge#4 filedepreciation, book value and capital gain (q.9, q.10, q.12) annual...

TRANSCRIPT

For ECON 103C GE#4

Q.1 – Q.5 (1)

100/(1+ 0.05)105

0

Discounting @ r1 = 5%

100/(1+ 0.05)100

0

。。。

。。。

Let’s start with the first part:

PV1= 𝟏𝟓(𝟏. 𝟎𝟓)−𝒌𝟏𝟎𝟓𝒌=𝟏𝟎𝟎

Q.1 – Q.5 (2)

100/(1+ 0.06)300

0

Discounting @ r2 = 6%

100/(1+ 0.06)201

0

。。。

。。。

Now think about the second part but without (1.05)-150 :

Q.1 – Q.5 (3)

Now if we add back (1.05)-150 , what changes: PV2=

1

1+0.05 150* 100/(1+ 0.06)300

Discounting @ r1 = 5% r2 = 6%

1

1+0.05 150* 100/(1+ 0.06)201

。。。

=150+201

Q.1 – Q.5 (4)

Now bring two parts together:

。。。

。。。

PV1

PV2

PV

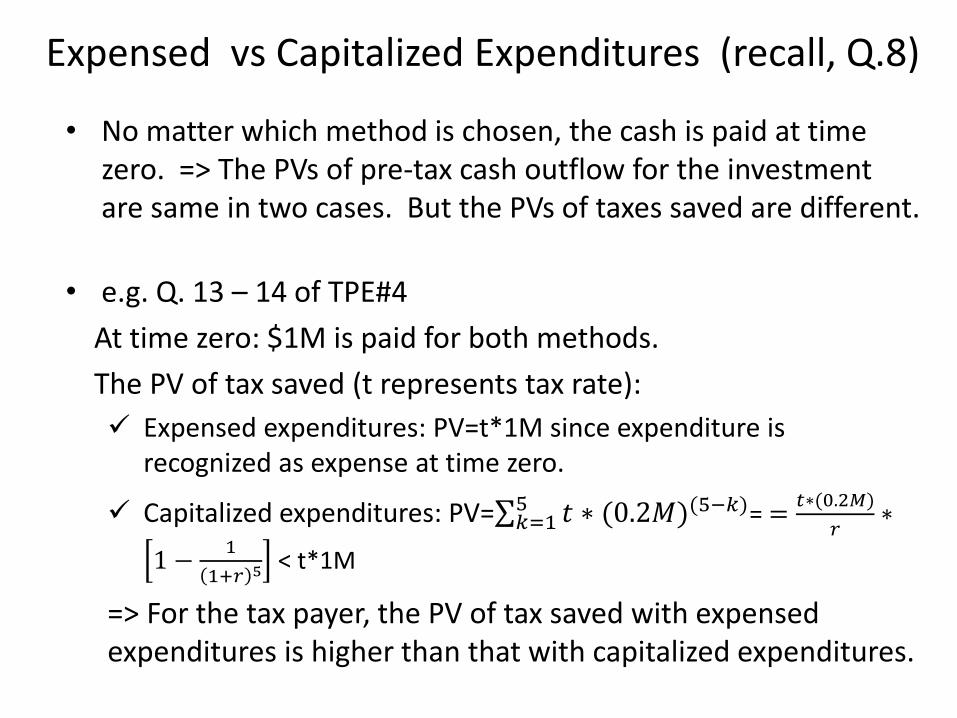

Expensed vs Capitalized Expenditures (recall, Q.8)

• No matter which method is chosen, the cash is paid at time zero. => The PVs of pre-tax cash outflow for the investment are same in two cases. But the PVs of taxes saved are different.

• e.g. Q. 13 – 14 of TPE#4

At time zero: $1M is paid for both methods.

The PV of tax saved (t represents tax rate):

Expensed expenditures: PV=t*1M since expenditure is recognized as expense at time zero.

Capitalized expenditures: PV= 𝑡 ∗ (0.2𝑀)(5−𝑘)5𝑘=1 = =

𝑡∗(0.2𝑀)

𝑟∗

1 −1

1+𝑟 5 < t*1M

=> For the tax payer, the PV of tax saved with expensed expenditures is higher than that with capitalized expenditures.

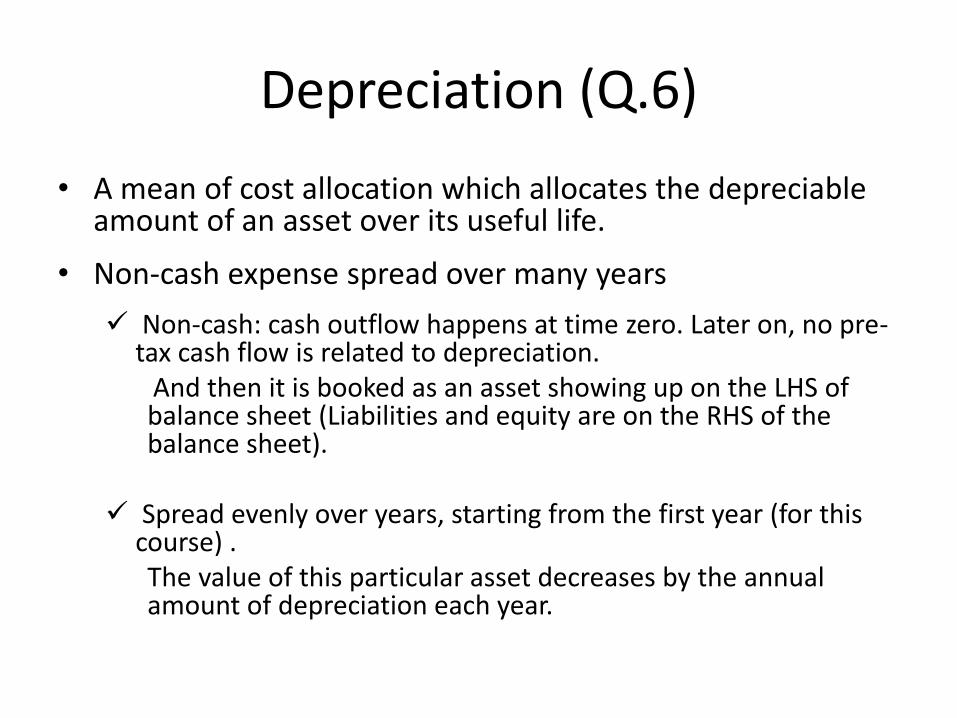

Depreciation (Q.6)

• A mean of cost allocation which allocates the depreciable amount of an asset over its useful life.

• Non-cash expense spread over many years

Non-cash: cash outflow happens at time zero. Later on, no pre-tax cash flow is related to depreciation.

And then it is booked as an asset showing up on the LHS of balance sheet (Liabilities and equity are on the RHS of the balance sheet).

Spread evenly over years, starting from the first year (for this

course) . The value of this particular asset decreases by the annual amount of depreciation each year.

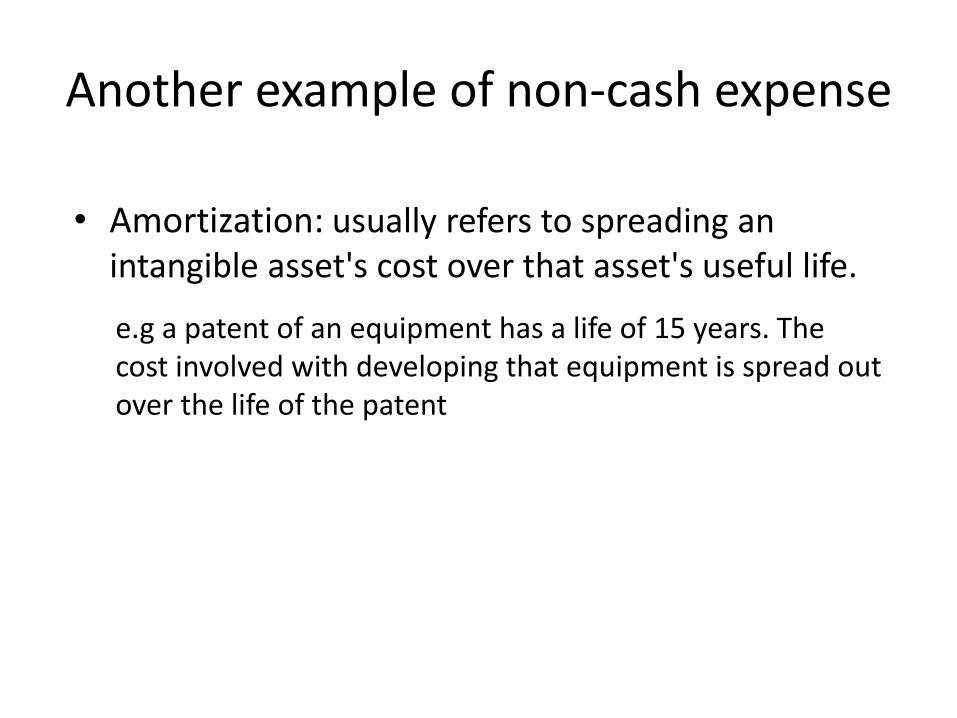

Another example of non-cash expense

• Amortization: usually refers to spreading an intangible asset's cost over that asset's useful life.

e.g a patent of an equipment has a life of 15 years. The cost involved with developing that equipment is spread out over the life of the patent

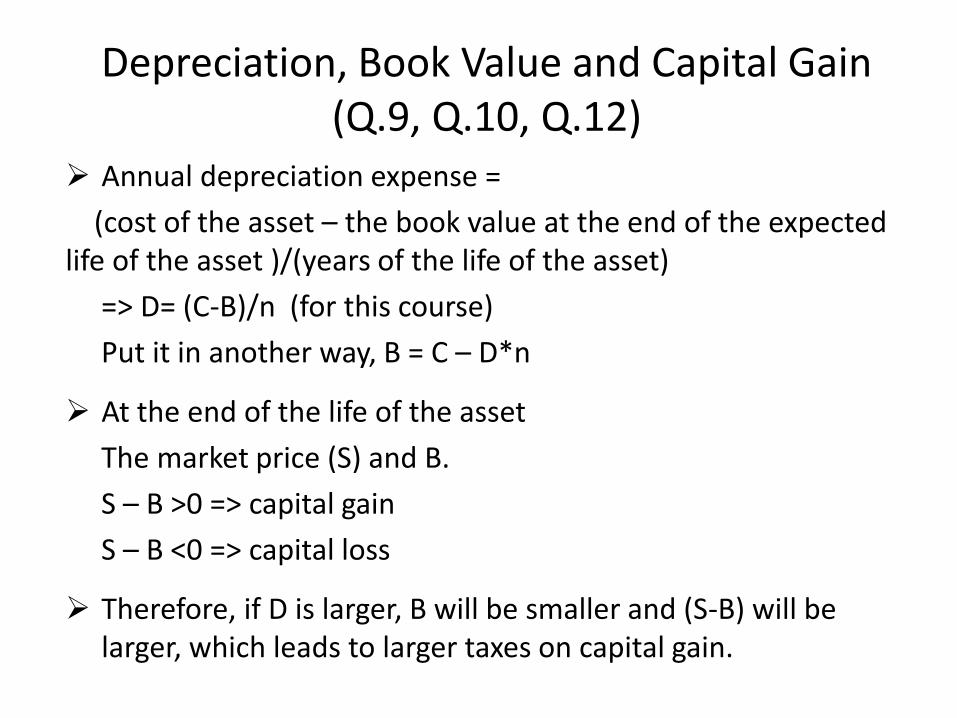

Depreciation, Book Value and Capital Gain (Q.9, Q.10, Q.12)

Annual depreciation expense =

(cost of the asset – the book value at the end of the expected life of the asset )/(years of the life of the asset)

=> D= (C-B)/n (for this course)

Put it in another way, B = C – D*n

At the end of the life of the asset

The market price (S) and B.

S – B >0 => capital gain

S – B <0 => capital loss

Therefore, if D is larger, B will be smaller and (S-B) will be larger, which leads to larger taxes on capital gain.

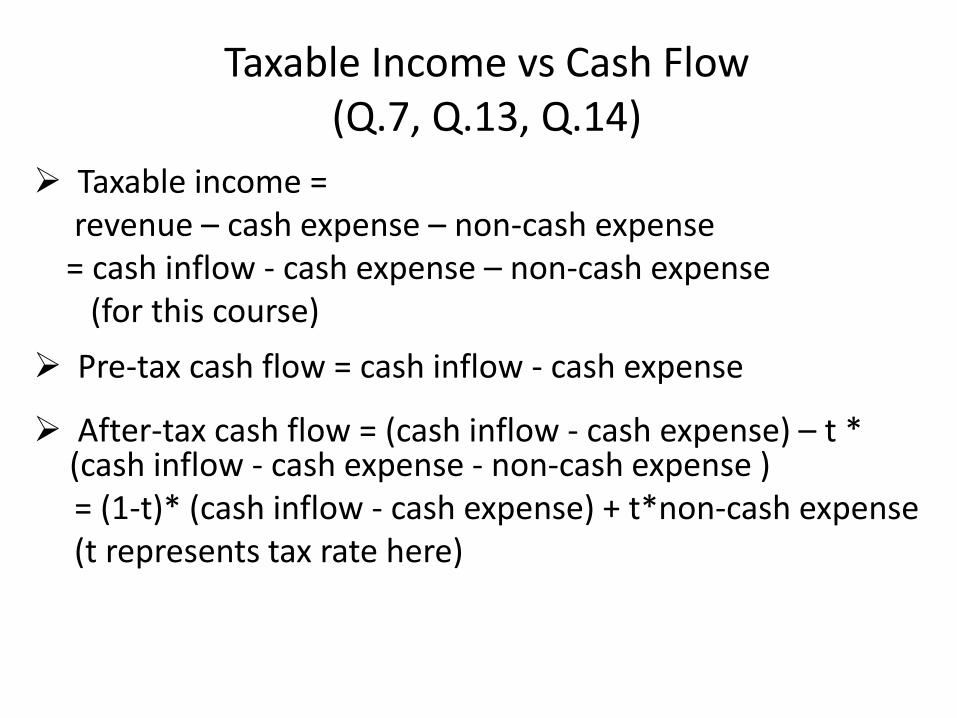

Taxable Income vs Cash Flow (Q.7, Q.13, Q.14)

Taxable income = revenue – cash expense – non-cash expense = cash inflow - cash expense – non-cash expense (for this course)

Pre-tax cash flow = cash inflow - cash expense

After-tax cash flow = (cash inflow - cash expense) – t * (cash inflow - cash expense - non-cash expense )

= (1-t)* (cash inflow - cash expense) + t*non-cash expense (t represents tax rate here)

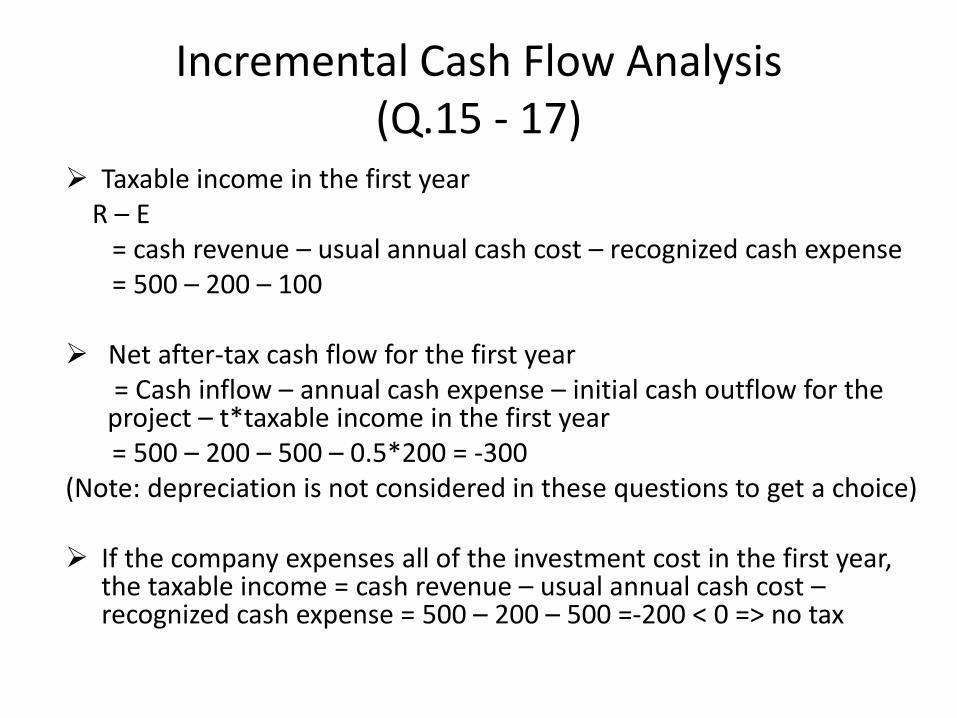

Incremental Cash Flow Analysis (Q.15 - 17)

Taxable income in the first year R – E = cash revenue – usual annual cash cost – recognized cash expense = 500 – 200 – 100 Net after-tax cash flow for the first year

= Cash inflow – annual cash expense – initial cash outflow for the project – t*taxable income in the first year

= 500 – 200 – 500 – 0.5*200 = -300 (Note: depreciation is not considered in these questions to get a choice) If the company expenses all of the investment cost in the first year,

the taxable income = cash revenue – usual annual cash cost – recognized cash expense = 500 – 200 – 500 =-200 < 0 => no tax

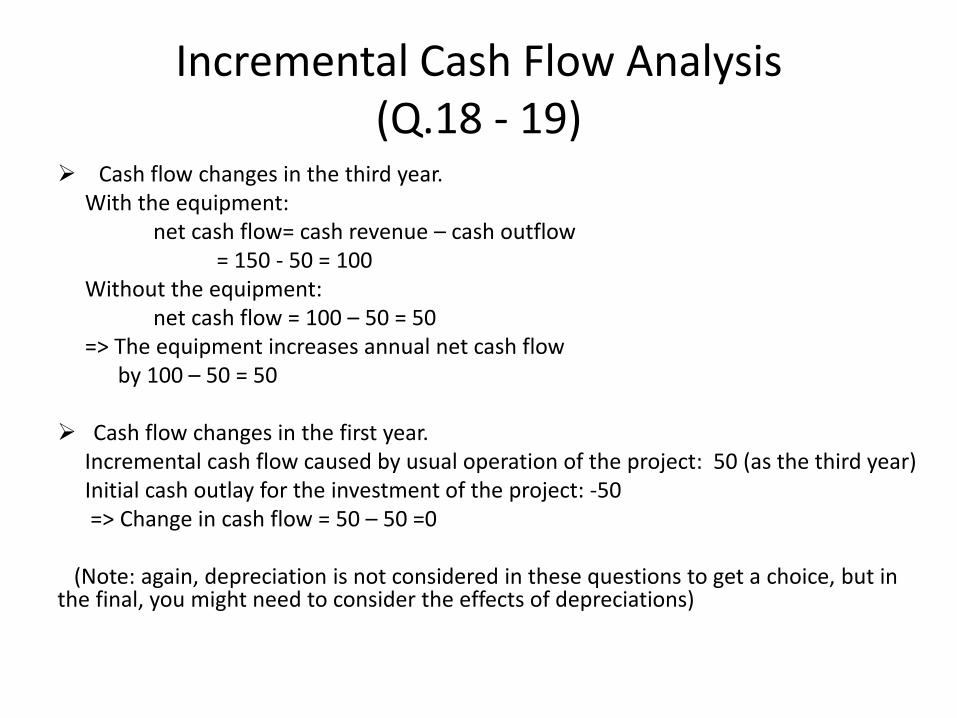

Incremental Cash Flow Analysis (Q.18 - 19)

Cash flow changes in the third year. With the equipment: net cash flow= cash revenue – cash outflow = 150 - 50 = 100 Without the equipment: net cash flow = 100 – 50 = 50 => The equipment increases annual net cash flow by 100 – 50 = 50 Cash flow changes in the first year. Incremental cash flow caused by usual operation of the project: 50 (as the third year) Initial cash outlay for the investment of the project: -50 => Change in cash flow = 50 – 50 =0 (Note: again, depreciation is not considered in these questions to get a choice, but in the final, you might need to consider the effects of depreciations)