for ca ipcc taxation amendmentscaclubindia.s3.amazonaws.com/cdn/forum/files/... · 3/27/2012 ·...

TRANSCRIPT

FOR CA IPCC Taxation

AMENDMENTS INCOME-TAX & SERVICE TAX

AY 2012-13

for May 2012 attempt

visit us at : www.saraogi.co.in

CA. PANKAJ SARAOGI Visiting faculty ICAI

ACA, B. Com (H) – SRCC, LCS, B. Ed., M. Com., DISA (ICAI)

Amendments – AY 2012-13 CA. Pankaj Saraogi

AMENDMENTS

for IPCC May 2012 attempt

INDEX

S.

No. Income-tax

Page

no.

1. Tax Rates for AY 2012-13 1

2. Expenditure on scientific research – Section 35 3

3. Deduction in respect of expenditure on specified business –

Section 35AD 3

4. Employer’s contribution to pension fund referred u/s 80CCD –

Section 36 & 80CCE 4

5. Subscription to Long-term Infrastructure Bonds – Section 80CCF 4

6. Deposit in PPF – Section 80C 5

7. Mineral Oil Business – Section 80-IB 5

8. Power Distribution Business – Section 80-IA 5

9. Cost Inflation Index (CII) for FY 2011-12 5

10. Interest on Post Office Savings Bank Account – Section 10(15) 6

11. Allowances or perquisites to member of UPSC – Section 10(45) 6

12. Exemption of specified income of notified entities not engaged in

commercial activity – Section 10(46) 6

13. Income of notified infrastructure debt funds – Section 10(47) 7

14. TDS on income by way of interest from infrastructure debt fund –

Section 194LB 7

15. Return of specified institutions – Section 139(4C) 7

Amendments – AY 2012-13 CA. Pankaj Saraogi

16. DDT exemption withdrawn on dividend by SEZ – Section 10(34)

& 115-O 7

17. Specified class or classes of persons to be exempted from filing

return of income – Section 139(1C) 8

18. Due date – Explanation 2 to Section 139(1) 8

19. Documents/transactions in which PAN required to be quoted –

Rule 114B 8

20. Permanent Account Number – Section 139A 9

21. Statement of tax deducted & deposited – Section 200 9

22. Rate of interest exempted in case of RPF 9

23. Charitable purpose – Section 2(15) 10

SCHEDULE Amendment Classes Revisionary Classes

Venue

AOC Connaught Place, Arya Public School, Raja Bajar,

Baba Kharak Singh Marg, Connaught Place, New Delhi – 110 001.

2336 2250, 93138 30650 (2.00pm – 8.00pm)

Starting date March 1st, 2012 (approx. 6 lectures) March 27

th, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm

Fees Rs. 100/student Free

Seats Limited (registration open)

SALIENT FEATURES Amendments Classes Revisionary Classes

Covers amendments by Finance Act, 2011 Revision through PPTs on various topics

Includes notifications, etc. issued upto

31/10/2011

Classroom practice of important questions

Covers Point of Taxation Rules, 2011 with

detailed analysis

Discussion on November 2011 paper

Covers 8 services in detail alongwith questions Discussion on May 2012 RTP issued by ICAI

Class room practice of questions Special emphasis on amendments, POT Rules

2011 & 8 services

Discussion on November 2011 paper Followed by 3 hours test of full course as per

CA examination pattern

Amendments – AY 2012-13 CA. Pankaj Saraogi

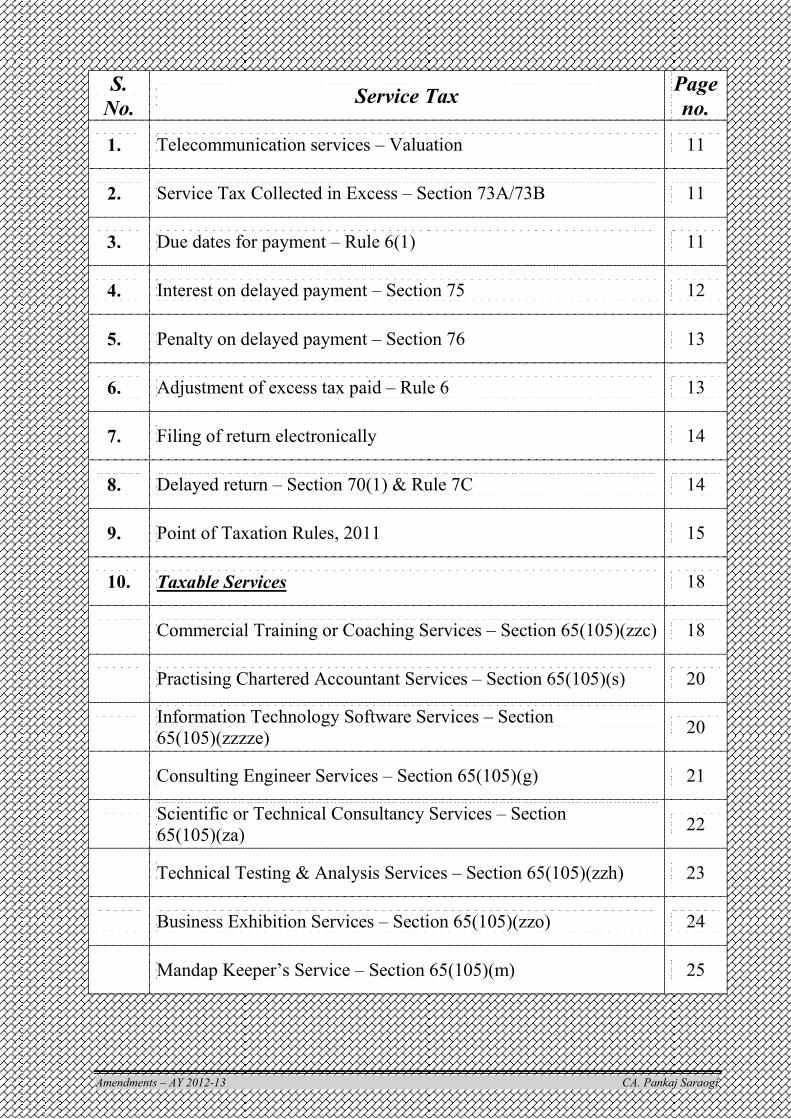

S.

No. Service Tax

Page

no.

1. Telecommunication services – Valuation 11

2. Service Tax Collected in Excess – Section 73A/73B 11

3. Due dates for payment – Rule 6(1) 11

4. Interest on delayed payment – Section 75 12

5. Penalty on delayed payment – Section 76 13

6. Adjustment of excess tax paid – Rule 6 13

7. Filing of return electronically 14

8. Delayed return – Section 70(1) & Rule 7C 14

9. Point of Taxation Rules, 2011 15

10. Taxable Services 18

Commercial Training or Coaching Services – Section 65(105)(zzc) 18

Practising Chartered Accountant Services – Section 65(105)(s) 20

Information Technology Software Services – Section

65(105)(zzzze) 20

Consulting Engineer Services – Section 65(105)(g) 21

Scientific or Technical Consultancy Services – Section

65(105)(za) 22

Technical Testing & Analysis Services – Section 65(105)(zzh) 23

Business Exhibition Services – Section 65(105)(zzo) 24

Mandap Keeper’s Service – Section 65(105)(m) 25

Amendments – AY 2012-13 CA. Pankaj Saraogi

11. Miscellaneous 28

Transport of passengers by air services 28

Life Insurer carrying on Life Insurance Business 28

Purchase or sale of foreign currency including money changing 28

Services provided by State Governments under Centrally

Sponsored Schemes (CSS) are not liable to service tax 29

Optional Composition Scheme for payment of service tax in case

of distributor or selling agents of lotteries 30

© Author

All rights reserved. No part of this book shall be reproduced, stored

in a retrieval system, or transmitted by any means without written

permission from the author.

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

1

1. Tax Rates for AY 2012-13

INDIVIDUAL/HUF/AOP/BOI/Artificial Juridical Person

(I) In the case of every individual other than the individual referred to in items (II), (III) and (IV)

of this Paragraph or HUF or AOP/BOI or every artificial juridical person -

(1) where the total income does not exceed Rs.

1,80,000

Nil

(2) where the total income exceeds Rs. 1,80,000

but does not exceed Rs. 5,00,000

10% of the amount by which the total

income exceeds Rs. 1,80,000

(3) where the total income exceeds Rs. 5,00,000

but does not exceed Rs. 8,00,000

Rs. 32,000 plus 20% of the amount by

which the total income exceeds Rs. 5,00,000

(4) where the total income exceeds Rs. 8,00,000 Rs. 92,000 plus 30% of the amount by

which the total income exceeds Rs. 8,00,000

(II) In the case of every individual, being a woman resident in India, and below the age of 6560

years at any time during the previous year, - (Amendment by Finance Act, 2011 w.e.f. AY 2012-13)

(1) where the total income does not exceed Rs.

1,90,000

Nil

(2) where the total income exceeds Rs. 1,90,000

but does not exceed Rs. 5,00,000

10% of the amount by which the total

income exceeds Rs. 1,90,000

(3) where the total income exceeds Rs. 5,00,000

but does not exceed Rs. 8,00,000

Rs. 31,000 plus 20% of the amount by

which the total income exceeds Rs. 5,00,000

(4) where the total income exceeds Rs. 8,00,000 Rs. 91,000 plus 30% of the amount by

which the total income exceeds Rs. 8,00,000

(III) In the case of every individual, being a resident in India, who is of the age of 60 years or more

but less than 80 years at any time during the previous year, -

(1) where the total income does not exceed Rs.

2,50,000

Nil

(2) where the total income exceeds Rs. 2,50,000

but does not exceed Rs. 5,00,000

10% of the amount by which the total

income exceeds Rs. 2,50,000

(3) where the total income exceeds Rs. 5,00,000

but does not exceed Rs. 8,00,000

Rs. 25,000 plus 20% of the amount by

which the total income exceeds Rs. 5,00,000

(4) where the total income exceeds Rs. 8,00,000 Rs. 85,000 plus 30% of the amount by

which the total income exceeds Rs. 8,00,000

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

2

(IV) In the case of every individual, being a resident in India, who is of the age of 80 years or more

at any time during the previous year, -

(1) where the total income does not exceed Rs.

5,00,000

Nil

(2) where the total income exceeds Rs. 5,00,000

but does not exceed Rs. 8,00,000

20% of the amount by which the total

income exceeds Rs. 5,00,000

(3) where the total income exceeds Rs. 8,00,000 Rs. 60,000 plus 30% of the amount by

which the total income exceeds Rs. 8,00,000

OTHERS

Person Tax Rate Surcharge

Firm, LLP, Local Authority 30% -NA-

Domestic Company 30% 5%*

Company other than domestic company 40% 2%*

* Surcharge shall be charged only if total income exceeds Rs. 1 crore.

* Marginal relief: In the case of every company having a total income exceeding Rs. 1 crore, the

total amount payable as income-tax and surcharge on such income shall not

exceed the total amount payable as income-tax on a total income of Rs. 1 crore

by more than the amount of income that exceeds Rs. 1 crore.

Analysis

Join amendment classes for analysis (visit www.saraogi.co.in)

Co-operative society Upto Rs. 10,000 10%

Surcharge -NA- Rs. 10,000 – Rs. 20,000 20%

Rs. 20,000 - ҄ 30%

EC & SHEC

Education Cess 2%*

Secondary & Higher Education Cess 1%*

* 2% & 1% shall be of tax + surcharge (if any)

Analysis

Join amendment classes for analysis (visit www.saraogi.co.in)

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

3

2. Expenditure on scientific research – Section 35

(w.e.f. AY 2012-13)

PAYMENT TO OUTSIDE AGENCIES

Purpose Donee Deduction Scientific research National laboratory, IIT, Specified person 200% of donation

Scientific research Research association, university, college,

other institutions, national laboratory, IIT

175% of donation

Scientific research Company (company’s main object being is

to carry on scientific research)

125% of donation

Research in social sciences,

statistical research

Research association, university, college,

other institutions

125% of donation

3. Deduction in respect of expenditure on specified business – Section 35AD

Specified business Eligible assessee

Date of

commencement of

business on or after

Setting up & operating a cold chain facility for

agricultural produce, meat, poultry products, processed

food, etc.

Any assessee April 1, 2009

Setting up & operating a warehousing facility for

storage of agricultural produce Any assessee April 1, 2009

Laying & operating a cross-country natural gas

pipeline network for distribution including storage

facilities

Indian company

or consortium of

such companies

April 1, 2007

Laying & operating a cross-country crude/ petroleum

oil pipeline network for distribution including storage

facilities

Indian company

or consortium of

such companies

April 1, 2009

Building & operating, anywhere in India, a new hotel

of 2 star or above (w.e.f. AY 2011-12) Any assessee April 1, 2010

Building & operating, anywhere in India, a new

hospital with atleast 100 beds (w.e.f. AY 2011-12) Any assessee April 1, 2010

Developing & building a housing project under a

scheme for redevelopment or rehabilitation Any assessee April 1, 2010

Developing and building a housing project under a

scheme for affordable housing (w.e.f. AY 2012-13) Any assessee April 1, 2011

Production of fertilizer in India (w.e.f. AY 2012-13) Any assessee April 1, 2011

Deduction

� 100% deduction of capital expenditure incurred during the previous year.

� 100% of capital expenditure incurred prior to commencement of business shall be allowed in

year of commencement of business only if same has been capitalized on the date of

commencement of business.

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

4

� Capital expenditure shall not include land, goodwill & financial instrument.

Other provisions

1. Business should be new business i.e. should not be formed by splitting/reconstruction of old

business.

2. Business should not be set up by transfer of old plant & machinery. Old plant & machinery

should not be more than 20% of total plant & machinery used for the business.

3. Deduction u/c VI-A shall not be allowed in respect of such business for any assessment year.

4. Actual cost of the asset for which deduction has been allowed u/s 35AD shall be taken as NIL.

Further, receipts on account of sale of these assets shall be taxable u/h PGBP only, whatever the

amount may be.

Analysis

Join amendment classes for analysis (visit www.saraogi.co.in)

4. Employer’s contribution to pension fund referred u/s 80CCD – Section 36 & 80CCE

(w.e.f. AY 2012-13)

1. Employer’s contribution to pension fund referred u/s 80CCD shall be allowed as an expense to

employer.

2. Allowance shall be limited to 10% of employee’s salary.

3. Salary, for this purpose, includes basic salary & dearness allowance, if the terms of employment

so provide.

4. Employer’s contribution shall be treated as income u/h salaries in the hands of employee without

any limit.

5. U/s 80CCD, employee is eligible to claim deduction of employer’s contribution as well as

employee’s contribution.

6. Deduction of employer’s contribution is limited to 10% of basic salary & dearness allowance, if

the terms of employment so provide.

7. Similarly, deduction of employee’s contribution is limited to 10% of basic salary & dearness

allowance, if the terms of employment so provide.

8. i.e. an employee can claim maximum deduction of 20% of basic + DA.

9. As per section 80CCE, deduction u/s 80C, 80CCC & 80CCD cannot exceed Rs. 1,00,000. But

w.e.f. AY 2012-13, 80CCE shall not apply on deduction on account of employer’s contribution.

i.e. deduction on account of employer’s contribution shall be over & above Rs. 1,00,000

deduction.

5. Subscription to Long-term Infrastructure Bonds – Section 80CCF

(section extended to AY 2012-13)

Allowed to : Individual & HUF Quantum : Maximum Rs. 20,000

Deduction is allowed for any amount paid or deposited as subscription to long-term infrastructure

bonds as may be notified by the CG.

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

5

6. Deposit in PPF – Section 80C

(w.e.f. 01/12/2011)

Deduction u/s 80C is allowed for deposit in PPF in the name of self, spouse, any child or any

member of HUF.

Deduction u/s 80C including on account of deposit in PPF cannot exceed Rs. 1,00,000.

Earlier, as per PPF Scheme, deposit in a name of single individual cannot exceed Rs. 70,000 in a

financial year. Now this limit has been increased to Rs. 1,00,000.

7. Mineral Oil Business – Section 80-IB

(w.e.f. AY 2012-13)

U/s 80-IB, income based deduction has been provided to business of commercial production and

refining of mineral oil.

Deduction in these businesses is of 100% of the profits for 7 consecutive years starting from the

year in commercial production or refining of mineral oil commences.

W.e.f. AY 2012-13, no deduction shall be allowed for business of commercial production if

licence awarded after 31/03/2011.

Businesses already claiming deduction u/s 80-IB shall continue to claim deduction.

Further, if licence is awarded on or before 31/03/2011 but business of commercial production is

started after 31/03/2011, deduction u/s 80-IB shall be allowed from the year of commercial

production.

For refining business, business shall start on or before 31/03/2012.

8. Power Distribution Business – Section 80-IA

(w.e.f. AY 2012-13)

Deduction u/s 80-IA of 100% of the profits has been provided to business of generation,

transmission & distribution of power for 10 consecutive assessment years out of first 15

consecutive assessment years starting from the year in which operation starts.

Section 80-IA also provides that deduction for such business shall be allowed only if business

commenced on or before 31/03/2011.

This sunset clause of 31/03/2011 has been extended by 1 year. i.e. deduction u/s 80-IA shall be

available if operation started on or before 31/03/2012.

9. Cost Inflation Index (CII) for FY 2011-12

Cost inflation index for FY 2011-12 shall be 785. i.e. for capital assets transferred during PY 2011-

12, CII shall be 785.

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

6

10. Interest on Post Office Savings Bank Account – Section 10(15)

(w.e.f. AY 2012-13)

Earlier, interest on Post Office Savings Bank Account was fully exempt u/s 10(15).

Now, such interest shall be exempt to the extent of Rs. 3,500 in the case of an individual account

and Rs. 7,000 in the case of joint account.

11. Allowances or perquisites to member of UPSC – Section 10(45)

(w.r.e.f. AY 2008-09)

Any allowance or perquisite, as may be notified by the Central Government, paid to the Chairman or

a retired Chairman or any other member or retired member of the Union Public Service Commission.

Notification No. 49/2011 dated 06/09/2011

In exercise of the powers conferred by section 10(45) of the Income-tax Act, 1961, the Central

Government hereby notifies the following allowances and perquisites for the purposes of the said

clause, namely:—

(1) in case of serving Chairman and members of Union Public Service Commission :—

(i) the value of rent free official residence;

(ii) the value of conveyance facilities including transport allowance;

(iii) the sumptuary allowance;

(iv) the value of leave travel concession provided to a serving Chairman or member of the

Union Public Service Commission and members of his family;

(2) in case of the retired Chairman and retired members of the Union Public Service Commission

:—

(i) a sum of maximum Rs. 14,000pm for defraying the service of an orderly and for meeting

expenses incurred towards secretarial assistance on contract basis;

(ii) the value of a residential telephone free of cost and the number of free calls to the extent of

1500pm (over and above the number of free calls per month allowed by the telephone

authorities).

This notification shall come into force retrospectively w.e.f. 1st day of April, 2008

12. Exemption of specified income of notified entities not engaged in commercial

activity – Section 10(46)

(w.e.f. 01/06/2011)

any specified income arising to a body or authority or Board or Trust or Commission which -

(a) has been established or constituted by or under a Central, State or Provincial Act, or constituted

by the Central Government or a State Government, with the object of regulating or administering

any activity for the benefit of the general public;

(b) is not engaged in any commercial activity; and

(c) is notified by the Central Government for the purposes of this clause.

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

7

Explanation

For the purposes of this clause, “specified income” means the income, of the nature and to the extent

arising to a body or authority or Board or Trust or Commission referred to in this clause, which the

Central Government may, by notification, specify in this behalf.

13. Income of notified infrastructure debt funds – Section 10(47)

(w.e.f. 01/06/2011)

Any income of an infrastructure debt fund, set up in accordance with the guidelines as may be

prescribed, which is notified by the Central Government for the purposes of this clause.

14. TDS on income by way of interest from infrastructure debt fund – Section 194LB

(w.e.f. 01/06/2011)

Where any income by way of interest is payable to a non-resident, not being a company, or to a

foreign company, by an infrastructure debt fund referred to in section 10(47), the person responsible

for making the payment shall, at the time of credit of such income to the account of the payee or at

the time of payment thereof in cash or by issue of a cheque or draft or by any other mode, whichever

is earlier, deduct income-tax thereon at the rate of 5%.

15. Return of specified institutions – Section 139(4C)

(w.e.f. 01/06/2011)

− If the total income of

o Research association – section 10(21)

o News agency – section 10(22B)

o Association or institution – section 10(23A)

o Institutions – section 10(23B)

o Fund or trust or university or other educational institution or hospital or other medical

institution – section 10(23C)

o Trade union – section 10(24)

o body or authority or Board or Trust or Commission – section 10(46)

o infrastructure debt fund – section 10(47)

− exceeds maximum amount not chargeable to tax before claiming exemption u/s 10

− shall furnish a return of income on or before time allowed u/s 139(1) and it shall be deemed to

have been filed u/s 139(1)

16. DDT exemption withdrawn on dividend by SEZ – Section 10(34) & 115-O

(w.e.f. 01/06/2011)

Earlier dividend distributed by SEZ developer or enterprise was exempt from DDT and even same

was not taxable in the hands of shareholders.

W.e.f. 01/06/2011 same has been made subject to DDT but in hands of shareholder same will

continue to be exempt.

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

8

17. Specified class or classes of persons to be exempted from filing return of

income – Section 139(1C)

(inserted newly w.e.f. 01/06/2011)

Notwithstanding anything contained in section 139(1), the Central Government may, by notification,

exempt any class or classes of persons from the requirement of furnishing a return of income having

regard to such conditions as may be specified in that notification.

Analysis

Join amendment classes for analysis (visit www.saraogi.co.in)

18. Due date – Explanation 2 to Section 139(1)

“due date” means, -

(a) where the assessee is -

(i) a company other than a company referred to in clause (aa); or

(ii) a person (other than a company) whose accounts are required to be audited under this Act

(i.e. under any section including section 44AB) or under any other law for the time being

in force; or

(iii) a working partner of a firm whose accounts are required to be audited under this Act or

under any other law for the time being in force,

the 30th day of September of the assessment year; (i.e. 30/09/2012)

(aa) in the case of an assessee being a company, which is required to furnish a report referred to in

section 92E, the 30th day of November of the assessment year; (i.e. 30/11/2012)

(b) ---

(c) in the case of any other assessee, the 31st day of July of the assessment year. (i.e. 31/07/2012) (Words in box added by Finance Act, 2011 w.e.f. AY 2011-12)

Analysis

Join amendment classes for analysis (visit www.saraogi.co.in)

19. Documents/transactions in which PAN required to be quoted – Rule 114B

(Notification no. 27/2011 dated 26/05/2011)

(w.e.f. 01/07/2011)

Rule 114B states the documents/transactions in which it is mandatory to quote the PAN of the

assessee.

Following three documents/transactions have been added, in which it is mandatory to quote PAN

(i) Making an application for issue of a debit card (credit card already covered)

(ii) payment of an amount aggregating Rs. 50,000 or more in a year as life insurance premium

to an insurer

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

9

(iii) payment to a dealer, -

(a) of an amount of Rs. 5,00,000 or more at any one time; or

(b) against a bill for an amount of Rs. 5,00,000 or more,

for purchase of bullion or jewellery:

20. Permanent Account Number – Section 139A

(w.e.f. 01/11/2011)

1) Every person, -

i. if his total income during any previous year exceeded the maximum amount which is not

chargeable to income-tax; or

ii. carrying on any business or profession whose total sales, turnover or gross receipts are or

is likely to exceed five lakh rupees in any previous year;

iii. who is required to furnish a return of income under sub-section (4A) of section 139; or

iv. who is entitled to receive any sum or income or amount, on which TDS is deductible in

any financial year,

and who has not been allotted a permanent account number shall, within such time, as may be

prescribed, apply to the Assessing Officer for the allotment of a permanent account number.

Prescribed time for making application:

− In case of (i) above – by May 31st of the relevant assessment year

− In (ii), (iii) & (iv) above – by end of the financial year

21. Statement of tax deducted & deposited – Section 200

(w.e.f. 01/11/2011)

Earlier, due dates for deposit of quarterly statements of TDS deducted & deposited were same for all

assessees.

Now, due dates w.e.f. 01/11/2011 are as follows:

If Government is the deductor: 31st July, 31

st October, 31

st January and 15

th May

If any other person is the deductor: 15th July, 15

th October, 15

th January and 15

th May.

22. Rate of interest exempted in case of RPF

In case of an employee participating in RPF, interest credited to RPF account is exempt upto 9.5%pa

upto 31/08/2010 and 8.5%pa w.e.f. 01/09/2010. Interest in excess of above is taxable in the hands of

employee u/h salaries.

By notification 24/2011 dated 13/05/2011, exemption of interest credited has been increased to

9.5%pa w.r.e.f. 01/09/2010. i.e. for whole year (whether PY 2010-11 or PY 2011-12) interest

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

10

credited to RPF account shall be exempt upto 9.5%pa and in excess of that only shall be taxable in

the hands of employee u/h salaries.

23. Charitable purpose – Section 2(15)

“charitable purpose” includes relief of the poor, education, medical relief, preservation of

environment (including watersheds, forests and wildlife) and preservation of monuments or places or

objects of artistic or historic interest, and the advancement of any other object of general public

utility:

Provided that the advancement of any other object of general public utility shall not be a charitable

purpose, if it involves the carrying on of any activity in the nature of trade, commerce or business, or

any activity of rendering any service in relation to any trade, commerce or business, for a cess or fee

or any other consideration, irrespective of the nature of use or application, or retention, of the income

from such activity:

Provided further that the first proviso shall not apply if the aggregate value of the receipts from the

activities referred to therein is Rs. 10 lacs 25 lacs or less in the previous year. (Amendment by Finance Act, 2011 w.e.f. AY 2012-13)

Analysis

Join amendment classes for analysis (visit www.saraogi.co.in)

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

11

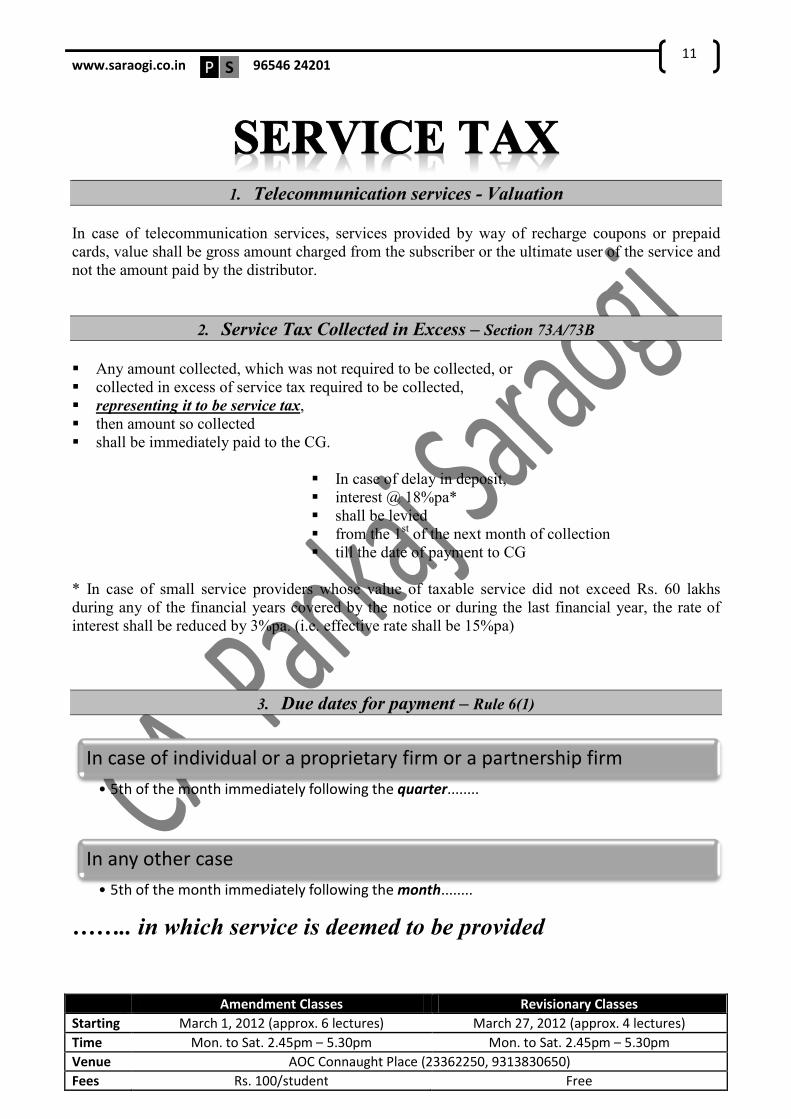

1. Telecommunication services - Valuation

In case of telecommunication services, services provided by way of recharge coupons or prepaid

cards, value shall be gross amount charged from the subscriber or the ultimate user of the service and

not the amount paid by the distributor.

2. Service Tax Collected in Excess – Section 73A/73B

� Any amount collected, which was not required to be collected, or

� collected in excess of service tax required to be collected,

� representing it to be service tax,

� then amount so collected

� shall be immediately paid to the CG.

� In case of delay in deposit,

� interest @ 18%pa*

� shall be levied

� from the 1st of the next month of collection

� till the date of payment to CG

* In case of small service providers whose value of taxable service did not exceed Rs. 60 lakhs

during any of the financial years covered by the notice or during the last financial year, the rate of

interest shall be reduced by 3%pa. (i.e. effective rate shall be 15%pa)

3. Due dates for payment – Rule 6(1)

…….. in which service is deemed to be provided

In case of individual or a proprietary firm or a partnership firm

• 5th of the month immediately following the quarter........

In any other case

• 5th of the month immediately following the month........

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

12

1. In case of e-payment of tax, substitute 5th with 6

th.

2. In case of month of March or quarter ending March, in any case, due date shall be 31st

March.

3. If the last day of payment of service tax is a public holiday, tax can be paid on next working

day.

4. Date of deposit of service tax, in case of deposit by cash, shall be the date on which cash is

tendered.

5. Date of deposit of service tax, in case of deposit by cheque, shall be the date on which cheque

is presented, subject to realization of cheque.

6. Deposit of service tax shall be only with bank designated by CBEC having ‘EASIEST’

facility. Payment of service tax into non-designated banks does not amount to payment of

service tax.

7. Deposit of service tax shall be in Form GAR-7 (earlier TR-6).

8. GAR-7 challan is a single copy challan with tax payer’s counterfoil at the bottom of challan.

Both challan and counterfoil are to be filled in by assessee. The challan should be on white

paper with black printing.

9. The challans should be serially numbered.

10. The counterfoil duly receipted by Bank with stamp of Bank will be given by receiving Bank

to assessee. The stamp of receiving bank will contain Challan Identification Number (CIN).

11. The Taxpayers acknowledgement is the evidence of payment. The Challan Identification

Number (CIN) appearing on this acknowledgement will have to be quoted in the return. The

banks will be giving the tax payer a computer generated acknowledgement/receipt with the

various details including the CIN.

12. A single GAR-7 form can be used for multiple services provided by a single provider.

However amounts attributable to each such service along with concerned accounting codes

should be mentioned clearly in the column provided for this purpose in the GAR-7 challan.

Alternatively, separate GAR-7 challans may be used for payment of service tax for each

service provided by the service provider.

13. W.e.f. 01/04/2010 – Assessee has to deposit service tax electronically in case he has

deposited service tax of Rs. 10 lakhs or more (including the amount of service tax paid by

utilisation of CENVAT credit) in the preceding financial year.

14. Payment should be rounded off in multiple of rupees.

4. Interest on delayed payment – Section 75

� In case of delay in deposit,

� interest @ 18%pa* (CG has power to notify interest rate between 10%pa to 36%pa both

inclusive)

� shall be levied

� from the day following the due date of payment (i.e. 6th/7

th/1

st)

� till the date of payment to CG.

* In case of small service providers whose value of taxable service did not exceed Rs. 60 lakhs

during any of the financial years covered by the notice or during the last financial year, the rate of

interest shall be reduced by 3%pa. (i.e. effective rate shall be 15%pa)

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

13

Notes:

Interest is mandatory.

No provision for waiver of the same.

5. Penalty on delayed payment – Section 76

� In case of delay in deposit,

� penalty may be levied

Quantum of Penalty:

� Rs. 100/day for every day during which such failure continues

� @ 1%pm (i.e. 12%pa) of shortfall in tax

whichever is higher, but restricted to:

� 50% of the service tax that the assessee has failed to pay.

6. Adjustment of excess tax paid – Rule 6

Service tax, in excess, may be paid because of following reasons:

1. Taxable service not provided later on

2. Correct estimate of service tax payable cannot be made at the time of deposit

3. Ant other reason – refund can be claimed

Situation 1

Where an assessee has issued an invoice, or received any payment, against a service to be provided

� which is not so provided by him either wholly or partially for any reason,

OR

� where the amount of invoice is renegotiated due to deficient provision of service, or any terms

contained in a contract,

the assessee may take the credit of such excess service tax paid by him, if the assessee -

(a) has refunded the payment or part thereof, so received for the service provided to the person from

whom it was received; or

(b) has issued a credit note for the value of the service not so provided to the person to whom such

an invoice had been issued.

Clarification:

If the amount of invoice is renegotiated due to deficient provision or in any other way changed in

terms of conditions of the contract (e.g. contingent on the happening or non-happening of a future

event), the tax will be payable on the revised amount provided the excess amount is either refunded

or a suitable credit note is issued to the service receiver. However, concession is not available for

bad debts.

Situation 2

In case of payment of service tax to the CG in excess of the amount required to be paid, assessee

may adjust such excess in the succeeding month/quarter, subject to following conditions:

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

14

i. Self-adjustment not allowed in case of reasons involving interpretation of law, taxability,

classification, valuation or applicability of any exemption notification.

ii. Excess amount paid or proposed to be adjusted should not exceed Rs. 2,00,000 for the

relevant month/quarter.

� Except in case of centralized registration where excess amount paid is on account of

delayed receipt of details of payments from branch offices.

iii. The details of self-adjustment should be intimated to the Superintendent of Central Excise

within a period of 15 days from the date of such adjustment.

7. Filing of return electronically

Upto 30/09/2011 – If assessee has deposited service tax of Rs. 10 lakhs or more (including the

amount of service tax paid by utilization of CENVAT credit) in the preceding financial year, then he

has to submit return electronically. W.e.f. 01/10/2011 – Every assessee shall submit the service tax

return electronically.

8. Delayed return – Section 70(1) & Rule 7C

In case of delay in filing the return, a late fee not exceeding Rs. 20,000, as may be prescribed, shall

be deposited alongwith return {section 70(1)}.

Rule 7C

Period of delay

from the date of submission

Late fee

≤ 15 days Rs. 500

> 15 days but ≤ 30 days Rs. 1,000

> 30 days Rs. 1,000 + Rs. 100/day in excess of 30 days (Max. Rs. 20,000)

� Where the assessee has paid the prescribed late fee for delayed submission of return, the

proceedings, if any, in respect of such delayed submission of return shall be deemed to be

concluded.

� Where the gross amount of service tax payable is nil, the CEO may, on being satisfied that there

is sufficient reason for not filing the return, reduce or waive the penalty (late fee).

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

15

9. POINT OF TAXATION RULES, 2011

Determination of point of taxation – Rule 3

‘Point of taxation’ shall be, -

(a) the time when the invoice for the service provided or to be provided is issued:

Provided that where the invoice is not issued within 14 days of the completion of the provision

of the service, the point of taxation shall be date of such completion.

(b) in a case, where the person providing the service, receives a payment before the time specified in

clause (a), the time, when he receives such payment, to the extent of such payment.

Explanation

Wherever any advance is received by the service provider towards the provision of taxable service,

the point of taxation shall be the date of receipt of each such advance.

Determination of point of taxation in case of change in effective rate of tax – Rule 4

Notwithstanding anything contained in rule 3, the point of taxation, in cases where there is a change

in effective rate of tax in respect of a service, shall be determined in the following manner, namely:-

(a) in case a taxable service has been provided before the change in effective rate of tax, -

(i) where the invoice for the same has been issued and the payment received after the change

in effective rate of tax, the point of taxation shall be date of payment or issuing of invoice,

whichever is earlier; or

(ii) where the invoice has also been issued prior to change in effective rate of tax but the

payment is received after the change in effective rate of tax, the point of taxation shall be

the date of issuing of invoice; or

(iii) where the payment is also received before the change in effective rate of tax, but the

invoice for the same has been issued after the change in effective rate of tax, the point of

taxation shall be the date of payment;

(b) in case a taxable service has been provided after the change in effective rate of tax, -

(i) where the payment for the invoice is also made after the change in effective rate of tax but

the invoice has been issued prior to the change in effective rate of tax, the point of taxation

shall be the date of payment; or

(ii) where the invoice has been issued and the payment for the invoice received before the

change in effective rate of tax, the point of taxation shall be the date of receipt of payment

or date of issuance of invoice, whichever is earlier; or

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

16

(iii) where the invoice has also been raised after the change in effective rate of tax but the

payment has been received before the change in effective rate of tax , the point of taxation

shall be date of issuing of invoice.

Explanation

For the purposes of this rule, “change in effective rate of tax” shall include a change in the portion of

value on which tax is payable in terms of a notification issued under the provisions of Finance Act,

1994 or rules made thereunder.

Payment of tax in cases of new services – Rule 5

Where a service is taxed for the first time, then, -

(a) no tax shall be payable to the extent the invoice has been issued and the payment received against

such invoice before such service became taxable;

(b) no tax shall be payable if the payment has been received before the service becomes taxable and

invoice has been issued within the period referred to in rule 4A of the Service Tax Rules, 1994

(i.e. within 14 days).

Determination of point of taxation in case of continuous supply of service – Rule 6

Rule 2(c)

“Continuous supply of service” means any service which is provided, or to be provided continuously,

under a contract, for a period exceeding 3 months, or where the Central Government, by a

notification, prescribes provision of a particular service to be a continuous supply of service, whether

or not subject to any condition

Notified:

(a) Telecommunication service [65(105)(zzzx)]

(b) Commercial or industrial construction [65(105)(zzq)]

(c) Construction of residential complex [65(105)(zzzh)]

(d) Internet Telecommunication Service [65(105)(zzzu)]

(e) Works contract service [65(105)(zzzza)]

Thus these services will constitute “continuous supply of services” irrespective of the period for

which they are provided or agreed to be provided. Other services will be considered continuous

supply only if they are provided or agreed to be provided continuously for a period exceeding three

months.

Rule 6

In case of continuous supply of service, the ‘point of taxation’ shall be, -

(a) the time when the invoice for the service provided or to be provided is issued:

Provided that where the invoice is not issued within 14 days of the completion of the provision

of the service, the point of taxation shall be date of such completion.

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

17

(b) in a case, where the person providing the service, receives a payment before the time specified in

clause (a), the time, when he receives such payment, to the extent of such payment.

Explanation 1

For the purpose of this rule, where the provision of the whole or part of the service is determined

periodically on the completion of an event in terms of a contract, which requires the service receiver

to make any payment to service provider, the date of completion of each such event as specified in

the contract shall be deemed to be the date of completion of provision of service.

Explanation 2

For the purpose of this rule, wherever any advance, by whatever name known, is received by the

service provider towards the provision of taxable service, the point of taxation shall be the date of

receipt of each such advance.

Determination of point of taxation in case of specified services or persons – Rule 7

Notwithstanding anything contained in these rules, the point of taxation in respect of,-

(a) the services covered by rule 3(1) of Export of Services Rules, 2005;

(b) the persons required to pay tax as recipients under the rules made in this regard in respect of

services notified u/s 68(2) of the Finance Act, 1994 (i.e. reverse charge);

(c) individuals or proprietary firms or partnership firms providing taxable services referred to in

sub-clauses (g), (p), (q), (s), (t), (u), (za), (zzzzm) of section 65(105) of the Finance Act, 1994,

shall be the date on which payment is received or made, as the case may be:

65(105)(g) consulting engineer

65(105) (p) architect

65(105) (q) interior decorator

65(105) (s) practising Chartered Accountant

65(105) (t) practising Cost Accountant

65(105) (u) practising Company Secretary

65(105) (za) scientific or technical consultancy

65(105) (zzzzm) legal consultancy

Provided that in case of services referred to in clause (a), where payment is not received within the

period specified by the Reserve Bank of India, the point of taxation shall be determined, as if this

rule does not exist.

Provided further that in case of services referred to in clause (b) where the payment is not made

within a period of six months of the date of invoice, the point of taxation shall be determined as if

this rule does not exist.

Provided also that in case of “associated enterprises”, where the person providing the service is

located outside India, the point of taxation shall be the date of credit in the books of account of the

person receiving the service or date of making the payment whichever is earlier.

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

18

10. TAXABLE SERVICES

Commercial Training or Coaching Services – Section 65(105)(zzc)

⇒ shall mean any service provided or to be provided

⇒ to any person,

⇒ by any institute or establishment providing commercial training or coaching

⇒ for imparting skill or knowledge or lessons

⇒ on any subject or field,

⇒ whether with or without issuance of a certificate,

⇒ and includes

� coaching or tutorial classes

� computer training institute

Exemptions:

sports

any preschool coaching or training

any coaching or training leading to grant of a certificate or diploma or degree or any educational

qualification which is recognised by any law

� If institute/establishment is also providing coaching or training leading to a grant of a

certificate/degree not recognized by law at the time of conducting the course, then such

service shall be taxable

� Recognised: University, deemed university under UGC Act

� If de-recognised by AICTE, MCI, ICAR, BCI, etc. then organization shall be treated as not

recognised by law.

� Collaboration with foreign institutes/universities – recognised only if recognised by law in

India

training or coaching forming essential part of course/curriculum of law recognized

degree/certificate

� Exemption not available if charges directly paid to training centre

vocational training – skills to enable person to seek employment (including self-employment)

recreational training – dance, singing, etc.

services by individuals at the premise of receiver (but not tuition bureau)

Clarifications/Explanations:

Intention of profit motive is irrelevant. In either case service tax shall be leviable.

By Finance Act, 2010, it has been cleared w.r.e.f. 01/07/2003 that commercial training or

coaching centre includes any centre/institute where training/coaching is imparted for

consideration, whether or not such centre or institute is registered as a trust/society/similar other

organization under any law and carrying on its activity with or without profit motive.

Term ‘commercial’ appearing in definition only means that such training or coaching should be

provided for a consideration, whether or not such training or coaching is conducted with a profit

motive.

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

19

Recreational training institute means a commercial training or coaching centre which provides

coaching or training relating to recreational activities such as dance, singing, martial arts,

hobbies.

Computer training institute means a commercial training or coaching centre which provides

coaching or training relating to computer software or hardware.

Vocational training institute (w.e.f. 27/02/2010) means an Industrial Training Institute (are

owned by Govt.) or an Industrial Training Centre (are owned by private parties) affiliated to the

National Council for Vocational Training, offering courses in designated trades as notified under

the Apprentices Act, 1961. (e.g. cutting and tailoring trades, beautician trades, agricultural trades,

electrical trades, glass and ceramic trades, heat engine trades, hi-tech trades)

� W.e.f. 29/04/2010, service provided in relation to Modular Employable Skill courses

approved by the National Council of Vocational Training, by a Vocational Training Provider

registered under the Skill Development Initiative Scheme with the Directorate General of

Employment and Training, Ministry of Labour and Employment, Government of India shall

also be exempt.

� Institutes offering general course on improving communication skills, how to be effective in

group discussions or personal interviews, personality development, general grooming and

finishing etc. are not covered under the definition of vocational training institute because they

only improve the chances of success for a candidate possessing required skill and do not

impart training to enable the trainee to seek employment or self-employment.

Whether donations and grants-in-aid received from different sources by a charitable Foundation

imparting free livelihood training to the poor and marginalized youth, will be treated as

‘consideration' received for such training and subjected to service tax under ‘commercial

training or coaching service'?

The important point here is regarding the presence or absence of a link between ‘consideration'

and taxable service. It is a settled legal position that unless the link or nexus between the amount

and the taxable activity can be established, the amount cannot be subjected to service tax.

Donation or grant-in-aid is not specifically meant for a person receiving such training or to the

specific activity, but is in general meant for the charitable cause championed by the registered

Foundation. Between the provider of donation/grant and the trainee there is no relationship other

than universal humanitarian interest. In such a situation, service tax is not leviable, since the

donation or grant-in-aid is not linked to specific trainee or training. (Circular No. 127/9/2010

dated August 16, 2010)

If training is provided by employer to employees in-house that shall not be taxable, but, however,

if some outside agency is appointed for the purpose, then same shall be taxable.

It does not matter if training is provided online.

Even postal coaching is liable to service tax.

Continuous education programs for professional development and creating awareness are not

commercial training and hence not taxable.

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

20

Practising Chartered Accountant Services – Section 65(105)(s)

⇒ shall mean any service provided or to be provided

⇒ to any person,

⇒ by a practising chartered accountant

⇒ in his professional capacity,

⇒ in any manner.

Exemptions:

Services relating to representing the client before any statutory authority in the course of proceedings

initiated under any law, by way of issue of notice. (omitted w.e.f. 01/05/2011)

Clarifications/Explanations:

Practising Chartered Accountant means a person who is a member of the Institute of Chartered

Accountants of India and is holding a certificate of practice granted under the provisions of

Chartered Accountants Act, 1949 and includes any concern engaged in rendering services in the field

of chartered accountancy.

In case of services by Practising Chartered Accountants, Point of Taxation Rules, 2011 provides that

services shall be deemed to be provided on the date of receipt of amount (i.e. service tax shall be

deposited on receipt basis and not on accrual basis).

Information Technology Software Services – Section 65(105)(zzzze)

⇒ shall mean any service provided or to be provided

⇒ to any person,

⇒ by any other person

⇒ in relation to information technology software

⇒ for use in the course, or furtherance, of business or commerce (omitted w.e.f. 01/07/2010)

Information technology software includes:

i. development of information technology software

ii. study, analysis, design and programming of information technology software

iii. adaptation, upgradation, enhancement, implementation and other similar services related to

information technology software

iv. providing advice, consultancy and assistance on matters related to information technology

software

v. providing the right to use ITS for commercial exploitation

vi. providing the right to use software components for the creation of and inclusion in other ITS

products

vii. providing the right to use ITS supplied electronically

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

21

Information technology software means any representation of instructions, data, sound or image,

including source code and object code, recorded in a machine readable form, and capable of being

manipulated or providing interactivity to a user, by means of computer or an automatic data

processing machine or any other device or equipment.

Exemptions:

Notification No. 53/2010-S.T. has been issued to exempt the service of providing the right to use

(whether single use or multiple use) the packaged or canned software (hereinafter referred to as ‘said

goods’) under ‘information technology software services’ from the whole of service tax, subject to

the condition that -

(i) the value of the said goods has been determined on the basis of MRP valuation (i.e. u/s 4A of

the Central Excise Act, 1944) and

(ii) (a) In case of domestic production: the excise duty has been paid; or

(b) In case of import: the custom duty has been paid.

(iii) a declaration made by the service provider on the invoice that no amount in excess of the retail

sale price declared on the said goods has been recovered from the customer.

Consulting Engineer Services – Section 65(105)(g)

⇒ shall mean any service provided or to be provided

⇒ to any person,

⇒ by a consulting engineer

⇒ in relation to

⇒ advice, consultancy or technical assistance

⇒ in any manner

⇒ in one or more disciplines of engineering

⇒ including the discipline of computer hardware engineering.

Clarifications/Explanations:

Consulting engineer means any professionally qualified engineer or any body corporate or any

other firm who, either directly or indirectly, renders this service.

Consulting engineers include self-employed professionally qualified engineer, whether or not

employing others for assistance.

Services in disciplines of both computer hardware engineering and computer software

engineering shall be taxable here only.

Disciplines of engineering includes:

� Structural engineering works

� Civil engineering works

� Mechanical engineering works

� Electrical engineering works

� Construction management

In case of Consulting Engineer Services, Point of Taxation Rules, 2011 provides that services

shall be deemed to be provided on the date of receipt of amount (i.e. service tax shall be

deposited on receipt basis and not on accrual basis).

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

22

Exemptions:

Inspection & certification by certifying agencies (covered under technical inspection &

certification service)

Service in the field of insurance survey or loss assessment

Architectural services (separately covered)

The taxable services provided by a consulting engineer to any person on transfer of technology is

exempt from so much of the service tax leviable thereon as is equivalent to the amount of cess

payable on the said transfer of technology under the provisions of section 3 of the Research and

Development Cess Act, 1986, subject to the following conditions, namely:-

(A) the said amount of Research and Development Cess is paid within six months from the date

of invoice or in case of associated enterprises the date of credit in the books of account:

Provided that the exemption shall be available only if the Research and Development Cess is

paid at the time or before the payment for the service;

(B) records of Research and Development Cess are maintained for establishing the linkage

between the invoice or the credit entry, as the case may be, and the Research and

Development Cess payment challan.

Scientific or Technical Consultancy Services – Section 65(105)(za)

⇒ shall mean any service provided or to be provided

⇒ to any person,

⇒ by a scientist or a technocrat, or any science or technology institution or organisation,

⇒ in relation to

⇒ scientific or technical consultancy.

⇒ “Scientific or technical consultancy” means

⇒ any advice, consultancy, or scientific or technical assistance,

⇒ rendered in any manner, either directly or indirectly,

⇒ by a scientist or a technocrat, or any science or technology institution or organisation,

⇒ to any person,

⇒ in one or more disciplines of science or technology.

Clarifications/Explanations:

Consultation may be in nature of an expert opinion/advice.

Service tax will be payable by public funded research institutions like CSIR, ICAR, DRDO, IIT,

IISc, Regional Engineering Colleges, etc.

Service tax will be payable even if consultancy is provided to Government Department for which

consultation fee is received.

In case of Scientific or Technical Consultancy Services, Point of Taxation Rules, 2011 provides

that services shall be deemed to be provided on the date of receipt of amount (i.e. service tax

shall be deposited on receipt basis and not on accrual basis).

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

23

Exemptions:

By doctors, medical colleges, nursing homes, hospitals, diagnostic and pathological labs, etc. as

in common parlance they are not known as scientists, technocrats, etc.

Technical Testing & Analysis Services – Section 65(105)(zzh)

⇒ shall mean any service provided or to be provided

⇒ to any person,

⇒ by a technical testing and analysis agency,

⇒ in relation to

⇒ technical testing & analysis.

⇒ Technical testing and analysis agency means

⇒ any agency or person

⇒ engaged in providing service

⇒ in relation to

⇒ technical testing and analysis.

⇒ Technical testing and analysis means

⇒ any service in relation to

⇒ physical, chemical, biological or any other scientific testing or analysis of

⇒ goods or material or information technology software or any immovable property,

⇒ but does not include

⇒ any testing or analysis services provided in relation to

⇒ human beings or animals.

Clarifications/Explanations:

Includes testing and analysis undertaken for the purpose of clinical testing of drugs and

formulations; but does not include testing or analysis for the purpose of determination of the

nature of diseased condition, identification of a disease, prevention of any disease or disorder in

human beings or animals. (i.e. medical testing & diagnosis has been excluded from service tax)

Exemptions:

Clinical testing of newly developed drugs

Testing & analysis services provided in relation to water quality testing by Government owned

State & District level laboratories

Testing & analysis of seed done by Central or State Laboratory and Central or State Certifying

Agency.

Any testing or analysis services provided in relation to human beings or animals

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

24

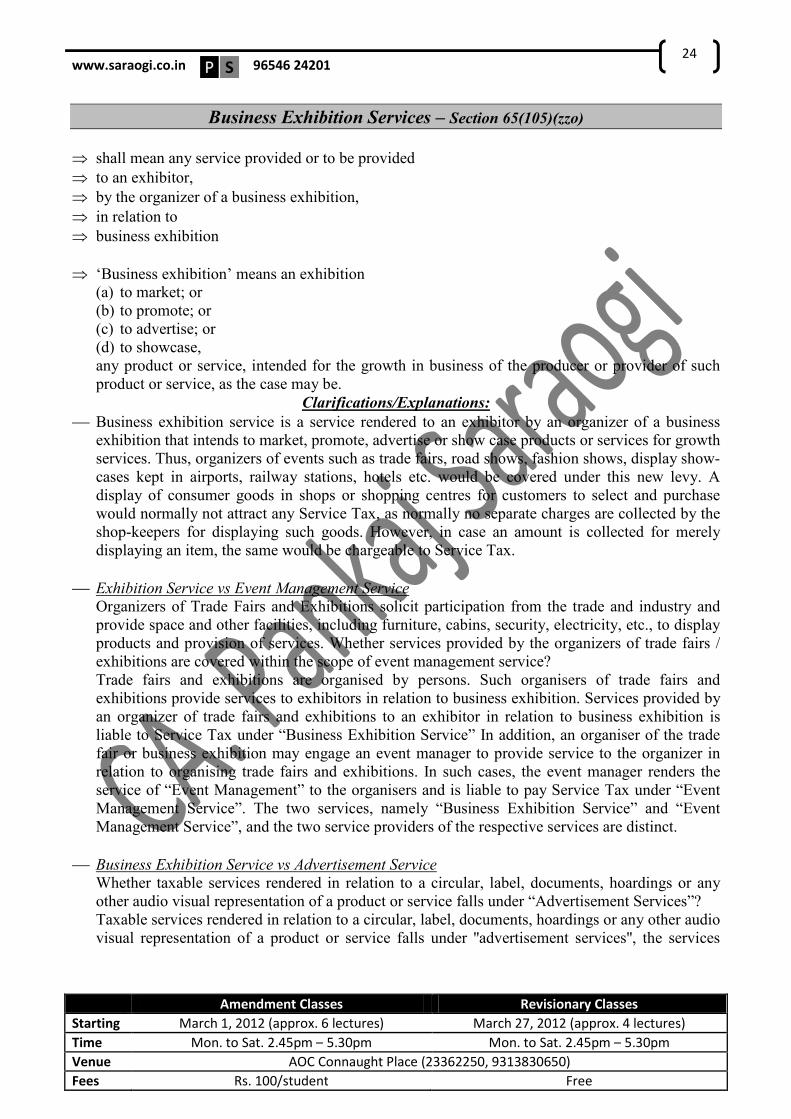

Business Exhibition Services – Section 65(105)(zzo)

⇒ shall mean any service provided or to be provided

⇒ to an exhibitor,

⇒ by the organizer of a business exhibition,

⇒ in relation to

⇒ business exhibition

⇒ ‘Business exhibition’ means an exhibition

(a) to market; or

(b) to promote; or

(c) to advertise; or

(d) to showcase,

any product or service, intended for the growth in business of the producer or provider of such

product or service, as the case may be.

Clarifications/Explanations:

Business exhibition service is a service rendered to an exhibitor by an organizer of a business

exhibition that intends to market, promote, advertise or show case products or services for growth

services. Thus, organizers of events such as trade fairs, road shows, fashion shows, display show-

cases kept in airports, railway stations, hotels etc. would be covered under this new levy. A

display of consumer goods in shops or shopping centres for customers to select and purchase

would normally not attract any Service Tax, as normally no separate charges are collected by the

shop-keepers for displaying such goods. However, in case an amount is collected for merely

displaying an item, the same would be chargeable to Service Tax.

Exhibition Service vs Event Management Service

Organizers of Trade Fairs and Exhibitions solicit participation from the trade and industry and

provide space and other facilities, including furniture, cabins, security, electricity, etc., to display

products and provision of services. Whether services provided by the organizers of trade fairs /

exhibitions are covered within the scope of event management service?

Trade fairs and exhibitions are organised by persons. Such organisers of trade fairs and

exhibitions provide services to exhibitors in relation to business exhibition. Services provided by

an organizer of trade fairs and exhibitions to an exhibitor in relation to business exhibition is

liable to Service Tax under “Business Exhibition Service” In addition, an organiser of the trade

fair or business exhibition may engage an event manager to provide service to the organizer in

relation to organising trade fairs and exhibitions. In such cases, the event manager renders the

service of “Event Management” to the organisers and is liable to pay Service Tax under “Event

Management Service”. The two services, namely “Business Exhibition Service” and “Event

Management Service”, and the two service providers of the respective services are distinct.

Business Exhibition Service vs Advertisement Service

Whether taxable services rendered in relation to a circular, label, documents, hoardings or any

other audio visual representation of a product or service falls under “Advertisement Services”?

Taxable services rendered in relation to a circular, label, documents, hoardings or any other audio

visual representation of a product or service falls under ''advertisement services'', the services

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

25

relating to actual exhibition or display of the product or services would fall under the category of

''Business Exhibition Services''.

Exemptions:

Services provided by an organiser of business exhibition for holding a business exhibition

outside India.

Mandap Keeper’s Service – Section 65(105)(m)

⇒ shall mean any service provided or to be provided

⇒ to any person,

⇒ by a mandap keeper

⇒ in relation to

⇒ the use of a mandap

⇒ in any manner

⇒ including the facilities provided or to be provided to such person in relation to such use

⇒ and also the services, if any, provided or to be provided as a caterer

⇒ “Mandap” means

any immovable property as defined in the section 3 of the Transfer of Property Act, 1882

and includes any furniture, fixtures, light fittings and floor coverings therein

let out for consideration

for organizing any official, social or business function

⇒ For this purpose, social function includes marriage.

⇒ “Mandap keeper” means

a person who allows

temporary occupation of a mandap

for consideration

for organizing any official, social or business function

⇒ “Caterer” means

any person

who supplies, either directly or indirectly,

any food, edible preparations, alcoholic or non-alcoholic beverages

or crockery and similar articles or accoutrements

for any purpose or occasion.

Clarifications/Explanations:

1. Dance, drama or music programme or competitions are social functions and allowing

temporary occupation of a hall for a consideration for organizing such functions are liable to

service tax under Mandap Keeper Service.

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

26

2. Halls, rooms etc. let out by hotels/restaurants for a consideration for organising social, official

or business functions are covered within the scope of “mandap”, and such hotels and

restaurants are covered within the scope of “mandap keeper”.

Accordingly, service tax is leviable on services provided by hotels and restaurants in relation to

letting out of halls, rooms, etc. for organizing any official, social or business function under

mandap keeper service.

3. Political meetings, film shooting are not social function and hence not taxable.

4. Renting of art gallery will get covered under Business Exhibition Service.

5. It also includes the following :-

� Kalyana mandap or marriage halls

� Banquet halls, Barat Ghar

� Conference halls etc

� Hotels and restaurants providing any such service for organising any social, official or

business function (mere reservation of seats not taxable)

6. Services of letting out of boats for organizing boat parties or events would not be liable to

service tax being boat is not an immovable property.

7. Any sports stadium or Gymkhana let out their premises for a consideration for holding official,

social or business functions would fall within the purview of Mandap.

8. The renting of Banquet halls for conducting the Seminars/conferences would fall within the

ambit of the definition of the taxable service provided by a Mandap Keeper as such

seminars/conferences are considered as official/business function.

9. Mandap let out for stay of “Barratis” for a consideration would attract Service Tax, as

“Barratis” is a part of marriage, which is a social function.

10. Letting out of school/college building or open land for marriage function, which is also a social

function, would attract Service Tax.

11. Open land /ground is to be treated as an “immovable property” as per the definition given in

section 3 of Transfer of Property Act, 1882 and hence the above premises let out for

consideration will fall under the category “Mandap” for the levy of Service Tax.

12. Screening of feature films in cinema theatres is not an official, social or business function and,

therefore, no service tax would be leviable under the category of "Mandap Keeper” for giving

the theatre on rent for showing premier shows of movies which is a part of the entire process

of making and relating the feature films in cinema theatres.

13. Meeting of Board of directors of a company is an example of business function, opening

ceremony of a shop is also a type of business function and birthday, marriage function, etc. are

instances of social function, when a company holds a seminar for their staff/officers, it would

be an official function of the company.

14. Services rendered by mandap keepers is taxable service only when he has let out some room,

halls, etc. and essentially hand over the temporary possession to the person to whom it is let

out. In other words, there is a certain exclusivity, which has been afforded to the person to

whom it has been let out. The activity of mere reservation of seats in a restaurant, hence, shall

not attract service tax.

15. Letting out furniture or any other items will not be called as 'mandap keeper' services because

no immovable property is involved.

16. Mandap keeper may not be owner of the premises.

17. If it is temporary structure, service will be taxed under Pandal or Shamiana Contractor’s

Service.

18. No tax on general donations received.

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

27

19. Service charge (even if later on distributed as tips to employees) and amenities charge shall be

included in value of taxable service being charge is on gross amount charged.

20. Sales Tax, Expenditure Tax are statutory levies, they cannot be included in the value of the

taxable services. Any calculation of the Service Tax has to be on the value of service excluding

the statutory taxes.

21. Car parking charges collected from client who availed mandap keeper service also includible in

the taxable value and liable to be taxed.

22. The charges of vessels, furniture, decoration etc, provided by the third party other than the

mandap keepers are not includible in the taxable value if the mandap keeper is not associated

with such supply in any way since the said facility is not provided by the mandap keeper.

23. If the mandap keeper raise separate bill for the charges for other facilities like furniture,

fixtures, lighting, vessels, crockery, cutlery, etc. all these charges are includible in the value of

taxable service for levy of service tax.

Exemptions/Abatements:

The taxable services provided to any person by a mandap keeper for the use of the precincts of a

religious place as a mandap are exempt from service tax leviable thereon. Religious place means

a place which is meant for conduct of prayers or worship pertaining to a religion

40% abatement is available if, value of taxable service includes use of mandap, facilities

provided to the client in relation to such use and also for the catering charges where the mandap

keeper also provides catering services, that is, supply of food and the invoice, bill or challan

issued indicates that it is inclusive of the charges for catering service. Effective rate of duty

would be 60% of normal rate in such cases.

40% abatement is available if, taxable service provided by a hotel as Mandap keeper in such

cases where services provided include catering services, that is, supply of food alongwith any

service in relation to use of a Mandap. The invoice, bill or challan issued indicates that it is

inclusive of charges for catering services. Effective rate of duty would be 60% of normal rate in

such cases. Here, the expression “hotel” means a place that provides boarding and lodging

facilities to public on commercial basis.

The expression "food” means a substantial and satisfying meal. High tea or unlimited breakfast is

a substantial meal.

Notification 12/2003 shall not apply in case of Mandap Keeper Services if catering services are

also being provided. Notification 12/2003 applies only in case contract is divisible and further

sale of goods is not covered by definition of service. In case of mandap keeper services, supply

of food & drinks has been made integral part of services and even practically supply of food &

drinks is indivisible part of mandap keeper services. (controversial matter)

www.saraogi.co.in

96546 24201

Amendment Classes Revisionary Classes

Starting March 1, 2012 (approx. 6 lectures) March 27, 2012 (approx. 4 lectures)

Time Mon. to Sat. 2.45pm – 5.30pm Mon. to Sat. 2.45pm – 5.30pm

Venue AOC Connaught Place (23362250, 9313830650)

Fees Rs. 100/student Free

28

11. MISCELLANEOUS

Special provision for payment of service tax

� Transport of passengers by air services

Notification No. 26/2010 as amended by Notification 4/2011 exempts the services of transport of

passengers by air services from so much of service tax as is in excess of –