footwear industry analysis: nike, inc. and adidas€¦ · web view · 2010-12-04with the recent...

TRANSCRIPT

2010

Andy Johnson

Anna Neugent

BJ Granack

Footwear Industry Analysis: Nike, Inc. and Adidas

Table of Contents

PART I: DESCRIBE TWO PUBLICLY TRADED BUSINESS RIVALS…………………..3

Question 1…………………...……………………………………………………………3

PART II: OPPORTUNITY……………………………………………………………………..4

Question 1…………………………………………………………………………….…..4

Question 2………………………………………………………………………………...5

PART III: INDUSTRY ANALYSIS……………………………………………………………6

Question 1………………………………………………………………………………..6

Question 2………………………………………………………………………………..9

Question 3………………………………………………………………………………..9

Question 4……………………………………………………………………………….11

PART IV: STRENGTH ASSESSMENT……………………………………………………..12

Citations…………………………………………………………………………………………13

2

PART I: DESCRIBE TWO PUBLICLY TRADED BUSINESS RIVALS

1. What two publicly traded business rivals is this paper about? Give their Corporate addresses.

Describe the businesses in which they compete against each other. What industry are these

businesses competing in?

Nike Inc. and Adidas AG are the two largest and arguably well known sportswear companies in the

world. Both companies compete against one another in the numerous industries including the athletic

footwear industry. Nike Inc. is in itself the world’s largest athletic footwear supplier, holding an

astonishing 50% of a 20 billion dollar global industry (S&P, 2010) and 40% of the US market (IBIS,

2010). Nike powers its massive lead on the market with innovative technology and product creation often

bringing all new ideas and offerings to the market before any other. Nike Inc. describes their principle

business activity as “the design, development and worldwide marketing of high quality footwear, apparel,

equipment, and accessory products” Nike earned 2009 revenues of $19,014,000,000, netting

$1,906,700,000 in profits (Nike 10-K, 2010). Nike boasts an extremely lucrative stable of world renowned

endorsers. Those endorsers include Tiger Woods, Michael Jordan, Roger Federer and Kobe Bryant to

name a few. Nike also outfits high profile sports teams such as the U.S. National basketball and soccer

teams, as well as many top tier collegiate programs across the country including Ohio State, USC and

Oregon. In 2012, Nike Inc. will also equip the National Football League (NFL) for all on-field and

officially licensed apparel. Nike’s world headquarters are located at Nike World Headquarters, One

Bowerman Drive, Beaverton, OR 97005.

Nike Inc.’s main competitor and 2nd place occupant is Adidas AG, located in Herzogenaurach, Germany.

Although Adidas falls significantly below Nike in global market share, the US is an entirely different

situation. With the recent acquisition of Reebok, Adidas AG now boasts a 40% share of the US athletic

footwear market and is a direct competitor with rival Nike (IBIS, 2010). In 2009, the Adidas Group

3

earned 10,381,000,000 euro in revenues ($13,656,209,752) (AG Annual, 2010). Primarily, Adidas had

been focused on soccer and other sports that flourished globally. Yet with their increased presence in the

United States, Adidas has launched an all out assault on territories once believed to be untouchable by

anyone other than Nike, namely the basketball market. Adidas holds significant endorsement deals just as

Nike does, with namesakes such as Kareem Abdul-Jabaar, Tyson Gay, Jim Furyk and Dwight Howard.

Adidas also is the exclusive outfitter of the NBA, as well as numerous collegiate programs such as

Michigan, NC State, and UCLA.

PART II: OPPORTUNITY

1. Define or describe the industry that these businesses compete in.

As stated, both Nike Inc. and Adidas AG have many facets to their businesses, and compete in several

industries. The athletic footwear industry is the marquee industry in which most athletic companies are

judged, and is the topic of this discussion. In the United States, sports are a way of life. Whether it is for

fashion, sport, or leisure, the athletic footwear industry in the United States is a significant industry, with

2009 sales reaching $27.4 billion (S&P, 2010). As lucrative as the business has been for a companies

such as Nike or Adidas, the tightening economy has played a role in the faltering performance of the

industry. As previously mentioned, $27.4 billion was earned in 2009, which was a drop in percentage

from 2008 figures. Over the past 5 years, industry sales revenues have decreased on an average annual

rate of 0.3% (IBIS, 2010). In the future, it will be imperative for both Nike and Adidas to develop strong

branding and desirability to appeal to the U.S. market. Nike must plan for a head on competitive battle

against Adidas and their emergence as a power in the U.S., as the business has become much more

competitive than before. The footwear industry is like a chess match, in which each decision is critical to

the immediate future of a company. For instance, Adidas’ acquisition of Reebok has proven to be

extremely valuable in garnishing a huge share of the female athletic footwear market. So much so that

Nike has refused to even enter into the women’s toning market, occupied heavily by Reebok’s Easy -

4

Tone brand and rival Sketchers. In 2009 alone, Reebok “more than doubled” its share of the female

athletic shoe market to 6.7%, in large part due to the emergence of the toning footwear market. Coupled

with Sketchers brand tripling its share to 17%, Nike lost over 7% of its market leading 31% share

(Townsend, 2010).

According to 2009 numbers, the US footwear manufacturing industry is on the steady decline, projected

to decrease at an average of 5.2% annually. Coupled with the surprising fact that over 90% of footwear

sold in the US is sourced from foreign manufacturers, the industry truly has “one foot in the grave” (IBIS,

2010). With increased competition and rising prices in the U.S., it comes as no surprise that both Nike

and Adidas have moved overseas in search of both market growth opportunities and lower production

costs.

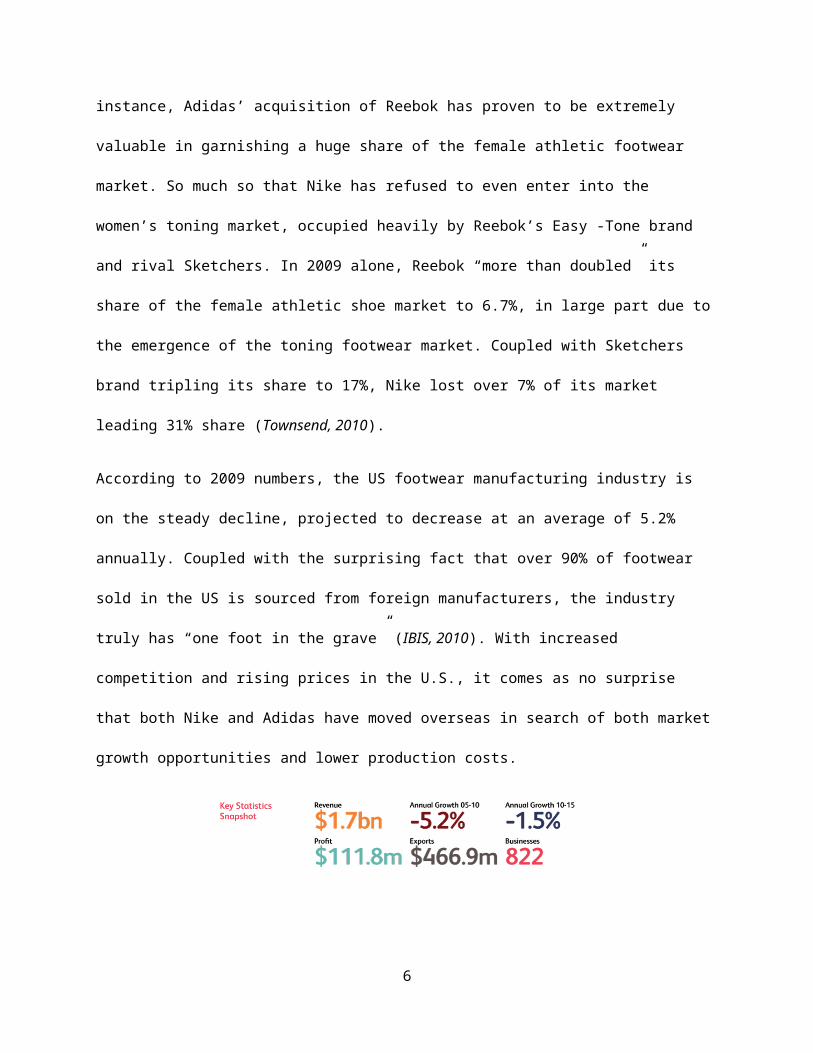

Listed above are 2009 figures, courtesy of IBISWorld, that depict the steady decline of the US athletic

footwear manufacturing industry.

This increased competition has also positioned the two companies to compete in an area traditionally

dominated by Adidas: soccer. As the 2010 South Africa World Cup sponsor, Adidas has enjoyed a firm

grasp of the market. However Nike has made a push in the segment, even making an attempt to sponsor

the German national team during the 2010 World Cup. However Adidas CEO Herbert Hainer

immediately doubled their existing offer with the Germans, whom they had sponsored since 1954, stating

that “soccer is, of course, the heart and soul of our company” (Townsend/Holger, 2010).

2. In the industry as you defined it, which geographic area is there currently the largest amount of

demand? How large is the amount of demand in this geographic area? How fast is demand

growing in this geographic area?

5

Currently, the North American market produces the highest demand for athletic footwear. At the end of

August, Nike had increased its North American market share by almost $1 billion, an increase of 8% over

quarter 2 figures. Nike complemented their North American success with gains in China, rising 11% to

$460 million (Townsend/Fenner, 2010). Adidas, who has emerged as a major player in the North

American market, reported Q2 to Q3 growth of 14% in North America and 9% in China, besting rival

Nike in its home country for only the 2nd time (Adidas Q3, 2010). Adidas group CEO Hainer echoed the

importance of the Chinese market, as well as the attempt by Adidas to directly compete in North America

with Nike in his statement, saying “I am pleased to report that the third quarter met our high expectations.

Double-digit revenue growth in football, Adidas Sport Style and Reebok year-to-date, as well as a

resumption of growth in Greater China in the third quarter all reflect a well executed 2010 strategy.”

PART III: INDUSTRY ANALYSIS

1. Do a “5-forces” Analysis for the industry you identified above. For each force, state its power

magnitude as either High, Moderate, or Low; and explain why you assigned it that magnitude of

power using the most current facts available from required sources.

With the Footwear Manufacturing dwindling in the US, buyers are beginning to gain more and more

power. Because of this, the threat of buyers is classified as high. This added power does come with a

cost though. The number of US wholesalers will drop to 1,325 in 2015 due to cheaper imports and labor

continuing to be ship overseas (IBISWorld). In 2010, footwear wholesalers made up 36.1% of the market

for manufacturers (IBISWorld). This number is expected to decline as footwear retailers also begin to

gain power. Wholesaler margins have decreased due to retailers sourcing directly from the manufacturer

(Driscoll). Fewer wholesaler buyers with diminishing profit margins mean each wholesaler is very

important to the manufacturer. Established wholesalers are acquiring increasingly larger market shares

due to smaller companies being forced out of business, thus their contracts with manufactures are

instrumental in keeping the manufacturer in business. Another reason why wholesaler contracts are

important is because the wholesale market is declining as well. This leaves a concentrated group of

6

wholesale companies who are vital to obtaining a sustainable competitive advantage. Even though the

US Footwear Retailers market segment is gaining market share on the wholesale segment, it is also

feeling the effects of off shoring. Retailers only account for 31.6% of the market (IBISWorld). These

difficult conditions have forced many retailers out of business. Enterprise numbers have fallen from

10,985 in 2005 to 10,415 in 2010 (IBISWorld). This is pushing the retail market in the same direction as

the wholesale market. Manufacturers will begin to rely more heavily on the established retailers who can

provide them enough business to maintain their own market share within the footwear manufacturing

industry. Without these wholesale and retail buyers, the manufacturer would lose a substantial amount of

profit and ultimately be forced out of business by competitors who are stronger in key success factors.

Rivalry is a high-power threat in the Footwear Manufacturing industry. This is partly due to a

diminishing US Footwear Manufacturing industry and the increase in buyer power. IBISWorld forecasts

industry revenue will decline at a five-year annual rate of 1.5% to $1.6 billion by 2015 (IBISWorld). Less

revenue and the shift of the power to the buyers makes each buyer more and more important to a

manufacturer. Also, with their increase in power, buyers are able place orders infrequently which

increases the threat of rivalry. To further the threat of rivalry, there are many competitors that are roughly

the same size. Nike, Adidas AG, and The Timberland Company are 3 of the largest footwear

manufacturers (IBISWorld). The threat of rivalry is even more prevalent in offshore manufacturing. The

opportunity for low cost labor has driven many manufacturers to transplant operations abroad. Because

of this you have these large companies such as Nike and Adidas competing for resources in the same

regions. Some companies, like Nike, are posting revenue declines even with these opportunities for low-

cost labor. Nike's revenues dropped to $19.0 billion at the end of the 2010 fiscal year (Nike).

Substitutes were classified as a high power threat. When determining power magnitude of Substitutes, it

is important to distinguish the difference between the US Footwear Manufacturing industry and US

companies that have their footwear manufactured overseas. The US Footwear Manufacturing industry

encompasses companies that manufacture shoes within the borders of the United States. Due to the trend

7

of outsourcing and the declining US Footwear Manufacturing industry, the threat of substitutes is

classified as “High”. Even if a US company was created and instituting a low cost leadership strategy, it

would not be able to compete in the cost of doing business when compared to a company that has

outsourced their manufacturing. Wholesalers and retailers are much more likely to purchase footwear

from manufacturing industries in Asia, where Adidas does 97% of its total footwear production, or in

Vietnam, where Nike does 37% of its manufacturing, because it is cheaper (IBISWorld). The US

footwear consumer market continues to thrive off of imported shoes. China remains the single largest

importer of footwear into the United States, accounting for 76.3% of total imports, an estimated $14.7

billion in 2010 (IBISWorld). If a company that is currently manufacturing in the United States is

unwilling to outsource its labor, it will not be able to compete with the larger companies such as Nike and

Adidas on a price based strategy.

Due to the various geographic locations that are typically associated with outsourcing manufacturing and

their abundance of resources, the threat of suppliers was given a moderate power-level. While Adidas

produces 97% of their total production in Asia, most of this comes from China. This has forced

companies such as Nike to look for other suppliers and have spread out their manufacturing to Vietnam,

Thailand, and Indonesia (IBISWorld). The vast majority of these suppliers are not capable of forward

integration and look to manufacturing companies to purchase their supplies. With the increase in demand

for low-cost labor, came an increase in the amount of suppliers. There is not, however, a surplus in

supplies as larger companies seek to engage in contracts with these companies as soon as possible

(Driscoll).

Currently, the US Footwear Manufacturing industry is not a very attractive option for new entrants.

Because of this, the threat of entry has been classified as low-to-moderate. Imports continue to infiltrate

the industry, growing at an average rate of 2.5% annually and satisfying nearly 95.0% of domestic

demand by 2015. This will force participants out of the industry at an average annual rate of 1.5% to 662

companies in 2015 (1). This is a result of weak domestic demand and strong price competition from low-

8

cost importers. Companies have not been able to sustain profits or operations, sending the industry into a

state of decline (4). The future does not look promising either. IBISWorld forecasts imports to grow at

an annual rate of 2.5% to $21.8 billion from 2010 to 2015 (5). In order to enter the US Footwear

Manufacturing industry, a company would have to identify a niche market and focus their efforts on

that. One benefit to the Footwear Manufacturing industry is that the start-up investment requirement is

relatively low. Footwear manufacturers operating within this industry use approximately 10.6 units of

labor for each unit of capital. A labor-to-capital ratio of 10.6:1 indicates a low level of capital

requirements (6). Also, the level of technological advancement in the Footwear Manufacturing industry

is low. This means machinery turn-over due to innovation is low and thus capital spent in acquiring the

machine is well spent. Even with benefits such as these, the declining US Footwear Manufacturing

industry is not attractive due to the lack of opportunities for profit.

2. Count the LOW-power forces you identified in your 5-forces analysis and use the count to make a

conclusion about whether the expected profitability for the average rival is High, Moderate, or

Low. Briefly explain what that magnitude of profitability means financially.

The footwear industry only has one low-power force, threat of entry. Due to this, the expected

profitability for a company with no unique strengths or weaknesses on key success factors will be less

than the cost of capital. This makes the industry very unattractive to potential businesses. If an average

business was to enter this industry, it would more than likely be forced to cease its operations by a larger,

more established manufacturer.

3. Explain the meaning of the term “Key Success Factor?” List and describe (in words, like a

definition) at least six Key Success Factors that any competitor in this industry must be good at to

be profitable. For each KSF, give a calculation that you can use to measure each rival on it.

9

A Key Success Factor (KSF) is a specific resource or activity a company must be good at in order to be

profitable within an industry. Key Success Factors allow a company to defend against high power threats

to profit and satisfy consumer demand (Young).

Low internal cost is a key success factor that a company must be strong on when competing in the

footwear manufacturing industry. Manufacturing a product at the lowest possible cost is very important

in today's Footwear Manufacturing industry. The outsourcing of manufacturing is very prevalent and

because of this, the US Footwear Manufacturing industry is declining. In order to stay competitive,

manufacturers must lower their internal cost. Low internal cost is determined by looking at cost of good

sold.

Another key success factor is economies of scope. Footwear manufacturing firms that produce a wide

range of footwear products can satisfy various segments of consumer demand. Economies of scope is

important in footwear manufacturing because fixed costs associated with production can be spread across

multiple product lines. This lowers the cost per item and increased profit. Economies of scope is

calculated by dividing the number of product lines by the cost of goods sold.

Economies of Scale are based on achieving a lower cost of production due to an increased amount of

production. Producing footwear items at the lowest marginal cost is an important competitive factor. A

larger amount of production spreads the costs of production over a wider range and thus reduces the cost

of production per product.

G* is calculated by taking (1 minus the dividend payout ratio) multiplied by the Return on Equity. G* is

used to determine the potential growth from a financial standpoint. The higher the G*, the more potential

for growth. If the G* is a negative number, the company will require more financial investment in order

to maintain its current place in the market.

10

Manufacturing Efficiency is calculated by taking the total sales number and dividing them by the cost of

goods sold. In this case, the lower the percentage, the better. Manufacturing efficiency is important

because it gives the company an idea of how much their costs are factored into their sales. If a company

is high in manufacturing efficiency, they can manufacture more products that will meet the demands of

their customers.

The final key success factor is outsourcing a portion of manufacturing. This can be seen by looking at the

total amount of production done within the United States compared to production doneIn order to keep

input costs down, manufacturers must be willing to source their products from low-priced foreign

providers, either by establishing supply contracts with third parties or moving their own facilities

overseas. This is vital for success in the footwear manufacturing industry because approximately 67.7%

of manufacturers business comes from wholesalers and retailers who typically look to purchase the

cheapest product (IBISWorld). By outsourcing some manufacturing, internal costs are kept to a

minimum and the manufacturer can sell their product at a lower price. If a manufacturer does not

outsource, they will not be able to compete and be forced out of business by larger, more integrated

companies.

4. For one KSF you listed, explain how it protects profit from one Hi-Power Threat you listed in

(III.1). If there are no Hi-power threats, then explain for a Moderate-Power threat.

One major key success factor that will protect profit is having low internal cost. Having a low internal

cost allows the manufacturer to be competitive on price. This helps protect profit from the high-power

threat of rivalry. In order to stay competitive in the waning US Footwear Manufacturing industry, a

manufacturer must be able to compete on price. By being strong in having a low internal cost, the

manufacturer can pass these cost savings onto the price of the product and thus charge less to wholesalers

and retailers looking to purchase their footwear.

11

PART IV: STRENGTH ASSESSMENT

Key Success Factor Formula Nike Distinctive Competency Score(Scale of 1-5, 1=Weakest,

5=Strongest)Low Internal Costs Cost of Goods Sold $10,571,700 1Economies of Scope Product Lines/Cost of Goods Sold (33/$10,571,700)=

.000003121

Economies of Scale Costs/Total Assets $10,571,700/$13,249,600=.79788824

1

G-Star (G*) Rating (1-Dividend Payout) * ROE (1-.31963409) * .17101479=.11635263 or 11.635263%

5

Manufacturing Efficiency Sales/Cost of Goods Sold $19,176,100/$10,571,700=1.81390883

5

Willingness to Outsource a % of Manufacturing

Total % of Manufacturing done outside of the US

100% 3

Average 2.66

Key Success Factor Formula Adidas Distinctive Competency Score(Scale of 1-5, 1=Weakest,

5=Strongest)Low Internal Costs Cost of Goods Sold $7,586,255 5Economies of Scope Product Lines/Cost of Goods Sold (27/$7,586,255)=

.000003565

Economies of Scale Costs/Total Assets ($7,586,355/$11,876,525)=.63876892

5

G-Star (G*) Rating (1-Dividend Payout) * ROE [(1-.28000956) * .04854992]=.03495548 or 3.495548%

1

Manufacturing Efficiency Sales/Cost of Goods Sold ($13,891,854.20/$7,586,260)=1.83118216

1

Willingness to Outsource a % of Manufacturing

Total % of Manufacturing done outside of the US

100% 3

Average 3.33

***Based on the strength assessment of the key success factors for both Nike, Inc. and Adidas, Adidas comes out with the higher strength average. This makes Adidas a stronger competitor in comparison to Nike, Inc. based on the Key Success Factors from the Footwear Industry.

12

Citations

Adidas, Group. Adidas Group 9 Months 2010 Results. Adidas AG, 4 Nov. 2010. Web. 1 Dec. 2010.

<http://www.adidas-group.com/en/pressroom/archive/2010/04Nov2010.aspx>.

Adidas Group 2009 Annual Report. Adidas Group, 2010. Web. 1 Dec. 2010. <http://adidas

group.corporate-publications.com/2009/gb/en/adidas-kompakt/financial-highlights.html>.

Adidas Consolidated Balance Sheet. Adidas Group, 2010. Web. 1 Dec. 2010.

<http://adidasgroup.corporate-publications.com/2009/gb/en/consolidated-financial-statements/

consolidated-balance-sheet.html>

Adidas Consolidated Income Statement. Adidas Group, 2010. Web. 1 Dec. 2010. <http://adidas

group.corporate-publications.com/2009/gb/en/consolidated-financial-statements/consolidated-

income-statement.html>

Driscoll, Marie. Apparel & Footwear: Retailers & Brands. Standard & Poor's, 2 Sept. 2010. Web. 2 Dec.

2010. <http://www.netadvantage.standardandpoors.com.www.lib.ncsu.edu:2048/NASApp

/NetAdvantage/showIndustrySurvey.do?code=apf>.

Footwear Manufacturing in the US. IBISWorld, October 2010. Web. 1 Dec. 2010.

<http://www.ibisworld.com.www.lib.ncsu.edu:2048/industryus/default.aspx?indid=369>.

IBIS World U.S. Footwear Manufacturing. IBISWorld, 2010. Web. 1 Dec. 2010.<http://www.

ibisworld.com.www.lib.ncsu.edu:2048/industryus/Majorcompanies.aspx?indid=369>.

Nike, Inc. Form 10-K. United States Securities and Exchange Commission. 20 July 2010. Web. 1 Dec.

2010. <http://secfilings.com/SearchResults.aspx?ticker=NKE>.

Nike Incorporated: Highlights. MSN, 2010. Web. 1 Dec. 2010.<http://moneycentral.msn.com/investor/

invsub/results/hilite.asp?Symbol=US:NKE>

13

Nike/SEC,. United States Securities and Exchange Commission Form 10-K. Nike Inc., 31 May 2010.

Web. 1 Dec. 2010.<http://investing.businessweek.com/research/stocks/financials/drawFiling

.asp?formType=10-K>.

Paula L. Stepankowsky. (2007, September 21). Nike's Net Gets Big Boost From Overseas Markets. Wall

Street Journal (Eastern Edition), p. B.3. Retrieved December 3, 2010, from Wall Street Journal.

(Document ID: 1339233611).

Standard and Poor's Net Advantage. Standard & Poor\'s, 2010. Web. 1 Dec. 2010.

<http://www.netadvantage.standardandpoors.com.www.lib.ncsu.edu:2048/NASApp/NetAdvanta

ge/simpleSearchRun.do?ControlName=HomePageSearch>.

Standard & Poor's Net Advantage. Standard & Poor\'s, 2010. Web. 1 Dec. 2010.

<http://www.netadvantage.standardandpoors.com.www.lib.ncsu.edu:2048/NASApp/

NetAdvantage/simpleSearchRun.do?ControlName=CompaniesSimpleSearch>.

Townsend, Matt. As Nike Scoffs, Toning Shoes Gain Traction. Business Week, 6 June 2010. Web. 1 Dec.

2010.<http://web.ebscohost.com.www.lib.ncsu.edu:2048/ehost/detail?

vid=2&hid=112&sid=2891efef-8823-4e3f

af4933b0f7944408%40sessionmgr113&bdata=JnNpdGU9ZWhvc3QtbGl2ZSZz

Y29 wZT1zaXRl#db=buh&AN=51241985>.

Townsend, Matt, and Holger Elfes "Adidas' Big Boney Defense Against Nike." Bloomberg Businessweek

2/3.4179 (2010): 22. NCSU Libraries. Web. 1 Dec.2010.<http://web.ebscohost.com.www.lib.

ncsu.edu:2048/ehost/detail?vid=6&hid=112&sid=2891efef-8823-4e3f-af49-

33b0f7944408%40sessionmgr113&bdata=JnNpdGU9ZWhvc3QtbGl2ZSZzY29wZT1zaXRl#

db=buh&AN=50542554>.

Townsend, Matt & Robert Fenner. Nike China Orders Rise 25% on Demand for Basketball Sportswear.

Bloomberg, 24 Sep. 2010. Web. 1 Dec. 2010. <http://www.bloomberg.com/news/2010-09

23/nike-s-first-quarter-profit-beats-somes-estimates-as-china-sales-climb-10-.html>.

Young, Greg. Strategic Vision, Mission, and Plan. North Carolina State University. 25 Aug. 2010. Web.

30 Nov. 2010 <http://mie480.files.wordpress.com/2010/08/mie480_lec03.ppt>.

14

15