food packaging market 2014 2024

TRANSCRIPT

©noticeThis material is copyright by visiongain. It is against the law to reproduce any of this material without the prior written agreement of vision-gain. You cannot photocopy, fax, download to database or duplicate in any other way any of the material contained in this report. Each pur-chase and single copy is for personal use only.

Food Packaging Market Forecast 2014-2024 & Future Prospects for

Leading Companies

www.visiongain.com

Contents 1. Executive Summary

1.1 Global Market Overview

1.2 Benefits of this Report

1.3 Who is this Report for?

1.4 Methodology

1.5 Global Food Packaging Market Forecast 2014-2024

1.6 Food Packaging Submarkets Forecasts 2014-2024

1.7 Leading National Food Packaging Market Forecasts 2014-2024

2. Introduction to the Food Packaging Market 2.1 Food Packaging Market Structure Overview

2.2 Food Packaging at a Resource Level

2.3 Metal Resources

2.4 Paperboard Resources

2.5 Plastics and Glass Resources

2.6 Energy Costs

2.7 Health Concerns

2.8 Changing Demographics

2.9 Durability

2.10 Reversing Disposability

2.11 Packaging Perceptions

2.12 Limit Reached

2.13 New Materials in Development

2.14 A Glance at the Decade

3. Global Food Packaging Market 2014-2024 3.1 Global Food Packaging Market Outlook

3.2 Western European Food Packaging Market 2014-2024

3.3 Eastern European Food Packaging Market 2014-2024

3.4 Asia-Pacific Food Packaging Market 2014-2024

3.5 South American Food Packaging Market 2014-2024

3.6 North American Food Packaging Market 2014-2024

3.7 Middle Eastern Food Packaging Market 2014-2024

3.8 Oceanic Food Packaging Market 2014-2024

3.9 African Food Packaging Market 2014-2024

www.visiongain.com

Contents 4. Food Packaging Material Submarkets 2014-2024 4.1 Food Packaging Market Outlook by Submarket

4.2 Rigid Plastic Food Packaging Market 2014-2024

4.2.1 Rigid Plastics Market Fundamentals

4.2.2 Are Plastics The Dominating Material?

4.2.3 Rigid Plastics Easier on Design and Branding

4.2.4 A Convenient Material

4.2.5 Are We Moving Towards Non Traditional Plastics?

4.2.6 Plastic in the West

4.3 Flexible Plastic Food Packaging Market 2014-2024

4.3.1 Flexible Plastics Market Fundamentals

4.3.2 Flexible Pouches Are Leading The Way In Which Market?

4.4 Paper Food Packaging Market 2014-2024

4.4.1 Paperboard Food Packaging Market Fundamentals

4.4.2 What Niche Market Does Paperboard Excel In?

4.4.3 Paperboard Claims The Middle And Higher Consumer Tiers

4.4.4 Is Paperboard As Environmental As We Think It Is?

4.4.5 Market Outlook

4.5 Metal Food Packaging Market 2014-2024

4.5.1 Metal Food Packaging Market Fundamentals

4.5.2 Meeting the Growing Needs Of The New Demographic

4.5.3 The Need for Tamper Proof Packaging

4.5.4 100% Recoverable

4.5.5 Hesitation In The Industry

4.6 Glass Food Packaging Market 2014-2024

4.6.1 Glass Food Packaging Market Fundamentals

4.6.2 Starting Strong But Lacking Follow Through

4.6.3 The Most Resilient Material?

4.6.4 Who Is Driving The Growth In Glass?

4.6.5 Cost Reduction Strategise Aiding The Glass Market

4.6.6 What Does The Future Hold For Glass?

4.7 Other Food Packaging Market 2014-2024

4.7.1 Other Food Packaging Market Fundamentals

4.7.2 Is There A Lack Of Funding For Research And Development?

4.7.3 Once The Short Run Is Over What Will Happen?

www.visiongain.com

Contents 5. Leading National Food Packaging Markets 2014-2024 5.1 Food Packaging Market Outlook by Country

5.2 US Food Packaging Market 2014-2024

5.2.1 US Food Packaging Market Fundamentals

5.2.2 Which Packaging Material Does the US Favour?

5.2.3 A Very Linear Growth Pattern

5.3 Japanese Food Packaging Market 2014-2024

5.3.1 Japanese Food Packaging Market Fundamentals

5.3.2 Why Does The Japanese Food Packaging Market Stand Out?

5.3.3 Is Japan’s Food Packaging Industry Ready for the New Demographic?

5.4 German Food Packaging Market 2014-2024

5.4.1 German Food Packaging Market Fundamentals

5.4.2 Neither Excelling Or Declining

5.4.3 What Trend is On Germany’s Mind

5.4.4 Artisan Foods Are the Growing Urban German Food Trend

5.5 French Food Packaging Market 2014-2024

5.5.1 French Food Packaging Market Fundamentals

5.5.2 France Tails Germany in the Food Packaging Market

5.5.3 How Does The French Food Market Operate?

5.5.4 The French Food Collaboration

5.5.5 New Regulations And Plastics

5.6 Chinese Food Packaging Market 2014-2024

5.6.1 The Third Largest Market And Growing

5.6.2 Civil Unrest Slowing Growth

5.6.3 Why Is Packaged Food in China Perceived So Well?

5.6.4 What Do The Chinese Classes Want From Their Food Packaging?

5.7 UK Food Packaging Market 2014-2024

5.7.1 A Dwindling UK Market

5.7.2 Is The UK Market Expecting Growth?

5.7.3 The Worlds Most Innovative Packaging Market

5.7.4 Which Way Is The UK Food Packaging Market Heading?

5.8 Italian Food Packaging Market 2014-2024

5.8.1 Italian Food Packaging Market Fundamentals

5.8.2 Declining Initially But Re-emergence Not Too Far Away

5.8.3 Cost Effective Food Packaging Is The Italian Trend

5.9 Canadian Food Packaging Market 2014-2024

5.9.1 Canadian Food Packaging Market Fundamentals

www.visiongain.com

Contents 5.9.2 How Are Canadian Demographics Affecting The Market?

5.9.3 Market Outlook

5.10 Spanish Food Packaging Market 2014-2024

5.10.1 The Smallest European Market at $6.3bn

5.10.2 Food And Charity In Spain

5.10.3 The Spanish Food Market Is In Decline

5.10.4 A 0.1% Increase In AGR And A Lost Generation

5.11 Australian Food Packaging Market 2014-2024

5.11.1 Australia Is Rising But How High Does It Get?

5.11.2 Where Do Australians Eat?

5.11.3 Why Australians Want More See-Through Packaging

5.12 South Korean Food Packaging Market 2014-2024

5.12.1 South Korean Food Packaging Market Fundamentals

5.12.2 Japanese Influences

5.12.3 Augmented Packaging Will Be Seen Here First

5.12.4 The Leading Food Packaging Material In South Korea

5.13 Brazilian Food Packaging Market 2014-2024

5.13.1 Brazil At The End Of The Table

5.13.2 Catching Up With A 6% Growth Rate

5.13.3 Brazil Is At The Food Consumption Trend Cross Road

5.13.4 Will Brazil Ever Match The Western Economies?

5.14 Russian Food Packaging Market 2014-2024

5.14.1 One of the Fastest Growing Food Packaging Markets

5.14.2 A Developing Import and Domestic Russian Food Market

5.14.3 A Different Demographic Target

5.15 Indian Food Packaging Market 2014-2024

5.15.1 Still Less Than 1% Of The Global Market

5.15.2 What Is Holding The Indian Market Back?

5.15.3 On The Go Eating

5.15.4 What Do The Other Indian Economic Classes Do?

5.16 Rest of World Food Packaging Market 2014-2024

5.16.1 The Rest Of The World Food Packaging Market Fundamentals

5.16.2 The Next 11 Leading National Food Packaging Markets

5.16.3 Technology Versus Population

www.visiongain.com

Contents 6. SWOT Analysis of the Global Food Packaging Market

7. Expert Opinion 7.1 Expert – Mark Smyth, Business Development & Marketing Intelligence Director, Metal –

Europe, Ardagh Group

7.1.1 What would you say are the key developments in packaging and the food packaging

market?

7.1.2 Do you think metal packaging and glass packaging can compete with other materials

in the packaging market in terms of light weighting?

7.1.3 Would you say the dynamics of the food packaging market will remain the same in

the near future?

7.1.4 Do you think the drive towards more sustainability is an advantage for metal and

glass packaging?

7.1.5 Would you say the quality of packaging differs in the developed markets compared to

the developing markets?

7.1.6 How does the price of metals affect the metal packaging industry?

7.1.7 So would you say that metal packaging is more affected by the price of metals than

plastic packaging is affected by the price of oil?

7.1.8 Do you think branding will play an even larger part in the future, more so than the

packaging itself?

7.1.9 What are the other drivers for food packaging growth other than the GDP growth a

country experiences?

7.1.10 Do you think metal and glass packaging have an advantage over other food

packaging materials in terms of them being perceived as being more luxurious or

higher quality?

7.1.11 Do you think plastic packaging has an advantage over metal and glass in terms of

transportation costs because it is a lot lighter?

8. The Leading Food Packaging Companies 2014 8.1 Amcor

8.1.1 Amcor Analysis

8.2 Ardagh Group

8.2.1 Ardagh Group Analysis

8.3 Ball Corporation

8.3.1 Ball Corporation Analysis

www.visiongain.com

Contents 8.4 Bemis Company Inc

8.4.1 Bemis Company Inc Analysis

8.5 Crown Holdings Inc

8.5.1 Crown Holdings Inc Analysis

8.6 DS Smith Plc

8.6.1 DS Smith Plc Analysis

8.7 MeadWestVaco Corporation

8.7.1 MeadWestVaco Corporation Analysis

8.8 Mondi Group

8.8.1 Mondi Group Analysis

8.9 Owens-Illinois, Inc

8.9.1 Owens-Illinois, Inc Analysis

8.10 Reynolds Group Holdings

8.10.1 Reynolds Group Holdings Analysis

8.11 Rexam Plc

8.11.1 Rexam Plc Analysis

8.12 Saint Gobain

8.12.1 Saint Gobain Analysis

8.13 Tetra Laval Group

8.13.1 Tetra Laval Group Analysis

8.14 Other Leading Companies in the Food Packaging Market

9. Conclusion 9.1 Market Outlook

9.2 Global Food Packaging Market Forecast 2014-2024

9.3 Food Packaging Submarket Forecasts 2014-2024

9.4 Leading National Food Packaging Market Forecasts 2014-2024

10. Glossary

www.visiongain.com

Contents List of Tables Table 1.1 Global Food Packaging Market Forecast Summary 2014, 2019, 2024 ($bn, CAGR %)

Table 1.2 Food Packaging Submarkets Forecasts Summary 2014, 2019, 2024 ($bn, CAGR %)

Table 1.3 Leading National Food Packaging Market Forecasts Summary 2014, 2019, 2024 ($bn,

CAGR %)

Table 3.1 Global Food Packaging Market Forecast 2014-2024 ($bn, AGR %, CAGR%, Cumulative)

Table 4.1 Food Packaging Submarket Forecasts 2014-2024 ($bn, AGR %)

Table 4.2 Rigid Plastic Food Packaging Submarket Forecast 2014-2024 ($bn, AGR %, CAGR%,

Cumulative)

Table 4.3 Flexible Plastic Food Packaging Submarket Forecast 2014-2024 ($bn, AGR %, CAGR%,

Cumulative)

Table 4.4 Paper Food Packaging Submarket Forecast 2014-2024 ($bn, AGR %, CAGR%,

Cumulative)

Table 4.5 Metal Food Packaging Submarket Forecast 2014-2024 ($bn, AGR %, CAGR%,

Cumulative)

Table 4.6 Glass Food Packaging Submarket Forecast 2014-2024 ($bn, AGR %, CAGR%,

Cumulative)

Table 4.7 Other Food Packaging Submarket Forecast 2014-2024 ($bn, AGR %, CAGR%,

Cumulative)

Table 5.1 Leading National Food Packaging Markets Forecast 2014-2024 ($bn, AGR %)

Table 5.2 US Food Packaging Market Forecast 2014-2024 ($bn, AGR %, CAGR%, Cumulative)

Table 5.3 Japanese Food Packaging Market Forecast 2014-2024 ($bn, AGR %, CAGR%,

Cumulative)

Table 5.4 German Food Packaging Market Forecast 2014-2024 ($bn, AGR %, CAGR%,

Cumulative)

Table 5.5 French Food Packaging Market Forecast 2014-2024 ($bn, AGR %, CAGR%,

Cumulative)

Table 5.6 Chinese Food Packaging Market Forecast 2014-2024 ($bn, AGR %, CAGR%,

Cumulative)

Table 5.7 UK Food Packaging Market Forecast 2014-2024 ($bn, AGR %, CAGR%, Cumulative)

Table 5.8 Italian Food Packaging Market Forecast 2014-2024 ($bn, AGR %, CAGR%, Cumulative)

Table 5.9 Canadian Food Packaging Market Forecast 2014-2024 ($bn, AGR %, CAGR%,

Cumulative)

Table 5.10 Spanish Food Packaging Market Forecast 2014-2024 ($bn, AGR %, CAGR%,

Cumulative)

Table 5.11 Australian Food Packaging Market Forecast 2014-2024 ($bn, AGR %, CAGR%,

www.visiongain.com

Contents Cumulative)

Table 5.12 South Korean Food Packaging Market Forecast 2014-2024 ($bn, AGR %, CAGR%,

Cumulative)

Table 5.13 Brazilian Food Packaging Market Forecast 2014-2024 ($bn, AGR %, CAGR%,

Cumulative)

Table 5.14 Russian Food Packaging Market Forecast 2014-2024 ($bn, AGR %, CAGR%,

Cumulative)

Table 5.15 Indian Food Packaging Market Forecast 2014-2024 ($bn, AGR %, CAGR%,

Cumulative)

Table 5.16 Rest of the World Food Packaging Market Forecast 2014-2024 ($bn, AGR %, CAGR%,

Cumulative)

Table 6.1 SWOT Analysis of the Food Packaging Market 2014-2024

Table 8.1 Leading 13 Packaging Companies With a Presence in Food Packaging 2014 (Market

Ranking, Total Revenue $bn)

Table 8.2 Amcor Company Overview 2014 (Total Revenue, HQ, Ticker, Contact, Website)

Table 8.3 Ardagh Group Company Overview 2014 (Total Revenue, HQ, Website)

Table 8.4 Ball Corporation Company Overview 2014 (Total Revenue, HQ, Ticker, Contact,

Website)

Table 8.6 Crown Holdings Inc Company Overview 2014 (Total Revenue, HQ, Ticker, Contact,

Website)

Table 8.7 DS Smith Plc Company Overview 2014 (Total Revenue, HQ, Ticker, Contact, Website)

Table 8.8 MeadWestVaco Company Overview 2014 (Total Revenue, HQ, Ticker, Contact,

Website)

Table 8.9 Mondi Group Company Overview 2014 (Total Revenue, HQ, Ticker, Contact, Website)

Table 8.10 Owens-Illinois, Inc Company Overview 2014 (Total Revenue, HQ, Ticker, Contact,

Website)

Table 8.11 Reynolds Group Holdings Company Overview 2014 (Total Revenue, HQ, Website)

Table 8.12 Rexam Plc Company Overview 2014 (Total Revenue, HQ, Ticker, Contact, Website)

Table 8.13 Saint Gobain Company Overview 2014 (Total Revenue, HQ, Ticker, Contact, Website)

Table 8.14 Tetra Laval Group Company Overview 2014 (Total Revenue, HQ, Website)

Table 8.15 Other Leading Companies in the Food Packaging Market 2014 (Company, Description)

Table 9.1 Global Food Packaging Market Forecast Summary 2014, 2019, 2024 ($bn, CAGR %)

Table 9.2 Food Packaging Submarkets Forecasts Summary 2014, 2019, 2024 ($bn, CAGR %)

Table 9.3 Leading National Food Packaging Market Forecasts Summary 2014, 2019, 2024 ($bn,

CAGR %)

www.visiongain.com

Contents List of Figures Figure 2.1 Global Food Packaging Market Structure Overview

Figure 3.1 Global Food Packaging Market Forecast 2014-2024 ($bn, AGR%)

Figure 4.1 Food Packaging Submarket Forecasts 2014-2024 ($bn)

Figure 4.2 Food Packaging Submarkets Share Forecast 2014 (%)

Figure 4.3 Food Packaging Submarkets Share Forecast 2019 (%)

Figure 4.4 Food Packaging Submarkets Share Forecast 2024 (%)

Figure 4.5 Rigid Plastic Food Packaging Submarket Forecast 2014-2024 ($bn, AGR%)

Figure 4.6 Rigid Plastic Food Packaging Submarket Share Forecast 2014, 2019 and 2024 (%)

Figure 4.7 Flexible Plastic Food Packaging Submarket Forecast 2014-2024 ($bn, AGR%)

Figure 4.8 Flexible Plastic Food Packaging Submarket Share Forecast 2014, 2019 and 2024 (%)

Figure 4.9 Paper Food Packaging Submarket Forecast 2014-2024 ($bn, AGR%)

Figure 4.10 Paper Food Packaging Submarket Share Forecast 2014, 2019 and 2024 (% Share)

Figure 4.11 Metal Food Packaging Submarket Forecast 2014-2024 ($bn, AGR%)

Figure 4.12 Metal Food Packaging Submarket Share Forecast 2014, 2019 and 2024 (% Share)

Figure 4.13 Glass Food Packaging Submarket Forecast 2014-2024 ($bn, AGR%)

Figure 4.14 Glass Food Packaging Submarket Share Forecast 2014, 2019 and 2024 (% Share)

Figure 4.15 Other Food Packaging Submarket Forecast 2014-2024 ($bn, AGR%)

Figure 4.16 Other Food Packaging Submarket Share Forecast 2014, 2019 and 2024 (% Share)

Figure 5.1 Leading National Food Packaging Markets Forecast 2014-2024 ($bn)

Figure 5.2 Leading National Food Packaging Markets Share Forecast 2014 (%)

Figure 5.3 Leading National Food Packaging Markets Share Forecast 2019 (%)

Figure 5.4 Leading National Food Packaging Markets Share Forecast 2024 (%)

Figure 5.5 US Food Packaging Market Forecast 2014-2024 ($bn, AGR%)

Figure 5.6 US Food Packaging Market Share Forecast 2014, 2019 and 2024 (% Share)

Figure 5.7 Japanese Food Packaging Market Forecast 2014-2024 ($bn, AGR%)

Figure 5.8 Japanese Food Packaging Market Share Forecast 2014, 2019 and 2024 (% Share)

Figure 5.9 German Food Packaging Market Forecast 2014-2024 ($bn, AGR%)

Figure 5.10 German Food Packaging Market Share Forecast 2014, 2019 and 2024 (% Share)

Figure 5.11 French Food Packaging Market Forecast 2014-2024 ($bn, AGR%)

Figure 5.12 French Food Packaging Market Share Forecast 2014, 2019 and 2024 (% Share)

Figure 5.13 Chinese Food Packaging Market Forecast 2014-2024 ($bn, AGR%)

Figure 5.14 Chinese Food Packaging Market Share Forecast 2014, 2019 and 2024 (% Share)

Figure 5.15 UK Food Packaging Market Forecast 2014-2024 ($bn, AGR%)

Figure 5.16 UK Food Packaging Market Share Forecast 2014, 2019 and 2024 (% Share)

Figure 5.17 Italian Food Packaging Market Forecast 2014-2024 ($bn, AGR%)

Figure 5.18 Italian Food Packaging Market Share Forecast 2014, 2019 and 2024 (% Share)

www.visiongain.com

Contents Figure 5.19 Canadian Food Packaging Market Forecast 2014-2024 ($bn, AGR%)

Figure 5.20 Canadian Food Packaging Market Share Forecast 2014, 2019 and 2024 (% Share)

Figure 5.21 Spanish Food Packaging Market Forecast 2014-2024 ($bn, AGR%)

Figure 5.22 Spanish Food Packaging Market Share Forecast 2014, 2019 and 2024 (% Share)

Figure 5.23 Australian Food Packaging Market Forecast 2014-2024 ($bn, AGR %, CAGR%,

Cumulative)

Figure 5.24 Australian Food Packaging Market Share Forecast 2014, 2019 and 2024 (% Share)

Figure 5.25 South Korean Food Packaging Market Forecast 2014-2024 ($bn, AGR%)

Figure 5.26 South Korean Food Packaging Market Share Forecast 2014, 2019 and 2024 (%

Share)

Figure 5.27 Brazilian Food Packaging Market Forecast 2014-2024 ($bn, AGR%)

Figure 5.28 Brazilian Food Packaging Market Share Forecast 2014, 2019 and 2024 (% Share)

Figure 5.29 Russian Food Packaging Market Forecast 2014-2024 ($bn, AGR%)

Figure 5.30 Russian Food Packaging Market Share Forecast 2014, 2019 and 2024 (% Share)

Figure 5.31 Indian Food Packaging Market Forecast 2014-2024 ($bn, AGR%)

Figure 5.32 Indian Food Packaging Market Share Forecast 2014, 2019 and 2024 (% Share)

Figure 5.33 Rest of the World Food Packaging Market Forecast 2014-2024 ($bn, AGR%)

Figure 5.34 Rest of the World Food Packaging Market Share Forecast 2014, 2019 and 2024 (%

Share)

Companies Mentioned in This Report

Acme Sales

Alufoil Products Pvt. Ltd.

Amcor

Anchor Europe Ltd

Anji Xingzhong Bamboo and Wooden Crafts Co. Ltd

Ardagh Group

ArpanFP

Asianet UK, Ltd

Ball Corporation

Bemis Company Inc

Biodegradable Food Service, LLC

BiodegradableStore.com

Cap-it-all Ltd.

Cartotecnica Olimpia s.r.l.

Chadwicks of Bury Ltd

www.visiongain.com

Contents Chien Fua Bio-tech Industry Co. Ltd

Coextruded Plastic Technologies, Inc.

Confoil Pty Ltd

Constar International

Crown Holdings Inc

Dempson Packaging Ltd

DS Smith Plc

Dyne-a-pak Inc.

Ekan Concepts Inc.

Finest City Paper, Inc

Framarx/Waxstar

Gelpa Packaging

Grays Packaging Co.

GTM Converting Ltd

Guillin Group

H.S. Inc.

HL Paper Products, Inc

Honor Plastic Industrial Co. Ltd

Huhtamaki Oyj

Innovatra

Intraplás S.A.

Kaboglu Plastic

Loynds International Ltd

Manjushree Technopack Ltd

MeadWestVaco Corporation

Metropolitan Tea Company Ltd

Modern Cups Enterprise Co, Ltd.

Mondi Group

MoranUSA, LLC

National Packaging Associates Corp.

Nicholl Food Packaging

Northpak Packaging

Owens-Illinois Inc

Pacific States Plastics

Packaging 4

Packaging Partners, Ltd.

Pakplast International Pty. Ltd.

www.visiongain.com

Contents Paterson Paper

Pinnacle Plastic Containers

Piz Industries

Print n Pack

Rapid'o Pack

Rexam Plc

Reynolds Group Holdings

Rieke Packaging Systems Englass

Saint Gobain

Scopenext Ltd

SEM Plastik Ltd

Sirane, Ltd

Soil Association

Supreme Foodservice AG

Taipei Pack Industries Corp.

Tech II, Inc.

Tetra Laval Group

Thinware Products Industries, Sdn. Bhd.

Tipper Tie Inc.

Wallace Packaging, LLC

www.visiongain.com

Contents Government Agencies and Other Organisations Mentioned in This

Report ASX

British Brands

Dublin Stock Exchange

DuPont Awards

European Union

FAO (Food and Agriculture Office of the UN)

INCPEN

International Aluminium Institute

JSE

LSE

MOO

NYSE

Paris Stock Exchange

Pro2Pac

Red Cross

The Packaging Federation

Trading Standards Office

UK Packaging Awards

UN (United Nations)

World Bank

Page 49

www.visiongain.com

Food Packaging Market Forecast 2014-2024 & Future Prospects for Leading Companies

4.6.4 Who Is Driving The Growth In Glass?

The growth that is seen in the glass food packaging market will be driven by the emerging market

as the more developed economies which were hit the hardest by the recession have reached a

plateau and their demand levels are falling for glass food packaging. The emerging market on the

other hand are finding their feet and embracing the luxury and import markets which they can now

afford, glass is placed extremely well within these markets to take advantage of this increased

demand. Within the emerging markets it is the wealthier middle classes that look to import glass

packaged food stuffs as they will want to trade up on food products and aim to access a higher

perceived quality of edible goods. Such products are luxury chocolate, refined pasta sauces and

condiments and spices such as honey, cinnamon, saffron and oils. Counteracting this trend,

western and European countries will remain stagnant and look to maintain their level of luxury and

premium foodstuffs and possibly cut down on such consumption in the short run.

4.6.5 Cost Reduction Strategise Aiding The Glass Market

Aiding the strength of glass in the food packaging market is the attempts of the glass food

manufacturers to light weight. Lightweight initiatives within glass food packaging are making glass

packaged food more convenient for the end consumer whilst also lowering the producers carbon

footprint and reducing distribution costs. Glass manufacturers are also trying to compete with the

plastics market by making glass packaging more brandable by emphasising and widening the

range of colours, sizes and design possibilities of glass packaging.

4.6.6 What Does The Future Hold For Glass?

The future for the glass food packaging market will follow a similar trend to that seen after the

financial crash where the rise of superstore and supermarket own branded goods have led to a rise

in the use of paperboard and both rigid and flexible plastic packaging,. The reasoning for this is

simply a cost one as glass is the most expensive packaging material, whereas plastics and

paperboard are the cheapest possible packaging. The rise in paperboard and plastic packaging did

not severely diminish sales looking forward due to the premium value associated with glass. Those

shoppers who buy supermarket own branded goods have traded, from goods that were previously

of a same level to supermarket own branded food and as such packaged in a relatively similar

packaging rather than traded down from luxury food stuffs packaged in glass.

Page 69

www.visiongain.com

Food Packaging Market Forecast 2014-2024 & Future Prospects for Leading Companies

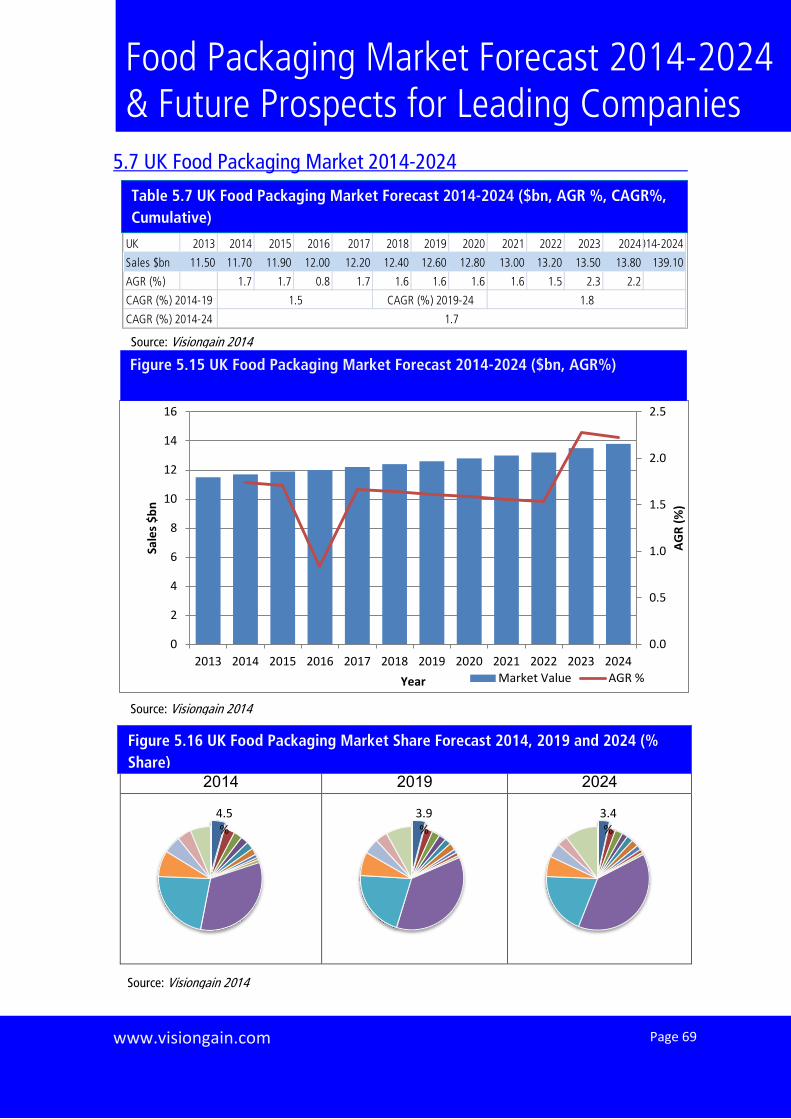

UK 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024014-2024

Sales $bn 11.50 11.70 11.90 12.00 12.20 12.40 12.60 12.80 13.00 13.20 13.50 13.80 139.10

AGR (%) 1.7 1.7 0.8 1.7 1.6 1.6 1.6 1.6 1.5 2.3 2.2

1.8CAGR (%) 2014-19

CAGR (%) 2014-24 1.7

CAGR (%) 2019-241.5

0.0

0.5

1.0

1.5

2.0

2.5

0

2

4

6

8

10

12

14

16

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024AG

R (%

)

Sale

s $b

n

Year Market Value AGR %

5.7 UK Food Packaging Market 2014-2024

2014 2019 2024

4.5%

3.9%

3.4%

Table 5.7 UK Food Packaging Market Forecast 2014-2024 ($bn, AGR %, CAGR%, Cumulative)

Figure 5.16 UK Food Packaging Market Share Forecast 2014, 2019 and 2024 (% Share)

Figure 5.15 UK Food Packaging Market Forecast 2014-2024 ($bn, AGR%) Source: Visiongain 2014

Source: Visiongain 2014

Source: Visiongain 2014

Page 109

www.visiongain.com

Food Packaging Market Forecast 2014-2024 & Future Prospects for Leading Companies

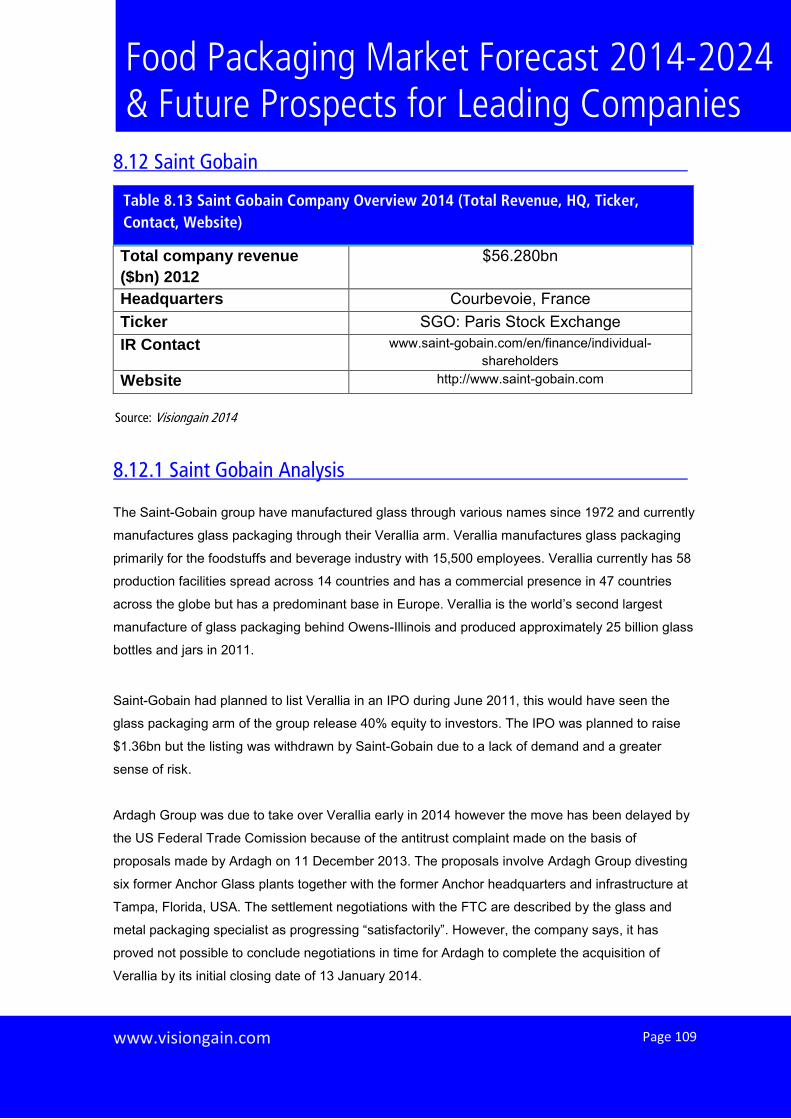

8.12 Saint Gobain

Total company revenue ($bn) 2012

$56.280bn

Headquarters Courbevoie, France Ticker SGO: Paris Stock Exchange IR Contact www.saint-gobain.com/en/finance/individual-

shareholders Website http://www.saint-gobain.com

8.12.1 Saint Gobain Analysis The Saint-Gobain group have manufactured glass through various names since 1972 and currently

manufactures glass packaging through their Verallia arm. Verallia manufactures glass packaging

primarily for the foodstuffs and beverage industry with 15,500 employees. Verallia currently has 58

production facilities spread across 14 countries and has a commercial presence in 47 countries

across the globe but has a predominant base in Europe. Verallia is the world’s second largest

manufacture of glass packaging behind Owens-Illinois and produced approximately 25 billion glass

bottles and jars in 2011.

Saint-Gobain had planned to list Verallia in an IPO during June 2011, this would have seen the

glass packaging arm of the group release 40% equity to investors. The IPO was planned to raise

$1.36bn but the listing was withdrawn by Saint-Gobain due to a lack of demand and a greater

sense of risk.

Ardagh Group was due to take over Verallia early in 2014 however the move has been delayed by

the US Federal Trade Comission because of the antitrust complaint made on the basis of

proposals made by Ardagh on 11 December 2013. The proposals involve Ardagh Group divesting

six former Anchor Glass plants together with the former Anchor headquarters and infrastructure at

Tampa, Florida, USA. The settlement negotiations with the FTC are described by the glass and

metal packaging specialist as progressing “satisfactorily”. However, the company says, it has

proved not possible to conclude negotiations in time for Ardagh to complete the acquisition of

Verallia by its initial closing date of 13 January 2014.

Table 8.13 Saint Gobain Company Overview 2014 (Total Revenue, HQ, Ticker, Contact, Website)

Source: Visiongain 2014