food bowl route - department of infrastructure ... bowl rail alignment would solve for the region...

TRANSCRIPT

FOOD BOWLROUTE Summary Report

3

Summary Report

The Food Bowl Inland Rail Alliance

The Food Bowl Inland Rail Alliance (FBIRA) represents the local governments of Mitchell, Greater Shepparton, and Moira in Victoria and Berrigan, Jerilderie, Urana, Griffith, Leeton and Narrandera in NSW. The Alliance has been formed with the aim of ensuring the Australian Government gives further consideration to routing the Melbourne to Brisbane Inland Rail via the Food Bowl Route through Shepparton, Tocumwal and Narrandera given the extraordinary export growths being experienced in Australia’s most economically diverse and prosperous primary production and food processing region. The FBIRA is strongly supported by the extensive network of producers, value adding processors and suppliers within the region.

Inland Rail Food Bowl RouteThe Melbourne–Brisbane Inland Rail project is a once-in-a-generation opportunity to transform the movement of goods in eastern Australia. This will unequivocally increase relationships between Australians living in rural, regional, and major urban areas and it will create greater ties and stronger affiliations between domestic goods and the ever growing export markets around the globe. For these reasons it has rightly been championed by the Australian Government as a key piece of national infrastructure. This project will dramatically increase the efficiency and productivity of Australia’s freight rail industry, resulting in a more competitive inter-capital freight transport market.

However, the Inland Rail project can be much more. The Food Bowl Route runs through Australia’s major agricultural heartlands which already produce over $10 billion of the nation’s annual agricultural yield, and this infrastructure has the potential to unlock unprecedented economic growth and productivity gains:

- The various geographic and climatic conditions across the Food Bowl, coupled with the extensive irrigation infrastructure, mean the region is home to a vast array of primary produce including dairy, grain, livestock, wine, fruit, vegetables, cotton, rice, tree nuts, timber and fertilisers. As the region continues to evolve, producers are adapting and diversifying into new and lucrative crops.

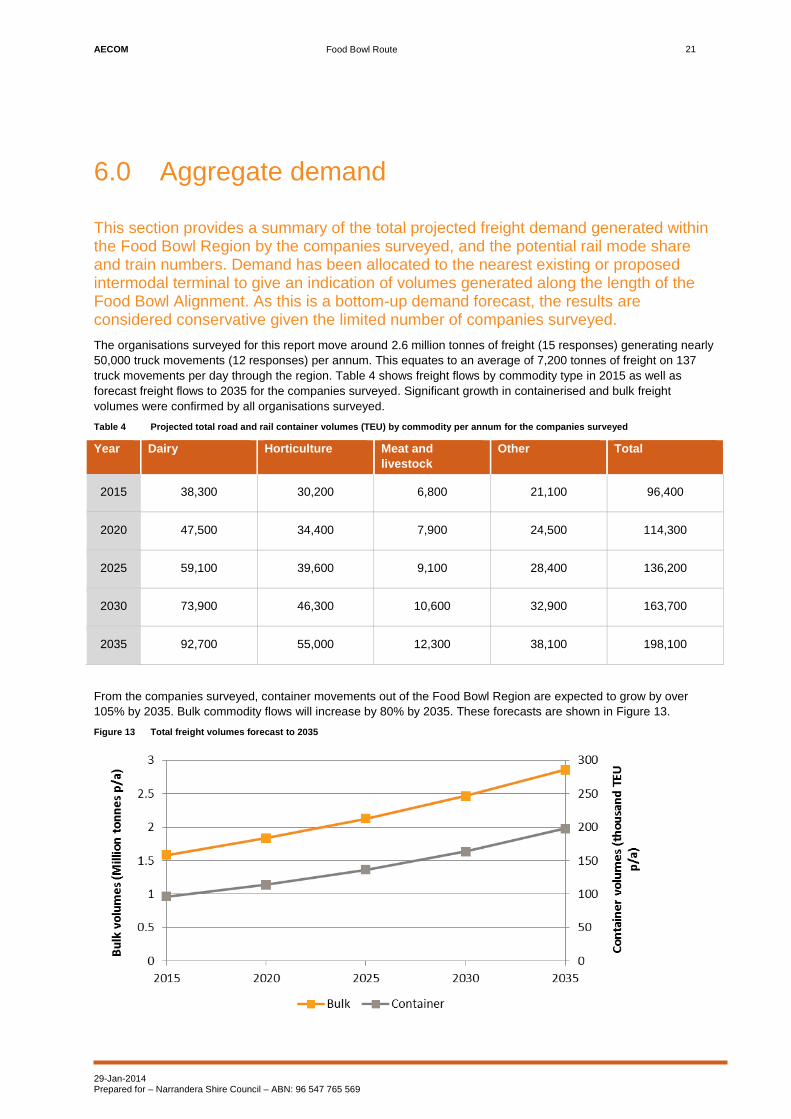

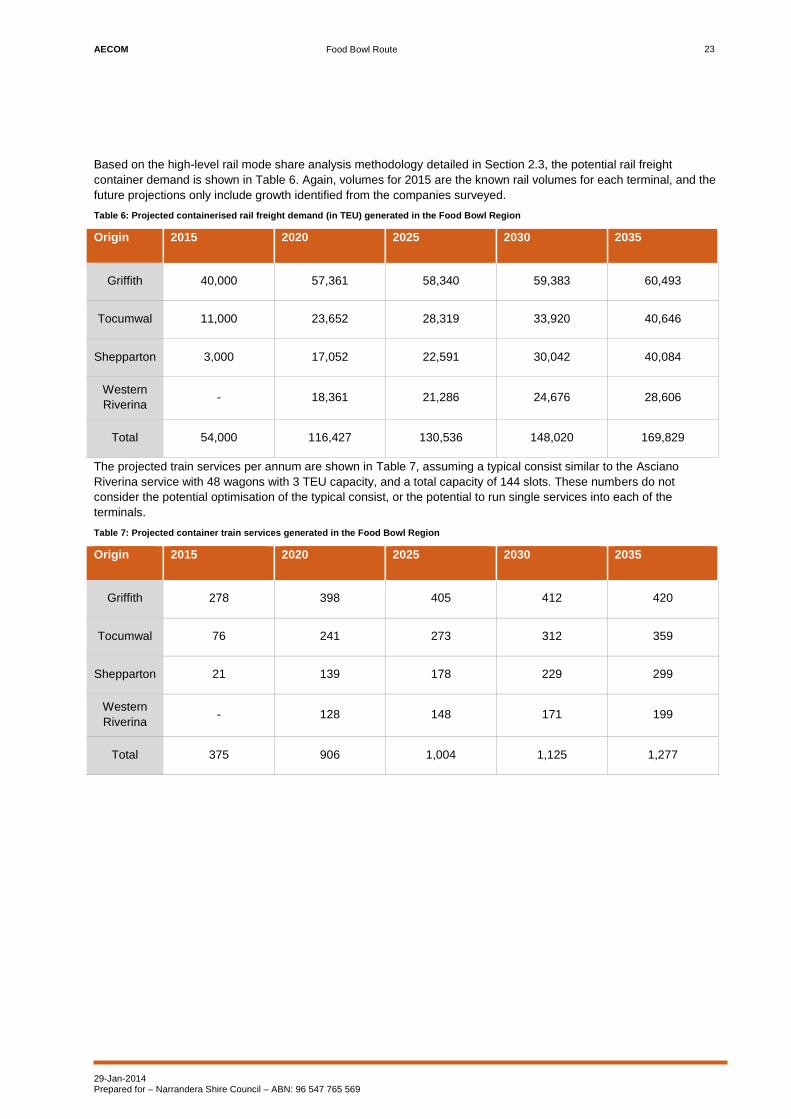

- The 2015 containerised rail freight demand in the Food Bowl Region is 54,000 TEU. The Food Bowl Route: Rail User Economics and Freight Commerce report projects this demand to more than double in the next five years to 116,427 TEU by 2020 and to more than triple to 169,829 TEU by 2035.

- In today’s global economy, international demand for fresh produce that has passed Australia’s world-leading processing standards can only increase. To meet this demand, Australian goods need unimpeded access to ports, to investment, to internal freighting and external exporting facilities and all this begins with careful consideration of this growing and economically impactful food bowl region.

3

- With appropriate planning, more detailed options analysis and shrewd foresight we can link some of our most innovative and diverse regional producers with domestic markets in our burgeoning cities, as well as the massive export market potential in Asia and beyond.

Whilst strongly supportive of the Inland Rail project, the FBIRA is adamant that the selection of the Albury–Wagga route recommended in the ARTC’s 2010 Melbourne–Brisbane Rail Alignment Study is flawed. Presently, the proposed route crosses southern NSW via Albury, Wagga Wagga, Junee and Cootamundra, and this decision was solely based on initial capital cost and the journey time between Melbourne and Brisbane. This conclusion of the 2010 study has several shortcomings that should be reconsidered, particularly in the context of selecting the Albury–Wagga Alignment over the Food Bowl Route:

- The two alternate options do not appear to have been costed on a like-for-like basis – the capital expenditure cost estimates used are too coarse for detailed options assessment and this must be remedied to fully appreciate the advantages of the FBIRA proposal.

- The study fails to adequately assess the potential demand from the Food Bowl Region, with the consequent benefits to the project gained through additional access and user revenues. In the five years since the 2010 study, the Food Bowl Region has experienced considerable growth as evidenced by the impressive private sector investment in the region.

- It is understood that the focus of the 2010 study is on Melbourne–Brisbane inter-capital freight; however, this should not preclude assessment of potential benefits for regional exporters and it should consider mutually beneficial alignment options that advantage both freight tasks. The forecast growth in the food bowl area, in both volume and diversity, merits further due diligence.

Benefits of the Food Bowl RouteThe Food Bowl Route provides significant freight efficiency for some producers when compared with the Wagga Wagga/Albury alignment. This is because receival sites located along the Food Bowl Route (for example at Wumbulgal) are closer than the intermodal freight terminals in Wagga Wagga and Albury. The reduced distance required to transport commodities to rail hubs located within close proximity to the prospective Food Bowl Inland Rail Route is an immediate saving to the producer and opens up additional export market opportunities.

Aside from the direct freight efficiency improvement, using the Food Bowl Route will also:

- provide greater opportunities for access to agricultural export markets, particularly through rail connection to the Port of Brisbane, as well as the Port of Melbourne, Port Botany and Port Kembla

- improve national freight network reliability and resilience and provide greater security of logistics chains

- generate the potential to reduce operating and maintenance costs through shorter route length and transit times, and lesser gradients and curvatures (subject to detailed investigation)

- maximise the use of existing intermodal and rail corridor infrastructure

- minimise externalities from road freight, particularly road damage costs borne by local government

- broaden the commercial agricultural opportunities between the states.

4

There have been many recent significant industry and external changes along the Food Bowl Route that will enhance industry’s ability to invest further, to attract investment, or to export. Three such examples are:

- The Connections Project which realises a $2 billion investment in the Murray Goulburn irrigation system. This project will help the area prepare for the massive demand from Asia for clean, green produce and it will attract investors who are keen to take advantage of these opportunities. This also presents an opportunity to provide for the market internally due to possible changes in food labelling legislation, driving shifts in consumer perceptions and buying habits.

- Baiada Poultry has submitted a $38 million development application to Griffith Council for a 20,000 square metre chicken hatchery capable of hatching three million chicks every week. Once completed, this will be the largest chicken processor in Australia.

- The establishment of the Agri Australis hazelnut plantation at Narrandera with over one million hazelnut trees is an example of a sub-industry which has enhanced the region’s ability to attract further investment and employment. There is also scope for growers to plant hazelnuts to complement cash crops and diversify their agribusinesses. In addition to Agri Australis’ exporting potential, this could lead to greater export opportunities for other local producers.

The Food Bowl region is home to almost 175,000 residents and produces over $10 billion of the nation’s agricultural produce:

DairyThe region produces over 20% of Australia’s dairy output, contributing approximately $4.3 billion to Australian GDP and directly employing around 10,000 people.

Broad acre cropsIn 2012-13 the region produced $3.8 billion in broad acre crops which is over 20% of Australia’s total supply.

Rice Rice production in Australia is located almost exclusively within the Food Bowl region, with 1,500 growers producing up to 1 million tonnes and generating annual revenues over $800 million.

CottonValue of exports from southern NSW reaching around $150 million in 2012-13.

LivestockProduction within the region was valued at almost $1.5 billion in 2012-13.

ChickenLargest poultry producer in Australia with plans for the largest hatchery in Australia to be built.

FruitsIn 2012-13 the region produced around 45% of Australia’s fruits.

Prunes Largest prune growing area in Australia.

5

Citrus FruitCitrus production is Australia’s largest fresh fruit export, with the Riverina producing 180,000 to 200,000 tonnes annually (70% of NSW production) worth $98 million.

WineThe region is Australia’s largest producer of wine (including 70% of NSW wine grapes) with Casella Wines responsible for 27% of Australian bottled table wine exports, including over 12.5 million cases per annum of the iconic Yellow Tail brand to 50 countries.

VegetablesVegetable production is worth over $400 million for the region.

Tree NutsThe value of almonds and walnuts grown in the region is over $1.2 billion annually and is expected to grow by over 30% to 2025 with exports accounting for 75% of production. This includes a new hazelnut plantation in Narrandera with over one million hazelnut trees.

RecommendationsARTC’s 2010 study notes appropriately that not all route combinations can be fully assessed given the sheer quantity; however the FBIRA believe that the Food Bowl Route is a viable alternative that deserves more detailed costing and value engineering.

The ARTC should conduct further due diligence including:

- detailed future demand forecasting of the food bowl area

- modelling of capital expenditure and return on investment

- investigation into Public Private Partnerships during the build stage to help facilitate the delivery of this important piece of infrastructure.

The FBIRA has already undertaken significant demand forecasting in the Food Bowl Route: Rail User Economics and Freight Commerce report and it has summarised key considerations in the Food Bowl Route: Council Challenges and Demand Information report. This most recent report addresses the major issues that the Food Bowl rail alignment would solve for the region and discusses issues which must be addressed by the Government if the Melbourne-Brisbane Inland Rail is not developed.

This project of national significance has the ability to guarantee Australian food security and also to allow greater access to lucrative export markets by attracting additional investment into the Food Bowl area. Thus, further investigation into the Food Bowl Route is essential before an informed final decision can be made on which rail route offers the greatest long-term benefit to Australia.

6

7

FOOD BOWLROUTE Council Challenges and Demand Information

3

Summary of Food Bowl Route Council Challenges and Demand Information

Further to the Food Bowl Inland Rail Alliance meeting with John Anderson (Chairperson, Inland Rail Implementation Group) it was requested that Councils along the Food Bowl Route be consulted, with the key considerations being as follows:

1. What are the major issues that the Food Bowl rail alignment would solve for our region?

2. What if the Melbourne-Brisbane Inland Rail is not developed? What are the issues that must be addressed by Government?

Responses from Shepparton City Council, Narrandera Shire Council, Griffith City Council, Berrigan Shire Council, Leeton Shire Council, Urana Shire Council and Jerilderie Shire Council have been collated.

1. What are the major issues that the Food Bowl rail alignment would solve for our region?

Australia deserves the best access to expansion and exporting. In today’s international climate, the demand for exports of fresh produce that have been exposed to Australia’s strict processing standards can only increase.

Further considerations include:

- Increased national freight network reliability, competitiveness and resilience and greater security of logistics chains.

- Benefits that creation of a true network will deliver for the freight rail industry, with gauge standardisation between all of north eastern Victoria and southern NSW and greater opportunity for private equity participation including public and private partnerships.

- Reduction in operating and maintenance costs through shorter route length and transit times, and lesser gradients and curvatures.

- Opportunities to maximise the use of existing intermodal and rail corridor infrastructure.

- The Food Bowl route will service areas that represent major irrigated food and fibre agriculture industries within eastern Australia. These industries are world leading in the production of enormous quantities of clean and green product that is valued worldwide.

- Wider externality benefits that will be derived through attracting more freight from the Food Bowl to rail, in particular reduced road damage costs which are borne by local government and the states. This will provide benefits for all interstate transport users and Councils.

- Fast, efficient, larger volume and cost effective freight movement from Food Bowl for export.

- A positive impact on the ability of business and industry in the Food Bowl Region to be globally competitive.

- The Food Bowl Route would create increased transport mode shift from road to rail. This will have a cumulative effect where the efficiencies would result in greater demand, in turn generating likely investment in intermodal terminals such as at Shepparton.

- Freight currently goes to the Port of Melbourne by road or rail and is then shipped internationally. The Food Bowl Route will mean that exports from the Berrigan area could be sent directly to the Port of Brisbane.

3

The Food Bowl Route provides significant freight efficiency for some producers when compared with the Wagga Wagga/Albury alignment. This is because receival sites (eg at Wumbulgal) located along the Food Bowl Route are closer than the intermodal freight terminals in Wagga Wagga and Albury. The reduction in distance required to transport commodities to rail hubs located within close proximity to the prospective Food Bowl Inland Rail Route is a direct saving to the producer and opens up additional export market opportunities.

An example of cost efficiency for industries in the Narrandera area utilising Wumbulgal rather than Wagga Wagga if the Food Bowl route existed is provided below:

Based on $5 per km haulage x2 (return of truck)

Narrandera to Wagga

$969 per 25 tonnes =

$38.76 per tonne

Narrandera to Wumbulgal

$688 per 25 tonnes =

$27.52 per tonne

Freight Transport Saving to producer $11.24 per tonne

6510 (TEU) x 25 tonnes = 162,750 x $11.24 saving in transport cost

Overall saving to producers annually $1,829,310

Not only is this a direct saving to the producer, it also streamlines commodity turnover enabling greater output and profitability.

Australian Grain Link have also stated that should the Food Bowl Route become operational, utilising the intermodal site at Wumbulgal would attract an additional 550,000 tonnes of grain that can be containerised and freighted to the Port of Melbourne. This could be achieved at a $10 per tonne efficiency resulting in a combined saving for the local grain industry of $5,500,000 annually. When factoring in other agricultural commodities produced in the Riverina such as cotton seed the figure would be significantly higher.

Whilst opportunity will exist for items to be freighted as far as Wagga Wagga by road and then transferred to rail for the remainder of the direct-to-port journey, this would be a secondary solution that would result in freight inefficiencies with costs borne by industry.

Industries such as Sunrice, JBS Swift (Riverina Beef) and Southern Cotton have indicated that they would prefer rail over road due to difficulty with truck companies, greater loading capacities, freight logistics and ability to access Brisbane or Sydney ports.

Additional issues that the Food Bowl rail alignment would solve for our region include:

- Assist in economic growth, allowing for industries to relocate from already overcrowded centres.

4

- Provide the impetus for further investment in the region. The options currently available for transfer of product to port are a major consideration of potential investors. Growing businesses such as the Agri Australis hazelnut plantation and Goulburn Valley Freight Logistics Centre (GV Link - land earmarked for this development located at Toolamba Road, Mooroopna) would have greater scope for freight transfer and export expansion. New export industries to China and Japan demonstrate the commitment from international investors in Leeton area exports.

- Efficient and cost effective access to ports will encourage other domestic producers to expand into the export market as well as increasing the global competitiveness of the food bowl route’s agricultural industry.

- Local economic growth through increased employment opportunities and incentive for people to move into the region.

The Hume region, as a single example, is a key generator of freight but with most freight currently transferred by road there is a significant opportunity to ensure the most productive and viable rail route is chosen through high yield cropping and irrigation country. This would increase the volume transported by rail which in turn would provide further benefits such as safety, reduced environmental impacts, lessened congestion, increased productivity and time savings.

Where freight is trucked in (for example empty wine bottles) and then trucked out again (as filled wine bottles) the producer would benefit from the opportunity to utilise rail for both options.

There have been significant industry and external changes in LGAs along the Food Bowl Route that will enhance industry’s ability to invest further, attract investment, or export. These include:

- Increase in grain production and movement through grain handling facilities.

- The Connections Project realises a $2B investment in the Murray Goulburn irrigation system. There is massive demand from Asia for clean, green, produce and investors are keen to take advantage of these opportunities.

- The possible changes to food labelling legislation ensuring imported foods list their country of origin may also positively impact local producers as the Australian reputation for quality agriculture and food production is renowned worldwide. This may further encourage consumer demand for Australian produce rather than imported (often cheaper) goods. Changing consumer perceptions and buying habits is achievable (for example, preference for free ranged eggs over caged eggs now evident across Australia).

- Baiada/ Steggles Griffith - with a $9.3m development application expansion - wanting to increase processing throughput to 2.8m chickens a week. This will be the largest chicken processor in Australia if not the Southern Hemisphere. Another major advancement includes a possible new Rail Hub and logistics park.

- The establishment of the Agri Australis hazelnut plantation at Narrandera (over 1 million hazelnut trees) is one example of a sub-industry which has enhanced the region’s ability to attract further investment and employment. There is also scope for growers to plant hazelnuts to complement cash crops and diversify their agribusinesses. In addition to Agri Australis’ exporting potential, this could lead to greater export potential for other local producers.

- A larger number of competitive grain handling firms provides grain producers with greater selling options. Increased on-farm storage allows for all year selling rather than only during and immediately after harvest.

- Massive and growing rail-contestable export demand from the Food Bowl Region, including the greater opportunity for competition between export gateways. Much of this demand is already conducive to rail and the diversity of produce will provide year-round demand.

5

2. What if the Melbourne-Brisbane Inland Rail is not developed? What are the issues that must be addressed by Government?

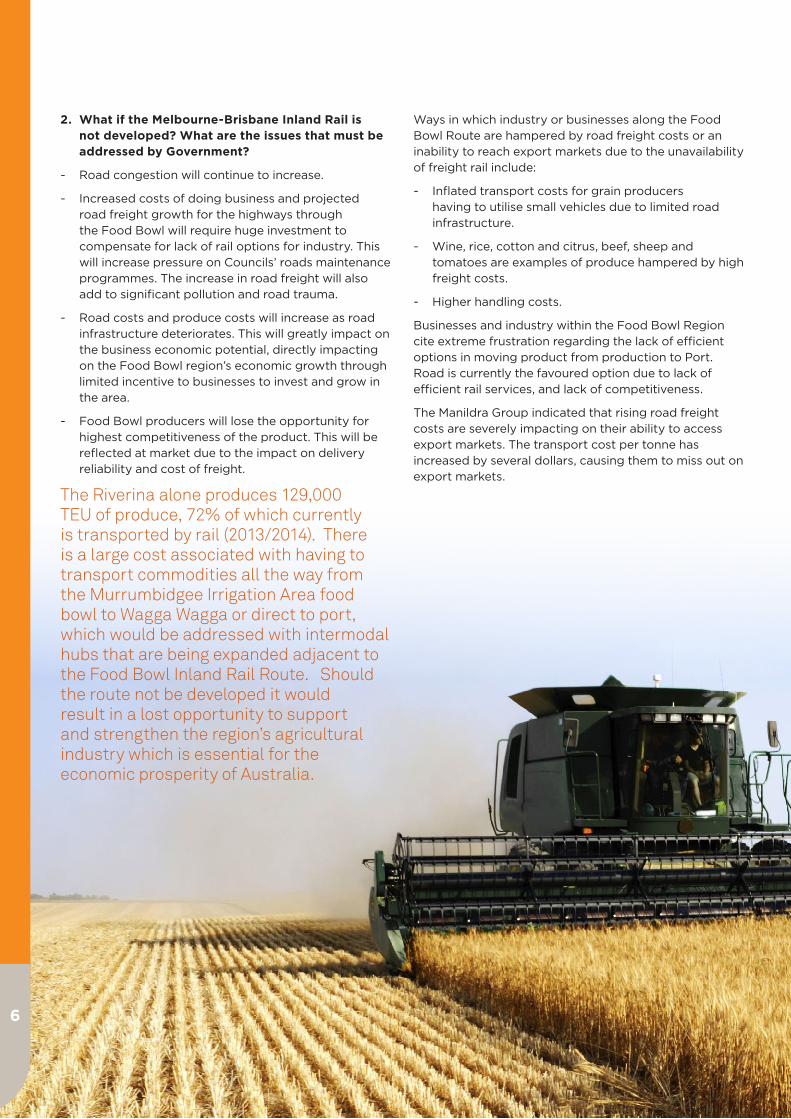

- Road congestion will continue to increase.

- Increased costs of doing business and projected road freight growth for the highways through the Food Bowl will require huge investment to compensate for lack of rail options for industry. This will increase pressure on Councils’ roads maintenance programmes. The increase in road freight will also add to significant pollution and road trauma.

- Road costs and produce costs will increase as road infrastructure deteriorates. This will greatly impact on the business economic potential, directly impacting on the Food Bowl region’s economic growth through limited incentive to businesses to invest and grow in the area.

- Food Bowl producers will lose the opportunity for highest competitiveness of the product. This will be reflected at market due to the impact on delivery reliability and cost of freight.

The Riverina alone produces 129,000 TEU of produce, 72% of which currently is transported by rail (2013/2014). There is a large cost associated with having to transport commodities all the way from the Murrumbidgee Irrigation Area food bowl to Wagga Wagga or direct to port, which would be addressed with intermodal hubs that are being expanded adjacent to the Food Bowl Inland Rail Route. Should the route not be developed it would result in a lost opportunity to support and strengthen the region’s agricultural industry which is essential for the economic prosperity of Australia.

Ways in which industry or businesses along the Food Bowl Route are hampered by road freight costs or an inability to reach export markets due to the unavailability of freight rail include:

- Inflated transport costs for grain producers having to utilise small vehicles due to limited road infrastructure.

- Wine, rice, cotton and citrus, beef, sheep and tomatoes are examples of produce hampered by high freight costs.

- Higher handling costs.

Businesses and industry within the Food Bowl Region cite extreme frustration regarding the lack of efficient options in moving product from production to Port. Road is currently the favoured option due to lack of efficient rail services, and lack of competitiveness.

The Manildra Group indicated that rising road freight costs are severely impacting on their ability to access export markets. The transport cost per tonne has increased by several dollars, causing them to miss out on export markets.

6

Furthermore in the absence of inland rail:

- Government subsidies could be provided to producers to support ‘local growers’ and generate profitability and expansion in both the domestic and export markets.

- Government could provide Councils, who are already investing heavily to attract investors, with assistance packages or grants to facilitate infrastructure upgrades. For example supply of power needed for the continued expansion of Baiada/Steggles in Griffith.

- Sealing of key roads would assist the establishment of Rail Hubs that would enable growth.

- Prioritisation of the duplication of the Goulburn Valley Highway is needed from Shepparton to the NSW/Victorian border.

- An upgrade is required at the rail to Port of Melbourne interchange. There is congestion on the railway interchange which has a significant impact on the efficiency of the operations throughout the supply chain.

- The Government policy of looking to shift transport from road to rail to realise productivity efficiencies, improve safety, and reduce environmental impacts and to allow producers to be globally competitive simply would not be met.

ConclusionDomestic freight is forecast to nearly double by 2030 and triple by 2050. If there is no incentive to shift freight from road to rail then long distance truck movements are anticipated to increase on the Newell Highway by 300 per cent by 2050. Australia has an enormous opportunity currently to dramatically increase exports globally. This cannot be realised effectively without an efficient, reliable and cost effective rail network.

There is a global shift towards ‘clean and green’ produce particularly in the lucrative China export market. This has become even more important with the recent Free Trade Agreement with China.

To create an inland rail which does not directly cross the heart of the Nation’s food bowls and primary producers fails to capitalise on the opportunities inherent within them.

The FBIRA reiterates the need for further due diligence (future demand, capital expenditure, return on investment and investigation of public and private partnerships) on the Southern Alignment of the Melbourne to Brisbane Inland Rail Project.

7

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

Quality Information

Document Food Bowl Route

Date 29-Jan-2014

Prepared by Eloise Modun and Oliver Baxter

Reviewed by Austin Kennedy

Revision History

Revision A B

Date 28-Jan-2014 29-Jan-2014

Authorised by

Austin Kennedy

Associate Director

Austin Kennedy

Associate Director

Food Bowl Route Rail User Economics and Freight Commerce

Client: Narrandera Shire Council

ABN: 96 547 765 569

Prepared by

AECOM Australia Pty Ltd

Level 9, 8 Exhibition Street, Melbourne VIC 3000, Australia

T +61 3 9653 1234 F +61 3 9654 7117 www.aecom.com

ABN 20 093 846 925

29-Jan-2014

AECOM in Australia and New Zealand is certified to the latest version of ISO9001, ISO14001, AS/NZS4801 and OHSAS18001.

© AECOM Australia Pty Ltd (AECOM). All rights reserved.

AECOM has prepared this document for the sole use of the Client and for a specific purpose, each as expressly stated in the document. No other

party should rely on this document without the prior written consent of AECOM. AECOM undertakes no duty, nor accepts any responsibility, to any

third party who may rely upon or use this document. This document has been prepared based on the Client’s description of its requirements and

AECOM’s experience, having regard to assumptions that AECOM can reasonably be expected to make in accordance with sound professional

principles. AECOM may also have relied upon information provided by the Client and other third parties to prepare this document, some of which

may not have been verified. Subject to the above conditions, this document may be transmitted, reproduced or disseminated only in its entirety.

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

Table of Contents Executive Summary i 1.0 Introduction 1

1.1 The Food Bowl Inland Rail Alliance 1 1.2 Purpose 1

2.0 Approach 3 2.1 Industry survey 3

2.1.1 Identification of freight generators 3 2.1.2 Industry engagement 3

2.2 Gross demand 3 2.3 Mode-share 3 2.4 Growth forecasting 4 2.5 Selected organisations surveyed 4 2.6 Assumptions and limitations 4

3.0 Geographic context 5 3.1 Geography 5 3.2 Population and regional centres 6 3.3 Existing transport networks 7

3.3.1 Road 8 3.3.2 Rail 8 3.3.3 Intermodal terminals 8 3.3.4 Grain receival and storage 8 3.3.5 Irrigation networks 8

4.0 Economic context 10 4.1.1 Employment 10 4.1.2 Revenue 10 4.1.3 Investment 10

5.0 Commodities 11 5.1 Grain 11

5.1.1 Wheat 11 5.1.2 Rice 14 5.1.3 Oilseeds 14

5.2 Dairy 15 5.3 Cotton 16 5.4 Horticulture 17

5.4.1 Fruit 17 5.4.2 Citrus 17 5.4.3 Tree nuts 17 5.4.4 Vegetables 17

5.5 Wine and beverages 18 5.6 Meat and livestock 19 5.7 Fibre and packaging 20 5.8 Other 20

6.0 Aggregate demand 21 6.1 Containerised freight demand 22 6.2 Bulk freight demand 24

7.0 Next Steps 25

Appendix A Engagement Pack A

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

i

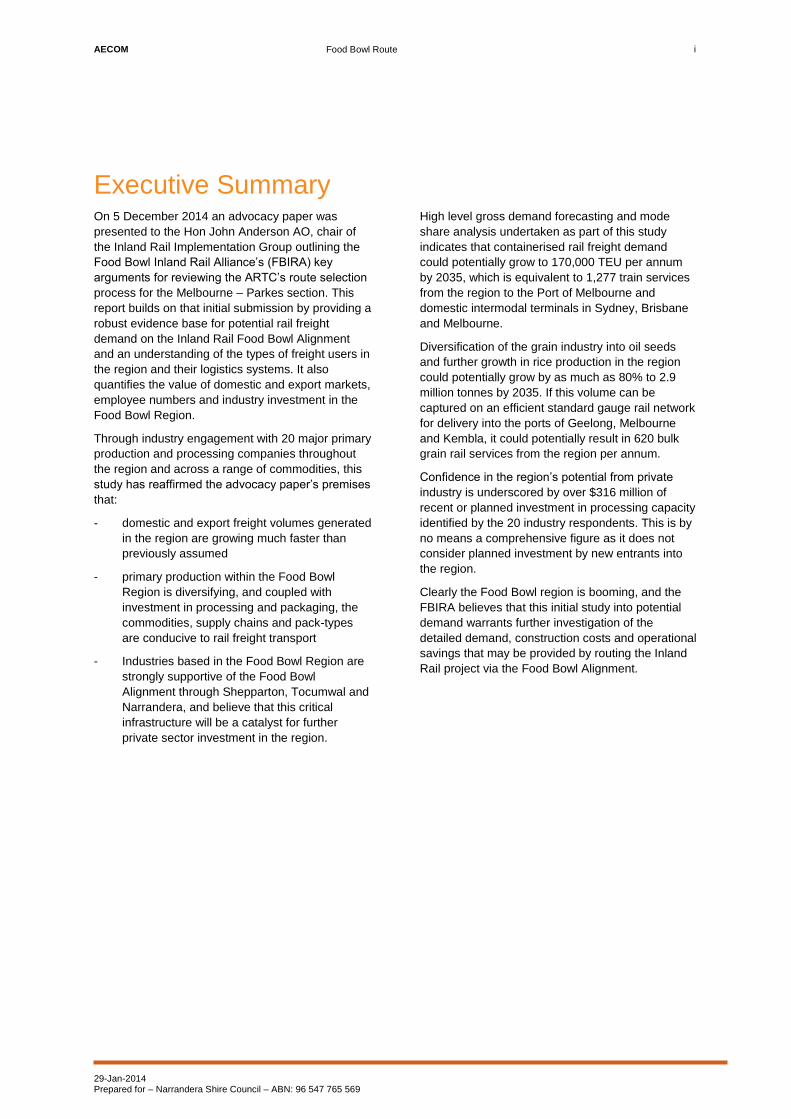

Executive Summary On 5 December 2014 an advocacy paper was

presented to the Hon John Anderson AO, chair of

the Inland Rail Implementation Group outlining the

Food Bowl Inland Rail Alliance’s (FBIRA) key

arguments for reviewing the ARTC’s route selection

process for the Melbourne – Parkes section. This

report builds on that initial submission by providing a

robust evidence base for potential rail freight

demand on the Inland Rail Food Bowl Alignment

and an understanding of the types of freight users in

the region and their logistics systems. It also

quantifies the value of domestic and export markets,

employee numbers and industry investment in the

Food Bowl Region.

Through industry engagement with 20 major primary

production and processing companies throughout

the region and across a range of commodities, this

study has reaffirmed the advocacy paper’s premises

that:

- domestic and export freight volumes generated

in the region are growing much faster than

previously assumed

- primary production within the Food Bowl

Region is diversifying, and coupled with

investment in processing and packaging, the

commodities, supply chains and pack-types

are conducive to rail freight transport

- Industries based in the Food Bowl Region are

strongly supportive of the Food Bowl

Alignment through Shepparton, Tocumwal and

Narrandera, and believe that this critical

infrastructure will be a catalyst for further

private sector investment in the region.

High level gross demand forecasting and mode

share analysis undertaken as part of this study

indicates that containerised rail freight demand

could potentially grow to 170,000 TEU per annum

by 2035, which is equivalent to 1,277 train services

from the region to the Port of Melbourne and

domestic intermodal terminals in Sydney, Brisbane

and Melbourne.

Diversification of the grain industry into oil seeds

and further growth in rice production in the region

could potentially grow by as much as 80% to 2.9

million tonnes by 2035. If this volume can be

captured on an efficient standard gauge rail network

for delivery into the ports of Geelong, Melbourne

and Kembla, it could potentially result in 620 bulk

grain rail services from the region per annum.

Confidence in the region’s potential from private

industry is underscored by over $316 million of

recent or planned investment in processing capacity

identified by the 20 industry respondents. This is by

no means a comprehensive figure as it does not

consider planned investment by new entrants into

the region.

Clearly the Food Bowl region is booming, and the

FBIRA believes that this initial study into potential

demand warrants further investigation of the

detailed demand, construction costs and operational

savings that may be provided by routing the Inland

Rail project via the Food Bowl Alignment.

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

1

1.0 Introduction

1.1 The Food Bowl Inland Rail

Alliance

The FBIRA represents the local governments of

Mitchell, Greater Shepparton, and Moira in Victoria

and Berrigan, Jerilderie, Urana, Griffith, Leeton and

Narrandera in NSW. The Alliance has been formed

with the aim of ensuring the Australian Government

gives further consideration to routing the Melbourne to

Brisbane Inland Rail via the Food Bowl Alignment

project through Shepparton, Tocumwal and

Narrandera given the extraordinary export growths

being experienced in Australia’s most economically

diverse and prosperous primary production and food

processing region. The FBIRA is strongly supported

by the extensive network of producers, value adding

processors and suppliers within the region.

1.2 Purpose

The ARTC’s 2010 Melbourne-Brisbane Inland Rail

Alignment Study recommended an alignment through

southern NSW via Albury, Wagga Wagga, Junee and

Cootamundra. Whilst strongly supportive of the Inland

Rail project, the FBIRA is adamant that the 2010

study has several shortcomings that should be

reconsidered particularly in relation to the selection of

the Albury-Wagga alignment over the Food Bowl

Alignment. These shortcomings include:

- The two alternate options do not appear to have

been costed on a like-for-like basis – the capex

cost estimates used are too coarse for detailed

options assessment. The 2010 study notes

appropriately that not all route combinations can

be fully assessed given the sheer number,

however the Food Bowl Alignment is a viable

alternative that merits more detailed costing and

value engineering.

- Despite the Terms of Reference for the study

requiring a determination of above rail

operational benefits, this does not appear to

have been adequately factored into the

evaluation criteria for the options assessment. In

particular it did not consider broader strategic

network benefits including network redundancy

and reliability improvements as well as the

operational benefits that gauge standardisation

will provide.

- The study did not adequately assess the

potential demand from the Food Bowl Region,

with the subsequent benefits to the project

through additional access and user revenues.

Understandably that the ARTC’s focus for the

project is on Melbourne – Brisbane inter-capital

freight; however this should not preclude

assessment of potential benefits for regional

exporters and considering mutually beneficial

alignment options that advantage both freight

tasks. In the five years since the 2010 study, the

Food Bowl Region has experienced

considerable growth as evidenced by the private

sector investment in the region. This growth, in

both volume and diversity merits further detailed

demand analysis.

This report provides an evidence base for the

FBIRA’s assertion regarding the third point – it

provides a bottom-up analysis of the potential

demand that could contribute to Inland Rail’s viability

through diversifying the infrastructure’s user base.

Through industry stakeholder engagement an

understanding of the sensitivities to time, reliability

and cost, and potential barriers to rail freight within

the region has been documented, along with the

unique opportunities that the Food Bowl alignment

presents.

Agricultural diversification, deregulation, irrigation

reforms and recent free trade agreements with China

and other south-east Asian trading partners will

continue to drive this growth in the Food Bowl region’s

agricultural output. The geographic relationship of the

region to our export gateways coupled with the

enormous private sector investment in value adding

industries in the regional centres of Seymour,

Shepparton, Griffith, Tocumwal, Leeton and

Narrandera means that much of this export growth is

ideally suited to intermodal rail transport.

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

2

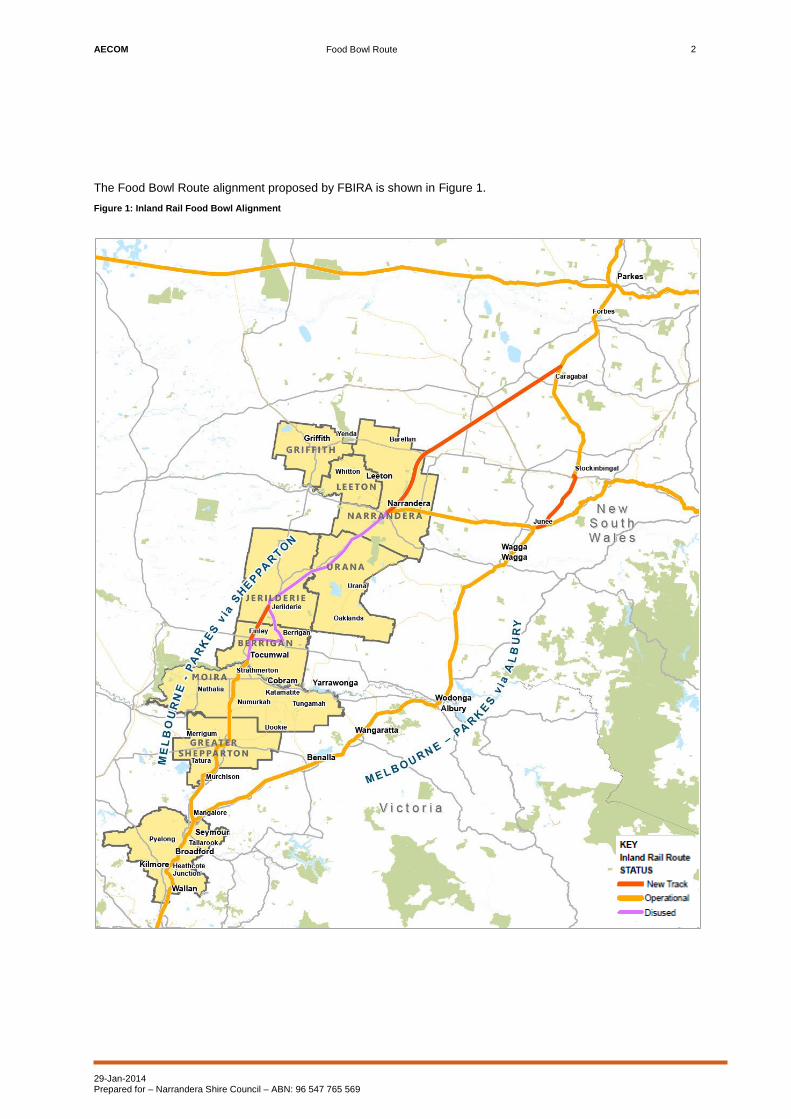

The Food Bowl Route alignment proposed by FBIRA is shown in Figure 1.

Figure 1: Inland Rail Food Bowl Alignment

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

3

2.0 Approach

This section details the approach to industry

stakeholder engagement, supply chain analysis and

agricultural production forecasting undertaken for this

study.

2.1 Industry survey

2.1.1 Identification of freight generators

In collaboration with FBIRA member Councils, and

building on the companies identified in the previous

stage of this work, a list of target industries was

compiled. Priority was given to companies that are

known to produce large volumes of freight and their

remoteness from Melbourne, Sydney and Brisbane.

Potential users were also considered from surrounding

municipalities that could benefit from the Food Bowl

Route.

Organisations targeted are major producers and value

adding industries including:

- Grain handlers, marketers and millers

- Dairy processors and exporters

- Wineries

- Horticultural processors (fruits, vegetables and

tree nuts)

- Meat processors and feedlots

- Other allied industries including packaging and

transport operators

Where possible, persons responsible for freight and

logistics at each company were identified and

approached, primarily via telephone. An “Industry

Engagement Pack” was then emailed and telephone

interview scheduled. During these interviews,

stakeholders were taken through the questionnaire

with the aim of collecting qualitative information that

may provide evidence for the Food Bowl Route

demand.

Information requested from each stakeholder was

based around the following themes:

- Information about the organisation’s background

and market position

- Current and future production capacity

- Details of the existing supply chain

- Any recent or planned industry investment

- Organisational perceptions of rail for freight

transport.

2.1.2 Industry engagement

An industry engagement pack was provided to each

company that agreed to take part in the study. An

example engagement pack is provided in Appendix A

which includes:

1) A cover letter introducing the FBIRA and the

Inland Rail project, and detailing the purpose of

the engagement

2) A short questionnaire detailing the types of

information sought for the project

A copy of the advocacy paper presented to the Inland

Rail Implementation Group was also provided.

2.2 Gross demand

Given the discrete nature of individual logistics chains

through the region, and the relative sizes of the larger

producers, gross demand was derived using a bottom-

up industry engagement approach via the extensive

stakeholder engagement process detailed in Section

2.1. Freight demand/generation was estimated for

individual organisations and summed to determine

total demand for the region. This approach uses the

fine details to build the “big picture”.

2.3 Mode-share

Organisations choose combinations of rail, sea, air and

road to transport freight. Each mode has attributes that

make them more suitable, and generally less

expensive, for particular freight movements. Choice is

strongly influenced by the nature of the goods

requiring transport, taking into account characteristics

such as density, mass, perishability, type and

durability. Road and rail play an important part in

transporting domestic freight, in some cases

competing for freight and in other cases working

together.

Mode-share was qualitatively assessed by assigning

High, Medium or Low ratings to account for:

- existing transport modes used

- distance to end-markets and suitability of existing

supply chains

- distance to an existing or potential intermodal

terminal within the Food Bowl Region

- sensitivity of the freight to time, cost and reliability

- annual volumes.

Logit modelling techniques were not deemed

appropriate given the short time frame for data

collection, collation and reporting, and the absence of

an appropriate generalised transport cost model.

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

4

Logit modelling techniques were not deemed

appropriate given the short time frame for data

collection, collation and reporting, and the absence of

an appropriate generalised transport cost model.

2.4 Growth forecasting

A set of standardised spreadsheets were developed to

collate the information gathered in the industry

engagement phase. Following each engagement, the

table was populated with each stakeholder’s

responses.

Gross forecasts were developed for each industry

participant accounting for changing land-uses,

investment and domestic and overseas demand.

Combining the growth forecasts with the potential rail

mode-shares, gross rail tonnages were developed.

These were then converted into container volumes and

ultimately into train loads.

2.5 Selected organisations

surveyed

A total of 35 different organisations from a wide range

of industries were contacted during the industry

engagement. Of these, representatives from 20

organisations were interviewed and Table 1 below

shows these companies grouped by commodity type.

To protect their confidentiality and commercial

information, the identities of the surveyed companies

have not been disclosed in this report.

2.6 Assumptions and limitations

The following conservative assumptions have been

adopted in the development of the demand forecasts:

- In order to aggregate the volume of freight in the

region, units of measurement (containers, pallets,

cases etc…) provided by each organisation have

been converted into equivalent containers and/or

tonnages, which in turn has been converted into

train numbers.

- No estimates of Capex and Opex of the FBR

have been made, or the impact of these costs on

user charges and ultimately freight costs.

- No estimate of the benefits of the operational

efficiencies for standard gauge conversion of the

Goulburn Valley Line has been made.

- A five year investment horizon for freight users is

assumed for any interventions affecting mode

shares. For example, a rail investment that is

projected to increase rail mode share by 5%

would have that mode share realised gradually

over a five year period.

- Detailed mode-share modelling incorporating

calibrated logit modelling of time, cost, reliability,

freight availability and customer preferences has

not been undertaken. High, Medium and Low

projections have been adopted based on

distance to end-market, distance to potential

intermodal terminal, time sensitivity of the freight

and annual volumes.

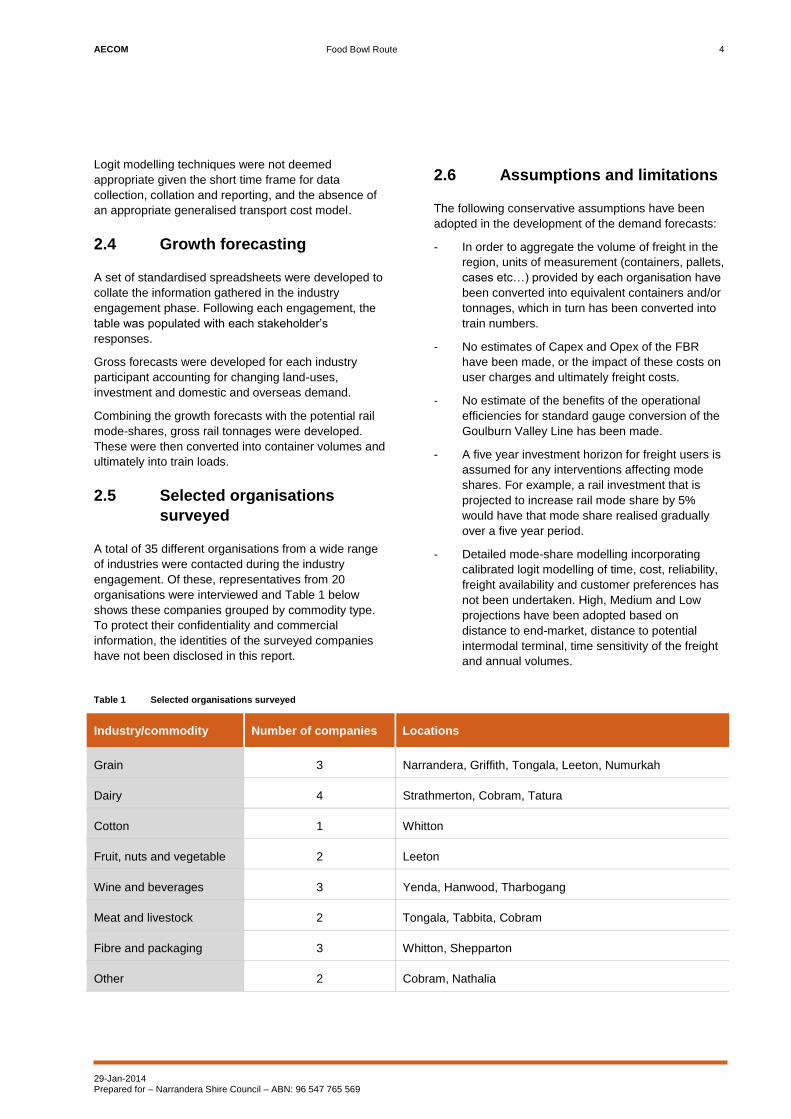

Table 1 Selected organisations surveyed

Industry/commodity Number of companies Locations

Grain 3 Narrandera, Griffith, Tongala, Leeton, Numurkah

Dairy 4 Strathmerton, Cobram, Tatura

Cotton 1 Whitton

Fruit, nuts and vegetable 2 Leeton

Wine and beverages 3 Yenda, Hanwood, Tharbogang

Meat and livestock 2 Tongala, Tabbita, Cobram

Fibre and packaging 3 Whitton, Shepparton

Other 2 Cobram, Nathalia

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

5

3.0 Geographic context

3.1 Geography

The Food Bowl region stretches from central Victoria

to southern NSW – see Figure 2, it covers an area of

approximately 25,100 square kilometres and supports

a population of around 180,000 people.

Mitchell Shire forms the southern-most boundary of

the FBIRA, just 30 kilometres north of Melbourne, and

the northern-most boundary is 520 kilometres west of

Sydney in Narrandera Shire. The area therefore

strategically offers urban, peri-urban and rural

landscapes and is situated along one of Australia’s

most significant transport corridors linking the capital

cities of the eastern seaboard.

The varied geographic and climatic conditions provide

diverse growing conditions for a vast array of

agricultural commodities being produced and

processed for consumption in both domestic and

international markets. Throughout the Food Bowl

region, the climate varies from semi-arid in the north

to temperate in the south. This results in fairly sparse

rainfall with hot summers and cold winters. The Great

Dividing Range which runs from the north of

Queensland, along the New South Wales coast and

into Victoria, produces a cooler, mountain climate on

the inland side of the mountains.

To mitigate the dry summer conditions, extensive

irrigation infrastructure across the region fed by the

Murray, Murrumbidgee and Goulburn Rivers ensure

both high agricultural yields and security of production

during periods of drought.

Figure 2: Terrain and major features of the Food Bowl Alignment

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

6

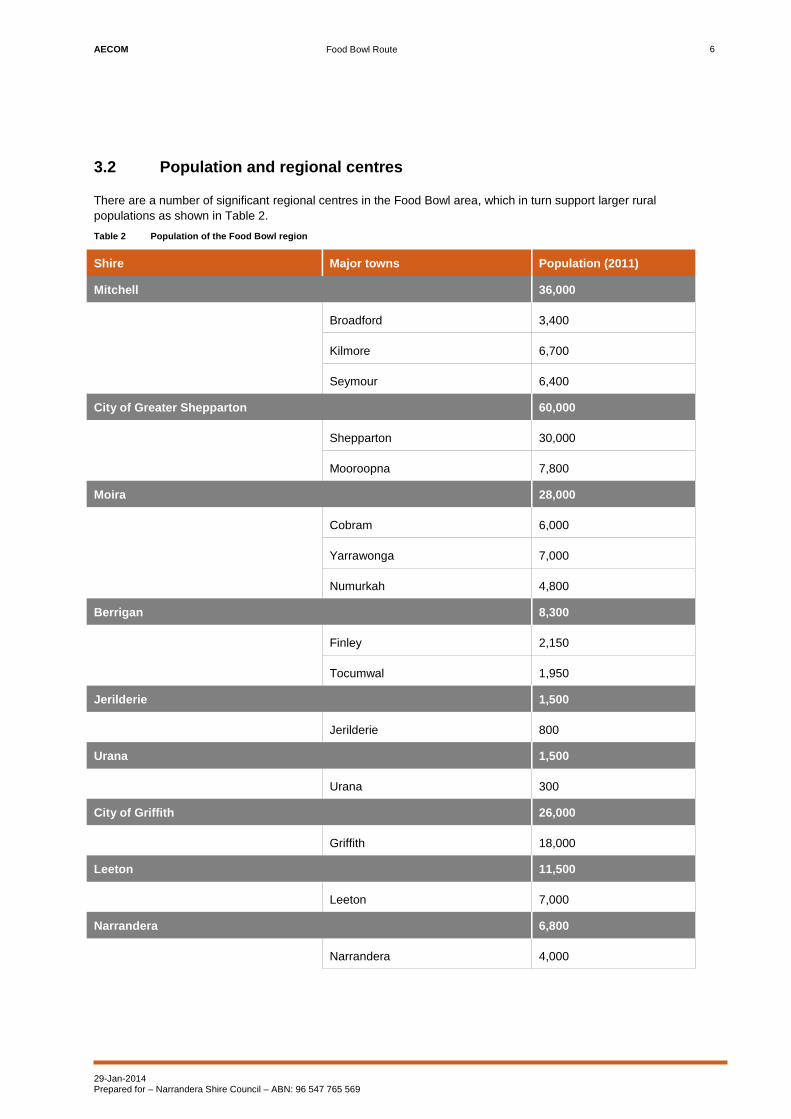

3.2 Population and regional centres

There are a number of significant regional centres in the Food Bowl area, which in turn support larger rural

populations as shown in Table 2.

Table 2 Population of the Food Bowl region

Shire Major towns Population (2011)

Mitchell 36,000

Broadford 3,400

Kilmore 6,700

Seymour 6,400

City of Greater Shepparton 60,000

Shepparton 30,000

Mooroopna 7,800

Moira 28,000

Cobram 6,000

Yarrawonga 7,000

Numurkah 4,800

Berrigan 8,300

Finley 2,150

Tocumwal 1,950

Jerilderie 1,500

Jerilderie 800

Urana 1,500

Urana 300

City of Griffith 26,000

Griffith 18,000

Leeton 11,500

Leeton 7,000

Narrandera 6,800

Narrandera 4,000

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

7

The regional City of Greater Shepparton in

northern Victoria began as a sheep station and river

crossing before transforming into a railway town.

Today the major fruit, vegetable and dairy

processing centre supports a population of over

60,000 and is forecast to grow to over 80,000 by

2031. Shepparton is also the centre of the Goulburn

Valley irrigation system, one of the largest in

Australia. Mooroopna, on the other side of the

Goulburn River, will have a critical place in the

proposed freight and logistics centre planned just

south of the town. This will consist of a terminal for

the transfer of freight between truck and rail, and

general freight area to provide direct rail access for

the Goulburn Valley to the Port of Melbourne.

Cobram, along with the nearby towns of Numurka

and Yarrawonga in the Shire of Moira in northern

Victoria is surrounded by orchards, dairy farms and

wineries. It is the birthplace of the Murray Goulburn

Co-operative which collects 35% of Australia’s milk

production.

Tocumwal, on the banks of the Murray River in

southern New South Wales, is surrounded by rich

farmland and State forest. While traditionally growth

in the region has been derived from primary

production there is now a strong a trend towards the

establishment of small and medium sized

manufacturing and processing facilities.

With a population of nearly 4,000, Narrandera is

situated at the junction of the Newell and Sturt

highways, adjacent to the Murrumbidgee River. The

town is surrounded to the east by extensive cereal

crops, sheep and wool production and to the west

rice, cereals, citrus, wine grapes and potatoes in the

Murrumbidgee Irrigation Area.

Leeton is a purpose-built town designed after the

New South Wales Government announced irrigation

schemes in the early 20th

century. With a population

of nearly 7,000, it is situated in an extremely

productive region with citrus, rice, grapes and wheat

grown in the area. It is also home to the SunRice

(Ricegrowers Limited) headquarters – one of the

largest employers in regional NSW.

Like Leeton, Griffith was also designed by Walter

Burley Griffin as a service town for the extensive

irrigation scheme that supports wine, citrus, rice and

poultry production in the area. The township’s

population of over 17,000 supports a much larger

hinterland of 26,000 with more than 60% of the

population having an Italian heritage.

3.3 Existing transport networks

Freight and logistics are a crucial part of the

economic health of the Food Bowl region and the

existing transport networks are described in the

following sections.

Forecasted freight growth will add significant

pressure to both road and rail networks in the area,

thus an integrated solution is required to avoid the

current network forming a barrier to growth.

Although the Port of Melbourne is closer than Port

Botany for container exports and Kembla for bulk

grain, producers in the region view improved port

access opportunities as a key benefit of the Food

Bowl Alignment resulting in greater competition

between the ports. Figure 3 below shows the major

road and rail networks through the region

Figure 3: Road and rail networks

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

8

3.3.1 Road

The Newell Highway runs the length of New South

Wales, parallel to the eastern coast and

approximately 400 kilometres inland. It is the main

inland direct road link from Melbourne to Brisbane,

bypassing the congested coastal areas near

Sydney.

The Newell Highway crosses the Murray River at

Tocumwal and continues south through Victoria as

the Goulburn Valley Highway which roughly follows

the course of the Goulburn River. Of the section

running through the Food Bowl region, about half of

the Goulburn Valley Highway is a two lane single

carriageway and half is a dual carriageway known

as the Goulburn Valley Freeway.

Just north of Seymour, the Goulburn Valley

Freeway has an interchange with the dual

carriageway Hume Freeway to connect to

Melbourne.

The large freight volumes and inadequate rail

alternatives results in very significant long distance

traffic volumes destined for major cities and ports.

3.3.2 Rail

Legacy breaks in rail gauges and the problems they

create for rail transport in Australia have been well

documented. These inefficiencies, coupled with

branch line closures during the latter half of last

century have resulted in growing road mode-shares.

At a national level, different rail gauges result in

fragmented operations due to the inability to quickly

and efficiently move rolling stock between networks,

resulting in higher operating costs due to sub-

optimal utilisation and minimal investment in fixed

infrastructure.

As with much of the state, freight rail in north-east

Victoria is divided into the interstate and intrastate

networks. The ARTC manage the standard gauge

interstate network from Melbourne to

Albury/Wodonga, as well as the recently gauge

converted Benalla – Oaklands branch used for bulk

grain transport. VicTrack manages the broad gauge

intrastate network running from Melbourne to

Mangalore with branches radiating from Shepparton

to Tocumwal, Dookie and Echuca. The Melbourne

to Tocumwal line is used to transport bulk grains

and other containerised freight with limited

passenger service, whilst the Dookie branch is

exclusively used for grain.

In southern New South Wales within the Food Bowl

region, there is a standard gauge line running from

Junee to Griffith via Narrandera. A branch line

operated from Narrandera to the break of gauge at

Tocumwal up until 1985.

3.3.3 Intermodal terminals

There are existing intermodal terminals located at

Griffith, Tocumwal and Shepparton, with a proposed

facility at Mooroopna and another terminal in the

western Riverina being investigated, potentially in

Leeton.

The Tocumwal Container Intermodal terminal,

operated by Pacific National, provides direct access

to the Port of Melbourne and up to three trains per

day for bulk containerised grain and refrigerated

dairy products. The Qube Riverina service from

Griffith via Wagga Wagga has recently switched

from the Port of Melbourne to Port Botany.

Despite the inadequate rail infrastructure currently

available to the region, the Food Bowl already

generates nearly 70,000 containers of intermodal

freight destined for the Port of Melbourne. This

consists of:

- 15,000 containers per year of rice with

services 6 days per week from Deniliquin

- 10,000 containers per year of hay, grain, rice,

cottonseed and dairy running 3 days per week

from Tocumwal

- 3,000 containers per year of cottonseed

attached to the Tocumwal train at Mooroopna

- 40,000 containers per year of grain, rice, wine

and grapes running 5 days per week from

Griffith and Leeton.

3.3.4 Grain receival and storage

The production and storage of grain is a major

industry in the Food Bowl Region with 25 grain

receival and storage sites. Major sites include

Murchison East, Dookie, Tocumwal, St James,

Warragoon, Benerembah, Carrathool and

Wumbulgal. A number of these facilities are situated

along the broad and standard gauge rail networks

described in Section 3.3.2.

3.3.5 Irrigation networks

Despite the link between water supply and yield,

producers in the Food Bowl region continue to

deliver higher yield rates whilst investing in water

efficient infrastructure and farming systems. Rice

growers in the Food Bowl region, for example,

delivered record breaking yields in 2010 with an

average of 11 tonnes per hectare.

The Food Bowl region relies heavily on a network of

irrigation schemes, including the 1 million hectare

Goulburn Murray Irrigation District (GMID). The

GMID comprises the Goulburn System, supplied

from Lake Eildon, and the Murray system, supplied

by weirs on the Murray River. It accounts for almost

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

9

90 percent of water used in irrigation and over 70

percent of water stored in Victoria.

In 2007, the Victorian Government commenced the

$2 billion Food Bowl Modernisation Project (also

known as the Northern Victorian Irrigation Renewal

Project, NVIRP) within the GMID. Stage one of the

project involved modernising the larger channels

and providing new connections to GMID customers,

whilst stage two involved installing new irrigation

metering. In 2012 the NVIRP was merged with

Goulburn-Murray Water and is due for completion in

2018. Now renamed the Connections Project, it will

redevelop the Goulburn Murray irrigation system

into a world’s best practice system, shortening order

times and providing more reliable delivery of water

to irrigators.

In southern NSW, the Murrumbidgee Irrigation

serves over 3,200 landholdings across 660,000

hectares. $149.6 million of funding has been

provided to Murrumbidgee Irrigation by the

Australian Government in 2015 for farm upgrades in

exchange for water rights.

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

10

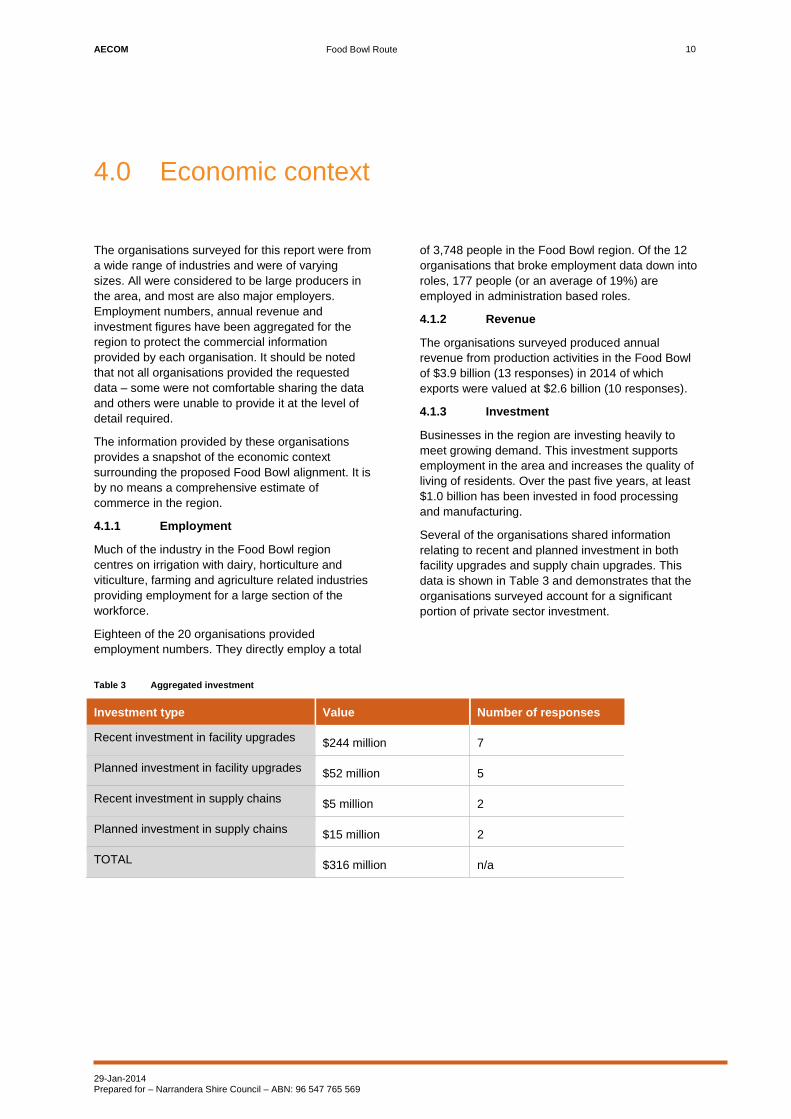

4.0 Economic context

The organisations surveyed for this report were from

a wide range of industries and were of varying

sizes. All were considered to be large producers in

the area, and most are also major employers.

Employment numbers, annual revenue and

investment figures have been aggregated for the

region to protect the commercial information

provided by each organisation. It should be noted

that not all organisations provided the requested

data – some were not comfortable sharing the data

and others were unable to provide it at the level of

detail required.

The information provided by these organisations

provides a snapshot of the economic context

surrounding the proposed Food Bowl alignment. It is

by no means a comprehensive estimate of

commerce in the region.

4.1.1 Employment

Much of the industry in the Food Bowl region

centres on irrigation with dairy, horticulture and

viticulture, farming and agriculture related industries

providing employment for a large section of the

workforce.

Eighteen of the 20 organisations provided

employment numbers. They directly employ a total

of 3,748 people in the Food Bowl region. Of the 12

organisations that broke employment data down into

roles, 177 people (or an average of 19%) are

employed in administration based roles.

4.1.2 Revenue

The organisations surveyed produced annual

revenue from production activities in the Food Bowl

of $3.9 billion (13 responses) in 2014 of which

exports were valued at $2.6 billion (10 responses).

4.1.3 Investment

Businesses in the region are investing heavily to

meet growing demand. This investment supports

employment in the area and increases the quality of

living of residents. Over the past five years, at least

$1.0 billion has been invested in food processing

and manufacturing.

Several of the organisations shared information

relating to recent and planned investment in both

facility upgrades and supply chain upgrades. This

data is shown in Table 3 and demonstrates that the

organisations surveyed account for a significant

portion of private sector investment.

Table 3 Aggregated investment

Investment type Value Number of responses

Recent investment in facility upgrades $244 million 7

Planned investment in facility upgrades $52 million 5

Recent investment in supply chains $5 million 2

Planned investment in supply chains $15 million 2

TOTAL $316 million n/a

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

11

5.0 Commodities

This section provides information about each of the industries examined including a description of the market, product destinations and supply chains. Many of the industries in the Food Bowl region are interlinked and this provides opportunities for economies of scale for transport and storage.

5.1 Grain

5.1.1 Wheat

The grain industry in Australia was once highly

regulated with a largely homogenous product

offering and monopoly control of handling and

export marketing, but since the 1980s deregulation

has led to a much more competitive industry with

products being differentiated on price and service

and a number of new, handlers, marketers and

exporters have emerged. This has resulted in more

specialised product that is increasingly attractive to

the global markets In 2012-13 the region produced

$3.8 billion in broad acre crops – over 20% of

Australia’s total supply.

Wheat for domestic consumption and feedstock is

generally grown on the east coast of Australia

where grain farms are primarily family run

enterprises with a large number of small farms and

a small number of large farms. Grain is sourced

from farms on the New South Wales western slopes

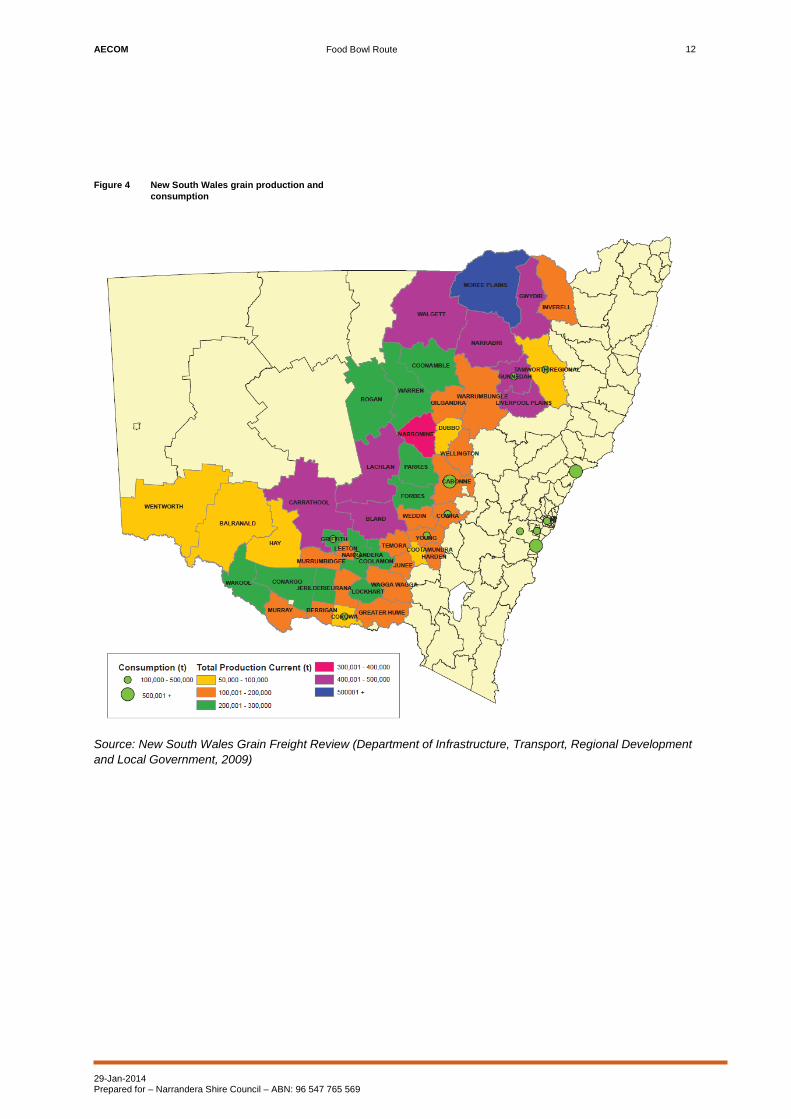

and plains, as shown in Figure 4, as well as

northern Victoria from Tocumwal through to the

South Australian border. Production occurs over the

year; however harvest is typically from November to

January. Farmers strive to continuously improve

yield expand global market share.

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

12

Figure 4 New South Wales grain production and

consumption

Source: New South Wales Grain Freight Review (Department of Infrastructure, Transport, Regional Development

and Local Government, 2009)

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

13

There is significant storage and processing

infrastructure located across the Food Bowl region

with all major grain, handers and marketers having

a presence. The grain is stored in both on-farm and

off- farm silos for transport to the domestic and

export market. Road and rail are both attractive for

the transport of grain, with the supply chain

decisions based on cost, proximity to growers and

consumers, level of control and competition. An

example of a typical supply chain is shown in Figure

5 and an example of a typical bulk grain supply

chain is shown in Figure 6.

Figure 5 Typical grain supply chain

Figure 6 Typical bulk grain supply chain

Central to the southern NSW growers, the Narrandera

flour mill produces flour for the Melbourne market and

internal trade between other facilities within the parent

organisation with stockfeed produced as a by-product.

There is little seasonality in the milling operations so

the number of trucks moving flour to Melbourne is

constant. From Melbourne, export material is put into

containers and shipped to the Philippines, Indonesia

and Thailand. Flour for inter-company trade is moved

via rail from the mill’s rail siding to Brisbane, Sydney

and Adelaide depending on the products being

blended.

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

14

5.1.2 Rice

Rice is a mature and vital industry with the vast

majority of Australia’s rice crop generated in the Food

Bowl region by a very large number of growers.

Australian rice growers generally achieve a yield per

hectare far in excess of the global average, a result

which is particularly impressive given the industry is

strictly regulated to ensure a minimal impact on the

environment. The industry is dominated by a few

processing organisations and generates over $800

million per year. Advances in recent years has seen

yields rise and water consumption decline, however

the Murrumbidgee and Murray irrigation districts will

always remain as the centre for Australian rice

production.

Most of Australia’s rice growers are located in the

Murray and Murrumbidgee areas of New South Wales

with a small number in Victoria, as shown in Figure 7

below. There are three mills, three stockfeed

manufacturing plants and 21 rice receival depots in the

Food Bowl region. The regional towns of Leeton,

Griffith, Deniliquin, Coleambally and Finley are

particularly supported by the industry.

Figure 7 Rice growing areas of Australia

Source: Ricegrowers’ Association of Australia (2015)

From the up-country mills, rail is generally the

preferred mode of transport to both domestic

markets and export gateways. The majority of the

crop is exported in bulk from the Port of Melbourne

to a large number of destinations overseas. The

remainder is distributed for domestic consumption.

The key factors in a rice producers supply chain are

reliability to get the product to the customer or port

on time and total cost to serve.

5.1.3 Oilseeds

Both at home and overseas, Australian oils and

oilseeds are in demand. The industry is mature with

a large number of organisations supplying and

exporting oilseed, oilseed meal, unrefined and

refined oils. There are several companies in and

around the Food Bowl region in this industry.

Seeds are crushed within the Food Bowl region and

the oil is sent to either Brisbane or Melbourne for

refining and to Melbourne for export, primarily to

Asia. Once a waste by-product, the oilseed meal is

now used for stockfeed and is sold to local farmers.

There is no seasonality in the production of oilseed

products and the integrated supply chain relies on

collaboration between seed breeders, growers,

storage handlers, refiners, millers and sellers.

Reliability is crucial and the freight task is currently

wholly carried by trucks.

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

15

5.2 Dairy

The Food Bowl region is one of the nation’s largest

dairying areas with many farms in the Goulburn and

Murray Valleys. Compared to the national average,

the farms in the area are generally smaller but carry

more cows and produce more milk. All of the major

dairy companies in Australia have a presence in the

region, producing over 20% of Australia’s dairy

output and contributing approximately $4.3 billion to

Australian GDP. Around 50% of production is

exported to destinations such as the Middle East

and Asia and the other 50% is consumed

domestically in line with population distributions.

Demand from China, India and Asia has driven

strong demand growth in the industry.

Within the dairy industry, some seasonality is

observed and the peak period is usually from

September to January. Farmers in Food Bowl

Region have achieved a shift towards a “flatter” milk

production (less seasonality) driven by low rainfall

and the associated cost of irrigation resulting in

more intensive feeding systems. Products

generated in the Food Bowl region include milk,

processed and cut cheese, infant formula and other

powders, cheese and butter.

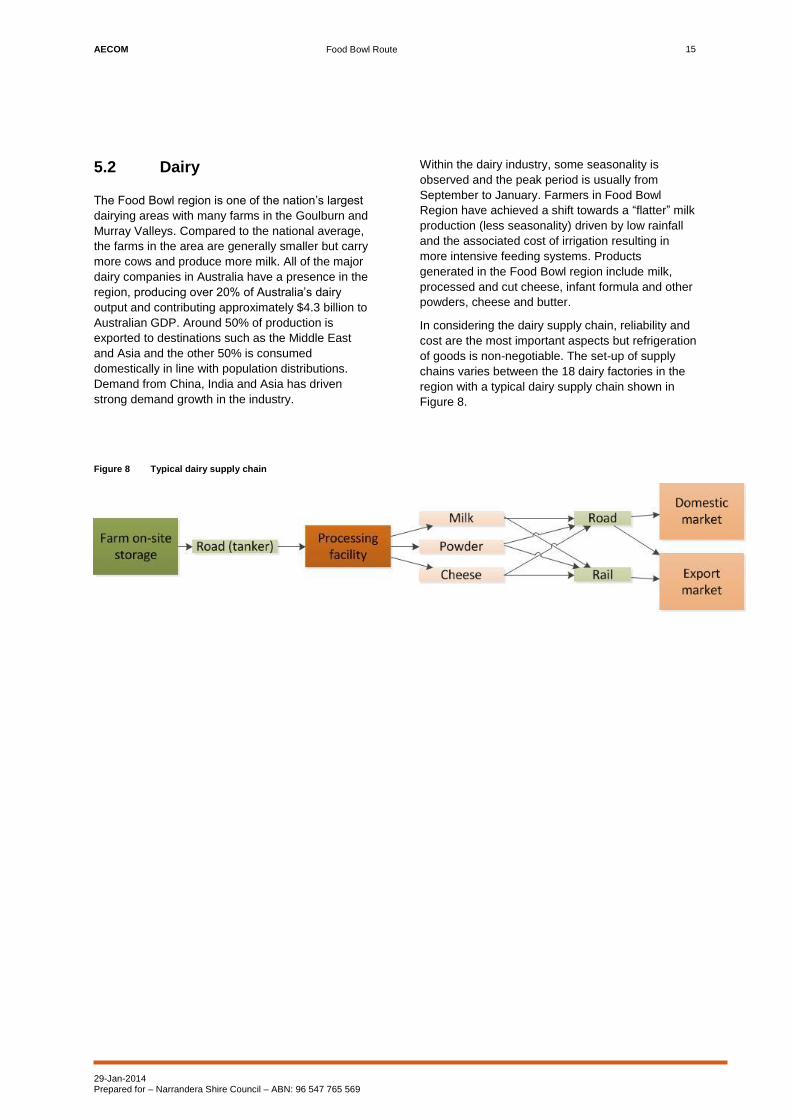

In considering the dairy supply chain, reliability and

cost are the most important aspects but refrigeration

of goods is non-negotiable. The set-up of supply

chains varies between the 18 dairy factories in the

region with a typical dairy supply chain shown in

Figure 8.

Figure 8 Typical dairy supply chain

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

16

Examples of supply chains in the Food Bowl region

include:

- One organisation’s bulk cheese product is

produced in Melbourne, sent to the Food Bowl

region for processing, then is either moved to

Shepparton to be put on rail for export from the

Port of Melbourne or is moved by road to

Melbourne for domestic distribution. Rail is used

for transporting products from Melbourne to

Perth. Packaging inputs mostly originate from

Victoria but some are shipped in from overseas.

- Another organisation interviewed produces large

volumes of milk powder which is not time

sensitive or seasonal but still requires food

grade containers. In this case, the supply chain

is relatively straight forward though the

organisation has little structure to the timing of

when the containers leave the site.

- A third dairy manufacturer’s processing plant

receives a large volume of raw milk daily which

is turned into cheese and milk powder. These

products are then brought to Melbourne using a

combination of rail and road for distribution to

the export and import markets.

5.3 Cotton

Most cotton farms are family owned and operated,

producing yields 2.5 times the global average.

Increases in yield have been attributed to plant

breeding and better water management and the

cotton industry is known for producing a high quality

fibre that is esteemed in Asia with a premium price to

match. Exports from southern New South Wales were

valued at $150 million in 2012-13. Within the Food

Bowl region there are currently two gins, in Whitton

and in Hillston, with two more under construction in

Hay and Carrathool which will become operational in

the near future. Cotton gins separate cottonseed and

trash from the raw cotton fibre in a series of stages.

The main export markets for Australian cotton are in

East Asia, with over 75% sold to China, and seed is

also exported to South East Asia and the US. The

domestic market is primarily based in Melbourne and

Sydney. Cotton and its by-products are used in the

production of bank notes, margarine, rubber and

medical supplies.

The highly seasonal crops in the Murrumbidgee area

are harvested from over 26,000 hectares with the

peak period being between April and September.

Recent high water prices in Queensland have

resulted in large producers migrating to New South

Wales. This expansion has flow on benefits to other

local industries such as freight operators, fertilisers

and fuel.

Due to the high volumes, time and reliability are the

most significant factors in the supply chain. Cotton

growers sell their cotton to one of a number of

independent Australian merchants before ginning and

these merchants pay the fee on behalf of the grower.

Farmers have the option of forward selling a crop for

up to three years which locks in a sale price.

Cottonseed represents 55% of ginned cotton’s weight

and is a major source of container use. A typical

supply chain is shown in Figure 9.

Figure 9 Typical cotton supply chain

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

17

5.4 Horticulture

5.4.1 Fruit

In 2011 there were over 800 fruit producers in the

Food Bowl region with a value of production of over

$440 million. In 2012-13, the region produced around

45% of Australia’s fruits including around 99% of the

national nashi crop, 86% of the national pear crop, and

70% of the national peach crop amongst other fruits.

The number of growers in the region has declined in

the past two decades due to consolidation of

properties but the fresh fruit market in general is

increasing.

There are around 300 fruit and nut farms in the

Shepparton region producing significant volumes of

pears, apples, tomatoes and stone fruit. Australia’s

largest producer of canned fruits, Coca Cola Amatil

(CCA) owned SPC Ardmona has production facilities

in Shepparton and Cobram. The Victorian Government

has recently invested $22 million in the Shepparton

plant to match CCA’s $78 million dollar investment.

Most of the fruit production is consumed domestically

with demand driven by increased consumer health

concerns, improved quality and greater availability.

Exports from the Goulburn Valley are a small but

important component and there is scope to grow the

Asian market.

5.4.2 Citrus

The Mediterranean-like conditions of the Riverina are

conducive to citrus growing with the area producing

180,000 to 200,000 tonnes of citrus for export, valued

at $98 million per annum. Around Griffith, Leeton and

Hillston, citrus planting is largely oranges with a small

proportion of lemons.

Recent improved trade relations have led to growth in

the key export markets of China, South Korea, Japan,

Thailand, Indonesia and the US. Growers have worked

hard to build a market in China where, as recently as

five years ago, exporting was considered to be too

hard.

The Berri Juice factory in Leeton processes over

70,000 tonnes of prime citrus fruit annually.

Traditionally processing oranges, apple and apple

combination juices are becoming a significant part of

the business. All products are sent to the domestic

market by road in cartons or in bulk and there are no

exports due to the short shelf life of the products. The

supply of oranges is seasonal with the peak occurring

between November and April. Time is the most

important factor in the supply chain, followed by

reliability and cost.

5.4.3 Tree nuts

The value of almond and walnuts grown in the Food

Bowl region is over $1.2 billion annually and expected

to grow by over 30% to 2025. Exports are expected to

account for 75% of production.

Tabbita in the Goulburn Valley near Shepparton and

the Leeton in the Riverina are two of the major walnut

production areas in Australia, with over 2,500 hectares

of orchards surrounding the two towns. A state-of-the-

art cracking facility was opened in Leeton in 2014.

Australian walnut producers are in a good position as

there is generally limited scope for expanded

production in the southern hemisphere outside of

Australia.

Walnuts are highly seasonal with a three month

harvest season beginning in March and a nine month

export period. Once the walnuts are graded they are

packed into bags, placed onto pallets and then slip

sheeted into export containers. The containers are

predominantly sent by road to Griffith to be put onto

trains for export from the Port of Melbourne. All

domestic freight is road based and flexibility and cost

are the major determinants for supply chain decisions.

Almonds have traditionally been a strong crop in the

Riverina with over 65,000 almond trees near Griffith

alone. Orchard ownership structures range from

medium sized family enterprises to large investment

companies. Consumer demand continues to grow,

particularly in the export market as living standards

rise in developing countries. Australian almonds supply

nearly all domestic consumption so the growth in

production is directed to markets in the US, Europe,

India, China and the Middle East.

The hazelnut industry in Australia is an emerging

sector with about 60 tonnes grown locally in contrast to

the 2,000 tonnes which are imported annually. To

redress this imbalance, one million hazelnut trees were

planted across 2,000 hectares of land in 2014 at the

Agri Australis hazelnut project site in Narrandera. The

first crop is expected to be harvested in the next three

years with full production generating 5,000 tonnes per

annum seven years from now. As crop yields grow

there is strong incentive to invest in processing within

the region.

5.4.4 Vegetables

With recent restructuring within the Goulburn Valley,

many fruit farms are diversifying into vegetable

production with current production valued at over $400

million per annum. Crops that grow well in the region

include zucchini and broccoli destined for the domestic

market.

AECOM

Food Bowl Route

29-Jan-2014 Prepared for – Narrandera Shire Council – ABN: 96 547 765 569

18

5.5 Wine and beverages

The Griffith and Leeton regions are the largest wine

producing areas in New South Wales and home to the

majority of exported Australian wine. In 2013,

vineyards covering an area of over 20,000 hectares

produced over 300,000 tonnes of grapes. These

wineries are generally large scale family owned

producers well suited for rail transport where possible.

Today there are more than 12 wineries based in the

region including major producers De Bortoli Wines,

Warburn Estate, McWilliams and Casella Wines –

makers of the world famous Yellow Tail brand. In

addition, Casella Wines and Coca Cola Amatil have

recently formed a joint venture to produce beer for the

Australian market aiming for a 15% market share

within 10 years.

Production of wine is partially seasonal with grapes

received from February to April and exports peaking

from September to December. Outputs are fairly

consistent with the domestic market evenly split

according to the spread of population and the major

export markets being the US and China. Most wineries

currently transport finished product by road but supply

chains can vary. Timing, availability of transport and

the care taken when handling the products are key

factors in supply chain decision making.

For example, the winery shown in Figure 10 transports

most of its wine by rail to the Port of Melbourne for

export.

Figure 10 Typical export focused winery supply chain

In contrast, another winery shown in Figure 11 sends its wine in bulk to Sydney for bottling. The majority of their

product is consumed domestically, with the small amount that is exported going through Port Botany.

Figure 11 Typical domestic focused winery supply chain

AECOM

Food Bowl Route