focusing your organization on strategy—with the brilliant ...€¦ · anced scorecard in your...

TRANSCRIPT

Included with this collection:

www.hbr.org

C O L L E C T I O N

2

Putting the Balanced Scorecard to Work

by Robert S. Kaplan and David P. Norton

19

Measuring the Strategic Readiness of Intangible Assets

by Robert S. Kaplan and David P. Norton

35

Using the Balanced Scorecard as a Strategic

Management System

by Robert S. Kaplan and David P. Norton

49

Having Trouble with Your Strategy? Then Map It

by Robert S. Kaplan and David P. Norton

Focusing Your Organization on Strategy—with the Balanced Scorecard, 2nd Edition

Your strategy’s brilliant—but can you

execute

it?

Product 5933

Collection Overview The Articles

page 1

CO

PYR

IGH

T ©

200

4 H

AR

VA

RD

BU

SIN

ESS

SC

HO

OL

PU

BLI

SHIN

G C

OR

PO

RA

TIO

N. A

LL R

IGH

TS

RE

SER

VE

D.

The Balanced Scorecard has transformed companies around the globe. This revolu-tionary performance management sys-tem has been helping top executives set corporate strategy and objectives—and translate them into a coherent set of mea-sures—since 1992.

What makes the Balanced Scorecard so powerful? It transforms strategy into a continuous process owned by every em-ployee, not just top managers. It also en-ables you to communicate high-level goals down to all organizational levels. Employees know not only

what

to do, but

why

.

But most important, the Balanced Score-card doesn’t treat strategy from only a fi-nancial perspective; it augments financial measures with objectives and metrics in three additional “perspectives”—cus-tomer relationships, internal processes, and learning and growth.

These less tangible areas are notoriously difficult to measure and influence. In 2004, Robert Kaplan and David Norton augmented the Scorecard methodology to include new tools that enable you to further unleash the power of intangible assets. In the article “Measuring the Strate-gic Readiness of Intangible Assets,” they describe how to assess how prepared your company’s people, systems, and cul-ture are to carry out your strategy—and turn it into long-term tangible results.

The four articles in this collection, all writ-ten by Kaplan and Norton, give you the tools to start building and using a Bal-anced Scorecard in your firm.

3

Article Summary

4

Putting the Balanced Scorecard to Work

by Robert S. Kaplan and David P. NortonYour Balanced Scorecard provides a top-down description of your company’s strategy and your assumptions about the corporate objectives and measures needed to implement that strategy.

To begin building your scorecard, ask: “If we successfully implement our strategy, how will we look different to our shareholders and customers? How will our internal processes change? What will happen to our ability to innovate and grow? What are each scorecard perspective’s critical success factors? What metrics will tell us whether we’re addressing those factors as planned?”

18

Further Reading

20

Article Summary

21

Measuring the Strategic Readiness of Intangible Assets

by Robert S. Kaplan and David P. NortonIt’s not enough to clarify your strategy; you must measure your intangible assets’ strategic readiness—how well your employees’ skills, information and technical systems, and leader-ship and culture align with your strategy. These intangible assets directly enhance the inter-nal processes that generate revenue needed to meet your long-term financial goals.

To measure strategic readiness, identify the intangible assets you need to perform the inter-nal processes

most

critical to your strategy. Then assess your current capabilities in all these areas, identifying changes needed to improve alignment.

34

Further Reading

36

Article Summary

37

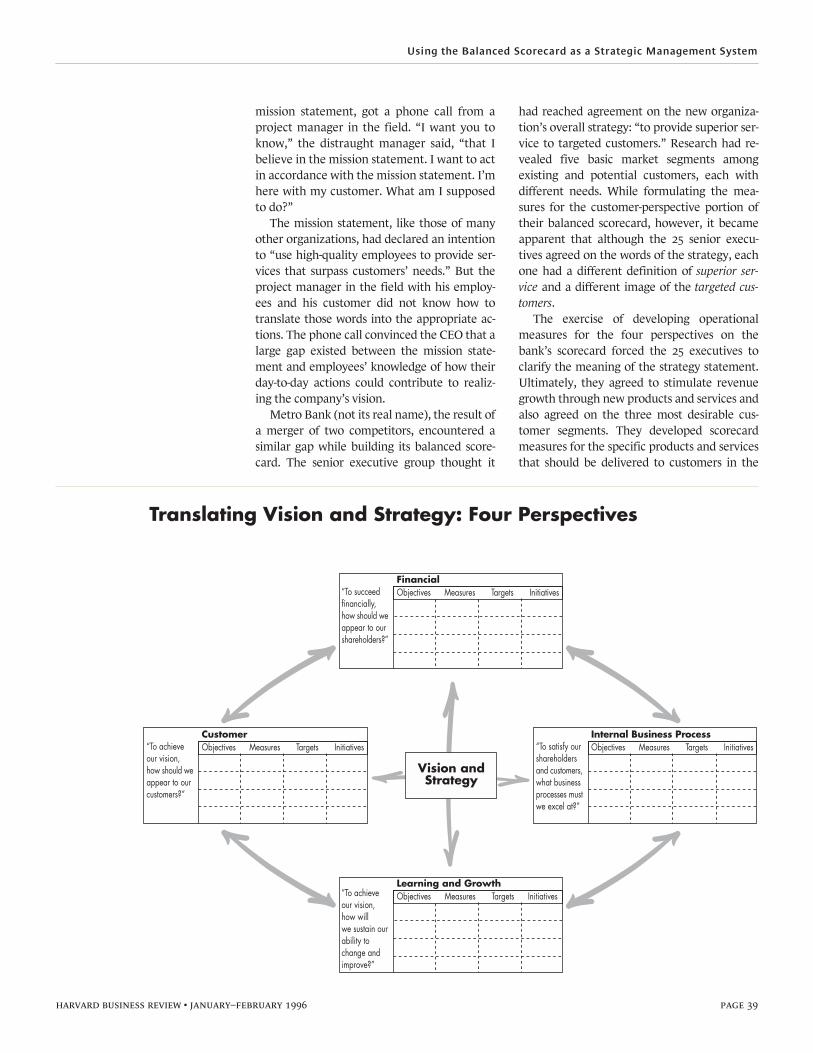

Using the Balanced Scorecard as a Strategic Management System

by Robert S. Kaplan and David P. NortonYou’ve defined strategic objectives and measures and measured your intangible assets’ stra-tegic readiness. Now link employees’ everyday actions to your company’s long-term goals: translate your vision into metrics everyone can understand; communicate high-level goals and link them to individual performance and compensation; and use scorecard data to test and revise your theories about which actions generate which results.

48

Further Reading

50

Article Summary

51

Having Trouble with Your Strategy? Then Map It

by Robert S. Kaplan and David P. NortonTo execute your strategy, you must communicate it throughout your organization so em-ployees see how their everyday actions support—or hamper—the strategy. How to send a clear, compelling message? Use a strategy map—a one-page, graphic depiction of the cause-and-effect connections among your Balanced Scorecard’s four perspectives. Concise and clear, your strategy map tells employees throughout your organization how to turn re-sources (especially intangible ones) into the tangible results promised by your strategy.

61

Further Reading

1st article from the collection:

Focusing Your Organization on Strategy—with the Balanced Score-card, 2nd Edition

page 2

Putting the Balanced Scorecard to Work

by Robert S. Kaplan and David P. Norton

Included with this full-text

Harvard Business Review

article:

The Idea in Brief—the core idea

The Idea in Practice—putting the idea to work

3

Article Summary

4

Putting the Balanced Scorecard to Work

A list of related materials, with annotations to guide further

exploration of the article’s ideas and applications

18

Further Reading

Product 4118

Putting the Balanced Scorecard to Work

page 3

The Idea in Brief The Idea in Practice

CO

PYR

IGH

T ©

200

0 H

AR

VA

RD

BU

SIN

ESS

SC

HO

OL

PU

BLI

SHIN

G C

OR

PO

RA

TIO

N. A

LL R

IGH

TS

RE

SER

VE

D.

What makes a balanced scorecard special? Four characteristics stand out:

1. It is a top-down reflection of the com-pany’s mission and strategy.

By contrast, the measures most companies track are bottom-up: deriving from local activities or ad hoc processes, they are often irrelevant to the overall strategy.

2. It is forward-looking.

It addresses cur-rent and future success. Traditional financial measures describe how the company per-formed during the last reporting period—without indicating how managers can im-prove performance during the next.

3. It integrates external and internal mea-sures.

This helps managers see where they have made trade-offs between perfor-mance measures in the past, and helps en-sure that future success on one measure does not come at the expense of another.

4. It helps you focus.

Many companies track more measures than they can possi-bly use. But a balanced scorecard requires managers to reach agreement on only those measures that are most critical to the success of the company's strategy. Fifteen to twenty distinct measures are usually enough, each measure custom-designed for the unit to which it applies.

Linking measurements to strategy is the heart of a successful scorecard development pro-cess. The three key questions to ask here:

1. If we succeed with our vision and strategy, how will we look different

•

to our shareholders and customers?

•

in terms of our internal processes?

•

in terms of our ability to innovate and grow?

2. What are the critical success factors in each of the four scorecard perspectives?

3. What are the key measurements that will tell us whether we’re addressing those success factors as planned?

The balanced scorecard also brings an organi-zational focus to the variety of local change programs under way in a company at any given time. As the benchmark against which all new projects are evaluated, the scorecard functions as more than just a measurement system. In the words of FMC Corp. executive Larry Brady, it becomes “the cornerstone of the way you run the business,” that is, “the core of the management system” itself.

Example:

Rockwater, an underwater engineering and construction firm, crafted a five-pronged strategy: to provide services that surpassed customers’ expectations and needs; to achieve high levels of customer satisfaction; to make continuous improvements in safety, equipment reliability, responsive-ness, and cost effectiveness; to recruit and retain high-quality employees; and to real-ize shareholder expectations. Using the bal-anced scorecard, Rockwater’s senior man-agement translated this strategy into tangible goals and actions.

• The financial measures they chose in-cluded return-on-capital employed and cash flow, because shareholders had indi-cated a preference for short-term results.

• Customer measures focused on those clients most interested in a high value-added relationship.

•

The

company introduced new bench-marks that emphasized the integration of key internal processes. It also added a safety index as a means of controlling indirect costs associated with accidents.

• Learning and growth targets emphasized the percentage of revenue coming from new services and the rate of improve-ment of safety and rework measures.

Putting the Balanced Scorecard to Work

by Robert S. Kaplan and David P. Norton

harvard business review • september–october 1993 page 4

CO

PYR

IGH

T ©

199

3 H

AR

VA

RD

BU

SIN

ESS

SC

HO

OL

PU

BLI

SHIN

G C

OR

PO

RA

TIO

N. A

LL R

IGH

TS

RE

SER

VE

D.

What do companies like Rockwater, Apple Computer, and Advanced

Micro Devices have in common? They’re using the scorecard to

measure performance and set strategy.

Today’s managers recognize the impact thatmeasures have on performance. But theyrarely think of measurement as an essentialpart of their strategy. For example, executivesmay introduce new strategies and innovativeoperating processes intended to achievebreakthrough performance, then continue touse the same short-term financial indicatorsthey have used for decades, measures like re-turn-on-investment, sales growth, and operat-ing income. These managers fail not only tointroduce new measures to monitor new goalsand processes but also to question whether ornot their old measures are relevant to the newinitiatives.

Effective measurement, however, must bean integral part of the management process.The balanced scorecard, first proposed in theJanuary-February 1992 issue of HBR (“The Bal-anced Scorecard—Measures that Drive Perfor-mance”), provides executives with a compre-hensive framework that translates acompany’s strategic objectives into a coherentset of performance measures. Much more than

a measurement exercise, the balanced score-card is a management system that can moti-vate breakthrough improvements in such criti-cal areas as product, process, customer, andmarket development.

The scorecard presents managers with fourdifferent perspectives from which to choosemeasures. It complements traditional financialindicators with measures of performance forcustomers, internal processes, and innovationand improvement activities. These measuresdiffer from those traditionally used by compa-nies in a few important ways:

Clearly, many companies already have myr-iad operational and physical measures for localactivities. But these local measures are bottom-up and derived from ad hoc processes. Thescorecard’s measures, on the other hand, aregrounded in an organization’s strategic objec-tives and competitive demands. And, by re-quiring managers to select a limited number ofcritical indicators within each of the four per-spectives, the scorecard helps focus this strate-gic vision.

Putting the Balanced Scorecard to Work

harvard business review • september–october 1993 page 5

In addition, while traditional financial mea-sures report on what happened last periodwithout indicating how managers can improveperformance in the next, the scorecard func-tions as the cornerstone of a company’s cur-rent

and

future success.Moreover, unlike conventional metrics,

the information from the four perspectivesprovides balance between external measureslike operating income and internal measureslike new product development. This balancedset of measures both reveals the trade-offs thatmanagers have already made among perfor-mance measures and encourages them toachieve their goals in the future without mak-ing trade-offs among key success factors.

Finally, many companies that are now at-tempting to implement local improvementprograms such as process reengineering, totalquality, and employee empowerment lack asense of integration. The balanced scorecardcan serve as the focal point for the organiza-tion’s efforts, defining and communicating pri-orities to managers, employees, investors, evencustomers. As a senior executive at one majorcompany said, “Previously, the one-year bud-get was our primary management planning de-vice. The balanced scorecard is now used asthe language, the benchmark against which allnew projects and businesses are evaluated.”

The balanced scorecard is not a templatethat can be applied to businesses in general oreven industrywide. Different market situa-tions, product strategies, and competitive envi-ronments require different scorecards. Busi-ness units devise customized scorecards to fittheir mission, strategy, technology, and cul-ture. In fact, a critical test of a scorecard’s suc-cess is its transparency: from the 15 to 20 score-card measures, an observer should be able tosee through to the business unit’s competitivestrategy. A few examples will illustrate howthe scorecard uniquely combines managementand measurement in different companies.

Rockwater: Responding to a Changing Industry

Rockwater, a wholly owned subsidiary ofBrown & Root/Halliburton, a global engineer-ing and construction company, is a worldwideleader in underwater engineering and con-struction. Norman Chambers, hired as CEO inlate 1989, knew that the industry’s competi-tive world had changed dramatically. “In the

1970s, we were a bunch of guys in wet suitsdiving off barges into the North Sea withburning torches,” Chambers said. But compe-tition in the subsea contracting business hadbecome keener in the 1980s, and manysmaller companies left the industry. In addi-tion, the focus of competition had shifted.Several leading oil companies wanted to de-velop long-term partnerships with their sup-pliers rather than choose suppliers based onlow-price competition.

With his senior management team, Cham-bers developed a vision: “As our customers’preferred provider, we shall be the industryleader in providing the highest standards ofsafety and quality to our clients.” He also de-veloped a strategy to implement the vision.The five elements of that strategy were: ser-vices that surpass customers’ expectations andneeds; high levels of customer satisfaction;continuous improvement of safety, equip-ment reliability, responsiveness, and cost ef-fectiveness; high-quality employees; and real-ization of shareholder expectations. Thoseelements were in turn developed into strate-gic objectives (see the chart “Rockwater’sStrategic Objectives”). If, however, the strate-gic objectives were to create value for thecompany, they had to be translated into tangi-ble goals and actions.

Rockwater’s senior management teamtransformed its vision and strategy into thebalanced scorecard’s four sets of performancemeasures (see the chart “Rockwater’s Bal-anced Scorecard”):

Financial Measures:

The financial perspec-tive included three measures of importance tothe shareholder. Return-on-capital-employedand cash flow reflected preferences for short-term results, while forecast reliability signaledthe corporate parent’s desire to reduce the his-torical uncertainty caused by unexpected vari-ations in performance. Rockwater manage-ment added two financial measures. Projectprofitability provided focus on the project asthe basic unit for planning and control, andsales backlog helped reduce uncertainty ofperformance.

Customer Satisfaction:

Rockwater wantedto recognize the distinction between its twotypes of customers: Tier I customers, oil com-panies that wanted a high value-added rela-tionship, and Tier II customers, those thatchose suppliers solely on the basis of price. A

Robert S. Kaplan

is the Arthur LowesDickinson Professor of Accounting atthe Harvard Business School.

David P.Norton

is founder and president of Re-naissance Strategy Group, a consultingfirm located in Lincoln, Massachusetts.

Putting the Balanced Scorecard to Work

harvard business review • september–october 1993 page 6

price index, incorporating the best availableintelligence on competitive position, was in-cluded to ensure that Rockwater could still re-tain Tier II customers’ business when requiredby competitive conditions.

The company’s strategy, however, was toemphasize value-based business. An indepen-dent organization conducted an annual surveyto rank customers’ perceptions of Rockwater’sservices compared to those of its competitors.In addition, Tier I customers were asked tosupply monthly satisfaction and performanceratings. Rockwater executives felt that imple-menting these ratings gave them a direct tie totheir customers and a level of market feedbackunsurpassed in most industries. Finally, mar-ket share by key accounts provided objectiveevidence that improvements in customer satis-faction were being translated into tangiblebenefits.

Internal Processes:

To develop measures ofinternal processes, Rockwater executives de-fined the life cycle of a project from launch(when a customer need was recognized) tocompletion (when the customer need had

been satisfied). Measures were formulated foreach of the five business-process phases in thisproject cycle (see the chart “How RockwaterFulfills Customer Needs”):

•

Identify:

number of hours spent with pros-pects discussing new work;

•

Win:

tender success rate;•

Prepare and Deliver:

project performanceeffectiveness index, safety/loss control, rework;

•

Closeout

: length of project closeout cycle.The internal business measures emphasized

a major shift in Rockwater’s thinking. For-merly, the company stressed performance foreach functional department. The new focusemphasized measures that integrated key busi-ness processes. The development of a compre-hensive and timely index of project perfor-mance effectiveness was viewed as a key corecompetency for the company. Rockwater feltthat safety was also a major competitive factor.Internal studies had revealed that the indirectcosts from an accident could be 5 to 50 timesthe direct costs. The scorecard included a safetyindex, derived from a comprehensive safetymeasurement system, that could identify and

Rockwater’s Strategic Objectives

The Vision

“As our customers’preferred provider,we shall be theindustry leader.This is our mission.”

Strategy

Services that Surpass Needs

Customer Satisfaction

Continuous Improvement

Quality of Employees

Shareholder Expectations

Fin

anci

alC

ust

om

erIn

tern

alG

row

th

Return on Capital

Cash Flow

Project Profitability

Reliability of Performance

Value for Money Tier ICompetitive Price Tier IIHassle-Free RelationshipHigh-Performance ProfessionalsInnovation

Shape Customer RequirementTender EffectivenessQuality ServiceSafety/Loss ControlSuperior Project Management

Continuous Improvement

Product and Service Innovation

Empowered Work Force

Putting the Balanced Scorecard to Work

harvard business review • september–october 1993 page 7

classify all undesired events with the potentialfor harm to people, property, or process.

The Rockwater team deliberated about thechoice of metric for the identification stage. Itrecognized that hours spent with key prospectsdiscussing new work was an input or processmeasure rather than an output measure. Themanagement team wanted a metric thatwould clearly communicate to all members ofthe organization the importance of buildingrelationships with and satisfying customers.The team believed that spending quality timewith key customers was a prerequisite for in-fluencing results. This input measure was de-liberately chosen to educate employees aboutthe importance of working closely to identifyand satisfy customer needs.

Innovation and Improvement:

The inno-vation and learning objectives are intended todrive improvement in financial, customer,and internal process performance. At Rockwa-ter, such improvements came from productand service innovation that would create newsources of revenue and market expansion, aswell as from continuous improvement in in-

ternal work processes. The first objective wasmeasured by percent revenue from new ser-vices and the second objective by a continuousimprovement index that represented the rateof improvement of several key operationalmeasures, such as safety and rework. But inorder to drive both product/service innovationand operational improvements, a supportiveclimate of empowered, motivated employeeswas believed necessary. A staff attitude surveyand a metric for the number of employee sug-gestions measured whether or not such a cli-mate was being created. Finally, revenue peremployee measured the outcomes of em-ployee commitment and training programs.

The balanced scorecard has helped Rockwa-ter’s management emphasize a process view ofoperations, motivate its employees, and incor-porate client feedback into its operations. Itdeveloped a consensus on the necessity of cre-ating partnerships with key customers, the im-portance of order-of-magnitude reductions insafety-related incidents, and the need for im-proved management at every phase of multi-year projects. Chambers sees the scorecard as

Rockwater’s Balanced Scorecard

Customer Perspective

Financial Perspective

Internal Business Perspective

Innovation and LearningPerspective

Pricing Index Tier II CustomersCustomer Ranking SurveyCustomer Satisfaction IndexMarket Share

Business Segment, Tier I Customers, Key Accounts

Return-on-Capital-Employed

Cash Flow

Project Profitability

Profit Forecast Reliability

Sales Backlog

Hours with Customers on New WorkTender Success RateReworkSafety Incident IndexProject Performance IndexProject Closeout Cycle

% Revenue from New ServicesRate of Improvement IndexStaff Attitude Survey# of Employee SuggestionsRevenue per Employee

Putting the Balanced Scorecard to Work

harvard business review • september–october 1993 page 8

an invaluable tool to help his company ulti-mately achieve its mission: to be number onein the industry.

Apple Computer: Adjusting Long-Term Performance

Apple Computer developed a balanced score-card to focus senior management on a strat-egy that would expand discussions beyondgross margin, return on equity, and marketshare. A small steering committee, intimatelyfamiliar with the deliberations and strategicthinking of Apple’s Executive ManagementTeam, chose to concentrate on measurementcategories within each of the four perspectivesand to select multiple measurements withineach category. For the financial perspective,Apple emphasized shareholder value; for thecustomer perspective, market share and cus-tomer satisfaction; for the internal processperspective, core competencies; and, finally,for the innovation and improvement perspec-tive, employee attitudes. Apple’s manage-ment stressed these categories in the follow-ing order:

Customer Satisfaction:

Historically, Applehad been a technology- and product-focusedcompany that competed by designing bettercomputers. Customer satisfaction metrics arejust being introduced to orient employees to-ward becoming a customer-driven company.J.D. Power & Associates, a customer-surveycompany, now works for the computer indus-try. However, because it recognized that itscustomer base was not homogeneous, Applefelt that it had to go beyond J.D. Power & As-sociates and develop its own independent sur-veys in order to track its key market segmentsaround the world.

Core Competencies:

Company executiveswanted employees to be highly focused on a

few key competencies: for example, user-friendly interfaces, powerful software archi-tectures, and effective distribution systems.However, senior executives recognized thatmeasuring performance along these compe-tency dimensions could be difficult. As a re-sult, the company is currently experimentingwith obtaining quantitative measures of thesehard-to-measure competencies.

Employee Commitment and Alignment:

Apple conducts a comprehensive employeesurvey in each of its organizations every twoyears; surveys of randomly selected employeesare performed more frequently. The surveyquestions are concerned with how well em-ployees understand the company’s strategy aswell as whether or not they are asked to de-liver results that are consistent with that strat-egy. The results of the survey are displayed interms of both the actual level of employee re-sponses and the overall trend of responses.

Market Share:

Achieving a critical thresh-old of market share was important to seniormanagement not only for the obvious salesgrowth benefits but also to attract and retainsoftware developers to Apple platforms.

Shareholder Value:

Shareholder value is in-cluded as a performance indicator, eventhough this measure is a result—not adriver—of performance. The measure is in-cluded to offset the previous emphasis ongross margin and sales growth, measures thatignored the investments required today togenerate growth for tomorrow. In contrast,the shareholder value metric quantifies theimpact of proposed investments for businesscreation and development. The majority ofApple’s business is organized on a functionalbasis—sales, product design, and worldwidemanufacturing and operations—so share-holder value can be calculated only for the en-tire company instead of at a decentralizedlevel. The measure, however, helps seniormanagers in each major organizational unitassess the impact of their activities on the en-tire company’s valuation and evaluate newbusiness ventures.

While these five performance indicatorshave only recently been developed, they havehelped Apple’s senior managers focus theirstrategy in a number of ways. First of all, thebalanced scorecard at Apple serves primarilyas a planning device, instead of as a control de-vice. To put it another way, Apple uses the

How Rockwater Fulfills Customer Needs

CustomerNeed

Recognized

CustomerNeedMet

Identify Win Prepare Perform Closeout

#1 #2 #3 #4 #5

DevelopmentCycle

Supply Cycle

Putting the Balanced Scorecard to Work

harvard business review • september–october 1993 page 9

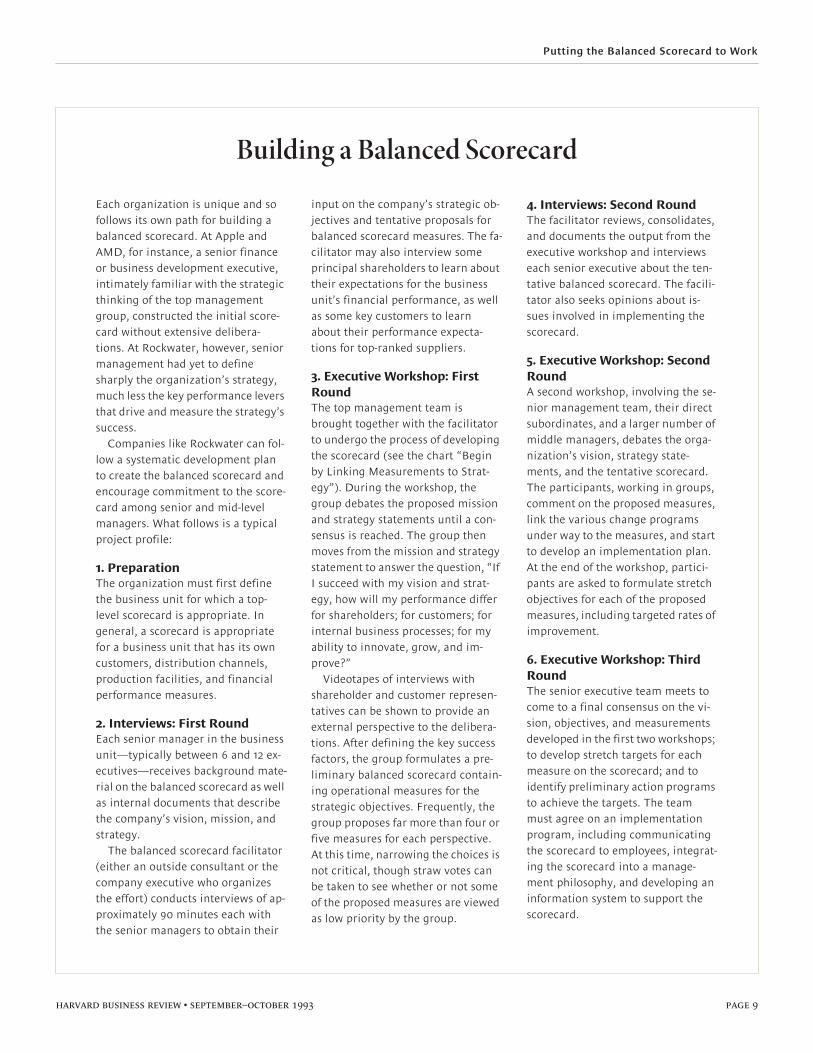

Building a Balanced Scorecard

Each organization is unique and so follows its own path for building a balanced scorecard. At Apple and AMD, for instance, a senior finance or business development executive, intimately familiar with the strategic thinking of the top management group, constructed the initial score-card without extensive delibera-tions. At Rockwater, however, senior management had yet to define sharply the organization’s strategy, much less the key performance levers that drive and measure the strategy’s success.

Companies like Rockwater can fol-low a systematic development plan to create the balanced scorecard and encourage commitment to the score-card among senior and mid-level managers. What follows is a typical project profile:

1. Preparation

The organization must first define the business unit for which a top-level scorecard is appropriate. In general, a scorecard is appropriate for a business unit that has its own customers, distribution channels, production facilities, and financial performance measures.

2. Interviews: First Round

Each senior manager in the business unit—typically between 6 and 12 ex-ecutives—receives background mate-rial on the balanced scorecard as well as internal documents that describe the company’s vision, mission, and strategy.

The balanced scorecard facilitator (either an outside consultant or the company executive who organizes the effort) conducts interviews of ap-proximately 90 minutes each with the senior managers to obtain their

input on the company’s strategic ob-jectives and tentative proposals for balanced scorecard measures. The fa-cilitator may also interview some principal shareholders to learn about their expectations for the business unit’s financial performance, as well as some key customers to learn about their performance expecta-tions for top-ranked suppliers.

3. Executive Workshop: First Round

The top management team is brought together with the facilitator to undergo the process of developing the scorecard (see the chart “Begin by Linking Measurements to Strat-egy”). During the workshop, the group debates the proposed mission and strategy statements until a con-sensus is reached. The group then moves from the mission and strategy statement to answer the question, “If I succeed with my vision and strat-egy, how will my performance differ for shareholders; for customers; for internal business processes; for my ability to innovate, grow, and im-prove?”

Videotapes of interviews with shareholder and customer represen-tatives can be shown to provide an external perspective to the delibera-tions. After defining the key success factors, the group formulates a pre-liminary balanced scorecard contain-ing operational measures for the strategic objectives. Frequently, the group proposes far more than four or five measures for each perspective. At this time, narrowing the choices is not critical, though straw votes can be taken to see whether or not some of the proposed measures are viewed as low priority by the group.

4. Interviews: Second Round

The facilitator reviews, consolidates, and documents the output from the executive workshop and interviews each senior executive about the ten-tative balanced scorecard. The facili-tator also seeks opinions about is-sues involved in implementing the scorecard.

5. Executive Workshop: Second Round

A second workshop, involving the se-nior management team, their direct subordinates, and a larger number of middle managers, debates the orga-nization’s vision, strategy state-ments, and the tentative scorecard. The participants, working in groups, comment on the proposed measures, link the various change programs under way to the measures, and start to develop an implementation plan. At the end of the workshop, partici-pants are asked to formulate stretch objectives for each of the proposed measures, including targeted rates of improvement.

6. Executive Workshop: Third Round

The senior executive team meets to come to a final consensus on the vi-sion, objectives, and measurements developed in the first two workshops; to develop stretch targets for each measure on the scorecard; and to identify preliminary action programs to achieve the targets. The team must agree on an implementation program, including communicating the scorecard to employees, integrat-ing the scorecard into a manage-ment philosophy, and developing an information system to support the scorecard.

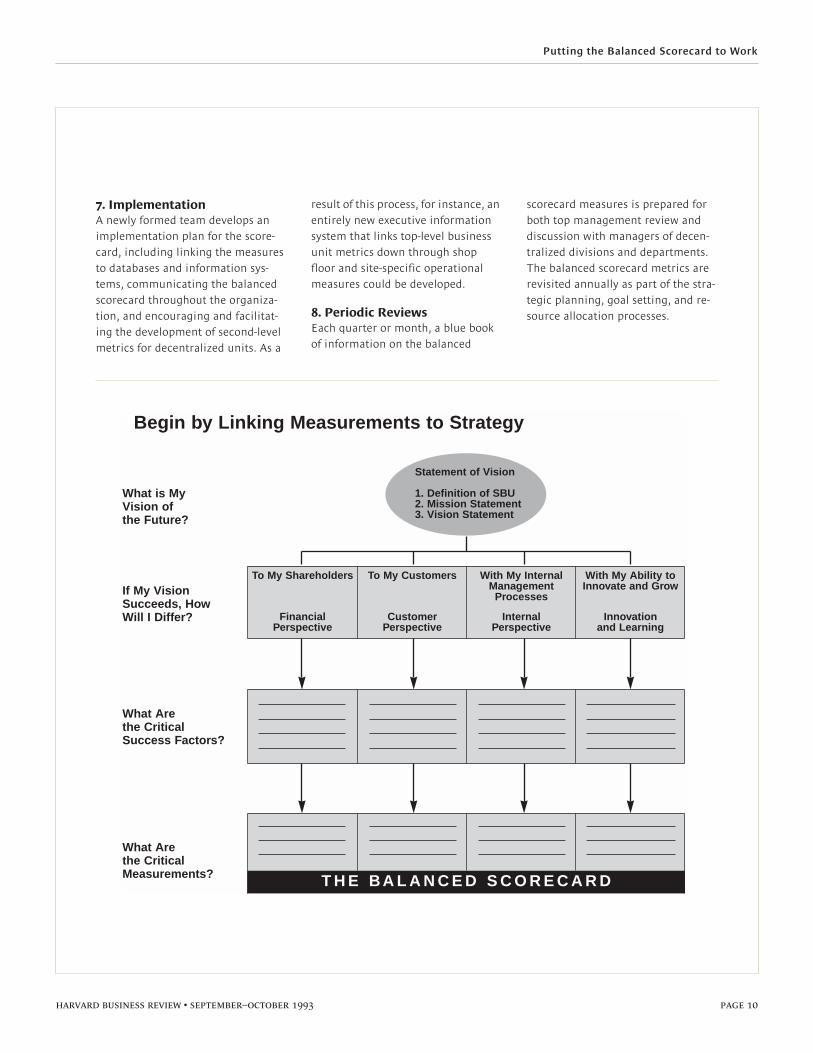

Putting the Balanced Scorecard to Work

harvard business review • september–october 1993 page 10

7. Implementation

A newly formed team develops an implementation plan for the score-card, including linking the measures to databases and information sys-tems, communicating the balanced scorecard throughout the organiza-tion, and encouraging and facilitat-ing the development of second-level metrics for decentralized units. As a

result of this process, for instance, an entirely new executive information system that links top-level business unit metrics down through shop floor and site-specific operational measures could be developed.

8. Periodic Reviews

Each quarter or month, a blue book of information on the balanced

scorecard measures is prepared for both top management review and discussion with managers of decen-tralized divisions and departments. The balanced scorecard metrics are revisited annually as part of the stra-tegic planning, goal setting, and re-source allocation processes.

With My Ability toInnovate and Grow

Innovationand Learning

To My Shareholders

FinancialPerspective

With My InternalManagement

Processes

Internal Perspective

To My Customers

CustomerPerspective

Begin by Linking Measurements to Strategy

T H E BA L A N C E D S C O R E C A R D

If My VisionSucceeds, HowWill I Differ?

What is MyVision ofthe Future?

What Arethe CriticalSuccess Factors?

What Arethe CriticalMeasurements?

Statement of Vision

1. Definition of SBU2. Mission Statement3. Vision Statement

Putting the Balanced Scorecard to Work

harvard business review • september–october 1993 page 11

measures to adjust the “long wave” of corpo-rate performance, not to drive operatingchanges. Moreover, the metrics at Apple, withthe exception of shareholder value, can bedriven both horizontally and vertically intoeach functional organization. Considered ver-tically, each individual measure can be brokendown into its component parts in order toevaluate how each part contributes to thefunctioning of the whole. Thought of horizon-tally, the measures can identify how, for ex-ample, design and manufacturing contributeto an area such as customer satisfaction. In ad-dition, Apple has found that its balancedscorecard has helped develop a language ofmeasurable outputs for how to launch and le-verage programs.

The five performance indicators at Appleare benchmarked against best-in-class organi-zations. Today they are used to build businessplans and are incorporated into senior execu-tives’ compensation plans.

Advanced Micro Devices: Consolidating Strategic Information

Advanced Micro Devices (AMD), a semicon-ductor company, executed a quick and easytransition to a balanced scorecard. It alreadyhad a clearly defined mission, strategy state-ment, and shared understanding among se-nior executives about its competitive niche. Italso had many performance measures frommany different sources and information sys-tems. The balanced scorecard consolidatedand focused these diverse measures into aquarterly briefing book that contained sevensections: financial measures; customer-basedmeasures, such as on-time delivery, lead time,and performance-to-schedule; measures ofcritical business processes in wafer fabrica-tion, assembly and test, new product develop-ment, process technology development (e.g.,submicron etching precision), and, finally,measures for corporate quality. In addition,organizational learning was measured by im-posing targeted rates of improvements for keyoperating parameters, such as cycle time andyields by process.

At present, AMD sees its scorecard as a sys-tematic repository for strategic informationthat facilitates long-term trend analysis forplanning and performance evaluation.

Driving the Process of Change

The experiences of these companies and oth-ers reveal that the balanced scorecard is mostsuccessful when it is used to drive the processof change. Rockwater, for instance, came intoexistence after the merger of two different or-ganizations. Employees came from differentcultures, spoke different languages, and haddifferent operating experiences and back-grounds. The balanced scorecard helped thecompany focus on what it had to do well inorder to become the industry leader.

Similarly, Joseph De Feo, chief executive ofService Businesses, one of the three operatingdivisions of Barclays Bank, had to transformwhat had been a captive, internal supplier ofservices into a global competitor. The score-card highlighted areas where, despite apparentconsensus on strategy, there still was consider-able disagreement about how to make thestrategy operational. With the help of thescorecard, the division eventually achievedconsensus concerning the highest priorityareas for achievement and improvement andidentified additional areas that needed atten-tion, such as quality and productivity. De Feoassessed the impact of the scorecard, saying,“It helped us to drive major change, to becomemore market oriented, throughout our organi-zation. It provided a shared understanding ofour goals and what it took to achieve them.”

Analog Devices, a semiconductor company,served as the prototype for the balanced score-card and now uses it each year to update thetargets and goals for division managers. JerryFishman, president of Analog, said, “At the be-ginning, the scorecard drove significant andconsiderable change. It still does when wefocus attention on particular areas, such as thegross margins on new products. But its mainimpact today is to help sustain programs thatour people have been working on for years.”Recently, the company has been attempting tointegrate the scorecard metrics with

hoshin

planning, a procedure that concentrates an en-tire company on achieving one or two key ob-jectives each year. Analog’s hoshin objectiveshave included customer service and new prod-uct development, for which measures alreadyexist on the company’s scorecard.

But the scorecard isn’t always the impetusfor such dramatic change. For example,AMD’s scorecard has yet to have a significantimpact because company management didn’t

The scorecard enables

managers to see the

breadth and totality of

company operations.

Putting the Balanced Scorecard to Work

harvard business review • september–october 1993 page 12

use it to drive the change process. Before turn-ing to the scorecard, senior managers had al-ready formulated and gained consensus for thecompany’s mission, strategy, and key perfor-mance measures. AMD competes in a singleindustry segment. The top 12 managers are in-timately familiar with the markets, engineer-ing, technology, and other key levers in thissegment. The summary and aggregate infor-mation in the scorecard were neither new norsurprising to them. And managers of decen-tralized production units also already had asignificant amount of information about theirown operations. The scorecard did enablethem to see the breadth and totality of com-pany operations, enhancing their ability to be-come better managers for the entire company.But, on balance, the scorecard could only en-capsulate knowledge that managers in generalhad already learned.

AMD’s limited success with the balancedscorecard demonstrates that the scorecard hasits greatest impact when used to drive achange process. Some companies link compen-sation of senior executives to achieving stretchtargets for the scorecard measures. Most areattempting to translate the scorecard into op-erational measures that become the focus forimprovement activities in local units. Thescorecard is not just a measurement system; itis a management system to motivate break-through competitive performance.

Implementing the Balanced Scorecard at FMC Corporation: An Interview with Larry D. Brady

FMC Corporation is one of the most diversifiedcompanies in the United States, producing morethan 300 product lines in 21 divisions organizedinto 5 business segments: industrial chemicals,performance chemicals, precious metals, de-fense systems, and machinery and equipment.Based in Chicago, FMC has worldwide revenuesin excess of $4 billion.

Since 1984, the company has realized annualreturns-on-investment of greater than 15%. Cou-pled with a major recapitalization in 1986, thesereturns resulted in an increasing shareholdervalue that significantly exceeded industrial aver-ages. In 1992, the company completed a strategicreview to determine the best future course tomaximize shareholder value. As a result of thatreview, FMC adopted a growth strategy to com-plement its strong operating performance. Thisstrategy required a greater external focus and ap-preciation of operating trade-offs.

To help make the shift, the company decidedto use the balanced scorecard. In this interviewconducted by Robert S. Kaplan, Larry D. Brady,executive vice president of FMC, talks about thecompany’s experience implementing the score-card.

Robert S. Kaplan:

What’s the status of thebalanced scorecard at FMC?

Larry D. Brady:

Although we are just com-pleting the pilot phase of implementation, Ithink that the balanced scorecard is likely to be-

The Scorecard’s Impact on External Reporting

Several managers have asked whether or not the balanced scorecard is applicable to external reporting. If the scorecard is indeed a driver of long-term performance, shouldn’t this information be relevant to the investment community?

In fact, the scorecard does not translate easily to the investment community. A scorecard makes sense primarily for busi-ness units and divisions with a well-defined strategy. Most companies have several divi-sions, each with its own mission and strat-egy, whose scorecards cannot be aggre-gated into an overall corporate scorecard. And if the scorecard does indeed provide a

transparent vision into a unit’s strategy, then the information, even the measures being used, might be highly sensitive data that could reveal much of value to competi-tors. But most important, as a relatively re-cent innovation, the scorecard would bene-fit from several years of experimentation within companies before it becomes a sys-tematic part of reporting to external constit-uencies.

Even if the scorecard itself were better suited to external reporting, at present the financial community itself shows little inter-est in making the change from financial to strategic reporting. One company president

has found the outside financial community leery of the principles that ground the score-card: “We use the scorecard more with our customers than with our investors. The fi-nancial community is skeptical about long-term indicators and occasionally tells us about some empirical evidence of a nega-tive correlation between stock prices and at-tention to total quality and internal pro-cesses.”

However, the investment community has begun to focus on some key metrics of new product performance. Could this be an early sign of a shift to strategic thinking?

Putting the Balanced Scorecard to Work

harvard business review • september–october 1993 page 13

come the cornerstone of the management sys-tem at FMC. It enables us to translate businessunit strategies into a measurement system thatmeshes with our entire system of management.

For instance, one manager reported thatwhile his division had measured many operat-ing variables in the past, now, because of thescorecard, it had chosen 12 parameters as thekey to its strategy implementation. Seven ofthese strategic variables were entirely newmeasurements for the division. The managerinterpreted this finding as verifying whatmany other managers were reporting: thescorecard improved the understanding andconsistency of strategy implementation. An-other manager reported that, unlike monthlyfinancial statements or even his strategic plan,if a rival were to see his scorecard, he wouldlose his competitive edge.

It’s rare to get that much enthusiasm among di-visional managers for a corporate initiative. Whatled you and them to the balanced scorecard?

FMC had a clearly defined mission: to be-come our customers’ most valued supplier. Wehad initiated many of the popular improve-ment programs: total quality, managing by ob-jectives, organizational effectiveness, buildinga high-performance organization. But these ef-forts had not been effective. Every time wepromoted a new program, people in each divi-sion would sit back and ask, “How is that sup-posed to fit in with the six other things we’resupposed to be doing?’’

Corporate staff groups were perceived byoperating managers as pushing their pet pro-grams on divisions. The diversity of initia-tives, each with its own slogan, created con-fusion and mixed signals about where toconcentrate and how the various programsinterrelated. At the end of the day, with allthese new initiatives, we were still asking di-vision managers to deliver consistent short-term financial performance.

What kinds of measures were you using?

The FMC corporate executive team, likemost corporate offices, reviews the financialperformance of each operating divisionmonthly. As a highly diversified company thatredeploys assets from mature cash generatorsto divisions with significant growth opportuni-ties, the return-on-capital-employed (ROCE)measure was especially important for us. Wewere one of the few companies to inflation-ad-just our internal financial measures so that we

could get a more accurate picture of a divi-sion’s economic profitability.

At year-end, we rewarded division manag-ers who delivered predictable financial perfor-mance. We had run the company tightly forthe past 20 years and had been successful. Butit was becoming less clear where future growthwould come from and where the companyshould look for breakthroughs into new areas.We had become a high return-on-investmentcompany but had less potential for furthergrowth. It was also not at all clear from our fi-nancial reports what progress we were makingin implementing long-term initiatives. Ques-tions from the corporate office about spendingversus budget also reinforced a focus on theshort-term and on internal operations.

But the problem went even deeper thanthat. Think about it. What is the value addedof a corporate office that concentrates on mak-ing division managers accountable for finan-cial results that can be added up across divi-sions? We combine a business that’s doing wellwith a business that’s doing poorly and have atotal business that performs at an averagelevel. Why not split the company up into inde-pendent companies and let the market reallo-cate capital? If we were going to create valueby managing a group of diversified companies,we had to understand and provide strategicfocus to their operations. We had to be surethat each division had a strategy that wouldgive it sustainable competitive advantage. Inaddition, we had to be able to assess, throughmeasurement of their operations, whether ornot the divisions were meeting their strategicobjectives.

If you’re going to ask a division or the cor-poration to change its strategy, you had betterchange the system of measurement to be con-sistent with the new strategy.

How did the balanced scorecard emerge asthe remedy to the limitations of measuring onlyshort-term financial results?

In early 1992, we assembled a task force tointegrate our various corporate initiatives. Wewanted to understand what had to be done dif-ferently to achieve dramatic improvements inoverall organizational effectiveness. We ac-knowledged that the company may have be-come too short-term and too internally fo-cused in its business measures. Defining whatshould replace the financial focus was moredifficult. We wanted managers to sustain their

“The diversity of

initiatives, each with its

own slogan, created

confusion and mixed

signals.”

Putting the Balanced Scorecard to Work

harvard business review • september–october 1993 page 14

search for continuous improvement, but wealso wanted them to identify the opportunitiesfor breakthrough performance.

When divisions missed financial targets, thereasons were generally not internal. Typically,division management had inaccurately esti-mated market demands or had failed to fore-cast competitive reactions. A new measure-ment system was needed to lead operatingmanagers beyond achieving internal goals tosearching for competitive breakthroughs inthe global marketplace. The system wouldhave to focus on measures of customer service,market position, and new products that couldgenerate long-term value for the business. Weused the scorecard as the focal point for thediscussion. It forced division managers to an-swer these questions: How do we become ourcustomers’ most valued supplier? How do webecome more externally focused? What is mydivision’s competitive advantage? What is itscompetitive vulnerability?

How did you launch the scorecard effort atFMC?

We decided to try a pilot program. We se-lected six division managers to develop proto-type scorecards for their operations. Each divi-sion had to perform a strategic analysis toidentify its sources of competitive advantage.The 15 to 20 measures in the balanced score-card had to be organization-specific and had tocommunicate clearly what short-term mea-sures of operating performance were consis-tent with a long-term trajectory of strategicsuccess.

Were the six division managers free to developtheir own scorecard?

We definitely wanted the division managersto perform their own strategic analysis and todevelop their own measures. That was an es-sential part of creating a consensus betweensenior and divisional management on operat-ing objectives. Senior management did, how-ever, place some conditions on the outcomes.

First of all, we wanted the measures to beobjective and quantifiable. Division managerswere to be just as accountable for improvingscorecard measures as they had been for usingmonthly financial reviews. Second, we wantedoutput measures not process-oriented mea-sures. Many of the improvement programsunder way were emphasizing time, quality,and cost measurements. Focusing on T-Q-Cmeasurements, however, encourages manag-

ers to seek narrow process improvements in-stead of breakthrough output targets. Focus-ing on achieving outputs forces divisionmanagers to understand their industry andstrategy and help them to quantify strategicsuccess through specific output targets.

Could you illustrate the distinction betweenprocess measures and output measures?

You have to understand your industry wellto develop the connection between process im-provements and outputs achieved. Take threedivisional examples of cycle-time measure-ment, a common process measure.

For much of our defense business, no pre-mium is earned for early delivery. And the con-tracts allow for reimbursement of inventoryholding costs. Therefore, attempts to reduceinventory or cycle times in this business pro-duce no benefit for which the customer is will-ing to pay. The only benefits from cycle timeor inventory reduction occur when reductionin factory-floor complexity leads to real reduc-tions in product cost. The output performancetargets must be real cash savings, not reducedinventory levels or cycle times.

In contrast, significant lead-time reductionscould be achieved for our packaging machin-ery business. This improvement led to lowerinventory and an option to access an addi-tional 35% of the market. In this case, thecycle-time improvements could be tied to spe-cific targets for increased sales and marketshare. It wasn’t linear, but output seemed toimprove each time we improved throughputtimes.

And in one of our agricultural machinerybusinesses, orders come within a narrow timewindow each year. The current build cycle islonger than the ordering window, so all unitsmust be built to the sales forecast. This processof building to forecast leads to high inven-tory—more than twice the levels of our otherbusinesses—and frequent overstocking and ob-solescence of equipment. Incremental reduc-tions in lead time do little to change the eco-nomics of this operation. But if the build cycletime could be reduced to less than the six-weekordering time window for part or all of thebuild schedule, then a breakthrough occurs.The division can shift to a build-to-order sched-ule and eliminate the excess inventory causedby building to forecasts. In this case, the bene-fit from cycle-time reductions is a step-func-tion that comes only when the cycle time

“If you’re going to ask a

division or the

corporation to change its

strategy, you had better

change the system of

measurement.”

Putting the Balanced Scorecard to Work

harvard business review • september–october 1993 page 15

drops below a critical level.So here we have three businesses, three dif-

ferent processes, all of which could have elabo-rate systems for measuring quality, cost, andtime but would feel the impact of improve-ments in radically different ways. With all thediversity in our business units, senior manage-ment really can’t have a detailed understand-ing of the relative impact of time and qualityimprovements on each unit. All of our seniormanagers, however, understand output tar-gets, particularly when they are displayed withhistorical trends and future targets.

Benchmarking has become popular with a lotof companies. Does it tie in to the balanced score-card measurements?

Unfortunately, benchmarking is one ofthose initially good ideas that has turned into afad. About 95% of those companies that havetried benchmarking have spent a lot of moneyand have gotten very little in return. And thedifference between benchmarking and thescorecard helps reinforce the difference be-tween process measures and output measures.It’s a lot easier to benchmark a process than tobenchmark an output. With the scorecard, weask each division manager to go outside theirorganization and determine the approachesthat will allow achievement of their long-termoutput targets. Each of our output measureshas an associated long-term target. We havebeen deliberately vague on specifying whenthe target is to be accomplished. We want tostimulate a thought process about how to dothings differently to achieve the target ratherthan how to do existing things better. The ac-tivity of searching externally for how othershave accomplished these breakthroughachievements is called target verification notbenchmarking.

Were the division managers able to developsuch output-oriented measures?

Well, the division managers did encountersome obstacles. Because of the emphasis onoutput measures and the previous focus on op-erations and financial measures, the customerand innovation perspectives proved the mostdifficult. These were also the two areas wherethe balanced scorecard process was most help-ful in refining and understanding our existingstrategies.

But the initial problem was that the man-agement teams ran afoul of both conditions:the measures they proposed tended to be non-

quantifiable and input- rather than output-oriented. Several divisions wanted to conductcustomer surveys and provide an index of theresults. We judged a single index to be of littlevalue and opted instead for harder measuressuch as price premiums over competitors.

We did conclude, however, that the full cus-tomer survey was an excellent vehicle for pro-moting external focus and, therefore, decidedto use survey results to kick-off discussion atour annual operating reviews.

Did you encounter any problems as youlaunched the six pilot projects?

At first, several divisional managers wereless than enthusiastic about the additionalfreedom they were being given from head-quarters. They knew that the heightened visi-bility and transparency of the scorecard tookaway the internal trade-offs they had gainedexperience in making. They initially inter-preted the increase in visibility of divisionalperformance as just the latest attempt by cor-porate staff to meddle in their internal busi-ness processes.

To offset this concern, we designed targetsaround long-term objectives. We still closelyexamine the monthly and quarterly statistics,but these statistics now relate to progress inachieving long-term objectives and justify theproper balance between short-term and long-term performance.

We also wanted to transfer quickly thefocus from a measurement system to achiev-ing performance results. A measurement ori-entation reinforces concerns about control anda short-term focus. By emphasizing targetsrather than measurements, we could demon-strate our purpose to achieve breakthroughperformance.

But the process was not easy. One divisionmanager described his own three-stage imple-mentation process after receiving our directiveto build a balanced scorecard: denial—hope itgoes away; medicinal—it won’t go away, solet’s do it quickly and get it over with; owner-ship—let’s do it for ourselves.

In the end, we were successful. We nowhave six converts who are helping us to spreadthe message throughout the organization.

I understand that you have started to applythe scorecard not just to operating units but tostaff groups as well.

Applying the scorecard approach to staffgroups has been even more eye-opening than

“I see the scorecard as a

strategic measurement

system, not a measure of

our strategy.”

Putting the Balanced Scorecard to Work

harvard business review • september–october 1993 page 16

our initial work with the six operating divi-sions. We have done very little to define ourstrategy for corporate staff utilization. I doubtthat many companies can respond crisply tothe question, “How does staff provide competi-tive advantage?’’ Yet we ask that questionevery day about our line operations. We havejust started to ask our staff departments to ex-plain to us whether they are offering low costor differentiated services. If they are offeringneither, we should probably outsource thefunction. This area is loaded with real poten-tial for organizational development and im-proved strategic capability.

My conversations with financial people in or-ganizations reveal some concern about the ex-panded responsibilities implied by developingand maintaining a balanced scorecard. Howdoes the role of the controller change as a com-pany shifts its primary measurement system froma purely financial one to the balanced scorecard?

Historically, we have had two corporate de-partments involved in overseeing business unitperformance. Corporate development was incharge of strategy, and the controller’s officekept the historical records and budgeted andmeasured short-term performance. Strategistscame up with five- and ten-year plans, control-lers one-year budgets and near-term forecasts.Little interplay occurred between the twogroups. But the scorecard now bridges the two.The financial perspective builds on the tradi-tional function performed by controllers. Theother three perspectives make the division’slong-term strategic objectives measurable.

In our old environment, division managerstried to balance short-term profits with long-term growth, while they were receiving differ-ent signals depending on whether or not theywere reviewing strategic plans or budgets. Thisstructure did not make the balancing of short-term profits and long-term growth an easytrade-off, and, frankly, it let senior manage-ment off the hook when it came to sharing re-sponsibility for making the trade-offs.

Perhaps the corporate controller shouldtake responsibility for all measurement andgoal setting, including the systems required toimplement these processes. The new corporatecontroller could be an outstanding system ad-ministrator, knowledgeable about the varioustrade-offs and balances, and skillful in report-ing and presenting them. This role does noteliminate the need for strategic planning. It

just makes the two systems more compatible.The scorecard can serve to motivate and evalu-ate performance. But I see its primary value asits ability to join together what had beenstrong but separated capabilities in strategy de-velopment and financial control. It’s the oper-ating performance bridge that corporationshave never had.

How often do you envision reviewing a divi-sion’s balanced scorecard?

I think we will ask group managers to re-view a monthly submission from each of theirdivisions, but the senior corporate team willprobably review scorecards quarterly on a ro-tating basis so that we can review up to sevenor eight division scorecards each month.

Isn’t it inconsistent to assess a division’s strat-egy on a monthly or quarterly basis? Doesn’t sucha review emphasize short-term performance?

I see the scorecard as a strategic measure-ment system, not a measure of our strategy.And I think that’s an important distinction.The monthly or quarterly scorecard measuresoperations that have been configured to beconsistent with our long-term strategy.

Here’s an example of the interaction be-tween the short and the long term. We havepushed division managers to choose measuresthat will require them to create change, for ex-ample, penetration of key markets in whichwe are not currently represented. We can mea-sure that penetration monthly and get valu-able short-term information about the ulti-mate success of our long-term strategy. Ofcourse, some measures, such as annual marketshare and innovation metrics, don’t lendthemselves to monthly updates. For themost part, however, the measures are calcu-lated monthly.

Any final thoughts on the scorecard?

I think that it’s important for companiesnot to approach the scorecard as the latest fad.I sense that a number of companies are turn-ing to scorecards in the same way they turnedto total quality management, high-perfor-mance organization, and so on. You hearabout a good idea, several people on corporatestaff work on it, probably with some expensiveoutside consultants, and you put in a systemthat’s a bit different from what existed before.Such systems are only incremental, and youdon’t gain much additional value from them.

It gets worse if you think of the scorecard asa new measurement system that eventually re-

Putting the Balanced Scorecard to Work

harvard business review • september–october 1993 page 17

quires hundreds and thousands of measure-ments and a big, expensive executive informa-tion system. These companies lose sight of theessence of the scorecard: its focus, its simplic-ity, and its vision. The real benefit comes frommaking the scorecard the cornerstone of theway you run the business. It should be the coreof the management system, not the measure-ment system. Senior managers alone will de-termine whether the scorecard becomes a

mere record-keeping exercise or the lever tostreamline and focus strategy that can lead tobreakthrough performance.

Reprint 93505;

Harvard Business Review

OnPoint 4118

To order, see the next pageor call 800-988-0886 or 617-783-7500or go to www.hbr.org

Putting the Balanced Scorecard to Work

To Order

For reprints, Harvard Business Review OnPoint orders, and subscriptions to Harvard Business Review:Call 800-988-0886 or 617-783-7500.Go to www.hbr.org

For customized and quantity orders of reprints and Harvard Business Review OnPoint products:Call Frank Tamoshunas at 617-783-7626, or e-mail him at [email protected]

page 18

Further ReadingA R T I C L E SThe Balanced Scorecard: Measures That Drive Performanceby Robert S. Kaplan and David P. NortonHarvard Business ReviewJanuary–February 1992Product no. 4096

This article introduced the concept of a bal-anced scorecard to Harvard Business Review readers. Traditional performance measure-ment systems focus on control, the authors argue—for example, measuring the number of widgets produced against the number budgeted. But a balanced scorecard approach to performance focuses on vision and strat-egy. It provides a comprehensive snapshot of a business by combining financial measures with metrics for customer satisfaction, key in-ternal processes, and organizational learning and growth.

Using the Balanced Scorecard as a Strategic Management Systemby Robert S. Kaplan and David P. NortonHarvard Business ReviewJanuary–February 1996Product no. 4126

Traditional management systems that rely heavily on financial metrics are typically un-able to link a company’s long-term strategy with its short-term actions. In their third Har-vard Business Review article about the bal-anced scorecard, Kaplan and Norton demon-strate how the scorecard helps a company clarify and update strategy, communicate that strategy throughout the company, align unit and individual goals with the strategy, link strategic objectives to long-term targets and annual budgets, and conduct periodic perfor-mance reviews to improve the strategy. In es-sence, a balanced scorecard functions best as the cornerstone of a strategic management system.

The Performance Measurement Manifestoby Robert G. EcclesHarvard Business ReviewJanuary–February 1991Product no. 91103

Eccles’s main contention echoes that of Ka-plan and Norton: the leading indicators of business performance cannot be found in fi-nancial data alone. More and more managers are changing their company’s performance measurement systems to track nonfinancial measures and reinforce new competitive strategies. Five activities are essential, writes the author: developing an information archi-tecture; putting the technology in place to support this architecture; aligning bonuses and other new incentives with the system; drawing on outside resources; and designing an internal process to ensure that the other four activities occur.

B O O KThe Balanced Scorecard: Translating Strategy into Actionby Robert S. Kaplan and David P. NortonHarvard Business School Press1996Product no. 6513

Developing and using a balanced scorecard helps executives solve what is perhaps their most central issue: how to implement strat-egy, particularly one that requires radical change. This book builds on the authors’ three Harvard Business Review articles, providing ad-ditional insight into the mechanics of choos-ing measures for each of the four scorecard perspectives. Extended examples from indus-tries such as oil, banking, insurance, and retail-ing demonstrate how companies have built scorecards tailored to their particular compet-itive challenges and strategic goals.

2nd article from the collection: Focusing Your Organization on Strategy—with the Balanced Score-card, 2nd Edition

page 19

Measuring the Strategic Readiness of Intangible Assets

by Robert S. Kaplan and David P. Norton

Included with this full-text Harvard Business Review article:

The Idea in Brief—the core idea

The Idea in Practice—putting the idea to work

20 Article Summary

21 Measuring the Strategic Readiness of Intangible Assets

A list of related materials, with annotations to guide further

exploration of the article’s ideas and applications

34 Further Reading

Product 5887

Measuring the Strategic Readiness of Intangible

Assets

page 20

The Idea in Brief The Idea in Practice

CO

PYR

IGH

T ©

200

4 H

AR

VA

RD

BU

SIN

ESS

SC

HO

OL

PU

BLI

SHIN

G C

OR

PO

RA

TIO

N. A

LL R

IGH

TS

RE

SER

VE

D.

You’ve formulated a sound strategy—but can you execute it? To answer that, mea-sure the strategic readiness of your intan-gible assets: how well your employees’ skills, your information and technical sys-tems, and your leadership and organiza-tional culture align with your strategy.

But how do you measure this alignment? Using Balanced Scorecard assessment tools, determine how strongly your intangi-ble assets enhance the processes—creat-ing, producing, and delivering valuable of-ferings to customers—that generate the revenue needed to meet your long-term fi-nancial goals.

When you measure your intangible assets’ alignment with your strategy, you more easily see ways to improve each asset’s alignment. For example:

• Strengthen skills of employees in the most strategically critical jobs—rather than all employees.

• Put the right technical systems in place (customer databases, knowledge man-agement systems) to execute your strat-egy.

• Cultivate exceptional leaders and a cohe-sive workforce committed to sharing knowledge and achieving strategic goals.

By assessing and then enhancing the align-ment of your company’s human, informa-tion, and organizational capital, you un-leash those intangible assets’ full power.

To measure your intangible assets’ strategic readiness, determine what human, informa-tion, and organizational capital your company needs to perform the internal processes most critical to your strategy. Then assess your cur-rent capabilities in all three areas. Finally, iden-tify and address gaps.

HUMAN CAPITAL

Certain jobs have a particularly significant im-pact on your organization’s ability to perform the processes most critical to your strategy. These strategic job families often employ less than 10% of a company’s workforce. Identify the strategic job families in your company, then list the knowledge and skills employees in those job families require. Watch for gaps between employees’ required and current ca-pabilities.

Example:Consumer Bank shifted its strategy from promoting individual products to offering customers one-stop financial-solutions shopping. For its critical internal process “cross-sell the product line,” financial plan-ning was the most crucial job—which re-quired solution selling, relationship man-agement, and other fundamental skills.

The bank estimated it needed 100 skilled fi-nancial planners for effective cross-selling. But assessments revealed only 40 proficient planners. The bank knew where to invest to improve its human capital’s strategic readi-ness.

INFORMATION CAPITAL

To gauge how well your information capital (IC) supports your organization’s strategy, identify the IT systems needed to support each critical internal process. These may in-clude infrastructure (central servers, commu-nication networks), software applications, and managerial expertise (standards, disaster plan-ning, security).

Determine whether needed systems:

• are available and operating normally

• have been identified and funded but aren’t installed or operational

• have been identified but not funded

To get the fullest picture of your IC readiness, combine these qualitative assessments with quantitative ones—such as user-satisfaction surveys and analyses of IT operations and maintenance costs.

ORGANIZATIONAL CAPITAL

To measure your organizational capital’s (OC) readiness, ask these questions:

• Culture: Which corporate-wide and unit-specific behaviors and attitudes (for exam-ple, commitment to customer satisfaction, respect, innovativeness) does executing your strategy require?

• Leadership: What competencies (ability to inculcate specific values or encourage teamwork and accountability) do your firm’s leaders need to implement strategy?

• Alignment: What communications (town meetings, training programs) and incen-tives (rewards for meeting personal and corporate targets) would help employees understand the strategy and their roles in supporting it?

• Teamwork and knowledge sharing: What must you do to encourage employees to share their ideas and knowledge with oth-ers? What formal knowledge management systems would help?

Measuring the Strategic Readiness of Intangible Assets

by Robert S. Kaplan and David P. Norton

harvard business review • february 2004 page 21

CO

PYR

IGH

T ©

200

4 H

AR

VA

RD

BU

SIN

ESS

SC

HO

OL

PU

BLI

SHIN

G C

OR

PO

RA

TIO

N. A

LL R

IGH

TS

RE

SER

VE

D.

A real—and revolutionary—opportunity lies in studying and

assessing how well prepared a company’s people, systems, and culture

are to carry out its strategy.

How valuable is a company culture that en-ables employees to understand and believe intheir organization’s mission, vision, and corevalues? What’s the payoff from investing in aknowledge management system or in a newcustomer database? Is it more important toimprove the skills of all employees or focus onthose in just a few key positions?

Measuring the value of such intangible as-sets is the holy grail of accounting. Employees’skills, IT systems, and organizational culturesare worth far more to many companies thantheir tangible assets. Unlike financial and phys-ical ones, intangible assets are hard for com-petitors to imitate, which makes them a pow-erful source of sustainable competitiveadvantage. If managers could find a way to es-timate the value of their intangible assets, theycould measure and manage their company’scompetitive position much more easily and ac-curately.

But that’s simpler said than done. Unlike fi-nancial and physical assets, intangible assetsare worth different things to different people.

An oil well, for example, is almost as valuableto a retail firm as it is to an oil exploration cor-poration because either company could sell itswiftly if necessary. But a workforce with astrong sense of customer service and satisfac-tion is worth far more to the retailer than itwould be to the oil company. Also, unlike tan-gible assets, intangible assets almost never cre-ate value by themselves. They need to be com-bined with other assets. Investments in IT, forexample, have little value unless comple-mented with HR training and incentive pro-grams. And, conversely, many HR training pro-grams have little value unless complementedwith modern technology tools. HR and IT in-vestments must be integrated and aligned withcorporate strategy if the organization is to real-ize their full potential. Indeed, when compa-nies separate functions like HR and IT organi-zationally, they usually end up with competingsilos of technical specialization. The HR de-partment argues for increases in employeetraining, while the IT department lobbies forbuying new hardware and software packages.

Measuring the Strategic Readiness of Intangible Assets

harvard business review • february 2004 page 22

What’s more, intangible assets seldom af-fect financial performance directly. Instead,they work indirectly through complex chainsof cause and effect. Training employees inTotal Quality Management and Six Sigma, forinstance, should improve process quality. Thatimprovement should then increase customersatisfaction and loyalty—and also create someexcess resource capacity. But only if the com-pany can transform that loyalty into improvedsales and margins and eliminate or redeploythe excess resources will the investment intraining pay off. By contrast, the impact of anew tangible asset is immediate: When a re-tailer develops a new site, it sees financial ben-efits from the sales in the newly opened outletright away.

Although these characteristics make it im-possible to value intangible assets on a free-standing basis, they also point the way to anew approach for quantifying how intangibleassets add value to the company. By under-standing the problems associated with valuingintangible assets, we learn that the measure-ment of the value they create is embedded inthe context of the strategy the company is pur-suing. Companies such as Dell, Wal-Mart, orMcDonald’s that are following a low-cost strat-egy derive value from Six Sigma and TQMtraining because their strategies are predicatedon continuous process improvement. Thestrategy of offering customers integrated solu-tions (rather than discrete products) pursuedby Goldman Sachs, IBM Consulting, and thelike requires employees good at establishingand maintaining long-term customer relation-ships. An organization cannot possibly assign ameaningful financial value to an intangibleasset like “a motivated and prepared work-force” in a vacuum because value can be de-rived only in the context of the strategy. Whatthe company can measure, however, iswhether its workforce is properly trained andmotivated to pursue a particular goal.

Viewed in this light, it becomes clear thatmeasuring the value of intangible assets is re-ally about estimating how closely alignedthose assets are to the company’s strategy. Ifthe company has a sound strategy and if the in-tangible assets are aligned with that strategy,then the assets will create value for the organi-zation. If the assets are not aligned with thestrategy or if the strategy is flawed, then intan-gible assets will create little value, even if large

amounts have been spent on them.In the following pages, we will draw on the

concepts and tools of the Balanced Scorecardto present a way to systematically measure thealignment of the company’s human, informa-tion, and organization capital—what we callits strategic readiness—without which even thebest strategy cannot succeed.

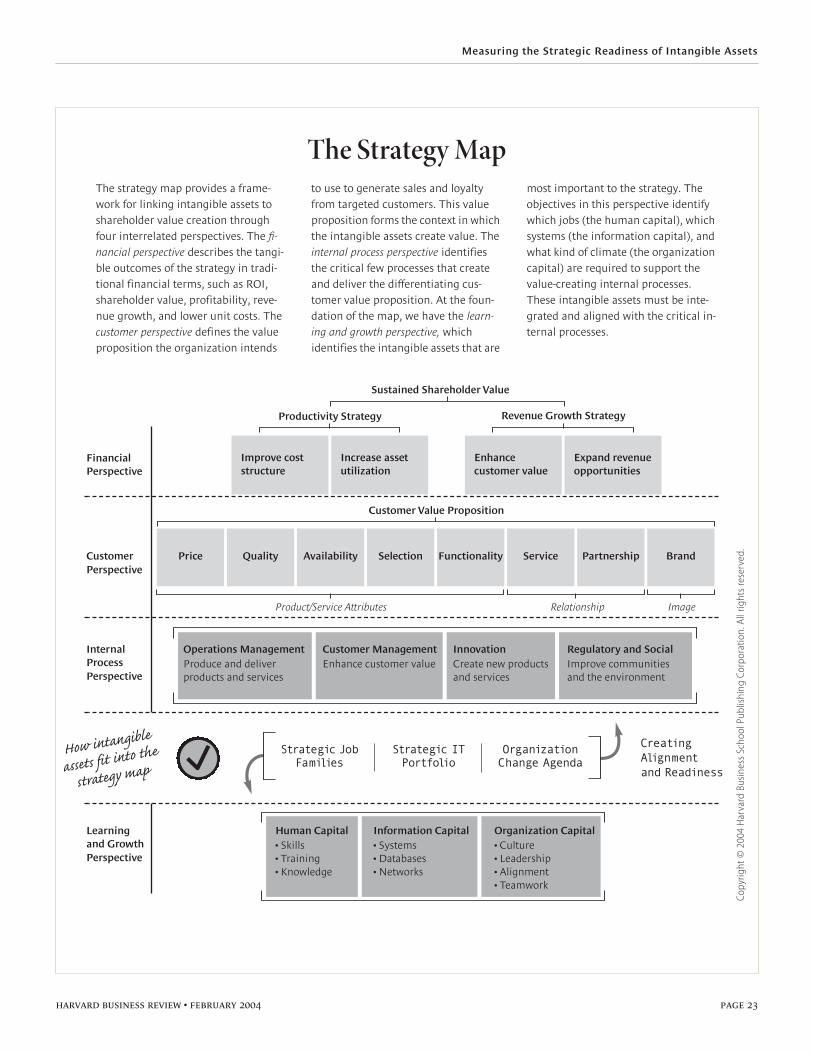

Defining Strategic ReadinessIn developing the Balanced Scorecard morethan a decade ago, we identified, in its Learn-ing and Growth Perspective, three categoriesof intangible assets essential for implement-ing any strategy:

• Human Capital: the skills, talent, andknowledge that a company’s employees pos-sess.

• Information Capital: the company’s data-bases, information systems, networks, andtechnology infrastructure.

• Organization Capital: the company’s cul-ture, its leadership, how aligned its people arewith its strategic goals, and employees’ abilityto share knowledge.

To link these intangible assets to a com-pany’s strategy and performance, we devel-oped a tool called the “strategy map,” whichwe first introduced in our previous article forHarvard Business Review, “Having Troublewith Your Strategy? Then Map It” (Septem-ber–October 2000). As the exhibit “The Strat-egy Map” shows, intangible assets influence acompany’s performance by enhancing the in-ternal processes most critical to creating valuefor customers and shareholders. Companiesbuild their strategy maps from the top down,starting with their long-term financial goalsand then determining the value propositionthat will deliver the revenue growth specifiedin those goals, identifying the processes mostcritical to creating and delivering that valueproposition, and, finally, determining the hu-man, information, and organization capitalthe processes require.