fixed index annuity – hedging and risk management arsen ... · equity-based insurance guarantees...

TRANSCRIPT

Equity-Based Insurance Guarantees Conference

Nov. 6-7, 2017

Baltimore, MD

Fixed Index Annuity – Hedging and Risk Management

Arsen Arutyunov, Pawel Konieczny

Sponsored by

Fixed Index Annuity –Hedging and Risk ManagementARSEN ARUTYUNOV, ASA

Session 2A: 1300 – 1530 hours

6 November 2017

PAWEL KONIECZNY, PHD, CFA, FRM

Agenda

• Introduction

• Industry survey• Background

• Common hedging practices

• Instrument exposure overview

• Closing remarks

2

INDUSTRY SURVEY

SURVEY BACKGROUND

• 12 companies contributed to the industry survey through an interview format, representing 65% of market share on FIA new sales

• Here are some key characteristics of the 12 participants:

• Most participants are ranked in LIMRAS top-20 list of highest annual FIA premium

• Most participants considered fixed index annuities (FIA) as their core product

• All individuals interviewed occupy a managerial role and oversee the hedging operation

• A total of 11 questions were asked around companies’ core hedging practice and strategies

4

5

CORE HEDGING STRATEGY

0%

5%

10%

15%

20%

25%

30%

0

1

2

3

4

5

6

7

StaticStaticStaticStatic Static w/Dynamic OverlayStatic w/Dynamic OverlayStatic w/Dynamic OverlayStatic w/Dynamic Overlay DynamicDynamicDynamicDynamic

% o

f M

ark

et

Sha

re%

of

Ma

rke

t Sh

are

% o

f M

ark

et

Sha

re%

of

Ma

rke

t Sh

are

Nu

mb

er

of

Pa

rtic

ipa

nts

Nu

mb

er

of

Pa

rtic

ipa

nts

Nu

mb

er

of

Pa

rtic

ipa

nts

Nu

mb

er

of

Pa

rtic

ipa

nts

Number of Companies % of Market Shares

RemarksRemarksRemarksRemarks

• The majority of participates deem static hedging with dynamic overlay as their core hedging strategies.

• Of the participants employing static with dynamic overlay strategy, a reported range of 50%-95% of issued account value (i.e. notional) are matched with a derivative of equivalent terms.

• On the contrary, some large FIA writers heavily utilize strictly static or pure dynamic hedging strategies for their FIA business.

DefinitionsDefinitionsDefinitionsDefinitions

StaticStaticStaticStatic: Under this strategy, the company will attempt to match the cash flows of issued liabilities (adjusted for expected decrements) with a derivative of equivalent terms.

Static with a Dynamic Overlay (DO)Static with a Dynamic Overlay (DO)Static with a Dynamic Overlay (DO)Static with a Dynamic Overlay (DO): Under this strategy, the company will match all issued liabilities (adjusted for expected decrements) up to a certain % of Account Value. The portfolio of liabilities and hedges is then rebalanced dynamically according to pre-defined Greeks.

DynamicDynamicDynamicDynamic: Under this strategy, the company will attempt to match the Greek profile of outstanding liabilities with offsetting hedge transactions.

FREQUENCY TO STRIKE AND HEDGE POLICIES

6

DefinitionsDefinitionsDefinitionsDefinitions

• Depending on the lag, the company will be exposed to basis risk due to the difference in the policy strike value and the hedge strike value.

• Of the participants who employ a dynamic component as part of their current strategy have admitted that they will rebalance their

exposure daily (or depending on predetermined limits). The lag component pertains to the static component of the core hedging strategy.

0

1

2

3

4

5

6

7

8

9

10

Daily Weekly Bi-Weekly

He

dge

Sch

ed

ule

He

dge

Sch

ed

ule

He

dge

Sch

ed

ule

He

dge

Sch

ed

ule

Strike FrequencyStrike FrequencyStrike FrequencyStrike Frequency

Same Day 1 Day Lag 1 Week Lag

Same day hedge scheduleSame day hedge scheduleSame day hedge scheduleSame day hedge schedule

• Majority of participants hedge on the same day as

they strike

• Clients with high daily volumes can employ a same

day hedge program to minimize basis risk

Lagged hedge scheduleLagged hedge scheduleLagged hedge scheduleLagged hedge schedule

• Participants who do not have a large trade volume

will tend to defer trading until enough exposure has

been accumulated to justify placing a hedge with a

counterparty

• Participants acknowledged that some basis risk

exists when employing a lag, but have deemed the

risk to be unbiased

COMPOSITES OF HEDGE PORTFOLIO

7

RemarksRemarksRemarksRemarks

• All participants leveraged OTC derivatives as part of their hedging programs

• Participants who have a large dynamic component as part of their strategy mentioned that they utilize

listed options to manage their near term exposure

• Equity futures are favored for dynamic hedgers to manage residual exposures

0

2

4

6

8

10

12

14

OTCOTCOTCOTC Equity FuturesEquity FuturesEquity FuturesEquity Futures Listed OptionsListed OptionsListed OptionsListed Options FLEX OptionsFLEX OptionsFLEX OptionsFLEX Options OtherOtherOtherOther

Nu

mb

er

of

Pa

rtic

ipa

nts

Nu

mb

er

of

Pa

rtic

ipa

nts

Nu

mb

er

of

Pa

rtic

ipa

nts

Nu

mb

er

of

Pa

rtic

ipa

nts

17%

42%

25%

8%

8%

Numbers of Derivative CategoriesNumbers of Derivative CategoriesNumbers of Derivative CategoriesNumbers of Derivative Categories

1

2

3

4

5

ADJUSTMENTS TO HEDGE TARGETS

FOR LIVING BENEFIT RIDERS

8

RemarksRemarksRemarksRemarks

Participants who are making an adjustment cited the following reasons:

• More accurate view of the forward liability.

Participants who are not making an adjustment, mentioned that they are currently not actively monitoring the

market risk / sensitivity of the living benefits offered on the base contract.

• Most participants agreed that taking a proactive approach to measuring this exposure is on their “to-do”

list

25%

75%

Are you incorporating the living benefit premium in the expected decrement value

used to derive the hedge value?

Yes

No

9

17%

83%

Yes No

UNHEDGED LIABILITIES

DefinitionsDefinitionsDefinitionsDefinitions

YesYesYesYes: Depending on the materiality of a given liability cohort, the company may leave this cohort or certain risks of the cohort unhedged

No: No: No: No: All liability cohorts are categorized into similar risk groups and hedged

RemarksRemarksRemarksRemarks

• Common rationale for leaving a particular cohort unhedged was due to cost and low liquidity associated with placing a hedge.

• In all cases when respondents who decided to leave a cohort unhedged mentioned that their companies’ macro-hedge program would eventually account for any residual risk left by the outstanding cohort.

• Mark-to-market valuations are done to determine the current exposure of any residual/unhedged risks.

• All participants commented that in instances when hedges cannot be grouped is similar risk, some form of cross-hedging was performed.

RISK METRICS

10

RemarksRemarksRemarksRemarks

• Most common risk metrics observed are: Greek sensitivity and mismatch & mark-to-market value of

liabilities and hedges.

• A common focus across all participants on their Greek exposure is inline with the overall trend observed

to employ a more dynamic strategy.

• Few participants mentioned that they utilize VaR to measure their tail exposure, and depending if limits

are breach will take action to rebalance their position.

0

2

4

6

8

10

12

MtM GreeksMtM GreeksMtM GreeksMtM Greeks MtM ValueMtM ValueMtM ValueMtM Value Stress TestsStress TestsStress TestsStress Tests PnLPnLPnLPnL VaRVaRVaRVaR

Nu

me

rix

of

Pa

rtic

ipan

tsN

um

eri

x o

f P

art

icip

ants

Nu

me

rix

of

Pa

rtic

ipan

tsN

um

eri

x o

f P

art

icip

ants

42%

8%

17%

25%

8%

Number of Risk MetricsNumber of Risk MetricsNumber of Risk MetricsNumber of Risk Metrics

2

1

5

3

4

OTHER KEY TOPICS SURVEYED

11

RemarksRemarksRemarksRemarks.

• Most respondents employ a reactive approach to set

rates based on current prevailing / most recently

known dealer quotes.

• Others utilize a proprietary model that will estimate

future option prices offered by dealers

0 1 2 3 4 5 6 7 8 9

PredictivePredictivePredictivePredictive

ReactiveReactiveReactiveReactive

Number of ParticipantsNumber of ParticipantsNumber of ParticipantsNumber of Participants

At a high level, which would best describe your

current approach for setting CAP and PAR rates

on newly issued policies?

RemarksRemarksRemarksRemarks

• Most participants are satisfied with their current

offering of hybrid indices.

• A few participants did respond that they would like

to offer more strategies that can add value to their

policyholders via a hybrid index.

• No participants seek to decrease offering to hybrid

indices.

IncreaseIncreaseIncreaseIncrease

33%33%33%33%

No ChangeNo ChangeNo ChangeNo Change

67%67%67%67%

DecreaseDecreaseDecreaseDecrease

0%0%0%0%

For the foreseeable future, are you looking to

increase or decrease your exposure to hybrid

indices?

HEDGING STRATEGY EVOLUTION TREND

12

RemarksRemarksRemarksRemarks

• Most participants expressed intentions or interests to move onto a more dynamic hedging approach

• to accommodate evolving product designs

• to improve hedging efficiency when prevailing dealer rates are deemed to be high

• One participant mentioned that they would like to focus more on managed strategies (e.g. smart beta) as a way of enhancing their portfolio

DefinitionsDefinitionsDefinitionsDefinitions

StaticStaticStaticStatic: Under this strategy, the company will attempt to match the cash flows of issued liabilities (adjusted for expected decrements) with a derivative of equivalent terms.

Static with a Dynamic OverlayStatic with a Dynamic OverlayStatic with a Dynamic OverlayStatic with a Dynamic Overlay: Under this strategy, the company will match all issued liabilities (adjusted for expected decrements) up to a certain % of Account Value. The portfolio of liabilities and hedges is then rebalanced dynamically according to pre-defined Greeks.

DynamicDynamicDynamicDynamic: Under this strategy, the company will attempt to match the Greek profile of outstanding liabilities with offsetting hedge transactions.

0 1 2 3 4 5 6 7

Static

Static w/ Dynamic Overlay

Dynamic

Number of ParticipantsNumber of ParticipantsNumber of ParticipantsNumber of Participants

More Dynamic No Change More Static

COMMON FIA HEDGE

INSTRUMENTS

14

ExampleExampleExampleExample

• Payoff definition:

• max (0, � − �)• Crediting methodologies hedged

• Annual Point-to-Point with a

participation rate

• Using a generic outer loop with daily

time-steps, simulate an ATM

European Call option with the

following terms:

• $1,000,000 in Notional

• 1yr term.

• Plot the Delta and Gamma values

across time for all scenarios.

ResultsResultsResultsResults

• Delta is strictly positive, and will grow

with the underlying.

• Gamma is strictly positive, can

become explosive when the option

approaches maturity and the spot

level is close the strike.

0

20000

40000

60000

80000

100000

120000

140000

6/3

0/2

01

7

7/1

2/2

01

7

7/2

1/2

01

7

8/1

/20

17

8/1

0/2

01

7

8/2

1/2

01

7

8/3

0/2

01

7

9/1

1/2

01

7

9/2

0/2

01

7

9/2

9/2

01

7

10

/10

/20

17

10

/19

/20

17

10

/30

/20

17

11

/8/2

01

7

11

/17

/20

17

11

/29

/20

17

12

/8/2

01

7

12

/19

/20

17

12

/29

/20

17

1/1

0/2

01

8

1/2

2/2

01

8

1/3

1/2

01

8

2/9

/20

18

2/2

1/2

01

8

3/2

/20

18

3/1

3/2

01

8

3/2

2/2

01

8

4/3

/20

18

4/1

2/2

01

8

4/2

3/2

01

8

5/2

/20

18

5/1

1/2

01

8

5/2

2/2

01

8

6/1

/20

18

6/1

2/2

01

8

Call – Delta Profile

0

10000

20000

30000

40000

50000

60000

70000

6/3

0/2

01

7

7/1

2/2

01

7

7/2

1/2

01

7

8/1

/20

17

8/1

0/2

01

7

8/2

1/2

01

7

8/3

0/2

01

7

9/1

1/2

01

7

9/2

0/2

01

7

9/2

9/2

01

7

10

/10

/20

17

10

/19

/20

17

10

/30

/20

17

11

/8/2

01

7

11

/17

/20

17

11

/29

/20

17

12

/8/2

01

7

12

/19

/20

17

12

/29

/20

17

1/1

0/2

01

8

1/2

2/2

01

8

1/3

1/2

01

8

2/9

/20

18

2/2

1/2

01

8

3/2

/20

18

3/1

3/2

01

8

3/2

2/2

01

8

4/3

/20

18

4/1

2/2

01

8

4/2

3/2

01

8

5/2

/20

18

5/1

1/2

01

8

5/2

2/2

01

8

6/1

/20

18

6/1

2/2

01

8

Call – Gamma Profile

EUROPEAN CALL

High positive gamma when spot

level approaches the strike at

maturity.

CALL SPREAD

15

ExampleExampleExampleExample

• Payoff definition

• max (0, min ���, ������

− 1 )• Crediting methodologies hedged

• Annual Point-to-Point with a

cap rate

• Using a generic outer loop with daily

time-steps, simulate a Call Spread

with the following terms:

• 7.25% CAP

• $1,000,000 in Notional

• 1yr term

• Plot the Delta and Gamma values

across time for all scenarios.

ResultsResultsResultsResults

• Call spread delta is again strictly

positive, and shows a more subdued

Delta profile.

• Call spread gamma can be explosive in

both positive and negative directions,

which can potentially make hedging

more difficult.

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

6/3

0/2

01

7

7/1

2/2

01

7

7/2

1/2

01

7

8/1

/20

17

8/1

0/2

01

7

8/2

1/2

01

7

8/3

0/2

01

7

9/1

1/2

01

7

9/2

0/2

01

7

9/2

9/2

01

7

10

/10

/20

17

10

/19

/20

17

10

/30

/20

17

11

/8/2

01

7

11

/17

/20

17

11

/29

/20

17

12

/8/2

01

7

12

/19

/20

17

12

/29

/20

17

1/1

0/2

01

8

1/2

2/2

01

8

1/3

1/2

01

8

2/9

/20

18

2/2

1/2

01

8

3/2

/20

18

3/1

3/2

01

8

3/2

2/2

01

8

4/3

/20

18

4/1

2/2

01

8

4/2

3/2

01

8

5/2

/20

18

5/1

1/2

01

8

5/2

2/2

01

8

6/1

/20

18

6/1

2/2

01

8

Call Spread – Delta Profile

-80000

-60000

-40000

-20000

0

20000

40000

60000

80000

6/3

0/2

01

7

7/1

2/2

01

7

7/2

1/2

01

7

8/1

/20

17

8/1

0/2

01

7

8/2

1/2

01

7

8/3

0/2

01

7

9/1

1/2

01

7

9/2

0/2

01

7

9/2

9/2

01

7

10

/10

/20

17

10

/19

/20

17

10

/30

/20

17

11

/8/2

01

7

11

/17

/20

17

11

/29

/20

17

12

/8/2

01

7

12

/19

/20

17

12

/29

/20

17

1/1

0/2

01

8

1/2

2/2

01

8

1/3

1/2

01

8

2/9

/20

18

2/2

1/2

01

8

3/2

/20

18

3/1

3/2

01

8

3/2

2/2

01

8

4/3

/20

18

4/1

2/2

01

8

4/2

3/2

01

8

5/2

/20

18

5/1

1/2

01

8

5/2

2/2

01

8

6/1

/20

18

6/1

2/2

01

8

Call Spread – Gamma Profile

High negative gamma when spot

level approaches the CAP at

maturity.

Delta is bounded, reaches

maximum when spot level is

between long leg and short leg.

High positive gamma when spot

level approaches strike of the long

leg at maturity.

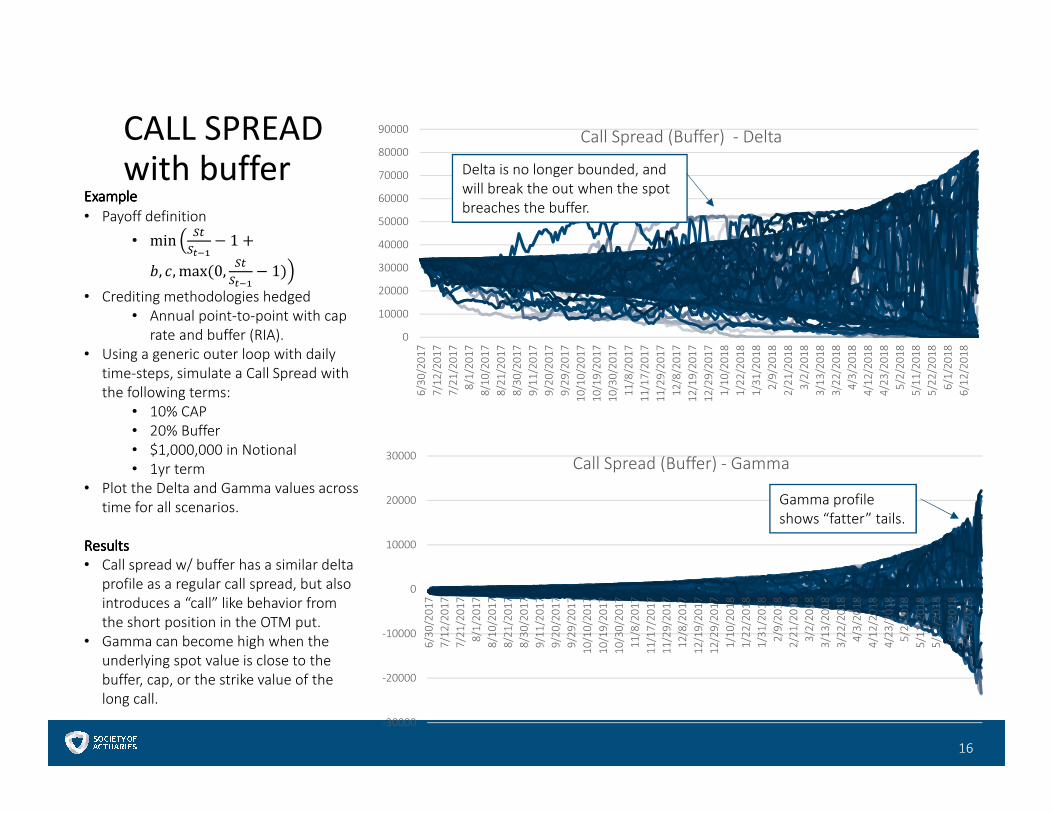

CALL SPREAD

with buffer

16

ExampleExampleExampleExample

• Payoff definition

• min � ������

− 1 +�, �, max (0, ��

����− 1)�

• Crediting methodologies hedged

• Annual point-to-point with cap

rate and buffer (RIA).

• Using a generic outer loop with daily

time-steps, simulate a Call Spread with

the following terms:

• 10% CAP

• 20% Buffer

• $1,000,000 in Notional

• 1yr term

• Plot the Delta and Gamma values across

time for all scenarios.

ResultsResultsResultsResults

• Call spread w/ buffer has a similar delta

profile as a regular call spread, but also

introduces a “call” like behavior from

the short position in the OTM put.

• Gamma can become high when the

underlying spot value is close to the

buffer, cap, or the strike value of the

long call.

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

6/3

0/2

01

7

7/1

2/2

01

7

7/2

1/2

01

7

8/1

/20

17

8/1

0/2

01

7

8/2

1/2

01

7

8/3

0/2

01

7

9/1

1/2

01

7

9/2

0/2

01

7

9/2

9/2

01

7

10

/10

/20

17

10

/19

/20

17

10

/30

/20

17

11

/8/2

01

7

11

/17

/20

17

11

/29

/20

17

12

/8/2

01

7

12

/19

/20

17

12

/29

/20

17

1/1

0/2

01

8

1/2

2/2

01

8

1/3

1/2

01

8

2/9

/20

18

2/2

1/2

01

8

3/2

/20

18

3/1

3/2

01

8

3/2

2/2

01

8

4/3

/20

18

4/1

2/2

01

8

4/2

3/2

01

8

5/2

/20

18

5/1

1/2

01

8

5/2

2/2

01

8

6/1

/20

18

6/1

2/2

01

8

Call Spread (Buffer) - Delta

Delta is no longer bounded, and

will break the out when the spot

breaches the buffer.

-30000

-20000

-10000

0

10000

20000

30000

6/3

0/2

01

7

7/1

2/2

01

7

7/2

1/2

01

7

8/1

/20

17

8/1

0/2

01

7

8/2

1/2

01

7

8/3

0/2

01

7

9/1

1/2

01

7

9/2

0/2

01

7

9/2

9/2

01

7

10

/10

/20

17

10

/19

/20

17

10

/30

/20

17

11

/8/2

01

7

11

/17

/20

17

11

/29

/20

17

12

/8/2

01

7

12

/19

/20

17

12

/29

/20

17

1/1

0/2

01

8

1/2

2/2

01

8

1/3

1/2

01

8

2/9

/20

18

2/2

1/2

01

8

3/2

/20

18

3/1

3/2

01

8

3/2

2/2

01

8

4/3

/20

18

4/1

2/2

01

8

4/2

3/2

01

8

5/2

/20

18

5/1

1/2

01

8

5/2

2/2

01

8

6/1

/20

18

6/1

2/2

01

8

Call Spread (Buffer) - Gamma

Gamma profile

shows “fatter” tails.

ASIAN OPTION

17

ExampleExampleExampleExample

• Payoff definition:

• max (0, ∑ ���� − �)

• Crediting methodologies hedged

• Monthly averaging

• Using a generic outer loop with daily

time-steps, simulate a Asian option

using following terms:

• $1,000,000 in Notional

• 1yr term

• Fixed strike & arithmetic mean

• Plot the Delta and Gamma values

across time for all scenarios.

ResultsResultsResultsResults

• A natural property of an averaging

option is that it’s price becomes more

certain through passage of time.

• Delta and Gamma profiles both reflect

the price stability that this option

exhibits leading up to maturity.

0

2000

4000

6000

8000

10000

12000

14000

6/3

0/2

01

7

7/1

2/2

01

7

7/2

1/2

01

7

8/1

/20

17

8/1

0/2

01

7

8/2

1/2

01

7

8/3

0/2

01

7

9/1

1/2

01

7

9/2

0/2

01

7

9/2

9/2

01

7

10

/10

/20

17

10

/19

/20

17

10

/30

/20

17

11

/8/2

01

7

11

/17

/20

17

11

/29

/20

17

12

/8/2

01

7

12

/19

/20

17

12

/29

/20

17

1/1

0/2

01

8

1/2

2/2

01

8

1/3

1/2

01

8

2/9

/20

18

2/2

1/2

01

8

3/2

/20

18

3/1

3/2

01

8

3/2

2/2

01

8

4/3

/20

18

4/1

2/2

01

8

4/2

3/2

01

8

5/2

/20

18

5/1

1/2

01

8

5/2

2/2

01

8

6/1

/20

18

6/1

2/2

01

8

Asian - Delta

0

200

400

600

800

1000

1200

6/3

0/2

01

7

7/1

2/2

01

7

7/2

1/2

01

7

8/1

/20

17

8/1

0/2

01

7

8/2

1/2

01

7

8/3

0/2

01

7

9/1

1/2

01

7

9/2

0/2

01

7

9/2

9/2

01

7

10

/10

/20

17

10

/19

/20

17

10

/30

/20

17

11

/8/2

01

7

11

/17

/20

17

11

/29

/20

17

12

/8/2

01

7

12

/19

/20

17

12

/29

/20

17

1/1

0/2

01

8

1/2

2/2

01

8

1/3

1/2

01

8

2/9

/20

18

2/2

1/2

01

8

3/2

/20

18

3/1

3/2

01

8

3/2

2/2

01

8

4/3

/20

18

4/1

2/2

01

8

4/2

3/2

01

8

5/2

/20

18

5/1

1/2

01

8

5/2

2/2

01

8

6/1

/20

18

6/1

2/2

01

8

Asian - GammaDelta decays as the option

approaches maturity.

CLIQUET

18

ExampleExampleExampleExample

• Payoff definition

• max (0, ∑ min (���, ������

− 1)) !

• Crediting methodologies hedged

• Monthly sum cap

• Using a generic outer loop with daily

time-steps, simulate a Cliquet with

the following terms:

• 2% local CAP

• 0% global floor

• $1,000,000 in Notional

• 1yr term

• Monthly resets

• Plot the Delta and Gamma values

across time for all scenarios.

ResultsResultsResultsResults

• Cliquet delta profile shows a similar

diffusion as the call spread, with

maximum delta value peaking around

reset dates.

• Cliquet gamma can be explosive,

change signs, which can potentially

make hedging more difficult.

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

6/3

0/2

01

7

7/1

2/2

01

7

7/2

1/2

01

7

8/1

/20

17

8/1

0/2

01

7

8/2

1/2

01

7

8/3

0/2

01

7

9/1

1/2

01

7

9/2

0/2

01

7

9/2

9/2

01

7

10

/10

/20

17

10

/19

/20

17

10

/30

/20

17

11

/8/2

01

7

11

/17

/20

17

11

/29

/20

17

12

/8/2

01

7

12

/19

/20

17

12

/29

/20

17

1/1

0/2

01

8

1/2

2/2

01

8

1/3

1/2

01

8

2/9

/20

18

2/2

1/2

01

8

3/2

/20

18

3/1

3/2

01

8

3/2

2/2

01

8

4/3

/20

18

4/1

2/2

01

8

4/2

3/2

01

8

5/2

/20

18

5/1

1/2

01

8

5/2

2/2

01

8

6/1

/20

18

6/1

2/2

01

8

Cliquet - Delta

-4000

-3000

-2000

-1000

0

1000

2000

3000

6/3

0/2

01

7

7/1

2/2

01

7

7/2

1/2

01

7

8/1

/20

17

8/1

0/2

01

7

8/2

1/2

01

7

8/3

0/2

01

7

9/1

1/2

01

7

9/2

0/2

01

7

9/2

9/2

01

7

10

/10

/20

17

10

/19

/20

17

10

/30

/20

17

11

/8/2

01

7

11

/17

/20

17

11

/29

/20

17

12

/8/2

01

7

12

/19

/20

17

12

/29

/20

17

1/1

0/2

01

8

1/2

2/2

01

8

1/3

1/2

01

8

2/9

/20

18

2/2

1/2

01

8

3/2

/20

18

3/1

3/2

01

8

3/2

2/2

01

8

4/3

/20

18

4/1

2/2

01

8

4/2

3/2

01

8

5/2

/20

18

5/1

1/2

01

8

5/2

2/2

01

8

6/1

/20

18

6/1

2/2

01

8

Cliquet - Gamma

Delta can become explosive

before reset dates.

High negative gamma is also seen

around resets.

Q&A