fixed asset inventory system - west virginia …wvde.state.wv.us/finance/manuals/famanrr.pdf · an...

TRANSCRIPT

PROCEDURES MANUAL

FIXED ASSET INVENTORY SYSTEM

FOR COUNTY BOARDS OF EDUCATION

IN THE STATE OF WEST VIRGINIA

Office of School Finance

West Virginia Department of Education

PROCEDURES MANUAL

FIXED ASSET INVENTORY SYSTEM

FOR COUNTY BOARDS OF EDUCATION

IN THE STATE OF WEST VIRGINIA

Revised July 16, 2001

Copies may be obtained from:West Virginia Department of Education

Office of School FinanceBuilding 6, Room 215

1900 Kanawha Boulevard E.Charleston, West Virginia 25305

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

FOREWORD

Allocating, operating, and accounting for the physical assets of a school system are among themost important responsibilities of school administrators. Expenditures for fixed assets aregenerally the most visible costs a school district incurs. Yet, the accounting for such assets, onceacquired, has generally received little attention.

Implementation of a fixed asset inventory accounting system will enable local education agenciesto maintain an inventory of all assets, including those purchased with federal funds. In addition,the system will assist all agencies in obtaining an unqualified opinion on their audited financialstatements, and will assign responsibility and accountability for the security of fixed assets. Thesystem can also be used for purposes of insurance and proof of loss.

This manual has been developed by the West Virginia Department of Education in order toprovide uniform standards throughout the State for all county boards of education, regionaleducation service agencies, and multi-county vocational centers to use in developing a fixed assetinventory accounting system. The manual prescribes the minimum requirements that are to beencompassed in establishing such a system, and provides a list of the codes that are to be usedin classifying fixed assets.

The standards presented in this manual were developed by the Office of School Finance, inconsultation and cooperation with the Accounting Procedures Committee, various federal programadministrators at the Department of Education, and a number of other knowledgeable sources.Their dedicated work is greatly appreciated.

Sincerely,

David StewartState Superintendent of Schools

iTABLE OF CONTENTS

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

Page

I. Introduction 1

II. Requirements 2

III. Responsibilities 4

IV. Definitions 5

V. Accounting Policies 7

VI. Required Category, Classification and Description Codes 10

VII. Reporting Cycle 12

VIII. Tagging of Equipment 13

IX. Control of Assets 14

X. Annual Physical Inventory 16

Appendixes:

Appendix A - Optional Description Codes 17

Appendix B - Sample Forms 26

ii

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-1-

I. INTRODUCTION:

In recent years, government officials have come under increased pressure to demonstratethat they are properly fulfilling their stewardship responsibilities. In regard to the stewardshipof fixed assets, officials are concerned as to whether the entity’s assets are beingsafeguarded and used in a proper and efficient manner. Accordingly, this requires theestablishment of an inventory system to ensure that fixed assets are adequately controlled.

Control over fixed assets requires both accounting control as well as physical control. Thiscontrol is most effective when physical and accounting controls are integrated. To maintainan accurate fixed asset inventory system, it is necessary to have control over the underlyingacquisition, use and disposition of the assets.

A fixed asset system is a set of methods, policies, and procedures for recording and usingfixed assets. The specific components of a fixed asset inventory system vary considerablydepending on the type of assets, size of the organization, personnel resources available,and various other factors that are unique to each governmental entity.

The major steps involved in establishing a fixed asset inventory system include: planning;taking a physical inventory of existing assets; recording the assets in the accounting records;establishing a value for the assets; and implementing the system to record the acquisitionof new assets.

During the planning stage, input should be obtained from every functional area, such asfinance, transportation, facilities, etc., as well as all program directors, to ensure the fixedasset inventory system will meet the needs of each.

Implementation of a comprehensive fixed asset inventory system will enable each entity toaccurately reflect the value of its assets in its financial statements and preclude auditfindings. The system will also eliminate the need for each federal program director tomaintain a stand alone system and it will provide an inventory of all resources purchased,regardless of the source of funds. Additional benefits include: information that could beuseful to control capital expenditures and avoid duplicate purchases; a reduction in lossesdue to theft and unauthorized use of assets; and information needed to file insurance claims.

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-2-

II. REQUIREMENTS:

The purpose of this procedures manual is to establish the minimum requirements that areto be adopted by each county board of education, regional education service agency, andmulti-county vocational center, jointly referred to as a local education agency (LEA), inimplementing a fixed asset inventory system. Each LEA must adopt its own policies andprocedures to specifically address the factors that are unique to the organization. Forconsistency throughout the state, however, the following requirements must be implemented:

A. WVEIS - The fixed asset inventory system must be maintained on the WestVirginia Education Information System (WVEIS).

The Fixed Asset Inventory System User’s Guide published by National ComputerSystems, Inc. is to be used as the guidance for operating the software. Theinstructions included in the user’s guide are not duplicated in this manual.

B. Capitalization Level - An asset whose original cost exceeds $1,000 on anindividual basis or a donated asset whose fair market value exceeds $1,000 on anindividual basis must be included in the property record as a fixed asset.

The LEA may select a control level below $1,000 after evaluating the needs of thecounty staff, the federal program administrators and the local school personnel. Boththe control level and capitalization level may be $1,000. Neither level may be definedat greater than $1,000.

All financial statements and reports, including those submitted to the WestVirginia Department of Education, must utilize the capitalization level of $1,000.

C. Sensitive Items - Those items of equipment whose cost is generally less than thecounty’s control level but which are identified within the fixed asset system forpurposes of tracking. The accounting treatment of these assets is unchanged. Thefollowing items must be included in this control classification, but LEAs may includeother items:

Computers, printers, televisions, video cassette recorders and video cameras.

D. Depreciation - The total cost of all fixed assets is to be recorded as an expenseat the time of purchase. Depreciation expense is not to be reflected in the GFAAG.

Depreciation expense, however, is to be reported annually to the State Department ofEducation, Office of Child Nutrition for all equipment purchased with Child NutritionProgram funds that cost $5,000 or more. The expense is to be calculated using thestraight-line method of depreciation. To provide this information, the following controloptions must be selected when initially setting up the fixed asset inventory system onWVEIS:

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-3-

Depreciation - Select Yes to indicate that you wish to depreciate certain assets.

Depreciation Method - Select the Straight Line Method

E. Program Assets - In order to identify the assets purchased with State or Federalgrant funds, the first two digits of the project code element of the account codestructure must be completed. The last three digits do not need to be entered wheninventorying assets that have already been purchased. The full five digit project codewill be entered automatically by the system for all assets that are purchased after theimplementation of the fixed asset inventory system.

In addition to tracking assets by program, vocational directors have historically trackedassets according to the course of study in which the assets are used. If a countyvocational director desires to continue tracking this information, the subject element ofthe account code will need to be completed for every asset belonging to the vocationalprogram. This includes the assets that are already on hand as well as those that arepurchased in the future.

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-4-

III. RESPONSIBILITIES:

The superintendent, or director of a RESA or MCVC, has the overall responsibility for theproper operation and maintenance of the fixed asset inventory accounting system.Responsibility for the efficient daily operation of the system to order, receive and record fixedassets and sensitive items into the property record is delegated to the chief school businessofficial (CSBO) of each district. Federal program directors, all other directors or managersand all school principals are responsible for the control and security of the assets assignedto the location or administrative unit for which they are responsible.

The chief school business official, or his/her designee is responsible for:

• the monthly transfer of account activity to the fixed asset system and reconciliation.• the supervision and coordination of the initial inventory.• the fulfillment of the property record input function for all expenditures classified as

land, buildings, equipment, and vehicles for both acquisitions and retirements.• the timely creation of all asset reports.

All items of equipment which exceed the capitalization level or are considered to be sensitiveitems as defined in Section IV, including those purchased through school activity funds ordonated by school support organizations or other benefactors, must be entered into the fixedasset inventory accounting system. For each asset that is acquired, an individual must beassigned the responsibility to:

1. Receive and inspect the asset.2. Return any damaged merchandise.3. Apply a property tag(s) to the asset.4. Enter the equipment into the asset system.5. Safeguard the asset.6. Inventory the asset periodically and reconcile differences with the asset records.7. Delete from the asset record any equipment that is being disposed.

A local education agency may want to document the delegation of responsibility through theuse of a form. A sample is included in Appendix B.

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-5-

IV. DEFINITIONS:

For purposes of this manual, the term “assets” will include all fixed assets and sensitiveitems tracked in the property record. These items are defined below.

Asset Classifications - These asset classifications comprise the General Fixed AssetAccount Group (GFAAG) of the county board’s chart of accounts.

a. Land - All land owned by the LEA (Use object code 711).

b. Buildings - All buildings owned or leased by the LEA, such as school buildingsadministration buildings, maintenance garages, warehouses, athletic facilities, andportable classrooms (Use object code 721).

c. Equipment - All furniture or equipment contained in the buildings whose original costexceeds the control level established by the LEA, including furniture and equipmentacquired through a capital lease (Use object codes 731, 733, 734 or 739). Forequipment whose original cost is less than the control level, use object code 738.

d. Vehicles - All school buses, automobiles, trucks and vans owned or leased by theLEA. (Use object code 732.)

Capital Leases - All fixed assets that are being acquired under a lease/purchase agreement.See Section V for a more detailed discussion of capital leases.

Capitalization Level - The level at which fixed assets are reported for financial statementpurposes. All financial statements, including reports submitted to the West VirginiaDepartment of Education, must use a capitalization level of $1,000.

Construction in Progress - All building expenditures for facilities under construction as ofthe accounting period ending date.

Control Level - The level at which fixed assets are entered into the fixed asset inventorysystem. Each county board, RESA and MCVC may select a control level that is less thanthe capitalization level of $1,000.

Equipment - An equipment item is any instrument, machine, apparatus, or set of articleswhich meets all of the following criteria:

• It retains its original shape, appearance, and character with use;• It does not lose its identity through fabrication or incorporation into a different or more

complex unit or substance;• It is nonexpendable; that is, if the item is damaged or some of its parts are lost or

worn out, it is more feasible to repair the item than to replace it;• Under normal conditions of use, it can be expected to serve its principal purpose for

at least one year.Fixed Assets - Assets whose installed cost is greater than the capitalization level and

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-6-

whose useful life exceeds one year.

Fixtures - Attachments to a building that are not intended to be removed without damageto the building. An example is a lab table with a sink that is affixed to the floor. Cabinetsaffixed to the wall are also an example of a fixture.

Historical (Original) Cost - The actual full cost to place the asset in service to includeequipment freight and installation charges and building hard and soft costs as described indetail in Section V. Generally Accepted Accounting Principles (GAAP) requires assets to berecorded at actual or estimated historical cost.

Improvement - An addition made to, or change made in, a building, other than maintenance,to prolong its life or to increase its efficiency. The replacement of a roof is an example ofan improvement.

Replacement Cost - The amount of cash that would be required as of a certain date toreplace an asset with one of equal utility at current labor and material rates. This term ismost often used with insurance.

Sensitive Items - Those items of equipment whose cost is generally less than the county’scontrol level but which are identified within the fixed asset system for purposes of tracking.The accounting treatment of these assets is unchanged. The following items must beincluded in this control classification, but LEAs may include other items:

Computers, printers, televisions, video cassette recorders and video cameras.

Supply - An item should be classified as a supply item if it does not meet all of the criteriaestablished for an equipment item.

Useful Life - The period of time during which an asset is physically performing its function.

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-7-

V. ACCOUNTING POLICIES:

Fixed assets of governmental fund types are general fixed assets. General fixed assets areassociated with governmental funds which operate on a modified accrual basis ofaccounting. General fixed assets represent past expenditures, not financial resourcesavailable to finance current governmental activities. For this reason, general fixed assetsof a governmental unit are not presented in a specific fund, but rather are accounted for inthe General Fixed Asset Account Group (GFAAG). The GFAAG is not a fund, and does notreport results of operations. The GFAAG provides a basis for the accountability and controlof governmental fund fixed assets. Additions to and deletions from the GFAAG aredisclosed in the notes to the financial statements. Depreciation is not recorded in thefinancial statements for general fixed assets.

A. Assets Acquired Through Lease Agreements - Assets acquired through leaseagreements satisfying criteria established by the Financial Accounting Standards Board(FASB) Statement No. 13 “Accounting for Leases,” must be capitalized. FASB StatementNo. 13 requires that noncancellable leases meeting any one of the following criteriaconstitutes a capital lease, and the related asset must be recorded as a fixed asset of thelessee (LEA):

A lease is a capital lease if it qualifies under one of these criteria:

a. Ownership of the property transfers to the lessee by the end of the lease term.

b. The lease contains a bargain purchase option.

c. The lease term is equal to 75% of estimated useful life of the asset.

d. Present value of minimum lease payments exceeds 90% of fair value of the assetat the beginning of the lease.

Assets leased through agreements failing to meet any of the above criteria should not berecorded as a fixed asset.

All leases with governmental agencies in the State of West Virginia must include a fiscalfunding clause which provides for cancellation if sufficient funds are not available in a futureyear to make the required lease payments. The likelihood of cancellation due to such aclause has been deemed a remote possibility; therefore, lease agreements are considerednoncancellable. So, if the criteria established above are met, the asset must be recordedas a fixed asset of the lessee.

B. Valuation - All fixed assets are valued using historical cost which is defined as all costsexpended by the county to place the asset into service. All hard and soft costs related to theacquisition of land and building should be included. Freight and installation costs related toequipment should also be added to the invoiced cost of the asset.

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-8-

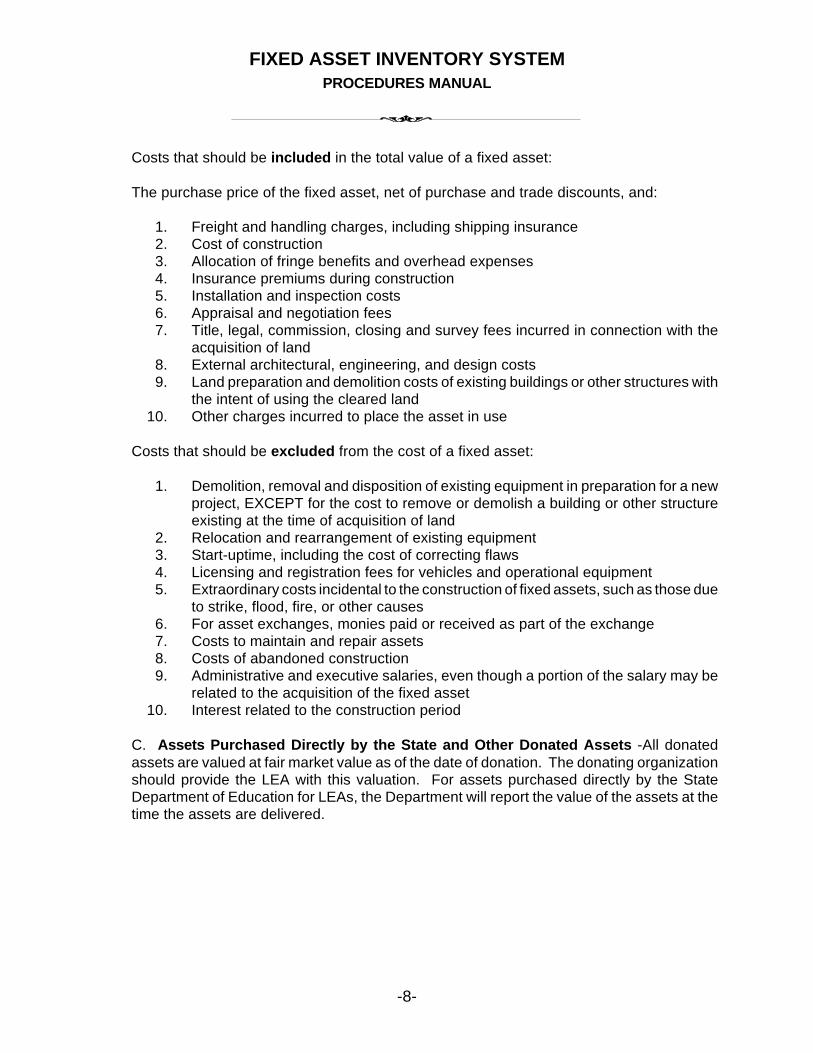

Costs that should be included in the total value of a fixed asset:

The purchase price of the fixed asset, net of purchase and trade discounts, and:

1. Freight and handling charges, including shipping insurance2. Cost of construction3. Allocation of fringe benefits and overhead expenses 4. Insurance premiums during construction5. Installation and inspection costs6. Appraisal and negotiation fees7. Title, legal, commission, closing and survey fees incurred in connection with the

acquisition of land8. External architectural, engineering, and design costs9. Land preparation and demolition costs of existing buildings or other structures with

the intent of using the cleared land10. Other charges incurred to place the asset in use

Costs that should be excluded from the cost of a fixed asset:

1. Demolition, removal and disposition of existing equipment in preparation for a newproject, EXCEPT for the cost to remove or demolish a building or other structureexisting at the time of acquisition of land

2. Relocation and rearrangement of existing equipment 3. Start-uptime, including the cost of correcting flaws4. Licensing and registration fees for vehicles and operational equipment5. Extraordinary costs incidental to the construction of fixed assets, such as those due

to strike, flood, fire, or other causes6. For asset exchanges, monies paid or received as part of the exchange 7. Costs to maintain and repair assets 8. Costs of abandoned construction9. Administrative and executive salaries, even though a portion of the salary may be

related to the acquisition of the fixed asset 10. Interest related to the construction period

C. Assets Purchased Directly by the State and Other Donated Assets -All donatedassets are valued at fair market value as of the date of donation. The donating organizationshould provide the LEA with this valuation. For assets purchased directly by the StateDepartment of Education for LEAs, the Department will report the value of the assets at thetime the assets are delivered.

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-9-

D. Capitalization Level - A purchased asset whose original cost exceeds $1,000 on anindividual basis or a donated asset whose fair market value exceeds $1,000 on an individualbasis must be included in the property record as a fixed asset. A sensitive item whose costis less than $1,000 on an individual basis is not capitalized in the GFAAG but must be addedto the property record for purposes of control.

Both the control level and capitalization level may be $1,000. Neither level may be definedat greater than $1,000.

All financial statements and reports, including those submitted to the West VirginiaDepartment of Education, must utilize the capitalization level of $1,000.

E. Control Level - The LEA may select a control level below $1,000 after evaluating theneeds of the county staff, the federal program administrators and the local school personnel.When considering a lower level, several factors are important:

1. The lower the control level, the larger the number of assets which must berecorded

2. The larger the number of assets, the greater the amount of time required toproperly track and control these assets

3. It is better to control the big dollar items than to waste time and effort attemptingto track minor equipment

Regardless of the control level selected by the LEA, all financial reporting must utilize thecapitalization level of $1,000 for consistency.

F. Equipment vs. Supply - The purchase of any item which meets the definition of anequipment item, as described in Section IV of this manual, is to be coded for financialstatement reporting purposes as an equipment purchase, regardless of whether the costexceeds the control level established by the LEA, or not. For furniture or equipment whoseoriginal cost exceeds the control level, including furniture and equipment acquired througha capital lease, use object codes 731, 733, 734 or 739. For equipment whose original costdoes not exceed the control level, use object code 738. If an item does not meet thedefinition for an equipment item, it is to be coded as a supply item.

G. Depreciation - The total cost of all fixed assets, including the equipment purchased withChild Nutrition funds, is to be recorded as an expense at the time of purchase. Depreciationexpense is not to be reflected in the GFAAG.

Depreciation expense, however, is to be reported annually to the State Department ofEducation, Office of Child Nutrition for all equipment purchased with Child Nutrition Programfunds that cost $5,000 or more. The expense is to be calculated using the straight-linemethod of depreciation. The WVEIS software has the capability to calculate thedepreciation amount that is to be reported.

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-10-

VI. REQUIRED CATEGORY AND CLASSIFICATION CODES:

For standardization, all fixed assets must be classified according to the following categoryand classification codes. In addition, for computer assets, the following list of descriptioncodes must be used. If it is determined that additional codes are needed in thesecategories, they must be assigned by the Office of School Finance.

A list of optional description codes is provided in Appendix A for other types of assets. Theuse of these codes, however, is not required. LEAs may use these optional codes or othercodes which they wish to create.

CATEGORY CODES100000 Land and Improvements200000 Buildings and Improvements400000 Furniture and Equipment500000 Vehicles

CLASSIFICATION CODES100000 Land150000 Land Improvements

200000 Buildings, Original210000 Building Additions220000 Building Improvements

400000 Computers401000 Copiers402000 Equipment, Athletic403000 Equipment, Audio Visual404000 Equipment, Building Support405000 Equipment, Classroom406000 Equipment, Communications407000 Equipment, Custodial (Inside)408000 Equipment, Food Service409000 Equipment, Grounds (Outside)410000 Equipment, Library411000 Equipment, Medical412000 Equipment, Miscellaneous413000 Equipment, Office414000 Equipment, Playground415000 Equipment, Shop416000 Furniture, Classroom417000 Furniture, Food Service418000 Furniture, Library419000 Furniture, Miscellaneous420000 Furniture, Office421000 Musical Instruments

500000 Automobile

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-11-

501000 Bus502000 Truck503000 Van504000 Other Vehicle

REQUIRED DESCRIPTION CODES

400001 Back up Storage400003 Computer Workstation, Compaq400004 Computer Workstation, Dell400005 Computer Workstation, Hewlett Packard400006 Computer Workstation, IBM400009 Computer Workstation, Packard Bell400012 Computer Workstation, Apple/MAC400015 Computer Workstation, Gateway400017 Computer Workstation, Clone400019 Computer Laptop, Compaq400020 Computer Laptop, Dell400021 Computer Laptop, Hewlett Packard400022 Computer Laptop, IBM400023 Computer Laptop, Apple/MAC400024 Computer Laptop, Gateway400025 Computer Laptop, Clone400030 Computer Terminal400055 Computer Fileserver, Compaq400056 Computer Fileserver, Dell400057 Computer Fileserver, Hewlett Packard400058 Computer Fileserver, IBM400059 Computer Fileserver, Apple/MAC400060 Computer Fileserver, Gateway400061 Computer Fileserver, Clone400062 Plotter400064 Printer, Braille400066 Printer, Laser400067 Printer, Color Laser400070 Printer, Ink Jet400071 Printer, Color Ink Jet400072 Printer, Line400075 Scanner400078 Software400092 Hub400093 Switch400094 Router

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-12-

VII. REPORTING CYCLE:

The following reports are to be extracted from the property records on at least an annualbasis:

A. Fixed Asset Summary by Category

This report lists the assets within each major asset category, as well as sensitive items, asof the end of the month. This report is an accounting document and provides support to themonthly balance sheet.

B. Fixed Asset Additions

This report lists all asset additions to the property record by asset classification, as well assensitive items occurring during the preceding month. This is an accounting document andprovides an itemized audit trail.

C. Fixed Asset Retirements

This report lists all retirements from the property record due to abandonment, loss or salefor each asset classification, as well as sensitive items, during the month and provides anitemized audit trail.

D. Detailed Listing of Fixed Assets by Asset Class

This report lists all asset detail by asset classification as of a certain date. This reportprovides support to the audited GFAAG valuation.

E. Detailed Listing of Fixed Assets by Location

This report lists all asset detail by asset classification/sensitive items by location on an asrequired basis (but not less than annually) for use in control and accountability by theprincipals and directors. This is an internal document used for purposes of asset control.

F. Insurable Value Report

This report lists all assets by asset classification as well as sensitive items within location onan annual basis for use in obtaining appropriate insurance coverage and establishing proofof loss. Replacement cost new and insurable value is calculated by the software annuallyusing indices.

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-13-

VIII. TAGGING OF EQUIPMENT:

All assets must be tagged including: those whose historical cost meets the capitalizationlevel; donated items whose fair market value at the time of donation meets the capitalizationlevel; and assets defined as sensitive items.

Tags must have a human readable identification number and be pre-numbered. Countyboards may use tags with a scannable bar code in addition to the identification number.

Consistency of placement is a primary consideration in the tagging process. The placementof the tag should facilitate its usefulness during the annual inventory process withouthindering the operation of the asset. Generally, property tags are affixed in one of twolocations, (1) near the serial number plate or (2) near the upper right-hand corner of the itemwhich is fully visible without movement of the asset. The first location is easy to determine.The second location requires the judgement of the chief school business official.

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-14-

IX. CONTROL OF ASSETS:

A. Land and Buildings:

The chief school business official classifies all costs related to the building account bysubclassification for entry into the property record. Land and building retirements will becompleted by the chief school business official. When a building is improved, the chiefschool business official will retire the appropriate portion of the building and add the cost ofthe improvement to the property record.

The chief school business official, or other authorized individual, is responsible for inputtinginformation related to land, building, and construction-in-progress to the property record.This information must be added to the property record in sufficient time to meet theaccounting period cutoff dates.

B. Equipment:

LEAs need to establish their own procedures concerning how the equipment is to bepurchased and identified for entry into the fixed asset inventory system. Some of the issuesthat should be addressed in the procedures include:

1. Requisition and Purchase

All requisitions for purchase of equipment should be processed in accordance with eachentity’s established purchasing procedures.

Procedures should be established to ensure that all items to be recorded in the fixed assetinventory system are identified. The procedures should also ensure that, at the time thepurchase order is issued, all costs related to the acquisition of the equipment, such asinstallation, warranty and freight charges, are included on the original purchase order. Costof service agreements related to the asset should be presented on a separate purchaseorder. If software is purchased with computer hardware, the value of the software shouldbe identified separately and coded as an expense. The value of a trade-in should be clearlyitemized on the purchase order.

2. Receipt of Equipment

When the asset is received, the procedures need to specify how the equipment is to bereceipted and entered into the fixed asset inventory system. The information also needs tobe conveyed to the accounts payable clerk for payment of the invoice.

Information that needs to be entered when the equipment is received includes: the datereceived; the purchase order number; the vendor; quantity; asset description; location; modelnumber; serial number; and county tag number. A tag is to be affixed to each asset at thetime of receipt. This can be done at the central board office, central warehouse, or otherlocations, such as the schools, if goods are delivered to these locations.

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-15-

The asset is recorded in the property record in accordance with the instructions detailed inthe Fixed Asset Inventory System User’s Guide as soon as practical after the item isreceived.

The same procedure should be followed whether receiving full or partial shipments. Specialattention should be paid to monthly accounting cutoff dates. All asset additions received onthe last day of an accounting month should be entered in the fixed asset inventory systemon that day.

3. Control of Property Tags

The procedures should specify the controls that are to be used to maintain control of theproperty tags.

4. Transfer and Retirement Advice

A form should be developed for use in reporting when a useable item is transferred toanother location for continued use or when an item is retired from service, so that theinformation can be entered into the fixed asset inventory system. A sample form ispresented in Appendix B.

5. Report of Lost, Damaged or Stolen Property

If an item is retired due to loss, damage or theft, the chief school business official needs tobe notified so that the incident can be reported to the insurance carrier and arrangementsmade for proof of loss and reimbursement if appropriate. A sample form is presented inAppendix B.

C. Vehicles:

The transportation director is responsible for all transportation assets. All other vehicles arethe responsibility of the individual(s) assigned by the LEA. The transportation directoradvises the chief school business official that equipment is received. The chief schoolbusiness official ensures the Vehicle Identification Number and date of acquisition are inputinto the property record. A property tag is not affixed to transportation equipment. Theannual inventory of transportation assets is completed by the transportation director throughphysical count and matched to the Vehicle Identification Number.

D. Property Under Capital Leases:

The chief school business official calculates the original cost of the asset as the presentvalue of the minimum monthly payments at a rate equal to the county’s current incrementalcost of borrowing and applies the appropriate cost. More specific instructions on capitalleases are included in the Accounting Procedures Manual. The asset must then added tothe property record in sufficient time to meet the accounting period cutoff dates.

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-16-

X. ANNUAL PHYSICAL INVENTORY:

To assure the accuracy of the fixed asset inventory system, a physical inventory should beperformed annually of all land, buildings, equipment and vehicles recorded in the fixed assetinventory system. The inventory may be performed by LEA personnel or by an outsidecompany.

If it is performed by LEA personnel, a work plan should be developed to serve as a guidefor the inventory taking process. A training session may need to be held to instructpersonnel in inventory procedures.

A reconciliation between the physical count and the fixed asset property record should alsobe completed. A listing should be printed of all discrepancies noted between the inventoryrecords and the actual inventory by location or administrative unit. All discrepancies shouldbe resolved within thirty days. This process is known as the location accounting.

The chief school business official is responsible for coordinating this activity and reconcilingthe property records during the location accounting by (1) correcting the file for the assetslocated during the location accounting, (2) recording the assets that are identified during thephysical inventory that are not listed in the inventory system, and (3) retiring the assets whichcannot be located following the location accounting.

Assets which are still missing at the end of the thirty days should be reported to thesuperintendent and chief school business official for appropriate action.

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

APPENDIX A

OPTIONAL DESCRIPTION CODES

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-18-

DESCRIPTION CODESCODE

100000150001150002150003150005200001210001210002210006210007220001220002220003220004220005220007220008220009220015220020401001401005402001402005402010402020402030402040402050402053402060402070402075402076402080403001403002403005403006403007403010403014403015 403020403025403030403035403040

DESCRIPTION

LandLand Improvement, LandscapeLand Improvement, PavingLand Improvement, Gravel/GradingLand Improvement, ConcreteBuilding, Original ConstructionBuilding Construction, AdditionsBuilding Construction, RoofingBuilding Construction, StairwellsBuilding Construction, ElevatorsBuilding Improvement, WindowsBuilding Improvement, MechanicalBuilding Improvement, CarpetCurtains, StageBuilding Improvement, BlindsBuilding Improvement, Television SystemBuilding Improvement, DividersBuilding Improvement, Hall GateAlarm SystemBleachersCopier, Plain PaperRisographBalance BeamTrampolineMat, GymnasticMat, WrestlingScoreboardWeight BenchWeight MachineLeg Curl MachineWeight Machine, SquatWeight SetPopcorn MachineStop LightWhirlpool BathCamera, 35mmCamera, DigitalCamera, VideoEnlargerSafelightSound Level MeterCassette Player, AudioCompact Disk PlayerLaser Disk PlayerP A, AmplifierP A, PortableProjector, FilmProjector, 35mm Slide

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-19-

403045403050403055403060403066403069403070403071403072403073403075403080403086403087403090404025404030405001405002405003405004405005405008405012405014405016405017405018405019405020405021405022405023405024405025405027405028405029405030405040405050405051405055405056405061405062405065405066405067405068405069405070405071

Projector, OpaqueProjector, OverheadSatellite SystemSpeakers, StereoMicrophoneVideo Editing ProcessorTelevisionTelevision w/built-in VCRMixer, DigitalMixer, AudioDigitizerVideo Cassette Recorder (VCR)Video ProcessorLCD PanelMeter, Digital MultiLockerClock, TimeMicrofiche Reader and/or PrinterSpectroscopeCelestial GlobeMagnetizerLab OvenMicroscopeVideo MicroscopeSpectrum Opt ElecOscillatorDewar FlaskLife Pak DefibulatorDefibulator SimulatorOscilloscopeRain BoxIncubatorAutoclavePH MeterCentrifugeLaserFrequency GeneratorStrobe ScopeDryer, Laundry DomesticRange, Kitchen DomesticWasher, Laundry DomesticWasher/Dryer CombinationDry-cleaning MachineMixer, Heavy Duty, Home EcGoggle SanitizerMat Cutter/EdgerSkeletonAnatomical ModelSterilizerVandegraph GeneratorRotometerHeat MantilesPressure Gauge

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-20-

405072405073405074405080405081405083406005406020406025406030406035407001407002407005407006407007407010407011407015407020408001408002408003408004408005408006408007408010408011408015408018408021408024408027408030408031408032408033408035408036408037408039408042408045408048408051408054408057408058408059408060408061408062

Strip Chart RecorderWatt MeterSpectrophoto MeterPendulum, FoucoultFly MeterWater BathBus RadioMarker boardCell PhonePagerWalkie/TalkieCart, CustodialDollyFloor Machine, BufferFloor Machine, ScrubberFloor Machine, CarpetVacuum CleanerVacuum, BackpackVacuum, ShopVacuum, Wet or DryBeverage DispenserCart, Food ServiceCart, TrayCart, GarbageCan OpenerCash RegisterSteam TableChopper, FoodBlenderDishwasherDisposalDough DividerFreezerFreezer, Walk-inFryer, Deep-fatCooking Range, GasCooking Range, ElectricHot PlateMachine, IceCoffee MakerJuicerMachine, Ice CreamMachine. PopcornMilk CoolerMixer, FoodOven, ConventionalOven, ConvectionOven, MicrowaveOven, ToasterToasterRack, Food StorageRack, TrayRack, Pan

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-21-

408063408066408069408072408073408075408078408081408083408086408087408093408094408095409050409055409060409065409070409073409076409079409081409084409087409090409096411001411002411003411004411005411007411008411009411010411011411012411015411016411017411018411019411020411021411022411023411024411025412001412020412059412060

Refrigerator, Regular Refrigerator, SmallRefrigerator, Walk-inScalesSharpenerSlicerSteam KettleSteamerVertical CutterWarmerBooster, Hot Water HeaterSinkSink, HandwashTilt SkilletSnake, PowerTap & Die SetWasher, PowerWrench, PneumaticBlower, LeafEdger/Trimmer, Gas PoweredHedge Trimmer, Gas PoweredMower, LawnSprayerTractor Attachment, FarmTractor Attachment, MowerTractor, Lawn Mower TypeTrailer EquipmentRecovery CouchRecovery CotPhone StandLifterScales, ClinicGrasshopperVestibulatorVestibulator SwingWheelchairCPR DummyAD TrainerEar ScanSuction MachineThermoscanSide BoardBelly BoardAdaptability ExerciserWedgeTumble FormAudiometerOxygen PacTitmus Vision TesterBar Code Reader (POT)LaminatorBraillerOil Drain

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-22-

412075412098412099413001413002413003 413004413005413006413007413008413009413010413012413015413020413021413022413025413026413030413031413040413045413046413050413051413060414001414005414010414020414030414040415001415005415006415007415008415009415010415011415012415013415015415016415020415025415026415030415031415032

Popcorn MachineFanHeater, PortableMachine, BindingBursterFolderCheck SignerSign MakerLabel MakerPoster MakerCollatorDe collatorMachine, Dictating/TranscribingEllison Letter MachineShredderMachine, FAXTelephone, cordlessStapler, PowerSwitchboardAnswering MachinePaper ShredderHole Punch, ElectricPostage MeterCalculatorCash RegisterPostage ScaleScales, Weight (Clinical)Word ProcessorJungle Gym ClimberAdaptive Playground EquipmentMerry-go-roundSlideSwing SetTeeter TotterKilnPotter’s WheelSander, Belt DiskStrip HeaterDust CollectorCutter, BiscuitDrill PressInjection MolderHydraulic Engine HoistJack, HydraulicJoinerToolboxLathe, MetalLathe, WoodMiter BoxPlanerRadius BenderSand Blaster

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-23-

415033415034415035415038415039415040415041415043415045415046415047415048415049415050415055415056415059415060415062415063415064415065415066415069415070415071415072415073415074415075415076415077415078415079415080415085415086416005416008416009416010416011416012416013416020416025416028416029416030416035416040416045

Hydraulic PressGrinder, PedestalSaw, BankMetric RacewaySharpener, Chain SawSaw, chainSaw, JigSaw, CircularSaw, Radial ArmSaw, MiterSaw, ReciprocatingSaw, Compound Miter SlideSaw, SabreSaw, ScrollSaw, TableShop Oven, SmallWelder, BoxWelder, ArcCrucibleForge FurnaceSheet Metal ShearWelder, MigWelding Torch SetRouter TableWelder, TigPlasma CutterRobot ArmFertilizer DispenserRouterDrills, Electric Hand HeldGrinder, L, HeadHydraulic TrainerLevelSander, HandPlaner Grinding AttachmentWater PumpGenerator, MotorApplied Mechanisms TrainerAir TableBattery Tester/ChargerScale, Precision BalancePower SupplyVoltage MeterSolvent TankSewing MachineBookcaseTrayCartCarrel, StudyArtworkDisplay CaseRiser, choral Standing

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-24-

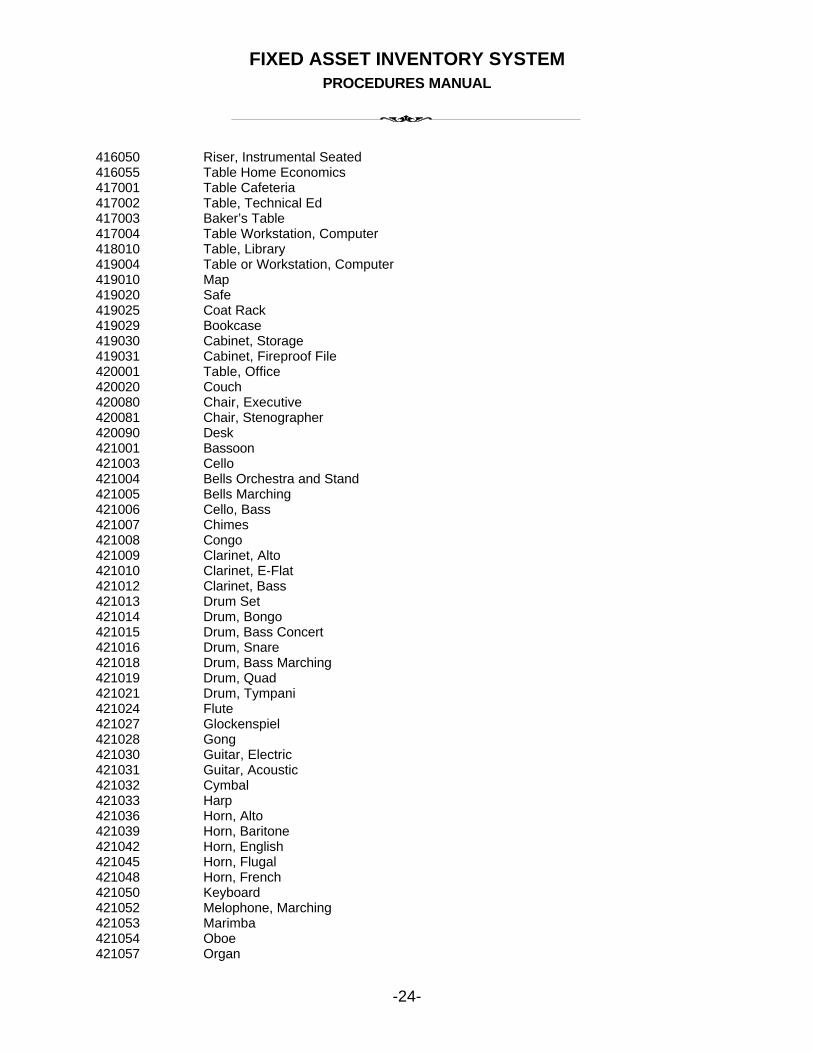

416050416055417001417002417003417004418010419004419010419020419025419029419030419031420001420020420080420081420090421001421003421004421005421006421007421008421009421010421012421013421014421015421016421018421019421021421024421027421028421030421031421032421033421036421039421042421045421048421050421052421053421054421057

Riser, Instrumental SeatedTable Home EconomicsTable CafeteriaTable, Technical EdBaker’s TableTable Workstation, ComputerTable, LibraryTable or Workstation, ComputerMapSafeCoat RackBookcaseCabinet, StorageCabinet, Fireproof FileTable, OfficeCouchChair, ExecutiveChair, StenographerDeskBassoonCelloBells Orchestra and StandBells MarchingCello, BassChimesCongoClarinet, AltoClarinet, E-FlatClarinet, BassDrum SetDrum, BongoDrum, Bass ConcertDrum, SnareDrum, Bass MarchingDrum, QuadDrum, TympaniFluteGlockenspielGongGuitar, ElectricGuitar, AcousticCymbalHarpHorn, AltoHorn, BaritoneHorn, EnglishHorn, FlugalHorn, FrenchKeyboardMelophone, MarchingMarimbaOboeOrgan

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-25-

421060421061421063421066421069421072421075421078421081421084421087421089421090421093421096421099480001490005490010490011490015490020490030490040490045490048500001500005500010501001502001503001503005504001

PianoClavinovaPiccoloSax, AltoSax, BaritoneSax, SopranoSax, TenorSousaphoneTrombone, BassTrombone, TenorTrumpetTunerTubaViolaViolinXylophoneCement MixerCharger, BatteryCompressor, AirVacuum PumpForkliftGeneratorJack, PalletJack, Floor HydraulicLadderFan, CommercialAutomobile, CompactAutomobile, Mid-SizeAutomobile, Full-SizeBus, SmallTruckVan, RegularVan, ExtendedOther Vehicle

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-26-

APPENDIX B

SAMPLE FORMS

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-27-

DELEGATION OF RESPONSIBILITY FORM

County Board of Education

School/Location/Department:

The following person is responsible for the property inventory for the named above.

Name: Title: is responsible for all inventory items during the school year.

Accepted:

Signature

Printed Name

Title

Date

Two part form routed to: Chief School Business Official (Original)Signor

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-28-

TRANSFER AND RETIREMENT ADVICE FORM

County Board of Education

TO BE COMPLETED BY ORIGINATOR

Mark one: Transfer to Retire Property Tag Number Serial No.

Item Description

Current location

Reason for transfer or retirement

Originator’s Signature Date

TO BE COMPLETED BY CHIEF SCHOOL BUSINESS OFFICIAL

Date asset received from location

Method received: District pick-up Vendor pick-up

Transferred to

Date transferred or disposed Date entered into property record

Comments

Fixed Asset Manager’s Signature Date

FIXED ASSET INVENTORY SYSTEMPROCEDURES MANUAL

-29-

REPORT OF LOST, DAMAGED OR STOLEN PROPERTY

(Report on Arson, Burglary, Vandalism, Theft, Unexplained Loss, and Failure to Return)

School/Department

Date loss discovered

Who discovered the loss

Reported to the Police: Yes No

Police Department

Date of Report Police Complaint No

Briefly explain circumstances:

Quantity Asset Description Serial No. Tag Number

Signature Date