fiscal year 2018 image result for rmi seal

TRANSCRIPT

0 | P a g e

Republic of the Marshall Islands Office of the Banking

Commission Annual Report

Fiscal

Year

2018

1 | P a g e

Republic of the Marshall Islands

Office of the Banking Commission P.O. Box 1408 ~ Majuro ~ Marshall Islands ~ 96960

Commissioner Phone No. (692) 625-2310 ~ Office Phone No. (692) 625-6309

Email: [email protected]: www.rmibankingcomm.org

September 24, 2019

Commissioner's Letter to the Minister of Finance, Banking and Postal Services

Hon. Brenson S. Wase

Minister of Finance, Banking

and Postal Services

Republic of the Marshall Islands

Government

RE: Banking Commission Annual Report FY 2018 (October 2017 to September 2018)

Dear Honorable Minister Wase,

I hereby present to you the Banking Commission's Annual Report FY 2018

covering office tasks and activities from October 2017 to September 2018. Included in

the Report under Part III is the Financial Intelligence Unit (FIU) Report for the Republic

of the Marshall Islands (RMI) Cabinet issued pursuant to Part 13 Section 167 (1) (o) of

the Banking Act 1987.

On behalf of the staff and management of the Banking Commission, I would like

to convey our sincere gratitude and appreciation for your great leadership and support.

Sincerely,

Sultan Korean

Banking Commissioner

2 | P a g e

Banking Commission Team & Organizational Structure

Minister of Finance, Banking and Postal Services

Hon. Brenson S. Wase

Banking Commissioner

Mr.Sultan T. Korean

Manager Financial Institutions

Mr.Rendy Johnny

Examiner

Ms. Tracy Oliver

Examiner Ms.Tatiana Sawej

Examiner Vacant

Manager Financial Intelligence Unit Ms.Samelda Leon

Analyst Ms.Sana Anien

Manager Financial Sector Development

Mr.Neumi N W Usumaki

Analyst Ms.Marlynn Lakabung

Administration Officer Mr.Souvenir

Ned

IT Officer Mr. Matt Muller

3 | P a g e

I. BACKGROUND

The Office of the Banking Commission (Commission) was established under Title

17 Chapter 1 Banking Act 1987 (the Act) to ensure the safety and soundness of the

Republic of the Marshall Islands (RMI) banking sector and also deter money laundering

(ML) and terrorist financing (TF) in the financial system. Pursuant to Section 104 of the

Act the Commissioner of Banking reports to the Minister of Finance, Banking and Postal

Services.

The Financial Institution Supervision (FIS) division is responsible for the

licensing and supervision of banks, other non-bank financial institutions, and cash

dealers as defined under Section 102 of the Banking Act 1987 to ensure their safety and

soundness and full compliance with AML statutes and regulations. The FIS is also a

member of the Regulatory Policy Review Committee (RPRC) that was just recently

established in the formulation and revision of new operating policies and procedures,

including new regulations and guidelines for licensed banks and other reporting

entities.

In 2015, the RMI Cabinet issued a Cabinet Policy authorizing the Banking

Commissioner to secure domestic banks' access to international payments and clearing

systems, in particular, the U.S. Federal Reserve Payment System in response to the

impact of global de-risking on our banking sector.1 Due to the importance of securing

permanent access to international clearing and payment facilities for banks and

financial institutions, the RMI Cabinet approved the establishment of a Financial Sector

Development function of the Banking Commission. The primary objective of the

Financial Sector Development (FSD) division of the Banking Commission is to assist the

Banking Commissioner in the management of all activities related to financial sector

development and ensure the effective implementation of key strategies under the

Financial Sector Development Plan (FSDP) 2016-2020. This division will also be

responsible for coordinating with key stakeholders on the revision and development of

future FSDPs.

1 the termination of correspondent banking relations by larger foreign banks in response to tougher enforcement of anti-

money laundering and counter financing of terrorism laws in the U.S. and around the world. In the RMI's case, domestic banks

rely heavily on the payment and settlement services offered through a U.S. bank CBR in order to continue operating as a bank

using the U.S. dollar.

4 | P a g e

The Commission is the lead agency in the RMI on

national anti-money laundering (AML) efforts pursuant to

Part 13 of the Act. It is empowered under Section 167 of the

Act to combat money laundering (ML) and terrorist

financing (TF) in the RMI. Under Section 167, the Banking

Commission acts as the financial intelligence unit (FIU) of

the RMI. One of the key responsibilities of the

Commissioner of Banking under Section 167 is to receive

from banks and financial institutions certain financial

reports. Financial information from such reports is

analyzed and disseminated to law enforcement when there

are reasonable grounds of ML activity within a bank,

financial institution, or cash dealer.

"The Financial

Institution

Supervision (FIS)

division is responsible

for the licensing and

supervision of banks

and financial

institutions to ensure

their safety and

soundness and full

compliance with AML

statutes and

regulations."

5 | P a g e

II. FINANCIAL INSTITUTION SUPERVISION (FIS)

Key Responsibility: Supervision of Banks and Financial Institutions

Prudential Supervision: The Banking Commission is mandated under the Banking Act

1987 to perform effective supervision of licensed banks to ensure their safety and

soundness. The Banking Commission operates within a regulatory framework allowed

under the Act to conduct the following key responsibilities: (a) register and license

banks, (b) conduct ongoing offsite surveillance and onsite examination of their financial

performance to ensure their safety and soundness, (c) address compliance with all

provisions of the Banking Act, regulations, directives, including instructions and

other internal banking by laws.

Off-site Bank Surveillance Process

Offsite surveillance tasks involve:

• the receiving of financial returns from licensed banks in accordance with

requirements of the Banking Act 1987;

• using returns to extract crucial financial data and key ratios to analyze the

financial performance of licensed banks on an ongoing basis;

• compile banking data extracted from regulatory returns by inputting into a

spreadsheet or maintain in a database for analytical purposes;

• Financial Reports-financial data

• Received by Banking Commission

Data cleaning and input into OBSS

• Onsite visits

• Calls

• Memorandums

Cleaning, verification, prudential consultation

with banks • Further analysis, review, and verification

• Input data and conduct analysis

Examiners- analyze key ratios and produce

OSMR

6 | P a g e

• based on the analysis the Banking Commission is

able to determine whether or not a bank needs to undergo

onsite examination due to its current financial state;

• financial returns are submitted weekly, monthly

and quarterly by licensed banks and provide the status on

the bank's current liquidity position, capital adequacy,

statement of income and balance sheets, interest rates for

loans and deposits, allowance for loan loss reserves, credit

risk exposures and limits in comparison with

requirements of the Banking Act 1987.

New Developments

Offsite Bank Surveillance System (OBSS) - With

the aim of strengthening the prudential supervision of

licensed banks operating in the RMI, the FIS continues to

improve the effective implementation of the Offsite Bank

Surveillance System (OBSS). The OBSS acts as an early

warning system for examiners as it allows for the timely

detection of emerging problems or risks in banks and the

banking system as a whole. The OBSS uses a CAELS

framework for both banks (Capital Adequacy-Asset

Quality-Earnings-Liquidity-Sensitivity to Market Risks).

Under the framework, banks are required to submit

financial reports to the Banking Commission on a weekly,

monthly, and quarterly basis, with the exception of the

Capital Adequacy Report that the foreign bank branch is

not required to file with the Banking Commission.

Through these financial reports, the FIS is able to produce

the Offsite Surveillance Monitoring Report (OSMR) each

quarter for both banks. The OSMR continues to be a

useful tool in assessing the financial condition of a bank

and used as a basis for conducting further onsite

examination by the FIS as it sees fit. The Banking

Commission has commenced the production of the

quarterly OSMR report for the domestic bank since 2016.

"With the aim of

strengthening

prudential supervision

of licensed banks

operating in the RMI,

the FIS continues to

improve the effective

implementation of the

Offsite Bank

Surveillance System"

7 | P a g e

Regular Production of Banking Sector Report - In order to provide a regular update to

the Minister of Finance, Banking, and Postal Services on banking matters in the RMI,

the FIS has started producing banking sector report that is done every quarter. The FIS

continues to stress the importance for all banks to disclose all financial returns required

under the OBSS for it to continue the regular production of the banking sector report.

Although faced with some challenges in trying to collect all the necessary data from

banks, FIS was able to produce a sector assessment on banks’ financial condition based

on data available to us from both banks. We also managed to required BOG to submit

financial return that enables the assessment of its loan quality. The report is referred to

as the “Loan Classification” report and is submitted every quarter. This financial return

was finalized in late 2018 and was included for the first time into the bank’s first-

quarter fiscal year 2018 assessment report in December. Going forward, the FIS has

fully engaged both banks to ensure financial data are accurate and sound for quality

assessment and monitoring of the whole banking system.

Offsite Surveillance Linked with Onsite Examination Process

Prudential Onsite Examination

The Banking Commission uses the CAMELS framework (Capital Adequacy-

Asset Quality- Management Performance - Earnings Performance-Liquidity-Sensitivity

OSMR ProducedSupervisory Issues

warrant further examination

Determine whether target or

full scope examination

Scope and Planning stage

request information/data

Conduct onsite examination using ROCA or CAMELS

framework

8 | P a g e

to Market Risks) to conduct an onsite examination of the

domestic bank. Onsite examination tasks using the CAMELS

framework involve the following tasks:

• CAMEL Examination- a key examination that provides a

clear picture into a bank's overall safety and soundness broken

down into these key elements: Capital Adequacy, Asset

Quality (mostly loans), Management Quality, Earnings, and

Liquidity;

• Review of a bank's compliance with applicable statutes,

directives, guidelines, and regulations set by the Banking

Commission.

New Developments

Implementation of the SOSA and ROCA Frameworks -

There is an ongoing review of new supervisory frameworks for

branches of foreign banks that are licensed to operate in the

RMI. The Banking Commission is currently reviewing the

applicability of the Strength of Support Assessment (SOSA) and

Risk Management-Operational Control-Compliance-Asset

Quality (ROCA) Frameworks for branches of foreign banks.

The SOSA and ROCA frameworks were developed by the U.S.

Federal Reserve as tools for supervising branches of foreign

banks operating in the U.S. Existing manuals produced by the

Federal Reserve to undertake SOSA and ROCA examinations

are currently reviewed by the Banking Commission for future

use. The plan is to tailor manuals to suit the RMI context based

on size, scale, and complexity of institutions supervised. The

existing CAELS framework is an important component of the

new SOSA framework and will be incorporated once the

revision is done.

Additionally, a team from the Financial Services Volunteer

Corps (FSVC) has agreed to work with the Commissioner and

the FIS develop a framework for the onsite examination of

foreign bank branches which will be mirrored into the ROCA

framework and best suited the need of the Banking

"Prudential

supervisory

oversight of MIDB

operations will

ensure that MIDB

continues to

operate in a safe

and sound manner

and that

Government assets

are safeguarded

and protected at

all times."

9 | P a g e

Commission. Under the same arrangement with FSVC, the team will also be assessing

and suggests where appropriate changes to the current AML/CFT manual for use by FIS

during AML/CFT onsite examination. The team will be coming into the RMI in mid-

February 2018 for week engagement with FIS.

During the fiscal year 2018, the FIS did not conduct an onsite review of any of the

reporting entities due to the National Risk Assessment (NRA) that kicked off in 2018. It

is an effort that requires partnership commitment between the public and the private

sector. The product of the NRA when finalized will hopefully inform of the risks and

vulnerabilities in the context of money laundering in the RMI. This will then assist the

government and the stakeholders better when addressing AML/CFT and prioritize

resources accordingly. FIS was given the task to lead the risk assessment effort that may

be associated with the banking, insurance and other financial institutions sector that is

currently operating in the RMI.

Prudential Supervision of Marshall Islands Development Bank - The RMI

Cabinet authorized the Banking Commission under Cabinet Minute (C.M. 133) to

conduct prudential supervision of the Marshall Islands Development Bank in

accordance with new prudential guidelines that shall be set by the Banking

Commission. Prudential supervisory oversight of MIDB is a means to ensure that

MIDB continues to operate in a safe and sound manner and that Government assets are

safeguarded and protected at all times. Several countries in the world including the

Pacific have started supervising their development banks for the same reasons i.e.

Reserve Bank of Fiji, Central Bank of Nigeria, Palau Financial Institutions Commission.

10 | P a g e

The RMI Cabinet also authorized the Banking

Commission to conduct a compliance examination of

MIDB's adherence to the Marshall Islands Development

Bank Act and to report all findings to the Minister of

Finance and the RMI Cabinet. The recent Cabinet

decision is based on past recommendations by the

International Monetary Fund stated in Article IV mission

reports for the RMI that stressed the need for the RMI

Government to bring MIDB under the Banking

Commission's regulatory framework. Furthermore, The

Banking Commission is still in the process of developing

the appropriate prudential guidelines and will commence

its supervisory work once guidelines have been set and

introduced to the Board of Directors and Management.

This will require a transition period for MIDB to adopt

and implement the guidelines. We are engaged with

PFTAC-IMF for assistance in putting in place the best-

suited framework for MIDB in 2019.

IMF PFTAC Annual Meeting for Pacific Islands

Bank Supervisors Vanuatu August 2018 - Mr. Sultan

Korean Commissioner of Banking, Manager of Financial

Institution Supervision, Mr. Rendy Johnny, and two

Financial Institution Examiners, Sharon Ading and Tracy

Oliver participated in the 2018 Annual Meeting IMF

PFTAC for Bank Supervisors in Vanuatu. During the

meeting, PFTAC facilitated a series of workshops centered

on bank regulatory and supervisory approaches to

managing cyber risks in the financial system and potential

implications of Fintech for financial sector supervision.

The annual meeting also provided an opportunity to

update the association on the Secretariat's activities and

PFTAC's ongoing technical assistance programs.

Opportunities were given to every member country to

give a presentation on issues and challenges faced by each

member country in relation to the banking environment in

each jurisdiction respectively.

"The FIS in

conjunction with

Financial Sector

Development division

are exploring

opportunities for

capacity building of

the examiners to

ensure that they are

well equipped with the

skills and knowledge

to undertake their

responsibilities as

young professionals"

"The Banking

Commission is also

mandated to regulate

banks, financial

institutions and cash

dealers for AML/CFT

compliance pursuant to

the anti-money

laundering provisions

under Part 13 of the

Act."

11 | P a g e

AML/CFT Supervision

The Banking Commission is also mandated to regulate banks, financial

institutions and cash dealers for AML/CFT compliance pursuant to the anti-money

laundering provisions under Part 13 of the Act. All reporting entities are required to

comply with AML Regulations 2002 pertaining to customer due diligence, enhanced

due diligence for higher-risk customers, internal anti-money training program,

reporting of suspicious activity, reporting of currency transactions, maintenance of

bank records and other regulatory requirements stipulated under the Act and

associated regulations and guidelines.

Supervision of reporting entities involve the following activities:

• Offsite review of bank and other reporting entity data and files prior to

examination;

• Onsite examination of bank and other reporting entity's anti-money laundering

program to ensure full compliance with standards set by the Banking

Commission;

• Enforcing compliance with law and regulations through regulatory fines and

penalties for apparent violations;

• Ensure that apparent violations of the Act and regulations are rectified and

corrective actions implemented across the institution.

New Developments

AML/CFT Onsite Examinations - The FIS has deferred the scheduled for follow

up onsite examinations that were scheduled until further notice due to the need to

provide support work for the FIU in facilitating the National Risk Assessment process

(further information on the NRA is explained in the FIU section of the report).

Capacity Building and Training for Examiners - The FIS in conjunction with

Financial Sector Development division are exploring opportunities for capacity building

of the examiners to ensure that they are well equipped with the skills and knowledge to

undertake their responsibilities as young professionals. Training opportunities through

the IMF's PFTAC office in Fiji, the Financial Services Volunteer Corp, UNDP, ADB, and

the World Bank are currently explored by the FSD. There is a long-term plan to enroll

examiners in the Federal Deposit Insurance Corporation Risk Management School in

12 | P a g e

Washington D.C. in the future. The FDIC School is a highly reputable institution that

provides the requisite certification for bank examiners in the U.S. who upon completion

of the five (5) - year program will be certified as Commissioned Examiners.

Additionally, FIS manager and one examiner had an attached arrangement with FIDC

examiners for the ANZ bank onsite full-scope examination in early 2018. The bank was

assessed on the basis of the CAMELS framework.

Licensing of Banks

The Banking Commission also has full responsibility for the licensing of all banks

operating in the RMI. The Banking Commission reviews the bank license application

pursuant to Section 111 of the Act and may extend additional conditions of license for

the proposed activity. The Banking Commission can deny or revoke the license if it

does not meet licensing requirements under the Act.

Banks are required to pay an annual licensing fee including a separate fee for

each branch establishment.

Approved License Renewal: In FY 2018, the Banking Commission granted license

renewal for the following banks:

• Bank of Marshall Islands- Uliga Branch, Airport Branch, Jaluit Branch, Ebeye

Branch, Kwajalein Branch, Wotje Branch and (6 Branches);

• Note: Kili Branch has come to closure during late 2018 due to land dispute

• BOG- Majuro Branch.

New Developments

There are two major revisions to the Banking Act 1987 that will require the

formulation and revisions of current directives, guidelines, and instructions that the

Banking Commission currently uses: Upon successful passage of the proposed

amendments to the Act, all financial service providers will shift under the scope of the

Banking Commission’s licensing regime.

Amendment to the Banking Act 2017 (Bill 94) - The Minister of Finance, Banking,

and Postal Service plans to introduce Bill 94 to the Nitijela during the January 2018

session. The proposed bill will provide additional powers for the Banking Commission

to supervise other financial service providers such as insurance companies and credit

institutions. The overall safety and soundness of the RMI financial system is crucial for

13 | P a g e

the continued support in economic development and also to protect consumers of

financial products and services such as borrowers and insurance policyholders. The

new bill once passed into law will also establish a licensing regime for these entities and

provide the powers to the Banking Commission to collect fees and to deposit funds into

a new Banking Commission special revenues fund that will be non-lapsing. Long-term

financial self-reliance is one of the key objectives of the Banking Commission taking into

consideration fiscal constraints within the Government due to projected revenue

reductions and annual decrease in Compact grant assistance from the U.S. The bill also

establishes the Financial Intelligence Unit, Anti-Money Laundering Council, and

definition of Designated Non-Financial Service Providers (DNFBPs) as newly regulated

entities under Part 13 of the Act and to further comply with Financial Action Task Force

recommendations.

Revision of Banking Act 1987 and Directives - As part of its key strategy to

address the impact of de-risking in the RMI banking as stated in the Financial Sector

Development Framework the Banking Commission was able to secure technical

assistance (TA) from the IMF to further strengthen the banking regulations. Two TA

came to the RMI and brought in legal experts from the IMF head office in D.C. to assist

in the revision of the Banking Act and Directives. A legal review was conducted by the

TAs introducing the amendment made to the reporting directives and

recommendations towards what is needed to be in the regulation. The Banking

Commissioner, Ms. Claire Loeak (Assistant Attorney General), Rendy Johnny (FIS

Manager), and the two examiners Tracy Oliver and Sharon Ading participated in the

legal review. The IMF legal team will work closely with the Attorney General's office in

the drafting of the new legislation and prudential statements.

Existing and New Regulations, Directives, Instructions, and Guidelines for Banks

and Financial Institutions

The following regulations, directives, guidelines, instructions, and advisories are

currently effective and used by FIS in ensuring the safety and soundness of banks. Also

banks, other financial institutions and cash dealers’ compliance with AML/CFT

requirements under the Act.

14 | P a g e

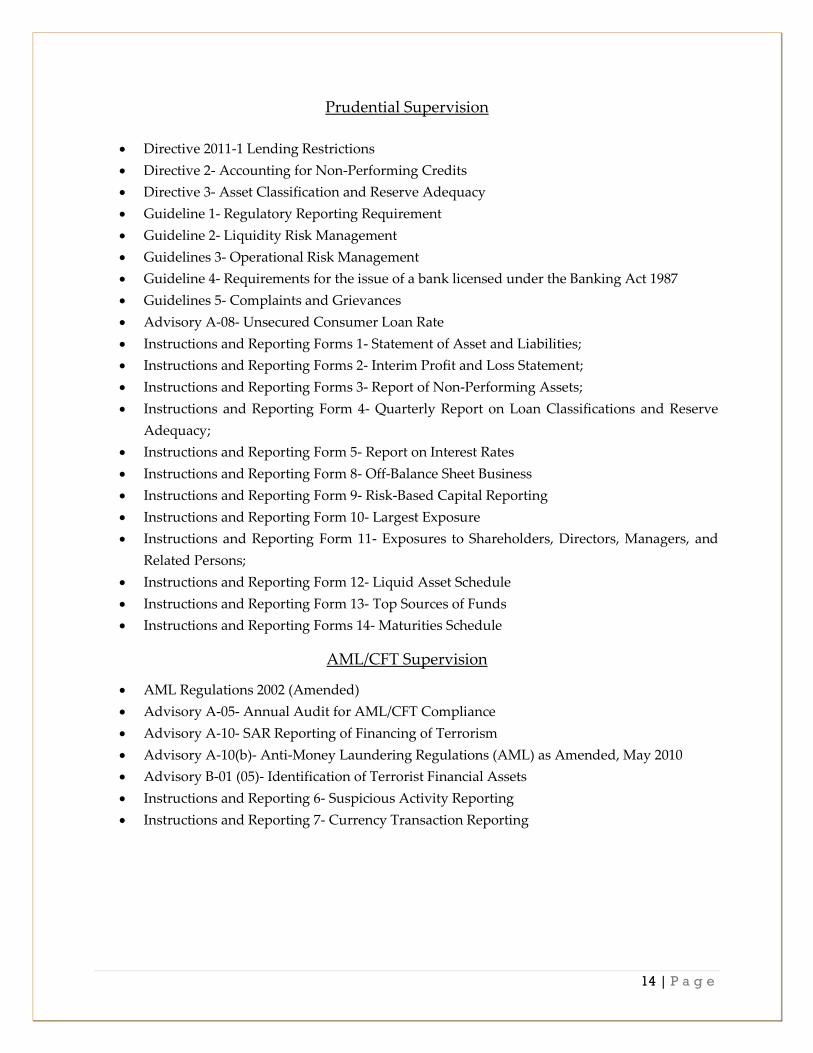

Prudential Supervision

• Directive 2011-1 Lending Restrictions

• Directive 2- Accounting for Non-Performing Credits

• Directive 3- Asset Classification and Reserve Adequacy

• Guideline 1- Regulatory Reporting Requirement

• Guideline 2- Liquidity Risk Management

• Guidelines 3- Operational Risk Management

• Guideline 4- Requirements for the issue of a bank licensed under the Banking Act 1987

• Guidelines 5- Complaints and Grievances

• Advisory A-08- Unsecured Consumer Loan Rate

• Instructions and Reporting Forms 1- Statement of Asset and Liabilities;

• Instructions and Reporting Forms 2- Interim Profit and Loss Statement;

• Instructions and Reporting Forms 3- Report of Non-Performing Assets;

• Instructions and Reporting Form 4- Quarterly Report on Loan Classifications and Reserve

Adequacy;

• Instructions and Reporting Form 5- Report on Interest Rates

• Instructions and Reporting Form 8- Off-Balance Sheet Business

• Instructions and Reporting Form 9- Risk-Based Capital Reporting

• Instructions and Reporting Form 10- Largest Exposure

• Instructions and Reporting Form 11- Exposures to Shareholders, Directors, Managers, and

Related Persons;

• Instructions and Reporting Form 12- Liquid Asset Schedule

• Instructions and Reporting Form 13- Top Sources of Funds

• Instructions and Reporting Forms 14- Maturities Schedule

AML/CFT Supervision

• AML Regulations 2002 (Amended)

• Advisory A-05- Annual Audit for AML/CFT Compliance

• Advisory A-10- SAR Reporting of Financing of Terrorism

• Advisory A-10(b)- Anti-Money Laundering Regulations (AML) as Amended, May 2010

• Advisory B-01 (05)- Identification of Terrorist Financial Assets

• Instructions and Reporting 6- Suspicious Activity Reporting

• Instructions and Reporting 7- Currency Transaction Reporting

15 | P a g e

Financial Sector Overview

The RMI financial sector consists of two commercial banks, Bank of Marshall

Islands and BOG (U.S. bank and FDIC insured) including other smaller financial

institutions and cash dealers that provide other types of financial services. There is also

the Marshall Islands Development Bank (MIDB) which is a government-owned

institution that is governed by the MIDB Act. Both commercial banks fall under the

supervisory framework of the Banking Commission and are required by the Banking

Act 1987 to adhere to prudential banking standards. MIDB has been recently added

into the regulatory framework where it will be subject to prudential and AML/CFT

supervision.

BOMI, BOG and other reporting entities defined as financial institutions and

cash dealers are required to adhere to anti-money laundering provisions under Part 13

of the Banking Act 1987 and the revised AML Regulations 2002. Below is a list of the

identified reporting entities that fall under the Commission’s purview as of the end of

FY 2018

Supervision of Reporting Entities

REPORTING ENTITIES

BANKS PRUDENTIAL SUPERVISION

or AML/CFT SUPERVISION

BANK of Marshall Islands BOTH

Uliga Branch BOTH

Majuro Airport Branch BOTH

Jaluit Branch BOTH

Wotje Branch BOTH

Kwajalein Branch BOTH

Bank of Guam

Majuro Branch BOTH

CREDIT INSTITUTIONS

Marshall Islands Services

Corporation

AML/CFT Supervision

Majuro Branch AML/CFT Supervision

Ebeye Branch AML/CFT Supervision

AjejdrikdrikInc Majuro AML/CFT Supervision

JAJ Corporation Majuro AML/CFT Supervision

Family Mart AML/CFT Supervision

Enewatak Ugelang Community

Loan Program

AML/CFT Supervision

MONEY TRANSFER

OPERATOR (MTO)

16 | P a g e

Money Gram AML/CFT Supervision

Western Union AML/CFT Supervision

INSURANCE

Moylans Insurance AML/CFT Supervision

Marshall Islands insurance

Agency

AML/CFT Supervision

IAC Insurance AML/CFT Supervision

AML/CFT Supervision

CREDIT UNION AML/CFT Supervision

Kwajalein Employee Credit

Union

AML/CFT Supervision

New Developments

Completion of Financial Sector Profile - The FIS in FY 2018 continued to

develop a Financial Sector Profile of all reporting entities in the RMI. This included

banks, insurance companies, and other financial services, providers. Sector Profiling is

an ongoing work and effort is also part of the FIS’s work plan for continuation and

improvement in FY 2019. The Financial Sector Profile will assist the Banking

Commission in understanding the size of the market based on the respective shares of

each entity in terms of asset size. Additionally, the sectoring profile gives fair idea and

expectation of business activities that may be associated with each service provider

respectively and will be utilized from time to time by examiners when planning

examination work. The sector profile will also be crucial when assessing the whole

financial system in the RMI.

Creation of three (3) Examination Groups under FIS for FY 2018 – In FY 2018,

the FIS was able to secure two more examiner positions in early February. An

additional examiner position has been entertained by PSC although it has not been

filled. The FIS intends to plan and structure its activities into three (3) groups each

comprising of banks, financial institutions and cash dealers, where the FIS Manager will

lead each group with the assigned examiner. This way the heavy workload to

supervise all these entities will be fairly spread out amongst the three examiners with

the FIS Manager as the lead examiner. Offsite bank surveillance work will be carried

out by each examiner for the bank that they have been assigned for.

Assisting the FIU in facilitating the NRA – The FIS, in FY 2018, collaborated

with the FIU in completing the NRA as one of the 2020 goals of the Cabinet. The FIS

was assigned to assess the Banking Sector and Other Financial Institutions Sector to

17 | P a g e

determine a country assessment that will show how vulnerable

and risky the RMI is to money laundering. (further information

on NRA will be explained on the FIU section of the report)

Banking Sector Report

The overall condition of the banking sector has continued

to be satisfactorily. The domestic bank is well-capitalized based

on the tier-1 risk-based capital ratio set by the Banking

Commission. The U.S. bank branch has adequate capital

support from the head office to support its operations in the

RMI. Asset quality continues to be satisfying and improving

throughout 2018.

Earnings performance overall is satisfactory. It has shown

consistent resulting from the net interest margin in both banks

and a decrease in overhead costs and interest expense. There is

excess liquidity in the system indicative of the ability of both

banks to meet their future obligations.

Capital Adequacy

The risk-based capital ratio for the uninsured domestic

bank reached the highest record of 38.2% during September. The

ratio has always been increasing since the beginning of the year.

The RMI domestic bank is well-capitalized based on strong

earnings performance from the past. Capital adequacy is

assessed based on minimum standards set by the Banking

Commission through regulatory financial returns. Licensed

Domestic banks are required to maintain at all-time 15% or more

of risk-based capital. The bank’s risk-based capital has always

been well above the statutory minimum reported during quart

ending March, June, and September at 36.8%, 37.6%, and 38.2%

respectively.

The foreign bank branch has adequate capital support

from its head office. The Banking Commission continues to

monitor the level of capital for the domestic bank on a regular

basis through its offsite bank surveillance system.

"The overall

condition of the

banking sector is

Satisfactory. The

domestic bank is

well capitalized

based on the tier-1

risk based capital

ratio set by the

Banking

Commission. The

U.S. bank branch

has adequate

capital support

from head office to

support its

operations in the

RMI."

18 | P a g e

Asset Quality

The quality of the aggregated asset portfolio continues to be Satisfactory and

considerably stable although it has gone up to reach 3.02% Non-Performing during the

fourth quarter dated September. The chart below shows the movement and level of

Non-Performing Loans (NPL) to Gross Loans between first, second, third and fourth

quarters during the fiscal year 2018. It is relatively stable although it has increased to

reach the highest level during the fourth quarter. The decline in the NPL ratio is

indicative of improvement in the overall loan underwriting process to further enhance

credit risk management.

Aggregate assets in the banking sector equated to $256.9M as of September 30

2018, a decline by 5.86% from $272.9M record in prior quarter primarily due to an

increase in cash paid out during this period as reflected in the reduction of liquid asset

by approximated 13% and 9% between March and June and to September respectively.

The gross loan has been relatively stable at 122.6M, 125.3M and 122.0M during March,

June, and September.

19 | P a g e

There is active lending in the sector but there still remains excess deposit funds in

the system. Loans to deposit ratio for both banks as of reporting period (September 30,

2018) recorded 54.4%, which shows that there is sufficient liquidity in the system and

the potential for banks to lend available funds to further strengthen economic activity.

The RMI Banking Act permits up to 70% of the total deposits that could be made

available for loans.

The Allowance for Loan Losses and Leases (ALLL) for the uninsured domestic

bank has been in excess of the regulatory minimum required under Directive 3. During

September, the aggregated bank recorded an ALLL of $7.8 Million. The amount appears

to be sufficient at current to act as a cushion for potential loan losses or when there is

deterioration in asset quality when compared with the ALLL minimum that should be

maintained based on minimum requirements set by the Banking Commission’s

regulatory limit which would have been 1.5M correspondingly.

Earnings Performance

Earnings performance in the banking sector is Satisfactory and has shown a stable

pattern throughout the year. Net interest income at quarter-ending March, June, and

September was estimated to 3.37M, 3.48M, and 3.43M respectively. The overall

profitability of the banking sector is mainly affected by the spread between the yield on

earning assets and the cost of funding sources. The gap between the two buckets is

measured by the spread 2 . The spread has been stable during March, June, and

September at roughly 9.4%, 9.5%, and 9.5% respectively. The banking sector has

2 Spread is the difference between Internet on earning asset minus interest expenses or cost of

funding.

20 | P a g e

enjoyed the spread which is quite high when compared with other jurisdictions in the

region and the trend may be continuing or at least stable into the near future provided

that government policies remain unchanged. Before-tax profit although experienced

with a 14% drop from 2.5M to 2.1M June it picked up again by 7% from 2.1M to 2.3M at

quarter ending dated September 2018. The decline between March and June was mainly

influenced by the approximated 30% spike in overhead expenses during the

corresponding period.

Return on Assets (ROA) has reached the highest level during September with an

average of 3.5% slightly moved from 3.4% and 3.3% during March and June

respectively. The favorable ratio is indicative of how well banks have generated returns

on every asset invested during the year. Net Interest Margin (NIM) has also been

growing consistently and stable at a range from 9%, 9.21%, and 9.26% during March,

June, and September.

Liquidity

Liquidity in the banking sector remains Strong. As of the reporting period, sector

liquidity was reported to be 62.97% indicative of sufficient liquidity in the system and

compliance with a statutory minimum of 20% pursuant to section 122 of the Banking

Act. Sufficient liquidity in the system demonstrates the ability of banks to meet cash

needs to continue carrying out banks’ operations such as loan disbursements,

significant deposit withdrawals, and other operational purposes that require the

immediate use of cash. Sector liquidity has not been dropped below 60% all through the

year.

21 | P a g e

III. FINANCIAL INTELLIGENCE UNIT (FIU)

The Republic of the Marshall Islands (RMI), as a member of the international

community, has an obligation to participate in the international efforts to combat

financial crimes such as money laundering (ML) and terrorist financing (TF). To help

meet this obligation, the RMI Cabinet established the Domestic Financial Intelligence

Unit (DFIU), housed in the Banking Commission.

The DFIU was established by Cabinet Minute 236 (2000). At its meeting on 20

November 2000, the Cabinet approved the establishment of a DFIU spearheaded by the

Commissioner of Banking. The DFIU comprises of the Commissioner of Banking, Police

Commissioner, Tax and Customs Division Chief, a representative from the Attorney

General's Office, and the Trust Company of the Marshall Islands (TCMI).

The powers of the DFIU of the RMI are provided specifically in section 167, and

more broadly in sections 170 and 180 of the Banking Act 1987 (Act). Section 167 of the

Act provides the Commissioner of Banking with the full powers equivalent to a

Financial Intelligence Unit (FIU). Furthermore, Section 167 of the Act provides the

Commissioner of Banking with a range of statutory powers, including to receive, store

and disseminate reports from reporting entities to law enforcement authorities (LEAs)

for further investigation. Law enforcement authorities involved in regime to combat ML

in the RMI are the Attorney General, Auditor General, and Police Commissioner.

In October 2000, the Nitijela of the Marshall Islands passed the Banking Act

(Amendment) 2000. The purpose of the amendment to the Act is to make provision for

the prevention of money laundering and enable the illicit proceeds of serious crimes to

be identified, traced, frozen, and seized or confiscated.

Key Responsibilities

The role and function of the Financial Intelligence Unit are provided under Part

XIII, Section 167 of the Act. The Banking Commission is the lead agency in the RMI

responsible for the detection and prevention of ML and TF activities. The powers are

provided to the Commissioner of Banking, as the Head of the FIU, specifically in

Sections 167, and more broadly in sections 170 and 180 of the Banking Act.

The FIU's core objective is to protect the RMI from money laundering. The key

role and responsibilities of the FIU according to Section 167 of the Act are as follows:

➢ Assist the RMI Government in combating ML, TF, and other serious crimes;

22 | P a g e

➢ Receive, analyze, and develop financial intelligence from transaction reports

submitted by financial institutions and cash dealers;

➢ Share financial intelligence with LEAs if there are reasonable grounds for ML;

➢ Enforce compliance by reporting entities with the requirements of the

Banking Act and Anti Money Laundering Regulations;

➢ Compile statistics and records

➢ Disseminate information within the RMI or elsewhere;

➢ Create training and workshops for financial institutions and cash dealers with

respect to record-keeping and reporting obligations;

➢ Exchange information between international administrative authorities and

also assist international administrative authorities in conducting a money-

laundering investigation; and

➢ Investigate, in association with law enforcement authorities, money

laundering when there are reasonable grounds to suspect money laundering

activity is happening.

Regulated Entities

Under Part 13 of the Act, financial institutions and cash dealers are subject to the

supervision of the Banking Commission. The Financial Institutions Supervision (FIS)

Division of the Banking commission plays a key role in the supervision of all financial

institutions and cash dealers to ensure compliance with the Anti-Money

Laundering/Countering the Financing of Terrorism (AML/CFT) standards.

The Financial Intelligence Unit complements this role through joint examinations

with the FIS Division and participates in each AML/CFT examination that FIS conducts.

Financial institutions and entities that are subject to AML/CFT requirements of the RMI

are listed in the following diagram.

23 | P a g e

Governance Structure

Minister of Finance, Banking and Postal Services

The Banking Commission – FIU falls under the portfolio of the Minister of

Finance, Banking and Postal Services, Honorable Minister Brenson S. Wase. The

Banking Commission – Financial Intelligence Unit is accountable to the Commissioner

of Banking and ultimately to the Minister of Finance, Banking and Postal Services.

Commissioner of Banking

The Commissioner of Banking is responsible for the administration and

enforcement of the provisions of the Banking Act. The Commissioner is the Head of the

FIU and has specific powers under Part 13, Section 167 of the Act which is the same as

those of the FIU. The Commissioner of Banking is required under the Act to develop

and submit an annual FIU Report to the Cabinet at the end of every financial year.

Within a year, quarterly progress reports on the FIU are also submitted to the Minister

of Finance, Banking and Postal Services.

Banks

• Bank of the Marshall Islands (BOMI)

• Bank of Guam (BOG)

Credit Institutions

• MISCO

• Ajejdrikdrik inc.

• JAJ Coporation

• Enewetak Atoll Local Government

Money Transfer

Operators ("MTO")

• Money Gram

• Western Union

Insurance• Moylans Insurance

• IAC Insurance

• MIA

Credit Union

• Kwajalein Employee Credit Union

24 | P a g e

Manager of the Financial Intelligence Unit (FIU)

The FIU Manager post was established by Cabinet Minute (C.M.) 201 (2016) on

November 15, 2016. A key responsibility of the FIU Manager is to manage the affairs of

the FIU under the guidance and supervision of the Commissioner of Banking in the

implementation of Section 167 of the Banking Act on combating ML in the RMI. The

FIU Manager is the point of contact and lead member in all AML/CFT efforts

nationwide and primary contact for Egmont Group of FIUs and is tasked with Asia

Pacific Group on Money Laundering (APG) and Financial Action Task Force (FATF)

related matters.

Analysis of Financial Information Received

A key function of the FIU is to analyze reports of financial transactions –

Currency Transaction Reports (CTR) and Suspicious Activity Reports (SAR) – it receives

from financial institutions and cash dealers in the RMI. Financial institutions and cash

dealers are required under the Banking Act to report CTRs and SARs to the Banking

Commission – Financial Intelligence Unit.

Highlights of the financial reports received by the FIU in FY 2015 through FY

2017 are provided below. During FY 2016, the FIU received a total of 3756 financial

Minister of Finance, Banking and Postal Services

Honorable Min. Brenson S Wase

Banking Commissioner

Mr. Sultan T. Korean

FIU Manager

Ms. Samelda Neimon Leon

FIinancial Intelligence Analyst

Ms. Sana Grace Anien

FIinancial Intelligence Examiner

(Vacant)

25 | P a g e

transaction reports, which includes CTR and SAR submissions. Furthermore, during FY

2017, the FIU received a total of 3471 financial transaction reports, which shows a

significant 7.6% decrease in financial transaction reporting. The highlight of the

financial reports provided below shows a significant increase of 34 suspicious activity

reports submitted in FY2017 compared with FY2016. During FY 2017, there were 3,426

currency transactions and 45 suspicious activities reported to the Banking Commission -

FIU. On average, 289 financial transaction reports are submitted to the FIU every month

during FY 2017.

Currency Transaction Reports (CTR)

Financial institutions and cash dealers are required under Section 180 of the

Banking Act to report to the Commissioner of Banking, all transactions involving the

currency of a value greater than $10,000 in a single transaction or multiple transactions

within a 24-hour period when aggregated. Financial institutions and cash dealers are

required to file CTRs to the Banking Commission within 10 working days since the date

of the transaction, per the Anti-Money Laundering Regulations. All records of currency

transaction reports shall be kept by the Banking Commission for a period of 15 years.

Oct Nov Dec Jan Feb Mar Apr May June July Aug Sept

FY 16 362 238 307 310 257 251 325 263 316 366 284 256

FY17 363 307 305 329 236 311 249 312 240 298 254 222

0

50

100

150

200

250

300

350

400

# o

f C

TR

s R

ec

eiv

ed

Currency Transactions Reported(FY 2016 & FY 2017)

FY 2015 FY 2016

FY 2017

CTR 3,535 3,745 3,426 SAR 8 11 45

Total 3,543 3,756 3,471 Total Monthly

Average 295 313 289

26 | P a g e

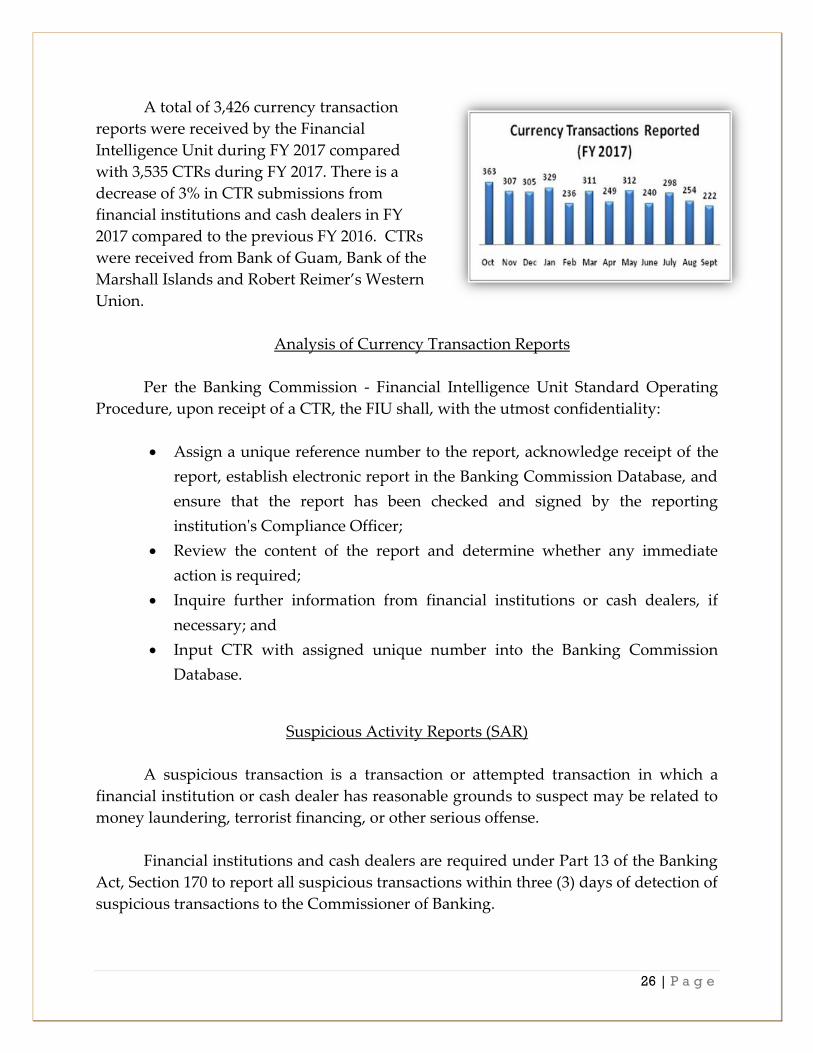

A total of 3,426 currency transaction

reports were received by the Financial

Intelligence Unit during FY 2017 compared

with 3,535 CTRs during FY 2017. There is a

decrease of 3% in CTR submissions from

financial institutions and cash dealers in FY

2017 compared to the previous FY 2016. CTRs

were received from Bank of Guam, Bank of the

Marshall Islands and Robert Reimer’s Western

Union.

Analysis of Currency Transaction Reports

Per the Banking Commission - Financial Intelligence Unit Standard Operating

Procedure, upon receipt of a CTR, the FIU shall, with the utmost confidentiality:

• Assign a unique reference number to the report, acknowledge receipt of the

report, establish electronic report in the Banking Commission Database, and

ensure that the report has been checked and signed by the reporting

institution's Compliance Officer;

• Review the content of the report and determine whether any immediate

action is required;

• Inquire further information from financial institutions or cash dealers, if

necessary; and

• Input CTR with assigned unique number into the Banking Commission

Database.

Suspicious Activity Reports (SAR)

A suspicious transaction is a transaction or attempted transaction in which a

financial institution or cash dealer has reasonable grounds to suspect may be related to

money laundering, terrorist financing, or other serious offense.

Financial institutions and cash dealers are required under Part 13 of the Banking

Act, Section 170 to report all suspicious transactions within three (3) days of detection of

suspicious transactions to the Commissioner of Banking.

27 | P a g e

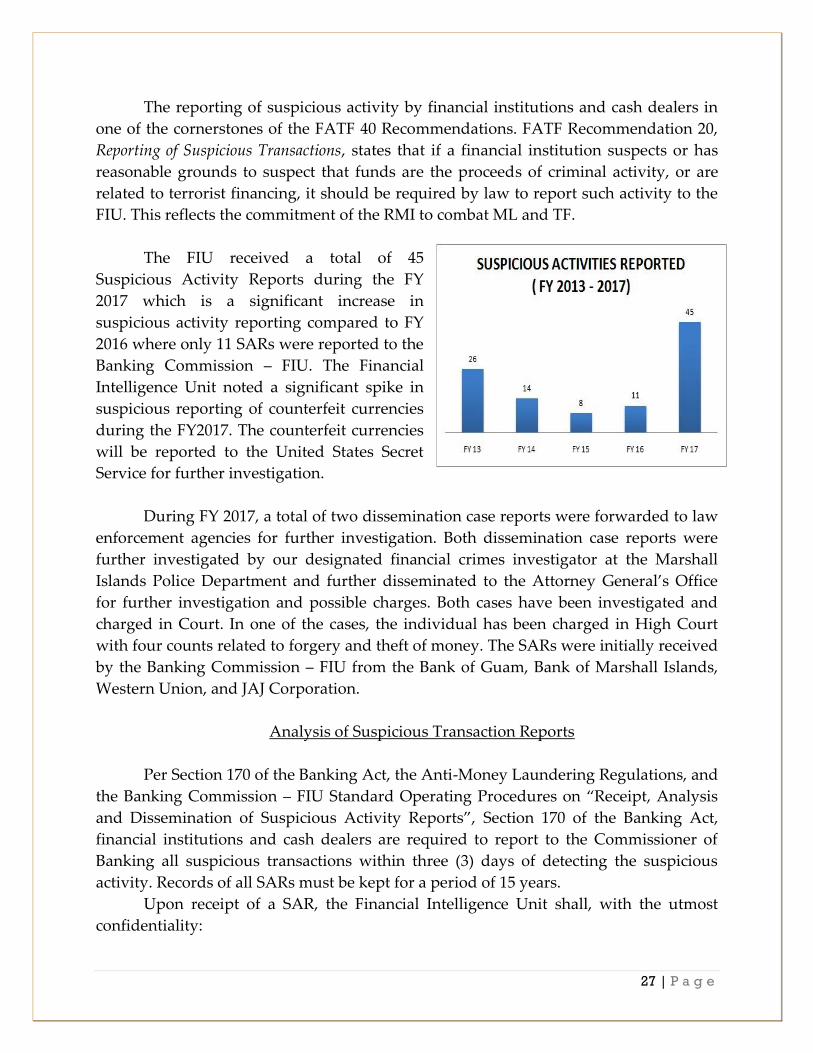

The reporting of suspicious activity by financial institutions and cash dealers in

one of the cornerstones of the FATF 40 Recommendations. FATF Recommendation 20,

Reporting of Suspicious Transactions, states that if a financial institution suspects or has

reasonable grounds to suspect that funds are the proceeds of criminal activity, or are

related to terrorist financing, it should be required by law to report such activity to the

FIU. This reflects the commitment of the RMI to combat ML and TF.

The FIU received a total of 45

Suspicious Activity Reports during the FY

2017 which is a significant increase in

suspicious activity reporting compared to FY

2016 where only 11 SARs were reported to the

Banking Commission – FIU. The Financial

Intelligence Unit noted a significant spike in

suspicious reporting of counterfeit currencies

during the FY2017. The counterfeit currencies

will be reported to the United States Secret

Service for further investigation.

During FY 2017, a total of two dissemination case reports were forwarded to law

enforcement agencies for further investigation. Both dissemination case reports were

further investigated by our designated financial crimes investigator at the Marshall

Islands Police Department and further disseminated to the Attorney General’s Office

for further investigation and possible charges. Both cases have been investigated and

charged in Court. In one of the cases, the individual has been charged in High Court

with four counts related to forgery and theft of money. The SARs were initially received

by the Banking Commission – FIU from the Bank of Guam, Bank of Marshall Islands,

Western Union, and JAJ Corporation.

Analysis of Suspicious Transaction Reports

Per Section 170 of the Banking Act, the Anti-Money Laundering Regulations, and

the Banking Commission – FIU Standard Operating Procedures on “Receipt, Analysis

and Dissemination of Suspicious Activity Reports”, Section 170 of the Banking Act,

financial institutions and cash dealers are required to report to the Commissioner of

Banking all suspicious transactions within three (3) days of detecting the suspicious

activity. Records of all SARs must be kept for a period of 15 years.

Upon receipt of a SAR, the Financial Intelligence Unit shall, with the utmost

confidentiality:

28 | P a g e

• Assign a unique reference number to the report, acknowledge receipt of the report, establish

an electronic record of the report in the Banking Commission Database, and ensure that the

report has been checked by the reporting institution’s Compliance Officer;

• Review the content of the report and determine whether any immediate action, as listed

under Section 1.4 and 1.5 of the Banking Commission – FIU Standard Operating Procedures

on “Receipt, Analysis, and Dissemination of Suspicious Activity Reports”, is required;

• Inquire further information from financial institutions or cash dealers, if necessary

• Request for background information from external agencies on the subject to see if there are

any previous reports and known criminal activity, both domestic and foreign; and

• If additional information gathered on SAR confirms the hypothesis developed, the SAR will

either be disseminated to the relevant LEA or filed away with the endorsement of the

Commissioner of Banking.

Dissemination of Financial Intelligence

Dissemination of financial intelligence to relevant law enforcement agencies is a

core function of the Banking Commission - FIU as stipulated under Section 167 of the

Banking Act. The FIU receives, analyses and disseminates financial intelligence to

relevant law enforcement, such as the Attorney General's Office, Auditor General's

Office, and Police Commission, enabling the investigation of predicate crimes, money

laundering and terrorist financing activities.

The FIU analyses suspicious transaction and currency transaction reports

received from financial institutions and cash dealers to develop intelligence.

Additionally, if there are reasonable grounds to suspect that a transaction is suspicious

and additional requested information from internal and external agencies confirm the

hypothesis developed, the FIU will prepare an investigative file and disseminate a

cover report to the relevant LEAs. Under Section 167 of the Act, the Commissioner of

Banking, in association with law enforcement, may conduct an investigation if there are

reasonable grounds to suspect that money laundering activity is occurring.

After the analysis of a SAR and the intelligence gathering from internal and

external agencies, the SARs that are not disseminated to LEAs are filed away for future

intelligence reference and analysis.

29 | P a g e

Domestic Coordination and Engagement

AML/CFT Working Group

There is an Adhoc AML/CFT Working Group that has been active in

coordinating all activities related to the strengthening of the RMI's AML/CFT regime, in

particular, dealing with FATF and APG related issues. The working group currently

comprises of the Commissioner of Banking, Attorney General, Police Commissioner,

Chief of Customs and Taxation, Trust Company of the Marshall Islands, and other

members from other government agencies that may join upon invitation. The AML/CFT

Working Group is currently striving to ensure full implementation of all 40 FATF

Recommendations and aims at developing an effective national system in place to

combat ML and TF.

The Adhoc AML/CFT Working Group is also responsible for the timely

rectification of all the deficiencies that are identified in the RMI's most recent Mutual

Evaluation Report 2011 conducted by Asia Pacific Group on Money Laundering

(APGML) in preparation of the RMI's next round of evaluations scheduled for 2020. The

AML/CFT Working Group is also responsible for the planning and organization of the

RMI's 1st National Risk Assessment, as required under Recommendation 1 of the FATF

40 Recommendations. Additionally, the Working Group is responsible for improving

the overall AML/CFT framework for the RMI aligning it with the existing international

standards for the purpose of combating financial crimes domestically and

internationally.

Counter-Terrorism Committee (CTC)

The Banking Commission - FIU is a member of the Counter-Terrorism

Committee, a committee overlooked by the Permanent Secretary of the Ministry of

Foreign Affairs, and Trade (MOFAT) and is responsible for countering terrorism

implementation strategies. CTC is currently chaired by Commissioner of Banking

Sultan T. Korean. During FY 2018, the Banking Commission - FIU continued to

contribute to the meetings and works of the CTC.

Other members of CTC include the Attorney General and Registrar of Domestic

Corporations, Police Commissioner, MOFAT Permanent Secretary, and the Trust

Company of the Marshall Islands - Registrar of Non-Domestic Corporations.

30 | P a g e

Investment Reform Working Group

The Investment Reform Working Group kick-started with a workshop conducted

by the Office of Commerce and Investment (OCI) on May 9, 2017, at MIR Jemanun

Room regarding the drafting of a Universal Form for Foreign Investment Business

Licenses (FIBL). The Universal Form is designed to expedite the application process for

setting up a business in the RMI by foreign investors.

It was agreed by all task force members

that RMI FIU and Marshall Islands Police

Department (MIPD), particularly Interpol are

key players for a foreign investment license

application to go through. Interpol will do

criminal background checks and RMI FIU will

provide financial clearance on FIBL

incorporator and shareholders to make sure

investment is not derived from illicit

activities. The task force is in the process of

finalizing the Universal Form which will be available online for foreign investors.

Per the suggestion of the Attorney General's Office and the Universal Form

Taskforce, the FIU is now required to provide financial clearance on all FIBL

applications. The FIU started receiving FIBL clearance requests in September 2017.

Credibility checks are conducted per the Banking Commission-FIU SOP on Due

Diligence Checks. Once checks have been conducted on both the legal and natural

persons involved, the Commissioner of Banking will sign off on whether the Banking

Commission - FIU has any objection over the establishment of the business. The

Financial Intelligence Unit received and processed twelve (12) financial background and

credibility checks at the request of the President’s Office, Attorney General’s Office,

Chief Secretary’s Office, FIBL Unit, and OCI.

The final universal form has been submitted to the FIBL Unit for final review and

approval by the Finance Minister and Secretary. Additionally, a Memorandum of

Understanding (MOU) between the Tier 1 agencies to establish a cooperative

relationship between all the agencies involved in the FIBL process has been completed

and ready for signing by Head of Departments. Tier 1 agencies comprise of the

following:

• Division of Immigration

31 | P a g e

• Division of Labor

• FIBL Registrar (Tax & Revenue)

• Marshall Islands Social Security Administration

• Attorney General's Office

• Marshall Islands Police Department (Interpol)

• RMI Banking Commission - FIU

Currency Declaration – Arrival & Departure Card

One of the key recommendations put forth in the RMI's Mutual Evaluations

Report 2011 is to rectify the deficiencies in the current Currency Declaration Act 2009 in

order to comply with Recommendation 32, Cash Couriers, of the FATF 40

Recommendation. A team comprising of the following government agencies, met

together to amend the current Currency Declaration Act (CDA) to address the

deficiencies in the Act:

i. Customs Division, Ministry of Finance, Banking & Postal,

ii. Financial Intelligence Unit of the Banking Commission, Ministry of Finance,

Banking & Postal,

iii. Division of Immigration, Ministry of Justice, Immigration & Labor, and

iv. Division of Agriculture & Quarantine, Ministry of Natural Resources &

Commerce.

Amendments were included in the CDA to include:

• Definition of natural, legal persons, and currency to include bearer

negotiable instruments;

• Declaration to include mail and cargo;

• Inclusion of legal persons to the CDA;

• Inclusion of RMI Banking Commission - FIU and Quarantine Officer as an

authorized officer under the CDA; and

• Immunity for an authorized officer.

The Currency Declaration (Amendment) Act 2019 is currently with the Committee of

Ways and Means for final review before submitting to Nitijela for voting. The team also

32 | P a g e

met to revise the current Arrival Card and to create a Departure Card for the RMI. The

team is later joined by the OCI and the Ministry of Health to collaborate together to

finalize the arrival and departure cards. The revised Arrival Card and the new

Departure Card are in their final revision stages.

A MOU for Inter-Agency Collaboration & Information Sharing on Matters

Related to Ports of Entry Declaration Forms between the listed members above,

including OCI and Ministry of Health to improve the border security control and

monitoring of all ports of entry and desire to share information and collaborate on

exchange of resources and intelligence to promote effectiveness and efficiency in their

respective mandates and efforts on the movement of dangerous and prohibited

merchandise, food and animal products and all forms of currency amounting to at least

$10,000.

1st National Risk Assessment (NRA)

At its meeting on August 22, 2017, the Cabinet approved the establishment of the

Republic of the Marshall Islands' National Risk Assessment Working Group (NRAWG)

comprising of key stakeholders from the government and private sectors as follows:

• Office of the Auditor General

• Banking Commission

• Immigration Division

• Judiciary/ Courts

• Kwajalein Atoll Local

Government

• Marshall Islands Development

Bank

• Tax and Customs, MOFBPS

• FIBL, MOFBPS

• Police Commission

• RMI Law Society

• Trust Company of the Marshall

Islands (Non-Resident Domestic

Corporate Registry and Maritime

Administrator)

• Ajejdrikdrik, Inc.

• Bank of Guam

• Bank of the Marshall Islands

• Enewetak Credit Union

• Family Mart

• Individual Assurance Company

(IAC)

• Jurelang, Alice, Jessica (JAJ)

Corporation

• Marshall Insurance Company

• Marshall Islands Service

Corporation

• Money Gram

• Moylan’s Insurance

• Western Union, and

• Chamber of Commerce

33 | P a g e

Identifying, assessing, and understanding ML and TF risks is an essential part of the

implementation and development of a national AML/CFT regime, which includes laws,

regulations, enforcement and other measures to mitigate ML/TF risks. The NRA will

assist the RMI Government in identifying ML risks and efficiently allocating its

resources to mitigate the identified risks, i.e., the risk-based approach – which is central

to the FATF standards set out in Recommendation 1.

NRA Team Leaders - Video Conference

with World Bank

The NRA is also important in

addressing the impact of the U.S. de-

risking by U.S banks on our banking

sector. The Banking Commission has

prioritized the NRA as a key strategy in

strengthening the AML/CFT regime of the

RMI and providing assurance to foreign

authorities that the country, its authorities,

and citizen are fully aware of the ML/TF threats and vulnerabilities in the system and

that appropriate actions are taken to mitigate the potential ML/TF risks.

The NRAWG Coordinators and Team Leaders met with Mr. Stuart Yikona and

Mr. Nigel Bartlett, Senior Financial Sector Specialists at the World Bank via a video

conference on September 28, 2017, at Banking Commission's Conference Room. During

the workshop, the date for the first workshop for all team members was agreed upon

and the full NRA tool was shared and discussed with the NRA Coordinators and Team

Leaders.

The First NRA Workshop organized by the

Marshall Islands Banking Commission – Financial

Intelligence Unit in coordination with the World

Bank was conducted at the International

Convention Center (ICC) on January 15-17, 2018.

The workshop familiarized the participants with

the NRA and risk-based approach concepts and

relevant documents, facilitate brainstorming and

exchange of news on ML/TF risks in the Marshall

Islands, and to introduce the National ML/TF risk

assessment tools and process. The sessions of the

workshop are designed as interactive work sessions to allow the participants to

comprehending the NRA tool and process.

34 | P a g e

Basic Investigations Program

Financial Intelligence Unit participated in the one-week Basic Investigations

Program conducted on February 13-18, 2018 at the Marshall Islands Resort by

Australian Federal Police and Marshall Islands Police Department.

The program is an in-country training

program based on the fundamental

principles and processes of investigating

criminal offenses. The program covers the

progressive investigation system from

receipt of the initial complaint through to

preparing a case file for prosecution and

giving evidence in Court. The program

provides participants with a thorough

foundation of investigative skills whilst

laying a solid platform to build on to

become an efficient and effective

investigator.

OECD Working Group – Global Forum on

Transparency and Exchange of Information for

Tax Purposes

The Banking Commission, as a member of the

OECD Working Group – Global Forum on

Transparency and Exchange of Information for

Tax Purposes collaborated with the other

members of the OECD Working Group to

prepare the Republic of the Marshall Islands for

the Mock On-site Visit on May 17-18, 2018. The

members of the OECD Working Group include

the Competent Authority – MOFBPS’ Tax Division, Attorney General’s Office, the

Banking Commission, Domestic Corporate Registry, Non-Resident Domestic Corporate

Registry, FIBL, and MISSA.

The OECD Working Group collaborated together to finalize the lengthy

questionnaire and prepare for the next round of Exchange of Information Request

(EOIR) Reviews for the Republic of the Marshall Islands.

35 | P a g e

International Engagement and Contribution

Workshop on Implementing the International AML/CFT Standards

The IMF Legal Department and the IMF-Singapore Regional Training Institute

(STI) jointly offered a one-week workshop on Implementing the International AML/CFT

Standards – Enhancing Entity Transparency during June 4-8, 2018. The objective

discussed issues and best practices related to managing the transparency of legal

persons and arrangements including: (i) the creation and registration of legal persons

and arrangements, (ii) types of registries and roles of registrars; (iii) the role of

gatekeepers; (iv) obligations of legal persons and arrangements; (v) legal persons and

arrangements as customers of financial institutions and designated non-financial

business or professions (DNFBPs); (vi) international cooperation; and (vii) effective

supervision and enforcement. The discussions of the issues assisted in the increase in

participants’’ understanding of the requirements of the revised international AML/CFT

standards, the 2012 FATF 40 Recommendations, and the 2013 Methodology for

Assessing Compliance with the 40 Recommendations and the Effectiveness of

AML/CFT Systems relating to entity transparency.

FATF TREIN – FATF Standards Training Course

The Financial Intelligence Unit Manager and Analyst attended the FATF

Standards Training Course facilitated by the FATF TREIN in Busan, the Republic of

Korea from September 3-7, 2018. The 5-day program promoted better understanding

and implementation of the FATF 40 Recommendations and Standards and provided

practical insights into the key areas of the FATF Recommendations, including:

36 | P a g e

• Risk in-context,

• International cooperation,

• Risk-based supervision,

• Preventative measures,

• Financial Intelligence & Investigations,

• Counter-Terrorism Financing,

including NPOs & Implementation of

Targeted Financial Sanctions,

• Counter-Proliferation Financing, and

• Beneficial Ownership.

Egmont Secure Web

The FIU continues to participate in activities of the Egmont Group of Financial

Intelligence Units. As a member of the Egmont Group of FIUs, the RMI is committed to

sharing information with other Egmont Group members when needed. During FY 2017,

the FIU continued to provide assistance and information to other Egmont Group

members upon request via Egmont Secure Web.

Per the Banking Commission - FIU Standard Operating Procedure, upon receipt

of a request by a foreign counterpart for assistance, the FIU, under the direction of the

Commissioner of Banking, shall enter data relative to the request into the International

Administrative Authority Spreadsheet with the name and address of the agency,

contact person, type of agency - whether administrative or investigative, and the type of

information jurisdiction is requesting. The FIU must ensure the authenticity, and

reasonableness of the request and respond to the request, in a timely manner.

During FY 2017, the FIU received a total of thirteen (13) incoming requests

through the Egmont Secure Web regarding beneficial ownership information on non-

resident domestic corporations registered with the Trust Company of the Marshall

Islands. Each request that came in sought for beneficial ownership information on one

or more non-resident domestic corporations. Each of those requests was responded to

in a timely manner through the cooperation of relevant agencies within the RMI.

Additionally, the FIU received thirty (30) spontaneous dissemination through the

Egmont Secure Web from our partner jurisdictions. The RMI-FIU made four (4)

outgoing requests to our partner FIU jurisdictions regarding possible a possible money

laundering case.

37 | P a g e

Egmont Secure Web FY 2017

Incoming Request 13

Outgoing Request 4

Spontaneous Dissemination 30

In 2012-2013, the FIU received a total of 30 incoming requests for information

from foreign counterparts and a total of 20 incoming requests received in 2014-2015. In

addition to receiving reports from financial institutions and cash dealers, one of the

FIU's most significant responsibilities is to respond to requests for information from

foreign partner jurisdictions. The Financial Intelligence Unit submitted the following

reports to Egmont: (i) The Biennial Census 2017 and (ii) World Bank – Egmont Group of

FIUs Joint Study on FIUs working with LEAs/Prosecutors.

Carnegie Mellon University Student Consultation to the Banking Commission –

Phase II

During the FY 2017, the Banking Commissioner Mr. Sultan Korean signed an MOU

with Carnegie Mellon University for Technical Assistance for troubleshooting and the

improvement of the current FIU database to include data mining and other additional

features to the FIU database on May 24,

2018.

The FIU engaged and assisted in the

Technical Assistance with Carnegie

Mellon University (Ms. Daisy Nkweteyim

and Mr. Nikolas Rebovich) to further

develop and troubleshoot the FIU

Database for CTR and SAR, including the

creation of forms and reports as well as

printing capabilities. Currently, reporting

entities, Bank of the Marshall Islands and

Bank of Guam, are submitting CTRs and

SARs online and are imported to the database that has more capabilities than before.

The FIU Database is now managed by

the FIU Analyst and is overseen by the

Head of FIU and FIU Manager. Tutorials

and guides were given by the Carnegie

Mellon University Consultants to the

Banking Commission – FIU and IT staff on

data modifications to make table, forms,

38 | P a g e

and reports in the database, how to import into the database and ways to identify and

fix importation errors, which was something the FIU lacked during Phase I of the

Database Consultation. The Consultants were able to troubleshoot the problems with

the FIU database and the [email protected] email, including the networking of

all departments of the Banking Commission.

Asia-Pacific Group (APG) on Money Laundering

The Asia Pacific Group on Money Laundering ("APGML") is an autonomous and

collaborative international organization currently comprising of 41 member countries.

The Republic of the Marshall Islands has been a member of the APG since June 2002.

Per Cabinet Minute 072 (2002), the Cabinet at its meeting on 23 May 2002,

endorsed the RMI's membership bid to join the APGML. CM 072 endorsed the

appointment of the Commissioner of Banking as the central contact person for the APG

Secretariat. The Police Commissioner, Chief of Customs and Taxation, Registrar of

Foreign and Domestic Corporations, and the Attorney General were all endorsed to

assist in all APG related initiatives. The Financial Intelligence Unit submitted the

following reports during the FY17, (i) FATF/APG Wildlife Crime Report, (ii) 2017

Typologies Report, and (iii)APG Annual Status Report.

APG/ FATF TREIN Typologies Workshop

The Financial Action Task Force Training and Research Institute (FATF-TREIN)

and the Asia/Pacific Group on Money Laundering hosted the 2017 Joint Typologies and

Building Workshop between November 13-16, 2017 in Busan, Korea.

The APG/FATF TREIN Typologies workshop brought together over 200 law

enforcement, prosecutors, financial intelligence unit and regulatory practitioners from

many of the 41 APG member jurisdictions, observer jurisdictions, and organizations, as

well as participants from non-government and private sector entities. The Typologies

workshop provided an opportunity for participants to discuss terrorist financing risks,

39 | P a g e

trends, and methodologies, policy issues emerging from those trends as well as other

challenged facing the regions. The workshop facilitated a valuable exchange of

expertise which will improve regional cooperation and implementation of the FATF

Recommendations. The workshop had three concurrent sessions that focused on: (i)

proliferation financing, (ii) human trafficking and people smuggling, and(iii)

investigating and prosecuting internet facilitated money laundering and terrorist

financing.

21st APG Annual Meeting and Technical Assistance Forum

The 21st APG Annual Meeting and Technical Assistance Forum 2018, consisted

of pre-plenary mutual evaluation-related meetings, working group and steering group

meetings, technical seminar, and plenary and technical assistance forum. 2018 APG

Annual Meeting was held in Soaltee Crowne Plaza, in Kathmandu, Nepal from July 21-

27, 2018. Financial Sector Development Manager represented the Republic of the

Marshall Islands during the 21st Annual APG Meeting in Kathmandu, Nepal.

40 | P a g e

IV. FINANCIAL SECTOR DEVELOPMENT (FSD)

Key Responsibilities

The key responsibilities of FSD are to assist the

Commissioner of Banking in:

(i) Establishment of a monetary authority per the Cabinet’s

adoption of a policy for the establishment that will

undertake all the necessary functions of a central bank

apart from the issue of domestic currency and conduct of

monetary policy;

(ii) Identification, development and implementation of key

strategies for financial sector development in the RMI and

collaborate with relevant stakeholders in the development

and implementation of the financial sector development

plan.

(iii) Act as a secondary contact with key organizations

such as the IMF, World Bank, Asian Development Bank,

and other key international organizations and

development partners for technical assistance engagement

and other related policy advice and issues with respect to

financial sector development;

(iv) Coordinate with international organizations with

respect to surveys and reports on global de-risking and

correspondent banking in the RMI, and assist in

identifying and developing a viable contingency plan for

the existing CBR arrangement between local banks and

U.S banks;

(v) Develop, compile and analyze financial data from the

financial institutions for the purpose of understanding the financial linkages

"The primary objective

of the Financial Sector

Development (FSD)

division of the Banking

Commission is to

oversee all activities

related to financial

sector development and

ensure the effective

implementation of key

strategies for Financial

Sector Development in

the RMI."

41 | P a g e

of the RMI financial system with the global financial

system and the impact of global de-risking on the

domestic financial sector.

Monetary Authority (MA), Access to the U.S. Financial

System and Financial Sector Challenges

The RMI Cabinet in December 2015, adopted the

policy to establish a Monetary Authority which is

envisaged to strengthen links of the RMI financial system

to the international and U.S. financial system. The