fiscal policy, monetary policy and inequality in the uk · paul johnson 19/05/2017 fiscal policy,...

TRANSCRIPT

Paul Johnson 19/05/2017

Fiscal Policy, Monetary Policy and Intergenerational Inequality in the UK

Output per head only just above 2008Q1 level

© Institute for Fiscal Studies

90

100

110

120

130

140

2008

Q1

2009

Q1

2010

Q1

2011

Q1

2012

Q1

2013

Q1

2014

Q1

2015

Q1

2016

Q1

2017

Q1

2018

Q1

2019

Q1

2020

Q1

2021

Q1

2022

Q1

2008

Q1

= 10

0

Source: Office for Budget Responsibility

GDP per person aged 16+

2% per year growth

15% gap

And forecast growth also weak …

© Institute for Fiscal Studies

90

100

110

120

130

140

2008

Q1

2009

Q1

2010

Q1

2011

Q1

2012

Q1

2013

Q1

2014

Q1

2015

Q1

2016

Q1

2017

Q1

2018

Q1

2019

Q1

2020

Q1

2021

Q1

2022

Q1

2008

Q1

= 10

0

Source: Office for Budget Responsibility

GDP per person aged 16+

2% per year growth 18% gap

Income and earnings inequality down recently

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

3.0

3.2

3.4

3.6

3.8

4.0

4.2

4.4

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

90:10 ratio for UK Net Equivalised Household income and Gross Weekly Earnings

Earnings

Source: Family Expenditure Survey; Family Resources Survey; Annual Survey of Hours and Earnings

Income and earnings inequality down recently

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

3.0

3.2

3.4

3.6

3.8

4.0

4.2

4.4

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

90:10 ratio for UK Net Equivalised Household income and Gross Weekly Earnings

Income

Earnings

Source: Family Expenditure Survey; Family Resources Survey; Annual Survey of Hours and Earnings

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0.20

0.22

0.24

0.26

0.28

0.30

0.32

0.34

0.36

0.38

1961 1966 1971 1976 1981 1986 1991 1996 2001 2006 2011

90

:10

ra

tio

Gin

i co

eff

icie

nt

Gini coefficient

90:10 ratio

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0.20

0.22

0.24

0.26

0.28

0.30

0.32

0.34

0.36

0.38

1961 1966 1971 1976 1981 1986 1991 1996 2001 2006 2011

90

:10

ra

tio

Gin

i co

eff

icie

nt

Source: Figures 3.6 and 3.7 of Living Standards, Poverty and Inequality: 2016

Having grown sharply over 1980s

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

1

2

3

4

5

6

7

8

9

10

1961 1966 1971 1976 1981 1986 1991 1996 2001 2006 2011

Top

1% s

hare

90:1

0 ra

tio

90:10 ratio

Top 1% share

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

1

2

3

4

5

6

7

8

9

10

1961 1966 1971 1976 1981 1986 1991 1996 2001 2006 2011

Top

1% s

hare

90:1

0 ra

tio

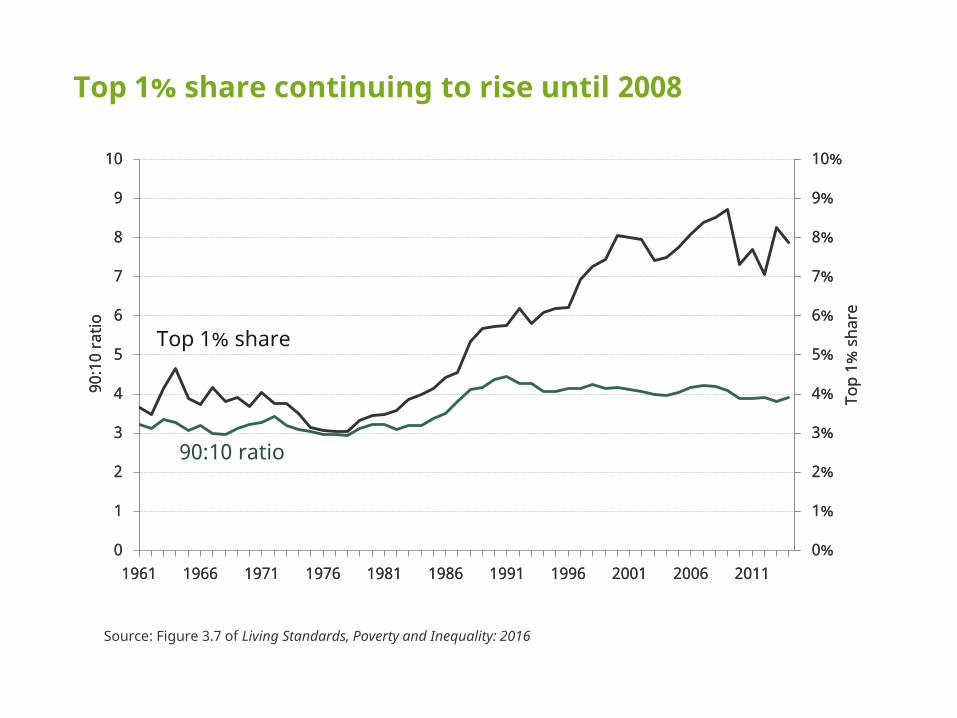

Source: Figure 3.7 of Living Standards, Poverty and Inequality: 2016

Top 1% share continuing to rise until 2008

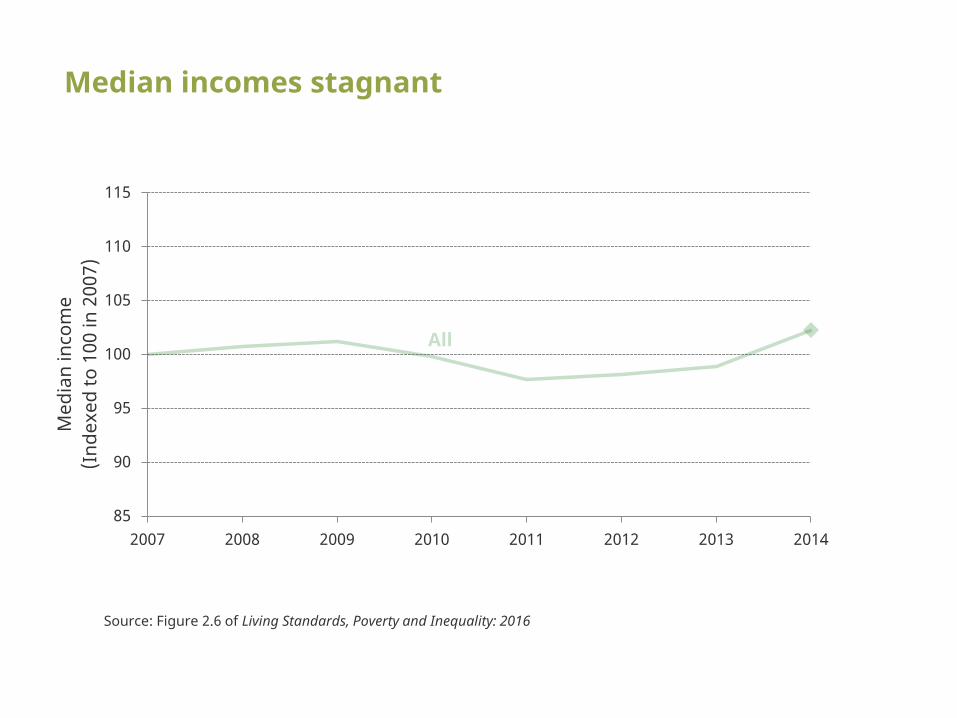

Median incomes stagnant

85

90

95

100

105

110

115

2007 2008 2009 2010 2011 2012 2013 2014

Med

ian

inco

me

(Ind

exed

to 1

00 in

200

7)

Source: Figure 2.6 of Living Standards, Poverty and Inequality: 2016

Much worse for the young

85

90

95

100

105

110

115

2007 2008 2009 2010 2011 2012 2013 2014

Med

ian

inco

me

(Ind

exed

to 1

00 in

200

7)

-7%

Source: Figure 2.6 of Living Standards, Poverty and Inequality: 2016

22-30

Much better for the old

85

90

95

100

105

110

115

2007 2008 2009 2010 2011 2012 2013 2014

Med

ian

inco

me

(Ind

exed

to 1

00 in

200

7)

-7%

0%

Source: Figure 2.6 of Living Standards, Poverty and Inequality: 2016

22-30

31-59

60+

+11%

The distribution of wealth

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

And concentrated at older ages

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

£0

£100,000

£200,000

£300,000

£400,000

£500,000

£600,000

£700,000

£800,000

£900,000

16

-24

25

-34

35

-44

45

-54

55

-64

65

-74

75

-84

85

+

All

Net

ho

us

eh

old

wealth

Age group

Mean p25 p75 Median

Of course the old hold the cash

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

£0

£5,000

£10,000

£15,000

£20,000

£25,000

£30,000

£35,000

£40,000

£45,000

20-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75-79 80+

Cash

/nea

r ca

sh h

oldi

ngs

Age-group

25th percentile Median 75th percentile

But it’s the young who can’t build up savings

If you work until 67, die at 90, and have earnings that grow 2% p.a.

With 4% real interest rate you need to save 10% of income to replace 50% in retirement

With 0% real interest rate saving rate needs to be 30%

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

The old also hold the housing wealth

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

16-24 25-34 35-44 45-64 65-74 75+

Perc

enta

ge o

f ind

ivid

uals

who

ow

n th

eir

own

hom

e

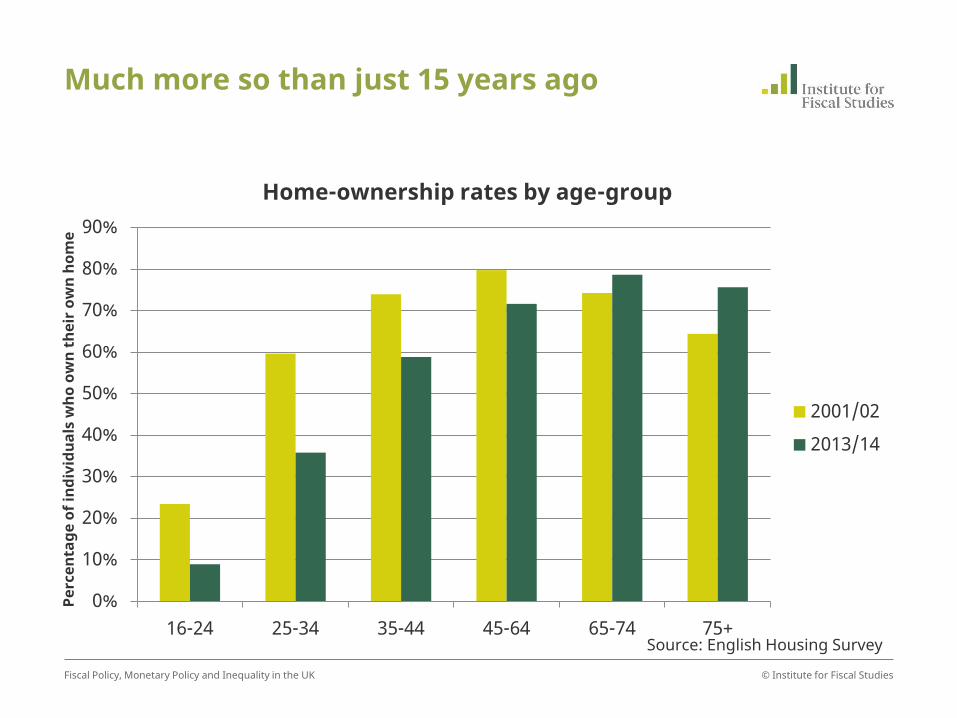

Home-ownership rates by age-group

2013/14

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

Source: English Housing Survey

Much more so than just 15 years ago

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

16-24 25-34 35-44 45-64 65-74 75+

Perc

enta

ge o

f ind

ivid

uals

who

ow

n th

eir

own

hom

e

Home-ownership rates by age-group

2001/02

2013/14

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

Source: English Housing Survey

Younger cohorts much less likely to be owner occupiers

20%

30%

40%

50%

60%

70%

80%

90%

25 30 35 40 45 50 55 60

Hom

eow

ners

hip

rate

Age

1930s

1940s 1950s

1960s 1970s

Early 1980s

And DB pensions have collapsed

0%

10%

20%

30%

40%

50%

60%

16 - 21 22 - 29 30 - 39 40 - 49 50 - 54 55 - 59 60 - 64 Age-group of employee

Percentage of employee jobs in a defined benefit pension scheme

1997

2016

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

Source: ONS

Proportion of private sector employees in DB scheme 1997 and 2015

© Institute for Fiscal Studies

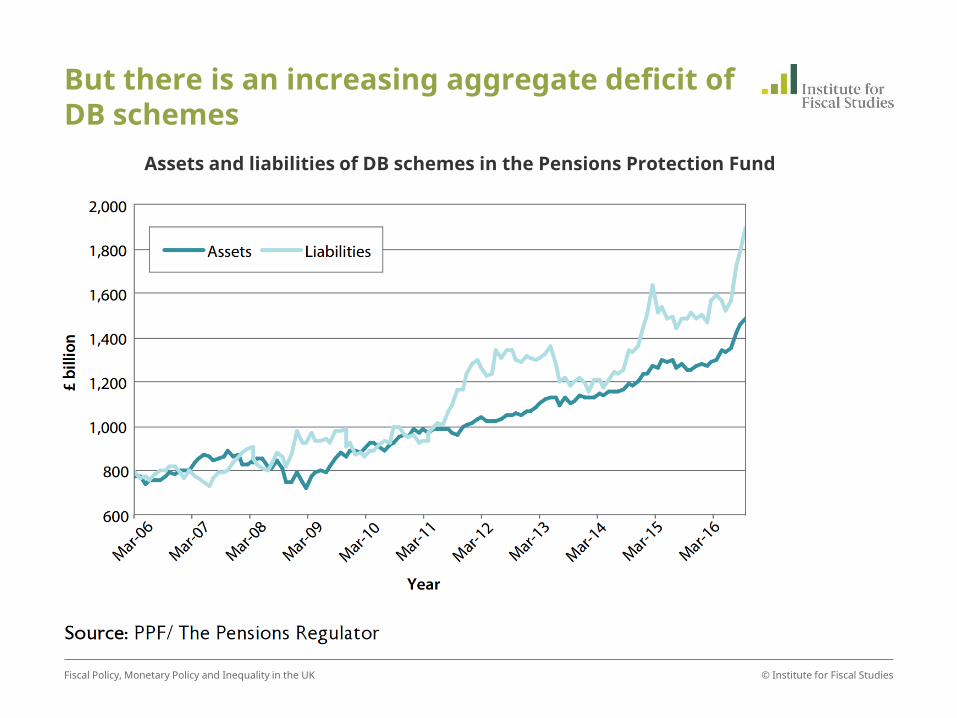

But there is an increasing aggregate deficit of DB schemes

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

Assets and liabilities of DB schemes in the Pensions Protection Fund

Overall younger cohorts accumulating less wealth

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

Loose monetary policy supporting tight fiscal policy

30%

32%

34%

36%

38%

40%

42%

44%

46%

2007

-08

2008

-09

2009

-10

2010

-11

2011

-12

2012

-13

2013

-14

2014

-15

2015

-16

2016

-17

2017

-18

2018

-19

2019

-20

2020

-21

2021

-22

Latest outturn and forecast for total Government spending and receipts

Spending

Receipts

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

Source: OBR

Crucial point: after 8 years of “austerity” the size of the state is just back at pre crisis levels

© Institute for Fiscal Studies Budget 2017: the fastest u-turn since Budget 2016?

39.0 39.3

37

38

39

40

41

42 Sp

endi

ng in

200

7–08

Pens

ione

r ben

efits

Hea

lth

Ove

rsea

s ai

d

Wor

king

-age

be

nefit

s

Deb

t int

eres

t

Scho

ols

Def

ence

Oth

er

Publ

ic o

rder

& s

afet

y

Spen

ding

in 2

016–

17

Per c

ent o

f nat

iona

l inc

ome

Increases in spending on pensions and health offset cuts elsewhere

© Institute for Fiscal Studies Budget 2017: the fastest u-turn since Budget 2016?

39.0 39.3

+0.8

+0.7

+0.3 0.2 –0.2

–0.3 –0.3

–0.4 –0.5

37

38

39

40

41

42 Sp

endi

ng in

200

7–08

Pens

ione

r ben

efits

Hea

lth

Ove

rsea

s ai

d

Wor

king

-age

be

nefit

s

Deb

t int

eres

t

Scho

ols

Def

ence

Oth

er

Publ

ic o

rder

& s

afet

y

Spen

ding

in 2

016–

17

Per c

ent o

f nat

iona

l inc

ome

Tax and benefit changes have hit the bottom half and the very top

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

Perc

enta

ge c

hang

e in

net

hou

seho

ld in

com

e

Income decile

Percentage change in net household income as a result of tax and benefit policies implemented under the coalition government

Benefits

Taxes

All

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

Source: IFS

Pensioners protected, those with children hit hardest

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

Perc

enta

ge c

hang

e in

net

hou

seho

ld in

com

e

Income decile

Impact of coalition government tax and benefit policies by group

Working-age without children Working-age with children

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

Source: IFS

Fiscal policy has worked with monetary policy and underlying trends to protect the old and hit the young

1. Triple lock means basic state pension has grown 9%pts more than average earnings since 2010-11.

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

The triple lock

85

90

95

100

105

110

115

Inde

x of

sta

te p

ensi

on le

vel

Growth rate of basic state pension compared to average earnings (2010-11 level = 100)

Actual

Earnings

Double Lock

CPI

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

Source: OBR and author’s calculations

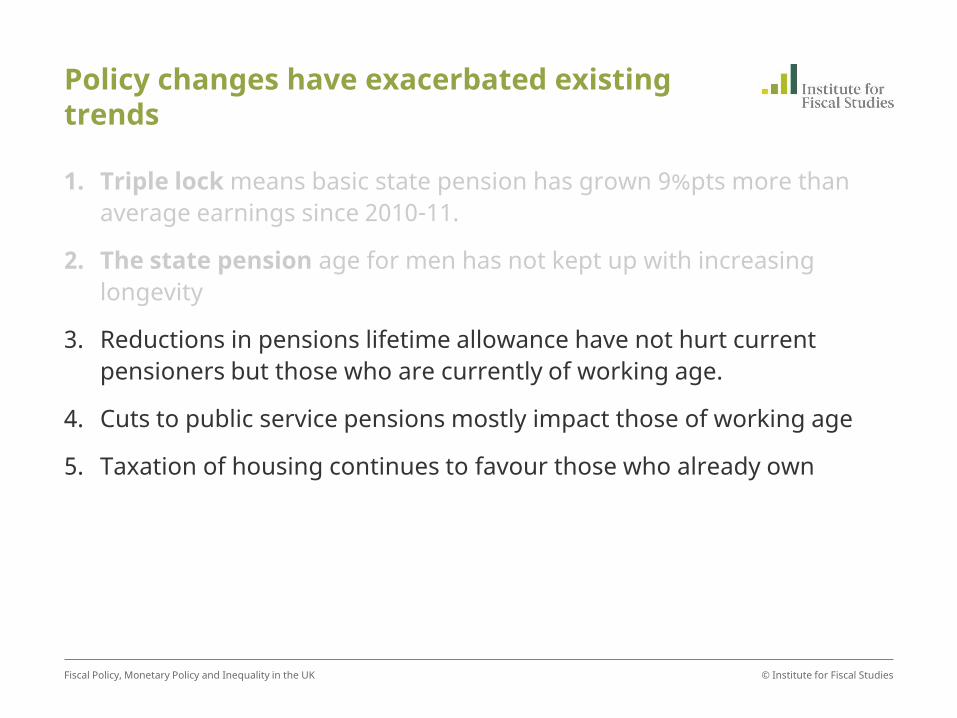

Policy changes have exacerbated existing trends

1. Triple lock means basic state pension has grown 9%pts more than average earnings since 2010-11.

2. The state pension age for men has not kept up with increasing longevity

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

Dramatic increase in numbers living longer in recent decades

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

65 70 75 80 85 90 95 100

Proportion of male 65-year-olds surviving to given age

65 in 1987

65 in 2017

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

Source: ONS Life Tables

Policy changes have exacerbated existing trends

1. Triple lock means basic state pension has grown 9%pts more than average earnings since 2010-11.

2. The state pension age for men has not kept up with increasing longevity

Without further rises in the state pension age, pension spending will rise rapidly as a share of GDP, and require other spending cuts or tax rises.

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

Even without triple lock, state pension spending will rise as a share of GDP

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

2016

-17

2018

-19

2020

-21

2022

-23

2024

-25

2026

-27

2028

-29

2030

-31

2032

-33

2034

-35

2036

-37

2038

-39

2040

-41

2042

-43

2044

-45

2046

-47

2048

-49

2050

-51

2052

-53

2054

-55

2056

-57

2058

-59

2060

-61

2062

-63

2064

-65

2066

-67

Perc

enta

ge p

oint

s of

GD

P

Long-term State Pension Spending Projections

FSR 2017 central

FSR 2017 (No triple lock)

FSR 2017 (Only legislated changes to SPA)

Source: OBR Fiscal Sustainability Report

Policy changes have exacerbated existing trends

1. Triple lock means basic state pension has grown 9%pts more than average earnings since 2010-11.

2. The state pension age for men has not kept up with increasing longevity

3. Reductions in pensions lifetime allowance have not hurt current pensioners but those who are currently of working age.

4. Cuts to public service pensions mostly impact those of working age

5. Taxation of housing continues to favour those who already own

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

Fiscal attempts to offset have been minimal, counter-productive or ineffective

1. Ending requirement to annuitise pensions

response to low interest rates

2. “Help-to-buy” intended to help first time buyers

has likely raised prices

3. Attempts to increase housebuilding ineffective

4. Taxes on buy-to-let as a ‘third best’ response

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK

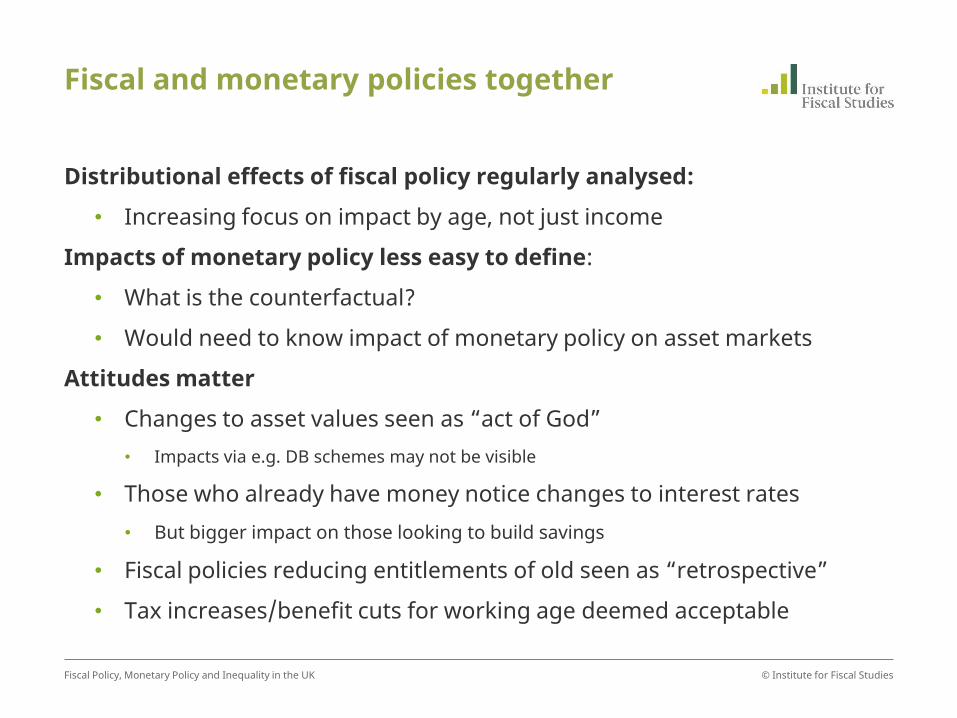

Fiscal and monetary policies together

Distributional effects of fiscal policy regularly analysed:

• Increasing focus on impact by age, not just income

Impacts of monetary policy less easy to define:

• What is the counterfactual?

• Would need to know impact of monetary policy on asset markets

Attitudes matter

• Changes to asset values seen as “act of God” • Impacts via e.g. DB schemes may not be visible

• Those who already have money notice changes to interest rates • But bigger impact on those looking to build savings

• Fiscal policies reducing entitlements of old seen as “retrospective”

• Tax increases/benefit cuts for working age deemed acceptable

© Institute for Fiscal Studies Fiscal Policy, Monetary Policy and Inequality in the UK