first.doc 97

DESCRIPTION

kjkjkjTRANSCRIPT

CHAPTER-4ANALYSES &

INTERPRATION

50

AnalysisStatistics

the number of the queue should be increased

various schemeo

f the bank are attractive

to the custome

r

account

oppening

system is

eassy

clients are

satisfied with

employee's

behaviour

yearly account maintan

ance charge is reasona

ble

(house loan)interest rate

is acceptab

le

advertisement/

promotional activities

are satisfied

online banking facilities

are adequat

e

loan processing

is easier then other

bank

overall bankin

g activitie

s are satisfie

d

location of the bank is

suitableN Vali

d50 50 50 49 50 50 50 50 50 50 50

Missing

0 0 0 1 0 0 0 0 0 0 0

Mean 4.0200 4.0800 4.2000 4.1224 3.2400 3.1800 3.4800 3.5000 3.4200 3.9200 4.4200Median 4.0000 4.0000 4.0000 4.0000 3.0000 3.0000 3.0000 4.0000 3.0000 4.0000 5.0000Mode 4.00 4.00 4.00 4.00 4.00(a) 3.00 3.00 4.00 3.00 4.00 5.00Std. Deviation .76904 .72393 .72843 .88111 1.06061 .74751 .67733 .99488 .83520 .48823 .73095Variance .59143 .52408 .53061 .77636 1.12490 .55878 .45878 .98980 .69755 .23837 .53429Range 4.00 3.00 3.00 3.00 3.00 3.00 3.00 3.00 3.00 3.00 3.00Minimum 1.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00 2.00Maximum 5.00 5.00 5.00 5.00 5.00 5.00 5.00 5.00 5.00 5.00 5.00Sum 201.00 204.00 210.00 202.00 162.00 159.00 174.00 175.00 171.00 196.00 221.00

A Multiple modes exist. The smallest value is shownComment: The table shows that all the sample size is counted in research that means no one is missing. Here higher mean are located under account opening system is easy& location of the bank is suitable. Higher modes are Account opening system is easy& location of the bank is suitable. Standard Deviation is lower (0.48823) in overall banking activities are satisfied. Lower Standard Deviation indicate higher acceptance. So, we conclude that here overall banking activities are highly satisfied

51

Factor analysis

KMO and Bartlett's Test

Kaiser-Meyer-Olkin Measure of Sampling Adequacy..495

Bartlett's Test of Sphericity

Approx. Chi-Square

165.575

Df 55 Sig. .000

Kaiser- Meyer- Olkin (KMO) measure of sampling adequacy represents that factor analysis is not appropriate because the calculated value 0.495 is not between (0.5 – 1.0). If the value were grater then 0.5 it could be appropriate.

52

Correlation Matrix(a)

the number of the queue should

be increase

d

various of the

bank are attractive

to the customer

account

oppening

system is

eassy

clients are

satisfied with

employee's

behaviour

yearly account maintan

ance charge

is reasona

ble

(house loan)interest

rate is acceptable

advertisement/promoti

onal activitie

s are satisfied

online banking facilities

are adequat

e

loan processi

ng is easier then other bank

overall banking activitie

s are satisfied

location of the

bank is suitabl

eCorrelation

the number of the queue should be increased

1.000 .474 .357 -.125 -.006 -.149 .335 .335 -.045 .059 -.016

various of the bank are attractive to the customer

.474 1.000 .433 .243 .243 .236 -.040 .285 .012 .365 .088

account oppening system is eassy

.357 .433 1.000 .121 .126 -.219 .004 .483 -.070 .047 .143

clients are satisfied with employee's behaviour

-.125 .243 .121 1.000 .081 -.066 -.102 -.234 .269

.023

.142

yearly -.006 .243 .126 .081 1.000 .595 -.097 .343 .501 .075 -.338

53

account maintanance charge is reasonable

(house loan)interest rate is acceptable

-.149 .236 -.219 -.066 .595 1.000 .024 .154 .438 .265 -.257

advertisement/promotional activities are satisfied

.335 -.040 .004 -.102 -.097 .024 1.000 .130 .153 -.003 -.137

online banking facilities are adequate

.335 .285 .483 -.234 .343 .154 .130 1.000 .079 .125 -.036

loan processing is easier then other bank

-.045 .012 -.070 .269 .501 .438 .153 .079 1.000 .233 -.491

overall banking activities are satisfied

.059 .365 .047 .023 .075 .265 -.003 .125 .233 1.000

-.246

54

location of the bank is suitable

-.016 .088 .143 .142 -.338 -.257 -.137 -.036 -.491 -.246 1.000

Sig. (1-tailed)

the number of the queue should be increased

.000 .006 .195 .485 .154 .009 .009 .379 .344 .458

various of the bank are attractive to the customer

.000 .001 .046 .046 .051 .392 .023 .466 .005 .273

account oppening system is eassy

.006 .001 .203 .193 .065 .488 .000 .316 .374 .164

clients are satisfied with employee's behaviour

.195 .046 .203 .290 .327 .243 .052 .031 .436 .165

yearly account maintanance charge is reasonable

.485 .046 .193 .290 .000 .253 .008 .000

.304

.009

55

(house loan)interest rate is acceptable

.154 .051 .065

.327

.000 .435 .145 .001 .033 .037

advertisement/promotional activities are satisfied

.009 .392 .488 .243 .253 .435 .187 .147 .493 .175

online banking facilities are adequate

.009 .023 .000 .052 .008 .145 .187 .294 .197 .402

loan processing is easier then other bank

.379 .466 .316 .031 .000 .001 .147 .294 .053 .000

overall banking activities are satisfied

.344 .005 .374 .436 .304 .033 .493 .197 .053 .044

location of the bank is suitable

.458 .273 .164 .165 .009 .037 .175 .402 .000 .044

a Determinant = .022

56

Communalities

Initial Extractionthe number of the queue should be increased 1.000 .726

various scheme of the bank are attractive to the customer 1.000 .817

account oppening system is eassy 1.000 .721

clients are satisfied with employee's behaviour 1.000 .924

yearly account maintanance charge is reasonable 1.000 .846(house loan)interest rate is acceptable 1.000 .702

advertisement/promotional activities are satisfied 1.000 .750

online banking facilities are adequate 1.000 .757

loan processing is easier then other bank 1.000 .811

overall banking activities are satisfied 1.000 .829

location of the bank is suitable 1.000 .601

Extraction Method: Principal Component Analysis.

Under Communalities, Initial column, it can be seen that the communality for each variable advertisement/promotional activities are satisfied to the overall banking activities, is 1.0 as unites were inserted in the diagonal of the correlation matrix. And the second column Extraction’s variables are different because all of the variances are associated with the variables are not explained unless all the factors are retained.

57

Total Variance Explained

Component Initial Eigen values Extraction Sums of Squared Loadings Rotation Sums of Squared Loadings

Total% of

Variance Cumulative % Total % of VarianceCumulative

% Total % of VarianceCumulative

%1 2.659 24.177 24.177 2.659 24.177 24.177 2.393 21.750 21.7502 2.180 19.820 43.997 2.180 19.820 43.997 2.156 19.601 41.3523 1.464 13.313 57.310 1.464 13.313 57.310 1.339 12.172 53.5244 1.150 10.451 67.761 1.150 10.451 67.761 1.299 11.807 65.3315 1.030 9.361 77.122 1.030 9.361 77.122 1.297 11.791 77.1226 .801 7.281 84.4037 .635 5.774 90.1778 .381 3.461 93.6389 .299 2.721 96.35910 .244 2.221 98.58011 .156 1.420 100.000

Extraction Method: Principal Component Analysis.

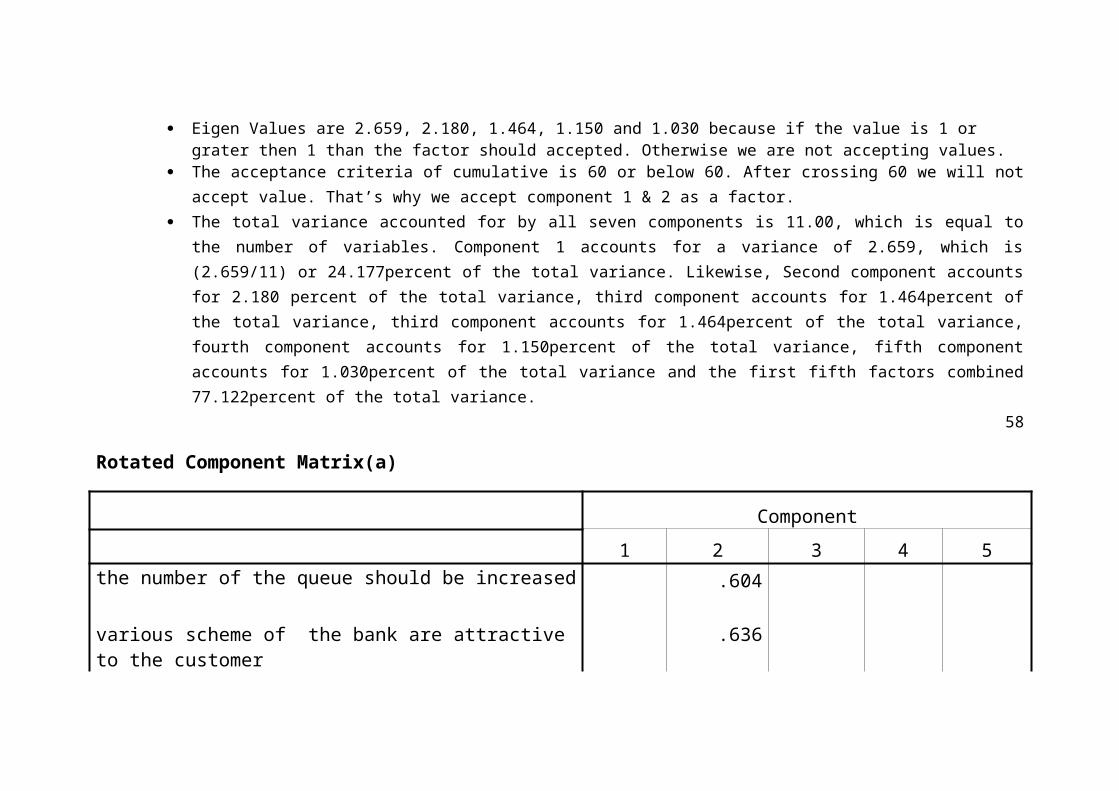

Eigen Values are 2.659, 2.180, 1.464, 1.150 and 1.030 because if the value is 1 or grater then 1 than the factor should accepted. Otherwise we are not accepting values.

The acceptance criteria of cumulative is 60 or below 60. After crossing 60 we will not accept value. That’s why we accept component 1 & 2 as a factor.

The total variance accounted for by all seven components is 11.00, which is equal to the number of variables. Component 1 accounts for a variance of 2.659, which is (2.659/11) or 24.177percent of the total variance. Likewise, Second component accounts for 2.180 percent of the total variance, third component accounts for 1.464percent of the total variance, third component accounts for 1.464percent of the total variance, fourth component accounts for 1.150percent of the total variance, fifth component accounts for 1.030percent of the total variance and the first fifth factors combined 77.122percent of the total variance.

58

Rotated Component Matrix(a)

Component

1 2 3 4 5the number of the queue should be increased .604

various scheme of the bank are attractive to the customer.636

account oppening system is eassy.827

clients are satisfied with employee's behaviour.955

yearly account maintanance charge is reasonable .841

(house loan)interest rate is acceptable .753

advertisement/promotional activities are satisfied .861

online banking facilities are adequate .737

loan processing is easier then other bank .778

overall banking activities are satisfied .892

location of the bank is suitable-.603

59

Rotated Component Matrix(a)

Component

1 2 3 4 5the number of the queue should be increased .604

various scheme of the bank are attractive to the customer.636

account oppening system is eassy.827

clients are satisfied with employee's behaviour.955

yearly account maintanance charge is reasonable .841

(house loan)interest rate is acceptable .753

advertisement/promotional activities are satisfied .861

online banking facilities are adequate .737

loan processing is easier then other bank .778

overall banking activities are satisfied .892

location of the bank is suitable-.603

60

Extraction Method: Principal Component Analysis. Rotation Method: Varimax with Kaiser Normalization.a Rotation converged in 8 iterations.

Factor-1: Has high coefficients for (yearly account maintenance charge,(house loan) interest rate, loan processing is easier and location of the bank is suitable).Therefore, this factor indicates as actual cost factor.

Factor-2: Is highly related for (the number of the queue, various scheme of the bank, account opening system is easy and online banking facilities) Thus, factor 2 indicates as actual benefit factor.

Factor-3: Is highly related for (advertisement and promotional activities are satisfied).Thus, factor 3 indicates as actual benefit factor.

Factor-4: Has high coefficients for (overall banking activities are satisfied).Therefore, this factor indicates as actual benefit factor.

Factor-5: Is highly related for (clients are satisfied with employee’s behavior).Thus, factor 5 indicates as actual benefit factor.

61

Component Transformation Matrix

Extraction Method: Principal Component Analysis. Rotation Method: Varimax with Kaiser Normalization.

62

Component 1 2 3 4 51 .796 .446 .143 .381 .0372 -.533 .830 .134 .093 -.0313 -.042 .090 -.675 .167 .7114 -.163 -.225 .689 .285 .6065 .233 .231 .175 -.858 .353

Descriptive Statistics

N RangeMinimu

mMaximu

m Sum MeanStd.

Deviation Variancelocation of the bank is suitable 50 3.00 2.00 5.00 221.00 4.4200 .73095 .534

account oppening system is eassy 50 3.00 2.00 5.00 210.00 4.2000 .72843 .531

clients are satisfied with employee's behaviour

49 3.00 2.00 5.00 202.00 4.1224 .88111 .776

various scheme of the bank are attractive to the customer

50 3.00 2.00 5.00 204.00 4.0800 .72393 .524

the number of the queue should be increased

50 4.00 1.00 5.00 201.00 4.0200 .76904 .591

overall banking activities are satisfied 50 3.00 2.00 5.00 196.00 3.9200 .48823 .238

online banking facilities are adequate 50 3.00 2.00 5.00 175.00 3.5000 .99488 .990

advertisement/promotional activities are satisfied

50 3.00 2.00 5.00 174.00 3.4800 .67733 .459

loan processing is easier then other bank

50 3.00 2.00 5.00 171.00 3.4200 .83520 .698

yearly account maintanance charge is reasonable 50 3.00 2.00 5.00 162.00 3.2400 1.06061 1.125

(house loan)interest rate is acceptable 50 3.00 2.00 5.00 159.00 3.1800 .74751 .559

Valid N (listwise) 49

63

The number of the queue should be increased

Frequency PercentValid

PercentCumulative

PercentValid strongly agree 12 24.0 24.0 24.0 agree 29 58.0 58.0 82.0 neutral 8 16.0 16.0 98.0 strongly disagree 1 2.0 2.0 100.0

Total 50 100.0 100.0

Comment: 58.00% of the respondents are responding that number of the queue should be increased in ucbl. But 16.00% of the respondent is neutral. So we can say that most of the respondent recommends That number of the queue should be increased in ucbl

64

Various scheme of the bank are attractive to the customer

Frequency PercentValid

PercentCumulative

PercentValid strongly

agree13 26.0 26.0 26.0

agree 30 60.0 60.0 86.0 neutral 5 10.0 10.0 96.0 disagree 2 4.0 4.0 100.0 Total 50 100.0 100.0

Comment: 60.00% of the respondents are responding that various scheme of the bank are attractive in ucbl. But 10.00% of the respondent is neutral. So we can say that most of the respondent recommends that various scheme of the bank are attractive in ucbl

65

account opening system is easy

Freque

ncyPercent

Valid Percent

Cumulative Percent

Valid strongly agree 17 34.0 34.0 34.0 agree 28 56.0 56.0 90.0 neutral 3 6.0 6.0 96.0 disagree 2 4.0 4.0 100.0 Total 50 100.0 100.0

Comment: 56.00 % of the respondents are agreed & 34.00% of the respondents are

strongly agreed with the statement that account opening system is easy in ucbl. But 6.00% of the respondent is neutral. So we can say that most of the respondent recommends that account opening system is easy in ucbl.

66

clients are satisfied with employee's behaviour

Freque

ncyPercen

tValid

Percent

Cumulative

PercentValid strongly

agree18 36.0 36.7 36.7

agree 23 46.0 46.9 83.7neutral 4 8.0 8.2 91.8disagree

4 8.0 8.2 100.0

Total 49 98.0 100.0Missing System 1 2.0Total 50 100.0

Comment: 46.00 % of the respondents are agreed & 36.00% of the respondents are

strongly agreed with the statement that client is satisfied with employee’s behavior. But 8.00% of the respondent is neutral. So we can say that most of the respondent recommends that they are satisfied with employee’s behavior in ucbl.

67

yearly account maintanance charge is reasonable

Frequen

cy PercentValid

PercentCumulative Percent

Valid strongly agree

6 12.0 12.0 12.0

agree 17 34.0 34.0 46.0neutral 10 20.0 20.0 66.0disagree 17 34.0 34.0 100.0Total 50 100.0 100.0

Comment: 34.00 % of the respondents are agreed & 20.00% of the respondents are neutral with the statement that yearly account maintenance is reasonable. But 34.00% of the respondent is disagreeing. So we can say that most of the respondent recommends that they are satisfied /dissatisfied in ucbl yearly service charge.

68

(House loan)interest rate is acceptable

Freque

ncy PercentValid

PercentCumulative

PercentValid strongly

agree2 4.0 4.0 4.0

agree 13 26.0 26.0 30.0 neutral 27 54.0 54.0 84.0 disagree 8 16.0 16.0 100.0 Total 50 100.0 100.0

Comment: 26.00% of the respondents are agreeing with the statement that (house loan) interest rate is acceptable in ucbl. But 54.00% of the respondent is neutral. So we can say that most of the respondent recommends that they are not understand about house lone interest rate in ucbl.

69

advertisement/promotional activities are satisfied

Frequency PercentValid

PercentCumulative

PercentValid strongly

agree3 6.0 6.0 6.0

agree 20 40.0 40.0 46.0 neutral 25 50.0 50.0 96.0 disagree 2 4.0 4.0 100.0 Total 50 100.0 100.0

Comment: 40.00% of the respondents are agreeing with the statement that advertisement/promotional activities are satisfied in ucbl. But 50.00% of the respondent is neutral. So we can say that most of the respondent recommends that they are not understand about the advertisement/promotional activities in ucbl.

70

Online banking facilities are adequate

Frequency PercentValid

PercentCumulative

PercentValid strongly

agree7 14.0 14.0 14.0

agree 22 44.0 44.0 58.0 neutral 10 20.0 20.0 78.0 disagree 11 22.0 22.0 100.0 Total 50 100.0 100.0

Comment: 44.00 % of the respondents are agreed & 20.00% of the respondents are neutral with the statement that online banking facilities are adequate in ucbl. But 22.00% of the respondent is disagreeing. So we can say that most of the respondent recommends that online

banking facilities are adequate in ucbl.

71

loan processing is easier then other bank

Frequency PercentValid

PercentCumulative

PercentValid strongly

agree5 10.0 10.0 10.0

agree 17 34.0 34.0 44.0 neutral 22 44.0 44.0 88.0 disagree 6 12.0 12.0 100.0 Total 50 100.0 100.0

Comment: 34.00% of the respondents are agreeing with the statement that loan processing is easier then other bank In ucbl. But 44.00% of the respondent is neutral. So we can say that most of the respondent recommends that they are not understand about loan processing system in ucbl.

72

Overall banking activities are satisfied

Frequency PercentValid

PercentCumulative

PercentValid strongly

agree3 6.0 6.0 6.0

agree 41 82.0 82.0 88.0 neutral 5 10.0 10.0 98.0 disagree 1 2.0 2.0 100.0 Total 50 100.0 100.0

Comment:82.00% of the respondents are agreeing with the statement that overall banking activities are satisfied. But 10.00% of the respondent is neutral. So we can say that most of the respondent recommends that they are satisfied with the overall banking activities in this bank.

73

location of the bank is suitable

Frequency PercentValid

PercentCumulative

PercentValid strongly

agree26 52.0 52.0 52.0

agree 21 42.0 42.0 94.0 neutral 1 2.0 2.0 96.0 disagree 2 4.0 4.0 100.0 Total 50 100.0 100.0

Comment: 42.00 % of the respondents are agreed & 52.00% of the respondents are strongly agreed with the statement that location of the bank is suitable in ucbl. But 4.00% of the respondent is disagreeing. So we can say that most of the respondent recommends that location of the bank is suitable in ucbl.

74

CHAPTER-5

FINDINGS, RECOMMENDATION & CONCLUSION

75

5.0 Findings of the Report

General baking is the main or the heart of any banking sector. So when we find out analysis

on the general banking it is not possible to cover up all the aspect of general banking. We are

new in banking sector but there are some discrepancies in UCBL and other private bank in

Bangladesh. I am trying to figure out the problems of general banking and the customer are

facing.

Process of a customer when he/she wants to withdrawal of money from bank they

many people are involved on that process.

Every process involve separate person who give the token is not the person who give

the payment. And who check the cheque is not the person who put the payment seal.

Their transaction system is manual and they use LAN network but only the branch

individually can use it.

When they need to take any decision they have to search customer details manually.

They use automated system for debit and credit the customer accounts. But rest of the

work they need to do manually.

Customer could not know the balance of his/her accounts without coming to bank.

Because they have to ensure the customer privacy. If it is in online then the customer

can easily search their accounts through online.

76

Customer Take Token Check by the Officer

Check the balance

If balance is sufficient then transact

Put payment seal on the check

Took back the Token

Mak

e Pa

ymen

t

Some time cheques are rejected for insufficient balance in the accounts.

It takes huge time to withdrawal of money from any kind of accounts in the banks.

They follow the 1st generation banking style on the operation of general banking in all

the branches.

They have quality and experienced people for work but the lack of computer skills is

one of the disadvantages of the banks.

They have a training institute but the lower level employee can not attend in the

training program. But they use more than the upper level of employee.

They are trying to implement the computerized system in their banks. And recently

they give loan to the employee to buy Personal Computer so that they can learn

computer easily.

From the customer satisfaction survey study I have found some findings. This are described in below:

Yearly account maintenance charge is not reasonable for the customers. Because only

34% respondent are agreeing with this statement.

(Home loan) interest ret is not reasonable for the customers. Because only 26%%

respondent are agreeing with this statement.

Advertisement and promotional activities are not highly acceptable to the customers

because 50% respondents are neutral in this statement.

Respondent can’t give any clear statement that loan processing system is easier or not

because 44% respondent is neutral.

After analyzing the data collection from the survey, I figured out that not a single respondent

who participated in the survey was entirely satisfied with all the attributes of UCBL

( Nabinagar branch).but at the moment UCBL should enhance its ability to perform any

promised service dependably and accurately and should provide caring individual to its

customers.

77

5.0 Recommendation

Recommendations of these report has been made on the basis of the research findings for the

further improvement of the general banking division and customer satisfaction survey of

United Commercial Bank Limited(Nabinagar branch).

They have to introduce new product to the market and attract people to deposit or loan

from this bank. If they want to compete with the others they have to follow or creating

new idea about general banking. They can introduce personal credit scheme, Special

deposit scheme, and Personal loan.

They should cover most of their branches with online banking facilities. Otherwise

they may not be the competitor of third generation banks. Their slogan should be

“Banking in anywhere”.

They have skilled people on banking sector and they should give them proper trained

to compete with the market demand from bank. They can also learn from the other

banks in our country.

They have to train their employee with computer knowledge. Now a days every

private or any company uses computer and it is an easy way to do work, if know the

computer by the user.

The Yearly account maintenance charge should be decrease.

(Home loan) interest rate should be reasonable for the customers.

Try to increase the Advertisement and promotional activities.

UCBL should consider building new branches and ATMs within Dhaka city as well

as other metropolitan cities in Bangladesh.

UCBL should reduce the amount of time required to provide new ATM card.

The quality of the ATM network should be improved.

78

United Commercial Bank is a very big bank with 116 branches all over the country. And

it is a profitable organization also. So their attitude should be the market leader in banking

sector. They have the ability to be a market leader, now they have to implement those

ideas to become a market leader.

5.0 Conclusion

General banking is the most and important department of any kind of banks. I have worked

general bank division in United Commercial Bank Limited (Nabinagar Branch).I talk to

employee about the general banking procedure they maintain and also talk to the client of the

banks. Mainly they focus about the other banks online banking system. Online banking

system is more helpful for not only the fastest service but also the accuracy of the banking

transaction.

They have not a lot of scheme of the general people. They have some corporate clients and

they are their main clients. There should be some attractive scheme for the clients because the

clients are the most important source of money. They deposit their money in the bank and

bank give this money to Loan others who required.

UCBL do not have any motivational loan scheme like personal loan, furniture loan, cur loan

etc. Now every private bank have attractive and reasonable loan or deposit scheme. This

scheme attracts people about the bank and bank can get a great benefit from those clients.

The management of UCBL should consider the findings and take all necessary steps foe

further research and if they think that the customer of UCBL are homogeneous in their choice

and preference they may consider the following recommendation to gain more customer

satisfaction along with maintaining existing customers delights.

Before I conclude this section, I would like to mention that the internship of UCBL has

increased my practical knowledge of business administration, I have created different short of

real life acquaintance, which I belief will be of great help in future.

79

Reference:

www.United commercial Bankl Ltd, Annual Report,2009

www.United commercial Bankl Ltd, Annual Report,2010

www.United commercial Bankl Ltd, Head office circular,june 30,2008

www.united commercial bank.com

Chowdhury,L.R, A Textbook on bankers advance ,2nd edition paradise

printer,2002

UCBL general banking part-1

80