finxpress_27_january_2013

DESCRIPTION

ÂTRANSCRIPT

IN THIS IS

SUE Fi

nX

pre

ss

January 27, 2013

Company In Focus

Editoria

l

1

Company in

Focus

2

Term of t

he Week

4

Mark

et this

Week

6

News of t

he Week

8

Cover Sto

ry

10

Fun Corner

13

Term of the Week Triangular Arbitrage

INSTITUTE OF MANAGEMENT TECHNOLOGY, GHAZIABAD

Cover Story

EDITORIAL

Dear Readers,

Greetings from FinNiche!

After crossing the third milestone, first year students are all ready for the fourth one. So again the time has come for all those who said “yaar agli baar se shuru se he padhunga” in the last term. Team FinNiche would like to take this opportunity to wish the First year students all the best for their new endeavour.

In this edition of FinXpress, we have Mindtree Limited as the ‘Company in Focus’. After the MM arbitrage of the CF end term, in the ‘Term of the Week’ section, we would like to explore ‘Triangular Arbitrage’. Moving to the ‘Markets This Week’, markets ended the week marginally higher on the back of strong corporate earnings from major Sensex companies. The special page features a review on the “How does Private Equity work in India”. We sincerely hope that the readers will find the content engaging. We would appreciate feedback and suggestions for improvement. We look forward to keeping you updated and adding to your knowledge base. Till then, “Enjoy Reading”!

Yours Sincerely,

The Editorial Board

FinXpress

January 27, 2013 PAGE 1 http://www.imtgfinxpress.co.cc

COMPANY IN FOCUS

January 27, 2013 PAGE 2 http://www.imtgfinxpress.co.cc

Mindtree Limited

Mindtree Limited, formerly known as Mindtree Consulting Limited (BSE: 532819), is a mid-sized international information technology (IT), consulting and implementation company. Mindtree was started in 1999 by ten industry professionals from Cambridge Technology Partners, Lucent Technologies, and Wipro. It is currently co-headquartered in Warren (New Jersey), and Bangalore (India). It has three development centers in India and 15 offices in Asia, Europe, and the United States. Mindtree is ranked #18 in Indian IT companies and overall #445 in Fortune India 500 list of 2011. It was the First Indian IT firm that went public, and offered an IPO Mindtree Ltd. surpassed USD 100 million in revenues in April 2006. Mindtree was involved in the creation of Bluetooth technology and is an Associate Member of the Bluetooth Special Interest Group. Its Bluetooth protocol stack is licensed to NEC. It operates in two units: Product engineering Services and IT Services. IT Services and R&D Services. It has clients that range from Fortune 10 companies to enterprise software organizations. It has offices across USA, United Kingdom, Germany, Switzerland, United Arab Emirates, India, Singapore, Australia and Japan.

Key Events and Milestones 1. September 2004 : Acquisition of the software division of ASAP and ARPSL. 2. January 2004 : Execution of contract with AIG Offshore Systems Service Inc. for supply of IT

Services. 3. October 2001 : Investment by Franklin Templeton Holding Limited. 4. December 2001 : Commencement of IT outsourcing partnership with Volvo Information

Technology. In 2010 MindTree signed a pact with Carlyle Group, one of the world's largest private equity firms. MindTree agreed to provide IT infrastructure management and support services for Carlyle's global data centres. They would monitor and manage all of Carlyle's IT production servers at Carlyle's data centres in the US, the UK and Hong Kong, as well as its disaster recovery data centre in Virginia. MindTree will also monitor and manage file servers located in Carlyle offices throughout the world, as well as other classes of hardware and applications. Mindtree Ltd, the IT solutions firm, bagged a contract from government’s Unique Identification Project (UID) for application development and maintenance services. MindTree Ltd launched Security Services to help businesses solidify and execute their security and compliance strategies.

January 27, 2013 PAGE 3 http://www.imtgfinxpress.co.cc

MARKET CAP (RS CR) 3,256.14

P/E 9.89

BOOK VALUE (RS) 229.98

DIV (%) 40.00%

INDUSTRY P/E 20.34

EPS (TTM) 78.97

PRICE/BOOK 3.40

DIV YIELD.(%) 0.51%

FACE VALUE (RS) 10.00

TERM OF THE WEEK : Triangular Arbitrage

Triangular arbitrage (also referred to as cross currency arbitrage or three-point arbitrage) is the act of exploiting an arbitrage opportunity resulting from a pricing discrepancy among three different currencies in the foreign exchange mar-ket. A triangular arbitrage strategy involves three trades, ex-changing the initial currency for a second, the second currency for a third, and the third currency for the initial. During the second trade, the arbitrageur locks in a zero-risk profit from the discrepancy that exists when the market cross exchange rate is not aligned with the implicit cross exchange rate. Triangular arbitrage opportunities may only exist when a banks quoted exchange rate is not equal to the market's implicit cross exchange rate. The following equation represents the calculation of an implicit cross exchange rate, the exchange rate one would expect in the market as implied from the ratio of two currencies other than the base currency.

Where

is the implicit cross exchange rate for dollars in terms of currency a

is the quoted market cross exchange rate for b in terms of currency a

is the quoted market cross exchange rate for dollars in terms of currency b

is merely the reciprocal exchange rate for currency b in dollar terms, in which case division is used in the calculation If the market cross exchange rate quoted by a bank is equal to the implicit cross exchange rate as implied from the exchange rates of other currencies, then a no-arbitrage condition is sustained. However, if an

inequality exists between the market cross exchange rate - , and the implicit cross exchange rate -

, then there exists an opportunity for arbitrage profits on the difference between the two exchange rates As an example, suppose you have $1 million and you are provided with the following exchange rates: EUR/USD = 0.8631, EUR/GBP = 1.4600 and USD/GBP = 1.6939. With these exchange rates there is an arbitrage opportunity: Sell dollars for Euros: $1 million x 0.8631 = 863,100 Euros Sell Euros for pounds: 863,100/1.4600 = 591,164.40 pounds Sell pounds for dollars: 591,164.40 x 1.6939 = $1,001,373 dollars $1,001,373 - $1,000,000 = $1,373 From these transactions, you would receive an arbitrage profit of $1,373 (assuming no transaction costs or taxes).

January 27, 2013 PAGE 4 http://www.imtgfinxpress.co.cc

Research examining high-frequency exchange rate data has found that mispricing do occur in the foreign exchange market such that executable triangular arbitrage opportunities appear possible. In observations of triangular arbitrage, the constituent exchange rates have exhibited strong correlation. A study examining exchange rate data provided by HSBC Bank for the Japanese yen (JPY) and the Swiss franc (CHF) found that although a limited number of arbitrage opportunities appeared to exist for as many as 100 seconds, 95% of them lasted for 5 seconds or less, and 60% lasted for 1 second or less. Further, most arbitrage opportunities were found to have small magnitudes, with 94% of JPY and CHF opportunities existing at a difference of 1 basis point, which translates into a potential arbitrage profit of $100 USD per $1 million USD transacted. Tests for seasonality in the amount and duration of triangular arbitrage opportunities have shown that incidence of arbitrage opportunities and mean duration is consistent from day to day. However, significant variations have been identified during different times of day. Transactions involving the JPY and CHF have demonstrated a smaller number of opportunities and long average duration during 10:00am and 1:00am UTC, contrasted with a greater number of opportunities and short average duration during 1:00pm and 4:00pm UTC. Such variations in incidence and duration of arbitrage opportunities can be explained by variations in market liquidity during the trading day. The periods of highest liquidity correspond with the periods of greatest incidence of opportunities for triangular arbitrage. However, market forces are driven to correct for mispricings due to a high frequency of trades that will trade away fleeting arbitrage opportunities. Mere existence of triangular arbitrage opportunities does not necessarily imply that a trading strategy seeking to exploit currency mispricings is consistently profitable. Electronic trading systems allow the three constituent trades in a triangular arbitrage transaction to be submitted very rapidly. However, there exists a delay between the identification of such an opportunity, the initiation of trades, and the arrival of trades to the party quoting the mispricing. Even though such delays are only milliseconds in duration, they are deemed significant. For example, if a trader places each trade as a limit order to be filled only at the arbitrage price and a price moves due to market activity or new price is quoted by the third party, then the triangular transaction will not be completed. In such a case, the arbitrageur will face a cost to close out the position that is equal to the change in price that eliminated the arbitrage condition. In the foreign exchange market there are many market participants competing for each arbitrage opportunity; for arbitrage to be profitable a trader would need to identify and execute each arbitrage opportunity faster than competitors. Competing arbitrageurs are expected to persist in striving to increase their execution speed of trades by engaging in what some researchers describe as an "electronic trading 'arms race'.” The costs involved in keeping ahead in such a competition present difficulty in consistently beating other arbitrageurs over the long term. Other factors such as transaction costs, brokerage fees, network access fees, and sophisticated electronic trading platforms further challenge the feasibility of significant arbitrage profits over prolonged periods.

January 27, 2013 PAGE 5 http://www.imtgfinxpress.co.cc

MARKET THIS WEEK

SENSEX

SENSEX gained 0.32% from last week and ended at 20103.53 this week.

Simple Moving Averages

NIFTY

The Nifty gained 0.17% from last week and ended at 6074.65 this week.

Simple Moving Averages

30 Days 50 Days 150 Days 200 Days

19,669.64 19,385.00 18,403.88 17,975.15

30 Days 50 Days 150 Days 200 Days

5,969.65 5,888.42 5,585.46 5,454.55

January 27, 2013 PAGE 6 http://www.imtgfinxpress.co.cc

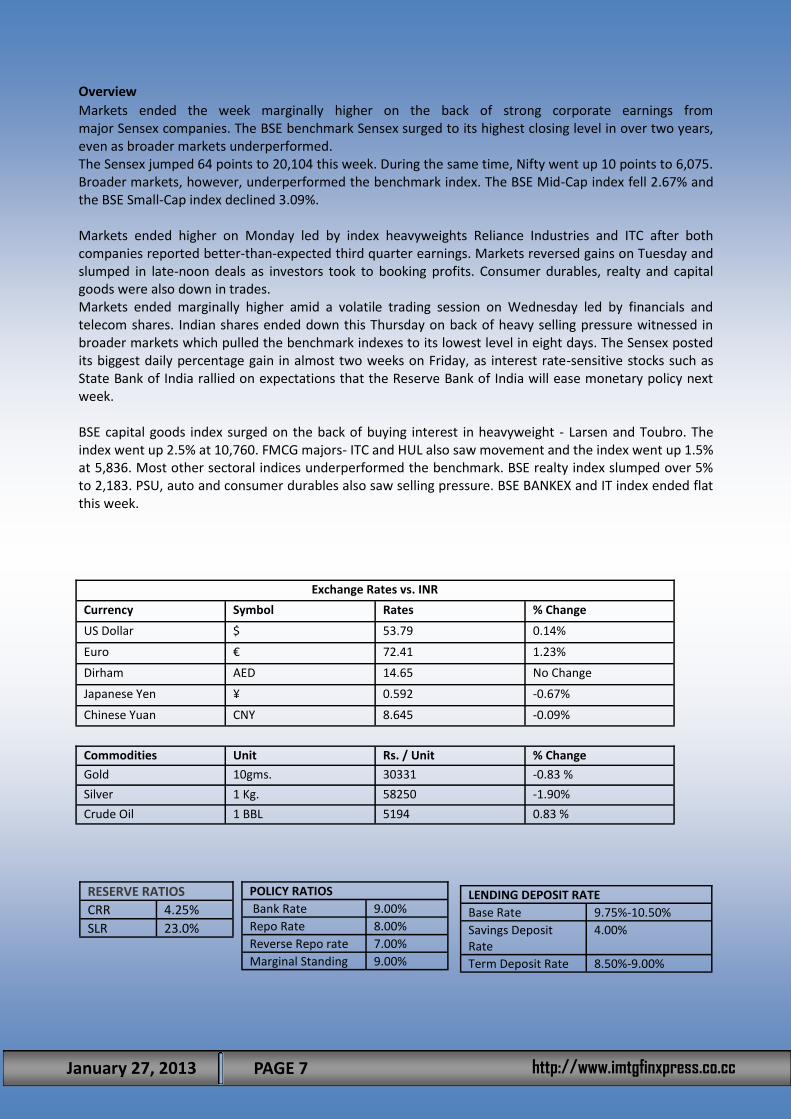

Overview

Markets ended the week marginally higher on the back of strong corporate earnings from major Sensex companies. The BSE benchmark Sensex surged to its highest closing level in over two years, even as broader markets underperformed. The Sensex jumped 64 points to 20,104 this week. During the same time, Nifty went up 10 points to 6,075. Broader markets, however, underperformed the benchmark index. The BSE Mid-Cap index fell 2.67% and the BSE Small-Cap index declined 3.09%. Markets ended higher on Monday led by index heavyweights Reliance Industries and ITC after both companies reported better-than-expected third quarter earnings. Markets reversed gains on Tuesday and slumped in late-noon deals as investors took to booking profits. Consumer durables, realty and capital goods were also down in trades. Markets ended marginally higher amid a volatile trading session on Wednesday led by financials and telecom shares. Indian shares ended down this Thursday on back of heavy selling pressure witnessed in broader markets which pulled the benchmark indexes to its lowest level in eight days. The Sensex posted its biggest daily percentage gain in almost two weeks on Friday, as interest rate-sensitive stocks such as State Bank of India rallied on expectations that the Reserve Bank of India will ease monetary policy next week. BSE capital goods index surged on the back of buying interest in heavyweight - Larsen and Toubro. The index went up 2.5% at 10,760. FMCG majors- ITC and HUL also saw movement and the index went up 1.5% at 5,836. Most other sectoral indices underperformed the benchmark. BSE realty index slumped over 5% to 2,183. PSU, auto and consumer durables also saw selling pressure. BSE BANKEX and IT index ended flat this week.

January 27, 2013 PAGE 7 http://www.imtgfinxpress.co.cc

Exchange Rates vs. INR

Currency Symbol Rates % Change

US Dollar $ 53.79 0.14%

Euro € 72.41 1.23%

Dirham AED 14.65 No Change

Japanese Yen ¥ 0.592 -0.67%

Chinese Yuan CNY 8.645 -0.09%

Commodities Unit Rs. / Unit % Change

Gold 10gms. 30331 -0.83 %

Silver 1 Kg. 58250 -1.90%

Crude Oil 1 BBL 5194 0.83 %

RESERVE RATIOS

CRR 4.25%

SLR 23.0%

POLICY RATIOS

Bank Rate 9.00%

Repo Rate 8.00%

Reverse Repo rate 7.00%

Marginal Standing 9.00%

LENDING DEPOSIT RATE

Base Rate 9.75%-10.50%

Savings Deposit Rate

4.00%

Term Deposit Rate 8.50%-9.00%

NEWS OF THE WEEK

Reserve Bank eases rules for FII investment in debt The Reserve Bank of India (RBI), on Thursday, notified the enhanced limit of investing in government securities (G-Secs) by foreign institutional investors (FIIs) and long-term investors by $5 billion to $25 billion from $20 billion. It also hiked the investment limit in corporate bonds by these entities by $5 billion $50 billion from $45 billion. Long-term investors include SEBI-registered sovereign wealth funds (SWFs), multilateral agencies, endowment funds, insurance funds, pension funds and foreign central banks. The RBI also relaxed some investment rules by removing the maturity restrictions for first time foreign investors on dated G-Secs. Earlier it was mandated that the first time foreign investors of G-Secs must buy securities with at least three-year residual maturity. But such investments would not be allowed in short-term paper like Treasury Bills.

Cabinet gives nod for Walmart probe panel The Union Cabinet, on Thursday, gave approval to the constitution of a one-man committee to look into the bribery allegations and lobbying activities against retail giant Walmart. The probe was approved at a meeting of the Cabinet, chaired by Prime Minister Manmohan Singh. The committee will submit its report within three months time. The terms of reference of the Committee include: (i) To inquire into recent media reports on disclosures of Walmart before the US Senate regarding its lobbying activities and details; (ii) Whether Walmart undertook any activities in India in contravention of any Indian law; (iii) Any other matter relevant or incidental to the above. In the last quarter, ended September 30, 2012, the company spent $1.65 million (about Rs. 10 crore) on various lobbying issues, which included discussions related to FDI in India. Bharti Wal-Mart has already denied wrongdoing, saying the allegations of corruption are “entirely false”.

RBI revises rules for bulk deposits The Reserve Bank of India has revised the rules for bulk deposits, offering differential interest rates, which would be applicable with effect from April 1. The RBI said that a bank, on request from a depositor, would allow withdrawal of a term-deposit before completion of the period of the deposit agreed upon at the time of making a deposit. The bank shall have the freedom to determine its own penal interest rate of premature withdrawal of term deposits. The bank shall ensure that the depositors are made aware of the applicable penal rate along with the deposit rate. However, the RBI said that the bank, at its discretion, would disallow premature withdrawal of large rupee term deposits of Rs.1 crore and above. In that case the bank should notify such depositors of its policy at the time of accepting such deposits.

Barclays may move many back-office jobs to India Britain’s leading financial services giant Barclays is planning to move hundreds of back-office jobs to India as part of cost-cutting measures. With around 2,000 jobs on the line at its troubled investment banking unit in the U.K., Barclays is believed to have dispatched a team to recruit and train new staff in India to replace workers in London and New York. It had sent out emails to staff at its investment bank consulting on the planned job cuts earlier this week. Those affected will be largely linked to back-office and support functions. News of further offshoring and job losses could generate fresh controversy, particularly among workers’ unions, given that the roles slated to move to India will be primarily relatively modestly paid ones.

January 27, 2013 PAGE 8 http://www.imtgfinxpress.co.cc

Morgan Stanley to exit India banking on stricter rules, new regulations At a time when business houses are lobbying hard to own banks, US financial services group Morgan Stanley has chosen to surrender its banking licence in India. The decision is driven by a reassessment of business strategy in the face of new regulations and stringent capital rules. Morgan Stanley, the sixth-largest US bank by assets, will, however, continue to run its investment bank in India and stay registered as a non-banking finance c o m p a n y w i t h t h e R e s e r v e B a n k o f I n d i a ( R B I ) . Morgan Stanley declined comment for the report. In March 2012, the Wall Street biggie received the licence to set up a bank. It is now planning to let the licence lapse as it does not want to tie up capital and other resources on account of a review of its strategy.

India’s 5-year steel output second highest in the world India’s 33 per cent growth in steel production in the last five years was second only to China among the top-five producing nations. China’s production grew by 39 per cent during 2008-2012, the latest World Steel Association (WSA) data has revealed. India’s production grew constantly in the last five years from 57.8 MT in 2008 to 63.5 MT in 2009, 69 MT in 2010, 73.6 MT in 2011 and 76.7 MT in 2012. China, which produces nearly half of world’s steel, had output of 512.3 MT in 2008, 577.1 MT in 2009, 638.7 MT in 2010, 694.8 MT in 2011 and 716.5 MT in 2012. India is projected to grab the second slot in the world of steel production within a year or two on new capacity expansions, mainly through the brown field route.

Indian pleads guilty to defrauding investors of over $2.3 mn An Indian-origin investment adviser from California has pleaded guilty to defrauding investors of more than $2.3 million, and now faces the prospect of 20 years in jail along with a hefty fine. Janamjot Singh Sodhi, 35 pleaded guilty to four counts of mail fraud and one count of wire fraud and is scheduled to be sentenced on April 29, when he faces a maximum 20 years in prison and a 250,000 dollar fine, US Attorney Benjamin Wagner said. According to court documents, during 2005 through 2011, Sodhi solicited investments from individuals using false pretences, promising various investment opportunities with high rates of return in a relatively short period of time. Sodhi, who owned a financial services firm, never disclosed to his investors that the New York Stock Exchange had permanently debarred him and that he was never certified by the California Department of Corporations to operate as an investment adviser in California.

Week ahead: RBI, FOMC policy meet, Bharti, ICICI Bank results to set the tone The week ahead will keep India Inc and Dalal Street on their toes. The Reserve Bank of India will take key decision on interest rates. The US Federal Reserve will also decide its further course on bond buying programme. Bellwethers like Bharti Airtel, ICICI Bank, BHEL will declare their results, which will set the next direction for markets. Investors and analysts will closely watch the management commentary as this could cause revision in future earnings forecast of the company for fiscal year ahead. The Reserve Bank of India is likely to announce its monetary policy on Tuesday, January 29. According to Reuter's poll most economists expect RBI to cut its policy repo rate by 25 basis points to 7.75% and follow it up with a cumulative 75 basis points cut by the end of September 2013.

January 27, 2013 PAGE 9 http://www.imtgfinxpress.co.cc

COVER STORY

Across the skyline of India's cities, countless cranes and towers of bamboo scaffolding offer testament to the building of a new economy. "India is in the middle of a high growth phase," says Ashish Dhawan, co-founder of ChrysCapital which manages $2.5 billion in six funds. "We're starting from a low per capita income and we've yet to reach middle income status. If you look at that macro backdrop—8% real growth, 13% or 14% nominal growth—the appropriate role for private equity is really to provide growth capital for companies that are serving the consumer." Dhawan and others in the field make a clear distinction between private equity in India and other parts of the world. "Our belief has been that over the last decade, the sweet spot for private equity is really not what it is in the Western world, which is leveraged buyouts, financial re-engineering, taking family-owned businesses and professionalizing them," he says. "Instead it's working with entrepreneurs who have a mid-sized business, putting in capital and helping the business to become three or four times its size over a five-year period of time." ChrysCapital has completed nearly 60 deals since 1999. The legal environment further shapes the industry. "We don't do turnarounds," says Dhawan. "India's bankruptcy laws are fairly out of date. There is no real distressed market here. The banks have healthy capital ratios, so they're not looking to sell off loans. It's hard to come in and get a sweetheart deal on a failing company." Dhanpal Jhaveri, partner and CEO of Everstone Capital Management, a firm with $1.5 billion under management, sees this growth-focused approach continuing. "Demand-supply gaps will continue for at least another 10 years, allowing for this growth model to continue. With 58% of GDP driven by domestic consumption, a rapid growth of the middle class, and urbanization, we think that domestic consumption is likely to be the cornerstone of Indian growth for the next 10 to 20 years."

How Does Private Equity Work in India?

January 27, 2013 PAGE 10 http://www.imtgfinxpress.co.cc

A Flood of Foreign Capital The allure of rapid growth has attracted foreign capital. The money typically comes from institutional investors: endowments, sovereign wealth funds, pension funds, funds of funds, and family offices. A common pattern among firms is to start with U.S. based sources, then to diversify, with subsequent funds drawing on investors from Europe and Asia. Domestic institutional investors shepherding Indian capital have tight regulations on their ability to make equity investments and limited experience with alternative asset classes like private equity. "We are still ramping up as a country in terms of our understanding of this asset class," says Sanjeev Aggarwal, co-founder and senior managing director of Helion Venture Partners, a $600 million India-focused venture fund. "It is very high-risk—you can lose all your money. And returns take a long time because company-building is a long process. Right now, this asset class is better understood in the Western world, but that will change over time." The overall size of private equity and venture capital is relatively small, but experts see it as an important component of the economy. "I think the industry is extraordinarily significant," says G. Sabarinathan, a professor of finance and entrepreneurship at the Indian Institute of Management, Bangalore. "In order to harness the tremendous entrepreneurial energy of India in the most optimal way, you need enlightened capital that is willing to wait three to five years, back the right team, and give the right post-investment support." But Sabarinathan sees a major challenge: "There is so much competition for deals," he says. That competition developed because interest in India came as a flood, according to Dhawan. "There has been a rush of capital coming in. Many emerging markets became very attractive in the period 2006-2007. ChrysCapital had generated particularly good returns in the five years prior to that. A couple of global firms that have been here longer, like Warburg Pincus and Citibank, also generated good returns. That attracted all the global funds to India." He adds, "They came in all at once, and there was this massive crowding effect. The overhang of capital led to regulations going up and a lot of competition." That competition to invest has made it harder to meet targets on returns. "Valuations are going through the roof," Sabarinathan said. "Part of the reason people lose money is that they pay far too much up front." Making Do With a Minority Share With a booming economy in recent years, entrepreneurs have been succeeding and saw little reason to hand over their company for growth capital. "Indian management is very control-sensitive," Sabarinathan says. "They try to defer raising external capital as long as they are able. One way they do that is by using a lot of leverage: the debt market is a lot more forgiving in India, so founders tend to borrow a lot." Ashish Dhawan says that one of the biggest challenges to private equity in India is minority ownership stakes. "You're not in control. You're at the mercy of the entrepreneur, because the entrepreneur typically owns 51%." He adds, "We only selectively help when there are one or two key hires that need to be made, but we're not really involved with changing the whole management team or bringing in a new CEO. In that sense, we're different from a firm in the Western world where they would also have senior operating partners on the team who would get involved with portfolio companies." Where's the Exit? "There are few instances of VC/PE funded companies that go through a second funding round," Sabarinathan says. "In India it is almost an article of faith that there will be one round of financing and then the company will go public." That may change, at least in the short run. "The IPO market is not looking good at all, currently," Sabarinathan says. "The IPO windows tend to be fickle. They open for a short period of time." However, when those windows do open, even small to mid-sized companies have gone public.

January 27, 2013 PAGE 11 http://www.imtgfinxpress.co.cc

The periodic option for going public while relatively small gives private equity additional opportunities. "Private equity here is not just investing in private companies, but also in public companies," says Dhawan. On the other hand, he adds, the public market can act as a competitor to private equity. "If a company is already public, it can easily do a follow-on offering as opposed to looking to the private equity sphere for funds." On top of that, exits are a concern. "Our market is still not very liquid. It's not a very deep market," says Dhawan. "In good times, clearly, you can exit even from the 500 largest listed companies by market cap. In slightly more difficult times the liquidity tends to be concentrated in the top couple hundred companies. Given the private equity invested in mid-sized companies, and you may have a large stake—20, 25, 30%—it may be difficult to exit some of these companies, particularly with entrepreneurs that are not ready for a strategic sale, which is the case in a vast majority of situations." Sabarinathan registers concern about exits as well. "There has been a recent trend in foreign funds to shut down their Indian outposts and to cut back on the India allocations. I think that is partially driven by the perception that exits are going to get more and more difficult." Competing Globally, Growing Locally Given that India's economic liberalization happened in 1991, the sector, which depends heavily on Western-style business practices and entrepreneurialism, is maturing quickly, though not without some false starts. "I think investors are now discerning and demanding," Sabarinathan says. "There is an enormous maturing in the businesses they fund. These businesses could be in any part of the world; they are globally competitive. It doesn't matter that they are in India. Whether it's pharmaceuticals, media, technology, or manufacturing, in terms of scale, scope and quality they are globally competitive. That is a very significant difference." More and more private equity firms are Indian owned and managed. Sabarinathan is waiting for data to find out if that will make a difference to returns, but he does believe that "it's important that foreign investors have Indians, raised in India, on their team." He adds, "Although Indian businessmen are trying to learn Western best practices, cultural and social factors contribute to making this a very different market. Law and property rights are very different. Many things you take for granted simply don't work the way they would in the United States or the UK. On very crucial matters, the average Indian tends to be quite clannish—or to put it even less charitably, they tend to be rather parochial." Meanwhile, Indians who have had successful entrepreneurial careers overseas are returning to India, further strengthening the industry. "Entrepreneurs who made money in the last couple of decades want to give that money back to help create more entrepreneurship," says Aggarwal. "An angel investor community is emerging."

January 27, 2013 PAGE 12 http://www.imtgfinxpress.co.cc

CAN YOU SOLVE IT?

**Rush in your entries to : [email protected]

The right entries will get their name featured in the next issue of FinXpress. So hit the quiz fast & get yourself visible among 1000 odd in the campus.

Feel free to write to us at : [email protected]

Drop in your suggestions to the editorial team :

Magazine design/news : [email protected]

Articles/quiz : [email protected]

LAST WEEK’S ANSWERS:

1. Federal Bank - Shyam Srinivasan

2. HDFC - Aditya Puri

3. Axis Bank - Shikha Sharma

4. ING Vysya - Shailendra Bhandari

5. IndusInd - Romesh Sobti

Winner : Ajay Maheska

We are on the web !

http://www.facebook.com/FinNiche

http://www.imtgfinxpress.co.cc

CARTOONS:

FinQuiz

Match the Following

January 27, 2013 PAGE 13 http://www.imtgfinxpress.co.cc

General Electric

JPMC

Goldman Sachs

Bank Of America

Deloitte

A.W. Clausen

Barry Salzberg

Jeffrey R. Immelt

Lloyd C. Blankfein

Jamie Dimon