fintelligence - vivro financial services : credit … - issue … · · 2017-01-16been raised...

TRANSCRIPT

FINTELLIGENCE ISSUE 8 | NOVEMBER - DECEMBER 2016

FOREWORD

External Commercial Borrowings and Foreign Currency Convertible Bonds have been popular forms of raising debt resources from foreign investors and institutions. Indian Companies which have a significant export business or those who wish to raise debt from banks and institutions abroad have been tapping these sources through such structures since several years. Since the past 10 years, a total of USD 282.08 billion (~ INR 16 lakh crores) have been raised through ECB and FCCB. However, Indian Companies and borrowers carry a risk of currency depreciation which could result in a disproportionate outflow of rupees at the time of repayment of interest and installments to cover the tenure of the debt. With the cost of hedging, the interest rates work out quite close to domestic borrowing rates. The Reserve Bank of India has issued guidelines allowing certain eligible Indian Companies to issue Rupee Denominated Bonds, also known as Masala Bonds and raise debt from investors and institutions abroad which would transfer the current risk to the lender. In this issue we have written about Masala Bonds and how they compare with ECBs.

International Trade functions smoothly through banking channels and systems that have been established, accepted and practiced since decades. With advances in technology there has been further development in the manner in which trade is conducted through physical and virtual movements of documents of trade. The Letter of Credit is a crucial part of the entire international transaction which works not only as a guarantee that the transaction will be completed as agreed mutually but also brings in reliability in the transactions. In this issue we have written about Letter of Credit as an important tool for trade finance.

It is important to have an aim in life. It enables you to plan material aspects of your life to reach this aim. When it comes to planning your investments, the same holds true. Goals and aspirations drive our fundamental needs to save and plan for a future. Goal based financial planning has been accepted as the preferred approach to planning investments to ensure that you achieve the right mix of investment for each goal, based on the perceived risks of each goal type. Our article on Goal Based Investing shares a structured approach to ensure you plan your investments well to secure your future.

Government initiatives towards infrastructure development have turned the Indian landscape drastically. Such large scale urbanization and modernization have catalyzed economic development and created large positive externalities for in and around surrounding areas, resulting into value creation for property owners. Working on the directives of Prime Minister’s Office, the Cabinet has given its consensus to India’s first VCF policy, which is aimed to help the government recover some value that public infrastructure investments generate for private landowners. Our article on Value Capture Financing - A Government Mechanism to Monetize Value captures some of these aspects.

We are happy to release our Eighth issue of Fintelligence, for the month of November – December, 2016. We wish you a very Happy Diwali and a Prosperous New Year. We hope you enjoy this edition of Fintelligence. Please write back to us on [email protected] with your valuable feedback and comments.

VIVEK VAISHNAV ROSHAN VAISHNAV

Masala Bonds - Internationalising the Indian Rupee 05

Letter of Credit - A Tool of Trade Finance 10

Goal based Investing - A Structured Approach 15

Value Captue Financing - A Government Mechanism to Monetize Value 19

About Vivro 24

TABLE OF CONTENTS

Introduction“Masala Bonds” refers to financial instruments, through which Indian entities can raise money from the overseas financial markets in Rupee. These bonds are rupee-denominated and issued to offshore investors, which are settled in dollars and, therefore, the currency risk resides with the investors. Such bonds are popularly known as

“Masala Bonds” after the International Financial Corporation (IFC) first issued rupee denominated bond under the name “Masala Bonds”, linking the name to the Indian spices, which have been popular across the world. Similar offerings from other countries are named after the food or culture of that country like “Dim Sum” for Chinese offshore issues or “Samurai” for Japanese offshore issues.

Benefits of Masala BondsThe rupee denominated bond is an attempt to shield issuers from currency risk and transfer this risk to the investors. As the currency risk is borne by the investor during the repayment of the bond coupon and the maturity, the Reserve Bank of India (RBI) will realize marginal saving if the Rupee depreciates & vice-versa. However, it is believed that the investors in Masala Bonds would bear the currency risk, for which, the coupon would carry a currency risk premium, and hence, the borrowing cost for Indian corporates through this route would be slightly higher than other similar routes such as ECBs. But any such increase could be negated by the fact that these bonds provide access to international markets for INR denominated

securities that are generally priced higher than other foreign currency denominated securities, which would increase investor participation. As the investors would be global entities, “Masala Bonds” are a step to internationalize the Indian Rupee. A clear understanding on INR with a stable currency will hold the key to the success of these bonds.

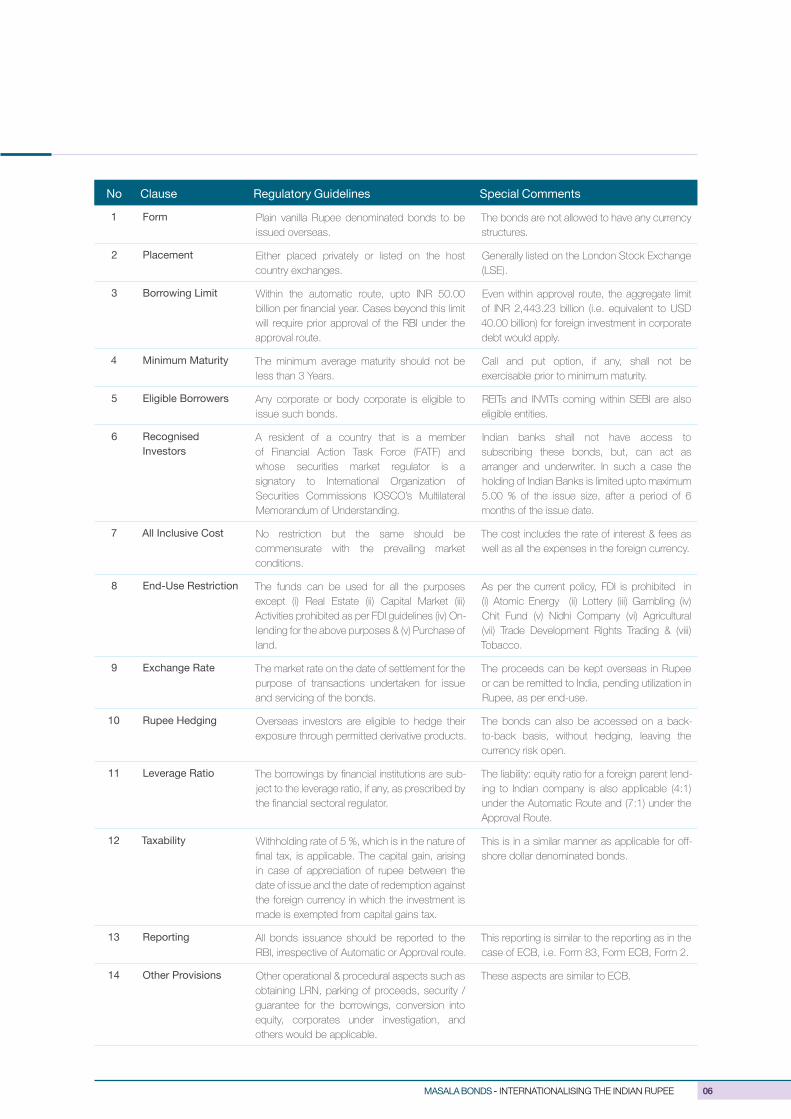

Regulatory Guidelines Governing Masala BondsMasala Bonds fall within the purview of the RBI ECB guidelines (Framework for Issuance of Rupee Denominated Bonds Overseas), and hence, the regulations applicable to ECB, to the extent not specifically modified for Masala Bonds, are equally applicable to Masala Bonds. The master circular on ECB, which is the guiding principle for the issuance of Masala Bonds, alongwith the relevant extract of the Income Tax Act, for the applicability of income tax on interest and capital gain tax on redemption, specifies the below mentioned important points:

MASALA BONDS INTERNATIONALISING

THE INDIAN RUPEE

05 MASALA BONDS - INTERNATIONALISING THE INDIAN RUPEE

MASALA BONDS - INTERNATIONALISING THE INDIAN RUPEE 06

No Clause Regulatory Guidelines Special Comments

1 Form Plain vanilla Rupee denominated bonds to be issued overseas.

The bonds are not allowed to have any currency structures.

2 Placement Either placed privately or listed on the host country exchanges.

Generally listed on the London Stock Exchange (LSE).

3 Borrowing Limit Within the automatic route, upto INR 50.00 billion per financial year. Cases beyond this limit will require prior approval of the RBI under the approval route.

Even within approval route, the aggregate limit of INR 2,443.23 billion (i.e. equivalent to USD 40.00 billion) for foreign investment in corporate debt would apply.

4 Minimum Maturity The minimum average maturity should not be less than 3 Years.

Call and put option, if any, shall not be exercisable prior to minimum maturity.

5 Eligible Borrowers Any corporate or body corporate is eligible to issue such bonds.

REITs and INVITs coming within SEBI are also eligible entities.

6 Recognised Investors

A resident of a country that is a member of Financial Action Task Force (FATF) and whose securities market regulator is a signatory to International Organization of Securities Commissions IOSCO’s Multilateral Memorandum of Understanding.

Indian banks shall not have access to subscribing these bonds, but, can act as arranger and underwriter. In such a case the holding of Indian Banks is limited upto maximum 5.00 % of the issue size, after a period of 6 months of the issue date.

7 All Inclusive Cost No restriction but the same should be commensurate with the prevailing market conditions.

The cost includes the rate of interest & fees as well as all the expenses in the foreign currency.

8 End-Use Restriction The funds can be used for all the purposes except (i) Real Estate (ii) Capital Market (iii) Activities prohibited as per FDI guidelines (iv) On-lending for the above purposes & (v) Purchase of land.

As per the current policy, FDI is prohibited in (i) Atomic Energy (ii) Lottery (iii) Gambling (iv) Chit Fund (v) Nidhi Company (vi) Agricultural (vii) Trade Development Rights Trading & (viii) Tobacco.

9 Exchange Rate The market rate on the date of settlement for the purpose of transactions undertaken for issue and servicing of the bonds.

The proceeds can be kept overseas in Rupee or can be remitted to India, pending utilization in Rupee, as per end-use.

10 Rupee Hedging Overseas investors are eligible to hedge their exposure through permitted derivative products.

The bonds can also be accessed on a back-to-back basis, without hedging, leaving the currency risk open.

11 Leverage Ratio The borrowings by financial institutions are sub-ject to the leverage ratio, if any, as prescribed by the financial sectoral regulator.

The liability: equity ratio for a foreign parent lend-ing to Indian company is also applicable (4:1) under the Automatic Route and (7:1) under the Approval Route.

12 Taxability Withholding rate of 5 %, which is in the nature of final tax, is applicable. The capital gain, arising in case of appreciation of rupee between the date of issue and the date of redemption against the foreign currency in which the investment is made is exempted from capital gains tax.

This is in a similar manner as applicable for off-shore dollar denominated bonds.

13 Reporting All bonds issuance should be reported to the RBI, irrespective of Automatic or Approval route.

This reporting is similar to the reporting as in the case of ECB, i.e. Form 83, Form ECB, Form 2.

14 Other Provisions Other operational & procedural aspects such as obtaining LRN, parking of proceeds, security / guarantee for the borrowings, conversion into equity, corporates under investigation, and others would be applicable.

These aspects are similar to ECB.

Indian Foreign Currency Debt MarketExternal Commercial Borrowing (ECB) and Foreign Currency Convertible Bond (FCCB) has generally been the preferred borrowing instrument for Indian Corporates, for a variety of reasons. ECB has been traditionally favoured over Rupee borrowings, primarily due to the low cost of borrowing associated with ECB, which can be in the range of 6 Month USD LIBOR + 300 bps to 6 Month LIBOR + 500 bps (Around 5% p.a. - 7% p.a., on an un-hedged basis), as compared to a rupee term loan, which would be available at around 10% p.a. - 12% p.a.).

ECBs are considered to be the best instrument for overseas acquisitions as well as capital expenditure by corporates with sizable exports. However, the end-use restrictions and minimum average maturity guidelines continue to be deterrrents. Additionally, in case of companies having no exports, the hedging cost of 7% p.a.

– 8% p.a., renders the ECB unattractive in comparison to Rupee borrowings. FCCBs, though highly attractive earlier, are now not finding much favour, due to uncertainties of conversion and high coupon rates.

Since the past 10 years, a total of USD 282.08 billion (~ INR 16 lakh crores) have been availed through ECB and FCCB establishing them as the barometer of the Indian Corporate Foreign Currency Market. Masala Bonds have the potential to replace ECBs & FCCBs in this barometer in the near future, depending on various factors such as the volatility of the Indian Rupee and the interest rate regime. While Masala Bonds provide the favourable transformation of currency risk from the borrower to the lender, there are certain roadblocks which include size of issue and appetite for foreign investors as well as sovereign credit risk of India.

Masala Bonds vs ECBThe Indian corporates would compare the characteristics of Masala Bonds to their closest counterpart, i.e. ECB – Term Loan, before aggressively pursuing the issuance of such bonds. Though, technically, Masala Bonds are considered as “ECB” due to regulatory coverage in the same circular, but fundamentally, are very different. A comparison reveals the following:

ECB & FCCB Trends – Guiding Patterns for Masala Bonds

40,000

35,000

30,000

25,000

20,000

15,000

10,000

5,000

0FY07 FY10 FY14FY08 FY11 FY15FY09

ECB & FCCB Borrowing By Indian Corporates (USD Million)

(Source: Reserve Bank of India – ECB Archives: www.rbi.org.in/scripts/ECBView.aspx)

FY13FY12 FY16 FY17

07 MASALA BONDS - INTERNATIONALISING THE INDIAN RUPEE

MASALA BONDS - INTERNATIONALISING THE INDIAN RUPEE 08

Particulars ECB – Term Loan Masala Bonds

Framework 3 Tracks: Track-I (Medium term foreign currency loan), Track-II (Long term foreign currency loan), Track-III (INR denominated ECB not including Masala Bonds) – Automatic Route & Approval Route

Issuance of Rupee denominated bonds overseas – Automatic Route & Approval Route (Initial guidelines issued on September 29, 2015 have since been replaced on January 1, 2016)

Minimum Average Maturity

Track-I & Track-III – 3 Years (Upto USD 50.0 million) & 5 Years (Above USD 50.0 million), Track-II – 10 Years

3 Years without specific reference to the amount

Eligible Borrowers Companies & other entities as defined sector-wise for Track-I; Track-II; Track-III

All companies without specific reference to sector

Recognised Lender Track-I: International banks and financial institutions, Overseas branch/subsidiary of Indian banks, Foreign equity holders, Suppliers, Export Credit Agencies;

Track-II & Track-III: All of the mentioned above but excluding overseas branch / subsidiary of Indian Banks

Resident of country wherein the bond is issued within FATF (FATF includes almost all countries in North America & Western Europe, Russia, China, Japan, Australia, New Zealand, Brazil, Argentina, South Africa and a few countries in the Middle East and South East Asia).

All Inclusive Cost Track-I: 3 - 5 Years: 6 Month LIBOR + 300 bps; Above 5 Years: 6 Month LIBOR + 450 bps;

Track-II: 6 Month LIBOR + 500 bps;

Track-III: Pricing should be in line with the markets

No specific price restriction but are generally priced in the range of 7.00% p.a. - 8.00%. The pricing also factors in the amount of the currency risk premium.

End-Use Restriction Track-I: Capital Goods, New Project, Expansion, Overseas investment, Refinancing of earlier ECB;

Track-II & Track-III: Can be for any purposes except (i) Real Estate (ii) Capital Market (iii) Equity Investment (iv) On-Lending for the above purposes & (v) Purchase of land

Can be for any purposes except (i) Real Estate (ii) Capital Market (iii) Activities prohibited as per FDI guidelines (iv) On-Lending for the above and (v) Purchase of Land

Borrowing Limit Total under Track-I; Track-II; Track-III: (i) Manufacturing & Infrastructure: USD 750.0 million; (ii) Software Development: USD 200.0 million; (iii) Micro Finance Institutes: USD 100.0 million (iv) Other remaining entities: USD 500.0 million

Automatic Route - Upto INR 50.00 billion per financial year; Approval Route – Beyond USD 50.00 billion subject to total limit of INR 2,443.23 billion for total foreign investments.

Currency Risk Resides with the Issuer Resides with the Investor

Masala Bond IssuancesMasala Bonds can be either freely traded after listing on any international stock exchange or can be privately placed. These bonds are generally listed on London Stock Exchange (LSE), Singapore Stock Exchange (SGX), Luxembourg Stock Exchange (BDL) and Stock Exchange of Mauritius (SEM).

LSE listed the first issue of such bonds in 2007 from Barclays Bank PLC while SGX listed the first global rupee denominated bond from International Finance Corporation (IFC) in 2013. Since 2007, 33 bonds have listed on LSE, raising more than Rs. 230.00 billion and since 2010, 16 bonds have listed on SGX, raising around Rs. 150.00 billion. Recently, in October 2016, the Province of British Columbia Canada became the first foreign government entity to issue Masala Bonds, raising Rs. 5.00 billion for 4

years at 6.60% p.a. However, the term, “Masala Bonds” was coined by IFC, a member of the World Bank Group, which is the most aggressive international issuer of Masala Bonds. Till date, IFC has raised more than Rs. 110.00 billion through this instrument, with maturities ranging from 3 years to 15 years, for funding infrastructure projects in India, channelling private sector investment in India and promoting green energy in India. In addition to the listed Masala Bonds, in March 2016, IFC has issued Uridashi Masala Bonds to mobilise Rs. 0.30 billion for 3 years at 5.36%, which were all subscribed directly from Japanese retail investors.

Among Indian corporates, HDFC Limited has successfully placed the entire permissible amount of Masala Bonds under automatic route, i.e. Rs. 50.00 billion. NTPC Limited, Indiabulls Housing Finance Limited, Fullerton India Credit

09 MASALA BONDS - INTERNATIONALISING THE INDIAN RUPEE

Company Limited and ECL Finance Limited have also successfully tapped the market. In November 2016, the RBI has issued guidelines, expressly permitting Indian Banks to issue Perpetual Debt Instruments (PDI) qualifying for inclusion as Additional Tier 1 capital and Debt Capital Instruments qualifying for inclusion as Tier 2 capital, by way of Rupee Denominated Bonds overseas. In addition to this, banks can also raise long term Rupee Denominated Bonds overseas for financing infrastructure as well as for affordable housing.

The Road AheadMasala Bonds are currently at a nascent stage. Due to the Indian Rupee’s limited convertibility, the instruments, though denominated in Rupee, are subscribed by

the investors into Rupee equivalent in their respective currency, which are then converted into Rupee, alongwith entering into optional hedging for currency fluctuation, all to the investors account. A similar process is followed for redemption. As the currency risk premium has to be borne by the investor, the same is factored into the pricing. The Rupee, which was trading as low as INR 62/USD in February 2015 was trading as high as INR 68/USD in February 2016. This high volatility, which affects a borrower of ECB but does not affect the lender of ECB, has a vice-versa effect in Masala Bonds. The pricing of Masala Bonds is linked to the Rupee volatility, and a stable Rupee would hold the key to the increased popularity of the Masala Bonds.

The global banking system is a large facilitator of global economic activity and trade through trade finance facilities which make transactions more efficient and bring in reliability and transparency into transactions. Accordingly, there are facilities of trade finance which drive economic development and maintains the flow of credit and cash within the global economic framework. It is estimated that 80-90% of annual global trade worth around $10 trillion is reliant on trade finance.

Trade finance has evolved over centuries across the globe from local practices to global practices bridging the gap between economies through advancement of transactions and technologies. The need of trade finance emanates from varying factors. While a seller can require the purchaser to prepay for goods shipped, the purchaser may wish to reduce risk by requiring the seller to document the goods that have been shipped. In such circumstances, a Bank based system of facilitating credit for Trade has evolved which involves documents of trade as well as Bank based assurances. With the advent of technology, the world has become smaller, which has facilitated in creating a methodology of trade and trade finance which is similar across the globe, which is a standard norm of the industry and which facilitates quick turnaround of goods, services and funds. Over the years, Banks and other financial intermediaries have participated to make domestic and international trade viable, accessible and practical.

Today, one of the main modes of Trade Finance, facilitated by the financial system, is through Letter of Credit. A plain understanding of Letter of Credit would mean as under:

A Letter of Credit has become the norm for International dealings. Factors such as distance between parties, differing laws in each country, and difficulty in knowing each party personally has resulted in the continued rise of use of letters of credit to facilitate international trade.

LETTER OF CREDIT A TOOL OF TRADE FINANCE

LETTER OF CREDIT - A TOOL OF TRADE FINANCE 10

LETTER OF CREDIT

It is an undertaking/promise given by a Bank or Financial Institution on behalf of the Buyer/Importer to the Seller/Exporter, that, if the Seller/Exporter presents the complying documents to the Buyer’s designated Bank/Financial Institution as specified by the Buyer/Importer in the Purchase Agreement then the Buyer’s Bank/Financial Institution will make payment to the Seller/Exporter.

11 LETTER OF CREDIT - A TOOL OF TRADE FINANCE

Parties to a Letter of Credit transaction:Generally, there are four parties to the transaction of a Letter of Credit (LC):

The letter of credit states the documents the beneficiary must present, the information they must contain, and the place and date it expires. Beneficiaries who sell goods and utilize a letter of credit as the method of payment, have the assurance of the issuing bank that if the beneficiary presents the documents stated in the letter of credit, the issuing bank will honour the demand for payment.

The bank that writes the letter of credit will act on behalf of the buyer and make sure that all documentary conditions have been met before making the payment to the seller.

As a letter of credit is a negotiable instrument, the issuing bank shall honour the payment in favour of the beneficiary or any bank nominated by the beneficiary. Where a letter of credit is transferrable, the beneficiary may assign the right to draw payment to another entity, such as a corporate parent or a third party.

Types of Letters of CreditThere are several types of letter of credit which are being issued by the banks depending upon the request and requirements of the clients:

With respect to trade terms of credit, LCs can be Sight LCs or Usance LCs. A broader understanding of these types of LCs is as follows:

APPLICANT ISSUING BANK BENEFICIARY BENEFICIARY BANK

The entity who has requested for the opening of LC, i.e. buyer or importer

The bank which issues LC for the buyer/importer

The exporter and in whose favour the LC is opened

Beneficiary bank which informs the exporter about the letter of credit being opened on the behest of the issuing bank. The Beneficiary Bank is generally based in the same place as exporter/seller

SIGHT LC

USANCE LC

A Sight LC causes payment to be made immediately to the beneficiary/seller/exporter upon presentation of the correct documents.

A Usance LC specifies when payment is to be made at a future date and upon presentation of the required documents.

LETTER OF CREDIT - A TOOL OF TRADE FINANCE 12

While the LCs mentioned above relate to the time period within which the payment may be made in the underlying LC and Trade transaction, the following LCs focus on the method of assurance of payment.

In the current business environment, the above mentioned types of letter of credit are popular and prevalent across business dealings. However, there are certain other types of LCs as well, which are used now-a-days. Some of them are mentioned below:

STANDBY LETTER OF CREDIT

REVOLVING LETTER OF CREDIT

TRANSFERABLE LETTER OF CREDIT

A Stand by Letter of Credit is like a guarantee that is used as support where an alternative, less secure, method of payment is agreed. It is an assurance from bank that a buyer is able to pay a seller. The seller doesn’t expect to have to draw on the letter of credit to get paid.

A transferable letter of credit can be passed from one beneficiary to others. They are commonly used when intermediaries are involved in the transaction.

The revolving letter of credit is usually used in construction industry. It allows beneficiary to draw on the letter of credit, up-to a certain amount, usually without presentation of documents. The account party replenishes the account.

Revocable Letter of Credit

This type of LC allows for amendments, modifications and cancellation of the terms outlined in the letter of credit at any time and without the consent of the exporter or beneficiary. Generally such LCs are not popular in business transactions.

Irrevocable Letter of Credit

This type of LC requires the consent of the issuing bank, the beneficiary and the applicant before any amendments, modifications and cancellation of the terms outlined in the letter of credit can be made. Irrevocable letter of credit can be

a. Confirmed: The seller/beneficiary may also look for additional credit comfort from confirming bank for payment assurance.

b. Unconfirmed: When letter of credit is not confirmed by any bank other than the issuing bank.

c. Back to Back: Opened with another letter of credit as security i.e. if a foreign buyer issues a letter of credit to an exporter, certain banks and trade finance companies would issue independent letter of credits to the exporter’s supplier so that the required goods can be purchased.

Deferred Payment Letter of Credit

Deferred Payment LC allows the issuing banks to make payment to the beneficiary in instalments. The timing and amount of these instalments are predetermined. The buyer accepts the documents and agrees to pay the issuing bank on fixed maturity date; ensuring that the buyer gets benefit of periodic payments.

1. An Illustrative understanding of the flow of an ‘At Sight’ LC is as follows: The buyer and seller agree upon the contract for purchase and sale of goods at agreed upon LC terms.

2. The buyer requests its bank, the issuing bank, to open a LC for the purchase of goods from the particular seller under the specified terms and conditions for payment against all documents.

3. The issuing bank opens the LC.

4. The LC is given to the seller’s bank – the advising bank.

5. Once seller gets the LC under the accepted terms and conditions, goods are shipped to buyer.

6. The seller produces shipping documents to its advising bank.

7. The advising Bank communicates with the issuing bank and on confirmation, makes payment to the Seller.

Correspondence between the Issuing Bank and the Advising Bank:Issuing Bank represents the Buyer or importer who has requested for the Letter of Credit to be opened for the purchase or import of goods. The Advising Bank represents the seller of the goods. Once the LC is issued by the Issuing Bank and given to the seller, the seller goes to its advising bank and requests for the payment of the LC.

The transaction involves a movement of communication between Banks to facilitate this trade, something which has been standardised over the years. The International Chamber of Commerce have published the Uniform Customs and Practice for Documentary Credits

(UCP Guidelines), which govern the method in which communication transpires between Banks for facilitating LC transactions. The rules stated in UCP 600 cover the method in which LCs/document of credit are issued and the standardised terms used to communicate between banks for LCs.

In the modern electronic world, the banking community use SWIFT messages, an Electronic medium of transmitting and receiving instructions between banks, which has standardised the flow of information and instruction. For E.g.: a Bank must use MT700 - Issue of Documentary Credit when issuing a letter of credit and MT 734 advice for refusal when giving its refusal message.

It is pertinent to note that domestically the law of contracts apply to Letters of Credit; however, the idea of standardising the nomenclature, rules and regulations of Letter of Credit is to avoid any litigation on account of misrepresentation or miscommunication of trade terms. Accordingly, the UCPs are not laws but are standardised which form part of every contract of LCs in order to remove any ambiguity and consequential litigation.

Letter of Credit in the Digital AgeAs the world moves to a digital way of doing business, banks have started to issue On-Line Letters of Credit, which reduces the time and effort for the successful conclusion of the transaction.

In India, banks issue On-Line Letter of Credit for the clients who have online banking accounts. Bank issue a ‘SFMS’ code to the company after opening the LC and by putting this code on the website, the advising bank can see the LC online. After uploading the documents online, the advising banks can ask for the confirmation from the issuing bank

13 LETTER OF CREDIT - A TOOL OF TRADE FINANCE

SELLER

1. Sales contract with LC terms

7. Reimbursement is claimed under the LC

6. Shipping documents are presented

4. LC advised (delivered)

2. LC application

5. Goods are shipped

3. LC issued (drawing under buyer’s line of credit)

Exporter’s Bank Advising and

Confirming Bank

Importer’s Bank Issuing Bank

BUYER

Flow of the LC Transaction:

Letter of Credit: Figure A

online. This has significantly reduced time and increased the efficiency of the transaction. It is only a matter of time before more business will be traded in paper less format to facilitate faster trade.

Conclusion Letters of Credit have been a cornerstone of international trade dating back to the early 1900s and continue to play a critical role in modern world of global trade. The letter of credit allocates risk between the applicant and the beneficiary. By receiving a letter of credit, the beneficiary may greatly reduce the risk of not being paid and ultimately allowing the beneficiary of the letter to reallocate the risk of non-payment for delivered goods which do not conform to the underlying sale contract. Generally, banks are reluctant to dishonour a credit as it may damage the bank’s reputation as a credit issuer. For any company entering the international market, Letters of Credit are an important payment mechanism which helps eliminate several trade risks. As time goes by, this will be the most prevalent form of trade finance and as technology improves, the time and cost of such transactions will come down, eventually helping businesses all across.

LETTER OF CREDIT - A TOOL OF TRADE FINANCE 14

GOAL BASED INVESTINGA STRUCTURED APPROACH

15 GOAL BASED INVESTING - A STRUCTURED APPROACH

We all want to live the Indian dream – owning the house we want, holidays at dream destinations, a well-provided future for children and a relaxed retirement. The dream is possible to live if you plan your finances well in life, for good times and not so good times, and maintain a strategy for investments which are modelled to achieving this dream. There are three basic disciplines that one may need to follow – plan your goals, invest wisely and monitor your investments.

Goals-Based Investing - A Rewarding ApproachEvery Important Journey has a destination. Similarly every investment should have a Goal, and each Goal should be time based. Quantifying the amount of money needed to achieve that goal is important. Goals-based investing is a powerful tool to help empower every individual against market fear and uncertainty by better managing your personal preferences, biases and behaviors that can undermine your financial success. Investing according to your unique needs, desires and time horizons in a way that encourages you to look beyond intermittent market volatility, economic transformation and International uncertainties can differentiate your portfolio and improve your own odds for long term success. Early Start is the mantra to achieving your Goals timely.

The efficacy of an investment strategy is not measured only by traditional yardsticks like market indices, benchmarks and standard deviation. Specific goals are very meaningful, and that is what distinguishes the modern

approach from others where investment strategies are specifically designed around each person’s personal goals. Performance is measured by a person’s progress toward achieving each stated goal and risk is viewed as the probable failure to fully achieve each goal. Goals-based investing also recognizes that investors have multiple and sometimes conflicting goals. Rather than pool all assets into a single portfolio, a separate portfolio “bucket” can be created for each goal - accumulate assets for retirement, save for a vacation home, build a legacy for heirs, child’s education or achieve any other number of goals. A Professional Wealth Advisor can structure an investment strategy that can be specifically tailored to each goal.

Traditional Approach vs. the Modern Approach to InvestingThe Traditional Investment Approach was - Identify two or three goals, and identify a single investment avenue or investment bucket to meet all the identified goals. At that point, you are prepared to expect a given return based on the historic or expected performance and volatility of various market benchmarks.

The Modern Portfolio Theory considers every goal as a separate milestone. Selecting the right mix of investments is the key driver to meeting these milestones. Goals can be broadly bifurcated into 2 types – Have-to-Have Goals and Nice-to-Have Goals. One would want to take less risk with the funds designated for “have-to-have” financial goals, such as covering day-to-day living expenses, while accepting more risk for discretionary “nice-to-have” goals,

HAVE TO Pay Insurance Premiums /Living

ExpensesChilds Marriage House Retirement University Degree

GOAL BASED INVESTING - A STRUCTURED APPROACH 16

like luxury vacations. “Have-to-have” financial goals are characterized as fixed in nature and cannot be mitigated or have no substitutes whereas “nice-to-have” goals have the inherent freedom of amendment. For example: You can also convert an International Holiday into a Domestic Holiday but there is no substitute for ensuring a good education for your children.

It’s not another TO-DO-LIST Goal setting should be taken seriously rather than treating it as another to-do-list. Every goal has a financial implication. While there is a structured approach to goal setting the perspectives of various goals for members of a family may be different which could take a few days at times to arrive at the right set of goals for which a plan is to be made. Goal setting is not just dreaming of the

“what if” but should be rational and well within a person’s means and perceived financial ability. Goals evolve over a period of time with changing circumstances and hence it is important to re-visit these goals when the time comes and rebalance your strategy and investments.

Short, Medium and Long term GoalsShort-term goals are priorities that can be accomplished within a period of 12 to 15 months. These are easiest to plan as they are immediate in nature and hence are relatively easier to achieve.

Mid-term goals are priorities that can be accomplished within 2 to 5 years. Mid-term goals should be realistic, flexible and rational.

Long-term financial goals are priorities that have a horizon of more than 5 years to accomplish. Long-term goals require good planning and an investment plan which is regular and dependable. Long term goals have many facets but retirement is an important aspect that many fail to factor into their long term goals.

SHORT TERM LONG TERMMEDIUM TERM

Paying Insurance Premiums every year

A foreign holiday once a year

Renovation of house or purchase of home décor

Buy a house after 3 years

Child is going to pursue a professional degree after 3 years

Wish to take a sabbatical after 2 years

Childs marriage after 10 years

Retirement after 20 years

World tour post retirement

WANT TOVacation Car 2nd Home

The Perception of Risk and InvestingTraditional financial planning places market volatility at the top of the list of risks to mitigate. Therefore, an investor’s risk tolerance or risk preference (i.e., an investor’s aversion to risk) is gauged to help drive his or her investment strategy. Alternatively, in the goals-based approach, while mitigating market volatility is an important consideration, the chief risk is the failure to reach a specific goal. With goals-based planning, not only is an investor’s risk tolerance gauged, but also the investor’s risk capacity for each goal

— with a greater emphasis on risk capacity.

In terms of risk, traditional planning can leave investors exposed to unintended consequences. When an investor’s

risk tolerance exceeds his or her risk capacity, there can be a detrimental effect on the portfolio, slowing the progress toward achieving life goals.

In contrast, by aligning an investor’s asset allocation to an investor’s risk capacity for each goal, the planning process can be made both more efficient and more flexible. For example, a person would have less risk capacity for an essential goal (e.g., funding a child’s education), which calls for a more conservative investing approach, but would have greater risk capacity for a non-essential or discretionary goal (e.g., buying a vacation home), which calls for a more aggressive one.

Benefits of Goal Based PlanningCompared to the traditional approach, the goal based approach certainly has several benefits. The following are some key benefits of goal based investment planning:

Key Differences between the Traditional Approach and the Goal Based Approach

17 GOAL BASED INVESTING - A STRUCTURED APPROACH

Traditional Approach Goal Based Approach

An investment plan is created based on a common risk analysis as well as parameters of expected return and such other finan-cial factors

An investment plan is created based on planned goals, identified risk profile for each goal and expected capital at defined points in life with goal specific returns expectation aligned to goal specific risks.

Assets are allocated to a single portfolio and monitored at an overall level

Assets are allocated based on specified goals and monitored as per expected risks and returns for each goal.

Overall risks are managed in this approach Goal specific risks are managed in this approach considering the failure to meet a specific goal

Performance assessed to benchmark performance Performance is measured based on goal specific expectations

Is sharper and more focused to investment planning for the individual investor as well as his/her financial advisor

Identified goals and mapped to specific risk appetite and time horizon for each goal which creates a better understanding on the importance of each goal and the type of investment avenue to be chosen for each type of goal

It increases the risk/return understanding and increases trust and confidence in the client-advisor relationship as well as in the investment planning process

Creates a sense of understanding in the investor that the importance is not only on meeting expected returns but also in making sure that the expected capital is available for each importance phase in his/her life based on anticipated goals

Reduces the chances of volatility in planned need vs actual available funds when the goal is reached as investments are planned and monitored regularly with goal achievement as the primary focus

Provides an opportunity to rebalance the portfolio, based on changing market circumstances, in a meaningful manner to ensure goals are not compromised

New identified goals can be planned within the existing investment plan or new investment plan can be easily made/carved out for the new goal identified

⎖Rationalises the expectation of an advisor meeting expected return to achieving planned goals

Benefits of Goal Based Planning

Conclusion The investment planning and management process is successful only if an investor meets his/her investment objectives. Defining these objectives is where goal based investing comes into play. Goals are not static and will change as and when circumstances in life evolve and hence the plan should be monitored on a periodic basis.

At Vivro Wealth Advisors we understand that investing without an objective or goals is like shooting in the dark. We have encouraged our clients to identify goals and quantify the capital needed when those goals come up – whether long term, medium-term or short term. Goals-based investing gives us a powerful framework for customizing an investment approach and assisting our clients realise their important financial goals. Goal based planning deepens our understanding of our clients and makes the process of investment planning more interactive, focused and effective. It improves upon the traditional portfolio construction and risk management. With our goal based planning approach, we are able to bring greater discipline to investment planning with an aim to bring our clients dreams and desire into reality.

GOAL BASED INVESTING - A STRUCTURED APPROACH 18

IntroductionOne of the roles the government plays in a country, be it at a local body, district, state or central level, is to create public infrastructure to meet the growing needs of an economy and to facilitate the development and prosperity of land available as well as the people within the community. Solid, effective and efficient infrastructure is an essential factor which affects the quality of life, health and livability of people in the society. For a country like India, Increased migration from rural areas to cities has led to rapid expansion of urban areas. The high economic growth rates and rapid urbanization of the last two decades has brought about the need to have supportive infrastructure from public investments as well as private.

While the government has been instrumental in making huge investments in infrastructure assets like roads, airports and mass transit to open up suburban vicinities, private investments in townships, industries, and commercial establishments have catalyzed rapid economic development in these areas, resulting into large positive externalities, most of which gets captured by the property owners in value terms. However, the value which accretes to private owners does not make itself available in constant value terms to the people of that community. Land Value Capture or Value Capture Financing is a method adopted by governments where such unearned increments can be captured at least in part, in a structured and well defined manner for the betterment and benefit of the people of that community. As per the Vancouver Action Plan – the

founding document of the UN Habitat (United Nations, 1976) – “The unearned increment resulting from the rise in land values resulting from change in use of lands, from public investment or decision, or due to the general growth of the community must be subject to appropriate recapture by public bodies”.

Global Practices Land Value Capture has long been advocated by international organizations as a funding source to support local improvements in urban infrastructure and services. Developed countries across the globe have more often adopted the concept of Land Value Tax (LVT), a method of raising public revenue by means of an annual charge on the rental value of land. Land value taxation is currently implemented throughout Denmark, Estonia, Lithuania, Russia, Hong Kong, Singapore, Taiwan and sub regions of Australia, Mexico and the United States.

Although several approaches have been used and debated on, it can be broadly classified into two main categories: A one-time fee and associated taxes and annually recurring taxes.

VALUE CAPTURE FINANCING A GOVERNMENT MECHANISM

TO MONETIZE VALUE

19 VALUE CAPTURE FINANCING A GOVERNMENT MECHANISM TO MONETIZE VALUE

VALUE CAPTURE FINANCING A GOVERNMENT MECHANISM TO MONETIZE VALUE 20

Practices in IndiaTraditionally, urban infrastructure is financed through higher government grants/transfers, augmentation of local self-revenues above operating expenses and long term borrowing in India. However, Indian cities continue to need heavy amounts of capital for financing urban infrastructure; an estimate by McKinsey Global Institute pegs it at $1.2 trillion over the next 20 years. It is a matter of challenge owing to the prevailing scarcity of public financing.

Urban and Non-Urban areas in India have used different methods to capture the benefits accruing to private people, such as impact fee, betterment charges, etc. The most common strategy to capture value created by investment externalities is through different forms of taxation. A brief description of an illustrative list of such VCF methods is outlined below.

Country Policy in Practice

Canada The value of every parcel of land in Canada would be assessed regularly and the land value tax levied as a percent-age of those assessed values.

Land means the site alone, not counting any improvements. Any improvement or addition which people have erected or carried out on each plot of land is assumed to be developed as at the time of the valuation.

United States

Various cities of Pennsylvania in United States have adopted a two-rate tax mechanism, i.e. Taxing the value of land at a higher rate and the value of the buildings and improvements at a lower one. Two-rate taxation may be seen as a form that allows gradual transformation of the traditional real estate property tax into a pure land value tax.

Russia Land Tax is a municipal tax levied on the cadastral land value and the applicable rate varies depending on the use of the land and the property tax is levied on buildings, apartments, constructions and garages ranging from 0.1% to 2.2% depending on the value of the property.

United Kingdom

Multiple attempts have been made to implement the land value capture tax in some or the other form, however, it is still under active discussions owing to greater non acceptability. Most recently in 2011, it has begun to implement a Community infrastructure levy intended to recover the cost of infrastructure investments.

Countries like China, Ireland, Kenya, Namibia, Scotland, etc. are under active discussion and consideration stage to implement the value capture financing concept in some or the other acceptable form.

Practices Explanation

Property Tax This mechanism of taxation is one of the oldest systems in India which includes tax on land and improvements on land, with the government appraising the monetary value of each such property and assessing the tax in proportion to its value.

The proceeds are generally used to develop local amenities including road repairs, maintenance of parks and public schools, etc. and vary from location to location and can be different in different cities and municipalities.

Fees for Change in Use

Land in its original form is and can be owned by the agriculturists only. Hence, individuals and corporates intending to purchase land have to mandatory register for change in use from agriculture to commercial/ residential/industrial.

For conversion and change in use of the land, the owner has to pay a one -time premium amount in line with the defined rates which may defer from location to location.

Impact Fee Impact Fee structure has been widely used across major states of India like Andhra Pradesh, Gujarat, Maharashtra, Tamil Nadu and Madhya Pradesh. Impact Fee is a type of area development charges which covers land and build-ings equally.

While impact fee norm gives Illegal buildings and construction an opportunity to get legalized in some states like Gu-jarat, some governments charge it to the land parcels/ properties which are expected to get appreciation in property prices due to its proximity to big ticket infrastructure projects.

Impact fee rates are payable by the owner at the time of legalizing the illegal construction and at time of sale/ develop-ment of a particular zone which is expected to appreciate.

21 VALUE CAPTURE FINANCING A GOVERNMENT MECHANISM TO MONETIZE VALUE

Practices Explanation

Charges on Transfer/ Extension of Rights

Transferable Development Rights (TDR) permit certain amount of additional built up area in lieu of the area relinquished or surrendered by the owner of the land. Although a TDR program is most commonly considered a means to preserve farmland, forest or open space, it can also be used to preserve affordable housing in urban areas.

States like Gujarat, Maharashtra and Karnataka are enabling laws for this mechanism.

Town Planning Schemes

States like Gujarat and Haryana have used Town Planning Schemes to use the owners barren lands for infrastructure serviced smaller plots. Gujarat has more often used this mechanism to develop in and around areas of cities like Ahmedabad.

Value Capture Financing PolicyValue Capture Financing (VCF) is a type of public financing that acts as a tax collection mechanism and aims to recover part or full of the value that public infrastructure generates for private landowners. It owes to act as a funding source for urban investment. It works on the principle that the appreciation in land valuation occurs due to regulatory changes, investments in public infrastructure that increases quality of housing, jobs access, transportation or social benefits and emergence of an important commercial, cultural, institutional, or residential developments in the neighborhood.

State urban regulators have been developing and exercising several VCF mechanisms to mobilise resources from the benefits accruing to the private owners under various heads. However, this practice is restrictive to the state regulators only and do not cater to the requirement of other government bodies like Railways, Roads and Highways, Urban Development, etc. Moreover, these practices are not uniformly practiced across India. Non-urban areas are hardly known to these mechanisms due to lack of deployment of any systematic methods. Hence, there was a need felt to formalize this value capture mechanisms.

Working on the directives of Prime Minister’s Office, the Centre has given a final shape to India’s first Value Capture Financing policy, which would help the government recover some value that public infrastructure investments generate for private landowners. Apart from state governments, following bodies are anticipated to benefit from the mechanism:

Targeted Agencies Typologies of Projects

Ministry of Urban Development

Missions initiated by Government of India, Promote Smart City Mission

Ministry of Railways High Speed Rail Projects, Expansion of rail network

Ministry of Road & Transport

Metro Projects, Infrastructure Upgrade Projects, Heritage Conversion

Department of Industrial Policy and Promotion

Special Economic Zones, Industrial Parks, Initiatives for industrial development

Ministry of Power Power Generation Parks

Ministry of Shipping Expansion of Cargo Terminals, Free Trade Zones, Constructions of Ferry and Cruise Terminals

VALUE CAPTURE FINANCING A GOVERNMENT MECHANISM TO MONETIZE VALUE 22

As stated above, the resources raised from such financing are largely aimed to be used for further infrastructure developments, pass on the benefit of government infrastructure to the uncultivated and suburban/ non-urban areas.

Proposed FrameworkThe VCF policy framework has been recommended by the committee headed by Mr. Sameer Sharma, Additional Secretary of Urban Development Department. The framework differentiates urban areas from non-urban areas and supports the view that various factors like multiplicity of investment partners, the difference in the types of projects and the resources involved, the local and state regulations, the location etc. should be considered to determine the complexity of devising a standard VCF policy. It seeks to offer multiple options across agencies and projects and greater flexibility to design VCF methods.

The urban areas will have various options to choose from any of the VCF methods after assessing the existing VCF tools prevalent in the State and identify areas

where it is required. They may choose to extend existing value capture tool or put it forth with revision in rates or procedures so as to make it acceptable to the applicable crowd.

The framework proposes the challenge method for the non-urban areas. This challenge will be in respect to selection of the site and the infrastructure project. It means different areas in a state could compete against each other to bag an SEZ project. It could also be applied to a bouquet of projects with the government initiating a project which has a VCF model.

The policy intends to create uniformity in regulation and practices across the country in respect to land value capturing, hence, allowing fair allocation of costs among all stakeholders as well as a positive feedback loop where value is created, realized, captured and recycled to be given back to the society, which will usher prosperity and growth for all. It will act as a powerful tool to trigger urban transformation through new public infrastructure creation as well as promote suburban areas towards development.

Value Capture Financing -

A Positive LoopValue

ReinvestedValue

Realization

Value Creation

Value Capturing

Actual increase in prices due to the

positive externalities

Value Capture Financing in form of

fees/ charges/ taxes to Government

Public/ Private Investments

Value of Barren/ Under used asset to increase after public/

private investments

Conclusion Effective Land Value Capturing is crucial and requires strong political and decentralized authority to implement it. Efficient and accurate land valuation is an essential step towards an effective value capture system. A well thought out and regulated methodology to capture value of appreciating land resources shall ensure efficient recoveries of cost from existing projects and shall ensure availability of funds for future projects of development.

Although the VCF policy gets a cabinet nod, the formal policy is yet not public. Introduction of a policy aligning the different prevalent mechanisms is definitely going to be one of the most important legislative reforms in the country which will streamline and systemize government revenues and provide them with more room for planning and executing envisaged developments.

23 VALUE CAPTURE FINANCING A GOVERNMENT MECHANISM TO MONETIZE VALUE

ABOUTVIVRO

About VivroVivro is a Financial Services Group engaged in the business of providing Investment Banking, Corporate Finance, Corporate & Financial Advisory and Wealth Management Services. Vivro Financial Services Private Limited is a Merchant Banker registered with the Securities Exchange Board of India (SEBI).

Our TeamVivro is founded by experienced professionals who have been engaged in Capital Market and Corporate Finance services for the last three decades. Our company is supported by a team of more than 90 enthusiastic and motivated people from different backgrounds with varied educational accomplishments and expertise. The talent pool of our company comprises of Chartered Accountants, Company Secretaries, MBAs, Lawyers as well as Ex-Bankers who have held senior positions at various banks and financial institutions. This mix of people infuses elements of creativity and professionalism in our workplace, which adds tremendous value to the services that we offer. With a strong team in place, Vivro is able to deliver value added solutions, tailor-made to suit the requirements of our clients.

Our Value PropositionVivro has emerged as a knowledgeable and reliable partner for businesses both in India and Abroad. Vivro has catered to several companies over the years and it enjoys tremendous confidence from clients, investors, lenders, brokers and financial institutions. Our advisory services and our ability to access the right capital for the right investment opportunity have resulted in significant stakeholder value creation. Vivro has a disciplined and demonstrated process specifically tailored for each client and transaction to maximize value.

ABOUT VIVRO 24

Capital Market ServicesOur Capital Markets team assists private companies to raise capital from capital markets through Initial Public Offers of Equity & Debt, Placements, while they assist public limited companies in a host of capital market transactions ranging from Rights Issue, Qualified Institutional Placements, Institutional Placement Program, Takeovers and Open Offers, Buybacks, Delistings, etc.

Corporate FinanceVivro syndicates and structures debt finance from banks and financial institutions through several instruments such as:

• Term Loans/ Project Loans

• Working Capital Finance/ Corporate Loans/Letter of Credits/Bank Guarantees/External Commercial Borrowings

• Factoring/Commercial Paper

• Inter Corporate Deposits, Structured Finance, Infrastructure Financing, etc.

Corporate AdvisoryOur corporate advisory services include:

• Private Equity and Venture Capital placement and advisory

• Mergers and Acquisitions: Buy/ Sell advisory as well as Schemes of Arrangement for Corporate Reorganization

• Valuation Services and Fairness Opinions

• ESOP Structuring and Valuation

• Business and Expansion Plans and Strategies

• Corporate Governance Reporting

• Succession Planning

• Entry into India Services

Wealth ManagementVivro Wealth Advisors Private Limited, a wholly owned subsidiary of Vivro Financial Services Private Limited provides Wealth Management solutions to its retail and corporate clients. Our Wealth Advisory journey begins with understanding the needs of our clients, which forms the basis of our investment solutions across asset classes. We deliver solutions which are aligned to our client’s goals, priorities, aspirations and risk tolerance. We follow the maxim – ‘What is right for the client is right for us’ while delivering the Financial Plan. We also offer our Treasury Management solutions to corporates through which we assist in planning and making investments in a variety of financial instruments such as fixed income funds, equity funds, commodity funds etc.

25 ABOUT VIVRO

Mumbai607-608 Marathon Icon, Veer Santaji Lane, Opp. Peninsula Corporate Park, Off Ganpatrao Kadam Marg, Lower Parel, Mumbai- 400013.E [email protected]: +91 22 6666 8040

Vadodara2, Maruti Flats, 31, Haribhakti Colony,Race Course Circle, Baroda - 390007E: [email protected]: +91 265 235 7339

SuratShiv Smruti Complex, Flat No. M - 1, B- Block, Mezzanine Floor, Besides Turning Point, Ghod Dod Road, Surat – 395001E: [email protected]: +91 261 223 2740

ChennaiAppaswamy Manor, Old No.9/New No.16, IInd Floor 4th Cross Street, CIT Colony, Mylapore Chennai - 600 004E: [email protected]: +91 44 2498 6774

AhmedabadVivro House 11, Shashi Colony, Opposite Suvidha Shopping Center, Paldi, Ahmedabad – 380007Gujarat, India.E: [email protected]: +91 79 4040 4242

OFFICES

www.vivro.net | [email protected]

CORPORATE OFFICE

The information contained herein is of general nature prepared by Vivro Financial Services Private Limited (‘VFSPL’, ’Vivro) on a particular subject or subjects and is not an exhaustive treatment of such subject(s). It is not intended to address the circumstances of any particular individual or entity. This material contains information sourced from third party sites (external sites). Vivro is not responsible for any loss whatsoever caused due to reliance placed on information sourced from such external sites. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2016 Vivro Financial Services Private Limited