fintech adoption index client presentation · page 9 ey fintech adoption index imperative #1:...

TRANSCRIPT

EY FinTech adoption index

Key findings

Page 1 EY FinTech adoption index

Introduction to EY’s FinTech adoption index

Overview

► Survey of over 10,000 online users

across six markets

► Respondents were asked about their

awareness and usage of a range of online

financial services products

► Careful explanation of products (avoiding

jargon, using brand names)

► Questions on reasons why/or why not use

the services

► Key topics covered in the study:

► Who is using FinTech?

► What services are being used?

► Why are they using it?

Page 2 EY FinTech adoption index

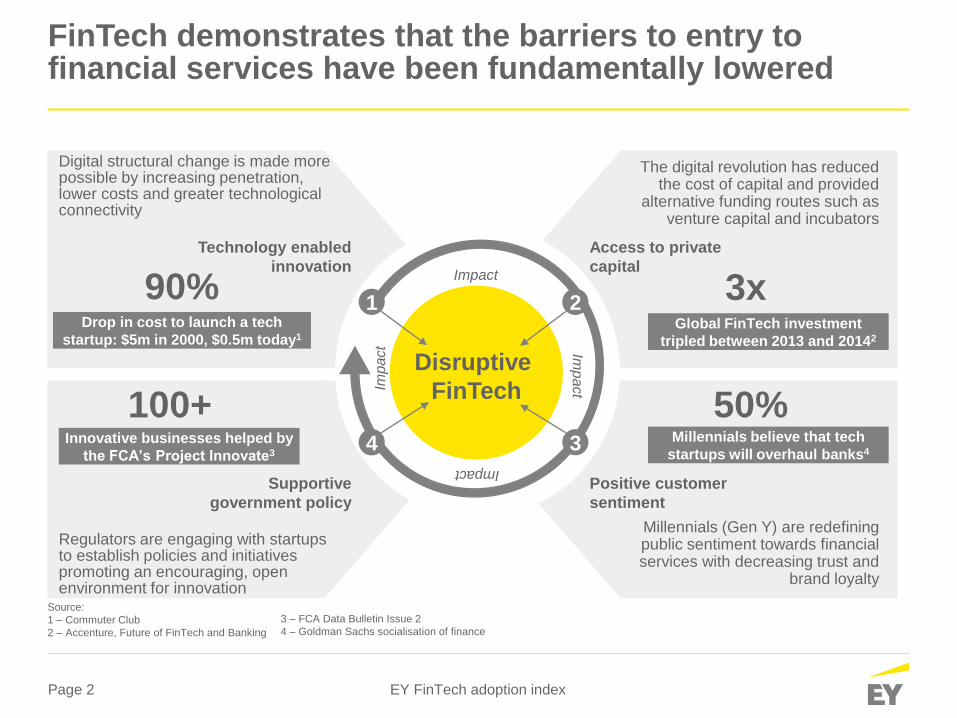

FinTech demonstrates that the barriers to entry to financial services have been fundamentally lowered

Digital structural change is made more possible by increasing penetration, lower costs and greater technological connectivity

Regulators are engaging with startups to establish policies and initiatives promoting an encouraging, open environment for innovation

Drop in cost to launch a tech

startup: $5m in 2000, $0.5m today1

90%

Innovative businesses helped by

the FCA’s Project Innovate3

100+

3x

Source:

1 – Commuter Club

2 – Accenture, Future of FinTech and Banking

Supportive

government policy

3 – FCA Data Bulletin Issue 2

4 – Goldman Sachs socialisation of finance

Global FinTech investment

tripled between 2013 and 20142

The digital revolution has reduced the cost of capital and provided

alternative funding routes such as venture capital and incubators

Millennials (Gen Y) are redefining public sentiment towards financial services with decreasing trust and

brand loyalty

Millennials believe that tech

startups will overhaul banks4

50%

Positive customer

sentiment

Imp

act

Disruptive

FinTechIm

pact

Impact

ImpactTechnology enabled

innovation

Access to private

capital

21

4 3

Page 3 EY FinTech adoption index

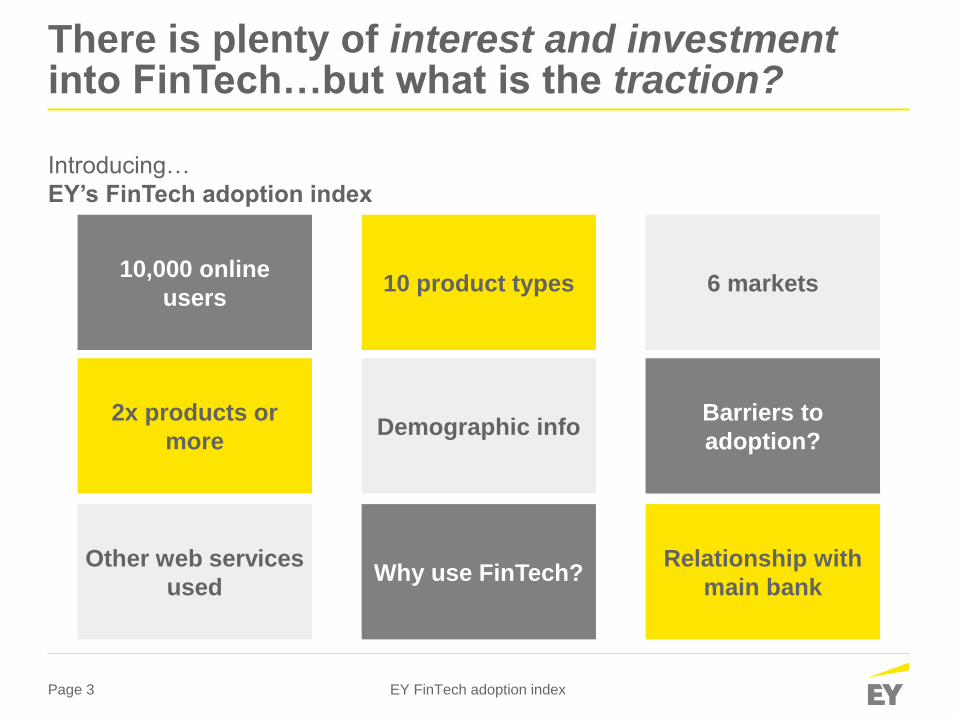

There is plenty of interest and investment into FinTech…but what is the traction?

Introducing…

EY’s FinTech adoption index

10,000 online

users10 product types 6 markets

2x products or

moreDemographic info

Barriers to

adoption?

Other web services

usedWhy use FinTech?

Relationship with

main bank

Page 4 EY FinTech adoption index

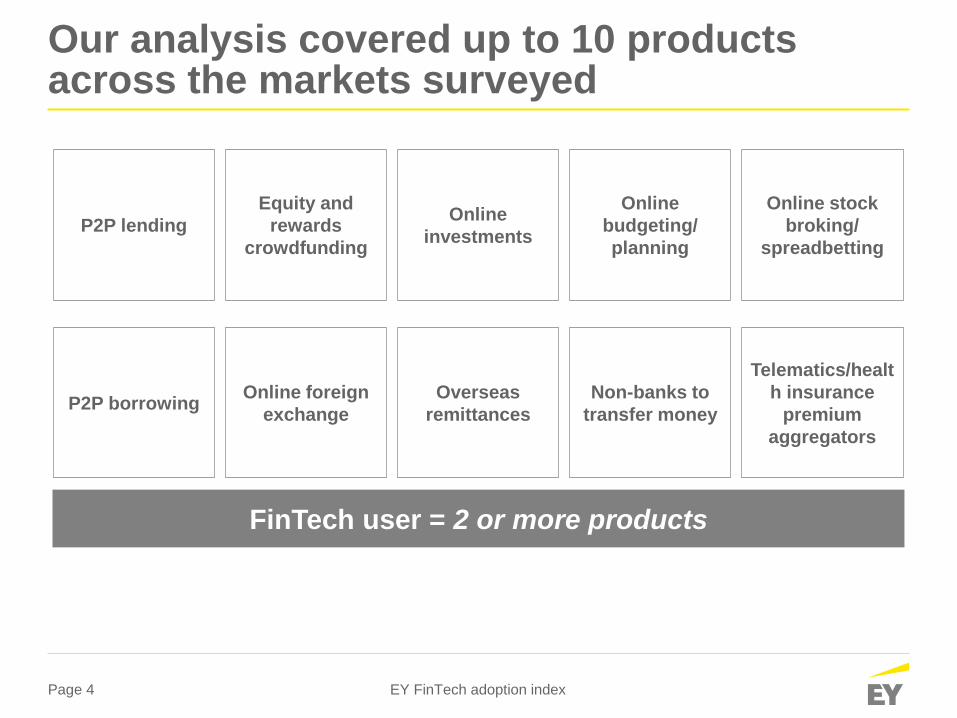

Our analysis covered up to 10 products across the markets surveyed

P2P lending

Equity and

rewards

crowdfunding

Online

investments

Online

budgeting/

planning

Online stock

broking/

spreadbetting

P2P borrowingOnline foreign

exchange

Overseas

remittances

Non-banks to

transfer money

Telematics/healt

h insurance

premium

aggregators

FinTech user = 2 or more products

Page 5 EY FinTech adoption index

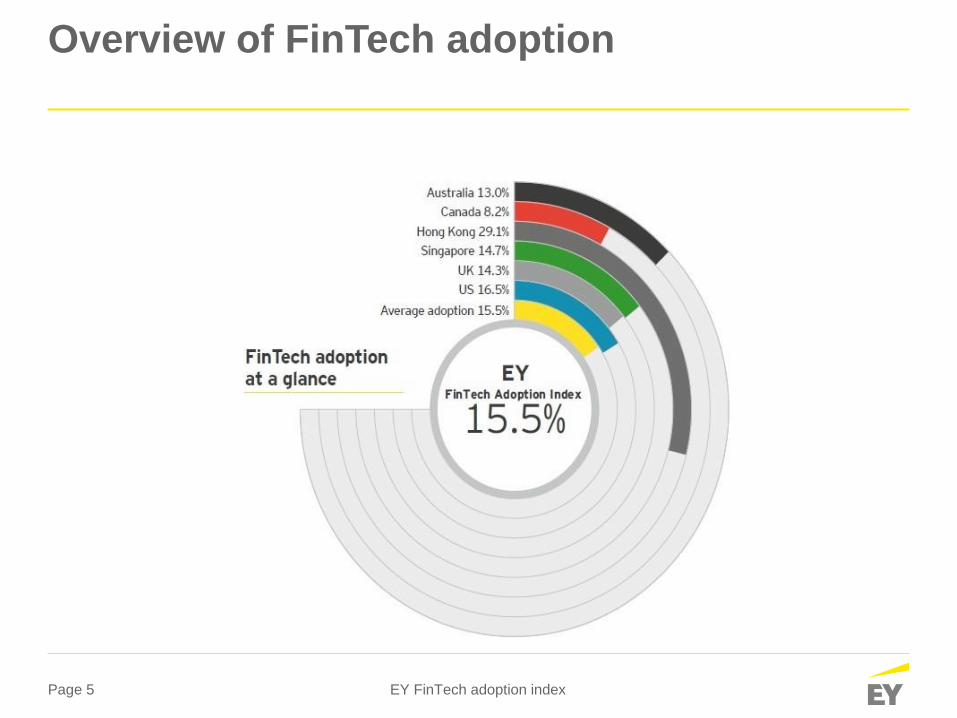

Overview of FinTech adoption

Page 6 EY FinTech adoption index

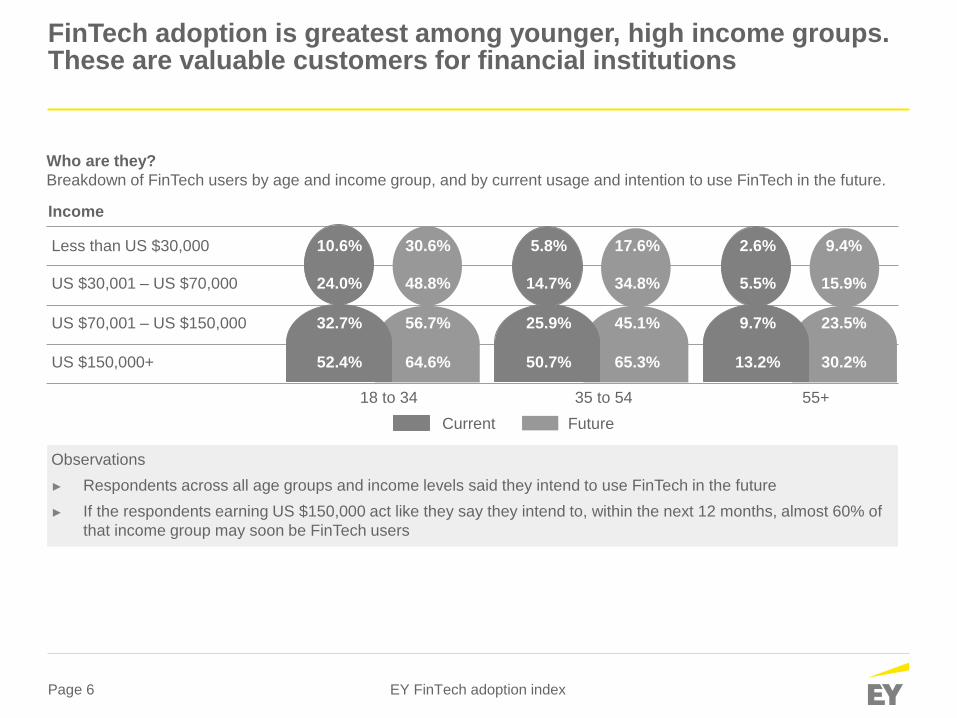

FinTech adoption is greatest among younger, high income groups. These are valuable customers for financial institutions

Who are they?

Breakdown of FinTech users by age and income group, and by current usage and intention to use FinTech in the future.

Observations

► Respondents across all age groups and income levels said they intend to use FinTech in the future

► If the respondents earning US $150,000 act like they say they intend to, within the next 12 months, almost 60% of

that income group may soon be FinTech users

Less than US $30,000

US $30,001 – US $70,000

US $70,001 – US $150,000

US $150,000+

Income

Current Future

10.6% 30.6% 5.8% 17.6% 2.6% 9.4%

24.0% 48.8% 14.7% 34.8% 5.5% 15.9%

32.7% 56.7% 25.9% 45.1% 9.7% 23.5%

52.4% 64.6% 50.7% 65.3% 13.2% 30.2%

18 to 34 35 to 54 55+

Page 7 EY FinTech adoption index

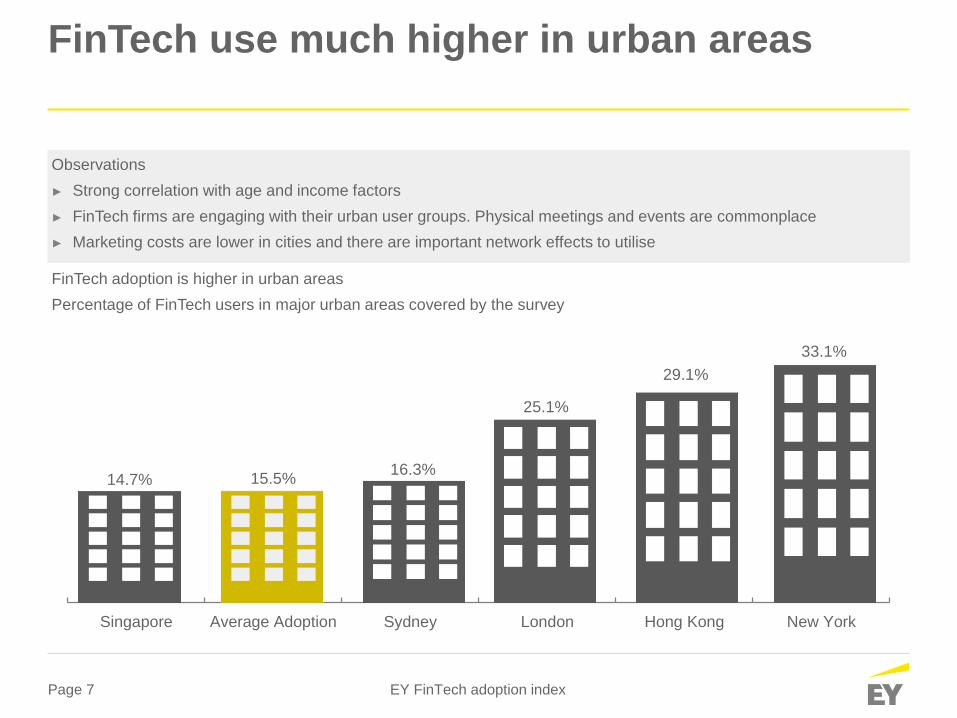

FinTech use much higher in urban areas

FinTech adoption is higher in urban areas

Percentage of FinTech users in major urban areas covered by the survey

14.7% 15.5%16.3%

25.1%

29.1%

33.1%

Singapore Average Adoption Sydney London Hong Kong New York

Observations

► Strong correlation with age and income factors

► FinTech firms are engaging with their urban user groups. Physical meetings and events are commonplace

► Marketing costs are lower in cities and there are important network effects to utilise

Page 8 EY FinTech adoption index

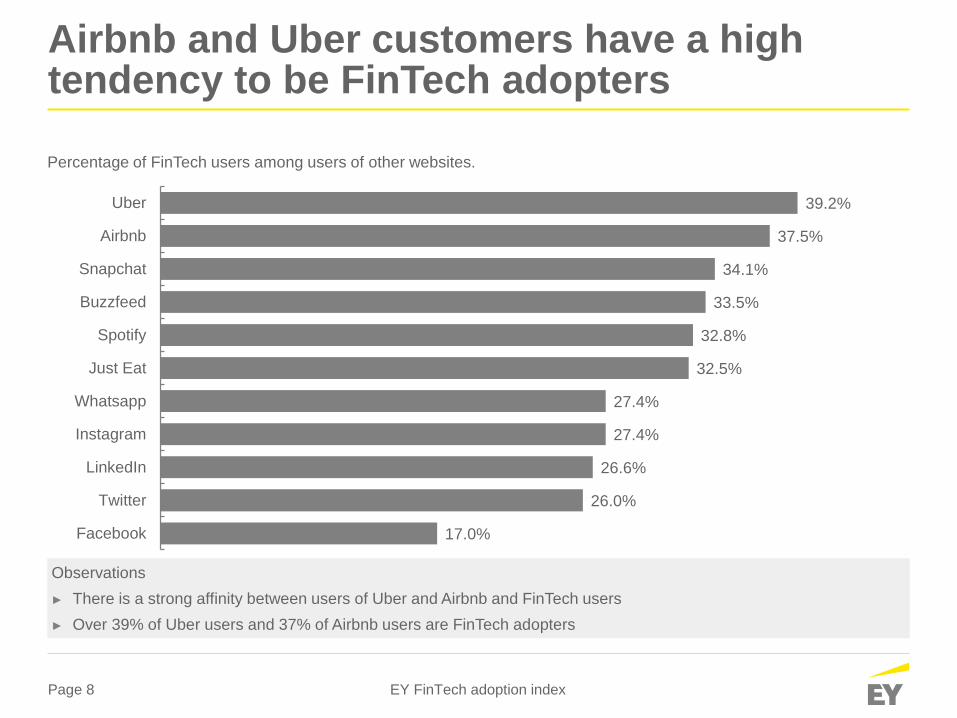

Airbnb and Uber customers have a high tendency to be FinTech adopters

17.0%

26.0%

26.6%

27.4%

27.4%

32.5%

32.8%

33.5%

34.1%

37.5%

39.2%

Just Eat

Spotify

Buzzfeed

Snapchat

Airbnb

Uber

Percentage of FinTech users among users of other websites.

Observations

► There is a strong affinity between users of Uber and Airbnb and FinTech users

► Over 39% of Uber users and 37% of Airbnb users are FinTech adopters

Page 9 EY FinTech adoption index

Imperative #1: Invest in the new customer segments that will drive future value

Young

1 in 4 respondents ages 25

to 34 has is a FinTech

adopters

High income

44% of respondents with

incomes above US

$150,000 are

FinTech adopters

$

Urban

City dwellers are

significantly above average

in their use of FinTech

products

Implications

► New battlegrounds are emerging for share of wallet. Young, high income, highly digitally active, urban

► FinTechs are gaining traction with these segments but will face increasing competition

► Incumbent financial institutions need to protect and serve clients in these segments:

► Review segment strategy and service model

► Revisit multi-channel strategy to enhance services and weaknesses of current online experience

Highly digitally active

Over 1 in 3 Airbnb and

Uber users are FinTech

adopters

$

Page 10 EY FinTech adoption index

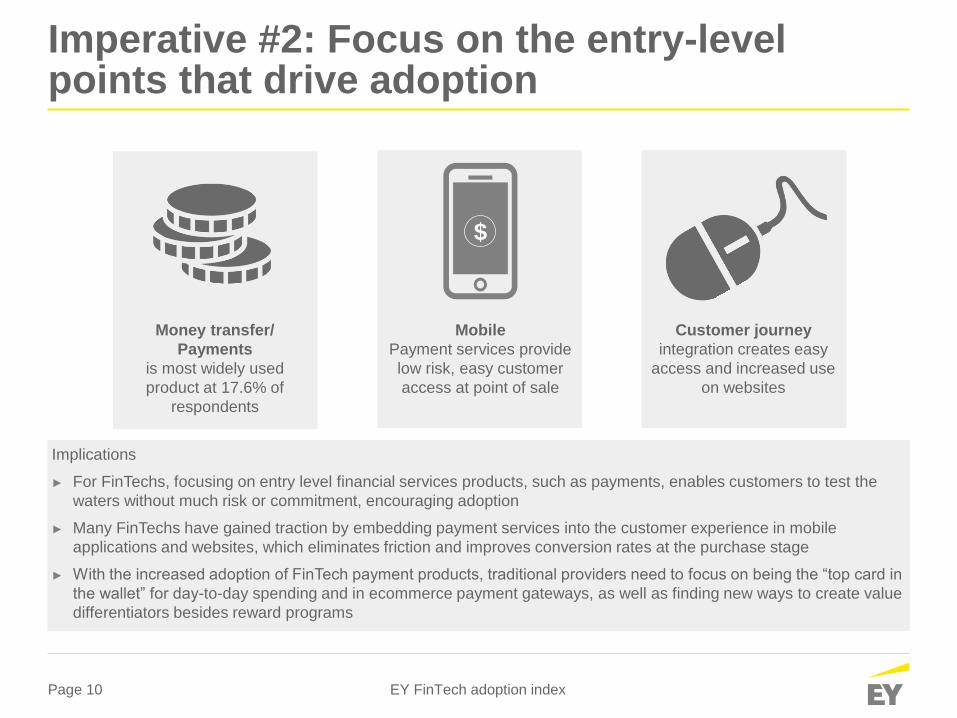

Imperative #2: Focus on the entry-level points that drive adoption

Implications

► For FinTechs, focusing on entry level financial services products, such as payments, enables customers to test the

waters without much risk or commitment, encouraging adoption

► Many FinTechs have gained traction by embedding payment services into the customer experience in mobile

applications and websites, which eliminates friction and improves conversion rates at the purchase stage

► With the increased adoption of FinTech payment products, traditional providers need to focus on being the “top card in

the wallet” for day-to-day spending and in ecommerce payment gateways, as well as finding new ways to create value

differentiators besides reward programs

Mobile

Payment services provide

low risk, easy customer

access at point of sale

Money transfer/

Payments

is most widely used

product at 17.6% of

respondents

Customer journey

integration creates easy

access and increased use

on websites

$

Page 11 EY FinTech adoption index

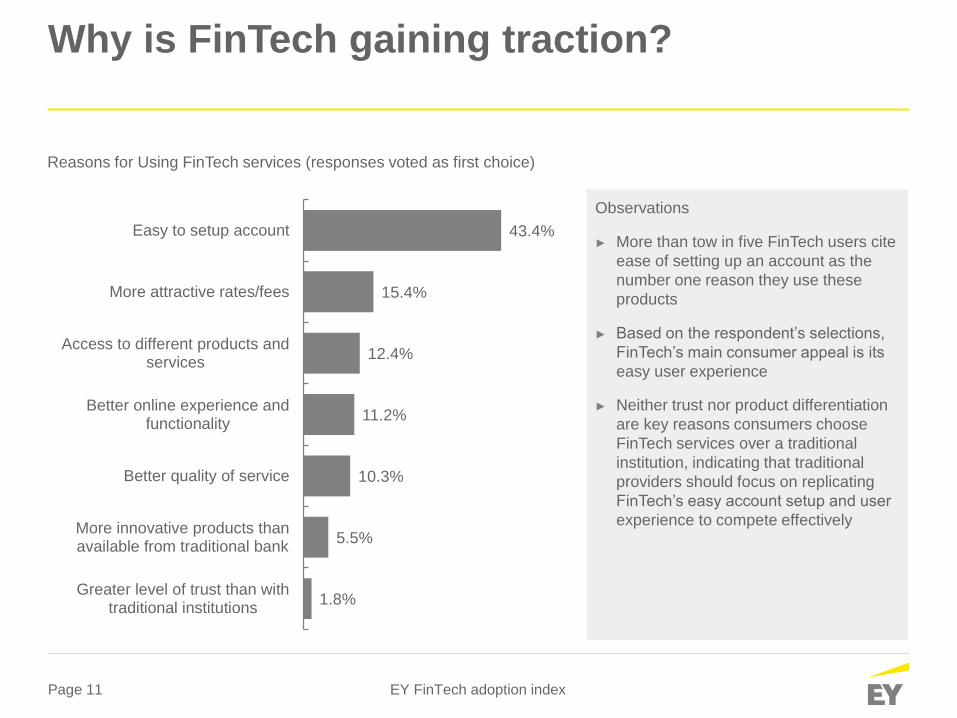

Why is FinTech gaining traction?

Observations

► More than tow in five FinTech users cite

ease of setting up an account as the

number one reason they use these

products

► Based on the respondent’s selections,

FinTech’s main consumer appeal is its

easy user experience

► Neither trust nor product differentiation

are key reasons consumers choose

FinTech services over a traditional

institution, indicating that traditional

providers should focus on replicating

FinTech’s easy account setup and user

experience to compete effectively

1.8%

5.5%

10.3%

11.2%

12.4%

15.4%

43.4%

Greater level of trust than withtraditional institutions

More innovative products thanavailable from traditional bank

Better quality of service

Better online experience andfunctionality

Access to different products andservices

More attractive rates/fees

Easy to setup account

Reasons for Using FinTech services (responses voted as first choice)

Page 12 EY FinTech adoption index

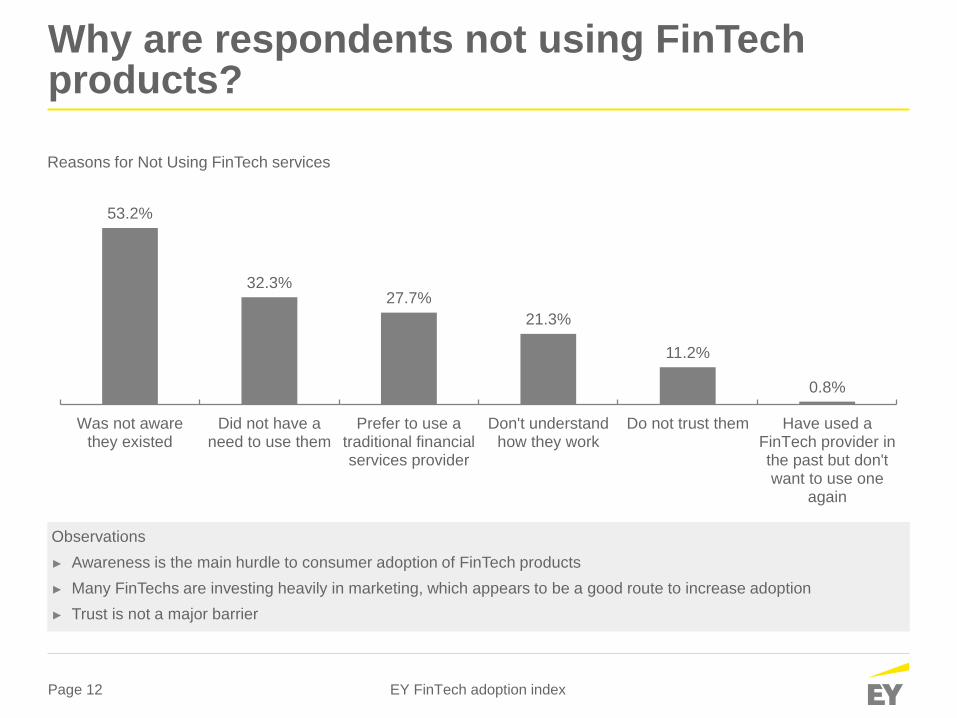

Why are respondents not using FinTech products?

53.2%

32.3%27.7%

21.3%

11.2%

0.8%

Was not awarethey existed

Did not have aneed to use them

Prefer to use atraditional financialservices provider

Don't understandhow they work

Do not trust them Have used aFinTech provider inthe past but don'twant to use one

again

Observations

► Awareness is the main hurdle to consumer adoption of FinTech products

► Many FinTechs are investing heavily in marketing, which appears to be a good route to increase adoption

► Trust is not a major barrier

Reasons for Not Using FinTech services

Page 13 EY FinTech adoption index

Imperative #3: Master the design principles that support service excellence

Implications for FinTechs

► Many FinTech firms have adopted the following design principles to develop their services.

► This approach is supported by an iterative approach to design. FinTechs are able to measure performance and iterate

their

► FinTechs need to formalised and embedded these design principles into their processes in order to obtain maximum

value for this IP

Construction and delivery of the proposition entirely around the consumer,

ideally embedded in non-financial services use case

Simple and entirely intuitive customer visuals and journey with easy onboarding

Simple product constructs (customizable, but with limited variability), and no

penalties or commitments

Page 14 EY FinTech adoption index

Imperative #3: Master the design principles that support service excellence

Incubate

Apply design tools to research and

test services:

► Customer experience laboratories

► Rapid-prototyping

Work with FinTech providers to

leverage their ideas and processes.

Incubate FinTech operations within

the institution.

Re-think design Partner

Implications for FinTechs

► Traditional players are often constrained by a culture of product silos, legacy product suites and pricing structures, as

well as legacy core IT systems

► These factors result in cumbersome user interfaces underpinned by complex and manual processes

► Traditional providers cannot used iterative design in the same way as FinTechs but need to adopt, in their own way,

the design elements that make FinTech services so engaging and easy to use

Page 15 EY FinTech adoption index

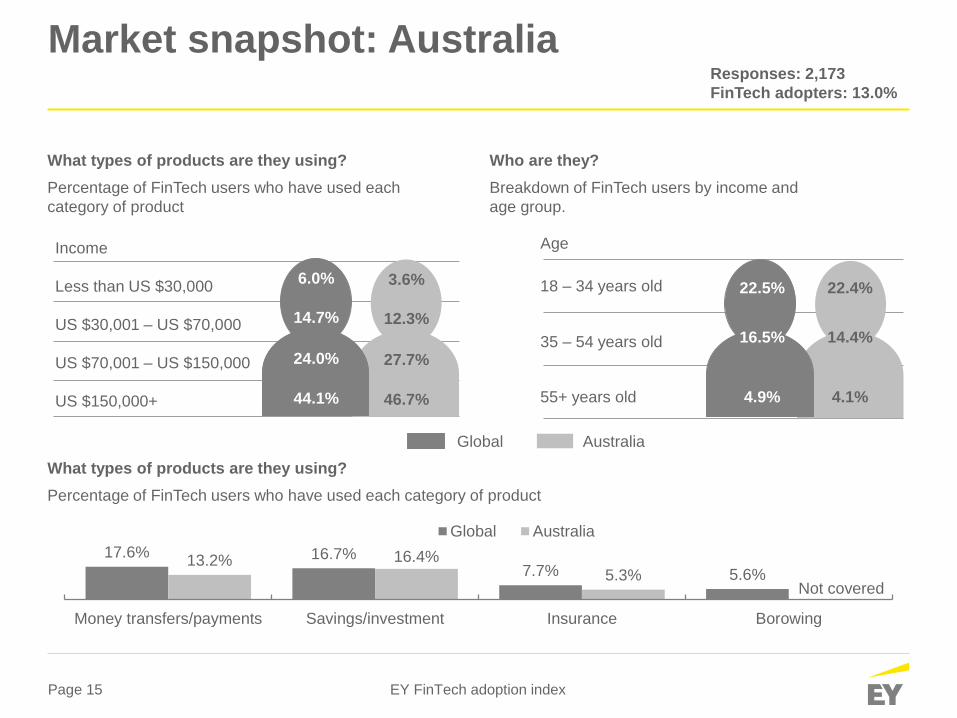

Market snapshot: Australia

Who are they?

Breakdown of FinTech users by income and

age group.

What types of products are they using?

Percentage of FinTech users who have used each

category of product

What types of products are they using?

Percentage of FinTech users who have used each category of product

Global Australia

17.6% 16.7%7.7% 5.6%

13.2% 16.4%5.3%

Money transfers/payments Savings/investment Insurance Borowing

Global Australia

Less than US $30,000

US $30,001 – US $70,000

US $70,001 – US $150,000

US $150,000+

Income

22.4%

14.4%

4.1%

18 – 34 years old

35 – 54 years old

55+ years old

Age

22.5%

16.5%

4.9%

Responses: 2,173

FinTech adopters: 13.0%

Not covered

3.6%

12.3%

27.7%

46.7%

6.0%

14.7%

24.0%

44.1%

Page 16 EY FinTech adoption index

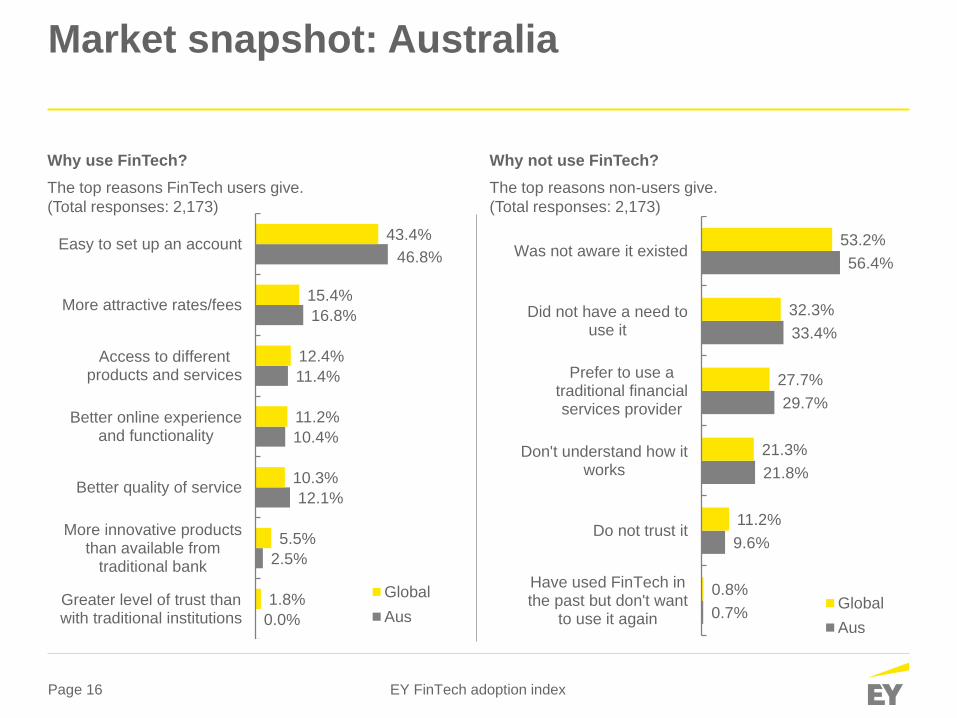

Market snapshot: Australia

Why not use FinTech?

The top reasons non-users give.

(Total responses: 2,173)

0.0%

2.5%

12.1%

10.4%

11.4%

16.8%

46.8%

1.8%

5.5%

10.3%

11.2%

12.4%

15.4%

43.4%

Greater level of trust thanwith traditional institutions

More innovative productsthan available from

traditional bank

Better quality of service

Better online experienceand functionality

Access to differentproducts and services

More attractive rates/fees

Easy to set up an account

Global

Aus

Why use FinTech?

The top reasons FinTech users give.

(Total responses: 2,173)

0.7%

9.6%

21.8%

29.7%

33.4%

56.4%

0.8%

11.2%

21.3%

27.7%

32.3%

53.2%

Have used FinTech inthe past but don't want

to use it again

Do not trust it

Don't understand how itworks

Prefer to use atraditional financialservices provider

Did not have a need touse it

Was not aware it existed

Global

Aus