finnvera plc: an international evaluation -...

TRANSCRIPT

Finnvera Plc:An International Evaluation

Ministry of Trade and IndustryPublications

1/2004Industries Department

Series title and number of the publication Aleksanterinkatu 4

P.O. Box 32 Tel. +358 9 16001 Publications FIN-00170 Helsinki FINLAND

FIN-00023 GOVERNMENT Helsinki FINLAND

Telefax +358 9 1606 3666 1/2004

Date February 2004

Commissioned by Ministry of Trade and Industry

Authors D.Sc., Jarna Heinonen (Director, Small Business Institute, Turku School of Economics and Business Administration) Diana Smallridge (President, International Financial Consulting Ltd.) Date of appointment

Title Finnvera Plc: An International Evaluation

Abstract Finnvera plc started its operations in 1999 following the merger of Kera Corporation and the Finnish Guarantee Board. The motives for this merger were the need to reorganise the administration of publicly supported special financing, to improve the efficiency and effectiveness of the State’s special financing and to streamline the State’s corporate governance. The evaluation of Finnvera plc aims at examining the cornerstones on which the future activities of the company will be based, taking into account the development of the market, the impacts of the European Union and other international legal framework and the availability of public funding. The evaluation covers Finnvera plc’s Export Credit Guarantee Activities, Domestic Financing and Overall Organisation. The evaluation report reviews each of the areas separately. Summary conclusions (answers to the evaluation questions) and recommendations are given for each area. According to the evaluators, export companies and banks are mostly satisfied with the activity of Finnvera plc’s Major Customers Unit, although there is some room for developing the company’s risk-taking and pricing policies. In the case of domestic financing, the evaluators recommend a stronger emphasis on guarantees and risk-sharing with banks. They further propose that the State’s credit loss compensations should be highlighted instead of interest subsidies. In addition, the evaluation contains proposals for restructuring the company’s domestic financing activities. In reviewing the operations of Finnvera plc five years after the merger, it can be concluded that the objectives of the merger have been met relatively well. However, the merger has not resulted in as much efficiency gains or stream-lining of the organisation as had been expected. In the evaluators’ view, this is hardly surprising, as domestic fi-nancing and export financing activities differ by their very nature in terms of their focus of business, customers and the risks taken. As far as the company structure is concerned, the evaluators recommend adoption of a holding company structure. Furthermore, the evaluators regard Finnvera plc’s tax liability and inability to set aside provi-sions as unnecessary limitations. MTI contacts: Industries Department/Risto Paaermaa tel. +358 (0)9 1606 3575, Sakari Arkio, tel. +358 (0)9 1606 3567

Key words Finnvera plc, evaluation, export credit guarantees, SME financing

ISSN 1236-1623

ISBN 951-739-753-4

Pages 263

Language English/Finnish partly

Price € 36

Published by Ministry of Trade and Industry

Sold by Edita Publishing Ltd

Foreword

Finnvera plc, a state-owned specialised financing company, started its operationsfrom the beginning of 1999. The company was founded by merging the activities ofKera Corporation (loans and guarantees for domestic business activities) and theFinnish Guarantee Board (export credit guarantees and special guarantees). Themain objective of the merger was to improve the availability of financial instru-ments for Finnish companies through Kera’s regional offices and to obtain econo-mies of scale through the merger.

According to the policy of the Ministry of Trade and Industry, governmentalorganisations and State aid schemes are evaluated on a regular basis by independentevaluators. Finnvera plc has now operated approximately five years and it wastherefore reasonable to examine and evaluate its operations and organisationalstructure.

The overall aim of the evaluation was to find out the cornerstones on which thefuture activities of the company will be based, taking into account the developmentof the market, the impacts of the European Union and other international legalframework and the need for availability of public funding.

The Ministry of Trade and Industry wishes to thank the evaluators, Ms DianaSmallridge, President of International Financial Consulting, Canada, and Ms JarnaHeinonen, Director of the Small Business Institute of the Turku School of Econo-mics and Business Administration, for their skilful and future orientated work.Special thanks are also extended to the steering group of the evaluation process aswell as to all others that have contributed to this project.

The findings of the evaluation will be utilised in the further development of thepublic export and domestic financing system in Finland.

Helsinki, 13 February 2004

Erkki VirtanenPermanent SecretaryMinistry of Trade and Industry

Table of Contents

Foreword . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Table of Contents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

1.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

1.1.1 Background . . . . . . . . . . . . . . . . . . . . . . . . 221.1.2 Structure of the Report . . . . . . . . . . . . . . . . . . 24

1.2 Methodology and Analytical Framework. . . . . . . . . . . . . 25

1.3 Finnvera Plc . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

1.3.1 Background . . . . . . . . . . . . . . . . . . . . . . . . 271.3.2 Business Activities . . . . . . . . . . . . . . . . . . . . 271.3.3 Mandate . . . . . . . . . . . . . . . . . . . . . . . . . . 291.3.4 Legislative Framework . . . . . . . . . . . . . . . . . . 291.3.5 Objectives . . . . . . . . . . . . . . . . . . . . . . . . . 301.3.6 Market Failure . . . . . . . . . . . . . . . . . . . . . . . 31

2 Evaluation of Finnvera Plc's Export Credit GuaranteeActivities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

2.1 Introduction and Background . . . . . . . . . . . . . . . . . . . 32

2.1.1 Government Involvement in Export Credit . . . . . . . . 322.1.2 ECA Market Segments . . . . . . . . . . . . . . . . . . 33

2.1.2.1 Export Credit Insurance . . . . . . . . . . . . . . 342.1.2.2 Investment Insurance . . . . . . . . . . . . . . . 352.1.2.3 Other Facilities . . . . . . . . . . . . . . . . . . 36

2.1.3 Accounting and Financial Aspects . . . . . . . . . . . . 372.1.3.1 General . . . . . . . . . . . . . . . . . . . . . . 392.1.3.2 Open and Closed Years . . . . . . . . . . . . . . 392.1.3.3 Premium . . . . . . . . . . . . . . . . . . . . . . 392.1.3.4 Provisions . . . . . . . . . . . . . . . . . . . . . 392.1.3.5 Reserves . . . . . . . . . . . . . . . . . . . . . . 40

2.1.4 Key Developments in the Export Credit Market . . . . . 402.1.4.1 Globalisation . . . . . . . . . . . . . . . . . . . 402.1.4.2 Competition and Consolidation . . . . . . . . . . 412.1.4.3 Development of Private Reinsurance Capacity . . 412.1.4.4 Substantial Claims and Write-Offs . . . . . . . . 422.1.4.5 Elimination of Export Credit Subsidies . . . . . . 422.1.4.6 Privatisation . . . . . . . . . . . . . . . . . . . . 432.1.4.7 Growth in Commercial Risks . . . . . . . . . . . 432.1.4.8 Overlap between Political and Commercial Risks 44

2.1.5 Current Critical Issues Facing ECAs . . . . . . . . . . . 452.1.5.1 Operational Challenges . . . . . . . . . . . . . . 452.1.5.2 Policy Challenges . . . . . . . . . . . . . . . . . 482.1.5.3 International Legal and Regulatory Challenges. . 49

2.2 Review of the Finnish Export Credit System . . . . . . . . . . . 51

2.2.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . 512.2.2 Sources of Export Credit Support . . . . . . . . . . . . . 51

2.2.2.1 Private Sector Sources. . . . . . . . . . . . . . . 522.2.2.2 Official Sources . . . . . . . . . . . . . . . . . . 54

2.2.3 Demand for Export Credit Support . . . . . . . . . . . . 562.2.4 Market Gaps . . . . . . . . . . . . . . . . . . . . . . . . 57

2.3 Review of Finnvera Plc’s Export Credit and Special GuaranteesActivities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

2.3.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . 592.3.2 Legislation . . . . . . . . . . . . . . . . . . . . . . . . . 602.3.3 Underwriting. . . . . . . . . . . . . . . . . . . . . . . . 602.3.4 Guarantee Products . . . . . . . . . . . . . . . . . . . . 612.3.5 Special Guarantee Products . . . . . . . . . . . . . . . . 622.3.6 Portfolio Concentrations and Risk Management . . . . . 622.3.7 State Guarantee Fund . . . . . . . . . . . . . . . . . . . 642.3.8 Customers . . . . . . . . . . . . . . . . . . . . . . . . . 64

2.3.8.1 Bank Survey . . . . . . . . . . . . . . . . . . . . 642.3.8.2 Exporter Survey . . . . . . . . . . . . . . . . . . 66

2.3.9 Regional Offices . . . . . . . . . . . . . . . . . . . . . . 68

2.4 Export Credit System Health Assessment . . . . . . . . . . . . 69

2.4.1 Finland’s Export Credit System Health Assessment . . . 69Exporter Focus/Service . . . . . . . . . . . . . . 70Government Control/Oversight . . . . . . . . . . 71Institutional Strength . . . . . . . . . . . . . . . 72Private Sector Involvement . . . . . . . . . . . . 73

2.5 Conclusions and Recommendations . . . . . . . . . . . . . . . 75

2.5.1 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . 752.5.2 Recommendations . . . . . . . . . . . . . . . . . . . . . 77

3 An Evaluation of Finnvera Plc's Domestic Financing . . . 80

3.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

3.2 Financing of SMEs in Finland . . . . . . . . . . . . . . . . . . 81

3.2.1 Financing Theory . . . . . . . . . . . . . . . . . . . . . 813.2.2 Financial Sources of an SME . . . . . . . . . . . . . . . 843.2.3 An SME's Financing Functions and Financial Challenges 883.2.4 Changes on the Financial Market . . . . . . . . . . . . . 91

3.2.4.1 General Changes . . . . . . . . . . . . . . . . . 913.2.4.2 Basel II Accord . . . . . . . . . . . . . . . . . . 93

3.3 Domestic Financing of Finnvera Plc . . . . . . . . . . . . . . . 94

3.3.1 Government Control/Oversight . . . . . . . . . . . . . . 943.3.1.1 Objectives . . . . . . . . . . . . . . . . . . . . . 943.3.1.2 Government Involvement . . . . . . . . . . . . . 953.3.1.3 Regular Review of Activities . . . . . . . . . . . 96

3.3.2 Domestic Financial Service and Products . . . . . . . . . 973.3.2.1 Product Range and Customers . . . . . . . . . . 973.3.2.2 Market Failure . . . . . . . . . . . . . . . . . . . 993.3.2.3 Regional Availability . . . . . . . . . . . . . . . 1033.3.2.4 Pricing . . . . . . . . . . . . . . . . . . . . . . . 1053.3.2.5 Proactivity of Operations . . . . . . . . . . . . . 1063.3.2.6 Venture Capital Investment – Veraventure Ltd . . 107

3.3.3 Institutional Setting . . . . . . . . . . . . . . . . . . . . 1093.3.3.1 Expertise and Competence . . . . . . . . . . . . 1093.3.3.2 Active Portfolio Management . . . . . . . . . . . 1103.3.3.3 Internal Processes . . . . . . . . . . . . . . . . . 1113.3.3.4 Human Resources and Decision-Making . . . . . 113

3.3.4 Cooperation with Other Organisations . . . . . . . . . . 1153.3.4.1 Cooperation and/or Competition with Banks . . . 1153.3.4.2 Catalysation of the Private Sector . . . . . . . . . 1163.3.4.3 Cooperation with Public Organisations . . . . . . 118

3.4 Conclusions and Recommendations . . . . . . . . . . . . . . . 119

3.4.1 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . 1193.4.2 Recommendations . . . . . . . . . . . . . . . . . . . . . 125

4 An Evaluation of Finnvera Plc's Overall Organisation . . 129

4.1 Evaluation of Finnvera Plc as a whole . . . . . . . . . . . . . . . 129

4.1.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . 1294.1.2 Efficiency . . . . . . . . . . . . . . . . . . . . . . . . . 129

4.1.2.1 Information Systems . . . . . . . . . . . . . . . 1304.1.2.2 Financial Systems . . . . . . . . . . . . . . . . . 1304.1.2.3 Claims and Recoveries . . . . . . . . . . . . . . 1304.1.2.4 Treasury . . . . . . . . . . . . . . . . . . . . . . 1314.1.2.5 Management Practices. . . . . . . . . . . . . . . 1314.1.2.6 Human Resources . . . . . . . . . . . . . . . . . 1324.1.2.7 Application of the Balanced Scorecard . . . . . . 1324.1.2.8 Marketing . . . . . . . . . . . . . . . . . . . . . 1334.1.2.9 Productivity Gains. . . . . . . . . . . . . . . . . 1344.1.2.10 Market Presence . . . . . . . . . . . . . . . . . . 1344.1.2.11 Culture . . . . . . . . . . . . . . . . . . . . . . . 134

4.1.3 Transparency . . . . . . . . . . . . . . . . . . . . . . . 1364.1.3.1 Ownership Policy . . . . . . . . . . . . . . . . . 1374.1.3.2 Industrial Policy . . . . . . . . . . . . . . . . . . 137

4.1.4 Regional Availability . . . . . . . . . . . . . . . . . . . 1404.1.5 Streamlining of the State’s Corporate Governance . . . . 1404.1.6 Internal Structure . . . . . . . . . . . . . . . . . . . . . 1424.1.7 Fiscal Status . . . . . . . . . . . . . . . . . . . . . . . . 1434.1.8 Structural Options . . . . . . . . . . . . . . . . . . . . . 146

4.1.8.1 Description of Options . . . . . . . . . . . . . . 1464.1.8.2 Options Analysis . . . . . . . . . . . . . . . . . 148

4.2 Conclusions and Recommendations . . . . . . . . . . . . . . . 149

4.2.1 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . 1494.2.2 Recommendations . . . . . . . . . . . . . . . . . . . . . 150

Luku 3 alkuperäisenä suomenkielisenä tekstinä sekäluku 4 ja yhteenveto englannista suomen kielellekäännettyinä . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 153

3 Finnvera Oyj:n kotimaisen rahoituksen arviointi . . . . . 155

3.1 Johdanto . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 155

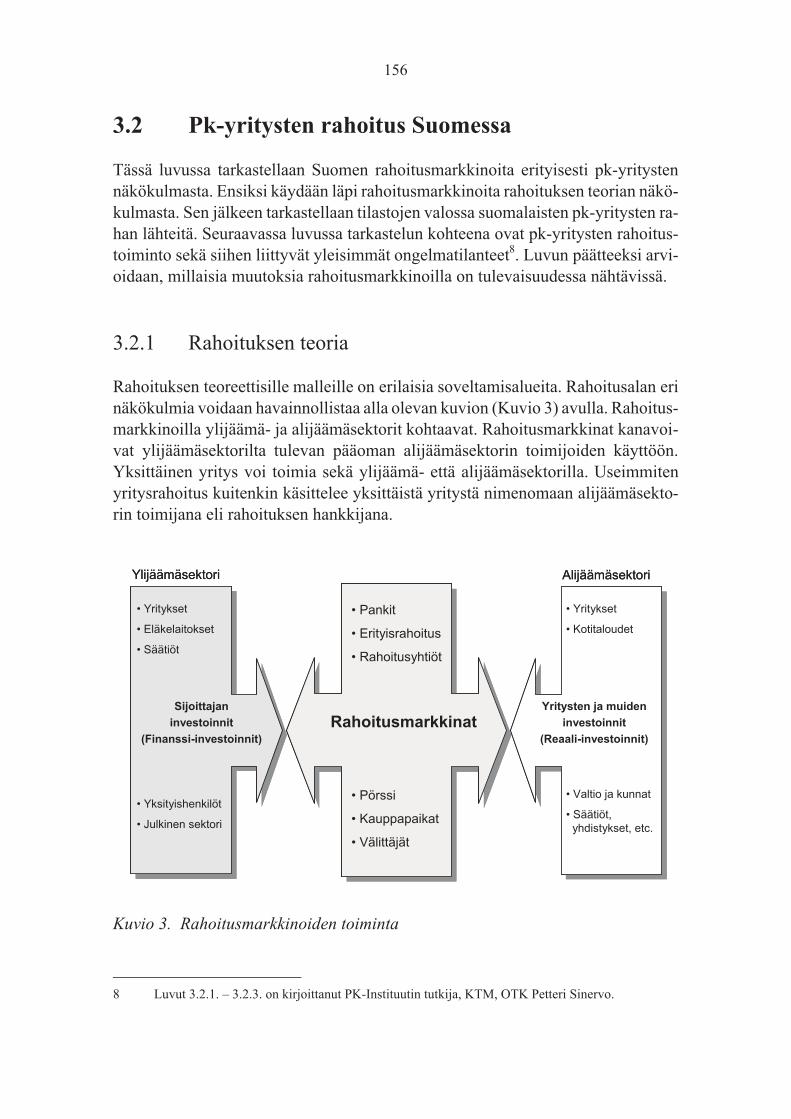

3.2 Pk-yritysten rahoitus Suomessa . . . . . . . . . . . . . . . . . . 156

3.2.1 Rahoituksen teoria . . . . . . . . . . . . . . . . . . . . . 1563.2.2 Pk-yrityksen rahan lähteet . . . . . . . . . . . . . . . . . 159

3.2.3 Pk-yrityksen rahoitustoiminnot ja tyypillisetongelmatilanteet . . . . . . . . . . . . . . . . . . . . . . . . . . 1623.2.4 Muutokset rahoitusmarkkinoilla. . . . . . . . . . . . . . 165

3.2.4.1 Yleiset muutokset . . . . . . . . . . . . . . . . . 1653.2.4.2 Basel II -sääntely . . . . . . . . . . . . . . . . . 167

3.3 Finnvera Oyj:n kotimaan rahoitus . . . . . . . . . . . . . . . . 168

3.3.1 Omistajan kontrolli . . . . . . . . . . . . . . . . . . . . 1683.3.1.1 Asetetut tavoitteet . . . . . . . . . . . . . . . . . 1683.3.1.2 Omistajan osallistuminen toimintaan . . . . . . . 1693.3.1.3 Toiminnan arviointi . . . . . . . . . . . . . . . . 170

3.3.2 Kotimaan rahoituspalvelu ja -tuotteet . . . . . . . . . . . 1713.3.2.1 Tuotevalikoima ja asiakkaat. . . . . . . . . . . . 1713.3.2.2 Markkinapuute . . . . . . . . . . . . . . . . . . 1733.3.2.3 Alueellinen saatavuus . . . . . . . . . . . . . . . 1773.3.2.4 Hinnoittelu. . . . . . . . . . . . . . . . . . . . . 1793.3.2.5 Toiminnan proaktiivisuus . . . . . . . . . . . . . 1803.3.2.6 Pääomasijoitustoiminta – Veraventure Oy . . . . 181

3.3.3 Finnvera organisaationa . . . . . . . . . . . . . . . . . . 1823.3.3.1 Ammattitaito ja osaaminen . . . . . . . . . . . . 1823.3.3.2 Vastuu-/lainakannan aktiivinen hoitaminen. . . . 1843.3.3.3 Sisäiset prosessit. . . . . . . . . . . . . . . . . . 1843.3.3.4 Henkilöstöresurssit ja päätöksenteko . . . . . . . 186

3.3.4 Yhteistyö muiden organisaatioiden kanssa . . . . . . . . 1883.3.4.1 Yhteistyö ja/tai kilpailu pankkien kanssa . . . . . 1883.3.4.2 Yksityisen sektorin katalysointi . . . . . . . . . . 1893.3.4.3 Yhteistyö julkisten organisaatioiden kanssa . . . 191

3.4 Johtopäätökset ja toimenpidesuositukset . . . . . . . . . . . . . 192

3.4.1 Johtopäätökset . . . . . . . . . . . . . . . . . . . . . . . 1923.4.2 Toimenpidesuositukset . . . . . . . . . . . . . . . . . . 197

4 Finnvera Oyj:n organisaatiokokonaisuuden arviointi. . . 201

4.1 Finnvera Oyj:n organisaatiokokonaisuuden arviointi . . . . . . . 201

4.1.1 Johdanto . . . . . . . . . . . . . . . . . . . . . . . . . . 2014.1.2 Tehokkuus . . . . . . . . . . . . . . . . . . . . . . . . . 202

4.1.2.1 Tietojärjestelmät. . . . . . . . . . . . . . . . . . 2024.1.2.2 Laskentajärjestelmät. . . . . . . . . . . . . . . . 2024.1.2.3 Korvaukset ja takaisinperintä . . . . . . . . . . . 2024.1.2.4 Varainhallinta . . . . . . . . . . . . . . . . . . . 2034.1.2.5 Johtamiskäytännöt. . . . . . . . . . . . . . . . . 203

4.1.2.6 Henkilöstöhallinto . . . . . . . . . . . . . . . . . 2044.1.2.7 Tasapainotetun tuloskortin soveltaminen . . . . . 2054.1.2.8 Markkinointi. . . . . . . . . . . . . . . . . . . . 2064.1.2.9 Tuottavuuden parantuminen. . . . . . . . . . . . 2064.1.2.10 Toiminta markkinoilla. . . . . . . . . . . . . . . 2064.1.2.11 Yrityskulttuuri . . . . . . . . . . . . . . . . . . . 207

4.1.3 Läpinäkyvyys . . . . . . . . . . . . . . . . . . . . . . . 2094.1.3.1 Omistajapoliittiset tavoitteet . . . . . . . . . . . 2104.1.3.2 Elinkeinopoliittiset tavoitteet . . . . . . . . . . . 210

4.1.4 Alueellinen saatavuus . . . . . . . . . . . . . . . . . . . 2134.1.5 Valtion hallinnointi- ja ohjausjärjestelmienyksinkertaistaminen . . . . . . . . . . . . . . . . . . . . . . . . 2144.1.6 Sisäinen rakenne. . . . . . . . . . . . . . . . . . . . . . 2154.1.7 Verotuksellinen asema. . . . . . . . . . . . . . . . . . . 2164.1.8 Organisaatiorakenteen vaihtoehdot . . . . . . . . . . . . 220

4.1.8.1 Vaihtoehtojen kuvaus . . . . . . . . . . . . . . . 2204.1.8.2 Vaihtoehtojen analyysi . . . . . . . . . . . . . . 221

4.2 Johtopäätökset ja suositukset . . . . . . . . . . . . . . . . . . . 222

4.2.1 Johtopäätökset . . . . . . . . . . . . . . . . . . . . . . . 2224.2.2 Suositukset. . . . . . . . . . . . . . . . . . . . . . . . . 224

Yhteenveto . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 227

References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 235

Appendix 1: List of Interviews Conducted . . . . . . . . . . . . . . . . 239

Appendix 2: Online Surveys . . . . . . . . . . . . . . . . . . . . . . . 246

2A: Bank Survey . . . . . . . . . . . . . . . . . . . . . . . . . . . . 246

2B: Exporter Survey . . . . . . . . . . . . . . . . . . . . . . . . . . 252

2C: Employee Survey. . . . . . . . . . . . . . . . . . . . . . . . . . 260

Executive Summary

Finnvera began operating in 1999 following the merger of Kera Corporation andthe Finnish Guarantee Board. Motivating this merger was a desire to renew theadministration of publicly supported special financing, improve the effectivenessof the State’s special financing and simplify the State’s ownership steering.

The evaluation of Finnvera aims at examining the cornerstones on which the futureactivities of the company will be based, taking into account the development of themarket, the impacts of the European Union and other international legal frameworkand the availability of public funding. The evaluation covers Finnvera´s ExportCredit Guarantee Activities (evaluated by an international consultant, Diana Small-ridge), Domestic Financing (evaluated by a domestic evaluator, Jarna Heinonen )and Overall Organisation (joint responsibility).

Finnvera´s financing activities were reviewed by using an analytical framework –The Export Credit System Health Scorecard© developed by International FinancialConsulting Ltd. – which considers the strength of the government’s institutionalinvolvement in financing activities through Finnvera and the health of the overalldomestic and export financing system as a whole, taking into account all the officialplayers and private sector. Background material was reviewed and interviews wereconducted with a number of people. On-line surveys were also undertaken withbanks, Finnish exporters and Finnvera employees.

The range of Finnvera’s activities is reflected in the following three elements ofFinnvera’s mandate to:

1. Provide risk financing for, and development of SMEs;

2. Promote internationalization and exports of enterprises; and

3. Promote the government’s regional policy measures.

Finnvera meets these objectives largely through its two general business lines:financing of enterprise activities in Finland; and granting of export credit guaran-tees through foreign risk-taking. There are numerous Acts which govern Finnvera´sactivities on the export credit guarantees and the domestic financing.

13

An important public policy objective for Finnvera is to address market failure. It iscrucial that Finnvera is not impeding the private sector or operating in a part of themarket in which the private sector would otherwise be willing to operate. The con-cept of market gap is not straightforward. There are perhaps three characteristics ofgaps in the supply of a given product or service: 1) supply does not exist at all, or 2)supply does exist but is exceeded by demand; or 3) supply may exist but at a pricethat firms are not willing to pay. Finally, market gaps are not static, but change overtime and sometimes very rapidly.

Based on the evaluation on Finnvera´s export credit and special guarantee

activities the following recommendations are given:

1. Establishment of a National Interest Account

To be able to maintain financial integrity of Finnvera and meet thegovernment’s needs, the establishment of a National Interest Account(NIA) is recommended.

The NIA would assume all guarantee business approved by the govern-ment (under export credit or special guarantees) that is outside Finn-vera’s normal underwriting criteria (either due to size or to nature of therisk) and would be fully funded by the government as a separate accountfrom Finnvera.

Although Article 6 of the Act of the State’s Export Credit Guarantees(422/2001) refers to special risk-taking, there is no special account thatcurrently exists. The State Guarantee Fund could play the role of anNIA. The governance structure of the SGF would need to be reviewedand clarified in order that the proper accountabilities are in place.

In addition, where Finland is providing concessional financing (tied aid)and Finnvera is asked to credit guarantee the non-grant portion, thisshould be done on the NIA.

2. Role of Regional Offices

Customers in the Regional Offices, although not potential Export Creditguarantees clients, are in fact exporters which face very typicalchallenges – access to working capital and credit risk associated withforeign buyers.

14

The Regional Offices should require that all its domestic customers havetheir foreign buyers credit insured and, in fact, insist that its domesticcustomers provide Finnvera with a credit insurance policy as collateralagainst which to lend.

3. Private Credit Insurance Market

The requirement for credit insurance for Finnvera’s domestic customersmeans that the availability of credit insurance in the private market mustbe fully examined. It is therefore recommended that the government andFinnvera have detailed discussions with the senior management of theexisting private credit insurers to explore their willingness to supportSMEs in Finland. The purpose of these discussions is to get from thecredit insurers what they see as the obstacles to doing more business inFinland, if any, and what is the basis for these obstacles. The validity oftheir points can then be analysed and consideration given to anythingwhich might be reasonably be done to try to solve the perceived diffi-culties and problems.

4. Underwriting

Because Finnvera’s pricing can be higher than other Export CreditAgencies, it is important that Finnvera consider other possible means forflexibility, such as turnaround times. This does not mean that Finnverashould lower its underwriting standards. It might be helpful for Finnverato examine its approach to risk sharing requirements for markets, suchas Russia.

5. Efficiency of Resources

Given that FIDE is now a subsidiary of Finnvera, better allocation ofresources between the two organisations should be sought. For example,representation at international meetings on OECD and EU mattersshould be led by Finnvera and current resources from FIDE devoted tothese matters should be made available to Finnvera.

6. Simplification of Legislation

It is recommended that consideration be given to the consolidation ofthe acts governing Finnvera’s special guarantees into the Act on ExportCredit Guarantees.

15

Respectively there are number of recommendations resulting from the evaluationof Finnvera´s domestic financing activities:

1. Simplifying the product range

The basic Finnvera product range covers three products: loans,guarantees and export guarantees, which can all be provided on differentterms to different target groups. In practice the concepts of product andmarket segment in the Finnvera range of products are blurred which hascaused further extension of the product range. As such, there are toomany products to be manageable either by the clients or the personnel.

2. Stronger emphasis on guarantees and risk-sharing with banks

Lack of collateral for SMEs is shown to be a greater difficulty thaneither access to finance or the cost of funds, especially at current lowinterest rates. The regional interest subsidies have lost their relevance,due both to the market situation and the changed society. What isexpected of Finnvera is stronger risk-taking and risk-sharing with thebanks. By removing the regional interest subsidies and allocating thecorresponding amount of money to state credit loss compensationsrisk-taking can be increased and stronger regional policy implementedespecially in the more remote areas. Thus, the state support can inprinciple be targeted for the benefit of a larger number of enterprises. Ifrisk-sharing with the banks further increases, there is a need forFinnvera and the banks to jointly negotiate and identify the means forcase by case financing arrangements. The margin offered by the bankshould reflect the guarantee given and risk taken by Finnvera.

Nationally, there is need of special loans for business start-ups and smallenterprises, because the banks are not eager to finance these enterprisegroups. In addition, the risk-sharing involved in these cases is notreasonable and cost effective.

The role of Finnvera as a so-called broker of SME-financing in solvingthe financing problems of enterprises would alleviate the poor financingability typical to SMEs as well as their inferior status on the financingmarket. SME-brokerage could be a product liable to fee of Finnvera,which would correct the market deficit by catalysing the private sectorby its competence and complement the bank financing according toneed.

16

3. Reorganising domestic financing and dismantling of the matrix organi-sation

The matrix organisation (field unit and SME unit) has been a viablesolution at the merger stage, but the transition period is over and it hasnow served its purpose. Domestic financing needs one clear head ofmanagement, who enjoys the trust of the field staff in terms of thecustomer, financing and business competence areas. When reorganisingdomestic financing, the focus of attention, in addition to the pointsmentioned above, has to be turned to a) the need to intensify communi-cation between the regional offices and the head office and b) thechallenge of increasing the understanding of business dynamics andversatility on the client interface.

Actually all these points speak for a line organisation working under themanaging director of Finnvera, where responsibility and know-how istransferred down the line within the organisation. The manager of thisline organisation has to have responsibility for the field work. In practicethis would, within a certain time-span, mean increasing the decisionmaking powers on all the organisation levels according to competencedevelopment. This should not, however, mean that the regional or otherline of management could go as far up as to the company board ofdirectors for advice and consultation, if necessary.

4. Strengthening the competence of the regional office network

The Finnvera regional office network is a key strength of the company.In the offices, competence has to be continuously and systematicallydeveloped according to the changes in the market and society. Under-standing the regional and international enterprise networks and thebusiness logic of the growth companies is essential. Competencedevelopment cannot be a voluntary activity, but based on commontargeting and planning. Organisational changes in 2003 give a solidground for systematic competence development.

5. Effective resource allocation and use

As to resource allocation there is a marked imbalance not only betweenregional offices, but also between them and the head office. In relation tothe regional offices the head office seems to be somewhatover-resourced. Partly because of this, maybe, the head office has

17

developed different systems relevant as such, which in the opinion of theregional offices, however, are serving the purposes of the head officebetter than those of clients or the company core business. Therefore, it isrecommended that there be a better balance between Head Office andRegional Office staff taking into account the needs of customers and thevalue-added that Head Office provides.

6. Intensifying impact evaluation

Finnvera evaluates and measures several operations-related indicatorsregularly and with commendable accuracy. Compared to these theevaluation of the impact of activities has had a minor role. Especially theimpact of Finnvera on employment and regional policies needs to beexplicitly defined and stated both on the target and impact level. Somemeasures have already been taken recently within the MTI and Finnveraconcerning both of these areas.

7. Alleviating and simplifying Government steering

The Government steering is visible in Finnvera activities in multipleways and the steering impulses are not necessary in line with each other.The Ministry steers Finnvera, in many parts, like a civil servicedepartment thus causing in places needless bureaucracy in the companyactions. The direction and control of a state-owned industrial policyinstrument in a way, that would take into consideration the nature of thebusiness and the client face, is an extremely challenging task. TheMinistry does well to critically consider, how the tradition of steeringcould be from doing things right towards doing the right things. It is ofcrucial importance that Ministry systematically assesses the nature andwidth of the market failure.

Finally, the following recommendations are given based on the evaluation ofFinnvera´s overall organisation:

1. Structure

In terms of structure, the recommended approach is to create a parentcompany structure with all supporting and back office functions, havingtwo subsidiaries for export and domestic business.

18

2. Fiscal Status

a. Separation of Accounts

Finnvera should have two separate accounts for the domestic and exportcredit sides. The export credit side needs to be able show a break-even tomeet the WTO obligations.

In addition, it is recommended that a National Interest Account (NIA) beestablished for large ECG transactions outside the normal underwritingcriteria for which the government is directly responsible.

b. Provisions

Finnvera should be able to set aside from its premium income earned ina given year an amount to cover expected future losses (general provi-sions), as well an amount against unexpected losses. Specific provisionscould then be made once a claim is expected to be paid or a loss to be suf-fered.

The annual surplus/deficit could then be calculated after these provi-sions have been made.

c. Taxation

Taxation of Finnvera should not been seen as a source of income for thegovernment. Finnvera pays tax on its annual surplus to the state accord-ing to the normal corporate tax rates. The starting point has obviouslybeen, that Finnvera should not get a competitive advantage compared tothe banks through its tax exemption. The law on credit institutions willnot, however, be applied to Finnvera, so Finnvera is not allowed to makeany reserves for credit losses eligible in taxation. Thus Finnvera is actu-ally in a weaker position than the banks or private sector credit insurersin that respect.

To be internationally competitive with other ECAs, there should be notaxation of Finnvera’s surpluses. The only reason taxes might be consid-ered justified would be if Finnvera were competing against the privatemarket. This is not the case for Finnvera’s export credit guarantee busi-ness.

19

In domestic financing, taxation leads not only to unnecessary bureau-cracy, but also weakens the Finnvera capacity to take larger risks (orserve a larger clientele).

3. Responsibility of the Board

While the Board would be less in involved in day-to-day managementand approval of transactions, its focus should be on:

a. How strategy is set in Finnvera

b. How the objectives set by the MTI Working Group are integratedinto Finnvera’s Balanced Scorecard system

c. The relationship of the Balanced Scorecard to the bonus schemesfor individual units

In order to streamline the governance process, the Board of Directorsshould increase the size of ECG transactions which management canapprove, but leave open the possibility that management seeks theadvice of the Board for sensitive and difficult cases.

NIA deals would be taken to the Board but, for reasons of the nature ofthe risk or the size of the transaction, the Board would make a decisionwhether a case should be taken to the NIA and take a view on whether ornot it recommends the government support the case.

4. Strategic and Business Planning

It is recommended that a formal process for Strategic Planning andtarget setting be undertaken annually at the Board which includes:

a. A Strategic Committee of the Board be formed

b. The MTI Working Group interface with this Board committeeregularly

c. Management report quarterly to the Board on “PerformanceAgainst Objectives”

5. Supervisory Board

It is recommended that some consideration be given to the role and func-tion of the Supervisory Board as compared to the Board of Directors.

20

6. Marketing

The marketing functions can be combined, but retain in MajorCustomers and Export Credit Guarantees Unit the part of the marketingfunction that is more development oriented.

7. Claims and Recoveries

Given the specialisation in the claims and recoveries field, it is recom-mended that there be no loss of specialisation between domestic and in-ternational sides.

21

1 Introduction

1.1 Introduction

1.1.1 Background

In May 2003, the Finnish Ministry of Trade and Industry commissioned theEvaluation of Finnvera plc to be conducted by a domestic evaluator, Jarna Heino-nen from Turku School of Economics and Business Administration, and aninternational consultant, Diana Smallridge from International Financial ConsultingLtd. The Evaluation was conducted from June to December 2003.

The Terms of Reference for the Evaluation were set forth in the tender documents.The evaluation of Finnvera had the following aim:

“To examine the cornerstones on which the future activities of thecompany will be based, taking into account the development of themarket, the impacts of the European Union and other international legalframework and the availability of public funding.”

A series of questions were raised which highlight the key focus of the evaluation,and which will be considered by this report. The questions are as follows:

1. Review of Export Credit Guarantee Activities

a) Is Finnvera plc’s export guarantee activity competitive interna-tionally and aimed at addressing market failures?

b) What drivers for change can be seen in international exportguarantee activity and how should they be taken into account indevelopment of export guarantee activities?

c) Is Finnvera plc’s export guarantee activity in accordance with theobjectives of the activity and is the volume of the activity correctlysized?

d) Is Finnvera plc’s risk management process relating to its exportguarantee activity up to date and what kinds of needs for develop-

22

ing risk management can be foreseen and are the protective mea-sures taken by Finnvera plc sufficient?

e) Are the swiftness of handling financing matters, expertise inservice and client counselling sufficient from the standpoint of theexporter, buyer and the bank?

f) Is the Ministry of Trade and Industry’s industrial policy controlover Finnvera plc’s export guarantee activity appropriate and howshould the targets of industrial policy, including the self-suffi-ciency target, set by the Ministry be developed in terms of exportguarantee activity?

g) In regard to its size and internal structure, is the organization ofFinnvera plc’s export guarantee activity and the company’spersonnel appropriate considering the challenges set for it andthose that are now predictable?

h) Overall evaluation of Finnvera plc’s special guarantee activity(guarantee products based on specific laws and regulations)

2. Domestic Financing

a) Does Finnvera plc have a distinct and appropriate assignment asthe executor of the State’s special financing and have the SME andregional policy objectives set been achieved?

b) Is Finnvera plc’s domestic financing activity correctly sized?

c) In its current forms, is the effectiveness of State aid allocated forFinnvera plc’s domestic financing to the point?

d) Are Finnvera plc’s financing products well adapted to the prevail-ing market failures and has Finnvera plc’s cooperation with bankson using them been sufficient?

e) Within the next few years, what kinds of changes can be expectedon the market that should be taken into account when developingthe company’s activities?

f) Does Finnvera plc evaluate enough the effectiveness of its differ-ent financing instruments?

23

g) Does Finnvera plc have sufficient personnel and expert resourcesfor effectuating the necessary changes/for adapting to the chang-ing requirements?

h) Has the client’s perspective been taken sufficiently into account inFinnvera plc’s activities?

i) Is the Ministry of Trade and Industry’s industrial policy controlover Finnvera plc expedient and how should the industry policyrelated targets of domestic financing be developed?

3. Overall Organisation

1) As a whole, has the establishment of Finnvera plc by merging theformer Kera Corporation and the Finnish Guarantee Board beensuccessful, when considering the targets: efficiency of special fi-nancing, transparency and regional availability of the share of pub-lic funding, and streamlining of the State’s corporate governance?

2) In regard to its size and internal structure, is the organisation ofFinnvera plc’s financing activity appropriate considering the chal-lenges set for it and those that are now predictable?

3) How should Finnvera plc’s fiscal status be developed?

1.1.2 Structure of the Report

The report has four sections.

Section 1: Introduction

Section 2: Evaluation of Finnvera´s Export Credit Guarantee Activities

Section 3: Evaluation of Finnvera´s Domestic Financing

Section 4: Evaluation of Finnvera´s Overall Organisation

Following the Introduction, Sections 2, 3 and 4 focus on each of the areas outlinedabove: Export Credit Guarantees; Domestic Financing; Overall Organisation.Summary conclusions and recommendations are given for each section.

24

The evaluators would like to extend their gratitude in particular to Sakari Arkio,Markus Lounela and Risto Paaermaa from the Ministry of Trade and Industry, theSupporting Group (or Steering Group) members, as well as all the staff andmanagement of Finnvera for their time, patience and willingness to providedetailed responses to our many questions.

1.2 Methodology and Analytical Framework

The methodology followed in the evaluation process is depicted in Figure 1 below.

Figure 1. Evaluation process

Background material was reviewed and interviews were conducted with a numberof people. The list of interviews is in Appendix 1. On-line surveys were alsoundertaken with banks, Finnish exporters and Finnvera employees. These surveysare found in Appendix 2.

25

Backgroundmaterial:- Legislation- Statistics- Finnvera-material- Other material

Interviews, surveys:- Finnveraplc- Stakeholders:

• Finnish exporters• entrepreneurs• ministries• federations• banks• private credit insurers

Operatingenvironment:- Export credit market- SME sector andfinancingmarket

Evaluation:

* Finnvera plc´s export creditguarantee activities

* Finnvera plc´s domesticfinancing activities

* Finnvera plc`s overall organisation

Synthesis :

Conclusions andrecommendations

Steering

group

AN

AL

YT

ICA

LF

RA

ME

WO

RK

:T

he

Exp

ort

Cre

dit

Syste

mH

ea

lthS

core

card

©

Backgroundmaterial:- Legislation- Statistics- Finnvera-material- Other material

Interviews, surveys:- Finnveraplc- Stakeholders:

• Finnish exporters• entrepreneurs• ministries• federations• banks• private credit insurers

Operatingenvironment:- Export credit market- SME sector andfinancingmarket

Evaluation:

* Finnvera plc´s export creditguarantee activities

* Finnvera plc´s domesticfinancing activities

* Finnvera plc`s overall organisation

Synthesis:

Conclusions andrecommendations

Steering

group

AN

AL

YT

ICA

LF

RA

ME

WO

RK

:

Th

eE

xpo

rtC

red

itS

ystem

He

alth

Sco

reca

rd©

Backgroundmaterial:- Legislation- Statistics- Finnvera-material- Other material

Interviews, surveys:- Finnveraplc- Stakeholders:

• Finnish exporters• entrepreneurs• ministries• federations• banks• private credit insurers

Operatingenvironment:- Export credit market- SME sector andfinancingmarket

Evaluation:

* Finnvera plc´s export creditguarantee activities

* Finnvera plc´s domesticfinancing activities

* Finnvera plc`s overall organisation

Synthesis :

Conclusions andrecommendations

Steering

group

AN

AL

YT

ICA

LF

RA

ME

WO

RK

:T

he

Exp

ort

Cre

dit

Syste

mH

ea

lthS

core

card

©

Backgroundmaterial:- Legislation- Statistics- Finnvera-material- Other material

Interviews, surveys:- Finnveraplc- Stakeholders:

• Finnish exporters• entrepreneurs• ministries• federations• banks• private credit insurers

Operatingenvironment:- Export credit market- SME sector andfinancingmarket

Evaluation:

* Finnvera plc´s export creditguarantee activities

* Finnvera plc´s domesticfinancing activities

* Finnvera plc`s overall organisation

Synthesis:

Conclusions andrecommendations

Steering

group

AN

AL

YT

ICA

LF

RA

ME

WO

RK

:

Th

eE

xpo

rtC

red

itS

ystem

He

alth

Sco

reca

rd©

In previous assignments undertaken by International Financial Consulting Ltd. toreview national export credit systems, an analytic framework was developed andapplied to assess the overall “health” of the export credit system. This frameworkhas been used previously to assess the health of a number of countries’ export creditsystems.

It therefore has been applied to Finland and this review of Finnvera. In addition, theframework has been adapted for the evaluation of the domestic financing business,as many of the same dimensions are relevant.

The Export Credit System Health Scorecard© considers the strength of the govern-ment’s institutional involvement in export credits through Finnvera and the healthof the overall export credit system as a whole, taking into account all the officialplayers and private sector. This analysis covers four key parameters which areoutlined below:

1. Exporter Focus /Services

This parameter considers the extent to which exporters’ needs are beingmet in the foreign markets in which they are doing business and atinternationally competitive prices.

2. Government Control and Oversight

This parameter considers the extent to which the government as Finn-vera’s shareholder has sufficient control and oversight, communicatesits objectives and both measures and manages fiscal costs.

3. Institutional Strength

This parameter considers the overall health of the entity, Finnvera.

4. Private Sector Involvement

This parameter examines the level of private sector participation inexport credits.

These parameters will be further expanded as they are applied in the subsequentsections.

26

The Domestic Financing evaluation is based on the evaluative framework of theExport Credit System Health with customised key parameters. While the evalua-tion framework of the domestic business is similar, no scoring is given for the do-mestic financing evaluation.

1.3 Finnvera Plc

1.3.1 Background

Finnvera began operating in 1999 following the merger of Kera Corporation andthe Finnish Guarantee Board. Motivating this merger was a desire to renew theadministration of publicly supported special financing, improve the effectivenessof the State’s special financing and simplify the State’s ownership steering.

1.3.2 Business Activities

On the export credit side, Finnvera is a key contributor to the Government’s overallexport credit activities (with its subsidiary Fide Ltd, as well as Finnish ExportCredit plc), and represents Finland internationally in the Paris Club, the EuropeanCouncil Working Group on Export Credits and the OECD Export Credit Group. Inrespect of its domestic financing, Finnvera is represented on the Network ofEuropean Financial Institutions for SMEs (NEFI), and other regional and inter-national bodies.

Total domestic financing activity has been increasing steadily over the past 3 years.The most significant increase was from 2001 to 2002 which saw total domesticfinancing jump close to 9%. The increase in the other years has been much morestable at 1–3%. The first half results of 2003 suggest higher business volume thanprevious years. However, by comparison in 2002, the first 6 months represented61% of the annual total.

The product mix has been relatively stable over the three-year period, with the onlytrend being a slight decrease in special guarantees.

Over the past three years, the number of clients has decreased. This decrease wasfelt most in the number of micro-enterprises which declined, however, wasbalanced by the increase in the number of SME’s during the same period.

27

Table 1. Domestic Financing

Domestic Operations (EUR Million)

2000 2001 2002 6 months2003

Total domestic financing 688.5 708.3 770.2 447.3

Financing granted by product

Loans

Domestic guarantees

Special guarantees

318.6

308.0

61.9

332.0

323.1

53.2

352.1

361.7

56.4

216.5

198.3

32.5

Financing by sector:

Industry

Services for Business

Trade and consumer services

Tourism and rural trades

476.2

101.9

66.0

44.4

462,8

108.2

88.3

49.0

463.5

150.5

105.0

51.2

274.5

73.2

67.5

32.1

Total number of clients

Micro-enterprises (#)

SMEs (#)

LEs and other business (#)

26,351

22,283

3,584

484

26,761

22,341

3,970

450

25,676

21,055

4,244

377

25,468

20,756

4,157

555

The export credit guarantees saw greater fluctuations in the level of business thanthe domestic operations did. The total guarantees granted appeared to be remainingfairly consistent over the period 2000 to 2002. However, the first 6 months of 2003produced results consistent with full year results for the three previous years.

There are no real trends which can be detected for Finnvera’s export creditguarantees business as this business tends to be large and lumpy. The proportionalimpact of one contract can have a significant skewing effect on the shape of theportfolio.

28

Table 2. Export Credit Guarantees

Export Credit Guarantees (EUR Million)

2000 2001 2002 6 months2003

Total Guarantees Granted 1,665.2 1,764.1 1,708.8 1,732.8

Guarantees granted by region:

Asia

CIS

Central and Eastern Europe

Latin America

Middle East and North Africa

Sub-Saharan Africa

Industrialised countries

659.3

9.6

66.6

446.3

268.3

5.9

209.2

934.8

25.6

51.0

594.9

147.3

0.0

10.5

200.3

58.6

387.0

211.5

138.3

23.8

689.3

28.1

18.5

4.8

439.0

84.6

3.8

1,154.0

1.3.3 Mandate

The range of Finnvera’s activities is reflected in the following three elements ofFinnvera’s mandate to:

1. Provide risk financing for, and development of SMEs;2. Promote internationalization and exports of enterprises; and3. Promote the government’s regional policy measures.

Finnvera meets these objectives largely through its two general business lines: fi-nancing of enterprise activities in Finland; and granting of export credit guaranteesthrough foreign risk-taking. Finnvera is the official ECA of Finland. Its activitiesalso include providing support to domestic SMEs.

1.3.4 Legislative Framework

There are numerous Acts which govern Finnvera’s activities on both the exportcredit guarantees side and the domestic financing side.

In the area of export credit and special guarantees, the most important Act is the Actof the State’s Export Credit Guarantees (422/2001) which dictates the State’sinvolvement in this area. The Government Decree (558/2001) on principles to befollowed in export credit guarantee activities further elaborates these areas.

29

There are other Acts which govern “special guarantee” activities, including ship-building (572/1972), investments promoting environmental protection (609/1973)and ensuring the supply of raw materials (651/1985).

According to the Act in the State’s Export Credit Guarantees (422/2001), thepurpose of Finnvera’s export credit guarantee activity is: “to strengthen Finland’seconomic development by promoting exports and the internationalisation of enter-prises”. Finnvera is also required to take into account certain factors when grantingexport credit guarantees, such as:

• international rules and regulations;

• international competitive factors; and

• environmental impact of the project.

In addition, a key objective of the export credit guarantees is to “correct anydeficiencies that may exist on the financial market”.

In the domestic financing the Act on the State-Owned Specialised FinancingCompany (443/1998) dictates the purpose of Finnvera: to provide financingservices to promote and develop business, particularly that of SMEs and to promoteand develop the exports and internationalisation of enterprises. In addition to thisFinnvera is to promote State´s regional policy goals and focus its activities onshortcomings in the supply of financing services, i.e. on market failures. The Act onCredits and Guarantees provided by Finnvera (445/1998) further targets theoperations.

1.3.5 Objectives

Every year, the government provides Finnvera with its Public Policy Objectives.This area is dictated by the MTI’s working group and sets out the government’sOwnership Policy and Industrial Policy.

The government’s ownership policy objectives cover two points: Efficiency andCapital adequacy. With respect to the industrial policy, there are a number ofobjectives set out by the government:

• Financial self-sufficiency

• Market Gaps/failures

30

• SME objectives

• Internationalization objectives

• Regional policy objectives

• Customer service

1.3.6 Market Failure

An important public policy objective for Finnvera is to address market failure. It iscrucial that Finnvera is not impeding the private sector or operating in a part of themarket in which the private sector would otherwise be willing to operate. Thiswould be market distorting and would be in contravention of the government’sintent in requiring Finnvera to operate within the market gaps.

A market gap is by definition the unmet demand for a given product or service.However, the concept of a market gap is not straightforward. It is crucial to takeaccount of the difference between (a) the existence of a gap, i.e. lack of availabilityfrom existing sources of supply and (b) the unwillingness or inability of companiesto pay the price sought by suppliers.

In fact, there are perhaps three characteristics of gaps in the supply of a givenproduct or service:

i) supply does not exist at all; or

ii) supply does exist but is exceeded by demand; or

iii) supply may exist but at a price that firms are not willing to pay

Further, market gaps are not static, but change over time and sometimes veryrapidly.

31

2 Evaluation of Finnvera Plc'sExport Credit Guarantee Activities

2.1 Introduction and Background

In conducting the evaluation of Finnvera’s Export Credit Guarantees business, it ishelpful to examine the overall background of export credit globally and well asconsider what is happening to Export Credit Agencies (ECAs) in other countries. Itis in this context that the review of Finnvera’s Export Credit Guarantee program isconsidered.

This section therefore is divided into four parts:

1. Review of the Overall Finnish Export Credit System

2. Review of Finnvera’s Export Credit and Special Guarantees

3. Export Credit System Health Scorecard

4. Conclusions and Recommendations

The first part provides a background to export credit business in the world,considering the recent trends and key challenges. The second part looks at thespecific situation in Finland. Part 2 is the specific review of Finnvera’s activities inthis area. Part 3 evaluates the Finnish export credit system using the HealthScorecard.

The final part of this section offers conclusions, by addressing the issues raised inthe Terms of Reference for the Review of Export Credit Guarantee Activities, andoffers a set of recommendations which relate to Finnvera’s export credit guaranteebusiness.

2.1.1 Government Involvement in Export Credit

Government involvement in export credit can take many forms. While the man-dates and roles of all ECAs are broadly similar, there is no such thing as a “typical”ECA: their business models, status, objectives, institutional arrangements, and gov-ernment involvement vary widely from country to country, reflecting their ownunique national circumstances.

32

It is therefore difficult to generalise about ECAs, as no two ECAs are identical.However, they share some common characteristics and mandates. The reasonECAs exist is the same across all countries – to support and facilitate exports andoutward investment.

There is no single or perfect model or status or organisation or – for that matter –structure for government involvement in an official export credit scheme. Nor isthere such a thing as a typical ECA. Finnvera is unique amongst OECD countries inhaving both the domestic financing business and export credit business under oneroof.

Some ECAs are government departments, some are public corporations and someare private companies. Some of the latter may underwrite most of their business ontheir own account but, under an arrangement/agreement with their government,may also write business on the government’s account. Some do only short-termbusiness, some do only medium- and long-term business and some do both. Someonly insure or issue guarantees, some lend and some do both. Some are calledinsurers and some export/import banks. Some offer interest stabilisation and exportcredit under one roof, while others offer these through different schemes. Someonly offer export credit and some only investment insurance but most do both.Some primarily underwrite political risks and some write primarily commercialrisks, but most now cover both categories.

Finland is unique in having three different entities (Finnvera, FIDE and FEC)which provide different aspects of the government’s scheme – export credit guaran-tees, interest stabilisation and lender of record for withholding tax exemptions.

2.1.2 ECA Market Segments

The main focus of ECAs is to take political and commercial risks in support ofexports or investments made by national companies. The market in which ECAsoperate is made up of different sectors which are subject to different pressures anddynamics, especially growth in the private sector’s participation in some of theseareas. The three main categories or segments of ECA activities are:

• Export Credit Insurance

– short-term export credit

– medium- and long-term export credit

33

• Investment Insurance

• Other facilities such as working capital and bonding facilities

2.1.2.1 Export Credit Insurance

In the Export Credit Insurance world the insurance policies are often called“guarantees”. This is the case in Finland and other European countries. However,the term “guarantees” can be misleading and it is important to note that they are notguarantees in the normal sense in which the word is used, especially by commercialbanks, as being fully unconditional and on-demand.

Export Credit Insurance facilities are always conditional insurance policies. Thelevels of conditionality may vary from one ECA to another, though a few ECAs(EXIM in the US and ECGD in the UK) get close to a full unconditional guarantee.Importantly, this means that a claim will only be paid if the default in payment bythe buyer is caused by one of the insured events or situations set out in the policy. Inother words, the fact that a buyer has not paid does not mean that the insurer willautomatically pay a claim. Credit insurance does not provide protection againstfailure of the exporters or of non-payment by the buyer because the exporter hasfailed to perform in accordance with the contract.

It is important to note that there are two different types of credit insurance: suppliercredit and buyer credit. Supplier credit is one where the credit involved in atransaction is extended by an exporter/supplier to the overseas buyer/importer andthe terms of the credit are set out as part of the export contract.

Most short credit business is conducted on this basis. Supplier credit would not of-ten be used for projects or medium and long term credits. When supplier credit isused in the area of medium term credit, it would be normal for the exporter to acceptbills of exchange or to issue promissory notes which would apply to repayments ofthe sum outstanding, including interest, in individual credit repayments on speci-fied dates during the credit period.

Buyer credit is the technique which would normally be used for projects but canalso be used for sales of capital goods where medium or long term credit isinvolved. The normal contractual arrangements would be that an exporter entersinto a contract with a buyer. The contract would concentrate on the goods andservices to be supplied and the appropriate specifications and delivery date etc. Theterms of the credit would not be included in the contract, but would be set out in aseparate loan Agreement, often between the exporter’s bank and the buyer’s bank.

34

Short-Term Business

Short-term business is the traditional and main product of export credit insurance.This is not surprising since at least 90% of world trade is conducted on the basis ofcash or short-term credit.

Activities of the private sector insurers have grown most substantially in theshort-term area and there is now very significant capacity within the privatereinsurance market. The private insurance market is now primarily concentrated inthree big players (Euler-Hermes, Gerling NCM – now Atradius – and COFACE)which are now active and dominant worldwide.

In addition, it is in this area that there is the greatest competition for business, bothbetween private companies and also between private insurers and public insurers.The European Union has reacted to this by setting guidelines on the activities ofpublic insurers: public insurers are only allowed to underwrite “non-marketablerisks” whereas private insurers and reinsurers within the European Union canunderwrite any risks which they are willing to cover (see Section 2.1.5.3 for moreinformation).

The bulk of short-term credit insurance in OECD countries (with the exception ofJapan and Canada) is now provided by the private sector and is supported by privatesector reinsurance The involvement of most official ECAs in the provision ofshort-term credit insurance is lessening. An increasingly common role for ECAs isas a contingent reinsurer or, in for some ECAs, including Finnvera, as a directinsurer for single higher-risk transactions.

Medium and Long-Term Export Credit

Medium and Long-Term (MLT) export credit insurance is a market traditionallydominated by ECAs. As such, private sector insurers are relatively few and theinvolvement of private sector insurance has been limited. However, some privatesector insurers are now prepared to consider longer-term risks (i.e. up to 5 years).AIG, Zurich Emerging Markets, Chubb, Unistrat, Exporters Insurance Company(EIC) and Lloyds are considered to be the biggest medium term private sector creditinsurers. Their main activities have been political risk insurance, rather thancomprehensive cover (covering both commercial and political risks).

2.1.2.2 Investment Insurance

Originally, investment insurance only covered equity investment but now the bulkof new business is in relation to untied loans into projects. There is therefore an

35

overlap between export credit insurance and investment insurance loans. Exportcredit insurance is tied to supply, but investment insurance is in support of an untiedloan.

Most official insurers have enjoyed much better results from investment insurancethan from export credit insurance. This has been partly because investmentinsurance cases have been exempt from reschedulings under the Paris Club, andpartly because claims have been fewer and smaller and more have been recovered.This has led to great interest from the private sector in underwriting this class ofbusiness and thus considerable potential for competition and cooperation betweenprivate and public insurers. In fact there has been so far more co-operation betweenprivate and public insurers in terms of co-insuring and reinsuring and risk sharing inthis area than in medium- and long-term export credit insurance. Some majorprivate insurers (e.g. AIG, Zurich, and Sovereign) operate in this area and aresubstantial underwriters with large capacity. In terms of new business, the activitiesof these large private insurers are now bigger than most official schemes.

2.1.2.3 Other Facilities

Working capital is the financing required to carry out the production/processingfrom the time an export order is obtained until the goods are delivered to/acceptedby overseas buyers. Normally, ECAs are not directly involved in providingworking capital, although exporters often are able to obtain working capital fromtheir banks because the exporter can provide as security the ECA credit insurancepolicy (which may include cover of pre-credit risks) sometimes through theassignment of the policy to the bank.

A few ECAs are directly involved in the provision of working capital, offeringfacilities directly to the banks and, in certain developing countries, working capitalloans are provided by the ECA directly. In a few OECD countries, where ECAs areinvolved in working capital facilities, such facilities are usually restricted to theSME sector whose access to finance may be limited by the size of their balancesheet.

Not usually included as a segment of ECA business is finance for exporters to makeinvestments, such as to increase the capacity of companies to produce more and soexport more. This area might also cover investment in new plants or funds forgeneral export research and export marketing. In FInland, this category of businessis done by Finnvera’s domestic financing operations.

With respect to bonding and letters of guarantees, most ECAs provide cover to acommercial bank or surety company that issues a facility to a buyer on behalf of an

36

exporter. The bonds can be tender, advance payment, bid, performance orretention. A performance bond, for example, is a guarantee that the exporter willmeet the terms of its contract with the buyer.

An unfair call on the bond will result in a claim paid by the ECA, if the call can beshown to be unfair for political reasons. It is not normally the case that an ECA willcover fair calls as well as the main risk is the performance of the exporter. Thedifference between the two relates to recourse to the exporter.

2.1.3 Accounting and Financial Aspects

Export Credit Insurance is essentially a long-time scale business. This is of courseespecially true of MLT facilities. This simply reflects the fact that many years willelapse between the time that a piece of business is underwritten and the time whenthe extent of any losses can be assessed or fixed with any real degree of confidenceor certainty.

It is possible, for example, that only in year 15 that the extent of the loss suffered bythe insurer (i.e. the net claim or the difference between the amount paid as a claimand the amount recovered, taking account also of loss of interest) can be finallyassessed. Figure 2 below shows how the chain of events of a shipbuilding trans-action might occur.

37

Figure 2. Time Line

It is very important that the financial management and accounting of an insurerreflects these basic features of credit insurance and especially:

i) That it is a “long tail” long-term business.

ii) That some claims and losses are inevitable

iii) That claims are not the same as losses in that some recoveries will bemore – this is true both of claims paid in respect of commercial risks andclaims paid in respect of political risks.

iv) That premium rates should be set to try to cover all net losses, includingloss of interest.

38

• Contract signed and premium pass to insurer

• Ship is built

• Ship is delivered to buyer who – under the terms of thecontract – will be in 6 monthly instalments over 12 years

• Payments made by buyer on due dates

• Default in payment as the buyer is in financial difficulties

• Buyer goes insolvent, insurer pays claim to shipbuilderand its bank. Ship is repossessed and sold to another buyerwith payments to be spread over 5 years

• New buyer makes some repayments thus allowing insurerto make some recoveries of the amount paid as a claim

• New buyer defaults and becomes insolvent

• Ship repossessed and efforts made to find buyer

• Efforts to find new buyer fail and so ship is sold for scrap

bringing limited funds which do not fully cover the amountpaid by the insurer as a claim

Year 1

Year 2-3

Year 4

Year 5-8

Year 10

Year 11-12

Year 13

Year 14

Year 15

Year 9

Timeline Events

• Contract signed and premium pass to insurer

• Ship is built

• Ship is delivered to buyer who – under the terms of thecontract – will be in 6 monthly instalments over 12 years

• Payments made by buyer on due dates

• Default in payment as the buyer is in financial difficulties

• Buyer goes insolvent, insurer pays claim to shipbuilderand its bank. Ship is repossessed and sold to another buyerwith payments to be spread over 5 years

• New buyer makes some repayments thus allowing insurerto make some recoveries of the amount paid as a claim

• New buyer defaults and becomes insolvent

• Ship repossessed and efforts made to find buyer

• Efforts to find new buyer fail and so ship is sold for scrap

bringing limited funds which do not fully cover the amountpaid by the insurer as a claim

Year 1

Year 2-3

Year 4

Year 5-8

Year 10

Year 11-12

Year 13

Year 14

Year 15

Year 9

Timeline Events

• Contract signed and premium pass to insurer

• Ship is built

• Ship is delivered to buyer who – under the terms of thecontract – will be in 6 monthly instalments over 12 years

• Payments made by buyer on due dates

• Default in payment as the buyer is in financial difficulties

• Buyer goes insolvent, insurer pays claim to shipbuilderand its bank. Ship is repossessed and sold to another buyerwith payments to be spread over 5 years

• New buyer makes some repayments thus allowing insurerto make some recoveries of the amount paid as a claim

• New buyer defaults and becomes insolvent

• Ship repossessed and efforts made to find buyer

• Efforts to find new buyer fail and so ship is sold for scrap

bringing limited funds which do not fully cover the amountpaid by the insurer as a claim

Year 1

Year 2-3

Year 4

Year 5-8

Year 10

Year 11-12

Year 13

Year 14

Year 15

Year 9

Timeline Events

• Contract signed and premium pass to insurer

• Ship is built

• Ship is delivered to buyer who – under the terms of thecontract – will be in 6 monthly instalments over 12 years

• Payments made by buyer on due dates

• Default in payment as the buyer is in financial difficulties

• Buyer goes insolvent, insurer pays claim to shipbuilderand its bank. Ship is repossessed and sold to another buyerwith payments to be spread over 5 years

• New buyer makes some repayments thus allowing insurerto make some recoveries of the amount paid as a claim

• New buyer defaults and becomes insolvent

• Ship repossessed and efforts made to find buyer

• Efforts to find new buyer fail and so ship is sold for scrap

bringing limited funds which do not fully cover the amountpaid by the insurer as a claim

Year 1

Year 2-3

Year 4

Year 5-8

Year 10

Year 11-12

Year 13

Year 14

Year 15

Year 9

Timeline Events

2.1.3.1 General

Few ECA’s now account only on a cash flow basis, because the results can be verymisleading. In other words, premium may be received in one year, claims paidsome years later and recoveries made later still.

2.1.3.2 Open and Closed Years

Some insurers try to approach these problems by not closing their accounts at theend of each year, but keeping the accounts open for, say, 3 years. At the end of year3, it will be easier to try to form a financial view on the out turn of businessunderwritten in year 1. A balance showing a surplus or loss can then be struck andthe accounts closed.

2.1.3.3 Premium

Another approach is not to take all premium into “profit” or income until it has beenearned. For example, if a case has a 5 year horizon of risk then even if the fullpremium is received in Year 1, only 1/5th of the premium will be credited to theaccounts in year 1 with the balance being spread over the accounts during the next 4years.

2.1.3.4 Provisions

However, probably the most important factor relates to provisions in the amount ofincome that is set aside in respect of future claims.

There are two main types of provisions: General and Specific. General provisionsare made in the financial year in which the business is underwritten. Such provi-sions are not made in respect of any particular case or country but reflect the knowl-edge that some claims are inevitable. They can be based, for example, on correlatedstatistics in respect of experience on business underwritten over, say, the previous10 years.

The key point is that General Provisions are deducted before any balance or surplusis struck. They are, therefore, in accounting terms above the line.

Specific provisions are those made in respect of particular cases or countries. Theseare usually made as a result of reviewing the portfolio of existing business of theinsurer. Where there are reasons to believe that projects or countries are already indifficulty or are likely to get into difficulty, then an assessment should be made of

39

possible/probable loss and a specific provision made for accounting. This can takeaccount of any provisions already made. There is no need to wait until claims arepaid or losses suffered before making provisions, which indeed can be a dangerousand misleading approach.

2.1.3.5 Reserves

It is very important that insurers, including ECA’s should seek to accumulatereserves. This reflects the points made earlier and also the basic fact that exportcredit insurance is a cyclical business. Thus in some years, income will exceedexpenditure and in other years the reverse will be the case.

In some countries depending on accounting practice, accumulated General andSpecific Provisions are treated as reserves. But this should not be the whole story.Thus it can be very helpful for an ECA to put all or most of surpluses from any yearinto reserves against possible losses/deficits in future years. This is not onlyprudent, but can avoid the need for Guardian Authorities to be required to find largeamounts of cash at short notice. But, importantly, it also takes account of the veryuncertain nature and long risk horizon involved in the business and avoids the riskof cash flow surpluses being wrongly regarded as “profits”.

2.1.4 Key Developments in the Export Credit Market

Over the past decade or so, traditional export credit systems and models have beensubject to significant change. In most cases, the process of change has not yet cometo an end. These changes have been driven by a range of national and global factors.These factors may not be the same in every export credit system but some globaltrends can be seen. Some of the key factors that are driving the change are coveredbelow.

2.1.4.1 Globalisation

Globalisation of companies and banks has inevitably impacted on credit insurers: towin the business insurers most want (i.e. providing cover to the largest multi-nationals), they must become similarly “global”. Therefore, national ECAs with amandate to operate support their national exporters find it difficult to serve theirmultinational customers which may be selling out of third countries.

The globalisation of the banking sector has also played an important role in theevolution of the export credit market, particularly in the medium and long-term

40

area. Global banks with representation in most, if not all, major markets areincreasingly crucial players in financing exports, especially capital goods andproject exports.

2.1.4.2 Competition and Consolidation

Competition has become an important and growing factor of export credit. Thisembraces not only competition between private companies but also actual andpotential competition for business between the private sector and the public sector.

Owing primarily to takeovers and consolidations, the “Big 3” large private creditinsurers now operate in – and out of – various countries. The competition betweenthese groups is vigorous and they are operating as both domestic and export creditinsurers, via branches, acquisitions, or “regional offices" in a growing number ofcountries in Europe and abroad.

Consolidation in the industry has been partly driven by the huge increase inoverheads – particularly IT expenditure – which meant that successful companiesneeded to spread these overheads over the largest volume of insured business.

Since 2001, the maturity of the private market has been proven by the fact that nomajor credit insurer or reinsurer has left the business.

2.1.4.3 Development of Private Reinsurance Capacity

Triggered by the 1991 privatisation of ECGD’s short-term insurance business, theprivate reinsurance market has fundamentally changed its position. Private re-insurers have also lost their fear of this category of business. This was helped by thefact that until 2001, the previous seven or eight years have, to some extent, been a“golden period” for such business and most underwriters enjoyed surpluses. Thusthe breadth and depth of the private reinsurance market has increased hugely andsubstantial private reinsurance market capacity for export credit insurance is nowavailable, embracing both political and commercial risks.

The post 9–11 period has seen a combination of events and trends which have in-creased problems for the sector. Some events have affected the whole insuranceand reinsurance market, while other events have been specific to the credit insur-ance business. Very large claims have been paid on the 9–11 events themselves but,in addition and of more direct and immediate concern to the credit insurance and

41

surety market, have been the fall out of Enron and WorldCom, the situation in Ar-gentina and heavy claims in respect of buyer failures in Germany and the USA.