finding new revenue sources in a down economy how ns short lines can enhance their customers’...

TRANSCRIPT

Finding New Revenue Sourcesin a Down Economy

How NS short lines can enhance their customers’ competitive advantage

Norfolk Southern Short line Conference,

Brosnan Forest, April 2009Roy Blanchard, The Blanchard Company

Railway Age Contributing Editor

TRAINS Contributor

March 18, 2009 www.rblanchard.com 2

Agenda• Infrastructure and Equipment

– Classifying NS short lines– Be careful what you ask for

• Trends Going Forward– “Heat and eat”– Consolidation and abandonment

• Markets and Competition– Creating a shortline niche– Understanding the customer perspective

• The Smarter Railroad– Asset productivity– Doing more with less

March 18, 2009 www.rblanchard.com 3

The purpose of any business is to create customers.

-- Peter Drucker

Customers will increasingly focus on the complete door-to-door trip. -- Dr. Joe Giglio, Mobility

March 18, 2009 www.rblanchard.com 4

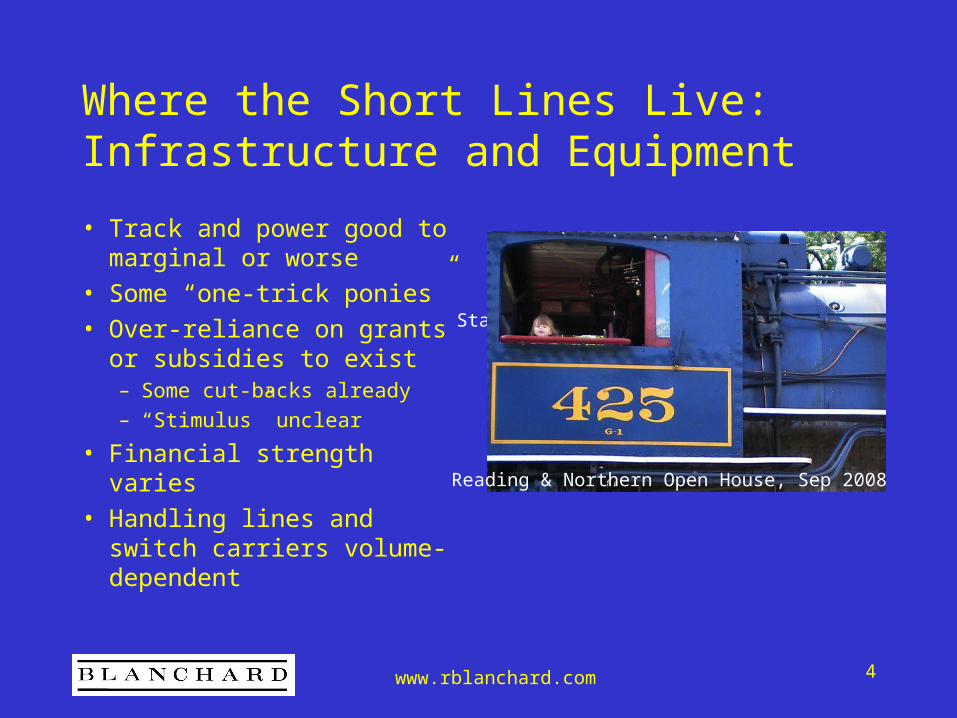

Where the Short Lines Live: Infrastructure and Equipment

• Track and power good to marginal or worse

• Some “one-trick ponies”

• Over-reliance on grants or subsidies to exist– Some cut-backs already

– “Stimulus” unclear

• Financial strength varies

• Handling lines and switch carriers volume-dependent

Staged accident, NC, 1996

Reading & Northern Open House, Sep 2008

March 18, 2009 www.rblanchard.com 5

Where the Short Lines Live: Good Track Equals Competitive advantage

Short Line, Virginia, 2006 NKCR, Nebraska, 2005

March 18, 2009 www.rblanchard.com 6

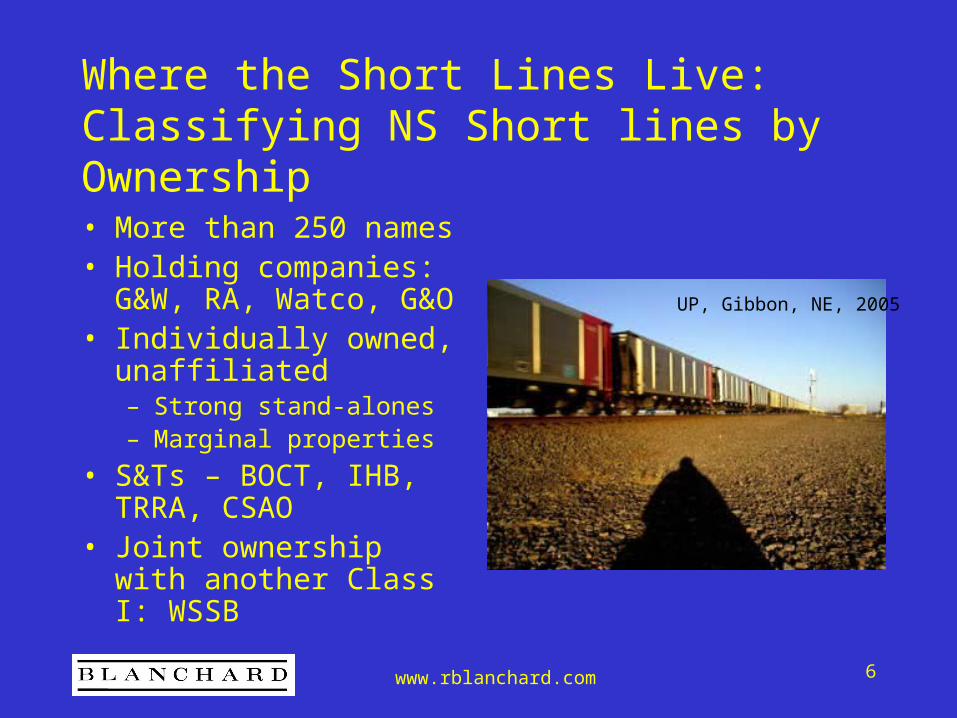

Where the Short Lines Live: Classifying NS Short lines by Ownership

• More than 250 names• Holding companies:

G&W, RA, Watco, G&O • Individually owned,

unaffiliated– Strong stand-alones– Marginal properties

• S&Ts – BOCT, IHB, TRRA, CSAO

• Joint ownership with another Class I: WSSB

UP, Gibbon, NE, 2005

March 18, 2009 www.rblanchard.com 7

Where We are and What’s Coming: Ownership Trends in 2009 and beyond

• Strong unaffiliateds bought by holcos with economies of scale and marketing savvy

• Merch service in single-car lots of low-rated commodities going away

• Financially weak names are at risk

• “Heat and eat” here to stay

NKCR, Nebraska, 2005NKCR, Nebraska, 2005

March 18, 2009 www.rblanchard.com 8

Where We are and What’s Coming: Service

• Merch carload service improving

• Focus on service to improve volumes, revenues, or both

• Customer and market segmentation

• Scalpel, not a meat ax

Maine 2-foot gauge, 2008Maine 2-foot gauge, 2008

March 18, 2009 www.rblanchard.com 9

Is the business model profitable and growing? It must be for both to prosper

Customer/Railroad Customer/Railroad

Yes/Yes

A winning combination. Nurture and grow.

No/Yes

Going out of business sale? Using the RR because he can’t afford trucks? Kill

Yes/No

Can go either way. Why are you losing share? Can you recover margin and share?

Grow or kill, depending.

No/No

Dead meat. Run, do not walk, to the nearest exit.

March 18, 2009 www.rblanchard.com 10

Cash Cow or Sacred Cow?Milk the cash cow, kill the sacred cow

Revenue-cost ratio

Volume

High Medium Low

High Cash Cash Cash

Medium Cash Depends Sacred

Low Cash Depends Sacred

March 18, 2009 www.rblanchard.com 11

Markets and Competition: Creating a Shortline Niche

• Marcellus Shale formation in Pennsylvania

• 353 new drilling permits– 300 tons frac sand in 100-

ton PD hoppers– 200 pieces casting pipe in

OT gons, 150 per car

• Transmission pipe 24-42” diameter on TTX flats– Up to 20 sections per car– Arrives in 20-car cuts Natural gas pipe, Lycoming Valley RR, 2008

March 18, 2009 www.rblanchard.com 12

Markets and Competition: Creating a Shortline Niche

• Create a bypass– Offer a 40 mph RR to

parallel the Class I’s 60 mph core route

– State grants, RRIF loans

• Expand service offerings– Local service

– Transload

– Bridge traffic

Western NY & Pa first run

March 18, 2009 www.rblanchard.com 13

Markets and Competition: Creating a Shortline Niche

INRD increases unit train to 100 cars from 65 cars for utility– New aluminum cars– 286 vs. 263 – New SD90 MACs– Same tonnage with

45% fewer trains– Increased available

track capacity– Lowered operating

expense

March 18, 2009 www.rblanchard.com 14

Markets and Competition: Understanding the Shipper Perspective

• We need our shipments on time every time; easily as bad as late

• We need an end to transit L&D

• We need an end to RR-caused demurrage problems

• We need to have the right car in the right place at the right time

• We need total shipment visibility door-to-door

• We need a quality product on a consistent basis

• Everything else is irrelevant N&W, Waverly, VA, late 1950s

March 18, 2009 www.rblanchard.com 15

The Smarter Railroad: Doing More with Less

• Use technology to produce more revenue per asset

• Increase throughput on existing corridors – short lines as alternate routes?

• Price to the market but contain costs

• Match service design to customer supply chain

• The smart and nimble will prosper.

DM&E, South Dakota

March 18, 2009 www.rblanchard.com 16

Rule 99 in Effect. Hope you enjoyed the ride.

NYC, Briarcliff Manor, NY July, 1954

March 18, 2009 www.rblanchard.com 17

Personal Savings Ratehttp://research.stlouisfed.org/fred2/series/PSAVERT