financing power and energy ebrd perspective · (€, us$, rub, pln, ron etc.) •support of...

TRANSCRIPT

Financing Power and Energy EBRD perspective April 2016

What is the EBRD?

International financial institution, promotes transition to market economies in 36 countries from central Europe to central Asia and the Southern and Eastern Mediterranean – SEMED region

In 2014 and 2015, the EBRD welcomed Cyprus and Greece as recipient countries.

• Owned by 65 countries and two inter-governmental institutions.

• Capital base of €30 billion.

As at end December 2015:

• Invested €107 billion in c.4,500 projects

• In 2015 only, €9.4 billion invested in 381 projects

• Private sector accounted for 70% share

• Debt 82%, Equity 14% & Guarantee 4%

2

05101520253035404550556065707580859095100105110

0

2

4

6

8

10

12

Net

cum

ulat

ive

busi

ness

vol

ume

Annu

al b

usin

ess

inve

stm

ent (

ABI)

Equity ABIDebt ABI Net Cumulative Business Investments

€ billion

Where we invest

7 April, 2016 3

The EBRD and its objectives

Objectives: • To promote transition to market economies by investing mainly in the private

sector • To mobilise significant foreign direct investment and facilitate inward and cross

border investments in the region • To support market focused reforms, privatizations • Promotes policy dialogue with regards to investment climate, business and

policy matter • To encourage environmentally sound and financially sustainable development

4

Benefits of working with the EBRD

5

• Flexible deal structure • Debt finance to both public

and private sector • Syndication under preferred

creditor status • Catalyst to access

additional debt • LT (up to 10y or more) or

ST revolving • Floating/ Fixed rates • Choice of currencies

(€, US$, RUB, PLN, RON etc.)

• Support of strategic investors • Perception of quality investment • Sector expertise through

Board of Directors • Good corporate governance • Catalyst to access additional

equity • Positioning as neutral party • Common stock, preferred,

mezzanine • Minority position only (up to 35%)

• Strong, internationally recognized partner with long term perspective

• AAA rated, commercially focused • Mitigation of political and regulatory risks • Policy dialogue with government and regulators • Grant-funded technical assistance • Finance and operations monitoring

Shareholder ’ s Value

EBRD value - added

Equity Financing

LT Debt Financing

Shareholder Value

-

EBRD Value-added

Equity Debt

Power and Energy Utilities Team – Financing by sub-sector

• In 2015 EBRD invested €1.2bn in 15 projects in the power & energy sector.

• In 2015 the EBRD signed € 591m of financing for 13 renewables deals with a total gross project value of €2.2bn.

• In each of the last six years, annual power & energy investments exceeded €1bn and at least 20% of those funds went towards renewable energy generation projects.

Updated as of 31 December, 2015. Source: EBRD data

Electric Power Generation

40%

Electric Power Transmission

6%

Electric Power Distribution

11%

Renewable Power 29%

Large Hydro 13%

Natural Gas Distribution

1%

Financing by Sector (2011–2015)

6

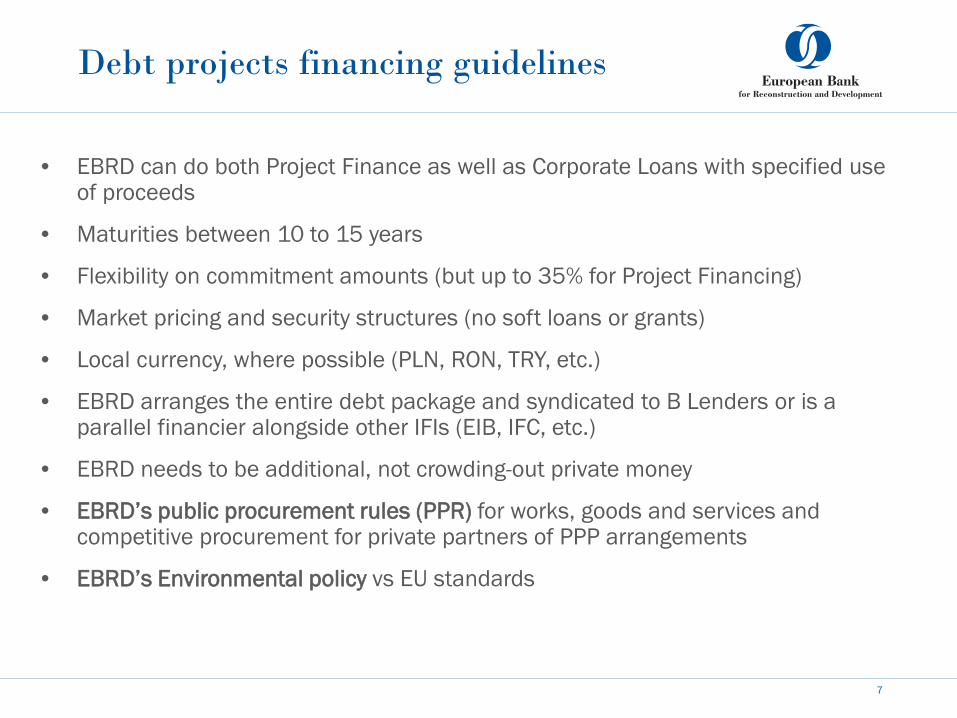

Debt projects financing guidelines

• EBRD can do both Project Finance as well as Corporate Loans with specified use of proceeds

• Maturities between 10 to 15 years

• Flexibility on commitment amounts (but up to 35% for Project Financing)

• Market pricing and security structures (no soft loans or grants)

• Local currency, where possible (PLN, RON, TRY, etc.)

• EBRD arranges the entire debt package and syndicated to B Lenders or is a parallel financier alongside other IFIs (EIB, IFC, etc.)

• EBRD needs to be additional, not crowding-out private money

• EBRD’s public procurement rules (PPR) for works, goods and services and competitive procurement for private partners of PPP arrangements

• EBRD’s Environmental policy vs EU standards

7

8

Technical

• Feasibility study • Completion risk • Production capacity •Management

Environ. & Social

• EIA •Natura 2000 •Health & Safety • Expropriations/Resettle

ments •Management systems • ESAP / Gap Analysis

Market • Supply-demand • Competitors • Price projections • FX exposure

Legal & Contracts

• Security • Charter / Incorporation •Ownership and title • Licenses, permits • Legal agreements • Insurance

EBRD Due Diligence

Process

Concept Review

Structure Review

Final Review

Board Approval

Signing

Due Diligence Term Sheet

KYC

Final Documentation

Our a

ppro

val p

roce

ss

EBRD Internal Approval Process

•Historical financials • Projections • Financial Model • Credit Ratios

Financial

Due Diligence Required

• Technical due diligence – EBRD needs to hire an independent advisor to review the Feasibility Study, wind study, etc. BOP, Grid Connection are important aspects as well.

• Financial due diligence will decide final leverage (for Project Finance) or the appropriate mix of Corporate Debt and Grant (if necessary). EBRD build its own financial models from scratch.

• Environmental due diligence - as most transmission lines and wind farms are falling under EBRD’s A category due to their size, they require 120 and 60 days respectively public disclosure of EIA including Non-technical Summary, Environmental Monitoring and Management Plan and Stakeholder Engagement Plan.

• Other aspects: status of permitting and licenses, land plots, etc.

9

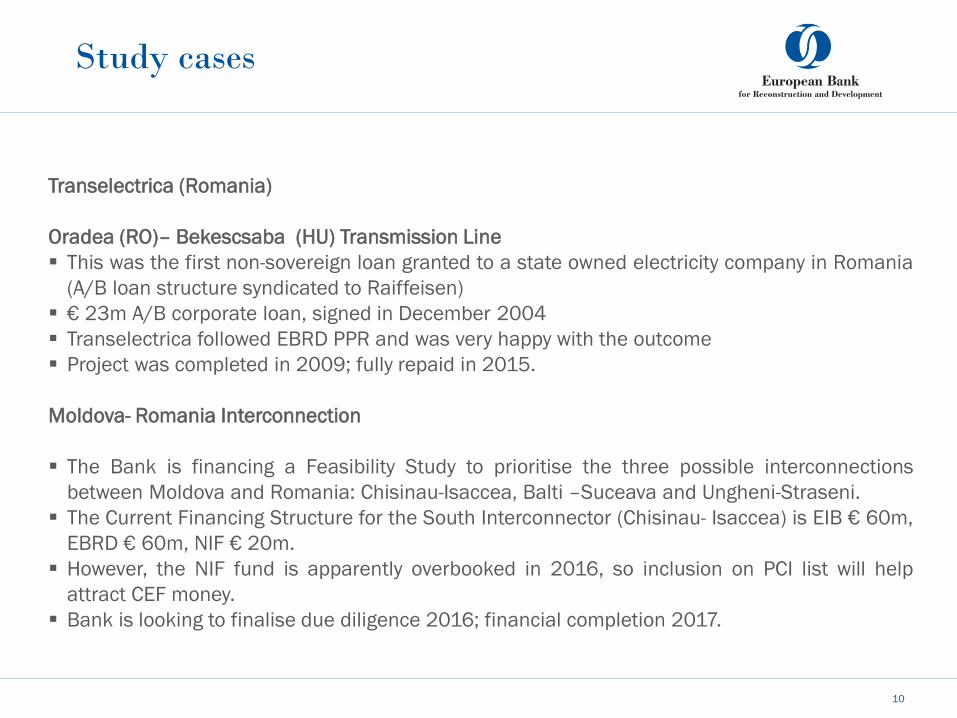

Study cases

Transelectrica (Romania) Oradea (RO)– Bekescsaba (HU) Transmission Line This was the first non-sovereign loan granted to a state owned electricity company in Romania

(A/B loan structure syndicated to Raiffeisen) € 23m A/B corporate loan, signed in December 2004 Transelectrica followed EBRD PPR and was very happy with the outcome Project was completed in 2009; fully repaid in 2015. Moldova- Romania Interconnection The Bank is financing a Feasibility Study to prioritise the three possible interconnections

between Moldova and Romania: Chisinau-Isaccea, Balti –Suceava and Ungheni-Straseni. The Current Financing Structure for the South Interconnector (Chisinau- Isaccea) is EIB € 60m,

EBRD € 60m, NIF € 20m. However, the NIF fund is apparently overbooked in 2016, so inclusion on PCI list will help

attract CEF money. Bank is looking to finalise due diligence 2016; financial completion 2017.

10

Thank you for you attention

For all further enquiries, please contact:

Roxana Simon Principal Banker Power & Energy Utilities Tel: + 44 207 338 6181 Email: [email protected]

EBRD, One Exchange Square London, EC2A 2JN UK www.ebrd.com

11