financing for off-grid solar home lighting systems

DESCRIPTION

A Guide for solar financing procedures with Regional Rural Banks and Other InstitutionsThe predominant reason for solar technology not to flourish is the inability to facilitate the appropriate form of financing for the same. SELCO has over eighteen years followed the below approach in order to overcome this scenario: This is the normal approach when solutions are provided in cities and other well-served towns. But in remote and under-served regions, the tendency is to distribute the cheapest products without any effort being put in to study the best and sustainable solution, often for fear of the effort not being profitable. One of the key factors that can bring about a change in this mindset is to learn about the different options of financial linkages available or that can be created in remote and under-served areas. SELCO has, by utilizing financial linkages available in Karnataka, run as a commercial entity with social objectives very sustainably since 1995. This manual, which has used the extensive experience of SELCO, aims to help all the parties concerned, the system provider, end user and the finance provider to understand and utilize financial linkages to bring light and power to energy deprived areas of the country.TRANSCRIPT

SELCO Incubation Centre 1

FINANCING FOR OFF- GRID SOLAR HOME LIGHTING SYSTEMSA GUIDE FOR SOLAR FINANCING PROCEDURES WITH REGIONAL RURAL BANKS AND OTHER INSTITUTIONS

SELCO Incubation Centre 3

Eighteen years of SELCO’s innovation is entirely

dedicated to the staff members who have

continuously improvised and experimented

on making solar technology affordable /

maintained / utilized by the under-served

communities. If not for the drive of the SELCO

staff members we would not have been able

to see how a technology which is nearly five or

ten times a family’s income or rather the second

highest investment in their life after their house

can be utilized by them.

We dedicate the series of manuals comprising

of – Solar Technology, Sales & Marketing and

Financial linkages for solar products which

documents SELCO’s work, to all of its staff

members which has reached 220+ individuals.

We thank the training team at SELCO headed by

Jagdeesh Pai & Sudhir Kulkarni for their guidance

on the structure of the manual. We also thank our

colleagues – Sathyanarayan B, Ramanath N Dixit

(consultants for financial institution relationships

Acknowledgements

at SELCO both former bankers and hence

have pertinent observations on the schemes

operative and the procedures for the same)

and Surabhi Rajagopalan (part of the SELCO

Foundation managing the policy initiative). We

would like to thank Sameera Mushini, a graduate

from Institute of Rural Management Anand who

authored the first draft for the manual. Lastly,

we also thank and acknowledge our funding

partners for recognizing and supporting us –

GIZ, The Swiss Agency for Development and

Cooperation (SDC), Doen Foundation and Asian

Development Bank: Energy for all.

The spirit and objective of these manuals

are to serve as guiding principles for the new

enterprises which will emerge from the SELCO

Incubation Centre across India. This is part of

an initiative to make SELCO an open source

organization which wants to spread its business

process and principles available to one and all

to make its mission reach far and wide.

Index

1. Acknowledgements .................................................3

2. Introduction ..............................................................6

3. Solar Financing: Structure and Design .................7

3.1 How do we determine if the customer needs financing? ............................................................................................7

3.2 How do we determine if the customer can afford the equipment even if financed? ..................................................7

3.3 How should financing be designed for the customer? ............................................................................................7

3.4 Financing Institutions...................................................................8

4. Banks .............................................................................9

4.1 History of Banks in India and their Role ............................9

4.2 Banks and Solar financing ...................................................... 10

4.3 Benefits accruing to banks from lending for Solar home lighting system ............................................................... 10

4.3.1Categorized under Priority Sector lending: ................ 10

4.3.2 Differential Rate of Interest (DRI) scheme targets: 10

4.3.3 Credit access under financial inclusion: ....................... 10

4.3.4 Refinance from NABARD: ...................................................... 11

4.3.5 Claiming carbon credits: ....................................................... 11

4.3.6 Corporate Social Responsibility (CSR) funds: ............ 11

4.3.7 Ensuring repayment through promotion of livelihoods, rural betterment: ............................................... 11

4.4 Who is eligible for Financing? .............................................. 12

4.5 What are the pre-requisites, conditions and requirements for granting the loan? ............................... 12

SELCO Incubation Centre 5

4.5.1 Loan Proposal ............................................................................... 12

4.5.2 Appraisal of the Proposal ...................................................... 13

4.5.3 Technical Aspects....................................................................... 13

4.5.4 Legal Aspects ............................................................................... 14

4.5.5 Repayment Capacity................................................................ 14

4.5.6 Sanctioning Authority............................................................. 14

4.5.7 Documentation & Disbursement .................................... 14

4.5.8 Rate of Interest ............................................................................ 14

4.5.9 Service Charges .......................................................................... 15

4.5.10 Security .......................................................................................... 15

4.5.11Surety/ Guarantor .................................................................... 15

4.5.12 Repayment .................................................................................. 15

4.5.13 Classification .............................................................................. 15

4.6 Borrower Assessment - Checkpoints ............................... 15

Table 1: Check points for assessing the customer ............ 16

4.7 What are the Dos and Don’ts while filling the form for a loan? ......................................................................................... 16

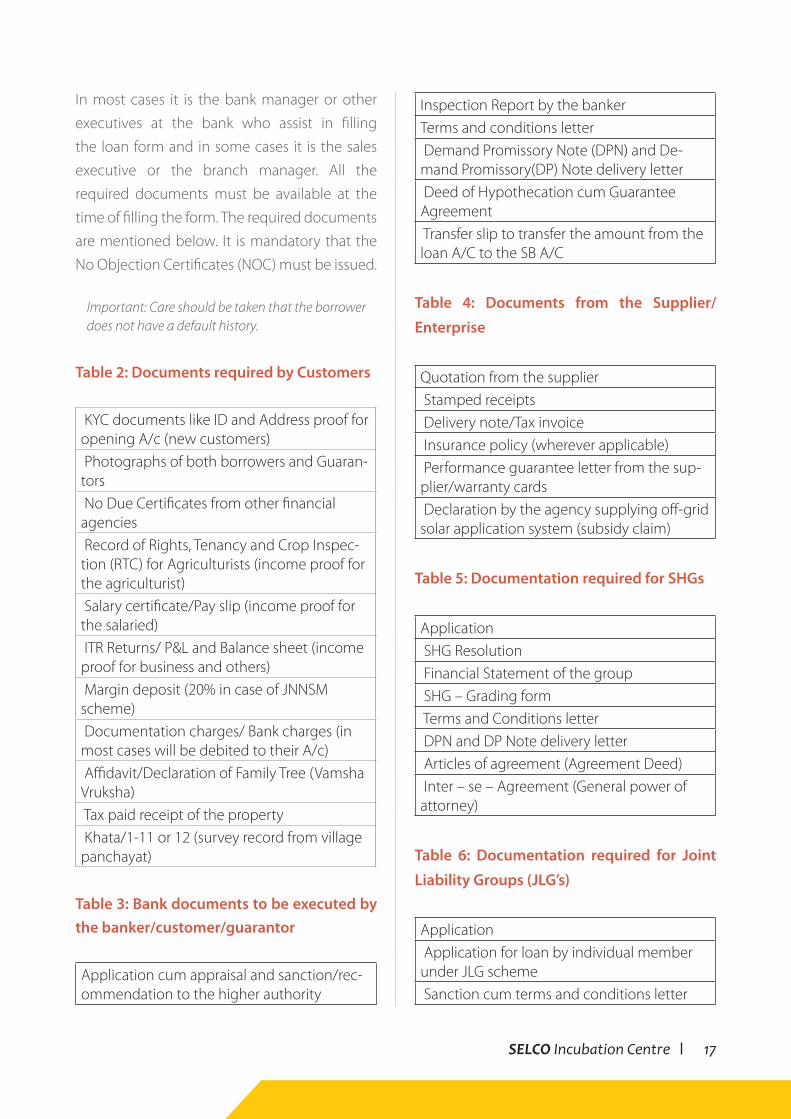

Table 2: Documents required by Customers ........................ 17

Table 3: Bank documents to be executed by the banker/customer/guarantor .................................................................. 17

Table 4: Documents from the Supplier/ Enterprise .......... 17

Table 5: Documentation required for SHGs .......................... 17

Table 6: Documentation required for Joint Liability Groups (JLG’s) ................................................................................. 17

4.8 When does the bank reject financing? .......................... 18

4.9 How can the service provider help the bank in the process of recovery? .................................................................. 18

4.10 Does Government of India provide support? ............ 18

5. Other Financing Mechanisms ................................ 20

5.1 For financial inclusion of extremely poor communities, how can grant amount be utilized? 20

6. Jawaharlal Nehru National Solar Mission (JNNSM) 23

What is the objective of JNNSM? ................................................. 23

What are the mission targets of JNNSM?................................ 23

6.1 Capital Subsidy Scheme .......................................................... 24

6.1.1 What are the objectives of the scheme? ..................... 24

6.1.2 What are Margin Money, Loan Period and Rate of Interest on Loan? ......................................................................... 25

6.1.3 Security & Monitoring ............................................................. 25

6.1.4 MNRE pre approved Models ............................................... 25

6.1.5 What is the process of getting subsidy from the bank? ................................................................................................... 26

7 Annexure................................................................. 27

7.1 Credit Approval Note .................................................................. 27

7.2 Claim Form ....................................................................................... 28

7.3 Capital Subsidy Form ................................................................. 31

7.4 Frequently Asked Questions ................................................. 33

8. Conclusion .............................................................. 35

9. Bibliography ........................................................... 36

2. INTRODUCTION

It is widely accepted that solar photovoltaic technology is the most promising solution to the energy crisis the world is facing today. But this technology has to reach the end user in a way that is most beneficial; otherwise there is a great danger of the technology being rejected by the public. Already in many places, where very cheap but low quality renewable energy products are being distributed among rural population, and where products have failed due to lack of service, the technology is being viewed negatively. Nothing can be more detri-mental to society than to be led to believe that renewable energy technology is worthless. The right way forward is to ensure that people are made aware of the benefits of renewable en-ergy, and the best way possible to access and use it in their daily lives. The method suggested here may require more time and effort on the part of the suppliers of renewable energy, but this is necessary to encourage people to switch to using renewable energy.

• First, foreachcustomersegmentthat istar-geted, all the current activities that use en-ergy, and the expenditure currently incurred for the same should be analyzed

• Next, itshouldbestudied if thereareotheractivities of this customer segment where energy access can improve their lives signifi-cantly

• Based on this, different technical solutionsshould be designed and the lifetime cost of each of these solutions should be studied. Lifetime cost and not initial cost should be

evaluated. Lifetime cost also includes service costs

• Oncethis isknown, itshouldbechecked ifthe solution with least lifetime cost is afford-able by the customer

• Ifitisnot,themostsuitabletypeoffinanciallinkage that would make the expense in-curred worthwhile for the customer should be worked out

• If thesolutionwith least lifetimecostdoesnot seem feasible from the customer view-point in near future, then the next solution should be considered

This is the normal approach when solutions are provided in cities and other well-served towns. But in remote and under-served regions, the tendency is to distribute the cheapest products without any effort being put in to study the best and sustainable solution, often for fear of the ef-fort not being profitable. One of the key factors that can bring about a change in this mindset is to learn about the different options of financial linkages available or that can be created in re-mote and under-served areas.

SELCO has, by utilizing financial linkages avail-able in Karnataka, run as a commercial entity with social objectives very sustainably since 1995. This manual, which has used the exten-sive experience of SELCO, aims to help all the parties concerned, the system provider, end user and the finance provider to understand and utilize financial linkages to bring light and power to energy deprived areas of the country.

SELCO Incubation Centre 7

3. SOLAR FINANCING: STRUCTURE AND DESIGN

3.1 How do we determine if the customer needs financing?

First, the best suited solution should be

identified for energy needs of a customer. If

the initial cost of this solution is not affordable

upfront by the customer, then financing can be

considered as a suitable alternative. The money

the family/household spends currently on fuel/

energy source can be diverted towards repaying

the loan.

For example, a rural household spending

Rs.150/- per month on kerosene for lighting

can avail of a loan to install a bright 2 light solar

system. The loan can be repaid fully within a

5 year period with monthly instalments of

Rs.150/-, an amount that it was spending for

kerosene. The system if properly serviced

has an average life of 7 to 8 years. An interim

replacement of the battery will add another 7

to 8 years of life. In addition, if the solar light

can support their livelihood activity for more

hours after dusk (extends the working hours of

their shop, weaving, handicraft making, etc), the

extra income will contribute amply towards the

repayment amount.

3.2 How do we determine if the customer can afford the equipment even if financed?

Affordability is determined based on the existing

income and expenditure of the household. The

expenditure on the existing source of fuel/light

is calculated and diverted towards paying for the

solar apparatus. For example, a household with

a monthly income of Rs. 5000 may be spending

Rs. 150 per month on kerosene for lighting.

The cost of the solar product is approximately

Rs. 7000 with no monthly expenditure. This

household can easily buy the product as well

as save Rs.150 per month that it was spending

on kerosene. Savings which can be made by

switching to solar as a mode of power supply

should also be kept in mind. This forms the basis

for calculating the affordability for the customer.

3.3 How should financing be designed for the customer?

Financing should be designed based on the cash

flow of the customer to significantly improve

the affordability of the product. For example,

a farmer growing a crop such as sugarcane

receives income once every six months. A

loan demanding monthly repayment can be

extremely inconvenient for him. However, the

same farmer can pay a six monthly instalment

as it matches with his cash flow.

Institutional finance for the consumer has

multiple benefits as well.

Financing Solar Home Lighting Systems (SHLS)

is a relatively new area for commercial banks,

Regional Rural Banks, and cooperatives. The

technical feasibility of SHLS has been established

beyond doubt. Photovoltaic (PV) lighting can

provide the user/customer with several benefits

such as financial, health, and convenience, if the

fairly large up-front capital cost can be financed

with reasonable and affordable terms. Financing

PV systems is more or less the same as financing

any other project/product. Each bank may have

its own specific guidelines on various aspects of

financing SHLS.

3.4 Financing Institutions

It is a myth that the financial assistance to poor

should always be in the form of subsidy or grant.

All the sustainable financial linkages available in

the country can also be utilized productively by

the poor, if a little effort is put in to implement

small innovations to overcome hindrances. Let

us try to understand different financial linkages

available.

1. Banks / Regional Rural Banks (RRB)

2. Microfinance Institutions

3. Co-Operatives

4. Private financing modes (Chit funds, Marup,

Hundi etc)

5. Company self-financing (e.g. Pre paid model)

6. Intermediate entrepreneur model (e.g.

Hawker rental model)

7. Grant used as rolling fund or as margin

money support for loans

Out of the above mentioned options, Regional

Rural Banks (RRBs) are the best suited and most

reliable financial linkage in remote regions.

Hence banks will be discussed in the following

chapters. However brief explanation of other

options will also be found in the manual.

SELCO Incubation Centre 9

have matured into institutions that are largely

responsible for the financial inclusion objective

of the nation. RRBs are truly the last- mile bank

connectivity for end consumer financing.

SELCO’s objective of addressing energy needs

of the poor in the rural districts of India meant

that facilitation of financing had to be created

through the RRBs. RRBs are jointly owned by

Government of India, the concerned State

Government and a sponsor bank (which is a

scheduled commercial bank).

4.1 History of Banks in India and their Role

Since the late 18th century, banks have aided

the growth of commerce and economic activity

in India. It is imperative for any business activity

to have its financing needs fulfilled through

banking institutions. Banking institutions also

help the consumer by offering various options

of financing their needs. However, in all such

transactions it is vital for the bank to see it as

a profitable transaction that contributes to its

bottom-line.

The upfront high capital cost for solar

technology makes it essential that a financing

mechanism exists for consumers. However,

when SELCO started to advocate it in 1995, it

was almost unheard of. Further, the customer

segment SELCO wanted to focus on had almost

no exposure to banking and neither had the

banks dealt with this segment. However, this

equation has changed for the better today,

as a result of SELCO helping to create a loan

portfolio for under-served communities to avail

solar home lighting systems.

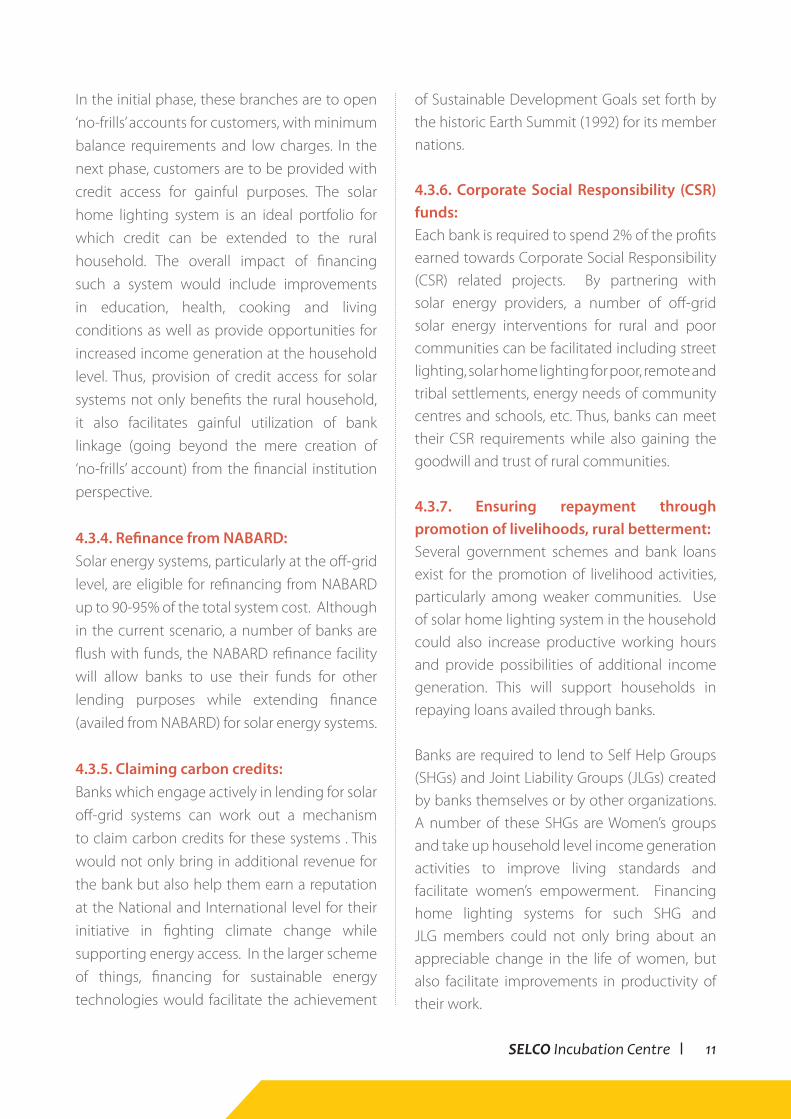

The illustration on this page explains the various

types of banks in India. Due to the customer

segment that SELCO has chosen to focus on,

the majority of transactions rely on the regional

rural banks (RRBs). RRBs were established with

the objective to ensure sufficient institutional

credit for agriculture and other rural sectors. They

Structure of the organised banking sector in India. Number of banks are in brackets

Image Courtesy: Wikipedia Commons* As on April 2013

RESERVE BANK OF INDIACentral bank and supreme monetary authority

SCHEDULED BANKS

Commerical banks

Foreign banks

(40)

Reginal rural banks

(64)*

Urbanco-opeative

(52)

Old (22)

State Cooperatives

(16)

New (8)

Public sector banks (27)

State bank of Indiaand associate banks (8)

Other nationalised banks(19)

Privatesector banks (30)

Co-operative

4. BANKS

4.2 Banks and Solar financing

It is vital to establish the crucial link between

economic activity and introduction of solar

lighting in a rural household. Only then will

a bank see it as a commercial success. It took

considerable efforts on the part of SELCO

to convince the erstwhile Syndicate Bank

sponsored – Mallaprabha Grameen Bank

headquartered in Dharwad to grant the first solar

loan in 1996. Ever since then SELCO has strived

to prove the credible link between livelihood

impact and availability of a reliable and healthy

source of lighting in a rural household.

We have another shining example of how

banks have made a significant contribution

to the local village economy by introducing

solar lighting in Aryavart Gramin Bank based

in Lucknow. In 2008 the RRB, based in one of

the most backward states of India, won the

prestigious Ashden Award, also known as the

Green Oscars for financing nearly 28,000 solar

systems by 2009. To quote Aryavart Gramin Bank

– Solar home systems have enabled people to

work in the evenings and earn more, which is

particularly useful to women. The main cottage

industry in the area is fine embroidery (Chikan

work), for which bright light is a real boon. One

family of nine female tailors and embroiderers

has seen their earnings increase by about Rs 450

per month each as a result of the PV lighting.

The bank organizes credit camps across its

operation areas where they demystify solar

technology and make financing available on

the spot for the systems. The bank found that

customers of other banks turned up for the

camps in the hope of getting a solar loan, and

this eventually led to Aryavart becoming their

banker for all their other needs.

4.3 Benefits accruing to banks from lending

for Solar home lighting system

4.3.1. Categorized under Priority Sector

lending:

Solar home lighting systems and other off-grid

systems have been included under Priority

sector lending based on guidelines by the

Reserve Bank of India. The banks can extend

financing as part of meeting their 40% priority

sector lending targets.

4.3.2. Differential Rate of Interest (DRI)

scheme targets:

As per guidelines of the Reserve Bank of India,

a differential rate of interest of 4% is applicable

on loans up to Rs. 15000, extended by banks to

weaker communities whose household income

does not exceed Rs. 18000 (in rural areas) and

Rs. 24000 (in urban and semi urban areas) per

annum. The loan is extended for any gainful

utilization.

Priority sector lending guidelines provide for

sub targets to ensure that every bank lends

at least 1% of its total advances towards the

DRI scheme . Lending for solar home lighting

systems to poorer households and weaker

communities can help an individual bank meet

its DRI targets.

4.3.3. Credit access under financial inclusion:

The existing policy for annual bank expansion

mandates that all Regional Rural Banks and

Commercial banks must establish at least 25%

of their new branches in unbanked rural areas .

These branches are meant to improve banking

penetration and accelerate financial inclusion by

catering to poor and middle class households in

rural areas.

SELCO Incubation Centre 11

In the initial phase, these branches are to open

‘no-frills’ accounts for customers, with minimum

balance requirements and low charges. In the

next phase, customers are to be provided with

credit access for gainful purposes. The solar

home lighting system is an ideal portfolio for

which credit can be extended to the rural

household. The overall impact of financing

such a system would include improvements

in education, health, cooking and living

conditions as well as provide opportunities for

increased income generation at the household

level. Thus, provision of credit access for solar

systems not only benefits the rural household,

it also facilitates gainful utilization of bank

linkage (going beyond the mere creation of

‘no-frills’ account) from the financial institution

perspective.

4.3.4. Refinance from NABARD:

Solar energy systems, particularly at the off-grid

level, are eligible for refinancing from NABARD

up to 90-95% of the total system cost. Although

in the current scenario, a number of banks are

flush with funds, the NABARD refinance facility

will allow banks to use their funds for other

lending purposes while extending finance

(availed from NABARD) for solar energy systems.

4.3.5. Claiming carbon credits:

Banks which engage actively in lending for solar

off-grid systems can work out a mechanism

to claim carbon credits for these systems . This

would not only bring in additional revenue for

the bank but also help them earn a reputation

at the National and International level for their

initiative in fighting climate change while

supporting energy access. In the larger scheme

of things, financing for sustainable energy

technologies would facilitate the achievement

of Sustainable Development Goals set forth by

the historic Earth Summit (1992) for its member

nations.

4.3.6. Corporate Social Responsibility (CSR) funds: Each bank is required to spend 2% of the profits

earned towards Corporate Social Responsibility

(CSR) related projects. By partnering with

solar energy providers, a number of off-grid

solar energy interventions for rural and poor

communities can be facilitated including street

lighting, solar home lighting for poor, remote and

tribal settlements, energy needs of community

centres and schools, etc. Thus, banks can meet

their CSR requirements while also gaining the

goodwill and trust of rural communities.

4.3.7. Ensuring repayment through promotion of livelihoods, rural betterment:Several government schemes and bank loans

exist for the promotion of livelihood activities,

particularly among weaker communities. Use

of solar home lighting system in the household

could also increase productive working hours

and provide possibilities of additional income

generation. This will support households in

repaying loans availed through banks.

Banks are required to lend to Self Help Groups

(SHGs) and Joint Liability Groups (JLGs) created

by banks themselves or by other organizations.

A number of these SHGs are Women’s groups

and take up household level income generation

activities to improve living standards and

facilitate women’s empowerment. Financing

home lighting systems for such SHG and

JLG members could not only bring about an

appreciable change in the life of women, but

also facilitate improvements in productivity of

their work.

Finally, RRBs and Commercial banks in different

areas take up village adoption programmes for

all round development of villages including

financial, social and educational activities.

Solar energy financing could support in this

development process by meeting the much

needed energy requirements at the village level.

Thus, financing for solar energy systems for

various developmental products and services

including lighting, productive use, mobile

charging, educational aids, etc. help the banks

in meeting their rural development agenda,

while also ensuring improvements in customer

incomes that would help them regularly repay

loans.

4.4 Who is eligible for Financing?

The eligibility criteria for financing are:

4.4.1. Individuals such as farmers, traders, professionals, businessmen, salaried persons including employees of the bank, artisans, craftsmen, daily wage earners, etc.

4.4.2. Organisations such as firms, companies, institutions, associations.

4.4.3. Individuals who have a source of income adequate enough to repay the loan with interest as stipulated by the bank

4.4.4. Individuals who are residents in the service area or the command area of the bank. (He/she need not be a permanent resident/domicile of that area especially in case of salaried persons.)

4.4. 5. An existing customer whose past dealings have been satisfactory.

4.5 What are the pre-requisites, conditions and requirements for granting the loan?

4.5.1. Loan Proposal

The loan application should be submitted

by the applicant in the form prescribed by

the bank. The applicant shall furnish all the

necessary information as required by the bank.

The enterprise team will help the customer in

furnishing the details. In addition, the following

requirements should be obtained depending

on the category of the applicant:

• Recordof Right (ROR) or village accountant’s certificate or Adangal or Chitta or Pahani or 10-1 extract or Patta book furnishing of land holding in case of farmers and agriculture.

• Copy of the Patta/Khatha or possessioncertificate issued by the Town Panchayat, Municipality or City Corporation in case of urban or metropolitan areas furnishing details of house property.

• Copy of the rent agreement or any otherproof of residence like the family ration card.

• Latest land revenue/Municipal Tax/ Housetax paid receipt.

• Proofoftenancyincasetheapplicantisthetenant occupant of the house.

• Tworecentpassportsizephotographsoftheapplicant.

• Proforma invoice/quotation from themanufacturer /supplier of the SHLS for the cost of the system including the accessories and the installation.

• Copyofthetest report issuedbytheSolarEnergy Centre or Authorised Test Centre.

• The applicant shall also submit originaltitle deeds of the property, encumbrance certificate, legal opinion, property valuation certificate, and other supporting documents whenever the loan is required to be secured by mortgage.

SELCO Incubation Centre 13

• In case of corporate clients and firms,audited financial statements for the last three years, partnership deed, memorandum of understanding, articles of associations, board resolution to borrow, etc.

• Income Tax assessment order or the copyof the return filled with the ITO (wherever applicable).

4.5.2. Appraisal of the ProposalOn receipt of the loan proposal for financing

SHLS along with the requirements, the Branch

Manager or any other officer designated by

him should undertake a pre-sanctioned spot inspection of the location/site where the

SHLS is to be installed. The proposal should be

thoroughly discussed with the applicant.

The proposal should be appraised taking into

consideration the technical, financial, economic,

commercial, managerial and legal aspects to

determine the technical feasibility, financial

viability and overall bankability of the proposal.

The repaying capacity of the borrower should

be carefully assessed.

4.5.3. Technical AspectsThe financing bank should get from the

manufacturer or his authorised dealer a copy

of the test report issued by the Solar Energy Centre (SEC)/Other Authorised Text Centre

(OATC) certifying that the SHLS being supplied

to the applicant conforms to the specifications

prescribed by the Ministry of New and

Renewable Energy (MNRE), Government of

India. In addition, the financing bank should

ensure that there is a minimum warranty of five years for the complete system including

battery (every component except the compact

fluorescent light or bulb), and a minimum

warranty of 10 years for the PV module. All

Warranties should commence from the date of

installation.

The bank should also ensure that the

manufacturer/ dealer of the systems offers

Annual Maintenance Contract (AMC) covering

supply of spares (excluding batteries) and

service for a minimum of five years mandatory

warranty period to ensure satisfactory operation

of the system on a sustainable basis. The terms of

the AMC should be agreed upon by the system

supplier and the end user on a reasonable basis.

The exact requirement and the design of the

SHLS should be determined by the end user in

discussion with the manufacturer/authorised

dealer.

4.5.4. Legal AspectsLegal problems if any, especially in installing the

system and, in case of finance for larger systems

should be looked into. Legal compliance with

respect to factors such as collateral security

must be ensured.

4.5.5. Repayment CapacityFirst, the product itself needs to be designed

such that the system cost when converted into

a loan or instalment, makes it affordable and

provides maximum benefit (or payback) within

the repayment period. This has to be true even

in the absence of subsidy. Commercial banks

stipulate that the loan for SHLS be repaid within

a stipulated period. The bank has to adopt a

“Holistic Approach” taking into consideration

the entire family income and expenditure of

the borrower. The bank has to be satisfied

about the repaying capacity of the borrower

who may be relying on other viable and known

sources of income as is being done in the case

of Personnel Banking or Consumer Durable Loans.

4.5.6. Sanctioning AuthorityAfter the credit proposal is thoroughly

appraised and its bankability is established,

the Bank Manager sanctions the proposal

with the terms and conditions if any. In other

cases, the proposal, along with the Branch

Manager’s recommendation is sent to higher

authorities for credit decision. Once the loan

is sanctioned, the manufacturer/ supplier who

gave the quotation/ proforma invoice should

be informed of the same, and asked to supply

the SHLS to the applicant. He should also be

told that the bank will remit the cost of the

SHLS to him upon its satisfactory installation

and confirmation of the same by the customer.

4.5.7. Documentation & DisbursementUpon fulfilment of the terms and conditions,

the loan is arranged by obtaining the loan

documents executed by the borrower and the

surety (wherever applicable). Depending on the

quantum of loan and its category, hypothecation

of the SHLS unit is obtained. Wherever required,

collateral like mortgage of land, building etc.

or pledge of NSC, KVP or assignment of LIP

etc. can be obtained. The loan amount along

with the margin contribution (generally held

in account of the borrower) shall be released to

the manufacturer or supplier upon a satisfactory

report of installation of the SHLS confirmed by

the borrower.

Note: The original invoice and stamped receipt must be obtained from the manufacturer/ dealer.

4.5.8. Rate of InterestThe RBI directives govern the interest rate on

SELCO Incubation Centre 15

loans up to Rs. 2 lakhs for priority sectors. The

interest rate on SHLS loans are eligible to be

classified under Priority Sector and should not

exceed the Prime Term Lending Rate (PTLR)

of the bank. In case the loan exceeds Rs. 2

lakhs under Priority Sector or where the SHLS

loan is outside the purview of Priority Sector,

the interest rate depends on the policy of the

lending bank. Penal interest at 2% above the

normal rate may be levied for overdue loans

where the loan amount exceeds Rs. 25,000 in

case of Priority Sector and Rs.5000 in case of

Non Priority Sector.

4.5.9. Service ChargesOne time processing and other charges are

normally at 0.1% to 0.25% of the loan amount

at the time of arranging the loan. The rate of

service charges varies from bank to bank, and

should be applied as per the bank’s guidelines.

4.5.10. Security• Hypothecation of the asset created out of

the loan is the SHLS

• Creation of charge on the property or

mortgage of immovable property as

collateral security wherever required

(normally when the loan amount exceeds Rs.

25,000)

• Collateralsuchas NSC, KVP, LIP of adequate

value are also acceptable.

4.5.11. Surety / GuarantorA credit worthy party (preferably third party) may

join as the loan transaction Surety / Guarantor.

4.5.12. RepaymentThe loan is to be repaid in monthly/ quarterly/

half yearly / yearly instalments over a period of

five years depending on the source of income

of the borrower. Interest, however, shall be paid

quarterly or as and when debited to the loan

account.

Note: Initial moratorium of three months from the date of loan may be given for repayment whenever found necessary.

4.5.13. ClassificationThe loan facility for SHLS is generally extended in

the form of a Term Loan. As per RBI regulations,

loans extended for SHLS or any other solar

appliance shall be classified depending on the

occupation or vocation of the borrower. For

instance an SHLS loan extended to a farmer

should be classified as an agricultural advance.

The SHLS loan extended to retail trade shall be

classified as a retail trade loan under priority

sector. A loan granted to a salaried person for

SHLS shall be classified as a non priority sector

advance.

Note: Classification of advance has a direct bearing on the interest rate charged.

4.6. Borrower Assessment - Checkpoints

This section of the manual is designed to

instruct the Bank officials on the methods

to be adopted for financing the installation

of SHLS, typically including a PV module and

appropriate balance-of-system components

necessary to provide reliable, safe, and

affordable electricity from sunlight for domestic

and other similar usage. The SHLS includes a

module, battery, charge controller and a set

of compact fluorescent lights. Larger systems

may also include an inverter (to convert the

DC electricity generated by the PV modules to

AC) and connections for televisions, radios, and

other domestic electrical appliances.

To frame a proposal quickly, bankers and

promoters must meet and discuss. The

assessment standards will vary from person

to person, depending upon the size of the

loan, experience of the banker, dealings of the

borrower and so on. The following brief should

help the banker to prepare the loan proposal

efficiently:

Table 1: Check points for assessing the customer

The background of the promoter/beneficiary/

entrepreneur must also include the following

details –

- Who is the borrower?

- What business is he doing?

- Is he a customer of the bank?

- If he is not, which bank has he been dealing

with so far?

- Why did he not approach that bank for credit

requirements?

- If he is a customer of the bank, then has he

borrowed from it in the past? What is his

track record?

- In case of a new borrower / promoter, the

banker may wish to collect further details.

The banker may prefer to meet the promoter/

borrower directly and not through any

agency or third person. Such a meeting

provides an opportunity to collect first hand

information for discussion. It also helps the

banker to check the various statements and

figures furnished in the proposal/ application.

It must be seen whether the cost estimates

are reasonable as per the standard rates, and

whether any capital and/or interest subsidy is

available.

The time required to install and energize

the equipment is to be specified clearly and

correctly.

All documents required by the banker are to be

submitted along with the application.

The availability of after-sales services must

be ensured. There should be arrangement to

provide spares in case of defective materials

supplied or for replacement, whenever required.

Initial payment holiday should be specific and

fixing of the instalments (whether monthly,

quarterly, half yearly, etc.) must be done

considering the source of income.

The following aspects must also be looked into

- What is the amount of loan required?

- What will the loan mean to the borrower

from the profit point of view?

- When and how will the loan be repaid?

- Where will the funds come from for repaying

the loan?

- Will the SHLS help the borrower to reduce

expenditure and increase savings to repay

the loan?

- Does the borrower have a basic idea about

the possible amount of net savings/ profit

after the installation?

- How will the borrower bring in the required

margin money?

- Does the borrower have the necessary

technical skill to handle the PV system and its

maintenance or does he need any training?

- Has he properly assessed the special features

such as number of lights required etc.?

4.7 What are the Dos and Don’ts while filling the form for a loan?

SELCO Incubation Centre 17

In most cases it is the bank manager or other

executives at the bank who assist in filling

the loan form and in some cases it is the sales

executive or the branch manager. All the

required documents must be available at the

time of filling the form. The required documents

are mentioned below. It is mandatory that the

No Objection Certificates (NOC) must be issued.

Important: Care should be taken that the borrower does not have a default history.

Table 2: Documents required by Customers

KYC documents like ID and Address proof for opening A/c (new customers)

Photographs of both borrowers and Guaran-tors

No Due Certificates from other financial agencies

Record of Rights, Tenancy and Crop Inspec-tion (RTC) for Agriculturists (income proof for the agriculturist)

Salary certificate/Pay slip (income proof for the salaried)

ITR Returns/ P&L and Balance sheet (income proof for business and others)

Margin deposit (20% in case of JNNSM scheme)

Documentation charges/ Bank charges (in most cases will be debited to their A/c)

Affidavit/Declaration of Family Tree (Vamsha Vruksha)

Tax paid receipt of the property

Khata/1-11 or 12 (survey record from village panchayat)

Table 3: Bank documents to be executed by

the banker/customer/guarantor

Application cum appraisal and sanction/rec-ommendation to the higher authority

Inspection Report by the banker

Terms and conditions letter

Demand Promissory Note (DPN) and De-mand Promissory(DP) Note delivery letter

Deed of Hypothecation cum Guarantee Agreement

Transfer slip to transfer the amount from the loan A/C to the SB A/C

Table 4: Documents from the Supplier/

Enterprise

Quotation from the supplier

Stamped receipts

Delivery note/Tax invoice

Insurance policy (wherever applicable)

Performance guarantee letter from the sup-plier/warranty cards

Declaration by the agency supplying off-grid solar application system (subsidy claim)

Table 5: Documentation required for SHGs

Application

SHG Resolution

Financial Statement of the group

SHG – Grading form

Terms and Conditions letter

DPN and DP Note delivery letter

Articles of agreement (Agreement Deed)

Inter – se – Agreement (General power of attorney)

Table 6: Documentation required for Joint

Liability Groups (JLG’s)

Application

Application for loan by individual member under JLG scheme

Sanction cum terms and conditions letter

Letter of Undertaking (to be obtained from each member of JLG as borrower with other

members as guarantors)

Inter – se – Agreement (executed by the members of JLG)

Mutual Agreement (to be stamped as an agreement)

DPN and DP Note delivery letter from each member

4.8 When does the bank reject financing?

• Theborrowerisadefaulter

• Theborrowerisnotbankable.Itmeansthat

he has no regular source of income or he is

not in a position to pay back the loan

• Theborrowerdoesnothavepropersecurity.

In case he owns assets, he may not have

proper records of them

• Thebankalsousesacreditworthiness form

to assess in detail if the customer is worthy of

loan

• Thebankattimesmaynothaveavalidreason

while rejecting the loan; the sales executive

must have the patience to find out why the

loan is rejected and help the borrower in

obtaining the loan or find another source of

funding

4.9 How can the service provider help the bank in the process of recovery?

The key to ensure smooth finance tenure for

both the beneficiary as well as the banker is to

have a good operational solar home lighting

system. This can only happen by ensuring

regular service or a mechanism by which the

customer can reach the service provider for

any help in case of a breakdown. At any point

when there is no service the system is rendered

useless, and automatically the customer sees no

point in continuing to repay the loan.

The other factor is to educate the terms of

financing in a clear medium to the customer.

The customer should have no ambiguity about

– total cost of the system, down payment, loan

term, interest rate, instalment frequency and

amount and the mechanism to repay as well as

familiarity with the bank staff. All this will result

in a good standing relationship for all the three

parties – beneficiary, bank as well as the service

provider.

In the event of any unforeseen circumstance

of the beneficiary defaulting on repayment,

the service provider must assist the bank in the

recovery process. Although as a commercial

transaction the service provider is not liable

to get involved in the recovery mechanism it

helps build a long standing relationship with

the financing institution in the process. The

service provider may make a courtesy visit to

the customer’s place to enquire the reason for

non-payment and the need for any assistance

in this matter.

Banks generally have a monitoring team whose

assistance is sought for any loan recovery. The

service provider should co-operate with this

team, if requested for any assistance.

4.10 Does Government of India provide support?

Government of India announces various support

schemes to popularize the usage of renewable

energy. Most of the times, banks are involved

in the process of disbursing monetary support

to the beneficiaries. From time to time, the

SELCO Incubation Centre 19

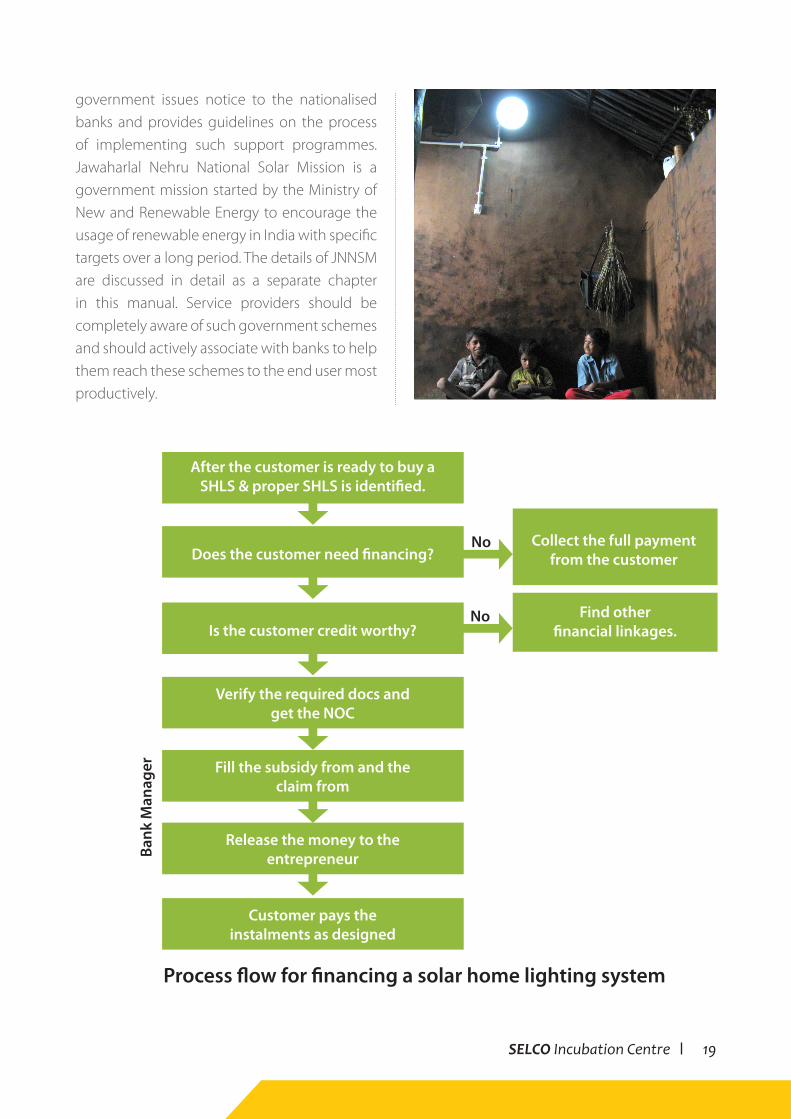

After the customer is ready to buy a SHLS & proper SHLS is identified.

Collect the full payment from the customer

No

No

Ban

k M

anag

er

Find other financial linkages.

Does the customer need financing?

Is the customer credit worthy?

Verify the required docs and get the NOC

Fill the subsidy from and the claim from

Release the money to the entrepreneur

Customer pays the instalments as designed

Process flow for financing a solar home lighting system

government issues notice to the nationalised

banks and provides guidelines on the process

of implementing such support programmes.

Jawaharlal Nehru National Solar Mission is a

government mission started by the Ministry of

New and Renewable Energy to encourage the

usage of renewable energy in India with specific

targets over a long period. The details of JNNSM

are discussed in detail as a separate chapter

in this manual. Service providers should be

completely aware of such government schemes

and should actively associate with banks to help

them reach these schemes to the end user most

productively.

Despite best efforts we have seen a number

of instances where end user financing has not

been possible through the banking channels

mentioned above. This can happen for a variety

of reasons including:

• Perceivedriskprofileofthecustomer

• Lackoforinsufficientessentialidentityproof

documents

• Nobanksoperatinginthecustomer’svicinity

In such cases where financing through banking

channels is not possible, some other financing

options can be considered. These are listed

below:

• Micro Finance Institutions (MFI): These

provide financial services to micro-

entrepreneurs, small businesses or to self-

help groups. They usually operate in areas

which lack access to banking due to high

transaction costs associated in servicing these

locations, or the risks associated with them.

The concept of microfinance institutions

was pioneered by Dr. Muhammad Yunus

in Bangaldesh through the Grameen Bank.

MFIs rely on the strength of group dynamics

to ensure the repayment capacity as well as

transaction costs.

• Private forms of finance – Chit funds,Hundis, Maroop: Each region has its own

form of savings scheme and are known by

various names across India chit, chit fund,

chitty, kuri or maroop (popular in Manipur).

They all represent an agreement with a

specified number of persons, who will each

subscribe a fixed amount each month over

a definite period. In return, each subscriber

is entitled to a prize amount which is

determined by an auction, lottery or a tender.

• Company self-financing through pre-paid payment options: A few companies

like Simpa have introduced a “pay-as-you-go”

pricing to household energy systems. Users

pre-pay based on actual usage and each

payment adds up towards the total purchase

price of the solar home system. Consumers

can send payments using a mobile phone.

Once fully paid, the solar home system

unlocks and delivers free electricity for the

expected 10-year life of the product.

5.1 For financial inclusion of extremely poor communities, how can grant amount be utilized?

SELCO business model has always been

about establishing strong innovative linkages

between end users, energy services, technology

and financing. SELCO views a product as a

combination of technology and finance and

hence uses a 2 pronged approach of door-step

service and door-step financing. It has been

5. OTHER FINANCING MECHANISMS

SELCO Incubation Centre 21

able to assess the end user needs and create a solution that best fits his/her need. This need can be technical, financial or a simple process innovation that could empower the lives of under-served or un-served households and small scale businesses. The key features of the model are:

i) Creating products based on end user needs - thus going beyond the role of just being a technology supplier to actual customizing the products to suit individual needs, along with dedicated installation and after sales services from well established energy service centre network.

ii) Flexible financial packages to suit the end users affordability and cash flow.

These approaches are further innovated under Mission Projects for effectively reaching out to those poorer sections that are generally never a part of the mainstream financing. In order to create the first time bridges to the financial institutions, Mission Projects uses several innovative mechanisms to facilitate linkages.

• Risk Guarantee – SELCO shares the risk of repayment with the financial institution by providing Buy Back Letters upon default or by opening Security Deposits to serve as collateral against the borrowed loan amount.

• Margin Money Financing - In order to enable the loans, the end users need to contribute certain percentage of the loan amount as down payment. In case of Mission projects, SELCO bears the costs towards this down payment by contributing the Margin money and ensures that loans are enabled.

• Interest Subsidy – In another mechanism, SELCO contributes towards waiver of certain

percentage of interest rate.

• Partial Contribution – Many a times, in

partnership with other organizations or

under any particular welfare schemes by

Government departments, SELCO directly

contributes a certain percent of the total cost

of the product.

• Smart Subsidies on Product Pricing – The

product prices are subsidized by providing

appropriate discounts and waivers for the

benefit of the end user.

• Products / Services Innovation – In certain

special cases, certain technical/ services

innovations are brought into the regular

systems in order to bring down the cost of

the product and make it affordable to the

end user.

• High Risk Projects – These are undertaken

with specific poor segments of the society

where the outcome of the project is

highly unpredictable, e.g. Basket weavers,

Shepherds, Silk reeling etc. A few other R&D

projects are also undertaken whose nature

of outcome is unknown, e.g. micro-energy

entrepreneurs.

As of now, the Mission Project initiative is

funded through the soft monies raised from

a few grants, awards, etc. The future plan is to

evolve into some sort of a sustainable Revolving

Fund structure which can be used for all above

mentioned purposes.

Some Highlights

• Nearly5000un-electrifiedhomeshavebeen

powered with solar lighting systems under

the project

• SELCO is continuously trying to engage

with the Siddi tribes (African tribes) based in

North Karnataka and has been successful in

electrifying 33 Siddi Households in Yellapur,

Uttar Kannada that was financed by KVGB.

• Urban poor- energy-financial linkage

established successfully and replicated

in three slums of Pragatinagar, Manipal;

Beedinagudde, Udupi and Peenya, Bangalore.

• SELCO has worked with the Maldhari

communities in the Rann of Kutchh who live

in completely cut off remote areas without

any access to clean energy and provided 20

lighting systems till date.

• SELCO has taken on the challenge of

financial-energy inclusion for 200 off-grid

non-bankable poor homes in Gulbarga,

Karnataka.

SELCO Incubation Centre 23

6. JAWAHARLAL NEHRU NATIONAL SOLAR MISSION (JNNSM)

The National Action Plan on Climate Change

points out: “India is a tropical country, where

sunshine is available for longer hours per day

and in great intensity. Solar energy, therefore,

has great potential as future energy source.

It also has the advantage of permitting the

decentralized distribution of energy, thereby

empowering people at the grassroots level”.

Based on this vision, a National Solar Mission is

being launched under the brand name “Solar

India”.

The National Solar Mission is a major initiative

of the Ministry of New and Renewable Energy,

Government of India (MNRE1), to promote

ecologically sustainable growth while

addressing India’s energy security challenge.

It will also constitute a major contribution by

India to the global effort to meet the challenges

of climate change.

What is the objective of JNNSM?

The objective of the National Solar Mission

is to establish India as a global leader in solar

energy, by creating the policy conditions for its

widespread usage across the country as quickly

as possible.

What are the mission targets of JNNSM? The mission targets of JNNSM are:

• To create anenablingpolicy framework for

the deployment of 20,000 MW of solar power

by 2022.

• To rampupthecapacityofgrid-connected

solar power generation to 1000 MW within

three years – by 2013; an additional 3000

MW by 2017 through the mandatory use

of the renewable purchase obligation by

utilities backed with a preferential tariff. The

ambitious target for 2022 of 20,000 MW or

more, will be dependent on the ‘learning’

of the first two phases, which if successful,

could lead to conditions of grid-competitive

solar power.

• To promote programmes for off grid

applications, reaching 1000 MW by 2017 and

2000 MW by 2022.

• Toachieve15millionsq.meterssolarthermal

collector area by 2017 and 20 million by 2022.

• Todeploy20millionsolarlightingsystemsin

rural areas by 2022.

Since the nationalization of 14 major commercial

banks in 1969 and 6 more banks in 1980, the

Government’s policy has been clearly directed

towards making these banks play an important

role in promoting rural development. Be it 1http://www.mnre.gov.in/solar-mission/jnnsm/introduction-2/

financing for investments, to increase agricultural

production or promoting small businesses or

industries, transport and communication, the

banks have pumped enormous amount of

money as credit assistance.

PLEASE NOTE: The details of the JNNSM

scheme, particularly the interest rates and

subsidy conditions are subject to revision.

The details mentioned in the book were taken

when the book was being compiled (Nov

2012). Please refer to the MNRE website for

current updates. http://www.mnre.gov.in/

solar-mission

6.1 Capital Subsidy Scheme 2

Capital Subsidy Scheme will be implemented

by NABARD through Regional Rural Banks and

other commercial Banks for Solar Lighting

Systems and Small Capacity PV Systems.

Under this scheme, NABARD will extend the

subsidy of 40% of the benchmark cost which is

Rs.270/- per watt peak subject to a maximum

of Rs. 108/- per watt peak, to the Regional Rural

Banks (RRBs) and other commercial Banks, for

purchase of solar lighting systems and other

small capacity PV systems by individuals. The

RRBs and other Commercial Banks could extend

the loan for the balance cost of the systems at

normal interest rates for the period decided by

the RRBs or the Banks.

While implementing this scheme, NABARD will

follow the minimal technical requirements and

Quality Standards in respect of the off-grid SPV

power plants/systems which are mentioned

in Annexure-3 enclosed with the Ministry’s

Administrative Approval No.5/23/2009-10/P&C

dated 8th July 2010.

6.1.1. What are the objectives of the scheme?

The main objectives of the scheme are to:

- Promote off-grid applications of solar energy

(both PV and Solar Thermal)

- Create a paradigm shift needed for

commoditization of off-grid solar applications

- Encourage replacement of non-renewable

energy sources like fossil fuels, kerosene and

diesel with solar energy to meet the energy

requirements.

6.1.2.What are Margin Money, Loan Period and Rate of Interest on Loan?

The borrowers are required to bring in 20% of

the cost of the project as the margin money for

accessing credit facilities from banks to acquire

the assets. The loans to cover the balance (within

the ceilings specified against each asset) after

reducing the eligible capital subsidy, would

be extended with a repayment period not

exceeding 5 years and would carry an interest

rate which is the regular rate of interest charged

by the bank. There is a minimum period of

3 years where the subsidy is locked. This is a

backend subsidy which helps to keep a track of

the repayment of the loan.

6.1.3.Security & Monitoring

The loans extended under the scheme would

be secured as per the existing RBI guidelines

in this regard. The financing banks will have to

maintain separate records for loans/subsidy

extended under the scheme and the details 2 http://mnre.gov.in/file-manager/UserFiles/bank_subsidy_scheme_jnnsm_st_29022012.pdf

SELCO Incubation Centre 25

3 http://mnre.gov.in/file manager / UserFiles /Revised_Capital_Subsidy_ and_Benchmark_ costofthe _SPV _system.pdf

will have to be submitted to MNRE/NABARD/

IREDA as and when required. MNRE/NABARD/

IREDA will also have the right to inspect the

books of accounts pertaining to such accounts

whenever required.

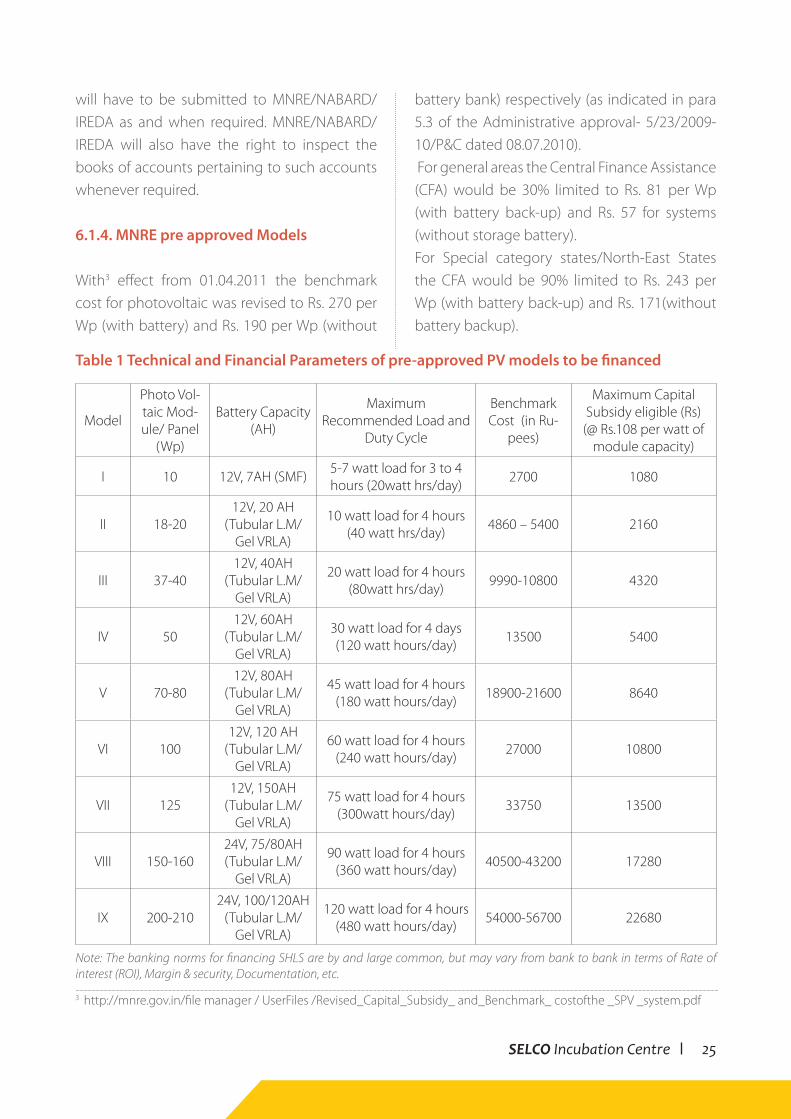

6.1.4. MNRE pre approved Models

With3 effect from 01.04.2011 the benchmark

cost for photovoltaic was revised to Rs. 270 per

Wp (with battery) and Rs. 190 per Wp (without

Note: The banking norms for financing SHLS are by and large common, but may vary from bank to bank in terms of Rate of interest (ROI), Margin & security, Documentation, etc.

battery bank) respectively (as indicated in para

5.3 of the Administrative approval- 5/23/2009-

10/P&C dated 08.07.2010).

For general areas the Central Finance Assistance

(CFA) would be 30% limited to Rs. 81 per Wp

(with battery back-up) and Rs. 57 for systems

(without storage battery).

For Special category states/North-East States

the CFA would be 90% limited to Rs. 243 per

Wp (with battery back-up) and Rs. 171(without

battery backup).

Table 1 Technical and Financial Parameters of pre-approved PV models to be financed

Model

Photo Vol-taic Mod-ule/ Panel

(Wp)

Battery Capacity (AH)

Maximum Recommended Load and

Duty Cycle

Benchmark Cost (in Ru-

pees)

Maximum Capital Subsidy eligible (Rs) (@ Rs.108 per watt of

module capacity)

I 10 12V, 7AH (SMF)5-7 watt load for 3 to 4 hours (20watt hrs/day)

2700 1080

II 18-2012V, 20 AH

(Tubular L.M/ Gel VRLA)

10 watt load for 4 hours (40 watt hrs/day)

4860 – 5400 2160

III 37-4012V, 40AH

(Tubular L.M/ Gel VRLA)

20 watt load for 4 hours (80watt hrs/day)

9990-10800 4320

IV 5012V, 60AH

(Tubular L.M/ Gel VRLA)

30 watt load for 4 days (120 watt hours/day)

13500 5400

V 70-8012V, 80AH

(Tubular L.M/ Gel VRLA)

45 watt load for 4 hours (180 watt hours/day)

18900-21600 8640

VI 10012V, 120 AH

(Tubular L.M/ Gel VRLA)

60 watt load for 4 hours (240 watt hours/day)

27000 10800

VII 12512V, 150AH

(Tubular L.M/ Gel VRLA)

75 watt load for 4 hours (300watt hours/day)

33750 13500

VIII 150-16024V, 75/80AH (Tubular L.M/

Gel VRLA)

90 watt load for 4 hours (360 watt hours/day)

40500-43200 17280

IX 200-21024V, 100/120AH

(Tubular L.M/ Gel VRLA)

120 watt load for 4 hours (480 watt hours/day)

54000-56700 22680

6.1.5. What is the process of getting subsidy from the bank?

Once the customer is identified and the

need for financing is accomplished, the sales

executive gets a formal approval from the bank

manager to finance. A credit approval note4

is authorised, on the basis of which the local

branch will install the system and ensure the

margin money is duly paid.

A subsidy form is filled by the bank. The bank

manager has to certify the Claim Form5 and the

Capital Subsidy form6 which are sent to the

Regional Office (RO) or the Zonal Office (ZO) of the particular RRB. Once it is approved, the

amount is released directly to the organisation

4 Annexure 15 Annexure 26 Annexure 3

SELCO Incubation Centre 27

7. ANNEXURE

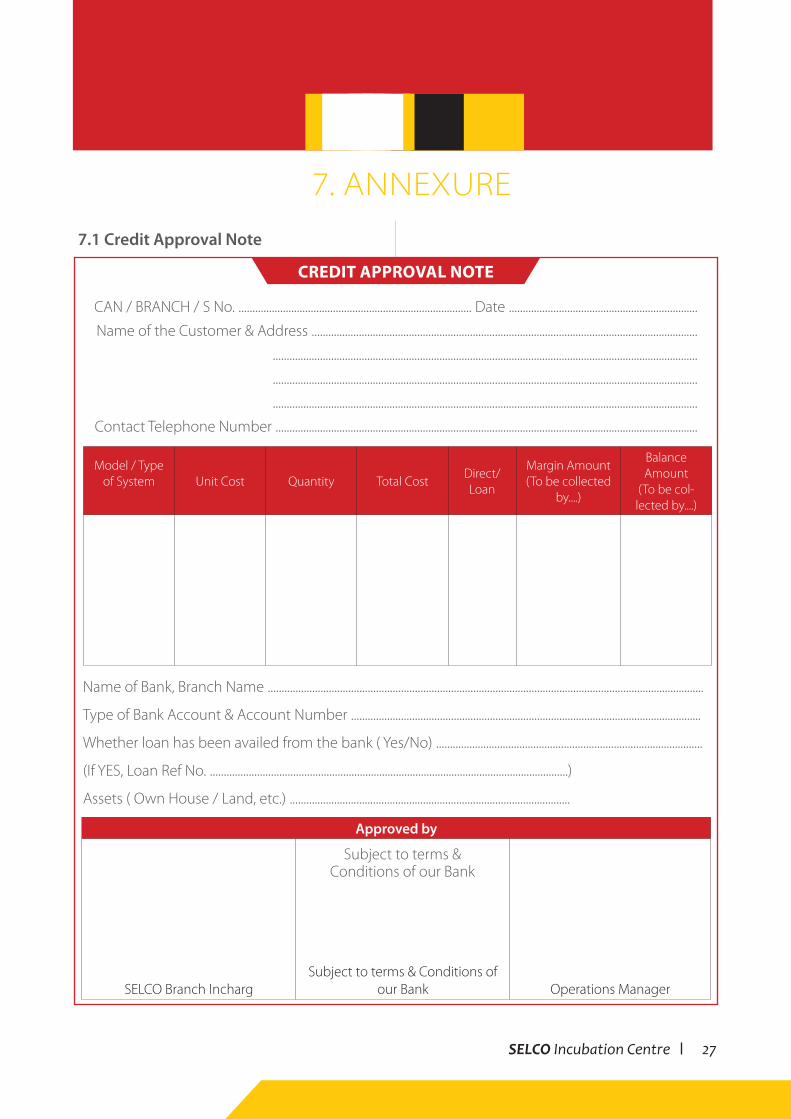

Model / Typeof System Unit Cost Quantity Total Cost

Direct/Loan

Margin Amount (To be collected

by....)

Balance Amount

(To be col-lected by....)

CAN / BRANCH / S No. .................................................................................... Date ....................................................................

Name of the Customer & Address ...........................................................................................................................................

.........................................................................................................................................................

.........................................................................................................................................................

.........................................................................................................................................................

Contact Telephone Number ........................................................................................................................................................

7.1 Credit Approval Note

Name of Bank, Branch Name .............................................................................................................................................................

Type of Bank Account & Account Number ..............................................................................................................................

Whether loan has been availed from the bank ( Yes/No) ................................................................................................

(If YES, Loan Ref No. .................................................................................................................................)

Assets ( Own House / Land, etc.) .....................................................................................................

Approved by

SELCO Branch InchargSubject to terms & Conditions of

our Bank Operations Manager

CREDIT APPROVAL NOTE

Subject to terms & Conditions of our Bank

Loans under JNNSM Scheme of GOI

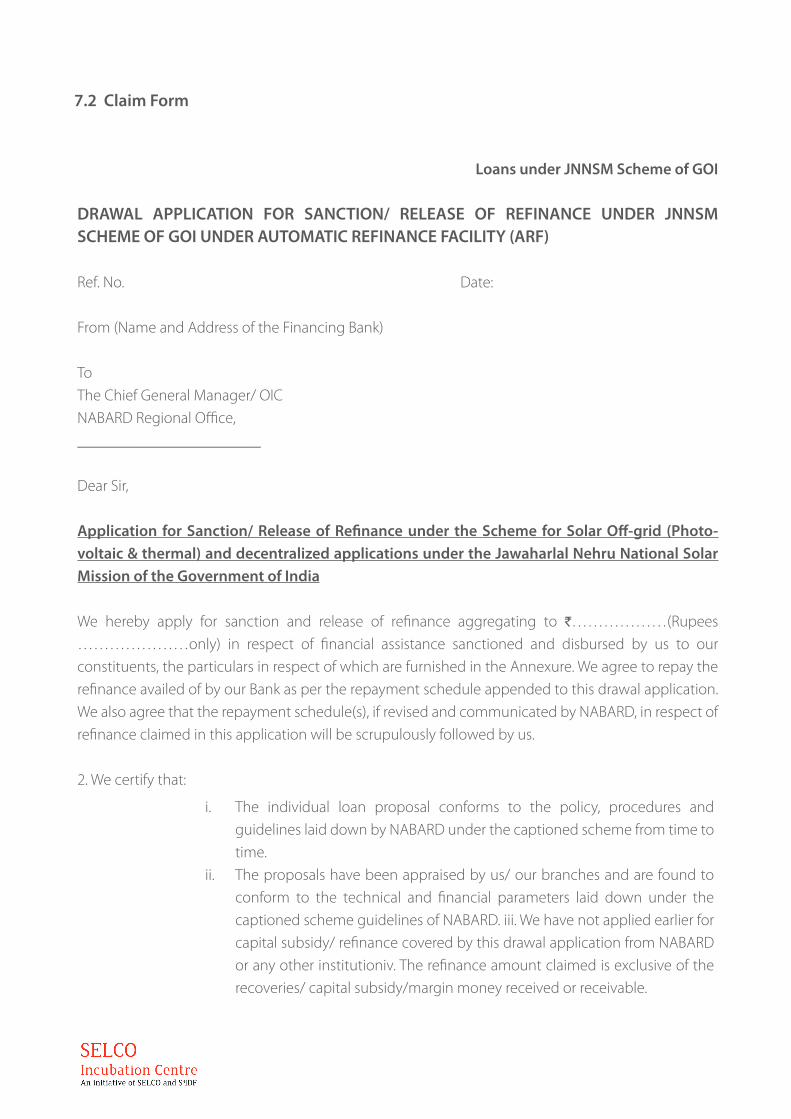

DRAWAL APPLICATION FOR SANCTION/ RELEASE OF REFINANCE UNDER JNNSM SCHEME OF GOI UNDER AUTOMATIC REFINANCE FACILITY (ARF)

Ref. No. Date:

From (Name and Address of the Financing Bank)

To

The Chief General Manager/ OIC

NABARD Regional Office,

_______________________

Dear Sir,

Application for Sanction/ Release of Refinance under the Scheme for Solar Off-grid (Photo-voltaic & thermal) and decentralized applications under the Jawaharlal Nehru National Solar Mission of the Government of India

We hereby apply for sanction and release of refinance aggregating to `………………(Rupees

…………………only) in respect of financial assistance sanctioned and disbursed by us to our

constituents, the particulars in respect of which are furnished in the Annexure. We agree to repay the

refinance availed of by our Bank as per the repayment schedule appended to this drawal application.

We also agree that the repayment schedule(s), if revised and communicated by NABARD, in respect of

refinance claimed in this application will be scrupulously followed by us.

2. We certify that:

i. The individual loan proposal conforms to the policy, procedures and

guidelines laid down by NABARD under the captioned scheme from time to

time.

ii. The proposals have been appraised by us/ our branches and are found to

conform to the technical and financial parameters laid down under the

captioned scheme guidelines of NABARD. iii. We have not applied earlier for

capital subsidy/ refinance covered by this drawal application from NABARD

or any other institutioniv. The refinance amount claimed is exclusive of the

recoveries/ capital subsidy/margin money received or receivable.

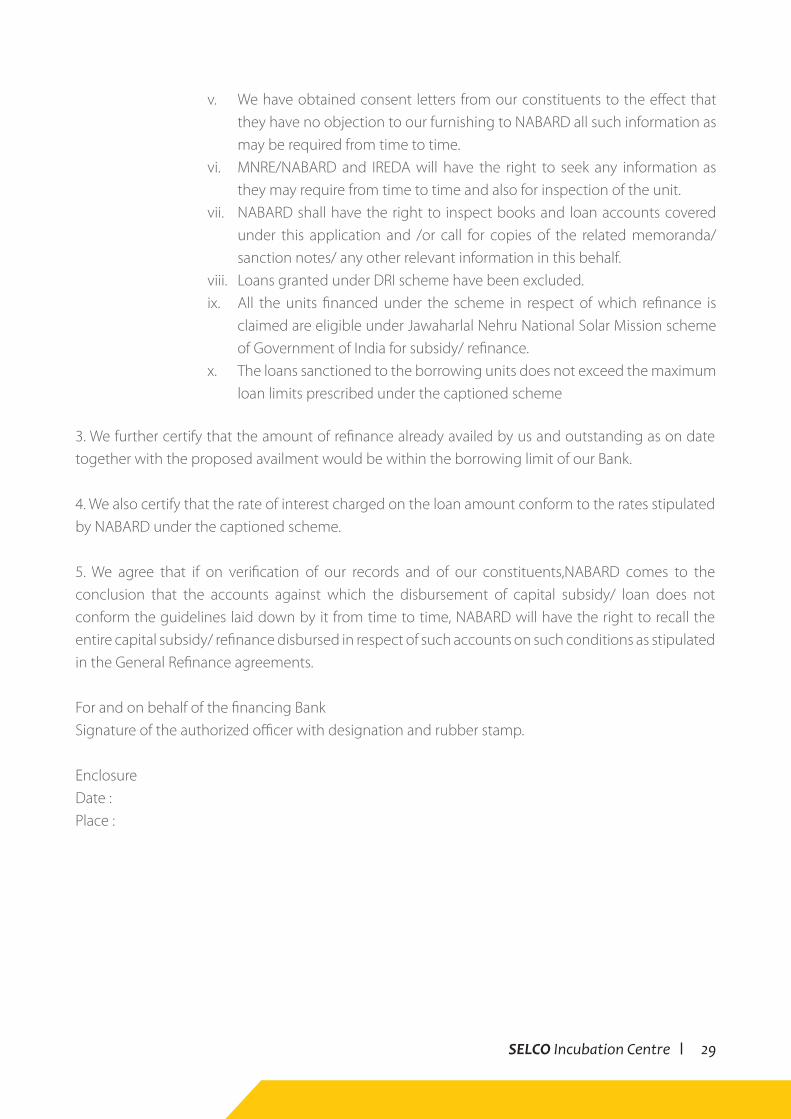

7.2 Claim Form

SELCO Incubation Centre 29

v. We have obtained consent letters from our constituents to the effect that

they have no objection to our furnishing to NABARD all such information as

may be required from time to time.

vi. MNRE/NABARD and IREDA will have the right to seek any information as

they may require from time to time and also for inspection of the unit.

vii. NABARD shall have the right to inspect books and loan accounts covered

under this application and /or call for copies of the related memoranda/

sanction notes/ any other relevant information in this behalf.

viii. Loans granted under DRI scheme have been excluded.

ix. All the units financed under the scheme in respect of which refinance is

claimed are eligible under Jawaharlal Nehru National Solar Mission scheme

of Government of India for subsidy/ refinance.

x. The loans sanctioned to the borrowing units does not exceed the maximum

loan limits prescribed under the captioned scheme

3. We further certify that the amount of refinance already availed by us and outstanding as on date

together with the proposed availment would be within the borrowing limit of our Bank.

4. We also certify that the rate of interest charged on the loan amount conform to the rates stipulated

by NABARD under the captioned scheme.

5. We agree that if on verification of our records and of our constituents,NABARD comes to the

conclusion that the accounts against which the disbursement of capital subsidy/ loan does not

conform the guidelines laid down by it from time to time, NABARD will have the right to recall the

entire capital subsidy/ refinance disbursed in respect of such accounts on such conditions as stipulated

in the General Refinance agreements.

For and on behalf of the financing Bank

Signature of the authorized officer with designation and rubber stamp.

Enclosure

Date :

Place :

From Borrower to Bank(Repayment received during)

From bank to NABARD

Date Amount (`) (Repayable as on) Amount (`)

01 July … to 31 December …..

31 January …..

01 January …. To 30 June ………

31 July ……

01 July … to 31 December …..

31 January …..

01 January …. To 30 June ………

31 July ……

01 July … to 31 December …..

31 January …..

01 January …. To 30 June ………

31 July ……

01 July … to 31 December …..

31 January …..

01 January …. To 30 June ………

31 July ……

01 July … to 31 December …..

31 January …..

01 January …. To 30 June ………

31 July ……

SELCO Incubation Centre 31

Sl. No.

1

Pre-approved Model Nos.

2

1

3

2

4

3

5

4

6

5

7

....

8

....

9

11

10

Solar Water

HeatingSystem

11

Total

12

Individuals

Groups

Category - SC

- ST

- OBC

Minority Community

No. - Female

Total cost of the sys-tem for units claimed

Capital Subsidy Amount eligible for units claimed (`)

Loan Amount exclud-ing capital subsidy for units claimed (`)

Margin Money by the borrower for the units claimed (`)

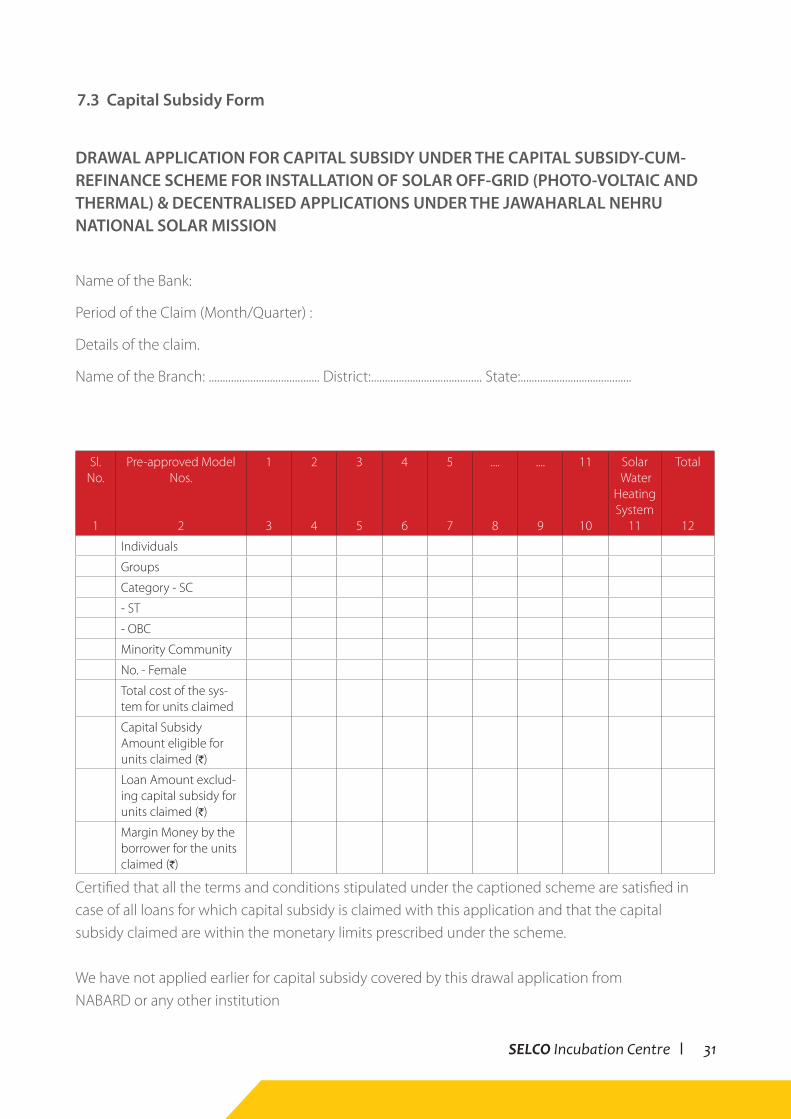

Certified that all the terms and conditions stipulated under the captioned scheme are satisfied in

case of all loans for which capital subsidy is claimed with this application and that the capital

subsidy claimed are within the monetary limits prescribed under the scheme.

We have not applied earlier for capital subsidy covered by this drawal application from

NABARD or any other institution

DRAWAL APPLICATION FOR CAPITAL SUBSIDY UNDER THE CAPITAL SUBSIDY-CUM-REFINANCE SCHEME FOR INSTALLATION OF SOLAR OFF-GRID (PHOTO-VOLTAIC AND THERMAL) & DECENTRALISED APPLICATIONS UNDER THE JAWAHARLAL NEHRU NATIONAL SOLAR MISSION

Name of the Bank:

Period of the Claim (Month/Quarter) :

Details of the claim.

Name of the Branch: ........................................ District:........................................ State:........................................

7.3 Capital Subsidy Form

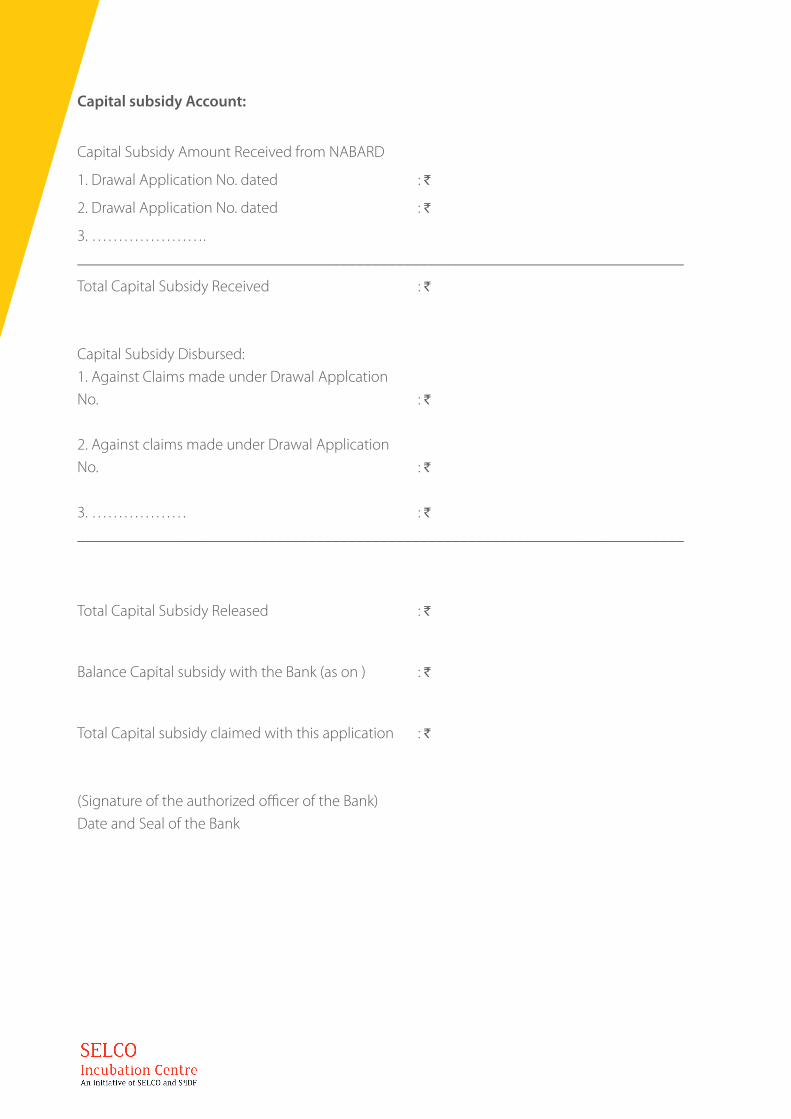

Capital subsidy Account:

Capital Subsidy Amount Received from NABARD

1. Drawal Application No. dated : `

2. Drawal Application No. dated : `

3. ………………….

____________________________________________________________________________

Total Capital Subsidy Received : `

Capital Subsidy Disbursed:

1. Against Claims made under Drawal Applcation

No. : `

2. Against claims made under Drawal Application

No. : `

3. ……………… : `

____________________________________________________________________________

Total Capital Subsidy Released : `

Balance Capital subsidy with the Bank (as on ) : `

Total Capital subsidy claimed with this application : `

(Signature of the authorized officer of the Bank)

Date and Seal of the Bank

SELCO Incubation Centre 33

7.4.1 Is financing a SHLS a bankable proposition?

If only the direct benefits accruing as a result

of savings in electricity charges and /or other

conventional sources of lighting like kerosene,

candle, etc., are taken into consideration, the

SHLS needs about 10 – 15 years to be viable,

which is still well within the economic life of the

major component in the system i.e. the panel.

If the generation of additional income by way

of extended hours of work etc., consequent to

providing SHLS is considered, it becomes viable

and bankable even more quickly, within 5- 7

years.

7.4.2 Does financing of SHLS fall into the category of priority sector banking?

As per the existing guidelines of the Reserve

Bank of India, finance extended by banks to

devices of renewable energy shall be classified

based on the major activity of the borrower.

Hence, a loan granted for SHLS to a farmer, retail

trader, professional & self employed person has

to be classified under Priority sector. A loan for

SHLS granted to a salaried person will have to

be classified as a Non priority sector advance.

8.3 Can any model of SHLS be financed?

Bank may choose to finance any SHLS model

depending on the general policy followed by

the bank management. It is advisable that the

bank observes appropriate due diligence on the

service provider of the system so that fly-by–

night operators’ products do not get financed.

Poor quality models destroy the customer’s faith

in SHLS. Certification on the quality of systems

from reputed national institutions such as

central Power Research Institute (CPRI) should

make banks more comfortable with providing

financial assistance.

7.4.4 Does the Solar Home Lighting System have BIS certification?

Currently, there is no BIS certification for SHLS.

Certification by Solar Energy Centre (SES)

Gwalpalhari, Gurgaon, Electronics Regional Test

Laboratory (ERTL) Kolkata, CPRI Trivandrum,

Electronics Testing & Development Center

Bangalore is available. Banks may insist on

certification from any one of the above certifying

agencies.

7.4.5 Is there a restriction on the size of SHLS while financing?

No, at present the demand is generally for

1/2/3/4 light systems. Banks can very well

extend finance for SHLS units comprising of

any number of lights, and /or lights with other

utilities like fans, powering transistor, radio,

refrigerator etc. Manufacturers/dealers/service

providers should provide customized units to

suit the requirement of the end user.

7.4.6 Can the financing of SHLS be made to the tenants who reside in the house or should it be made only to the house owner?

Generally it is a ‘NO”. But in some cases, banks

can provide finance to the tenant occupants, for

purchase and installation of SHLS.

7.4 Frequently Asked Questions

7.4.7 Are there any restrictions on the category of people who can borrow loans for SHLS?

There is no restriction on finance for any

individual. However, in the case of proprietorship

firms, or SHGs or institutions with board

members like religious places, trust or a co-

operative society, finance cannot be provided

as the position holder cannot be charged with

the liability of the loan.

7.4.8 Can a group of people qualify for a loan for the purchase of SHLS?

Yes, if the panel can be installed in a convenient

central location and electricity generated is

distributed on mutually agreed terms between

the end users (group members), then formal

or informal groups can be provided finance.

It is advisable to insist on a proper interest

agreement among group members specifying

borrowing, repayment utilization, maintenance

of the unit etc.

7.4.9 Is insurance mandatory for the system to be financed?

No it is not mandatory. It is left to the borrower to

decide in favor of or against a policy. However,

the policy that is popular with an individual

bank may be followed.

SELCO Incubation Centre 35

The idea that has germinated and bloomed in

the state of Karnataka now has to reach far and

wide across all states of India to ensure off-grid

solar systems reach the dark households and

bring a reliable light source into their lives. The

story of SELCO is impossible without the lifeline

of the robust banking network of our country.

The objective of the financial linkages manual

has been to demystify the roles / procedures

/ stakeholders involved in creating the end

consumer financing that is crucial to overcome