financial turnaround plan - harvey nash – global ... turnaround plan; and – review and revise...

TRANSCRIPT

Financial Turnaround Plan

2014-2016

Executive Summary

1

Glossary of Terms

A&E Accident and Emergency

AfC Agenda for Change

AMU Acute Medical Unit

AQuA Advancing Quality Alliance

Barnsley CCG Barnsley Clinical Commissioning Group

b/f Brought forward

BIC Best in class

Board Board of Directors

Borough Barnsley Metropolitan Borough

CAUTI Catheter-acquired urinary tract infection

CBE Commander of the Most Excellent Order of the

British Empire

CBU Clinical Business Unit

CCG Clinical Commissioning Group

CCU Critical Care Unit

CD Clinical Director

Cdiff Clostridium difficile

CEO Chief Executive Officer

CIP Cost Improvement Plan

Comms Communications

CQUIN Commissioning for Quality and Innovation

CSU Clinical Support Unit

Deloitte Deloitte LLP

DNA Did not attend

DoF Director of Finance

DVT Deep Vein Thrombosis

EBITDA Earnings before interest, taxes, depreciation,

and amortisation

ED Emergency Department

ENT Ear, Nose and Throat

EPR Electronic Patient Records

Executive Executive Team

FYE Full Year Effect

GM General Manager

GP General Practitioner

GUM Genito-urinary Medicine

HED Healthcare Evaluation Data

HoN Head of Nursing

HR Human Resources

HSMR Hospital Standardised Mortality Ratio

HWB Health and Wellbeing Board

ICT Information Communication Technology

ITDA Interest, taxes, depreciation, and amortisation

STCFF Short term cash flow forecast

2

Background and Overview

• In 2013/14 the Trust faced a year with challenging financial expectations, coupled with robust performance and quality targets, whilst at the same

time, forecasting an increase in the number of people who would attend the Emergency Department (ED).

• The challenging environment was compounded by a financial irregularity that was identified just prior to the 2013/14 year end.

• In March 2014, the Trust declared a serious incident into financial irregularities, commenced internal and external investigations into how finances

had been managed and submitted appropriate reports to Monitor.

• During the investigation it became evident that the in-year, monthly accounts have been misstated. The necessary corrections to the accounts

were made, which led to a significant adverse movement in the previously reported financial position. The Trust‟s performance showed an

„operating‟ deficit of £7.4 million. |Due to the changes in the Trust‟s properties in 2013/14, the value of the properties has declined, resulting in an

increase to the deficit of £2.5 million. The final reported deficit for the year is £9.9 million.

• In addition to this, the Trust also found it challenging to consistently meet the A&E target to see and treat 95% of all patients within 4 hours and

failed to do so during three quarters of 2013/14.

• Monitor formally opened their own investigations into Trust‟s financial position, its performance against the 4 hour wait target and into governance

arrangements in April 2014.

• In May 2014, Monitor confirmed the Trust was found to be in breach of its licence as a foundation trust and as such, requested a submission of a

robust two-year Turnaround Plan, detailing the actions the Trust will to take to turn its position around.

• Since March 2014, the Trust has taken significant steps to improve its position. These include:

– redress the A&E 4 hour breach, which has now been achieved;

– instigate robust internal and external investigations to identify how the deficit position arose, implement cost savings and develop a robust two-

year Turnaround Plan; and

– review and revise the governance structure, mindful of the issues above subject to external support.

• This plan sets out the Trust‟s current position and how it intends to turn the financial position around, whilst ensuring it maintains high standards of

quality.

3

Background and Overview The Trust and its demographics

• Barnsley Hospital NHS Foundation Trust provides acute hospital

services, including emergency and intensive care, medical and

surgical, elderly care, paediatric and maternity, along with

diagnostic and clinical support.

• The Trust also provides a number of specialised services, such as

cancer and surgical services in partnership with Sheffield

Teaching Hospitals NHS Foundation Trust.

• The Hospital was built in the 1970s and is a single site covering of

approximately 8.2 hectares, with circa 381 beds, 3,272

employees, and an annual income in the region of £165 million.

• During 2013/14, the Trust cared for 426,950 patients (418,712 in

2012/13), saw 216,771 clinic appointments (211,467 in 2012/13)

and treated 79,681 patients in the Emergency Department

(79,953 in 2012/13).

• The Trust serves a local population of approximately 234,400,

which is dispersed across an area matching the same

geographical boundaries as Barnsley Metropolitan Borough

Council and the Trust‟s main commissioner, Barnsley Clinical

Commissioning Group.

• The resident population distribution of Barnsley‟s 234,400 people

is similar to that seen nationally, except for a slightly lower

proportion of young people aged 25 to 39.

• In total 19% of the population is aged under 16, with 17% aged 65

or over. In 2011, there were 2,991 live births in Barnsley and

2,274 deaths.

• The total population of Barnsley is projected to rise by 7.2% by

2021.

• The number of over 65s in the Barnsley population is forecast to

increase to a projected 47,947 people by 2020.

• Overall health in Barnsley, although improving, is worse than the

average for England. Life expectancy at birth is 77.4 years for

men and 80.9 years for women, compared to 78.9 years and

82.9 years nationally.

• Death rates from the three main killers - cardiovascular disease

(heart disease and stroke), cancer and respiratory disease have

fallen over the last 10 years but still remain significantly higher

than the average for England.

• Cancer, particularly lung cancer, is the main cause of premature

death in Barnsley.

• The proportion of Barnsley residents living with a limiting long-

term illness is 24.4%. This is significantly higher when

compared to the average for England of 16.9%.

4

Background and Overview Trust and its demographics (continued)

• Barnsley is ranked as the 47th most deprived Borough of 326

English Boroughs, with 32% of the population living in the most

deprived quartile in the country.

• The deprivation is concentrated in the east of the Borough, with

23.8% of children in Barnsley currently living in poverty.

• 20.3% of working population in Barnsley are currently receiving

out of work benefits. This is the highest in South Yorkshire and

significantly higher than the national rate of 13.1%.

• Overall, there are substantial and persistent inequalities in the

health needs and outcomes of local people when compared to

the rest of the country.

Index of multiple deprivation 2010 in Barnsley

LSOAs ranked relative to England

5

Background and Overview Strategic context and the local health economy

• As part of the Trust‟s wider strategy, the Board has recently reviewed the Trust‟s vision and aims to ensure they are fit for purpose and

confirmed that the Trust‟s vision is “To be the best, integrated healthcare organisation of choice for our local communities and beyond”.

• The Trust recognises that as a small-medium sized district general hospital there is an increasing need to work in partnership with others

to improve pathways of care for patients.

• Accordingly, going forward the Trust intends to work closely with Barnsley Clinical Commissioning Group (CCG), whose key goals for

2014/15 include:

– reduce emergency hospital activity by 15% over five years by driving care closer to home;

– increase capacity and access to primary care and community services;

– improve the support to individuals to manage their own long term conditions in a community setting, through improved care co-

ordination; and

– radically redesign intermediate care facilities in Barnsley.

• The Trust will also continue to work with local partners, as a member of the Health and Wellbeing Board, on the key priorities of the

health and wellbeing strategy.

• Further supporting the approach to partnership working, the trust, together with Barnsley CCG, local authority and South West Yorkshire

Partnership NHS Foundation Trust were successful in 2013 in securing pioneer status for health and social care in Barnsley; this work is

entitled “Stronger Barnsley Together”.

• The Trust is fully committed and actively participating in the Working Together Programme, which is a collaboration with seven other

acute providers in South and Mid Yorkshire, and North Derbyshire.

6

Background and Overview Introduction to current position

Income and expenditure

2012/13 2013/14 2013/14 Variance Plan

£'million Actual Plan Actual to Actual

Income

Clinical income 145.3 144.1 147.2 3.1

Other income 22.3 21.0 22.5 1.5

Total income 167.6 165.1 169.7 4.6

Operating Expenses

Pay cost (111.6) (110.6) (115.8) (5.2)

Non pay cost (46.5) (43.4) (52.8) (9.4)

Total operating expenses (158.1) (154.0) (168.6) (14.6)

EBITDA 9.5 11.1 1.1 (10.0)

ITDA (8.1) (9.5) (8.5) 1.0

Total operating expenses (166.2) (163.5) (177.1) (13.6)

Net surplus/(deficit) pre-impairment 1.4 1.6 (7.4) (9.0)

Impairment - - (2.5) (2.5)

Net surplus/(deficit) post-impairment 1.4 1.6 (9.9) (11.5)

• Historically, the Trust has achieved its financial targets, reporting

a small surplus of £1.4 million in 2012/13. However, this was

achieved with non-recurrent funding from Barnsley PCT of circa

£6.4 million.

• Although the Trust‟s 2013/14 management accounts presented

operational deficits throughout the year, due to various

amendments (some of which were unsupported), small

surpluses were reported to the Board until February 2014.

• Following the identification of the financial reporting issues and

irregularities, the Trust completed an internal review to consider

the impact of these issues on its short-term cash flow, and to

determine the underlying financial position of the Trust is

2013/14 and 2014/15.

• The Trust has historically underperformed on its Cost

Improvement Programme (CIP) targets, in 2013/14 only

achieving £1.9 million of the initial £6.2 million CIP targeted.

• The Trust had an operating deficit of £7.4m for 2013/14.

However, due to changes to the Trust‟s properties in 2013/14,

the value of the properties has declined, resulting in an increase

to the deficit of £2.5m. The final reported deficit for the year is

£9.9m.

• Furthermore, the Trust breached the national A&E target in five

of the previous six quarters, which in conjunction with the

financial deficit led to the involvement of Monitor.

7

Background and Overview Clinical services

• Acute Paediatrics

• Anaesthetics/Critical Care

• Cardio Respiratory

• Care of the Elderly

• Emergency Medicine –

ED/AMU

• General Medicine

• General Surgery: Elective

Breast, Upper GI, Lower GI

• General Surgery: Elective

Urology, Vascular

• GUM

• Head and Neck: ENT,

Ophthalmology, Oral Surgery,

OMFS

• Obstetrics/Gynaecology

• Paediatrics

• Pathology

• Pharmacy

• Radiology

• Speciality Medicine:

Dermatology, Rheumatology,

Clinical Haematology

• Therapies: Physiotherapy,

OT, Dietetics, Speech &

Language

• Trauma and orthopaedics

The future

positioning of

these services

will be

determined by

health policy,

the Trust‟s

clinical strategy

and competition,

and will be

subject to a

sustainability

review.

The services currently provided by the Trust are detailed below.

8

Background and Overview Next Steps

Next steps

• The Trust understands that this document is part of a wider, long-term plan and has therefore developed “next steps” to ensure delivery

of the plan.

• These steps will focus on four key areas; high level details of which are outlined below and on the next page:

– Turnaround Plan;

– Governance;

– The Emergency Care Action Plan including input from ECIST; and

– The Clinical Service Sustainability Review and 5-year strategy.

• The Trust has developed detailed step plans for each of these areas.

• The progress of the plan will be monitored and reported to Board along with monthly meetings with Monitor.

5-year strategy

• In relation to the service review mentioned above, the Trust is currently agreeing the scope and timeline. The Trust anticipates that work

is likely to commence in August 2014, once the scope is agreed.

• The Trust will work with clinical teams and support departments to ensure they are profitable and sustainable, with an interim report due

in Quarter 3 2014.

• Options will be developed by service including working with others to provide services to ensure that patient needs continue to be met.

External engagement will be key to this and plans will be developed in line with commissioning intentions.

• The 5-year strategic plan is expected to be completed by December 2014.

9

Background and Overview Milestones

The Trust has identified key categories and milestones which must be achieved over the next two years in order to successfully deliver the Turnaround

Plan.

- Key milestone

The

turnaround

plan

Subject to Bob’s changes

Timeline

Key milestones

2014/15 2015/16

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Turnaround Plan

Plan approved by Board and sent to Monitor

Monitor visits to review progress

Key financial milestones

Key CIP milestones

Governance review

Deloitte’s Capability and Governance Review

Recommendations and Action Plan

Project Dearne findings and recommendations

Project Allerton 6 month follow up review

CBU structure fully in place

4 hour action plan

ECIST visits and recommendations

Updated action plan to Monitor

Monitor visits to review progress

Strategy

Agree scope for sustainability review

Benchmarking at a service level

CBU challenge sessions/workshops

Interim Report to be issued

Agree options, understand impacts and risks

External engagement

Submit 5 year plan to Monitor

Delivery of 5 year plan

Baseline Financials

11

Baseline Financials

Financials

• The Trust‟s „Run Rate‟ (an estimate of future financial performance assuming present trends continue without the benefit of deferred or

one off income) at the end of 2013/14 is approximately £16.6 million deficit.

• This run rate is immediately worsened at the start of 2014/15 by a reduction in the national rates at which we are paid to provide our

services, together with inflation to staff salaries and staff rising up pay increments. This gives an effective opening run rate for 2014/15 of

a deficit of £20.7m.

• Through delivery of this Turnaround Plan we aim to close 2015/16 with a run rate deficit of £2.8m.

Staffing

• The Trust budgeted for 2,727.9 Whole Time Equivalents (WTE) as at March 2014 (WTE is a calculation of the staff resource available,

taking into account full and part-time working). The total WTE was 2,821.1 (93.2 over the budget). The main reason for this difference is

primarily the need to support the delivery of non-recurring income and projects.

• The total WTE is made up of 2,578.1 contracted positions, 171.2 bank and overtime positions and 72.1 agency staff positions.

12

Baseline Financials: Income and expenditure

Income and Expenditure

£’million 2013/14

Baseline/

Run Rate

Income

Clinical income 147.2 143.5

Other income 22.5 15.7

Total income 169.7 159.2

Operating Expenses

Pay cost (115.8) (116.2)

Non pay cost (52.8) (50.9)

Total operating expenses (168.6) (167.1)

EBITDA 1.1 (7.9)

Depreciation and amortisation (6.3) (6.7)

Restructuring costs (0.2) -

Interest (0.1) (0.1)

PDC Dividend (1.9) (1.9)

ITDA (8.5) (8.7)

Total operating expenses (177.1) (175.8)

Net deficit pre-impairment (7.4) (16.6)

Impairment (2.5) -

Net deficit post-impairment (9.9) (16.6)

Overview

• In Q4 2013/14, the Trust operated at an underlying Run Rate deficit of £16.6 million. The actual position at the end of 2013/14

was an operating deficit of £7.4m, with a final reported deficit of £9.9m (with the impact of changes to the Trust‟s properties

taken into account).

• The main reasons for the difference between the Run Rate and the actual position are non-recurrent incomes, release of

deferred income (with no directly associated costs), release of provisions (money put aside to cover a future liability), and

higher operating expenses towards the end of the year.

13

Baseline Financials: Assumptions

Area/2013/14

value 2013/14 actual

Baseline

adjustment Baseline assumption

Clinical

income

£147.2

million

• Clinical income includes all patient related

activity and constituted 87% of total income

in 2013/14, of which 85% (£124.8 million)

was received from Barnsley CCG. The

remaining clinical income sources are:

– other CCGs – £10.5 million; and

– other trusts and organisations – £11.9

million.

• Barnsley CCG income includes an element

of non-recurrent income for service

improvement and efficiency projects.

• Furthermore, the CCG income includes

CQUIN income which is conditional based

on specific target achievements. The

amount available is 2.4% of the value of our

contract with the CCG.

• £3.7

million

• During 2013/14, we received £4.7 million as non-recurrent

income. Of this total, £3.7 million was included within

clinical income from Barnsley CCG (and therefore does

not form part of the baseline) and £0.9 million was

included in other income (as adjusted below). The

remaining balance was properly deferred into 2014/15.

• The Trust has historically achieved approximately 80% -

85% of CQUIN, with the current estimate of 84% for

2013/14. There have therefore been no CQUIN related

adjustments.

The following table outlines the assumptions we have made in establishing our baseline finances for 2014/15.

14

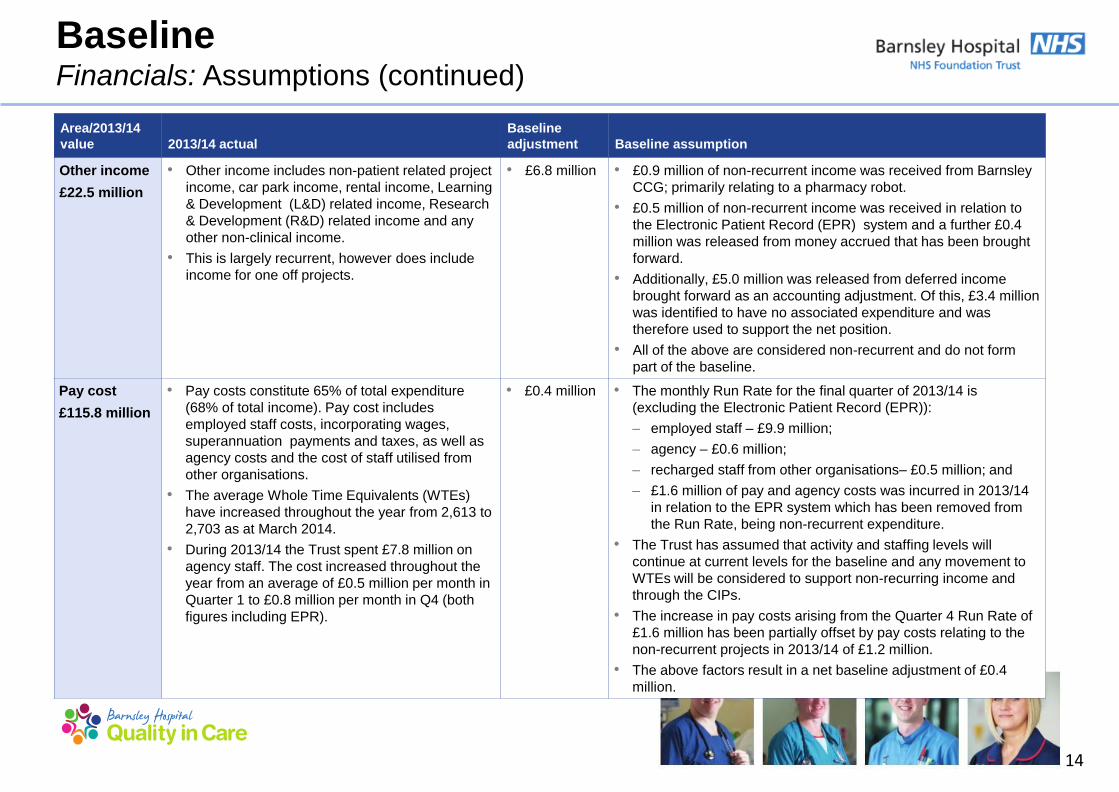

Baseline Financials: Assumptions (continued)

Area/2013/14

value 2013/14 actual

Baseline

adjustment Baseline assumption

Other income

£22.5 million

• Other income includes non-patient related project

income, car park income, rental income, Learning

& Development (L&D) related income, Research

& Development (R&D) related income and any

other non-clinical income.

• This is largely recurrent, however does include

income for one off projects.

• £6.8 million • £0.9 million of non-recurrent income was received from Barnsley

CCG; primarily relating to a pharmacy robot.

• £0.5 million of non-recurrent income was received in relation to

the Electronic Patient Record (EPR) system and a further £0.4

million was released from money accrued that has been brought

forward.

• Additionally, £5.0 million was released from deferred income

brought forward as an accounting adjustment. Of this, £3.4 million

was identified to have no associated expenditure and was

therefore used to support the net position.

• All of the above are considered non-recurrent and do not form

part of the baseline.

Pay cost

£115.8 million

• Pay costs constitute 65% of total expenditure

(68% of total income). Pay cost includes

employed staff costs, incorporating wages,

superannuation payments and taxes, as well as

agency costs and the cost of staff utilised from

other organisations.

• The average Whole Time Equivalents (WTEs)

have increased throughout the year from 2,613 to

2,703 as at March 2014.

• During 2013/14 the Trust spent £7.8 million on

agency staff. The cost increased throughout the

year from an average of £0.5 million per month in

Quarter 1 to £0.8 million per month in Q4 (both

figures including EPR).

• £0.4 million • The monthly Run Rate for the final quarter of 2013/14 is

(excluding the Electronic Patient Record (EPR)):

– employed staff – £9.9 million;

– agency – £0.6 million;

– recharged staff from other organisations– £0.5 million; and

– £1.6 million of pay and agency costs was incurred in 2013/14

in relation to the EPR system which has been removed from

the Run Rate, being non-recurrent expenditure.

• The Trust has assumed that activity and staffing levels will

continue at current levels for the baseline and any movement to

WTEs will be considered to support non-recurring income and

through the CIPs.

• The increase in pay costs arising from the Quarter 4 Run Rate of

£1.6 million has been partially offset by pay costs relating to the

non-recurrent projects in 2013/14 of £1.2 million.

• The above factors result in a net baseline adjustment of £0.4

million.

15

Baseline Financials: Assumptions (continued)

Area/2013/14

value 2013/14 actual

Baseline

adjustment Baseline assumption

Non-pay cost

£52.8 million

• Non-pay costs includes all other operating

expenditure.

• In 2013/14, non-pay cost accounted for 30% of

total expenditure (31% of total income).

• The most significant elements of 2013/14 non-

pay costs included:

– medical consumables – £14.3 million;

– drugs – £11.3 million; and

– other consumables – £10.1 million.

• £1.9 million • In relation to the £5.0 million of deferred income released in the

year the Trust incurred associated expenditure of £1.6 million.

This was considered non-recurrent expenditure.

• Furthermore, non-recurrent entries totalling £0.8 million,

primarily relating to one off costs and accounting adjustments,

were incurred in 2013/14.

• The reduction in cost is partially off set by cost pressures of

£0.7 million, resulting from higher expenditure towards the end

of the year.

• The above three adjustments results in a net £1.7 million

decrease on 2013/14 non-pay costs. This results in a 2013/14

baseline of £51.1 million.

ITDA

£8.6 million

• ITDA (Interest, Taxes, Depreciation and

Amortization) largely comprises:

– depreciation of £6.3 million; and

– Public Dividend Capital (PDC) dividend of

£1.9 million.

• £0.2 million • As a result of £19.1 million of capital expenditure incurred, the

depreciation Run Rate stands at £6.7 million increased from

actual £6.3 million.

• PDC dividends and interest are assumed to remain consistent

for the 2013/14 baseline.

Impairment

£2.5 million

• Impairment charge of £2.5 million. • £2.5 million • The impairment charge of £2.5 million (as a result of changes

to the Trust‟s property) is considered non-recurrent and has

therefore been removed from the baseline.

16

Contracted WTEs

• Contracted WTEs is the actual basic contracted hours of

employed full time and part time staff as at March 2014. This does

not include any overtime hours.

Bank and overtime

• Bank and overtime is based on all actual hours worked over and

above the contracted hours by contracted staff. This also includes

employees on zero hour contracts, forming the bank staff.

WTE summary WTEs

Contracted WTEs 2,578.1

Bank and overtime 171.2

Agency 72.1

Total WTE 2,821.4

Budgeted Establishment 2,727.9

Variance 93.5

Baseline Financials: Staffing as at March 2014

The table below summarises the WTEs the Trust is currently operating at against budgeted establishment levels. This represents the

opening position of WTEs from which the workforce plan is developed.

Agency

• Agency WTEs is based on the average cost by major staff group

divided by the hourly rates towards the end of the 2013/14. This

takes into consideration any months with excessive usage which

may skew the numbers.

Budgeted Staffing Levels

• In order to be fully staffed to deliver all of the agreed services,

the Trust requires a WTE of 2,727.9 as at March 2014. This

does not include the WTE requirement for any non-recurrent

business cases that were approved and delivered during the

year.

Variance

• The Trust is currently operating at 93.5 WTEs over the budgeted

levels.

• The primary reasons for this include:

− Staffing required to deliver services funded through non-

recurring revenues;

− Delivery of the EPR project; and

− Cover for key posts on long-term sickness and higher than

average rates of maternity leave.

Baseline Clinical and operational

18

Baseline Clinical

• The Trust provides a range of district hospital services and is proud to have obtained a CQC Band 6 rating (the best available) in March

2014, in recognition of the quality of care offered by the Trust. Other notable examples of delivering high quality healthcare include:

– The latest PLACE environment assessment shows the Trust ratios exceed all national averages;

– No „Never Events‟ in last 12 months;

– No incidents of grade 4 pressure ulcers during 2013/14; and

– Excellent performance meeting all targets for C Diff and no MRSA bacteraemia for our 4th year running.

• Key areas reviewed as part of the turnaround planning process have been: appropriate use of beds; effective theatre utilisation; and

outpatient efficiency. Significant areas of opportunity have been identified through this exercise, which include:

– Appropriate use of beds; it is recognised that, while the Trust compares well against peers for LoS at Trust-level, there is significant

opportunity at specialty level to reduce admissions and LoS;

– Theatre utilisation figures suggest that some specialties have more theatre capacity than may be warranted by demand;

– Benchmarking indicates that the Trust is an outlier when compared to peers for outpatient efficiency.

• Further to this there is significant opportunity for service redesign. The Trust will work closely with the Clinical Business Units to develop

a clinical strategy at a service line level.

• To support this, the Trust will be commissioning a clinical sustainability review to inform the development of its 5-year plan and to provide

a framework for discussion with commissioners and key partner.

19

Baseline Clinical and operational: Overview

Savings Schemes

As part of the Turnaround Plan, the Trust has developed a number of savings schemes. In doing this, the Trust has reviewed key indicators

of operational efficiency. Key areas reviewed have been:

• Appropriate use of beds – Although the Trust compares well against peers for length of stay at Trust level, there is significant opportunity

at specialty level to reduce admissions and length of stay. The key target area is General Medicine, with a potential bed saving of 35 beds

if „best in class‟ length of stay targets were to be achieved. Collaborative working with primary, community and social care will be required

to achieve this.

• Effective theatre utilisation – The Trust is working with an external company to ensure that theatre resources are better utilised and that

theatre sessions are allocated appropriately to the specialties most in need, in order to release capacity where possible.

• Outpatients efficiency - Benchmarking indicates that the Trust is an outlier when compared to peers for outpatient efficiency. With Did

Not Attend (DNA) rates at 9.6%, compared to a peer average of 7.9%, this is another key area for the Trust to drive cost savings.

Service Redesign Opportunities

While the above opportunities will be vital in delivering financial turnaround, the Trust also recognises that, as a small-medium sized district

general hospital, there are a number of strategic factors that need to be taken into account when formulating its long-term strategy and

assessing its future financial and operational sustainability. These include consideration of:

• the financial and workforce implications of the commissioning drive for seven day working and access to services;

• which services will remain solely provided by the Trust from the single hospital site, and which may become regionally networked or

shared services;

• which services may no longer be delivered from the hospital site – either due to centralisation or transferring care into the community; and

• the role of the Trust in developing community services to enable the delivery of care outside the acute environment, particularly for

patients with long-term conditions, requiring complex domiciliary care.

In order to consider these questions, the Trust will also be commissioning a clinical sustainability review to inform the development of its 5-

year plan and to provide a framework for discussion with commissioners and key partners.

20

Baseline Clinical and operational: SWOT analysis

• Underlying recurrent deficit position of £16.6 million in 2013/14. • High levels of locum usage due to difficulties in recruitment. • Diagnostic wait times under pressure, largely due to limited imaging capacity

related to workforce. • Lack of clarity regarding service level operating costs and income. • Poor track record of CIP delivery in prior years. • Historical under-achievement of A&E 4 hour access target, which has been

met for the first two months of 2014/15 – new model of care may be put at risk by financial position.

• Establishment of collaborative working arrangements for specialised or

smaller specialty services, to ensure service sustainability and local provision where clinically appropriate. For example urology, vascular surgery, and ENT.

• CQC rating 6. • Successful partnership model for pathology services with Rotherham NHS

Foundation Trust, enabling delivery of efficient high quality and cost-effective services.

• Development of A&E model of care and review of non-elective pathways has enabled achievement of 4 hour access target for first two months of 2014/15.

• Provision of bowel cancer screening.

• Expansion of collaborative working in certain specialties to attract skilled

workforce and maintain local services. • Development of ambulatory care pathways, including care of the elderly and

paediatrics. • Partnership working with community services to avoid unnecessary hospital

admissions and attendances. For example development of Deep VeinThrombosis (DVT) community pathway and GUM integration with community services.

• Use of technology to reduce pressure on capacity. For example telephone follow ups and telemedicine links with GPs to promote community management of specific conditions.

• Development of advanced non-medical roles to address reduction in training posts and provide consistency of care.

• Investment in technology including the launch of our EPR programme in September 2014.

• Development of commercial opportunities via Barnsley Hospital Support Services.

• Difficulty in recruitment and retention of skilled workforce for both medical

and non-medical roles. • Reduction in national training posts impacting on capacity to maintain

service delivery and medical rotas. • Commissioning agendas including centralisation and the need for 7 day

working may put services at Barnsley at risk if standards, minimum volume and workforce requirements cannot be met.

• Increasing demand for certain services related to demographic change and changes in clinical behaviour, driven by an aging population and availability of new diagnostics/treatments.

The Trust has undertaken a high level SWOT analysis in order to determine its strengths, weaknesses, opportunities and threats.

Strengths Weaknesses

Opportunities Threats

21

Baseline Clinical and operational: Activity overview

• The Trust has seen an increase in activity over the previous three financial years, which has been largely driven by growth in day case

procedures and outpatient attendances. In terms of percentage variances, the Trust ended the year close to plan.

• ED attendances were slightly down during 2013/14, but volumes were similar to 2012/13 ,which saw a significant increase in

attendance due to ED unplanned service changes at Mid Yorkshire Hospitals NHS Trust.

The below graph shows the breakdown of Trust activity for the past three financial years:

0.0

0.1

0.2

0.3

0.4

0.5

FY12 FY13 FY14

Tru

st A

ctivity (

mill

ions)

Trust activity over previous 3 financial years

Daycases Elective inpatients Non elective inpatients

Outpatients - new Outpatient - follow ups ED Attendances

22

Baseline Clinical and operational: Benchmarking overview

Source: HED; based on comparison with peers as defined by HED for time period Jan 2013 – Dec 2013.

Days LoS (all)

LoS above 30

days (all)

LoS excl. zero

days (all)

Pre-operative

bed days (all)

Day case

rates

Readmission

within 30 days

of discharge

New to follow

up ratios DNA rates

Trust 3.6 43.5 5.0 0.3 84.1% 9.6% 3.2 9.6%

Best in class 3.2 42.9 4.5 0.24 87.4% 7.7% 1.5 6.0%

Peer average 3.9 48.3 5.3 0.4 80.3% 8.7% 2.4 7.9%

Upper quartile 3.5 44.4 5.0 0.3 84.0% 8.0% 1.7 7.1%

The table below compares key operational efficiency indicators of the Trust with peer average, upper quartile and best in class.

23

Baseline Clinical and operational: Specialty level LoS

Source: HED; based on comparison with peers as defined by HED for time period Jan 2013 – Dec 2013.

Specialty level analysis of

LoS indicates priority areas

where there may be potential

for bed day reduction.

The biggest opportunity when

the Trust is compared to best

in class and upper quartile against its peer group is in

General Medicine. This group

of patients is likely to include

Geriatric Medicine patients

who have been coded to

General Medicine.

The Trust is currently

undertaking a number of

initiatives aimed at reducing

bed days overall (including

unnecessary admissions,

LoS, readmissions), and will

review benchmarking

information as necessary to

measure improvement and

identify issues.

The Trust Analysis

Treatment specialty

Total spell

duration Spells

Average total spell

duration

Peer group

BIC

BIC opportunity

(bed days)

Beds saved at

BIC

Peer group

UQ

UQ opportunity

(bed days)

Beds saved at

UQ

Accident & Emergency

732 647 1.1 0.6 324 1 1.2 - -

Breast Surgery 236 105 2.2 1.5 74 - 1.6 63 -

Cardiology 195 44 4.4 1.0 150 - 2.6 79 -

Clinical haematology 1,078 271 4.0 1.3 732 2 3.8 54 -

Dermatology 27 16 1.7 0.7 16 - 1.2 8 -

ENT 1,116 677 1.6 0.9 474 1 1.1 372 1

General medicine 91,568 15,771 5.8 5.0 12,617 35 5.8 789 2

Gynaecology 2,406 1,475 1.6 0.9 1,033 3 1.2 664 2

Neonatology 4,050 420 9.6 4.2 2,268 6 7.9 714 2

Rheumatology 50 9 5.6 0.2 49 - 2.1 32 -

Trauma & Orthopaedics

15,161 2,920 5.2 4.4 2,336 6 5.3 - -

Well Babies 2,904 2,249 1.3 0.9 900 2 1.3 112 -

The below table demonstrates how the Trust compares against peers for Length of Stay (LoS) at specialty level, for all inpatient spells.

24

Baseline Clinical and operational: Bed capacity and utilisation

• Alongside operational efficiency benchmarking information,

the Trust reviews important internal factors such as its bed

occupancy

• Review of bed occupancy figures demonstrates that:

– bed occupancy at Trust level is on average 85.6%; and

– there is seasonal variation in bed occupancy levels,

although medical beds are consistently utilised at 90%

and above.

• When assessing bed occupancy, LoS, and admission data,

opportunities for bed day reduction can be identified. The

Trust has therefore established initiatives to target key

areas, including care of the elderly.

• It is recognised that the Trust currently has a higher

readmission rate when compared to peers, and that any

initiatives looking to reduce bed days will need to identify

this as a risk, defining key mitigating actions. These

mitigating actions and readmission rates will be monitored

at service and Trust level to ensure any issues are

identified and acted upon rapidly.

Source:

Note 1 – Based on bed occupancy at midnight for time period Jan 2013 – Dec 2013

Note 2 – Excludes CCU and SAU

Bed occupancy Jan 2013 – Dec 2013

Specialty Number of beds Occupancy %

Gynaecology 20 65.7%

Medical 232 92.4%

Surgical 49 85.2%

Trauma & Orthopaedics 56 78.7%

Paediatrics 24 53.2%

Total 381 85.6%

25

Theatre utilisation by specialty Jan 2013 – Dec 2013

Type Specialty No of

sessions In session

Day surgery ENT 155 91.1%

General Surgery 158 82.8%

Gynaecology 189 78.7%

Oral & Maxillo Facial Surgery 221 76.9%

Trauma & Orthopaedics 122 69.1%

Urology 177 77.3%

Vascular Surgery 26 74.8%

Total 1,048 79.3%

Main theatres

Breast Surgery 131 95.4%

ENT 177 89.8%

General Surgery 552 88.1%

Gynaecology 333 89.2%

Obstetrics 85 70.7%

Ophthalmology 388 79.9%

Trauma & Orthopaedics 1,005 87.8%

Urology 98 85.7%

Total 2,769 86.7%

Trauma Trauma & Orthopaedics 378 73.9%

Grand total 4,195 83.7%

Baseline Clinical and operational: Effective theatre utilisation

• Review of theatre utilisation figures demonstrates that:

– there is significant opportunity to improve efficiency,

particularly in day case theatres;

– there is an urgent need to undertake a robust capacity

and demand analysis, to review allocation of lists and

ensure that these are correctly matched with demand.

– a more effective theatre scheduling system is required,

to ensure appropriate listing of cases, taking into

account case mix, to best utilise theatre time; and

– there is a need to monitor and improve late starts and

early finishes, to drive improved efficiency and

throughput of lists.

• The Trust is proposing to work with an external company to

review drivers of inefficiency across theatres, with a view

to improving theatre scheduling; increasing productivity

and utilisation; and reducing over-runs and additional

sessions.

26

Baseline Clinical and operational: Outpatient efficiency and utilisation

• The Trust also appears to be an outlier in terms of new to follow up ratios when compared to peers, suggesting opportunity for

improvement . Various initiatives are progressing to improve this, including:

– telephone follow up models;

– MDT “one-stop” clinics;

– increased use of technology for specimen results;

– development of a joint teledermatology service with GPs; and

– development of community pathways, including the implementation of protocols to allow early discharge from rheumatology,

dermatology and haematology.

• The Trust has identified significant opportunity to improve outpatient productivity and efficiency.

• Through the CBU restructure, a Clinical Director for outpatients has been identified, enabling clinical leadership of the improvement

programme.

• DNA rates have been highlighted as higher than peer average, and there is an ongoing project to address these.

• It is recognised that in order to achieve outpatient efficiencies, the Trust needs to work effectively with its partners. Close working with

GPs in the development of community pathways is particularly important.

Source: HED, based on comparison with peers as defined by HED for time period Jan 2013 – Dec 2013.

New to follow up ratios DNA rates

The Trust 3.2 9.6%

Best in Class 1.5 6.0%

Peer Average 2.3 7.9%

Upper Quartile 1.7 7.1%

27

Baseline Clinical and operational: Performance indicators

Source:

Monitoring performance

• The Trust monitors operational performance on a regular basis, reporting key indicators both internally and externally.

28

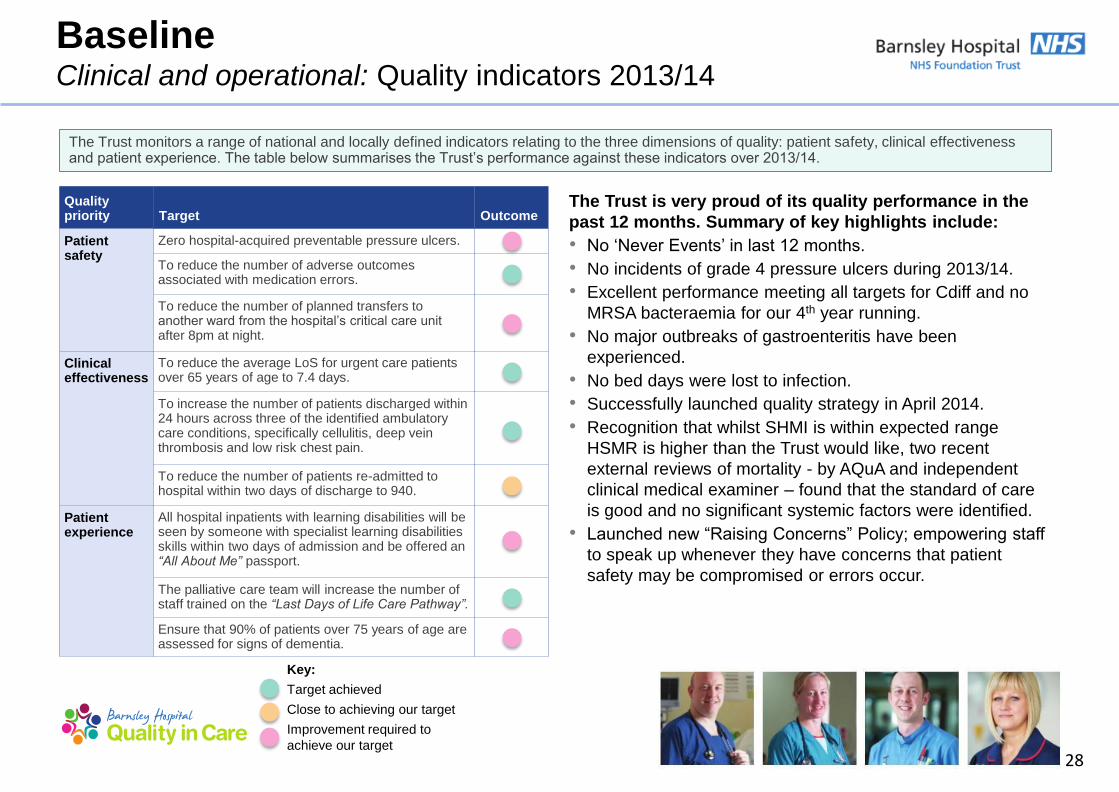

The Trust monitors a range of national and locally defined indicators relating to the three dimensions of quality: patient safety, clinical effectiveness and patient experience. The table below summarises the Trust‟s performance against these indicators over 2013/14.

The Trust is very proud of its quality performance in the

past 12 months. Summary of key highlights include:

• No „Never Events‟ in last 12 months.

• No incidents of grade 4 pressure ulcers during 2013/14.

• Excellent performance meeting all targets for Cdiff and no

MRSA bacteraemia for our 4th year running.

• No major outbreaks of gastroenteritis have been

experienced.

• No bed days were lost to infection.

• Successfully launched quality strategy in April 2014.

• Recognition that whilst SHMI is within expected range

HSMR is higher than the Trust would like, two recent

external reviews of mortality - by AQuA and independent

clinical medical examiner – found that the standard of care

is good and no significant systemic factors were identified.

• Launched new “Raising Concerns” Policy; empowering staff

to speak up whenever they have concerns that patient

safety may be compromised or errors occur.

Quality priority Target Outcome

Patient safety

Zero hospital-acquired preventable pressure ulcers.

To reduce the number of adverse outcomes associated with medication errors.

To reduce the number of planned transfers to another ward from the hospital‟s critical care unit after 8pm at night.

Clinical effectiveness

To reduce the average LoS for urgent care patients over 65 years of age to 7.4 days.

To increase the number of patients discharged within 24 hours across three of the identified ambulatory care conditions, specifically cellulitis, deep vein thrombosis and low risk chest pain.

To reduce the number of patients re-admitted to hospital within two days of discharge to 940.

Patient experience

All hospital inpatients with learning disabilities will be seen by someone with specialist learning disabilities skills within two days of admission and be offered an “All About Me” passport.

The palliative care team will increase the number of staff trained on the “Last Days of Life Care Pathway”.

Ensure that 90% of patients over 75 years of age are assessed for signs of dementia.

Baseline Clinical and operational: Quality indicators 2013/14

Key:

Target achieved

Close to achieving our target

Improvement required to

achieve our target

29

Quality goal Aim/objective Quality indicators

Patient experience;

ensure we deliver patient-

centred care

To identify key patient experience metrics which will drive improvement

in the way we deliver care.

Implementation of core data across all inpatient areas to

consistently measure and benchmark patient experience.

To improve the experience of care provided to patients with dementia

and their carers.

Undertake case finding for at least 90% of patients 75 years

and over admitted as an emergency for >72 hours; ensuring

that, where patients are identified as potentially having

dementia or delirium, at least 90% are appropriately

assessed; and ensuring that, where appropriate, patients

with dementia are referred onto specialist services.

To implement the NHS Friends & Family Test throughout the hospital. Wider roll out of patient experience questionnaires through

the expansion of Open & Honest Care, ensuring openness

and transparency on the reporting of harms or injury to

patients.

Delivering consistently

safe care

To reduce hospital acquired harms in relation to VTEs, Falls, CAUTIs

and pressure ulcers.

During 2014/15 we want to see a reduction in hospital

acquired harms in relation to VTEs, falls, CAUTIs and

pressure ulcers with the aim of achieving the national

average for harm-free care against all areas. Each area will

be monitored separately.

To reduce inpatient falls. In 2013/14 there were 1,030 reported inpatient falls. During

2014/15 we want to see this number being reduced by at

least 50%.

To improve clinical note keeping standards, thereby ensuring robust

patient assessments and plans of care.

By April 2015 we will be able to demonstrate 75%

compliance with clinical note keeping standard audits.

The tables on the following two pages describe the Trust‟s current quality goals, objectives and quality markers for 2014/15. These drive the Trust‟s

current approach to improving patient experience, safety and effectiveness of care.

Baseline Clinical and operational: Quality indicators 2014/15

30

Quality goal Aim/objective Quality markers

Delivering consistently

effective care

To further reduce unavoidable deaths. Our rolling 12 month HSMR value in December 2013 is

112. We aim to reduce this rate further to 105 by January

2015 and 100 by January 2016.

Improve recognition and management of the adult deteriorating patient. We implement NEWS across the organisation in January

2014. By April 2015 we aim to demonstrate 95%

compliance with the implementation of NEWS in the adult

patient.

To improve sepsis recognition and response. For 2014/15 the sepsis recognition and management tool

will be embedded further across the Trust with a

multifaceted approach to educating staff in the use of the

tool. By April 2015 we aim to demonstrate 95% compliance

with the implementation of the sepsis screening and

management tool.

To ensure scrutiny of all in-hospital deaths to ensure learning is

achieved where possible.

From April 2014 we implemented a formal process for

reviewing all in-hospital deaths in a consistent and timely

manner. By April 2015 we aim to demonstrate that 95% of

all in-hospital deaths are being formally reviewed within 15

working days of the death occurring.

Building capacity and

capability

Review HR processes to ensure that we recruit staff with the values that

underpin compassionate care.

Reduce sickness absence to 3.5%.

Review skills mix and team structures where required to ensure that we

have the right people with the right skills at the right time.

Demonstrate 90% compliance with staff appraisals.

Identify and implement competency-based training for non-registered

staff.

Demonstrate 90% compliance with mandatory training.

Baseline Clinical and operational: Quality indicators 2014/15 (continued)

Strategy Turnaround Plan Delivery

32

2014/15

Comms

2015/16

Risks

Benefits

Risks

Governance

Service

review and

redesign

PMO

Financials

Savings

schemes Delivery

The

turnaround

plan

Strategy: Turnaround Plan Delivery

The Turnaround Plan

• The diagram displays the fundamental aspects of the Turnaround Plan which is driven by the Vision of the Trust.

Our four quality goals are:

• Delivering patient-centred care;

• Delivering consistently safe care;

• Delivering consistently effective care; and

• Building on capacity and capability.

The

turnaround

plan

Overview

• Quality is at the heart of everything the Trust does.

• The plan is built on delivery of saving schemes, which will allow the Trust to bridge the existing financial deficit.

Delivery

• The Trust recognises that delivery of saving schemes is critical to success of this Turnaround Plan.

• The Trust put in place structures which will ensure delivery of these schemes.

There are four themes underpinning the plan:

• quality & safety;

• accountability;

• delivery and culture; and

• financial control.

Governance

• The Trust recognises the importance of good governance and has ensured that a robust action plan is in place.

33

1. Patients will experience safe

care

• Action to reduce harm to our

patients in relation to VTE,

falls, catheter acquired

urinary tract infections and

pressure ulcers.

• Implement NHS Friends &

Family Test throughout the

hospital.

• Achieve a 50% reduction in

inpatient falls.

• Continued improvements in

our HSMR value.

• Delivery of a 7 day service,

including radiology therapies

and pharmacy.

• Improve our patients

experience of care for those

who have dementia.

2. Partnerships will be our

strength

• Being open with the public

and our patients, to receive

feedback that will improve

our care.

• Drive changes through

partnership working with the

HWB, including reduction of

emergency activity, increase

capacity and access to

primary care services, assist

in supporting patients in

managing their long-term

conditions in the community.

• Partnership working with the

Working Together

Programme in sharing good

practice, increasing quality of

care.

3. People will be proud to

work at the Trust

• Develop and strengthen our

leaders and teams and CBU

structure.

• Create a motivated and

highly skilled workforce to

have the right people and

right skills to deliver safe and

compassionate care.

• Value and look after our

staff‟s health and wellbeing.

4. Performance matters

• Implement a performance

management framework.

• Achieve our performance

targets.

• Invest wisely in required

technology, such as the EPR.

• Optimise the use of our

estate.

• Cost-effective procurement.

• Development of commercial

partnerships and business

proposals to drive income.

Turnaround Strategy: Trust‟s Vision

The Trust‟s Vision is to be the best integrated healthcare organisation of choice for our local communities and beyond.

Quality goal: Deliver consistently safe and effective patient-centred care, building on our capacity and capability.

The

turnaround

plan

34

1 Quality:

Quality and safety drive our clinical strategy and our future remaining at the heart of

our core business.

2 Accountability:

Teams and individuals are held to account through robust governance to ensure

delivery.

3 Delivery and culture:

Create a “can do” culture; clinically lead with a bottom up approach.

4 Financial control:

To do what we get paid to do: the provision of high quality, cost effective services.

Turnaround Strategy: Themes underpinning the plan

The

turnaround

plan

35

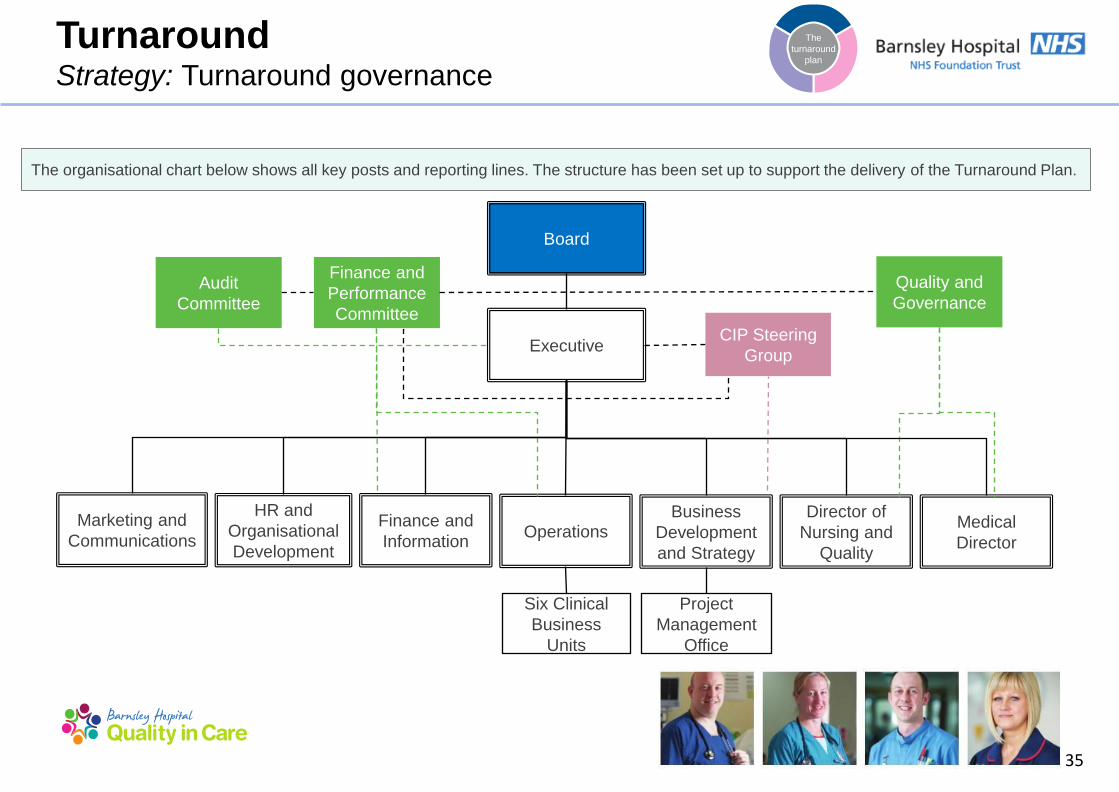

Turnaround Strategy: Turnaround governance

The organisational chart below shows all key posts and reporting lines. The structure has been set up to support the delivery of the Turnaround Plan.

Board

Executive

HR and

Organisational

Development

Finance and

Information

Business

Development

and Strategy

Director of

Nursing and

Quality

Medical

Director

Finance and

Performance

Committee

Project

Management

Office

Six Clinical

Business

Units

Quality and

Governance

Marketing and

Communications Operations

CIP Steering

Group

Audit

Committee

The

turnaround

plan

36

Turnaround Strategy: Turnaround Plan responsibilities

Role Name Appointment Date Responsibilities

Board - Executive Ms D Wake

Dr J Mahajan

Mr D W Peverelle (until 30 June

2014)

Mrs K Kelly

Mrs H Mcnair

Mr S Diggles

Other Directors

Ms H Brearley

Ms E Parkes

Mr R Kirton

Mr J Bradley

Mrs L Christopher

Oct 2013

Sept 2009

May 2000

Jul 2014

Dec 2011

Apr 2014

• Meet weekly to oversee all Trust business, including progress against business and Turnaround Plan.

• Key decision making body for the Trust.

• Consider key business cases for service improvement, develop

strategies for Board approval. The Board is the major decision

making body for the Trust, the Executive ensure the business

plan is executed.

• Plan implementation and monitor progress against Board

approved strategies and plans.

• Monitor performance against the Trust‟s Turnaround Plan.

Accountability for delivery.

• Provide executive sponsorship for generation, identification and

delivery of CIP schemes.

• Provide assurance to Non-Executive Directors and to the

assurance committees.

• Other directors don‟t have voting rights but form part of the

Executive Team but share all of the above responsibilities.

The

turnaround

plan

37

Turnaround Strategy: Turnaround Plan responsibilities

Role Name Appointment

Date

Responsibilities

Board - Non

executive

Mr S Wragg (Chairman)

Mrs S Brain England OBE

Mrs L Christon

Sir Stephen Houghton CBE

Mr P Spinks

Mr F Patton

Jan 2009

Jan 2012

Jan 2010

Jan 2012

Sept 2012

Jan 2008

• Hold the Executive Directors to account.

• Accountable to the Governors.

• Provide assurance to governors regarding the Trust‟s strategy

and performance including the Turnaround Plan.

• Non-Executive Directors will chair all assurance committees (in

particular, Finance & Performance Committee).

Governors Various • Hold the Non-Executive Directors to account.

CEO Ms D Wake Oct 2013 • Overall control and accountability of the Turnaround Plan.

• Chair of Executive meetings – see above.

• Chair of CIP steering group – leading the CIP steering group to

monitor delivery against the CIP plan via CIP tracker. Links to

performance meetings.

• Holds the Executive to account.

Interim Director of

Finance

Mr S Diggles April 2014 • Responsible for all financial information, including:

– baselining;

– cashflow forecast;

– assisting and monitoring the CIP financial information;

– lead on ICT Turnaround Plans; and

– member of the CIP steering group.

The

turnaround

plan

38

Turnaround Strategy: Turnaround Plan responsibilities (continued)

Role Name Appointment

Date

Responsibilities

Director of Strategy

and Business

Development

Mr R Kirton Apr 2014 • Accountable for the delivery of the Turnaround Plan, co-

ordinating the PMO team.

• Member and deputy chair of the CIP steering group.

• Workstream sponsor for support services and non pay.

Director of HR &

Organisational

Development

Ms H Brearley Apr 2010 • Executive lead on:

– workforce Turnaround Plans; and

– responsible for workforce information, analysis and planning.

• Workstream sponsor for workforce.

• Implementation of workforce change.

• Member of CIP steering group.

Director of

Marketing &

Communications

Ms E Parkes Feb 2014 • Responsible for the communication of the plan to employees

and internal and external stakeholders relating to the Trust.

Medical Director Dr J Mahajan Sept 2009 • Executive lead on medical workforce Turnaround Plans.

• To provide quality assurance on all elements of turnaround

programme.

• Member of CIP steering group.

Director of Nursing

& Quality

Mrs H Mcnair Dec 2011 • Executive lead on nursing and quality Turnaround Plans.

• To provide quality assurance on all elements of turnaround

programme.

• Member of CIP steering group.

The

turnaround

plan

39

Turnaround Strategy: Turnaround Plan responsibilities (continued)

Role Name Appointment

Date

Responsibilities

Director of

Operations

Ms K Kelly Apr 2014 • Executive lead on operational and CBU Turnaround Plans.

• Member of CIP steering group.

• Workstream sponsor for frontline and clinical.

CBU leads CBU leadership team – consists of

General Manager, Clinical Director

and Head of Nursing.

General Manager

Clinical Director

Head of Nursing

• Lead in operational delivery of Trust-wide Turnaround Plans.

• Responsible for design and delivery of CBU service,

improvement and development plans, and meeting KPIs.

• Report to performance meetings on progress against CBU plan.

• Overall responsibility for the delivery of Turnaround Plan,

identifying and implementation of CIP schemes, ensuring

delivery of savings.

• Clinical leadership and engagement in Turnaround Plans

(internal and external stakeholder e.g. via clinical senate).

• Professional leadership for the delivery of the Turnaround Plan.

The

turnaround

plan

40

Turnaround Strategy: Turnaround Plan responsibilities (continued)

Role Name Appointment Date Responsibilities

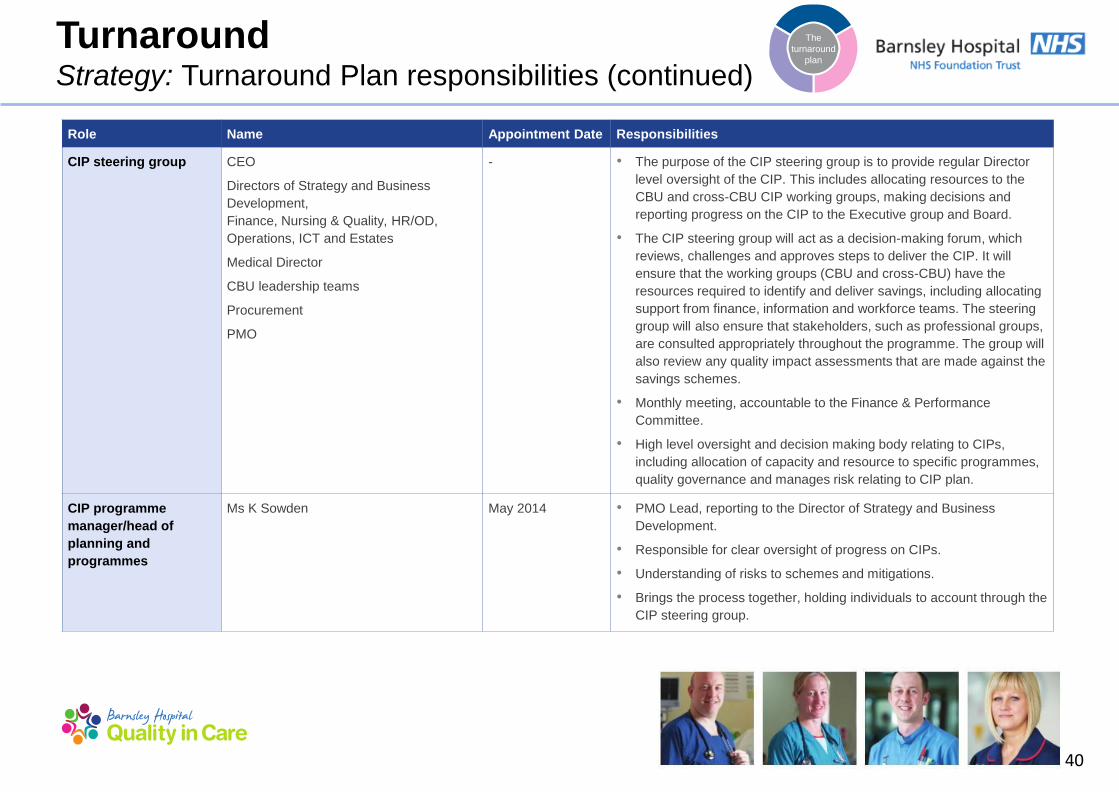

CIP steering group CEO

Directors of Strategy and Business

Development,

Finance, Nursing & Quality, HR/OD,

Operations, ICT and Estates

Medical Director

CBU leadership teams

Procurement

PMO

- • The purpose of the CIP steering group is to provide regular Director

level oversight of the CIP. This includes allocating resources to the

CBU and cross-CBU CIP working groups, making decisions and

reporting progress on the CIP to the Executive group and Board.

• The CIP steering group will act as a decision-making forum, which

reviews, challenges and approves steps to deliver the CIP. It will

ensure that the working groups (CBU and cross-CBU) have the

resources required to identify and deliver savings, including allocating

support from finance, information and workforce teams. The steering

group will also ensure that stakeholders, such as professional groups,

are consulted appropriately throughout the programme. The group will

also review any quality impact assessments that are made against the

savings schemes.

• Monthly meeting, accountable to the Finance & Performance

Committee.

• High level oversight and decision making body relating to CIPs,

including allocation of capacity and resource to specific programmes,

quality governance and manages risk relating to CIP plan.

CIP programme

manager/head of

planning and

programmes

Ms K Sowden May 2014 • PMO Lead, reporting to the Director of Strategy and Business

Development.

• Responsible for clear oversight of progress on CIPs.

• Understanding of risks to schemes and mitigations.

• Brings the process together, holding individuals to account through the

CIP steering group.

The

turnaround

plan

41

Turnaround Strategy: Turnaround Plan responsibilities (continued)

Role Name Appointment Date Responsibilities

CIP lead Various - • Implementation of CIP, reporting to sponsor.

• Primary day-to-day interface with the working group leads, working

group members and technical leads.

• Providing hands on support to drive the detailed planning for each

shared scheme and supporting on analysis required.

• Co-ordinate technical leads in finance, information and HR to provide

data and analytical support to each workstream.

Information lead Various - • Responsible for information and analysis for CIP/Turnaround Plans.

• Technical leads will provide advice within the meeting specific to their

area and may also be required to gather information, conduct analysis

or consult others as part of the process of identifying and

implementing the CIP initiatives for their working group.

Finance leads Various - • Responsible for financial information and analysis for CIP/Turnaround

Plans.

• Technical leads will provide advice within the meeting specific to their

area and may also be required to gather information, conduct analysis

or consult others as part of the process of identifying and

implementing the CIP initiatives for their working group.

Workforce lead Various - • Responsible for co-ordination of workforce Turnaround Plans.

• Workforce planning, numbers etc.

• Technical leads will provide advice within the meeting specific to their

area and may also be required to gather information, conduct analysis

or consult others as part of the process of identifying and

implementing the CIP initiatives for their working group.

The

turnaround

plan

42

Turnaround Strategy: Quality

• The Trust is committed to ensuring that quality drives its clinical strategy and its future and that this remains at the heart of the Trust‟s core business.

• The Trust has developed a quality strategy to support the provision of safe, effective and dignified care, which has defined key metrics and stretch

targets for the next three years.

• This focus on quality will be crucial when maintaining the quality of services during financial turnaround, enabling the Trust to deliver financially and

clinically sustainable services for the future.

• The Trust has recently reviewed its quality governance structures, to ensure an integrated approach to quality management, embedded throughout

all levels of the organisation. The revised structures are shown in the schematic below.

What does quality mean for our patients?

• Every patient will receive the right treatment at the right time, by the

right person.

• Every patient will be kept safe and protected from all avoidable harm

whilst in our care.

• Every patient will receive treatment that follows national guidelines.

• Every patient will be treated with dignity, compassion and respect.

• Every patient will be listened to.

• Every patient will be kept informed regarding their treatment and will

play a key part of any decision making process.

• Every concern or complaint received will be treated with the

importance it deserves and issues will be dealt with in a timely and

open manner.

Board of Directors

Review effectiveness of processes

Clinical Business Units

Identify and monitor local quality targets and

quality impacts

Quality, performance and integrated

governance

Measure, monitor and improve

Quality Quality

The Trust recognises the importance of maintaining quality. This is paramount to the Trust‟s turnaround strategy. The Trust‟s quality approach is set out

below.

The

turnaround

plan

43

Turnaround Strategy: Quality (continued)

• The Trust recognises that a robust approach to quality

management throughout the turnaround process is

required, to closely monitor and mitigate any risks to the

quality of service provided by the Trust.

• Therefore, quality impact assessment and ongoing

monitoring have been identified as integral aspects of the

wider CIP governance. This approach is shown in the

diagram to the left and follows the following steps:

1. Scheme approval

2. Scheme development

3. Quality monitoring

Scheme

approval

Quality

approach

Panel to

review QIA

The

turnaround

plan

The Trust‟s plan to maintain quality during turnaround is set out below.

44

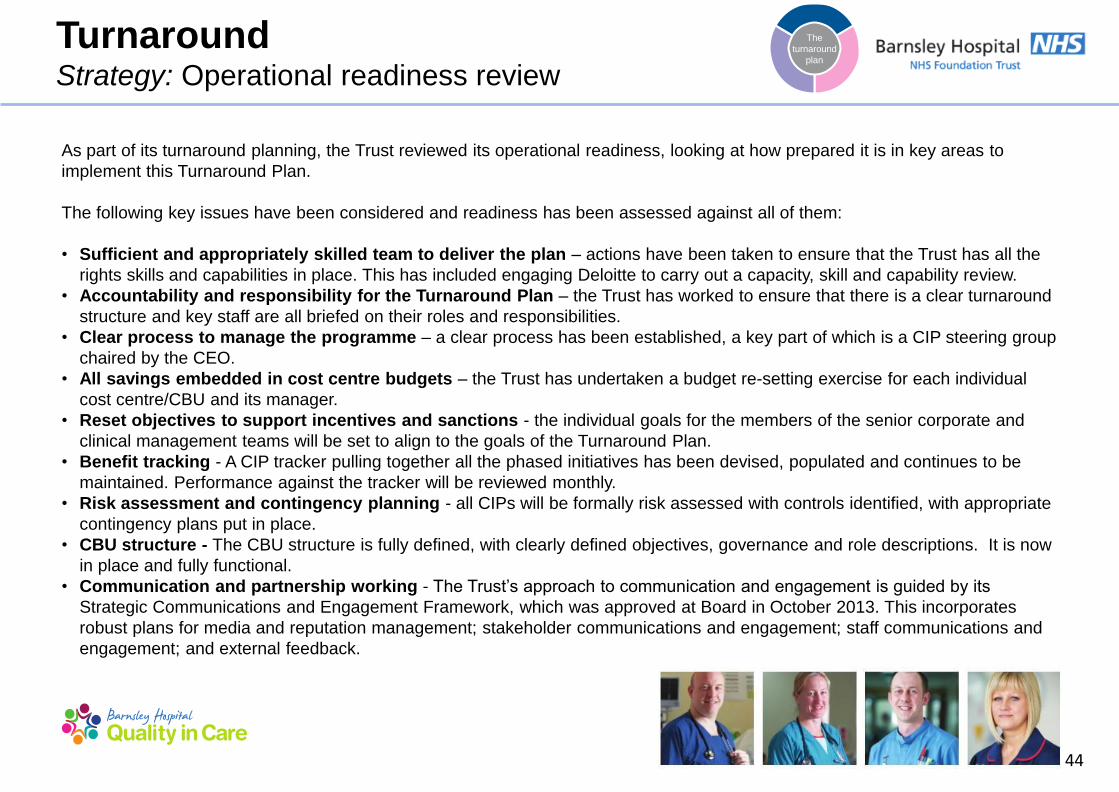

Turnaround Strategy: Operational readiness review

The

turnaround

plan

As part of its turnaround planning, the Trust reviewed its operational readiness, looking at how prepared it is in key areas to

implement this Turnaround Plan.

The following key issues have been considered and readiness has been assessed against all of them:

• Sufficient and appropriately skilled team to deliver the plan – actions have been taken to ensure that the Trust has all the

rights skills and capabilities in place. This has included engaging Deloitte to carry out a capacity, skill and capability review.

• Accountability and responsibility for the Turnaround Plan – the Trust has worked to ensure that there is a clear turnaround

structure and key staff are all briefed on their roles and responsibilities.

• Clear process to manage the programme – a clear process has been established, a key part of which is a CIP steering group

chaired by the CEO.

• All savings embedded in cost centre budgets – the Trust has undertaken a budget re-setting exercise for each individual

cost centre/CBU and its manager.

• Reset objectives to support incentives and sanctions - the individual goals for the members of the senior corporate and

clinical management teams will be set to align to the goals of the Turnaround Plan.

• Benefit tracking - A CIP tracker pulling together all the phased initiatives has been devised, populated and continues to be

maintained. Performance against the tracker will be reviewed monthly.

• Risk assessment and contingency planning - all CIPs will be formally risk assessed with controls identified, with appropriate

contingency plans put in place.

• CBU structure - The CBU structure is fully defined, with clearly defined objectives, governance and role descriptions. It is now

in place and fully functional.

• Communication and partnership working - The Trust‟s approach to communication and engagement is guided by its

Strategic Communications and Engagement Framework, which was approved at Board in October 2013. This incorporates

robust plans for media and reputation management; stakeholder communications and engagement; staff communications and

engagement; and external feedback.

45

Turnaround Strategy: Operational readiness review (continued)

The

turnaround

plan

• CCG relationship - The Trust is working to continually improve the relationship and communications with Barnsley CCG by

actively participating in regular meetings and continuous dialogue.

• Cultural change – Actions are being taken to enact a fundamental change in the culture of the organisation towards a culture

of empowerment and ownership. These include a series of road shows for staff outlining their role in the Turnaround Plan;

regular staff communications outlining progress against the plan; clear targets and milestones; and clearly defined objectives

for management and staff

• Workforce plan - A detailed workforce plan has been produced as part of the Turnaround Plan, incorporating the expected

workforce movements during the two-year period.

• Clear vision - The Trust‟s vision, reflecting its focus on patients, people and partnerships has been in place since 2014 and has

been extensively communicated to the Trust‟s staff and partners in April 2014. This will be reviewed following the planned

sustainability review, and, if necessary, updated

• Internal communications - The Trust has made improvements to internal communications and engagement channels in line

with its Strategic Communications and Engagement Framework 2013-16. These communications explain key milestones, what

is expected of staff regarding the delivery of the plan and also seek to identify further money saving ideas

• Staff engagement - The Trust is committed to effective, honest and regular communication with all members of staff. The

purpose and importance of the Turnaround Plan will be communicated and a message delivered that the successful

achievement of the turnaround will depend on the commitment of all members of staff.

46

Turnaround Strategy: Key risks

The Trust has identified a number of risks that could impact its

ability to deliver the Turnaround Plan. These risks have been

classified in the following areas:

Financial

• A number of financial risks, including achieving the required

forecast activity levels, CQUIN targets and averting CCG

penalties have been identified.

Governance

• The Trust engaged KPMG to undertake an external review of

the governance structure and to make recommendations in

respect of implementation of a more robust budget setting

process. This identified a number of risks which the Trust has

mitigated against.

CIPs

• The achievement of the proposed CIP plan is essential to the

Trust‟s financial turnaround.

• Failure to identify, develop and achieve these savings within the

timeframe detailed within this plan will have a significant impact

on the turnaround.

Delivery

• A number of delivery risks have been identified and are set out

on the following pages.

The

turnaround

plan

2014/15

Comms

2015/16

Risks

Benefits

Risks

Governance

Service

review and

redesign

PMO

Financials

Savings

schemes Delivery

The turnaround

plan

47

Turnaround Strategy: Delivery risks

The

turnaround

plan

The Trust has identified key risks to the delivery of the Turnaround Plan, together with mitigations. Examples of these risks and mitigations are given

below.

• Skillset of turnaround team - Any skills gap could result in either a delay or the failure of the Turnaround Plan. Mitigation includes: a skills and

capability review, carried out by Deloitte, of both the Executive and the Board to ensure that the Trust is able to deliver the Turnaround Plan.

• Accountability and responsibility for the Turnaround Plan - There is a risk that without each member of the turnaround team taking

responsibility and being held accountable, the delivery of the turnaround could be unsuccessful. Mitigation includes: the Trust has ensured that

each member of the turnaround team has been briefed on the responsibilities, anticipated deliverables, timelines and key milestones.

• Adequate internal resources - Following some reductions to „back office functions‟, such as the Finance team (undertaken over a period of

time), there is an underlying risk that there are insufficient internal resources to maintain on-going services and support turnaround activity.

Mitigation includes: The Trust will, for each function affected by the Turnaround Plan, complete an internal capabilities review to identify whether

the current resource has the necessary capacity to support the plan.

• Director of Finance (DoF) role - The Trust‟s current interim DoF, who specialises in supporting distressed organisations, was appointed on an

interim basis. There is a fundamental risk that, without a suitable permanent DoF who has relevant skills and turnaround experience in place, a

two-year turnaround cannot be achieved. Mitigation includes: While more intensive support is required, the interim DoF has agreed a contract

extension until December 2014.

• CBU structures - Specifically relating to the CIPs, there is a risk to delivery of savings due to the limited project management capacity across the

Trust. In particular, this risk relates to the limited number of dedicated project managers within the PMO structure to support delivery of CIP.

Mitigation includes: Establishment of CIP steering group; Each CIP to continue to have a CIP sponsor and CIP lead.

• Clear process to manage the programme - Without a clear process to manage the savings schemes which incorporates robust challenge and

tracking of benefits, there is a risk that the savings will not be achieved. Mitigation includes: The CBUs and the Executive are meeting on monthly

basis to assess CBUs performance and delivery.

• Culture - There is a risk that some Trust employees will be resistant to the changes detailed within this plan which, if not addressed, could delay

implementation. Mitigation includes: the Trust will deliver a series of interactive roadshows which will provide details of the plan, explain key

milestones, what is expect of the staff regarding the delivery of the plan and seek further money saving ideas. The Trust will also ensure that there

are regular follow on communications to re-emphasise the key message regarding the plan, updates on its delivery and further need for change.

Turnaround Financials

49

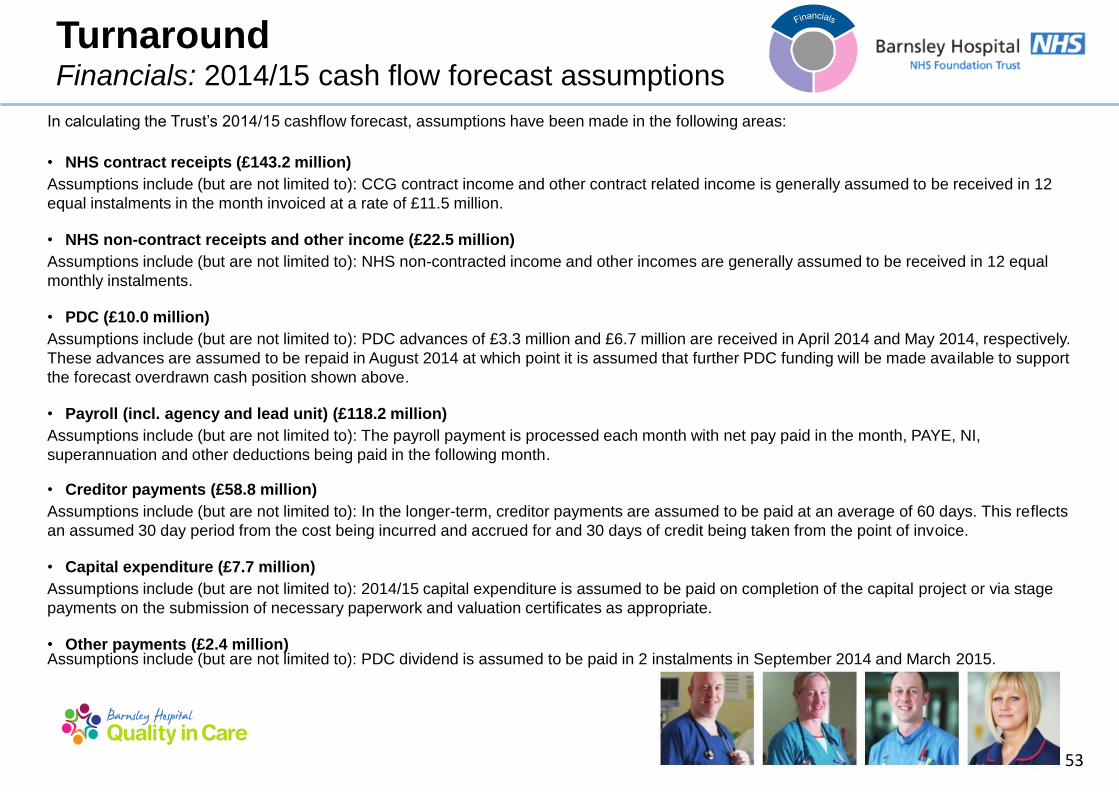

Turnaround Financials: 2014/15 and 2015/16 summary

2014/15

• Contract based income increases to baseline by £1.1 million

incorporating the effects of activity and Tariff (the national rate at

which we get paid for our services). Other income including non-

recurrent income increases by £4.4 million to baseline.

• Pay costs increase to support the non-recurring income and due to

cost increases under AfC. Planned savings on agency usage

reduce the total movement to baseline to £6.6 million.

• Non-pay costs increase to baseline based on activity and

inflationary pressures by £1.2 million. ITDA reduces by £0.7 million.

• CIPs are assumed to deliver in year a £6.0 million (4.3%)

improvement to baseline with a further £0.3 million improvement

due to VAT savings on agency costs. The CIP full year effect is

£8.7 million (6.2%).

• The forecast deficit for the year is £11.9 million. Accounting for the

full year effect of CIPs and the Q4 Run Rate, the underlying closing

Run Rate is a deficit of £8.0 million.

2015/16

• Contract based incomes assume activity levels remain the same with a

1.5% reduction to tariff. Other income including non-recurring incomes

(excluding EPR) are assumed to continue at the same level as 2014/15.

• Pay costs are initially assumed to rise in line with AfC. Agency costs are

assumed to reduce by a further £0.9 million.

• Non-pay costs increase due to inflationary pressures assumed between 1-

5% which are then set off by £1.1 million of savings on consultancy and

advisory costs.

• A further £6.0 million (4.3%) of CIP savings are planned to be delivered in

year in 2015/16. The CIP full year effect is £8.3 million (6.0%).

• The forecast deficit for the year is £6.3 million. Accounting for the full year

effect of CIPs and the Q4 Run Rate, the underlying closing run rate is a

deficit of £2.8 million.

Note: CIP percentage savings are calculated

on contracted activity based income.

50

Turnaround Financials: 2014/15 forecast summary

Income and Expenditure

£‘million

2013/14

Actual

Baseline/

Run Rate 2014/15 2015/16

Income

Income from activities 147.2 143.5 149.3 147.3

Other income 22.5 15.7 15.7 14.9

Total income 169.7 159.2 165.0 162.2

Operating Expenses

Pay cost (115.8) (116.2) (117.8) (112.4)

Non pay cost (52.8) (50.9) (51.1) (48.1)

Total operating expenses (168.6) (167.1) (168.9) (160.5)

EBITDA 1.1 (7.9) (3.9) 1.7

Depreciation and amortisation (6.3) (6.7) (5.8) (5.8)

Restructuring costs (0.2) - (0.3) (0.6)

Interest (0.1) (0.1) - -

PDC Dividend (1.9) (1.9) (1.9) (1.6)

ITDA (8.5) (8.7) (8.0) (8.0)

Total operating expenses (177.1) (175.8) (176.9) (168.5)