financial statements: disclosure overload - what … statements: disclosure overload - what ... •...

TRANSCRIPT

Financial Statements: Disclosure overload -

What can be done to reduce the clutter?

By Vik Bhandari

Managing Partner

Financial Reporting Specialists

www.frsgroup.com.au

Agenda

• Problem with financial reporting

• Cutter in financial statements

• Practical example: review financial

statements

• Recap and reflection.

Agenda

• Problem with financial reporting

• Cutter in financial statements

• Practical example: review financial

statements

• Recap and reflection.

Problem with financial reporting

Lack of useability

– Complex and unintuitive

– Excessive disclosures

– Unable to be understood.

Only will get worse

– with myriad of new standards/interpretations (eg AASB 9)

Problem with financial reporting

• Likely response from users:

“The financial statements are too

complicated to read. I only look at

profit figure, dividend figure, what

the directors and auditors earn

and, post GFC, whether the company

is solvent.”

• Press reports – questioned the benefit of Australia adopting IFRS and the so called disclosure overload

• Some auditors are promoting streamlining.

Problem with financial reporting

Reduced Disclosure Regime (stage 1 of ED192 Revised Differential

Reporting Framework) has added another layer of complexity:

– Full General Purpose Financial Statements (GPFS)

– General Purpose Financial Statements Reduced Disclosure

Requirements (RDR)

– Special Purpose Financial Statements (SPFS)

• Is the right framework being used?

• Do users know which is which?

AASB concerned about

abuse of SPFS:

(i) Application

(ii) Recognition and

remeasurement

(iii) Disclosures

All recognition &

measurement.

Disclosures of

AASB 101, 107,

108, 1048, 1054

As

appropriate

for users.

Disclose

policies

GPFS

Tier 1 or

not early

adopt

RDR

Full

compliance

with

standards

All recognition

and

measurement,

reduced but

mandatory

disclosure

Tier 2

and early

adopt

RDR

SPFS

Ch 2M.3 Other

Agenda

• Problem with financial reporting

• Clutter in financial statements

• Practical example: review financial

statements

• Recap and reflection.

Clutter in financial statements

• Too much detail in accounts

– Unnecessary/immaterial information

• Important information lost/obscured

• Investors/users being “Blinded”

• Information rolled forward with little/no thought

– Prior period accounts

– Explanatory information

– Disordered/non-logical layout.

Clutter in financial statements

• How true is this statement:

“generally, if regulations require a disclosure, it goes in the report –

regardless of the materiality or importance to the business”

UK FRC, April 2011

• Auditors, company directors, preparers and regulators would

rather ‘over disclose’

i.e. when in doubt, disclose approach.

Clutter in financial statements

“… there is concern that the volume and complexity of disclosure

has a potentially negative impact by distracting users from the

information that is relevant to their decision making. In essence,

there is a risk that quantity is outweighing quality.”

The Group of 100, Oct 2009

Clutter in financial statements

“… since the introduction of IFRS, the accumulation of accounting

rules and accompanying disclosures, the pace of change and the

growing complexity of business, have led to calls for reductions in,

and simplification of, various requirements.”

Managing Complexity Report

Australian FRC, May 12

Clutter in financial statements

• Using model accounts/templates without thought

• Adding disclosures to comply with checklists

– for checklist sake!

• Not using materiality from disclosure perspective

• Financial reporting process

– an after thought (not enough time spent on them).

Significant focus in the area of clutter

‘Less is more’ report

• Group of 100, Oct 2009

• Concern about volume, complexity and usefulness of certain

disclosures

• Contradiction:

‘Principles-based’ approach => used in standards settings

‘Rules-based’ approach => used for disclosures.

Common pitfalls/clarity

Clutter – “Losing the excess baggage”

Reducing disclosures in financial statements to what’s important (July 2011) ICAS and NZICA joint project, on behalf of IASB • “Whilst requirement of each standard seemed

reasonable at time of standard development, the combined impact of existing requirements has lead to lengthy financial statements cluttered by excessive detail”

Recommendation:

• Deleting specific requirements (A ‘top down’ lens should be applied – balanced and relevant to users); and

• Enhancing use of materiality in financial reporting disclosures

• 30-40% reduction in disclosure.

Current materiality approach

Source: Losing the excess baggage discussion paper, July 2011, NZICA/ICAS

Proposed materiality approach

Source: Losing the excess baggage discussion paper, July 2011, NZICA/ICAS

Significant focus in the area of clutter

FRC Australia

• Managing Complexity Report, Oct 12

• FRC Survey on Financial Literacy of Australian Directors, Sept 12

• Corporate Governance Principals to reflect steps entities undertake

to ensure directors have adequate financial literacy when signing

financial statements (post-Centro)

• Examine current financial reporting regime – better

explained/understood, and (if necessary) rationalisation.

Significant focus in the area of clutter

ASIC bi-annual surveillance project

• Surveillance will focus on material disclosures of information useful

to investors and other users of financial reports; and

• ASIC will not pursue immaterial disclosures that may add

unnecessary clutter to financial reports.

Significant focus in the area of clutter

Financial Reporting Specialists ‘EFLICKS’

• Reduce disclosure by thinking EFLICKS

Essential

Fundamental

Legacy

Important

Critical

Key

Significant.

Give the disclosures the EFLICKS

Significant focus in the area of clutter

‘To disclose or not to disclose: Materiality is the question’

• AASB staff paper, Feb 2014

• Identified following reasons for disclosure overload:

– Time pressure – no time to reduce clutter

– Work (effort) required - time taken to justify something

immaterial, easier to just disclose

– Lengthy debates with auditors - default position to include

disclosure; discussion required on using AASB 101.31 to

reduce immaterial disclose.

Significant focus in the area of clutter

‘To disclose or not to disclose: Materiality is the question’

• Identified following reasons for disclosure overload (continued) :

– Judgement – required for not disclosing; easier not to make

decision and just disclose

– Following the leader – follow others especially in same

industry. “Two wrongs don’t make a right” (auditors also guilty

= point to other examples to justify disclosures being

required)

– Fear of regulators – ASIC!

Significant focus in the area of clutter

Use of materiality

• Although AASB 1031 has been withdrawn, AASB 101.31 states:

“An entity need not provide a specific disclosure required by an

Australian Accounting Standard, if the information is not

material.”

• AASB 101.7 states:

“Items are considered material if their omission or

misstatement, individually or collectively, could influence the

economic decisions that users make on the basis of the

financial statements”.

Significant focus in the area of clutter

Use of materiality

• Materiality

– Consider size and nature of the item

– Professional judgement required (consider both quantitative and

qualitative aspects of information)

– Entity specific.

• Disclosure must be useful:

– For resource allocation decision making

– Possess the qualitative characteristics

– Not include immaterial information.

Significant focus in the area of clutter

Amendments to AASB 101 / IAS 1

• ED issued Q1, 2014 with Final standard expected Q4, 2014

• Limited clarifying amendments

• Removes language that prevents (perceived) rigid

presentation/format

• Proposals: • Materiality – apply to primary statements and notes

• Line items – disaggregation, subtotals

• Notes – flexibility of ordering

• Significant accounting policies – remove unhelpful examples.

Significant focus in the area of clutter

Other activities of IASB

• AASB 7 amendment: Reconciliation of financial liabilities from

financing activities

• Research projects on:

• Materiality – consistent application

• Principals of disclosure – that apply across IFRS (parallel

with Conceptual Framework)

• Review of existing standards for redundancies, conflicts and

duplications

• Digital reporting – IFRS Taxonomy, XBRL.

Streamlining – restructuring financial statements

• Structure notes in order of importance

• Group notes by nature

• Disclose only those significant accounting policies – combine with

relevant notes

Streamlining – restructuring financial statements

Advantages Disadvantages

Easier to understand? Bunching

together like items

Difficult to find things

More important items at front (least

important at back)

Logical layout?

Requires judgement

Looks different – outside the norm

Trendy?

Not really reducing clutter

Improves shareholder

communication

Reduces comparability between

companies

Streamlining – Wesfarmers 2014 Annual Report

Investor confidence

• Uncluttered and well thought-out financial statements improves

investor/user confidence

• Cluttered financial statements (especially if riddled with errors)

decreases investor/user confidence

• Consider materiality rather than just disclose ‘everything but the

kitchen sink’.

Agenda

• Problem with financial reporting

• Cutter in financial statements

• Practical example: review financial

statements

• Recap and reflection.

Practical example

Please review the example financial statements “Pinnacle Defect Pty

Limited” and identify:

- Areas of clutter that could be removed

- Errors that you would want to change

Note:

- Assume all numbers tie in, add up and cross-cast and referencing is

correct

- Only look at what is there, not what is not there.

Practical example –directors’ report

- Employee numbers no longer required

- Why not round?

- Comparatives not required

- Potential breach of insurance policy.

Practical example – P&L section

- Function vs nature

- Profit and loss.

Practical example – balance sheet section

- Negative figure should be reclassified (this is also common for income tax).

Practical example – equity section

- consistency!

Practical example – New accounting standards adopted

- Shopping list of irrelevant new standards that are not applicable or

insignificant

Practical example – Basis of preparation

- Special purpose can not state compliance with IFRS.

Practical example – significant accounting policies

- Policy not tailored to the client.

Practical example – significant accounting policies

- redundant policy as no disposal group or held for sale.

Practical example – New standards not early adopted

- Simple way to comply with AASB 108.31 without shopping list

Caution: not advisable for listed entities.

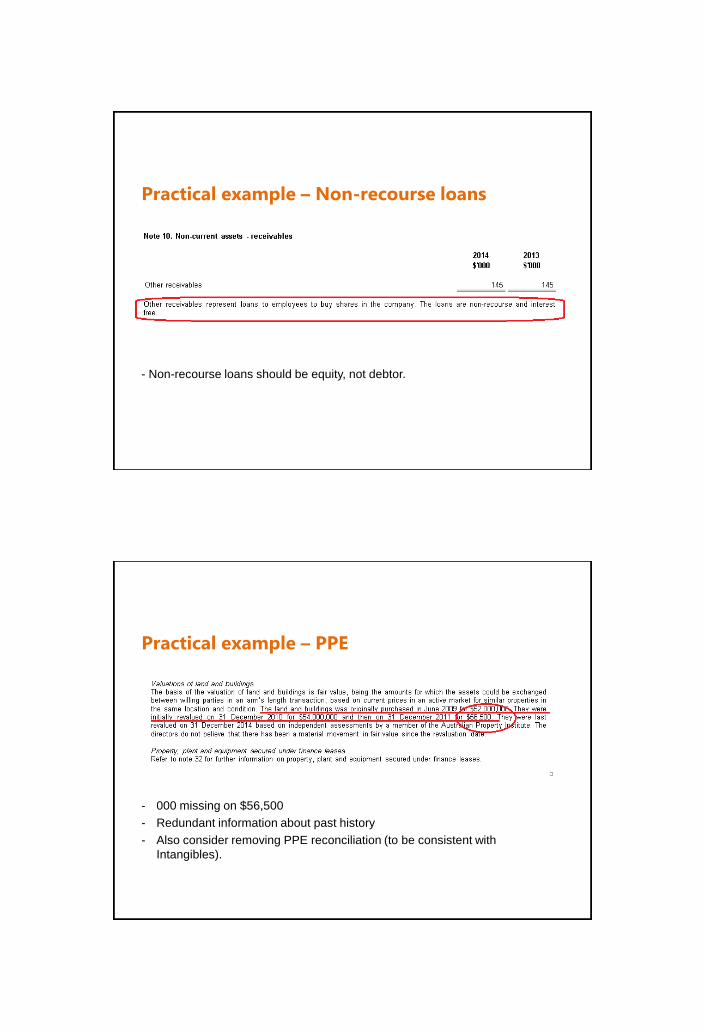

Practical example – Non-recourse loans

- Non-recourse loans should be equity, not debtor.

Practical example – PPE

- 000 missing on $56,500

- Redundant information about past history

- Also consider removing PPE reconciliation (to be consistent with

Intangibles).

Practical example – employee benefits

- New AASB 119 , equally applies to AL as LSL.

Practical example – convertible note

- No $, and why A$ ?

- Where is equity component?

- Current classification ?

- What about information on how conversion will occur? e.g. number of shares etc.

rather than what happened in 2003.

Practical example - remuneration of auditors

- Split wrong

- Should be unrounded in accordance with CO 98/100 (similar comment to KMP and related party disclosures).

Practical example – finance leases

How can the total commitment < 1yr be lower than the liability recorded?

Practical example – economic dependency

- Economic dependency no longer required.

Practical example – directors’ declaration

- CFO/CEO declaration only required for listed entities.

Practical example – Increase/(decrease) order

Others not covered in practical example

• Profit/(loss) or (Loss)/profit => change for change sake!

• Always “Other comprehensive income”, and not:

– Other comprehensive income/(loss)

– Other comprehensive loss

• Not rounding in narrative

• Removing unnecessary notes that add no value?

Others not covered in practical example –

Auditors report

• Report referring to note 1 for going concern when it could be note 2

• Referring to statement of profit and loss and other comprehensive

income

• Referring to statement of comprehensive income (when statements

have adopted new name)

• Referring to ‘condensed’ in interim, when primary statements are not

condensed.

Agenda

• Problem with financial reporting

• Clutter in financial statements

• Practical example: review financial

statements

• Recap and reflection.

Recap and reflection

• Quality of financial statements could improve by reducing clutter

• Good financial statements improves investor confidence

• Time and effort is required

• Co-operation between auditors and preparers required

• Ensure proper application of :

- Checklists

- Review procedures

- Model accounts

- Significant judgement

- Materiality concept.

Recap and reflection

• Use clear, concise, plain language

• Logical layout of financial statements

• Don’t simply repeat last year, as circumstances change

• Don’t blindly copy other entity disclosures

• Remove immaterial accounting policies

• Don’t fear ASIC – not pursuing immaterial disclosures

• Auditors – not to qualify if non-disclosure is justified on materiality

• Think EFLICKS.

Disclaimer

This slide deck is intended for presentation purposes only. It is general

information and is not specific business advice or financial advice and no

person should rely on the contents without first obtaining advice from a

qualified professional person acting in that role or reference to source materials

such as the Corporations Act or Accounting Standards.

Neither Financial Reporting Specialists, related entities, directors, officers and

employees do not accept any contractual, tortuous or other form of liability for

this content or for any consequence arising from its use or for omissions or

errors, including responsibility to any person by reason of negligence.

© 2014 Financial Reporting Specialists