financial statements and taxes - lakehead...

TRANSCRIPT

Financial Statements and Taxes

RWJR, Chapter 2

September 2004

Outline of the Lecture

2.1 The Balance Sheet

2.2 The Income Statement

2.3 Cash Flow

2.4 Taxes

2.5 Capital Cost Allowance

2

2.1 The Balance Sheet

The balance sheet is asnapshotof the firm.

It summarizes what the firm owns (assets) and what it owes

(liabilities).

Assets minus liabilities belongs to owners. It is defined as

shareholders’ equity.

Assets− Liabilities ≡ Shareholders’ Equity.

3

2.1 The Balance Sheet

Assetsappear on the left-hand side of the balance sheet, and can

be of two types:

Current Assets: Assets that have a life of less than one year.

Cash, inventoryandaccounts receivableare examples of

current assets.

Fixed Assets: Assets that have a relatively long life. Fixed

assets can betangibleor intangible.

A building is a tangible asset.

A patent is an intangible asset.

4

2.1 The Balance Sheet

Liabilities appear on the right-hand side of the balance sheet,

and can also be of two types:

Current Liabilities: Liabilities that mature in less than one

year.Bank borrowingsandaccounts payableare examples

of current liabilities.

Long-Term Liabilities: Liabilities that mature in more than one

year.Long-term debtandemployee future benefitsare

examples of long-term liabilities.

5

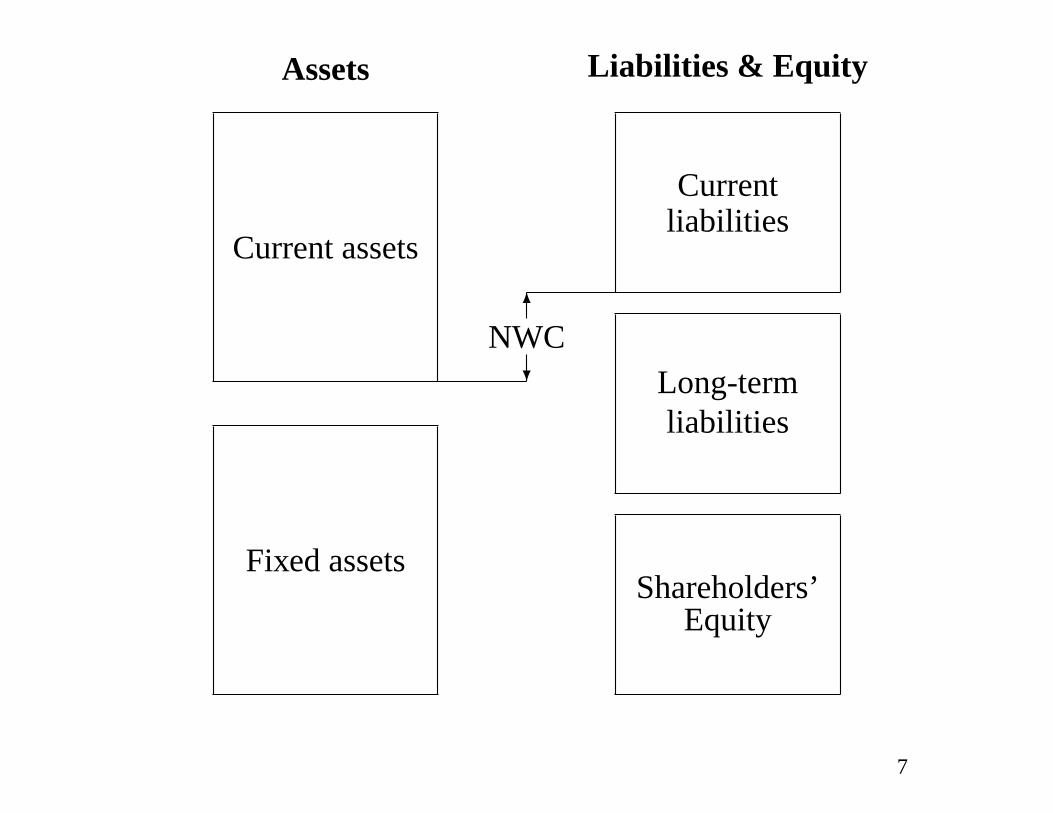

2.1 The Balance Sheet

TheNet Working Capital(NWC) is the difference between

current assets and current liabilities.

A positive NWC means that the cash available over the next 12

months exceeds what will have to be paid over that period.

NWC is usually positive in healthy firms.

6

Assets Liabilities & Equity

Current assets

Fixed assets

6NWC

?

Currentliabilities

Long-termliabilities

Shareholders’Equity

7

Liquidity

Liquidity refers to the ease with which an asset can be converted

to cash.

Bank accounts, T-bills and similar assets are relatively liquid.

Inventory is less liquid: There is no guarantee the merchandise

will be sold.

Fixed assets are relatively illiquid.

Assets on the balance sheet are listed from the most liquid to the

least liquid.

8

Debt Versus Equity

Debtholders are the first claimants to the firm’s cash flows.

Shareholders are the residual claimants to the firm’s cash flows.

Were the firm liquidated today, the proceeds from the sale of

assets would first be used to repay debt and anything left would

be distributed among shareholders.

The use of debt in the firm’s capital structure is calledfinancial

leverage.

9

Sun-Rype Products LTD

Dec. 31, 2003, and Dec. 31, 2002, Balance Sheets ($000)

Assets Liabilities and Owners’ Equity

2003 2002 2003 2002

Cash & ST investments 8,595 1,894 Promissory notes 675 675Accounts receivable 10,259 10,183 Accounts payables 14,257 13,603Income taxes receivable 0 1,388 Income taxes payable 647 0Inventories 13,271 10,520 Current portion of LTD 504 30Prepaid expenses 416 372 Total current liabilities 16,083 14,308Future income tax benefit 288 401Total current assets 32,829 24,758 Long-term debt 153 389

Future income taxes 1,486 1,016Net fixed assets (NFA) 23,173 24,006 Total liabilities 17,722 15,713

Share capital & c. s. 18,797 18,688Retained earnings 19,483 14,363Total equity 38,280 33,051

Total assets 56,002 48,764 Total liabilities and equity 56,002 48,764

10

Market Value vs Book Value

Under theGenerally Accepted Accounting Principles, financial

statements show assets athistorical cost.

Assets are carried in the books at their purchase price, as this is

an objective, easily verifiable measure.

Market and book values may be close in the case of current

assets due to their short life.

In the case of fixed assets and equity, there may be substantial

differences between market and book values. Book values often

understate market values.

11

2.2 The Income Statement

Theincome statementmeasures the firm performance over some

period of time, generally a year.

The income shows what has happened between two balance

sheets.

The bottom line of the income statement is the net income or

earnings per share.

12

2.2 The Income Statement

Accounting principles are such that income is reported according

to an “accrual” rule, which provides a measure of current

operating performance.

Revenue and expense recognition are governed by thematching

principle, which states that operating performance can be

measured only if related revenues and expenses are accounted for

during the same period.

Hence accounting income and actual cash flow may be very

different.

13

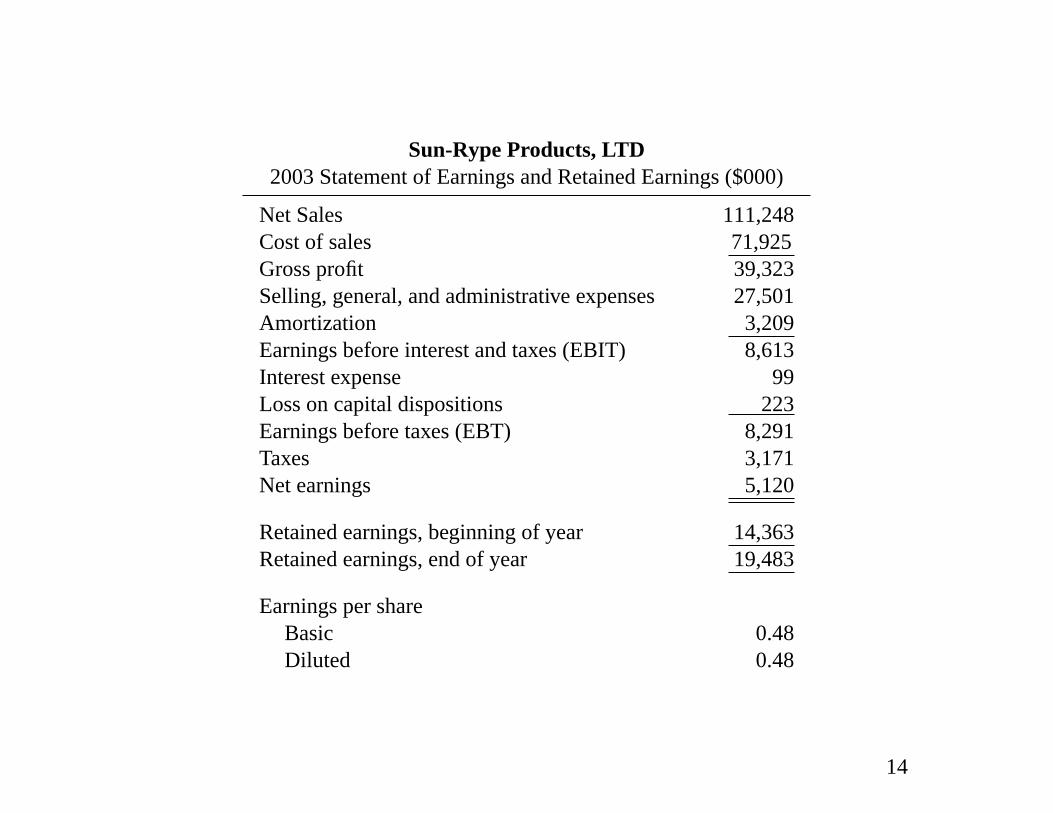

Sun-Rype Products, LTD2003 Statement of Earnings and Retained Earnings ($000)

Net Sales 111,248Cost of sales 71,925Gross profit 39,323Selling, general, and administrative expenses 27,501Amortization 3,209Earnings before interest and taxes (EBIT) 8,613Interest expense 99Loss on capital dispositions 223Earnings before taxes (EBT) 8,291Taxes 3,171Net earnings 5,120

Retained earnings, beginning of year 14,363Retained earnings, end of year 19,483

Earnings per shareBasic 0.48Diluted 0.48

14

2.2 The Income Statement

Due to the matching principle, accounting income differs from

cash flow because the income statement containsnon-cash items.

Amortizationandloss on capital dispositionsare examples of

non-cash expenses.

There are other non-cash expenses that do not appear explicitely

on the income statement. For example, some of the taxes

reported on the income statement may not be paid in the current

period.Deferred taxesaccumulate in a long-term liability

account on the balance sheet.

15

2.2 The Income Statement

Amortization is a good example of the accrual concept of

income: Consider a $5,000 machine that will be used over five

years, at the end of which its value is expected to be zero. If

depreciation is straight-line, this machine loses $1,000 of its

value per year, seemingly the cost of using the machine as it

produces output.

16

2.2 The Income Statement

In the case of Sun-Rype, deferred taxes is the net change is all

thefuture tax itemson the balance sheets.

From 2002 to 2003, the current asset “future income tax benefit”

has decreases by 113, i.e. from 401 to 288, and the liability

“future income taxes” has increased by 470, i.e. from 1,016 to

1,486.

Deferred taxes in 2003 is then the net change in future taxes, i.e.(1,486−288

)−

(1,016−401

)= 583.

17

The Statement of Cash Flows

This is another financial statement companies must complete.

It provides a summary of inflows and outflows of cash over the

same period as the income statement.

This statement provides insight into the firm’s operating,

investing and financing cash flows and reconciles them with

changes in cash and marketable securities.

18

The Statement of Cash Flows

The statement of cash flow takes a closer look at the cash events

that occurred during the year.

To this end, sources and uses of cash need to be defined.

• Activities that bring cash to the firm are calledsources of

cash.

• Activities that involve spending cash are calleduses of cash.

19

The Statement of Cash Flows

Sources and Uses of Cash

An increase in a liability, (e.g. accounts payable) is a source of

cash.

A decrease in a liability is a use of cash.

An increase in an asset (e.g. inventory) is a use of cash.

A decrease in an asset is a source of cash.

20

The Statement of Cash Flows

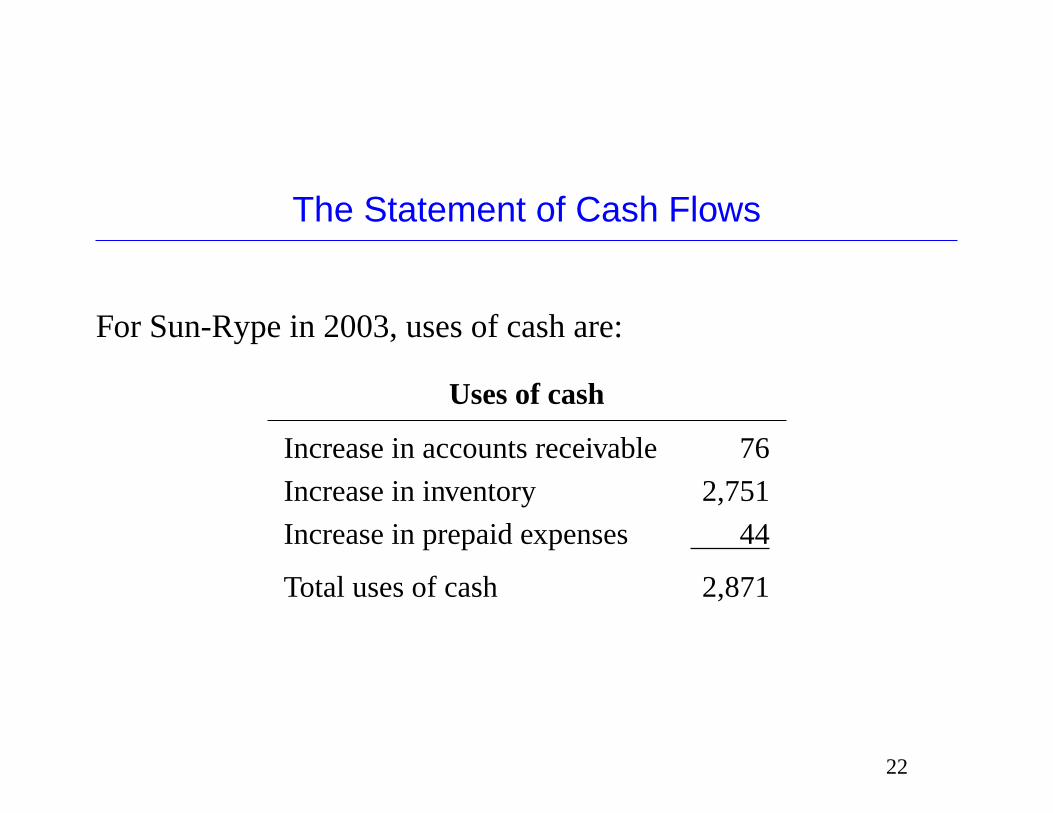

For Sun-Rype in 2003, sources of cash are:

Sources of cash

Decrease in income taxes receivable 1,388Decrease in future income tax benefit 113Decrease in net fixed assets 833Increase in accounts payable 654Increase in income taxes payable 647Increase in long-term debt 238Increase in future income taxes 470Increase in share capital 109Increase in retained earnings 5,120Total sources of cash 9,572

21

The Statement of Cash Flows

For Sun-Rype in 2003, uses of cash are:

Uses of cash

Increase in accounts receivable 76

Increase in inventory 2,751

Increase in prepaid expenses 44

Total uses of cash 2,871

22

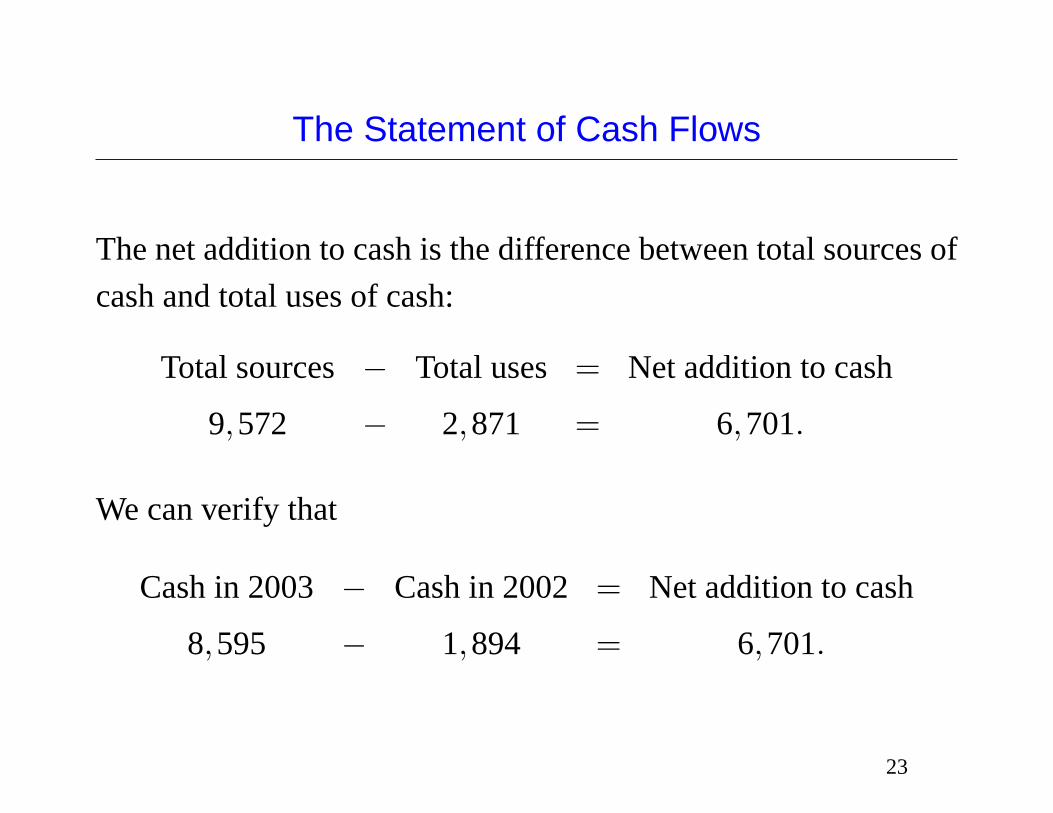

The Statement of Cash Flows

The net addition to cash is the difference between total sources of

cash and total uses of cash:

Total sources− Total uses = Net addition to cash

9,572 − 2,871 = 6,701.

We can verify that

Cash in 2003 − Cash in 2002 = Net addition to cash

8,595 − 1,894 = 6,701.

23

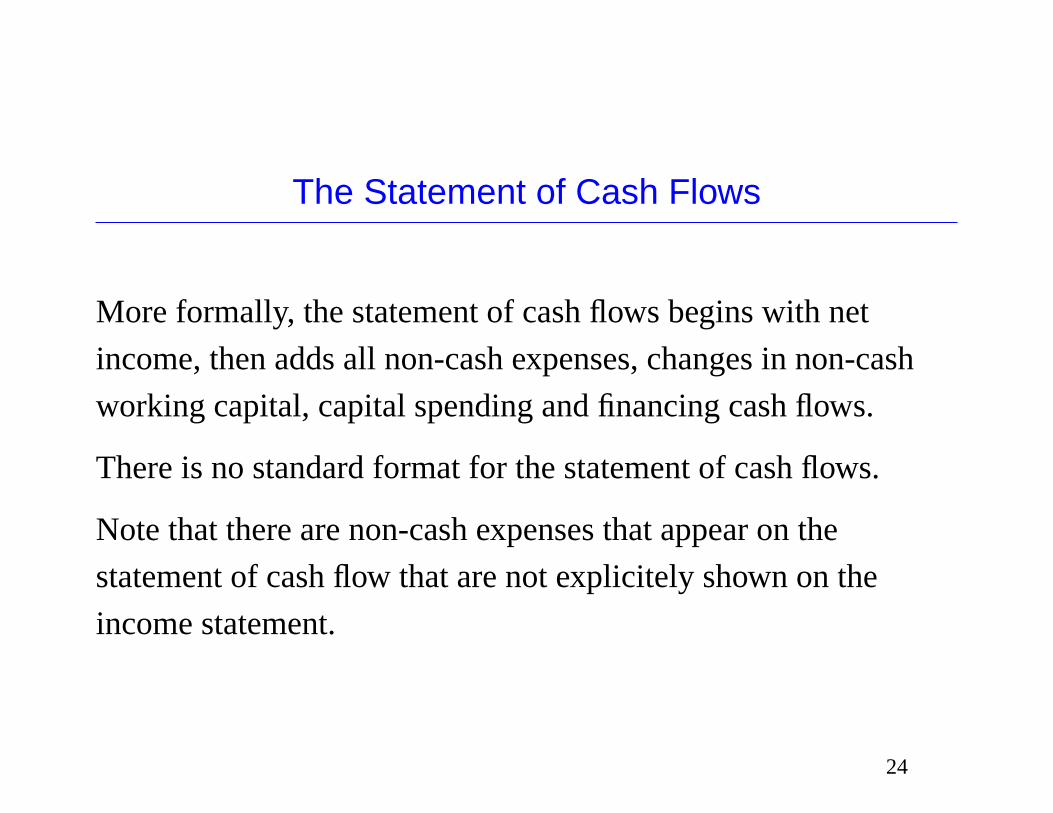

The Statement of Cash Flows

More formally, the statement of cash flows begins with net

income, then adds all non-cash expenses, changes in non-cash

working capital, capital spending and financing cash flows.

There is no standard format for the statement of cash flows.

Note that there are non-cash expenses that appear on the

statement of cash flow that are not explicitely shown on the

income statement.

24

Sun-Rype Products, LTD2003 Statement of Cash Flows

Cash from operating activitiesNet earnings 5,120Non-cash items:

Amortization 3,209Loss on capital dispositions 223Deferred taxes 583Other 267

Net cash from operations 9,420Changes in non-cash working capital items (182)

Net cash from operating activities 9,220

Cash from investing activitiesNet capital spending (2,599)

Net cash from investing activities (2,599)

Cash from financing activitiesCapital lease payment (29)Change in share capital 109

Net cash from financing activities 80

Net change in cash 6,701

25

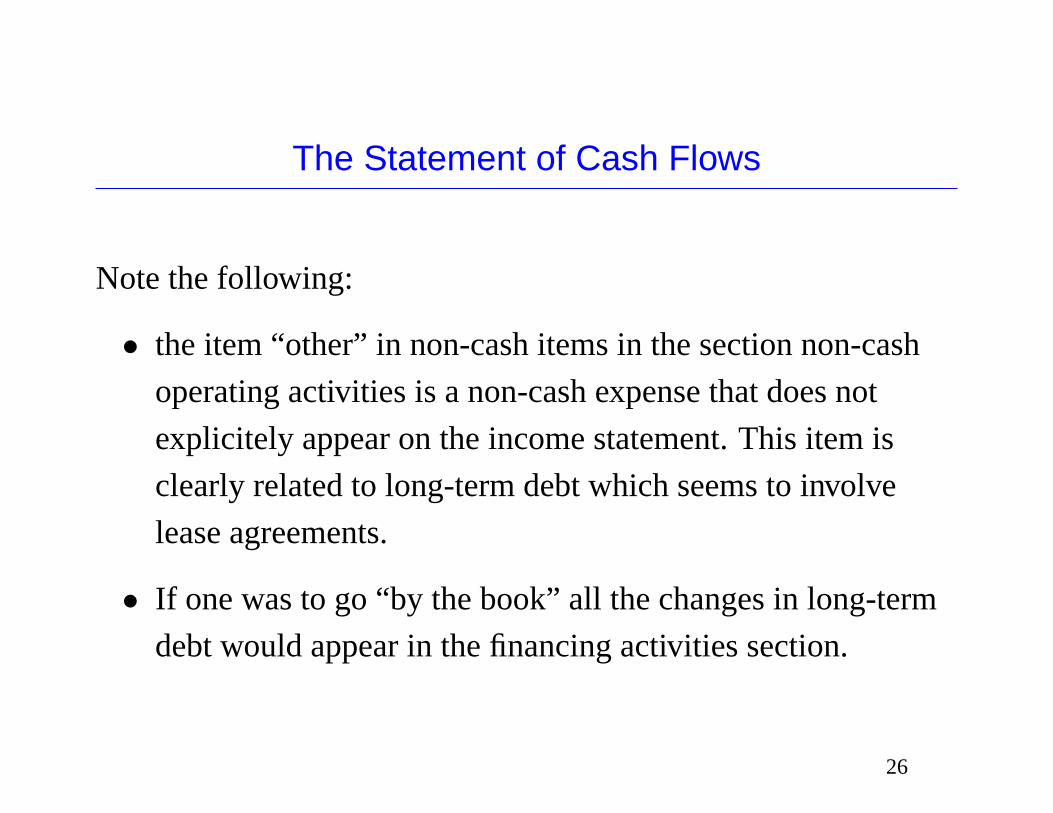

The Statement of Cash Flows

Note the following:

• the item “other” in non-cash items in the section non-cash

operating activities is a non-cash expense that does not

explicitely appear on the income statement. This item is

clearly related to long-term debt which seems to involve

lease agreements.

• If one was to go “by the book” all the changes in long-term

debt would appear in the financing activities section.

26

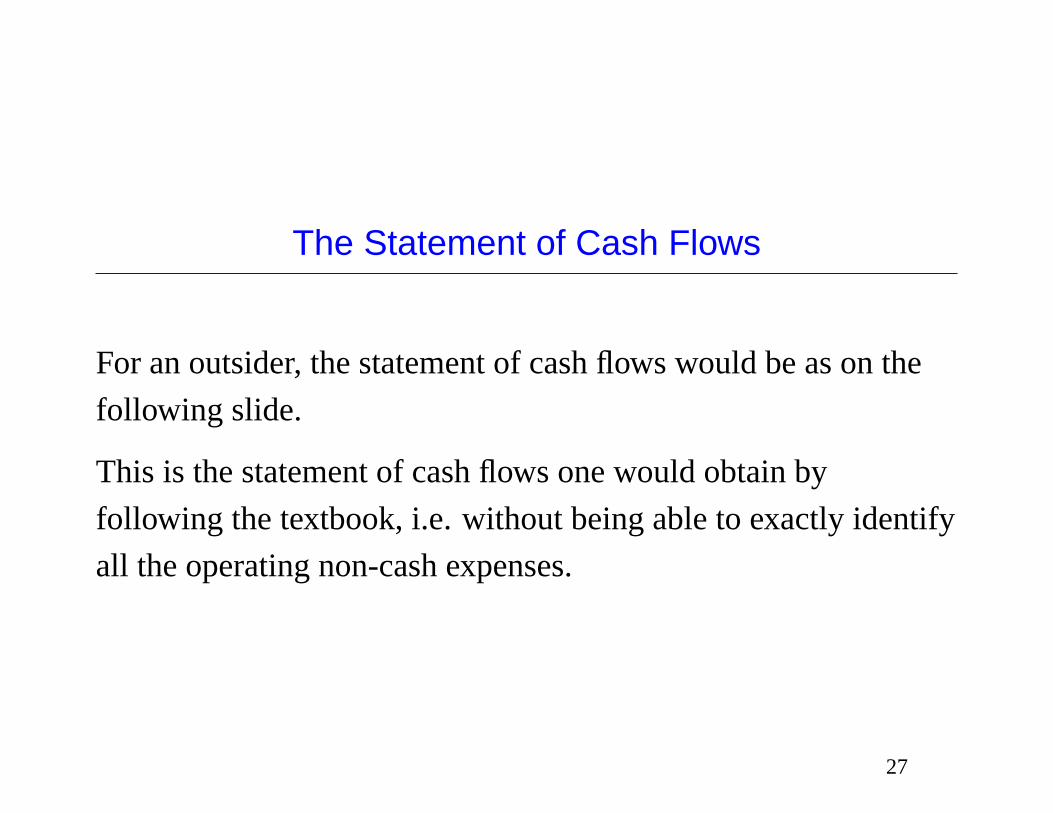

The Statement of Cash Flows

For an outsider, the statement of cash flows would be as on the

following slide.

This is the statement of cash flows one would obtain by

following the textbook, i.e. without being able to exactly identify

all the operating non-cash expenses.

27

Sun-Rype Products, LTD2003 Statement of Cash Flows (Textbook Method)

Cash from operating activitiesNet earnings 5,120Non-cash items:

Amortization 3,209Loss on capital dispositions 223Deferred taxes 583

Net cash from operations 9,135Changes in non-cash working capital items (182)

Net cash from operating activities 8,953

Cash from investing activitiesNet capital spending (2,599)

Net cash from investing activities (2,599)

Cash from financing activitiesChange in promissory notes 0Change in LTD 238Change in share capital 109

Net cash from financing activities 347

Net change in cash 6,701

28

2.3 Cash Flow

Cash flowis one of the most important piece of information that

can be obtained from financial statements.

Cash flow is the most reliable measure of a borrower’s ability to

repay its debts.

In what follows, we calculatecash flow from asset, which may

also be calledfree cash flow. Note that there are different

definitions of free cash flow.

29

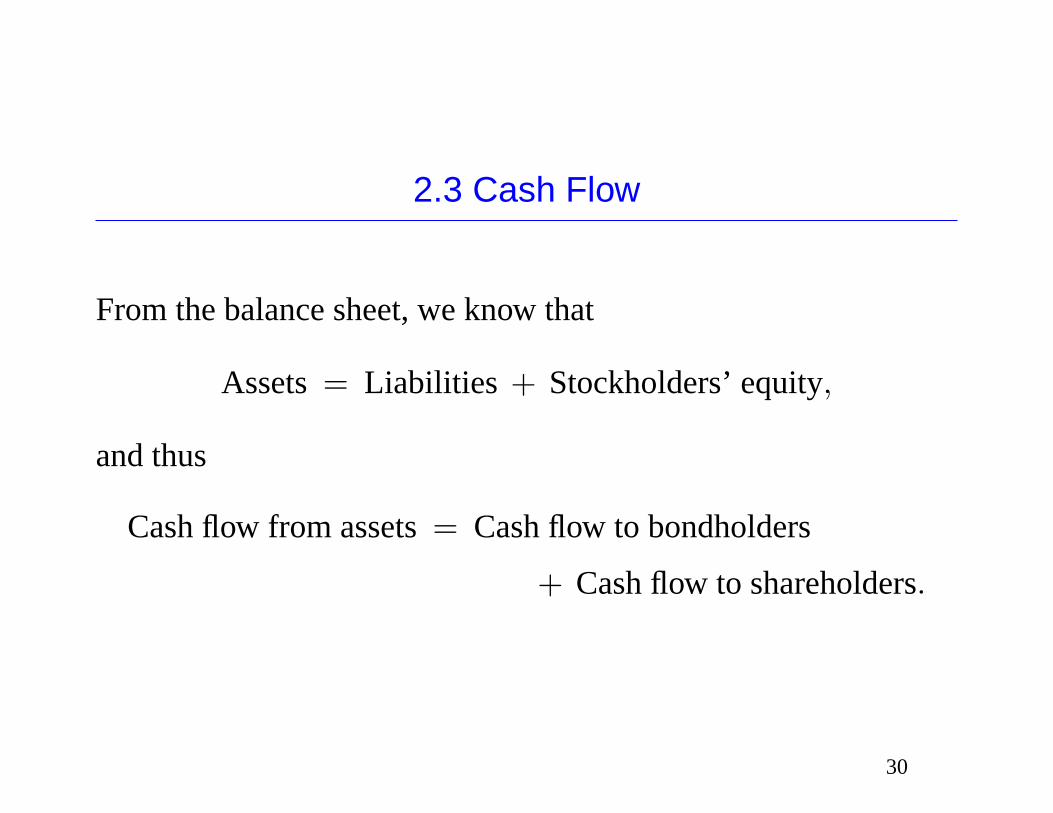

2.3 Cash Flow

From the balance sheet, we know that

Assets= Liabilities + Stockholders’ equity,

and thus

Cash flow from assets= Cash flow to bondholders

+ Cash flow to shareholders.

30

2.3 Cash Flow

Cash flow from assets (CF(A))has three components:

Operating cash flow (OCF): Cash flow resulting from

day-to-day activities.

Additions to net working capital (∆NWC): Net change in

short-term assets.

Net Capital spending (NCS): Net purchases of fixed assets.

31

2.3 Cash Flow

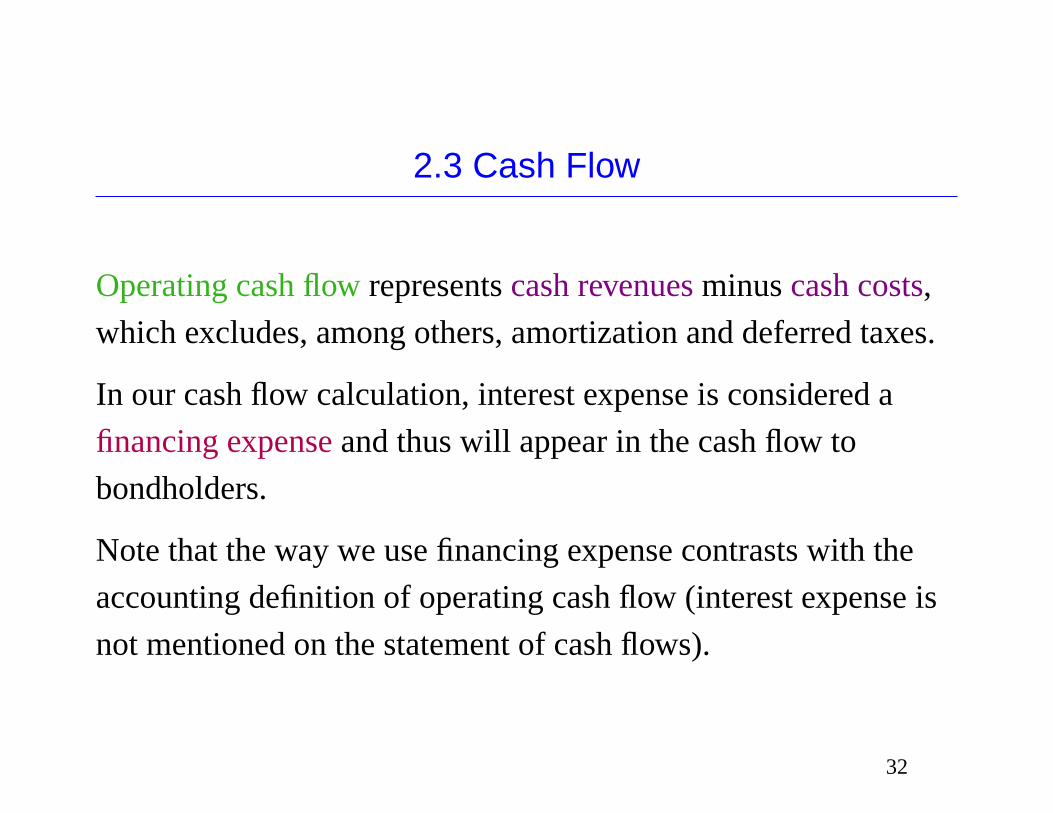

Operating cash flowrepresentscash revenuesminuscash costs,

which excludes, among others, amortization and deferred taxes.

In our cash flow calculation, interest expense is considered a

financing expenseand thus will appear in the cash flow to

bondholders.

Note that the way we use financing expense contrasts with the

accounting definition of operating cash flow (interest expense is

not mentioned on the statement of cash flows).

32

2.3 Cash Flow

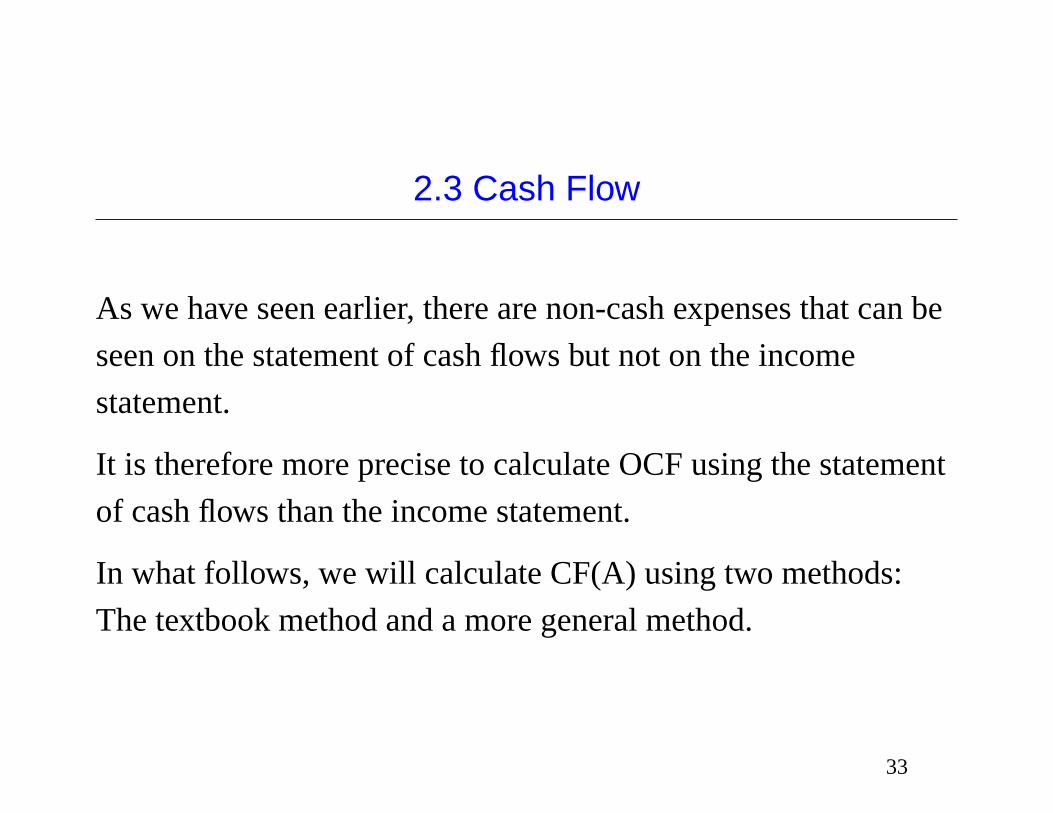

As we have seen earlier, there are non-cash expenses that can be

seen on the statement of cash flows but not on the income

statement.

It is therefore more precise to calculate OCF using the statement

of cash flows than the income statement.

In what follows, we will calculate CF(A) using two methods:

The textbook method and a more general method.

33

Cash Flow from Assets: Textbook Method

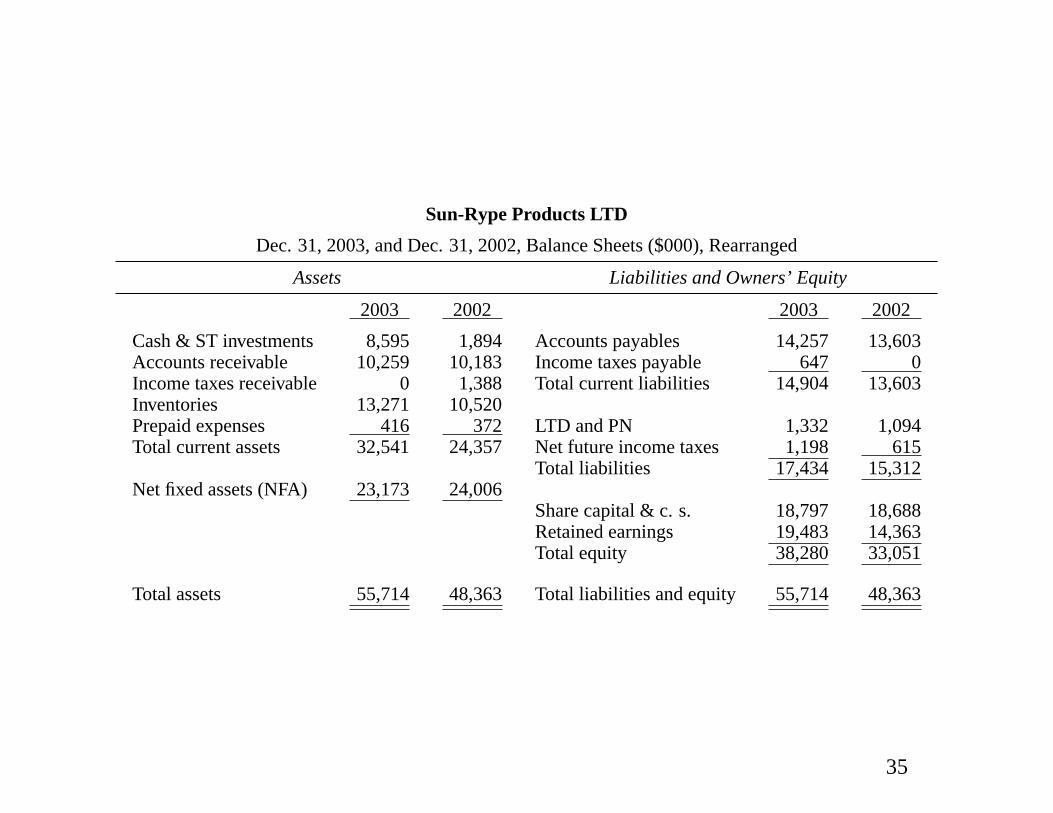

In order to follow the textbook method using Sun-Rype’s

financial statements, we will rearrange Sun-Rype’s balance sheet.

We will lump all future income taxes items in one “net future

income taxes” item and promissory notes and all long-term debt

items together.

34

Sun-Rype Products LTD

Dec. 31, 2003, and Dec. 31, 2002, Balance Sheets ($000), Rearranged

Assets Liabilities and Owners’ Equity

2003 2002 2003 2002

Cash & ST investments 8,595 1,894 Accounts payables 14,257 13,603Accounts receivable 10,259 10,183 Income taxes payable 647 0Income taxes receivable 0 1,388 Total current liabilities 14,904 13,603Inventories 13,271 10,520Prepaid expenses 416 372 LTD and PN 1,332 1,094Total current assets 32,541 24,357 Net future income taxes 1,198 615

Total liabilities 17,434 15,312Net fixed assets (NFA) 23,173 24,006

Share capital & c. s. 18,797 18,688Retained earnings 19,483 14,363Total equity 38,280 33,051

Total assets 55,714 48,363 Total liabilities and equity 55,714 48,363

35

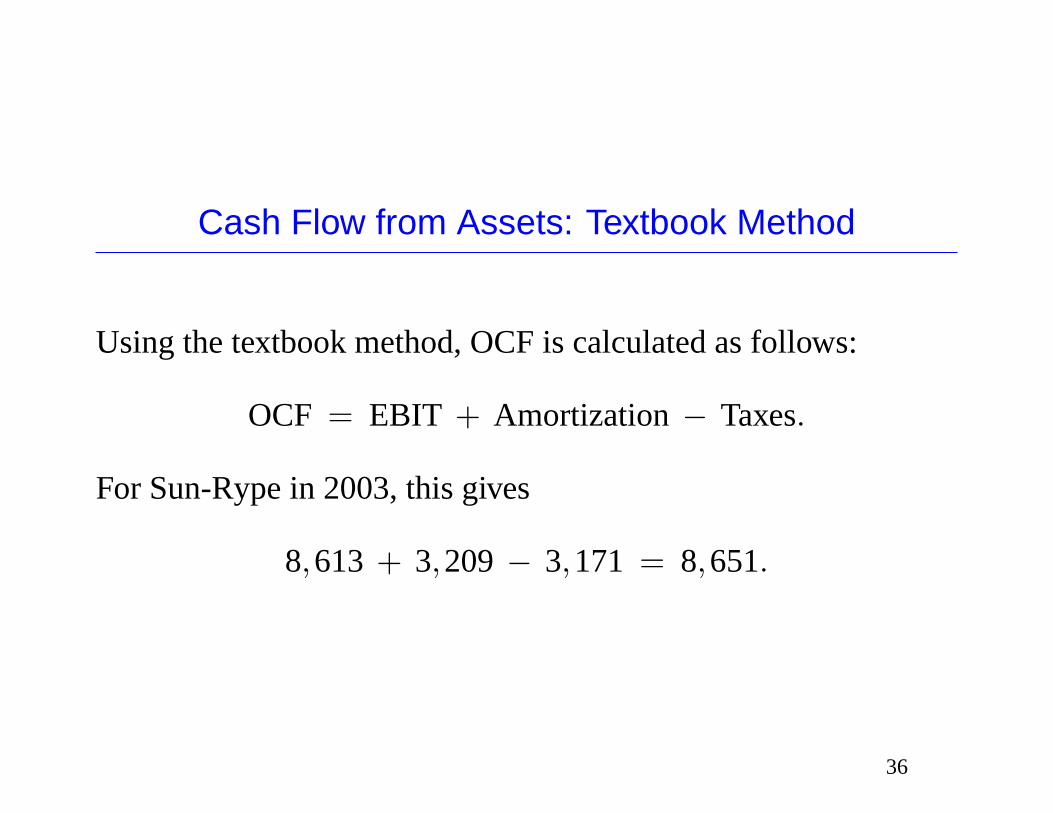

Cash Flow from Assets: Textbook Method

Using the textbook method, OCF is calculated as follows:

OCF = EBIT + Amortization− Taxes.

For Sun-Rype in 2003, this gives

8,613 + 3,209− 3,171 = 8,651.

36

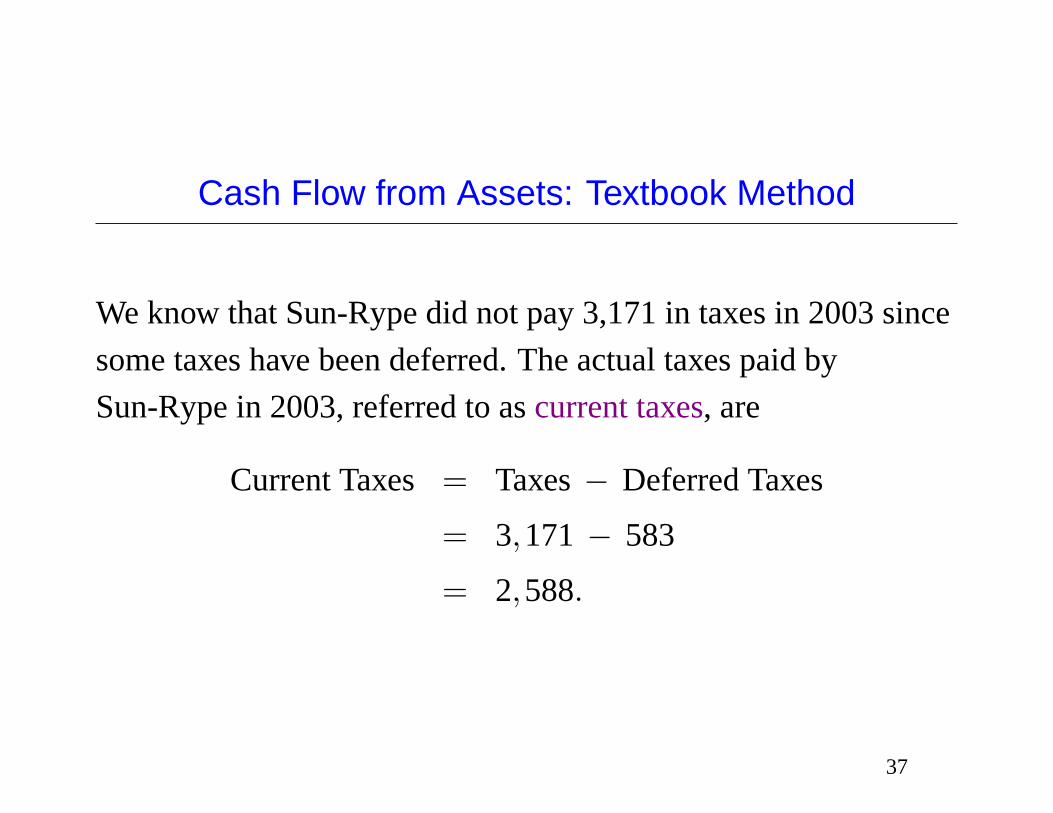

Cash Flow from Assets: Textbook Method

We know that Sun-Rype did not pay 3,171 in taxes in 2003 since

some taxes have been deferred. The actual taxes paid by

Sun-Rype in 2003, referred to ascurrent taxes, are

Current Taxes = Taxes− Deferred Taxes

= 3,171− 583

= 2,588.

37

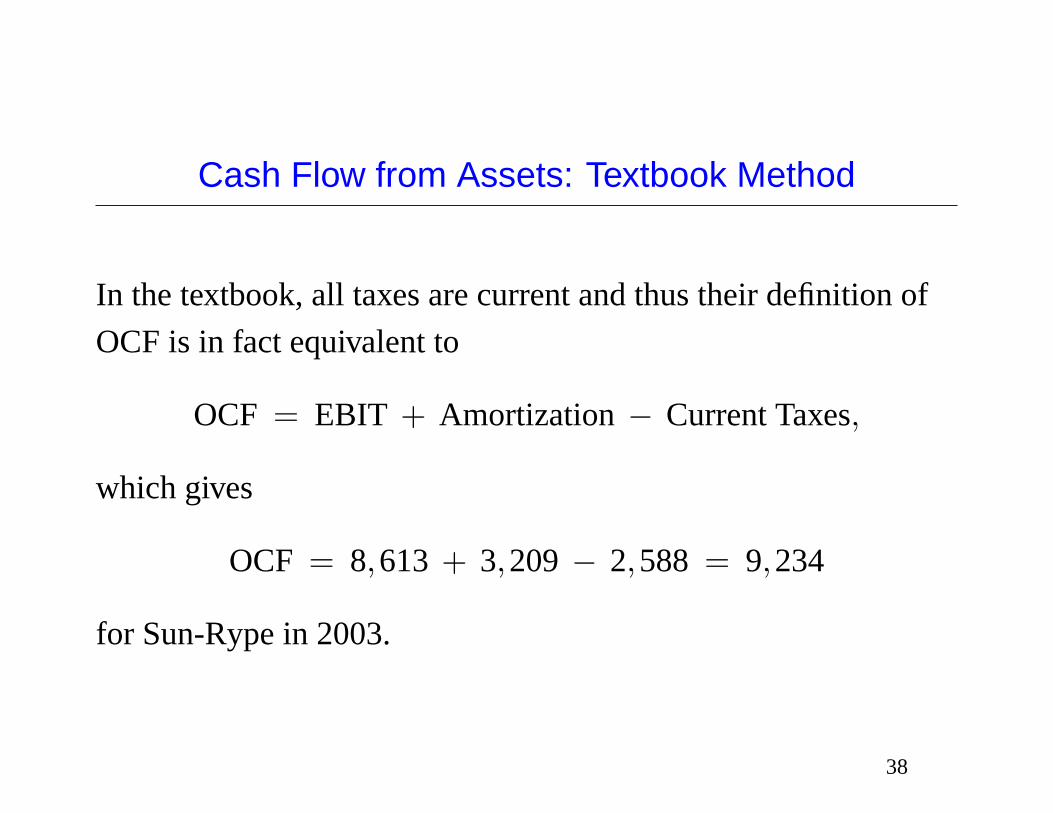

Cash Flow from Assets: Textbook Method

In the textbook, all taxes are current and thus their definition of

OCF is in fact equivalent to

OCF = EBIT + Amortization− Current Taxes,

which gives

OCF = 8,613 + 3,209− 2,588 = 9,234

for Sun-Rype in 2003.

38

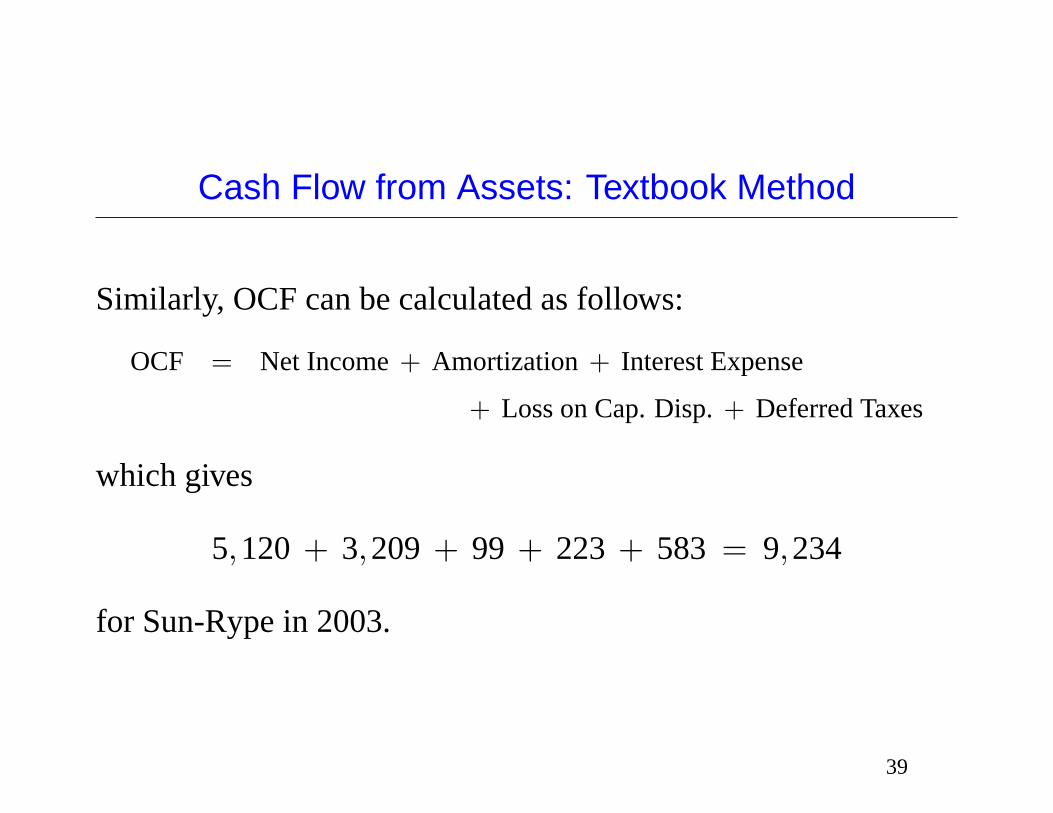

Cash Flow from Assets: Textbook Method

Similarly, OCF can be calculated as follows:

OCF = Net Income+ Amortization + Interest Expense

+ Loss on Cap. Disp.+ Deferred Taxes

which gives

5,120 + 3,209 + 99 + 223 + 583 = 9,234

for Sun-Rype in 2003.

39

Cash Flow from Assets: Textbook Method

∆NWC, in the textbook, is calculated as follows:

∆NWC = NWCend − NWCbeg.

For Sun-Rype in 2003, this gives

32,541−14,904−(

24,357−13,603)

= 6,883.

40

Cash Flow from Assets: Textbook Method

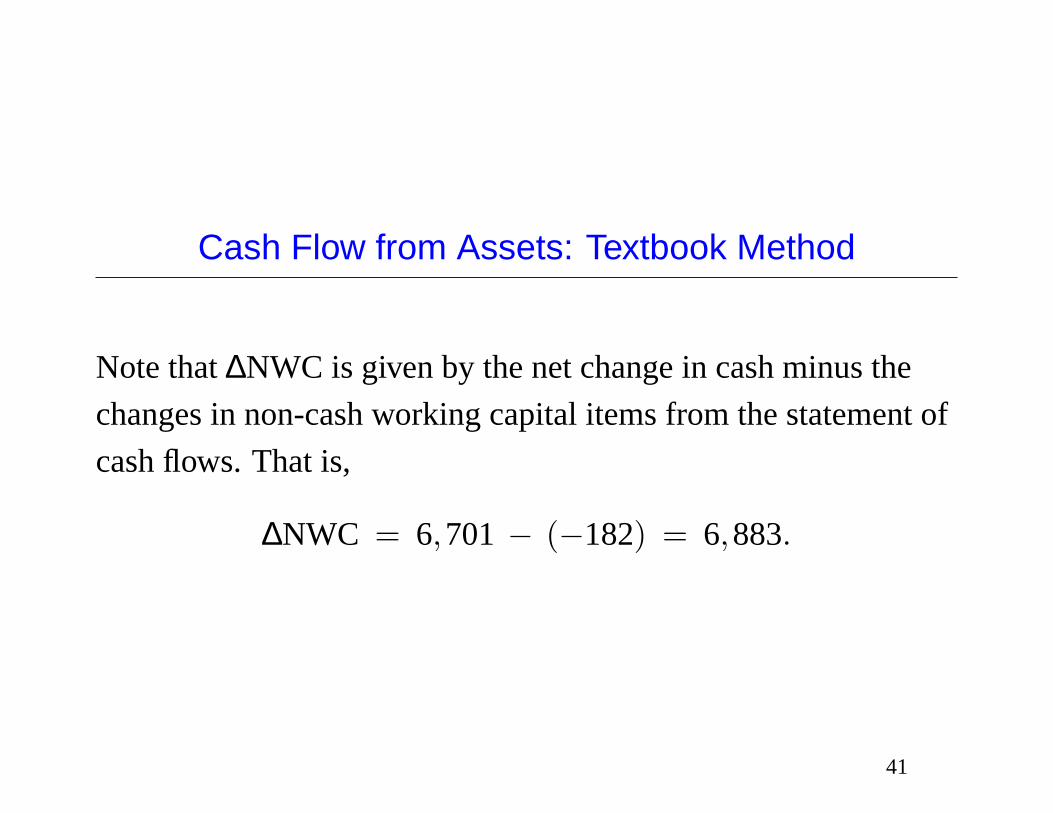

Note that∆NWC is given by the net change in cash minus the

changes in non-cash working capital items from the statement of

cash flows. That is,

∆NWC = 6,701− (−182) = 6,883.

41

Cash Flow from Assets: Textbook Method

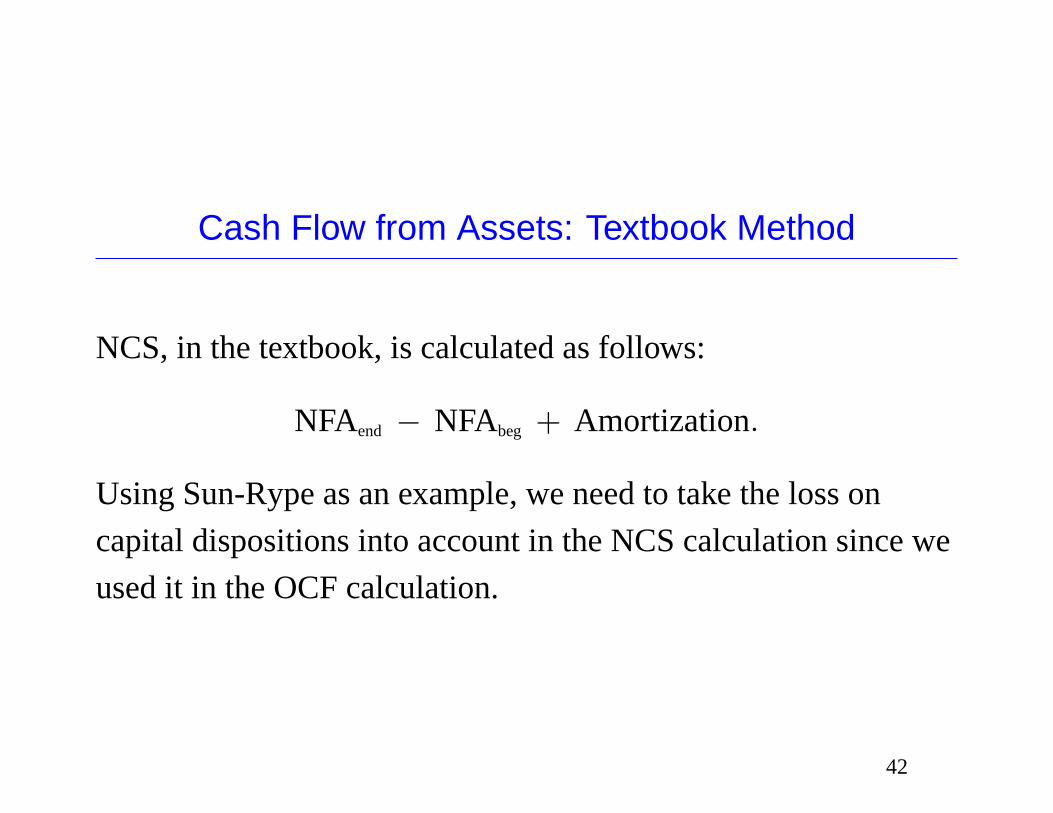

NCS, in the textbook, is calculated as follows:

NFAend − NFAbeg + Amortization.

Using Sun-Rype as an example, we need to take the loss on

capital dispositions into account in the NCS calculation since we

used it in the OCF calculation.

42

Cash Flow from Assets: Textbook Method

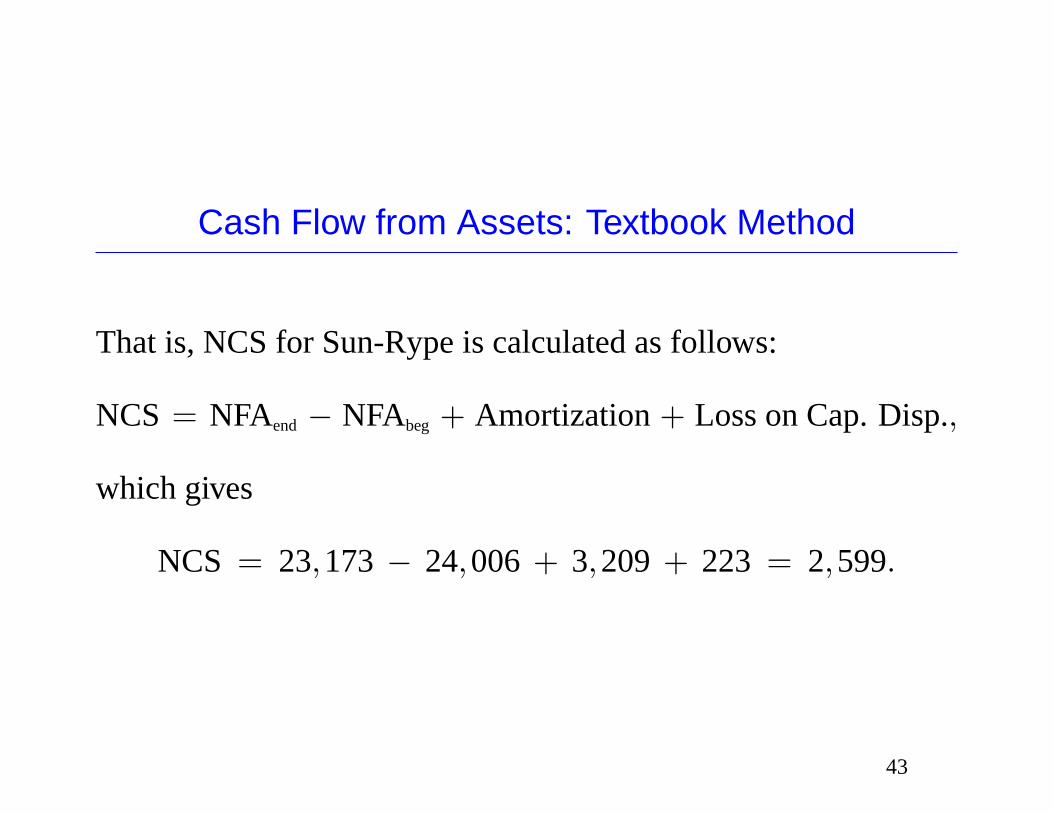

That is, NCS for Sun-Rype is calculated as follows:

NCS = NFAend− NFAbeg + Amortization+ Loss on Cap. Disp.,

which gives

NCS = 23,173− 24,006 + 3,209 + 223 = 2,599.

43

Cash Flow from Assets: Textbook Method

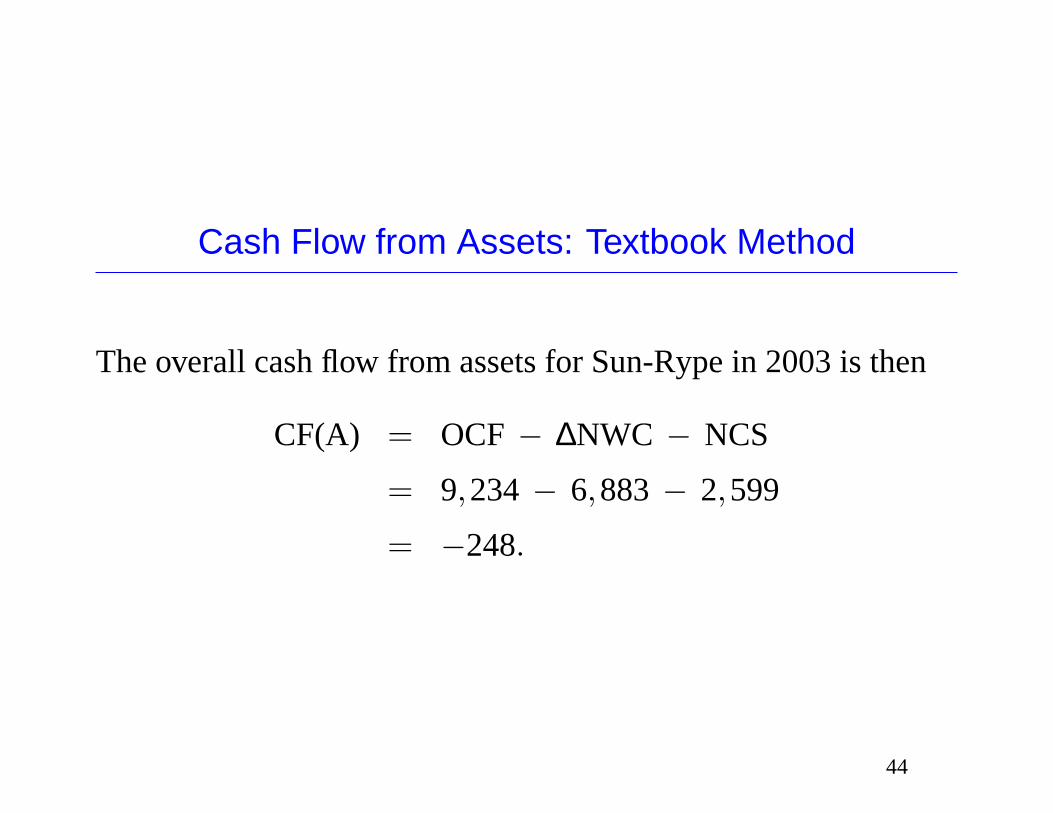

The overall cash flow from assets for Sun-Rype in 2003 is then

CF(A) = OCF− ∆NWC − NCS

= 9,234− 6,883− 2,599

= −248.

44

Cash Flow from Assets: Textbook Method

Let

CF(B) = Cash Flow to Bondholders

CF(S) = Cash Flow to Shareholders

and thus

CF(A) = CF(B) + CF(S).

45

Cash Flow from Assets: Textbook Method

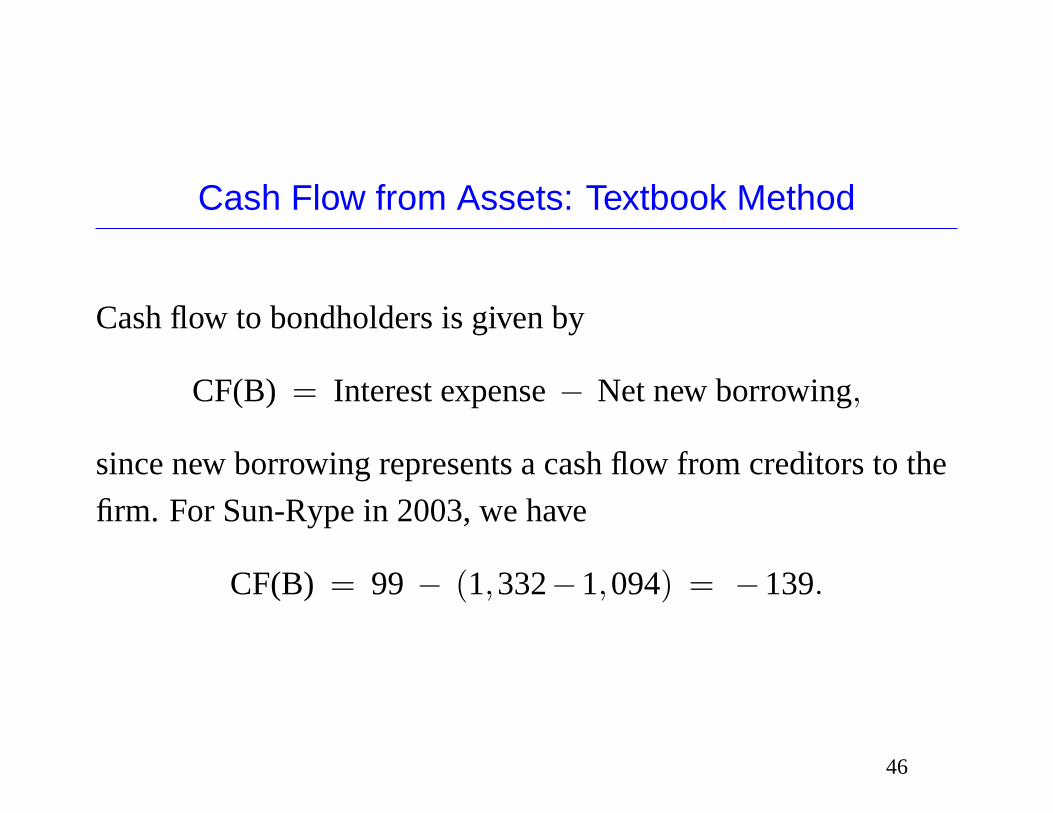

Cash flow to bondholders is given by

CF(B) = Interest expense− Net new borrowing,

since new borrowing represents a cash flow from creditors to the

firm. For Sun-Rype in 2003, we have

CF(B) = 99 − (1,332−1,094) = −139.

46

Cash Flow from Assets: Textbook Method

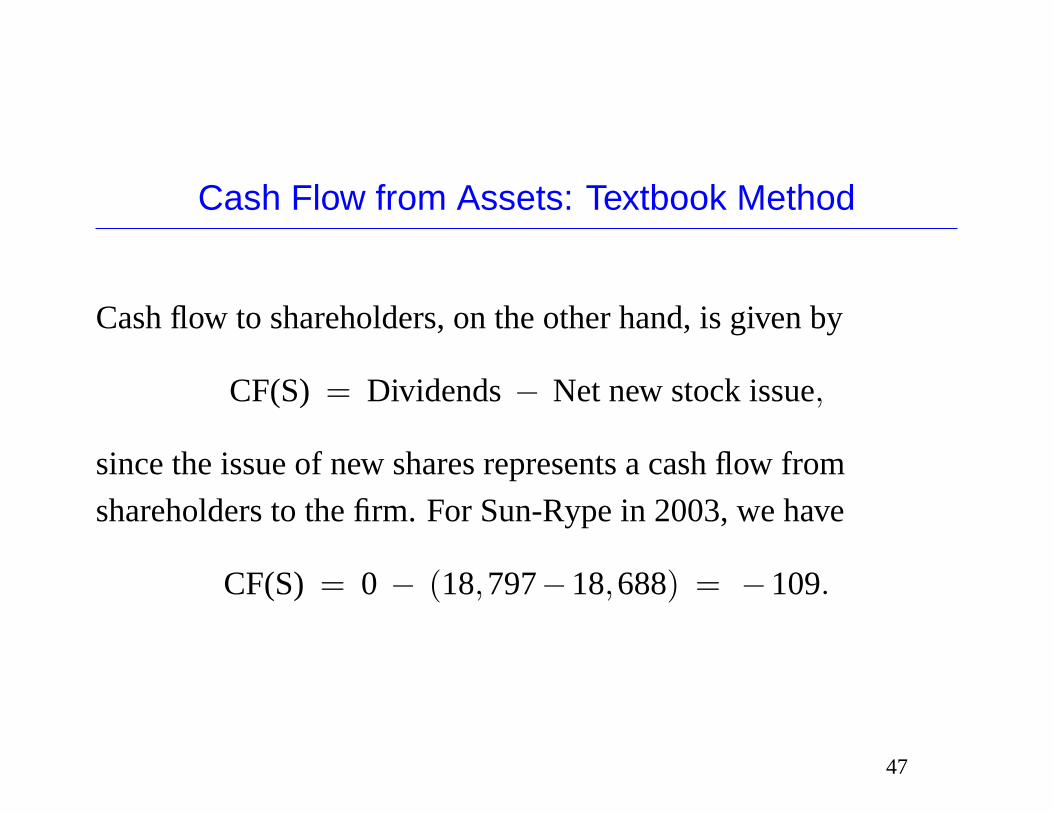

Cash flow to shareholders, on the other hand, is given by

CF(S) = Dividends− Net new stock issue,

since the issue of new shares represents a cash flow from

shareholders to the firm. For Sun-Rype in 2003, we have

CF(S) = 0 − (18,797−18,688) = −109.

47

Cash Flow from Assets: Textbook Method

We can see that

CF(A) = CF(B) + CF(S) = (−139) + (−109) = −248.

48

Cash Flow from Assets: A Different Method (optional)

We have seen that the statement of cash flows lists some non-cash

expenses that do not explicitely appear on the income statement.

Also, the changes in non-cash working capital items that appear

on the statement of cash flows may differ from what can be

calculated from the balance sheet.

49

Cash Flow from Assets: A Different Method (optional)

Let us first have a look atcash flow from operations (CFO).

CFO considers all operating cash flows, including changes in

non-cash working capital.

50

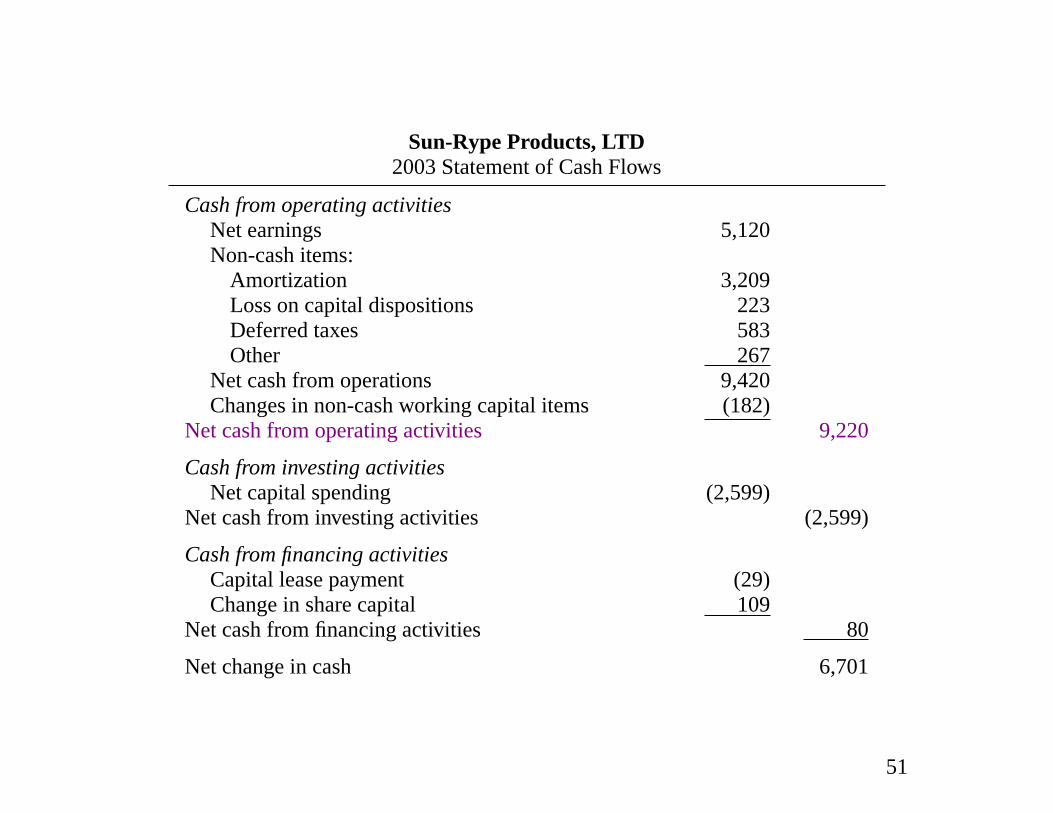

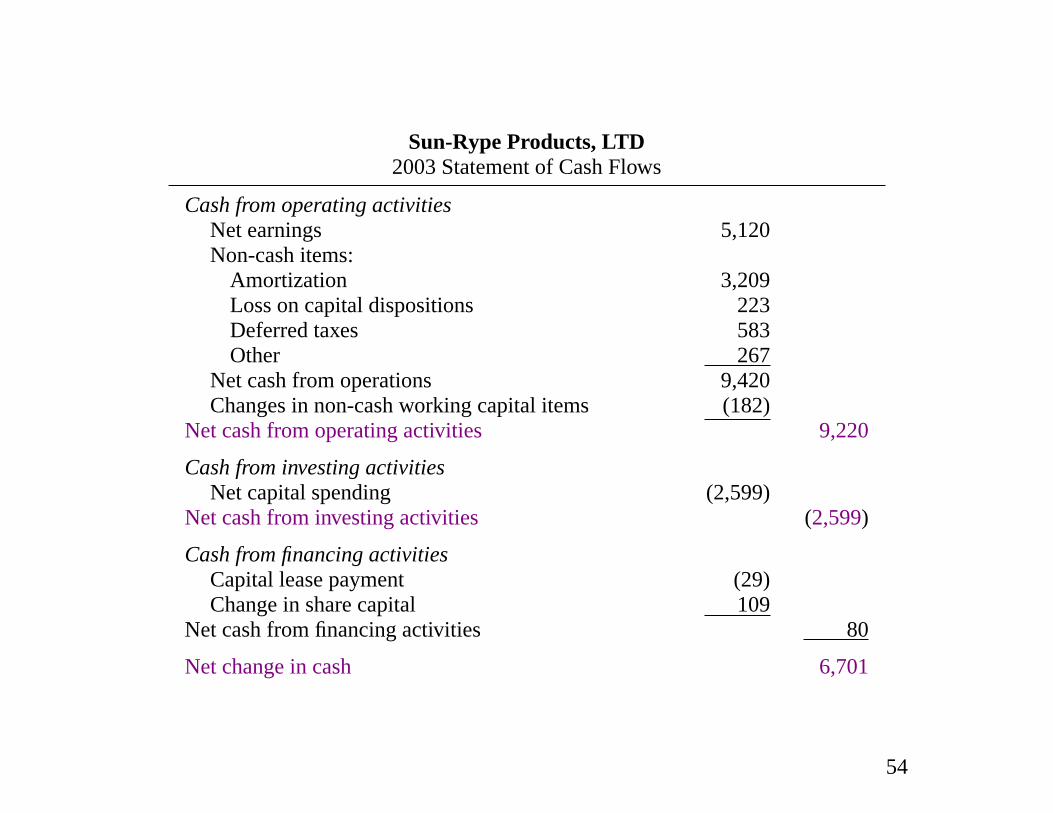

Sun-Rype Products, LTD2003 Statement of Cash Flows

Cash from operating activitiesNet earnings 5,120Non-cash items:

Amortization 3,209Loss on capital dispositions 223Deferred taxes 583Other 267

Net cash from operations 9,420Changes in non-cash working capital items (182)

Net cash from operating activities 9,220

Cash from investing activitiesNet capital spending (2,599)

Net cash from investing activities (2,599)

Cash from financing activitiesCapital lease payment (29)Change in share capital 109

Net cash from financing activities 80

Net change in cash 6,701

51

Cash Flow from Assets: A Different Method (optional)

CFO considers interest as an operating expense, we consider it as

a financing expense. We must therefore add back interest to CFO

in order to measure cash flow.

Note, however, that interest expense saves the company taxes

since interest is a tax-deductible expense.

To have a better feeling of the company’s ability to generate cash,

it then makes sense to add back theafter-tax interest expense.

52

Cash Flow from Assets: A Different Method (optional)

Net capital spending can also be found on the statement of cash

flows.

That is, we can usecash flow from investing activities (CFI)to

measure the firm’s net capital spending.

To finish, we also need to consider the change in cash. Whatever

is added to the firm’s cash account is not distributed to investors

and is thus condidered an outflow.

53

Sun-Rype Products, LTD2003 Statement of Cash Flows

Cash from operating activitiesNet earnings 5,120Non-cash items:

Amortization 3,209Loss on capital dispositions 223Deferred taxes 583Other 267

Net cash from operations 9,420Changes in non-cash working capital items (182)

Net cash from operating activities 9,220

Cash from investing activitiesNet capital spending (2,599)

Net cash from investing activities (2,599)

Cash from financing activitiesCapital lease payment (29)Change in share capital 109

Net cash from financing activities 80

Net change in cash 6,701

54

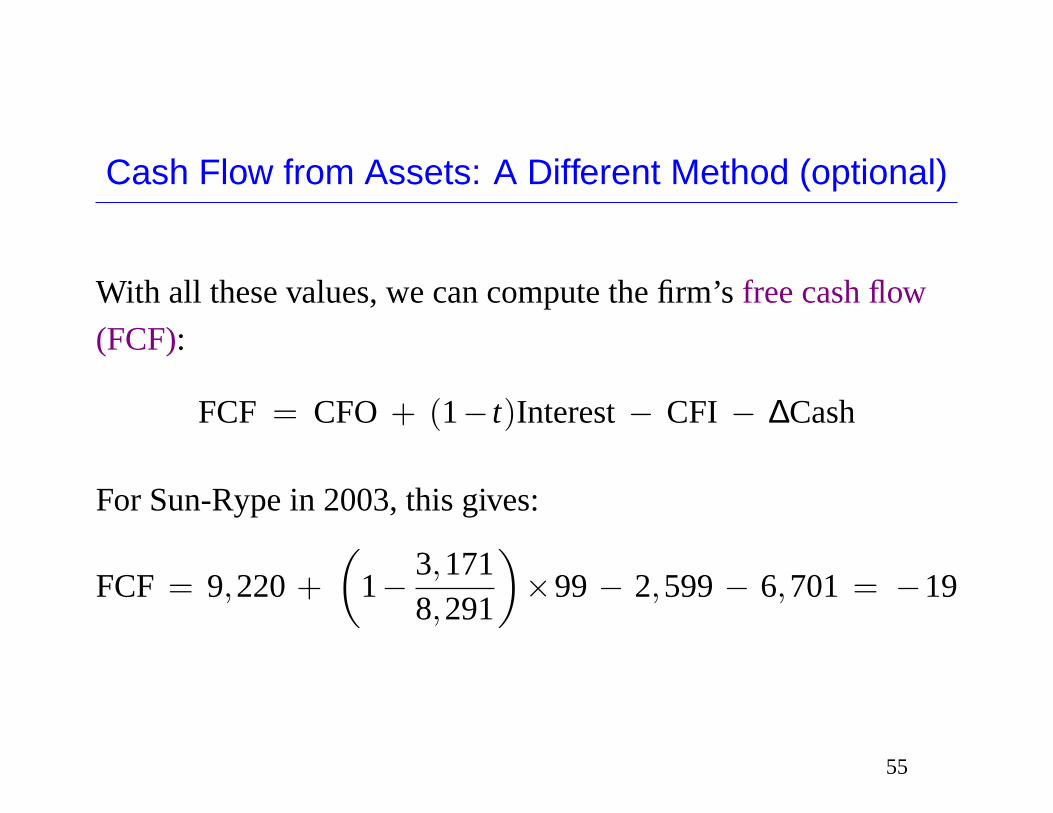

Cash Flow from Assets: A Different Method (optional)

With all these values, we can compute the firm’sfree cash flow

(FCF):

FCF = CFO + (1− t)Interest− CFI − ∆Cash

For Sun-Rype in 2003, this gives:

FCF = 9,220 +(

1− 3,1718,291

)×99− 2,599− 6,701 = −19

55

Cash Flow from Assets: Conclusion

Operating cash flowis a crucial indicator of a firm’s capacity to

generate return to its stakeholders. A firm with a negative

operating cash flow does generate enough revenue to cover

operating costs.

A negativetotal cash flowis not alarming when the firm is

growing. It should nevertheless be positive at some point in time

otherwise the return from investing in the firm cannot be positive.

56

2.5 Capital Cost Allowance

Capital cost allowance(CCA) is depreciation for tax purposes in

Canada. CCA provides atax shieldfor Canadian corporations.

To calculate the CCA for an asset, we must know its asset class,

which determines the rate to be used. (e.g. 4% for buildings

acquired after 1987, 30% for vans and trucks)

57

2.5 Capital Cost Allowance

The half-year rule: Only one half of an asset value can be

depreciated for tax purposes in the first year. This ensures that

the tax shield is applied on assets that have actually been used

during the year.

58

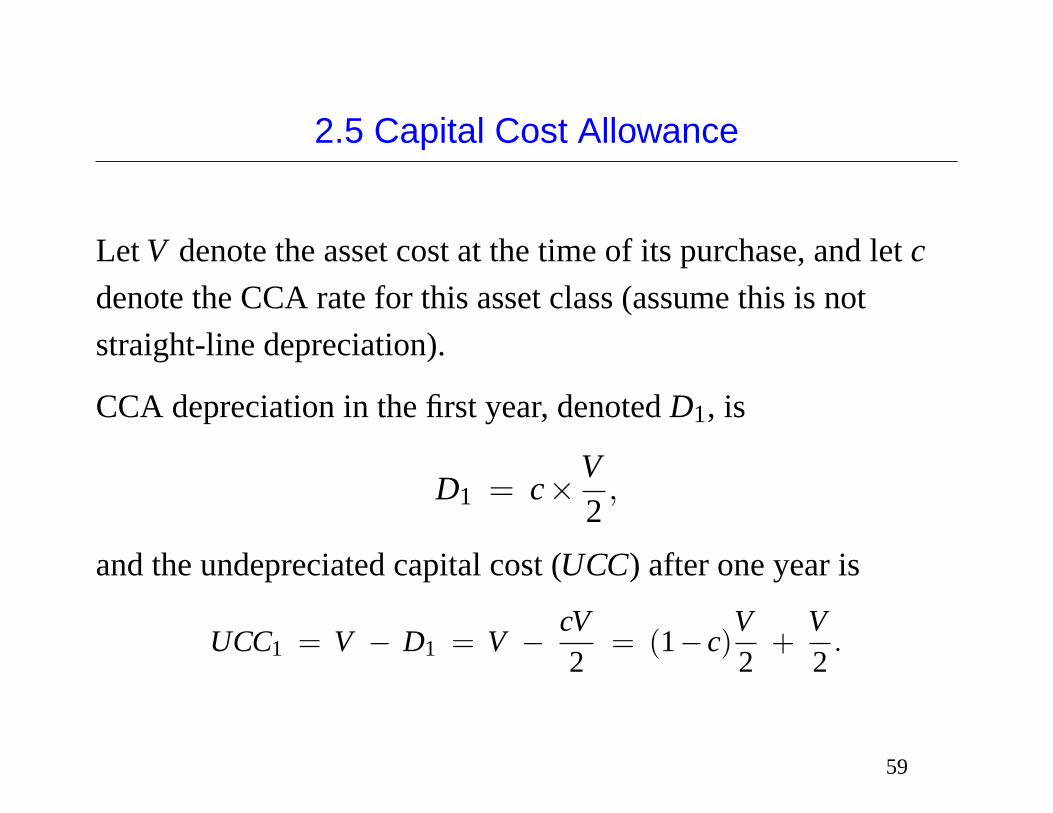

2.5 Capital Cost Allowance

Let V denote the asset cost at the time of its purchase, and letc

denote the CCA rate for this asset class (assume this is not

straight-line depreciation).

CCA depreciation in the first year, denotedD1, is

D1 = c×V2

,

and the undepreciated capital cost (UCC) after one year is

UCC1 = V − D1 = V − cV2

= (1−c)V2

+V2

.

59

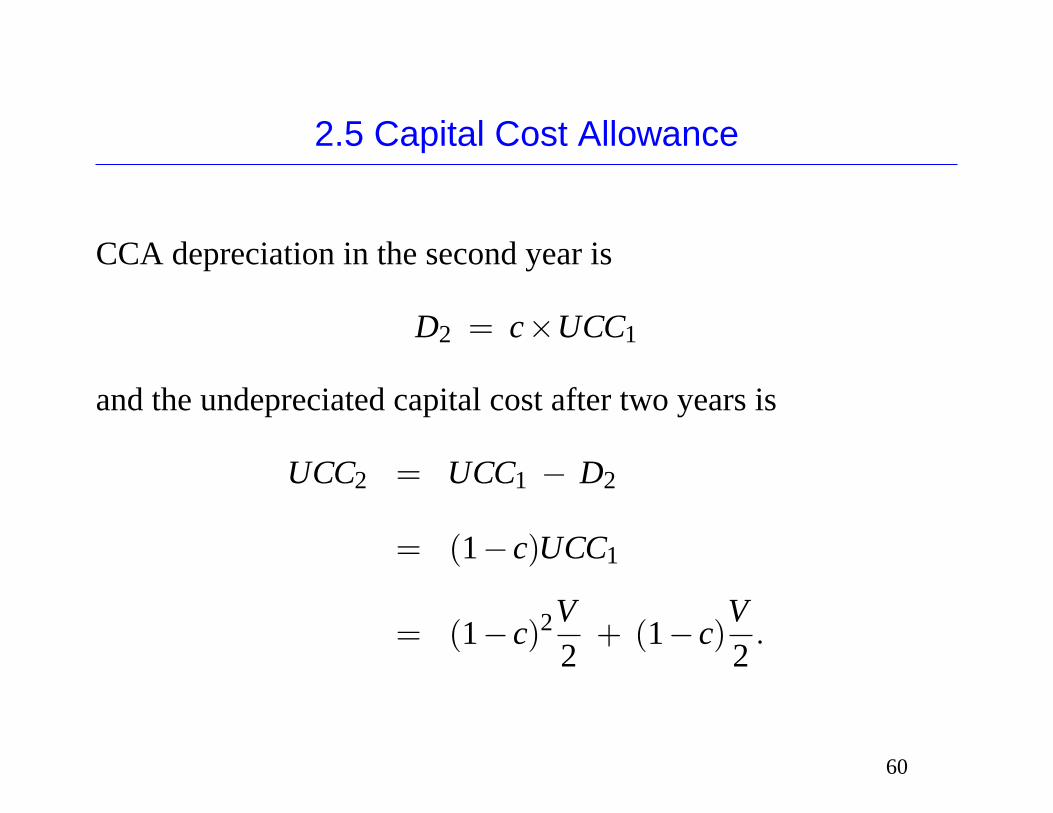

2.5 Capital Cost Allowance

CCA depreciation in the second year is

D2 = c×UCC1

and the undepreciated capital cost after two years is

UCC2 = UCC1 − D2

= (1−c)UCC1

= (1−c)2V2

+ (1−c)V2

.

60

2.5 Capital Cost Allowance

Similarly, in the third year is

D3 = c×UCC2

and thus

UCC3 = UCC2 − D3

= (1−c)UCC2

= (1−c)3V2

+ (1−c)2V2

.

61

2.5 Capital Cost Allowance

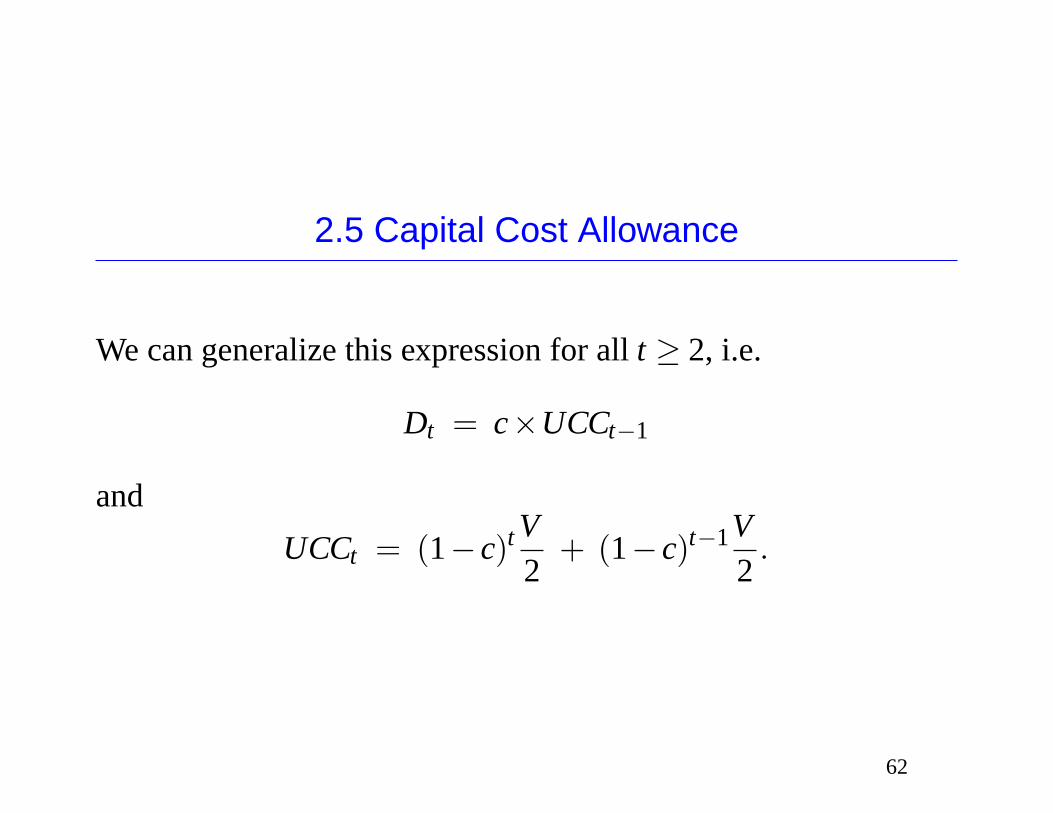

We can generalize this expression for allt ≥ 2, i.e.

Dt = c×UCCt−1

and

UCCt = (1−c)t V2

+ (1−c)t−1V2

.

62

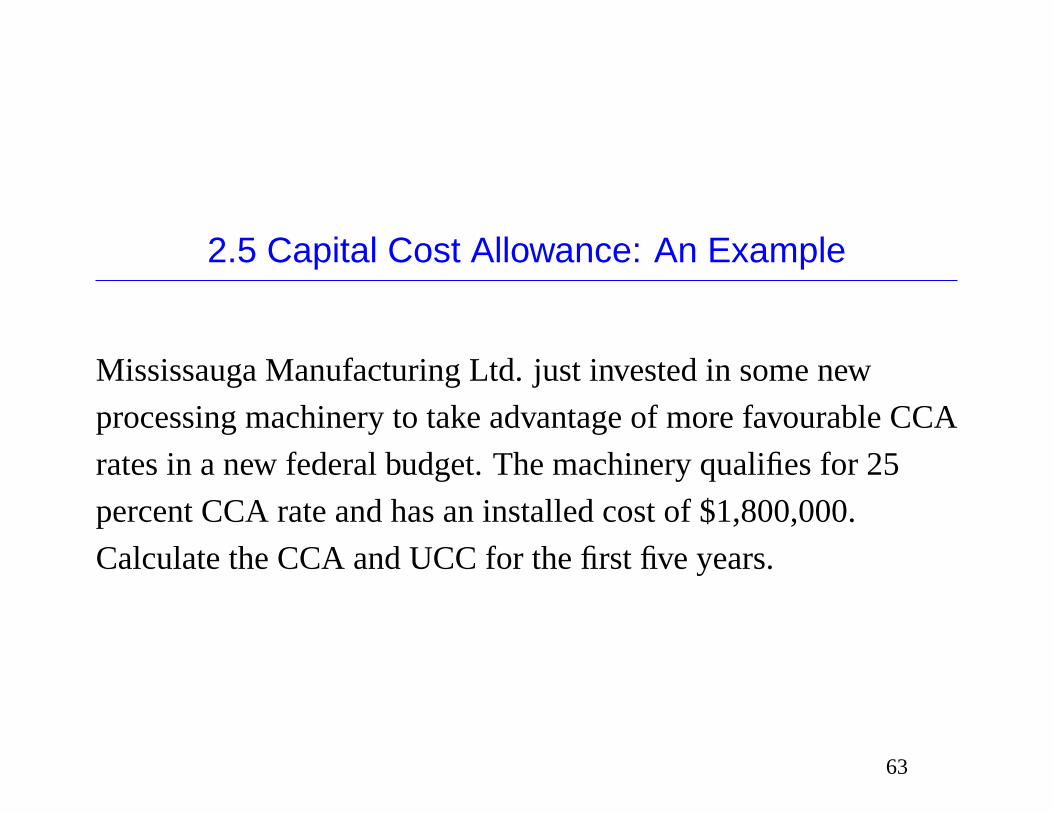

2.5 Capital Cost Allowance: An Example

Mississauga Manufacturing Ltd. just invested in some new

processing machinery to take advantage of more favourable CCA

rates in a new federal budget. The machinery qualifies for 25

percent CCA rate and has an installed cost of $1,800,000.

Calculate the CCA and UCC for the first five years.

63

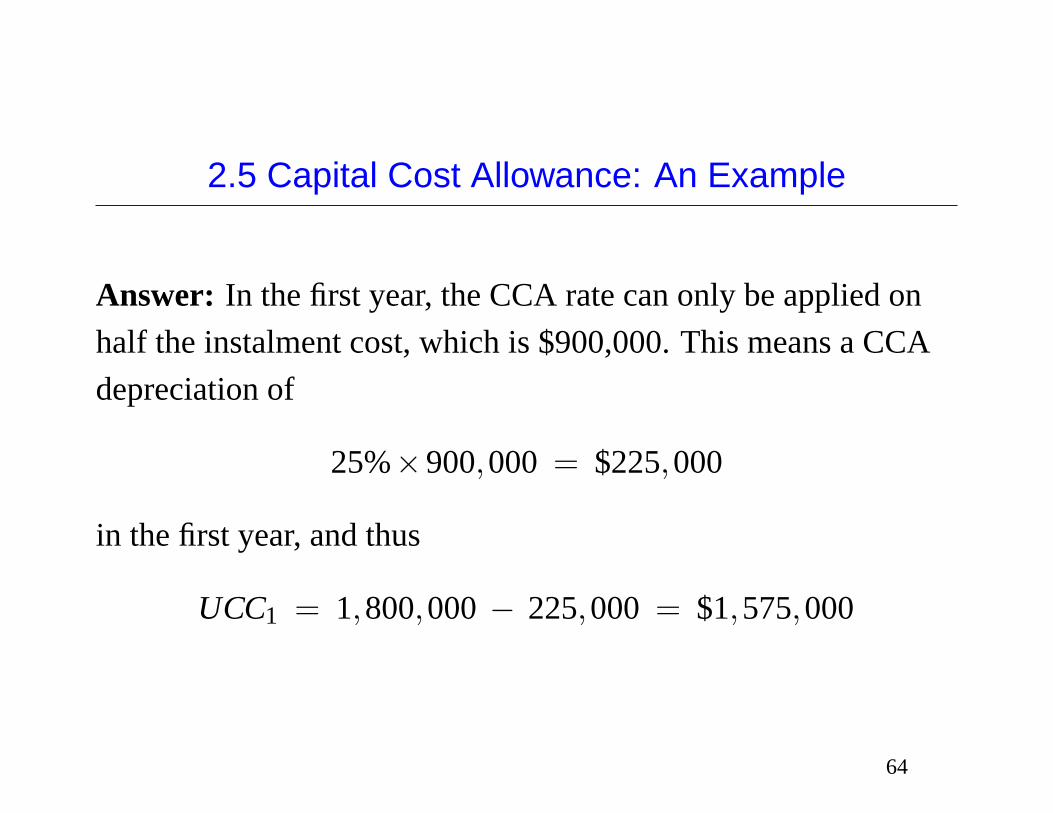

2.5 Capital Cost Allowance: An Example

Answer: In the first year, the CCA rate can only be applied on

half the instalment cost, which is $900,000. This means a CCA

depreciation of

25%×900,000 = $225,000

in the first year, and thus

UCC1 = 1,800,000− 225,000 = $1,575,000

64

2.5 Capital Cost Allowance: An Example

The CCA depreciation in the second year is

25%×1,575,000 = $393,750,

and thus

UCC2 = 1,575,000− 393,750 = $1,181,250.

65

2.5 Capital Cost Allowance: An Example

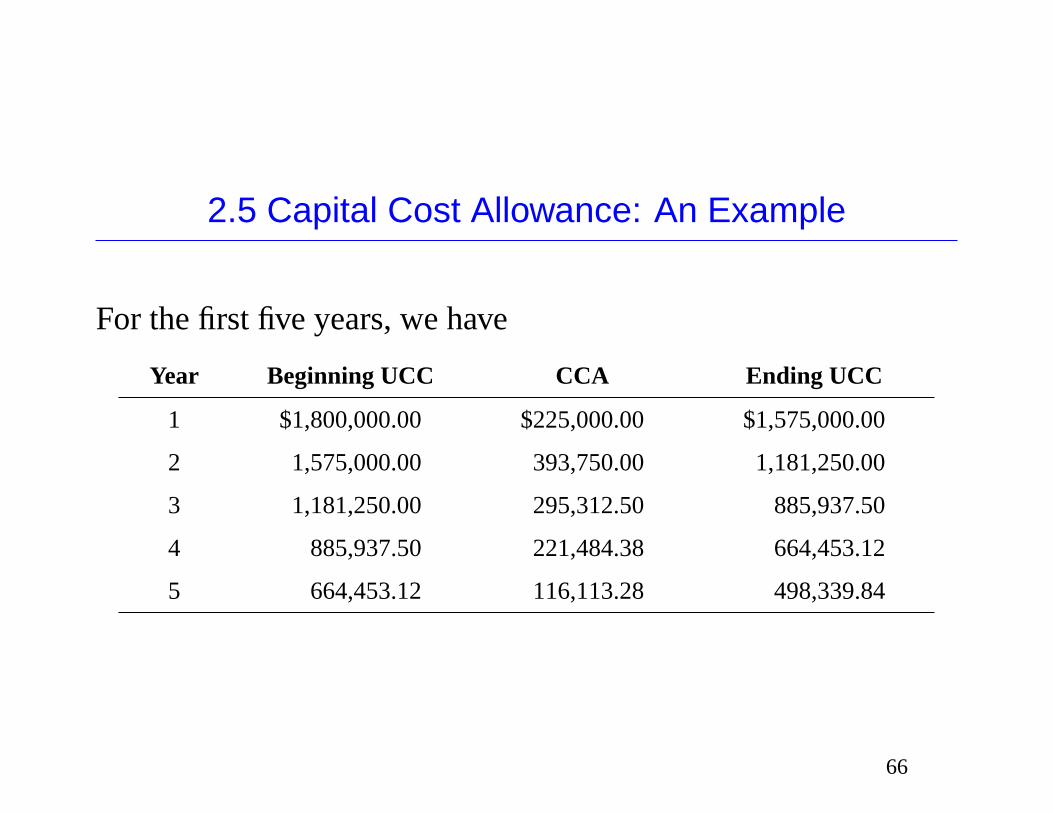

For the first five years, we have

Year Beginning UCC CCA Ending UCC

1 $1,800,000.00 $225,000.00 $1,575,000.00

2 1,575,000.00 393,750.00 1,181,250.00

3 1,181,250.00 295,312.50 885,937.50

4 885,937.50 221,484.38 664,453.12

5 664,453.12 116,113.28 498,339.84

66

Asset Purchases and Sales

Suppose an asset is sold at timeT for $S. Two things may

happen:

S> UCCT : If S> UCC0, the differenceS−UCC0 is taxed as

capital gain, and the differenceUCC0−UCCT is substracted

from the asset pool (assuming the asset pool is continued).

S≤UCCT : In this case, the differenceUCCT −S is added to the

asset pool and depreciates until the asset pool is terminated

(possibly forever).

67

Asset Purchases and Sales

In reality, this procedure will be applied on net acquisitions of

assets. That is, what is added to or subtracted from the asset pool

depends on the net proceeds from asset sales and purchases.

When an asset pool is terminated (the last asset in it has just been

sold), then the difference between UCC and the sale proceeds are

either added to or subtracted from the income. If the sales price

is below UCC, the terminal loss (UCC−S) is subtracted from the

income. On the other hand, ifS> UCC, then the difference

(S−UCC) is added to the income and CCA is recaptured.

68