financial statement analysis (ias 1)

TRANSCRIPT

BEESGREEN

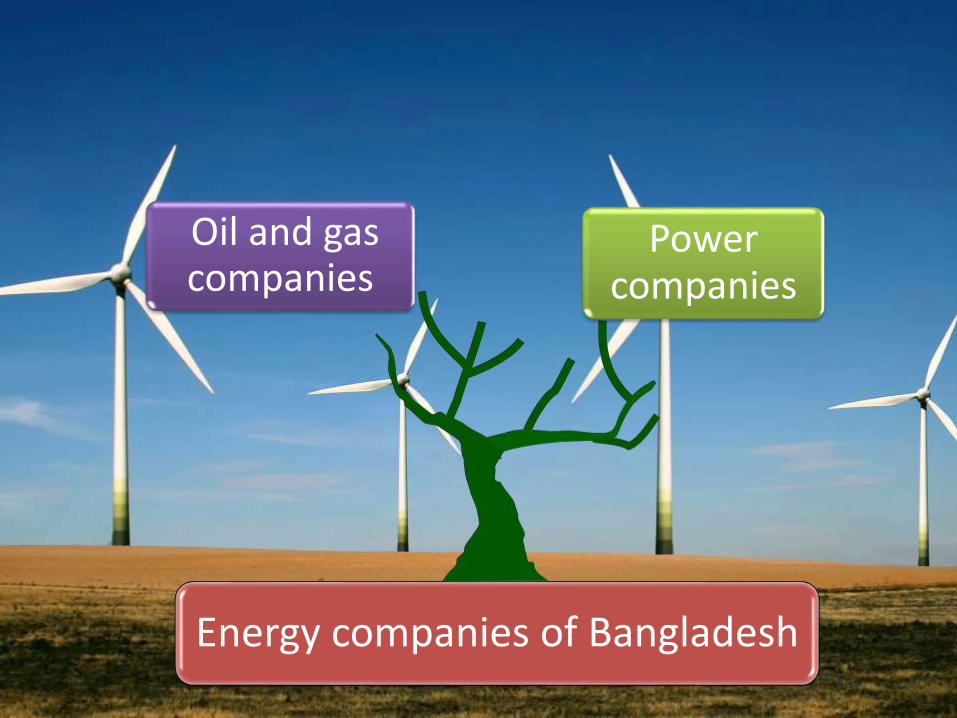

Power and Energy Companies in Bangladesh

Energy companies of Bangladesh

Power companies

Oil and gas companies

Oil and gas companies

Power companies

1.Bangladesh Petroleum CorporationBurmah Oil

2.Gas Transmission Company Limited

3. Jamuna Oil Company

4.Padma Oil CompanyPetrobangla

5.Titas Gas

1.Dhaka Electric Supply Company Limited

2.Power Grid Company of Bangladesh

3.Regent Power Limited

Summit- Power

Jamuna Oil

Mobil Jamuna BD

Chevron BD

Petrobangla

Identification and components of financial statements

(1)

Are the financial statements identified clearly (using an

unambiguous title) and distinguished from other

information in the same document?

(2)Do the financial statements identify clearly and include all of the following: a. A statement of financial position as at the end of the reporting period

(2)b. A statement of comprehensive income for the reporting period showing the components of profit or loss as part of a single statement of comprehensive income

(2)

c. A statement of changes in equity for the reporting period

(2)

d. A statement of cash flows for the reporting period

(2)

e . Notes , comprising a summary of significant accounting policies and other explanatory notes

(4)

If necessary for a proper understanding of the information

presented, does the entity display prominently and repeat the

following:

a. The name of the reporting entity or other means of identification, and any change in that information from the end of the preceding reporting period

(4)

b. Whether the financial statements cover the individual entity or a group of entities

(4)

d. The presentation currency

(5)

If not disclosed elsewhere in information published with the financial statements, does the entity disclose the following:b. The legal form of the entity

(5)

c. The entity’s country of incorporation

(5)

d. The address of the registered office (or principal place of business, if different from the registered office)

(5)

e. The nature of the entity’s operations and its principal activities

(5)

f. The name of the parent entity

Comparative information

(14)Does the entity disclose comparative information for the previous period for all amounts reported in the financial statements, unless an IFRS permits or requires otherwise

(18)Does the entity retain in the financial statements from one period to the next: a. The presentation of items

(18)

b. The classification of items

Date of authorization

(19)Does the entity disclose: a. The date when the financial statements were authorized for issue:

(19)

c. Who authorized the financial statements:

(19)d. The fact that the entity’s owners or others have the power to amend the financial statements after issue. If applicable

(41)Unless required or permitted by another IFRS, does the entity present separately, and not offset, assets and liabilities

(44)If the entity separately presents current and non-current assets, and current and non- current liabilities in its statement of financial position, does the entity: IAS 1.66 a. Classify an asset as current when it:a. Is cash or a cash equivalent asset unless it is restricted from being exchanged or used to settle a liability for at least 12 months after the reporting period

Information presented in the statement of financial position

(49)As a minimum, does the entity include the following line items in its statement of financial position:

a. Property, plant and equipment

(49)

b. Intangible assets

(51) Does the entity present additional line items, headings and subtotals in the statement of financial position if such presentation is relevant to an understanding of the entity’s financial position

(54)Does the entity present all items of income and expense recognized in a reporting period:

a. In a single statement of comprehensive income

(63)As a minimum, does the entity include the following line items in the statement of comprehensive income or separate income statement:

a. Revenue

(63)

b. Finance costs

(63)

c. Share of the profit or loss of associates and joint ventures accounted for using the equity method

(63)

d. Tax expense

(63)

f. Profit or loss

Information presented either in statement of comprehensive income or in the notes

(75)If items of income and expense are material, does the entity disclose the following:

a. The amount

(75)

b. The nature of the item

(76)Does the entity present or disclose an analysis of expenses using a classification (whichever is reliable and more relevant) based on either:

The nature of expenses

Signing Out!

Think Green!

Plant Green!!

Live Green!!!

BEESGREEN

powered by