financial sector development program charter - arabia saudita · develop promising local companies...

TRANSCRIPT

Financial Sector Development Program CharterDelivery Plan 2020

2 Financial Sector Development Program

3

4

788

9

11121315

232431

33343840

434454

636466

Table of contents

List of key abbreviations

Chapter 1: Financial Sector Development Program ScopeA) Financial Sector Development Program DescriptionB) Vision 2030 Objectives Directly related to the Financial Sector

Development ProgramC) Vision 2030 Objectives Indirectly related to the Financial Sector

Development Program Chapter 2: Financial Sector Development Program AspirationsA) 2030 AspirationsB) 2020 CommitmentsC) Financial Sector Development Program Metrics and Targets Chapter 3: Current StatusA) Major ChallengesB) Current Efforts

Chapter 4: Program StrategyA) Strategic PillarsB) Strategic ConsiderationsC) Tradeoffs and Interdependencies with other VRPs

Chapter 5: Initiatives PortfolioA) Initiatives PortfolioB) Game-Changers Chapter 6: EnablersA) Governance ModelB) Risk Mitigation and Required Actions

4 Financial Sector Development Program

List of key abbreviationsAP: Authorized Person

AuM: Assets under Management

CAGR: Compounded Annual Growth Rate

CCHI: Council of Cooperative Health Insurance

CCP: Central Counterparty

CEDA: Council of Economic and Developmental Affairs

CMA: Capital Market Authority

DCM: Debt Capital Markets

DMO: Debt Management Office

ECM: Equity Capital Markets

ETF: Exchange Traded Funds

FDI: Foreign Direct Investment

FLE: Financial Literacy Entity

FSDP: Financial Sector Development Program

GAZT: General Authority of Zakat and Tax

GCC: Gulf Cooperation Council

GDP: Gross Domestic Product

GOSI: General Authority of Social Insurance

GWP: Gross Written Premiums

IDPS: Integrated Digital Payment Strategy

IPO: Initial Public Offering

JCC: Job Creation and Employment Commission

KYC: Know Your Customer

LDR: Loan Deposit Ratio

MEP: Ministry of Economy and Planning

MSME: Micro, Small and Medium Enterprises

MOCI: Ministry of Commerce and Industry

5

MoH: Ministry of Housing

MoI: Ministry of Interior

MoJ: Ministry of Justice

MoL: Ministry of Labor

NDU: National Digitalization Unit

NIDLP: National Industrial Development and Logistics Program

NPL: Non-performing Loans

NSE: National Savings Entity

NTP: National Transformation Program

PE: Private Equity

PIF: Public Investment Fund

PMO: Program Management Office

PPA: Public Pension Agency

PoS: Point of Sale

REDF: Real Estate Development Fund

SDB: Saudi Development Bank

QFI: Qualified Foreign Investor

ROA: Return on Assets

SAGIA: Saudi Arabian General Investment Authority

SAMA: Saudi Arabian Monetary Authority

SCEP: Saudi Character Enrichment Program

SME: Small and Medium Enterprises

SPP: Strategic Partnerships Program

SRC: Saudi Real Estate Refinancing Company

VC: Venture Capital

VRP: Vision Realization Program

Chapter 1

7

Financial Sector Development Program - Scope

A) Financial Sector Development Program Description

B) Vision 2030 Objectives Directly related to the Financial Sector

Development Program

C) Vision 2030 Objectives Indirectly related to the Financial Sector

Development Program

8 Financial Sector Development Program

Level 1 Level 2 Level 3

1

2

3

4

5

6

Vibrant society

A ThrivingEconomy

An AmbitiousNation

Strengthen Islamic values& national identity

Enable fullfilling lives Maximize value captured fromthe energy sector

Unlock state-owned assets forthe Private Sector

Enhance ease of doing businessGrow contribution of the PrivateSector to the economy

Grow & diversify the Economy

Enable social responsibility

Increase employment

Enhance government effectiveness Position KSA as a global logistic hub

Grow non-oil exports

Enable social contributionof businesses

Enable larger impact ofnon-profit sector

Encourage volunteering

Enable citizen responsibility Promote & enable financial planning

Create special zones forrehabilitate economic cities

Further integrate SaudiEconomy regionally & globally Attract foreign direct investment

Enable financial institutionsto support Private Sector growth

Grow the Public Investment Fund’sassets and role as a growth engine

Ensure the formation of anadvanced capital market

Unlock potential of non-oil sectors Privatize selectedgovernment services

1. Scope of Financial Sector Development ProgramA) Financial Sector Development Program Description

On April 24, 2017, the Council of Economic and Development Affairs (CEDA) launched ten delivery programs to realize Vision 2030. The most prominent of these programs is the Financial Sector Development Program (FSDP) that aims at developing the national economy and contribute to achieving the remaining VRPs.The FSDP’s role is to create a diversified and effective financial services sector to support the development of the national economy, diversify its sources of income, and stimulate savings, finance, and investment. The FSDP will achieve this ambition by enabling financial institutions to support private sector growth, ensuring the formation of an advanced capital market, and promoting and enabling financial planning, without impeding the strategic objectives intended to maintain the financial services sector’s stability.

B) Vision 2030 Objectives Directly related to the Financial Sector Development Program

The FSDP has 3 main objective that contribute to achieving vision 2030:First Objective: Ensure the formation of an advanced capital marketSecond Objective: Enable financial institutions to support private sector growthThird Objective: Promote and enable financial planning (retirement, savings, etc.)

Vision 2030

9

C) The FSDP also indirectly contributes to 19 other Vision 2030 objectives:

1. Grow and capture maximum value from the mining sector

2. Develop the digital economy3. Localize promising manufacturing

industries 4. Localize military industry5. Enable the development of the retail

sector6. Unlock state-owned assets for the Private

Sector7. Increase localization of non-oil sectors8. Enable the development of the tourism

sector9. Privatize selected government services10. Push forward the GCC integration

agenda

11. Develop economic ties with the region beyond GCC

12. Develop economic ties with global partners

13. Support national champions consolidate their leadership globally

14. Develop promising local companies into regional and global leaders

15. Grow contribution of renewables to nation energy mix

16. Attract foreign direct investment17. Grow SME contribution to the economy18. Enable suitable home ownership among

Saudi families19. Support growth of non-profit sector

Chapter 2

11

Financial Sector Development Program Aspirations

A) 2030 Aspirations

B) 2020 Commitment

C) Financial Sector Development Program Metrics and Targets

12 Financial Sector Development Program

1) Bank for International Settlements2) International Organization of Securities Commissions

2. Financial Sector Development Program Aspirations

A) 2030 Aspirations

The Financial Sector Development Program’s objective is to create a thriving financial sector that serves as a key enabler in achieving Vision 2030’s objectives. By 2030, the sector is expected to grow large enough to fund Vision 2030 objectives, offer a diverse set of products and services through traditional and newly emerging players, give citizens thus far excluded from the financial system access to it with an inclusive structure, achieve a high degree of digitization and maintain financial stability.

First, the sector is expected to grow to achieve a sufficient level of financial assets relative to GDP ratio. Growth will be commensurate with an increase in private sector involvement in GDP creation, while reducing oil sector and government contributions in line with Vision 2030 objectives.

Second, in terms of diversity, a transformational change will occur. On one hand, the share of capital markets assets as a percentage of financial assets (total domestic market capitalization and outstanding debt issuances registered at the exchange) is expected to increase. On the other, emerging players (i.e., FinTechs) are expected to stimulate innovation and competition by 2030.

Third, significant improvement toward an inclusive structure will be realized in two ways: an increase in bank account penetration across the adult demographic in the Kingdom, and greater access to productive financing assets such as SME lending and mortgages. Accordingly, it is anticipated that the share of SME financing, together with share of mortgages in banks, will increase.

Fourth, the program envisions a digitized infrastructure that moves toward a cashless society. Accordingly, the share of non-cash transactions (in absolute number of transactions) is expected to increase. Moreover, the sector will provide superior customer experience and achieve higher operational efficiency.

Finally, and of critical importance, the program aims to maintain financial stability. This will ensure long-term sustainability and continued health of the financial services sector. In doing so, the program has been designed to comply with international standards of financial stability, including BIS1 and IOSCO2 requirements.

13

B) 2020 Commitments

As it looks forward to 2030 aspirations, the program has also defined a set of commitments to be achieved by 2020 that will constitute the foundations in the realization of 2030 aspirations.First, to continue the growth trajectory required to achieve 2030 aspirations, the Financial Sector program commits to increasing the total size of financial assets to GDP ratio to reach 201% by 2020 from 192% registered in 2016.

Second, to further diversify the structure of financial services sector, the program will increase share of capital markets assets (total domestic market capitalization and outstanding debt issuances registered at the exchange) from 41% in 2016 to 45% by 2020. Furthermore, emerging players (FinTechs) in the financial services sector will begin to spur innovation and growth.

Third, to enhance inclusiveness and productive financing, the program commits to increasing the share of SME financing at banks from the 2% level currently to 5% by 2020. Similarly, the share of mortgages in bank financing will increase to 16% by 2020 from its 2016 level (7%).

Fourth, to achieve digitization aspirations, specifically a cashless society, the program commits to increasing the share of non-cash transactions from 18% in 2016 to 28% by 2020. Lastly, as previously mentioned, the program commits to fully complying with international standards to ensure the overall financial stability of financial services sector.

14 Financial Sector Development Program

[1]. The ratio represents loans from banks, specialized credit institutions, domestic market capitalization (excluding the market capitalization of potential ARAMCO listing) and debt registered at the exchange. 2. Equity capital markets target defined based on increase in the domestic market capitalization of the exchange (excluding the market capitalization of potential ARAMCO listing) driven by growth in listings through privatization program as well as listings from the private sector.3. Debt capital markets target defined based on increase in debt registered at the exchange, including issuances of the government, issuances of the Saudi Real Estate Refinance Company (SRC), and the funding needs of the private sector outside the banking sector.4. Number of adults (15 years and above) who have at least one active bank account5. Number of card based, electronic and ACH transactions.

Rationale

Financial sector asset to GDP (%)

Output from FSDP VRP Funding Model based on agreed Financial Sectorassumptions with SAMA and CMA

Output from FSDP VRP Funding Model based on agreed Financial Sectorassumptions with SAMA and CMA

Based on linear growth assumption toward achieving the 2030 target

Based on SAMA estimates; linear growth from as-is to 2030 target

Share of ECM and DCM in the financial sector (%)

Number of adults with abank account (%)

Share of non-cashtransactions (% of total)

[1]. The ratio represents loans from banks, specialized credit institutions, domestic market capitalization (excluding the market capitalization of potential ARAMCO listing) and debt registered at the exchange. 2. Equity capital markets target defined based on increase in the domestic market capitalization of the exchange (excluding the market capitalization of potential ARAMCO listing) driven by growth in listings through privatization program as well as listings from the private sector.3. Debt capital markets target defined based on increase in debt registered at the exchange, including issuances of the government, issuances of the Saudi Real Estate Refinance Company (SRC), and the funding needs of the private sector outside the banking sector.4. Number of adults (15 years and above) who have at least one active bank account5. Number of card based, electronic and ACH transactions.

Rationale

Financial sector asset to GDP (%)

Output from FSDP VRP Funding Model based on agreed Financial Sectorassumptions with SAMA and CMA

Output from FSDP VRP Funding Model based on agreed Financial Sectorassumptions with SAMA and CMA

Based on linear growth assumption toward achieving the 2030 target

Based on SAMA estimates; linear growth from as-is to 2030 target

Share of ECM and DCM in the financial sector (%)

Number of adults with abank account (%)

Share of non-cashtransactions (% of total)

2016 level 2020 commitments

Financial sector asset to GDP (%)1

Share of ECM2 andDCM3 in the financialsector (%)

Number of adults witha bank account4 (%)

Share of non-cashtransactions5 (% of total)

192% (4.7 trillion Saudi Riyals)

41% (1.9 trillion Saudi Riyals)

74%

18%

201% (6.3 trillion Saudi Riyals)

45% (2.68 trillion Saudi Riyals)

80%

28%

2020 Commitments

15

C) Financial Sector Development Program Metrics and Targets

1) Establishing the level of ambition

Achieving the objectives and aspirations of the Vision will require a transformational change in the structure and scale of the existing Saudi economy. Vision 2030 aspires to reduce Saudi Arabia’s dependence on the oil industry and to foster the development of private sector. Estimates from the Ministry of Economy and Planning forecast the tripling of Saudi GDP by 2030 to >6T SAR from what it is today (2.4T SAR).

Tripling the size of the economy will require significant funding requirements for the required projects and investments of the Vision. As such, a detailed assessment of funding requirements has been conducted and the size of financing sector has been determined. Two methodologies have been utilized for this assessment:

• A top-down benchmarking methodology, which analyzes the historical relationship between GDP and the primary financial sector assets of countries with similar characteristics to Saudi Arabia’s economic aspirations in 2030 and applies them to determine Saudi Arabia’s required Financial Sector size for projected GDP levels.

• A Saudi Arabia-specific analysis, which analyzes historic relationship between growth in financial service sector and growth in government, oil industry and private sector, and projects the future funding requirements of KSA’s economic sectors by 2030. The methodology applies additional assumptions regarding structural shifts in the nature and size of financing in the oil industry and government.

2) Contribution of the VRP to the macro-economic metrics

Key macro-economic metrics impacted by the program have been identified and assessed by working with relevant teams from the Ministry of Economy and Planning and the Ministry of Labor and Social development.

More importantly, it is critical to emphasize the nature of the FSDP as a key facilitator of the other VRPs and Vision 2030 more broadly. The development and strengthening of the financial services sector is the cornerstone to the development of the Saudi economy and aspirations articulated in Vision 2030. The targets below take into account the direct impact only, and do not evaluate the indirect influence achieved by facilitating economic growth overall.

16 Financial Sector Development Program

Macroeconomic indicators Metric name 2016 2018 2019 2020 RationaleGDP % - - - %0,2 Key drivers include credit

to the private sector and increasing the stock market capitalization in order to provide adequate funding for the aspirations of the Kingdom's Vision 2030

Employment in Private Sector, # of additional jobs

- 200 400 800 Key drivers include the establishment of FinTech companies, the development of asset management and insurance sector. Given the trends through digitalization, financial sector and the banking sector will not be a major driver in direct employment generation. Meanwhile, the program aims to maintain the level of localization within the sector.

Contribution to local content B SAR

- 43,5 47,1 50,7 The main factor is the remaining Cash in the Kingdom

Non- oil revenues,

- 0,22 0,43 0,75 Through increased Tax and Zakat based on the profitability growth in the sector

Non-Government investment

- - - - The program’s impact on the non-governmental investment is negligible, where planned investments of the sector will be sufficient to advance the aspirations of the program (i.e., no additional investments required by the sector due to the program)

17

Metric name 2016 2018 2019 2020 RationaleBalance of Payment, B SAR

- - - - The program’s impact on Balance of Payments (specifically current account balance) is negligible, where the planned imports of the sector will be sufficient to achieve the program’s objectives (i.e., no additional imports of substance due to the program directly in the financial sector)

Consumption rate, in %

- - - %96 Program aims to mainly increase financing for productive producing assets. This implies a relatively negative impact on consumption.

Inflation, in % %0,79 Deposit growth as a key factor contributing to the growth of the cash reserve base.

18 Financial Sector Development Program

Metric Type Metric name 2016 2018 2019 2020 Rationale

“Enable financial institutionsto support private sector growth” metrics

Total GWP to GDP non-oil,

2.1% 2.5% 2.7% 2.9% Driven by stronger enforcement of mandatory insurance

# of Fintech players

- - - 3 Global benchmarking and SAMA input

SME loans as % of bank loans

2% 2% 3% 5% Modest growth to 2020, driven by need to establish necessary ecosystem prior to incentivizing banks to finance SMEs (in line with benchmarks)

Value of SME funding through PE/VC vehicles, Bn SAR

- - 13 23 Based on CMA estimates

Life GWP per capita, SAR

33 35 37 40 Based on SAMA Saudi Insurance Market Report, 2016

Metric name 2016 2018 2019 2020 RationaleFinancial sector assets to GDP,

192% 196% 198% 201% Output from FSDP VRP Funding Model based on agreed Financial Sector assumptions with SAMA and CMA

Share of ECM and DCM in the financial sector, %

41% 42% 43% 45% Output from FSDP VRP Funding Model based on agreed Financial Sector assumptions with SAMA and CMA

# of adults with a bank account

74% 77% 79% 80% Based on linear growth assumption toward achieving the 2030 target

Share of non-cash transactions,

18% 23% 25% 28% Based on SAMA estimates; linear growth from as-is to 2030 target

3) Program Metrics

19

Metric Type Metric name 2016 2018 2019 2020 Rationale

“Enable financial institutionsto support private sector growth” metrics

Coverage ratio of insurance schemes,%

38% (health)

45%(motor)

40% (health)

55%(motor)

42% (health)

65%(motor)

45%(health)

75%(motor)

Health insurance: Enforcing insurance for small/medium sized companies which currently has low current coverage ratioMotor insurance: assuming mandatory motor insurance covers all vehicles in KSA

Share of non-cash transactions, %

18% 23% 25% 28% Based on SAMA estimates; linear growth from as-is to 2030 target

Outstanding real estate mortgages, Bn SAR

290 304 368 502 Meeting residential requirements of Saudi citizens.Defined by the Housing VRP

“Ensure formation of an advanced capital market” metrics

Total market capitalization (shares and debt) as % of GDP

78% >=81% >=83% >=85% Output from FSDP VRP Funding Model based on agreed Financial Sector assumptions with SAMA and CMA

Assets under Management, as % of GDP

12% >=15% >=18% >=22% Baseline and 2020 estimates from CMA Strategy report; selected emerging markets benchmarks for setting 2020 commitments and 2030 aspirations

Market concentration of top 10 companies by market cap , in %

57% 56% 56% 55% Based on alignment discussions with CMA and selected emerging markets

Institutional investors’ share of value traded%

18% >=19% >=19% >=20% Baseline and 2020 estimates from CMA Strategy report; selected emerging markets benchmarks for setting 2020 commitments and 2030 aspirations

20 Financial Sector Development Program

Metric Type Metric name 2016 2018 2019 2020 Rationale

“Ensure formation of an advanced capital market” metrics

Foreign Investor ownership of the equity market cap , in %

4% >=5% >=10% >=15% Baseline and 2020 estimates from CMA Strategy report; selected emerging markets benchmarks for setting 2020 commitments and 2030 aspirations

# of micro and small cap companies listed, as % of total number of companies listed

34% >=36% >=39% >=40%

Based on alignment discussions with CMA; assumed linear growth between today and 2020

Share of investment accounts opened through eKYC,

0% 0% 5% 10% Global benchmarking

Minimum free float of equity market cap., in % of total outstanding shares

46% >=45% >=45% >=45% Based on alignment discussion with CMA

“Promote and enable financial planning (retirement, savings, etc.)” metrics

Total amount of savings held in savings products,B SAR

315 345 367 400

Output from FSDP VRP Funding Model based on agreed Financial Sector assumptions with SAMA

Number of available types of savings products,Absolute number

4 4 5 9

Based on approved recommendations from National Savings Strategy Steering Committee 3#

% of households savings on a regular basis

19% 19% 25% 29%

Based on approved recommendations from National Savings Strategy Steering Committee 3#

Share of A/C opened through eKYC,%

- 2% 5% 10% Global benchmarking

21

Metric Type Metric name 2016 2018 2019 2020 Rationale

Household savings ratio, % of disposable income

6.2% 6.4% 7/0% 7.5% Global benchmarking

Assuming a 2020 GDP of 3.15T SAR and a 2030 GDP of 6.3T SAR, we project the following figures for the previously outlined metrics:

Metric Type Metric name 2016 2018 2019 2020 Rationale

MEP Macro-economic indication

Total market capitalization, Tr SAR

>=2.24 >=2.45 >=2.68

Output from FSDP VRP Funding Model based on agreed Financial Sector assumptions with SAMA and CMA

Assets under Management, Tr SAR

>=0.41 >=0.53 >=0.69

Baseline and 2020 estimates from CMA Strategy report; selected emerging markets benchmarks for setting 2020 commitments and 2030 aspirations

Program-level metric

Financial sector assets, Tr SAR 4.66 5.43 5.86

Output from FSDP VRP Funding Model based on agreed Financial Sector assumptions with SAMA

“Enable financial institutions to support private sector growth” metrics

Total GWP, Bn SAR 50 61 75 Driven by enforcement of

mandatory insurance

“Ensure formation of an advanced capital market” metrics

Assets under Management, Tr SAR

0.29 0.29 >=0.41 >=0.53

Baseline and 2020 estimates from CMA Strategy report; selected emerging markets benchmarks for setting 2020 commitments and 2030 aspirations

Chapter 3

23

Current Status

A) Major challenges

B) Current Efforts

24 Financial Sector Development Program

%55

0 25 50 75 100

%13%45 %20%22

%4 %30 %37 %28

%15%29 %30%25

%50 %21 %21 %8

%24 %15%6 MicroSmile

MidLarge

Yet, relatively related number of large cap stocks compared to regional peersBreakdown of listed companies by size

%74

%60

%44

%40

%35

%21

%32

%57

GCCEmerging

Developing

Relatively high market concentration of top 10 stocks by market capTotal market cap, of top 10 stocks, as % of total market cap

500

200

100

0

%408

%241

%490

%114%67

%0%0%0

Furthermore, debt capital markets appear to be completely illiquid

• 80-90% of local bond

Issued purchased by local banks treasuries by relationship based pricing, hindering tradability due to limited attractiveness.• Therefore, pricing not fully reflect true risk rating

100

75

50

25

0

94 94 90 87

6 6 10 13

83 76

18

17 24 82

%4

Overall, debt capital markets are limited in sizeBreakdown of total debt and equity issued,2016, as % of total issuance

ECMDCM

3. Current Status

Prior to designing the program’s strategy, the current situation has been studied from two primary angles: first, major challenges facing the financial services sector and second, on-going transformation efforts that are aligned with Program aspirations. This section provides details on both of these aspects.

A) Major Challenges

This program addresses the major challenges faced by the financial services sector in five key areas:

i. High dependence on bank financingFinancial services are mainly driven by bank financing. Share of equity capital markets, measured in terms of domestic market capitalization, and debt capital markets, measured in terms of registered debt at the exchange, stood at 78% of GDP in 2016.

Moreover, equity capital markets are highly concentrated. Total market capitalization of SABIC and the financial sector is >40% of total equity market capitalization alone. The program’s objective is to address this challenge by diversifying the sector similar to the actions of other comparable countries.

25

0 25 50 75 100

%47 %53

%48 %52

%73 %27

%55 %45

%95 %5

Breakdown of value turnover by investor geography

HKeX

QSE

Bursa Malaysia

Tadawul

DFM

Domestic

Foreign

% of value traded (2016)

0 25 50 75 100

%22 %78

%30 %70

%82 %18

Breakdown of value turnover by investor type

Bursa Malaysia

HKeX

Tadawul Institutional

Retail

% of value traded (2016)

9999989390

747269

63542928

9999969696

7869656144393722

99999696948169696857533627

96969695877663585551442922

KSA behind peers in terms of the share account holdersat a formal financial institution

All figures in %

RuralIncome, bottom 40%FemaleOverall

ii. Gaps in financial inclusion and productive financingOne of the key success factors of a thriving financial services sector is its ability to serve a broad set of economic players. In 2016, 74% of adults had a bank account in Saudi Arabia, while developed markets registered over 90% inclusion. More specifically, financial inclusion among female adults and residents in rural areas is low at 61% and 72%, respectively, in 2016.

In addition, Saudi Arabia has a nascent asset management industry. In 2016, the assets under management to GDP stood at 12%. This also affects the nature of trading activity in the exchange, where share of institutional investors at 18% as measured in 2016 trading is low.

26 Financial Sector Development Program

نسبة إقراض المنشآت الصغيرة والمتوسطة أقل من %5 من القروض التجارية، وهي نسبة أدنى بكثير من المقاييس المرجعية

SME lending as a percentage of bank loans

المصدر: مؤسسة النقد العربي السعودي، منظمة التعاون االقتصادي والتنمية، تقرير عن تمويل الشركات الصغيرةوالمتوسطة ورجال األعمال 2016

74% 65% 16% 38% 36% 23% 22% 21% 19% 13% 2%

Average SME in benchmarks is about 33%

Proportion (%) of SME lending in total commercial loans

SME in the Kingdom SAR 32 billion

KSA total outstanding loans:

SAR 1420 billion

Estimated KSA SME share of

lending is about 2%

Financial services sector also has room for significant improvement in providing financing to SMEs and increasing penetration of mortgages through banks. In 2016, the share of SME financing in banking assets stood at <5% and in mortgage financing at 7%. Finally, fostering development of certified credit bureau agencies and rating firms would improve risk assessment capabilities in the Kingdom.

27

39

23

19

16

1099766543

2.4

Household saving rate across key economies (2014)1

Italy Canada USA Netherlands KSA Korea Noway Australia Germany Sweden Switzerland India China

1. All 2014 data, save for date on Saudi Arabia, are reported by OECD. KSA 6% rate is based on the most recent data from the General Authority for Statistics (2013), where the total monthly income of household was SAR10723. Based on the same source, the rate for Saudi nationals (excluding expatriates/residents) is only 2.4%, where the total monthly income for Saudi households were SAR 13610. As KSA data is based on 2013, the baseline 6% �gure may change due to oil volatility and other reasons. Figures include all �gures of household expenditures, including capital expenditures.

Household saving ratio for Saudi nationals is only 2.4%

% of household disposable income

iii. Low savings ratio Currently, the Saudi household savings rate is very low, standing at ~2.4% of annual disposable income. The rate is significantly below the 10% global standard, recognized as the minimum level to ensure long-term financial independence.

Beyond its negative effect on household long-term financial planning, a low savings rate typically translates into lower levels of long-term deposits for the banking industry, decreased levels of retail collective investment schemes managed by APs, as well as lower level of deposits placed in savings-oriented insurance products (e.g., life / protection insurance scheme). As an example, life / protection insurance today represents <0.1% of total GWP over GDP, significantly below benchmarks found in Switzerland (5.5%) or the UK (8.7%). The current low savings ratio hinders the development of the financial services sector overall.

Several root causes contribute to the above-mentioned challenges: a limited appetite for private sector (especially banks) to promote interest-bearing savings, and limited availability of incentives (e.g., tax breaks) that are typically leveraged to incentivize savings. Therefore, the existing savings market is underdeveloped and has not yet matured.

28 Financial Sector Development Program

iv. Evolving infrastructure for digitization

Similar to most other sectors, financial services is rapidly changing toward a higher level of digitization. While Saudi Arabia has invested heavily in various components of technical infrastructure (e.g., payments infrastructure), significant improvement is still possible in the use of this infrastructure toward a cashless society. In 2016, share of non-cash transactions stood at 18% of total transactions.

Euro monitor 2016 : المصدر

70

65

63

53

51

37

30

24

97

91

84

69

69

46

38

26

Indonesia

KSA

Malaysia

Turkey

China

USA

Singapore

UK

22

16

15

12

12

9

8

1

12

3

3

2

1

<1%

<1%

<1%

الدفع النقدي سائد في المملكة

Direct payments as share of total payments for the year of (2016)

In terms of value, % In terms of Volume, %

In terms of value, % In terms of Volume, %

Direct payments as share of total payments for the year of (2016)

29

غياب إطار العمل الالزم إلشراك األطراف المبتكرة

Leading Banking Regulators allow non-banking licences for Fintech companies

E-money licencePSP licence Country

KSA

Singapore

Hongkong UK

Switzerland

USA

Canada

India

Fintech HubRank

Singapore

Zurich

Hong Kong

Hong Kong

Toronto

London

New York City

San FranciscoMumbai

These countries lead global Fintech Hub rankings.

1

2

3

4

5

6

7

8

26

10

9

9

9

9

9

9

8

3

Score (Max 10)

KSA not present in the list

غياب إطار العمل الالزم إلشراك األطراف المبتكرة

Leading Banking Regulators allow non-banking licences for Fintech companies

E-money licencePSP licence Country

KSA

Singapore

Hongkong UK

Switzerland

USA

Canada

India

Fintech HubRank

Singapore

Zurich

Hong Kong

Hong Kong

Toronto

London

New York City

San FranciscoMumbai

These countries lead global Fintech Hub rankings.

1

2

3

4

5

6

7

8

26

10

9

9

9

9

9

9

8

3

Score (Max 10)

KSA not present in the list

30 Financial Sector Development Program

80

60

40

20

0

363531

27272524

42

71716766666461

52

Financial literacy rate, as % of total aduls based on World Bank survey results. %

Turk

ey

Philip

pine

s

Egyp

t

Iraq

KSA

Braz

il

Mal

aysi

a

Sout

hAf

rica

Fran

ce

New

Zeal

and

Aust

ralia

Net

herla

nds

Ger

man

y

UK

Nor

way

Swed

en

Financial literacy is low in comparison to similar countries

v. Challenges in financial literacy

Financial literacy is low in comparison to similar countries. Only 30% of adults are considered financially literate.

B) Current Efforts

In designing the program, we have reviewed existing strategies and initiatives defined by the contributing entities of the program. Currently, there are 297 initiatives planned or under implementation, including:• 143 initiatives planned or under implementation defined across 4 strategic programs of

SAMA:o Banking visiono Insurance visiono Integrated payments strategyo National savings strategy

• 108 initiatives planned or under implementation defined by CMA strategy,• 22 initiatives planned or under implementation defined by Ministry of Finance’s Strategic

Plan,• 17 initiatives planned or under implementation defined by SME Authority’s SME Financing

Strategy, and • 7 initiatives planned or under implementation defined by Ministry of Economy and Planning

study on unlocking credit for private sector. We have reviewed the impact and ease of implementation of these initiatives, to define the program’s portfolio of initatives.

31

Chapter 4

33

Program Strategy

A) Strategic Pillars

B) Strategic Considerations

C) Tradeoffs and interdependencies with other VRPs

34 Financial Sector Development Program

Enable financial institutions to support private sector

growth

Ensure the formation of anadvanced capital market

Promote and enablefinancial planning

1 2 3

4. Program Strategy

This section summarizes the program’s execution strategy, and how the aspirations and commitments will be realized. This section comprises strategic pillars, strategic considerations, as well as expected trade-offs at the Program level.

A) Strategic Pillars

Vision 2030 objectives require

Pillar Target

Enable financial institutions to support private sector growth

Enhancing depth and breadth of financial services and products offeredBuilding an innovative financial infrastructureManaging risks through a thriving insurance sectorEnhancing capabilities of the talent force

Ensure the formation of an advanced capital market

Facilitating raising capital by government and private sectorOffering an efficient platform to encourage investment and diversify the investor baseProviding a safe and transparent infrastructure (maintaining financial markets stability)Enhancing market participants capacity and sophistication

Promote and enable financial planning

Stimulate and bolster sustainable demand for savings schemesDrive expansion of savings products and channels available in the marketImprove and strengthen savings ecosystemEnhance financial literacy

35

I. Enable financial institution to support private sector growth

1. Enhancing depth and breadth of financial services and products offeredThe program will promote a diverse and inclusive sector that drives innovation and serves the financing needs of a broader population. In doing so, it will open the sector to emerging FinTech players, remove obstacles that hinder growth of finance companies, unlock financing for SMEs, and increase mortgage penetration. Further, the program will improve access to financing and enhance product offerings to better serve the needs of economic sectors.

2. Building an innovative financial infrastructureThe program will promote innovation through implementation of the Integrated Digital Payment Strategy to move toward a cashless society, through digitizing KYC and end-to-end digital processing at KSA banks, as well as through the development of the national online factoring platform to enhance cash management for SMEs. The enhanced infrastructure will make available banking solutions to a larger population, while also improving customer experience through better technical standards.

3. Managing risks through a thriving insurance sectorThe program will develop a sustainable and thriving insurance sector in Saudi Arabia. In so doing, it focuses on enhancing the existing regulatory environment to drive consolidation and strengthen balance sheet capacity. Emphasis on enforcing insurance regulations will also ensure further development and market growth.

4. Enhancing capabilities of the talent forceThe program will also enhance the professional and technical capabilities of existing talent by preparing them to become high quality industry professionals with the capacity for facilitating innovation in financial services. This will be done by establishing a Financial Sector Academy covering all sub-sectors of financial services.

II. Ensure the formation of advance capital market

1. Facilitating raising capital by government and private sectorThe program aims to diversify sources of funding for government and private sector by further growing and deepening liquidity of the equity and debt capital markets. In doing so, the program will encourage the planned privatization of state-owned entities to be performed through IPOs on the Saudi Stock Exchange. This action will increase equity market capitalization and further diversify investment options available for investors. At the same time, the program will seek to further deepen the debt capital markets in Saudi Arabia to provide alternative funding away from banking and equity.

36 Financial Sector Development Program

Additionally, to further diversify alternative sources of available funding, especially for specific economic segments (e.g., start-ups, entrepreneurs, NGOs), the program will emphasize the growth of private equity, venture capital, financing investment funds, and endowments.

2. Offering an efficient platform to encourage investment and diversify the investor baseBeyond simply increasing the liquidity available on equity and debt capital markets, the program will further develop investment and trading strategies available to investors through the introduction of derivatives. It is believed that this action will further attract institutional investors, diversifying away from today’s retail-driven market.

Furthermore, the program will seek to attract foreign investors to bring capital into the economy, as it continues to diversify the investor base. It will do so by enhancing Qualified Foreign Investor access and the account opening process. Concurrently, the program will establish co-trading linkage with selected developed markets to provide remote access to Saudi markets, thereby attracting further foreign liquidity into the Kingdom.

Moreover, the program aims to establish the necessary environment to grow the asset management industry by further enhancing the capabilities of current players and attracting new players, where necessary.

3. Providing a safe and transparent infrastructure (maintaining financial markets stability)

While developing aforementioned key initiatives, the program will put strong emphasis on ensuring stability, security and transparency of its infrastructure to bolster investor / issuer confidence. In so doing, the program will seek to further digitize the process to enhance investor experience. It will also strengthen cybersecurity to secure the stability and safety of the infrastructure. Finally, to upgrade its post-trade model and risk management model, the program will focus on the establishment of a clearing house based on CCP principles.

4. Enhancing market participants capacity and sophisticationEnhancing capabilities and sophistication of market participants (e.g., investors, financial intermediaries) is often cited as key area of focus to further develop Financial Services in Saudi Arabia. As shown by Financial Literacy rate, Saudi Arabia has only <30% of adults that can be considered literate, the lowest in the Gulf region. As such, the program will focus on enhancing local capacity, sophistication and capabilities by establishing a financial sector academy covering all sub-sectors to upgrade local skills and capabilities. In addition, the potential establishment of a regulatory entity to supervise the audit offices of listed companies will be assessed to ensure compliance with highest standards of disclosures and transparency. To promote and enable financial planning (retirement, savings, etc.), the program has four

37

key objectives which have been outlined and further detailed as part of the National Savings Strategy, led by the National Savings Committee. The project includes extensive stakeholder engagement and collaboration with GOSI, PPA, SDB, Ministry of Housing, Ministry of Education, SAMA and CMA to outline the National Savings Strategy.

III. Promote and enable financial planning

1. Stimulate and bolster sustainable demand for savings schemesThe program will seek at promoting and enabling individuals’ long term financial planning and financial independence, which are core objectives of Vision 2030. Given the limited appetite today from private sector (e.g., banks) to promote interest-bearing savings accounts, the program will seek the establishment of a National Savings Entity, a standalone entity distributing government-backed retail savings products (e.g., savings Sukuks) to ignite and bolster competition for savings deposits with private sector.

The program recognizes the importance of changing social attitudes toward savings to achieve Vision 2030 objectives. In this regard, a Kingdom-wide financial literacy program will be implemented encouraging both current and future generations to save more.

2. Drive expansion of savings products and channels available in the marketThe program will encourage the development of tailored government-backed savings products to spearhead efforts in motivating long-term savings. Tailored products geared around key basic needs (e.g., home ownership, retirement, education) will be developed and distributed to drive long-term savings, and savings incentives for a low income demographic will also be developed to ensure inclusiveness.

Ensuring broad, fair and equal access to these products is cornerstone to the program. As such, the program will seek removal of existing distribution constraints hindering access in remote areas or for access to certain products. For example, the program will encourage the distribution of certain collective investment schemes through non-AP entities and simplify access to banking savings products (e.g., bancassurance)

3. Improve and strengthen savings ecosystemProdding the increase of private sector involvement in driving long-term savings is critical to the program. In this way, the program will seek to introduce incentives for banks to attract long-term deposits by providing advantage to deposits placed in longer term deposits and savings accounts.

38 Financial Sector Development Program

4. Enhance financial literacyGiven the low level of financial literacy in the Kingdom and limited uncoordinated initiatives to drive financial education, the program will encourage the establishment of a dedicated “Financial Literacy Entity” to coordinate and synchronize efforts revolving around financial education to ensure quality and consistency of materials and messages, as well as reach and scale.

The program has taken some decisions with regard to strategic consideration within the time frame based on the following analysis:

B) Strategic Considerations

Topic Description Decision taken & consequencesFinancial stability We considered various

scenarios to achieve growth while maintaining overall stability of the sector

The program carefully considered the financial stability implications of the level of growth to target in the banking sector. The global financial crisis and past crises in developing nations show that inability to balance banking growth with stability will impose significant downside risks to economy in the medium to long-term. As such, the program will comply with international standards of stability to monitor and maintain the health of the sector. In order not to risk the achievement of Vision 2030 targets, the program will diversify the sources of funding by deepening the debt and equity capital markets. In addition, the program supports the independence of the regulatory bodies in conducting their supervisory role of the sector.

Introduction of sophisticated capital market products

The program considered the right time for introducing sophisticated capital markets products (i.e., derivatives)

One of the main objectives of the program is to diversify the asset classes available for investors in the capital markets. However, currently retail investors heavily contribute to trading in the market and institutional capabilities are yet to be built. As such, the program decided that derivatives should be introduced in a gradual manner starting with simpler instruments and after the setup of relevant risk management infrastructure (i.e., central counterparty) and the financial sector academy, which can provide necessary training for the market participants. Meanwhile, the program is supportive of the current ETF program in place at Tadawul to diversify the asset classes.

39

Topic Description Decision taken & consequencesGovernment backing for savings products

The program considered the competition with private sector for savings. The program also carefully considered potential government outlays to fund potential incentives linked to tailored government backed products

Given the limited appetite of private sector to promote long-term savings, it is believed that government should spearhead and drive promotion of long-term savings to ignite and bolster competition for retail savings. This has been observed in multiple successful benchmark examples (e.g., National Savings & Investments in UK). Yet, while tailored products will be designed and developed by relevant government entities (e.g., Ministry of Education, Housing), the program will also enable private sector entities (e.g., banks) to distribute these products. Additionally, competition will be circumscribed solely to long-term savings.Given limited availability of incentives (e.g., tax breaks) in Saudi Arabia, effective government incentives such as matching contributions have been considered to incentivize savings in tailored products. These incentives have been modeled and structured to become fully self-funding in the medium term (10-8 years).

Islamic Finance focus The program considered two options to define the right focus to further enhance the Islamic finance offerings in the Kingdom

Enhancing the Islamic finance offerings in the Kingdom is among the key objectives of the program. The program considered two options to achieve this goal: an explicit initiative focusing solely on Islamic finance vs. relevant initiatives focusing on enhancing right Shari’ah compliant products within their domain. The program decided to go with the second option. Initiatives focusing on enhancing the current product offering (e.g., debt capital markets, savings products) will define right mechanisms to provide the necessary Shari’ah compliant offerings. This will enable the correct specialization within each domain and avoid overlap/ cannibalization with conventional products that will be offered.

40 Financial Sector Development Program

C) Trade-offs and Interdependencies with other VRPs

The financial sector development program team has defined potential trade-offs and interdependencies with other VRPs in order to obtain the leadership’s guidance toward resolving them. These trade-offs and interdependencies are detailed as follows:

Interdependencies Relevant programs Strategic decisionsLabor upskilling SCEP SCEP is involved in ensuring continuous

education of the Saudi population and in developing talent in priority fields to align education output and labor market. FSDP is dependent on SCEP in addressing financial literacy at schoolsand training needed talent for the financial sector through education

SME empowerment NTP, Housing, NIDLP Various programs depend on empowering SMEs. By providing access to financing, FSDP enables the empowerment of the SME sector. Meanwhile, FSDP depends on the SME Authority for improving the supply and nurturing of creditworthy SME businesses.

Business environment development

PIF, SPP, Privatization, National Companies, Housing and NIDLP

FSDP will improve access to financing and diversify funding opportunities for the private sector. Several programs will benefit from these activities.

Capital market development

PIF, SP, Privatization, National Companies, Housing and NIDLP

Development of an advanced capital market will enable various programs to achieve their funding and financial enablement objectives with more diversified funding instruments.

Trade-offs Relevant programs Strategic decisionsFinancial planning and focus on savings

NTP Increased focus on savings might negatively impact economic growth in the short-term as citizens divert away from consumption. However, long-term, the impact will stabilize and will support productive growth.

41

Chapter 5

43

Initiatives Portfolio

A) Initiatives Portfolio

B) Detailing Game-Changers

44 Financial Sector Development Program

A) Initiatives Portfolio

The Program’s aspirations, commitments, strategic pillars and strategic considerations have been translated into a number of initiatives to help achieve commitments made by the program. These initiatives also constitute a foundation on which the aspirations of KSA Vision 2030 shall be achieved.

The current relevant initiatives to the program and commitments by various entities have been reviewed and linked to the strategic pillars.

Additionally, initiatives were designed according to a comprehensive review of the Program’s requirements, and a thorough review of global best practices. The most suitable alternative was selected to make up a portfolio of initiatives, which are detailed below.

Pillar 1: Enable financial institutions to support the growth of the private sector

Initiative name Description Leading entity

Expected impact

Program metrics impacted by initiative

Open Financial Services to new types of players

Enable market entry of new types of players (e.g., Fintech, telcos) to foster development of an innovative ecosystem in Financial Services, encourage entrepreneurship / job creation and bolster private sector competition to drive innovation and service quality

SAMA Increase number of licensed Fintech players to minimum of 3 by 2020

1) Share of non-cash transactions2) Number of Fintech players3) Satisfaction index of Fintech with

KSA Fintech ecosystem4) Financial sector assets to GDP5) Credit to Private Sector

Create a level playing field for finance companies

Address key challenges for finance companies (e.g., access to funding, taxation) to strengthen competition with banks

SAMA Increase share of SME financing

1) Financial sector assets to GDP2) Credit to Private Sector3) ROA for financing company

sector4) NPL in financing company sector

45

Initiative name Description Leading entity

Expected impact

Program metrics impacted by initiative

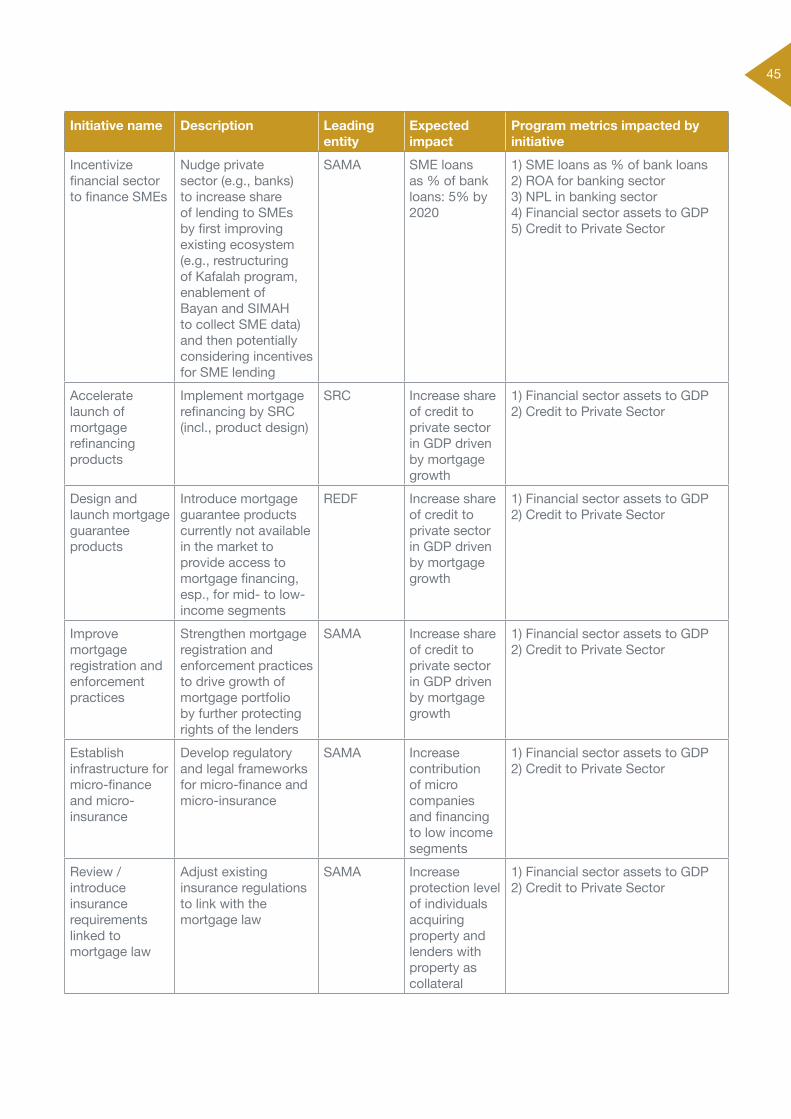

Incentivize financial sector to finance SMEs

Nudge private sector (e.g., banks) to increase share of lending to SMEs by first improving existing ecosystem (e.g., restructuring of Kafalah program, enablement of Bayan and SIMAH to collect SME data) and then potentially considering incentives for SME lending

SAMA SME loans as % of bank loans: 5% by 2020

1) SME loans as % of bank loans2) ROA for banking sector3) NPL in banking sector4) Financial sector assets to GDP5) Credit to Private Sector

Accelerate launch of mortgage refinancing products

Implement mortgage refinancing by SRC (incl., product design)

SRC Increase share of credit to private sector in GDP driven by mortgage growth

1) Financial sector assets to GDP2) Credit to Private Sector

Design and launch mortgage guarantee products

Introduce mortgage guarantee products currently not available in the market to provide access to mortgage financing, esp., for mid- to low-income segments

REDF Increase share of credit to private sector in GDP driven by mortgage growth

1) Financial sector assets to GDP2) Credit to Private Sector

Improve mortgage registration and enforcement practices

Strengthen mortgage registration and enforcement practices to drive growth of mortgage portfolio by further protecting rights of the lenders

SAMA Increase share of credit to private sector in GDP driven by mortgage growth

1) Financial sector assets to GDP2) Credit to Private Sector

Establish infrastructure for micro-finance and micro-insurance

Develop regulatory and legal frameworks for micro-finance and micro-insurance

SAMA Increase contribution of micro companies and financing to low income segments

1) Financial sector assets to GDP2) Credit to Private Sector

Review / introduce insurance requirements linked to mortgage law

Adjust existing insurance regulations to link with the mortgage law

SAMA Increase protection level of individuals acquiring property and lenders with property as collateral

1) Financial sector assets to GDP2) Credit to Private Sector

46 Financial Sector Development Program

Initiative name Description Leading entity

Expected impact

Program metrics impacted by initiative

Drive toward cashless society

Reduce use of cash by implementing IDPS 2017 and introducing additional incentives to foster use of cashless payment solutions by merchants and consumers

SAMA Share of non-cash transactions as % of total transactions: 28% by 2020

1) Share of non-cash transactions2) Number of Fintech players3) Satisfaction index of Fintechs

with the KSA Fintech ecosystem

Digitize KYC process and facilitate end-to-end digital processing

Revise existing regulations to allow digital customer on-boarding, KYC, and end-to-end processing (e.g., e-signatures, fingerprints)

SAMA 1) Simplify and increase access to banking products2) Enhance efficiency of banking operations

1) # of adults with a bank account2) Number of Fintech players3) Satisfaction index of Fintechs

with the KSA Fintech ecosystem

Build a national online factoring platform

Developing a factoring platform on top of the newly-developed SADAD e-invoicing platform

SAMA Growth of SME sector in the economy

1) Financial sector assets to GDP2) Credit to Private Sector3) SME loans as % of bank loans

Strengthen compulsory insurance enforcement

Ensure enforcement of mandatory motor and health insurance to limit fraudulent practices and further develop existing insurance sector (e.g., additional GWP, increased scale, lower cost-to-income ratio) through tighter supervision

SAMA 1) Additional GWP to non-oil GDP: 2.9% by 20202) % of insured vehicles(mandatory motor): 75% by 20203) % of insured private sector employees (mandatory health): 45% by 2020

1) Total GWP / GDP non-oil2) Coverage ratio of insurance

schemes3) Solvency ratio

Facilitate insurance market M&A to increase scale and solvency

Enhance existing rules and regulations around M&A to facilitate consolidation in the insurance sector by clarifying / easing process of winding up companies, resulting in better capitalized insurers with capacity and capability to better serve market needs

SAMA Consolidation of insurance market resulting in lower cost-income, increased scale and stronger balance sheet capacity

1) Capital adequacy ratio2) Total GWP / GDP non-oil 3) Solvency ratio

47

Initiative name Description Leading entity

Expected impact

Program metrics impacted by initiative

Enhance existing insurance laws and regulations

Overhaul existing insurance regulations and revisit the allocation of responsibilities across regulators to reduce existing overlaps in mandates (e.g., SAMA, CCHI)

SAMA Clearer / more comprehensive insurance laws and regulations in line with global standards

Coverage ratio of insurance schemes

Develop a fiscal risk management framework

This initiative focuses on developing a comprehensive framework for classifying, assessing, and monitoring fiscal risks to ensure a clear alignment between the public sector and financial sector

MoF This initiative will result in best practices and interactions in risk management across the financial sector

1) NPL in banking sector2) Net stable funding ratio3) Capital adequacy ratio

Set up a unit to promote one narrative to int’l audience

The initiative focuses on establishing a coordinating entity to be the only source of information for government entities wishing to reach international investors or vice versa. As international presence / participation in the Kingdom increases, there is a need to align between government entities to ensure that there is a single source of information

MoF This initiative will lead to a better coordination while communicating with int’l audience

Foreign investor ownership of the equity market

Establish financial sector academy covering all sub-sectors

Institutionalize upskilling of existing capabilities / knowledge/ expertise across all sub-sectors on the basis of the existing Institute of Finance

SAMA / CMA

Upskill knowledge, capabilities, expertise of talent force

1) Financial sector assets to GDP2) NPL in banking sector3) Credit to Private Sector4) Number of Fintech players

48 Financial Sector Development Program

Initiative name Description Leading entity

Expected impact

Program metrics impacted by initiative

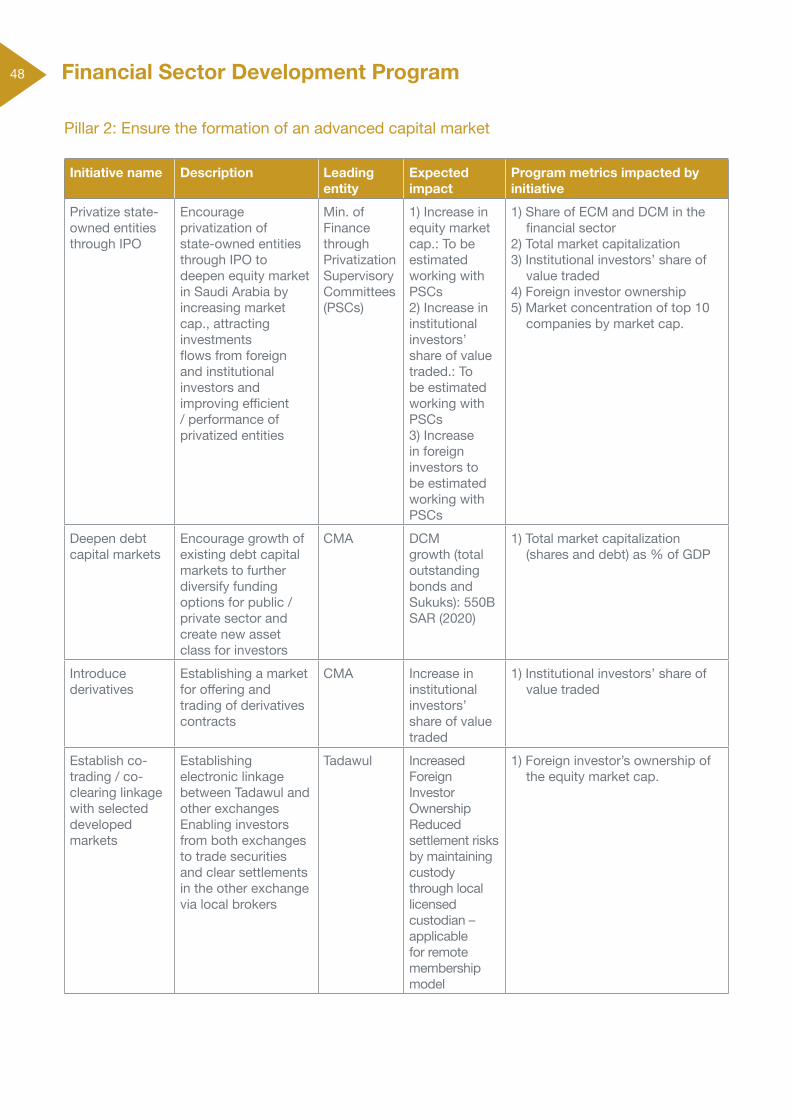

Privatize state-owned entities through IPO

Encourage privatization of state-owned entities through IPO to deepen equity market in Saudi Arabia by increasing market cap., attracting investments flows from foreign and institutional investors and improving efficient / performance of privatized entities

Min. of Finance through Privatization Supervisory Committees (PSCs)

1) Increase in equity market cap.: To be estimated working with PSCs2) Increase in institutional investors’ share of value traded.: To be estimated working with PSCs3) Increase in foreign investors to be estimated working with PSCs

1) Share of ECM and DCM in the financial sector

2) Total market capitalization3) Institutional investors’ share of

value traded4) Foreign investor ownership5) Market concentration of top 10

companies by market cap.

Deepen debt capital markets

Encourage growth of existing debt capital markets to further diversify funding options for public / private sector and create new asset class for investors

CMA DCM growth (total outstanding bonds and Sukuks): 550B SAR (2020)

1) Total market capitalization (shares and debt) as % of GDP

Introduce derivatives

Establishing a market for offering and trading of derivatives contracts

CMA Increase in institutional investors’ share of value traded

1) Institutional investors’ share of value traded

Establish co-trading / co-clearing linkage with selected developed markets

Establishing electronic linkage between Tadawul and other exchangesEnabling investors from both exchanges to trade securities and clear settlements in the other exchange via local brokers

Tadawul Increased Foreign Investor OwnershipReduced settlement risks by maintaining custody through local licensed custodian – applicable for remote membership model

1) Foreign investor’s ownership of the equity market cap.

Pillar 2: Ensure the formation of an advanced capital market

49

Initiative name Description Leading entity

Expected impact

Program metrics impacted by initiative

Support growth and expansion of PE / VC

Broadening investment funds available to sophisticated investors

CMA 1) Increase size and participation of PE / VC funds2) Increase startup funding / seed funding

1) Financial sector assets to GDP2) Number of micro and small cap

companies listed as % of total number of companies listed

3) Asset under Management as % of GDP

Enable growth and expansion of Financing Investment Funds

Increasing amount of investment funds available, adding more funding streams to the economy

CMA Increase size of investment funds

1) Financial sector assets to GDP2) Asset under Management as %

of GDP

Facilitate establishment and development of Endowment Funds

Building the infrastructure for Endowment funds

CMA Increase Waqf funds offered and managed by authorized financial institutions

1) Financial sector assets to GDP2) Asset under Management as %

of GDP

Collaborate with government funds to support asset management and custody activities of domestic APs

Allocating part of government-managed assets to be managed by local authorized persons

CMA 1) Increase Assets under Management as % of GDP2) Improved capabilities of financial intermediaries

1) Asset under Management as % of GDP

Enhance QFI access and account opening process to access the market

Providing quick and direct access to the Saudi Capital Market for Qualified Foreign Investors

CMA 1) Reduce time and improve convenience for QFI account opening process2) Increase Foreign Investor Ownership in equity market cap.3) Increase Foreign Investor contribution to value traded

1) Foreign Investor Ownership of equity market cap.

2) Institutional investors’ share of value traded

50 Financial Sector Development Program

Initiative name Description Leading entity

Expected impact

Program metrics impacted by initiative

Incentivize and encourage private companies to offer and list their shares on the stock market

Increasing the offering and listing of private companies on the stock market

MEP (ownership under review)

1) Increase equity market cap. As % of GDP2) Increase free float adjusted market cap.

1) Share of ECM and DCM in the financial sector

2) Total market capitalization (shares and debt) as % of GDP

3) Market concentration of top 10 companies by market cap.

4) Number of micro and small cap companies listed, as % of total number of companies listed

5) Min. free float of equity market cap

Enable a digital process for investment account opening

Establishing a digital KYC process and investment account opening

CMA 1) Increase number of investors in capital markets2) Increase ease of access to Saudi market3) Increase fair competition among APs especially the local ones

1) Share of investments accounts opened through eKYC

Strengthen cybersecurity

Improving the cybersecurity of capital markets through information exchange, monitoring, and applying international best practices

CMA 1) Decrease number of cyber-attacks incidents2) Improve Global Cybersecurity Index score

1) Share of investment account opened through eKYC

2) Institutional investors’ share of value traded

3) Foreign Investor Ownership of the equity market cap.

Establish a clearing house based on CCP principles

Establishing a clearing house operating in line with CCP principles to ensure introduction of adequate risk management methods in line with best-in-class international standards

CMA 1) Increase post-trade revenue for Saudi Stock Exchange2) Increase operational efficiency3) Decrease operational risk4) Facilitate introduction of dividends

1) Institutional investors’ share of value traded

2) Foreign Investor Ownership of the equity market cap.

3) Volatility of Saudi stock market index (Average of -90days)

Assess feasibility of establishing an independent regulatory structure to oversee public companies audits

Enhance the quality of audit of public companies, resulting in facilitating the flow and quality of information to investors, so as to enhance transparency and reduce risk in securities transactions

CMA 1) Attract domestic and foreign investors2) Increase in local and foreign investor confidence3) Improve governance standards

1) Institutional investors’ share of value traded

2) Foreign Investor Ownership of equity market cap.

51

Initiative name Description Leading entity

Expected impact

Program metrics impacted by initiative

Establish National Savings Entity (gov’t backed retail savings products)

Setup a standalone government-backed savings scheme provider to stimulate private savings by providing tailored products, bolstering competition for savings and allowing retail customers to save in government guaranteed products without accessing bond market directly

Min. of Finance (primary owner)Min. of Economy and Planning (secondary owner)

1) Total amount of savings held in NSE savings schemes: 6B SAR by 2020

1) Financial sector assets to GDP2) Assets under Management as %

of GDP3) Net stable funding ratio4) Capital adequacy ratio5) Total amount of savings held in

savings products6) Number of available types of

savings products

Develop tailored product: Home ownership savings scheme

Provide local consumers with tailored savings scheme designed and targeted to home ownership scheme

Ministry of Housing

1) Increase in savings deposited into savings accounts from 1 to 2 billion SAR/year2) Number of additional available types of savings products: + 1 saving plan

1) Financial assets to GDP2) Asset under Management as %

of GDP3) Total amount of savings held in

savings products4) Number of available types of

savings products

Pillar 3: Promote and enable financial planning (retirement, savings, etc.)

52 Financial Sector Development Program

Initiative name Description Leading entity

Expected impact

Program metrics impacted by initiative

Develop tailored product: Education savings scheme

Provide local consumers with tailored savings scheme designed and targeted to higher private education for children

Ministry of Education

1) Increase in savings deposited into savings A/C: 1.5 to 2 billion SAR / year2) Number of additional available types of savings products: + 1 saving plan

1) Financial sector assets to GDP2) Asset under Management as %

of GDP3) Total amount of savings held in

savings products4) Number of available types of

savings products

Distribute certain collective investment schemes through non-AP entities

Extend reach and increase penetration of collective investment schemes products by enabling APs to leverage existing distribution channels, including banks, to reach end consumers

CMA Increase in savings deposited into collective investment schemes products due to ease of distribution constraints

1) Financial sector assets to GDP2) Total amount of savings held in

savings products3) Asset under Management as %

of GDP

Develop tailored product for low income segments

Increase savings level of low income segments by designing, developing and launching savings products linked to social lending

SDB 1) Increase in savings deposited into savings A/C: 1 to 2 billion SAR/year2) Number of additional available types of savings products

1) Financial sector assets to GDP2) Asset under Management as %

of GDP3) Total amount of savings held in

savings products4) Number of available types of

savings products

Auto-enroll Citizen Account holders in National Savings Entity

Nudge local consumers to save on a regular basis, especially lower income segments, by leveraging insights from behavioral economics

MEP 1) Increase in savings deposited into savings A/C: 1 to 1.5 billion SAR/year2) Increase in number of households savings on a regular basis: 630K / year (%15 of current households)

1) Financial sector assets to GDP2) Asset under Management as %

of GDP3) Total amount of savings held in

savings products4) Net stable funding ratio

53

Initiative name Description Leading entity

Expected impact

Program metrics impacted by initiative

Simplify access to banking savings products

Extend reach and distribution of financial servicesDevelop the environment in which alternative service providers (e.g. agents, microfinance institutions) can emerge

SAMA 1) Increase in savings deposited into banking savings products due to increased reach in remote areas2) Increase in savings deposited into insurance savings products due to enhanced bancassurance rules

1) Financial sector assets to GDP2) Total amount of savings held in

savings products3) Net stable funding ratio4) # of adults with a bank account5) Total GWP / GDP non-oil6) Life GWP per capita7) Share of A/C opened through

eKYC

Establish a dedicated Financial Literacy Entity

Establish a standalone entity responsible for coordinating and driving financial education across KSA and all entities involved in financial education to limit existing overlaps and maximize impact and reach

SAMA 1) Overall level of adult financial literacy in KSA: %34 by 20202) % of households saving on a regular basis: %29 by 2020

1) Financial sector assets to GDP2) # of adults with a bank account3) % of household saving on a

regular basis

Introduce incentives for banks to attract long-term deposits

Consider incentivizing banks through adjustments in regulatory ratios to promote stable and longer-term deposits instead of current account deposits

SAMA Increase in savings deposited into banking savings products due to increased regulatory requirement needs for private sector

1) Net stable funding ratio2) Capital adequacy ratio3) Total amount of savings held in

savings products

54 Financial Sector Development Program

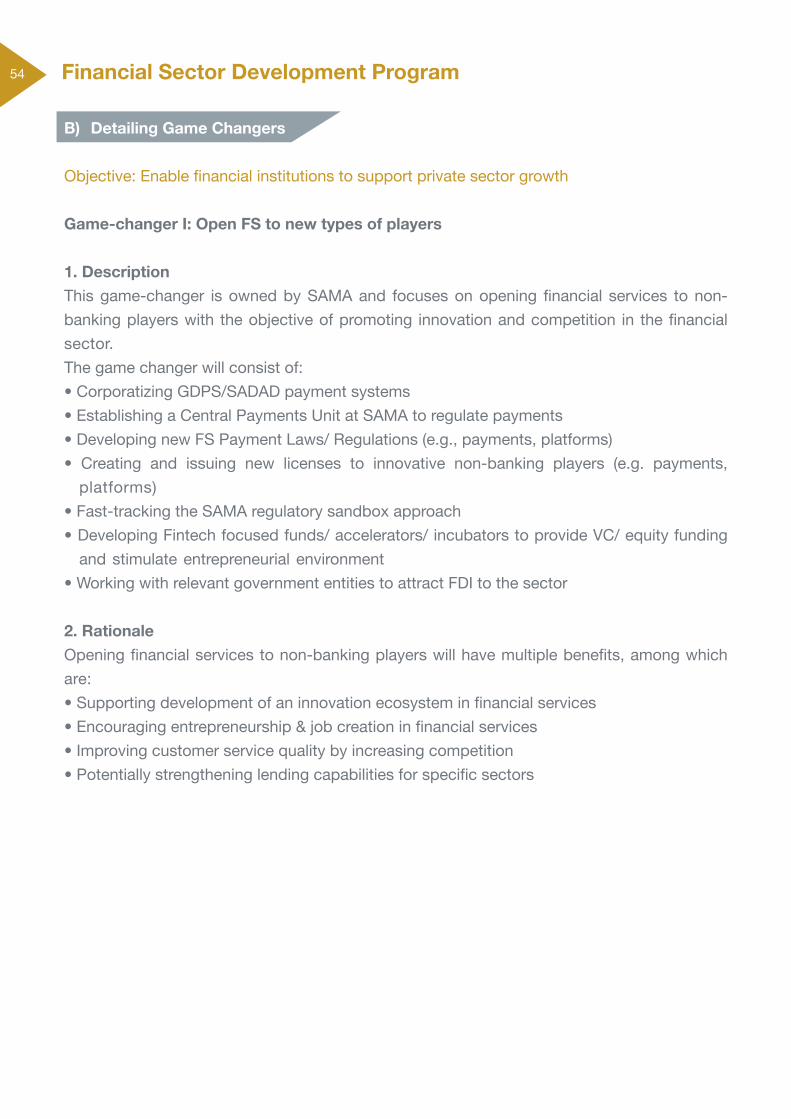

B) Detailing Game Changers

Objective: Enable financial institutions to support private sector growth

Game-changer I: Open FS to new types of players

1. DescriptionThis game-changer is owned by SAMA and focuses on opening financial services to non-banking players with the objective of promoting innovation and competition in the financial sector.The game changer will consist of:• Corporatizing GDPS/SADAD payment systems• Establishing a Central Payments Unit at SAMA to regulate payments• Developing new FS Payment Laws/ Regulations (e.g., payments, platforms)• Creating and issuing new licenses to innovative non-banking players (e.g. payments,

platforms)• Fast-tracking the SAMA regulatory sandbox approach• Developing Fintech focused funds/ accelerators/ incubators to provide VC/ equity funding

and stimulate entrepreneurial environment• Working with relevant government entities to attract FDI to the sector

2. RationaleOpening financial services to non-banking players will have multiple benefits, among which are:• Supporting development of an innovation ecosystem in financial services• Encouraging entrepreneurship & job creation in financial services• Improving customer service quality by increasing competition• Potentially strengthening lending capabilities for specific sectors

55

3. Estimated impactThis game-changer will have the following impact on the economy• Increase the number of Fintech players:

o 2 tp 3 by 2020• Establish Saudi Arabia as a strong Fintech hub and ensure a high satisfaction index of

Fintech players within the overall KSA Fintech ecosystemA satisfaction index is a survey-based indicator assessing regulatory environment, access

to funding, government programs, taxation policies, availability of skillful workforce. The first survey should be performed early 2019 for the GCC startups to understand the key ecosystem attributes, that startups are looking for, when making a decision to enter a country. These attributes should be used later for surveys across KSA fintech players, after first players enter the KSA market (after 2020)

Game-changer II: Incentivize financial sector to finance SMEs

1. DescriptionThis game-changer is owned by SAMA and focuses on introducing initiatives to incentivize the financial services sector with the objective of increasing SMEs contribution to the economy.The game changer will consist of:• Improving the SMEs financing ecosystem by:

o Strengthening the legal framework (including collateral enforcement)o Restructuring the Kafalah programo Ensuring government commitment to allocate more contracts directly to SMEso Enabling Bayan and SIMAH to collect and update comprehensive SME datao Establishing a local rating agency for SME credit assessmento Providing alternative SME funding options (e.g. PE and VC vehicles)o Developing a program to improve the financial literacy of SMEs

• Communicating lending targets to banks by 2020o If SME lending from banks is below communicated target by 2020, SAMA will consider

incentives to encourage underperforming institutions

2. RationaleIncentivizing the financial services sector to finance SMEs will result in multiple benefits to the private sector, among which are:• Increasing SMEs contribution to the economy and strengthening the private sector• Increasing job creation and employment rate• Addressing core bankability and SME growth issues

56 Financial Sector Development Program

3. Estimated impactBased on initiatives to be implemented and other benchmarked countries, this game-changer will have the following impact on SME lending• Increase SME loans as % of bank loans:

o 5% in 2020• Value of SMEs funded through PE / VC vehicles

o 23B SAR in 2020

Game-changer III: Drive toward cashless society

1. DescriptionThis game-changer is owned by SAMA and focuses on reducing cash in circulation by 2030.The game changer will consist of:• Implementing IDPS 2017, e.g.,

o Growing MADA infrastructure (PoS, cards in circulation)o Expanding number of SADAD billers (incl. SME)o Introducing SADAD e-invoicingo Setting up P2P through SADAD and MADAo Building real-time ACH

• Introducing additional incentives:o Implementing an «Elevation program» to incentivize merchants and cardholders to grow

cashless paymentso Capping the value of customer cash transactions with corporate merchants

• Potentially considering additional measures (e.g., fees for cash withdrawals/ depositing) if the above measures do not allow to reach the targets

2. RationaleReducing cash in circulation will have multiple benefits for the economy, among which are:• Reducing cost of cash on economy • Ensuring greater transparency for governments to monitor cash flows for taxation purposes• Enabling better information to support SME financing and easier performance tracking

3. Estimated impactThis game-changer will have the following impact on the economy:• Increasing the share of non-cash transactions (as % of total transactions):

o 28% in 2020

57

Game-changer IV: Enforce mandatory insurance