financial reporting presentation

TRANSCRIPT

1

Balanced ScorecardManagement ControlMBA HR Group 2

What is Balanced Scorecard?

Few Interesting Aspects of BSC

Short & Long Term Measures

Strategy FormulationFinancial & Non

Financial Aspects

Its an approach

Organizational Alignment

Strategic Performance

Measurement

Communication Media

Balanced Scorecard

Gives Big Picture

Mission(Why we exist)

Values(What’s Important to us)

Vision(What we want to be)

Strategy(Our Game Plan)

SatisfiedShareholders

Delighted Customer

Efficient and Effective

Processes

Motivated Workforce

Strategic Outcomes

What is Balanced Scorecard (BSC)?

The Balanced Scorecard

Applicability

BSC – ‘The Multi purpose Bridge’

Shareholders

Senior Managers

Functional Managers

• Contract between FM & SM

• Bridge strategy and personal objectives

• Unlike normal budgeting vision mission and strategy are cascades to measurable objectives

• Coordinate between strategies and short-term managerial targets

Aspects Balanced Scarecard

Motivation & StressProvide guidance and may limit managers ‘Best Guess’

Balances Leading KPIs & Lagging KPIs

Prevents Sub Optimization

Used for Performance Management

Consensual Space & Budgetary Slack?

Something to Think About…

Shareholder expectations may not

always be financial

Interpretation of the Model and Feasibility

Issues

Introduction to the Company

Welcome to OMEGA LINE

• Fully Italian

• Exporting non quota garments

• Largest exporter to Europe Sales volume $ 0.819 Billion (2015)

• Employees over 12000 youth State of the art facilities located in

• Badalgama• Bingiriya• Polgahawela• Sandalankawa• Vauniya

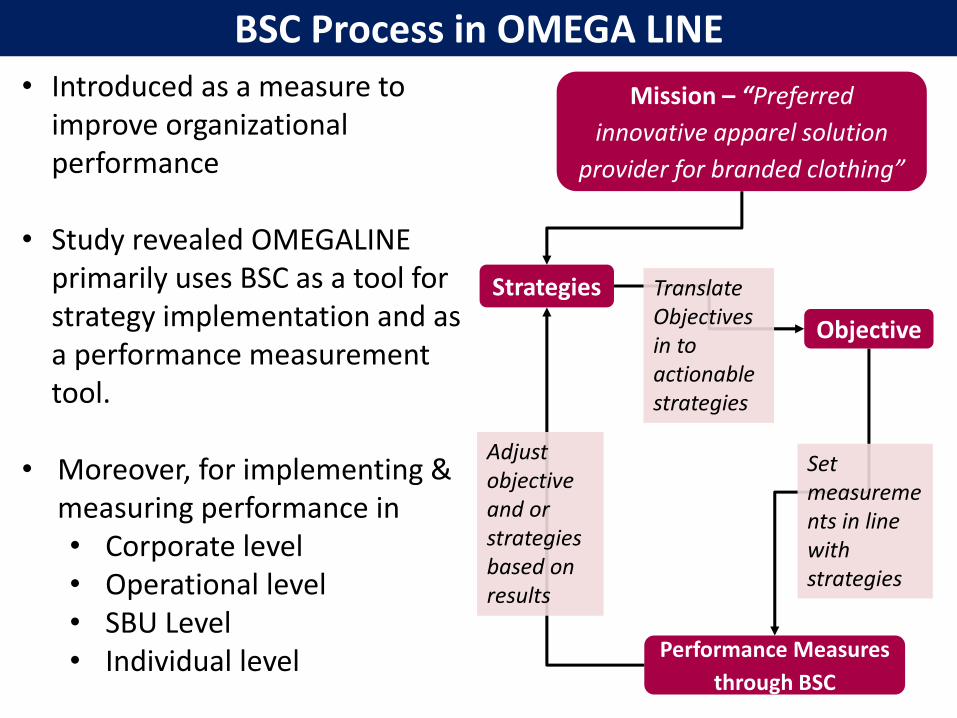

BSC Process in OMEGA LINE

Mission – “Preferred

innovative apparel solution

provider for branded clothing”

Objective

Strategies

Performance Measures

through BSC

Translate Objectives in to actionable strategies

Set measurements in line with strategies

Adjust objective and or strategies based on results

• Introduced as a measure to improve organizational performance

• Study revealed OMEGALINE primarily uses BSC as a tool for strategy implementation and as a performance measurement tool.

• Moreover, for implementing & measuring performance in• Corporate level• Operational level• SBU Level • Individual level

Omega Line KPIs

Corporate Level KPIs

Level of

Analysis

Perspective

Finance Learning & GrowthInternal Business

ProcessCustomer

Corporate

Level

Contribution for

standard unit

Cadre composition

ratio

Forecast Accuracy

On Time

Delivery

Overhead cost per unitMachine Capacity

Utilization

Account Receivables Labor turnover

Total inventory daysLabor

absenteeism

Business Level KPIs

Level of

Analysis Sector

Perspective

FinanceLearning

& Growth

Internal Business

ProcessCustomer

Business

Level

1.Apparel

1.Cut ship ratio

2.Sewing efficiency

3.On time tracking

4.Sample order CT

5.Sample hit rate

2.Textile

1.Efficiency 1.Customer

Complaints

2.Lap dip CT Avg .CT. for Sample

Dev.

3.Manufacturing CT 3.Product Dev. Hit

Rate4.Supplier Lead time

3. Finishing

1.Final QC – 1st pass 1. Overall CT

2.Despatch Hit rate

3.Sample cycle time

Mini Research

Methodology

• Used Last 12 months averageKPI Information for the Study

• Used only CKPI information's

• Employs Multiple regressionAnalysis for 4 Perspective

• Used Single Regression Analysisfor each perspective

Data Analysis

1- Four BSC Perspective & OrganizationalPerformance are positively correlated

2 - Learning & Growth, Financial, InternalBusiness Process & Customer Perspectiveshave a greater impact on OrganizationalPerformanceHYPOTHSIS

Interpretation of Parameters

1. Adjusted coefficient of determination (R2) = 20.5%

2. Learning & Growth and Financial Perspectives are

statistically significant at 0.001 levels.

3. Hence the 1st Hypothesis;

Total perspectives have a certain impact on Organizational Performance is partially (LGP & FP)

accepted in Omega Line.

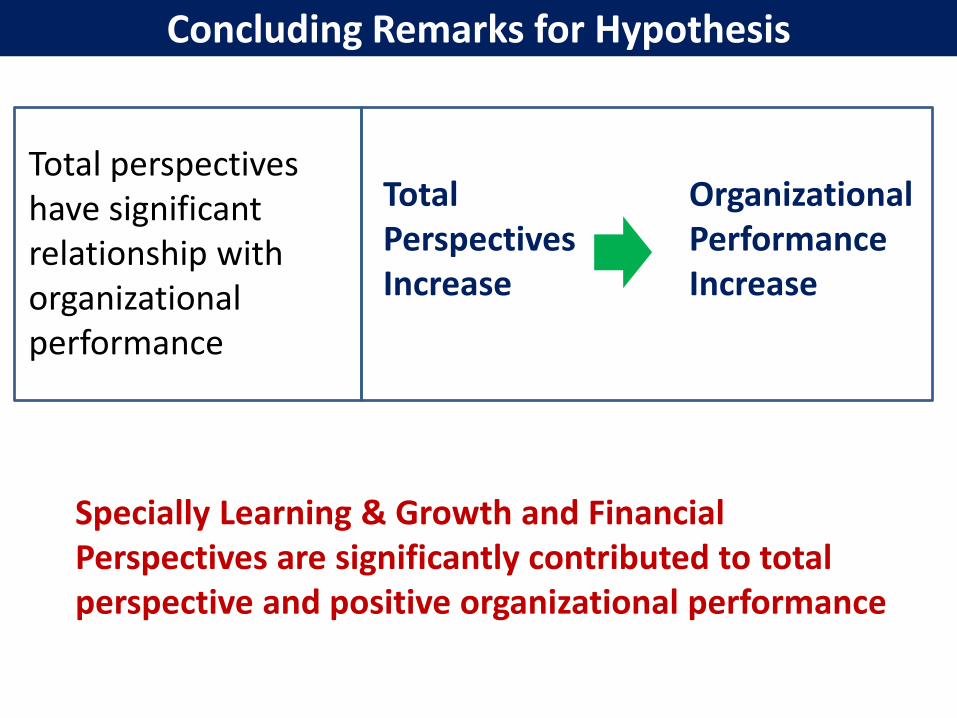

Concluding Remarks for Hypothesis

Total perspectives have significant relationship with organizational performance

Specially Learning & Growth and Financial Perspectives are significantly contributed to total perspective and positive organizational performance

Total Perspectives Increase

Organizational PerformanceIncrease

Conclusion

Conclusion

Clear deviation of CP and IBP

Appropriateness of the model to our culture

Alienation

References

Johnson, H. T. and R. S. Kaplan (1987) Relevance Lost: The Rise and Fall ofManagement Accounting, Boston: Harvard Business School Press.

Howell, R., J. Brown, S. Soucy, and A. Seed (1987) Management Accounting in the NewManufacturing Environment, Montvale, NJ: National Assn. of Accountants andCAM-I

Huselid, Mark A (1995) The Impact of Human Resource Management Practices on Turnover,Productivity, and Corporate Financial Performance, Academy of Management Journal: 635-672

Kaplan, R. S. and D.P. Norton (1996a) The Balanced Scorecard: Translating Strategy intoAction, Boston: HBS Press.

Kaplan, R. S. and D.P. Norton (1996b) Using the Balanced Scorecard as a StrategicManagement System,” Harvard Business Review (January-February):75-85.

Kaplan, R. S. and D.P. Norton (1993) Putting the Balanced Scorecard to Work, HarvardBusiness Review (September-October).

Kaplan, R. S. and D.P. Norton (1992) The Balanced Scorecard: Measures that DrivePerformance, Harvard Business Review, (January-February): 71-79.

Thank You