financial planning and analysis: the latest trends

TRANSCRIPT

Financial Planning and Analysis: The Latest Trends

By Larysa Melnychuk

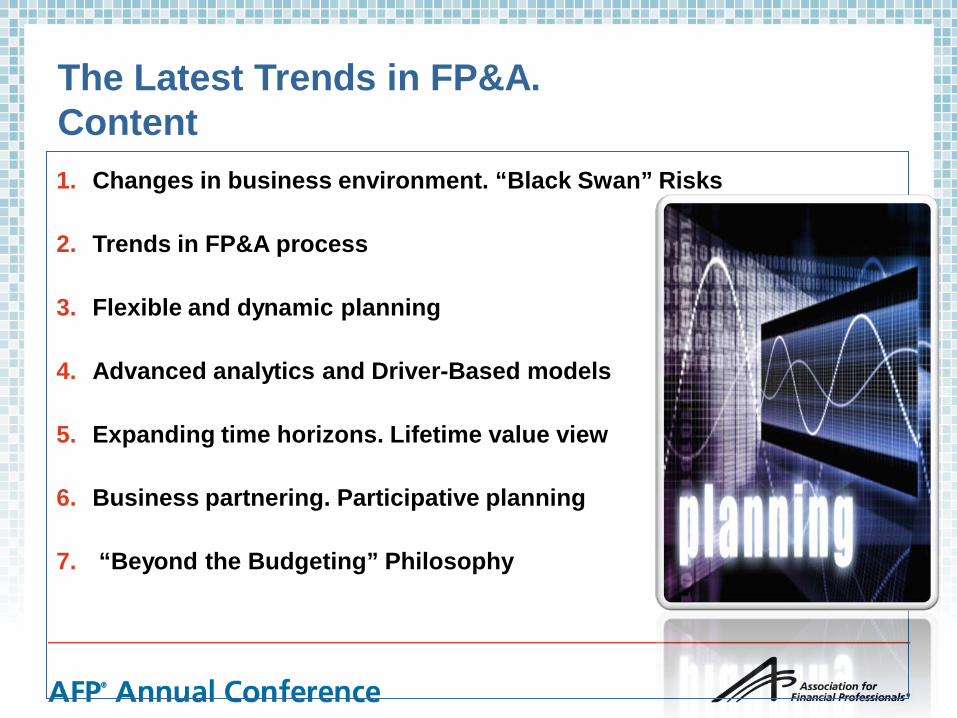

The Latest Trends in FP&A. Content 1. Changes in business environment. “Black Swan” Risks

2. Trends in FP&A process

3. Flexible and dynamic planning

4. Advanced analytics and Driver-Based models

5. Expanding time horizons. Lifetime value view

6. Business partnering. Participative planning

7. “Beyond the Budgeting” Philosophy

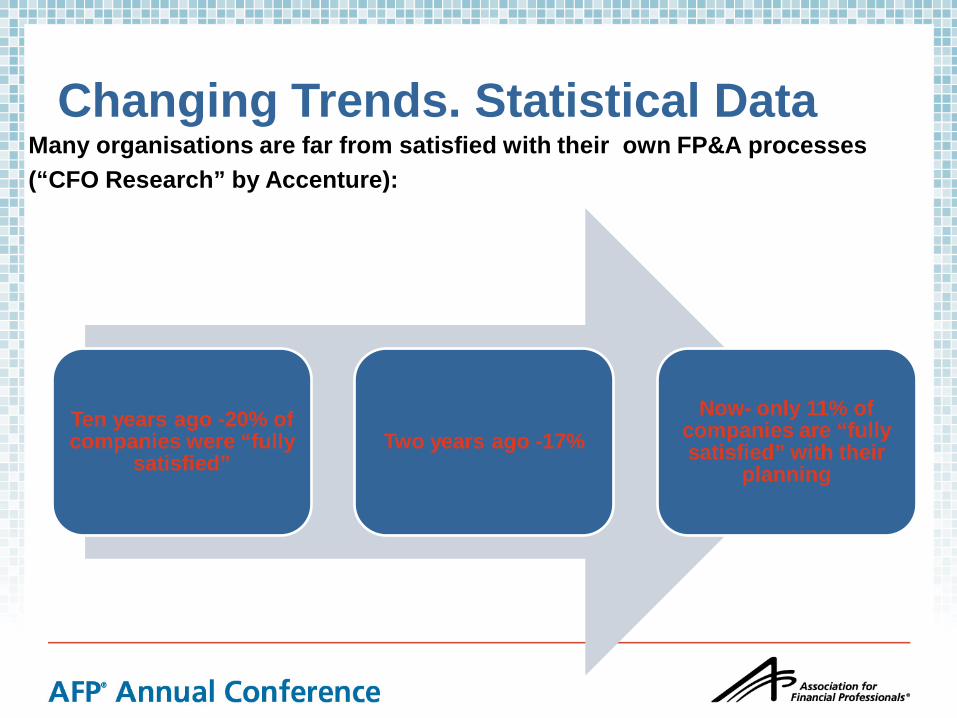

Many organisations are far from satisfied with their own FP&A processes (“CFO Research” by Accenture):

Ten years ago -20% of companies were “fully

satisfied” Two years ago -17%

Now- only 11% of companies are “fully satisfied” with their

planning

Changing Trends. Statistical Data

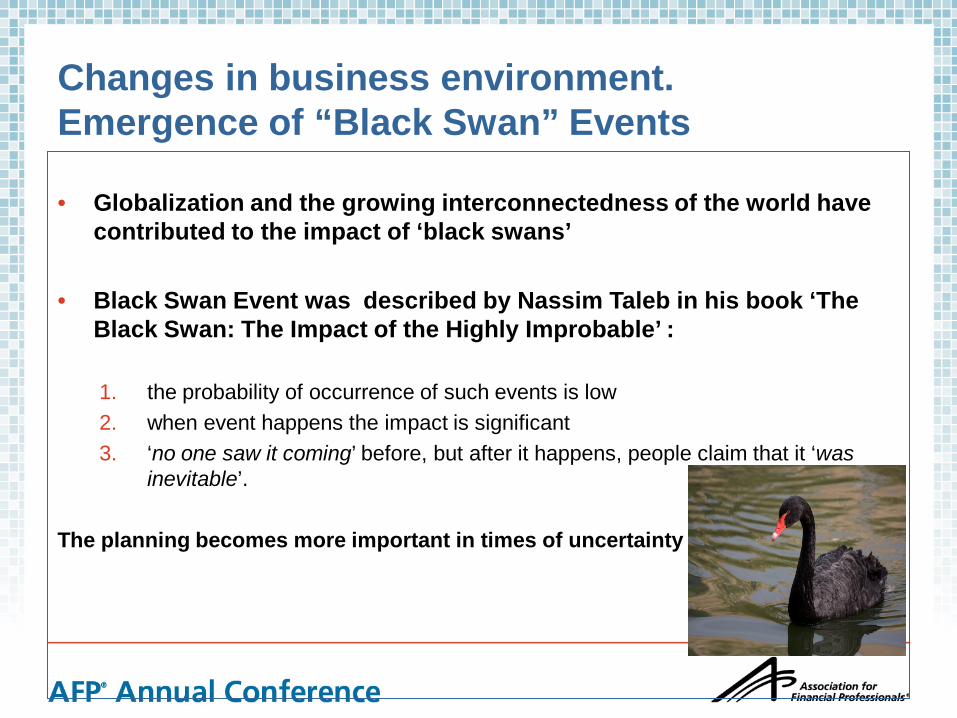

Changes in business environment. Emergence of “Black Swan” Events

• Globalization and the growing interconnectedness of the world have

contributed to the impact of ‘black swans’

• Black Swan Event was described by Nassim Taleb in his book ‘The Black Swan: The Impact of the Highly Improbable’ : 1. the probability of occurrence of such events is low 2. when event happens the impact is significant 3. ‘no one saw it coming’ before, but after it happens, people claim that it ‘was

inevitable’.

The planning becomes more important in times of uncertainty

The Latest Trends in FP&A

Moving from:

• Internal • Short-term • Centralized • Accounting profit

view • Tangible • Static

Moving to:

• External • Long-term • Participative • Lifetime value view • Intangible • Dynamic

Changing Views and Processes

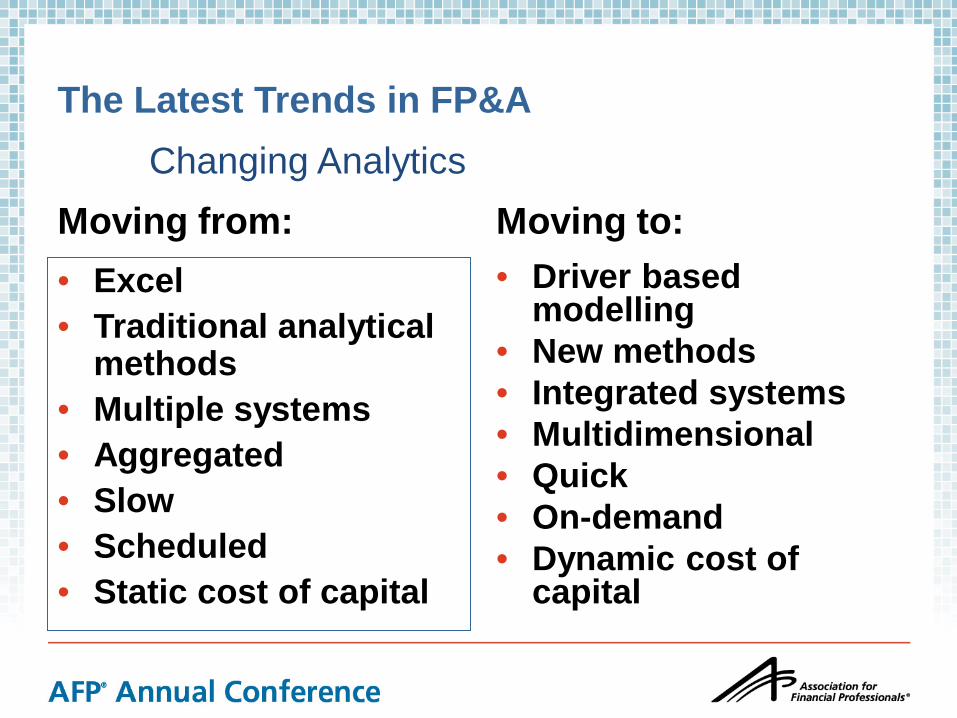

The Latest Trends in FP&A

Moving from: • Excel • Traditional analytical

methods • Multiple systems • Aggregated • Slow • Scheduled • Static cost of capital

Moving to: • Driver based

modelling • New methods • Integrated systems • Multidimensional • Quick • On-demand • Dynamic cost of

capital

Changing Analytics

The Latest Trends in FP&A

Changing Environment.“Black Swan”

Events

1. Flexible and dynamic planning

2. Driver-Based models

3. Expanding time horizons

4. Participative planning

5. “Beyond the Budgeting”

Trend N1. Flexible and Dynamic Planning Process

Examples:

i. Risk-adjusted planning

ii. Rolling forecasts

iii.Activity-based budgeting

iv.Participative planning

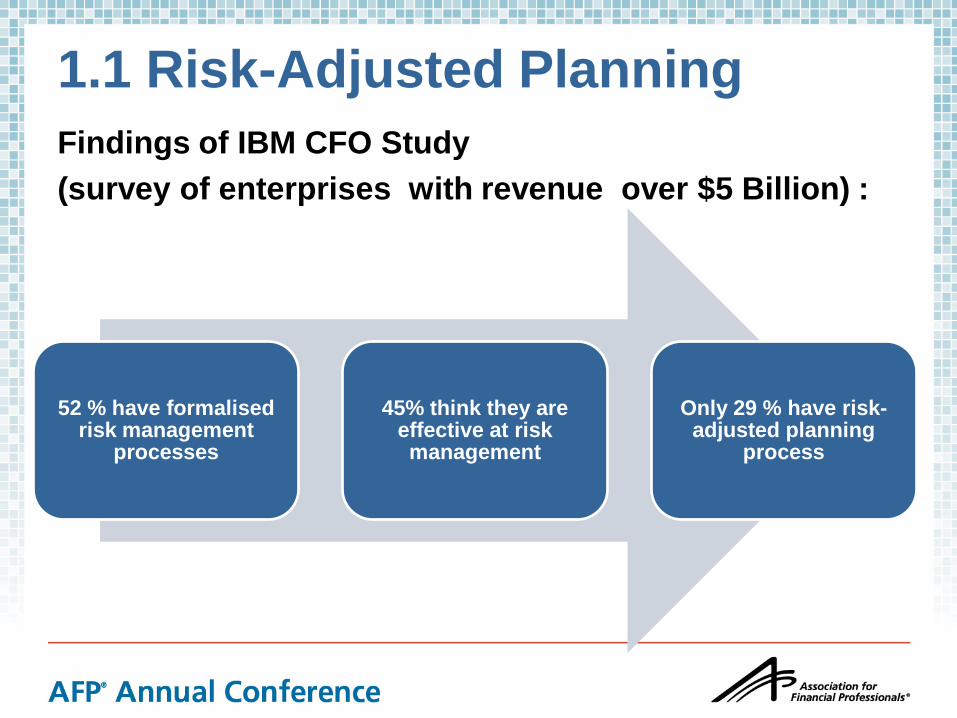

1.1 RISK-ADJUSTED PLANNING

1.1 Risk-Adjusted Planning Findings of IBM CFO Study (survey of enterprises with revenue over $5 Billion) :

52 % have formalised risk management

processes

45% think they are effective at risk management

Only 29 % have risk-adjusted planning

process

1.1 Risk - Adjusted Planning

1. Identify risks

• identifying material risks both financial and non-financial

2. Prioritise them in terms of effect

• risk threshold and effect

3. Play scenarios for risk events

• sensitivity analysis

• Probabilities • Expected values

4. Incorporate risk

• into planning process

Page 11

4 steps in Incorporating Risk into Planning Process:

1.2 ROLLING FORECASTS

1.2 Rolling Forecasts

Page 13

Year X Year X + 1

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

1st review

2nd review

3rd review

4th review

KEY:

= Actuals = Forecast

Example of Five-Quarterly Rolling Forecast

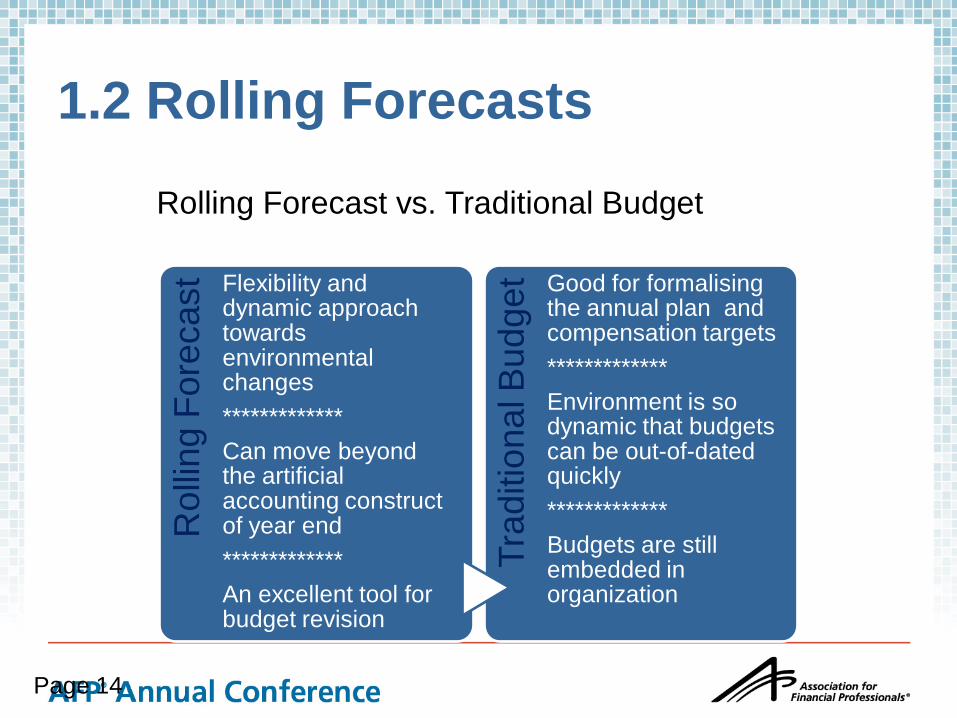

1.2 Rolling Forecasts

Page 14

Rol

ling

Fore

cast

Flexibility and dynamic approach towards environmental changes ************* Can move beyond the artificial accounting construct of year end ************* An excellent tool for budget revision

Trad

ition

al B

udge

t Good for formalising the annual plan and compensation targets ************* Environment is so dynamic that budgets can be out-of-dated quickly ************* Budgets are still embedded in organization

Rolling Forecast vs. Traditional Budget

1.3 Activity-Based Budgeting

1.3 Activity-Based Budgeting • This is a very useful technique for Cost Management

• Variable costs in the forecast are adjusted to the

activity level

• Therefore budget is dynamic, not static

• The concept needs to be communicated to the departmental managers, it needs to be controlled and analysed by finance business partner before it becomes part of the business culture in traditional budget organisation

Page 16

1.4 Participative Planning

1.4 Participative Planning • Flexible planning process should be participative

• It should allow key people to contribute to the process

– from the top to the down – and from the down to the top

• Participative planning process helps with the following

– Risks identification – Connecting strategy with the operational plan – Improving communication and understanding business drivers

• That is why one of the most important elements for FP&A professionals

is the strength of their business partnerships

Page 18

2. DRIVER-BASED MODELLING

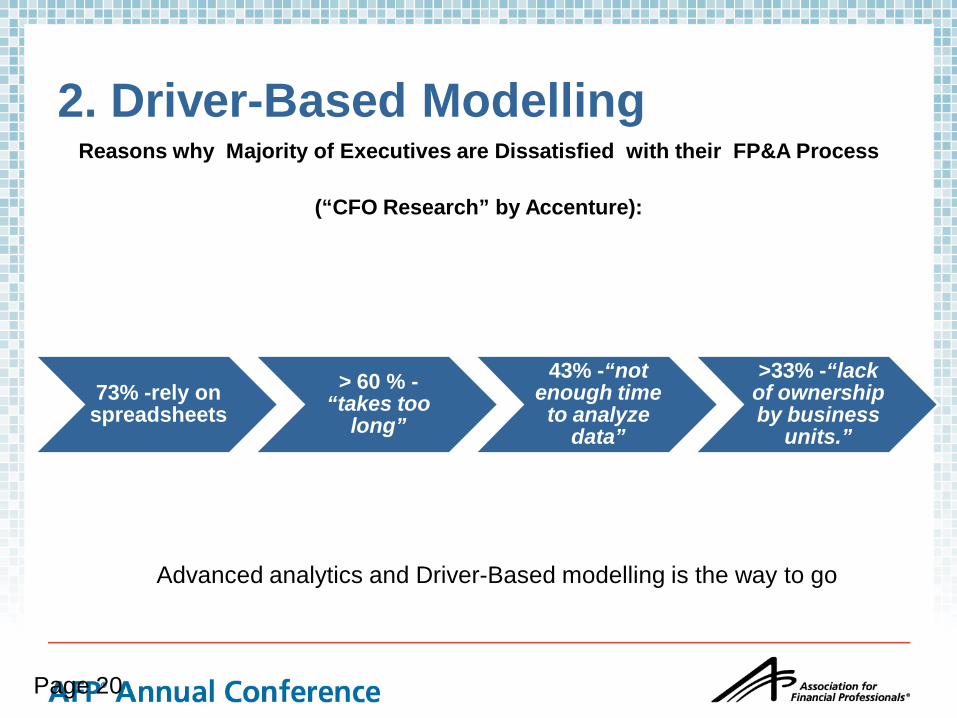

2. Driver-Based Modelling Reasons why Majority of Executives are Dissatisfied with their FP&A Process

(“CFO Research” by Accenture):

Page 20

73% -rely on spreadsheets

> 60 % -“takes too

long”

43% -“not enough time

to analyze data”

>33% -“lack of ownership by business

units.”

Advanced analytics and Driver-Based modelling is the way to go

2. Driver-Based Modelling

• It is important to concentrate on top 10-15 business drivers

• Analyse and manage the drivers

• Look at their interdependence

• Explain the variances through the drivers

• True-up driver-based modelling on a regular basis, avoid “black boxes”

Page 21

2. Driver-Based Modelling

–

Page 22

Examples of Powerful Forecasting Tools in Modern Systems:

• Detects trends like seasonality and automatically adjusts forecast

Historical trend forecasting

• Automatically selects the appropriate forecasting technique based on data

Multiple forecast methods

• Create forecast at a country level and apply it to the lowest level of details

Forecasting at many data levels

• Detect and correct data that falls outside of confidence level

Outlier detection/ Correction

• Change results based on internal business rules

Override scenarios

• Flag and adjust figures for months with special events Event planning

3. EXPANDING TIME/OTHER HORIZONS

3. Expanding Time/Other Horizons

• Accounting period is an artificial concept and it does not show us the “whole picture” – Life-time value of the product/ customer – This is important factor when we defer

acquisition costs

• Rolling forecast is an important concept in breaking artificial accounting period views

• Survival analysis techniques are becoming very popular in forecasting true future profitability of the business

Page 24

3. Expanding Other Horizons

• External drivers are important

• Managing and analysing non-tangible assets is a big trend

• Qualitative KPI’s are as important as quantitative

Page 25

4. “BEYOND BUDGETING”

4. “Beyond the Budgeting”

• The corporate budget has been an unquestioned activity for many organisations

• The anti-budgeting movement has grown ever louder since the nineties • The proponents of “Beyond Budgeting” argue that something is seriously

wrong with the budgeting process: – it makes organizations inward-looking and sclerotic – people spend their time on gaming the budget and negotiating the targets

• "It makes no sense to use a 19th-century tool to manage a 21st-century

company in a volatile global economy," contends Steve Player, an expert on budgeting and planning and the North American program director at the Beyond Budgeting Roundtable,

• Instead people should use their time on value-adding activates

Page 27

4. “Beyond Budgeting” Movement

• Beyond Budgeting is an alternative management philosophy that aims to redirect peoples’ creativity and energy towards activities that truly create value.

• “Jack Welsh, former CEO of General Electric, called the budgeting exercise the «bane of corporate America».

• Bob Lutz, former vice-chairman of Chrysler, saw it as a «tool for repression».

• Jan Wallander, former chief executive of Svenska Handelsbanken, the Swedish Bank, called it an «unnecessary evil».

• An increasing number of companies recognise that the budgeting system is perhaps the greatest barrier to change.

Page 28

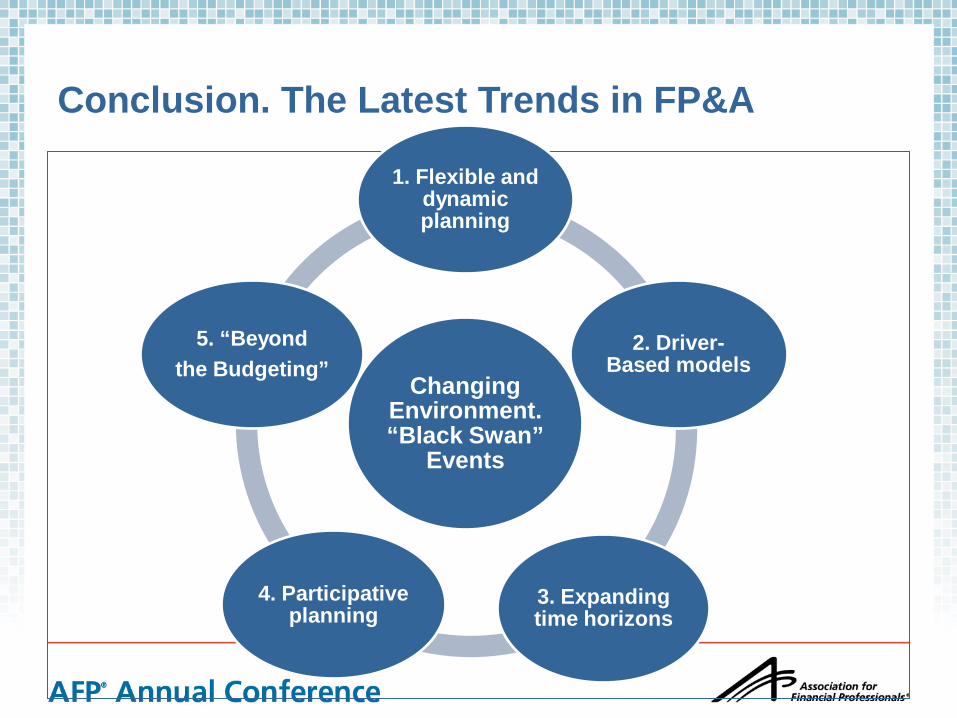

Conclusion. The Latest Trends in FP&A

Changing Environment.“Black Swan”

Events

1. Flexible and dynamic planning

2. Driver-Based models

3. Expanding time horizons

4. Participative planning

5. “Beyond the Budgeting”

Final Quote My favourite quote by professor J. Brian Quinn from Dartmouth:

“A good deal of corporate planning is like a ritual rain dance; it has no effect on the weather that follows, but those who engage in it think

it does. It seems to me that much of the advice and instruction related to corporate

planning is directed at improving the dancing, not the weather.” This the simple reminder for us in FP&A world to constantly ask: "Am I focused on improving the dance, or the weather?"

Page 30

Thank you!