financial performance of national bank limited

DESCRIPTION

Every student of Master of Business Administration (MBA) Program has to undergo a practical orientation (Internship) in any organization for fulfilling the requirements of program. In order to fulfill this requirement of the Internship program I have chosen National Bank Limited. The main purpose of the program is to know the real world situation. The tropic of my report is “Financial Performance of National Bank Limited”.In this regard I have opportunity to make my internship in National Bank Limited (Elephant Road Branch). The National Bank Limited is a scheduled private commercial bank established on 23rd March, 1983.TRANSCRIPT

Financial Performance of National Bank Limited

CHAPTER: 1

INTRODUCTION OF THE REPORT

1.0 Origin of the report:

Every student of Master of Business Administration (MBA) Program has to undergo a practical orientation (Internship) in any organization for fulfilling the requirements of program. In order to fulfill this requirement of the Internship program I have chosen National Bank Limited. The main purpose of the program is to know the real world situation. The tropic of my report is “Financial Performance of National Bank Limited”. In this regard I have opportunity to make my internship in National Bank Limited (Elephant Road Branch). The National Bank Limited is a scheduled private commercial bank established on 23rd March, 1983. During this short span of time, the bank has been successful to position itself as a progressive and dynamic financial institution in the country.

National bank was born as the first hundred percent Bangladeshi owned bank in Private sector. The then President of the People’s Republic of Bangladesh Justice Ahsanuddin Chowdhury inaugurated the bank formally on March 28, 1983. NBL was first domestic bank to establish agency arrangement with the world famous Western Union in order to facilitate quick and safe remittance of the valuable foreign exchanges earned by the expatriate Bangladeshi nationals. NBL was also the first among domestic banks to introduce Master Card in Bangladesh. Since the very beginning, the bank exerted much emphasis on overseas operation and handled a sizeable quantum of homebound foreign remittances. The Bank established extensive drawing arrangement network with banks and exchange companies located in important countries of the world.

The success status of the National Bank Limited is determined by the effectiveness of the Foreign Exchange Operation. Foreign exchange plays an important role in any country. The foreign exchange market has played a vital role in the last decade in guiding the purchase and sale of the goods, service and raw materials globally. The market directly affects each country bond, equities, private property, manufacturing and all assets that are available to foreign investors. In the foreign exchange, I saw that we had to import a lot more than we export. Other than export the remittance by non-resident Bangladeshi and foreign aid is another source of foreign currency. In

the foreign exchange business exchange rates has been declared floating and central bank has taken its full control from the market.

1.1 Importance of commercial banking in the economy of Bangladesh:

Banking system occupies an important place in a nation’s economy because of its intermediary role; it ensures allocation and reallocation of resources and keeps up the momentum of economic activities. A banking institution is indispensable in a modern society. It plays a pivotal role in the economic development of a country and forms the core at the money market of any country. In a developing country like Bangladesh the banking system as a whole has a vital role to play in the progress of economic development. The overall purpose of banking is to collect money from surplus unit and transfer it to the deficit unit. The subject of my report is “Financial Performance of National Bank Ltd”. So my focus is mainly on financial activities of NBL for contributing to the profit of the bank.

Foreign trade plays an important role in economic development of a country. The economic development of a country is comprised with domestic production and foreign trade (especially the balance of export and import). It plays a vital role in the balance of payment (BOP) of a country. Surplus (export-import) is favorable for a country. Although Bangladesh usually has deficit BOP (import-export) it has to continue foreign trade. Because it needs to import the essential goods and services, which are not produced domestically. In this sense, foreign trade is essential for each and every country for its complete economic development Devaluation or exchange rate fluctuation may influence the export import business and inward remittance.

To conduct foreign trade of a country, bank plays an important role; usually this duty is played by commercial banks. As a commercial bank, National Bank Limited (NBL) is also engaged in the foreign trade of Bangladesh. Foreign trade operations play a significant role in the overall business of NBL in order to strengthen its position. NBL has further consolidated its relationship with the existing network of international correspondents.

Banking sector is one of the fastest growing sectors in our country. There are more than 50 banks operating in BD which includes local and foreign bank. Some new banks are coming in the market. Therefore, the banking industry is very much lucrative and at the same time very competitive too. All banks are offering newer products and facilities to attract the customers and retain them. To get new customers and hold the existing customers depend mostly on satisfying them. If any bank can satisfy its existing customers, they will not leave it, as there is a question of security.

Attracting new customers depends on the launching of new products and lucrative offers to them, in the past, theorists emphasized on satisfying the customers but they now are emphasizing on delighting the customers. To delight a customer, a bank will have to give more than its competitors do. Nowadays customer satisfaction has become a very vital issue in business arena. It directly affects the profitability of a firm. Satisfied customers mean the profitable customers. Therefore knowing the customer satisfaction level is very important.

From this study, the bank authority will be able to detect their problems in providing and what people are expecting from them. In this study, I tried to find out their financial performance. From

the findings of the study, the management would be able to have a real scenario of their present condition and take proper steps to make a better and profitable future.

1.2 Objectives of the Study

The result of a study depends upon the proper selection of the objectives. Before starting the fieldwork, it is essential to set up the objectives and then arrange the total procedures according to the objectives. I have some objectives about preparing the report. Some of these are related directly with welfare of the bank and some are related with my program. These can be divided into the following types –

Broad Objective Specific Objective

1.2.1 Broad Objective:

The broad objective is to evaluate the financial performance of the bank through ratio analysis.

1.2.2 Secondary Objectives:

The secondary objectives of the study are to gather practical knowledge regarding banking system and its operations. To fulfill these objectives, some specific areas were studied which include the following:

To present an overview of NBL; To know how the services could be made more customers responsive; To apply theoretical knowledge in the banking sector; To find out the position of NBL in the banking industry; To know about the remittance of funds; To know about the general banking performance of the NBL; To know the performance of NBL in foreign exchange aspect. To find out the growth rate of export and import operation of NBL. To examine the rules and regulations of NBL; To find out existing problems of the bank; To know the risk factors and SWOT relating to the bank; To formulate alternative strategies for solving the problems; To formulate a contingency plan as a safeguard for changing situation; To study the existing overall banker customer relationship.

1.3 Scope of the study:

My Internship period was about three months. This period is not enough to learn or have practical orientation of every banking activity. I was assigned to the Elephant Road Branch of National Bank Limited. I have had an opportunity to gather experience by working in all departments of the branch. For making this case study survey were conducted on Head Office and Elephant Road Branch of National Bank Limited.

The report will cover the all departmental activities as performed by National Bank Ltd. Analysis of the facts and figures and conclusion will be drawn based on the findings. These will help for the development & in the audited financial statements of the National Bank Ltd.

An overview of the National Bank Ltd. General Banking activities of the National Bank Ltd. Foreign Exchange activities and its contribution to total income. Loans and advances of the National Bank Ltd. Main focus of this report is financial performance of the bank on the basis of

Annual report data which was funded by the banking activities.

1.4 Methodology:

Methods followed to perform a job or conducting activities to complete a task is called methodology. Data collection is very important to prepare a report. The report was written on the basis of information collected from primary as well secondary sources. The primary information was collected by discussions with the customers of bank as well as with some officials of the bank. The Secondary information was collected from the bank’s records, corporate newsletter, branch manuals, various publications of the bank and Bangladesh Bank. Annual report (Income Statement) and made discussion with the officials of Elephant Road Branch, international division and other department about methods and procedures of export-import business, problems related to foreign exchange transactions etc. I also had to talk to the exporters and importers for getting impression about NBL.

Sources of data: In this report, I have relied on both primary and secondary sources of data. The sources are as follows:

Primary Sources:

Oral and informal interview of officers and employees in National Bank. Practical work exposure achieved from different desks of the bank. Informal interview with the exporters and importers. Personal observation

Secondary Sources:

Annual report of National Bank Ltd. Printed forms and documents supplier by NBL. Relevant books, journals, Booklets. Booklets of international Division of NBL. Various Web sites related with this topic. Officials records of National Bank Ltd.

For successful completion of the report, I will use the following tools and techniques:

I will present the report in a descriptive as well as analytical way.

Various ratios- ROA, ROI, ROE, Leverage Ratio, Profitability Ratios etc. will be used.

Various graphs and tables will be used for analyzing the collected data. For analysis I use different types of statistical tools such as Regression Line,

Correlation of Coefficient, and Coefficient of variation. These methods help me to finds the true calculation. But as statically methods, we know those methods have some limitation, which also may affect the calculation of this report.

Questionnaire Design:

Questionnaire designing is a very tough task as it will be worthless if it does not serve the objective of the survey. In designing the questionnaire, I had to keep in mind all these things. I have used normally 5-point scale. But for the questionnaire in which I wanted to know the satisfaction level directly, there I used 4-point scale, because if I would use the option "neutral" some respondents would use it to avoid giving direct answer.

1.5 Limitations of the report:

Every thing has its limitations. My report is not also out of weakness. There were several constrains while preparing this report. I have considered the following causes as the limitations of the study.

Although I have obtained wholehearted co-operation from employees of NBL, Elephant Road branch but they could not manage enough time to deal with my report.

The main limitation for me was the fact I was working away from the foreign exchange department for one month for the internship program. Therefore, I have too short time to understand the process of foreign Exchange in NBL, which is not sufficient to have a complete knowledge about the topic.

The annual reports are the main secondary source of the information but this information was not enough to complete the report.

The data in some cases may suffer from lack of reliability to some extent.

The study was not done very successfully due to inexperience.

National Bank Limited has no regular publication.

It was very difficult to identify the present situation of the organization in such a small period of time.

Another limitation of this report is Bank’s policy of not disclosing some data and information for obvious reason, which could be very much useful.

Despite the limitations, I have tried my best to prepare the report in a fruitful manner.

The next chapter deals with the Profile of National Bank Limited.

CHAPTER: 2PROFILE OF NATIONAL BANK

2.0 Backdrop of the Bank:

The banking sector of Bangladesh comprises of three categories of schedule banks. These are nationalized commercial banks (NCBs), private commercial banks (PCBs) and foreign commercial banks (FCBs). Private commercial banks are again divided into three categories- First generation, Second generation and Third generation. National bank falls into the first generation segment and undoubtedly leads its own generation. As an intern from business discipline with major in finance I have got the opportunity to work with this bank and try to put my effort to make a depth study.

Banking system occupies an important place in a nation’s economy. Banking institution is indispensable in a modern society and it plays a vital role in the economic development of a country. Against the background of liberalization of economic policies in Bangladesh, National bank Limited emerged as a new commercial bank to provide efficient banking services with a view to improving the socio-economic development of the country.

National Bank Limited was born as the first hundred percent Bangladeshi owned Bank in the private sector. From the very inception it is the firm determination of National Bank Limited to play a vital role in the national economy. NBL are determined to bring back the long forgotten taste of banking services and flavors. Want to serve each one promptly and with a sense of dedication and dignity. The then President of the People's Republic of Bangladesh Justice Ahsanuddin Chowdhury inaugurated the bank formally on March 15, 1983 under Companies Act 1913 (Companies Act. 1994) to carry out banking business. And it obtained license from Bangladesh Bank for carrying out banking business on 22 March 1983. But the first branch at 48, Dilkusha Commercial Area, Dhaka started commercial operation on March 23, 1983 with authorized capital TK. 10.00 million and paid up capital of TK. 80 million was subscribed by the sponsors/directors and TK. 4.00 million was subscribed to the government and remaining TK. 36 million has been fully subscribed by the public. The 2nd Branch was opened on 11th May 1983 at Khatungonj, Chittagong. During this short span of time, the Bank has been successful to position itself as a progressive and dynamic financial institution in the country.

NBL has its prosperous past, glorious present, prospective future and under processing projects and activities. Established as the first private sector Bank fully owned by Bangladeshi entrepreneurs, NBL has been flourishing as the largest private sector Bank with the passage of time after facing many stress and strain. The member of the board of directors is creative businessman and leading industrialist of the country. To keep pace with time and in harmony with national and international economic activities and for rendering all modern services, NBL, as a financial institution automated all its branches with computer network in accordance with the competitive commercial demand of time. Moreover, considering its forth-coming future the infrastructure of the Bank has been rearranging.

The Bank had been widely welcome by the business community, from small entrepreneurs for forward-looking business outlook and innovative financing solutions. Thus, within this very short

period it has been able to create an image for itself and has earned significant reputation in the country’s banking sector as a bank with vision. The company Philosophy –“A Bank for Performance with Potential” has been exactly the essence of success of this Bank. One of the main objectives of the bank is to be a provider of high quality products and services to attract its potential market .The bank also caters to the needs of it corporate clients and provides a comprehensive range of financial services to national and multinational companies.

National Bank Limited has been licensed by the Government of Bangladesh as a scheduled Bank in the private sector in the process of the policy of liberalization of banking and financial services or Bangladesh. In view of the above, the Bank has, within a period of twenty five years of its operation, achieved a remarkable success and has always met up capital adequacy requirement set by Bangladesh Bank.

There are eighteen Sponsors involved in creating National Bank Limited; the sponsors of the Bank have a long heritage of trade, commerce and industry. They are highly regarded for their entrepreneurial competence. The sponsors happen to be member of different professional groups among whom are also renowned banking professionals having vast range of banking knowledge. There are also members who are associated with other financial institution like companies, leasing company’s etc.

The board of directors consists of fourteen members elected from the sponsor of the bank. And the board of directors is the apex body of e bank. All route matters beyond delegated owners of management are decided upon by or routed through the executive committee, subject to ratification by the board of directors.

2.1 Social Responsibility of this Bank:

Banking is not only a profit-oriented commercial institution but it has a public base and social commitment. Admitting this true NBL is going on with its diversified banking activities. The bank set up National Bank foundation for extending charitable and beneficial social services to the society. National Bank has been able to manage sound position for it in innovative deposit schemes. NBL has performed well in the foreign trade. The volume of trade is growing in both import and export business. The bank is increasing its level of performance, which is evident in the increase of asset utilization of ratio, net profit, and asset portfolio. We observe that National Bank has a suitable position for its foreign exchange reserve, liquidity positions and relationship with financial institutions. But the bank cannot operate with its full capacity for its conservative nature.

Despite the stiff competition in the banking industry, this bank also considers it essential for company to behave in responsible manner towards both the environment and society. This belief exists on two pillars. First, to be successful on a long-term basis, they need to trust their stakeholders-customers, shareholders, employee patrons and well-wishers and society. Behaving responsibility towards society and the environment strengthens this trust. Second, by taking ecological and social risks and reward into account.

This bank commitment has always been to behave ethically and to contribute towards the quality of life of our people, the local community and generally the society. The corporate social responsibility focuses on:

Sustainable Banking products: These have introduced a number of banking products for people who have traditionally been excluded from the banking services. This National Bank has also offered SME banking products for marginal people. Small and marginal savers are encouraged to use banking services and attractive rates of interest are offered for small savers as well.

Employment: NBL has been continuously creating new fields of employment every year by way of expansion of its business activities and branch networks. In 2009, the bank created employment for 305 personnel.

Supporting Education: National Bank Foundation was established in 1989 for fulfilling responsibilities for welfare of the society .It has been running the National Bank public School and collage in Moghbazar, Dhaka. There are 892 students studying in the school section form class 1 to class 10, while there a total of 234 students in the collage section. In 2008, 53 students appeared at the SSC Examination and among them, 25 students achieved Golden A+ while 32 students appeared at the H.S.C. examination out of which 4 students achieved Golden A+. The bank has been accommodating prospective graduates o recognized universities for completing their internship. NBL also awarded stipends and scholarships to the brilliant children of the employees of the bank.

Rural Credit Program: Under its Rural Credit Program, NBL, with joint collaboration of the Barendra Bahumukhi Unnayan Katripakkha, has been providing improved technology, irrigation facility, agricultural equipments, etc. through disbursement of small credit to the farmers of three districts (Rajshahi, Naogaon, & Chapai Nawabgonj) of Rajshahi Division. A total of TK.133.70 million has been disbursed among 24,473 farmers under the program up to 31 December 2008. The rate of recovery is 95%. Besides, NBL disbursed TK.144.78 million and TK.32.05 million among small and medium entrepreneurs respectively under the Agro based Industries & Technology Development Project (ATDP) for setting up of agro based industries and extension of agricultural technology.

Supporting Sports and Culture: National Bank Ltd. has a tradition of patronizing and sponsoring sports and cultural activities of the country. The “National Bank Volleyball league -2007” was arranged under patronization of the Bank. NBL has been arranging annual picnic for gathering and recreation of its executives, officers and staff. Besides, the Bank stands as a friend by the side of helpless people in times of calamities. Thus, as a token of sincere fellow feeling and sympathy, NBL distributed winter clothes among the cold stricken destitute people in northern region of the country from its own funds and with one day's salary of the Officers and Executives of the Bank.

Disaster and relief: NBL always extends its helping hands and stands by the suffering and helpless people in times of natural calamities. In 2007, NBL donated TK.40 Lac to help the victims of flood, TK.20 Lac for relief operation for landslide victims and TK50 Lac for Sidr victims to the relief fund of the Chief advisor and the Army Chief. The Bank has also taken a pilot project for post flood agricultural rehabilitation at Sirajgonj.

On 10th March, 2009 a Payment Order for Tk.25.00 Lac has been handed over to the Honorable Prime Minister as a donation/financial assistance to the bereaved family members of the martyred Army Officers killed in the BDR carnage held on 25th February, 2009. On 1st April, 2009, NBL donated Tk. 24.00 Lac to the Hon'ble Prime Minister to hand over the same to the family members of the martyred Army Officer which will be paid to 5 (five) families @ Tk. 40,000/- per month to each family for 1 year which will continue for 10 years. Thus total amount of donation will be Tk. 2.40 Crore.NBL has always maintained their corporate social responsibility in various ways. NBL always appreciate various kinds of fair, festival and other gatherings organized by different private or public sectors.

Assisting the rural economy: The bank is well aware of the socio-economic condition of the country. The bank has emphasized to expand its operation in rural areas to help boost the agriculture and rural economy. National Bank opened 11 branches in 2008 of which ten are located in rural areas. The bank provides collateral free loans to marginal farmers. Moreover, the bank has introduced collateral free festival small business loan and NBL small business loan to cater the need of small traders. Beneficiaries of this scheme are mostly from rural areas. The schemes are playing important role in changing the living standard of the small businessmen.

2.2 Divisions of NBL:

Name of the divisions of NBL are as follows:

Human Resource Divisions (HRD): It is one of the important divisions of the Bank. The Division formulates the draft policies of the Bank that is usually placed in the Board meeting to accept. This division controls all the administrative activities of the Banks. It is assigned to the responsibilities of recruitment, posting, transfer, promotion and development of human resources of the bank. They also maintain service record of the employees, take disciplinary action, look for the employee’s welfare, salary reconciliation, specimen signature etc.

General Banking Divisions: General banking is the staring point of all the banking operations. This department carried out the most important and basic works of the bank. It also provides various instant saves to the customers. Administrative activities are mainly done in general banking division- To control these activities divisions’ issues necessary circulars.

NBL other activities regarding general Banking are:

Opening New Branches, Issuance of power of attorney to the officer of the bank, Customer Service’s, Legal Affairs, General Correspondence with Bangladesh Cash affairs of the Bank.

Internal Control and Compliance Division: The main responsibilities of this division are to maintain inter branch accounts and maintaining everything of all the branches all over the country including Head Office also. At the time of inspection the officers audit

the books accounts, observe their performances and takes note on the issues, which they think, are not fit to the originality. In this way each and every branch all over the country comes under H/O's supervision.

Financial Administration Division (FAD): This Division is responsible for maintaining and enhancing standard of customer service, mobilize deposits for the bank and deals with public relation affairs.

International Division: International Division of National Bank Limited performs the responsibilities of foreign trade and foreign remittance on behalf of its branches. It plays a middlemen role between a Branch of NBL and Foreign correspondents in the case of Export-Import and other Foreign Exchange activities.

Import Department: The import department deals with all the issues regarding opening, lodgment and payment of import letter of credit.

Export Department: This department also deals with the matters relating to export such as advising, negotiation export documents etc.

General Service: This department is maintaining all sorts of accounts of a bank, performs fund management, management information system, expenditure control etc. They procure and supply dead lock such as furniture, machinery, equipment, stationary, and vehicles, render some other common services and control central dispatch service.

Information Technology Division: This division is assigned to lead the computerization of the bank. As all Branches of NBL expect sandpit become computerized this Division have a lot of activities to maintain all Branches. If any problem is faced by any officer of any Branches he/she can get help by telephone and get guidance from this Department. For significant problem this Division sends their related specialist to this Branch to correct this problem. On the other tins Division always helps by providing latest software of banking sector. They procure and maintain computer hardware, and software, conduct computer training for the employees.

Card Division: The Bank sets this Division only for implementation purpose of its Credit Card service. This Division controls all activities dealing with operation of Credit Card. The Bank implemented its Credit Card operation on March 20, 1997.

Marketing Division: It is directly related to the marketing of the Bank's services. It takes all the arrangement in Deposit mobilization, customer service related activities and all other marketing related activities. The main task of this Division is to formulate strategies for achieving the Bank's corporate objectives.

Credit and Investment Division: This division is one of the most important divisions of a bank because it controls all loans and advances. One of the main objectives of the bank is to take part of the Capital market and Money market in the country. To achieve this objective the bank established investment division in which several departments are working.

Law and Recovery Division: NBL has a separate Division for recovery of classified stuck up advances and to take lawful actions against these types of defaulters. The main task of this Division is to make proposal to take lawful action against the classified and stuck-up loan holders.

2.3 Network of the Branches:

National Bank has 121 existing branches & 10 SME centers, and some other proposed branch all over Bangladesh to provide better services to their valuable customer. The bank has one or more branches in important & lucrative places so that the customer can easily reach to it. Because NBL knows- speed & convenience of place and time for the customers are becoming important determinants in service delivery strategy. Some important location on NBL can represent their sense of place & timing. The objective of NBL is not only to earn profit but also keep the social commitment and to ensure its co-operation to the persons of all levels, to the businessmen, industrialists-specially who are engaged in establishing large scale industries by consortium and the agro-based export oriented medium and small scale industries by self inspiration. NBL as the largest private bank is committed to continue its endeavor by rapidly increasing the investment of honorable shareholders into asset.

NBL has many international branches. Those branches are situated in all over the world.Those branches are in USA, Switzerland, Singapore, Malaysia, Oman, Qatar, UAE, Kuwait and Saudi Arabia.

Figure: Branches of National Bank limited in Bangladesh.

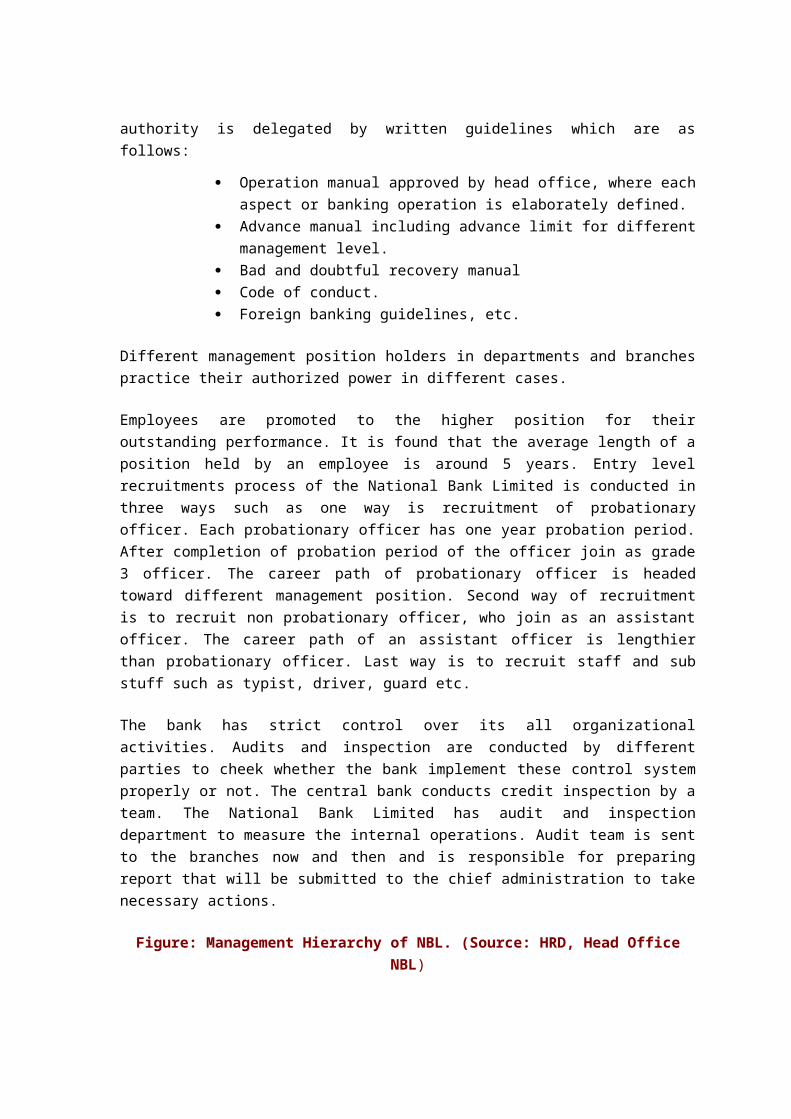

2.4 Management Hierarchy of NBL:

Highly qualified and efficient professionals manage this bank. Board of Directors who also decides the composition of each committee determines the responsibilities of each committee. All routine matters beyond delegated powers of management are decided by or routed through the executive committee, subject to ratification by the Board of Directors. In operating the organization, management plays a vital role. Many things are dependent on the management. So every organization should be very careful about the management structure. It depends on the company's business ethics.

From the top to the bottom management body can be divided into four levels:

Top-level Management Executive level Management Mid level Management Junior level

The management processes are as follows:

The strategic planning approach in NBL is top down. Top management formulates strategy at the corporate level and then it transmits through the division to the individual objects. Board of directors usually takes the decisions. Organization of National Bank Limited is based on departmentalization. The organization is divided into twelve departments headed by Executive Vice President or Senior Vice President. In the National Bank Limited the whole operation is centralized and authority is delegated by written guidelines which are as follows:

Operation manual approved by head office, where each aspect or banking operation is elaborately defined.

Advance manual including advance limit for different management level. Bad and doubtful recovery manual Code of conduct. Foreign banking guidelines, etc.

Different management position holders in departments and branches practice their authorized power in different cases.

Employees are promoted to the higher position for their outstanding performance. It is found that the average length of a position held by an employee is around 5 years. Entry level recruitments process of the National Bank Limited is conducted in three ways such as one way is recruitment of probationary officer. Each probationary officer has one year probation period. After completion of probation period of the officer join as grade 3 officer. The career path of probationary officer is headed toward different management position. Second way of recruitment is to recruit non probationary officer, who join as an assistant officer. The career path of an assistant officer is lengthier than probationary officer. Last way is to recruit staff and sub stuff such as typist, driver, guard etc.

The bank has strict control over its all organizational activities. Audits and inspection are conducted by different parties to cheek whether the bank implement these control system properly or not. The central bank conducts credit inspection by a team. The National Bank Limited has audit and inspection department to measure the internal operations. Audit team is sent to the branches now and then and is responsible for preparing report that will be submitted to the chief administration to take necessary actions.

Figure: Management Hierarchy of NBL. (Source: HRD, Head Office NBL)

Managing Director (CEO)

Additional Managing Director

Deputy Managing Director

Senior Executive Vice President

Executive Vice President

Senior Vice President

Vice President

Senior Assistant Vice President

Assistant Vice President

Senior Principal Officer

Principal Officer

Officer

Probationary Officer

Figure: Organizational configuration of Elephant Road Branch, National Bank Ltd.

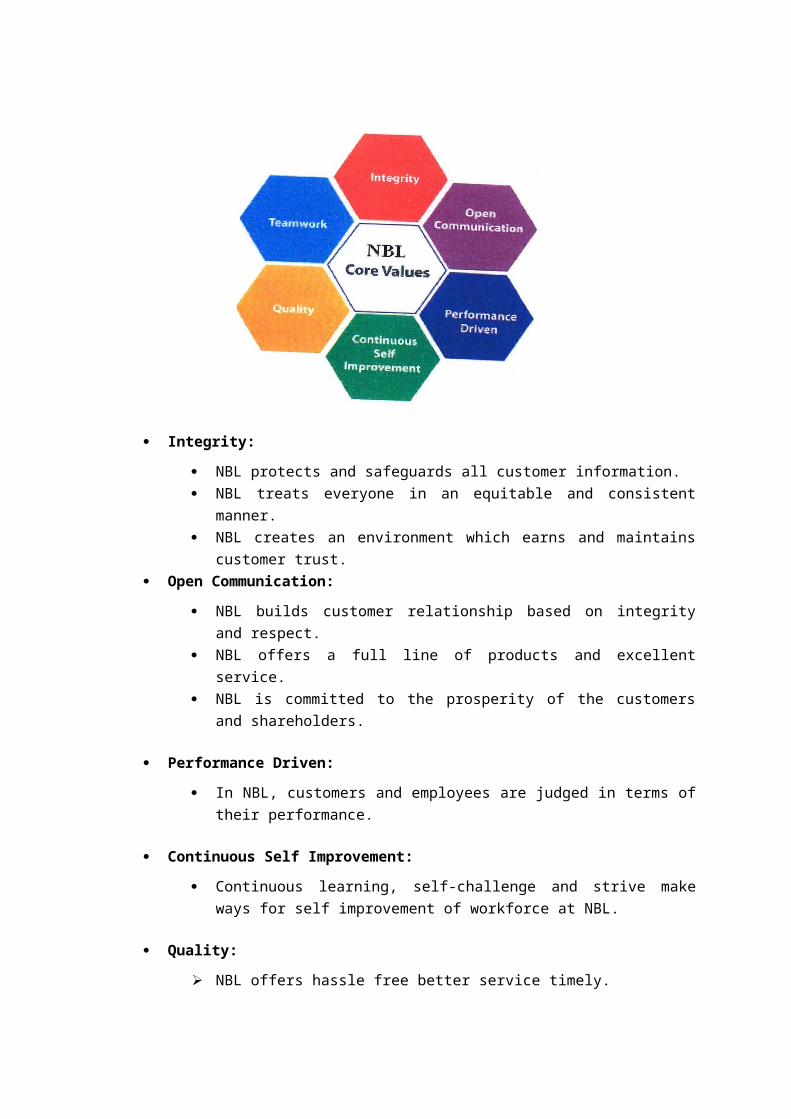

2.5 NBL Core Values:

NBL's core values consist of 6 key elements. These values bind their people together with an emphasis that their people are essential to everything being done in the bank.

Integrity:

NBL protects and safeguards all customer information. NBL treats everyone in an equitable and consistent manner. NBL creates an environment which earns and maintains customer trust.

BRANCH MANAGER

2nd OFFICER

GENERAL BANKINGFOREIGN EXCHANGE

SENIOR PRINCIPAL OFFICER

ASSISTANT VICE PRESIDENT

SENIOR PRINCIPAL OFFICER

OFFICER

JUNIOR OFFICER

OFFICER

JUNIOR OFFICER

TRAINEE ASSISTANT OFFICER

OFFICER

JUNIOR OFFICER

TRAINEE ASSISTANT OFFICER

FOREIGN EXCHANGE GENERAL BANKINGINVESTMENT

SENIOR PRINCIPAL OFFICER

Open Communication:

NBL builds customer relationship based on integrity and respect. NBL offers a full line of products and excellent service. NBL is committed to the prosperity of the customers and shareholders.

Performance Driven:

In NBL, customers and employees are judged in terms of their performance.

Continuous Self Improvement:

Continuous learning, self-challenge and strive make ways for self improvement of workforce at NBL.

Quality:

NBL offers hassle free better service timely. NBL builds-up quality assets in the portfolio.

Teamwork:

Interaction, open communication and maintaining a positive attitude reflect NBL's commitment to a supportive environment based on teamwork.

With this discussion of the profile of National Bank Limited the next section deals with General Banking operation of National Bank Limited.

CHAPTER: 3

GENERAL BANKING

3.0 Introduction:

Bangladesh is one of the least developed Countries. So the economic development of the country depends largely on the activities of commercial Banks. So I need to emphasis whether these commercial Banks are effectively and honestly performing their functions, their assigned duties and responsibilities. In thus respect I need to know about the general banking function of those Banks as well as the NBL.

The general banking department does the most important and basic works of the bank. All other departments are linked with this department. It also pays a vital role in deposit mobilization of the branches. NBL provides different types of accounts, locker facilities and special types of saving scheme under general banking. Since bank is confined to provide the services everyday, general banking is also known as ‘retail banking’. For proper functioning and excellent customer service this department is divided into various sections namely as follows:

1) Account opening section

2) Deposit section3) Cash section4) Remittance section5) Clearing section 6) Accounts section

According to the law and practice, the Banker-Customer relation arises only from contract between these two. And opening of account is the contract that establishes the relationship between a banker and a customer. So this section plays a very important role in attracting customer and therefore should be handled with extra care.

According to the international code of conduct banks should maintain the following steps regarding their customers-

Banks will act fairly and reasonably in all their dealings with their customers. Banks will help customers understand how their accounts operate and seek to give

them a good understanding of banking services. Banks should maintain confidence in the security and integrity of banking and

payment systems.

3.1 ACCOUNT OPENING SECTION:

Account opening is the gateway for clients to enter into business with bank. It is the foundation of banker customer relationship. This is one of the most important sections of a branch, because by opening accounts bank mobilizes funds for investment. Various rules and regulations are maintained and various documents are taken while opening an account. A customer can open different types of accounts through this department.

When a customer / organization / company / firm / society / club etc wants to open a bank account he/she has to filled a bank prescribed form and have to attach their organization’s documents are follows: Proprietorship Partnership Private Limited Trade License Trade License Trade LicensePhotograph Photograph Photograph of Directors

Partnership Deed Certificate copy of Memorandum and Articles of AssociationCertificate of Incorporation /IntroductionList of Directors as per Return of Joint Stock Company with SignatureResolution for opening account with the bank

After observation of all the formalities/documents mentioned above, an applicant is required to deposit minimum Tk.500 for opening a saving bank account and Tk.1000 for opening a current account, which is called initial deposit. As soon as this money is deposited, the bank opens an account in the name of the applicant. It should be noted that the permission of the competent authority for opening of an account is necessary.

3.1.1 Savings Account:

National Bank Limited offers customers a hassle free and low charges savings account through the branches all over Bangladesh. This deposit is primarily for small-scale savers. There are certain limitations in Savings Account, i.e., customer can draw only twice a week, if they want to get interest on the deposited money. If a customer draws more than twice in a week he will not receive any interest for that month. Heavy withdrawals are permitted only against prior notice. Customer Benefit:

Cheque book facility Opportunity to apply for safe deposit locker Utility payment service Collect foreign remittance Transfer of fund from one branch to another by-

o Demand drafto Mail transfero Telegraphic transfer

Online banking service.

Saving Accounts Interest Rate is 4.5%. For getting interest:

Minimum balance must be TK. 2000/= for any circumstances. Frequent of withdrawal not more than twice in a week (week start from day 1 of

current month). Maximum withdrawn in a single Cheque is 25% of balance. All Govt. Tax/Duty/ Levy will be applied on interest paid against the deposit.

3.1.2 Current Deposit Account:

National Bank Limited offers customers current deposit facility for day-to-day business transaction without any restriction. The Elephant Road branch of National Bank facilitates customers with different types of current account. There are current accounts for individuals, proprietorship firms; partnership firms, Joint Stock Company, school, college, association, trust and N.G.O. Account opening form for these categories are different. Some terms and documents may differ but the overall process of account opening is similar to that of the saving account. Here I like to state what kinds of information to be furnished in the form and which documents customer should provide.

Current Account (individual): Elephant Road branch uses the forms distributed by the NBL head office for opening a current personal/ individual account. A customer should meet the following requirements to see an account has been opened in his/ her name:

Name of the applicant Profession or business of applicant Address of the applicant Photographs of the applicant

Introduced by an account holder of the branch Signature on the application form Signature on the specimen signature card Verification of details and signatures by authorized officer.

Current Account (Proprietorship): To open a proprietorship current account photocopy of trade license, attached by the concerned officer, is required along with the procedure mentioned for individual current account.

Current Account (Partnership): Opening procedure of a partnership current account is almost same as the opening of individual current account but some additional documents are required which are follows:

Partnership deed Letter of partnership Trade license

Current Account (Joint Stock Company): All the formalities of individual current account opening should be met for the opening of Joint Stock Company; additionally following documents also should be submitted to the bank. These documents are:

Registration certificate from Register of joint stock companies Certificate incorporation Memorandum of association Articles of association Annual audit report Copy of board Resolution containing Name of the persons authorized to operate the bank account on behalf of the

company. Name of the persons authorized to deal documents with the bank.

NBL current account meets the needs of individual and commercial customers through its schedule benefit. Customer Benefits are:

Cheque book facility Opportunity to apply for safe deposit locker facility Collect foreign remittance in both T.C. and Draft. Transfer of fund from one branch to another by

Telegraphic Transfer Demand Draft Mail Transfer

Collection of cheque through clearing house. Online banking service.

3.1.3 Transfer of an Account:3.1.3 Transfer of an Account:

When an account is transferred from one office to another, the account opening form etc. signed at the time of opening account and any forms or documents which are necessary for its proper conduct at the time of transfer, must be forwarded under cover of form, to the office to which the

account is transferred together with the relative mail transfer, specimen signature card (s) and standing instruction if any, no exchange should be charged on such transfer. Attention is also invited in this connection. As per as possible the full information regarding the character, means and standing of the constituents and the way to the account has been conducted must be given to the receiving office.

3.1.4 Closing of an Account: The closing of an account may happen,

If the customer is desirous to close the account, If the NBL finds that the account is inoperative for a long duration. If the court of NBL issues garnishee order.

A customer may close his/her account any time by submitting an application to the branch. The customer should be asked to draw the final check for the amount standing to the credit of his/her account less the amount of closing an other incidental charge and surrender the unused check leaves. The account should be debited for the account closing charge etc. and the authorized officer of the bank should destroy unused check. In case of joint account the application for closing the account should be signed by the joint account holder. The fee for closing of an account is TK.100.00 for SB, CD or STD account.

3.2 DEPOSIT SECTION:

Deposit is the lifeblood of a bank. From the history and origin of the banking system we know that deposit collection is the main function of a bank.

3.2.1 Accepting deposits: The deposits that are accepted by National Bank like other banks may be classified in to—

a) Demand deposits: These deposits are withdrawn able without notice, e.g. current deposits. National Bank accepts demand deposits through the opening of-

Current account Savings account

b) Time deposits: A deposit which is payable at a fixed date or after a period of notice is a time deposit. National Bank accepts time deposits through Fixed Deposit Receipt (FDR), Short Term Deposit (STD) and Bearer Certificate Deposit (BCD) etc. While accepting these deposits, a contract is done between the bank and the customer. When the banker opens an account in the name of a customer, there arises a contract between the two. This contract will be valid one only when both the parties are competent to enter into contracts. As account opening initiates the fundamental relationship & since the banker has to deal with different kinds of persons with different legal status, National Bank officials remain very much careful about the competency of the customers.

3.2.2 Deposit Based Scheme:

Under deposit scheme, the National Bank Ltd offers different types of products (scheme) to help the fixed income people to save money and meet any future financial obligations. The schemes offer a large amount of money after a certain period of time if the account holders deposit a specific amount on monthly basis. The schemes are-

National Bank Monthly Savings Scheme (NMS): It is a deposit scheme where the depositor gets monthly benefit out of his deposit. The scheme is designed for the benefit of persons who intend to meet the monthly budget of their families from the income out of their deposit. It’s also known as DPS. Any citizen of Bangladesh can open this scheme. The scheme can be opened in the name of an individual only. NMS is perfect for those 18 of age or older. So one can save a fixed amount of money every month and get a lucrative amount of money after three, five or eight years. Effective rate of interest is 9% to 9.25% and 9.50% simultaneously. Some important features:

Monthly installment to be deposited 10th of the current month and installment of any amount can be deposited in advance.

For premature encashment interest at saving rate will be paid. Account will be automatically closed for failure of 3 consecutive

installments. Loan for 80% of deposit may be disbursed after 3 years. All Govt. Tax/Duty/ Levy will be applied on interest paid against the deposit.

Double Benefit Deposits Scheme (DBDS): Depositor’s money will be doubled in a seven-year period and the principal amount is refundable on maturity. Size and period of deposit

Tk. 10,000/= and multiple for 6 years For premature encashment interest at saving rate will be paid. Loan for 80% of deposit may be disbursed after 3 years. All Govt. Tax/Duty/ Levy will be applied on interest paid against the deposit.

3.3 CASH SECTION:

Banks, as a financial institution, accept surplus money from the people as deposit and give them opportunity to withdraw the same by cheque, etc. But among the banking activities, cash department play an important role. It does the main function of a commercial bank i.e. receiving the deposit and paying the cash on demand. As this department deals directly with the customers, the reputation of the bank depends much on it. The functions of a cash department are described below:

3.3.1 Function of Cash Department:

Cash Payment:

Cash payment is made only against cheque. This is the unique function of the banking system which is known as “payment on

demand”. It makes payment only against its printed valid Cheques.

Cash Receipt:

It receives deposits from the depositors in form of cash So it is the “mobilization unit” of the banking system It collects money only its receipts forms

Cash Packing:

After the banking hour cash is packed according to the denomination. Notes are counted and packed in bundles and stamped with initial.

3.4 LOCAL REMITTANCE:

Carrying cash money is troublesome and risky. That’s why money can be transferred from one place to another through banking channel. This is called remittance. Remittances of funds are one of the most important aspects of the Commercial Banks in rendering services to its customers.

3.4.1 Types of remittance:

Between banks and non banks customer. Between banks in the same country. Between banks in the different centers. Between banks and central bank in the same country. Between central bank of different customers.

The main instruments used by the National Bank of remittance of funds are:

Payment order ( PO) Demand Draft ( DD) Telegraphic Transfer (TT)

Payment Order (PO): Pay Order gives the payee the right to claim payment from the issuing bank. Payment is made from issuing branch only. Generally remit fund within the clearinghouse area of issuing branch. Bank charge only commission for this. However party must have an account with the bank, so that whenever the fund refund they (party) can collect it. But for the student and the pay order for job purpose of any applicant, account with the bank is not mandatory. Because in this case fund are non-refundable.

Demand Draft (DD): Demand Draft is an order of issuing bank on another branch of the same bank to pay specified sum of money to payee on demand. Payment is made from ordered branch. Generally remit fund outside the clearinghouse area of issuing branch. Payee can also be the purchaser. Bank confirm through checking the ‘Test Code’ Bank charge a commission and telex charge for it.

Telegraphic Transfer (TT): Issuing branch requests another branch to pay specified money to the specific payee on demand by Telegraph /Telephone. Payment is made from ordered branch. TT can be remit anywhere in the country. Bank charge a commission plus telephone charge. However this service is available only for a limited number of customers.

Mail Transfer Advice (MTA): Where the remitter desires the banker to remit the funds to the payee instead of purchasing a draft he, the banker does it though a Mail Transfer Advice. The payee must have an account with paying office as the amount remitted in such a manner, is meant for credit to the payee’s account and not for cash payment.

Balancing of remittance account: DD payable, TT payable, PO issued, DD paid without advice accounts should be balanced on monthly basis. The balances are agreed with the figure of concerned subsidiary account.

Issuance of duplicate Instruments: In case of losing or not receiving by the beneficiary the instrument issuing bank can issue of duplicate Pay Order or Demand Draft.

Cancellation of Instrument: If any reason the issued PO or DD is cancelled the branch cancelled the instrument and kept with the debit voucher for PO and for DD. No draft should be allowed to be cancelled without obtaining prior conformation from the draw branch.

3.4.2 Test – key Arrangement: Test key arrangement is a secret code maintained by the banks for the authentication for their telex messages. It is a systematic procedure by which a test number is and the person to whom this number is given can easily authenticate the same test number by maintaining that same procedure. National Bank has test key arrangement with so many banks for the authentication of LC message and for making payment.

3.4.3 Issuing FIXED DEPOSIT:

The Local Remittance section of National Bank Elephant Road Branch also issues FDR. They are also known as time deposit or time liabilities. These are deposits, which are made with the bank for a fixed period, specified in advance. The bank need not maintain cash reserves against these deposits and therefore, the bank offers higher of interest on such deposits. It’s a non-transferable account.

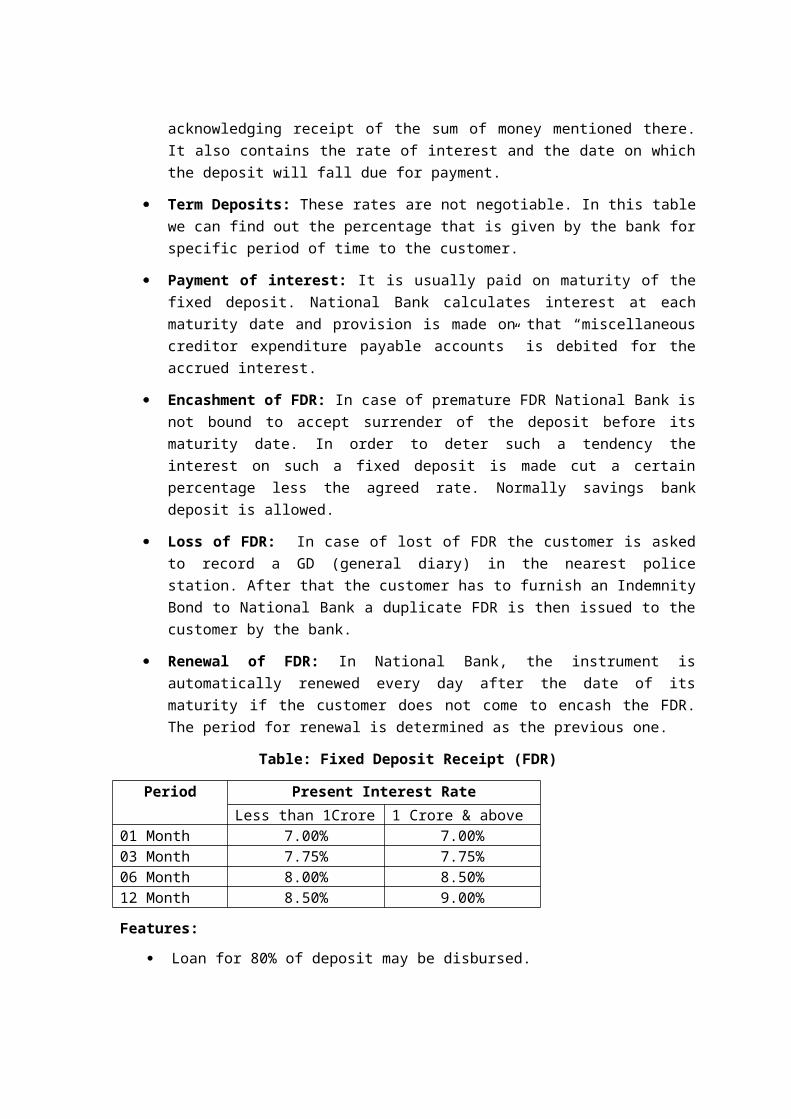

Opening of fixed Deposit Account: The depositor has to fill an account form where in the mentions the amount of deposit, the period for which deposit is to be made and name/names is which the fixed deposit receipt is to be issued. In case of a Joint name National Bank also takes the instructions regarding payment of money on maturity of the deposit. The banker also takes specimen signatures of the depositors. A fixed deposit account is then issued to the depositor acknowledging receipt of the sum of money mentioned there. It also contains the rate of interest and the date on which the deposit will fall due for payment.

Term Deposits: These rates are not negotiable. In this table we can find out the percentage that is given by the bank for specific period of time to the customer.

Payment of interest: It is usually paid on maturity of the fixed deposit. National Bank calculates interest at each maturity date and provision is made on that “miscellaneous creditor expenditure payable accounts” is debited for the accrued interest.

Encashment of FDR: In case of premature FDR National Bank is not bound to accept surrender of the deposit before its maturity date. In order to deter such a tendency the

interest on such a fixed deposit is made cut a certain percentage less the agreed rate. Normally savings bank deposit is allowed.

Loss of FDR: In case of lost of FDR the customer is asked to record a GD (general diary) in the nearest police station. After that the customer has to furnish an Indemnity Bond to National Bank a duplicate FDR is then issued to the customer by the bank.

Renewal of FDR: In National Bank, the instrument is automatically renewed every day after the date of its maturity if the customer does not come to encash the FDR. The period for renewal is determined as the previous one.

Table: Fixed Deposit Receipt (FDR)

Period Present Interest RateLess than 1Crore 1 Crore & above

01 Month 7.00% 7.00%03 Month 7.75% 7.75%06 Month 8.00% 8.50%12 Month 8.50% 9.00%

Features:

Loan for 80% of deposit may be disbursed. All Govt. Tax/Duty/ Levy will be applied on interest paid against the deposit.

3.4.4 Sundry Deposit:

This type of deposit is not directly opened for the public. No application is required to open this type of account. Any amount which cannot be debt or posted under any account head that amount is kept under the head of sundry deposit account. There are some account which are not transacted very frequent and some time the customer encase their money through passbook but they forget to mention their account or and sometime people deposit some amount in an account.

3.4.5 Resident Foreign Currency Deposit (RFCD):

Specially designed foreign currency account for resident Bangladeshis offers wonderful opportunity to build a deposit base in foreign currency. Helps make for overseas commitments and dues like credit card bills, traveling, expense, recreation tours etc. This service is offered in currencies like USD, GBP and Yen. The interest that NBL offers is very competitive, but the deposit can only be made in foreign currency. The withdrawals can only be made in local currency. It offers fund remittance in LCY and FCY to any place in and out of the country.

3.4.6 Non-Resident Foreign Currency Deposit (NFCD):

National Bank Limited gives opportunity to maintain foreign currency account through its Authorized Dealer Branches. All non-resident Bangladeshi nationals and persons of Bangladesh origin including those having dual nationality and ordinarily residing abroad may maintain interest bearing NFCD Account. NFCD Account can be opened for One month, Three months,

Six months and One Year through US Dollar, Pound Starling, Japanese Yen and Euro. Interest is paid on the balance maintain in the Account. This interest is tax free in Bangladesh

3.4.7 Short Term Deposit (STD):

National Bank Limited offers interest on customer's short term savings and gives facility to withdraw money any time.

Minimum balance Tk. 2000. Standing Instruction Arrangement are available for operating account.

3.5 CLEARING SECTION:

Cheques, Pay Order (P.O), Demand Draft (D.D.) Collection of amount of other banks on behalf of its customer are a basic function of a Clearing Department.

Clearing: Clearing is a system by which a bank can collect customers fund from one bank to another through clearing house.

Clearing House: Clearing House is a place where the representatives of different banks get together to receive and deliver Cheques with another banks. Normally, Bangladesh Bank performs the Clearing House in Dhaka, Chittagong, Rajshahi, Khulna & Bogra. Where there is no branch of Bangladesh Bank, Sonali bank arranges this function.

Member of Clearing House: National Bank Ltd. is a scheduled Bank. According to the Article 37(2) of Bangladesh Bank Order, 1972, the banks, which are the member of the clearinghouse, are called as Scheduled Banks. The scheduled banks clear the cheque drawn upon one another through the clearinghouse.

3.5.1 Types of Clearing:

a) Outward Clearing: When the Branches of a Bank receive cheque from its customers drawn on the other Banks within the local clearing zone for collection through Clearing House, it is Outward Clearing.

b) Inward Clearing: When the Banks receive cheque drawn on them from other Banks in the Clearing House, it is Inward Clearing.

3.5.2 Types of clearing house:

a) Normal clearing house:

1st house: 1st house normally stands at 10 a.m. to 11a.m 2nd house: 2nd house normally stands after 3 p.m. and it is known as return house.

b) Same day clearing house:

1st House: 1st house normally stands at 11 a.m. to 12 pm 2nd House: 2nd house normally stands after 2 p.m. and it is known as return house.

Who will deposit cheque for Clearing: Only the regular customers i.e. who have Savings, Current, STD & Loan Account in the bank can deposit cheque for collection of fund through Clearing house.

Precaution at the time of cheque receiving for Clearing, Collection of LBC, OBC & Transfer:

Name of the account holder same in the cheque & deposit slip. Amount in The cheque & deposit slip must be same in words & in figures. Date in the cheque may be on or before (but not more than six months back)

clearing house date. Bank & Branch name of the cheque, its number & date in the Deposit slip. Cheque must be signed. Signature for confirmation of date, amount in words / in figure Cutting & Mutilation of cheque. Cheque should be crossed (not for bearer cheque). Account number in the deposit slip must be clear. Depositor’s signature in the deposit slip.

3.5.3 Return house:

Return House means 2nd house where the representatives of the Bank meet after 3 p.m. to receive and deliver dishonored cheque, which placed in the 1st Clearing House.

Cheque may be dishonored for any one of the following reasons:

Insufficient fund. Amount in figure and word differs. Cheque out of date/ post dated / mutilated. Payment stopped by the drawer. Payee’s endorsement irregular / illegible / required. Drawer’s signatures differ / required. Crossed cheque to be presented through a bank. Collection Bank's discharge irregular/ required. Effect not clear in the check. Exceed arrangement in check. Clearing stamp required cancellation. Check crossed “Accounts pay only". Other specific reasons not mentioned above.

The dishonor cheque entry in the Return Register & the party is informed about it. Party‘s signature required in the return register to deliver the dishonor cheque. After duration, the return cheque is sent to the party’s mailing address with Return Memo. If the cheque is dishonored due to insufficiency of funds than National Bank charges. 25/=as penalty.

Responsibility of the concerned officer for the Clearing Cheque:

Crossing of the cheque. (Computer) posting of the cheque. Clearing seal & proper endorsement of the cheque. Separation of cheque from deposit slip. Sorting of cheque 1st bank wise and then on branch wise. Computer print 1st branch wise & then bank wise. Preparation of 1st Clearing House computer validation sheet. Examine computer validation sheet with the deposit slip to justify the computer

posting Copy of computer posting in the floppy disk.

3.5.4 Bills Collection:

In modern banking the mechanism has become complex as far as smooth transaction and safety is concerned. Customer does pay and receive bill from their counterpart as a result of transaction. Commercial bank’s duty is to collect bills on behalf of their customer.

3.5.5 Types of Bills for Collection:

a) Outward Bills for Collection (OBC): OBC means Outward Bills for Collection. OBC exists with different branches of different banks outside the local clearing house. Normally two types of OBC:

OBC with different branches of other banks. OBC with different branches of the same bank.

Procedure of OBC:

Entry in the OBC register. Put OBC number in the cheque. “Crossing seal” on the left corner of the cheque & “payees account will be

credited on realization “seal on the back of the cheque with signature of the concerned officer.

Dispatch the OBC cheque with forwarding. Reserve the photocopy of the cheque, carbon copy of the forwarding and deposit

slip of the cheque in the OBC file.

b) Inward bills for collection (IBC): When the banks collect bills as an agent of the collecting branch, the system is known as IBC. In this case the bank will work as an agent of the collection bank. The branch receives a forwarding letter and the bill.

Procedure of IBC:

IBC against OBC: To receive the OBC cheque first we have to give entry in the IBC Register .The IBC number should put on the forwarding of the OBC with date.

Deposit of OBC amount: OBC cheque amount is put into the “sundry deposit-sundry Creditors account”, prepare debit & credit voucher of it. If the OBC cheque is honored, send credit advice (IBCA) with signature & advice number of the concern branch for the OBC amount.

If the OBC cheque is dishonored, the concerned branch is informed about it.

Again place in the clearing house or send the OBC cheque with Return Memo to the issuing branch according to their information.

3.5.6 Inter Branch Credit Advice (IBCA):

IBCA means Inter Branch Credit Advice. It's an advice written by originating branch to the responding branch to the responding branch to credit the general account of responding branch for the transactions mentioned. Every IBCA has two copies. One copy remains in the bank as a office copy another is sent IBCA contains the following information-

Originating branch name with its code number. Responding branch name with its code number. Date of issuing IBCA. Transaction Code. Advice number. Instrument number. Particulars. Amount in wards and in figure. Order to debit general account originating Branch. Responding date.

3.7 ACCOUNTS SECTION:

Accounts Department is called as the nerve Centre of the bank. In banking business, transactions are done every day and these transactions are to be recorded properly and systematically as the banks deal with the depositors’ money. Improper recording of transactions will lead to the mismatch in the debit side and in the credit side. To avoid these mishaps, the bank provides a separate department; whose function is to check the mistakes in passing vouchers or wrong entries or fraud or forgery. This department is called as Accounts Department. If any discrepancy arises regarding any transaction this department report to the concerned department. Besides these, the branch has to prepare some internal statements as well as some statutory statements, which are to be submitted to the Central Bank and the Head Office. This department prepares all these statements.

Workings of this department:

Recording the transactions in the cash book.

Recording the transactions in general and subsidiary ledger. Preparing the daily position of the branch comprising of deposit and cash. Preparing the daily Statement of Affairs showing all the assets and liability of the branch

as per General Ledger and Subsidiary Ledger separately. Making payment of all the expenses of the branch. Recording inters branch fund transfer and providing accounting treatment in this regard. Preparing the monthly salary statements for the employees. Preparing the weekly position for the branch which is sent to the Head Office to maintain

Cash Reserve Requirement (C.R.R). Preparing the monthly position for the branch which is sent to the Head Office to

maintain Statutory Liquidity Requirement (S.L.R). Make charges for different types of duties. Checking of Transaction List. Statement of Affairs. Preparing the budget for the branch by fixing the target regarding profit and deposit so as

to take necessary steps to generate and mobilize deposit. Recording of the vouchers in the Voucher Register. Packing of the correct vouchers according to the debit voucher and the credit voucher.

3.8 Card Products of NBL:

Card Products:

National Bank Limited has not only initiated a new scheme but also brought a new life style concept in Bangladesh. Now the dangers and the worries of carrying cash money are memories of the past. NBL serves Card products to their valuable customers. NBL was the first among domestic banks to introduce Master Card in Bangladesh. In the meantime, NBL has also introduced the Visa Card and Power Card. The Bank has in its use the latest information technology services of SWIFT and REUTERS.

Credit Card:

NBL Credit Card is accepted in many merchant outlets around the country. Credit Card comes in both local and international forms, giving the client power to buy all over the World. Our wide range of merchants include hotels, restaurants, airlines, & travel agents, shopping malls and departmental stores, hospitals & diagnostic centers, jewelers, electronics & computer shops and many more.

Power Card:

NBL Power Card is the first debit card for which you don’t have to maintain any account with our any branch. Now enjoy the conveniences and advantages of Credit Card as you step into the new millennium.

It is a Pre-paid Card. Annual / Renewal Fee Tk. 200/- only. May be issued and refilled from RFCD/FC Account. Accepted at all VISA POS merchants.

Cash withdrawal at all ATM booths bearing VISA and Q-cash logo (Except HSBC in Bangladesh).

Drawing of Cash: (i) from NBL ATMs - Free of charges (ii) From ATMs under Q-cash network- Tk.10.00 per transaction (iii) From other ATM - Tk. 100.00 per transaction.

Cash Withdrawal Fee (aboard)-2.00% on the cash drawn amount or US$2.00, whichever is higher.

Only 1% loading fee against both International and Local Power Card at the time of Refilling.

Yearly Tk.100 for enrollment of SMS service.

3.8 Western Union:

Joining with the world's largest money transfer service "Western Union", NBL has introduced Bangladesh to the faster track of money remittance. NBL was first domestic bank to establish agency arrangement with the world famous Western Union in order to facilitate quick and safe remittance of the valuable foreign exchanges earned by the expatriate Bangladeshi nationals. Now money transfer between Bangladesh and any other part of the globe is safer and faster than ever before. It has a full time arrangement for speedy transfer of money all over the world. This simple transfer system, being on line eliminates the complex process and makes it easy and convenient for both the sender and the receiver. Through NBL - Western Union Money Transfer Service, your money will reach its destination within a few minutes.

National Bank Limited signed an agreement with the Western Union Financial Services, USA (or, Western Union in short) in 1993 and became its first agent in Bangladesh. Millions of people from different corners of the world have been sending their money to their near and dear ones with utmost confidence through the Western Union. Western Union has the most modern technology for remitting money within quickest possible time from any part of the world through its more than 2,45,000 representatives in 200 countries and regions spread all over the world. Western Union earns more than 3.5 billion US dollars as revenue every year. With the help of the hi-tech on-line computer system of Western Union, remittances made by Bangladeshis from different countries of the world reaches NBL within minutes, which are urgently delivered to the recipients through its 121 branches spread all over the country.

3.9 ATM Service:

National Bank Limited has introduced ATM service to its Customers. The card will enable to save our valued customers from any kind of predicament in emergency situation and time consuming formalities. NBL ATM Card will give our distinguished Clients the opportunity to withdraw cash at any time, even in holidays, 24 hours a day and 7 days a week.

The next chapter discusses the Loans & Advances of National Bank Limited.

CHAPTER: 4LOANS AND ADVANCES

4.0 Loan & Advances:

This is the survival unit of the bank because until and unless the success of this department is attained, the survival is a question to every bank. If this section does not properly work the bank itself may become bankrupt. This is important because this is the earning unit of the bank. Banks are accepting deposits from the depositors on condition of providing profit to them as well as safe keeping their deposit. Now the question may gradually arise how the bank will provide profit to the clients and the simple answer is – Investments & Advance.

4.1 Reason for which Bank provides Investment to the Borrowers:

To earn profit from the borrowers and give the depositors profit. To accelerate economic development by providing different industrial as well as

agricultural Investment. To create employment by providing industrial Investments. To pay the employees as well as meeting the profit groups.

Credit is continuous process. Recovery of one credit gives rise to another credit. In this process of revolving of funds, bank earns income in the form of profit. A bank can invest its fund in many ways. Bank makes Investment to traders, businessmen, and industrialists. Moreover nature of investment may differ in terms of security requirement, disbursement provision, terms and conditions etc.

4.2 Lending principles:

The Principle of lending is a collection of certain accepted time tested criteria, National Bank which ensures the proper use of Investment fund in a profitable way and its timely recovery. Different authors describe different principles for sound lending.

1. Safety2. Security3. Liquidity4. Adequate yield5. Diversity

1. Safety: Safety should get the prior importance in the time of sanctioning the Investment. At the time of maturity the borrower may not will or may unable to pay the Investment amount. Therefore, in the time of sanctioning the Investment adequate securities should be taken from the borrowers to recover the Investment. Banker should not sacrifice safety for profitability. National Bank Ltd. exercises the lending function only when it is safe and that the risk factor is adequately mitigated and covered. Safety depends upon:

The security offered by the borrower; and The repaying capacity and willingness of the debtor to repay the Investment with profit.

2. Security: Banker should be careful in the selection of security to maintain the safety of the Investment. Banker should properly evaluate the proper value of the security. If the estimated value is less than or equal to Investment amount, the Investment should be given against such

securities. The more the cash near item the good the security. In the time of valuing the security, the Banker should be more conservative.

3. Liquidity: Banker should consider the liquidity of the Investment in time of sanctioning it. Liquidity is necessary to meet the consumer need.

4. Adequate Yield: As a commercial origination, Banker should consider the profitability. So banker should consider the profit rate when go for lending. Always Banker should fix such an profit rate for its lending which should be higher than its savings deposits profit rate. To ensure this profitability Banker should consider the prospect of the project.

5. Diversity: Banker should minimize the portfolio risk by putting its fund in the different fields. If Bank put its entire Invest able fund in one sector it will increase the risk. Banker should distribute its Investment able fund in different sectors. So if it faces any problem in any sector it can be covered by the profit of another sector.

4.3 Reason for investment defaults:

There are many reasons for Investment default. The principal reasons are:

Sick management: Integrity Cooperation Financial/Marketing knowledge Technical

knowledge/Experience. Endurance and Judgment

Sick Finance: Working capital Repayment period Flexible rate of profit Assets matching to liabilities Collateral’s Capital market

Sick Product: Quality Competitiveness Demand Durability

Sick Operation: Efficient machinery’s Skilled labor/supervision Good labor relation Utilities of raw materials

Sick Market: Freedom Openness Growth Stability

Other Reasons: Reputation Analysis of balance sheet Lending risk analysis

4.4 4.4 Process of Investment:

Heads CharacteristicsApplication Applicant applies for the Investment in the prescribed form of the

bank describing the types and purpose of Investment.

Sanction 1. Collecting credit information about the applicant to determine the credit worthiness of the borrower. Sources of information

2. Personal Investigation, Confidential Report from other bank, Head Office/Branch/Chamber of Commerce.

3. CIB (Central Information Bureau) report from Central Bank.i. Evaluation of compliance with its lending policy.

ii. Evaluating the proposed security.4. LRA is must for the Investment exceeding one crore – as ordered

by Bangladesh Bank.5. If everything is in accordance the Investment is sanctioned

Documentation Then bank prepare an Investment proposal which contains terms and conditions of Investment for approval of H.O. or Manager.

Takes the necessary papers and signatures from borrower

Disbursement Investment Account is opened. Where customer A/C -------Dr. Respective Investment A/C ----------------------------------------------Cr.

4.5 Services offered by investment department:

The different types of Investments and Investment that National Bank offers are as follows:

1. Secured Overdraft (SOD)2. Investment against Imported Merchandise (LIM)3. Investment against Trust Receipt (LTR)4. Payment Against Document (PAD)5. House Building Investment 6. House Building Investment (staff)7. Term Investment.8. Investment (general)9. Bank Guarantee10. Export Cash Credit11. Cash Credit (Pledge)12. Cash Credit (Hypo)13. Foreign Documentary Bill Purchase (FDBP)14. Local Documentary Bill Purchase (LDBP)

4.5.1 Secured Overdraft (SOD):

It is a continue advance facility. By this agreement, the banker allows his customer to overdraft his current account up to his credit limits sanctioned by the bank. The profit is charged on the amount, which he withdraws, not on the sanctioned amount. National Bank sanctions SOD against different security.

SOD (general): Advance allowed to individual/ firms against financial obligation (i.e. lien on FDR/PSP/BSP/ insurance policy share etc.) This may or may not be a continuous Credit.

SOD (others): Investment allowed against assignment of work order or execution of contractual works falls under this head. This advance is generally allowed for a definite

period and specific purpose i.e. it is not a continuous credit. It falls under the category "others".

SOD (Export): Advance allowed for purchasing foreign currency for payment against L/Cs (Back to Back) where the exports do not materialize before the import payment. This is also an advance for temporary period, which is known as export finance and under the category “commercial lending".

4.5.2 Investment against Imported Merchandise (LIM):

Investment allowed for retirement of shipping documents and release of goods imported through L/C taking effective control over the goods by pledge in go downs under Banks lock & key fall under this type of advance. This is also a temporary advance connected with import, which is known as post-import financing, falls under the category “commercial lending".

4.5.3 Investment against Trust Receipt (LTR):

Advance allowed for retirement of shipping documents, release of goods imported through L/C falls under trust with the arrangement that sale proceed should be deposited to liquidate within a given period. This is also a temporary advance connected with import, which is known as post-import financing, falls under the category “commercial lending".

4.5.4 Payment Against Document (PAD):

Payment made by the Bank against lodgment of shipping documents of goods imported through L/C falls under this head. It is an interim advance connected with import and is generally liquidated against payments usually made by the party for retirement of the documents for release of imported goods from the customer’s authority. It falls under the category “commercial Bank".

4.5.5 House building Investment (General):