financial outlook for u.s. not-for-profit healthcare sector drew corrigan may 5, 2011

TRANSCRIPT

Financial Outlook for U.S. Not-for-Profit Healthcare Sector

Drew Corrigan

May 5, 2011

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 20637SEA

2

Generally, rating agencies continue to have a negative outlook for the U.S. Not-for-Profit Healthcare sector.

Slow economic recovery

Ongoing revenue pressures

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 20637SEA

3

U.S. Quarterly Unemployment Rate

Dec

200

8

Mar

200

9

Jun

2009

Sep

200

9

Dec

200

9

Mar

201

0

Jun

2010

Sep

201

0

Dec

201

0

Mar

201

1

6.9

8.6

9.59.8 10

9.7 9.5 9.6 9.48.8

% U

nem

plo

yed

Source: United Status Bureau of Labor Statistics

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 20637SEA

4

Slow Economic Growth Adds Pressure to Volume and Payer Mix Measures

Patients defer elective healthcare services

Rising charity care and bad debt expense

Budget pressures at federal and state levels impacting Medicare and Medicaid reimbursement rates

Unfavorable changes in payer mix away from commercial payers

Increased reimbursement pressures across all payers

Financial pressures and decreasing membership at health insurers

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 20637SEA

5

Declining Medicare Reimbursement Rates

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2.0

0.0

0.5

1.0

3.5

2.75

3.0

3.53.35

3.73.5

3.3

3.6

2.0

0.0

Payment increase

% I

ncr

ease

Source: Centers for Medicare and Medicaid Services

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 20637SEA

6

Hospital Revenues Threatened with Rate Reductions

Medicare payment rates declined for first time since 1998

Major hospital revenue sources under pressure

Medicaid rates at risk due to state budget deficits and expiring stimulus funds

Revenue Source % Revenue Factors

Medicare 43% RAC reviews, medical necessity, Medicare trust solvency

Medicaid 12% State budget gaps, expiring stimulus

Private insurance 43% Industry consolidation, membership losses

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 20637SEA

7

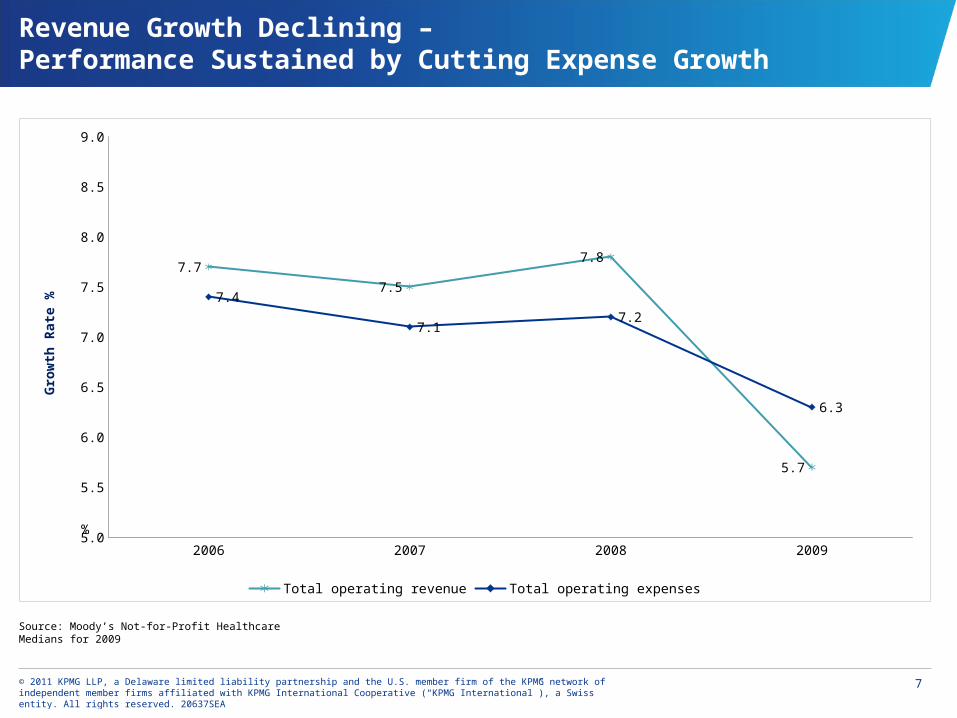

Revenue Growth Declining – Performance Sustained by Cutting Expense Growth

2006 2007 2008 20095.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

7.7

7.5

7.8

5.7

7.4

7.17.2

6.3

Total operating revenue Total operating expenses

Gro

wth

Rat

e %

Source: Moody’s Not-for-Profit Healthcare Medians for 2009

%

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 20637SEA

8

Expense Management will Likely Become More Difficult

Many systems have already done much to contain cost in areas of wages and supply chain

Other areas of anticipated increased expense:

– Pension expense due to declining interest rates

– Interest expense reflecting higher cost from shift to fixed rate bonds

– Bad debt expense

– Physician related costs due to increased alignment strategies

– IT expense of new systems to satisfy “meaningful use” requirements

– Strategic expense related to considerations of Accountable Care Organizations

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 20637SEA

9

LOC Expirations/Renewals

04 05 06 07 08 09 10 11 12 13 14 15

1,130

1,8421,520

1,1411,779 1,951

4,372

14,419

7,110

5,695

827253

($ in millions)

Source: Citigroup

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 20637SEA

10

Balance Sheets Retain a Number of Heightened Risks

Bank LOC renewal risk

Pension obligations

Exposure to non-cancelable operating leases

Negative valuation of swap portfolios

Increased capital spending funded with cash reserves

Changing views on “quality” of days cash metrics

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 20637SEA

11

Many Uncertainties Remain Regarding Healthcare Reform

Risks surrounding the legislation itself (additional management distraction or possible missed opportunities)

Legal challenges to the legislation and constitutionality

Many questions remain:

– How will it be implemented?

– How will compliance be defined?

– How should organizations proceed?

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 20637SEA

12

Positive Factors for the Not-for-Profit Healthcare Sector

Strong management teams respond well to challenges

Strong liquidity and stable investment returns

Provider fees in many states create short-term relief from Medicaid pressures

Generally stronger balance sheets emerging even in challenging environment

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 20637SEA

13

Factors Contributing to Greater Consolidation Within Healthcare

Increased need for capital relating to plant modernization and IT systems

Greater limitations on access to capital due to wider credit spreads and more expensive bank liquidity

Cost of compliance with Medicare audits and new requirements under health care reform

Increased reimbursement pressures across all payers

Large unfunded pension liabilities

Possibility that benefits of tax-exemption will further diminish

Benefits of economies of scale, including increased bargaining power with suppliers, payers, and labor