financial notes by jmr sir

TRANSCRIPT

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 1/70

1

PROJECTS/CREDIT MANUAL

1. What is HUF?

HUF stands for Hindu Undivided Family. The members of HUF are

Husband, Wife, Father, Mother, sons, daughters, Un-Married

brothers & un-Married sisters.

2. Who is a first generation Entrepreneurs?

The First Generation Entrepreneur is one who is establishing the

enterprise for the first time (No experience).

3. Who is Good Entrepreneur?

Existing customer satisfying the criteria.

4. Who is SSE?

Customers associated with other Banks / Institutions satisfying the

Criteria.

5. What is a medium term loan?

Medium term loan is given / extended for acquiring fixed assets oradditional working capital requirements and repayable over a

period of 3 to 5 years.

6. What is the risk capital fund?

Financial assistance extended to supplement promoter margin –

repayment period 5 years.

7. What is Primary Security?

All existing assets and assets proposed in the scheme which are

proposed to be mortgaged / Hypothecated.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 2/70

2

8. Who are New Customers?

Other than existing

9. Collateral Security?

Other than the Primary Security offered by the Party

10. What is lending Policy?

Lending Policy indicates the activities that are to be encouraged and

not encouraged.

11. What is the procedure for the activity not covered by either

encouraged / not to be encouraged?

Have to refer to Head Office for approval.

12. Delegation of powers, for approving lines not listed in encouraging not

is encouraging category?

- Rs 5 to 50 lakhs HOD (Development)

- Rs 50 to 100 lakhs HOPSC (Development)

- More the Rs 100 lakhs Project Department

13. What is the minimum Collateral Security for term loans to units under

encouraged category?

Minimum 50% or as per the Lending policy which ever is

higher.

14. What is the procedure for refund of Service Charges?

A.No refund if the loan is sanctioned.

B.Entire amount could be refunded if:

I.Application is withdrawn by the party before putting up to PSC.

Ii.Rejected by PSC/Sanctioning authority

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 3/70

3

iii. Approved by PSC but application with drawn by the party before

sanction of loan.

15. What is the Service Charge?

A mount collected from the party for processing of loan application.

16. When will the service charges can be refunded even if the loan is

sanctioned?

Yes. If loan is considered with higher Collateral Security, higher rate

of interest, reduction in loan amount if the party request by

withholding 30% (MDs Power)

17. What is project information Sheet (PIS)

PIS is a primary report forwarded by the branch about product,

promoter, market, cost and its recommendations

18. What is CRC?

CRC stands of Credit Recommending Committee headed by ED, with

all CGM’s as members.

19. What type of proposals are put up to CRC.

Proposals under MSME, MTL, MAS, RCFS

20. What is the lead time for processing of loan applications?

PSC - 7 days

OZSSC - 15 days

HOSC - 30 days

EC/Board - 60 days

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 4/70

4

21. What is appraisal?[Page No.55]

Appraisal is a comprehensive and systematic review of all aspects of the

project.

22. Who appraises the Project?

A team consisting of Technical and Financial Officers (T-Technical

feasibility and F- Financial Viability]

23. What is Technical Feasibility?

Whether machines are suitable, performance guaranteed etc.,.

24. Financial Viability

Whether project can generate enough to service the loan (DSCR)

25. What does the project appraisal consist of? [Page No-56]

The detailed project appraisal consists of following:

- Promoters Appraisal

- Technical Appraisal

- Financial Appraisal

- Market Appraisal- Risk Analysis

26. What is Technical Appraisal?

Technical appraisal (evaluation) involves critical examination of

manufacturing process, technology, capacities and revenues.

27. What is financial appraisal [Page No.61]

Financial appraisal tells us whether the project can generate enough

revenue to service the loan and profitable.

28. Whether the Corporation used to Register machinery suppliers?

Earlier Yes.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 5/70

5

29. What is the procedure Regarding imported used machinery?[Page

No.71]

Corporation insists on a chartered engineer’s certificate from place of origin

indicating the make, model year of manufacturing, residual life, condition

and price.

30. What is the loan eligibility for used imported machinery from

indigenous sources?

50%

31. What is the procedure for 2nd

hand indigenous machinery?

The second hand indigenous machinery can be considered with the

prior approval of:

i. For BSC / OZ SSC cases – HO PSC

ii. Ho Cases – HOSC / EC / Board

32. When does the Corporation retain amount for performance

verification [Page No.72]

Or

What is general procedure for retention of performance verification?

Why Corporation retains some amount for performance verification?

Where Corporation is not certain or doesn’t know about the performance

of machinery being supplied to its parties, Corporation retains some

amount for performance verification. This is being done to protect the

parties’ interest.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 6/70

6

PROJECT

1. What Is the loan eligibility for a building older than 5 years?

Only on the cost of land

2. What is extent of CS for the units set up in lease hold premises?

Minimum 50%

3. Whether Corporation insists on Collateral Security on Land and

Buildings for the units coming up in APIIC/ALEAP , Industrial Estates etc.

No.

4. What is minimum Promoter Contribution for SSI and other units

i. 22.5% for SSI &

ii. 25% for others

5. What are the DER Norms

Maximum 3:1 for projects up to Rs 10 lakhs and others 2:1

6. What is Economics of Working?

Economics of Working means estimation of Revenue & Expenditurebased on proposed capacity etc.

7. Name the intangible asset in the project cost?

Preliminary and Pre-operative expenses

8. What is Working Capital Margin?

The difference between the requirement and the amount provided

by Commercial Banks

9. Who has to bring the Working capital margin?

Promoter himself

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 7/70

7

10. How the finance required for setting up an industry is raised?

a. Long term finance for fixed assets

b. Short term finance for meeting Working Capital

11. What is meant by internal accruals?

The amount generated in the form of profits.

12. What is Cash Flow Statement?

The cash flow statement reveals movement of cash, peak borrowing

levels, surplus / deficit in requirement of cash from the existing

arrangements.

13. What are financial ratios?

Financial ratios facilitate meaningful analysis of financial situation

and performance.

14. Name the financial ratios and what do they reveal?

Financial ratios provide an idea on the financial heaith and operating

performance of a company.

They are as under:

1. DER

2. Current Ratio

3. DSCR

4. ROI

5. Turnover Rations

6. Total outstanding liabilities / Total net worth

7. Gearing Ratios

15. What is DER?

DER is ratio between long term debts to share holder’s funds

(equity). Maximum DER should be 2:1 meaning long term loans can

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 8/70

8

be twice the equity. DER indicates the capacity up to which company

will be able to borrow funds.

16. What is Debt?

Debt includes all long term loans including unsecured loan (interest

bearing).

17. What is Equity?

Equity consists of share holders funds i.e.,

a. Share Capital

b. Reserves and Surplus

c. Profit & Loss Account Credit balance

d. Unsecured loans (interest free)

e. Special / Seed Capital

18. What is Current Ratio?

Current ratio is ratio of Current Assets to Current liabilities and

should be 2:1 i.e. current assets should be twice the current liabilities

19. What is Current Asset?

Asset which can be converted into cash in shorter period of time

20. What is current liability?

All sums payable within 1 year.

21. What is net profit (page 95)

Net profit means profit after interest, taxes and preference

dividend.

22. What should be the ROI for the projects?

It should be minimum of Corporation Lending Rate.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 9/70

9

23. List a few profitability ratios?

a. Gross profit to sales

b. Net profit to salesc. Operating profit to sales

d. Material, conversion cost, administrative expenses,

selling expenses to sales

24. What is turnover ratio?

Turnover (also known as performance or activity ration) measures

how well the facilities at the disposal of unit are used.

25. What is financial Leverage Ratio?

The financial leverage is defined as “the tendency of residual net

income to vary disproportionately with net income.

26. Name two gearing Ratios

a. Financial leverage Ratio

b. Operating leverage Ratio

27. What is operation leverage?

The operation leverage is defined as “the tendency of net income to

vary disproportionately with sales.

28. What is Break Even Point

Break Even Point is the level of output where there is no profit or

loss

29. How the BEP is measured?

BEP measures the minimum required level of operation to sustain

continuity.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 10/70

10

30. What are fixed costs?

Fixed costs are those related to the company’s fixed assets which are

not amenable to change in a short or medium term.

31. What is Semi fixed cost?

Semi fixed costs are those which vary with the volume of sales but not in

the same proportion.

32. What are the variable costs?

Variable costs are those which vary with the volume of sales.

33. What is marginal costing?

Marginal costing or Direct Costing is the technique which measures

variable cost per unit of output.

34. What is IRR?

Internal Rate of Return[IRR] is that rate which makes present value of

earnings equal to investment or brings the Net Present Value to Zero.

35. What is Sensitivity Analysis?

Finding out impact of decrease in Revenue and increase in the cost

of raw material on cash flows.

36. What is the loan period for Term Loan & Medium term loan

Term loan - 8 years, Medium term loan – 5 years

37. How the loan period is fixed?

The loan period is fixed covering the period of operation for which

cash flows are worked out in computing DSCR plus the project

implementation period.

38. Whether the loan period includes moratorium period?

Yes.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 11/70

11

39. What is CIBIL?

Credit Information Bureau of India Limited.CIBIL is a premier service

organization providing information on the credit reports of various

entities – commercial and individual throughout the country.

40. What are the Risk Parameters with which a project is assessed and

evaluated?

The project is assessed/ evaluated for the following risk parameters:

a. Financial credit risk parameters

b. Business Risk parameters

c. Industry risk parameters

d. Management risk parameterse. Risk mitigation parameters.

41. Whether the Corporation is Rating all the loan proposals?

Only for loans above Rs.30 lakhs.

42. What is Multiple Banking?

Multiple Banking is a banking arrangement where the borrower

avails finance independently from more than one bank, withouthaving a common arrangement and understanding between them.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 12/70

12

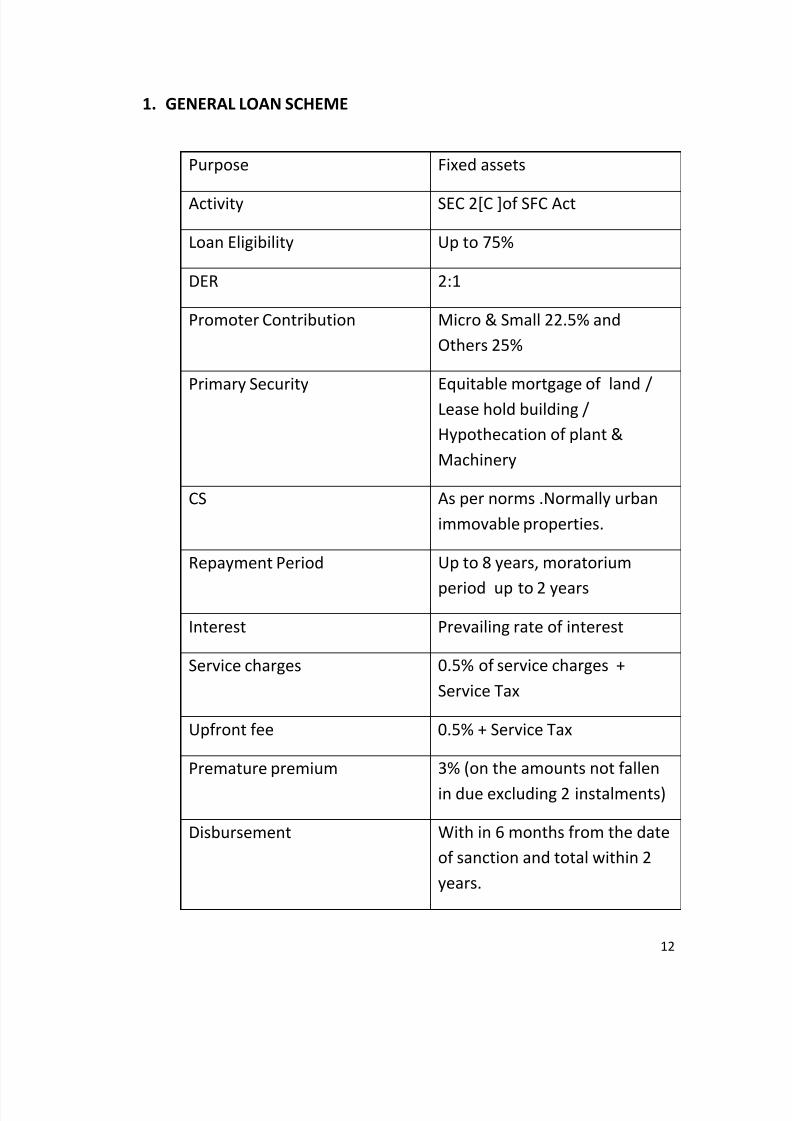

1. GENERAL LOAN SCHEME

Purpose Fixed assets

Activity SEC 2[C ]of SFC Act

Loan Eligibility Up to 75%

DER 2:1

Promoter Contribution Micro & Small 22.5% and

Others 25%

Primary Security Equitable mortgage of land /

Lease hold building /

Hypothecation of plant &

Machinery

CS As per norms .Normally urban

immovable properties.

Repayment Period Up to 8 years, moratorium

period up to 2 years

Interest Prevailing rate of interest

Service charges 0.5% of service charges +

Service Tax

Upfront fee 0.5% + Service Tax

Premature premium 3% (on the amounts not fallen

in due excluding 2 instalments)

Disbursement With in 6 months from the date

of sanction and total within 2

years.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 13/70

13

2. MARKETING ASSISTANCE SCHEME (MAS)

Purpose Various marketing activities like

show rooms, exhibition s,

Jewelry merchants, Super Bazars

etc.

Activity SEC 2[C] of SFC Act

Objective Activities to increase sales turn

over

Loan Eligibility a. 65% cost + Core Working

Capital Term loan subject

to a minimum of Rs.10

lakhs to Super Bazars

b. 65% minimum WCTL

Rs.20 lakhs

DER 2:1

Promoter Contribution 35%

Primary Security Equitable mortgage of land /

Lease hold building /

Hypothecation of plant &

Mechinery

CS Land & Building, civil works 25%loan component

Racks, Storage bins & furniture

100%

a. 100% General Market

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 14/70

14

loan

b. 150% Super Bazars

c. WCTL – 150%

d. Computer hardware 125%

to 150%Repayment Period Upto 3 to 5 years, moratorium

period upto 1 year

Interest Prevailing rate of interest

Service charges 0.5% of service charges +

Service Tax

Upront fee 0.5% + Service Tax

Premature premium 3% (on the amounts not fall in

due excludes 2 instalments)

Disbursement With in 6 months from the date

of sanction and total within 2

years

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 15/70

15

TRANSPORT LOAN:

Purpose vehicles

Activity SEC 2[C ]of SFC Act

Objective Activities to increase sales turn

over

Loan Eligibility Up to 75

c.

DER 2:1

Promoter Contribution 25%

Primary Security Hypothecation of vehicle

CS As per norms. urban immovable

properties.

Repayment Period Upto 4, moratorium period of 3

months.Monthly rests.

Interest Prevaling rate of interest

Service charges 0.5% of service charges +

Service Tax

Upront fee 0.5% + Service Tax

Premature premium 3% (on the amounts not fall in

due excludes 2 instalments)

Disbursement With in 3 months from the date

of sanction

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 16/70

16

DISBURSEMENT

1. Who are the authority for approving change of Machinery Suppliers

and change in machinery specifications?

In Respect of all lines of activities

a. Up to Rs.1.00 crore loan sanctioned - Branch Manager

b. Above Rs.1.00 and up to Rs.2.00 Crore - HOD(OpD)

c. Above Rs.2.00 crore - HOD (Projects)

2. What is diversification of savings?

When there are unspent amounts either in machinery account or civil

party requests the Corporation for utilizing the same for other

purpose.

3. Who is authority to approve diversification of savings from one head

to another?

a. Branch Sanctions

i. Up to 10% of loan sanctioned - Branch Manager

ii. Above 10% of loan sanctioned – HOD (OPD)b. OZSSC Sanction

i. Up to 10% of loan sanctioned - HOD (OPD)

ii. Above 10% of loan sanctioned – ED

c. All other sanctions - ED

4. Whether diversification of savings is allowed twice?

No. Only once for a term loan

5. Whether diversification of savings is considered for release towards

Preliminary and Pre-operative expenses?

No.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 17/70

17

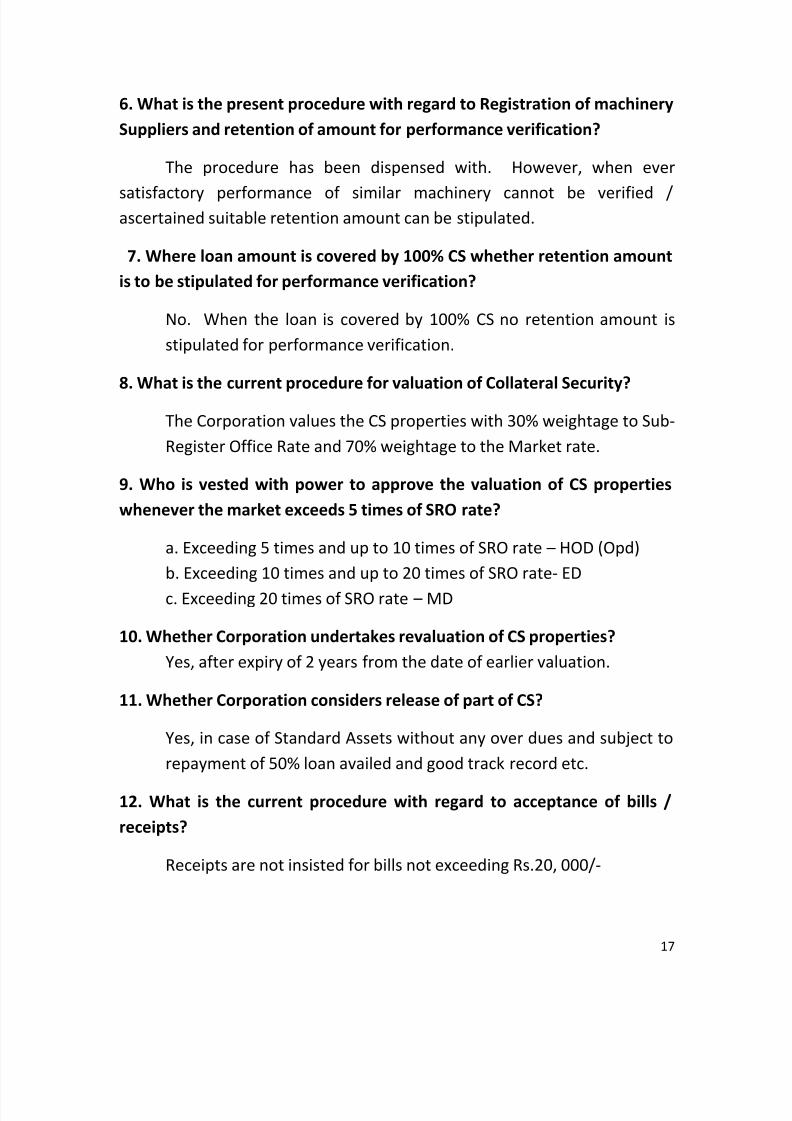

6. What is the present procedure with regard to Registration of machinery

Suppliers and retention of amount for performance verification?

The procedure has been dispensed with. However, when ever

satisfactory performance of similar machinery cannot be verified /ascertained suitable retention amount can be stipulated.

7. Where loan amount is covered by 100% CS whether retention amount

is to be stipulated for performance verification?

No. When the loan is covered by 100% CS no retention amount is

stipulated for performance verification.

8. What is the current procedure for valuation of Collateral Security?

The Corporation values the CS properties with 30% weightage to Sub-

Register Office Rate and 70% weightage to the Market rate.

9. Who is vested with power to approve the valuation of CS properties

whenever the market exceeds 5 times of SRO rate?

a. Exceeding 5 times and up to 10 times of SRO rate – HOD (Opd)

b. Exceeding 10 times and up to 20 times of SRO rate- ED

c. Exceeding 20 times of SRO rate – MD

10. Whether Corporation undertakes revaluation of CS properties?

Yes, after expiry of 2 years from the date of earlier valuation.

11. Whether Corporation considers release of part of CS?

Yes, in case of Standard Assets without any over dues and subject to

repayment of 50% loan availed and good track record etc.

12. What is the current procedure with regard to acceptance of bills /

receipts?

Receipts are not insisted for bills not exceeding Rs.20, 000/-

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 18/70

18

13. Whether Corporation insists on CA Certificate with regard to raising

of initial capital?

CA Certificate need not be insisted if the initial capital up to Rs.40.00

lakhs (Earlier 25 lakhs).

14. Whether Corporation insists on Key man insurance policy for

Practicing Doctors.

No.

15. What is the Delegation Of Authority for relaxation of up to 10% of CS

value in case of term loans?

Branch Sanction Powers - SBM/BM

Above BSC and up to OZSSC - DGM/AGM (O)

For All HO Sanctions - HOD (O)

16. What is the Delegation Of Authority for relaxation of above 10% of CS

value in case of term loans?

Board

17. What is the Delegation of Power for approving changes from Urban torural and Agricultural properties?

Branch Sanction Powers - SBM/BM

Above BSC and up to 50.00 LAKHS - DGM/AGM (O)

For Above Rs.50.00 Sanctions - HOD (O)

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 19/70

19

LEGAL

1. What was the stamp duty for Memo of Deposit of Title Deeds?

0.5% of the amount secured subject to maximum of Rs.50, 000/-

2. For Hypothecation deeds and pledge deeds?

0.5% Maximum Rs.2.00 lakhs

3. What is the present Stamp duty for SSI units?

a. Memorandum of Deposit of Title Deeds

0.5% of secured Amount. Maximum Rs.1, 000/-

b. For Hypothecation

0.5% of secured Amount. Maximum Rs.1, 000/-

4. What is the present stamp duty for others (Non-SSI Units)

Memorandum of Deposit of title deed 0.5% of the amount secured

subject to maximum of Rs.50, 000/-

For Hypothecation deeds and pledge deeds 0.5% Maximum Rs.2.00lakhs

5. When did the SARFAESI Act come into effect?

W.E.F. 21.06.2002

6. What is the purpose / objective /goal of SARFESI Act

For enabling Banks and Financial Institutions to recover amounts due

in NPA cases.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 20/70

20

7.What are the cases where Corporation can take action under SARFAESI

Act?

In the following cases Corporation can take action under SARFAESI

Act

a. When the account of the unit is declared as NPA

b. Where the account of the financial asset is more than Rs.1.00

lakh

c. When the amount due is more than 20% of the principal

amount and interest thereon.

8. Whether provisions of SARFESI Act can be enforced against Agricultural

lands?

NO

9. What is the procedure under SARFESI Act for recovering the dues?

1. 60 days notice

2. Pachnama of movable properties and deliveringpossession notice

3. Sale for giving paper advertisement (2 new papers)

10. Whether action under SARFESI and SFC’s Act can be taken

simultaneously?

No. If action under SARFESI Act is contemplated, the action pending

under SFC’s Act and other provision of law shall be withdrawn.

11. Whether aggrieved party can approach local court and High court for

the action imitated under SAFESI Act?

They can challenge the action only in the Debt Recovery Tribunal.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 21/70

21

12. What is the time limit for disposal of cases at DRT?

60 days.

13. Who are the authorized Officers for imitating recovery action under

SARFAESI Act 2002?

Branch Managers including Senior Manager, Assistant General

Manager and Deputy General Manager whoever is in charge of the

Branch Office at the branch level and General Manager

(MRD)/DGM(AMC) at Head Office.

14. What are the delegations for Power for initiatating recovery action

under SARFAESI Act 2002?

- Up to Disbursement of Rs 20 lakhs - BMS

- Over Rs 20 lakhs - AGM/DGM/(AMC)

/GM(MRD)

15. Who has the Power to take action SARFAESI Act against cases pending

under before BIFR?

AGM/DGM (AMC)/GM(MRD) (Power Delegated)

16. Whose approval is required for imitating or with drawing action under

SARFAESI Act 2002?

MD, (But as per the delegated powers where disbursement amount

is up to Rs.20 lakhs Branch Manager can initiate action, and for with

drawl OPD approval is required. If Disbursed amount is more than

Rs.20 lakhs GM(MRD), DGM/AGM(AMC). For cases pending before

BIFR (for Branch or HO cases) MD approval is required.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 22/70

22

17. What is the significance of case involving KSFC VS V. Narasimhaiah and

others?

Earlier SFC’s were taking action U/S.29 of SFC’s Act for recovering the

dues by proceeding against the primary asset and collateral security.However in this case the Hon’ble Supreme Court of India held that

SFC’s can proceed U/s 29 against assets of Industrial concern only

and not against the collateral security.

18. Whether action against agricultural properties can be taken under

SARFAESI Act ?

No. As per Section 31(1) of SARFAESI Act recovery action against

agricultural properties cannot be taken.

19. What is the other remedy available to the Corporation when action

against agricultural properties cannot be taken under SARFAESI Act?

Corporation can initiate action

- Under Section 31(1) (aa) of SFC’s act by filling an OP before the

District Judge.

b. By bringing the assets mortgaged for sale through court

c. Under Sec.32 (G) of SFC’s Act.

20. What is the problem with action under 31(1) (aa) of SFC’s Act

The process is very lengthy and time consuming /taking.

21. What is the Speediest remedy available for proceeding against

agricultural lands offered as Collateral Security?

By Proceeding under 32(G) of SFC’s Act.

22. What is so special about 32(G) of SFC’s Act

Under 32(G) of SFC’s Act Corporation can recover the amounts due

as arrears of land revenue.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 23/70

23

23. What was the position before the Honorable Supreme Court’s

judgment in Unique Butyl Limited?

Corporation was proceeding under Sec.52 (a) of APRR Act (under

which dues are treated as arrears of land revenue) for recovering the

dues in case of loss assets. However the Hon’ble Supreme Court of

India in the case of Unique Butyl Limited Vs. Haryana Financial

Corporation held that Corporation’s have to take action under 32(G)

SFC’s act only.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 24/70

24

MRD

1. When did the Revised Loan Recovery Policy guidelines (RLRP) / OTS

Guidelines approved?

At the Board Meeting held on 10.01.2013

2. When did the RLRP/OTS guidelines came into force?

w.e.f. 31.01.2013

3. What is the Objective of RLRP?

To maximize recovery of dues from NPAs

4. What is NPA?

Non-performing Asset. The asset not yielding any revenue in the

form of interest and principal repayment.

5. What is the date for deciding OTS Eligibility

31,03,2010 (Earlier 31.03.2004)

6. What type of Units are eligible for OTS?

Doubtful and loss assets

7. When did the Corporation formulate / implemented the Loan recovery

policy? (RLRP)

In the FY 2008-09

8. Whether LRP is a statutory policy?

No. It is a non-statutory policy and implemented by the Corporation

on voluntary basis.

9. Basic objective of LRP?

a. To maximize recovery of dues

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 25/70

25

b. Reducing the net NPAs to the minimum level

10. Aim / Objective of LRP?

To prevent loan accounts from becoming NPAs

11. Applicability of LRP

It applies to all the assisted units of corporation

12. What are the guiding principles of the LRP?

a. Dignity and respect of customers, Customer satisfaction

b. Fair treatment, preventing an account from becoming NPA

c. Delivering Demand notices

d. Giving reasonable time

13. Who looks after recovery work of DBT and LOSS category assets?

Operations Department (earlier Monitoring & Recovery Department

(MRD)

14. What does the MRD does now?

It looks after Recovery Policy matters, Asset Management and BIFR

etc.

15. What is a Standard Asset?

An asset which does not have any problem and did not default in

repayment.

16. How to prevent slippage of Standard Assets to NPA?

a. Proper market survey

b. Pro-active approach

c. Time and adequate finance

d. Proper documentatione. Watching market developments

17. What is a border line Standard asset?

Where interest and/or installment is remaining unpaid for more than

60 days.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 26/70

26

18. Why should the corporation be concerned about border line

standard assets?

Because they are potential NPAs

19. What strategies are to be adopted in case of borderline standard(BLS) asset

- To look for early warning signals

- Personal contact

- Putting pressure

- Examining rephasement / reschedulement

- Strict vigil

20. What is the goal of the Corporation for NPAs

To bring them down to 2.5%

21. What is ABC Analysis

Analysis of sub-standard assets into 3 categories i.e

- 3 months old

- 3 to 6 months old

- 6 to 12 months old

22. What is the well structured review mechanism

a. A well structured review mechanism implies the following

- Monitoring, follow-up and review of all NPAs and BLS

- Review of HODs (Operations)

- Periodical information to the board in respect of all NPA

accounts with one crore and above cases

- For above Rs.250.00 lakhs disbursed cases appraisal by outside

export.

23. What should be the focus of NPA review meetings?

a. All seized units pending for sale for more than 3 years

b. OTS approved but amounts not received fully.

c. BLS and sub standard assets

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 27/70

27

24. When should the Branch Office submit information about the down

gradation from Standard to Sub-standard etc.

Every month on or before 7th

.

25. What are the corrective measures to be adopted for maximizing

recoveries?

- Review by HOD (OPD) of follow up actions of BM / Area

Officer.

- Being in touch with other financial institutions

- Collecting 100% interest arrears in DBT 1

- Encouraging DBT 2 and DBT 3 and loss category for OTS

26. Difference between preventive and corrective measures?

a. Preventive steps are the ones taken for stopping the unit to

slip /down Grade from Standard to Sub-standard etc.

b. Corrective means steps taken after the unit defaulted for up-

gradation

27. What are the preventing measures to be taken to prevent

downgradation of units?- Watch and monitor

- No fresh NPAs

- Greater visual of Sub-standard

- Considering inter-se transfer , transfer of Management

- Regular inspections

28. Why the Corporation appoints Nomine Directors?

For Keeping track of unit’s health and for taking timely action

29. What is the present policy of the Corporation on Nomine Directors?

Corporation Nominates Officers where sanction amount is Rs.5.00

crore above.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 28/70

28

Recovery Follow-Up Action At A Glance

A. Standard Assets (not in arrears both principal and interest)

1. For Nonpayment Of One Interest/Principal Demand

a. Interest - First letter on the following day of expiry of grace Period

Installment- first letter on the following day of the due date.

b. If not paid another letter in 10 days from date of 1st

letter.

c. Still unpaid third letter (stiff)

1. if promised on the

2. in 10 days from 2nd

letter

If the cheque is bounced issue notice within 7 days from the date of

dishonor. Pays fine or else initiate action under NA act.

Follow-up, visit, collect at least before next interest/ principal demand

2. Non-payment of 2 of 3 monthly interest/installment demands and one

quarterly installment. This is called a Stressed Asset and requires closed

monitoring.

collect minimum amount before getting downgraded

all the steps stated/ discussed above and to inspect within 45

(days from earliest date of default)

genuine problems reschedule/ funding of interest (MD’s

power)

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 29/70

29

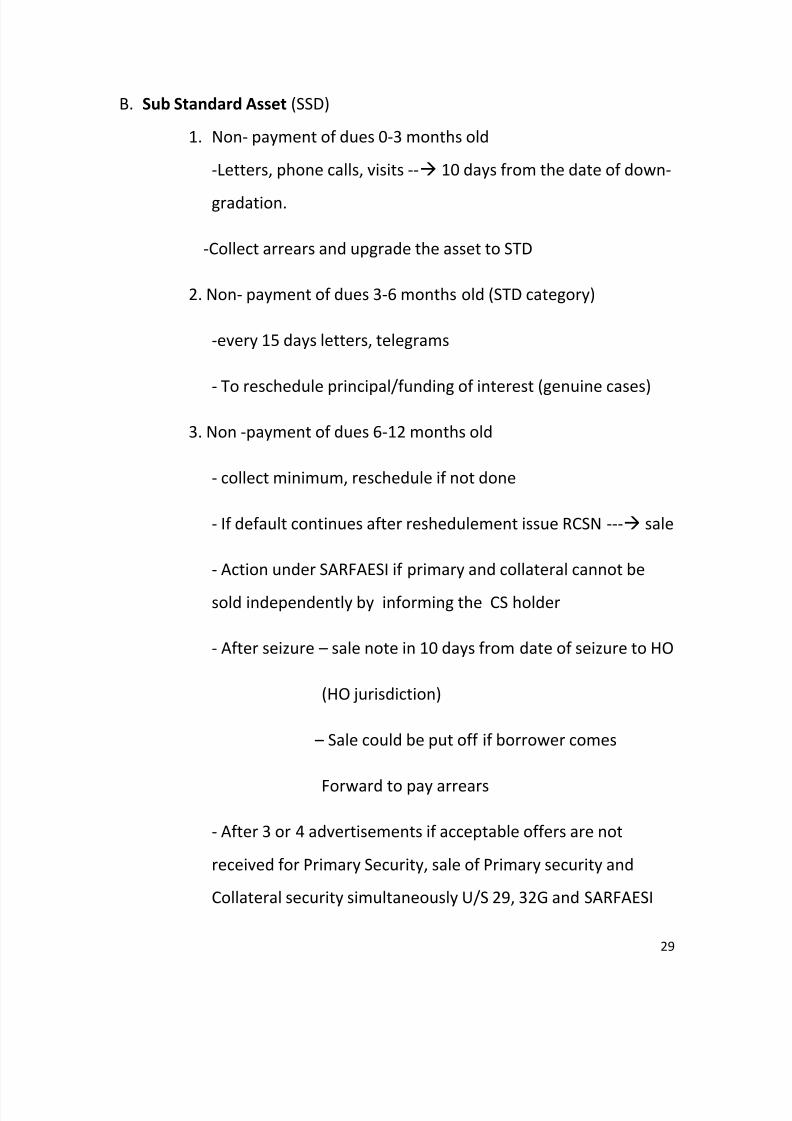

B. Sub Standard Asset (SSD)

1. Non- payment of dues 0-3 months old

-Letters, phone calls, visits -- 10 days from the date of down-

gradation.

-Collect arrears and upgrade the asset to STD

2. Non- payment of dues 3-6 months old (STD category)

-every 15 days letters, telegrams

- To reschedule principal/funding of interest (genuine cases)

3. Non -payment of dues 6-12 months old

- collect minimum, reschedule if not done

- If default continues after reshedulement issue RCSN --- sale

- Action under SARFAESI if primary and collateral cannot be

sold independently by informing the CS holder

- After seizure – sale note in 10 days from date of seizure to HO

(HO jurisdiction)

– Sale could be put off if borrower comes

Forward to pay arrears

- After 3 or 4 advertisements if acceptable offers are not

received for Primary Security, sale of Primary security and

Collateral security simultaneously U/S 29, 32G and SARFAESI

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 30/70

30

C. Doubt First Assets

- same as far as SSD

- if there is doubt of alienation/disposal by the party action U/S

31(1) (aa)

SNC : Sale Negotation Committee

LRP : Loan Recovery Policy

D. Loss Assets (primary security sold)

- Sec 32G of SFC act

- First notice, after sale of Primary Security- If no payment proposal to MD recovery certificate

- Distraint order (taking possession)

E. Sale U/S 32G of immovable properties

- Serve notice in form no 4 in 10 days after receiving the recovery

certificate from MD.

1. Applicability of revised guidelines of sale of assets U/s.29 of SFC’sAct?

To such improved offers / enquiries that are received after the expiry

of 7 days notice period, but before the issue of Sale contribution

tenderer on hand.

2. What should be the improved offer for considering sale U/s.29?

- Not less than 10% over and above offer on hand where offers is

up to Rs.40.00 lakhs

- 5% over and above the offer on hand where more than Rs.40.00

lakhs is

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 31/70

31

3. How much the EMD and other deposit the late tenderer should

submit while giving improved offer?

EMD of Additional deposit equivalent to 15% of improved offer

4. Whether the highest offer received in the process need to be

placed on the Notice Board?

No. Need not be placed.

5. What needs to be done If the existing tenderer does not turn up for

the SNC Meeting?

Give him another chance.

6. When did the Corporation formulate the Valuation Guidelines?

For valuing all assets of the Industry and property offered as

Collateral Security Corporation formulated valuation guidelines Vide

Office Order No.116, Dt.31.08.1999.

7. When the Corporation did modify the valuation guidelines?

The revised guidelines were issued Vide Officer Order No.107,

Dt.18.08.2010.

8. What should be the EMD for seized units lying/kept in the

Corporation godown?

10% of the estimated value of asset.

9. When did the Corporation revise the Loan recovery Policy and OTS

guidelines?

Board of Directors at the meeting held on 10.01.2013.

10. What is the objective of the revised LRP & OTS guidelines?

To maximize recovery of dues, especially NPS’s.

To reduce Net NPA’s

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 32/70

32

11. What are the charges in the revised OTS Guidelines?

- 31.03.2010 is the cut of date for OTS eligibility (earlier

31.03.2004)

- Doubtful category assets as on 31.3.2010

- All losses assets.

- 12. What should be the down payment in case of Inter-se transfer /

change of Management [Page 285]

- 25% total loan outstanding in case of Substandard & Doubtful

- In case of the Standard Assets 5% of Principal outstanding or

payment of total arrears whichever is higher

13. Why the Corporation waives part of the Penal Interest [Page

No.285]

To motivate the borrowers to regularize the loan account or to close

the loan account.

14. Who is the Approving Authority in case of deviations regarding

Down Payment, Collateral Security relating to inter-se transfer / change

of management [Page No.285]Managing Director.

15. Authorities to Approve Waiver Of Penal Interest:

Page 286

16. Is there any limit on waiver of penal interest amount?

Yes. The total concession by way of disallowed Special Interest

Rebate and Penal Interest shall be limited to interest outstanding in

the loan account.17. Delegation of powers for Reshedulement of loan without extension

of loan period?

Page 286

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 33/70

33

18. What is that approving authority should see while considering

reshedulement?

The approving authority shall examine the projected profitability and

cash flow statements submitted by the assisted units while

considering re-schedulements.

19. Why the Corporation is considering OTS?

As a strategy to reduce NPAs and for recovering amounts from

chronic defaulters.

20. When did the SARFESI Act come into being?

SARFESI Act comes into force w.e.f. 21.06.2002

21. What is so special about SAFESI Act?

The Act empowers to recover the amount in NPA account by seized

and selling primary security and Non-agricultural Collateral Security

without intervention of courts.

RMD

1. What is RMD?

ANS: RMD stands for risk management department.

2. When did the corporation introduce credit risk rating?

ANS: During September 2005.

3. For what type of proposals and categories Corporation introduced

credit risk rating?

ANS: A.For loans above Rs 1.00 Crore

B. Categories:

1. Risk rating model for Term loan

2. Credit risk rating model Additional Term Loan

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 34/70

34

3. Credit Risk Rating Model Working Capital Term Loan

4. When did the corporation started using Credit Rating for the loans

above Rs.60 .00 lakhs?

ANS: W.e.f. 1/7/2009

5. What are the models to be used for rating loans above Rs.60.00

Lakhs?

ANS: Model- I- Term loan at above 60.00 Lakhs

Model- II- Addl Term loan above 60 lakhs

Model- III- WCTL/ corporate loans marketing assistance loans

6. When the corporation implemented rating model for loans above 30

lakhs and upto 60 lakhs?

ANS: W.e.f 1/8/2009

7. What are the new rating model for rating loans above Rs.30 Lakhs

and upto Rs.60 Lakhs?

ANS: Model- IV- Term Loan and above 30 lakhs and upto 60 Lakhs

Model- V- Add Term Loan above 30 lakhs and upto 60 lakhs

Model- VI – WCTL, Corporate loans, Marketing assistance loans above

Rs.30 lakhs and Rs.60 lakhs

8. What is the Revised Rating Nomenclature?

ANS: The revised rating nomenclature (approved at the board meeting

held on 26/5/2009] is as under page 393. No 4

9. Which loan proposals are to be considered?Ans: Proposals with the credit rating of CR1, CR2, Cr3 & CR 4 only

shall be considered.

10. Who will carry out the Rating for loan proposals above Rs.60 lakhs

Ans: Project Dept at HO (using model 1,2&3)

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 35/70

35

11. How to calculate stress tested DSCR ?

Ans: With 5% decrease in revenue and 5% increase cost of raw

materials

12. Why Rating?

To assess the risk, to find out has safe our money is are.

13. Details of Grades To Be Accorded

Page No.393

14. What type of proposals shall be considered?

Ans: Proposals with a rating of CR1, CR2, Cr3 & CR 4 shall be

considered

15. When the proposals fall below CR4 what should the BM do?

Ans ; BM should refer such proposals to HO Project Department

16. When Collateral security being offered covers 100% or more of the

loan whether full marks can be given while rating?

Ans: Yes.

17. In case of party offering Corporate Guarantee,how the rating should

be done?

Credit rating issued by on outside leading Credit Rating Agency .

18. What is Stress Tested DSCR?Calculating DSCR

- By decreasing the revenue by 5%

- By increasing the cost of Raw Materials by 5%

- Average of above 2 shall be taken for rating.

19. Why Stress Tested is calculated (Sensitive analysis)?

Ans: Just TO know whether unit can with stand Turbulations in the

market.

20. When does the proposals can be rejected with out rating?

Ans: Proposals shall be rejected and no need for rating the same

when there is adverse reporting relating to:

- Integrity

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 36/70

36

- Corporate Governance

- Track record

- Managerial Competency

20. How the marks for track record and payment record are to be

awarded (given)?

Ans: Based on the Standardized Comments furnished by Branches in

the Due Diligence Report.

21. If the Unit is approaching the Corporation for the 1st

time, How to

award marks for track report and payment record?

Ans: Since there is no track record and payment record marks shall

be Zero .

STAFF REGULATIONS

1. What are the Staff Regulations?

Staff regulations define the terms and conditions of appointment

and service of the staff i.e. duties, conduct and the remuneration

payable to them.

2. Whom dos the Staff Regulations apply?

All permanent employees of the corporation.

3. Whom does the Staff Regulations not apply?

Managing Director, State/Central Government employees on

deputation to the Corporation.

4. Whether Corporation can vary / change the provisions of Staff

Regulations?

Yes. With consultation of SIDBI / State Government.

5. What is Board?

The Board means the Board of Directors of the Corporation.

6. What is Pay?

Pay means amount drawn monthly by an employee

- For the Sanctioned post / Entitled

- Special pay and personal pay

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 37/70

37

- Any other emoluments classified as pay by the Board

- 7. What is Substantive Pay?

Substantive pay means the pay to which an employee is entitled

(O/a of post).

7.a.What is Special Pay?

Emoluments granted:

I for the specially assigned arduous work

ii. Additional responsibility.

8. What is Personal Pay?Additional Pay Granted to an employee for the lose of substantive

pay and on other personal considerations.

9. What is Compensatory Allowance?

An allowance granted to meet expenditure necessitated by

special circumstances in which duty is performed .

10. Define family?

Family means employee’s spouse, legitimate and step children,parents, un-married brothers and sisters.

11. Whether family includes second wife/ husband?

No, Not more than one wife or husband.

12. Who has the power to interpret and implement staff regulations?

Managing Director.

13. What sort of relief is available to an aggrieved employee [such as

appealing to the next higher authority] ?

An aggrieved employee can appeal against the decision of Managing

Director to the Board.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 38/70

38

13. Whether the Board’s decision on the aggrieved employees

appeal is final

Yes. It is final and binding on all concerned.

14. Name the types of permanent staff of the corporation/

(classification / categorization of permanent staff)

The permanent staff have been devided/categorized into 3 groups

Class A Asst. Manager and Above

Class B Assistant & Junior Officer

Class C Subordinate staff.

15. Who has the power to decide the cadre strength (No, of posts)?

Board of Directors.

16. Who has the power to appoint temporary staff?

Managing Director in Class B & Class C categories.

17. Any restrictions on such power of MD to appoint temporary staff >

Yes. The terms and conditions should not be more favorable than

those laid down in the staff regulations for an appointment carrying

equivalent status or responsibility..

18. Who has the power to appoint employees in the Corporation ?

Managing Director. However, in the case of officers with prior

approval of Board.

19. Whether a certificate of health and good character is a must /

mandatory for an employee joining the duties of corporation?

Yes. No person shall be appointed with out being certified by a

qualified Medical Practitioner about health and also a certificate

about good character.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 39/70

39

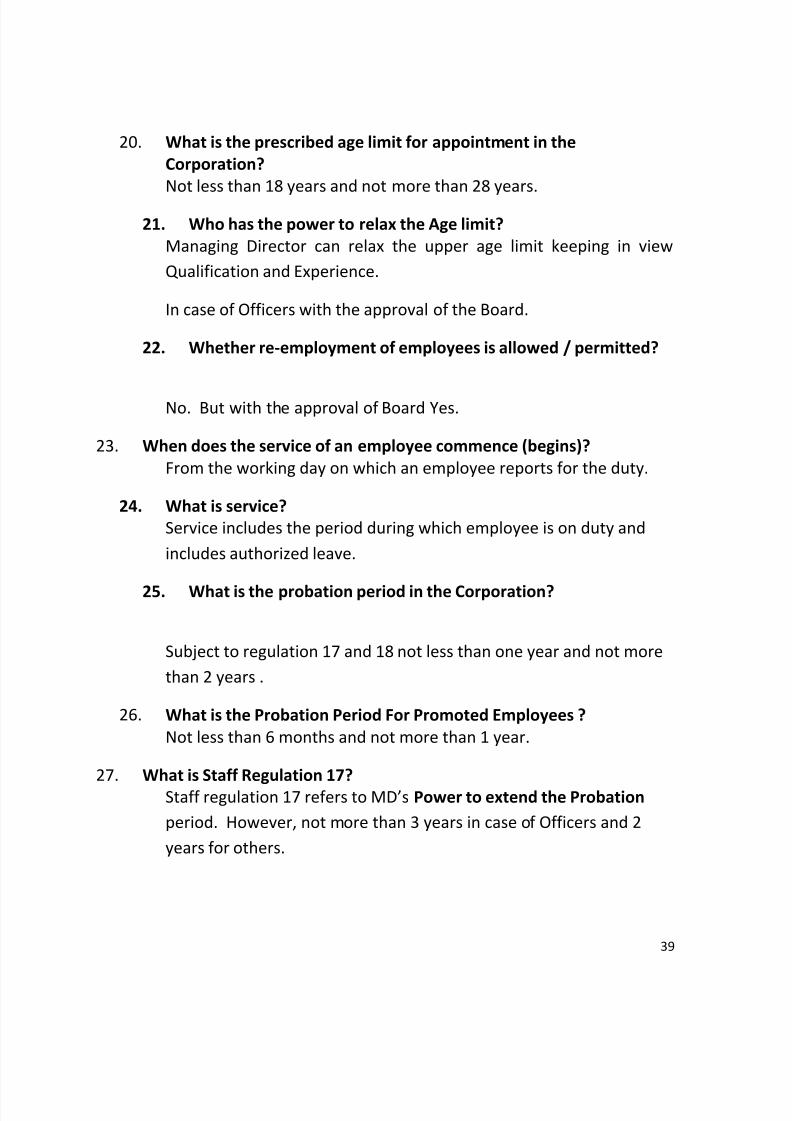

20. What is the prescribed age limit for appointment in the

Corporation?

Not less than 18 years and not more than 28 years.

21. Who has the power to relax the Age limit?

Managing Director can relax the upper age limit keeping in view

Qualification and Experience.

In case of Officers with the approval of the Board.

22. Whether re-employment of employees is allowed / permitted?

No. But with the approval of Board Yes.

23. When does the service of an employee commence (begins)?

From the working day on which an employee reports for the duty.

24. What is service?

Service includes the period during which employee is on duty and

includes authorized leave.

25. What is the probation period in the Corporation?

Subject to regulation 17 and 18 not less than one year and not more

than 2 years .

26. What is the Probation Period For Promoted Employees ?

Not less than 6 months and not more than 1 year.

27. What is Staff Regulation 17?

Staff regulation 17 refers to MD’s Power to extend the Probation

period. However, not more than 3 years in case of Officers and 2

years for others.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 40/70

40

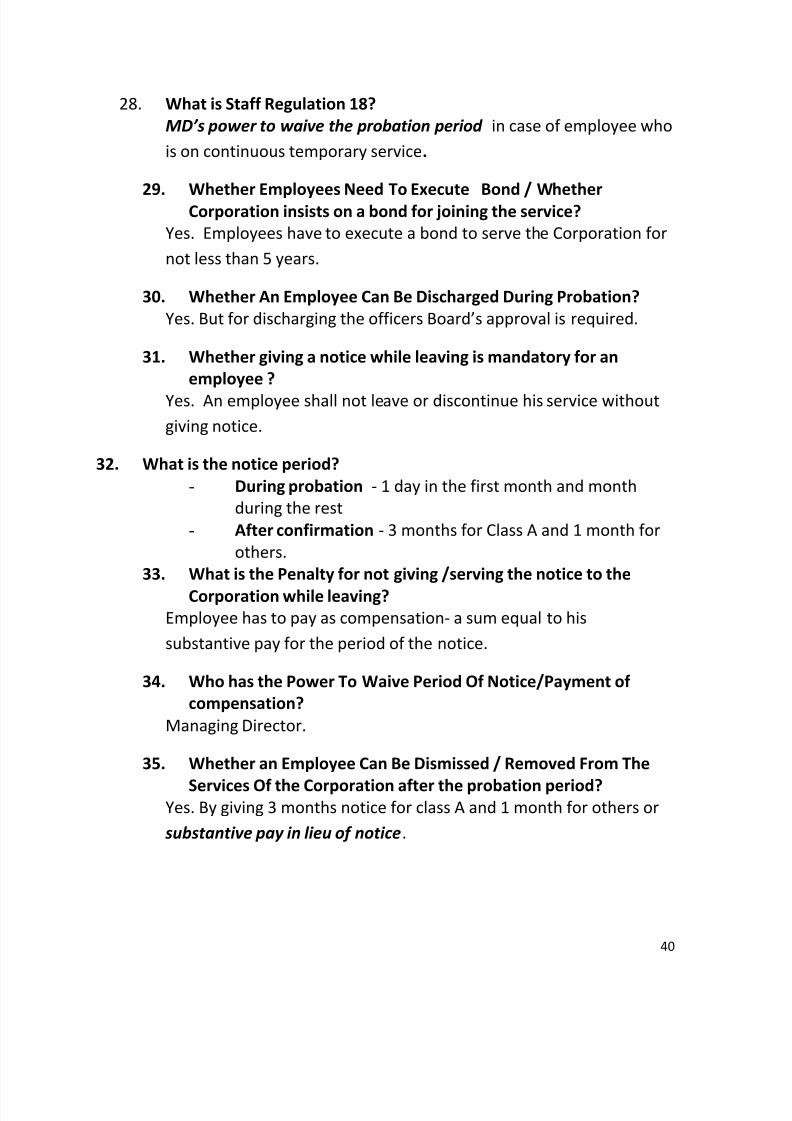

28. What is Staff Regulation 18?

MD’s power to waive the probation period in case of employee who

is on continuous temporary service.

29.

Whether Employees Need To Execute Bond / WhetherCorporation insists on a bond for joining the service?

Yes. Employees have to execute a bond to serve the Corporation for

not less than 5 years.

30. Whether An Employee Can Be Discharged During Probation?

Yes. But for discharging the officers Board’s approval is required.

31. Whether giving a notice while leaving is mandatory for an

employee ?

Yes. An employee shall not leave or discontinue his service without

giving notice.

32. What is the notice period?

- During probation - 1 day in the first month and month

during the rest

- After confirmation - 3 months for Class A and 1 month for

others.

33. What is the Penalty for not giving /serving the notice to the

Corporation while leaving?

Employee has to pay as compensation- a sum equal to his

substantive pay for the period of the notice.

34. Who has the Power To Waive Period Of Notice/Payment of

compensation?

Managing Director.

35. Whether an Employee Can Be Dismissed / Removed From The

Services Of the Corporation after the probation period?Yes. By giving 3 months notice for class A and 1 month for others or

substantive pay in lieu of notice.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 41/70

41

36. Whether an Employee Can Be Retired / Dismissed without notice / pay

in lieu thereof ?

Yes. In terms of Staff regulation 41 as penalty for breach of staff

regulations.

37. When does employee retire / when does superannuation and

retirement of an employee takes place?

On attaining 58 years. However Board may extend but maximum 60

years.

38. What is Reversion?

An employee, transferred or appointed to a higher post, being

brought back to his original post is called reversion.

39. When does An Employee Can Be Reverted?

With out notice within 1 year of such transfer / appointment.

40. What is Demotion?

As a punishment employees post being downgraded Eg. DM to Asst.

Manager.

41. Whether Staff Regulations Are Binding On All The Employees?

Yes. All the employees have to abide by the staff regulations.?

42. Whether Employees Can Seek Out Side Employment (even

honorary)?

No. MDs approval is required.

43. Whether Employees Can Seek Part Time Work?

No. How ever, MD may permit if it is not detrimental to his duties

and responsibilities.

44. Whether an Employee can Absent From His Station?

No. With out permission of MD(delegated authority)

No employee can absent from his station of working

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 42/70

42

46. Whether Employees of the Corporation can accept gifts?

No.They shall not accept any gift from the constituent of the

Corporation or from their subordinates.

47. Whether Employees of the Corporation can engage in any Commercial

business?

No.

48. Whether Employees of the Corporation are allowed to speculate in

stock, shares.

No. However, an employee can make bonafide investment of own funds.

49. What action Corporation takes Against Employees Who Are Arrested

For Debt Or Criminal Charge?

The concerned employee is placed under suspension.

50. When does an Employee can be Dismissed Other Than As A Penalty

For Breach Of Staff Regulations?

When an employee is committed a prison for debt or is convicted of any

offence involving moral turpitude (lack of integrity) .

51.What Short Of Relief Awaits An Employee Who Is Acquitted Of A

Charge?

The employee will be reinstated.

52.What are the grounds for which Corporation imposes penalties on the

employees (Staff regulation No.41)

1. Breach of Staff Regulations

2. Negligence

3. Inefficiency

4. Doing something knowingly detrimental to Corporations interests

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 43/70

43

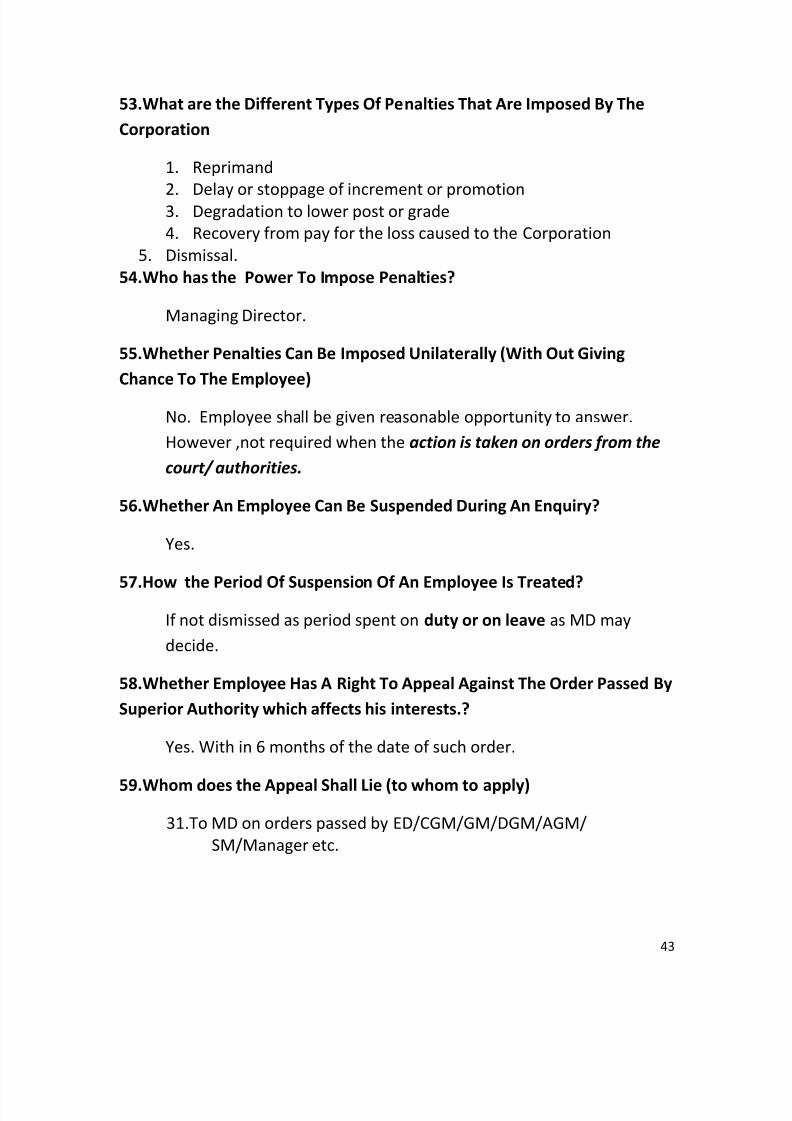

53.What are the Different Types Of Penalties That Are Imposed By The

Corporation

1. Reprimand

2.

Delay or stoppage of increment or promotion3. Degradation to lower post or grade

4. Recovery from pay for the loss caused to the Corporation

5. Dismissal.

54.Who has the Power To Impose Penalties?

Managing Director.

55.Whether Penalties Can Be Imposed Unilaterally (With Out Giving

Chance To The Employee)

No. Employee shall be given reasonable opportunity to answer.

However ,not required when the action is taken on orders from the

court/ authorities.

56.Whether An Employee Can Be Suspended During An Enquiry?

Yes.

57.How the Period Of Suspension Of An Employee Is Treated?

If not dismissed as period spent on duty or on leave as MD may

decide.

58.Whether Employee Has A Right To Appeal Against The Order Passed By

Superior Authority which affects his interests.?

Yes. With in 6 months of the date of such order.

59.Whom does the Appeal Shall Lie (to whom to apply)

31.To MD on orders passed by ED/CGM/GM/DGM/AGM/

SM/Manager etc.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 44/70

44

32. To the Board orders passed by MD

60. Whether an Employee Can Appeal Against the Order Passed On An

Appeal?

No.

61.What are the Requirements An Appeal Should Satisfy / fulfill?

(regulation 44)?

i. Shall be written in English or translated copy in English

ii. In polite and respectful language

iii. Specify the relief desired

iv. Shall be submitted through proper channelv. Shall contain all material statements and

Arguments.

62.Whether An Appeal Can Be Withheld ?

Yes . If the appeal does’t contain all the required information.

(Regulation 44) .

63.What are the Grounds On Which An Appeal Is Withheld?

An appeal is withheld by ED/CGM or the MD if

vi. It is illegible or unintelligible

vii. It deals with matters which do not concerned employee

personally.

viii. It does’t comply with regulation 44

ix. It repeats an appeal already rejected .

64.Whether the Employee Is Allowed To Know The Grounds On Which

His/Her Appeal Is Withheld? (Staff regulation 46)?

The authority shall inform the employee the fact of withhold the

appeal and the reasons for it.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 45/70

45

65. Whether an employee can appeal against the withholding of his

appeal?

No appeal shall lie against the withholding of an appeal(employees

can’t appeal against the withholding of his appeal.

Accounts

1. What was The System Of Accounting That Was Followed Earlier?

a. Corporation Followed Cash System Of Account till 31-3-2007

2. When did the Corporation Adopt Mercantile (accrued but not realized)

a. Mercantile system of accounting with effect from 1-4-2007

3. What are the principal books that are being maintained?

a. Bank book, Journal, general ledger.

4. When did the corporation introduce RCS and with whom/

a. Corporation entered RCS since 1-6-2001 with ING Vysya bank ltd.

5. What is RCS?

a. Rapid Collection Service for quick realization of local cheques received at

various branches of the corporation.

6. How the RCS system operates?

a. ING Vysya bank pools the amount of all the cheques deposited and

makes payment to HO on the following day for HYD, and on the second day

for the out station cheques.

7. How the credit is given to the loan accounts of the amount received from

the loanee’s?

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 46/70

46

a. Amount received by the way of cheques from the parties is credited to

the loan accounts only on the date of realization.

8. Any Exemption To The Way Of Crediting?

a. Yes, In the Month Of March Immediately Credit Is Given.

9. What is Appropriation Procedure?

a. If any bridge loan /seed capital, special capital the amount received shall

be adjusted towards these accounts first in the following manner and then

others.

1. OE

2. Commitment charges

3. Penal interest.

4. Principal.

10. While Appropriating Whether Any Priority is to be Given?

a. Priority shall be given to funded interest, term loan accounts and the RSR

scheme amount.

11. What sort of accounting methods followed for appropriation of

proceeds from Sale Of Collateral Security? (Page 339)

a. a. standard and substandard

-O.E

- Interest.

- Principal.

b. DBT and loss

-O.E

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 47/70

47

- Principal

- Interest.

12. How The Interest Is Calculated?

a. On products method.

13. What is the Procedure for Charging Compounding Interest?

a. The corporation charges interest on compounding basis at monthly on

the outstanding balances of principal, interest, O.E as exiting on all

accounts.

14. What is Shadow Account?

a. Shadow Account means those accounts where interest is provisional

reverse.

15. How the sale of units U/S 29 of SFC act takes place?

a. sale U/s 29 SFC’s act take place in two ways

- Outright basis i.e. 100% down payment

- Loan basis

16. What is Inter-se transfer?

a. Inter-se transfer is a tri- party agreement among the corporation, existing

borrower and the transferee.

17. What is the present applicable penal interest and how it is charged?

a. The present applicable penal interest is 2% pa it is charged on thedefaulted amount for the defaulted period.

18. What is the present rate of Special Interest Rebate?

a. 2%PA

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 48/70

48

19. What is the Present Procedure Of Extending The Special Interest

Rebate?

a. Special Interest Rebate is extended any month if account is regular

20. When did the Corporation Introduce Charging Of Interest On Monthly

Basis?

a. Corporation introduced charging of interest on monthly basis w.e.f 1-11-

2008.

21. What is Asset Carrying Cost?

a. Asset carrying cost is the cost incurred by the corporation for the seized

units in the form of watch and ward, insurance, etc.

22. What are Bank Charges? What is the procedure for debiting the same?

a. Bank charges are the charges incurred for cheque collection (charged by

the bank).Bank charges if less than Rs30 debited to P&L account, more than

Rs.30 debited to party’s account.

23. From which Date Corporation stated levying commitment charges?

a. Commitment charges are levied on all loan accounts sanctioned on or

after 1-12-2009.

24. On What Amount Commitment Charges Charged?

a. 1. Commitment charges is charged on undrawn portion of loan

2. Shall not be levied up to 6 months from the date of sanction.

25. What is the Present Rate Of Cc?

a. 1% + service tax

26. What is the Frequency Of Commitment Charges?

a. CC is levied at monthly frequency along with interest.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 49/70

49

27. Whether Commitment Charges Are Charged if 90% Of Loan Is Drawn?

a. No. CC shall not be levied when 90% sanctioned amount is drawn.

Whether balance loan amount ( unavailed) is cancelled or not .

28. What are Seizure Expenses?

a. All the expenses incurred in connection with seizure of the industrial

units, such as cost of locks purchased per seizure, tour expenses etc.

29. Why the Corporation Charges Premium On Premature

Closure/Prepayments?

a. Premium on premature closures is charged as redeployment of funds

may take some time and corporation shall not lose in between.

30. Whether Waiver Of Premium On Premature Closure Is Considered?

a. Yes. In deserving cases.

31. Are there any cases Where No Premium Is Charged ?

a. In following cases premium is not charged

1. The working capital term loan, special component term loan, seedcapital, soft loans.

2. Purchasers who bought U/S 29 of SFC act

3. Borrower repaying because different interest is being charged then

stipulated.

4. Term loan up to 5 lakhs.

5. DBT loss category.

32. Who is the Approving Authority for Waiver of Full/Partial Premium on

Premature Closure of Loan Account/Prepaid Accounts?

a. MD

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 50/70

50

33. What are Service Charges?

a. Service charges are the charges for processing of the application, i.e. to

meet part of the administrative and personal expenses.

34. Applicable Service Charges?

Item Applicable service charges

for composite loan NIL

Up to Rs. 5 lakh loan Rs. 1000/-+service tax

Above Rs.5 lakh 0.5% on applied amount

Additional working capital term

loans applied within 6 months from

closure and with existing security.

0.2 % on applied amount

35. Whether Corporation Charges For Any Other Service other than

processing of loan application?

a. Yes.Corporation levies service charges (in addition to the one for

processing of loan application) for the following services

1. Reshedulement

2. Evaluation of OTS

3. Consideration of Inter-se

4. Evaluation of collateral security.

5. Inspection of units.

35. Whether Corporation Levis Service Charges For Composite Loans?

a. NO.

36. What is the Amount of Service Charge for Loans upto o Rs.5 lakh

a. A lump sum service charge of Rs.1000

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 51/70

51

1. Whether service charges are levied on all types of loans account?

a. No. service charges shall be levied only on the term loan and working

capital term loan amounts sanctioned.

2. Does corporation refunds service charges?

a. Yes,

- If application is withdrawn before PSC or rejected by the

corporation by deducting 10 % of the amount paid.

- If proposal is approved by the PSC, but the party with draws or fails to

furnish required information by deduction 20% of the amount paid.

- No refund if the loan is sanctioned.

3. What is the up- front fee at present?

a. 0.5% of the loan amount.

4. When does the Corporation collect the upfront fee?

a. At the time of initial disbursement.

5. Whether upfront fee is collected on all the loan accounts?

a. No, in the following cases corporation doesn’t collect

. The special component plan loan accounts.

. IDBI/SIDBI seed capital and soft loans

. Loans under re-financial schemes for rehabilitation

6. How does the Corporation treat forfeiture of EMD amounts?

a. They are treated as miscellaneous income and credited to P&L account.

7. What is Gross Non Performing Asset (NPA)?

a. Gross NPA means Principal and OE outstanding in the non performing

assets.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 52/70

52

8. What is Net NPA?

a. Amount of principal and OE outstanding minus provision required on

such assets.

9. What is the Permissible Sealing Of Petty Cash Payments?

a. It is 200 per each voucher.

10. What is the Petty Cash Impressed Amount That Can Be Maintained?

a. At branch office Rs. 5000. and at F&A its Rs.10,000

11. What is the Minimum and the Maximum Period of Deposits?

a. The minimum period of deposits shall be one year and the maximum is 3

years.

12. What is the Procedure for Payment of Direct Taxes?

a. As per the CBDT (central board of direct access) notification dated 13-03-

2008 it is mandatory to pay all direct taxes only through electronic

payment with effect from 1-4-2008

13. What was the Purpose of establishing Credit Guarantee Trust for Microand Small Enterprises (CGTMSC)

a. CGTMSC was established by GOVT OF INDIA and SIDBI for the purpose of

guaranteeing credit facilities extended by the lending institutions to the

eligible borrowers without collateral security and 3rd

party guarantee.

14. When did the Corporation become eligible for the Guarantee under

CGTMSC?

a. CGTMSC registered corporation as member lending institution wide

letter 25-08-2010

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 53/70

53

15. What is the extent of financial assistance that can be given under

CGTMSE?

a. Not exceeding Rs. 50, 00, 000.

16. Who are eligible for the Credit Facility under CGTMSE?

a. New or existing Micro and Small Enterprises.

17. What are the Main Criteria For Extending The Credit Facility?

a. Purely Project Viability without CS and 3rd

party guarantee.

18. Whether Credit Facility for above Rs. 50 lakh is covered under CGTMSC

scheme?

a. No. the scheme covers loans not exceeding Rs. 50 lakh only

19. What is the applicable rate of interest?

a. The applicable rate of interest shall not be more than 3% over PLR of the

corporation.

20. When does the guarantee cover, provided under CGTMSC

commences/begins?

a. From the date of payment of guarantee fee and shall be available

throughout the agreed tenure (period) of the term loan?

21. What is the guarantee fee for the cover under CGTMSC?

a. A one time guarantee fee of 1% for loans upto 5lakh and 1.5% for loans

above 5 lakh. This fee is payable within 30 days from the date of 1st

disbursement.

22. Whether any annual service fee is payable for the CGTMSE cover

a. 0.5% for credit facility of 5lakh and 0.75% for Rs. above 5 lakh payable

within 60 days i.e on are before May 31st

of every year.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 54/70

54

23. When does the Corporation can invoke the guarantee provided by

CGTMSE?

a. 1. On issuing RCSN or initiation of recovery proceedings

2. After lapse of the lock in period of 18 months from the date of last

disbursement of credit to the borrower or from the date of guarantee cover

coming into force whichever is later.

3. Amount due and payable to the lending institution not being paid.

(NPA)

4. Guarantee shall be in force.

24. What are the Amounts That Qualify For The Guarantee cover under

CGTMSE?

a. 1. The trust pays the defaulted amount in respect of term loan ( including

interest up to date of NPA) and outstanding working capital advance (

including interest up to date of NPA)

2. Other charges such as penal interest, commitment charges, service

charge or any other levis/expenses shall not qualify *doesn’t pay+.

25. What is meant by credit facility?

a. Credit facility means the amount of financial assistance committed by the

lending institution to the borrower whether disbursed or not.

26. Who is eligible borrower under CGTMSC?

a. New or existing small scale industrial units to which credit facility has

been provided without any collateral or 3rd

party guarantee.

28. What is lending institution?

a. The one included in the second schedule to the RBI act 1934

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 55/70

55

29. What is material date?

a. The date on which the guarantee fee on the amount covered in respect

of eligible borrower becomes payable by the eligible institution to the trust.

30. What is NPA for the purpose of CGTMSE?

a. An asset classified as non -performing based on the instructions and

guidelines issued by RBI from time to time.

Financial Management

1. What is/Define Balance Sheet?

A financial statement that summarizes a company's assets, liabilities and

shareholders' equity at a specific point in time (31st March, 2013)

2. What is Profit and Loss Account?

A financial statement that summarizes the revenues, costs and expenses

incurred during a specific period of time - usually a fiscal year.

3. What is Gross Profit?

Gross profit is calculated by deducting cost of sales from turnover.

For example:

4. Difference between Balance Sheet and Profit & Loss

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 56/70

56

Balance Sheet is a snapshot whereas Profit and Loss is for a period. Balance

Sheet a stock concept while Profit and Loss is flow.

5. What is Funds Flow Statement?

The funds flow statement reports the flow of funds through the firm during

the year e.g., 1-4-2013 to 31-3-2014.

6. What are the Objectives /Uses of Fund Flow Statement?

1. Investors, creditors, bankers, government, etc., can understand the

managerial decisions regarding dividend distribution, utilization of funds

and earning capacity with the help of fund flow statement.

2. The quantum of working capital is revealed..

3. First source for judging the repaying capacity of an enterprise.

4. The management will be able to detect surplus/shortage of fund balance.

5. Separately calculated for the purpose of fund flow statement

7. What is Cash Flow Statement?

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 57/70

57

Summary of the actual or anticipated incomings and outgoings of cash in a

firm over an accounting period (month, quarter, year)

8. What is the difference between Cash Flow statement and Fund flow

statement?

A Cash Flow statement shows changes in cash position of the firm from one

period to another. Funds Flow statements states the changes in the

working capital of the business in relation to the operations in one time

period

Funds flow statement is based on broader concept i.e. working capital.

Cash flow statement is based on narrow concept i.e. cash, which is only one

of the elements of working capital.

9. What is Included in a Cash Flow Statement?

A Cash Flow Statement comprises (include) information on following 3

activities:

1. Operating Activities

2. Investing Activities

3. Financing Activities

10. What are the 3 basic financial statements that exist in the area of Financial Management?

The 3 basic financial statements that exist in the area of FinancialManagement are:

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 58/70

58

1. Balance Sheet.

2. Income Statement.

3. Cash Flow Statement.

11. What are the Advantages of Cash Flow Statement?

It shows the actual cash position available with the company

between the two balance sheet dates (funds flow and profit andloss account doesn’t show).

It helps the company in accurately projecting the future liquidity

position of the company so that it can arrange for any shortfall in

money

It acts like a filter and is used by many analyst and investors to judge whether company has prepared the financial statements properly or not

12. What are the Disadvantages of Cash Flow Statement?

It is not possible to deduce actual profit and loss of the company

by just looking at this statement.

In isolation this is of no use and it requires other financial

statements like balance sheet, profit and loss etc.

13. What are the Advantages of Fund Flow Statements?

A Funds flow statement is prepared to show changes in the assets, liabilitiesand equity between two balance sheet dates.

14. What is the other name for Fund Flow Statements?

It is also called Statement of Sources and Uses of Funds.

15. What are the Advantages of Fund Flow Statements/

The advantages of Funds F low statement are many .

Funds flow statement reveals the net result of Business operations

done by the company during the year.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 59/70

59

In addition to the balance sheet, it serves as an additional reference

for many interested parties like analysts, creditors, suppliers,government to look into financial position of the company.

shows how the funds were raised from various sources and also

how those funds were deployed by a company, It reveals the causes for the changes in liabilities and assets

between the two balance sheet dates therefore providing a detailedanalysis of the balance sheet of the company.

14. What are the Disadvantages of Fund Flow Statements?

Funds Flow statement has to be used along with balance sheet and profit and loss account for knowing financial strengths and

weakness of a company. It cannot be used alone.

does not reveal the cash position of the company, only rearranges the data which is there in the books of account and

therefore it lacks originality

basically historic in nature, that is it indicates what happened inthe past and it does not communicate anything about the future,

We can conclude that for shorter planning period “Cash Flow Statement isrelevant and for longer planning periods “Fund Flow Statement”

15. What is Capital Budgeting?

Capital budgeting is a process used by companies for evaluating and

ranking potential expenditures or investments that are significant in

amount

16. State the different Techniques used for Capital Budgeting?

Most popular techniques for analyzing a capital budgeting proposal.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 60/70

60

1. Payback Period

It is the length of time that it takes to recover your investment.

For example, to recover Rs30,000 at the rate of Rs10,000 per year would

take 3.0 years.

2. Net Present Value

The net present value of an investment is the present value of the cash

inflows minus the present value of the cash outflows. In other words the

net present value (NPV) is the present value of the benefits (PVB) minus the

present value of the costs (PVC)

NPV = PVB – PVC

3. Internal Rate of Return

The Internal Rate of Return (IRR) is the rate of return that an investor can

expect to earn on the investment. IRR method is actually the mostcommonly used method for evaluating capital budgeting proposals.

If the internal rate of return is greater than the interest Corporation chargeswe would accept the project

16. Which Method Is Better: the NPV or the IRR?

The NPV is better than the IRR. It is superior to the IRR method for at leasttwo reasons:

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 61/70

61

Reinvestment of Cash Flows: The NPV method assumes that the

project's cash inflows are reinvested to earn the hurdle rate; the IRR assumes that the cash inflows are reinvested to earn the IRR. Of the

two, the NPV's assumption is more realistic in most situations since

the IRR can be very high on some projects. Multiple Solutions for the IRR: It is possible for the IRR to have

more than one solution. If the cash flows experience a sign change(e.g., positive cash flow in one year, negative in the next), the IRR

method will have more than one solution. In other words, there will be more than one percentage number that will cause the PVB to equalthe PVC

17. What is Break Even Point?

A point where total revenue equals total costs (No profit No loss)

18. What is Breakeven Analysis?

Breakeven analysis is used to determine when your business will be able tocover all its expenses and begin to make a profit.

19. How to calculate the breakeven point?,

Breakeven point = fixed costs/ (unit selling price – variable costs)

20. What is Fixed Cost?

Fixed costs are expenses that do not vary with sales volume, such as rentand administrative salaries. These expenses must be paid regardless of sales,and are often referred to as overhead costs.

21. What is Variable Cost?

Variable costs fluctuate directly with sales volume, such as purchasing

inventory, shipping, and manufacturing a product

22. What is DSCR?

Also known as "Debt Coverage Ratio," (DCR) is the ratio of cash availablefor debt servicing to interest, principal and lease payments.

7/28/2019 Financial Notes by Jmr Sir

http://slidepdf.com/reader/full/financial-notes-by-jmr-sir 62/70

62

The higher this ratio is, the easier it is to obtain a loan.

23. What is Debt Equity Ratio?

A financial ratio which indicates the relative proportion of shareholders'

equity and debt used to finance a company's assets.