financial management seminar for the agricultural sector · financial management seminar for the...

TRANSCRIPT

Financial Management Seminar for the Agricultural Sector

Capital Budgeting DecisionsPresentation by:

CPA Cliff Nyandoro Technical Services Manager, ICPAK

23rd November 2017Merica Hotel, Nakuru

Uphold public interest

Capital budgeting definition

2

Capital budgeting is the process by which a companydetermines whether projects are worth pursuing.

Capital budgeting is also known as investment appraisal.

A project is worth pursuing if it increases the value of thecompany.

A project typically adds value to the company if it earns a rateof return that exceeds the cost of capital.

Capital budgeting definition

3

Simply put, it is the process of allocating resources for major capital,or investment expenditures.

Capital budgeting definition

4

simply put capital budgeting is the process of allocating resources for

major capital, or investment expenditures.

Capital budgeting

5

Examples of capital budgeting include:

investing in R&D,

purchasing new agricultural equipment

opening a new branch,

replacing a machine

construction of a farm house

A decision to invest in many other projects undertaken by anorganization qualify to be taken through and investment appraisalprocess.

Capital budgeting and cost of capital

6

A project is considered suitable for investment if its a rate of returnis greater than the cost of capital.

The opportunity cost of capital (also known as the hurdle rate) isthe expected return that is forgone by investing in the projectrather than in comparable financial securities, such as shares, withthe same risk as the project under consideration.

Always consider investing in projects whose rate of return is higherthan the price of capital unless they are projects for social good e.groads, airports, hospitals, schools, etc

Challenges in capital budgeting

7

While capital budgeting is a fairly straightforward process from aconceptual viewpoint, it can be very challenging in practice.

Not only is it difficult to determine the group's appropriate cost ofcapital, it is often even trickier to accurately forecast theincremental cash flows that result from taking on the project.

Other considerations in capital budgeting entail getting the righttools to aid in the investment appraisal process for complexprojects.

Capital budgeting illustrated

8

A construction company has to decide whether to construct a commercialbuilding for a client. The construction project requires an upfront outlay of£1m now and will generate a revenue of £1.25m in a year’s time when theclient pays for the completed building.

The expected return on investment is (£1.25m - £1m)/£1 million = 0.25 or 25per cent a year. The return on the project now has to be compared with thecompany's cost of capital. Instead of investing in the project, the group couldbuy, for example, bonds or shares in another construction company.

The return that could be achieved from investing in these securitiesrepresents the company’s opportunity cost of capital, assuming the return onthis portfolio of securities has the same risk profile as the project.

Capital budgeting illustrated

9

• If the opportunity cost of capital is less than 25 per cent, thenthe company should accept the project, and if it is less, then it shouldaccept. Clearly, if the company could earn 30 per cent in the financialmarket for a similar risk level, then it makes no sense to invest in a projectthat only offers 25 per cent.

• The net present value added to the company from taking on the projectcan be found by discounting the project’s incremental cash flows at theopportunity cost of capital. Assuming a cost of capital of 20 per cent, theproject’s net present value for the above example is: £1 million + £1.25million/(1+0.2) = £41667

• Note that future cash flows are discounted at a rate of 20 per cent toreflect the time value of money: a pound today is worth more than apound in a year’s time.

Techniques used in capital budgeting

10

Many formal methods are used in capital budgeting, including the techniques such as

• Accounting rate of return

• Average accounting return

• Payback period

• Net present value

• Profitability index

• Internal rate of return

• Modified internal rate of return

• Equivalent annual cost

• Real options valuation

Accounting Rate of Return

11

Accounting rate of return, also known as the Average rate ofreturn, or ARR is basically a financial ratio used in capital budgeting.

The ratio does not take into account the concept of time value ofmoney. ARR calculates the return, generated from net income ofthe proposed capital investment.

The ARR is a percentage return. Say, if ARR = 7%, then it means thatthe project is expected to earn seven cents out of each dollarinvested (yearly). If the ARR is equal to or greater than the requiredrate of return, the project is acceptable. If it is less than the desired

rate, it should be rejected.

Accounting Rate of Return

12

When comparing investments, the higher the ARR, the moreattractive the investment. More than half of large firms calculate ARRwhen appraising projects.

The key advantage of ARR is that is easy to compute and understand.

The main disadvantage of ARR is that it disregards the time factor interms of time value of money or risks for long term investments.

The ARR is built on evaluation of profits and it can be easilymanipulated with changes in depreciation methods. The ARR cangive misleading information when evaluating investments of differentsize.

Accounting Rate of Return

13

Payback Period

14

Payback period in capital budgeting refers to the period oftime required to recoup the funds expended in aninvestment, or to reach the break-even point.

For example, a $1000 investment made at the start of year 1which returned $500 at the end of year 1 and year 2respectively would have a two-year payback period.

Payback period is usually expressed in years. Starting frominvestment year by calculating Net Cash Flow for each year.

Payback Period

15

Net Cash Flow Year 1 = Cash Inflow Year 1 - Cash OutflowYear 1.

Then Cumulative Cash Flow = (Net Cash Flow Year 1 +

Net Cash Flow Year 2 + Net Cash Flow Year 3, etc.)

Accumulate by year until Cumulative Cash Flow is a positivenumber: that year is the payback year.

Payback Period

16

The time value of money is not taken into account. Payback periodintuitively measures how long something takes to "pay for itself."

All else being equal, shorter payback periods are preferable tolonger payback periods.

Payback period is popular due to its ease of use despite therecognized limitations described below.

Payback Period

17

It does not account for the time value of money, risk, financing, orother important considerations, such as the opportunity cost.

Whilst the time value of money can be rectified by applying aweighted average cost of capital discount, it is generally agreed thatthis tool for investment decisions should not be used in isolation.

Preferred alternative measures of "return" are net presentvalue and internal rate of return.

Payback Period assumption

18

An implicit assumption in the use of payback period is that returnsto the investment continue after the payback period.

Payback period does not specify any required comparison to otherinvestments or even to not making an investment.

Net Present Value (NPV)

19

The net present value (NPV) or net present worth (NPW) isa measurement of profit calculated by subtractingthe present values (PV) of cash outflows (including initialcost) from the present values of cash inflows over a periodof time.

Incoming and outgoing cash flows can also be described asbenefit and cost cash flows, respectively.

Time value of money dictates that time affects the value ofcash flows.

Net Present Value (NPV)

20

In other words, a lender may give you 99 cents for the promise ofreceiving $1.00 a month from now, but the promise to receive thatsame dollar 20 years in the future would be worth much less todayto that same person (lender), even if the payback in both cases wasequally certain.

This decrease in the current value of future cash flows is based onthe market dictated rate of return.

More technically, cash flows of nominal equal value over a timeseries result in different effective value cash flows that make futurecash flows less valuable over time.

Net Present Value (NPV)

21

If for example there exists a time series of identical cash flows, thecash flow in the present is the most valuable, with each future cashflow becoming less valuable than the previous cash flow.

A cash flow today is more valuable than an identical cash flow in thefuture because a present flow can be invested immediately andbegin earning returns, while a future flow cannot.

Net present value (NPV) is determined by calculating thecosts (negative cash flows) and benefits (positive cash flows)for each period of an investment

Net Present Value (NPV)

22

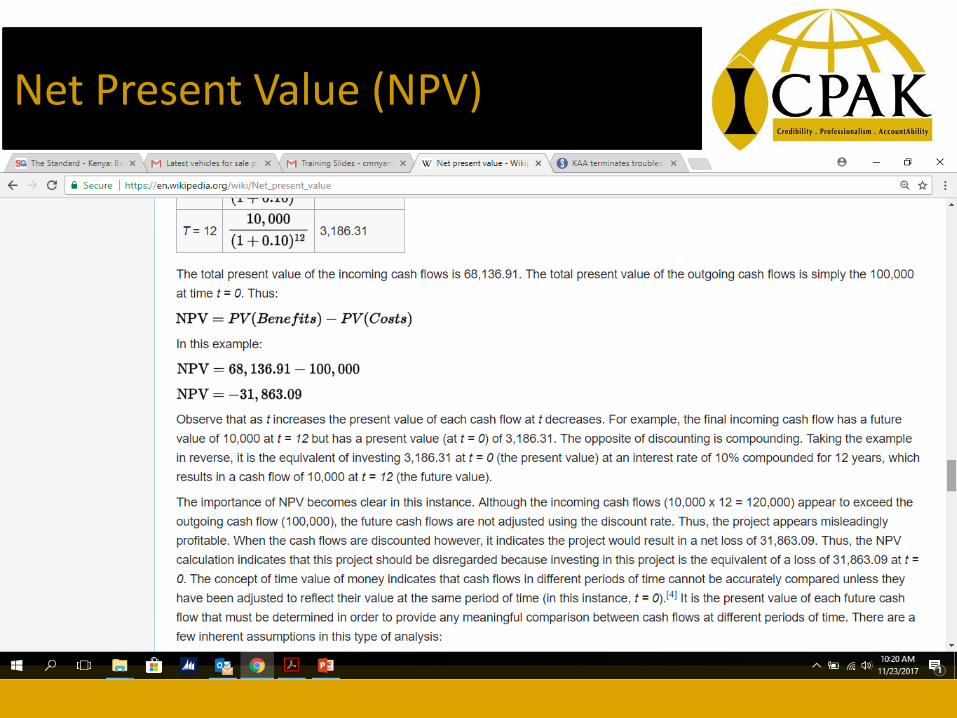

In a theoretical situation of unlimited capital budgeting acompany should pursue every investment with a positiveNPV.

However, in practical terms a company's capital constraintslimit investments to projects with the highest NPV whosecost cash flows, or initial cash investment, do not exceed thecompany's capital.

Refer to the illustration below on calculation of NPV.

Net Present Value (NPV)

23

Net Present Value (NPV)

24

Drawbacks of NPV

25

If, for example, the Rt are generally negative late in the project (e.g.,an industrial or mining project might have clean-up and restorationcosts), then at that stage the company owes money, so a highdiscount rate is not cautious but too optimistic. Some people seethis as a problem with NPV.

A way to avoid this problem is to include explicit provision forfinancing any losses after the initial investment, that is, explicitlycalculate the cost of financing such losses.

Drawbacks of NPV

26

Another common pitfall is to adjust for risk by adding a premium tothe discount rate.

Whilst a bank might charge a higher rate of interest for a riskyproject, that does not mean that this is a valid approach toadjusting a net present value for risk, although it can be areasonable approximation in some specific cases.

One reason such an approach may not work well can be seen fromthe following: if some risk is incurred resulting in some losses, thena discount rate in the NPV will reduce the effect of such lossesbelow their true financial cost.

Drawbacks of NPV

27

• Another issue with relying on NPV is that it does not provide anoverall picture of the gain or loss of executing a certain project.To see a percentage gain relative to the investments for theproject, usually, Internal rate of return or other efficiencymeasures are used as a complement to NPV.

• Non-specialist users frequently make the error of computingNPV based on cash flows after interest. This is wrong because itdouble counts the time value of money. Free cash flow should beused as the basis for NPV computations.

Internal Rate of Return (IRR)

28

Corporations use IRR in capital budgeting to comparethe profitability of capital projects in terms of the rate of return.

For instance, a corporation will compare an investment in a newplant versus an extension of an existing plant based on the IRR ofeach project.

To maximize returns, the higher a project's IRR, the more desirableit is to undertake the project. If all projects require the sameamount of up-front investment, the project with the highest IRRwould be considered the best and undertaken first.

Internal Rate of Return (IRR)

29

Applying the internal rate of return method to maximizethe value of the firm, any investment would be accepted, if itsprofitability, as measured by the internal rate of return, is greaterthan a minimum acceptable rate of return.

The appropriate minimum rate to maximize the value added to thefirm is the cost of capital, i.e. the internal rate of return of a newcapital project needs to be higher than the company's cost ofcapital.

This is because an investment with an internal rate of return whichexceeds the cost of capital has a positive net present value.

Internal Rate of Return (IRR)

30

However, the selection of investments may be subject to budgetconstraints, or they may be mutually exclusive competing projects,such as a choice between or the capacity or ability to manage moreprojects may be practically limited.

In the example cited above, of a corporation comparing aninvestment in a new plant versus an extension of an existing plant,there may be reasons the company would not engage in bothprojects.

Drawbacks of IRR

31

As a tool applied to making an investment decision, to decidewhether a project adds value or not, comparing the IRR of a singleproject with the required rate of return, in isolation from any otherprojects, is equivalent to the NPV method.

If the appropriate IRR (if such can be found correctly) is greater thanthe required rate of return, then using the required rate of return todiscount cash flows to their present value, the NPV of that projectwill be positive, and vice versa.

However, using IRR to sort projects in order of preference does notresult in the same order as using NPV.

Q & A

32