financial management: lecture 4 bond valuation the application of the present value concept

Post on 18-Dec-2015

215 views

TRANSCRIPT

Financial management: lecture 4

Bond valuation

The application of the present value concept

Financial management: lecture 4

Today’s plan

Review of what we have learned in the last lecture

Interest rates and compounding Some terminology about bonds Value bonds The yield curve Default risk

Financial management: lecture 4

What have we learned in the last lecture?

The present value formulas of perpetuity and annuity

The application of the PV of annuity

Financial management: lecture 4

My solution

year Beginningbalance

Interest payment

Principlepayment

Total payment

Ending balance

0

1

2

3

$20,000

13,809

7,154

$1,500 $6,191 $7,691 $13,809

1,036 6,655

537 7,154 7,691 0

7,691 7,154

Financial management: lecture 4

A problem John is 65 years old and wants to retire next

year. After retirement, he wants to have an annual income of $24,000 for 20 years from his retirement fund, which has an annual interest rate of 6%. Suppose John will get the first retirement income one year from now. Then• How much money should John have in his retirement

fund in the end of this year?• Suppose John started to work 19 years ago and put

the same amount of money every year in his retirement fund. How much should he put every year? ( including this year, there will be a total of 20 years)

Financial management: lecture 4

Nominal and real interest rates

Nominal interest rate• What is it?

Real interest rate• What is it?

Inflation• What is it?

Their relationship• 1+real rate =(1+nominal rate)/(1+inflation)

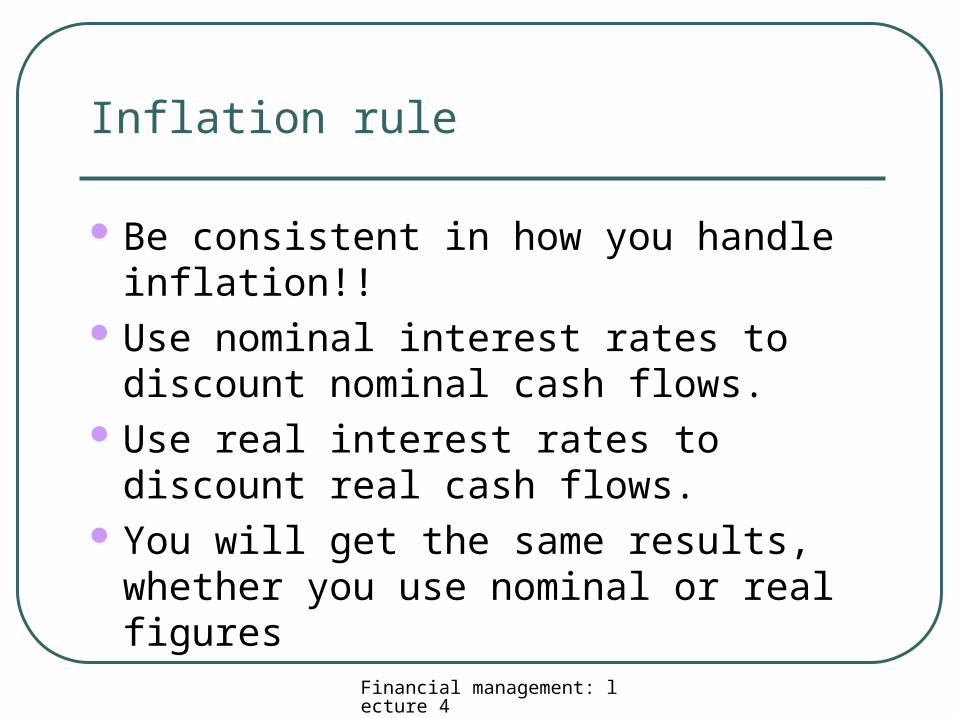

Financial management: lecture 4

Be consistent in how you handle inflation!! Use nominal interest rates to discount

nominal cash flows. Use real interest rates to discount real cash

flows. You will get the same results, whether you

use nominal or real figures

Inflation rule

Financial management: lecture 4

Example

You own a lease that will cost you $8,000 next year, increasing at 3% a year (the forecasted inflation rate) for 3 additional years (4 years total). If discount rates are 10% what is the present value cost of the lease?

1 real interest rate = 1+nominal interest rate1+inflation rate

Financial management: lecture 4

Inflation

Example - nominal figures

99.429,26$

78.59708741.82=8000x1.034

56.63768487.20=8000x1.033

92.68098240=8000x1.032

73.727280001

10% @ PVFlowCash Year

4

3

2

10.182.87413

10.120.84872

10.18240

1.108000

Financial management: lecture 4

Inflation

Example - real figures

Year Cash Flow [email protected]%

1 = 7766.99

2 = 7766.99

= 7766.99

= 7766.99

80001.03

7766.991.068

82401.03

8487.201.03

8741.821.03

2

3

4

7272 73

6809 92

3 6376 56

4 5970 78

26 429 99

7766 991 068

7766 991 068

7766 991 068

2

3

4

.

.

.

.

..

..

..

= $ , .

Financial management: lecture 4

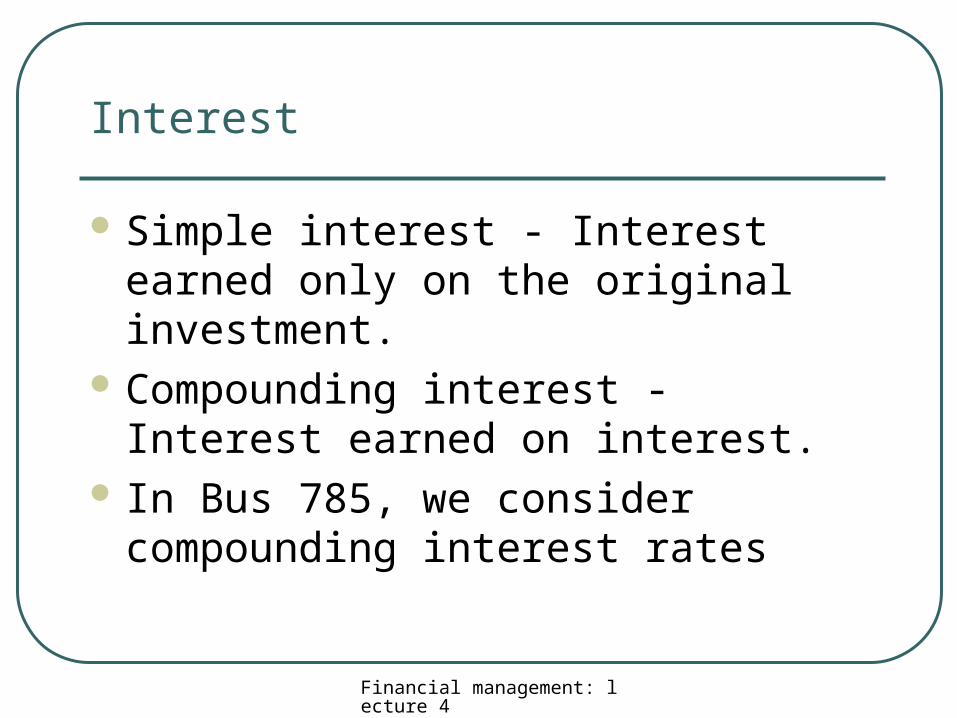

Interest

Simple interest - Interest earned only on the original investment.

Compounding interest - Interest earned on interest.

In Bus 785, we consider compounding interest rates

Financial management: lecture 4

Simple interest

Example

Simple interest is earned at a rate of 6% for five years on a principal balance of $100.

Financial management: lecture 4

Simple interest

Today Future Years

1 2 3 4 5

Interest Earned 6 6 6 6 6

Value 100 106 112 118 124 130

Value at the end of Year 5 = $130

Financial management: lecture 4

Compound interest

Example

Compound interest is earned at a rate of 6% for five years on $100.

Today Future Years

1 2 3 4 5

Interest Earned 6.00 6.36 6.74 7.15 7.57

Value 100 106.00 112.36 119.10 126.25133.82

Value at the end of Year 5 = $133.82

Financial management: lecture 4

Interest compounding

The interest rate is often quoted as APR, the annual percentage rate.

If the interest rate is compounded m times in each year and the APR is r, the effective annual interest rate is

11

m

mr

Financial management: lecture 4

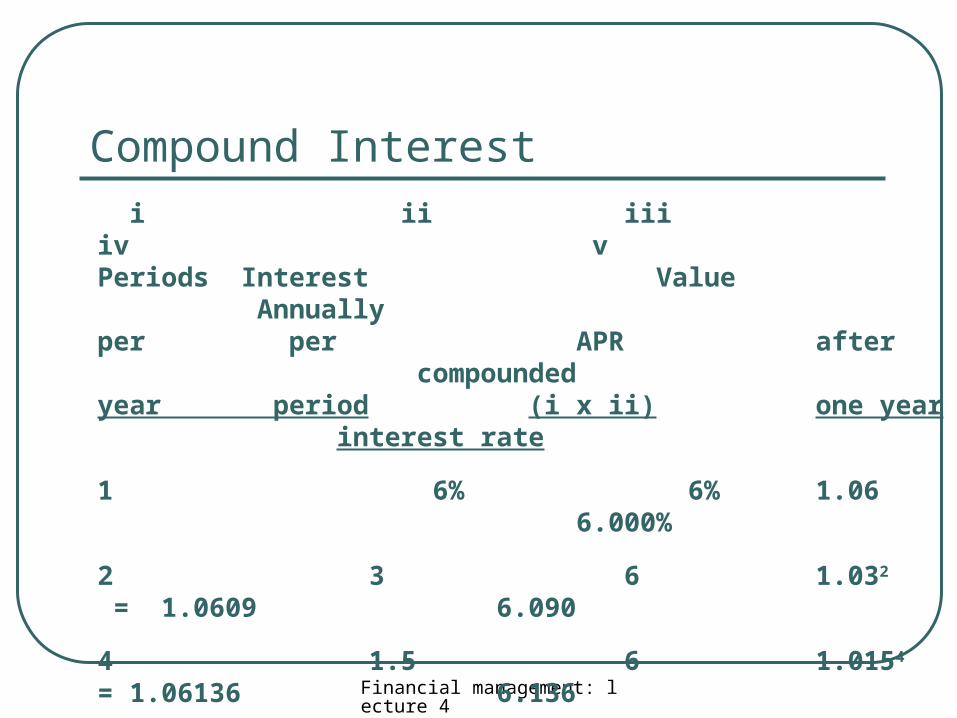

Compound Interest i ii iii iv vPeriods Interest Value Annuallyper per APR after compoundedyear period (i x ii) one year interest rate

1 6% 6% 1.06 6.000%

2 3 6 1.032 = 1.0609 6.090

4 1.5 6 1.0154 = 1.06136 6.136

12 .5 6 1.00512 = 1.06168 6.168

52 .1154 6 1.00115452 = 1.06180 6.180

365 .0164 6 1.000164365 = 1.06183 6.183

Financial management: lecture 4

Compound Interest

02468

1012141618

Number of Years

FV

of

$1

10% Simple

10% Compound

Financial management: lecture 4

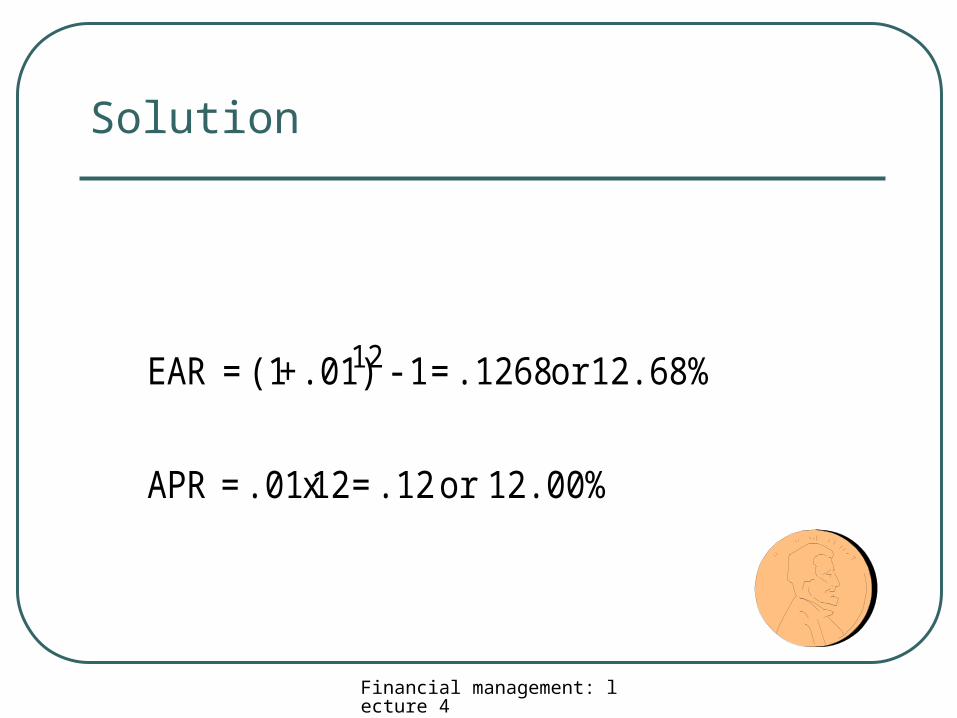

Interest Rates

Example

Given a monthly rate of 1% (interest is compounded monthly), what is the Effective Annual Rate(EAR)? What is the Annual Percentage Rate (APR)?

Financial management: lecture 4

Solution

12.00%or .12=12 x .01=APR

12.68%or .1268=1 - .01)+(1=EAR 12

Financial management: lecture 4

Interest Rates

Example

If the interest rate 12% annually and interest is compounded semi-annually, what is the Effective Annual Rate (EAR)? What is the Annual Percentage Rate (APR)?

Financial management: lecture 4

Solution

APR=12% EAR=(1+0.06)2-1=12.36%

Financial management: lecture 4

Bonds

Bond – a security or a financial instrument that obligates the issuer (borrower) to make specified payments to the bondholder during a time horizon.

Coupon - The interest payments made to the bondholder.

Face Value (Par Value, Face Value, Principal or Maturity Value) - Payment at the maturity of the bond.

Coupon Rate - Annual interest payment, as a percentage of face value.

Financial management: lecture 4

Bonds

A bond also has (legal) rights attached to it:• if the borrower doesn’t make the required

payments, bondholders can force bankruptcy proceedings

• in the event of bankruptcy, bond holders get paid before equity holders

Financial management: lecture 4

An example of a bond

A coupon bond that pays coupon of 10% annually, with a face value of $1000, has a discount rate of 8% and matures in three years.• The coupon payment is $100 annually

• The discount rate is different from the coupon rate.

• In the third year, the bondholder is supposed to get $100 coupon payment plus the face value of $1000.

• Can you visualize the cash flows pattern?

Financial management: lecture 4

Bonds

WARNINGWARNINGThe coupon rate IS NOT the discount rate used in the Present Value calculations. The coupon rate merely tells us what cash flow the bond will produce.

Since the coupon rate is listed as a %, this misconception is quite common.

Financial management: lecture 4

Bond Valuation

The price of a bond is the Present Value of all cash flows generated by the bond (i.e. coupons and face value) discounted at the required rate of return.

Nr

cpn

r

cpn

r

cpnPV

)1(

000,1...

)1()1( 21

Financial management: lecture 4

Zero coupon bonds

Zero coupon bonds are the simplest type of bond (also called stripped bonds, discount bonds)

You buy a zero coupon bond today (cash outflow) and you get paid back the bond’s face value at some point in the future (called the bond’s maturity )

How much is a 10-yr zero coupon bond worth today if the face value is $1,000 and the effective annual rate is 8% ?

PV

Facevalue

Time=tTime=0

Financial management: lecture 4

Zero coupon bonds (continue)

P0=1000/1.0810=$463.2 So for the zero-coupon bond, the price is

just the present value of the face value paid at the maturity of the bond

Do you know why it is also called a discount bond?

Financial management: lecture 4

Coupon bond

The price of a coupon bond is the Present Value of all cash flows generated by the bond (i.e. coupons and face value) discounted at the required rate of return.

)()()1()1(

11

)1(

)(....

)1()1( 21

parPVannuityPVr

par

rrrcpn

r

parcpn

r

cpn

r

cpnPV

tt

t

Financial management: lecture 4

Bond Pricing

Example

What is the price of a 6 % annual coupon bond, with a $1,000 face value, which matures in 3 years? Assume a required return of 5.6%.

Financial management: lecture 4

Bond Pricing

Example

What is the price of a 6 % annual coupon bond, with a $1,000 face value, which matures in 3 years? Assume a required return of 5.6%.

77.010,1$

)056.1(

060,1

)056.1(

60

)056.1(

60321

PV

PV

Financial management: lecture 4

Bond Pricing

Example (continued)

What is the price of the bond if the required rate of return is 6 %?

000,1$

)06.1(

060,1

)06.1(

60

)06.1(

60321

PV

PV

Financial management: lecture 4

Bond Pricing

Example (continued)

What is the price of the bond if the required rate of return is 15 %?

51.794$

)15.1(

060,1

)15.1(

60

)15.1(

60321

PV

PV

Financial management: lecture 4

Bond Pricing

Example (continued)

What is the price of the bond if the required rate of return is 5.6% AND the coupons are paid semi-annually?

Financial management: lecture 4

Bond Pricing

Example (continued)

What is the price of the bond if the required rate of return is 5.6% AND the coupons are paid semi-annually?

91.010,1$

)028.1(

030,1

)028.1(

30...

)028.1(

30

)028.1(

306521

PV

PV

Financial management: lecture 4

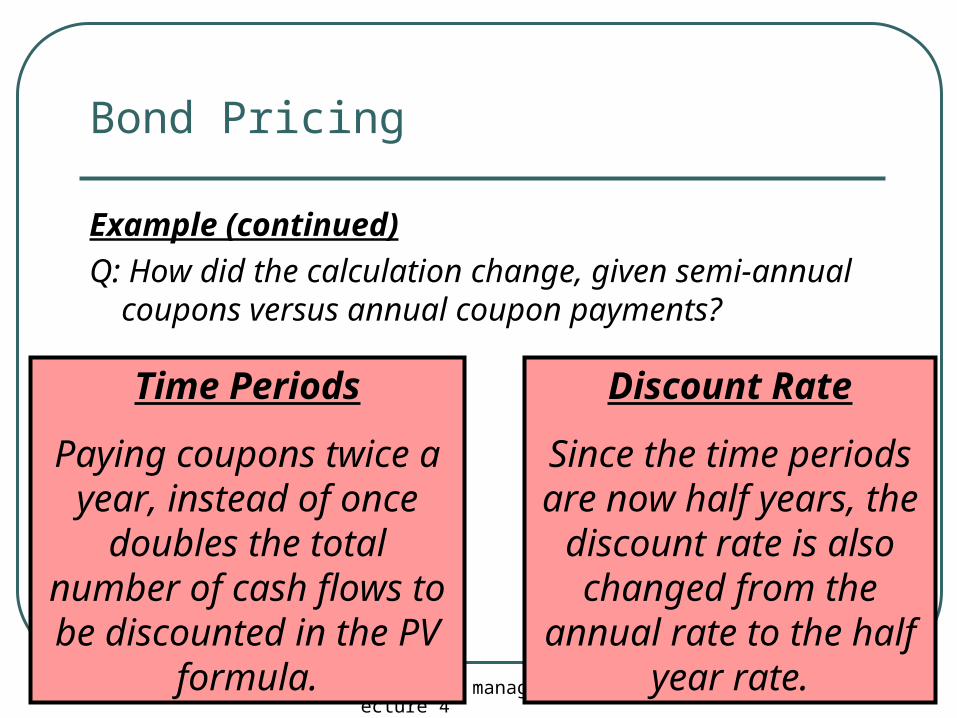

Bond Pricing

Example (continued)

Q: How did the calculation change, given semi-annual coupons versus annual coupon payments?

Financial management: lecture 4

Bond Pricing

Example (continued)

Q: How did the calculation change, given semi-annual coupons versus annual coupon payments?

Time Periods

Paying coupons twice a year, instead of once

doubles the total number of cash flows to be discounted

in the PV formula.

Financial management: lecture 4

Bond Pricing

Example (continued)

Q: How did the calculation change, given semi-annual coupons versus annual coupon payments?

Time Periods

Paying coupons twice a year, instead of once

doubles the total number of cash flows to be discounted

in the PV formula.

Discount Rate

Since the time periods are now half years, the discount rate is also

changed from the annual rate to the half year rate.

Financial management: lecture 4

Bond Yields

Current Yield - Annual coupon payments divided by bond price.

Yield To Maturity (YTM)- Interest rate for which the present value of the bond’s payments equal the market price of the bond.

ty

parcpn

y

cpn

y

cpnP

)1(

)(....

)1()1( 21

Financial management: lecture 4

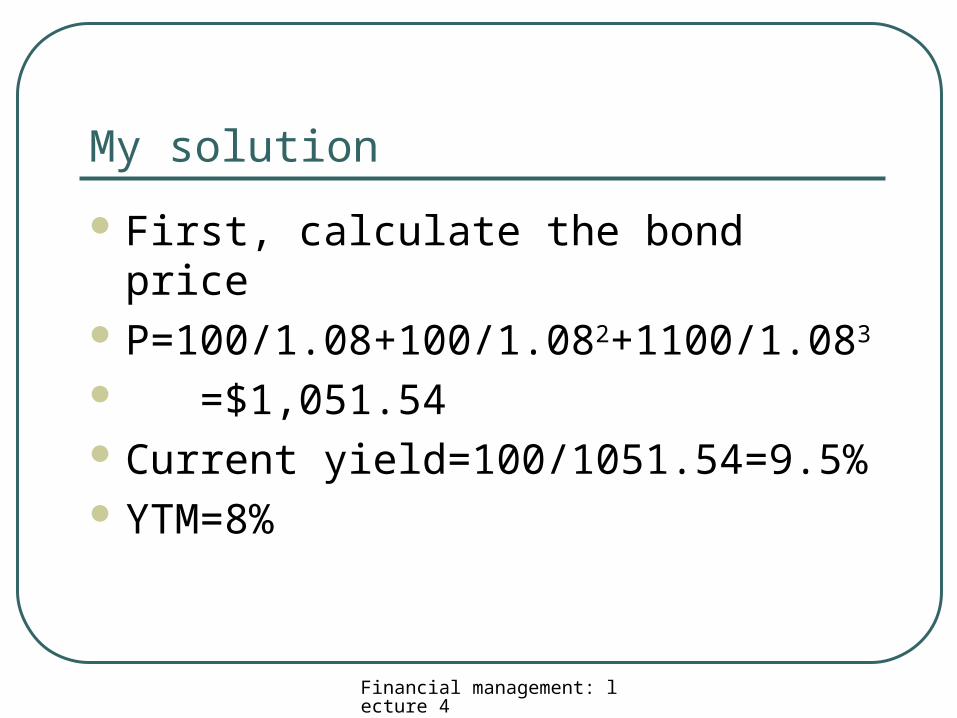

An example of a bond

A coupon bond that pays coupon of 10% annually, with a face value of $1000, has a discount rate of 8% and matures in three years. It is assumed that the market price of the bond is the same as the present value of the bond. • What is the current yield?

• What is the yield to maturity.

Financial management: lecture 4

My solution

First, calculate the bond price P=100/1.08+100/1.082+1100/1.083

=$1,051.54 Current yield=100/1051.54=9.5% YTM=8%

Financial management: lecture 4

Bond Yields

Calculating Yield to Maturity (YTM=r)

If you are given the market price of a bond (P) and the coupon rate, the yield to maturity can be found by solving for r.

ty

parcpn

y

cpn

y

cpnP

)1(

)(....

)1()1( 21

Financial management: lecture 4

Bond Yields

Example

What is the YTM of a 6 % annual coupon bond, with a $1,000 face value, which matures in 3 years? The market price of the bond is $1,010.77

77.010,1$

)1(

060,1

)1(

60

)1(

60321

PV

rrrPV

Financial management: lecture 4

Bond Yields

In general, there is no simple formula that can be used to calculate YTM unless for zero coupon bonds

Calculating YTM by hand can be very tedious. We don’t have this kind of problems in the quiz or exam

You may use the trial by errors approach get it.

Financial management: lecture 4

Bond Yields (3)

Can you guess which one is the solution in the previous example?

(a) 6.6%

(b) 7.1%

(c) 6.0%

(d) 5.6%

Financial management: lecture 4

The bond price, coupon rates and discount rates

If the coupon rate is larger than the discount rate, the bond price is larger than the face value.

If the coupon rate is smaller than the discount rate, the bond price is smaller than the face value.

Financial management: lecture 4

The rate of return on a bond

price bondor investmentchange price+incomeCoupon

=return of Rate

Example: An 8 percent coupon bond has a price of $110 dollars with maturity of 5 years

and a face value of $100. Next year, the expected bond price will be $105. If you

hold this bond this year, what is the rate of return?

investment ofcost

profit=return of Rate

Financial management: lecture 4

My solution

The expected rate of return for holing the bond this year is (8-5)/110=2.73%• Price change =105-110=-$5

• Coupon payment=100*8%=$8

• The investment or the initial price=$110

Financial management: lecture 4

The Yield Curve

Term Structure of Interest Rates - A listing of bond maturity dates and the interest rates that correspond with each date.

Yield Curve - Graph of the term structure.

Financial management: lecture 4

The term structure of interest rates (Yield curve)

Financial management: lecture 4

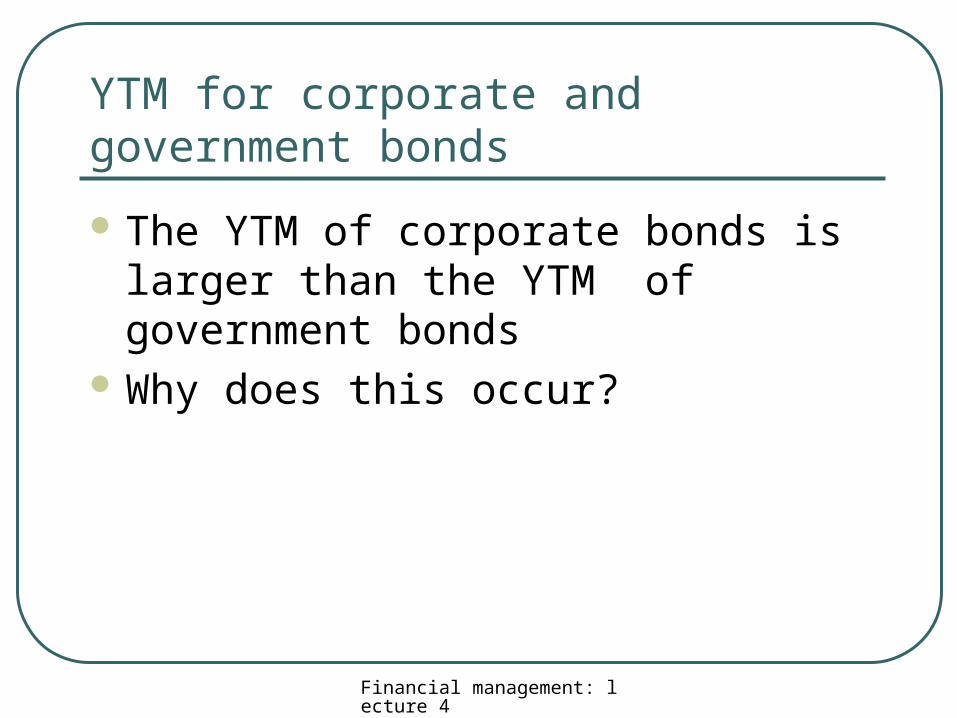

YTM for corporate and government bonds

The YTM of corporate bonds is larger than the YTM of government bonds

Why does this occur?

Financial management: lecture 4

Default Risk

Default risk• The risk associated with the failure of the

borrower to make the promised payments

Default premium• The amount of the increase of your discount

rate

Investment grade bonds Junk bonds

Financial management: lecture 4

Ranking bondsStandard

Moody' s & Poor's Safety

Aaa AAA The strongest rating; ability to repay interest and principalis very strong.

Aa AA Very strong likelihood that interest and principal will berepaid

A A Strong ability to repay, but some vulnerability to changes incircumstances

Baa BBB Adequate capacity to repay; more vulnerability to changesin economic circumstances

Ba BB Considerable uncertainty about ability to repay.B B Likelihood of interest and principal payments over

sustained periods is questionable.Caa CCC Bonds in the Caa/CCC and Ca/CC classes may already beCa CC in default or in danger of imminent defaultC C C-rated bonds offer little prospect for interest or principal

on the debt ever to be repaid.