financial management essentials for first nation …. financial management essentials. for . first...

TRANSCRIPT

1

Financial Management Essentialsfor

First Nation Health Managers

Terry Goodtrack, M.A. (P.Admin.), B.Admin., CGA, CAFM President & Chief Executive Officer, AFOA Canada

September 19, 2012, 11:00 – 12:30 a.m.

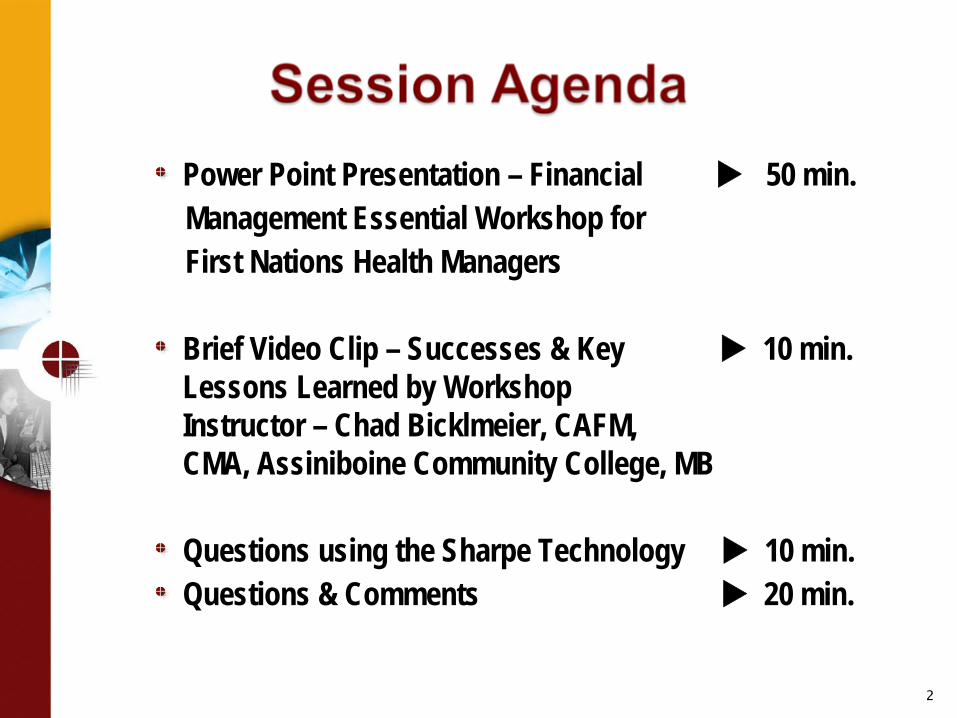

Power Point Presentation – Financial

50 min.Management Essential Workshop for First Nations Health Managers

Brief Video Clip – Successes & Key

10 min. Lessons Learned by Workshop Instructor – Chad Bicklmeier, CAFM, CMA, Assiniboine Community College, MB

Questions using the Sharpe Technology

10 min.Questions & Comments

20 min.

2

2011-2012 Health Canada, ON Region, funded the design & delivery of two 1 day workshops on Financial Management Essentials for First Nation Health Managers in Ontario

Worked with the Chiefs of Ontario and Grand Council Treaty 3 representatives to design the workshop

Delivered the workshops: Toronto – February 27, 2012 Kenora – March 19, 2012

Connected workshop content with the Financial Management and Accountability competency domain 5 from the First Nations Health Managers Competency Framework (July 2009)

3

1. Demonstrate an understanding of fiscal planning cycle and planning for the community.

2. Demonstrate an understanding of budgets and health service budgets.

3. Demonstrate awareness of accounting concepts and the process of evaluating, measuring and recording expenditures.

4

4. a) Interpret and present financial statements. b) Determine appropriate action to take to

address unexpected variances and balance the budget.

5. Demonstrate an understanding of Community and Health Canada reporting requirements.

6. Identify what needs to be done to prepare for the annual audit.

5

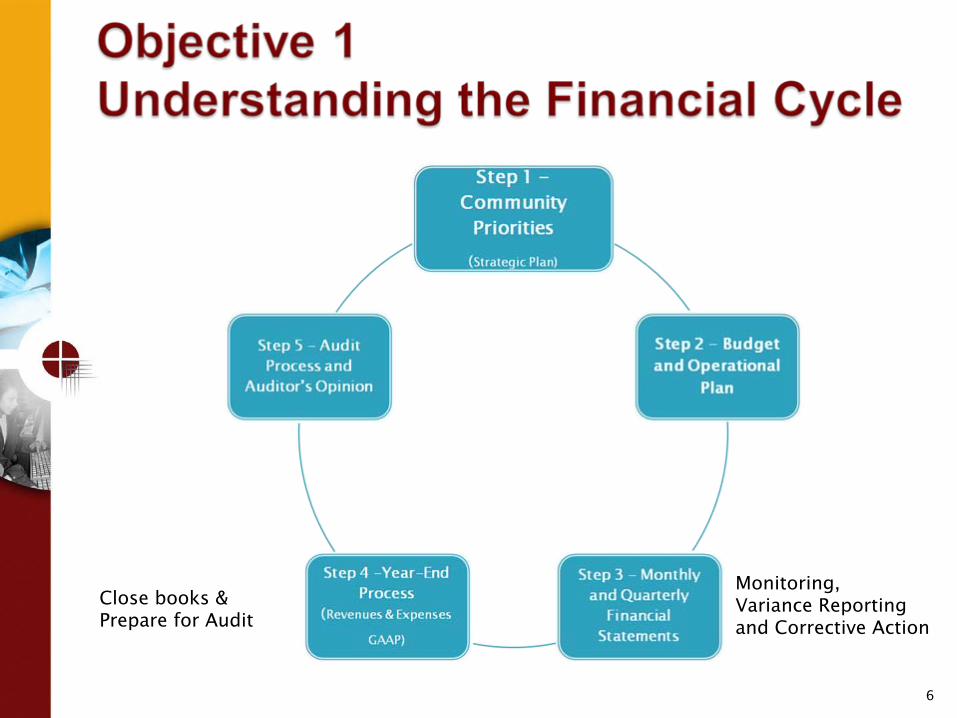

6

Monitoring, Variance Reporting and Corrective Action

Close books & Prepare for Audit

7

8

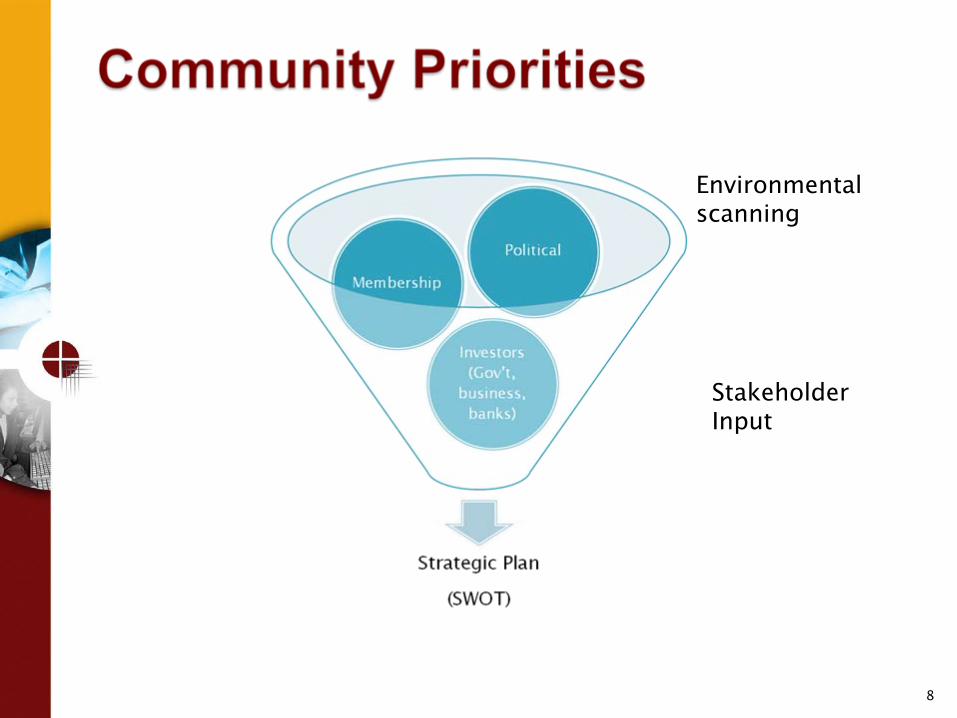

Environmental scanning

Stakeholder Input

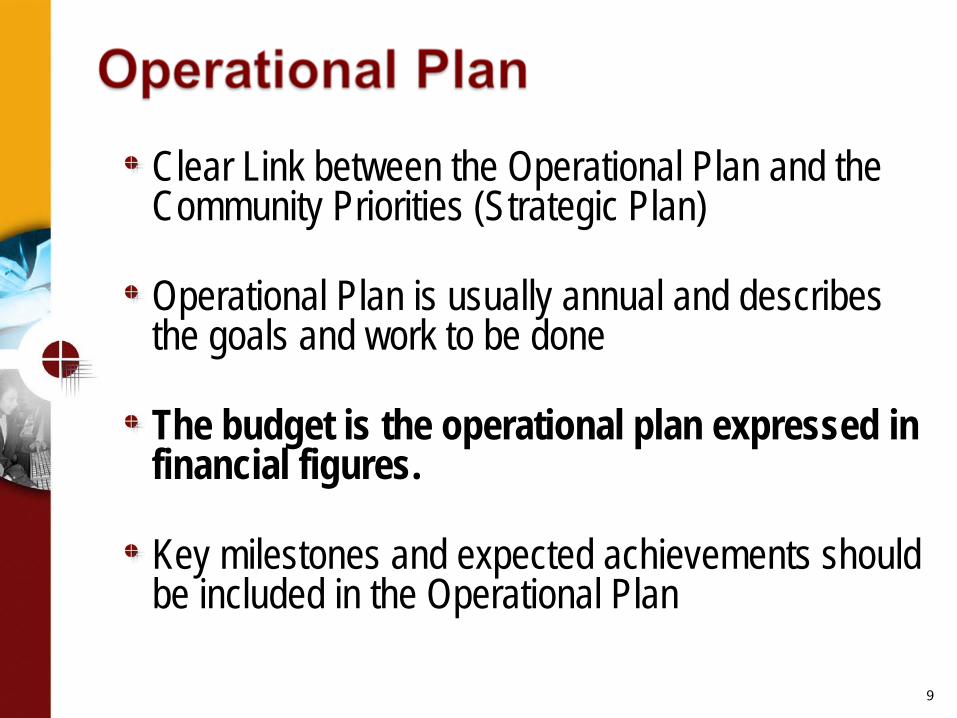

Clear Link between the Operational Plan and the Community Priorities (Strategic Plan)

Operational Plan is usually annual and describes the goals and work to be done

The budget is the operational plan expressed in financial figures.

Key milestones and expected achievements should be included in the Operational Plan

9

An overview of budgetingA few basic assumptionsPlanning the budgetThe budgeting processImplementationA sample budgetControls

10

11

At the start … it is a Plan…

What will your revenues (inputs) be?What will your expenses (outputs) be?

Will you have any money left over?Do you need more money to do what you want?

Do you have to change your plan?

12

During the year… it is a control…a gauge to monitor organizational

performance.

Did you get your expected revenues?Did you incur your expected expenses?

Do you have to change your plan?

13

When to StartSet GoalsDetermine needed resourcesDetermine costs of resourcesDetermine what funding is availableUse community priorities and funder deliverables to make choices.◦

What can/should we do?

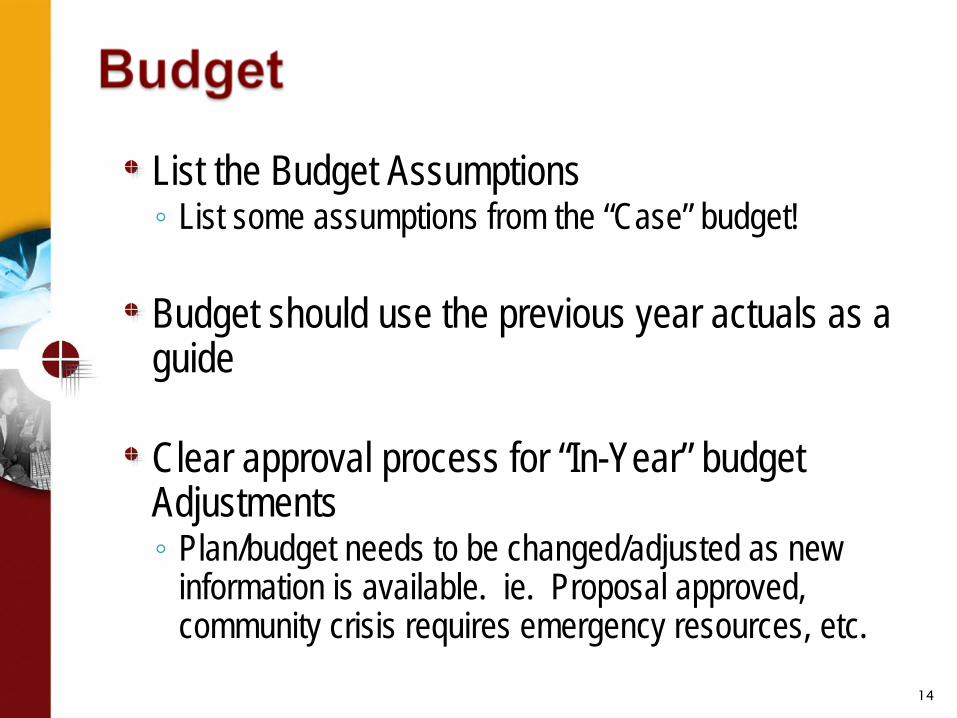

List the Budget Assumptions◦

List some assumptions from the “Case” budget!

Budget should use the previous year actuals as a guide

Clear approval process for “In-Year” budget Adjustments ◦

Plan/budget needs to be changed/adjusted as new information is available. ie. Proposal approved, community crisis requires emergency resources, etc.

14

Budget is a financial plan to control future operations and results

Budget allocates funds to achieve objectives

Annual and Multi-year Budgets

Important to have a budget development and approval Process ◦

(decision makers must be “vested” in process!!)

15

1616

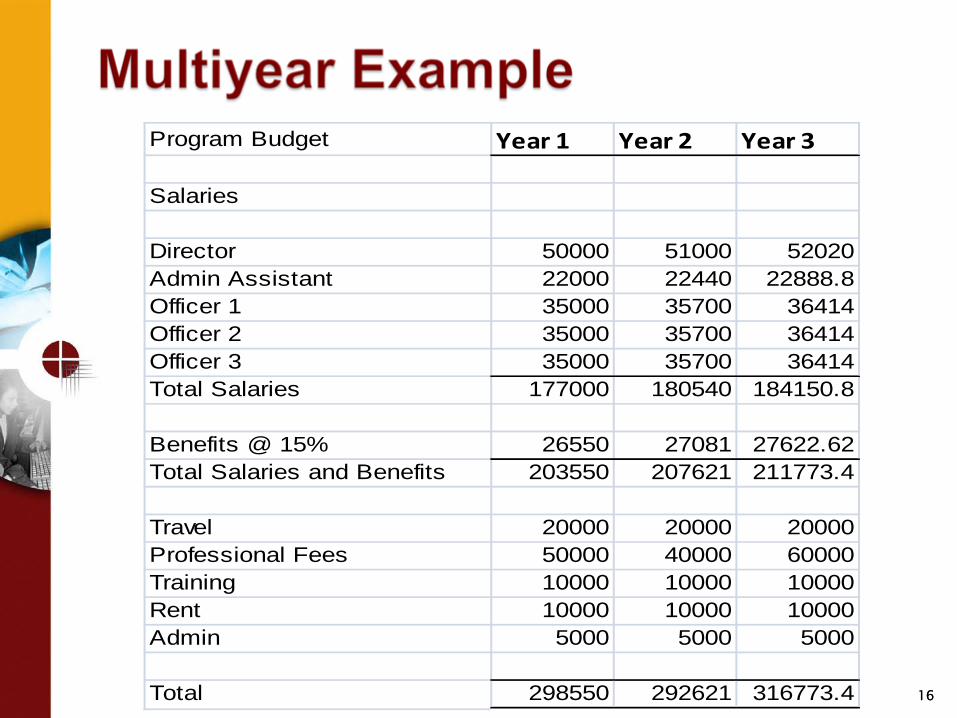

Program Budget Year 1 Year 2 Year 3

Salaries

Director 50000 51000 52020Admin Assistant 22000 22440 22888.8Officer 1 35000 35700 36414Officer 2 35000 35700 36414Officer 3 35000 35700 36414Total Salaries 177000 180540 184150.8

Benefits @ 15% 26550 27081 27622.62Total Salaries and Benefits 203550 207621 211773.4

Travel 20000 20000 20000Professional Fees 50000 40000 60000Training 10000 10000 10000Rent 10000 10000 10000Admin 5000 5000 5000

Total 298550 292621 316773.4

What is Accounting?Accrual basis vs. cash basis accountingAccounting TerminologyAccounting Concepts

17

18

Accounting is the process of recording, measuring, interpreting, and communicating financial data.

Accountants are guided by Generally Accepted Accounting Principles (GAAP) in order to achieve this goal. GAAP are the guidelines, rules, and procedures used in recording and reporting accounting information in audited financial statements.

19

CASH BASIS

Revenue recognized only when funds receivedExpenses recognized only when payments madeEntries made only when a deposit is made or a cheque is writtenLearn how much money is available today

20

ACCRUAL BASIS

Looks at cash available todayConsiders funds owed by setting up items as receivablesConsiders funds to be paid to others by setting up items as payablesAll First Nations are required to use the accrual basis to record and report financial information.

The Matching Principle – Revenues recognized in same period as expenses incurred; unused revenue deferred

The Recognition Principle – two of many rules: (1) Revenues recognized when organization has met requirements to receive the funding (2) Expenses are recognized when they are incurred

Full Disclosure Principle – Requires all situations, circumstances & events relevant to financial statement users have to be disclosed

21

Each user has different information needs... Dependent on their use of the information –the decisions they have to make.

22

Reporting should not be limited to FNIHB/HC format & requirements.

23

Aboriginal Affairs and Northern Development Canada (AANDC) requires First Nations to prepare financial statements in accordance with the Public Sector Accounting (PAS) Handbook.

Effective January 1, 2009, GAAP for local governments will be the same as the current standards for senior government levels.

24

The statement of operations presents the results of the organization’s activities over a

given period of time.

The statement of operations is based on the equation:

Revenues - Expenses = Surplus/(Deficit)

25

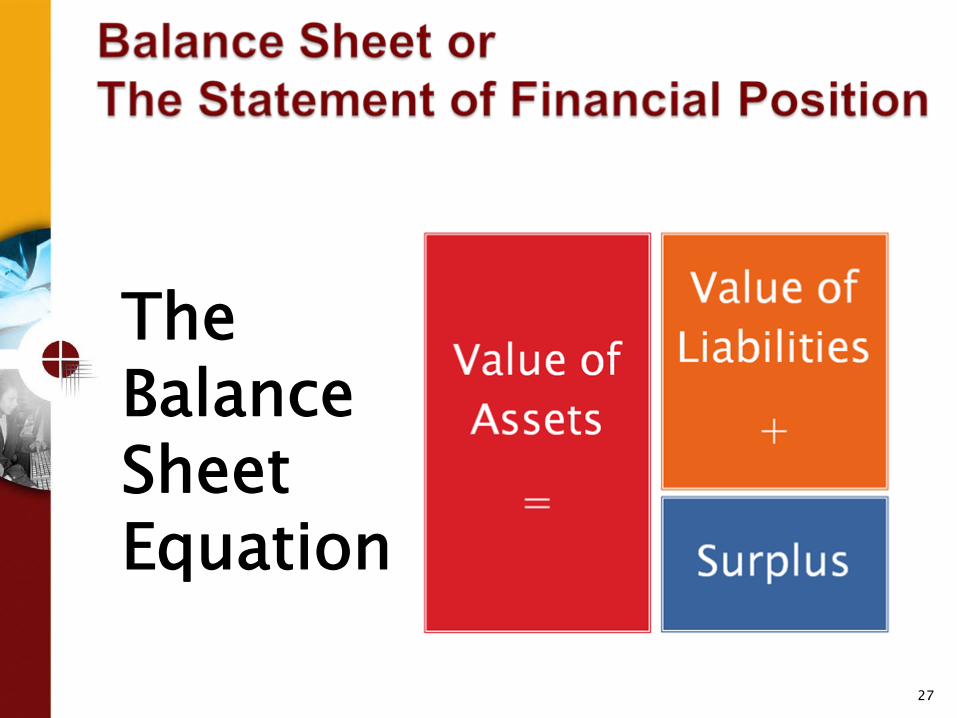

What Business Owns = Others Own + Owners Own

Assets = Liabilities + Equity

26

27

The Balance SheetEquation

Assets are economic resources controlled by an entity as a result of past transactions from

which future economic benefits may be obtained.

GAAP s1000.29

28

Liabilities are obligations of an entity arising from past transactions or events, the settlement of which may result in the transfer or use of assets, provision of services or other yielding of economic benefits in the future.

GAAP s1000.32

29

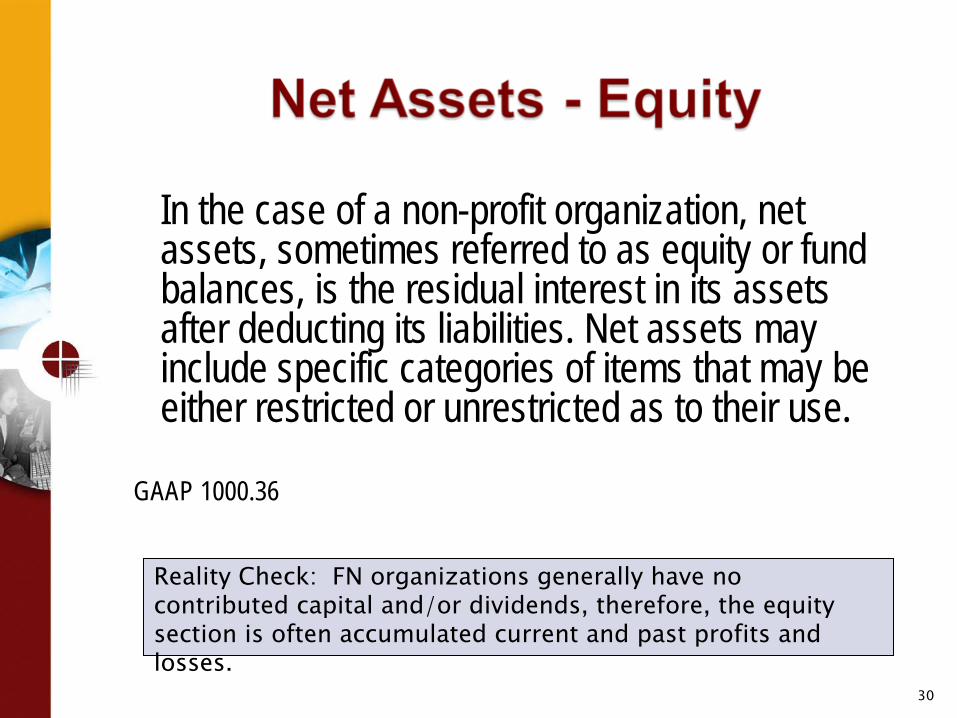

In the case of a non-profit organization, net assets, sometimes referred to as equity or fund balances, is the residual interest in its assets after deducting its liabilities. Net assets may include specific categories of items that may be either restricted or unrestricted as to their use.

GAAP 1000.36

30

Reality Check: FN organizations generally have no contributed capital and/or dividends, therefore, the equity section is often accumulated current and past profits and losses.

3131

FIRST NATIONBALANCE SHEET

Year ending March 31 2012 2011 Change

Cash 1,000 23,000 (22,000)

Accounts receivable 353,000 317,000 36,000

Prepaid Expenses 30,000 30,000 -

Total current assets 384,000 370,000 14,000

Total fixed assets 535,000 485,000 50,000

Less accumulated depreciation (70,000) (35,000) (35,000)

Net property, plant & equipment 465,000 450,000 15,000

Total assets 849,000 820,000 29,000

Accounts payable 150,000 190,000 (40,000)

Deferred revenues 100,000 100,000 -

Total current liabilities 250,000 290,000 (40,000)

Long-term debt 124,000 100,000 24,000

Deferred contributions related to

fixed assets 300,000 330,000 (30,000)

Total long-term liabilities 424,000 430,000 (6,000)

Total liabilities 674,000 720,000 (46,000)

Net assets/(deficiency) 175,000 100,000 75,000

Total liabilities and net assets 849,000 820,000 29,000

Comparison to budget Variance reportingForecastingAnalysisRecommendations◦

Curb spending◦

Budget adjustments◦

Change of goals

32

Listing of “significant” variances◦

Based on percentage and dollar value (i.e.)

20% or

$10,000

33

Negative Variance

Dept 6 – Health Careers◦

Small amounts created a variance over 20%◦

Dollar variance $$$

Dept 3 – Mental Health Unit◦

Expenses exceed funding, this is an annual challenge.◦

No funding increases since XXXX◦

$$,$$$ deficit is expected

Dept 101 – ADI Conference◦

Monies flowing slower than expenses◦

No deficit is expected.◦

We need to get more funding released.

34

Positive Variance

Dept 17 – Nursing (Transfer)◦

Wages increased by X%◦

Retro pay and overtime payout increased expenses by $,$$$ and $$,$$$◦

Surplus expected to be $$,$$$ to be used to offset underfunding in XXXX program(s).

Dept 19 – E Health◦

Wages to be allocated from Nursing Secretary ◦

No Surplus is expected.

Dept 118 – NNADAP◦

Funding received for training◦

ASSIST training planned◦

No surplus is expected.

35

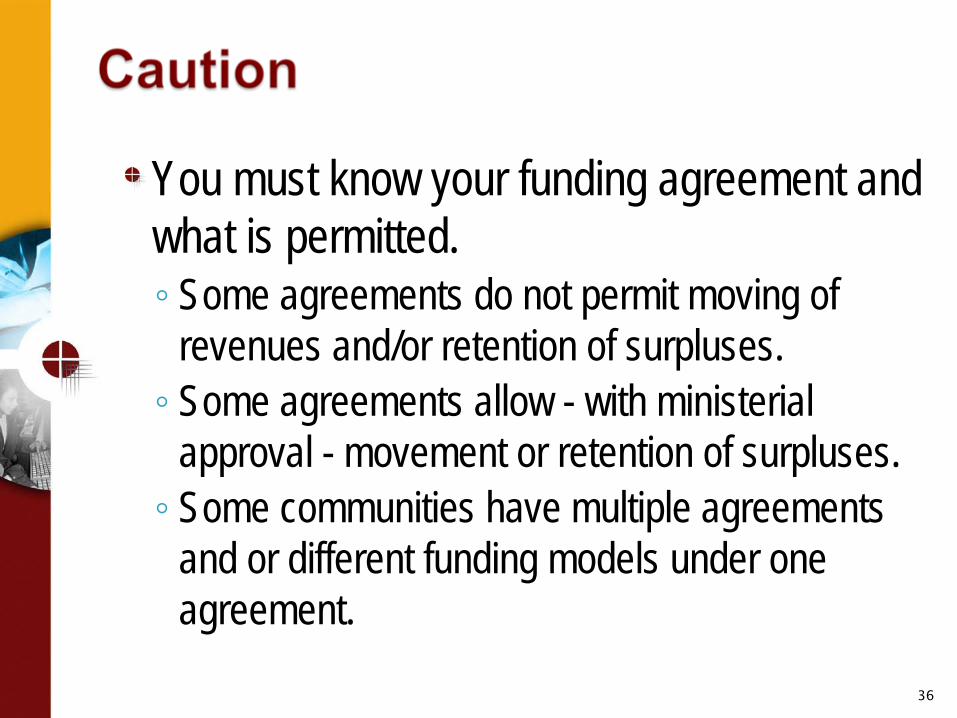

You must know your funding agreement and what is permitted.◦

Some agreements do not permit moving of revenues and/or retention of surpluses. ◦

Some agreements allow - with ministerial approval - movement or retention of surpluses.◦

Some communities have multiple agreements and or different funding models under one agreement.

36

These financial statements (including appropriate expense allocations) are the responsibility of Band’s (Health Department’s) management.

Source: Auditor’s Report

37

39

40

41

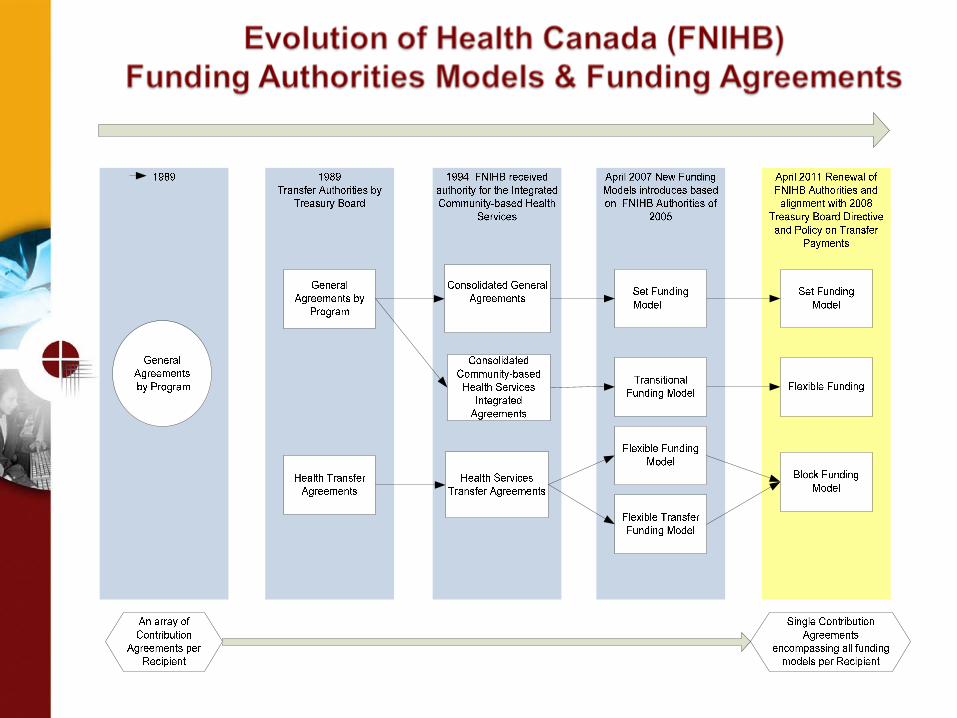

Duration: up to three (3) years

Movement of Resources: resources are to be used as indicated in the CA. However, should it be necessary, funds can be redirected among Programs and Services within a single sub-sub activity upon obtaining written approval of the Minister ◦

Note program exceptions: IRS/ NIHB/ HSIF

Surplus/Carry Forward: No retention of surplus and no carry forward for this funding model

Planning: • Project (corporate): Recipient delivers project based on Proposal/work plan which includes objectives and

activities as per the Terms & Conditions of the FNIHB Program Authorities• Community Based: Recipient must deliver programs and services as per the First Nations and Inuit Health

Branch Program Plan

42

Duration: two (2) to five (5) years (minimum 24 months)◦

ONTARIO REGION RECOMMENDATION 3 YEARSMovement of Resources: should it be necessary, funds can be redirected among sub- activity levels within an Activity (Authority) ◦

NOTE – no prior approval requiredCarry Forward: recipient has the ability to carry forward funds to the next fiscal year with

a plan and written approval of MinisterSurplus: No retention of surplus Planning:• Project (corporate): Recipient delivers project based on a Proposal/work plan which includes

objectives and activities as per the Terms & Conditions of the FNIHB Program Authorities• Community Based: Recipient delivers programs based on a Multi Year Work Plan; plan must be

updated to reflect changes – revised plan must be approved

43

(Currently only available for use with Community Based Agreements)

Planning: A comprehensive Health Plan must be provided which will serve as a basis for reporting; to be updated as changes occur – revised plan must be approvedMovement of Resources: Recipients are able to reallocate funds across all Activities (Authorities)

Block - FlexibleSurplus: recipients are allowed to retain surpluses as per their Health Plan ◦

(NOT APPLICABLE TO SET FUNDING)Duration: five (5) yearsMandatory Programs: recipients must ensure the provision of mandatory programs/services (Nursing is optional)

Block - Flexible TransferSurplus: recipients are allowed to retain surpluses as per their health priorities Duration: five (5) to ten (10) yearsMandatory Programs: recipients must ensure the provision of mandatory programs/services including:◦

Nursing, Professional Supervisory and Program Advisory functions

44

45

46

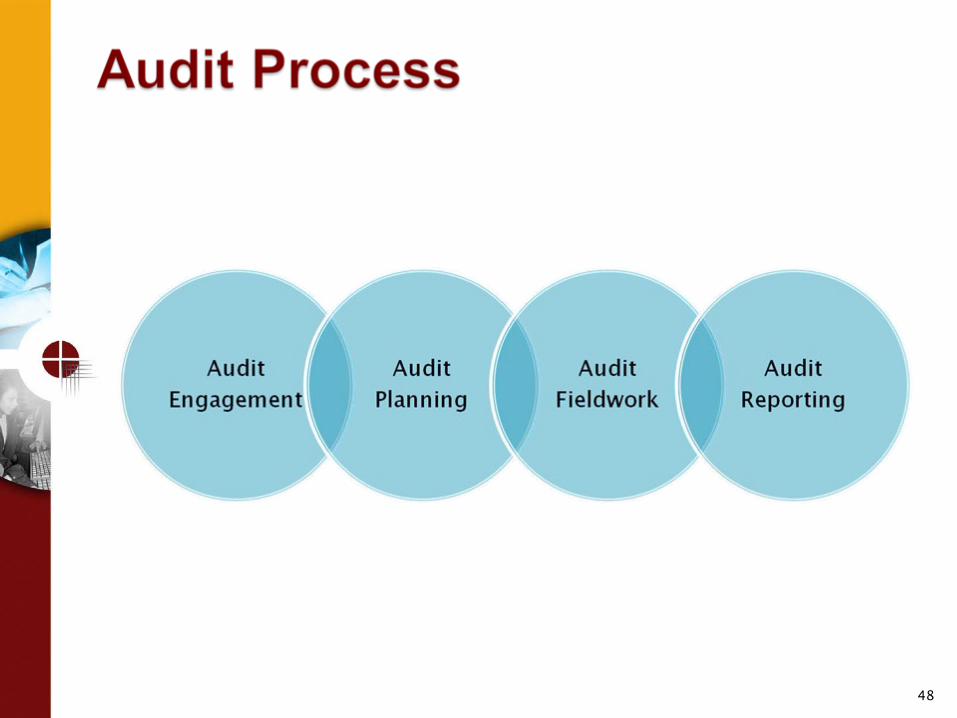

Financial Audit (focus of this discussion)Compliance AuditSpecial AuditValue for Money AuditForensic Audit

47

48

Expression of an OpinionAre financial statements presented fairlyAre financial Statements in conformity with GAAPThe audit is conducted by an independent auditor

49

The audit is conducted by an independent auditorGain an understanding of the organization.Establish the level of risk and materiality.Select a sample of transactions based on the level of risk.Perform tests on the sample transactions.Make observations of the operations of the organizationExpress an opinion based on the results of the tests and observations.

50

Unqualified (or clean) opinionUnqualified opinion with an explanationQualified opinionAdverse OpinionDisclaimer of Opinion

51

Prepared by auditorInforms client of recommendations to improve business processes or controlsDiffers from management representation letter

52

For more information please contact:

Dr. Paulette Tremblay, Ph.D. (Education), MA (Education),B.ED, BA (Sociology), ICD.D - Director of Education & Training, AFOA Canada [email protected]

Sheila Howard - Project & Event [email protected]

Telephone: 1-866-722-2362 www.afoa.ca53