financial long range planning dr. bruce capron honeoye falls – lima central school district...

TRANSCRIPT

Financial Long Range Planning

Dr. Bruce CapronHoneoye Falls – Lima Central School District

Livonia Central School District

Overview

Present a model budget Identify key drivers of budget increases Generate forecasts Consider reserve spending and

sustainability Simulate the impact of changes over five

years Summarize

Purpose of Multi-year Budgeting

Generate focus on the things that matter.

Make common sense of the obvious.

Understand how today’s decisions propagate forward.

Anticipate icebergs.

Plan soft landings

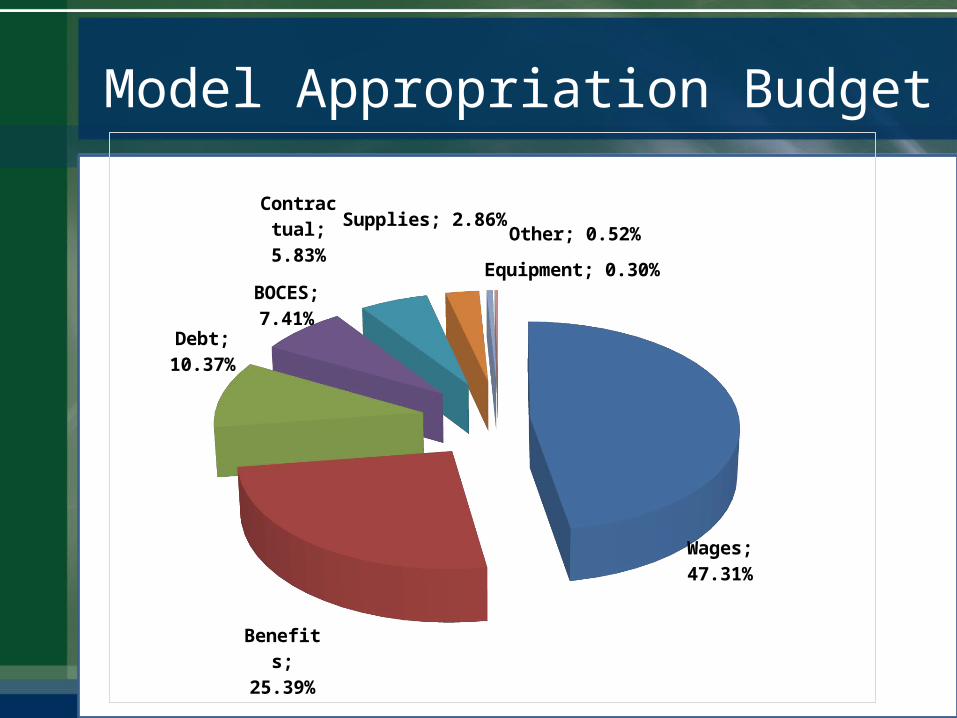

Model Appropriation Budget

Wages; 47.31%

Benefits; 25.39%

Debt; 10.37%

BOCES; 7.41%

Con-tractual;

5.83%Supplies; 2.86%

Other; 0.52%

Equipment; 0.30%

Size and Sensitivity

Budget Component

Percent of Budget

Change Impact on Budget

Required Increase in

LevyWages 47% 2% 0.94% 1.62%

Health Care 12.2% 8% 0.97% 1.68%

Debt Service 10.4% 1% 0.10% 0.18%Contractual + BOCES Expenses 8.3% 1% 0.08% 0.14%

TRS Pension 6.0% 2 Points 0.73% 1.27%

ERS Pension 2.2% 2 Points 0.21% 0.37%Other Employer Expenses 5.0% 2% 0.10% 0.17%

Energy 2.6% 5% 0.13% 0.22%

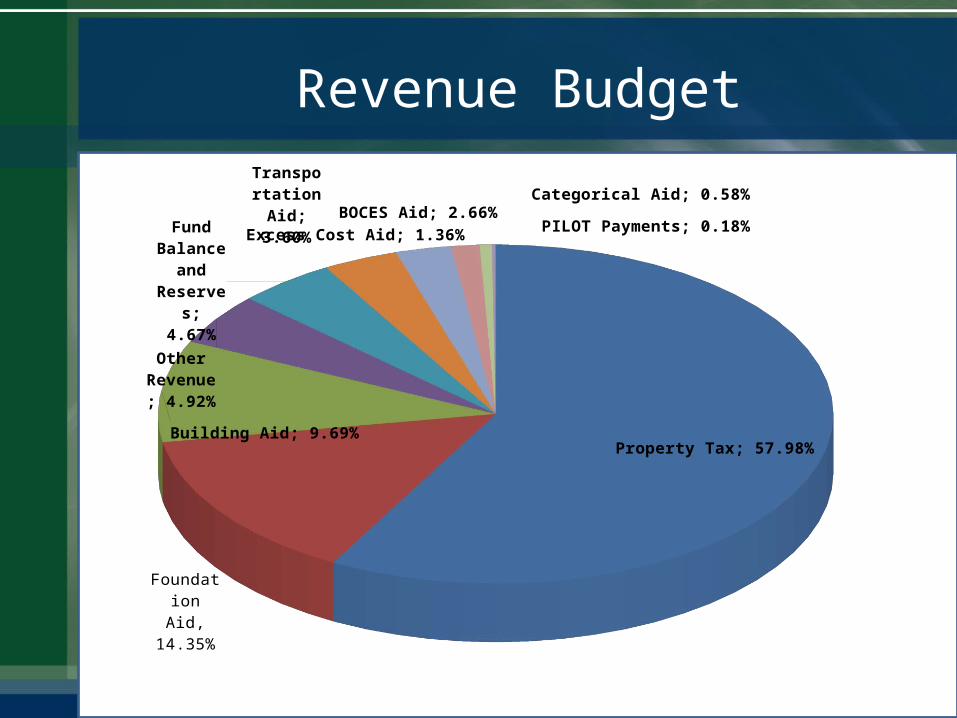

Revenue Budget

Property Tax; 57.98%

Foundation Aid, 14.35%

Building Aid; 9.69%

Other Revenue;

4.92%

Fund Balance and Re-serves; 4.67%

Trans-portation

Aid; 3.60%

BOCES Aid; 2.66%Excess Cost Aid; 1.36%

Categorical Aid; 0.58%

PILOT Payments; 0.18%

Revenue Budget

Property Tax; 57.98%

Foundation Aid, 14.35%

Building Aid; 9.69%

Other Rev-

enue; 4.92%

Fund Balance and Re-serves; 4.67%

Transportation Aid

BOCES Aid Excess Cost Aid Textbook, Software, Library, Hardware

PILOT Payments; 0.18%

Revenue Assumptions

Expense Driven Aid formulas remain unchanged.

Foundation + GEA Aid increase at 2X the CPI

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

CPI

20122013

Balancing the Budget

1. Gap = Budgeted Revenue + Reserves - Budgeted Expenses

2. What increase in the levy balances the budget?

3. Is this levy increase above the tax cap?

0.25%

0.75%

1.25%

1.75%

2.25%

2.75%

Levy Increase

Tax Cap Limit

Budget Increase

Perc

ent C

hang

e

Salary and Wages

Salaries and Wages

Consider a 2.5% annual wage increase

14-15 15-16 16-17 17-18 18-19

Levy Increase 0.0165653317566756 0.0149982434592269 0.0152832483282598 0.0148991932762118 0.0148930097363623

Tax Cap Limit 0.021634933405384 0.0251625199787012 0.0251615961447265 0.0251606689264575 0.025159778278335

Budget Increase 0.0148114322782486 0.0149594040342751 0.0151066621480497 0.0152531675459986 0.0153988820065604

0.25%

0.75%

1.25%

1.75%

2.25%

2.75%

Perc

ent C

hang

e

Retirements and Breakage

Retire without Rehiring Salary = $ 85,000 TRS = $ 13,813 FICA and Medicare = $ 6,522 Total $105,315

Retire and rehire an early career teacher Salary = $ 40,000 TRS = $ 6,500 FICA and Medicare = $ 3,600 Total $ 49,560

Breakage = $ 55,755

Employee Demographics(Minimal Upcoming Retirements)

1 2 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 29 30 32 350

2

4

6

8

10

12

14

16

18

20

Years of Service

Teac

her C

ount

Employee Demographics(Significant Upcoming Retirements)

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 320

2

4

6

8

10

12

Years of Experience

Teac

her C

ount

Other Factors

Review enrollment projections and carefully consider whether the position will be replaced.

If you are rehiring for this position:

What experience level is complimentary to your other staff?

Are you seeking second career teachers that have private sector experience?

What hiring practice will smooth annual breakage?

Salary Projections

Project 2.5% wage increase Assume 1.0% savings from breakage

14-15 15-16 16-17 17-18 18-19

Levy Increase 0.00638198559023331

0.00462648814412841

0.0047069951519886 0.00410022986028107

0.00386795759254989

Tax Cap Limit 0.021634933405384 0.0251631526038818 0.0251628617746268 0.0251625672707866 0.0251623117781729

Budget Increase 0.00890669539770408

0.00896024173446681

0.00901363281250119

0.0090668634519001 0.00911992853915222

0.25%

0.75%

1.25%

1.75%

2.25%

2.75%

Perc

ent C

hang

e

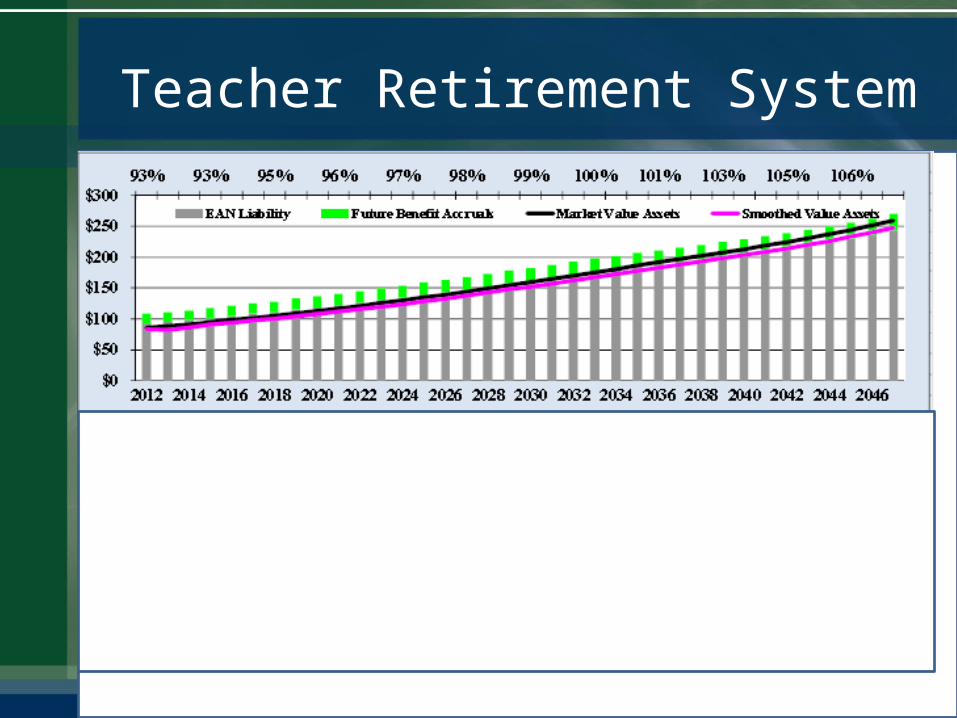

Teacher Retirement

System

Teacher Retirement System

TRS Employer Contribution Rate

Normal Rate

15.85%

Expense Rate

0.27%

Group Life Insurance Rate

0.13%

Excess Benefit Plan Rate 0. 0%

16.25%

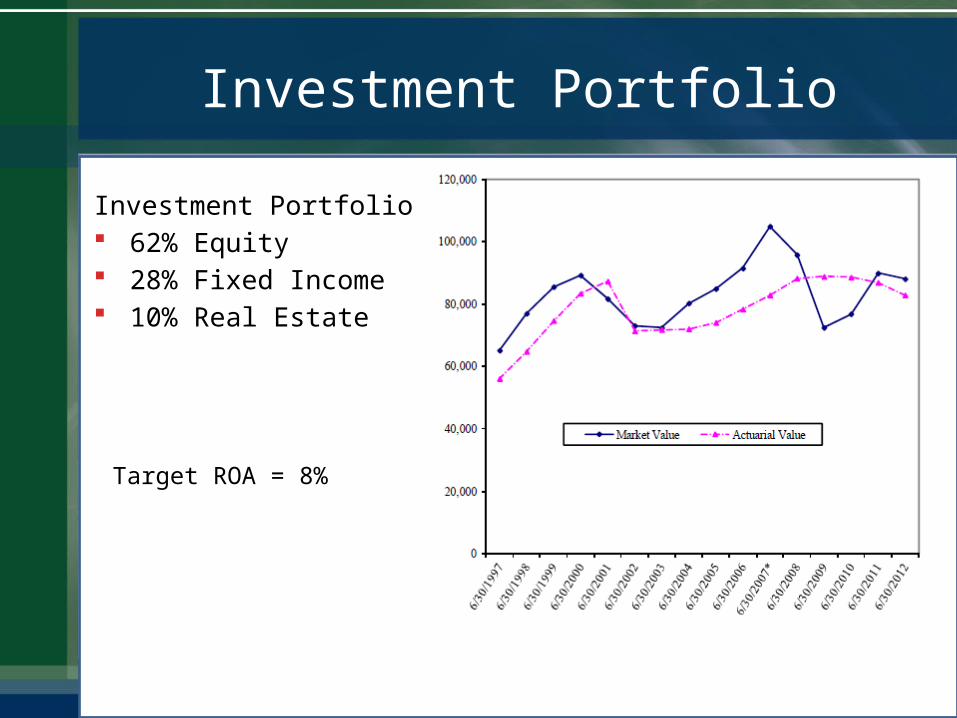

Investment Portfolio

Investment Portfolio 62% Equity 28% Fixed Income 10% Real Estate

Target ROA = 8%

TRS

Calculation of Normal Rates

Normal Rate = Total Liabilities – (Assets + Receivables)

Present Value of Future Salaries

Normal Rate = 108.2 billion – (82.8 billion + 3.6 billion)

138.2 billion

Normal Rate = 15.85%

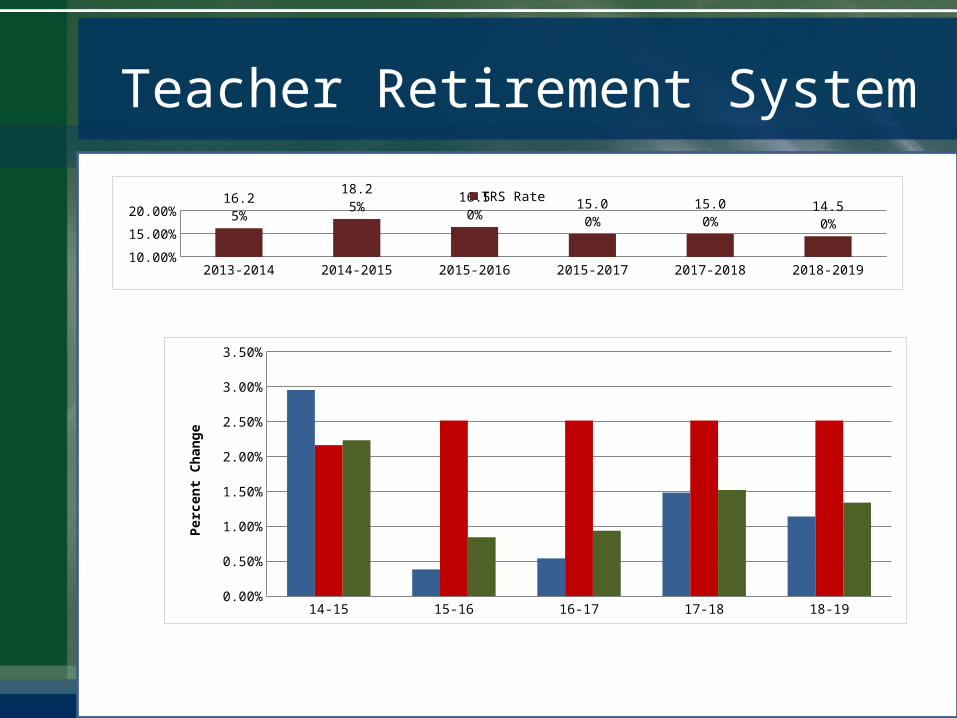

Teacher Retirement System

Teacher Retirement System

Teacher Retirement System

2013-2014 2014-2015 2015-2016 2015-2017 2017-2018 2018-201910.00%15.00%20.00%25.00%30.00%

16.25%

18.25%

18.60%

19.00%

20.00%

25.00%

TRS Rate

14-15 15-16 16-17 17-18 18-19

Levy Increase 0.0295408235236754

0.017384993444476

0.0180312091243687

0.0216287746429795

0.0480042998314389

Tax Cap Limit 0.021634933405384

0.0251617320279464

0.0251606771559874

0.0251596024517162

0.0448794199870425

Budget In-crease

0.0223351738389839

0.0163533832576127

0.0167144458146037

0.0191882089007291

0.0348174972334854

0.50%

1.50%

2.50%

3.50%

4.50%

5.50%

Perc

ent C

hang

e

Teacher Retirement System

Teacher Retirement System

2013-2014 2014-2015 2015-2016 2015-2017 2017-2018 2018-201910.00%

14.00%

18.00%16.25

%

18.25% 16.50

% 15.00%

15.00%

14.50%

TRS Rate

14-15 15-16 16-17 17-18 18-19

Levy Increase 0.0295408235236754

0.00382081736213266

0.00540576420350486

0.0148163673130363

0.0114135906330638

Tax Cap Limit 0.021634933405384

0.0251617320279464

0.0251614970589161

0.0251611664077385

0.0251602733752714

Budget In-crease

0.0223351738389839

0.00843286260846523

0.00936545297555171

0.0152068936156363

0.013387572844555

0.25%

0.75%

1.25%

1.75%

2.25%

2.75%

3.25%

Perc

ent C

hang

e

Employee Retirement

Pension

ERS Pension

Short Term Fixed Income4%

Government Bonds17%

Corporate Bonds

7%

Domestic Equity35%International Equity

16%

Private Equity9%

Real Estate7%

Other4%

Investment Portfolio

$160 billion 60% Equity 30% Fixed Income 10% Real Estate

• Return of 10.4% (3/13)

• 498,000 Active Members• 381,000 Retirees

Employee Retirement System

2013-2014 2014-2015 2015-2016 2015-2017 2017-2018 2018-201910.00%15.00%20.00%25.00%

21.90%

21.00%

21.00%

21.90%

21.90%

21.90%

ERS Rate (%)

14-15 15-16 16-17 17-18 18-19

Levy Increase 0.0149471430331683

0.0149822971855647

0.0152676034478901

0.0148827741311061

0.0148764167592928

Tax Cap Limit 0.021634933405384

0.0251626196579063

0.0251616953202828

0.0251607675454957

0.0251598764182867

Budget In-crease

0.0138731376863528

0.0149501119083238

0.0150974156431031

0.0152439691011229

0.0153897340064018

0.25%

0.75%

1.25%

1.75%

2.25%

2.75%

Perc

ent C

hang

e

Health Care Costs

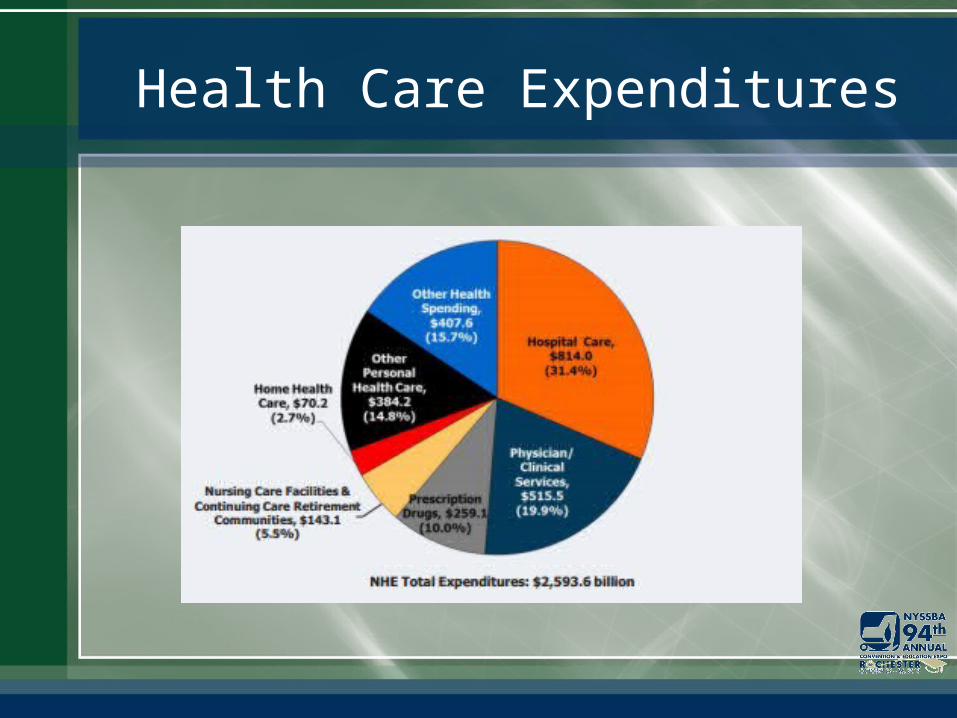

Health Care Expenditures

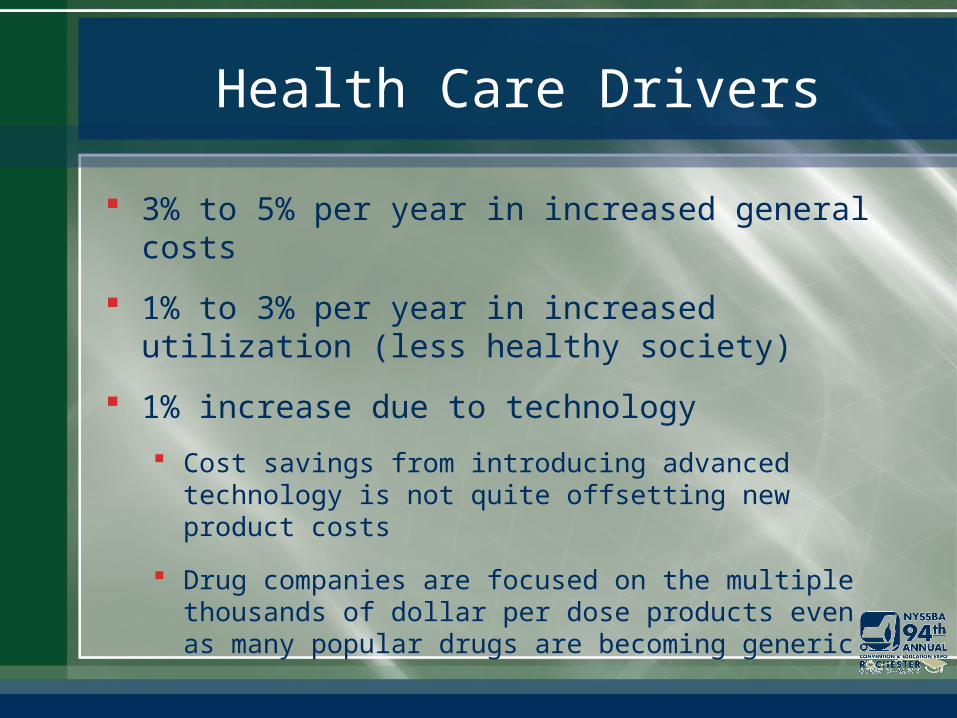

Health Care Drivers

3% to 5% per year in increased general costs

1% to 3% per year in increased utilization (less healthy society)

1% increase due to technology

Cost savings from introducing advanced technology is not quite offsetting new product costs

Drug companies are focused on the multiple thousands of dollar per dose products even as many popular drugs are becoming generic

Health Care Growth(Average Annual Change in National Health Care Expenditures)

Why is the apparent rate of Health Care Inflation Slowing?

Health Care Inflation is driven by the macro economy. Key influencers are:

1. Inflation rate this year and inflation rate in the preceding two years.

2. Real GDP growth this year and real GDP growth in the preceding five years

Result 77% of the historical health care costs are

explained by these macro-economic factors.

Health Care Projections

Health Insurance

2013-2014 2014-2015 2015-2016 2015-2017 2017-2018 2018-20195.0%

7.0%5.5%

6.5% 7.0% 7.5% 7.7% 7.5%Health Insurance Increase (%)

14-15 15-16 16-17 17-18 18-19

Levy Increase 0.0331915119753 0.0192769283000214

0.0223204476364974

0.0228344077073418

0.0228226474956898

Tax Cap Limit 0.021634933405384 0.0251615139034275

0.0251603505305768

0.0251590328900456

0.0251577150021555

Budget In-crease

0.0262001235005286

0.0202614277214254

0.022213744203463 0.0229341157874647

0.0231290999431066

0.25%

0.75%

1.25%

1.75%

2.25%

2.75%

3.25%

Perc

ent C

hang

e

Why not hope for low health care inflation?

Both health care and pension costs correlate with multi-year trailing averages that largely follow the economy.

Health care and pension costs tent to move in opposite directions

Low Health Care inflation -> Higher pension costs Higher Health Care inflation -> Lower pension costs

What’s Worse?

What is more challenging to the budget? $1 million in additional pension costs

or $1 million in additional health care

costs?

Health Care – the tax cap doesn’t go up with the cost of health insurance.

Energy, Contractual and

Supply Expenses

Natural Gas

19901992

19941996

19982000

20022004

20062008

20102012

20142016

20182020

20222024

20262028

20302032

20340.00

2.00

4.00

6.00

8.00

10.00

12.00 Natural Gas Forecast

Henry Hub Lower 48 Wellhead

$ /

MBT

U

Energy Information Administration www.eia.gov

Energy, Supply Contractual Expenses

2013-2014 2014-2015 2015-2016 2015-2017 2017-2018 2018-20191.00%1.50%2.00%2.50% 2.00%

1.65%2.00% 2.00% 2.00% 2.00%

Energy, Supplies, and Contractual Costs

14-15 15-16 16-17 17-18 18-19

Levy Increase 0.0185049500517156

0.0160469957199496

0.0159024317982054

0.0153219626852172

0.0151120451857229

Tax Cap Limit 0.021634933405384 0.0251624009170368

0.0251614153846226

0.0251604540187132

0.0251595417226603

Budget In-crease

0.0176842307457126

0.0183953033744516

0.0184968027859867

0.0185970860319208

0.0186961494918602

0.25%

0.75%

1.25%

1.75%

2.25%

2.75%

Perc

ent C

hang

e

Putting it All Together

Putting it all Together

Wages increase: 2.5%

Health Care increases: 6.5%-> 7.0% -> 7.5% -> 7.7% -> 7.5%

Pension costs follow projections TRS: 16.25% -> 18.25% -> 18%...

ERS: 21.9% -> 20.9% -> 20.9% ….

Energy, contractual expenses and supplies increase with the CPI CPI: 1.65% -> 2%...

Putting it all together

14-15 15-16 16-17 17-18 18-19

Levy Increase 0.0456099405140696 0.0319014398085219 0.0348757822276063 0.035290866754894 0.0351925840599098

Tax Cap Limit 0.021634933405384 0.0251607833193116 0.025158904190814 0.0251569190929246 0.0251549788419394

Budget Increase 0.0321691086441836 0.0261403934224605 0.028042775042416 0.0286929095046975 0.0288186718462718

0.25%

0.75%

1.25%

1.75%

2.25%

2.75%

3.25%

3.75%

4.25%

4.75%

Perc

ent C

hang

e

What do you do?

First, count the breakage from retirements.

Second, hope the legislative budget contains additional aid.

Impact of 1% Breakage

14-15 15-16 16-17 17-18 18-19

Levy Increase 0.0353157913911061 0.0219090910936982 0.0250629958209302 0.0256850251074979 0.0257853549515859

Tax Cap Limit 0.021634933405384 0.0251613876881028 0.0251600715745047 0.025158602812461 0.0251571352910752

Budget Increase 0.0262001235005286 0.0202614277214254 0.022213744203463 0.0229341157874647 0.0231290999431066

0.25%

0.75%

1.25%

1.75%

2.25%

2.75%

3.25%

3.75%

Perc

ent C

hang

e

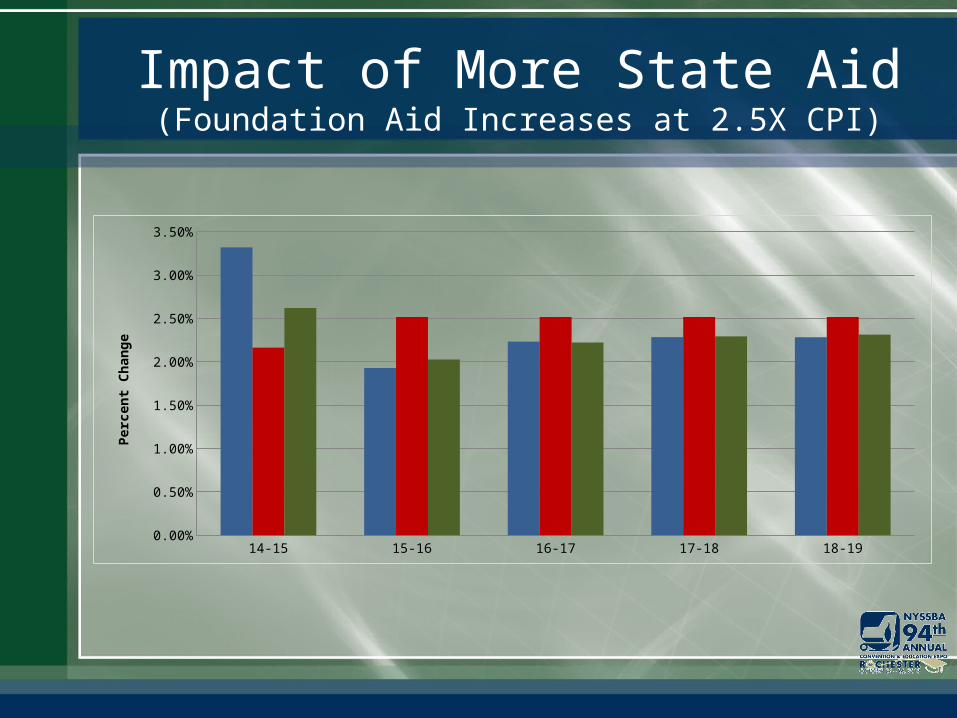

Impact of More State Aid(Foundation Aid Increases at 2.5X CPI)

14-15 15-16 16-17 17-18 18-19

Levy Increase 0.0331915119752998 0.019276928300022 0.0223204476364969 0.0228344077073412 0.022822647495716

Tax Cap Limit 0.021634933405384 0.0251615139034275 0.0251603505305768 0.0251590328900456 0.0251577150021555

Budget Increase 0.0262001235005286 0.0202614277214254 0.022213744203463 0.0229341157874647 0.0231290999431066

0.25%

0.75%

1.25%

1.75%

2.25%

2.75%

3.25%

Perc

ent C

hang

e

Reserves and Fund Balance

Reserves and Fund Balance

Fund Balance Excess of Revenues over Appropriations.

Renewable Reserve Use

Ongoing use of appropriated fund balance?

Generate enough fund balance to maintain 4% Unassigned Fund Balance?

Non-renewable Reserve Use Potential deficit spending spiral

But what about the $2 million in Restricted Reserves

What does it mean to the school if reserves are used to make up the budget gap rather than increasing taxes?

Recall the Budget that worked in most years

14-15 15-16 16-17 17-18 18-19

Levy Increase 0.0331915119753 0.0192769283000214

0.0223204476364974

0.0228344077073418

0.0228226474956898

Tax Cap Limit 0.021634933405384 0.0251615139034275

0.0251603505305768

0.0251590328900456

0.0251577150021555

Budget In-crease

0.0262001235005286

0.0202614277214254

0.022213744203463 0.0229341157874647

0.0231290999431066

0.25%

0.75%

1.25%

1.75%

2.25%

2.75%

3.25%

Perc

ent C

hang

e

• Note that only the 2014-2015 year budget requires exceeding the tax cap.

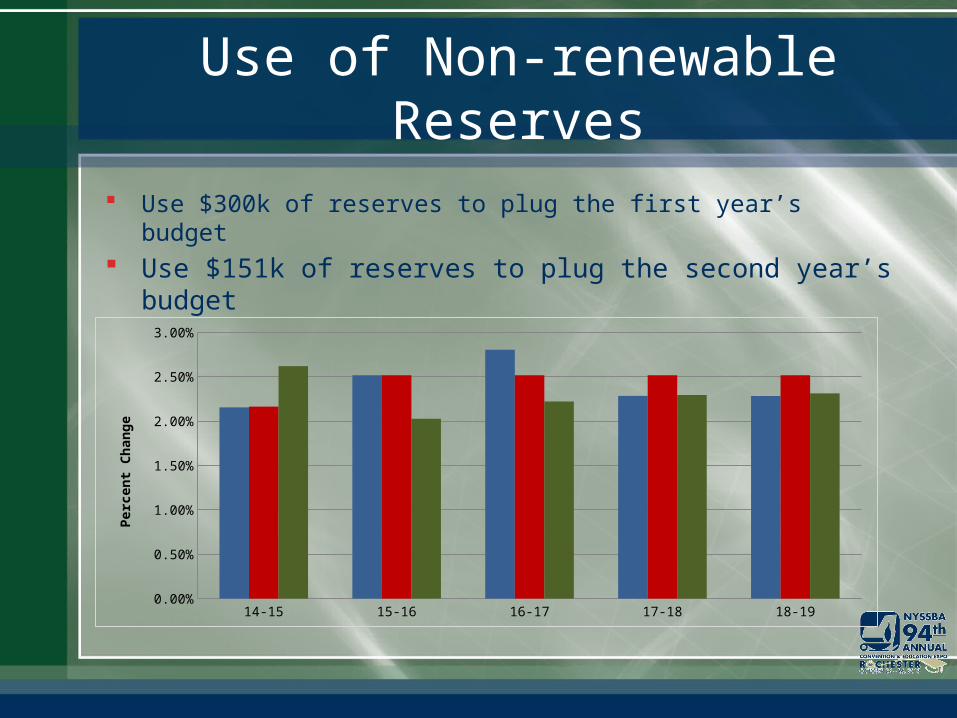

Use of Non-renewable Reserves

Use $300k of reserves to plug the first year’s budget

14-15 15-16 16-17 17-18 18-19

Levy Increase 0.0215433197639215

0.0308992778839889

0.022320447636497 0.0228344077073413

0.0228226474956912

Tax Cap Limit 0.021634933405384 0.0251622153183914

0.0251603505305768

0.0251590328900456

0.0251577150021555

Budget In-crease

0.0262001235005286

0.0202614277214254

0.022213744203463 0.0229341157874647

0.0231290999431066

0.25%

0.75%

1.25%

1.75%

2.25%

2.75%

3.25%

Perc

ent C

hang

e

Use of Non-renewable Reserves

Use $300k of reserves to plug the first year’s budget Use $151k of reserves to plug the second year’s budget

14-15 15-16 16-17 17-18 18-19

Levy Increase 0.0215433197639215

0.0251599976208517

0.0280438308950539

0.0228344077073413

0.022822647495691

Tax Cap Limit 0.021634933405384 0.0251622153183914

0.0251606883984313

0.0251590328900456

0.0251577150021556

Budget In-crease

0.0262001235005286

0.0202614277214254

0.022213744203463 0.0229341157874647

0.0231290999431066

0.25%

0.75%

1.25%

1.75%

2.25%

2.75%

Perc

ent C

hang

e

Use of Non-renewable Reserves

Use $300k of reserves to plug the first year’s budget Use $151k of reserves to plug the second year’s budget Use $77k of reserves to plug the third year’s budget

14-15 15-16 16-17 17-18 18-19

Levy Increase 0.0215433197639215

0.0251599976208517

0.0251519297919458

0.0257197711993308

0.0228226474956911

Tax Cap Limit 0.021634933405384 0.0251622153183914

0.0251606883984313

0.0251591994188057

0.0251577150021555

Budget In-crease

0.0262001235005286

0.0202614277214254

0.022213744203463 0.0229341157874647

0.0231290999431066

0.25%

0.75%

1.25%

1.75%

2.25%

2.75%

Perc

ent C

hang

e

Use of Non-renewable Reserves

Use $300k of reserves to plug the first year’s budget Use $151k of reserves to plug the second year’s budget Use $77k of reserves to plug the third year’s budget

Use $15k of reserves to plug the forth year’s budget

14-15 15-16 16-17 17-18 18-19

Levy Increase 0.0215433197639215

0.0251599976208517

0.0251519297919458

0.0251591980409279

0.0233819429915184

Tax Cap Limit 0.021634933405384 0.0251622153183914

0.0251606883984313

0.0251591994188057

0.0251577465616256

Budget In-crease

0.0262001235005286

0.0202614277214254

0.022213744203463 0.0229341157874647

0.0231290999431066

0.25%

0.75%

1.25%

1.75%

2.25%

2.75%

Perc

ent C

hang

e

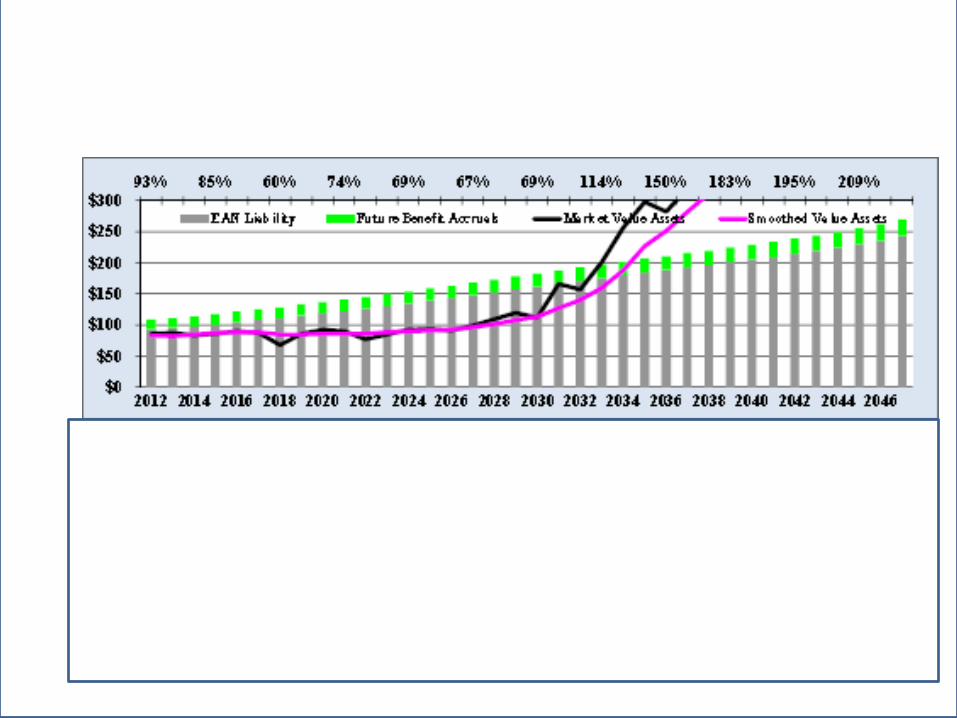

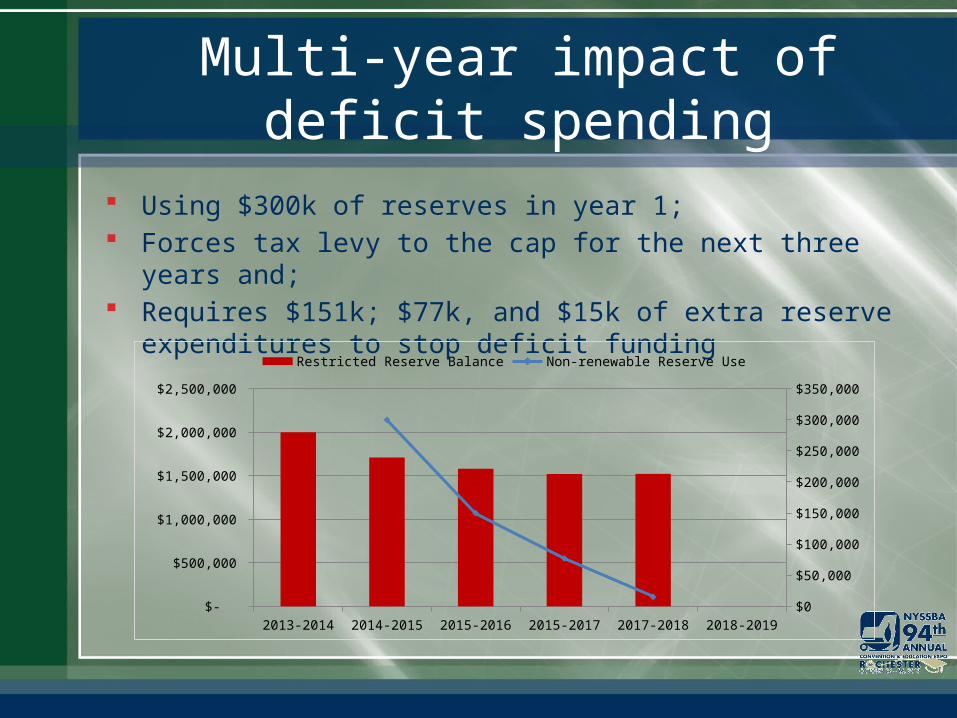

Multi-year impact of deficit spending

Using $300k of reserves in year 1; Forces tax levy to the cap for the next three years and; Requires $151k; $77k, and $15k of extra reserve

expenditures to stop deficit funding

2013-2014 2014-2015 2015-2016 2015-2017 2017-2018 2018-2019 $-

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

Restricted Reserve Balance Non-renewable Reserve Use

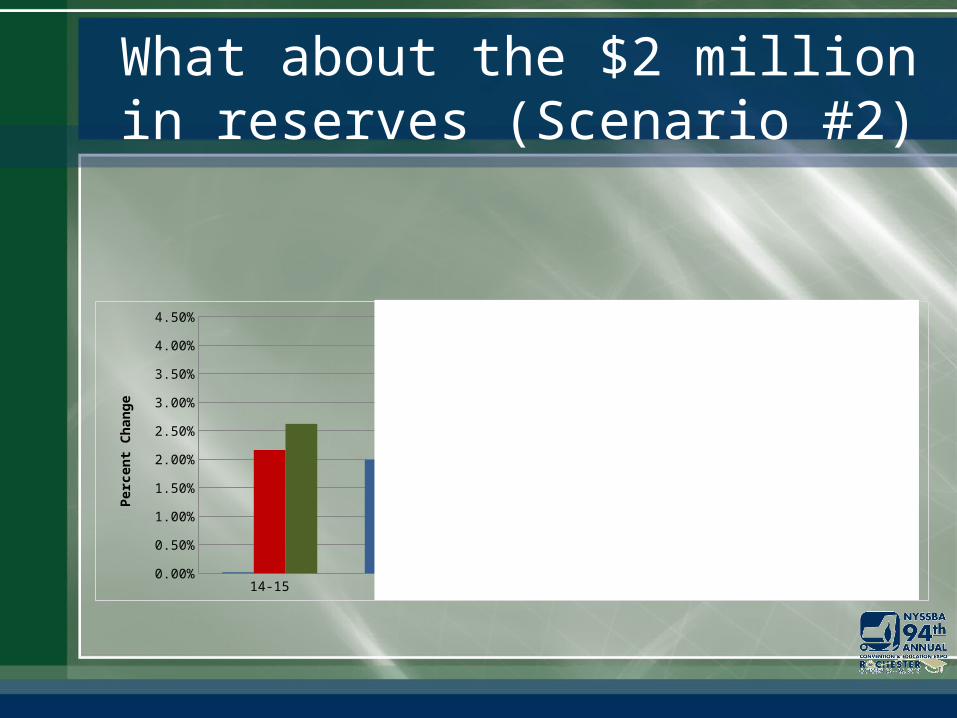

What about the $2 million in reserves (Scenario #2)

With $2 million in reserves, why shouldn’t the taxpayers have a year with no increase?

What about the $2 million in reserves (Scenario #2)

2013-2014 2014-2015 2015-2016 2015-2017 2017-2018 2018-2019 $-

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

$2,000,000

$1,160,427

$331,616

$716 $17,892

Restricted Reserve Balance Non-renewable Reserve Use

What about the $2 million in reserves (Scenario #2)

14-15 15-16 16-17 17-18 18-19

Levy Increase 0.000188300709727584

0.0199130090627998 0.0421116713499079 0.0358723444131398 0.0228226474956907

Tax Cap Limit 0.021634933405384 0.0251635436775702 0.0251623030366371 0.0251597853745906 0.0251577150021555

Budget Increase 0.0262001235005286 0.0202614277214254 0.022213744203463 0.0229341157874647 0.0231290999431066

0.25%0.75%1.25%1.75%2.25%2.75%3.25%3.75%4.25%

Perc

ent C

hang

e

What about the $2 million in reserves (Scenario #2)

2013-2014 2014-2015 2015-2016 2015-2017 2017-2018 2018-2019 $-

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

$2,000,000

$1,160,427

$331,616

$716 $17,892

Restricted Reserve Balance Non-renewable Reserve Use

What about the $2 million in reserves (Scenario #2)

14-15 15-16 16-17 17-18 18-19

Levy Increase 0.000188300709727584

0.0199130090627998 0.0421116713499079 0.0358723444131398 0.0228226474956907

Tax Cap Limit 0.021634933405384 0.0251635436775702 0.0251623030366371 0.0251597853745906 0.0251577150021555

Budget Increase 0.0262001235005286 0.0202614277214254 0.022213744203463 0.0229341157874647 0.0231290999431066

0.25%0.75%1.25%1.75%2.25%2.75%3.25%3.75%4.25%

Perc

ent C

hang

e

What about the $2 million in reserves (Scenario #2)

2013-2014 2014-2015 2015-2016 2015-2017 2017-2018 2018-2019 $-

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

$2,000,000

$1,160,427

$331,616

$716 $17,892

Restricted Reserve Balance Non-renewable Reserve Use

What about the $2 million in reserves (Scenario #2)

14-15 15-16 16-17 17-18 18-19

Levy Increase 0.000188300709727584

0.0199130090627998 0.0421116713499079 0.0358723444131398 0.0228226474956907

Tax Cap Limit 0.021634933405384 0.0251635436775702 0.0251623030366371 0.0251597853745906 0.0251577150021555

Budget Increase 0.0262001235005286 0.0202614277214254 0.022213744203463 0.0229341157874647 0.0231290999431066

0.25%0.75%1.25%1.75%2.25%2.75%3.25%3.75%4.25%

Perc

ent C

hang

e

Explain to the taxpayers why you need to exceed theTax Cap two years in a row for something done 3 years ago

So when should you use Non-renewable reserves?

When you have a plan to stop!

Sustainable Uses of Reserves

Fund first year start up costs for an aided program (e.g., BOCES aided software).

Bridge operating expenses until significant retirements occur.

Emergency repairs.

Retirement incentives.

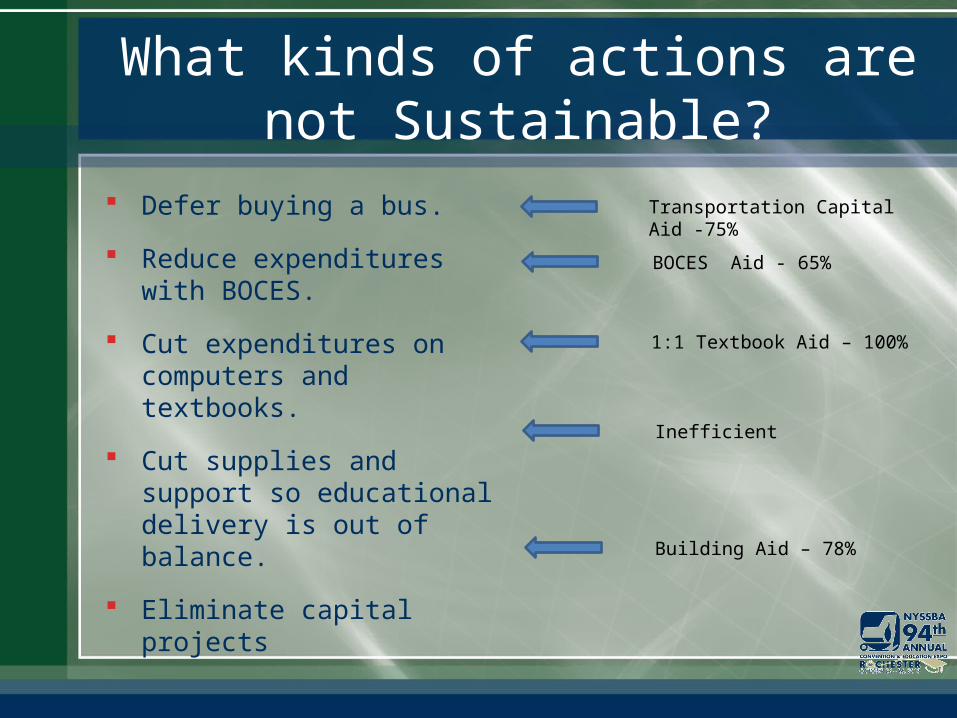

What kinds of actions are not Sustainable?

Defer buying a bus.

Reduce expenditures with BOCES.

Cut expenditures on computers and textbooks.

Cut supplies and support so educational delivery is out of balance.

Eliminate capital projects

Transportation Capital Aid -75%

BOCES Aid - 65%

1:1 Textbook Aid – 100%

Inefficient

Building Aid – 78%

Multi-year BudgetingPlanning for accelerating change!

Technology Networks and access

Collaboration

Content Management and Leaning Systems

Assessments Library and Information Subscriptions Data sources and data analysis 21st century skills

Summary

Multi-year budgeting exposes the consequences of current year decisions.

Allows schools to better manage reserves.

Provides an important tool for collective bargaining negotiations.

Helps the district manage public perceptions and expectations.