financial literacy: non profit finance 101

TRANSCRIPT

Financial Literacy: Non-Profit Finance 101

ACA Institute for Leadership Training

Learning Objectives

Financial Basics

• Financial Concepts• Monthly Reporting Information

InternalControls

• Concepts—separation of duties• Handling Money• Documentation

501(c)(3)

• Do• Don’t• What to look out for

2

Financial Basics – Financial Statements

Types of Financial Statements:

– Statement of Financial Position (Balance Sheet)

– Statement of Activities (Income Statement, P & L)

3

Financial Basics – Balance Sheet Terms

Assets: resources or things of value that are owned by an organization Cash and investments Accounts receivable Fixed assets

Liabilities: obligations of the organization Accounts payable Deferred revenue

Net Assets: net worth of an organization (aka Reserves)4

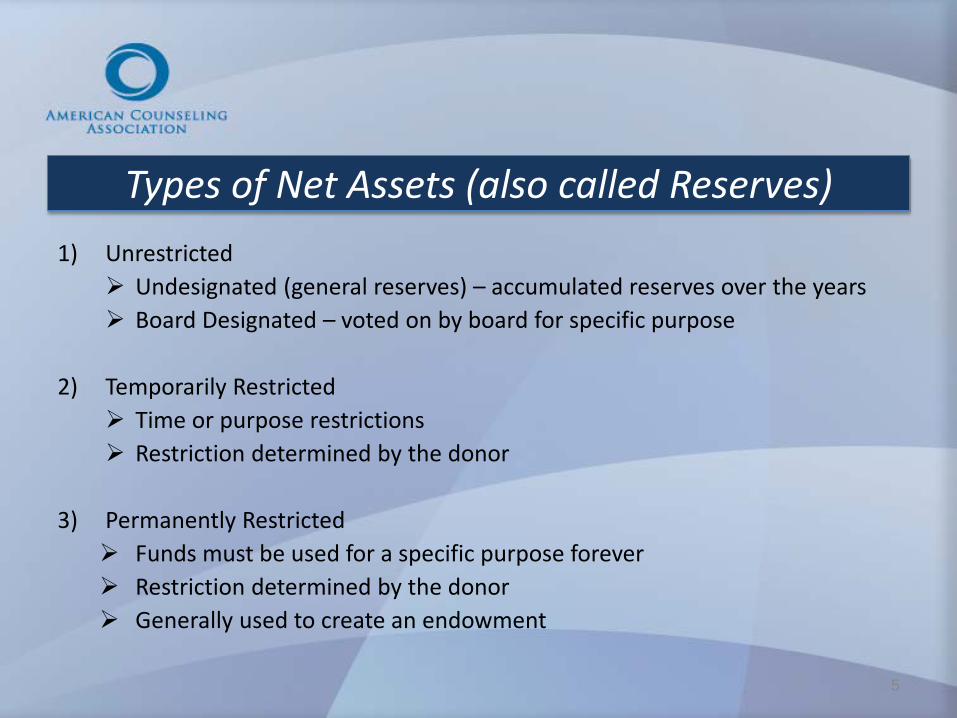

Types of Net Assets (also called Reserves)1) Unrestricted

Undesignated (general reserves) – accumulated reserves over the years Board Designated – voted on by board for specific purpose

2) Temporarily Restricted Time or purpose restrictions Restriction determined by the donor

3) Permanently Restricted Funds must be used for a specific purpose forever Restriction determined by the donor Generally used to create an endowment

5

Statement of Financial Position - at a particular point in time

As of 12/31/15

Assets

Cash & Investments 150,000

Accounts Receivable 50,000

Liabilities

Deferred Dues 25,000

Accounts Payable 25,000

Net Assets 150,000

6

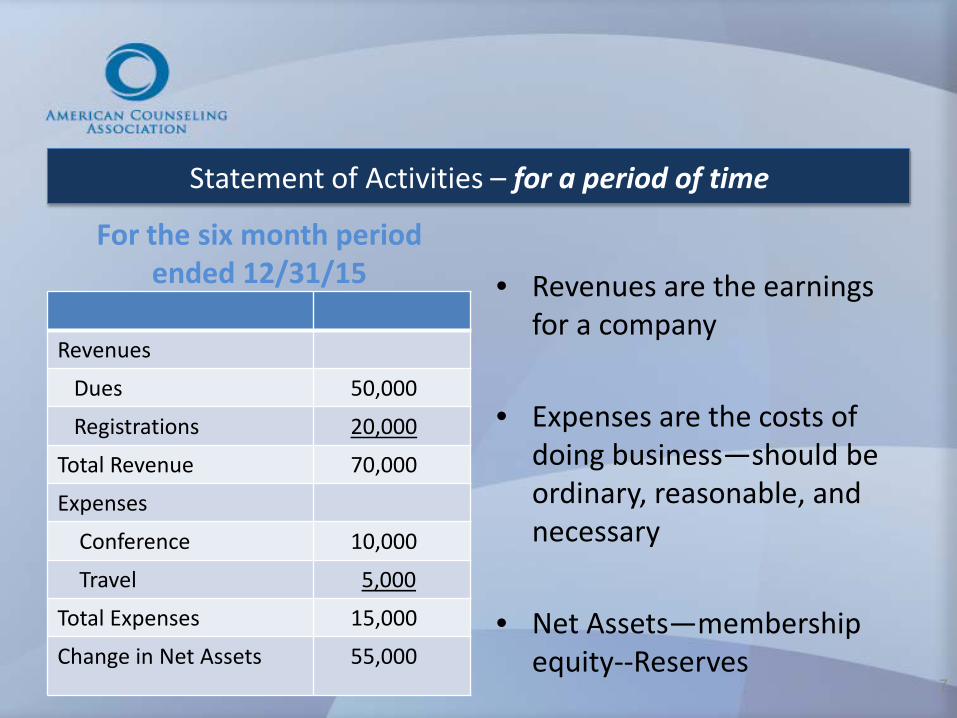

For the six month period ended 12/31/15

Revenues

Dues 50,000

Registrations 20,000

Total Revenue 70,000

Expenses

Conference 10,000

Travel 5,000

Total Expenses 15,000

Change in Net Assets 55,000

• Revenues are the earnings for a company

• Expenses are the costs of doing business—should be ordinary, reasonable, and necessary

• Net Assets—membership equity--Reserves

Statement of Activities – for a period of time

7

Cash Basis• Ex: Personal Checking

Account

• Revenue = Cash In

• Expense = Cash Out

Accrual Basis (GAAP)• Ex: Business, Organization,

Nonprofit

• Revenue = Income Earned

• Expense = Obligation Incurred

• Fixed Assets get capitalized

Financial Basics – Accounting Methods

8

Financial Basics - Budget

Budget Preparation• Review Strategic Plan

– What you want to accomplish• Review prior financial details

– Look back 2-5 years prior – Review for trends and opportunities for savings

• Budget a net neutral or positive result (Revenues>=Expenses)

Obtain formal budget approval from the Board

9

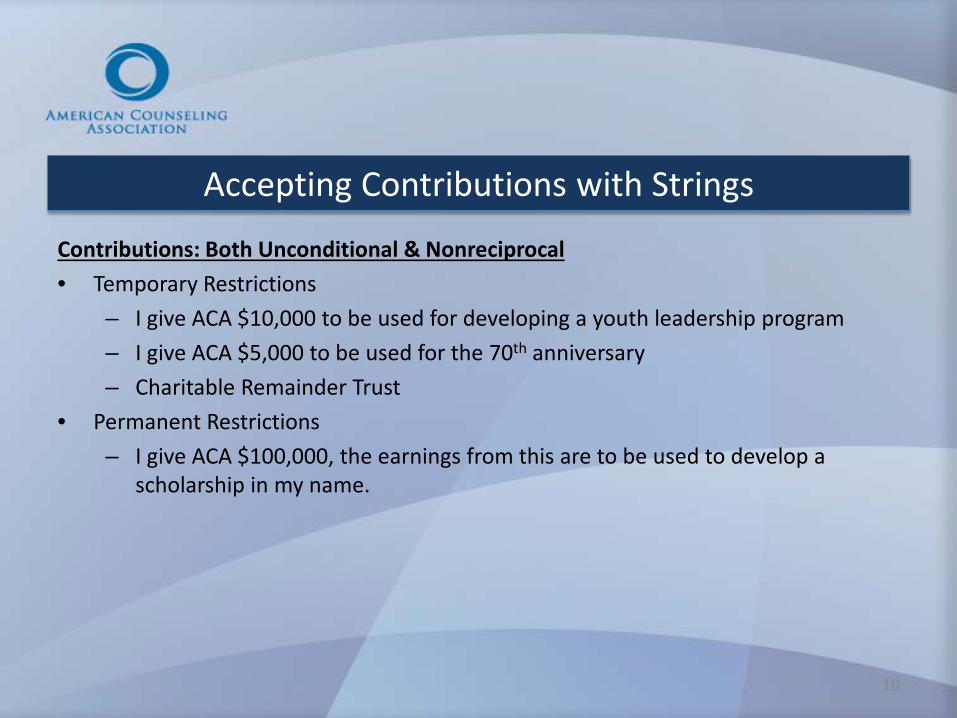

Accepting Contributions with Strings

Contributions: Both Unconditional & Nonreciprocal• Temporary Restrictions

– I give ACA $10,000 to be used for developing a youth leadership program – I give ACA $5,000 to be used for the 70th anniversary – Charitable Remainder Trust

• Permanent Restrictions– I give ACA $100,000, the earnings from this are to be used to develop a

scholarship in my name.

10

Boardroom Quiz

1) A motion comes before you to approve the use of reserves of $100,000.Where can it come from?

Unrestricted Undesignated Net Assets

2) A motion comes before you to spend Temp. Restricted net assets to fix the roof on your building. Should you approve it? Why?

No, Temp Restricted has donor restrictions—they rarely designate donations for a roof

3) A net operating deficit is projected for this fiscal year. Where will the money come from to cover this deficit?

Unrestricted Undesignated. Board could also create a Board Designated fund for this

11

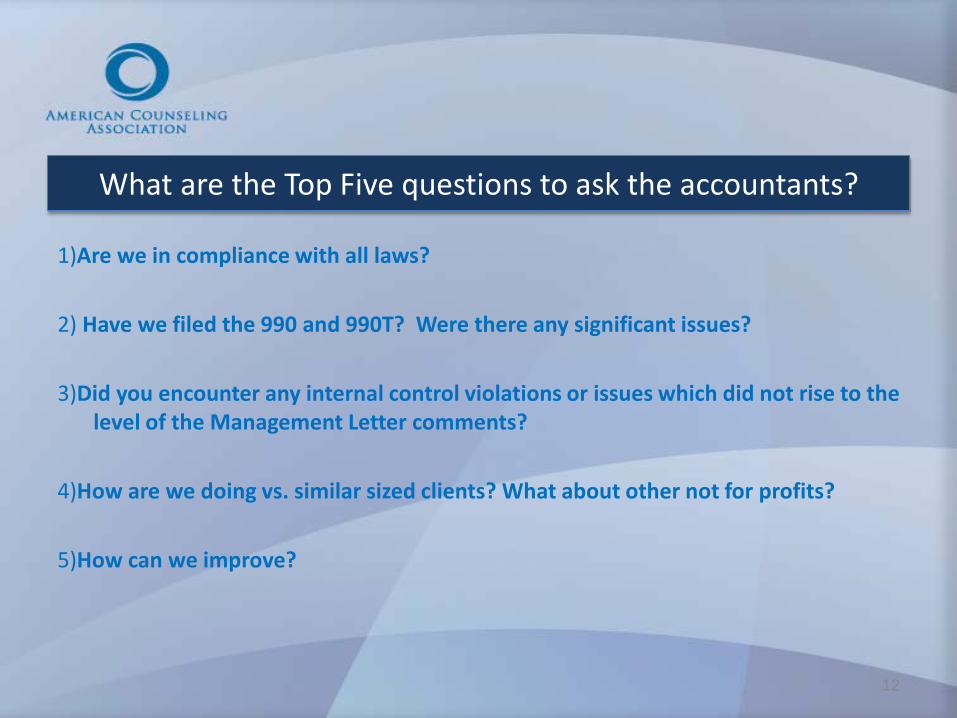

What are the Top Five questions to ask the accountants?

1)Are we in compliance with all laws?

2) Have we filed the 990 and 990T? Were there any significant issues?

3)Did you encounter any internal control violations or issues which did not rise to the level of the Management Letter comments?

4)How are we doing vs. similar sized clients? What about other not for profits?

5)How can we improve?

12

Internal Controls

Procedures and policies in place to prevent and detect errors and irregularities.

• Separation of duties– the approval function, the accounting/reconciling

function, and the asset custody function should be separated among employees

• Require approvals proactively; Perform reviews retroactively

13

Internal Controls

Examples of Separation of Duties

Different individuals responsible for:• Cutting checks/approving checks• Receiving checks/recording receipts/depositing checks

14

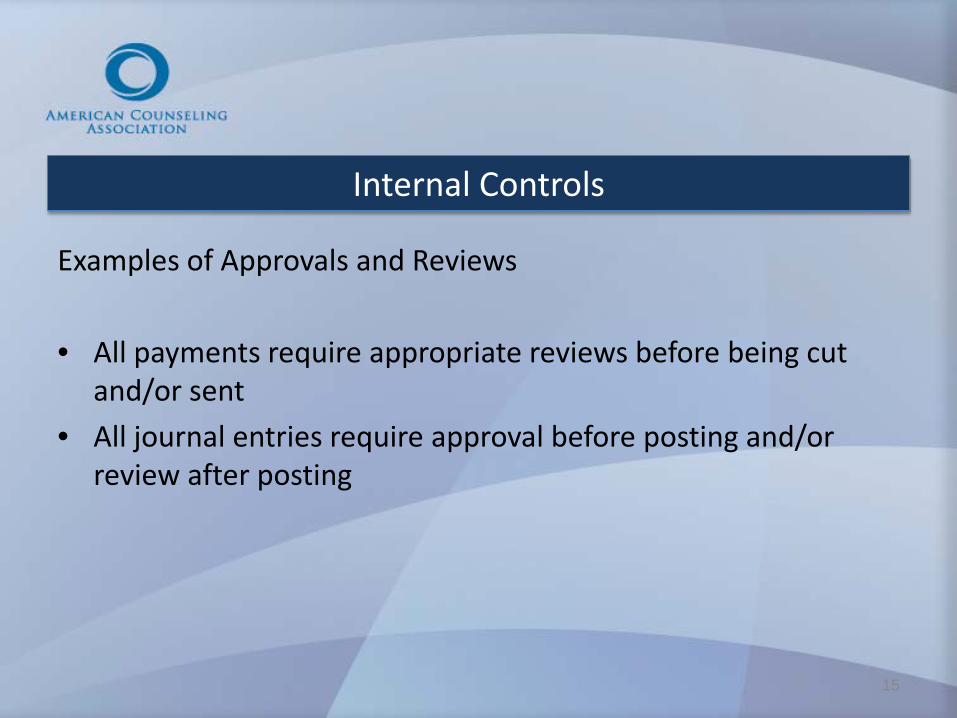

Internal Controls

Examples of Approvals and Reviews

• All payments require appropriate reviews before being cut and/or sent

• All journal entries require approval before posting and/or review after posting

15

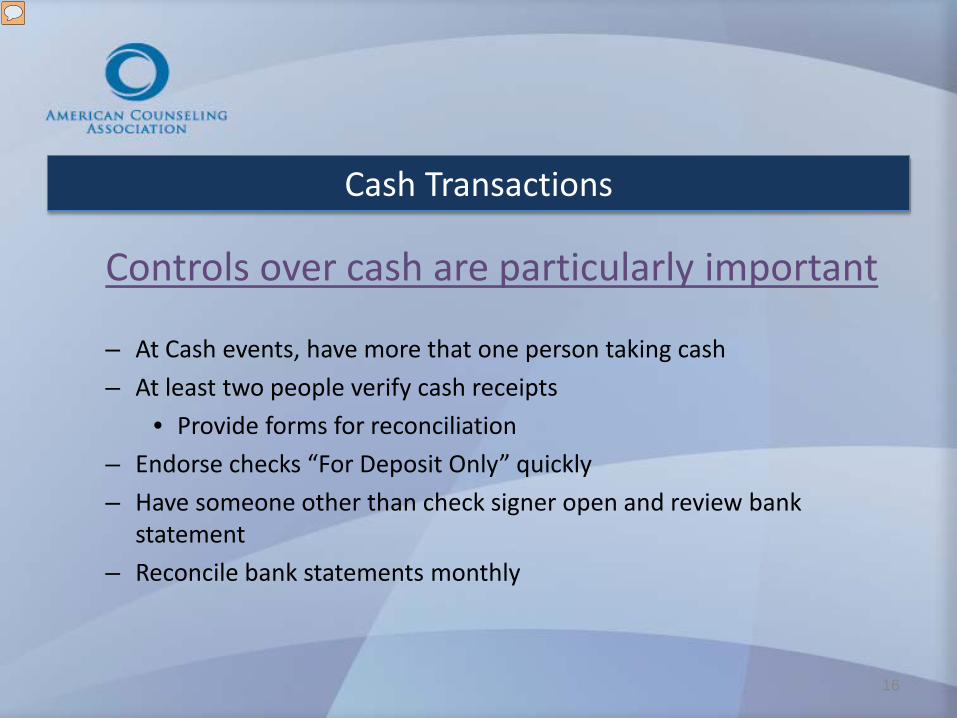

Cash Transactions

Controls over cash are particularly important

– At Cash events, have more that one person taking cash – At least two people verify cash receipts

• Provide forms for reconciliation– Endorse checks “For Deposit Only” quickly– Have someone other than check signer open and review bank

statement– Reconcile bank statements monthly

16

Internal Controls

Other Considerations:

Volunteers can obligate the organization-even unknowingly

Document the policies and procedures in place to help ensure they are followed

17

Documentation

18

Permanent files (please transfer to successor)• All minutes of Board meetings• IRS Form 1023 (1024 for (c)(6))• IRS determination letter• By-Laws• Articles of Incorporation• Policies and Procedures (including who can sign)

Federal Form 990s and 990TsContracts Donor records (if applicable)Transactions—forms with approvals

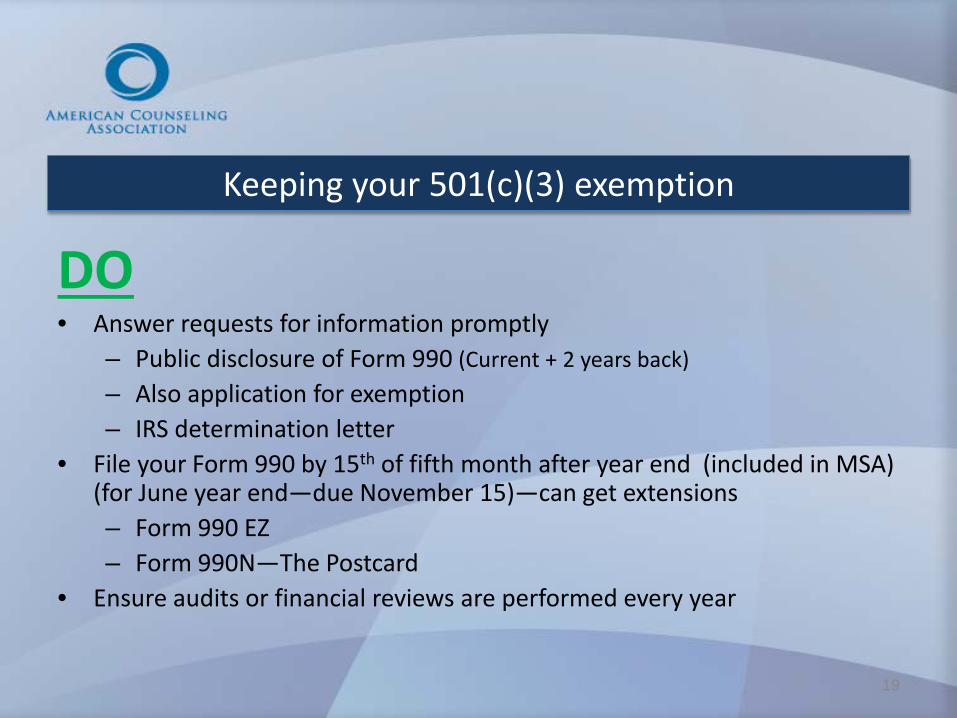

Keeping your 501(c)(3) exemption

DO• Answer requests for information promptly

– Public disclosure of Form 990 (Current + 2 years back)– Also application for exemption– IRS determination letter

• File your Form 990 by 15th of fifth month after year end (included in MSA) (for June year end—due November 15)—can get extensions– Form 990 EZ– Form 990N—The Postcard

• Ensure audits or financial reviews are performed every year

19

Tax Filing Requirements

20

Or short form

If an organization that is required to file a lower level return files a 990, it must file a complete 990.

Keeping your 501(c)(3) exemption

DON’T• Provide private benefit to anyone• Provide excessive benefits to Officers, Directors, or Key Employees• Legislative activities (lobbying)--can be limited• Political Campaign Intervention

If you realize after the fact that you might have done one of these—call your legal counsel.

21

Key Information IRS is looking for:

Form 990• Governance information• Salaries of Executives• Conflict of Interest policy and action plan• Whistleblower policy • Document retention/destruction policy

22

When you are considering something new…

Some things to think about:• Some types of revenue may obligate you to pay tax -

Unrelated Business Income (UBI)Ex: Advertising

• Hiring Employees = Payroll taxes• Accepting contributions with strings attached• Accepting contributions and providing goods or services

23

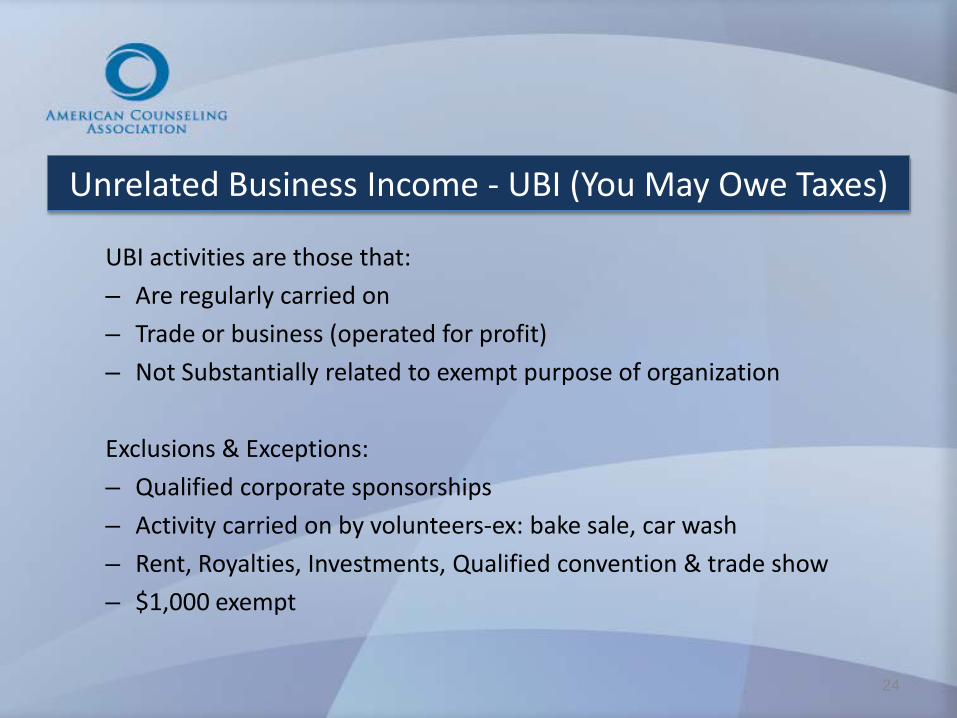

Unrelated Business Income - UBI (You May Owe Taxes)

UBI activities are those that:– Are regularly carried on– Trade or business (operated for profit)– Not Substantially related to exempt purpose of organization

Exclusions & Exceptions:– Qualified corporate sponsorships– Activity carried on by volunteers-ex: bake sale, car wash– Rent, Royalties, Investments, Qualified convention & trade show– $1,000 exempt

24

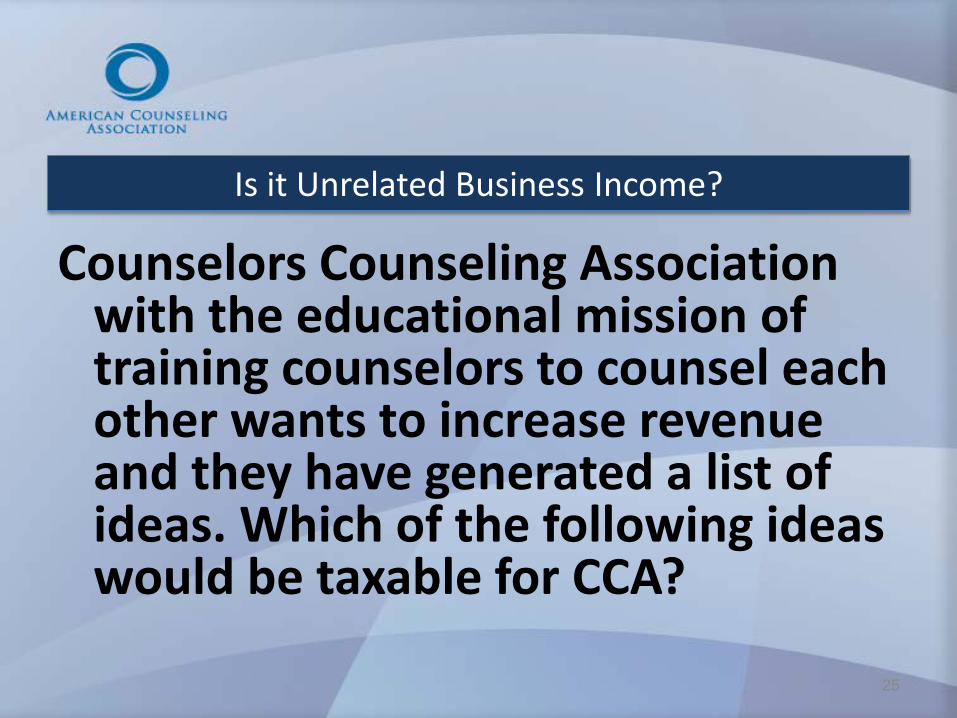

Is it Unrelated Business Income?

Counselors Counseling Association with the educational mission of training counselors to counsel each other wants to increase revenue and they have generated a list of ideas. Which of the following ideas would be taxable for CCA?

25

Is it Unrelated Business Income?

Advertising in the CCA journal? Taxable

CE webinar on group therapy? Not taxable

Renting mailing lists? Not taxable

Sponsorship of Smoothie Bar at Annual Conference?Not taxable as long as no substantial return benefit

Web banner #1? (Also for newsletters)ABC company congratulates CCA on Ten years of service to Counselors

Not taxable. This is sponsorship.26

Is it Unrelated Business Income?

Web Banner #2? (Also for newsletters)ABC Company: the best company in billing software for health professionals

with the lowest rates in town congratulates CCA for 10 years of service to the counseling profession.

Taxable because it is advertising

License CCA (mark) and mailing list to ABC bank for credit cards with CCA logo for % of gross revenue?

Not taxable(What if % of profits?)

If it is for % of profit it is considered a Joint Venture and is taxable

27

Accepting Contributions and Providing Goods & Services

• Qualified Sponsorship—2% rule

• Sponsorship with event tickets included– Give $1,000 sponsorship of event, get $100 event tickets?

• Token gift given to donor

28

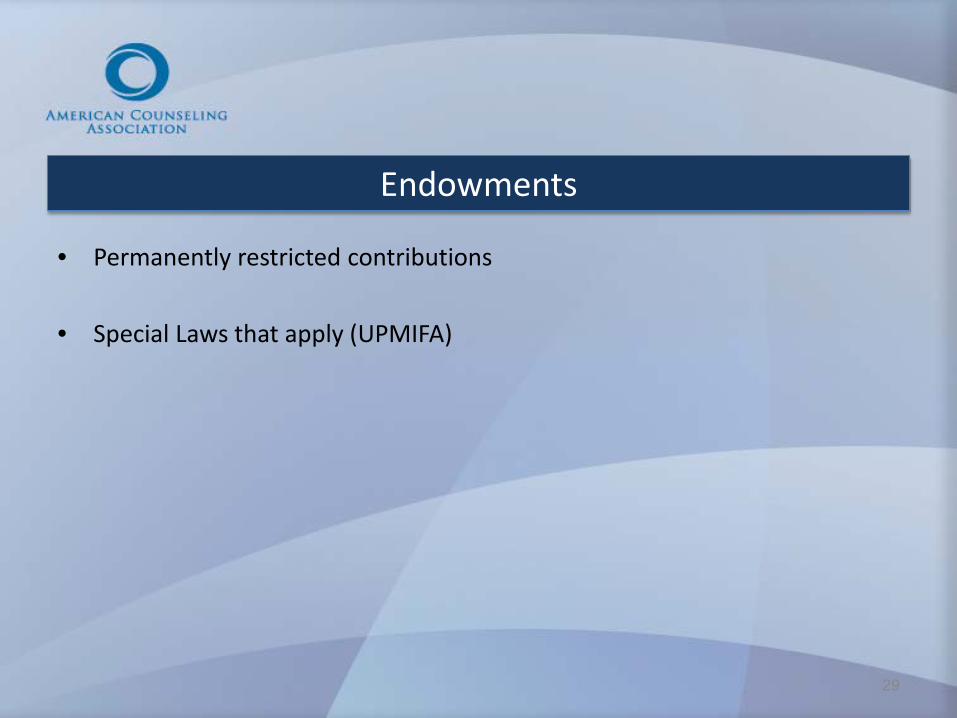

Endowments

• Permanently restricted contributions

• Special Laws that apply (UPMIFA)

29

Insurance & Risk Management

Financial health of organization

Debts and related covenants

Budget

Contracts

Insurance: D & O , General Liability, Workers Comp (among others)

Management Services Agreement (if applicable)

30

Additional Resources

• Small business Administration: www.sba.org• IRS: www.irs.gov (charities & non profits tab)• Guidestar: www.guidestar.org• American Society of Association Executives www.asaecenter.org

• Dave Jackson 703-823-9800 x255 [email protected]• Carol Salerno 703-823-9800 x228 [email protected]• Jackie DeMaio 703-823-9800 x308 [email protected]

31