financial legal trust structure

TRANSCRIPT

Trusts – A 21st Century Look At A Centuries Old Tool

Peter Bobbin Argyle Lawyers Pty Ltd

LEVEL 22, 1 MARKET STREET, SYDNEY NSW 2000 DX 876 SYDNEY TEL: 61 2 8263 6600 FAX: 61 2 8263 6633 LEVEL 22, 1 MARKET STREET, SYDNEY NSW 2000 TEL: 61 2 8263 6600 FAX: 61 2 8263 6633

File ref:PGB WWW.ARGYLELAWYERS.COM.AU

© Copyright in this document and the concepts it presents is strictly reserved by The Argyle Lawyers Pty Limited, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to the Argyle Lawyers Pty Limited and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of the Argyle Lawyers Pty Limited!

TABLE OF CONTENTS INTRODUCTION ........................................................................................................................... 1

1. CHECK YOUR TRUSTEES’ POWERS............................................................................ 3

2. THE SETTLOR ................................................................................................................. 9

3. STAMP DUTY LAWS ..................................................................................................... 14

4. THE APPOINTOR AND THE ISSUE OF CONTROL..................................................... 28

5. BENEFICIARY DISTRIBUTIONS................................................................................... 31

6. AMENDING TRUSTS - the tax considerations .............................................................. 41

7. FAMILY LAW AND TRUSTS.......................................................................................... 51

8. THE ALTER EGO TRUST FAILURE?............................................................................ 54

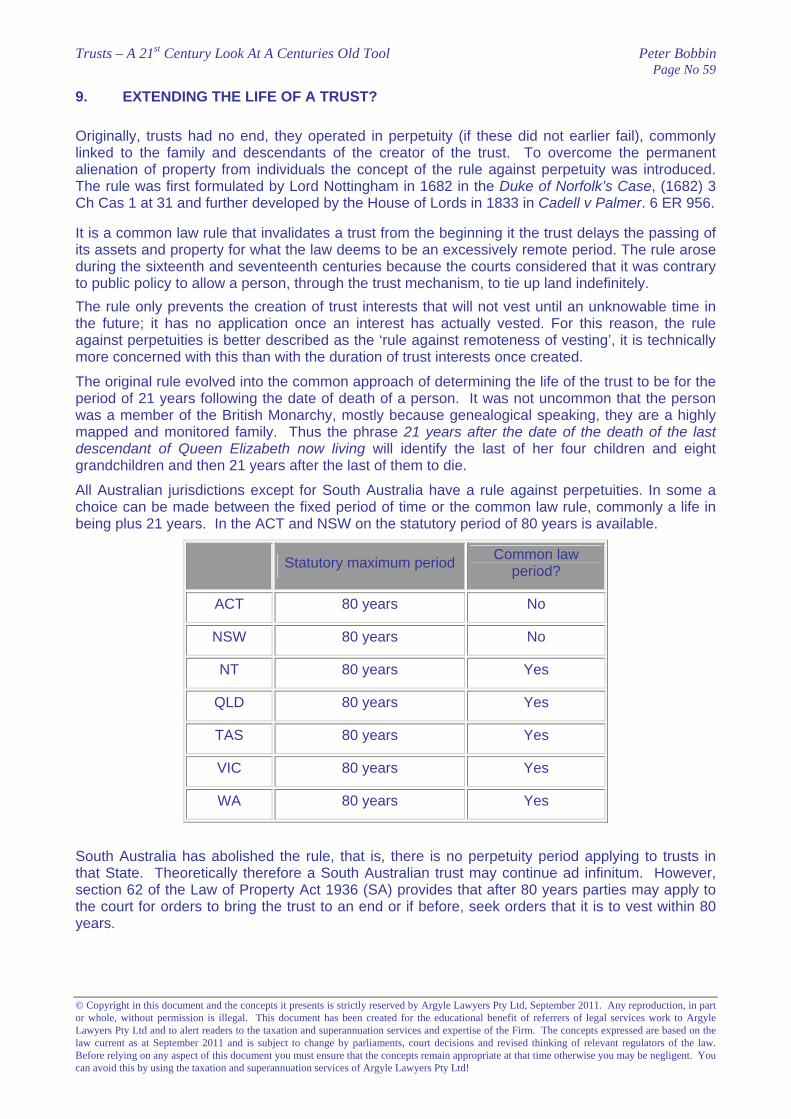

9. EXTENDING THE LIFE OF A TRUST? ......................................................................... 59

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 1

© Copyright in this document and the concepts it presents is strictly reserved by The Argyle Lawyers Pty Limited, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to the Argyle Lawyers Pty Limited and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of the Argyle Lawyers Pty Limited!

INTRODUCTION

In this paper, I return to the basics, the fundamental principles upon which the law of trusts is built. Before you cry “how boring” and “what a waste of time,” just consider this:

Without doubt trusts are the most favoured investment and business vehicles today and yet most professionals will have only completed less than 40 hours formal education in the law of trusts and the taxation of these.

How relevant are the fundamentals?

Very relevant, just look at the approaches adopted by the courts in Bamford, Broomhead, Faucilles, and Nichols Cabramatta. These cases, and others, are briefly profiled in this paper.

A conservative approach

In this paper, I seek to identify a range of practice points for practitioners to follow. But before doing so, let me make my admission of having taken a conservative approach in its preparation. No doubt some will not agree with the strength of the warnings that I feel some of the cases and principles reviewed in this paper may give. My view in this regard, however, is that, if a conservative approach can be followed, and does not add significant cost or time delays, then on simple best practice grounds, why not follow it.

Structure of the paper

The paper has been broken down so as to look at the essential elements of a trust. In Section 1 I examine the nature of trustee powers, not so much from an argument as to whether they are fiduciary in nature, but rather as to their adequacy, and what to beware of when assessing this.

Section 2 considers the settlor, the person who will have been said to have created the trust. The goal is to identify who should be a settlor.

Section 3 examines some of the stamp duty issues connected with a trust. Whilst a view based on the NSW Duties Act is adopted, many issues are transportable across the states and territories of Australia.

With the continuing growth of the estate planning industry, control and succession have become important issues for the management of trusts. Section 4 looks to the person who has control of the trust through the power of appointment.

One of the major proclaimed reasons for the use of trusts in the 21st Century is their inherent flexibility. Section 5 examines some aspects of beneficiary distributions and in some ways challenges the validity of the claim of absolute flexibility.

Family law is often described as a law unto itself. It is for this reason that just a small section of the paper – Section 6 – is dedicated to family law and trusts.

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 2

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

Have a contrary view?

The views expressed in this paper are mine, developed over a number of years. If you have a contrary view, or perhaps come across a case which supports some of the approaches expressed in this paper, I would be pleased to hear from you. Send a fax or a quick note, or better still, give me a call; I look forward to hearing from you.

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 3

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

1. CHECK YOUR TRUSTEES’ POWERS

Those who remember the old Companies Act (1961) will recall the need to ensure that the Memorandum and Articles of Association were drafted with sufficiently broad powers to ensure that the company was able to enter into the modern transactions and investments of that time. Many will no doubt recall the need to respond to bank enquiries about whether the power of a company was sufficient to enable it to enter into certain financial transactions.

The sufficiency of the corporate powers were overcome with the introduction of ‘powers equivalent to ‘an individual’’, which are found in Part 2.B.1 of the Corporations Act 2001, Company Powers and How They Are Exercised. Unfortunately, there is no equivalent in the area of trusts.

Thus, it is important to ensure that the terms of a trust deed, and the powers that are vested by it in the trustee, are sufficient to accommodate the need to which the trust will be applied. Whether this is done by granting general powers equivalent to that of full ownership, or by specifically stating the respective powers that a trustee may employ, is a choice for the legal draftsperson.

When deciding what approach to adopt keep in mind that other parties who may interact with trustee for the benefit of the trust will often need to see an express power that is consistent with the interaction. The most common is the need to identify an express power in the trustee to borrow monies. There is no general or common law authority that allows a trustee to borrow. Indeed, in a trust-historical sense a trustee borrowing is not permitted under the general law, it is only if a trustee has a specific borrowing power that the trustee may borrow.

Certainly, it is important to ensure that the trustee power of amendment itself is sufficiently broad to enable a trustee to update the investment and administration powers of a trust so as to meet the ever-emerging new and synthetic ways of making investments and creating business relationships.

In the absence of the powers of investment and administration being sufficiently broad, there lies a real risk that a trustee will breach the terms of the trust.

What are the consequences of such a breach?

This will largely turn upon the nature of the trust. In almost all cases, the trustee may be liable to restore the assets of the trust. The real practical question though, is whether a third party, who has suffered loss as a result of the trustee’s breach, may trace through the trustee to base a claim against the beneficiaries.

In this regard, the relevant general principle is that, where a trustee incurs a liability in conformity with the terms of the trust, the trustee is entitled in equity to indemnity, not only out of the trust estate (Trustee Act 1925 (NSW), subs 59(4), and equivalent provisions in other jurisdictions), but also from each beneficiary who is sui juris and absolutely entitled beneficially to the trust property. The leading authority usually cited for this proposition is Hardoon -v- Belilios (1901) AC 118.

The principle is well recognised as part of Australian law: Paul A Davies (Australia) Pty Limited (In Liq) -v- Davies (1983) 1 NSWLR 440; J W Broomhead (Vic) Pty Limited (In Liq) -v- J.W. Broomhead Pty Ltd (1985) VR 891 (McGarvie J) (“Broomhead”); McLean -v- Burns Philp Trustee Co Pty Ltd (1985) 2 NSWLR 623 (Young J); Rosanove -v- O’Rourke (1988) 1 Qd R 171; Countryside (No 3) Pty Ltd -v- Bayside Brunswick Pty Ltd, unreported, Supreme Court of New South Wales, Brownie J, 20 April 1994 (“Countryside”); Jacobs’ Law of Trusts in Australia (5th ed, 1986) at paragraph (2105); Ford and Lee’s Principles of Law of Trusts (2nd ed, 1990) at para 1404.2).

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 4

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

It is a well accepted principle in Australian law, therefore, that where a trustee acts at the direction of their fully entitled beneficiary and thereby suffers loss, then to the extent that the assets of the trust do not indemnify the loss by the trustee, the trustee may recover against the beneficiary.

As earlier stated, the original authority for this principle may be found in Hardoon -v- Belilios. In this case “the beneficial owner of shares was held to be personally bound, in the absence of a contract to the contrary, to indemnify the registered holder against calls upon them. “The plainest principles of justice require that the cestui que trust who gets all the benefit of the property should bear its burdens unless he can show some reason why his trustee should bear them himself.”

Standing alone, this case may not cause much concern. It involved a beneficiary who was fully entitled as to the assets of the trust, and who directed the trustee as to a particular course of action. It seems only fair, then, that the beneficiary should not escape responsibility for the directions given to the trustee.

But that is the point. The law of trusts is founded upon principles of equity and fairness. When called upon to consider how to approach new principles of law, the courts fall back upon the principles of fairness and equity.

This was the approach of the Victorian Supreme Court in J.W. Broomhead (Vic) Pty Ltd (In Liq) -v- J.W. Broomhead Pty Ltd (1985) VR 891.

In Broomhead a company which was trustee of a unit trust went into liquidation. Whilst conducting a building business for the unit holders it had properly incurred liabilities. The liquidator was unable to obtain a complete indemnity out of trust assets, and so he sought a personal indemnity from the unit holders. It was held that this right of personal indemnity extended beyond the well-established cases where there is only one beneficiary and that beneficiary is sui juris and absolutely entitled (such as Hardoon -v- Belilios). McGarvie J decided (at 936) that the right of personal indemnity extends to a case “where there is more than one beneficiary and all of them are sui juris and entitled to the same interest as absolute owners between them.”

A reference to “the same interest as absolute owners” should be read as meaning only that the interest must be a vested absolute interest, and not as requiring that each unit holder have the same number of units.

Further, it also appears from Broomhead (937) that a beneficiary with less than an absolute interest may be liable to the trustee if that beneficiary has requested the trustee to assume office or to incur what otherwise would be an unauthorised liability.

Exactly how these principles apply to trusts generally, is still a little uncertain. Certainly, these principles are relevant to unit trusts, particularly where all beneficiaries are fully entitled to the assets of the trust.

How this may apply to a discretionary trust, is somewhat more difficult to determine.

As can be seen from the above, one relevant principle that may be drawn from Broomhead’s case is that:

a trustee has a right to be protected from the denials of a beneficiary who directed the trustee to undertake a course of action. The law then enables a person who has rights against a trustee the benefit of subrogation or tracing of the right against and through the trustee to certain of the beneficiaries.

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 5

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

As mentioned earlier in this paper, Broomhead is not necessarily regarded as general authority that must be followed. From a practical sense, however, the issues raised by Broomhead, and in this section of the paper, apply daily in financing transactions. So what does this mean?

Consider the following Practice Point:

Practice Point

Seek to prepare active management minutes that reflect a trustee acting within its active trustee capacity and not at the direction of unitholders.

And so as to help reduce the risk of claims against beneficiaries of trusts through the actions of trustees that are without power:

Practice Point

Ensure that the investment management and administration powers are sufficiently broad to enable the trustee to carry out the investments, conduct the business, or administer the assets of the trust.

At least in this way, if a trustee has sufficient power to undertake all tasks, then it is less likely that a potential creditor may successfully claim against a beneficiary through the trustee acting at the direction of the beneficiary in breach of the terms of the trust.

From a practical point of view, this is particularly relevant for trusts that are likely to borrow money for investment purposes.

Some banks take a realistic approach, and will lend to a trustee provided that the bank has received a solicitor’s certificate to the effect that the trustee has power.

In my own experience, however, many a delay has resulted from a lender’s lawyers imposing the requirement that a trust deed be amended to incorporate an express power enabling the trustee to enter into the particular credit transaction. Not only does this raise time delays but also the further expense and anxiety that comes with preparing, signing, and implementing a deed of amendment to a trust.

A further Practice Point that may be drawn from the Broomhead case is:

Practice Point

Ensure that you provide a warning that the law in Australia may enable a creditor claiming against an insolvent trustee of a unit trust to trace a claim against the trust unitholders. Thus, it is not sufficient to have a corporate trustee of a unit trust and to believe therefore that asset protection exists.

If you want further confirmation of this, refer to the Supreme Court of New South Wales Court of Appeal decision of I.R. Causley & G.J. Causley -v- Countryside (No 5) Pty Ltd & Ors (1996).

In a unanimous decision, the Court of Appeal held:

(a) the trustee of the unit trust was entitled to be indemnified by unit holders (both original and those that became unit holders by subsequent application) in respect of the liability for

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 6

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

damages incurred by the trustee in circumstances where the liabilities exceeded trust assets;

(b) one of the unit holders was entitled to recover moneys from the trustee in respect of work done by it for the trustee, and where the trust assets were insufficient to meet that liability, that unit holder was also entitled to indemnity from the other unit holders in respect of the trustee’s unpaid liability to it.

Speaking for the Court, Cole JA stated:

It is established that, absent provision in the trust deed denying the right of indemnity, or circumstances indicating good reason why a trustee should not be so indemnified, a trustee is entitled to be indemnified by the cestui que trust in respect of liabilities incurred by the trustee in pursuit of functions within power where the cestui que trust is or, if more than one are the absolute beneficial owners of the trust property the legal title to which is vested in the trustee.

In the later decision of Countryside (No.3) v Best/Lawson [2001] NSWSC 1152 (14 December 2001), that court was asked to visit the issue of whether there was an indemnity and if yes, the amount of indemnity by the unitholders in respect of the trustee. There were mixed successes, depending on your view. The background to the facts were;

10 On 20 December 1983, a Unit Trust Deed (“the Deed”) was executed between Mr Buckley, Mr Savins, Mr Lawson and Mr Blair (an accountant who had replaced Mr McKerlie), who were called “the Managers”, Rokolat Pty Limited (a company which later changed its name to Bayside Brunswick Pty Limited (“Bayside Brunswick”)), the trustee, and Lex, which was the original unit holder. Lex paid $60 and took up one unit to establish the Brunswick Unit Trust (“the Trust”). The Deed was in general terms. I need not describe the terms other than to say that the Deed provided that the Managers should, subject to the overall control of the trustee, “administer and manage the affairs of the Trust”. The Managers were to collect and receive all income of the Trust and to pay out all costs and disbursements incurred on behalf of the Trust. The powers of the trustee were extensive but were limited by the words “as directed by the Managers”. It will be seen that it was intended that Bayside Brunswick would operate substantially as a bare trustee and that is effectively what happened. Decisions were taken by the Managers, although it seems that Mr Buckley, Mr Savins and Mr Lawson were also the directors of Bayside Brunswick and Mr Blair was its secretary. Probably, no clear distinction in functions was drawn.

The Court also approved the comments of Brownie J from the earlier Causley decision;

“The plaintiff’s claim was based on the statements of Lord Lindley, delivering the advice of the Judicial Committee, in Hardoon v Balilios [1901] AC 118 at 123-125: as between a trustee and a sole cestui que trust, who is under no disability, the plainest principles of justice, and the rules of equity require that the cestui que trust who gets the benefit of the trust property should bear its burden unless he can establish some good reason why the trustee should bear the burden himself; the right of the trustee to indemnity in respect of liabilities incurred by him within the scope of the trust is not limited to the assets of the trust, but extends to the imposition of a personal liability on the cestui que trust; and the liability of the cestui que trust arises from the mere fact of the relationship between the parties, and does not depend upon there having been any request from the cestui que trust to the trustee to incur the liability.”

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 7

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

33 However, in his conclusion, Brownie J relied, not merely on the fact that the unit holders were beneficiaries who were sui juris and absolutely entitled, but also upon the circumstance that Bayside Brunswick was established as the vehicle to carry out the particular venture . His Honour said:-

“On the evidence, the appropriate inference is that those who applied for units in 1984 did so as participants in some commercial arrangement, in the expectation of profit: they paid a total of $49,920 each for units in a trust the sole function of which was to pay for, subdivide, develop and then resell the land in question; and they did this in the expectation that the trustee would make a profit for them. To adapt the language of Lord Lindley in Hardoon, the plainest principles of justice require that the beneficiaries who get all the benefit of the trust property should bear its burden unless they can show some good reason why the trustee should bear it itself; and the fact that there are several beneficiaries, rather than one beneficiary, is not of itself a good reason.”

And later

38 I agree with the view expressed by Professor Ford that, in the case of multiple beneficiaries, in order to establish personal liability on the beneficiaries, there needs to be more than the mere fact that the beneficiaries are sui juris and absolutely entitled. An additional fact may arise from a circumstance such that the beneficiary is a settlor of the trust or contributed the funds which were managed or that the beneficiaries requested that the expenditure be incurred or approved of its being incurred or that the trustee was carrying on a business established for the benefit of the beneficiaries.

So it is not the nature of the trust and the beneficiaries interest in it, what is important are the facts and involvement of the beneficiaries in the actions of the trustee that gave rise to the liability. Perhaps, taken to its logical extreme, such a view could support a liability upon beneficiaries of discretionary trusts, where they where knowingly and directly involved with the actions of the trustee.

And later still….

44 In my view, GLI did not, by reason of this transaction (a subscription for units long after the initial establishment and subscription of the early unitholders), come under a liability to indemnify Bayside Brunswick in respect of the expenses which Bayside Brunswick had previously paid or incurred. In my opinion, no principle of trust law or of the law of unjust enrichment requires that GLI be held liable for debts incurred prior to that transaction. The transaction did not amount to adoption and approval of all that had previously occurred. It was merely a transaction whereby a modest sum was raised with a view to overcoming some of the problems which the venture then faced.

So the mere subscription for units at a later time did not make the unitholder/beneficiary liable for the past debts of the trustee.

When pressed, the court found that it could trace, for ‘debt’ purposes under the insolvent trading provisions, against the unitholders …..

Therefore, as Bayside Brunswick’s obligation was a debt, it seems to me that the corresponding obligation of each unit holder was likewise a debt for the purposes of s 592.

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 8

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

I do not accept the submission, which has been put to me on behalf of the defendants, that a trustee must necessarily have recourse to the Trust’s assets before seeking personal indemnity. The authorities are to the contrary.

However, on the facts, the insolvent trading provisions did not ‘make their way through’ the trust to the unitholders, but only because…..

67 On the facts before me, I cannot conclude, as a matter of probability, that, when Lex, GLI and Buckley Dowdle (the unitholders) took up their units, it was reasonable to expect that they or any of them would not be able to pay all their debts as and when they became due. On the evidence before the Court, both Countryside and the defendants expected that Bayside Brunswick would be able to pay the instalments of the purchase price due to Countryside.

Practice Point

A clear warning on the use of a trust and the interactions of the trustee and the beneficiaries seems appropriate. The more the interaction and involvement of the beneficiaries in the actions of the trustee, the more the likelihood they will be liable with the trustee for any excess of liabilities.

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 9

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

2. THE SETTLOR

The settlor is the person who first created the trust. As the name implies, this is the person who has given to the trustee the property over which the initial trust will be established (often cash). In practice, this person invites the trustee to accept the trustee role subject to the terms and conditions of trust powers that exist at general law, in statute (such as a Trustee Act), and as may exist or will be modified by the terms of the trust deed.

Who should be the settlor?

From a taxation perspective, the issue to be addressed is the potential application of section 102 of the Tax Act. It is not so much a question of the actual identity of the person, but rather the general class or category of who should be ‘invited’ to volunteer to be the settlor. In my view this depends on the type of trust that is being established.

If it is a superannuation fund trust, the question of who should be the settlor is rather simple. A superannuation fund may be originally settled by either of the member or an employer of the member. Superannuation funds do not have the problem created by section 102 of the Tax Act. This is because, for taxation purposes, Part 3-30 of the 1997 Tax Act is deemed to be a code for the taxation of superannuation entities (see section 950-150).

But what of discretionary trusts, unit trusts, bare trusts, hybrid trusts, and such? The potential application of section 102 of the Tax Act makes it important to ensure that proper procedures are followed for the settlement and that the correct identity of a settlor is adopted.

As far as is relevant for the purposes of this section of the paper, section 102 reads:

102(1) Where a person has created a trust in respect of any income or property (including money) and:

(a) he has power, whenever exercisable, to revoke or alter the trusts so as to acquire a beneficiary interest in the income derived by the trustee during the year of income, or the property producing that income, or any part of that income or property;

(b) …

the Commissioner may assess the trustee to pay income tax, under this section, and the trustee shall be liable to pay the tax so assessed.

102(2) The amount of the tax payable in pursuance of this section shall be the amount by which the tax actually payable on his own taxable income by the person who created the trust is less than the tax which would have been payable by him if he had received, in addition to any other income derived by him, so much of the net income of the trust estate as –

(a) is attributable to the property in which he has power to acquire the beneficial interest;

(b) represents the income, or the part of the income, in which he has power to acquire the beneficial interest; or

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 10

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

(c) is payable to or accumulated for, or applicable for the benefit of, a child or children of that person who is or are under the age of 18 years.

102(3) Where this section is applied to the assessment of income of a trust estate or part thereof derived in the year of income, no beneficiary shall be assessed in his individual capacity in respect of his individual interest in the income or part to which this section has been so applied, and the trustee shall not be assessed in respect of that income or part otherwise than under this section.

The first issue that may be drawn from section 102 is:

Practice Point

The settlor must not be a person who has any control or may in the future be capable of having any control over the whole or any part of the trust.

In an ordinary family discretionary trust situation, section 102 makes it clear that the settlor should not be the mum, the dad, or any relative of them. And for a unit trust, it certainly should not be a person who is or may become a unitholder.

But isn’t it just a name that is required, someone who says that they will act as settlor?

Isn’t the name enough?

The question, for section 102 purposes, is not who is the person named as settlor, but who is the settlor at law.

Thus, even though the accountant or solicitor may be named as the settlor, if it can be shown that the true source of the settlement sum came from the principal or guiding mind behind the trust (through perhaps being able to show that the solicitor or accountant charged the settlement amount paid by them as a disbursement), then the truth will prevail and section 102 will have application as though the true settlor were in fact named in the trust deed.

Compare case 16 TBRD Case R40:

Pursuant to applications signed by Y per X, his father, shares were allotted in Y’s name, the subscription moneys being supplied out of X’s private bank account, X’s private ledger indicating a loan to Y in that amount. Subsequently, the company’s articles having been amended permitted X to compel the transfer to him or his nominees of any shares, Y’s shares were transferred to X for a sum (at valuation) in excess of cost, the amount being credited to Y in X’s ledger leaving a credit balance in Y’s favour. Later, a holding company was formed and shares were allotted to A and B who declared in writing that they held them in trust for Y, then 21/2 years old. The subscription moneys were again paid out of X’s bank account and debited to Y’s account in his ledger. Held, by majority, the funds used to purchase the holding company’s shares were provided by X out of his funds and therefore he was creator of the trust and was properly assessed pursuant to sec. 102(1)(b). (1965) 16 T.B.R.D. Case R40.

[Extracted from CCH Federal Tax Reporter 30,510.]

Thus, the question is not who is the person named as settlor but rather who in fact is the settlor.

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 11

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

This is a genuine role, requiring a true gifting of the initial trust property for the purposes expressed in the trust deed. For this reason, it is appropriate that the settlor well understand the intent of their actions and the substance of the question that they are asking of the trustee.

Where this approach is followed, the parties and beneficiaries to the trust may be confident that the Taxation Office will not succeed in any challenge based upon section 102 of the Tax Act.

Practice Point

The settlement sum or property over which the trust is created must genuinely be gifted, there must be no expectation of reimbursement.

How much should the settlement sum be? That is an issue of the generosity of your settlor, certainly it should not be a trifling amount.

A mere nominal amount, it could be argued, is not sufficient to sustain the commencement of a trust. This, in my view, may support an argument that there was never in fact any intention by the settlor to establish the trust. They merely gifted money at the request of a family friend for a purpose that they may not have understood.

Of course, what is a trifling amount is a question of degree, and will no doubt differ among many people. For what it is worth, my preference is for the settlement amount to be not less than $100.

Who is preferable as the settlor? — Discretionary Family Trusts

For discretionary trusts, my personal preference for a settlor is a close family friend. Someone who can genuinely say that it was their personal wish to establish the trust, even if at the request of the principal of the family, for the benefit of the family.

Some guidance may be found from the AAT and Federal Court findings in Faucilles 90 ATC 4003 (profiled in further detail later in this paper).

Apart from its finding that John Kakridas intended that the terms of the trust deed should cloak his real intentions, the Tribunal made a clear finding that it was he who caused the trust to be established and was responsible for the manner in which it was structured. Necessarily involved in that finding is that John Kakridas caused Faucilles to execute the deed as trustee and that he procured Julia Sztainbok (his accountant’s wife) to assume the role of settlor and, as such, execute the deed. The settlor clearly played no other role and was not intended to do so.

Julia Sztainbok was not called as a witness before the Tribunal and there was no direct evidence before it as to the circumstances in which she was recruited to assume the role of settlor. In those circumstances, the Tribunal was required to draw inferences from the circumstances surrounding the relevant events. It was, in our opinion, open to the Tribunal, on the material before it, to infer that the settlor had no other intention than to assist John Kakridas in effectuating whatever purpose he had in mind in establishing the trust.

For a transaction to be a sham there must be an intention common to the parties to it that the transaction is a cloak or disguise for some other and real transaction, or sometimes as in Clyne -v- Federal Commissioner of Taxation (1983) 83 ATC 4508 for no transaction at all. It is, as Lockhart J, pointed out in Sharrment Pty Ltd -v- Official Trustee in Bankruptcy (1988) 18 FCR 449 at 454 something which is not genuine or true but false or deceptive.

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 12

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

Where it is alleged that the trusts of a settlement or some of them are a sham, of necessity it will need to be proved that it was the intention of the settlor that the settlement itself be a sham, or in a case such as the present that some of the trusts of that settlement are a cloak or disguise for the real trusts intended to bind the trustee. Commissioner of Stamp Duties -v- Jolliffe (1920) 28 CLR 178 at 181 is clear authority, if authority be needed, for the principle that intention is a necessary ingredient in the establishment of a valid express trust.

The Tribunal found, and it was open for it so to find, that the settlement was brought about by Mr Kakridas; that he “caused” it to be made. That fact, coupled with the fact that Mrs Sztainbok was the wife of the tax accountant to Mr Kakridas and could be expected to give effect to her husband’s client’s wishes, plus the inference which could properly be drawn from their failure to give evidence that the evidence of the accountant and his wife would assist the taxpayer, was sufficient in my opinion to permit the Tribunal to draw an inference as to the intention of Mrs Sztainbok and thereby justify the conclusion reached by the Tribunal that Mrs Sztainbok, like Mr Kakridas, did not intend that the default distribution provision would be effective.

In short, the AAT and the Federal Court placed a great deal on the identity or assumed intentions of the settlor when assessing how to apply tax principles to the trusts in Faucilles.

Who is preferable as the settlor? — Unit Trusts

Where the particular trust is a unit trust then the issue of “who?” turns upon the purpose to which the trust will be put.

Where the principal units in the unit trust are to be held by a superannuation fund, then, consistent with the purpose of the unit trust being a vehicle for investment by the superannuation fund, the superannuation fund trustee is quite acceptable as the settlor. Question, however, the potential application and requirement to comply with the Superannuation Industry (Supervision) Act, 1994.

At section 65 of the SIS Act, a trustee of a superannuation fund “must not give any other financial assistance using the resources of the fund to a member of the fund or a relative of the fund”.

In the context of this section, there is a potential argument that there may be a breach of this SIS rule where the trustee of a superannuation fund is the settlor of a trust, and subsequently the assets of the trust (which originate from the assets of the superannuation fund) are then used by the unit trust to provide mortgage security for a debt by unit holders who are members or relatives of members of the fund.

Whilst the process may nonetheless seem artificial, a conservative approach would suggest that, in such circumstances, the superannuation fund trustee should not be the settlor of the unit trust. If the superannuation fund becomes a unit holder through a subsequent application and allotment, the argument remains available that the superannuation fund did not actively engage in an indirect provision of financial assistance; it was merely a later investor rather than the originator of the trust structure and concept.

In the circumstances of a property investment based unit trust, where the sole unit holders are intended to be husband and wife, once again it is my view that a close family friend would be a suitable settlor.

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 13

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

In my view, there are very few circumstances where I would accept that it would be appropriate for a professional person such as a solicitor or an accountant to be the settlor of a trust. I appreciate that it is a fine line, however the need is to be in a position whereby a settlor, if questioned, can confidently say, “Yes, I was asked to be the settlor and to establish the trust, but I did so gladly, and with the intent that the moneys that I gave would establish the business/investment structure that would benefit my close friend’s family.”

The assumptions arrived upon by the AAT and accepted by the Federal Court in Faucilles should be avoided. Where there is no relationship between the settlor and the principal of the trust, other than one purely pertaining to professional advice, then it seems appropriate that the only reasonable assumption to be drawn is that the trust was established at the request/direction of the principal so as to achieve the known tax benefits.

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 14

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

3. STAMP DUTY LAWS

This part proposes to look at the stamp duty issues which, in my view, are of day to day practical application.

Establishment of a trust – stamp duty issues

Stamp duty applicable upon the creation of a trust is dependant upon the nature of the trust created and the property which may be said to be subject of the trust upon creation.

In New South Wales, the primary provisions relating to stamp duty upon execution of a trust may be found in Chapter 2 of the Duties Act 1997. The form and type of trust will determine whether ad valorum duty is payable or a fixed nominal rate only. Ad valorem duty will apply to the extent that there is a declaration of trust involving a change in beneficial ownership of dutiable property (refer section 8, 9, and 11). Other forms of stamp duty for trusts in Chapter 2 are found in section 54 to 59.

Form over substance – Ordinary Trusts

It is critical to understand that an instrument need not give effect to a valid trust at trust law before it can be subject to stamp duty. All that is required is that the instrument the subject of review satisfies the descriptive terms that are expressed under the heading “Declaration of Trust” in subsection 8(3).

‘Declaration of Trust’ means any declaration (other than by a Will or testamentary instrument) that any identified property vested or to be vested in the person making the declaration is or is to be held in trust for the person or persons, or the purpose or purposes, mentioned in the declaration although the beneficial owner of the property, or the person entitled to appoint the property, may not have joined in or assented to the declaration.

The heading “Declaration of Trust” is stated as being applicable to any instrument that refers to property that “is or is to be held in trust” – that is, it has operation in respect of future trusts, it extends to where no property is vested in the trustee and to cases to which no trust is presently operative.

It is not necessary that as at the date of execution by the first party that a validly constituted trust exists. Accordingly, the absence of a validly created trust does not render an instrument a legal nothing and therefore invalid for stamp duty purposes.

It would appear, however, that if the purported trust never comes into existence, the taxpayer can apply for a refund of stamp duty on the basis of a complete failure of the trust.

One of the clearest examples of an instrument being subject to stamp duty in circumstances where it very likely did not create a trust, may be found in Tooheys Ltd -v- Commissioner of Stamp Duties (1961) 105 CLR 602.

In this case, the Directors of Tooheys Limited executed a trust deed for the purpose of creating a superannuation pension fund. The Directors and the General Manager were stated as the first trustees. By clause 4, the company was to contribute an amount of £50,000 at a future date.

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 15

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

Walsh J, in the Supreme Court of NSW noted (and the High Court basically agreed with him) that, as at the date of creation, it was not clear:

• if any property was vested in the trustee; and

• whether, in regard to any individual employee, it could be said that an interest in the fund was conferred on him.

It was probable that two essential elements of a valid and effective trust at trust law were absent: property and beneficiaries. At trust law, it is commonly recognised that there are four essential elements to any validly created trust:

1 Trustee;

2 Property;

3 Beneficiaries; and

4 Trustee Duty.

It is often said that the existence of the trustee duty (found at trust law and in the trust deed) binds each of the other three elements together in the creation of a trust. In Tooheys case, upon execution there appeared to be neither property nor beneficiaries. It accordingly followed that, at trust law, no trust existed as at the date of execution.

The judgment does not clearly express this point, however, it would at least appear arguable that the promise under a trust deed by Tooheys Limited to contribute £50,000 at a future date would give rise to property which could be the subject of the superannuation pension trust. Even if this argument was accepted however, the absence of members would still render the document incapable of creating a legal trust as at execution.

Notwithstanding that it was accepted that no trust was created, the document was liable to stamp duty following first execution pursuant to paragraph 2(a) of the heading “Declaration of Trust” (now found in subsection 8(3));

the question is not, therefore, whether this deed is, in the ordinary sense of the term, a declaration of trust, but whether it satisfies the statutory definition. It is only to be expected that this description would go beyond the ordinary sense of the term, since ‘ordinary’ declarations of trust are included in the definition of ‘conveyance’, and are thus chargeable without recourse to the provision now under consideration.

From a stamp duty liability point of view, declarations of trust may arise even where there is no real intention to create a trust and where the trust would, in any event, as a result of the general law, be nonetheless imposed upon the trustee. In other words, a liability to stamp duty on a declaration of trust basis may arise where it need not have occurred.

The mere description of a person in a contract as “trustee” for a named beneficiary was enough for the Chief Commissioner to effectively impose “double” stamp duty (once for the conveyance and once for the trust declaration) in Farrar -v- Commissioner of Stamp Duties (1975) 5 ATR 364.

Generally, the ad valorem on declarations of trust can be avoided by taking advantage of the well founded principle that a person who intends to acquire property as a trustee cannot later deny the existence of the trust: Rochefoucauld -v- Boustead [1897] 1 Ch 196.

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 16

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

Practice Point

Tell clients. “If you wish to buy something in a trust do not name the trustee as acting as a trustee, ie do not write on the land contract or share application ‘XYZ Pty Ltd as trustee for the Smith Family Trust’, just write ‘XYZ Pty Ltd’. Let the minutes on the bank records show that the purchase was by the trustee as trustee.”

Form over substance – Bare Trusts

Following the decision of the High Court in Commissioner of Stamp Duties (NSW) -v- Pendal Nominees Pty Limited and Anor 89 ATC 4207, similar form over substance conclusions can be reached when reviewing ‘apparent purchaser’ or ‘bare trusts’.

Bare trusts are often employed where it is necessary to conceal the true owner or purchaser of the property (e.g. shares, land, businesses etc) which is to become the subject of the bare trust. The bare trustee holds the legal ownership of the subject property for the express and absolute benefit of the true owner. The bare trustee has no power or discretion as to the property as regards the true owner.

In my experience, this bare trust approach often arises for example where a second shareholder has been required for Corporations Act purposes and in property developments. In property developments, this arises because a property developer wishes to purchase property without the vendor becoming aware that the purchaser is a person who seeks to develop their property.

The use of a bare trust is significant when it is appreciated that the stamp duty cost of being able to conceal the true identity of the purchaser is only $10.00 (section 55). The commercial application of a bare trust is further enhanced when it is recognised that, for capital gains tax purposes, Section 106-50 of the Income Tax Assessment Act 1997 deems the true owner to be the relevant owner for the purpose of assessing any capital gains tax upon any subsequent disposal by the bare trustee. Section 55 provides:

55 (1) Duty of $10.00 is chargeable in respect of:

(a) a declaration of trust made by an apparent purchaser in respect of identified dutiable property:

(i) vested in the apparent purchaser upon trust for the real purchaser who provided the money for the purchase of the dutiable property, or

(ii) to be vested in the apparent purchaser upon trust for the real purchaser, if the Chief Commissioner is satisfied that the money for the purchase of the dutiable property has been or will be provided by the real purchaser, or

(b) a transfer of dutiable property from an apparent purchaser to the real purchaser, in a case where dutiable property is vested in the apparent purchaser upon trust for the real purchaser who provided the money for the purchase of the dutiable property.

(1A) For the purposes of subsection (1), money provided by a person other than the real purchaser is taken to have been provided by the real purchaser if

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 17

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

the Chief Commissioner is satisfied that the money was provided as a loan and has been or will be repaid by the real purchaser.

(1B) This section applies whether or not there has been a change in the legal

description of the dutiable property between the purchase of the property by the apparent purchaser and the transfer to the real purchaser.

Note: For example, if the dutiable property is land, this section continues to apply if there is a change in the legal description of the dutiable property as a consequence of the subdivision of the land.

(2) In this section, purchase includes an allotment.

A review of the Pendal Nominees decisions in the Supreme Court, the Court of Appeal, and subsequently the High Court confirms that, from a stamp duty point of view, the following rules that must be adopted in any circumstance where it is desired to evidence and have stamped a bare trust relationship:

1. The trustee must appear to be the only purchaser and is acting for them self

The relationship of the bare trustee and true owner should not be expressed in the original purchase documents. Such a relationship must only be expressed after acquisition of the subject property by the bare trustee (apparent purchaser). It is clear that the bare trustee must upon the face of the document pursuant to which they acquire legal title be expressed as the purchaser. Section 55 requires that the bare trustee be expressed in the purchasing document as the purchaser. As happened in Pendal Nominees, if the bare trustee is expressed as being a bare trustee, the concessional stamp duty of $10.00 shall fail and most likely ad valorem stamp duty shall arise.

2. Declare the bare trust before or after the purchase?

Paragraph 55(1)(a)(i) is expressed in the past tense, that is, it only relates to property “vested”, it is necessary that the bare trust only be declared after acquisition by the bare trustee of the subject property. Accordingly, it follows that the document evidencing the bare trust can only be entered into following the acquisition of the subject property. In terms of a property transaction this may be before settlement, but certainly it must occur after exchange of contracts.

Unlike the old apparent purchaser provision contained in the Stamp Duties Act, paragraph 55(1)(a)(ii) recognises that an apparent purchaser declaration of trust may be made in advance of the acquisition. As can be seen from the above quoted extract, an apparent purchaser declaration of trust made in advance of the purchase will only satisfy the criteria “if the Chief Commissioner is satisfied that the money for the purchase of the dutiable property has been or will be provided by the real purchaser”. Having regard to the fact that ad valorem stamp duty will be payable if the Chief Commissioner is not satisfied, great care must be taken when seeking to declare an apparent purchaser declaration of trust prior to entering into any relevant transaction. Since the earlier quoted authority of Rochefoucauld -v- Boustead [1987] clearly supports the principal that a trustee cannot later deny the existence of a trust, it is respectfully suggested that the safer course of action is to prepare and execute the apparent purchaser declaration of trust after the acquisition has been made.

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 18

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

3. Must be able to prove that the true owner actually paid for the purchase

Section 55 requires that the true purchaser be the one who has in fact paid the purchase monies for the property. It is my opinion that this requires a clear audit trail so as to easily prove to the Chief Commissioner of Stamp Duties that the money was in fact provided by the purchaser to the apparent purchaser (bare trustee) and then such monies were passed by the apparent purchaser to the vendor of the subject property. In my conservative experience, it is not sufficient for the true purchaser to arrange a loan and have the loan monies directed to the vendor. Rather, it is safer that the loan funds be drawn by the true purchaser in favour of the apparent purchaser who in turn should draw against these funds and pay the vendor.

Provided the three criteria expressed above are followed, a stamp duty liability of $10.00 only should arise, regardless of the value of the underlying dutiable property over which the bare trust has been expressed.

It is my opinion that a trust document of this nature should not exceed one page. The purpose of the document is to express nothing more than a bare trust; even a lawyer should be able to express this in one page. If the document includes covenants and obligations, the risk arises that the document will be acknowledged as more than that required for the purpose of a bare trust and more than what is necessary for the purpose of section 55. A far greater liability to stamp duty would likely arise under section 8, 9, and 11.

A sample of a bare trust is attached.

“Vested or to be Vested”

The concept of “declaration of trust” in section 8 and the effect of section 9 results in stamp duty based on the ad valorem value of the underlying dutiable property. If sections 8 and 9 do not apply, then it is very likely that section 58 will impose a flat rate of stamp duty of $500.00.

If the section 9 rate of duty applies, the calculation of dutiable value will be based on the property vested or to be vested.

Pendal Nominees once again represents a culmination of many prior stamp duty cases which have looked at the concept of “vested or to be vested”. From this case, and the many that preceded it, the following three principals can be drawn:

1. The property (whether vested or to be vested) the subject of a trust upon which stamp duty is to be calculated has to be both ascertainable and identifiable as at execution. This requirement can now be found within the definition of “declaration of trust” where it states that the declaration must be in respect of “identified property”.

2. “Vested” relates to property which, upon execution of the trust, either vests in the trustee at the point of execution or is already vested in the trustee at that time. For the draftsperson, the phrase “vested” can cause the most problems. As has already been stated, equity will not allow a trustee to deny the existence of the trust. The facts surrounding the way in which the trustee acquired the property is often sufficient to evidence the existence of a trust. As a safeguard, however, a draftsperson may like to restate the fact that the trustee holds the property for the benefit of the beneficiaries. This is where the problem occurs because, in so doing, the trustee will be stating that the property “is vested” in them and is declaring a trust already in existence. Ad valorem stamp duty will be payable in circumstances where it need not have been.

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 19

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

3. The phrase “to be vested” captures any property that is ascertainable and identifiable as at the date of execution which shall be vested to the trustee at some future time.

It is perhaps the latter point for which Pendal Nominees shall be remembered, although it raises and answers a number of other issues as well. Pendal Nominees has extended the “to be vested” principle expressed in DKLR Holding Co. (No. 2) Pty Limited -v- Commissioner of Stamp Duties (NSW) 82 ATC 4125.

DKLR Holding Co. appeared to have left the principle that if there was an expectation existing as at the date of execution over ascertainable and identifiable property that that property would in the future vest in the trustee, the value of that property must be included in any assessment of stamp duty of the relevant trust.

Pendal Nominees accepts this ‘expectation approach’ and extends it to include any property over which there exists a mere futurity of it being vested after execution into the trust.

What does this mean?

Unfortunately, the view adopted by the High Court is not readily capable of application. From a given set of circumstances it is not difficult to identify when the ‘mere futurity’ may exist, however, it is otherwise difficult to describe.

Certainly, some direction may be taken from the intention of the High Court to establish an objective test. Whilst it is not abundantly clear, it would appear that the High Court in Pendal Nominees is seeking to move away from the ‘expectation approach’ which seems to require an objective look at what was the subjective intent of the settlor at the time of the creation of the trust. Perhaps one way of looking at the ‘futurity test’ is to say ‘let the facts speak for themselves, with the benefit of hindsight’.

In view of the above, it is my preference that the documentation which establishes the trust be of such a nature that it reflects, as at the date of execution, that there could not have existed an expectation or mere futurity in respect of property which subsequently was vested into the trust.

Practice Point

Try to manage the trust creation process so as to avoid any inference at the creation time that further property will be settled upon the trust.

Re-settlements

The recent speed and volatility of changes in the Australian tax system has required practitioners to continually update their ideas and business structures. For discretionary trusts, these changes have brought a necessity for the discretionary trust deed to allow the trustee the power to distribute a capital gain, and to differentiate between the different types of income received, and the power to allocate the differing forms of income received to selected beneficiaries. It is by this mechanism that the trustee may have power to allocate franked dividends or capital gains to a beneficiary whose personal income tax position is such as to take advantage.

It is often also required that the trust deed be amended so as to introduce a new beneficiary to which the trustee may make distributions.

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 20

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

In each of the circumstances described above, where the trustee has amended to accommodate these, there exists a very real danger that the trust will have been resettled.

The courts have accepted the view that a settlement includes a re-settlement or reconstitution of trust. Accordingly, it follows that, where a trust deed of variation is such as to constitute a re-settlement, the document evidencing the re-settlement may fall within the definition of a transfer for the purpose of section 8, and accordingly, shall be subject to ad valorem stamp duty.

Subject to how the principles in Buckles case are to applied, the ad valorem stamp duty shall fall upon the whole of the unencumbered value of the property of the trust. Debts and liabilities of the trust are ignored when assessing the ad valorem stamp duty payable.

Can this be avoided where the trustee has power to amend the trust deed by resolution? The answer, very likely is no. Section 10 provides:

It is immaterial whether or not a dutiable transaction is effected by a written instrument or by any other means, including electronic means.

It follows therefore that the issue is not whether or not there is a declaration of trust, the issue is whether or not there is a declaration of trust within the concept of section 8 which has resulted in a change in beneficial ownership of the underlying trust (dutiable) property. Section 10 simply required that there be a declaration of trust resulting in the change of beneficial owner of dutiable property. The form of declaration of trust would appear to be irrelevant.

So what is the re-settlement?

It is easy to recognise but difficult to describe. In the writer’s opinion the best approach is to examine the original and the amending document and ask the question, “Does this amending document amend the charter of future rights and obligations of the parties to the trust deed?” If yes, it very likely will constitute a re-settlement.

The issue most often arises in the context of altering the beneficiaries of a trust, either by addition or exclusion.

From a trust law point of view, the distinction is that a new discretionary beneficiary, by being named as such, possesses nothing more than a mere expectancy. That is, they have an expectancy that the trustee may or may not exercise discretion in favour of them. If the trustee exercises its discretion to benefit beneficiaries, the new beneficiary has an expectancy that they are included within the class of persons whom the trustee may select, but nothing more.

By contrast, a default beneficiary has a contingent interest in that if the trustee does not exercise discretion to benefit any of the named beneficiaries, the default beneficiary shall, by virtue of the trust deed, become entitled to the income or capital over which the trustee had a right to exercise its discretion.

From a NSW stamp duty perspective the fear of ad valorem stamp duty has largely been accommodated under the Duties Act and Revenue Ruling DUT 17. This has been achieved not by a change to the view as to what constitutes a re-settlement; rather it is that for ad valorem stamp duty to apply there needs to be a passing of interest from the current beneficiaries to or from the altered beneficiaries. Without this ‘transfer’ of interest occurring there is no transfer within the context of sections 8 and 9.

Trusts – A 21st Century Look At A Centuries Old Tool Peter Bobbin Page No 21

© Copyright in this document and the concepts it presents is strictly reserved by Argyle Lawyers Pty Ltd, September 2011. Any reproduction, in part or whole, without permission is illegal. This document has been created for the educational benefit of referrers of legal services work to Argyle Lawyers Pty Ltd and to alert readers to the taxation and superannuation services and expertise of the Firm. The concepts expressed are based on the law current as at September 2011 and is subject to change by parliaments, court decisions and revised thinking of relevant regulators of the law. Before relying on any aspect of this document you must ensure that the concepts remain appropriate at that time otherwise you may be negligent. You can avoid this by using the taxation and superannuation services of Argyle Lawyers Pty Ltd!

But the principle of re-settlement remains nevertheless of relevance in the nature of the interests of the beneficiaries and the context of capital gains tax applying to these.

With regard to the income and capital view, it is the writer’s experience that the easiest way to accommodate this, and yet avoid a re-settlement, is to define the concept of income in circumstances that will satisfy the desired approach. Of course, care must be taken so as to achieve the desired Income Tax Assessment Act requirements and avoid the possibility of re-settlement.

The most recent case in this area of law is Nichols Cabramatta Wholesale Stationary Supplies Pty Limited v. Commissioner of Stamp Duties (NSW) 93ATC 4647.