financial highlights diffe nce er ismarket price per share 7.35 6.00 8.50 10.10 10.75 11.78 6.95...

TRANSCRIPT

LOLC

2011/12 REP

OR

TS & A

CCOU

NTS

No. 100/1 Sri Jayewardenepura Mawatha, Rajagiriya, Sri Lanka.

Tel: +94 11 5880880 Fax: +94 11 2865612 / 2868648

www.lolc.com FiNANCiAl HigHligHTS

For the year ended 31 March 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

gROUP

Performance Indicators (Rs. Mn)

Profit before tax 290 402 572 709 998 1,183 1,247 2,841 8,282 10,327

Profit after tax 278 391 575 689 1,050 1,343 1,055 2,385 7,023 8,937

Total assets 7,038 8,987 10,706 16,227 24,484 32,994 46,287 75,371 111,813 145,288

New executions 3,189 4,740 5,591 10,064 13,340 14,320 14,906 21,963 47,392 58,233

Gross portfolio (rentals receivable) 6,867 8,517 10,112 14,806 23,057 29,282 44,824 47,351 70,077 98,941

Deposits from customers – 197 716 1,194 1,746 3,340 5,229 10,095 16,348 25,197

Outstanding borrowings 4,615 5,952 6,634 10,475 17,001 22,887 31,764 38,235 50,813 66,075

Non-performing portfolio 815 883 865 113 137 526 1,933 1,431 1,159 1,702

Return on equity (%) 17 21 27 26 31 30 19 26 37 39

Key Indicators (Rs. per share)

Net asset value per share (adjusted) 3.60 3.92 4.92 6.10 7.96 10.78 12.65 16.63 27.35 40.59

Earnings per share (adjusted) 0.57 0.85 1.21 1.44 2.19 2.82 2.22 3.88 8.08 13.17

COmPANy

Performance Indicators (Rs. Mn)

Profit before tax 256 418 562 677 910 841 582 491 1,898 4,423

Profit after tax 256 418 562 664 987 1,059 505 327 1,523 4,301

Total assets 5,981 7,617 8,747 13,298 20,889 28,996 31,335 29,738 31,153 36,662

New executions 3,189 4,427 4,972 8,858 12,068 12,127 12,170 4,569 5,036 3,926

Gross portfolio (rentals receivable) 6,757 8,082 9,144 12,858 19,851 25,056 25,185 17,958 11,897 7,704

Outstanding borrowings 4,113 5,396 6,025 9,824 16,250 22,273 24,850 23,087 22,379 23,894

Non-performing portfolio 815 883 865 113 137 443 538 769 545 500

Key Indicators (Rs. per share)

Dividends per share 0.33 0.19 0.23 0.30 0.15 0.23 0.28 – – –

Market price per share 7.35 6.00 8.50 10.10 10.75 11.78 6.95 16.50 119.60 54.00

Net asset value per share 3.53 3.88 4.86 6.00 7.77 10.02 10.74 11.42 15.67 24.73

(Times)

Debt to equity ratio 2.45 2.93 2.61 3.45 4.40 4.66 4.87 4.25 3.00 2.03

Interest cover 1.52 1.85 2.56 1.96 1.63 1.28 1.14 1.16 1.80 2.74

Dividend cover 3.30 4.50 5.09 4.64 13.86 9.53 3.79 – – –

LOLC 2011/12 REPORTS & ACCOUNTS

erThe Diffe nce is...

The Diffe nce is...

er

For the year ended 31 March 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Group

Performance Indicators (Rs. Mn)

Profit before tax 290 402 572 709 998 1,183 1,247 2,841 8,282 10,327

Profit after tax 278 391 575 689 1,050 1,343 1,055 2,385 7,023 8,937

Total assets 7,038 8,987 10,706 16,227 24,484 32,994 46,287 75,371 111,813 145,288

New executions 3,189 4,740 5,591 10,064 13,340 14,320 14,906 21,963 47,392 58,233

Gross portfolio (rentals receivable) 6,867 8,517 10,112 14,806 23,057 29,282 44,824 47,351 70,077 98,941

Deposits from customers – 197 716 1,194 1,746 3,340 5,229 10,095 16,348 25,197

Outstanding borrowings 4,615 5,952 6,634 10,475 17,001 22,887 31,764 38,235 50,813 66,075

Non-performing portfolio 815 883 865 113 137 526 1,933 1,431 1,159 1,702

Return on equity (%) 17 21 27 26 31 30 19 26 37 39

Key Indicators (Rs. per share)

Net asset value per share (adjusted) 3.60 3.92 4.92 6.10 7.96 10.78 12.65 16.63 27.35 40.59

Earnings per share (adjusted) 0.57 0.85 1.21 1.44 2.19 2.82 2.22 3.88 8.08 13.17

Company

Performance Indicators (Rs. Mn)

Profit before tax 256 418 562 677 910 841 582 491 1,898 4,423

Profit after tax 256 418 562 664 987 1,059 505 327 1,523 4,301

Total assets 5,981 7,617 8,747 13,298 20,889 28,996 31,335 29,738 31,153 36,662

New executions 3,189 4,427 4,972 8,858 12,068 12,127 12,170 4,569 5,036 3,926

Gross portfolio (rentals receivable) 6,757 8,082 9,144 12,858 19,851 25,056 25,185 17,958 11,897 7,704

Outstanding borrowings 4,113 5,396 6,025 9,824 16,250 22,273 24,850 23,087 22,379 23,894

Non-performing portfolio 815 883 865 113 137 443 538 769 545 500

Key Indicators (Rs. per share)

Dividends per share 0.33 0.19 0.23 0.30 0.15 0.23 0.28 – – –

Market price per share 7.35 6.00 8.50 10.10 10.75 11.78 6.95 16.50 119.60 54.00

Net asset value per share 3.53 3.88 4.86 6.00 7.77 10.02 10.74 11.42 15.67 24.73

(Times)

Debt to equity ratio 2.45 2.93 2.61 3.45 4.40 4.66 4.87 4.25 3.00 2.03

Interest cover 1.52 1.85 2.56 1.96 1.63 1.28 1.14 1.16 1.80 2.74

Dividend cover 3.30 4.50 5.09 4.64 13.86 9.53 3.79 – – –

FinanCial HiGHliGHts

About these RepoRts And Accounts

LOLC is a COngLOmerate with a unique differenCe. it has just taken On, the faCe Of a parent, by beCOming a hOLding COmpany. Of humbLe beginnings tO a Leasing COmpany, it has grOwn tO beCOme the LOCaLLy diversified finanCiaL COngLOmerate Of tOday.

LOLC is simpLy unLike any Other. keeping with the differenCe Of the COmpany, is the distinCtive struCture Of these repOrts and aCCOunts.

the repOrts seCtiOn has been struCtured tO substantiate the differenCe thrOugh narratives.

the aCCOunts seCtiOn features mOre than just the finanCiaL statements. it aLsO Carries aCCOunts On areas suCh as gOvernanCe, risk management and Leadership.

in its entirety the repOrts and aCCOunts is the stOry Of a triumphant year fOregOne and the bright years ahead with fuLL Of prOmise and OppOrtunity.

REPORTSChairperson’s Statement 04Deputy Chairman’s Message 08Group Managing Director/CEO’s Review 16Business Review 24Financial Review 56The ORIX Connection 70Global Funding Partners 72

ACCOUNTSBoard of Directors 76Corporate Management Team 84Operational Management Team 90Annual Report of the Board of Directors on the Affairs of the Company 94Corporate Governance 102Report of the Remuneration Committee 107Report of the Nomination Committee 107Report of the Integrated Risk Management Committee 108

Corporate Governance Committee Report 109Audit Committee Report 110Risk Management with a Vision 111Directors’ Responsibility for Financial Reporting 117Chief Executive Officer’s and Chief Financial Officer’s Responsibility Statement 118Auditor’s Report 119Financial Statements 120

ANNEXESSustainability Report 208Information on the Company’s Real Estate Portfolio and Listed Debentures 217Ten Year Summary 218Summarised Quarterly Statistics 220Value Addition 221Awards 223Milestones 224Group Companies/Directors 227Share Information 231Glossary 233Notice of Meeting 235Corporate Information 236

Form of Proxy enclosedFinancial Calendar Inner back cover

REPORTS

4 LOLC 2011/12 REPORTS & ACCOUNTS

A conglomerate Responsive to Market needs

01.26

chAIRpeRson’s stAteMent It gives me great pleasure to present the report and accounts of LOLC for a

financial year in which the Group maintained steadfast growth in performance through our proactive business model.

It is noteworthy that such growth was in the face of many challenges, including a mixed and unsettled world and domestic

economic situation in which both positive and negative developments were seen.

the globAl econoMy The global economy remained fragile due to the slow growth of the US economy and the

financial turmoil in the Eurozone. Large injections of liquidity by governments in developed economies, coupled with

socio-political tensions in the Middle East and North Africa; caused oil prices to rise, increasing inflationary and fiscal

pressures as well as driving volatility in the financial markets.

However, the growth in Asia has remained better, with China and India continuing to grow strongly despite cautious

measures by the Chinese Government to rein in an economy in danger of overheating. The global economic downturn

had an impact on the Sri Lankan economy as well due to our dependence on exports to developed countries. More than

50% of our exports are to USA and Europe, regions which were impacted in the year under review.

LOLC 2011/12 REPORTS & ACCOUNTS 5

CHAIRPERSON’S STATEMENT

Nevertheless, Sri Lanka, with its strong fundamentals in monetary policy, rebounded quickly. The Government took

immediate action to buoy up the economy by liberalising the exchange rate policy and tightening both monetary and

fiscal policy, thus bringing under control the deficit in reserves that developed during the second half of the year.

The steady growth of worker foreign remittances was a positive factor to this effect.

the gRoup How did LOLC manage to weather these rough seas as an emerging conglomerate? Our strategy

is simple. We anticipate economic trends, work to understand changing customer needs and, most importantly,

stay responsive to the market.

An agile business model allows us to fine-tune our strategy by investing in growth sectors of the economy. In a relatively

short time we have ventured into leisure, construction and renewable energy, whilst expanding our financial services

portfolio further with insurance, stock-broking and factoring. This year, we continued the momentum by adding a

commodity trading company and a leading hotel on the South Coast. LOLC Leisure is looking forward to being an active

player in this sector, an identified key growth area of the Sri Lankan economy.

Our renewable energy portfolio will begin to earn returns in the upcoming months. All these strategic investments were

possible because of the success of our core financial-services business, which generates more than 55% of our income.

We have identified ourselves as the largest non-bank financial institution in the country by growing and diversifying,

often in unconventional ways, in response to changing market conditions. We were the pioneers in leasing to small

and medium enterprises; SMEs are now the largest contributor by sector to the Sri Lankan economy. We remain the

market leader in factoring, another LOLC innovation of particular significance to the SME community. We are also

moving strongly into microfinance, a largely-untapped market in most regions, with a diverse product mix ranging from

asset financing to group loans and now micro insurance - another first from the LOLC Group. The secret of our success

remains our sensitivity and responsiveness to market needs.

6 LOLC 2011/12 REPORTS & ACCOUNTS

the oRIX connectIon ORIX Corporation, a Japan-based multinational, is LOLC’s single largest shareholder.

Since inception, ORIX has always been a pillar of strength, offering support at every level from Board decision making

to routine operations. Compliance and good governance are of primary importance to ORIX Corporation’s Japanese

management, which explains why LOLC is the only financial institution in Sri Lanka to report according to the provisions

of the US Sarbanes-Oxley Act.

It gives me special pleasure to record that LOLC won a Special ORIX Award for Excellent Performance this year out of a field

of 100 overseas ORIX subsidiaries. This is, in fact, the second consecutive year that LOLC has received an accolade from ORIX.

tRIbutes LOLC was also recognised with another prestigious award, this time from the Open Compliance &

Ethics Group (OCEG), an international think-tank that works to promote principled performance among organisations

worldwide. OCEG named LOLC a winner of one of four 2012 GRC (Governance, Risk Management and Compliance)

Achievement Awards, which honour companies that have shown exceptional quality and integrity in terms of governance,

risk management and compliance.

Locally, we were named overall Runners-up at the National Business Excellence Awards 2011. This overall recognition

was achieved in less than three years of first participation of LOLC in the competition.

outlook In 2012 and possibly into 2013, trends indicate that global economic growth will remain subdued despite

signs of improvement in the US economy. Indeed, continuing financial turmoil in the Eurozone may impact other

countries leading to decline in our exports, diminished worker remittances and rises in commodity prices.

CHAIRPERSON’S STATEMENT

LOLC 2011/12 REPORTS & ACCOUNTS 7

Against this backdrop, domestic economic prospects for the year ahead still seem relatively positive so long as a prudent

fiscal and monetary policy stance is maintained. Growth, which topped 8% for two consecutive years for the first time

in history, is expected to slow down this year, though it will likely be higher than in Asia as a whole. Inflation is rising,

but will probably remain in the single digits, though interest rates may spike in the short term.

Investment in infrastructure, especially from the private sector, together with increased focus on education, training and

development and greater stability in the financial sector, particularly the stock market, will be elements essential to the

maintenance of a positive business climate.

As for LOLC, we are eager to exploit the opportunities that arise from the aggressive development goals of the economy,

especially in the regions and in sectors such as leisure, agriculture, construction and renewable energy. With our

flexible business model, extensive footprint, diverse product mix covering the entire financial value chain and a dynamic

workforce led by strong management, LOLC Group is very well poised to take advantage of these opportunities.

AcknowledgeMents I would like to conclude this Report by thanking the Board of Directors, our shareholders,

our staff and management, as well as our funding partners and banks, for their significant contributions to our success.

I thank all our stakeholders for their implicit trust and confidence in us. And as we move forward into the future,

I would like to assure them that LOLC will continue its diligent efforts to deliver value to all stakeholders.

Rohini NanayakkaraChairperson

CHAIRPERSON’S STATEMENT

8 LOLC 2011/12 REPORTS & ACCOUNTS

An open Mind and a Flexible Agenda

deputy chAIRMAn’s MessAge The Chairperson, in her statement to stakeholders this year, describes how

LOLC has evolved itself into a diversified conglomerate to explore opportunities arising from the Government-led efforts

on resurgence and rebuilding the nation.

I thought of sharing more detail on how we adapted to this transformation.

As a long-established major player in the Sri Lankan business landscape, LOLC is no stranger to change. Although

the main drivers of economic growth in the country have remained more or less the same in the last quarter-

century or more, the political and social environment have seen constant and rapid, almost a revolutionary change.

Economic policy, too, has undergone frequent revisions and adjustments, while the dramatic rollercoaster-ride taken by

the world economy in recent years show just how much of a challenge it has been for us, to survive and thrive through

these fluctuating times.

02.07

LOLC 2011/12 REPORTS & ACCOUNTS 9

Our policy on ‘change management’ has always been open-minded and holistic: we follow trends carefully, plan for the

most likely outcomes, but remain prepared for the unexpected. The agility of our business model is an essential factor

of our continued success. For us, the way to face the future is with an open mind and a flexible agenda. Starting out as

a leasing company, we first transformed ourselves into a broad-spectrum financial-service provider, adding lines of

business as opportunity dictated. Now we have gone further, investing in hotels and tourism, construction, agriculture

and plantations, renewable energy, trading and manufacturing and several other growth sectors. Some of these were

through mergers and acquisitions. For others we set up new entities ourselves or in collaboration with strategic partners.

Whatever the details of engagement, we always bring to the table the same professionalism, flexibility of approach and a

strong code of ethical practice.

tAkIng cARe oF the coRe To move successfully from pure financial services to a diversified business portfolio,

we started by nurturing the financial services business itself. Revenue and reputation earned in our core businesses

are what enabled us to diversify in the first place. Even today, 55% of the Group’s income is derived from financial

services. Starting out as a leasing company in the early days of the liberalised economy, we helped revolutionise the

small- and medium-scale sector by financing assets for productive use that were thus self-financing for the customer.

Having made our mark in this sector, we began adding financial services for which a growing economy fuelled demand.

In 2011, we transformed ourselves into a holding company with controlling interest in six firms offering diversified

financial services.

Briefly reviewing our investments in this sector, the two deposit-taking firms, Lanka ORIX Finance PLC and Commercial

Leasing & Finance Ltd. have surpassed expectations especially in terms of portfolio growth and profitability, as has

LOLC Micro Credit Ltd. which enjoys the advantage of competitive debt financing from our international funding

partners. Each of these three companies has its own well-defined market base and service offering. Thus, among them,

they effectively cover most of the microfinance and SME sectors.

DEPUTY CHAIRMAN’S MESSAGE

10 LOLC 2011/12 REPORTS & ACCOUNTS

We strongly believe that the LOLC Group has an important role to play in the future development of the microfinance

sector. This is why we strengthened our focus on this sector in the year under review. This harmonises with the

Government’s post-war development strategy, which is to concentrate on micro-enterprises and the lower end of the

SME sector. Looking at the figures in this sector since the inception of our microfinancing arm in 2009, we see the very

positive results of our efforts.

helpIng custoMeRs RIse up the lAddeR Presence and access are the keys to success in these grassroots

sectors. LOLC reaches out through its well positioned branch network of 183 comprising of main branches,

mini branches, post office and LIOC centres and branches dedicated for gold products and Islamic financing.

Our low cost but unique channel mechanism with Sri Lanka Post, offers the competitive edge not only in terms of reach

but also enhancing service excellence to otherwise untapped micro clientele. Further, we have the liberty to select

any post office for our operations out of 4,600 post/sub post offices across the island, thus ensuring our footprint is

strategically positioned.

We are the largest microfinance entity in Sri Lanka in terms of geographic presence and portfolio size and the largest

agriculture equipment provider through Brown & Company PLC. Microfinance comes in two varieties: asset-backed

and income-backed. Our group loan model is somewhat different to the popular Grameen Bank model. We have a

smaller group with a speedier and more effective step-up loan cycle. At present, 95% of our group loan portfolio

graduate to individual borrowers. This opportunity not only empowers working women in the microfinance sector,

but also facilitates their transition to an SME entrepreneur, alleviating poverty and uplifting the living standards

of their families. In fact, our microfinance model has been a business case, whereby our associate PRASAC, the largest

DEPUTY CHAIRMAN’S MESSAGE

LOLC 2011/12 REPORTS & ACCOUNTS 11

microfinance institution in Cambodia, has continuously transferred the know-how and best practices to their own

business model. Another value addition that was included during the year was our micro insurance initiative. Through

our insurance arm, LOLC Insurance Company Ltd. (LOIC), we were the first to offer a life insurance plan and a loan

protection cover with our microfinance facilities.

Within the first year of its operations since April 2011, LOLC Insurance Company Ltd., with its captive business alone is

already a significant player in the Insurance industry. In particular, as a catalyst to the micro insurance sector and its

potential to grow in leaps and bounds, LOIC has a promising future in the insurance business.

LOLC Investments Ltd. is the Company that carries our strategic investments in different entities. Among other equity

investments, Seylan Bank as well as Diriya Investments which holds a significant stake of Brown & Company PLC

are noteworthy.

We have a bespoke product portfolio for the SME sector. In addition to the conventional leasing and loan products,

we offer working capital solutions such as invoice discounting, cheque discounting and packing credit. As the pioneers

of factoring, we challenge our own status-quo by adding innovative products. This year, we initiated ‘gold cheque’

discounting - a timely solution to SME borrowers to suit their financial needs in rough times by using their existing

assets. And as our customers rise through the SME ranks, we are with them throughout, offering a diversified portfolio

of financial services to their changing demands.

DEPUTY CHAIRMAN’S MESSAGE

12 LOLC 2011/12 REPORTS & ACCOUNTS

LOLC Securities Ltd. (LOSEC), is our newest subsidiary in the year under review. Although, we are not new to the stock

broking business, LOSEC in less than 12 months of operations has become a leading stock broker to be included in the

top 10 brokers based on annualised turnover.

In fact, with revolving credit, savings and fixed deposits, foreign currency deposits, leases, hire purchases, fleet

management, diverse loan products, factoring and working capital, insurance, stock broking, Islamic financing,

microfinancing, pawning and equity investments such as HDFC bank, our range of financial services is broader than ever.

Small wonder, then, that we are the leading non-banking financial institution in Sri Lanka, and the leading microfinance,

Islamic, agricultural and factoring operations of all such entities - in addition to having the largest fleet and the vehicle

restoration centre in our possession.

leveRAgIng ouR stRengths Our dominance in the financial sector is the result of leveraging our strengths in

order to exploit opportunities as they arise. Sometimes these strengths are not the most obvious ones.

For example, as transparency and regulatory compliance have gained in importance in recent years, we have the

advantage of a well-established corporate governance history behind us, thanks to our long-standing affiliation with

ORIX Corporation, an international leasing-based financial group. Since ORIX is listed on both the Tokyo and New York

stock exchanges, we have long been obliged to follow the reporting and compliance procedures and standards imposed

by these entities as well.

Similarly, we have adopted and developed corporate social responsibility practices over the years thanks to our funding

partners, many of whom are international development funds with specific goals relating to social equity, transparency,

DEPUTY CHAIRMAN’S MESSAGE

LOLC 2011/12 REPORTS & ACCOUNTS 13

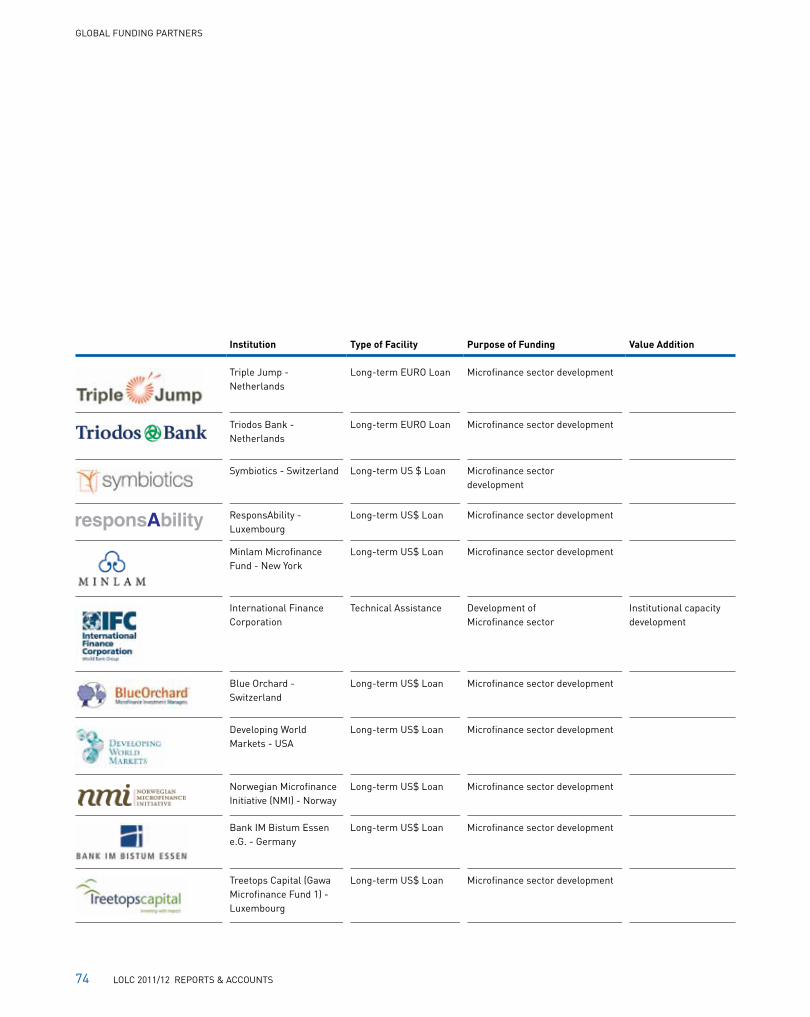

environment, etc. Working closely with our valued, long-term funding partners listed in page 72 have helped us develop

as a responsible corporate citizen. Today, credit from these partners accounts half of our lending, while the rest is

drawn from local commercial sources and our own depositors.

Needless to say, the guidance and assistance both financial and technical offered by ORIX and our long-standing

funding partners have made us what we are today in terms of size, penetration and profile, and I take this opportunity to

sincerely thank them for their confidence in us. We reciprocate their trust by continued financial stability led by sound

profitability, attractive return on investment, swift portfolio growth and above all maintaining one of the best NPL ratios

in the industry.

Into new teRRItoRy The decision to move beyond financial services was not taken lightly. Our main motive

was a desire to align ourselves with the economic goals of the nation, since by doing so we are more likely to secure

long-term operational viability and profitability. The prospect of developing a sustainable value chain by exploiting

synergies between our various investments was another strong inducement.

For example, consider our investment in Brown’s Group. This 137-year-old company is heavily involved in complementary

businesses. We are the largest micro financer and they are the largest agriculture equipment provider. Leveraging its

automotive interests further, Brown’s manufactures vehicle batteries and radiators, the market leader in these product

lines. Together with Browns we maintain a healthy portfolio of investments, ranging from banks to hotels, construction

to forestry; plantation to agri inputs. In partnership with Browns, LOLC now owns the Confifi Group and its portfolio of

hotel properties - Eden, Riverina and Club Palm Garden in addition to Tropical Villas, another hotel closely situated.

We are actively looking for a strategic partner to what might be the largest resort complex in the country on completion

of the proposed development.

DEPUTY CHAIRMAN’S MESSAGE

14 LOLC 2011/12 REPORTS & ACCOUNTS

We also acquired one of the most uniquely-positioned resorts in the Southern Coast - Dickwella Resort & Spa, in the year

under review. Our investment in the leisure sector is long term, with a view to being one of the leading players in the

nation’s most promising sector. Group investments in other areas follow a similar pattern.

The energy policy of the country indicated that by 2020, 100% of the country will be electrified with at least 20% of it

generated via renewable energy sources. Hence our venture into renewable energy with a 75% stake in United Dendro

Energy with its biomass power generating plants and plantation investments. Our decision to go with wood as an energy

source was taken after a careful analysis of geographical potential and the probable future impacts of climate change.

In a similar way, our stake in associate company Sierra Construction was taken on the basis of the growing demand

for large scale construction, their capability for major infrastructure projects. Through Sierra, we ventured into Agstar

Fertilizer, a leading fertilizer and agri input producer. This too is a long-term investment aimed at establishing synergies

with other Group companies and equity partners such as Browns. Our investment in Gal Oya Sugar, a public-private

partnership with the Government of Sri Lanka, follows a similar rationale.

conFIdence to FAce A chAngIng FutuRe Surviving and even thriving in turbulent times has given us

confidence in our ability to withstand changes and challenges the future would hold. In fact, our strength is in

identifying opportunities from these both in our core financial and non-financial areas of business. Overall, we will

continue to drive performance in all our financial services businesses, looking at key indicators such as profitability,

portfolio, NPLs and grassroots impact to steer us in the right direction. You will also see us changing our product mix

gradually from concentrated leasing to a wider range of SME and micro based products to cater the changing needs of

our prime customer base.

DEPUTY CHAIRMAN’S MESSAGE

LOLC 2011/12 REPORTS & ACCOUNTS 15

As for our non-finance businesses, they already contribute 45% of Group income. We will place them at the centre of

our strategic focus, keeping a keen eye out for synergies between them. We have already made our investment choices.

Long-term opportunity and a sense of timing will continue to determine our investment strategy. Continuous restructuring,

internal and external, will keep us agile and sensitive to economic and social currents.

Adapting to change is what we are good at. It is what makes us different!

Ishara NanayakkaraDeputy Chairman

DEPUTY CHAIRMAN’S MESSAGE

16 LOLC 2011/12 REPORTS & ACCOUNTS

Foresight and Fast Footwork

gRoup MAnAgIng dIRectoR/ceo’s RevIew The year under review was an exceptional one for the Group.

We achieved the unprecedented pre-tax profit of Rs. 10 Bn even as we transformed ourselves into a diversified business

conglomerate through strategic expansion and investments. Our success was mainly due to what I call ‘Foresight

and Fast Footwork’ - our often surprising ability to predict market and customer trends by leveraging our knowledge,

experience and intuition, as well as the competitive advantage lent to us by our local and international investment and

funding partners.

Financial services remain at the core of LOLC’s strategic business model. However, the irrepressible and dynamic

nature of the Group has witnessed active diversification into strategic growth areas of national significance such as

renewable energy, leisure, forestry and plantations, microfinance and other key sectors. By aligning its vision with that

of the Government, the Group is on the fast track to pursue its ambition to build one of the strongest conglomerates

in the country. The LOLC Group is confident of reaping the benefits of a resurgent economy poised to benefit from the

ongoing ports, aviation and roads and expressway infrastructure development.

01.51

LOLC 2011/12 REPORTS & ACCOUNTS 17

On the financial services side of the business, strong efforts by our marketing and recoveries teams further

strengthened Group collections ratios, which significantly improved the quality of our loan portfolio. Lanka ORIX

Finance PLC (LOFC), has taken over its parent company’s leasing and financial services business, including fixed

deposits, enabling LOLC itself to function more effectively as a holding company. LOFC has successfully sustained its

non-performing loans (NPL) ratio as among the lowest in the industry.

LOFC was listed in the Colombo Stock Exchange during the year under review. Further the LOLC Group’s subsidiary,

Commercial Leasing, received Central Bank approval to operate as a Registered Finance Company, and to reflect its

new status, the Company‘s name was changed to Commercial Leasing & Finance Ltd.

During the year, our microfinance subsidiary, LOLC Micro Credit Ltd., continued to thrive as its breadth and depth of

grassroots penetration increased by leaps and bounds. The Company was successful in bringing invaluable financial

services to this sector by expanding its branch network further. It was also instrumental in creating opportunities for

rural employment through regular training sessions held at its vocational training school, which equips rural youth to

meet the demands of their chosen vocation.

Our performance in 2011/12 was remarkable because it was such a challenging year in terms of competitive pressure.

Here, our sustainable, low-cost business model enabled us to expand and diversify vertically and horizontally.

Today, LOLC Group offers a full spectrum of non-bank financial products and services which makes it a one-stop shop

for customers looking to benefit from our joint Group synergies.

GROUP MANAGING DIRECTOR/CEO’S REVIEW

18 LOLC 2011/12 REPORTS & ACCOUNTS

GROUP MANAGING DIRECTOR/CEO’S REVIEW

LOLC 2011/12 REPORTS & ACCOUNTS 19

the vAlue oF pARtneRshIp The year was marked by several innovative and lucrative partnership agreements.

Lanka ORIX Finance (LOFC) joined hands with Valutrans Sp.A., a prominent international money transfer firm, in a

strategic expansion of our remittance business that will enable Sri Lankan workers in Italy to remit funds home cost

effectively and in real time, while receiving numerous attractive, value added benefits. Families receiving remittances

can withdraw their money from LOFC’s 64 branches and savings centres as well as from Commercial Bank ATMs

islandwide. These efforts by LOFC to promote remittances are timely in view of the fact that this is the first time that

Sri Lanka has recorded over Rs. 1 Bn in worker remittances.

LOFC also entered into a landmark partnership with the International Fund for Agricultural Development (IFAD),

in collaboration with the World Bank, in a programme to uplift the living standards of Sri Lanka’s rural poor by promoting

financial inclusion among those who seek foreign employment. Finally, completing a series of partnerships designed

to benefit remittance customers, the Company worked together with LOLC Micro Credit Ltd. to offer micro loans for

income generating activities in order to reduce beneficiaries’ dependence on remittances over time and help them

develop sustainable income resources.

GROUP MANAGING DIRECTOR/CEO’S REVIEW

20 LOLC 2011/12 REPORTS & ACCOUNTS

InnovAtIon And outReAch The product and service innovations for which we are reputed played a key role in

building and retaining business relationships. A new working capital product named Gold Cheque Financing was

introduced to offer a feasible option for entrepreneurs who lack property or vehicles as collateral. We reintroduced

our Shari’ah compliant children’s savings account, Al-Falaah Junior, with many added benefits. Our footprint grew

to encompass a total of 183 locations, including 39 main branches as well as Post Office service centres, Islamic

finance centres and factoring outlets, which include CLC, LOFC and LOMC branches as well. Locations in the North

and East of the country now account for over 25% of this total. LOFC branches were opened in the Northern Province at

Nelliady, Chunnakam and Chavakachcheri and in other parts of the country. Advanced Information and Communications

Technology systems link nodes on the branch network enabled us to offer sophisticated services even to rural customers,

while branch operations are backed by a round-the-clock customer service hotline. Aggressive marketing and

promotions support the efforts of our branch staff to build relationships and business.

we coMe FIRst becAuse ouR people do LOLC people are recruited for skill and competence, and trained

extensively further to meet LOLC customer service standards. Our HR strategy blends training and development,

rewards and promotion with leadership and management that promotes creativity and innovation among all employees.

Our agility and flexibility is made possible entirely by our talented and dedicated people, and we freely acknowledge that

the difference they make lies at the heart of our success.

GROUP MANAGING DIRECTOR/CEO’S REVIEW

LOLC 2011/12 REPORTS & ACCOUNTS 21

sustAInAbIlIty eMbedded Our strategic focus has long been on investing in innovative and sustainable initiatives,

making a visible difference to our stakeholders’ lives and promoting national development. Sustainability lies at the

heart of our operations and to underscore the importance we attach to sustainable operations, LOLC is a signatory to

the UN Global Compact and implements its charter in every aspect of its business.

LOLC headquarters has the largest solar power installation of any commercial building in the country - a 48kW plant that

meets 15% of monthly energy requirements. Our vision of a green energy portfolio consisting of mini hydro, biomass and

solid waste power generation is now becoming a reality through our investment in companies such as United Dendro

Energy and Gal Oya Plantations.

Social value generation is embedded into the LOLC business model, which is based on financial empowerment for rural

farmers, women and small entrepreneurs. We not only provide financial support for such entrepreneurs, but even help

ensure value chain creation by providing strong market linkages for their products.

A further testament of our commitment to sustainability is LOLC Motors’ state-of-the-art automotive workshop that

delivers such benefits as lower electricity and water usage, widespread use of natural lighting, solar power generation

and rainwater harvesting.

The Group now manifests its direct social responsibility commitments through LOLC Care, which will be the conduit

for all future CSR initiatives. Its current focus is on construction and equipping the Madiwela Special Education School

and Home for Boys.

GROUP MANAGING DIRECTOR/CEO’S REVIEW

22 LOLC 2011/12 REPORTS & ACCOUNTS

chAllenges AheAd We see a bright prospect ahead for the leisure industry, of which the recent uptick in

tourist arrivals is merely the first glimmer. Large scale infrastructure developments and the commissioning of the

Southern Expressway are generating opportunities, as the Government’s concentrated focus on tourism has begun

paying dividends. Our strategic entry into the sector two years ago with the acquisition of four hotels on the south coast

demonstrates the Group’s astute assessment of the sector’s future potential. We deepened our sectoral commitment

further during the period under review by acquiring the Dickwella Resort & Spa, a stunningly located 77-room property

in the deep south of the island. LOLC Leisure is already known as one of the largest leisure property owners in the

country. The upgrading of our Club Palm Garden, Riverina and Tropical Villas properties in tandem with several other

LOLC-owned properties along Sri Lanka’s ‘Golden Mile’ will witness the single largest beach resort block and complex

in the country.

outlook LOLC has created strong links between sectors vital for the country’s economic growth and its core

businesses. By aligning its business interests with these sectors, LOLC has placed itself on a strong upward trajectory

that will grow steeper as post-war growth and development begin to show returns.

GROUP MANAGING DIRECTOR/CEO’S REVIEW

LOLC 2011/12 REPORTS & ACCOUNTS 23

AcknowledgeMents In conclusion, I would like to express my sincere gratitude to the Chairperson and Board of

Directors for their wise counsel throughout the year. In a Company that moves with great agility, many vital decisions

have to be taken swiftly and I am grateful for the support from the Board in this regard. I would like to commend

the LOLC team and all Group companies for their responsive alignment with the vision of the Group. Operating in a

competitive sector requires forbearance and a tactical mindset. I am confident that our team will continue to exhibit

both qualities in equal measure through the coming months, thus creating a strong launching pad for future growth by

building on the gains achieved during the year.

Kapila JayawardenaGroup Managing Director/CEO

GROUP MANAGING DIRECTOR/CEO’S REVIEW

24 LOLC 2011/12 REPORTS & ACCOUNTS

we are committed to the grassroots level

busIness RevIew The year that just concluded was filled with both opportunities and challenges. Post-war

economic resurgence gained significant momentum, opening up tremendous opportunities for entrepreneurs and

financiers, especially in the North and East of the country where an immense reconstruction effort is underway.

The LOLC Group was quick to take advantage of these opportunities, looking to expand through organic growth and

strategic acquisitions while consolidating ourselves in the sectors we already inhabit. This expansionary phase is

expected to continue for the short to medium term.

Less encouragingly, the ongoing global recession had its inevitable effect on Sri Lanka’s economic and business

performance. Export-related businesses were particularly affected. The domestic economy also received shocks from

currency devaluation and inflation. The effects of these developments on the financial services sector were mixed,

though its effect on other sectors were generally negative.

Slower growth and high interest rates foreshadow a difficult year ahead. Some sectors of the economy, such as tourism,

services and construction, are likely to do well. A stable political environment and clear economic policy focusing on

agriculture and infrastructure will help drive growth in 2012. For the Group - as well as for its competitors - such a

clear policy direction makes it possible to invest confidently in these sectors, taking advantage of various incentives and

facilities offered by the Government.

Higher interest rates and lower liquidity will probably cause the volumes of non-performing advances to increase across

the financial services industry in 2012, which would pressurise in limiting the growth in lending. The resulting credit

demand will improve prospects for the various financial services businesses of the LOLC Group. In particular, credit

demand in the SME/micro-enterprise sectors are likely to grow, to the benefit of our own SME and micro-enterprise

operations. Our access to attractive lines of long-term credit for SME and micro-enterprise development from

international bilateral and multilateral funding agencies gives us a very strong advantage in these sectors, one we shall

leverage on increasingly in the months to come.

LOLC 2011/12 REPORTS & ACCOUNTS 25

BUSINESS REVIEW

stRAtegIc dIRectIon Our long-term strategy is to pursue growth in sectors that complement our profile in

financial services, where we continue to maintain our strength. However, the tactical means by which this strategy is

implemented will vary in the short to medium term.

In financial services, the main sources of growth will be our channel network, where we will build business by offering

attractive interest rates based on our sources of low cost funds and promote cross-selling by packaging products from

different Group companies as integrated customer service solutions. Effective collections systems and further back-end

integration through insurance, fleet management and vehicle repairs will also help drive growth in financial services.

Beyond this core sector, the Group will continue to consolidate investments already made in leisure, manufacturing

and trading, agriculture and plantations, renewable energy and construction. In all these sectors, we will consolidate

the positions we now hold through recently launched or acquired businesses, building long-term value and looking for

steady growth.

In financial services as well as in other sectors, we will strive to be always within arm’s reach of potential customers at

grassroots level, building infrastructure and honing our systems to achieve this.

FInAncIAl seRvIces While the LOLC Group continues to evolve into a broad-based conglomerate, we will never

lose our core commitment to financial services. It is on the success in this sector that our current expansion has been

founded, and it is from this sector that much of the resources for future growth will be drawn. Accordingly, we paid

increased attention to growth and integration in financial services throughout the year under review, with strategic

investments in accessibility, service provision and backup, information technology and cross-selling. In particular,

we strove to make our products and services evermore accessible to ordinary Sri Lankans all over the country.

26 LOLC 2011/12 REPORTS & ACCOUNTS

Starting with a leased tractor from LOLC, this successful farmer from Kurunegala has now bought his second tractor to grow his agri business.

Growing her cane basket weaving business through a group loan scheme, Devika of Mathugama now employs eight others to help her.

A seamstress from Divulapitiya who doubled her income through group microfinance.

A group microfinance customer in Chilaw harvesting her gotukola cultivation.

Producing savoury snacks that are packed and sold in Balangoda by a group microfinance-supported family business.

Rushika of Mathugama is now on her second cycle of the group microfinance scheme and is expanding her poultry business.

BUSINESS REVIEW

LOLC 2011/12 REPORTS & ACCOUNTS 27

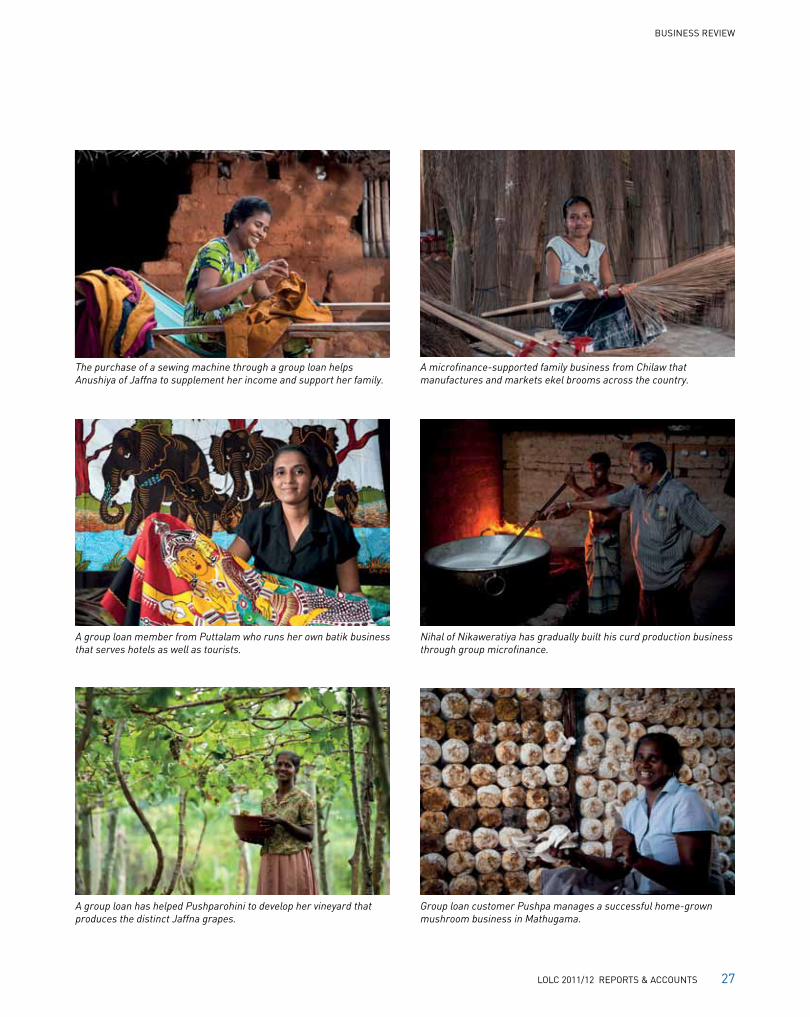

The purchase of a sewing machine through a group loan helps Anushiya of Jaffna to supplement her income and support her family.

A group loan member from Puttalam who runs her own batik business that serves hotels as well as tourists.

A group loan has helped Pushparohini to develop her vineyard that produces the distinct Jaffna grapes.

A microfinance-supported family business from Chilaw that manufactures and markets ekel brooms across the country.

Nihal of Nikaweratiya has gradually built his curd production business through group microfinance.

Group loan customer Pushpa manages a successful home-grown mushroom business in Mathugama.

BUSINESS REVIEW

28 LOLC 2011/12 REPORTS & ACCOUNTS

MIcRoFInAnce Nowhere was our commitment to the grassroots more apparent than in the burgeoning field of

microfinance. In a mere three years, LOLC Micro Credit Ltd. (LOMC) has become the leading microfinance solutions

provider in Sri Lanka, with a loan portfolio of Rs. 12.26 Bn (up from Rs. 8.22 Bn in 2010/11) disbursed through a total

of 100,981 loans, of which 74,821 were in the year under review. The active borrower base, 60% of which is female,

increased by 55%. LOMC also has one of the lowest non-performing loan ratios in the country.

These operations were partly financed by facilities from five international funding partners, amounting to Rs. 2.57 Bn in

total. Meanwhile, the Company’s pawning portfolio, acquired from the sister company Lanka ORIX Finance PLC (LOFC),

grew by 46% to Rs. 1.73 Bn.

In the year under review, LOMC recorded a profit before and after tax of Rs. 818 Mn and Rs. 658 Mn respectively, compared

with last year’s figures of Rs. 554 Mn and Rs. 415 Mn respectively.

Having aggressively expanded its network during the year, LOMC is now active in 23 districts through a total of 34

branches and 95 IsuruDiriya service centres. This strong rural presence also helps create employment opportunities

for local youth: the Company’s 277 loan officers were all recruited from the local towns around the branch network and

deployed in their respective hometowns. To support this initiative, a fully-equipped training and development centre for

loan officers was also set up during the year. In addition, LOMC was proud to be able to provide training for officers of

two overseas ORIX partners namely, Xac Leasing (Mongolia) and BRAC Bank (Bangladesh).

Plans for 2012 call for continued geographical expansion to serve borrowers who do not have access to mainstream

financial institutions - in particular, those resident in the North and East where the Company continues to receive

technical assistance for operational growth under a performance-based grant from the International Finance

Corporation. LOMC now derives 16% of its portfolio from its six branches and 15 service centres in this formerly

war-torn region.

BUSINESS REVIEW

LOLC 2011/12 REPORTS & ACCOUNTS 29

sMAll And MedIuM enteRpRIse FInAnce An important aspect of the LOLC Group’s commitment to national

development is its support for enterprise growth through incremental, need-based access to larger and more

sophisticated financial resources. The first step on this ladder is microfinance, which is the purview of LOMC; here,

at the deep grassroots, customers with no collateral resources guarantee each other’s loans. Once a customer has

outgrown the resources of microfinance, the next step up is to small-and-medium-scale enterprise (SME) financing,

the purview of LOFC.

More than 80% of Sri Lankan enterprises may be described as SMEs. Collectively, they contribute over 30% of GDP in

terms of value addition. The sector makes considerable use of lease financing, and LOLC has played a valuable role in

its development over the years. Our diverse SME portfolio includes customers engaged in agriculture, trading, services

and transport; our exposure to these different sectors is continuously monitored in order to manage risk.

Our operations in this important sector saw substantial growth in the year under review, driven by favourable Government

policy and a climate of economic confidence. Most of this growth was derived from motor vehicle financing, as duty

concessions to certain groups made new vehicles more affordable. Overall, leases and loans in the SME category

amounted Rs. 33 Bn compared with Rs. 20.8 Bn in 2010/11, an increase of 59%. Despite aggressive competitor action,

LOLC retained its edge, largely because of our policy of assessing credit worthiness based on a customer’s cash flow

rather than the collateral he or she can present.

In fact, our credit-assessment process provides a vital competitive advantage. We have developed the means to

gather relevant information from SMEs which, in many instances, cannot produce formal records to justify their

creditworthiness. Industry references and referrals from existing clients are an important part of this process.

Another advantage is our presence at grassroots level. We opened another 26 branches and other outlets during the

year under review, bringing the operating total to 135.

BUSINESS REVIEW

30 LOLC 2011/12 REPORTS & ACCOUNTS

Lease facilities on vehicle purchases, offered through collaborations with selected vehicle dealers, was a key element

of our marketing strategy in 2011-12. These were promoted through media advertising, telemarketing and regional

campaigns. We even entered into a bulk purchasing agreement with a leading commercial vehicle vendor in order to

shorten the delivery period for vehicles purchased with LOFC lease facilities.

In the third quarter of the year, certain Government decisions - increases in interest rates, limits on credit growth by

banks and financial institutions and the devaluation of the Rupee - caused a rise in vehicle prices and a consequent

decline in the demand for lease facilities.

As a result of these policy reversals, Sri Lanka may expect slower growth going forward. Businesses will incur higher

operating costs and margins will shrink. SMEs will be compelled to manage their costs more efficiently, and the LOLC

Group will have to adopt a more conservative approach to credit assessment and the management of exposure.

lAnkA oRIX FInAnce LOFC, a licensed finance company established in 2001, 90% of which is owned by LOLC, is the

main deposit-taking subsidiary of the Group. The Company maintained its growth momentum in the year under review,

with indicators such as deposits, available capital, credit growth, asset quality and profitability all showing impressive

gains. However, a shortage of market liquidity from October 2011 (as discussed above) reduced the overall growth

momentum of the deposit base. Deposits at the end of the year under review amounted to Rs. 25.1 Bn, growing by an

impressive Rs. 7.7 Bn or 44% over the previous year. Foreign-currency deposits did especially well, growing 173% to

reach Rs. 1.96 Bn at year’s end.

BUSINESS REVIEW

LOLC 2011/12 REPORTS & ACCOUNTS 31

Deposit Analysis, F.Y. 2011/12

Category Deposits (Rs. Bn)

Contribution (rounded %)

Fixed Deposits (short-term) 15.20 61Fixed Deposits (long-term) 4.06 16Savings Deposits 0.36 1Foreign Currency Deposits 1.96 8Al-Falaah Deposits 3.52 14Total Deposits 25.10 100

Assets and Liabilities LOFC enjoyed a 58% increase in its asset base, which reached Rs. 38 Bn by year’s end. Most

of this growth came from the accommodations portfolio, comprising finance leases, hire-purchases and other secured

advances, which itself grew by 59% to Rs. 33 Bn. Secured loans were the second highest contributor to asset growth.

Deposits, LOFC’s major source of funding, amounted to 75% of total liabilities, having grown by 44% to Rs. 25 Bn -

one of the largest deposit bases among licensed finance companies. Time deposits accounted for nearly 90% of the base.

Foreign currency deposits showed a spectacular increase. Overall, sustained profitability strengthened the Company’s

capital fund.

Capital & Profits Driven by higher profits and improved profit retention, the equity of LOFC grew by 35% to

Rs. 4.8 Bn. Capital adequacy ratios remained above the statutory minimum. The core capital ratio (as a percentage of

risk-weighted assets) stood at 14.4% at year’s end, in keeping with the industry average, while the ratio of capital to

deposits was 19%.

BUSINESS REVIEW

32 LOLC 2011/12 REPORTS & ACCOUNTS

A Substantial portion of LOLC Group profits under review was derived from the operations of LOFC in the Group’s

core businesses of lending and deposit-taking. At the end of the financial year, LOFC had recorded profit before tax of

Rs. 1.8 Bn, which represents 17% of Group profits and an increase of 20% over the previous financial year’s figure.

Other Lines of Business The contribution of remittances from Sri Lankans employed overseas was of salient

importance in 2011/12. LOFC made a strong contribution to inward remittance growth, handling over US$ 5 Mn

during the course of the year through agreements with exchange houses covering Europe and the Middle East.

The Company also embarked on a financial literacy initiative for beneficiaries of such remittances, supported by a grant

of US$ 245,000 from the Finance for Remittances (FFR) initiative of the International Fund for Agricultural Development

(IFAD). The project, targeting 10,000 migrant worker families, covers financial goal setting, savings, and access to credit

and insurance that will help broaden the Group’s rural customer base.

During the year, LOFC obtained the approval of the Central Bank of Sri Lanka to engage in the business of money

changing, which is now included in its portfolio of services. LOFC is also in the process of implementing a campaign to

promote this new line of business.

Risk Management Credit risk remained low, although non-performing accommodations rose by 5% to Rs. 336 Mn,

mainly due to ‘seasoning’ of the portfolio following rapid expansion. Exposure to NPAs relative to total loans outstanding

declined to 1.01%, a figure that compares very favourably with the industry average of 5.1%. With loan loss provision

considered, the net NPA ratio was 0.73%, compared to an average of 1.9% for the non-bank financial sector. Provision

coverage for NPAs was reduced to 29%.

BUSINESS REVIEW

LOLC 2011/12 REPORTS & ACCOUNTS 33

A single-digit interest rate regime coupled with increased business volumes boosted earnings for most of the

year. Net interest income grew by 123% to reach Rs. 3 Bn; as a percentage of total assets, it had reached 7.9% by

31 March 2012 compared to an average industry margin of 6.4% for the 12 month period ended December 2011.

Liquid assets amounted to Rs 2.95 Bn at the end of the review period, 12% higher than the minimum set by the Central

Bank. Liquid assets in approved securities were maintained at 33% above the stipulated minimum.

Strong and sustained portfolio expansion, augmented by the transfer of LOLC’s finance-leasing franchise, boosted

earnings. Profitability, too, continued to improve. The Company recorded a remarkable profit after tax figure of

Rs. 1.2 Bn. The increase was mainly attributable to business growth derived from LOFC’s expanding network of branches.

Islandwide Presence The year under review saw the Company greatly improve its geographical presence and

accessibility, opening 64 cash-collection centres (Isuru Diriya Centres) at post offices across the country as well as

three savings centres and 13 fully-fledged branches. The number of outlets in the Northern and Eastern Provinces

exceeded thrice over, growing from 8 to 25. Our commitment to financial inclusion was reflected in the operation of

three Al-Falaah centres (see below) in the Eastern Province, where many Muslim Sri Lankans make their homes.

coMMeRcIAl leAsIng And FInAnce ltd. (clc) CLC played a key role in the financial services sector of the

LOLC Group adding value in many fronts in terms of top line and bottom line contribution, island-wide reach, serving a

multitude of customer segments, brand value etc.

CLC’s business model enabled the Company and the Group to reach the clients and markets that have been deprived

of formal finance up to date, thus, developing the rural and newly-developing markets, especially those outside the

Western Province.

BUSINESS REVIEW

34 LOLC 2011/12 REPORTS & ACCOUNTS

The strategy paid rich dividends where the demand for formal credit was high and also backed by the high debt servicing

appetite and capacity. This resulted in high business volumes as well as exceptional collection ratios.

The asset book of CLC grew by 23% during the year from Rs. 21 Bn to Rs. 26 Bn. The non-performing loan ratio

was 2.8% as at 31 March 2012.

The Company recorded a very impressive profit before tax of Rs. 3.2 Bn for FY 2011/12 up from Rs. 741 Mn in the

previous year.

In addition to financial performance, CLC also achieved few key milestones during the year. The highlights of which

include receiving the licence to function as a finance company from the Central Bank of Sri Lanka (CBSL) and the

opening of the 50th branch in the strategic township of Kilinochchi by the Governor of CBSL. With the receipt of finance

company licence, the Company commenced its fixed deposits and savings operations in January 2012. Results to date

indicate that it would be a key player due to high public confidence in the popular CLC brand name developed over the

24-year history of the Company.

CLC Key Indicators

For the year ended 31 March 2012(Rs. Mn)

2011(Rs. Mn)

Increase(%)

Interest Income 5,245 3,402 54Profit Before Tax 3,182 741 329Portfolio Balance 24,104 18,371 31Factoring Portfolio 2,682 2,953 -9

BUSINESS REVIEW

LOLC 2011/12 REPORTS & ACCOUNTS 35

woRkIng cApItAl And FActoRIng Micro-enterprise and SMEs often struggle to find working capital to sustain

ongoing operations and expansion plans. Larger businesses, too, often find themselves short of funds due to delayed

payments from customers and other reasons. Factoring provides a solution for all these entrepreneurs. LOLC Factors

Ltd. (LOFAC) was incorporated to take over the activities of the Working Capital Business Unit of LOLC. Having a separate

firm to handle factoring supports the important shift in the new-business focus of the LOLC Group. For most of its

20-year history, factoring services were offered mainly to corporate customers in the Western Province. Although

LOFAC's first steps into regional markets commenced some years ago, it was the end of the war and the Government’s

declared commitment to rural and regional development that encouraged the Company to make a strong commitment

in this sector. Leveraging the growing branch network of the LOLC Group, LOFAC provided a record number of new

facilities to customers all over the country, successfully cross-selling other financial products through its sister company,

LOFC, at the same time.

The year under review saw LOFAC’s working capital/factoring operation record its highest-ever performance in:

Factoring funds in use

Monthly turnover

Profit per marketing employee

LOFAC also had the lowest expense margin amongst all business units within the Group. Thus, factoring became one of

the highest-yielding Group operations, with the best net return among all our lines of business.

Other highlights of the year included the successful launch of a new product, which brought in many customers

previously thought of as unbankable, by allowing them to offer gold as collateral against their borrowings.

BUSINESS REVIEW

36 LOLC 2011/12 REPORTS & ACCOUNTS

IslAMIc FInAnce LOLC Group’s involvement in Islamic Finance began in response to growing popular demand

for such services. In 2005, the Banking Act made provision for Islamic Finance, giving further recognition and creating

more scope for all stakeholders in the industry to reap the benefits of Islamic finance. With the challenges faced initially,

the scope and the need for a reputable Islamic Financier was immense to re-establish the confidence amongst the

stakeholders and the public at large. Seizing the opportunity, the Group established its Islamic Business Division in

2007. This Division now functions as Al-Falaah, the Islamic Business Unit of Lanka ORIX Finance PLC.

The decision has been borne out by its results. Today, Al-Falaah is a prominent player in an industry where the formal

and informal segments together is estimated to be worth over Rs. 100 Bn. However, more than 70% of Islamic financial

needs are fulfilled by the informal sector and the conventional banking and finance sector. Al-Falaah is moving to tap

this massive potential through the provision of relevant Shari’ah-compliant services at all levels from the grassroots

upward. Currently, Al-Falaah offers fully-Shari’ah-compliant alternatives for term and savings deposits, trade finance,

working capital and import-finance services. By broadening its product mix to include special savings accounts for

senior citizens and minors, the unit plans to serve the entire Muslim community, and ultimately to become the premier

provider of Islamic financial solutions in Sri Lanka.

In the year under review, Al-Falaah achieved its growth targets in deposits and assets. The mudharabah and wakalah

portfolio grew by 22% year on year, from Rs. 2.9 Bn in 2011 to Rs. 3.6 Bn in 2012, while the assets portfolio comprising

Ijarah, Murabaha, Diminishing Musharakah and Musawammah rose in value from Rs. 3.5 Bn to Rs. 4.7 Bn, an increase

of 32%. Collection and NPL ratios also exceeded expectations, the net NPL ratio was maintained at 0.09%.

Due to the efficient and effective management of its assets book, the award winning Al-Falaah Business Unit of LOFC

was able to distribute the highest profit distribution to its Mudharabah account holders. Hence, Al-Falaah was able to

dispel the myth of low returns to Islamic Finance investors through this high profit returns which at times exceeded the

conventional returns.

BUSINESS REVIEW

LOLC 2011/12 REPORTS & ACCOUNTS 37

Overall, the Division’s pre-tax profit showed a twofold increase in the current year compared to last year’s figure of

Rs. 92 Mn.

Operational highlights include the opening of the fifth Al-Falaah centre at Akkaraipattu in April 2012. Future plans include

further broadening of Al-Falaah’s regional and demographic reach, with particular concentration on microfinance for

agricultural and home-based enterprises, while continuing to serve the SME and corporate sectors; increasing the

number of LOLC staff dedicated to Al-Falaah operations and ultimately the establishment of Al-Falaah as an independent

corporate entity under the LOLC Group umbrella.

Al-Falaah is highly committed to run its business in accordance to Shari’ah principles and the Shari’ah Supervisory Board

(SSB) guidelines. This includes quarterly Shari’ah audits, whetting of all transactions by the in-house Shari’ah advisory,

continuous review of processes and procedures by the SSB etc. Al-Falaah intends to be a role model in the industry,

whereby the entire industry will follow suit and ultimately all stakeholders will reap the benefits of Islamic Finance.

Fleet MAnAgeMent Our commitment to providing financial and enterprise support to Sri Lankans in corporate

and other segments of the market across the country are further reflected in our fleet management operations which

we have continued to strengthen over the years. Our three-pronged strategy is to:

serve all segments of the market,

offer attractive rentals on all types of vehicles, and

be self-sufficient in funding asset purchases.

We entered the short-term rent-a-car market a few years ago, hiring out vehicles to walk-in clients as well as to

corporates that rent vehicles for a specified term. The long-term rental portfolio also increased, while our fleet itself

now numbers more than 1,500 vehicles and is still growing. Besides creating a steady, reliable cash flow, the long-term

BUSINESS REVIEW

38 LOLC 2011/12 REPORTS & ACCOUNTS

rental business also realises additional profits from the eventual sale of assets in a market where import duty increases

have raised prices for second-hand vehicles. We also finance the rental of heavy equipment used by the construction

industry. Here our strategy involves disposing of the equipment at the end of its tenure.

Going forward, LOLC will consolidate its positions in the short- and long-term car rental market, continue to augment

its vehicle fleet and introduce value additions such as fuel cards and tracking systems to enhance the efficiency of

customers’ vehicle use. We will also maintain the most important and fundamental value addition to our rental business,

namely our mechanical workshop.

lolc MotoRs Activity in the year under review was dominated by the launch of our new subsidiary, Speed Italia,

which commenced operations in September 2011. Speed Italia markets Fiat automobiles in Sri Lanka, commencing with

an initial order of 70 cars to the Air Force. The launch generated considerable press publicity, which was supplemented

by advertisements for Fiat cars. A radio promotion campaign was conducted in December and January, supported by

more press advertising and local street promotions in Anuradhapura, Jaffna, Kurunegala and Nawalapitiya.

lolc InsuRAnce LOLC Insurance is a new entrant to a highly competitive industry with more than 20 players

in which business volumes grew from Rs. 66.25* Bn in 2010 to an estimated Rs. 78.51 Bn in 2011. The market saw a

substantial growth in General Insurance during the year under review predominantly driven by motor insurance due to

a temporary reduction in vehicle import taxes that drove a boom in vehicle purchases. The industry is now in a period of

regulatory transition, with existing composite insurance companies being required to segregate their life and general

businesses in the next couple of years followed by mandatory listings in the stock exchange whilst rules on solvency

and supervision are also being revised.

* As per IBSL press release on 5 June 2012.

BUSINESS REVIEW

LOLC 2011/12 REPORTS & ACCOUNTS 39

LOLC Insurance obtained a composite insurance licence in 2010 and started writing business in mid-2011. Most of the

year under review was spent in setting up the infrastructure to commence operational activities and opening its office

in Colombo. The Company wrote Life Assurance Policies amounting to Gross Written Premium (GWP) of Rs. 51.4 Mn

and General Insurance GWP of Rs. 364.7 Mn during the period under review and has successfully tied up with leading

international reinsurers for underwriting capacity.

Going forward, LOLC Insurance will be establishing itself in the market as a major player in the industry with a full range

of insurance products and services on offer for both Life and General.

lolc secuRItIes Commencing operations in July 2011, LOLC Securities marks the return of the Group to stock

broking after a two-year hiatus. Leveraging a new operational model centered on investors’ portfolio management

strategies, the Company has captured a significant share of market in a very short period of time. Although it began

operating in a period when the market was declining and highly volatile, it ranked 11th out of 28 stock broking firms in

terms of monthly turnover at the end of the financial year.

In addition to its Colombo Headquarters, LOLC Securities has branches in Galle and Kurunegala and has mobilised

sufficient funds from regional and rural investors to make a positive contribution to its bottom line. The Company plans

to open offices in Kandy and Jaffna in the near future.

Attracting foreign investors to the Sri Lankan equity market is another component of the Company’s strategy: it has

already appointed agents in Malaysia and Dubai and is planning to widen its reach to include India and the United

Kingdom in the near future.

BUSINESS REVIEW

40 LOLC 2011/12 REPORTS & ACCOUNTS

dIveRsIFIed ActIvItIes In a market economy, growth and development depend upon the availability of capital.

Financial services providers thus become facilitators of growth.

This is a vital function as also an intermediary one. Purveyors of finance can have a powerful influence on the character

and direction of development by choosing which sectors, ventures and entrepreneurs they finance. However, this

influence is indirect, and in a reasonably open market for capital, an entrepreneur can usually find a source of funds

with fewer strings attached, especially if he is willing to pay a premium for this.

In the climate of opportunity created by post-war economic revival and with a sense of mission arising from our

commitment to the national agenda, the LOLC Group is no longer content to let its influence on development be wholly

indirect. Behind our recent metamorphosis into a business conglomerate with interests in agriculture and plantations,

renewable energy, leisure and construction is our determination to participate directly in the national effort.

The remaining pages of this Business Review cover our non-financial operations in 2011/12. From ethical tea production,

to renewable energy that lowers the nation’s carbon footprint to essential infrastructure construction projects,

they portray a Group engaged at the heart of Sri Lanka’s development effort and deeply committed to the future.

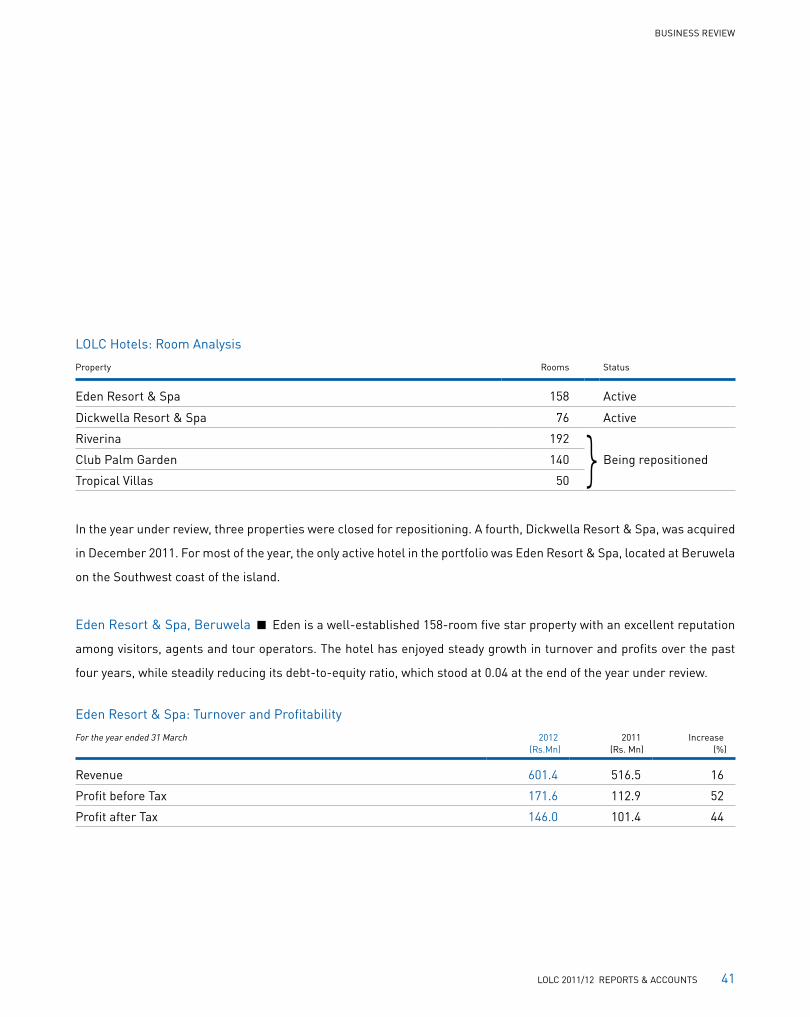

leIsuRe LOLC Group has identified the potential of tourism and has invested aggressively in leisure. The holdings

through LOLC Leisure Ltd., include five existing resort hotels with a combined room inventory of 616.

BUSINESS REVIEW

LOLC 2011/12 REPORTS & ACCOUNTS 41

LOLC Hotels: Room Analysis

Property Rooms Status

Eden Resort & Spa 158 Active

Dickwella Resort & Spa 76 Active

Riverina 192 }Club Palm Garden 140 Being repositioned

Tropical Villas 50

In the year under review, three properties were closed for repositioning. A fourth, Dickwella Resort & Spa, was acquired

in December 2011. For most of the year, the only active hotel in the portfolio was Eden Resort & Spa, located at Beruwela

on the Southwest coast of the island.

Eden Resort & Spa, Beruwela Eden is a well-established 158-room five star property with an excellent reputation

among visitors, agents and tour operators. The hotel has enjoyed steady growth in turnover and profits over the past

four years, while steadily reducing its debt-to-equity ratio, which stood at 0.04 at the end of the year under review.

Eden Resort & Spa: Turnover and Profitability

For the year ended 31 March 2012(Rs.Mn)

2011(Rs. Mn)

Increase (%)

Revenue 601.4 516.5 16

Profit before Tax 171.6 112.9 52

Profit after Tax 146.0 101.4 44

BUSINESS REVIEW

42 LOLC 2011/12 REPORTS & ACCOUNTS

Eden was the focus of intensive marketing and promotional activity throughout the year that witnessed the hotel

achieving its highest-ever profit before and after tax of Rs. 171.6 Mn and Rs. 146.0 Mn respectively. These demonstrate

the capacity and ability of the Company to contribute to the Group.

Dickwella Resort & Spa, Dickwella Acquired in December 2011 at a price of Rs. 1,014 Mn, this luxury 76-room

property is situated on a scenic promontory with the sea on three sides and an extraordinarily attractive beach frontage.

Access has been greatly improved since the opening of the Southern Expressway and planned developments in the

South of the country focused on Hambantota are expected to drive business in the medium term.

Dickwella Resort & Spa enjoyed a very good financial year, the first nine months of which were passed under its

previous owners. Gross annual turnover was Rs. 188 Mn, an increase of Rs. 35 Mn over the figure for the previous

year. The property has considerable potential and plans have been drawn up to expand room capacity to 150 over the

next few years.

Marketing activities for the hotel since its acquisition included telesales and press advertising promoting a weekend

getaway package.

Excel World Development Project The 6-acre Excel World site on Darley Road is ideally located to benefit from the

urban renaissance and renewal taking place around the Beira Lake at the centre of Colombo. Formerly underutilised as

a downmarket entertainment and leisure complex, it is now the focus of an ambitious development plan which includes

entertainment, shopping, conferencing, supermarket, leisure etc.

BUSINESS REVIEW

LOLC 2011/12 REPORTS & ACCOUNTS 43

Looking Forward LOLC Leisure is moving to occupy a strong position in the Sri Lankan tourism sector within the

next medium to long term, by which time it will have approximately 1,000 plus rooms in its portfolio. Most of these will

be in four or five-star hotels or exclusive boutique properties. Our existing properties, Eden Resort & Spa and Dickwella

Resort & Spa, together with the properties under refurbishment and the Kosgoda and Nasuvanthivu-Passekudah

development projects will position LOLC Leisure as a formidable force in the industry.

AgRIcultuRe And plAntAtIons Maturata Plantations Ltd. and Pussellawa Plantations Ltd. are two of the largest

tea producing companies in Sri Lanka.

Maturata Plantations Maturata Plantations operates 19 tea estates, of which significant acreage also accommodate

the cultivation of rubber, coconut and spices. The Company posted a turnover of Rs. 1,981 Mn during the year under

review, with tea accounting for 88% of the total, followed by rubber (10%), coconut and others. Plantations are labour

intensive, and wages are reviewed every two years. The last review in 2011 saw a substantial 30% increase in wages

based on the Collective Agreement between Regional Plantation Companies (RPC) represented by the Employers

Federation and trade unions.

Maturata Plantations recorded a landmark yield of 1,232 kg rubber per hectare in 2011, the best performance among

all RPCs. Further, the Company had the highest new planting of cinnamon for the year, reflecting a crop diversification

strategy which includes the large scale planting of trees for timber on uncultivated lands.

In recognition of its worker-friendly and environmentally sound policies, the Company obtained Ethical Tea Partnership

certification for eight tea factories during the year. Several awards were also won at events organised by the Tea

Brokers, while Maturata Plantations won the Gold, Silver and Bronze awards at the Ceylon Specialty Tea Award

Ceremony held in Moscow in September 2011.

BUSINESS REVIEW

44 LOLC 2011/12 REPORTS & ACCOUNTS

Pussellawa Plantations The principal activities of the firm are the cultivation and processing of tea and rubber

and the cultivation of timber. Its holdings comprise of ten tea plantations, including some historic estates originally

established as coffee plantations in the 1840s, nine rubber estates and five estates planted in a mix of tea and rubber.

The total area under cultivation is 9,165 ha.

The Company recorded a turnover of Rs. 3,546.7 Mn and a profit after tax of Rs. 483.6 Mn for the year. Timber tree

stocks were valued at fair value. Gain on change in fair value of timber tree stocks in the reported profit is Rs. 25.9 Mn.

The year’s results were achieved despite substantial drop in tea prices since April 2011 and rubber prices since

October 2011, and also with a high wage increase granted in April 2011.

Capital expenditure during the year under review amounted to Rs. 533.8 Mn, of which Rs. 432.6 Mn was invested in

re-planting and the maintenance of immature plantations. New plantings during the year consisted of 248 ha in rubber

and 16 ha in tea. In all, immature plantings amounted to 2,003 ha in rubber and 137 ha in tea.

Sustainability is a vital element of the Company’s operating ethos, and sustainable programmes to protect the

environment and improve the quality of life of workers continued to receive priority in the year under review. In 2011/12,

Pussellawa Plantations continued, with its own funding, a worker-housing project originally financed by the Plantation

Development Project (PDP), spending Rs. 13.5 Mn to re-roof 169 worker housing units, upgrade 22 staff housing units