financial analysts’ trip – india 2011 thierry prévot · financial analysts’ trip ... bcg...

TRANSCRIPT

Financial Analysts’ Trip – India 2011

Thierry PrévotGeneral Manager Financial Communications

& Strategic Prospective Analysis

Economy & Prospects1

L’Oréal’s positions3

Agenda

The Asian cosmetics market2

From Shanghai to Mumbai4

- 2 -

- 3 -

- 3 -

Economy

& Prospects

0%

20%

40%

60%

80%

100%

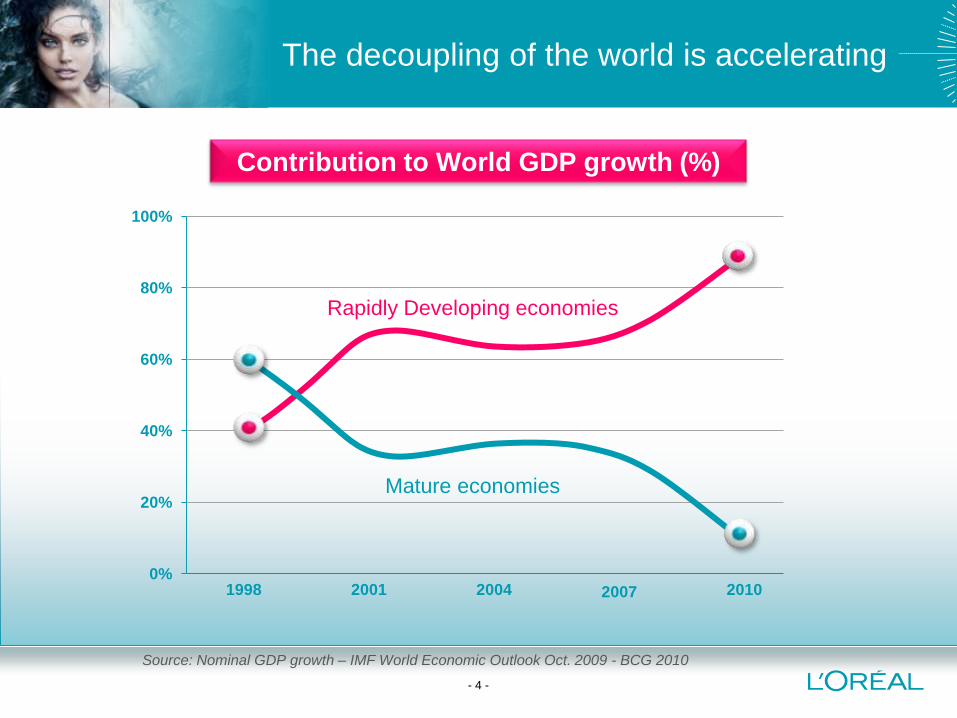

The decoupling of the world is accelerating

- 4 -

1998 2001 2004 2007 2010

Source: Nominal GDP growth – IMF World Economic Outlook Oct. 2009 - BCG 2010

Rapidly Developing economies

Mature economies

Contribution to World GDP growth (%)

The World’s Economic Center of Gravity:

from New York to Shanghai and New-Delhi?

Source: Wolfensohn Center for Development – The Emerging Middle Class in Developing Countries (Homi Kharas) March 2010

- 5 -

Economic Center of Gravity

21st

Century

will be Asian

again

19st

Century

has been

European

20th

Century

has been

American

Asian economies

Key economic indicators (2010)

- 6 -

JapanSouth

KoreaChina Hong Kong Taiwan Singapour India Thailand Indonesia Philippines Vietnam

GDP growth

2009-2010

(%)4.0 6.2 10.3 6.8 11.0 14.5 10.4 7.8 6.1 7.3 6.8

GDP growth

2010-2011

( %)1.4 4.5 9.6 5.4 5.4 5.2 8.2 4.0 6.2 5.0 6.3

Inflation rate

%

(2010)-0.7 3.0 3.3 2.4 1.0 2.8 12.1 3.3 5.1 3.8 9.2

Investments

2011

% GDP21.9 29.1 48.6 24.7 22.4 25.9 39.2 27.9 33.5 15.7 36.4

Trade

balance 2010

(US$ bn)84 48 169 -42 10 45 -110 15 23 -4 -12

Total GDP: IMF, International Financial Statistics. At constant prices, in € at fixed 2010 exchange rates, year-on-year growth

Inflation: IMF, International Financial Statistics. % growth.

Investment: IMF, International Financial Statistics, % of GDP

Trade Balance: The Economist, $US Billion

Total GDP by country (2006-2050)Ranking in terms of total GDP at current exchange rates up to 2010

- 7 -

USA

USA

China

China

Europe G8

Europe G8

India

India

Japan

Japan

2006 2010 2015 2020 2025 2030 2035 2040 2045 2050

N 1 N 1

N 2N 2

N 3 N 3

N 4 N 4

N 8 N 8

Rank 2006 Rank 2050

Source: PwC Research, « The World in 2050 »

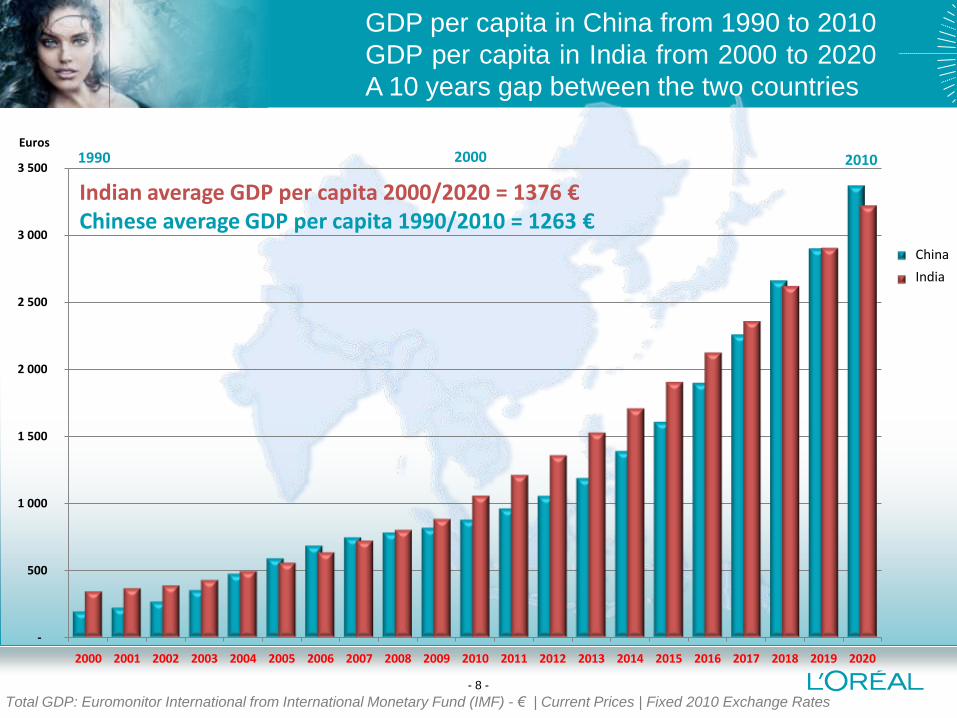

GDP per capita in China from 1990 to 2010

GDP per capita in India from 2000 to 2020

A 10 years gap between the two countries

- 8 -

1990 20102000

-

500

1 000

1 500

2 000

2 500

3 000

3 500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Chine

Inde

Indian average GDP per capita 2000/2020 = 1376 €Chinese average GDP per capita 1990/2010 = 1263 €

Total GDP: Euromonitor International from International Monetary Fund (IMF) - € | Current Prices | Fixed 2010 Exchange Rates

China

India

Euros

Economy & Prospects1

L’Oréal’s positions3

Agenda

The Asian cosmetics market2

From Shanghai to Mumbai4

- 9 -

The Asiancosmetics

market

- 10 -

A dynamic and resilient global cosmetics market*

(annual growth rate, 1995-2010)

- 11 -

*Source: L’Oréal estimates - Excluding soaps and toothpastes. Excluding exchange rate impact

€144bn

+4.2%

20081996 1997 1998 1999 2000 2001 200320021995 2004 20062005 2007 2009 2010

+5.3%+5.4% +5.5%

+5.3%

+4.9%

+4.3%+4.6%

+3.0 %

+3.4%

Worldwide Cosmetics Market* in 2010 (in billion euros)

* excluding soaps , razors, blades and toothpaste

L’Oréal Estimates – On a 2010 higher revised basis.

Translated into euros at foreign exchange rates of 12.31.2010

Europe 5 = France, Germany, UK, Italy & Spain

Next 15 = Argentina, South Africa, Colombia, Thailand, Indonesia, Ukraine, Poland, Saudi Arabia, Egypt, Nigeria, Philippines, Vietnam, Pakistan, Kazakhstan, Turkey

USA

27

Japan

19

China

9

Brazil

9

Europe 5

27

Russia

6.3

India 1.7Mexico 2.7

Next 15

12

- 12 -

80% of the worldwide market in 27 countries

- 13 -

The Asian Cosmetics Market* in 2010 (in billion euros)

Japan

19

Greater China

11.2

India

1.7

South Korea

3.1

ASEAN**

5.2

+1.3%

+7.8%

+8.1%

+16.2%

+8.5%

* excluding soaps , razors, blades and toothpaste

L’Oréal Estimates– On a 2010 higher revised basis.

Translated into euros at foreign exchange rates of 12.31.2010

**ASEAN : including here only Thailand, Indonesia, Malaysia, Philippines, Vietnam and Singapore.

94% of the Asia Pacific market in 5 “clusters”

Yearly cosmetics consumption

in the Asian markets (in euros per capita)

Excluding soaps, toothpastes and razors

L’Oréal estimates – 2010 Net manufacturing prices

Exchange rates at December 31st, 2010

France: €104.2

United States: €88.7

- 14 -

€1.4

€62.9

€6.7

€148.1

IndiaKoreaJapan China

€10.9

Philippines

€20.1

Thailand

€4.3

Vietnam

€5.4

Indonesia

€24.5

Malaysia

€88.6

Singapore

58,066,5

84,9

57,5

6,7

4,8

7,8

4,2

11,7

14,0

1,7

10,2

1,6

0,2

3,2

23,6

13,15,2

24,9

0

10

20

30

40

50

60

70

80

90

100

Japan China India Thailand

Direct sales

Pharmacies

Selective

Hair salon

Mass-Market

- 15 -

Source: L’Oréal estimates - Excluding soaps and toothpastes

Great diversity of the Asian cosmetics markets

in terms of retailing

%

6,1 2,7

13,8

3,7

21,3 29,4

27,8

19,4

18,7 10,6

6,9

14,9

39,2 44,9 31,7

32,2

3,75,2

6,3

12,8

3,7

5,3

8,6 13,21,2

1,9 4,9 3,86,1

0

10

20

30

40

50

60

70

80

90

100

Japan China India Thailand

Others

Fragrances

Hygiene

Body care

Face care

Make up

Hair care

Hair color

- 16 -

%

Great diversity of the Asian cosmetics markets

in terms of categories

Source: L’Oréal estimates - Excluding soaps and toothpastes

- 17 -

The New Countries

Sources of Growth in the Asia-Pacific Zone

Market Growth (2010-2015)

Countries

Market Size in Billion Euros

Growth Factor

2010 2015*

Japan 29.4 29.8 X 1.01

China 14.8 24.1 X 1.63

South Korea 4.8 6.3 X 1.32

India 2.9 5.9 X 2.04

Australia 3.3 3.9 X 1.17

Thailand 2.3 3.5 X 1.49

Indonesia 1.5 3.0 X 1.94

Philippines 1.5 2.1 X 1.43

Total Market 60.5 78.5 X 1.30

Source: Euromonitor (sell out) - *estimates.

Once fundamental needs have been met,

per capita cosmetics consumption grows rapidly

- 18 -

Sources: L’Oréal estimates – IMF World Economic Outlook

United Nations, Department of Economic and Social Affairs, Population Division (2008)

* Cosmetics consumption revised with sanitary equipment rate.

GDP/inhab.

Cosmetics

consumption/inhab*.

GDP growth and per capita cosmetics consumption

150

100

50

01 10 100

Japan

China

INDIA Indonesia

Vietnam

Philippines

Thaïland

South Korea

Per capita GDP (In thousands of US dollars) Per capita cosmetics consumption (US dollars)

A 12 years gap between the

Indian and the Chinese cosmetics market

- 19 -

20151997 2003

Source: Euromonitor – Manufacturing prices- Euros

€ million

0

2000

4000

6000

8000

10000

12000

14000

16000

1997 2000 2005 2010 2015

Chine

Inde

China

India

Asia in the Worldwide Cosmetics Market

From 2005 to 2020 (possible scenarii*)

- 20 -

€144bn€95bn

2020 scenario*20102005

Japan

11.6%

Asia excl. Japan

15.8%Japan

12.9%

Asia excl. Japan

16.9%

Japan

Asia excl. Japan

Sources: L’Oréal estimates

*L’Oréal possible scenario for 2020 – Excluding soaps, razors and toothpastes.

At current exchange rates.(2005-2010)

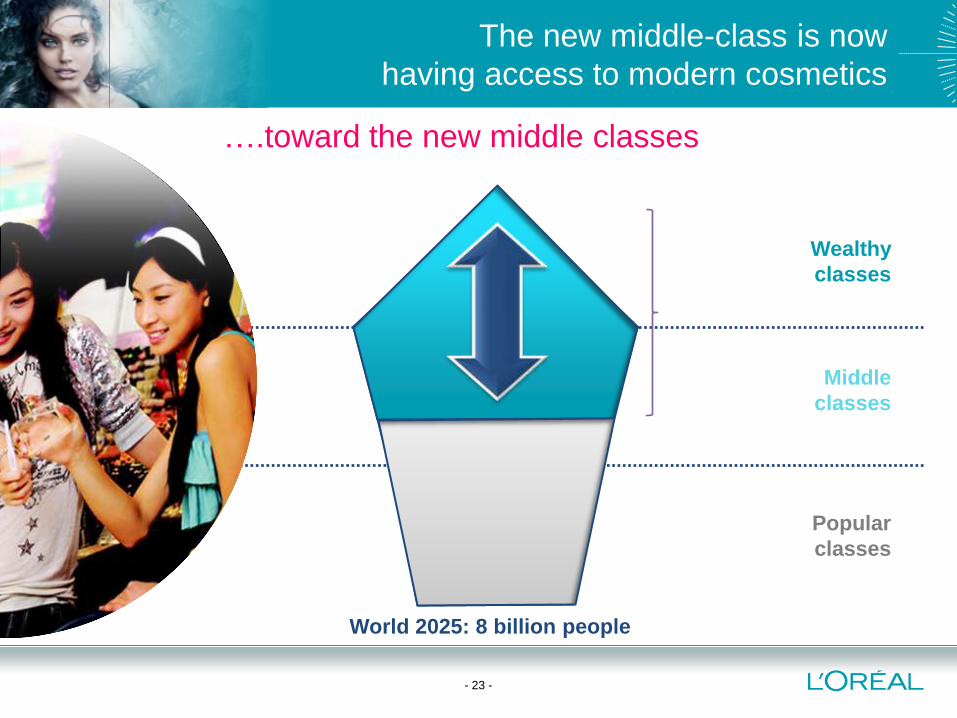

The new middle-class is now

having access to modern cosmetics

- 21 -

From the top of the Pyramid…

Middle

classes

Wealthy

classes

Popular

classes

World 2010: 6 billion people

World 2025: 8 billion people

….toward the new middle classes

The new middle-class is now

having access to modern cosmetics

- 22 -

Middle

classes

Wealthy

classes

Popular

classes

World 2025: 8 billion people

….toward the new middle classes

The new middle-class is now

having access to modern cosmetics

- 23 -

Middle

classes

Wealthy

classes

Popular

classes

Income projections for 2025: more and more consuming and

aspiring social classes, less struggling poor households

- 24 -

Global

Consuming

Aspiring

Struggling

Income segment

per capita ($ PPP)

100,000+

70,000-100,000

35,000-70,000

20,000-35,000

10,000-20,000

7,500-10,000

5,000-7,500

2,000-5,000

1,000-2,000

< 1,000

Number of households

(as a %)

2025

1

19

60

20

0

2007

0

4

32

61

3

Source: McKinsey Research – “Urban World” – 2011

China and India:

the rise of the middle-classes

- 25 -

Affluent

Upper Middle

Mid Middle

Lower middle

Income segment

per capita ($ PPP)

$ 20 per

person a day

$10-$20 per

person a day

$4 to $10 per

person a day

$2 to $4 per

person a day

Source: “The Rise of Asia’s Middle Class”, Asian Development Bank (August 2010)

Estimates based on 2007 data.

Poor< $2 per person

a day

Number of people

Urban+Rural

(as a %)

China

4

19

48

23

6

India

3

4

12

22

59

The privilege of late birth to modernity

● 2010: 89% of urban Chinese have a

mobile phone, 19% have 2 mobile

phones**

● China: 711 million Internet users

in 2020, 419 million today*

● India: 75 million Internet users in

2010*

● Indonesia 2010: 2nd “Facebook

country”**

- 26 -

Sources: * Euromonitor International 2010 / ** Forrester International research.

Economy & Prospects1

L’Oréal’s positions3

Agenda

The Asian cosmetics market2

From Shanghai to Mumbai4

- 27 -

and ?positions

- 28 -

N 8Japan2.6%

N 2China12%

L’Oréal’s market shares in Asia-Pacific Zone (2010)*based on L’Oréal’s evaluation of the global cosmetics market

L’Oréal World: 13.2%

Mature Markets: 16.9%

New Markets: 8.8%

L’Oréal Asia-Pacific: 7.3%excl. Japan: 11.0%

- 29 -

Excluding soaps and toothpastes – source: L’Oréal estimates

N 3India10%

(8% incl. hair oils) Thaïland10%

Philippines3%

Indonesia6%

Vietnam3%

Korea6%

Australia17%

N 2

N 3

N 1

N 3

N 3 N 9

Source: Euromonitor 2011 – Beauty market (excluding soaps, razors & oral care)

L’Oréal’s market share

in Asia-Pacific including Japan: 2001-2010

2.9

7.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

L'Oréal Groupe

%

%

%

%

%

%

%

- 30 -

Source: Euromonitor

L’Oréal

%

Source: Euromonitor 2011 – Beauty market (excluding soaps, razors & oral care)

5.0%

11.0%

0%

2%

4%

6%

8%

10%

12%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

L'Oréal

L’Oréal’s market share

in Asia-Pacific excluding Japan: 2001-2010

- 31 -

Source: Euromonitor

Top competitors by region, in Asia (2010)

- 32 -

Market Leaders in Asia Pacific Sub Zones

Asia-Pacific North Asia Greater China India + ASEAN Pacific

1 Shiseido Kao P & G Unilever L'Oréal

2 Kao Shiseido L'Oréal P & G P & G

3 P & G Kose Shiseido L'Oréal Unilever

4 L'Oréal P & G Unilever Johnson & Johnson Estée Lauder

5 Unilever LG Avon Beiersdorf Revlon

8 L'Oréal

Source: Euromonitor 2010

Economy & Prospects1

L’Oréal’s positions3

Agenda

The Asian cosmetics market2

From Shanghai to Mumbai4

- 33 -

- 34 -

From

Shanghaito Mumbai

- 34 -

A New Era

Universalisation and beauty for everyone

- 35 -

Sources:

* IFOP Nov-Dec. 2009 – Lancôme ”Preferred brand for face care” ; Maybelline “Preferred brand for make-up”

** TNS Sofres Brand image women – 2008 - China

Brand strategy

In China: Lancôme, L’Oréal Paris and Maybelline

LANCÔME

The favourite face care brand*

L’OREAL PARIS

The best brand image**

1 2MAYBELLINE

The preferred make-up brand*

3

- 36 -

GARNIER

The preferred brand of Indian women*

Brand strategy

Garnier, in close relationship with Indian consumers

* TNS Brand image & awareness – 2008- urban women aged 18-45 .

- 37 -

1

2

3

Adapting our product offer:

Accessible innovation and the “Trading Right”

- 38 -

TRADING RIGHT

1. Less ”niche” innovations

2. Highest innovation degree

at the heart of each market

3. A product offer completed

by entry-level products/formats

- 39 -

L’Oréal has 8 R&I centers in Asia

Evaluation centers

Research centers

MUMBAI

THAILAND

SHANGHAI

TOKYOKAWASAKIPUDONG

R&Icenters8

Hair Expertise

BB Cream Opti Straight

UV Expert MEN Powerlight

Turbo Light Oil control

Clearsmooth B.B. Silk

JAPAN CHINA INDIA THAILAND

Magnum Hyperdiamonds

Geocosmetics

Necessity for regional breakthrough innovations

- 40 -

INDIA (Pune)

- 41 -

L’Oréal has 5 factories in Asia

INDONESIA

Consumer Products

Luxury Products

factories5CHINA

JAPAN

Extending to new product categories

Latin America Eastern EuropeEastern Europe

Men cosmetics: Garnier and L’Oréal Paris Men Expert

L’OREAL PARIS MEN EXPERTN 1 in China

N 1 in Western Europe

GARNIER MENIndia, Southern Asia, China

- 42 -

0

200

400

600

800

1000

1200

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Chine

Inde

L’Oréal sales in China and in India:

Heading for € 1 billion L’Oréal sales in India

- 43 -

Source: L’Oréal – Manufacturing prices- Euros

1997 2010€ million

L’Oréal heading for

€1bn sales

in India ?

China

India

-------------------------Avertissement / Disclaimer -------------------------« Ce document ne constitue pas une offre de vente ou la sollicitation d’une offre d’achat de titres L’Oréal. Si vous souhaitez obtenir des informations plus complètes concernant L’Oréal, nous vousinvitons à vous reporter aux documents publics déposés en France auprès de l’Autorité des Marchés Financiers (également disponibles en version anglaise sur notre site Internet www.loreal-finance.com).Ce document peut contenir certaines déclarations de nature prévisionnelle. Bien que la Société estime que ces déclarations reposent sur des hypothèses raisonnables à la date depublication du présent communiqué, elles sont par nature soumises à des risques et incertitudes pouvant donner lieu à un écart entre les chiffres réels et ceux indiqués ou induits dans cesdéclarations.»

"This document does not constitute an offer to sell, or a solicitation of an offer to buy, L’Oréal shares. If you wish to obtainmore comprehensive information about L’Oréal, please refer to the publicdocuments registered in France with the Autorité des Marchés Financiers (which are also available in English on our Internet site: www.loreal-finance.com).This document may contain some forward-looking statements. Although the Company considers that these statements are based on reasonable hypotheses at the date of publication of this release, they are by their nature subject to risks anduncertainties which could cause actual results to differ materially from those indicated or projected in these statements."

Thierry PrévotGroup General Manager, Financial Communicationsand Strategic Prospective AnalysisTel. : + 33 1 47 56 86 22Fax : + 33 1 47 56 74 93email : [email protected]

Françoise LauvinHead of Investors Relations

Tel. : + 33 1 47 56 86 82Fax : + 33 1 47 56 74 93email : [email protected]

- 45 -