financial accounting advisory services - ey€¦ · we work across borders and with our financial...

TRANSCRIPT

Financial Accounting Advisory Services Building and sustaining accounting confidence

March 2015

Page 2 Accounting confidence

Building and sustaining accounting confidence 3 About EY 14 Contacts 16

Agenda

Page 3 Accounting confidence

Building and sustaining accounting confidence

Page 4 Accounting confidence

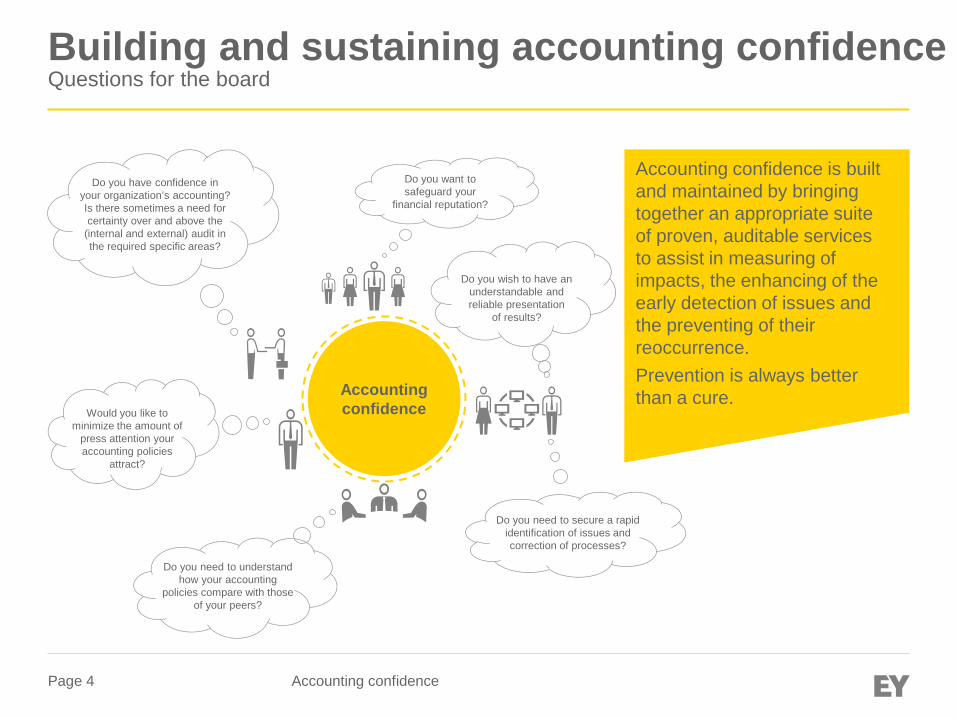

Do you have confidence in your organization’s accounting? Is there sometimes a need for certainty over and above the

(internal and external) audit in the required specific areas?

Would you like to

minimize the amount of press attention your accounting policies

attract?

Building and sustaining accounting confidence Questions for the board

Accounting confidence

Do you want to safeguard your

financial reputation?

Do you wish to have an

understandable and reliable presentation

of results?

Do you need to understand how your accounting

policies compare with those of your peers?

Do you need to secure a rapid identification of issues and correction of processes?

Accounting confidence is built and maintained by bringing together an appropriate suite of proven, auditable services to assist in measuring of impacts, the enhancing of the early detection of issues and the preventing of their reoccurrence. Prevention is always better than a cure.

Page 5 Accounting confidence

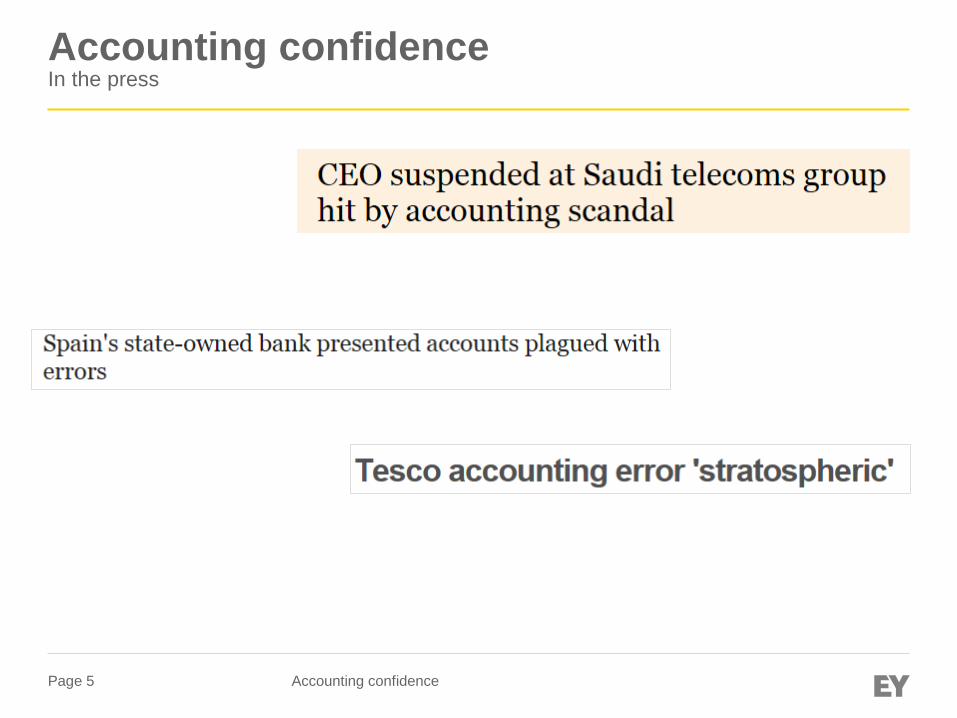

Accounting confidence In the press

Page 6 Accounting confidence

► Accounting confidence dissipates when any of a number of triggers occurs, across a broad spectrum.

► Often, a trigger for action is identified due to a breakdown in controls, but it can sometimes be due to a surprising set of poor results. At times, accounting policies have been pushed to, or even beyond, the limit.

Accounting confidence Spectrum of triggers

Normal accounting tolerance

Fraudulent Aggressive Careless Middle of the road

Overly prudent

Uncomfortable

Page 7 Accounting confidence

Do you recognize these challenges in your company?

Accounting confidence Self-assessment

Possible scenarios Self assessment

Often Sometimes Never

Unexplained results occur at divisional or group level. � � �

Careless mistakes are found in day-to-day accounting, year-end close or journals. � � �

“Rainy day provisions” are still recorded. � � �

Finance teams are uncomfortable in assisting management in achieving market expectations. � � �

Accounting policies are at the far end of the range of policies applied by your peers. � � �

Use of more and more non-GAAP measures to obtain “underlying performance.” � � �

Staff members are rewarded for getting aggressive policies approved by the auditors. � � �

Unexplained or unauthorized accounting entries in the IT system (might there be some, if you were to look?). � � �

Management is alerted by a whistle-blower. � � �

Each of the above may indicate that your accounting confidence may be waning

Page 8 Accounting confidence

Accounting confidence Timing of support

We find that companies often require support in building accounting confidence at the following times:

Before, during or after a transaction (e.g., vendor due diligence or bid defense)

During a period of regulatory change (e.g., moving from a local GAAP to IFRS)

When emerging from tough recession years, during which the focus has been

on achieving budget

When one KPI becomes a “must achieve at all costs” measure

When there are underlying performance issues and clear

communication is important for market stability

When a new CEO or CFO arrives and wants

a reset of policies and to amend their position on

the accounting policy spectrum

Timing of support

Page 9 Accounting confidence

Accounting confidence Your concerns, our solutions

Concerns

► Contract accounting uncertainties, assumptions and judgments

► Balance sheet accounting risks

Our services

► Reviewing contracts along with related accounting models ► Undertaking forensic contract accounting investigations with our Forensic

Investigation and Dispute Services (FIDS) team ► Reviewing accounting treatments and balance sheets for risk

► Aggressive or unusual accounting policies

► Preparing consistent, understandable accounting policies ► Resetting accounting policies to a new position among the peer group ► Ongoing testing and refreshing of policies and procedures

► Unusual journals ► One-off transactions ► Complex areas

► Providing treasury accounting advice and support ► Identifying and unblocking distributable reserves ► Identifying patterns and anomalies in data within the ERP system

► Communication improvements ► Remediation ► Knowledge enhancements

► Positioning the message to the market and to stakeholders ► Amending the year-end close process, particularly focusing on quality of

information ► Refreshing internal audit accounting controls and processes

Page 10 Accounting confidence

Accounting confidence The benefits

Creating accounting confidence breeds confidence throughout the organization, which permeates out to the market.

Confidence in accounting means that you can focus on operational and performance imperatives.

Market stability ► The appreciation of the

markets, which reward openness

► Increased confidence in the minds of investors, analysts and market commentators

Stakeholder confidence ► The appreciation of

stakeholders, who reward openness

► Clarity, with KPIs and management incentives matched to GAAP measures

Quality communication ► Transparent underlying

business performance with high-quality communication

► A chance to reset and to create consistency in global financial reporting

Internal ► Staff retention, through

honesty and integrity ► A repeatable process at

each period end and a smooth, efficient audit of the results

Page 11 Accounting confidence

► EY is uniquely placed to assist companies in recovering from a shock reduction in confidence or putting measures in place to mitigate the risks of such a deterioration occurring.

► We work across borders and with our Financial Accounting Advisory Services (FAAS) team members along with colleagues in Tax, Internal Audit, IT Risk and other teams.

► Projects have already taken place in Europe, the Middle East, North America and Australasia.

► Our global connectivity, practical approach, customer service culture and sensitivity to issues arising are the qualities that our clients most often highlight.

► We will support you in achieving a smooth audit process by ensuring early and frequent communication with your audit team.

Accounting confidence Why EY?

Page 12 Accounting confidence

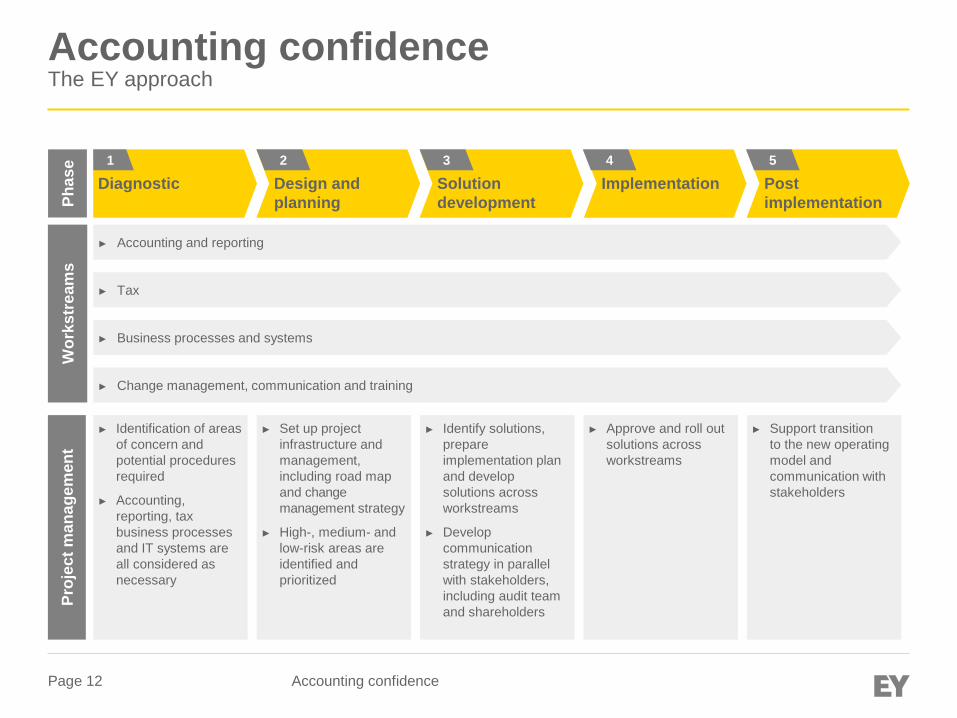

Accounting confidence The EY approach

Phas

e

Design and planning

2

Solution development

3

Implementation 4

Post implementation

5

► Identification of areas of concern and potential procedures required

► Accounting, reporting, tax business processes and IT systems are all considered as necessary

► Set up project infrastructure and management, including road map and change management strategy

► High-, medium- and low-risk areas are identified and prioritized

► Identify solutions, prepare implementation plan and develop solutions across workstreams

► Develop communication strategy in parallel with stakeholders, including audit team and shareholders

► Approve and roll out solutions across workstreams

► Support transition to the new operating model and communication with stakeholders

Proj

ect m

anag

emen

t W

orks

trea

ms

► Change management, communication and training

► Business processes and systems

► Accounting and reporting

► Tax

Diagnostic 1

Page 13 Accounting confidence

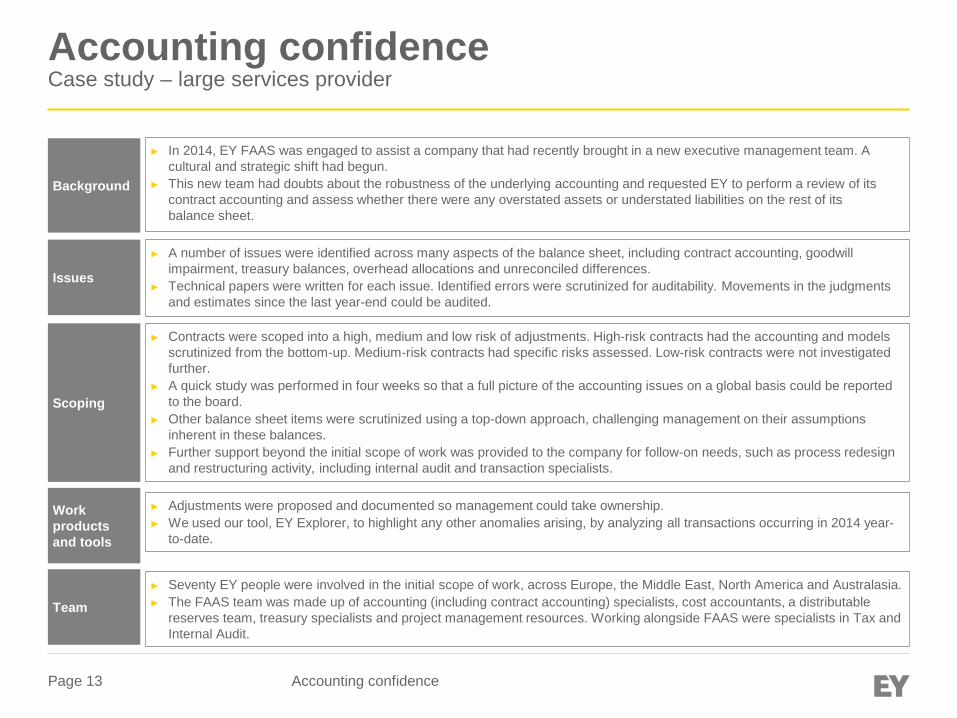

Accounting confidence Case study – large services provider

► In 2014, EY FAAS was engaged to assist a company that had recently brought in a new executive management team. A cultural and strategic shift had begun.

► This new team had doubts about the robustness of the underlying accounting and requested EY to perform a review of its contract accounting and assess whether there were any overstated assets or understated liabilities on the rest of its balance sheet.

Background

Issues

Scoping

Work products and tools

Team

► A number of issues were identified across many aspects of the balance sheet, including contract accounting, goodwill impairment, treasury balances, overhead allocations and unreconciled differences.

► Technical papers were written for each issue. Identified errors were scrutinized for auditability. Movements in the judgments and estimates since the last year-end could be audited.

► Contracts were scoped into a high, medium and low risk of adjustments. High-risk contracts had the accounting and models scrutinized from the bottom-up. Medium-risk contracts had specific risks assessed. Low-risk contracts were not investigated further.

► A quick study was performed in four weeks so that a full picture of the accounting issues on a global basis could be reported to the board.

► Other balance sheet items were scrutinized using a top-down approach, challenging management on their assumptions inherent in these balances.

► Further support beyond the initial scope of work was provided to the company for follow-on needs, such as process redesign and restructuring activity, including internal audit and transaction specialists.

► Adjustments were proposed and documented so management could take ownership. ► We used our tool, EY Explorer, to highlight any other anomalies arising, by analyzing all transactions occurring in 2014 year-

to-date.

► Seventy EY people were involved in the initial scope of work, across Europe, the Middle East, North America and Australasia. ► The FAAS team was made up of accounting (including contract accounting) specialists, cost accountants, a distributable

reserves team, treasury specialists and project management resources. Working alongside FAAS were specialists in Tax and Internal Audit.

Page 14 Accounting confidence

About EY

Page 15 Accounting confidence

Your regional EY network

Africa Angola, Botswana, Cameroon, Chad, Congo, Democratic Republic of Congo, Equatorial Guinea, Ethiopia, Gabon, Ghana, Guinea, Ivory Coast, Kenya, Madagascar, Malawi, Mauritius, Mozambique, Namibia, Nigeria, Rwanda, Senegal, Seychelles, South Africa, South Sudan, Tanzania, Uganda, Zambia, Zimbabwe

Belgium and Netherlands

Germany, Switzerland and Austria

Commonwealth of Independent States Armenia, Azerbaijan, Belarus, Georgia, Kazakhstan, Kyrgyzstan, Russia, Ukraine, Uzbekistan

Central and Southeast Europe Albania, Bosnia and Herzegovina, Bulgaria, Croatia, Cyprus, Czech Republic, Estonia, Greece, Hungary, Kosovo, Latvia, Lithuania, FYR of Macedonia, Malta, Moldova, Montenegro, Poland, Romania, Serbia, Slovakia, Slovenia, Turkey

France, Maghreb and Luxembourg Algeria, France, Luxembourg, Monaco, Morocco, Tunisia

Financial Services Organizations Belgium, Channel Islands, France, Germany, Ireland, Italy, Luxembourg, the Netherlands, Portugal, Spain, Switzerland, the UK

India Bangladesh, India

Mediterranean Italy, Portugal, Spain

Middle East and North Africa Afghanistan, Bahrain, Egypt, Iraq, Jordan, Kuwait, Lebanon, Libya, Oman, Pakistan, Palestinian Authority, Qatar, Saudi Arabia, Syria, Tunisia, United Arab Emirates

Nordics Denmark, Finland, Norway, Iceland, Sweden

United Kingdom and Ireland The UK, the Isle of Man, the Republic of Ireland

Page 16 Accounting confidence

Financial Accounting Advisory Services Contacts

Andy Davies Accounting confidence [email protected] +44 20 7951 3237

EY | Assurance | Tax | Transactions | Advisory

About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2015 EYGM Limited. All Rights Reserved.

EYG no. AU2975

BMC Agency GA 1001806

ED None In line with EY’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com