finance for non-finance professionals session 5

TRANSCRIPT

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 1/46

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 2/46

M.B.A. (Henley)

B.A. (Hons) Management

B.Comm.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 3/46

Finance for the Non-Financial

Professionals

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 4/46

Session 5

• Financing the business operations – Sources of Finance – Capital Gearing – Cost of debt and equity capital

– Weighted Average Cost of Capital – Shareholders’ wealth

• Strategic Management Accounting – Strategy in Accounting

– Financial implications of Business Strategies – The importance of both financial and non-financial

information

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 5/46

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 6/46

Financing the Business Operations

– Sources of Finance

– Gearing

– Cost of debt and equity capital – Weighted Average Cost of Capital

– Shareholders’ wealth

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 7/46

Sources of Finance

• Owners’ Capital

• Share Capital

• Loans• Suppliers

• Other Suppliers

• Retained Profits

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 8/46

Sources of Finance

• Owners’ capital.

• Many organizations start operating with the

owner(s) putting into the business some or

all of their money.

• This capital is used to buy assets which the

organizations subsequently use in the daily

operations of the business.

• Part of this capital is also used to fund the

daily operations through working capital.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 9/46

Sources of Finance

• Share Capital (also referred to as Equity Capital)

• If the respective organization is a limited liability

company, the capital is divided into shares which

are offered to the public for sale.• In exchange for their money, shareholders receive

a share certificate stating that they have a share in

the ownership of the company.

• Share capital represents a guarantee to creditors

that there are specific funds available within the

organization to repay debts that are due.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 10/46

Sources of Finance

• Loans.

• With small companies, loans are often provided from relatives of the owners, whilst

in the case of larger companies, banks normally provide a large amount, although loans from individuals are also obtained.

• All loans are referred to as Loan or Borrowed Capital, and are shown in the Statement of Financial Affairs as Long-Term Liabilities.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 11/46

Sources of Finance

• Suppliers.

• Rather than obtaining money from

suppliers, what happens is that companies

normally delay paying their bills, and so use their liquid funds a little longer than they

should.

• The difficulty with such financing is that suppliers may cease to want to do business

with companies adopting this policy,

particularly in the case of small companies.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 12/46

Sources of Finance

• Other creditors.

• Apart from suppliers, most companies find

that they owe money but have a while before

cash has to be paid out.

• A typical example is company tax on profits,

which is not due until the following year.

Dividends are another example, which are

normally paid at the end of the financial

year.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 13/46

Sources of Finance

• Retained profits.

• Once a business is making profits, these

become the main source of finance that is

generated by the business itself.

• In fact, what is not paid out to suppliers,

government or shareholders is retained

within the business for daily operations as an addition to the organization’s original

capital.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 14/46

Capital Gearing

• Gearing analyses a company’s capital structure. In other words,through gearing it is possible to determine how much of the totalcapital employed is owned by shareholders, and how much of it isowed to third parties through loans, long-term credits and otherlong-term liabilities.

• Such a position is found through a single ratio:

Gearing Ratio: Total Borrowed Capital x 100% Total Share Capital

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 15/46

Capital Gearing

• The question of whether high gearing is better than low gearing is not a clear-cut case.• In times of high profitability, high gearing is preferred

since less shareholding will eventually result in higherdividends being earned.

• However, in times of low profitability, companies withhigh levels of borrowing are at risk since theircommitments will have to be met, irrespective of thelevels of profits earned.

• It is very difficult to determine which is the acceptablelevel of gearing, as this depends on the company, its’products, markets, industry life cycle and eventually thelevel of risk that the owners and directors of thecompany are prepared to take.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 16/46

Cost of Capital

• Cost of capital refers to the minimum expectedreturn that is expected from a specificinvestment.

• The opportunity cost of placing funds in aspecific investment is the major driver behindthe cost of capital.

• However this is also affected by investors’

expectations, level of risk they are prepared totake, alternative investment opportunities andalso the prevalent interest rates of the alternative

investment opportunities.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 17/46

Cost of Debt Capital

• The cost of Debt Capital refers to the interest rate(s)that is payable annually on the loans and other third-party capital that has been invested within theorganization.

• The Debt Capital is normally covered by an agreementthat would have been entered into, and is normally insured through some form of guarantee.

• This guarantee has an effect upon the level and extentof usage of this Debt Capital, which may affect theinvestments opportunities for which the organizationeventually makes use of such capital.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 18/46

Cost of Equity Capital

• The cost of Equity Capital refers to the minimumreturn that owners or shareholders are expecting fromthe equity capital that they have retained within theorganization.

• Such equity capital may take the form of liquid funds,fixed assets, brand names, royalties or any other formof investment that has been made within theorganization.

• Equity capital is also affected by annual increases ordecreases in shareholders’ wealth: the higher theincreases in shareholders’ wealth, the higher will betheir expectations from the organization.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 19/46

Weighted Average Cost of Capital

• WACC is an average of various cost of capitalson the basis of given proportion of differentsources of finance.

• WACC is thus the total sum of all the averagecosts of different sources of capital afterconsidering their individual ratio to the total

capital. These individual ratios are termed as weights.

• WACC is used to reduce the cost of capital,

thereby generating further shareholders’ return.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 20/46

Shareholders’ Wealth

• Shareholders' wealth is basically the wealthshareholders get to accrue from their ownership of shares in a firm.

• One of the principal objectives of a business is toincrease shareholders’ wealth.

• Shareholders’ wealth increases by 2 possible means:

either by increases in share prices that bring aboutcapital gain or increase in dividend payments.

• A frequent indicator of accumulated shareholders’

wealth is the market share price.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 21/46

Strategic Management Accounting has been defined as"a form of management accounting in which emphasisis placed on information which relates to factorsexternal to the firm, as well as non-financial information

and internally generated information." Simmonds (1981)

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 22/46

Strategic Management Accounting

– Strategy in Accounting

– Financial implications of Business Strategies

– The importance of both financial and non-financial information

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 23/46

Strategy in Accounting

• The importance of strategy in Accounting canbe demonstrated through the financial resultsobtained by successful organizations.

• These results are the fruit of specific strategiesimplemented in other areas, which have in turnhad positive effects on the organizations’finances.

• Finance is an important link in an organisation’sstrategic review process.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 24/46

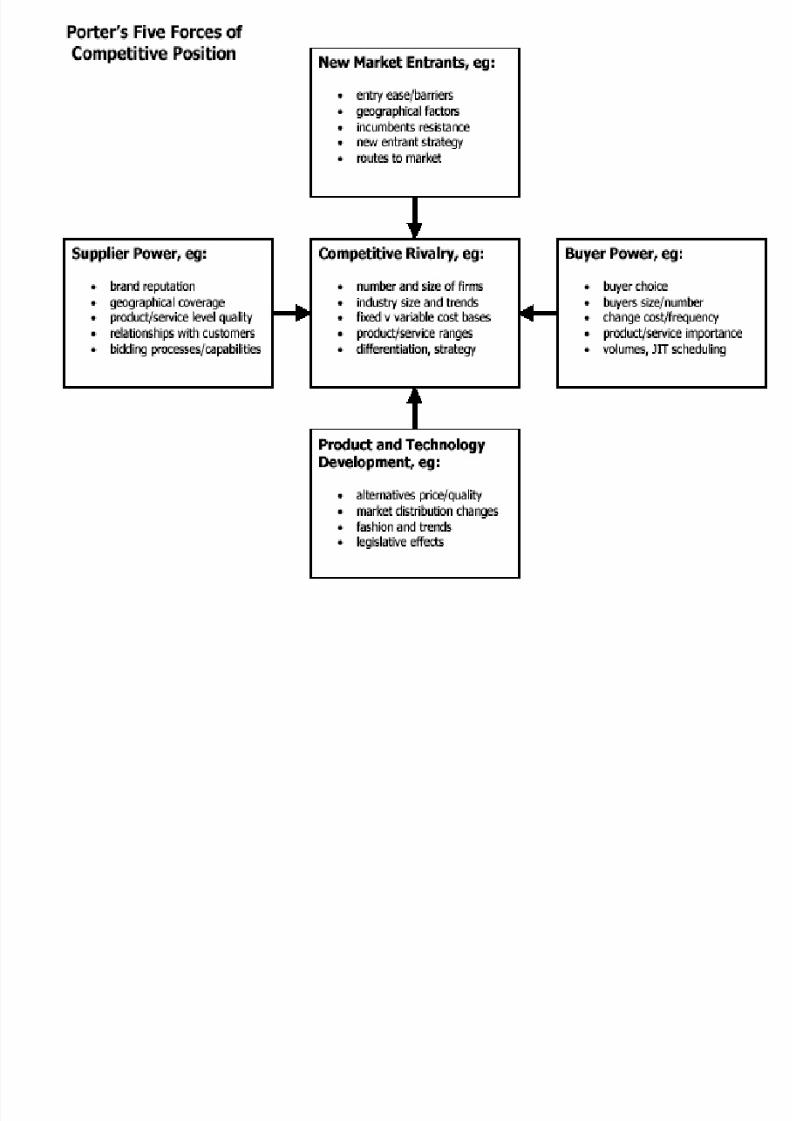

Strategy and Long-Term

Profitability• Porter (1985) assessed different industries in

terms of long-term profitability, and determinedfive competitive forces that contribute to a

strategic equation and long-term profitability.• Threat of New Entrants into the Market

• Threat of Substitute Products/Services

• Rivalry amongst existing organisations within theindustry

• Bargaining Power of Suppliers

• Bargaining Power of Consumers

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 25/46

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 26/46

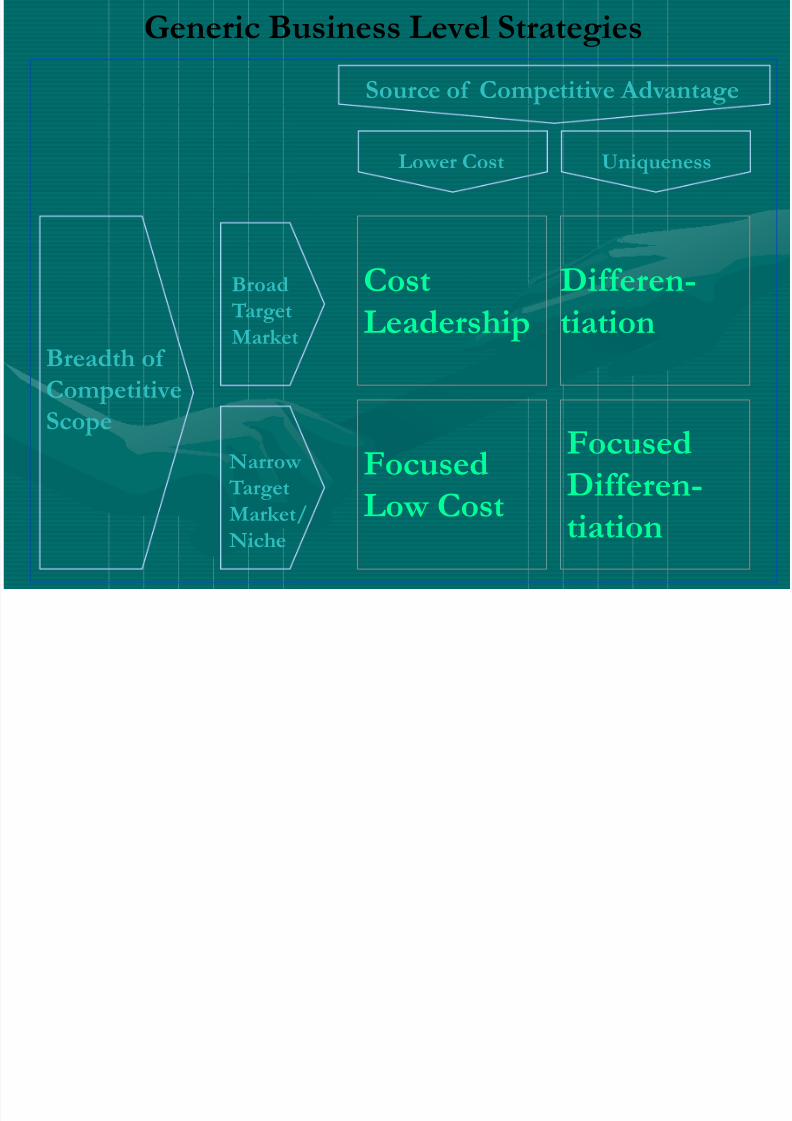

The Organisation’s

Generic Strategy

• Porter (1987) also developed different Genericstrategies that an organisation may pursue within

any specific industry to increase long-termprofitability.

• These are: Cost Leadership, Differentiation andFocus or Niche Strategies.

G i B i L l S i

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 27/46

Breadth of

Competitive

Scope

Source of Competitive Advantage

Broad Target

Market

Narrow

Target

Market/

Niche

Lower Cost

Focused

Differen-

tiation

CostLeadership

Differen-tiation

Focused

Low Cost

Generic Business Level Strategies

Uniqueness

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 28/46

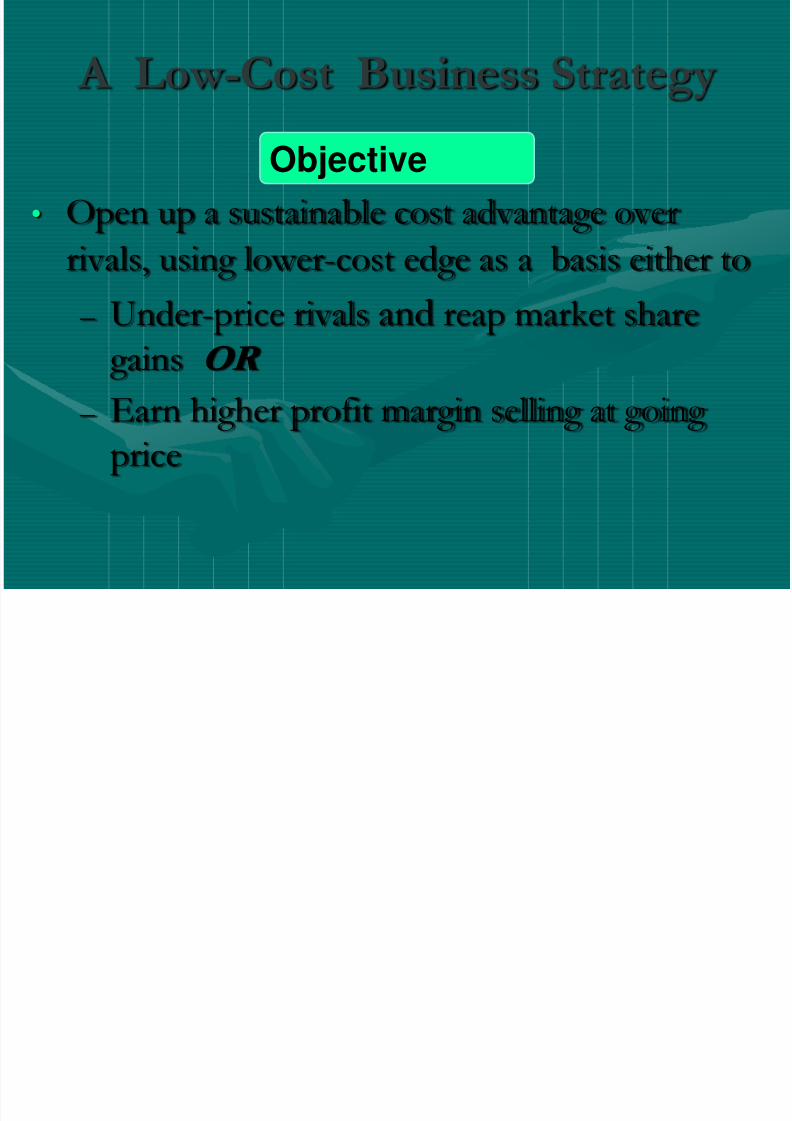

A Low-Cost Business Strategy

• Open up a sustainable cost advantage over

rivals, using lower-cost edge as a basis either to

– Under-price rivals and reap market share

gains OR

– Earn higher profit margin selling at going price

Objective

A L C S W k B

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 29/46

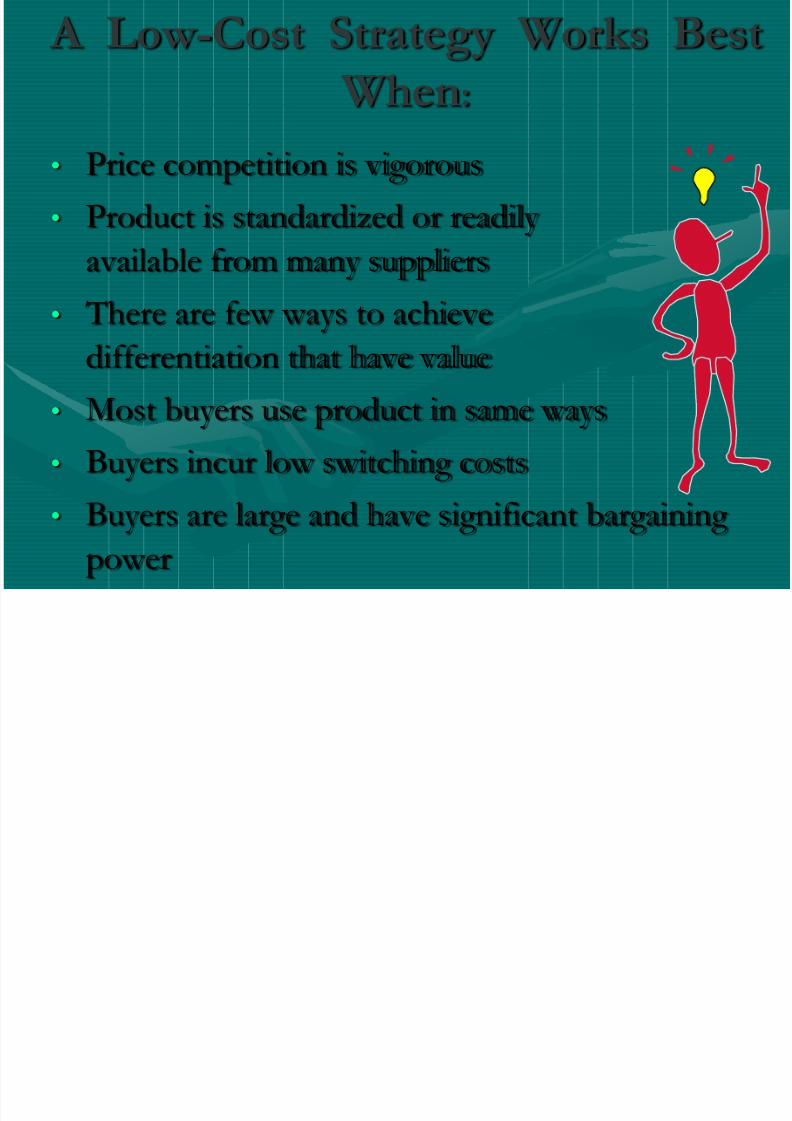

A Low-Cost Strategy Works Best

When:

• Price competition is vigorous

• Product is standardized or readily

available from many suppliers

• There are few ways to achieve

differentiation that have value

• Most buyers use product in same ways• Buyers incur low switching costs

• Buyers are large and have significant bargaining

power

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 30/46

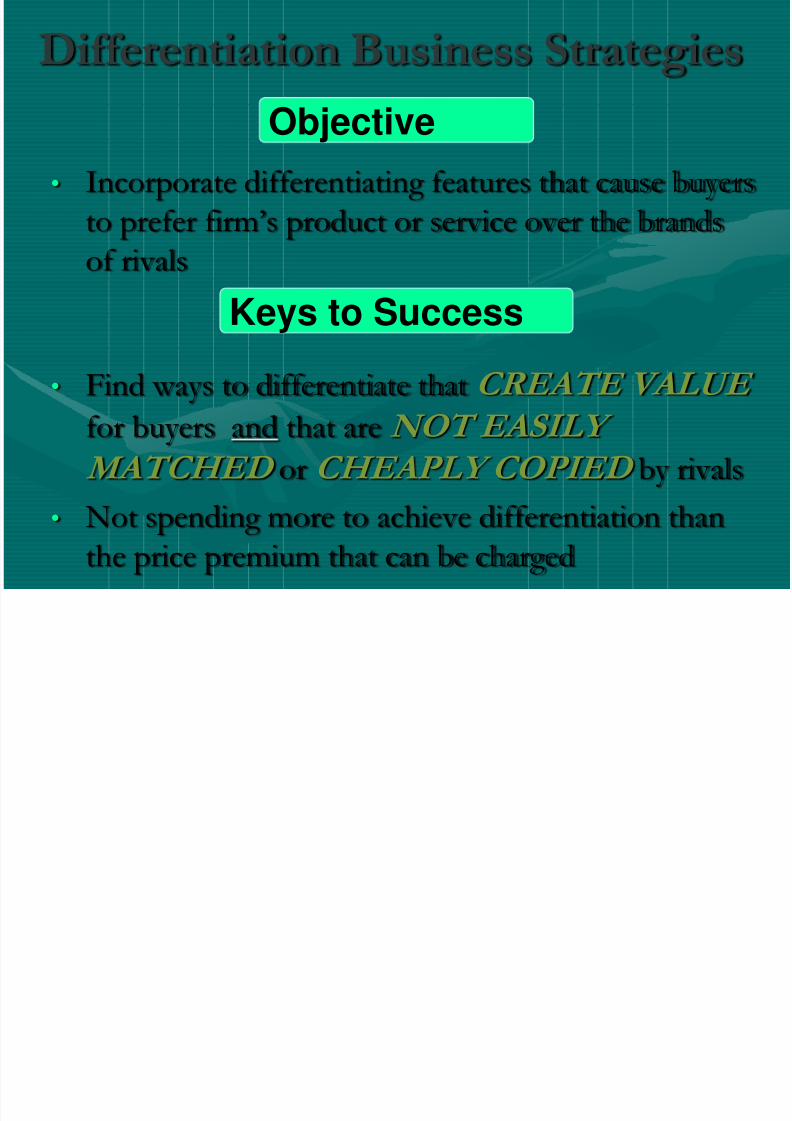

Differentiation Business Strategies

• Incorporate differentiating features that cause buyersto prefer firm’s product or service over the brands

of rivals

• Find ways to differentiate that CREATE VALUE

for buyers and that are NOT EASILY MATCHED or CHEAPLY COPIED by rivals

• Not spending more to achieve differentiation than

the price premium that can be charged

Keys to Success

Objective

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 31/46

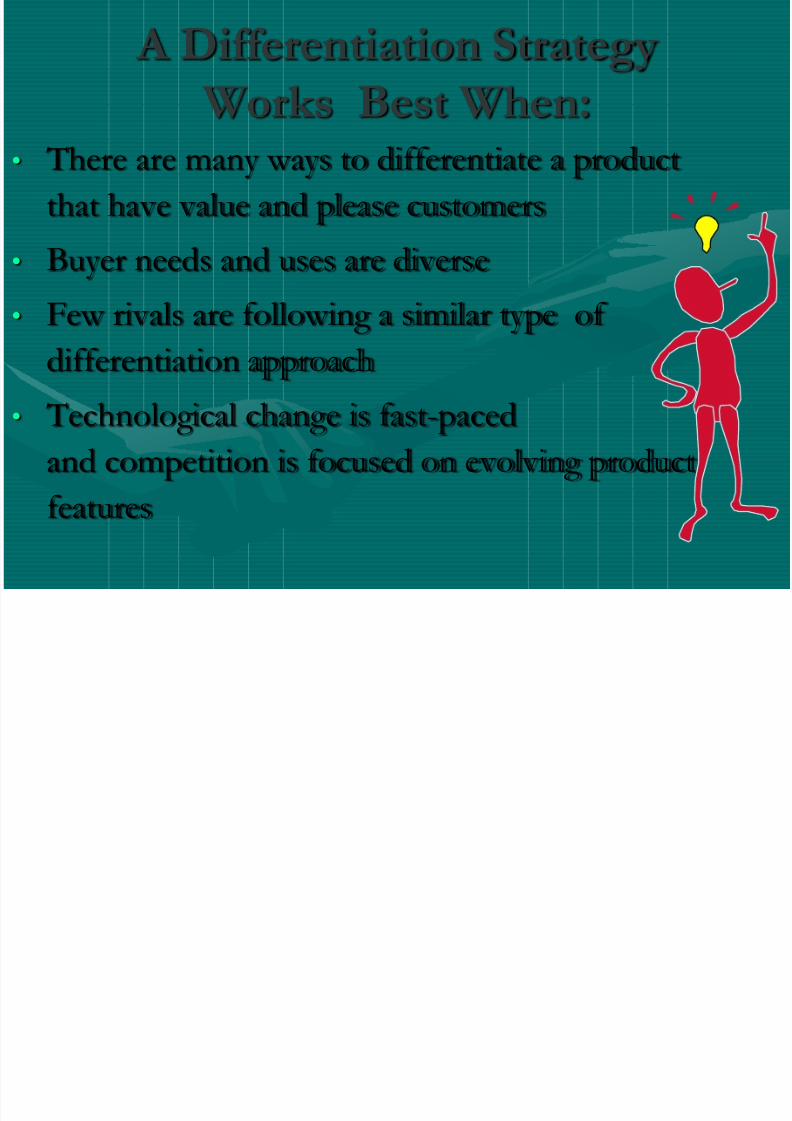

A Differentiation Strategy

Works Best When:• There are many ways to differentiate a product

that have value and please customers

• Buyer needs and uses are diverse

• Few rivals are following a similar type of

differentiation approach

• Technological change is fast-pacedand competition is focused on evolving product

features

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 32/46

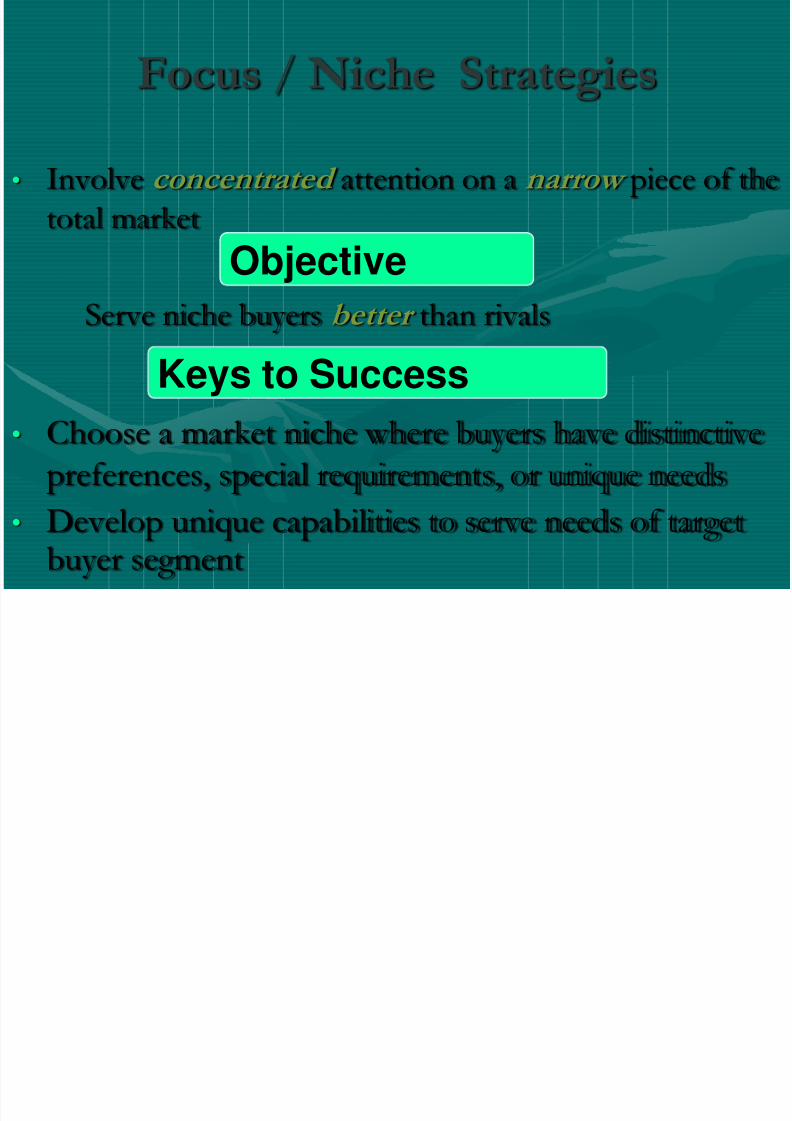

Focus / Niche Strategies

• Involve concentrated attention on a narrow piece of thetotal market

Serve niche buyers better than rivals

• Choose a market niche where buyers have distinctivepreferences, special requirements, or unique needs

• Develop unique capabilities to serve needs of target

buyer segment

Objective

Keys to Success

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 33/46

When Does a Focus

Strategy Work Best?

• Costly or difficult for multi-segment rivals to

serve specialized needs of target niche

• No other rivals are concentrating on samesegment

• Firm’s resources do not allow it to go

after a bigger piece of market• Industry has many different segments, creating

more focusing opportunities

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 34/46

Strategy in Accounting

• The importance and interlinking betweenStrategy and Accounting has also beenemphasised in recent years through different

organisations.

• Examples from the modern world illustrate theimportance of this interlinking that strategy has

had on business profitability and shareholders’ wealth.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 35/46

MODERN EXAMPLES OF

MASTERS OF STRATEGY

The Ferrari Team• The Ferrari Team have

been the most successful

sporting team in the pasttwo decades.

• The Ferrari team have

been studied by psychologists and

researchers to define their

winning concepts and

strategies.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 36/46

MODERN EXAMPLES OF

MASTERS OF STRATEGY AC MILAN ( 1899- to date)

• AC Milan has been one of the

most successful football clubs in

the past three decades.

• The club’s strategy has

continually focused on preparing

players both physically and

mentally to win.

• This has allowed the football clubto retain top-class footballers in

top form well beyond the normal

retirement age, thus lowering

players’ fees and transfer costs.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 37/46

MODERN EXAMPLES OF

MASTERS OF STRATEGY McDonalds

• McDonalds commands instant

recognition in every country in

the world.

• It has more than 30,000restaurants in over 120

countries, serving around 50

million people every day.

• Following its’ globalexpansion, in 2004 a new

Restaurant Supply Planning

Department was launched to

have enough stock to meet

demand but minimizing waste

This strategy is based upon a

Weblog purposely created forManagers to record daily stock

levels, as well as “Manugistics”,

that is information on factors

that may affect sales using two

years’ worth of data.

MODERN EXAMPLES OF

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 38/46

MODERN EXAMPLES OF

MASTERS OF STRATEGY

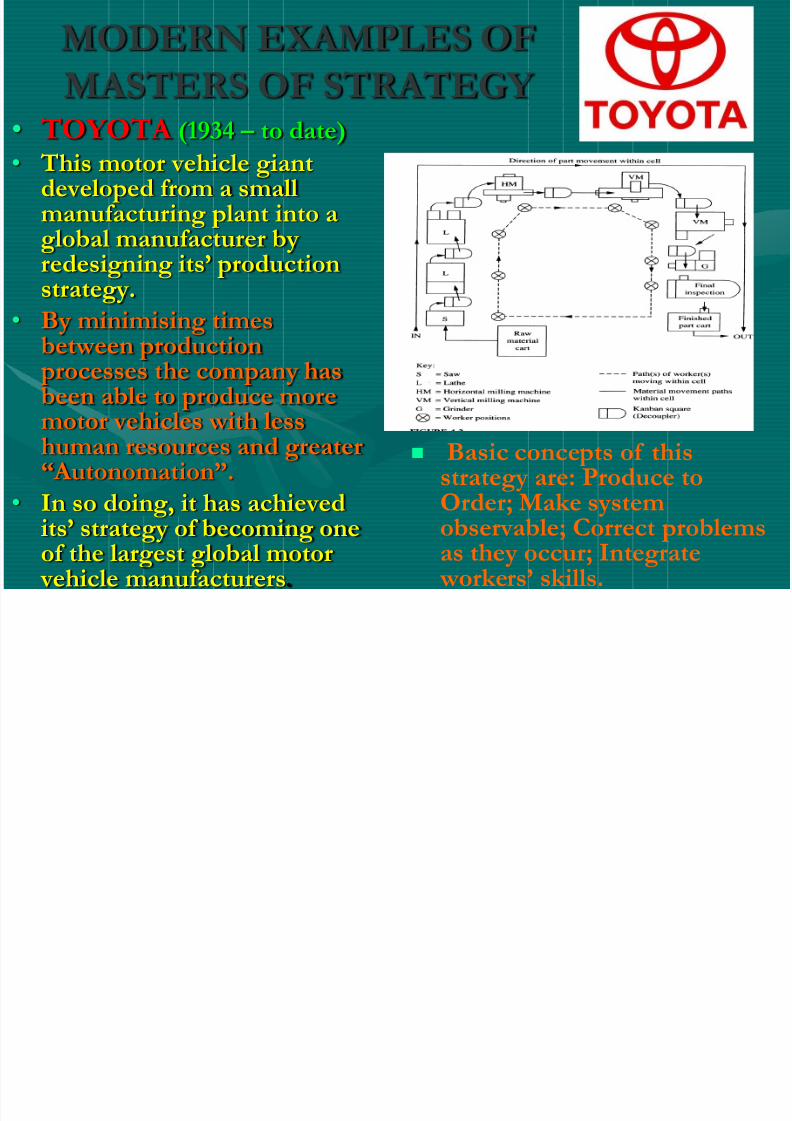

• TOYOTA (1934 – to date)• This motor vehicle giantdeveloped from a smallmanufacturing plant into aglobal manufacturer byredesigning its’ productionstrategy.

• By minimising timesbetween production

processes the company hasbeen able to produce more

motor vehicles with lesshuman resources and greater“Autonomation”.

• In so doing, it has achievedits’ strategy of becoming one

of the largest global motor vehicle manufacturers.

Basic concepts of thisstrategy are: Produce toOrder; Make systemobservable; Correct problems

as they occur; Integrate workers’ skills.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 39/46

MODERN EXAMPLES OF

MASTERS OF STRATEGY

APPLE From I-pods to ITunes

• Following the continued piracyand legal issues that arose withinthe music industry, Apple werequick to enter the market and

provide customers what they wanted: music on the move.

• This led to the creation of theIpods.

• Following the success of theIpods, the ITunes online digitalmusic store was also launched,enabling the music industry tolimit the threats of piracy bybringing their products within

financial reach of their clients.

MODERN EXAMPLES OF

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 40/46

MODERN EXAMPLES OF

MASTERS OF STRATEGY

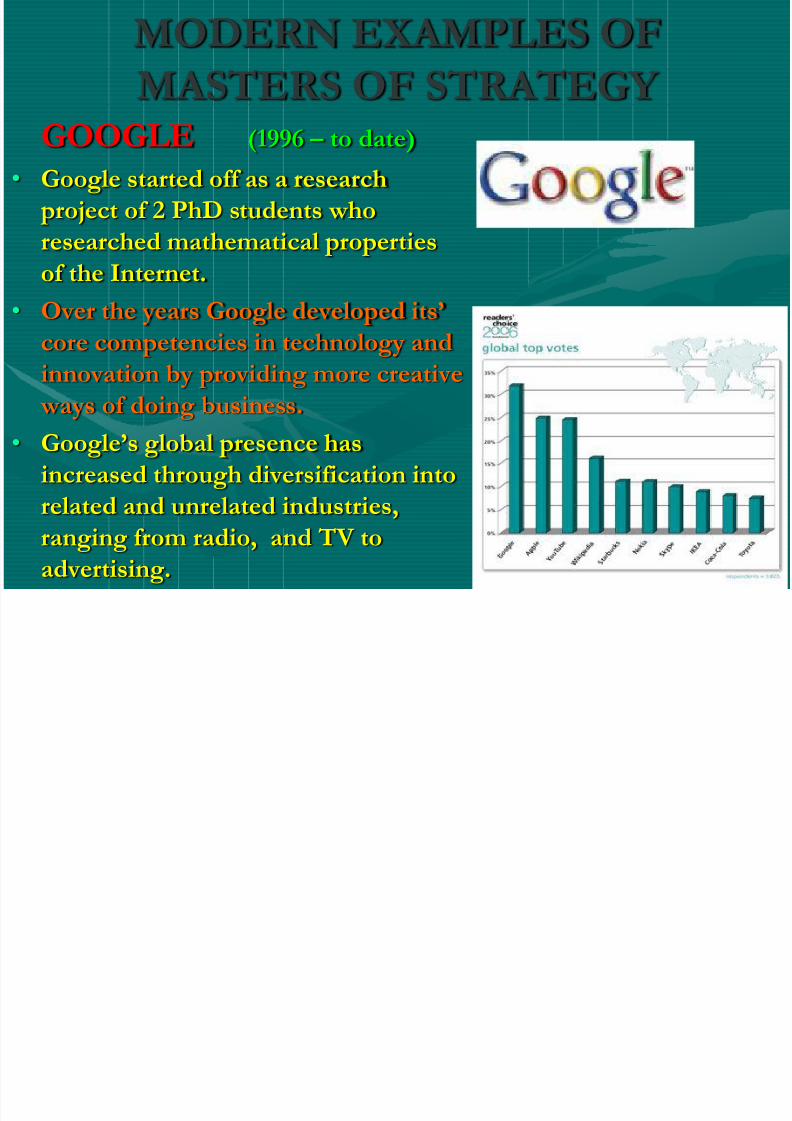

GOOGLE (1996 – to date)• Google started off as a research

project of 2 PhD students who

researched mathematical properties

of the Internet.• Over the years Google developed its’

core competencies in technology and

innovation by providing more creative

ways of doing business.

• Google’s global presence has

increased through diversification into

related and unrelated industries,

ranging from radio, and TV to

advertising.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 41/46

The importance of financial and non-

financial information

• Financial information enables the organizationto quantify options or decisions that have to betaken.

• Non-financial information is much moredifficult to gather, analyze and interpret, yet may have far-reaching consequences on any

managerial decision to be taken.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 42/46

Financial Information

• Financial information may be provided from thefollowing sources:

– Financial Statements

– Budgets

– Variance Analysis and Interpretations

– Interpretations of Financial Statements

– Market Statistics, market share and share prices

– Other comparative financial statistics that may beavailable to the organisation

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 43/46

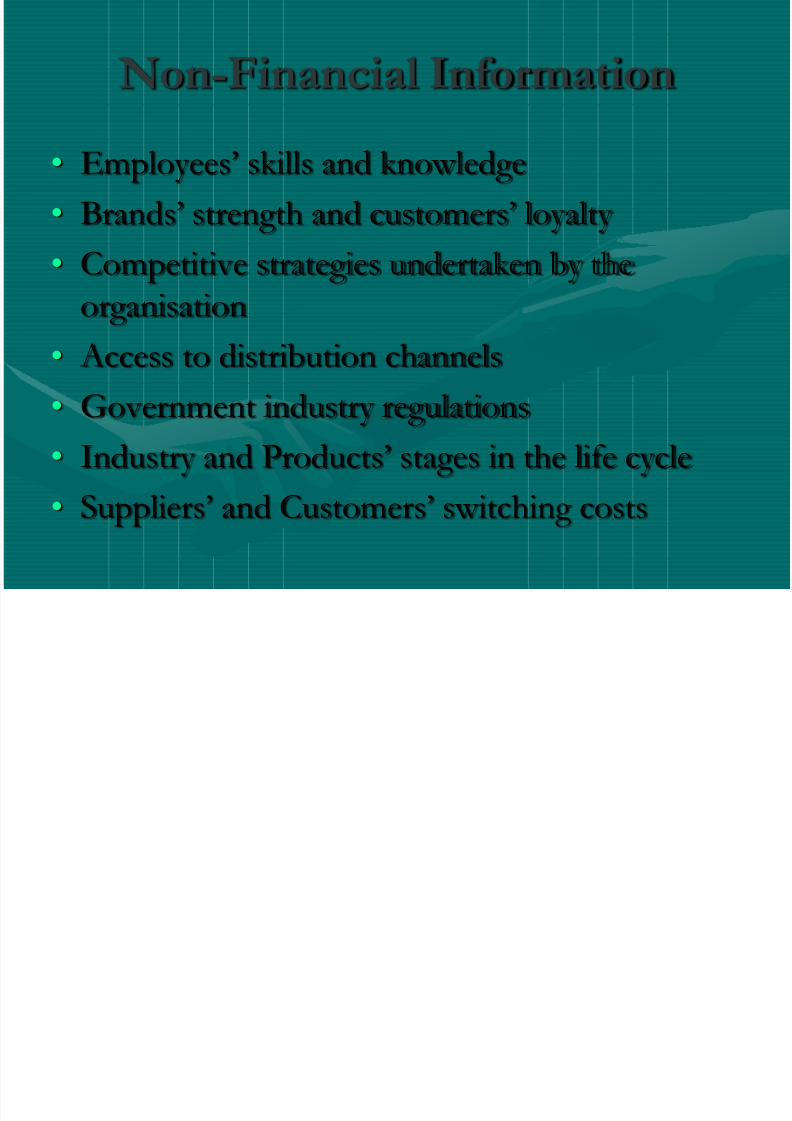

Non-Financial Information

• Employees’ skills and knowledge

• Brands’ strength and customers’ loyalty

• Competitive strategies undertaken by theorganisation

• Access to distribution channels

• Government industry regulations• Industry and Products’ stages in the life cycle

• Suppliers’ and Customers’ switching costs

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 44/46

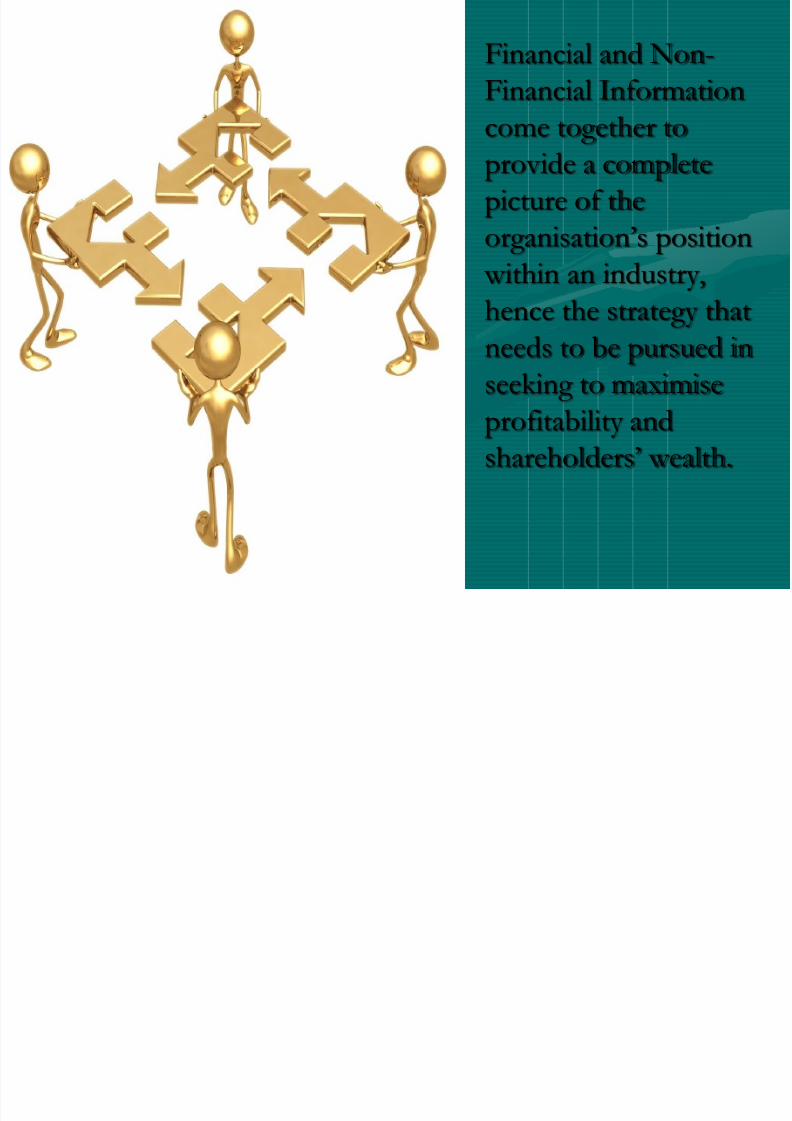

Financial and Non-Financial Informationcome together toprovide a completepicture of theorganisation’s position

within an industry,hence the strategy thatneeds to be pursued inseeking to maximise

profitability andshareholders’ wealth.

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 45/46

Questions

8/3/2019 Finance for Non-finance Professionals Session 5

http://slidepdf.com/reader/full/finance-for-non-finance-professionals-session-5 46/46

Next Session

ACCOUNTING IN MANAGEMENT