finance department cash handling internal … department – cash handling internal controls...

TRANSCRIPT

FINANCE DEPARTMENT – Cash Handling Internal Controls

Prepared By: Finance-ECH, Dec. 2011. Updated September 2013. Page 1

Each department (including faculties, academic and academic support departments, schools,

centres and institutes) within the University of Waterloo (“UW” or the “University”) is

responsible for implementing internal controls in order to protect the cash collected as well as

to ensure the safety of staff handling the cash. The following are recommendations to be

incorporated as appropriate for the business unit.

NB. “Cash” or “cash receipts” mean payments received from customers or other sources,

including cheques, cash, bank drafts or any similar items. This does not include bank, wire or

other funds transfers made electronically.

Cash handling internal controls are divided into the following five main areas:

Safeguarding assets – protect the physical cash/assets and the people handling the cash

Segregation of duties - separate cash handling duties among different people

Accountability – ensure cash transactions are authorized, properly accounted for,

documented and identifiable to specific cash handlers

Reconciliations – ensure all transactions are recorded correctly

Monitoring – regularly review processes to tighten controls, train staff, and investigate

unusual activity.

Safeguarding Assets

To help ensure a safe work environment, the following internal controls should be in place to

help protect the cash collected in Departments and the staff handling the cash.

Cheques, cash and similar items shall be safeguarded at all times. Physical access shall

be restricted to authorized personnel.

All cash must be stored in a locked drawer.

At the end of each day, any cash not deposited should be stored in a fire-proof vault, if

possible.

Combinations and passwords should be given to as few people as is necessary.

Combinations and passwords should be changed periodically, at least annually, or when

someone leaves the department.

All cheques are to be made payable to the University of Waterloo and mailed to Finance, ECH, 200 University Ave West, Waterloo ON N2L 3G1.

Cheques are stamped immediately “for deposit only to University of Waterloo [account #]

FINANCE DEPARTMENT – Cash Handling Internal Controls

Prepared By: Finance-ECH, Dec. 2011. Updated September 2013. Page 2

Segregation of Duties

The following cash handling duties should be performed by different people so that no one

person has control over the entire cash handling process. Separating the cash handling duties

among different people will minimize the risk of errors, decrease the opportunity for fraudulent

activity and increase the chance of detecting errors.

Receive cash

Disburse cash amounts for floats

Record transactions

Prepare bank deposit slip, (preparer and reviewer)

Make the deposit at the bank

Reconcile cash receipts to daily sales reports

Investigate and remediate discrepancies noted from reviews, reconciliations, and other analysis. Accountability Departments need to ensure cash transactions are authorized, properly accounted for,

documented and identifiable to specific cash handlers. Ensuring accountability among each

staff member also helps to reduce the risk of lost or stolen cash receipts and incorrect

recording of transactions.

Employees actually receiving and handling cash are responsible for: o Ensuring that all transactions are processed in accordance with University policy o Issuing receipts to customers, preferably sequentially numbered or provided

from POS system o Balancing cash to sales transactions at least daily and reporting overages or

shortages to management o Keeping funds physically secured

Department management is responsible for: o Identifying which individuals have access to cash handling processes and

documenting their respective responsibilities o Ensuring each cashier or cash handler has a separate float or change fund o Ensuring there is a process in place to identify irregularities and a tracking

system back to specific individuals o Approving returns, refunds and void transactions o Approving bank deposits o Overseeing the preparation of bank deposits for Brinks pickup

FINANCE DEPARTMENT – Cash Handling Internal Controls

Prepared By: Finance-ECH, Dec. 2011. Updated September 2013. Page 3

o Depositing all cash receipts to the University’s bank account the same day that they are received

o Keeping funds physically secured o Resolving overages or shortages o Ensuring deposit journal entries are loaded to SharePoint in a timely fashion for

the Finance Department to post

The Finance Department is responsible for: o Posting journal entries loaded to SharePoint by faculties/departments o Preparing cheque log for cheques received o Depositing all cash receipts to the University’s bank account the same day that

they are received NOTE: All University business is required to be administered through the established mechanisms and officially recognized accounts. There are no conditions under which external bank accounts would be appropriate for University business. Reconciliations In order to ensure all transactions have been recorded correctly, (completely and accurately), several reconciliations should occur on a timely basis.

Department management is responsible for: o Preparing a reconciliation of the daily sales from the POS system to the cash

receipts as recorded in the bank deposit. Cash receipts consist of cash, cheques, credit cards, Interac/debit cards, the University of Waterloo’s “WatCard”, gift cards, gift certificates, or any other form of tender accepted at the point of sale location, i.e. USD currency

o Preparing a reconciliation of the bank deposits to what has been recorded in the departmental accounts

o Preparing a reconciliation of movement in inventory to total sales, if applicable

The Finance Department is responsible for: o Preparing and approving monthly bank reconciliations on all University accounts o Reviewing outstanding deposits to ensure timely clearing

Monitoring and Review Management needs to continually review cash handling processes to ensure they are being followed, train staff, and investigate unusual activity. The following reviews should be done on a regular basis:

Review cash over/short account and investigate large or unusual amounts

Analyze sales forecasts and budgets to actual sales and investigate variances (and margins where applicable)

FINANCE DEPARTMENT – Cash Handling Internal Controls

Prepared By: Finance-ECH, Dec. 2011. Updated September 2013. Page 4

Review cash receipts ledger for unusual items or tampering

Review and approve returns, refunds and void transaction logs

Review system security access

Train and monitor new staff and provide continual training to existing staff on a regular basis, i.e. at least annually

Provide customer statements on a regular basis

Review overdue accounts on a monthly basis

FINANCE DEPARTMENT – Cash Handling Internal Controls Checklist Appendix A

Prepared By: Finance-ECH, Dec. 2011. Updated September 2013. Page 5

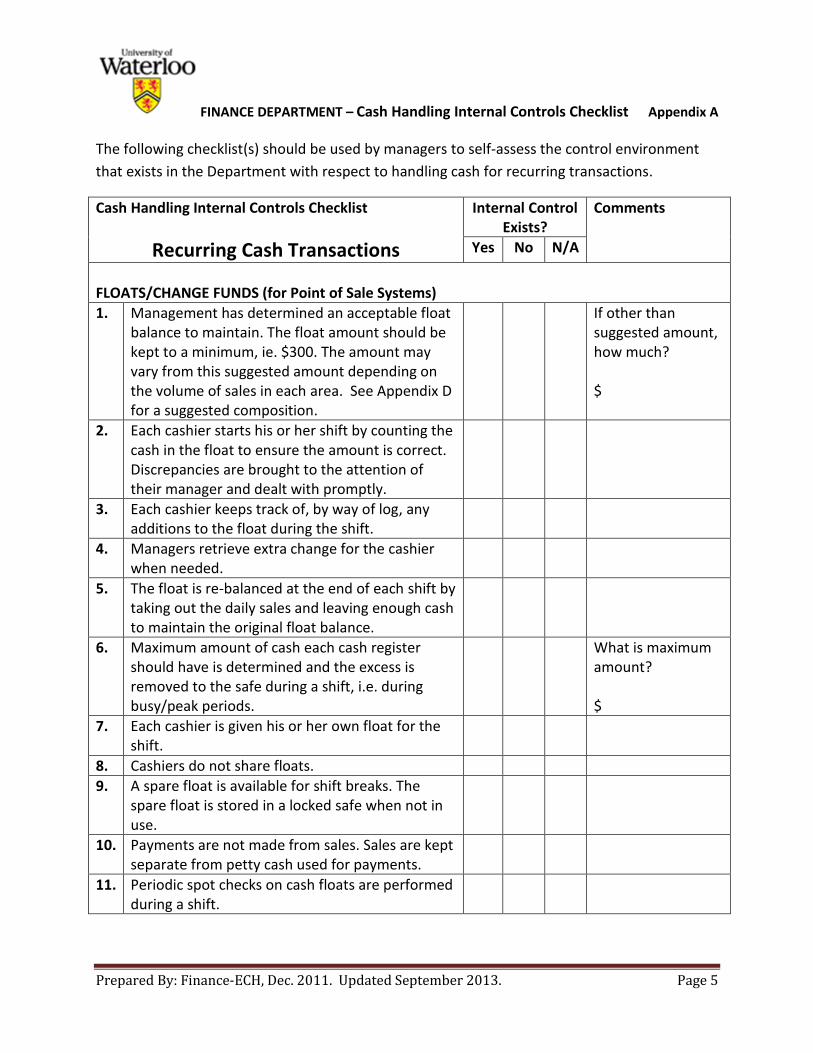

The following checklist(s) should be used by managers to self-assess the control environment

that exists in the Department with respect to handling cash for recurring transactions.

Cash Handling Internal Controls Checklist

Recurring Cash Transactions

Internal Control Exists?

Comments

Yes No N/A

FLOATS/CHANGE FUNDS (for Point of Sale Systems)

1. Management has determined an acceptable float balance to maintain. The float amount should be kept to a minimum, ie. $300. The amount may vary from this suggested amount depending on the volume of sales in each area. See Appendix D for a suggested composition.

If other than suggested amount, how much? $

2. Each cashier starts his or her shift by counting the cash in the float to ensure the amount is correct. Discrepancies are brought to the attention of their manager and dealt with promptly.

3. Each cashier keeps track of, by way of log, any additions to the float during the shift.

4. Managers retrieve extra change for the cashier when needed.

5. The float is re-balanced at the end of each shift by taking out the daily sales and leaving enough cash to maintain the original float balance.

6. Maximum amount of cash each cash register should have is determined and the excess is removed to the safe during a shift, i.e. during busy/peak periods.

What is maximum amount? $

7. Each cashier is given his or her own float for the shift.

8. Cashiers do not share floats.

9. A spare float is available for shift breaks. The spare float is stored in a locked safe when not in use.

10. Payments are not made from sales. Sales are kept separate from petty cash used for payments.

11. Periodic spot checks on cash floats are performed during a shift.

FINANCE DEPARTMENT – Cash Handling Internal Controls Checklist Appendix A

Prepared By: Finance-ECH, Dec. 2011. Updated September 2013. Page 6

SAFEGUARDING OF ASSETS

12. Access to cash is limited to as few as people as possible, i.e. one Custodian with access to each petty cash fund.

13. Department has a fire-proof safe/vault to keep all cash sales and/or bank deposits secure prior to deposit

14. Fire-proof safe/vault is stored in a low traffic area, out of sight from the public.

15. The number of people with access to combinations and passwords is limited.

How many?

16. A log is kept of everyone issued a key or given knowledge of a combination for a safe or room where cash is stored and handled.

How many?

17. Combinations are changed periodically; at least annually or when someone leaves the department.

BANK DEPOSITS

18. Bank deposit is prepared daily. If not daily, then the frequency is approved by Finance.

Frequency (if not daily)?

19. A second person verifies the bank deposits and signs the bank deposit slip as a reviewer/approver.

20. Daily bank deposits are not prepared for amounts less than $100.00. However, all cash receipts are deposited by the last business day of each month regardless of dollar amount.

TRANSFERING CASH

21. Coin, cash, cheques and first two copies of the Bank Deposit Currency Distribution Form are sealed in a CIBC security bag.

22. The CIBC security bag number, total deposit amount and date of deposit is recorded in a log.

23 The sealed bank deposit is delivered to the nearest Brinks drop-off location during the day. (Considered to be safer than at night)

24. Two persons deliver the bank deposit.

FINANCE DEPARTMENT – Cash Handling Internal Controls Checklist Appendix A

Prepared By: Finance-ECH, Dec. 2011. Updated September 2013. Page 7

25. The bank deposit is recorded in a Brinks log book at the drop-off location.

26. For departments delivering funds to Student Accounts for deposit:

Amounts are kept to a minimum

How much is sent to Student Accounts? How often?

How is it delivered? By whom? When?

RECONCILIATION OF SALES

27. The cash register tape is reconciled to the cash after every shift. Total sales net of refunds = sum of credit card + debit + WatCard + cheques + cash.

28. Cash over/short amounts are investigated. Amounts are tracked and reviewed by management (i.e. in a daily log).

29. Large amounts suspected of theft are reported to Police Services if necessary.

OTHER RECONCILIATIONS

30. Changes in inventory are reconciled to sales and discrepancies are accounted for.

31. Comparison is performed of actual to budgeted sales and variances are explained.

SEGREGATION OF DUTIES, (i.e. different people perform each of the functions)

32.

When delegating cash handling procedures, make sure to segregate the following duties:

Function:

receive cash,

disburse cash for floats,

record cash transactions,

prepare bank deposit,

make the bank deposit,

Person Responsible:

FINANCE DEPARTMENT – Cash Handling Internal Controls Checklist Appendix A

Prepared By: Finance-ECH, Dec. 2011. Updated September 2013. Page 8

reconcile cash receipts to sales register tapes,

reconcile bank deposits to general ledger and bank accounts,

monitor accounts (discounts, returns, and cash over/short), and

investigate discrepancies (in analysis, reconciliations, etc.)

33. Cash handling duties are rotated on a periodic basis.

34. Back-up exists to cover absences due to illnesses and vacations.

CASH REGISTERS, POS TERMINALS

35. Cash register sales tapes cannot be manipulated.

36. Cash registers are clustered to enhance visibility.

37. Cash registers should be located near the exit of the store.

38. ID is required to access cash registers and computer systems so that transactions can be traced to individual employees.

39. Register tapes are reviewed periodically. Review includes but is not limited to unusual transactions, excessive returns or mistakes, or signs of tampering or alterations.

40. Security cameras are at all point of sale locations.

41. Cash registers have automated change making devices.

42. If there are multiple cash registers and only one float, the 2nd register is designated as a “no-cash” register that accepts cheques/credit cards/debit/WatCard only. (ie. during times of high transaction volume)

FINANCE DEPARTMENT – Cash Handling Internal Controls Checklist Appendix A

Prepared By: Finance-ECH, Dec. 2011. Updated September 2013. Page 9

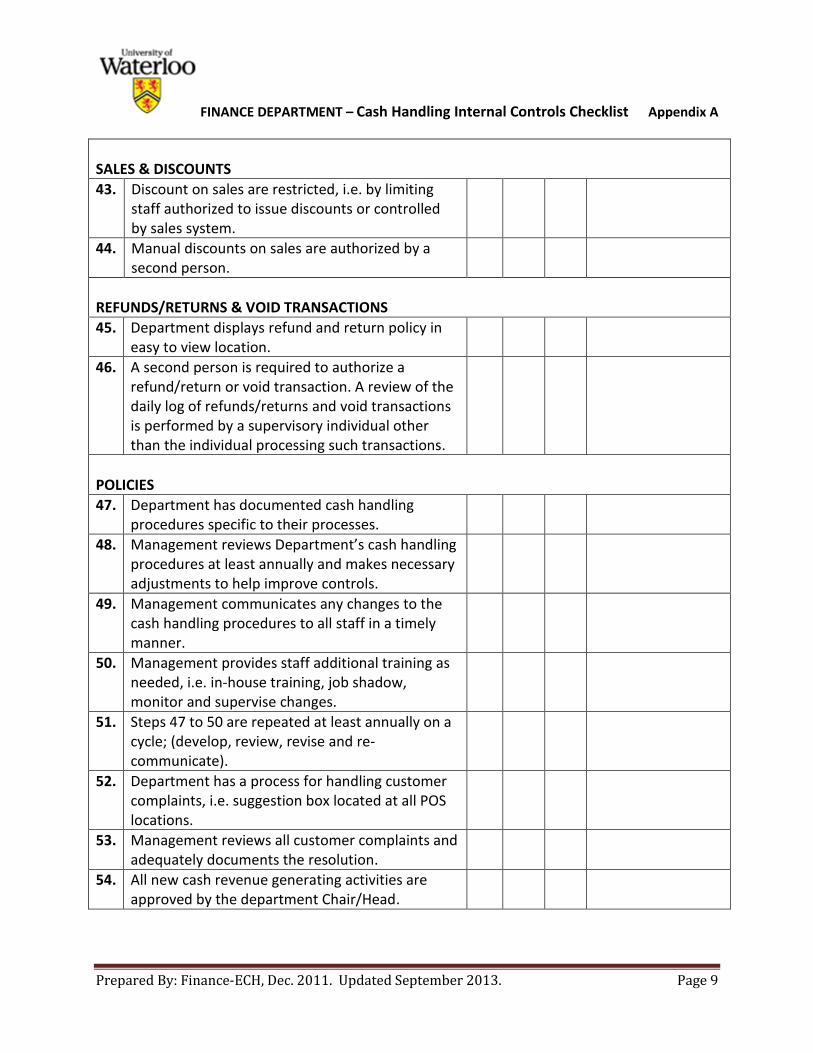

SALES & DISCOUNTS

43. Discount on sales are restricted, i.e. by limiting staff authorized to issue discounts or controlled by sales system.

44. Manual discounts on sales are authorized by a second person.

REFUNDS/RETURNS & VOID TRANSACTIONS

45. Department displays refund and return policy in easy to view location.

46. A second person is required to authorize a refund/return or void transaction. A review of the daily log of refunds/returns and void transactions is performed by a supervisory individual other than the individual processing such transactions.

POLICIES

47. Department has documented cash handling procedures specific to their processes.

48. Management reviews Department’s cash handling procedures at least annually and makes necessary adjustments to help improve controls.

49. Management communicates any changes to the cash handling procedures to all staff in a timely manner.

50. Management provides staff additional training as needed, i.e. in-house training, job shadow, monitor and supervise changes.

51. Steps 47 to 50 are repeated at least annually on a cycle; (develop, review, revise and re-communicate).

52. Department has a process for handling customer complaints, i.e. suggestion box located at all POS locations.

53. Management reviews all customer complaints and adequately documents the resolution.

54. All new cash revenue generating activities are approved by the department Chair/Head.

FINANCE DEPARTMENT – Cash Handling Internal Controls Checklist Appendix A

Prepared By: Finance-ECH, Dec. 2011. Updated September 2013. Page 10

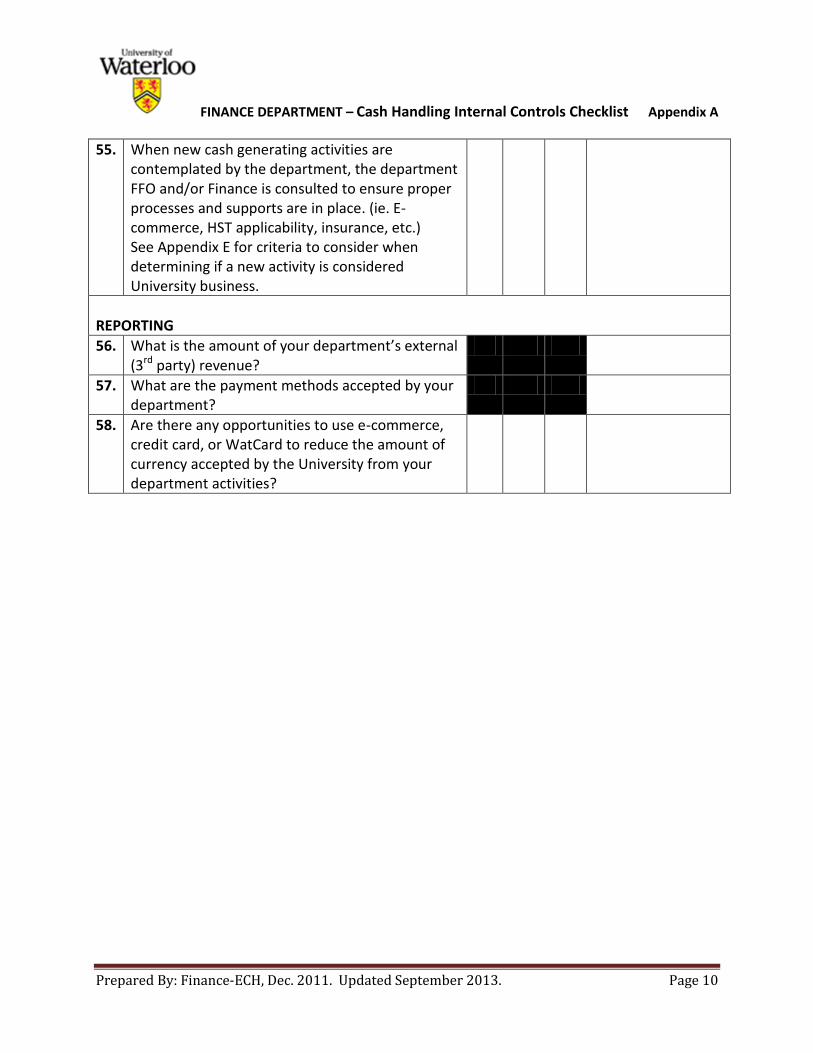

55. When new cash generating activities are contemplated by the department, the department FFO and/or Finance is consulted to ensure proper processes and supports are in place. (ie. E-commerce, HST applicability, insurance, etc.) See Appendix E for criteria to consider when determining if a new activity is considered University business.

REPORTING

56. What is the amount of your department’s external (3rd party) revenue?

57. What are the payment methods accepted by your department?

58. Are there any opportunities to use e-commerce, credit card, or WatCard to reduce the amount of currency accepted by the University from your department activities?

FINANCE DEPARTMENT – Cash Handling Internal Controls Checklist Appendix B

Prepared By: Finance-ECH, Dec. 2011. Updated September 2013. Page 11

The following checklist(s) should be used by managers to self-assess the control environment

that exists in the Department with respect to handling cash.

Cash Handling Internal Controls Checklist

Non-Recurring Cash Transactions

Internal Control Exists?

Comments

Yes No N/A

SAFEGUARDING OF ASSETS

1. Access to cash is limited to as few as people as possible, i.e. one Custodian with access to each petty cash fund.

2. Department has a secure area to keep all cash sales and/or bank deposits secure prior to deposit

3. Secure area is in a low traffic area, out of sight from the public.

4. The number of people with access or keys to the secure area is limited.

How many?

5. A log is kept of everyone issued a key or given knowledge of the secure area where cash is stored and handled.

How many?

6. Access to keys are controlled – keys cannot be duplicated and all copies are accounted for at all times (ie. ensure returned when someone leaves the department).

BANK DEPOSITS

7. Bank deposit is prepared daily. If not daily, then the frequency is approved by Finance.

Frequency (if not daily)?

8. A second person verifies the bank deposits and signs the bank deposit slip as a reviewer/approver.

9. Daily bank deposits are not prepared for amounts less than $100.00. However, all cash receipts are deposited by the last business day of each month regardless of dollar amount.

TRANSFERING CASH

10. Coin, cash, cheques and first two copies of the Bank Deposit Currency Distribution Form are sealed in a CIBC security bag.

FINANCE DEPARTMENT – Cash Handling Internal Controls Checklist Appendix B

Prepared By: Finance-ECH, Dec. 2011. Updated September 2013. Page 12

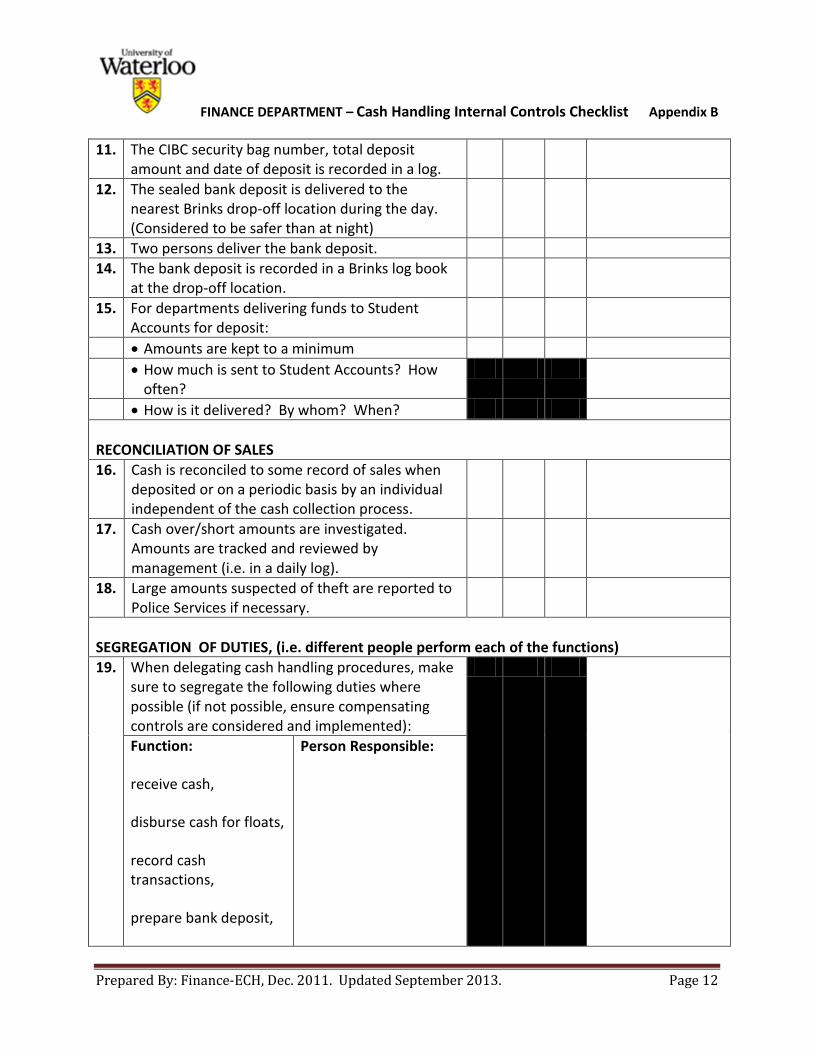

11. The CIBC security bag number, total deposit amount and date of deposit is recorded in a log.

12. The sealed bank deposit is delivered to the nearest Brinks drop-off location during the day. (Considered to be safer than at night)

13. Two persons deliver the bank deposit.

14. The bank deposit is recorded in a Brinks log book at the drop-off location.

15. For departments delivering funds to Student Accounts for deposit:

Amounts are kept to a minimum

How much is sent to Student Accounts? How often?

How is it delivered? By whom? When?

RECONCILIATION OF SALES

16. Cash is reconciled to some record of sales when deposited or on a periodic basis by an individual independent of the cash collection process.

17. Cash over/short amounts are investigated. Amounts are tracked and reviewed by management (i.e. in a daily log).

18. Large amounts suspected of theft are reported to Police Services if necessary.

SEGREGATION OF DUTIES, (i.e. different people perform each of the functions)

19.

When delegating cash handling procedures, make sure to segregate the following duties where possible (if not possible, ensure compensating controls are considered and implemented):

Function:

receive cash,

disburse cash for floats,

record cash transactions,

prepare bank deposit,

Person Responsible:

FINANCE DEPARTMENT – Cash Handling Internal Controls Checklist Appendix B

Prepared By: Finance-ECH, Dec. 2011. Updated September 2013. Page 13

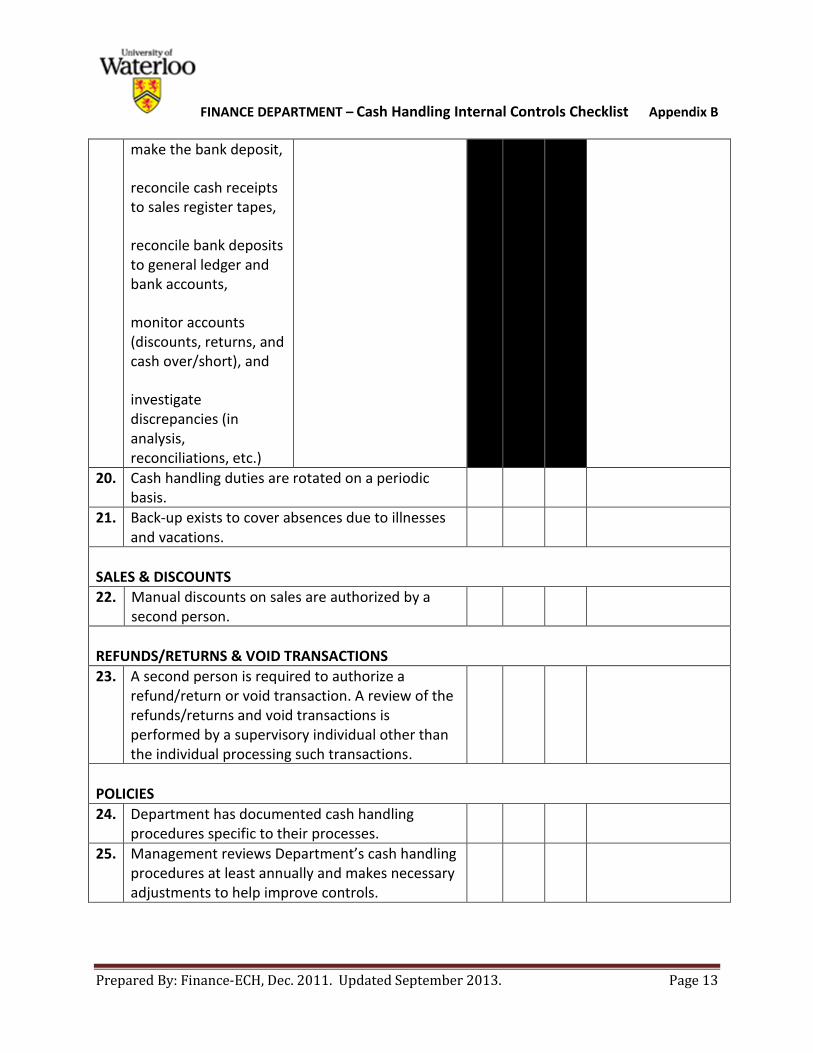

make the bank deposit,

reconcile cash receipts to sales register tapes,

reconcile bank deposits to general ledger and bank accounts,

monitor accounts (discounts, returns, and cash over/short), and

investigate discrepancies (in analysis, reconciliations, etc.)

20. Cash handling duties are rotated on a periodic basis.

21. Back-up exists to cover absences due to illnesses and vacations.

SALES & DISCOUNTS

22. Manual discounts on sales are authorized by a second person.

REFUNDS/RETURNS & VOID TRANSACTIONS

23. A second person is required to authorize a refund/return or void transaction. A review of the refunds/returns and void transactions is performed by a supervisory individual other than the individual processing such transactions.

POLICIES

24. Department has documented cash handling procedures specific to their processes.

25. Management reviews Department’s cash handling procedures at least annually and makes necessary adjustments to help improve controls.

FINANCE DEPARTMENT – Cash Handling Internal Controls Checklist Appendix B

Prepared By: Finance-ECH, Dec. 2011. Updated September 2013. Page 14

26. Management communicates any changes to the cash handling procedures to all staff in a timely manner.

27. Management provides staff additional training as needed, i.e. in-house training, job shadow, monitor and supervise changes.

28. Steps 24 to 27 are repeated at least annually on a cycle; (develop, review, revise and re-communicate).

29. Department has a process for handling customer complaints.

30. Management reviews all customer complaints and adequately documents the resolution.

31. All new cash revenue generating activities are approved by the department Chair/Head.

32. When new cash generating activities are contemplated by the department, the department FFO and/or Finance is consulted to ensure proper processes and supports are in place. (ie. E-commerce, HST applicability, insurance, etc.) See Appendix E for criteria to consider when determining if a new activity is considered University business.

REPORTING

33. What is the amount of your department’s external (3rd party) revenue?

34. What are the payment methods accepted by your department?

35. Are there any opportunities to use e-commerce, credit card, or WatCard to reduce the amount of currency accepted by the University from your department activities?

FINANCE DEPARTMENT – Cash Handling Internal Controls Appendix C

Prepared By: Finance-ECH, Dec. 2011. Updated September 2013. Page 15

For further information, please also refer to the following documents: Cash and Cheques for Deposit Procedures http://www.adm.uwaterloo.ca/infofin/Policy/Cash_&_Cheques_%20for_%20Deposit.pdf Petty Cash Procedures http://www.adm.uwaterloo.ca/infofin//Policy/PettyCash.html Change Fund Procedures http://www.adm.uwaterloo.ca/infofin/Policy/UWChangeFundProcedures.pdf Credit Card Procedures for Departments’ Point of Sale Terminals http://www.adm.uwaterloo.ca/infofin/Policy/ProcessingCreditCardTransactionsusingDepartmentPointofSaleTerminal.pdf Credit Card Procedures for Student Account’s Point of Sale Terminal http://www.adm.uwaterloo.ca/infofin/Policy/ProcessingCreditCardTransactionsUsingStudentAccountsPointofSaleTerminal.pdf

FINANCE DEPARTMENT – Float Composition Example Appendix D

Prepared By: Finance-ECH, Dec. 2011. Updated September 2013. Page 16

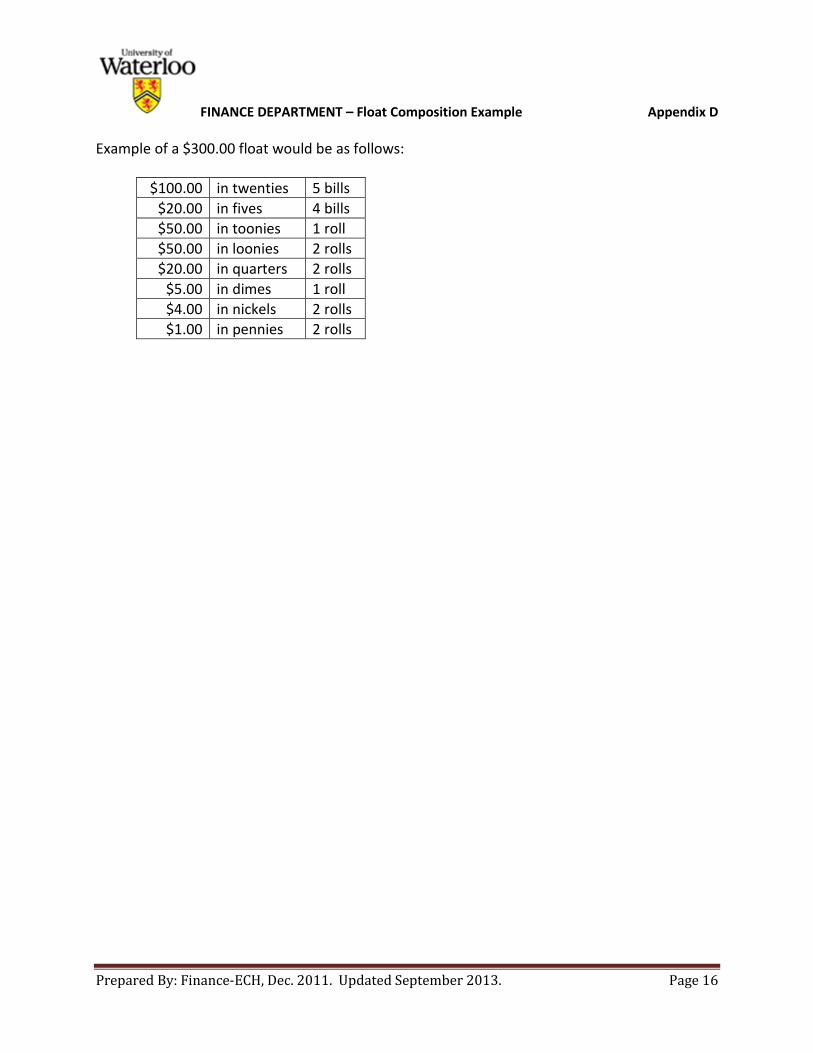

Example of a $300.00 float would be as follows:

$100.00 in twenties 5 bills

$20.00 in fives 4 bills

$50.00 in toonies 1 roll

$50.00 in loonies 2 rolls

$20.00 in quarters 2 rolls

$5.00 in dimes 1 roll

$4.00 in nickels 2 rolls

$1.00 in pennies 2 rolls

FINANCE DEPARTMENT – New Activity Considerations Questionnaire Appendix E

Prepared By: Finance-ECH, Dec. 2011. Updated September 2013. Page 17

As part of the preliminary analysis of a new activity undertaken by a department or faculty, the individual or individuals should assess whether the proposed transaction(s) meet the test of being University business.

Considerations: Response:

If the activity results in a surplus, will the University own the surplus and be entitled to (re)allocate funds as deemed appropriate?

If the activity results in a deficit, will the University be liable or obligated to fund the deficiency?

Who is the audience or what is the purpose for the activity and does it directly relate to the job description(s) of the requesting individual or the curriculum of the department?

Is the activity undertaken by a separate legal entity from the University under the University’s name?

Are University resources to be used in the activity, and if so, what is the nature of the resources required?

Is the general activity already being performed or is more appropriately or effectively performed by another department at the University?

If the new activity is determined to be University business, have you made arrangements for the proper application of tax (ie. HST)?

If the activity is University business, have you considered the insurance implications?

In the event the transaction meets the criteria, the method of payment should be selected to most efficiently process the transactions in accordance with the appropriate controls. Transactions which do not meet the criteria should not be administered through the University’s accounts or using department/faculty resources.