finance

DESCRIPTION

financial management articleTRANSCRIPT

Recent research in hospitalityfinancial management

Henry Tsai, Steve Pan and Jinsoo LeeSchool of Hotel & TourismManagement, The Hong Kong Polytechnic University,

Kowloon, Hong Kong SAR

Abstract

Purpose – The purpose of this paper is to review and synthesize published contemporary hospitalityfinancial management research from 1998 through 2009 and provide future research directions.

Design/methodology/approach – The authors began their initial literature search by entering intothe ABI/INFORM database via ProQuest 19 pre-identified keywords (i.e. debt, financing, ownership)related to the major functions of financial management, namely investing, financing, and dividenddecisions, as well as commonly indexed keywords in hospitality finance research. The paper thenexpanded the authors’ literature list through the reference lists of the studies that they initiallyidentified. The authors limited their search to published studies between 1998 and 2009 and withinhospitality journals written in English.

Findings – The paper identifies 98 published papers that represented the major work and efforts inexpanding the body of knowledge in both the theoretical and practical perspectives of hospitalityfinancial management. The major categories of papers include hospitality financing, investing,dividend policy, financial condition, and performance. Areas that warrant further investigation arenoted throughout the paper.

Research limitations/implications – The papers review provides academics and practitioners anoverview of the updated body of knowledge in the field and suggests the need for further in-depthresearch to extend the literature and prompt better financial decision making for practitioners.

Originality/value – Since Harris and Brown’s and Atkinson and Jones’s reviews of past hospitalityaccounting and finance studies which mostly focused on the former, hospitality financial managementresearch alone has grown noticeably in terms of diverse topics and sophistication of methodologies. Tothe authors’ knowledge, no updated reviews that focus solely on hospitality finance research have beenpublished in the last 12 years, and the need for such a task motivated them to conduct a review ofrecent research on this topic.

Keywords Dividends, Financing, Firm performance, Hospitality financial management, Investing

Paper type Literature review

1. IntroductionFinancial management is the backbone of any business, including firms involved inhospitality (including but not limited to hotels, restaurants, and casinos). In thehospitality industry, managers at the property level are charged with using owners’invested assets to enhance revenues and reduce expenses to achieve desired net profits.However, managers at the corporate level are more involved in issues related to investingexcess cash and raising debt and equity capital. Dividend policy and decisions, which tosome extent signal board-level views on the firm’s future development opportunities,also play a significant role in hospitality finance. The hospitality industry is fairlycapital-intensive (Karadeniz et al., 2009; Lee, 2007), requiring managers at all levels tohave adequate financial management skills and access to strategies for achieving thegoal of financial management, namely value enhancement or creation for owners

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/0959-6119.htm

Hospitalityfinancial

management

941

Received 22 August 2010Revised 10 January 2011

7 March 2011Accepted 9 March 2011

International Journal ofContemporary Hospitality

ManagementVol. 23 No. 7, 2011

pp. 941-971q Emerald Group Publishing Limited

0959-6119DOI 10.1108/09596111111167542

(Andrew et al., 2007). Nevertheless, given increasingly complicated operatingenvironments and more sophisticated and educated customers and stakeholders, goodfinancial management has become even more critical in coping with ever-changingoperating parameters. It is critical that practitioners as well as academics understand therecent research on financial decisions and phenomena.

Research in hospitality financial management has noticeably emerged since the late1980s and early 1990s. Many papers have been published to disseminate newknowledge or unveil existing phenomena in the field, and to explain the managerialimplications of financial management issues and problems to industry stakeholders.However, as Harris and Brown (1998) point out in their review of research anddevelopment in hospitality accounting and financial management (with more focus onaccounting than finance), some of this work has tended to be inward-looking, withinadequate methodologies and superficial results. Atkinson and Jones (2006) also notedin their review (with more focus on management accounting than finance) that notmuch progress has been observed in areas highlighted as “innovative” in 1998, andlittle evidence exists of the development of new theories. Another critique is thatstudies have tended to replicate mainstream financial research, with the only majordifference being the use of a hospitality sample. This contributes minimally, if at all, toour knowledge. While the hospitality industry does share some commonalities withother service industries, some unique operating characteristics necessitate separateexamination of particular topics. Since Harris and Brown’s (1998) and Atkinson andJones’s (2006) works, hospitality financial management research alone has grownnoticeably in terms of diverse topics and sophistication of methodologies. The need foran update motivated us to conduct a review of recent research. The goal of this paper isto present the status of contemporary hospitality financial management research from1998 through 2009 and to suggest future research opportunities.

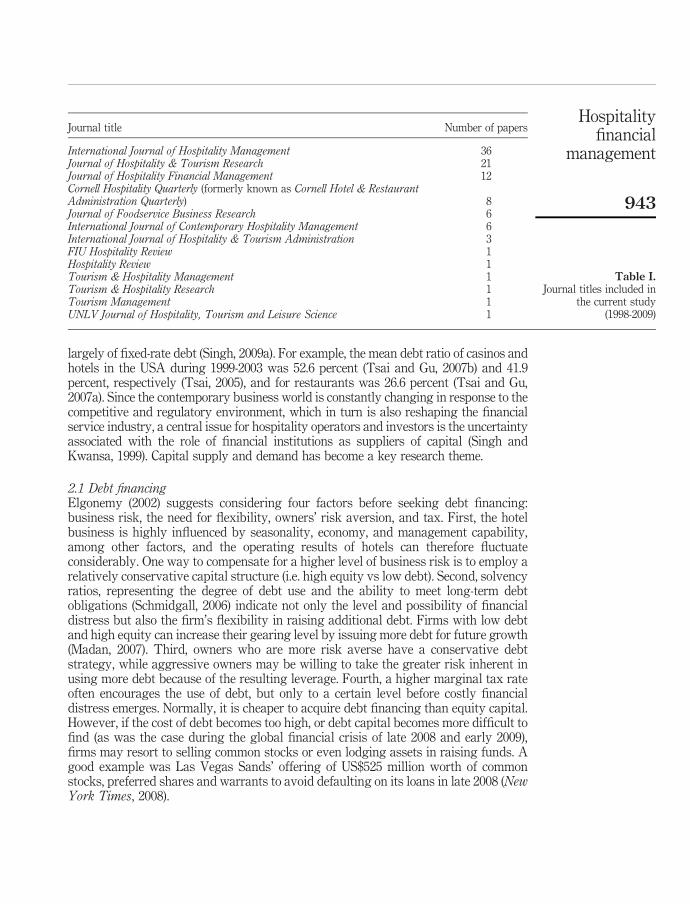

We began our initial literature search by entering into the ABI/INFORM databasevia ProQuest 19 pre-identified keywords related to the major functions of financialmanagement, namely investing, financing, and dividend decisions (Chatfield andDalbor, 2005), as well as commonly indexed keywords in hospitality finance research.The 19 keywords included risk, return, firm performance, stock, bond, weightedaverage cost of capital (WACC), capital structure, bankruptcy, financial, ownership,dividend, debt, financing, equity, asset, growth, financial management, shareholder,and corporate governance. We then expanded our literature list through the referencelists of the studies we identified. We have not included every possible piece of researchin this paper due to constraints regarding the availability of journals, language issues,and relevance, among other issues, but limited ourselves to papers published inhospitality journals between 1998 and 2009 and written in English. The list of journalswhich appeared during our search is presented in Table I.

This review is sequenced around the major functions of hospitality financialmanagement, namely hospitality financing, hospitality investing, and dividend policystudies. Studies relevant to financial conditions and performances are also reviewedand discussed. The literature included in this paper is summarized in Table II.

2. Hospitality financingHospitality firms are heavy users of long-term debt to support their asset investment(Singh and Upneja, 2008) and growth opportunities, and the debt structure is comprised

IJCHM23,7

942

largely of fixed-rate debt (Singh, 2009a). For example, the mean debt ratio of casinos andhotels in the USA during 1999-2003 was 52.6 percent (Tsai and Gu, 2007b) and 41.9percent, respectively (Tsai, 2005), and for restaurants was 26.6 percent (Tsai and Gu,2007a). Since the contemporary business world is constantly changing in response to thecompetitive and regulatory environment, which in turn is also reshaping the financialservice industry, a central issue for hospitality operators and investors is the uncertaintyassociated with the role of financial institutions as suppliers of capital (Singh andKwansa, 1999). Capital supply and demand has become a key research theme.

2.1 Debt financingElgonemy (2002) suggests considering four factors before seeking debt financing:business risk, the need for flexibility, owners’ risk aversion, and tax. First, the hotelbusiness is highly influenced by seasonality, economy, and management capability,among other factors, and the operating results of hotels can therefore fluctuateconsiderably. One way to compensate for a higher level of business risk is to employ arelatively conservative capital structure (i.e. high equity vs low debt). Second, solvencyratios, representing the degree of debt use and the ability to meet long-term debtobligations (Schmidgall, 2006) indicate not only the level and possibility of financialdistress but also the firm’s flexibility in raising additional debt. Firms with low debtand high equity can increase their gearing level by issuing more debt for future growth(Madan, 2007). Third, owners who are more risk averse have a conservative debtstrategy, while aggressive owners may be willing to take the greater risk inherent inusing more debt because of the resulting leverage. Fourth, a higher marginal tax rateoften encourages the use of debt, but only to a certain level before costly financialdistress emerges. Normally, it is cheaper to acquire debt financing than equity capital.However, if the cost of debt becomes too high, or debt capital becomes more difficult tofind (as was the case during the global financial crisis of late 2008 and early 2009),firms may resort to selling common stocks or even lodging assets in raising funds. Agood example was Las Vegas Sands’ offering of US$525 million worth of commonstocks, preferred shares and warrants to avoid defaulting on its loans in late 2008 (NewYork Times, 2008).

Journal title Number of papers

International Journal of Hospitality Management 36Journal of Hospitality & Tourism Research 21Journal of Hospitality Financial Management 12Cornell Hospitality Quarterly (formerly known as Cornell Hotel & RestaurantAdministration Quarterly) 8Journal of Foodservice Business Research 6International Journal of Contemporary Hospitality Management 6International Journal of Hospitality & Tourism Administration 3FIU Hospitality Review 1Hospitality Review 1Tourism & Hospitality Management 1Tourism & Hospitality Research 1Tourism Management 1UNLV Journal of Hospitality, Tourism and Leisure Science 1

Table I.Journal titles included in

the current study(1998-2009)

Hospitalityfinancial

management

943

Major function Area Sub-area Author

Financing Debt Generic Elgonemy (2002); Singh and Kwansa (1999)Long-term debt Dalbor and Upneja (2002); Dalbor and

Upneja (2004); Jang and Kim (2009); Jangand Ryu (2006); Jang et al. (2008); Kim andGu (2004); Tang and Jang (2007); Upneja andDalbor (2001a); Upneja and Dalbor (2001b)

Short-term debt Upneja and Dalbor (2001a); Jang and Kim(2009); Jang and Ryu (2006)

Interest rate Corgel and Gibson (2005); Kim and Gu(2004); Singh and Upneja (2007); Singh andUpneja (2008), Singh (2009b)

Leasing behavior Koh and Jang (2009); Upneja and Dalbor(1999); Whittaker (2008)

Equity Cost of equity Lee and Upneja (2008); Madanoglu andOlsen (2005); Madanoglu, Erdem andGursoy (2008)

Ownershipstructure

Gu and Kim (2001); Gu and Qian (1999); Kimet al. (2007); Leung and Lee (2006); Oak andDalbor (2008a); Skalpe (2003); Tsai and Gu(2007a); Tsai and Gu (2007b)

Capital structure Canina and Carvell (2008); Chathoth andOlsen (2007b); Jang and Tang (2009);Karadeniz et al. (2009); Kim et al. (2007); Lee(2007); Madan (2007); Ozer and Yamak(2000); Sharma (2007); Tang and Jang (2007)

Investing Risk and return Generic Borde (1998); Canina and Carvell (2008); Kimand Gu (2003); Lee (2008a); Madanoglu, Leeand Kwansa (2008); Mao and Gu (2007);Skalpe (2003)

Systematic risk Barber et al. (2008); Borde (1998); Kim et al.(2002a); Gu and Kim (2002)

Unsystematicrisk

Gu and Kim (2003); Hsu and Jang (2008);Kim et al. (2002a); Tang and Jang (2008)

Foreign currencyrisk exposure

Chang (2009); Singh and Upneja (2007);Singh and Upneja (2008)

Interest rate riskexposure

Singh (2009a); Singh (2009b); Singh andUpneja (2007); Singh and Upneja (2008)

Merger andacquisition

Canina (2009); Hsu and Jang (2007); Kim andArbel (1998); Oak et al. (2008); Yang et al.(2009)

Stock investment Chen (2007); Chen and Kim (2006); Chen et al.(2007); Chen et al. (2009); Chen et al. (2005);Denizci (2007); Gu and Kim (2003); Kim et al.(2002b); Upneja et al. (2008)

Capitalbudgeting

Ashley et al. (2000); Damitio and Schmidgall(2002); Guilding and Hargreaves (2003);Guilding and Lamminmaki (2007); Rubelj(2006)

(continued )

Table II.Hospitality financialmanagement studies(1998-2009)

IJCHM23,7

944

2.1.1 The use of long-term debt. The hospitality industry is capital-intensive andnormally requires heavy debt financing, particularly of long-term debt. In their study ofUS lodging firms’ debt choices, Upneja and Dalbor (2001b) tested three hypotheses(pecking order, trade-off (i.e. tax effects), and free cash flow) proposed by Barclay andSmith (1995). They showed that growth opportunities, firm risk, and fixed assets were allpositively correlated, and depreciation tax shields negatively correlated with long-termdebt. They measured growth opportunities by the ratio of market value to book value ofthe firm’s assets (MVA), firm risk by the probability of bankruptcy, and fixed assets bythe ratio of property, plant, and equipment (PP&E) to total assets. Contrary to Barclayand Smith’s suggestion that firms with greater growth opportunities should use lessdebt, Upneja and Dalbor found a tendency for lodging firms to use more debt to fundgrowth. This differs from restaurant firms (Upneja and Dalbor, 2001a) and otherindustries. To assess the appropriateness of using MVA as a proxy for growthopportunities, Dalbor and Upneja (2004) reexamined US lodging firms’ long-term debtdecisions using five different growth opportunity proxies and a different sample. Whilethe relationships between the five growth opportunity proxies and long-term debtdecisions were mixed, the results, as claimed by the authors, supported the notion thatthe lodging industry is distinct in financing its growth with long-term debt. Tang andJang (2007) also supported this finding. Lenders likely feel more comfortable with realestate-type investments and with secured collaterals; furthermore, debt capital worksbetter for controlling possible agency problems (Dalbor and Upneja, 2004).

Major function Area Sub-area Author

Dividend policy Borde et al. (1999); Canina et al. (2001);Dalbor and Upneja (2007); Kim and Gu(2009); Oak and Dalbor (2008b)

Financialcondition andperformance

Bankruptcy Dalbor and Upneja (2002); Dalbor andUpneja (2004); Diener (2009); Gu (2002); Janget al. (2008); Kim and Gu (2006a); Kim andGu (2006b); Upneja and Dalbor (2001a);Upneja and Dalbor (2001b); Youn and Gu(2009)

Firmperformancedeterminants

Canina and Carvell (2008); Chathoth andOlsen (2007a); Chi and Gursoy (2009); Huaand Upneja (2007); Jung (2008); Kang et al.(2009); Ketchen et al., 2006; Kim et al. (2003);Koh et al. (2009a); Koh et al. (2009b); Lee,2008(b); Lee and Park (2009); Madan (2007);Madanoglu, Erdem and Gursoy (2008);Madanoglu, Lee and Kwansa (2008); Maoand Gu (2008); McGehee et al. (2009); Parkand Lee (2009); Prasad and Dev (2000); Tsaiand Gu (2007a); Tsai and Gu (2007b); Younand Gu (2007)

CEOcompensationand turnover

Barber et al. (2006); Barber et al. (2009); Kimand Gu (2005); Gu and Choi (2004);Madanoglu and Karadag (2008) Table II.

Hospitalityfinancial

management

945

Nevertheless, identification of appropriate proxies for growth opportunities in thehospitality industry still remains a research need and is critical because growthopportunities not only determine hospitality firms’ long-term debt decisions (Upnejaand Dalbor, 2001b; Dalbor and Upneja, 2004; Tang and Jang, 2007) but also theliquidity of restaurant firms, for example (Chathoth and Olsen, 2007b). Hospitalityfirms in recent decades have noticeably expanded through management contracts andfranchising agreements (excepting casinos; Beals, 2006), and through investing inphysical assets. The power of intangible assets such as brand equity cannot beoverlooked when hospitality firms’ maintain or seek growth. A good research questionis whether or not traditional growth measures such as sales and asset growth can bestreflect the growth opportunities of hospitality firms of different types (e.g. hotels vsrestaurants) and different ownership/management structures (e.g. management vsfranchised) under different economic situations (e.g. favorable vs unfavorable).

Firm quality (or risk of going bankrupt) and size have been found to be significantlycorrelated to the long-term debt decisions of restaurant firms (Dalbor and Upneja, 2002)and lodging firms (Dalbor and Upneja, 2004). Both studies indicated that the lowerquality of those firms (i.e. having a higher risk of bankruptcy) was probably caused bya higher level of long-term debt usage. Larger firms tend to use more long-term debtbecause they can afford the higher fixed costs. Nevertheless, firm size was not found tobe a significant determinant of lodging firms’ long-term debt decisions by both Upnejaand Dalbor (2001b) and Tang and Jang (2007). This could be because hotel firmsprimarily expand by franchising, which limits the types of assets to be financed(Upneja and Dalbor, 2001b). Furthermore, hotel firms may find it more convenient toexpand using debt financing if they lack internal funding, so that equity becomes amuch more expensive route of financing as market value increases.

Hospitality firms with more investment in fixed assets such as land, buildings, andproperties have been found to use more long-term debt (Upneja and Dalbor, 2001b),which corresponds to the principle of maturity matching between assets and liabilities(Stowe et al., 1980). On the other hand, short-term assets are more likely to be financedusing short-term liabilities ( Jang et al., 2008). Such firms should be able to negotiatemore preferable debt arrangements, regardless of the associated risks, than theircounterparts with lower fixed assets, because the latter can serve as collateral (Tangand Jang, 2007; Jang et al., 2008). Older and more profitable firms with better cash flowseem not to need long-term debt (Upneja and Dalbor, 2001a).

2.1.2 The use of short-term debt. While current liabilities are closely related to afirm’s liquidity and net working capital, short-term debt financing is a relativelyless-studied topic. In their study of restaurant firms’ capital structure, Upneja andDalbor (2001a) argued that total debt should be examined along with short- andlong-term debt because of the operational uniqueness of restaurant firms. They showedthat firms with a high probability of bankruptcy use more short- than long-term debt.Furthermore, short-term debt is negatively related to operating cash flow. This impliesthat restaurant firms should focus more on generating operating cash flow to replace orcover costly short-term debt.

In their study of the interdependencies between investing and financing decisions ofUS restaurant firms, Jang and Ryu (2006) explained the unique financing behavior ofrestaurant firms. While their study generally supported the four cross-balance sheetinterdependencies as found in other industries, they also claimed that restaurant firms

IJCHM23,7

946

appear not to relate accounts receivable to short-term liabilities and that they financetheir operational assets with stockholders’ equity in addition to accounts payable.However, their study results contrast with previous studies’ findings that accountsreceivable is highly related to accounts payable and that current liabilities usuallyfinance operational assets. Jang and Ryu’s study was examined further by Jang andKim (2009) to assess the firm size effect on restaurant firms’ financing behavior. Jangand Kim found that small and medium restaurant firms rely more on accounts payablewhereas large firms use more long-term debts, and that long-term assets relate tostockholder equity among large firms but relate to supplier credit among small andmedium firms. Nevertheless, the reason behind the firm size effect on restaurant firms’financing behavior remains unclear.

The lack of research on short-term financing options in other hospitality segmentssuggests future research opportunities. The labor-intensive nature of hospitalitybusinesses and the system of trade credit both contribute significantly to theirpayables accounts (i.e. wages and accounts payable); short-term liquidity is critical. Forexample, casino firms rely heavily on cash transactions, but their operating cash flowscan be quite uncertain and can fluctuate significantly on a daily basis. Insufficient cashflows generated from operating activities will likely trigger a need for short-termfinancing such as taking advantage of revolving credit facilities.

2.1.3 Interest rate. Interest represents a tax shield benefit to a firm. However, itcould also cause financial distress if debt financing is not properly arranged andmonitored. Interest rates determine the amounts paid and therefore are an importantissue for firms making decisions about debt financing. Corgel and Gibson (2005)showed that for hotel firms, the frequency of financial distress from floating-ratefinancing is less than or equal to that from fixed-rate arrangements. They suggestedthat hotel owners should focus on managing financial distress by aligning operatingcash flow and debt-servicing obligations, within which floating-rate debt is preferred.

Interest rate derivatives have been used by hotel firms to hedge against the riskexposure of interest rates. Singh and Upneja (2007) indicated that bothvariable-to-fixed interest rate swaps and interest rate caps are used to hedge againstrising interest rates. Singh (2009b) also highlighted that small, unrated firms are morelikely to issue short-term debt and swap it into fixed-rate debt to reduce exposure tointerest rate risk. On the other hand, larger and higher-rated firms tend to swap fromfixed into floating-cash flow debt. Singh argued that smaller, unrated lodging firmsthat are more reliant on short-term debt in the form of floating-rate bank loans will findlong-term fixed debt too costly. By issuing floating-rate debt and swapping it intofixed-rate debt, smaller, unrated firms could benefit from lower costs of both financingand financial distress, and reduced exposure to interest rate risk. Additionally, theproportion of floating-rate debt has been found to be positively and significantlyrelated to a firm’s decision to hedge (Singh and Upneja, 2008). In other words, firmswith more floating-rate debt seem to be more likely to use derivatives to alter theirexposure from floating- to fixed-rate interest (Singh and Upneja, 2007).

The topic of interest rate has been extensively studied in mainstream economic andfinance research, and its role associated with the hospitality industry could be furtherexamined. First, while interest rate has been viewed and employed as a workable leverin signaling the monetary policy of an economy, no investigation has examined howthe hospitality industry has reacted to movements of interest rate in terms of

Hospitalityfinancial

management

947

borrowing or investing funds. Second, fluctuations of the prevailing interest rate couldaffect investors’ assessments of a firm’s intrinsic value resulting from their perceivedinvestment risks (Keown et al., 2005), thus possibly affecting firm value andstockholder wealth. The interplay between interest rate movements and stockholderwealth deserves empirical exploration. Third, while the hospitality industry appears toincreasingly rely on corporate bonds since the commencement of the century (Kim andGu, 2004), relatively less research has focused on how interest rate is related to bondissuance. The level of the prevailing interest rate not only affects the selling price of abond, but also determines a bond investor’s yield to maturity (YTM). Kim and Gu’sstudy only examined financial determinants of corporate bond ratings of hotel andcasino firms, creating a need for future research on topics such as corporate bondissuance decisions.

2.2 Leasing behaviorLeasing requires minimum upfront costs to acquire assets and provides tax advantagesfor some firms (Upneja and Dalbor, 1999). Firms in financial distress may find leasing aviable alternative to debt financing when acquiring equipment. In their study of theleasing behavior of restaurant firms, Upneja and Dalbor (1999) showed that both before-and after-financing tax rates are significantly and positively related to the use of capitalleases, and both relate significantly and negatively to the use of operating leases. Firmsin good financial standing are less likely to use operating leases. In other words, anincrease in the use of operating leases may signal deterioration in a firm’s financialhealth. The authors further indicated that firms that are closer to bankruptcy willgenerally choose operating rather than capital leases. Koh and Jang (2009) examined thedeterminants of using operating leases in the hotel industry and showed that hotels withfewer internal funds and/or higher debt ratios are more likely to use them. They alsoshowed that the use of operating leases decreases as firm size increases but only up to acertain level, after which use increases with firm size. In contrast to the restaurantindustry, less financially distressed hotel firms are more likely to use operating leases asfinancing instruments. The authors argued that using operating leases could serve as amanagement strategy, rather than a purely alternative financing instrument. The mixedconclusions reached by the researchers of the two studies on the use of operating leasesversus capital leases seem to relate to the type of industries under investigation.However, empirical comparisons of leasing behaviors between different segments of thehospitality industry within the same economic situation could help further illuminatehospitality firms’ leasing decision-making.

A number of investors are entering the sales and leaseback transactions (SLBT)market that provides alternative sources of funding for hotel firms. These investors,particularly private companies, have been using SLBT as means of acquiring orgrowing their portfolios (Whittaker, 2008). Meanwhile, hotel operators obtain cheaperfunding because of the increased supply of lease funds available in the market andmight therefore appear financially healthy from a debt-equity ratio perspective. Anoperating lease is considered to be a type of off-balance sheet financing, a term that isbecoming better known since the Enron collapse in late 2001. The level of operatinglease use may affect how creditors and investors use available information to evaluatea firm, its financial condition, and its growth and earnings potential. This could beanother topic for further investigation.

IJCHM23,7

948

2.3 Equity financing2.3.1 Cost of equity. Despite the limitations of and criticism towards the use of theCapital Asset Pricing Model (CAPM) in estimating the cost of capital, it was popularwith 65 percent of the Fortune 1000 companies in 1997 (Gitman and Vandenberg, 2000)and 60 percent of CFOs used it as their primary methodology (Graham and Harvey,2001). Arguing for the unique operating characteristics of the lodging industry, Leeand Upneja (2008) compared traditional methods of estimating the cost of equity(i.e. CAPM and the Fama and French (FF) three-factor model) with the implied cost ofequity (ICE) method. They showed that the price-to-forward earnings (PFE) using theICE approach offers a more reliable estimation of the cost of equity for the lodgingindustry.

In estimating the size effect on the estimation of cost of equity for casual-diningrestaurants, Madanoglu, Erdem and Gursoy (2008) concluded that investors couldexpect a higher return from the large-firm portfolio using the CAPM, but a higherexpected return from the small portfolio when using the FF model. However, theirconclusion is limited for two reasons. First, the two models were not able to estimatethe cost of equity for the 15-month period following September 11, 2001. Second, ashort estimation period was used in their study. While the two models producedseemingly conflicting results, the need for a hospitality industry-specific cost of equitymodel is justified.

Considering the attributes that are particularly important for the lodging industry,Madanoglu and Olsen (2005) proposed a theoretical model for estimating the riskpremium using the following five constructs: human capital (Hcap), technologyinvestment and utilization (Tech), brand strength index (BSI), safety and security index(SSI), and industry factors (IND). The first three are posited to contribute negatively tothe risk premium, and to SSI positively. The sign of the relationship between IND andthe risk premium remains unknown. They also argued that companies with higherbrand strength and that invest in and utilize technology more efficiently will be able toachieve a lower cost of equity capital. They further introduced the Lodging AssetPricing Model (LAPM) that incorporated two industry-specific variables to the Famaand French three-factor model excluding the HML (i.e. the difference between thereturns on portfolios of high- and low-book equity/market equity stocks) variable. TheLAPM is stated as follows:

E Rið Þ2 Rf ¼ biERP� �

þ sSMBð Þ þ ðiBSIÞ þ ð pPOSÞ

where E(Ri) is the expected return of a security i, Rf the risk free rate, ERP the equityrisk premium, SMB the size factor, BSI the brand strength index, and POS the propertyownership structure. The LAPM, compared to other traditional pricing models,appears to have the merit of more appropriately estimating the cost of capital for thelodging industry specifically considering the intangible nature of its products andservices. However, the proposed framework needs further empirical validation towarrant its practical application.

One potential issue is the measurement of the variables on the right hand side of theLAPM equation. For example, there seems to be no consensus in academic research onhow brand strength should be measured for the lodging industry. This lack ofconsensus exists despite the fact that some hospitality firms’ (e.g. McDonald’s, KFC,and Starbucks) brand values have been evaluated by commercial firms such as

Hospitalityfinancial

management

949

Interbrand (Interbrand, 2010) and that a few hotel brand equity studies (e.g. Kim et al.,2003; Prasad and Dev, 2000) have been conducted. Furthermore, the determination ofthe size factor could be challenging because many lodging firms expand throughmanagement contracts and franchising agreements in addition to investing in physicalassets as noted above.

2.3.2 Ownership structure. One central issue for equity financing is the topic ofownership structure and its impact on corporate governance and firm performance inlight of the agency relationship. Although Demsetz (Harold Demsetz, personalcommunication, March 3, 2004) stated that there is no reason to expect small firms withhighly concentrated ownership structures to perform better or worse than large firmswith more diffuse structures, empirical studies in mainstream finance mainly support apositive relationship between ownership structure and firm performance. Thisrelationship has been examined using multiple regression analyses to revealsignificant and positive relationships between managerial shareholdings and firmperformance for both the restaurant (Gu and Kim, 2001) and hotel (Gu and Qian, 1999)industries. Both studies used multiple accounting measures (i.e. return on equity (ROE)and return on assets (ROA)) and stock returns as firm performance proxies andconcluded that managerial ownership could be a proxy for the convergence of interestsbetween managers and owners, and could help improve accounting profitability andequity owners’ returns. Nevertheless, neither study considered other affiliates such ascreditors within the agency framework, nor did they address the possible endogenousrelationship between ownership structure and firm performance. As a result, theregression coefficients obtained in these studies could be biased and their conclusionsare potentially challengeable. Therefore, conclusions from Gu and Kim’s and Gu andQian’s studies require further validation addressing the above-mentionedshortcomings.

The increasing importance of institutions in the hospitality industry can beobserved from the growing volume of equity that they control (Tsai and Gu, 2007a),and as a result, several studies have been conducted on institutional investors.Studying the “Monday effect” on tourism stocks, Leung and Lee (2006) showed thatstocks followed by fewer institutional investors can cause negative Monday effects andthat the Monday return of a stock is positively correlated with its institutionalshareholdings. They argued that by attracting more institutional investors, thevolatility of tourism stock returns is reduced and the required rate of return forshareholders is lowered. Institutional investors’ preferences for lodging stockinvestment were examined by Oak and Dalbor (2008a). While institutions generallyprefer large firms, different types of institutions favor firms with different financialcharacteristics. For example, banks prefer lodging firms with low book-to-marketvalue ratios, high liquidity, and high growth opportunities, whereas insurancecompanies favor those with high capital expenditure-to-asset and high debt ratios.Mutual funds, pension funds, and brokerage firms were also examined in their study.However, Oak and Dalbor’s study suffered from the oversight of possible endogeneitybetween the ownership and performance variables.

The relationship between institutional ownership and firm performance in therestaurant (Tsai and Gu, 2007a) and casino (Tsai and Gu, 2007b) industries has alsobeen studied. Considering the possible ownership endogeneity issue and applying boththe ordinary least square (OLS) and two-stage least square (2SLS) approaches, both

IJCHM23,7

950

studies showed that institutional ownership has a significant impact on performancefor both casinos and restaurants. They also showed that institutional investors tend toinvest in better performing, larger, and more profitable firms with low financialleverage. Furthermore, they argued that institutional investors and creditors couldsubstitute for each other in their monitoring roles with respect to management incorporate governance.

Kim et al. (2007) found that the profit margin in restaurant firms depends on thelevel of ownership percentage and management type. Profit margin decreases as thelevel of primary ownership of the owner-manager decreases; however, it is higher forowner- than outside-manager firms. Profit margin is lower for owner-managed firmswhen the primary ownership percentage is under 50 percent. Skalpe (2003) argued thataccommodation providers and restaurant keepers have aims other than maximizingreturns, such as social prestige. Owners-managers’ personal values influence theirstrategies and ultimately their firms’ performance.

The ownership structure of a firm is a complicated issue. The level of variousownership types might affect corporate governance and the involvement of owners infirm management. This could influence a firm’s strategic direction and its long-termbottom line. Of particular interest is institutional shareholding in the casino industrydue to its strict regulation of significant shareholdings and the potential influence oncorporate governance. Ownership-related issues such as block holdings, familyholdings, and stock options could be interesting research topics in this field. Anothermarket worth investigating is China. A number of state-owned enterprises in Chinaunderwent privatization through share reform since the late 1990s, and there are nowmore types of ownership in Chinese corporations than in their Western counterparts.Despite their privatized status, these corporations are still significantly influenced bythe state. Future studies could investigate the interplay of privatized enterprises withthe state and the implications for firm performance and corporate governance.

2.4 Capital structureFrom a financial perspective, capital structure is one of the most importantdeterminants of a firm’s sustainable growth (Madan, 2007) because it relates to the costof capital or the required rate of return for the firm. Chathoth and Olsen (2007b) showedthat capital structure, along with environment risk and corporate strategy, helpsexplain a significant amount of the variance in firms’ performance. Facing highfinancial risks and volatile operating environments, it is important for lodging firms todetermine the composition of their capital structure and the factors affecting leveragedecisions and debt ratios (Karadeniz et al., 2009). A disadvantage of high financialleverage is the higher borrowing cost associated with debt facilities and the resultingdefault risk. If a firm’s profits are low, the high risk of default pushes up the lendingrate higher while increasing the interest costs (Madan, 2007). Madan (2007) also arguedthat firms with low share capital but high reserves and debt should either use theiraccumulated profits or issue fresh capital when contemplating expansion. The latterapproach should help control their gearing ratio and reduce investors’ perception ofrisk, which could help improve ROE.

In comparing the determinants of capital structure between US software andlodging firms, Tang and Jang (2007) showed that lodging firms’ leverage behavior didnot significantly respond to earning volatility, firm size, free cash flow, or profitability

Hospitalityfinancial

management

951

because they neither increased nor decreased their debt-financing costs. Jang and Tang(2009) indicated that a firm’s financial leverage has a direct inverted U-shapedrelationship with profitability and argued that financial, rather than business,strategies are a more direct and efficient way to achieve higher profitability. They alsosuggested that the maximum profitability, corresponding to optimal leverage, can beinflated by increasing the level of international diversification. In other words, a firmcan increase the positive impact of the former by increasing the latter. Neither strategicnor financial decisions can be mutually isolated to improve financial performance.Chathoth and Olsen (2007a) showed that smaller firms report higher ROE than biggerfirms when economic risk is lower and market risk is higher than for the average firm,given that the liquidity and debt ratio of such firms is lower than average. However,Lee (2007) suggested that changes during specific economic periods do not reflect anindustry-wide practice for determining the capital structure of lodging firms.

Ozer and Yamak (2000) examined the financial sources used by small hotels (lessthan 100 rooms) in Istanbul. They showed that such firms use internal funds and debtin their investment stage, and retained earnings at the operating stage. External debtappears to be negligible; owners do not even consider bank loans due to the difficultyof finding credit and the high costs of doing so. Also in the Turkish context, Karadenizet al. (2009) found that effective tax rates, tangibility of assets, and ROA are negativelyrelated to the debt ratio of lodging firms, while free cash flow, non-debt tax shields,growth opportunities, net commercial credit position, and firm size have norelationship with debt ratio. Neither the trade-off nor the pecking order theories seem toexplain the capital structure of Turkish lodging firms. Sharma (2007) showed that verysmall hotels (about 25 rooms) in Tanzania obtain most of their funds through personalsources or commercial banks. Their financing options are limited because theynormally lack the professionalism and collateral to obtain credit.

Financial leverage for single-family majority and minority firms will be differentdepending on the ownership percentage of the primary owner. Financial leverage has apositive relationship with the interaction between ownership percentage andsingle-family majority/minority ownership, while family majority ownership is asignificant factor in explaining asset utilization (Kim et al., 2007). Canina and Carvell(2008) reported that in terms of type of restaurant operations, owner-operators havehigher liquidity than franchisers, and can buffer more effectively between theirshort-term financial obligations and their cash on hand to meet these obligations.

There exists little, if any, room for hospitality firms to develop or invent unique orcompetitive capital structure tactics, compared to possible asset structure variations(Andrew et al., 2007). Therefore, previous studies related to capital structure focused onexamining the consequences of different levels of capital structures. Jang and Tang(2009) stated the importance of careful control of a firm’s financial leverage at anoptimal level. Although an optimal capital structure might, in theory, be reached byestablishing an equilibrium between the advantages (e.g. tax breaks) anddisadvantages (i.e. financial distress and bankruptcy-associated costs) of debt usage,there are few empirical studies of this topic in hospitality firms. This could be aninteresting topic to explore, contributing to both the hospitality financial managementfield and mainstream finance literature.

IJCHM23,7

952

2.5 Evolution in hospitality financingDuring the 1990-1991 recession, the hotel industry suffered from low occupancy rates,having overbuilt room inventory in the late 1980s (Hotel & Motel Management, 1994).Recovery had begun by late 1992 and the industry became profitable again in 1993(Block, 1998). Along with improved profitability and performance, renovations of guestrooms, restaurants, meeting rooms, lobbies, and other public spaces were initiated usingavailable cash flow and, more importantly, funding from increased institutionalinvestment (Hotel & Motel Management, 1994). As a result, pension funds and lifeinsurance companies became major sources of direct-equity capital for lodging realestate, while mutual funds, pension funds, and life insurance companies became thelargest purchasers of lodging company stocks (Singh and Kwansa, 1999). Singh andKwansa (1999) suggested that changes in the minimum loan sizes offered by financialinstitutions are clear indications of the competitive landscape that is expected to prevail.The overall differences in minimum loans between large, intermediate, and small lendershave been progressively narrowing. For example, small lenders can provide a minimumof US$1 million while large lenders will offer US$5-10 million. Different types of financialinstitutions can finance different types or modes of hospitality firms. For example, resorthotels have a high probability of borrowing from large lenders, given the expectedgrowth in spending on fitness, leisure, and recreation. Life insurance companies andpension funds have a high to moderate probability of financing convention hotels, but arelatively low chance of being involved in casino hotels due to overbuilding, high cost ofconstruction, and a preference to wait for more states to legalize gaming (Singh andKwansa, 1999). Singh and Kwansa’s prediction for casino hotel financing underestimatedthe growth potential of the casino (hotel) industry; the notion of “if you build it, they willcome” seems to have held since the mid-1990s.

The importance of private funding in the marketplace is expected to continueplaying an important role in hospitality capital (Elgonemy, 2002). For example, in thecasino industry, Harrah’s was acquired for US$15.05 billion in 2006 by a private-equityfirm owned by Apollo Advisors and TPG Capital. This was followed in 2007 by StationCasinos’ US$5.4 billion management-led buyout. In the hotel industry, one majorbuyout was that of the Four Seasons Hotels, which was taken private in 2007 byCascade Investment and Kingdom Hotels in a deal worth almost US$4 billion. Issuesrelated to the operations, management, and performance of these firms after thebuyouts have not yet been examined, so there is a need for such evaluation. Theimportance of institutional investors to the hospitality industry has been heightenedbecause they now control a significant portion of lodging, restaurant, and casino equity(Hotel & Motel Management, 2002; Tsai, 2005; Tsai and Gu, 2007a; Tsai and Gu,2007b). Continuing support from institutional investors can be expected, and theirinvolvement and interactions with firms and their management could be investigatedfurther, as could the possibility of differences in ownership structures and involvementin management and corporate governance in countries and regions other than the USA.

3. Hospitality investingActivities related to hospitality investing can be examined from two perspectives, namelythe firm and its investors, although a majority of published studies focus on the latter.From a firm perspective, research has provided capital budgeting guides, practices, andbenchmark comparisons (Guilding and Lamminmaki, 2007; Rubelj, 2006; Guilding and

Hospitalityfinancial

management

953

Hargreaves, 2003; Damitio and Schmidgall, 2002; Ashley et al., 2000). Capital budgetingrelates to how firms respond to their operating and business strategies, appraise capitalexpenditure projects and make informed decisions that will bring value to the firm andshareholders. For example, Guilding and Lamminmaki (2007) demonstrated a positiverelationship between hotel size and the use of financial investment appraisal techniques.Regarding the formalization of capital budgeting systems and investment techniques,hotels are less developed in reviewing required rates of return and in applyingpost-completion audits. Studies from the investors’ perspective are more diverse andinclude topics such as risk and return and performance measurement, among others.

3.1 Risk and returnExamining the restaurant industry in detail and categorizing it into three types (fullservice, fast food and economy/buffet), Kim and Gu (2003) showed that over the period1996-2000, the full-service restaurant segment had the lowest total risk, as measured bystandard deviation. However, in terms of three risk-adjusted performance measures(i.e. the Sharpe ratio, Treynor ratio, and Jensen index), the fast-food segment wasranked as the best performer, followed by full service and economy/buffet. Focusing oncasual-dining restaurants alone, Madanoglu, Erdem and Gursoy (2008) found thatlarge restaurants outperformed their smaller counterparts on a risk-adjusted basisduring 1998-2002. In their study, they employed both traditional risk-adjustedperformance measures (i.e. Sharpe, Treynor and Jensen) and contemporaryrisk-adjusted performance measures (e.g. the Sortino ratio and Fouse Index).

On the sector level, Mao and Gu (2007) investigated the risk/return relationship invarious industries of the hospitality sector during the economic downturn of 2000-2003.Four portfolio performance indexes (the Treynor index, Sharpe ratio, Jensen index, andappraisal ratio) were estimated to measure the firms’ risk-adjusted stock performances.The casino/gaming industry was found to have the highest return with medium risk,followed by the restaurant industry with mediocre return but lowest risk. Thehotel/motel industry had the weakest performance but highest risk. The results of Maoand Gu’s (2007) study contradict the traditional wisdom that risk and return go hand inhand, as suggested by the CAPM. That is, a higher level of risk should be compensatedby a higher level of return, if the investor is risk-averse.

Other studies of the risk/return relationship present similarly contradictory results(Borde, 1998; Kim and Gu, 2003; Madanoglu, Erdem and Gursoy, 2008; Madanoglu, Leeand Kwansa, 2008; Mao and Gu, 2007; Skalpe, 2003). Madanoglu, Lee and Kwansa(2008) confirmed that a casual-dining portfolio allows investors to earn a higher returnfor a lower level of risk compared to the fast-food segment. Much of the risk related tohotel and restaurant investment is unsystematic (Kim and Gu, 2003; Skalpe, 2003).Canina and Carvell (2008) showed that restaurant operations or franchising have highlevels of short-term financial risk in terms of liquidity measures.

In examining the relationship between four financial risk factors and futureperformance as measured by ROA and ROE, Lee (2008a) found that strategic and stockperformance risk factors represent a lodging firm’s financial risk better thanbankruptcy and firm performance risk factors. Furthermore, strategic and stockperformance risk factors each have a significant and negative predictive ability forfuture performance as measured by ROA. ROA outperforms ROE in estimatinglodging firm performance in terms of its relationship with financial risk.

IJCHM23,7

954

3.1.1 Systematic risk. Dividing risks into systematic and unsystematic, andexploring their determinants in the hospitality industry, has been a popular researchtopic. For example, in studying hotel real estate investment trusts’ (REITs) beta (i.e.systematic risk) determinants, Kim et al. (2002a) showed that systematic risk iscorrelated positively with debt leverage and growth but negatively with firm size asmeasured by capitalization. The positive correlation between debt ratio and betasuggests that using less debt and pursuing conservative growth could reducesystematic risk for hotel REITs, while the negative relationship between capitalizationand beta suggests that they have lower systematic risk and are less sensitive to marketmovements. Although synergy may enable large hotel REITs to benefit from lowoperating and capital costs, geographical diversity can help them achieve revenuestability (Kim et al., 2002a).

Using financial data from 75 US restaurant firms from 1996-1999, Gu and Kim(2002) applied weighted least-squares regression analysis to examine systematic riskdeterminants. They showed that restaurant systematic risk correlates negatively withasset turnover but positively with quick ratio. High efficiency in generating salesrevenue helps to lower systematic risk while excess liquidity tends to increase it.Echoing Gu and Kim (2002), Barber et al. (2008) showed that efficient use of existingrestaurant assets is the key to risk reduction and value enhancement. They argued thatproperly investing excess cash flow in operating assets and high asset turnover couldlower systematic risk, whereas director turnover could increase it (depending on afirm’s state of development).

Liquidity level is positively related to both systematic and total risk (Borde, 1998;Barber et al., 2008). High liquidity may imply that available resources are beinginvested in marketable securities, which could increase risk, and are not invested inhigh-earning operating assets. The dividend payout ratio is negatively related to bothsystematic and total risk (Borde, 1998; Barber et al., 2008). Firms are typically reluctantto vary their dividend payouts significantly once a certain level has been established,especially if this means cuts. Restaurants with a high level of operating risk are likelyto distribute a smaller fraction of their earnings than those with lower risk. However,leverage seems to be unrelated to either systematic or total risk since it has littleinfluence on market-based risk measures.

Estimation of the systematic risk for a capital investment, as compared to that for afirm’s stock, can be quite challenging because there might not be existing or historicalreferences available. The estimation can become even more complicated when theimpact of financial leverage is included (Van Horne, 2002), which further affects thecalculation of the cost of equity and capital. No published studies exist that assess theappropriateness of using various methods of estimating the systematic risk for acapital investment as suggested in finance textbooks. Future research could meet thisneed if empirical data become available.

3.1.2 Unsystematic risk. Studying hotel REITs’ risk features, Kim et al. (2002a) foundthat 84 percent of their total risk could be attributed to firm-specific, or unsystematic,risk. The proportion of unsystematic risk in the total risk of hotel REITs is higher thanthat of other US stocks. Gu and Kim (2003) indicated that hotel REITs’ unsystematic riskis associated positively with debt and dividend payouts but negatively withcapitalization. That is, hotel REITs with higher debt leverage could be subject togreater stock volatility when firm-specific events occur. Furthermore, large hotel REITs

Hospitalityfinancial

management

955

are less risky in terms of unsystematic risk. The authors suggested that consolidation,via mergers and acquisitions, could quickly increase a hotel REIT firm’s marketcapitalization and consequently help reduce unsystematic risk. Their results alsosuggest that the market reacts more strongly to firm-specific events affecting hotelREITs paying higher dividends. Higher dividend payout could increase unsystematicrisk, and hotel REITs must carefully consider the effect of this on investment capital andfinancing mix, and on unsystematic risk. The authors argued that large hotel REIT firmspaying lower dividends and using less debt are likely to have a valuation advantage.

Tang and Jang (2008) compared hotel C-corporations and REITs in terms of theprofitability impact of their requirements and showed that the latter pay less tax andhave higher levels of fixed assets, ownership diversification, and dividend payoutratios. They suggested that the relationship between profitability and dividend payoutmight be nonlinear. Hotel REITs not only pay more dividends than required but canalso pay more than their net income, because of extra cash from depreciation.Moreover, the only significant variable affecting the ROA of hotel REITs andC-corporations is the different dividend payout. ROA increased more quickly inC-corporations for the same amount of increase in payout, implying that this decreasesfree cash flow associated agency costs faster than for hotel REITs.

Comparing the unsystematic risk determinants of the hotel and restaurantindustries, Hsu and Jang (2008) showed that profitability is the most influential factor.That is, more profitable hospitality firms suffer less unsystematic risk. Financial andoperating leverage and firm size are also significantly associated with theunsystematic risk of the hospitality firms studied.

Previous studies focused on examining the relationship between a firm’sunsystematic risk and its financial features. However, unsystematic risk isfirm-specific, and future studies could explore how nonfinancial features of ahospitality firm relate to its unsystematic risk. For example, Rego et al. (2009) foundthat consumer-based brand equity has a stronger role in predicting firm-specificunsystematic risk than systematic risk.

3.1.3 Foreign currency risk exposure. Foreign exchange fluctuations are animportant determinant of risk for hotels operating internationally. Occupancy maydecline in strong currency environments, and the resulting loss could be compensatedfor by gains in exchange. A weak local currency may threaten dollar-denominatedearnings, and managers can make up for currency loss by increasing the average dailyrate (ADR) without reducing occupancy. Although about 60 percent of foreignexchange risk exposure could be attenuated or even eliminated (Chang, 2009), very fewhospitality firms manage such risk, because either the amount is immaterial or it is notcost effective to use derivatives (Singh and Upneja, 2007; Singh and Upneja, 2008).Singh and Upneja (2007) suggested that few lodging firms use derivatives such asforwards to hedge against foreign exchange risk exposure. They showed that theforeign sales ratio and diversification measures of a firm provide weak evidence fortheir use of derivatives, and that hospitality firms with higher growth opportunitieswill use derivatives more. However, firms have less incentive to take this approach ifthey have enough internal cash flow to cover fixed claims and fund future investment(Singh and Upneja, 2007).

Various currencies, such as the Australian dollar, Chinese yuan, and Japanese yen,have experienced volatile fluctuations in recent years and the gain or loss from such

IJCHM23,7

956

noticeable currency fluctuations might no longer be viewed as immaterial. Case studiesof the impact of currency fluctuations on those hospitality firms investing andoperating internationally could reveal the cost and benefit of managing currency risk.Another possible issue for future research into hedging is commodities. There appearto be no studies that explore how restaurant firms purchase futures on commodities toprotect themselves against fluctuation in food and beverage costs.

3.1.4 Interest rate risk exposure. Interest rate risk represents the most significantsource of market risk for many lodging firms (Singh, 2009b; Singh and Upneja, 2008).Two main sources of this risk are debt obligations and financial investments. Mostinterest rate exposure comes from floating-rate bank loans because changes in ratescan increase the volatility of cash flow and earnings in an uncertain interest rateenvironment. Many hospitality firms use a mix of short-term floating and long-termfixed debt to mitigate their risk exposure (Singh, 2009a) and to achieve an optimal debtratio in aligning the supply of internal funds from operations and borrowings to matchdemand for investment funds (Singh, 2009b; Singh and Upneja, 2008). Studyinglodging firms’ use of derivatives in managing interest rate risk exposure, Singh (2009a)showed that firm size, floating-rate debt, interest coverage ratio, book-to-market ratio,and foreign sales ratio are important determinants of interest rate exposure. Asignificant and negative relation between the use of derivatives and interest rateexposure implies a reduction in risk as the magnitude of derivative use increases.Interest rate exposure, along with yield spread and debt rating, is a significantdeterminant of a firm’s interest rate derivative positions (Singh, 2009b).

Market-to-book ratio significantly affects the amount that lodging firms hedge(Singh and Upneja, 2007). Underinvestment costs, financial distress costs, managerialrisk aversion, information asymmetry, cash-flow volatility, proportion of floating-ratedebt, foreign sales ratio, and firm size are all significant determinants of hedgingdecisions (Singh and Upneja, 2008). Larger firms are more likely to hedge, given theeconomies of scale available to a business with high cash-flow volatility.

Research on risk and return research can be expected to develop further, asinvestors weigh costs and benefits in response to an ever-changing businessenvironment. The increasing complication of the agency framework (including lender,manager, and owner) further challenges traditional thinking about the positiverelationship between risk and return. As well as including financial variables whenmeasuring this relationship, future studies could include nonfinancial variables andconsider the interplay of the parties in the agency framework, along withenvironmental risk factors. While the prevailing interest rate has been set athistorical low because of the most recent global financial crisis, it would be interestingto observe how hospitality firms react to or hedge against foreseeable interest ratehikes in the years to come.

3.2 Mergers and acquisitionsThere has been a long history of mergers and acquisitions (M&A) activities in thehospitality industry (Andrew et al., 2007). The goal of M&A is to improve overallperformance and contribute to the realization of shareholder value maximization (Hsuand Jang, 2007). As pointed out by Canina (2009) and Yang et al. (2009), the majorbenefits to owners, shareholders, and institutional investors are economies of scale andsynergy, resulting in reduction of expenses and the cost of capital. However, such

Hospitalityfinancial

management

957

expectations are less often realized due to issues with corporate culture or leadershipconflict. Canina (2009) showed that over two-thirds of M&A deals fail to createshareholder value, with failure usually occurring when firms attempt to combineoperations. There is growing recognition that all expected value creation, if any, takesplace after acquisition rather than at the initial stages (Canina, 2009). Yang et al.’sempirical review of 19 hospitality M&As showed that acquirers received positiveabnormal returns 12 months post-merger.

In their study of 15 acquiring firms using market measures and 23 firms usingaccounting measures, Hsu and Jang (2007) found no evidence that M&A benefited firmperformance measured by short- or long-term stock returns and profitability.Furthermore, performance deteriorated after merger. Not only did equity value declinein the long term, but also there were additional reductions in long-term profitability.Furthermore, no significant relationship was identified between merger announcementsand change in short-term equity value. Mergers also failed to generate better ROA orROE for the acquiring firms. However, the findings of Yang et al. (2009), using industryindices over the period 1996-2007, indicate significant long-term positive gain foracquiring firms. Although 75 percent of hospitality acquisitions are cash financed (Oaket al., 2008), Yang et al. (2009) showed that stock offers are preferable to acquirers’ equityvalue overall. Oak et al. (2008) further showed that acquiring firms with a higher debtratio are more likely to use cash than stock payments.

Hospitality firms with a lower price-to-book ratio, higher growth resourceimbalance, higher capital expenditure ratio, and larger size are found to be a morelikely target for M&A (Kim and Arbel, 1998). Because M&A has been one of the fastestways that firms expanded in the last decade, involving significant capital and leavingvirtually no room for failure, more empirical studies of the hospitality industry couldexplore why so many firms continue to pursue the M&A strategy despitedisappointing results as noted in Canina (2009) and Hsu and Jang (2007). SomeM&A activities in the casino industry (e.g. MGM Mirage’s acquisition of MandalayResort Group in 2005) could be a good case study for understanding this phenomenon.

Additionally, the topic of hostile takeover could be investigated. It would beinteresting to investigate the tactics (e.g. greenmail and poison pills) that could beemployed by management to avoid hostile takeovers (Andrew et al., 2007).

3.3 Hospitality stock investmentInvestors in hotel stocks care not only about risks and returns but also thedeterminants of volatility. From a macroeconomic perspective, money supply andunemployment rate have been shown to significantly explain the movement of hotelstock returns (Chen et al., 2005; Chen and Kim, 2006; Chen, 2007). Changes inunemployment rate reflect the strength of the economy and significantly correlate withhotel stock returns in restrictive monetary periods in Taiwan (Chen, 2007). An increasein unemployment symbolizes a sluggish economy and is accompanied by a decrease instock returns. The increase in money growth results in a wealth effect, which in turntends to stimulate consumption and production and increase investment. Furthermore,hotel stocks exhibit higher mean return and reward-to-risk ratio during expansivemonetary periods. Chen et al. (2005) indicated that non-macroeconomic variables suchas political events, natural disasters, and international sports events have a moresignificant impact on hotel stock returns than macroeconomic factors. For instance, a

IJCHM23,7

958

study of Taiwanese hotel stock performance after the SARS outbreak by Chen et al.(2007) showed that the industry experienced the most serious damage in terms of stockprice decline (approximately 29 percent) in the immediately following month amongmany industries on the Taiwan Stock Exchange. This was considered an irrationalmarket response because decreasing occupancy and average daily rate causedpanicking hotel investors to perceive an abnormally higher risk and sell off shares thatwere considered overvalued.

Kim et al. (2002b) argued that hotel REITs are no more attractive than other REITsectors because oversupply and low occupancy rates since 1997 have greatly hurt theirstock returns and increased volatility. They advised that hotel REITs must be verycautious about the financial risk associated with debt leverage and the negative impactof new equity issues. High debt leverage could greatly increase investment riskbecause of uncertainty about a hotel REIT firm, particularly if firm-specific eventsoccur, such as contract loss and earnings alerts, that may cause a drastic decline instock (Gu and Kim, 2003).

Earnings per share (EPS) has been shown to serve as a good proxy for thefundamental value of stock prices in the hospitality sector (Chen et al., 2009).Hospitality stock prices driven by EPS exist because the industry is involved in lessnoise trading and is smaller compared to other industries in terms of marketcapitalization. The authors argued that hospitality stock investors should pay moreattention to underlying performance in terms of EPS. They also demonstrated along-term relationship between stock prices and EPS, and that EPS significantlypredicts changes in stock returns for the hospitality industry. Similarly, Upneja et al.(2008) demonstrated a significant and positive relationship between earningsmanipulation indicators and stock price increases for restaurant firms.

Repricing stock options can also send certain messages to investors. Denizci (2007)showed that hospitality companies are more likely to reprice stock options after a stockprice decrease accompanied by a market-wide fall, compared to a control sample ofcompanies matched by size and price decrease. She found that repricing firms aresignificantly smaller (in terms of market capitalization) and have lower stock pricereturns and dividends per share.

Hospitality stock investment is rather complicated, because the volatility ofinvestment values can be attributed to many factors using either technical orfundamental analysis. While advanced mathematical models (e.g. Chen et al., 2007;Chen et al., 2009) have been introduced and tested with empirical data to offer investorssome guidance, it should be noted that stock price movements reflect investors’predictions and speculations for a firm’s future. That is, individual judgment, whetherrational or not, plays an important role in investment decisions. For example, Tsai andGu (2007c) argued that the interplay between stock market investment and casinogaming activities is a result of wealth and substitution effects. Future studies couldalso study hospitality stock investment qualitatively to explore the relevant factors.

4. Hospitality dividend policyFirms reward investors through cash or stock dividends or stock price appreciation.Using logistic regression analysis to examine the financial features of firms that didand did not pay dividends, Kim and Gu (2009) showed that firm size (measured by totalassets) and profitability (measured by ROA) are significant drivers of dividend payout

Hospitalityfinancial

management

959

decisions for US firms, while investment opportunities deter them from paying. Theseresults are consistent with those of Borde et al. (1999) and Dalbor and Upneja (2007) interms of the effect of firm size on dividend payout decisions and those of Canina et al.(2001) on investment opportunities and profitability (i.e. earnings). In other words,larger firms with higher profitability but fewer investment opportunities are morelikely to pay dividends. Smaller and less profitable firms with more investmentopportunities are less likely to pay dividends because they need to retain earnings topursue growth. Canina et al. (2001) argued that the average dividend payout forlodging firms is less than for other firms in the market due to higher investmentrequirements, highly volatile income, and/or high interest payments.

Similar to Canina et al. (2001), Dalbor and Upneja (2007) found a negativerelationship between total debt and dividend payout in the US restaurant industry anda positive relationship between firm size (measured by number of shareholders) anddividend payout. They argued that the latter could be a substitute for interestpayments and serve as a mechanism to constrain management within the agencyframework. Dividend initiations and increases imply an appreciation in firm value, sothe market reacts positively. Equally, the market reacts negatively to announcementsof dividend decreases (Borde et al., 1999; Canina et al., 2001). Borde et al. (1999)cautioned that changes in dividend policy could affect the availability of capital to fundgrowth. While investors perceive higher payouts positively, firms might need to seekfunding in the capital market if unforeseen opportunities emerge. Comparing lodgingcorporations and REITs in terms of the impact of dividend policy on institutionalshareholdings, Oak and Dalbor (2008b) found that institutional investors tend to preferREITs, most likely due to REITs’ committing a fixed percentage of earnings paid outas dividend.

Hospitality firms’ dividend policies have been far less studied than their financingand investment. How firms utilize operational earnings sends different messages totheir investors. While paying out more dividends would please stockholders, it couldalso indicate that the firm has few or no value-creating opportunities ahead, signalinglow growth. However, cutting or reducing dividends could displease investors even if itmeans growth opportunities are ahead. Dividend policy changes could be aninteresting topic for research, as could capital reduction, which triggers dividendpayments, stock price appreciation, and increases in other performance measures suchas ROE. An example of this occurred during Formosa International Hotels Corporationof Taipei’s capital reductions in 2002 and 2006 (Taipei Times, 2009).

5. Financial conditions and performance5.1 BankruptcyGiven the sector’s capital-intensive nature, sensitivity to the economy, and seasonality,firms are under significant pressure to generate enough operating cash flow to meetshort- and long-term debt obligations, including both interest and principal payments.Firms that fail to do so face various consequences including bankruptcy, andinsolvency has become a popular research topic.

The probability of bankruptcy is positively correlated with long-term debt in boththe restaurant (Dalbor and Upneja, 2002) and lodging (Upneja and Dalbor, 2001b;Dalbor and Upneja, 2004) industries. More leveraged firms are more vulnerable tofailure, especially when there is a financial shock. Jang et al. (2008) confirmed that

IJCHM23,7

960

lower leverage and higher cash levels can reduce the risk of insolvency. However,Upneja and Dalbor (2001a) showed that restaurant firms with more short- thanlong-term debt are more likely to go bankrupt, most likely due to a greater problemwith information asymmetry. Using a multiple-discriminant analysis model, Gu (2002)showed that restaurant firms with lower earnings before interest and taxes and highertotal liabilities (i.e. debt-burdened) are candidates for bankruptcy. This argument wassupported by Kim and Gu (2006a, 2006b) and Youn and Gu (2009). Kim and Gu (2006b)argued that what matters in restaurant bankruptcy is long-term debt; the more a firmrelies on debt financing, the higher its interest expenses, the lower the interest coverageratio, and the higher the probability of failure. Comparing Gu’s (2002)multiple-discriminant analysis model of restaurant bankruptcy, Kim and Gu (2006b)claimed that the logistic model is preferred because of its theoretical soundness,although both models give similar results. Comparing a logistic regression modelpredicting the failures of Korean lodging firms, Youn and Gu (2009) showed that theartificial neural network model outperforms the logistic model in terms of reducedType II errors. They stated that interest coverage is the most important signal ofbusiness failure in the Korean hotel industry.

Kim and Gu (2006a) argued that nonfinancial factors such as geographicdiversification and market segmentation may also help predict bankruptcy becausethey are likely to influence the firm’s financial variables and, ultimately, performance.Diener (2009) explained the regulatory changes in the bankruptcy code since the lastwave of hotel bankruptcies and suggested that the precipitous and concurrent drop inreal estate values and revenues has again raised the specter of insolvency for ownersand lenders. He argued that many other issues, such as utilities, critical vendors, andtaxes could influence this, as could owner-debt relations or favorable economic factors.While some financial variables clearly signal firm failures and have been wellexamined in previous studies, there is need for further investigation of non-financialissues related to hospitality firm bankruptcy, such as those that have been conductedin mainstream business (Wu, 2004).

5.2 Firm performance determinantsFirm performance has been a popular research variable. Depending on the context, itcan be measured from the accounting (such as ROA) and finance (stock returns)perspectives, or a combination of both (such as Tobin’s q). Hospitality researchers havebeen interested in what financial attributes lead to better performance. For example,institutional shareholding and firm size are significant and positive determinants offirm performance (as measured by a proxy for Tobin’s q) in both the restaurant andcasino industries, while debt has a positive performance impact on the latter only (Tsaiand Gu, 2007a; Tsai and Gu, 2007b). Mao and Gu (2008) indicated that financialleverage and activity are significant determinants of performance (as measured by aproxy for Tobin’s q) of US restaurants. They concluded that larger firms, with higherliquidity, asset turnover, profitability, and faster growth, tend to have higher values.Financial leverage has a significant but negative effect on restaurant firm performance,implying that heavy indebtedness tends to reduce firm value in the capital market.

From the accounting perspective, Jung (2008) proposed the application of the DuPont ratio for operators to identify the true value drivers and simultaneously the use ofthe WACC as the benchmark for performance. Canina and Carvell (2008) argued that

Hospitalityfinancial

management

961

static measures of liquidity, such as current and quick ratios, might be less useful inassessing a firm’s ability to cover current obligations. For unlisted companies, wherethere is no market price data available, ROE is still the best and most reliable tool todetermine financial performance (Madan, 2007). Youn and Gu (2007) showed thatKorean lodging firms’ operating costs are too high and operating profit margins toolow, negatively affecting ROA.

Researchers have recently started examining the potential determinants of firmperformance using non-financial factors (Mao and Gu, 2008). From a human resourcesmanagement perspective, for example, Chi and Gursoy (2009) suggested that greateremployee satisfaction could indirectly improve financial performance, as mediated bycustomer satisfaction. They claimed that the higher the customer satisfaction, thebetter the firm performance, indicating a key internal performance-enhancing successfactor for any service company. Corporate social responsibility (CSR) activities show apositive and simultaneous relationship with firm value and profitability for hotelcompanies (McGehee et al., 2009; Kang et al., 2009; Koh et al., 2009b), but not casinos(Lee and Park, 2009). However, the findings of Park and Lee’s (2009) study of therestaurant industry contradict this, indicating that CSR has a U-shaped effect onlong-term accounting performance, but no impact on firm performance. There are othervarious nonfinancial factors, such as internationalization (Lee, 2008b; Hua and Upneja,2007) and franchising (Koh et al., 2009a; Ketchen et al., 2006), that could be linkeddirectly or indirectly to performance and could be examined alongside financial issues.

5.3 Chief executive officer compensation and turnoverPerformance-related pay (PRP) has been another research area because it relates to theagency theory in terms of aligning the interests of owners and managers. Gu and Choi(2004) showed that chief executive officer (CEO) cash compensation in casino firms ispositively correlated with profitability (measured by ROA), firm size (total assets), debtleverage, and stock options but negatively associated with revenue efficiency, asmeasured by asset turnover. While the first of these correlations is consistent with thePRP principle, an insignificant relationship between stock performance and CEOcompensation was observed, which indicates otherwise. Nevertheless, an insignificantpositive association between stock options and stock performance suggests that theformer could drive the latter. In examining CEO cash compensation determinants inthe US restaurant industry, Kim and Gu (2005) showed that of 12 potential variables,only firm size (measured by the log of total assets) and operating efficiency (measuredby asset turnover ratio), are significant determinants. Firm size serves as a controlvariable rather than a performance indicator. PRP is not in evidence with respect toprofits and stock performance; however, CEOs are better rewarded in terms of revenuegeneration efficiency.

Barber et al. (2006) examined the relationship between CEO compensation(including salary, bonuses, restricted stock values, value of options, and other sources)and financial performance for the restaurant industry. Their results contrast with thoseof Kim and Gu (2005) because they found a positive but weak correlation between CEOcompensation, gross revenue, net income, and stock price. The authors claimed thatstock price is a significantly stronger predictor of CEO compensation. Madanoglu andKaradag (2008) assessed the relationship between changes in CEO compensation fromperiod to period rather than from firm to firm. They measured CEO PRP sensitivity

IJCHM23,7

962