final report of the regional energy demand planning project

TRANSCRIPT

FINAL REPORT OF THE REGIONAL ENERGY DEMAND PLANNING PROJECT

FUTURE ENERGY SCENARIOS IN SOUTHEAST EUROPE AND THE POTENTIAL FOR ENERGY EFFICIENCY

June 2008 This publication was produced for review by the United States Agency for International Development. It was prepared by International Resources Group.

FINAL REPORT OF THE REGIONAL ENERGY DEMAND PLANNING PROJECT FUTURE ENERGY SCENARIOS IN SOUTHEAST EUROPE AND THE POTENTIAL FOR ENERGY EFFICIENCY USAID Contract No. EPP-I-00-03-00006-00 Task Order No. 1

International Resources Group 1211 Connecticut Avenue, NW, Suite 700 Washington, DC 20036 202-289-0100 Fax 202-289-7601 www.irgltd.com

DISCLAIMER The author’s views expressed in this publication do not necessarily reflect the views of the United States Agency for International Development or the United States Government.

SOUTH EAST EUROPE REGIONAL ENERGY MARKET SUPPORT (SEE REMS) PROJECT i

CONTENTS

Executive Summary .......................................................................................................... 1 Context ................................................................................................................................................................. 1 Accomplishments ................................................................................................................................................ 1 Analytical Results ................................................................................................................................................ 2 Report Organization .......................................................................................................................................... 4

List of Tables ...................................................................................................................... 5

List of Figures ..................................................................................................................... 7

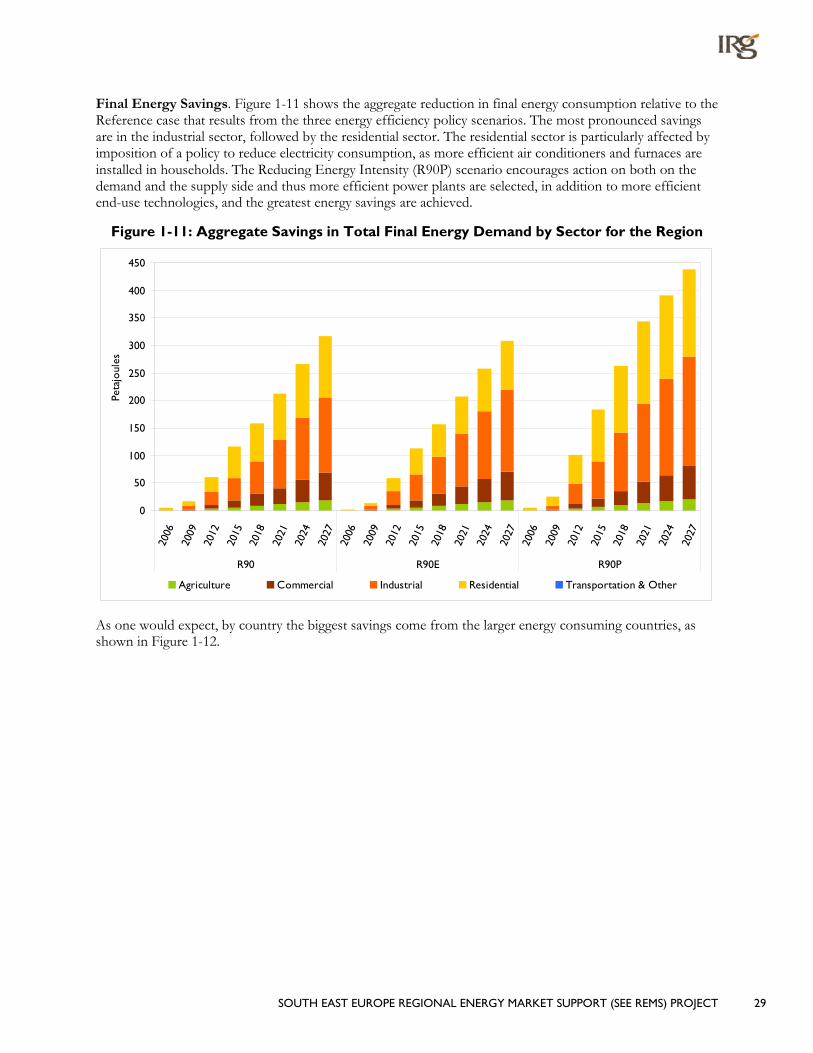

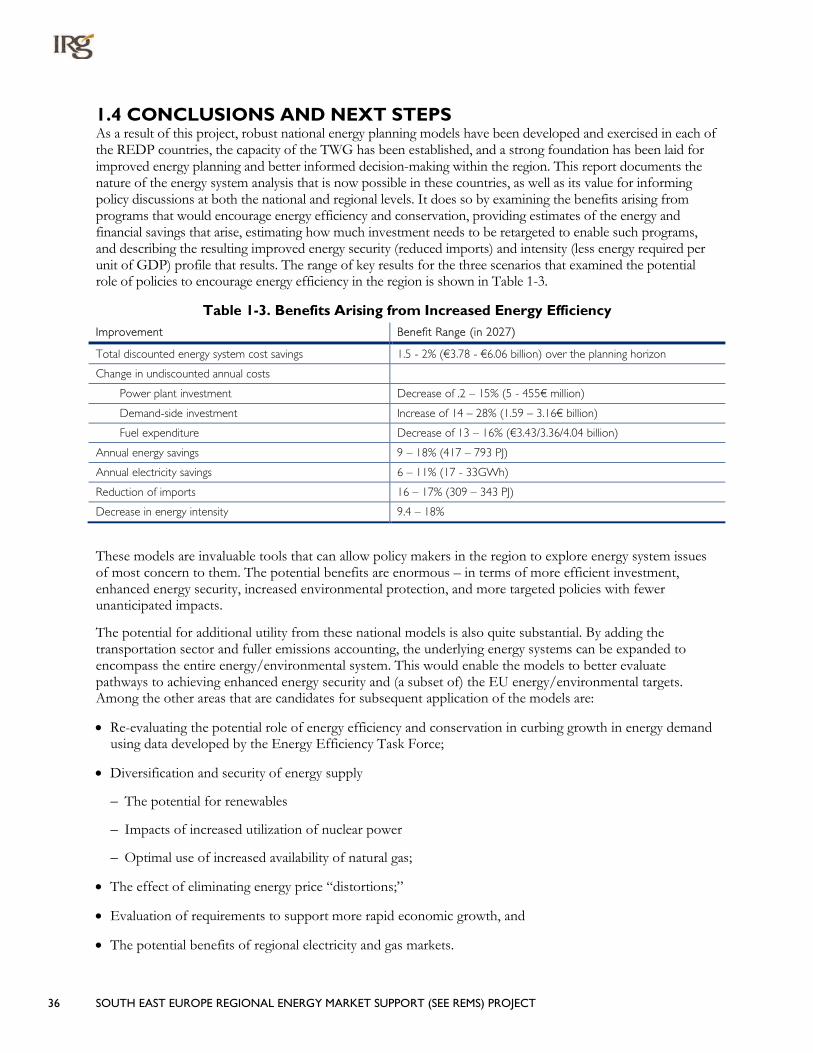

Section 1: Highlights ........................................................................................................ 18 1.1 Project Overview ....................................................................................................................................... 18 1.2 Reference Scenario Highlights ................................................................................................................ 21 1.3 Policy Scenario Highlights ........................................................................................................................ 28 1.4 Conclusions and Next Steps ................................................................................................................... 36

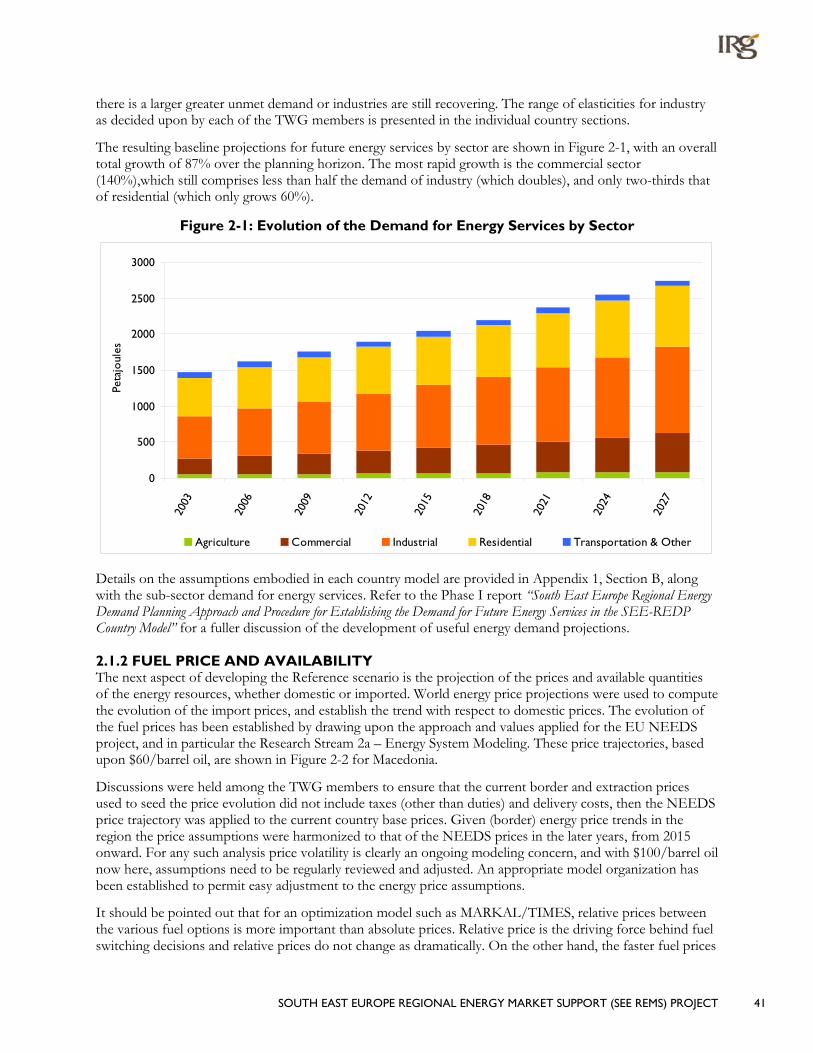

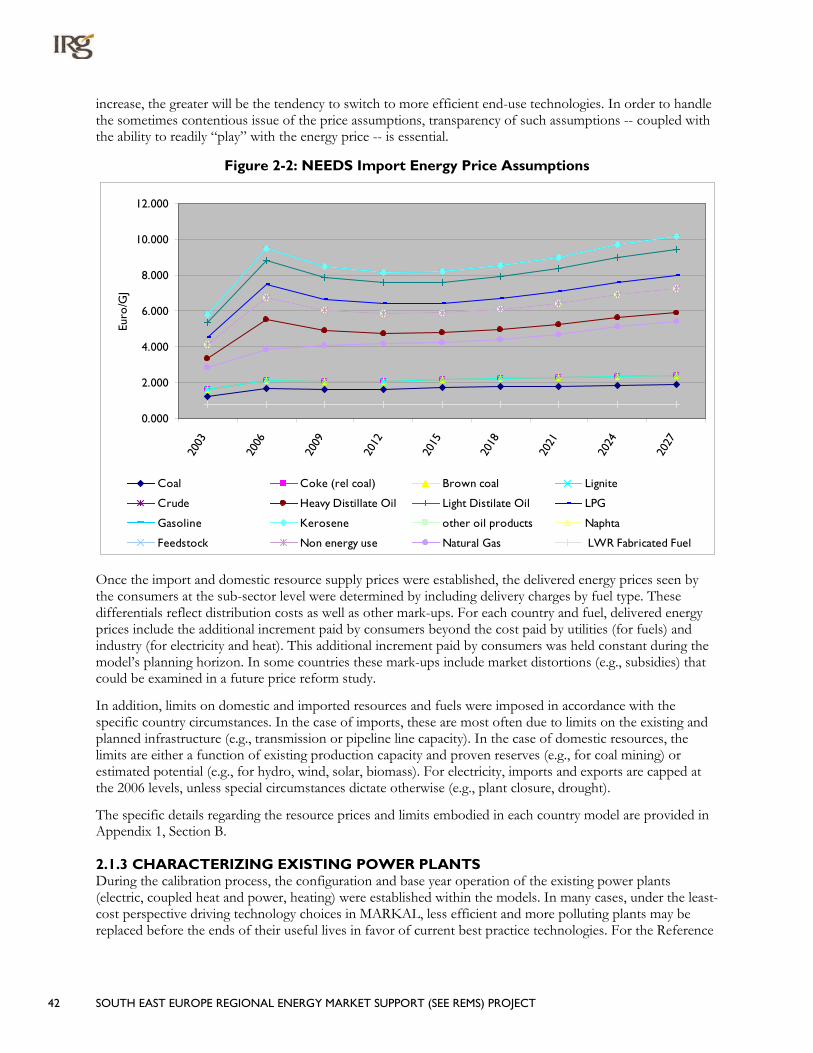

Section 2: Reference Scenario Development and Analysis ......................................... 38 2.1 Reference Scenario Development ......................................................................................................... 38

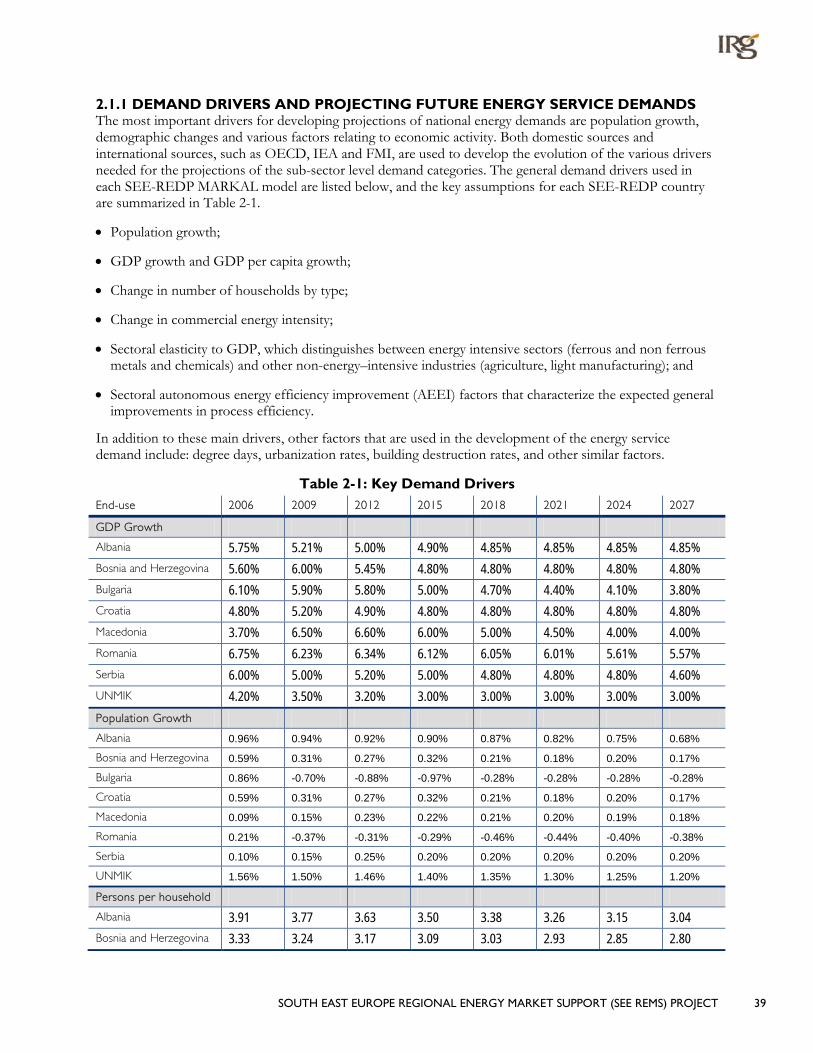

2.1.1 Demand Drivers and Projecting Future Energy Service Demands ..................................... 39 2.1.2 Fuel Price and Availability .............................................................................................................. 41 2.1.3 Characterizing Existing Power Plants ......................................................................................... 42 2.1.4 Fuel Share Evolution ....................................................................................................................... 43 2.1.5 Future Technology Options ......................................................................................................... 43 2.1.6 New Technology Adoption Rates ............................................................................................... 46

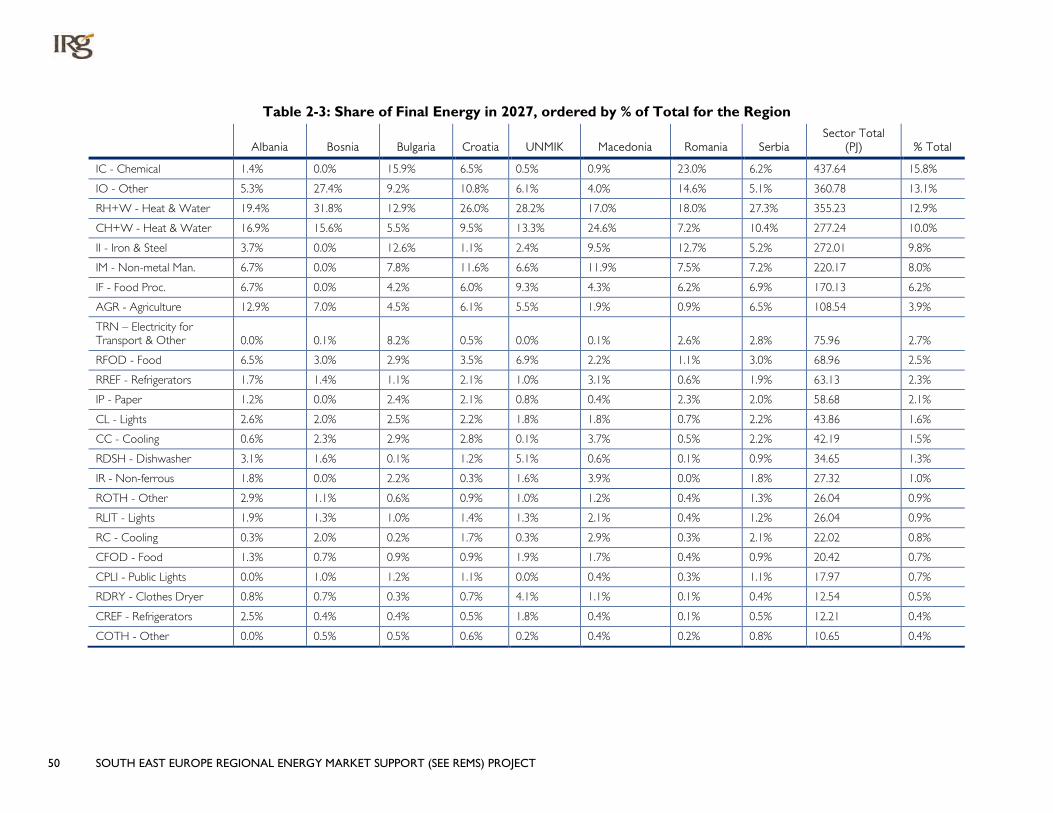

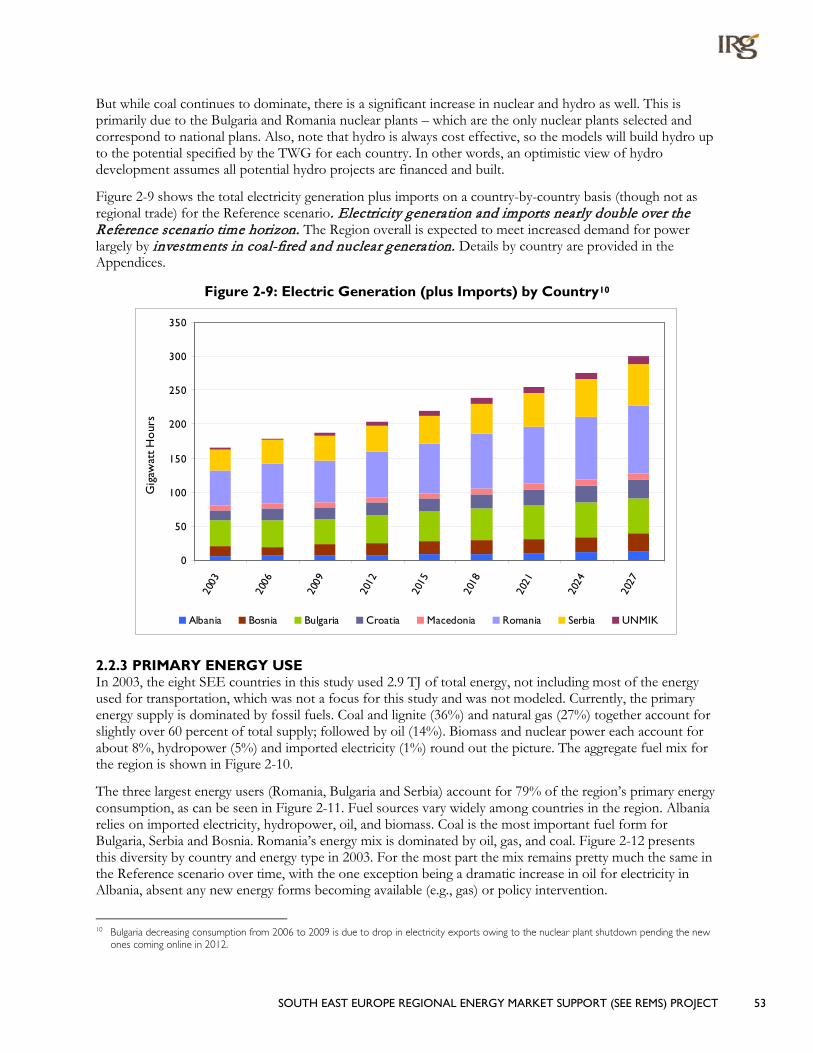

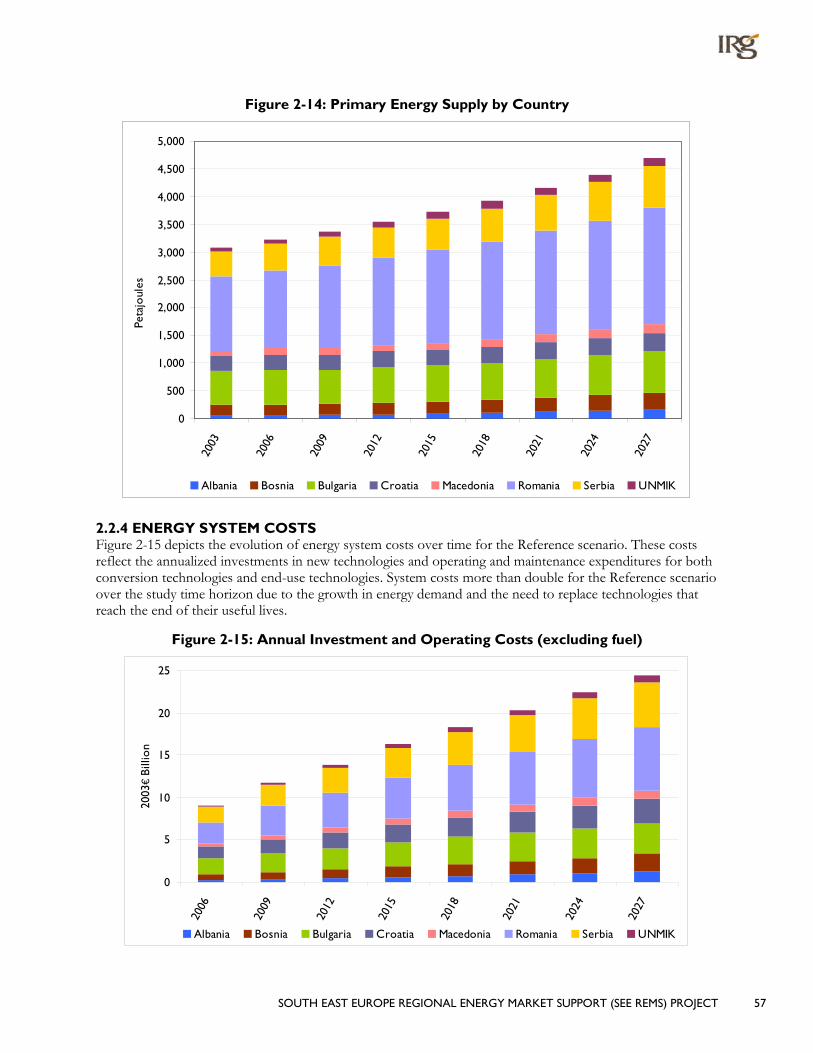

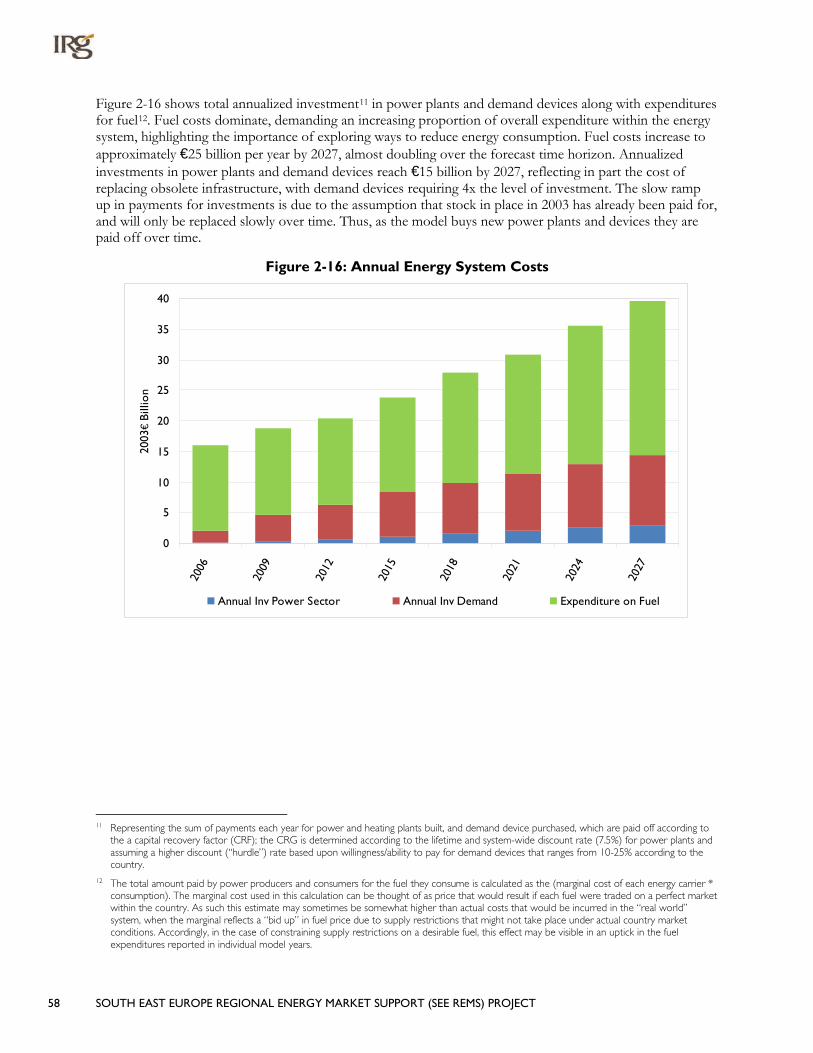

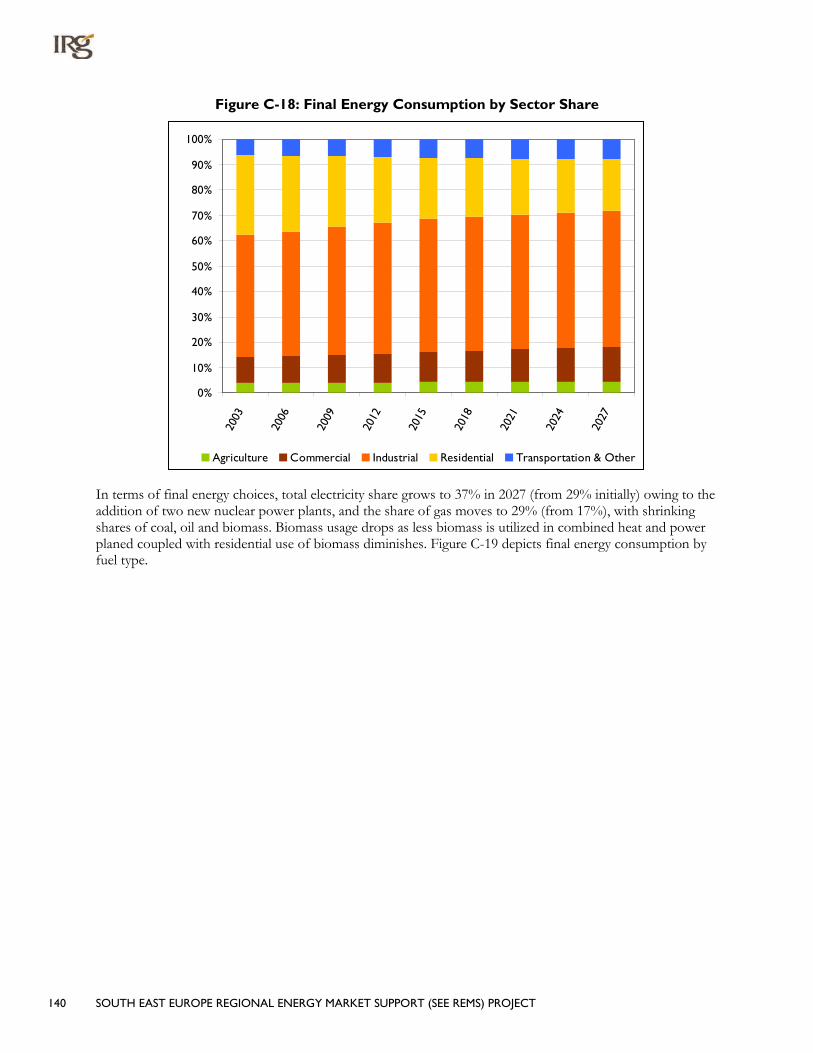

2.2 Reference Scenario Regional Results .................................................................................................... 46 2.2.1 Final Energy Consumption ............................................................................................................ 46 2.2.2 Electricity Generation and Imports ............................................................................................ 52 2.2.3 Primary Energy Use ........................................................................................................................ 53 2.2.4 Energy System Costs ...................................................................................................................... 57

Section 3: Scenario Analysis Regional Results .............................................................. 59 3.1 Scenario Definitions .................................................................................................................................. 59

Appendix 1: Individual Country Results ........................................................................ 72

A. Albania ......................................................................................................................... 73 A.1 Highlights ..................................................................................................................................................... 73

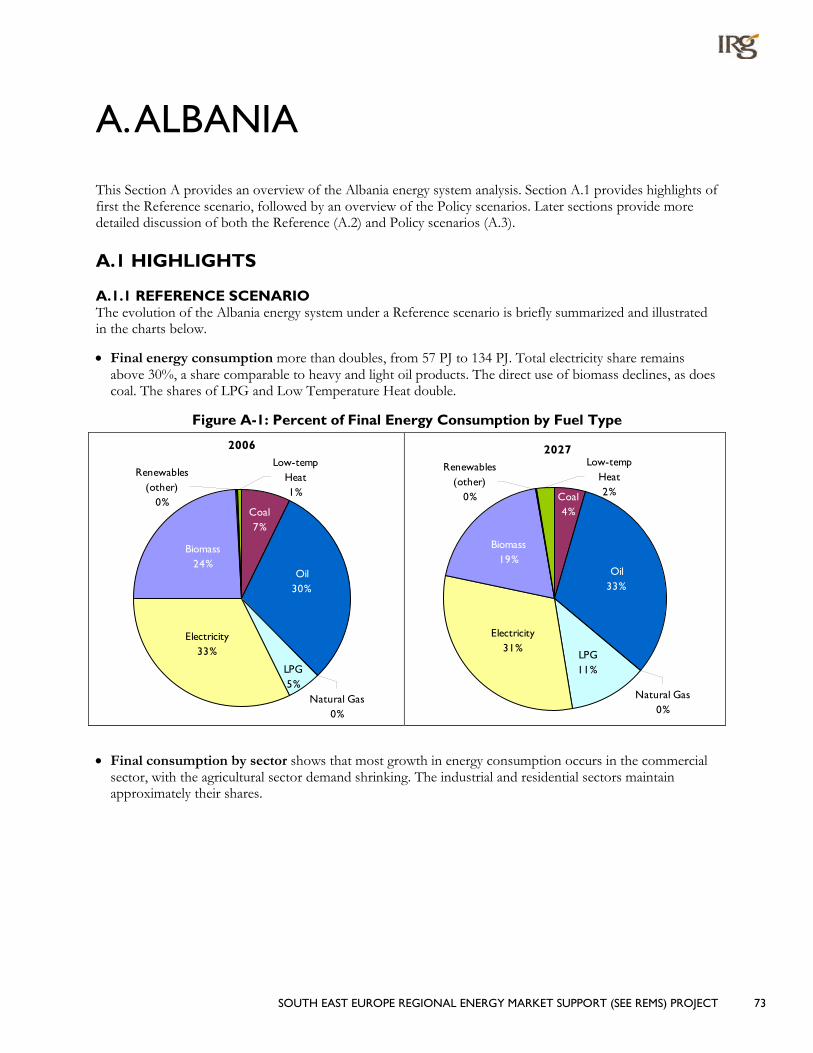

A.1.1 Reference Scenario ........................................................................................................................ 73 A.1.2 Policy Scenarios .............................................................................................................................. 75

ii SOUTH EAST EUROPE REGIONAL ENERGY MARKET SUPPORT (SEE REMS) PROJECT

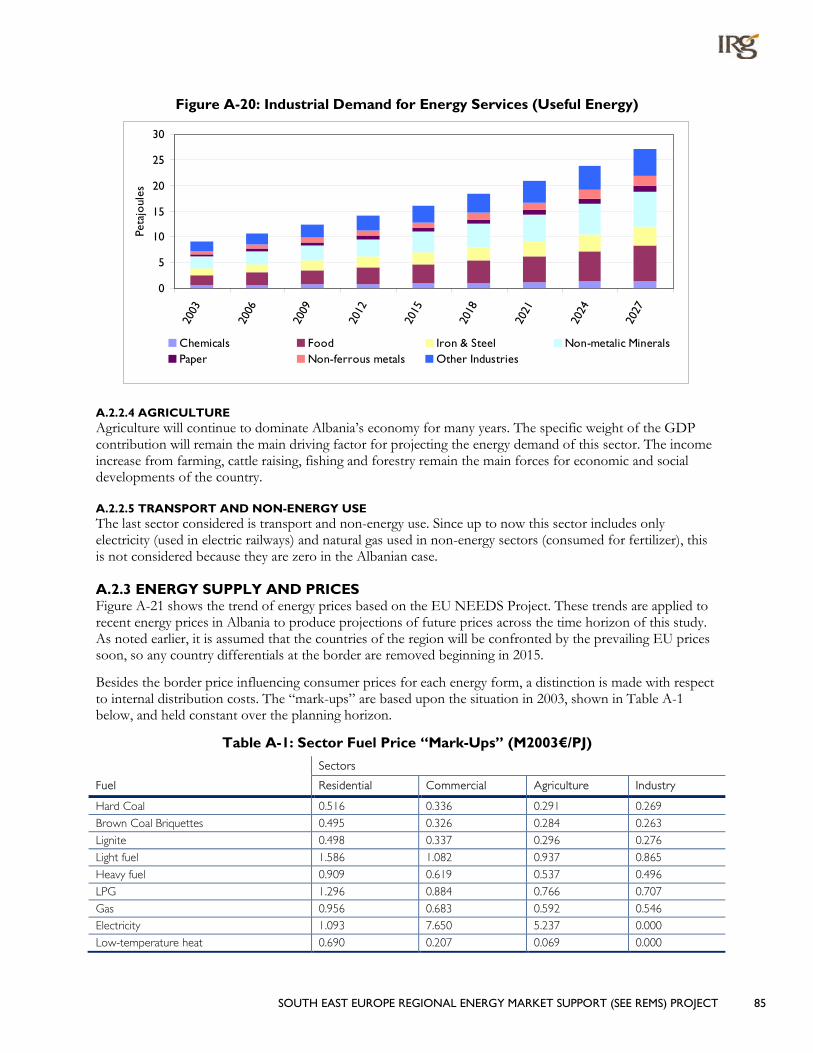

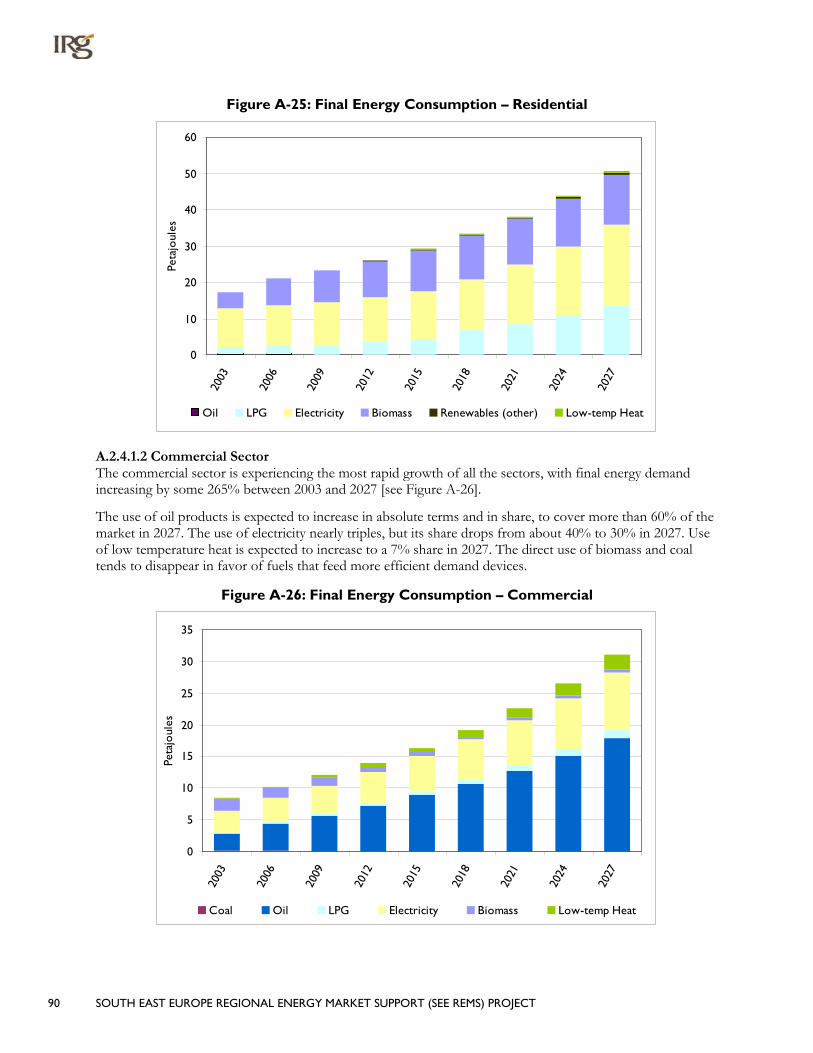

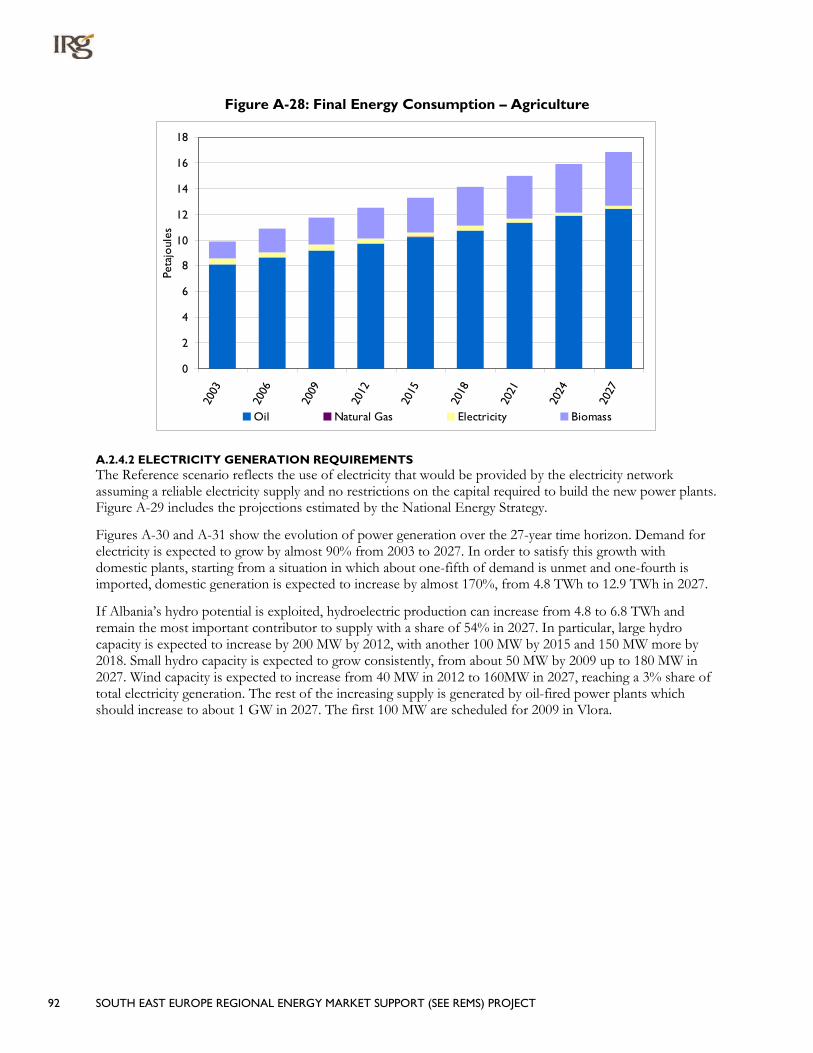

A.2 Energy System Under a Reference Scenario ...................................................................................... 78 A.2.1 Critical Driving Assumptions ....................................................................................................... 78 A.2.2 Energy Service Demand Projections .......................................................................................... 80 A.2.3 Energy Supply and Prices .............................................................................................................. 85 A.2.4 Reference Scenario Outline ......................................................................................................... 87

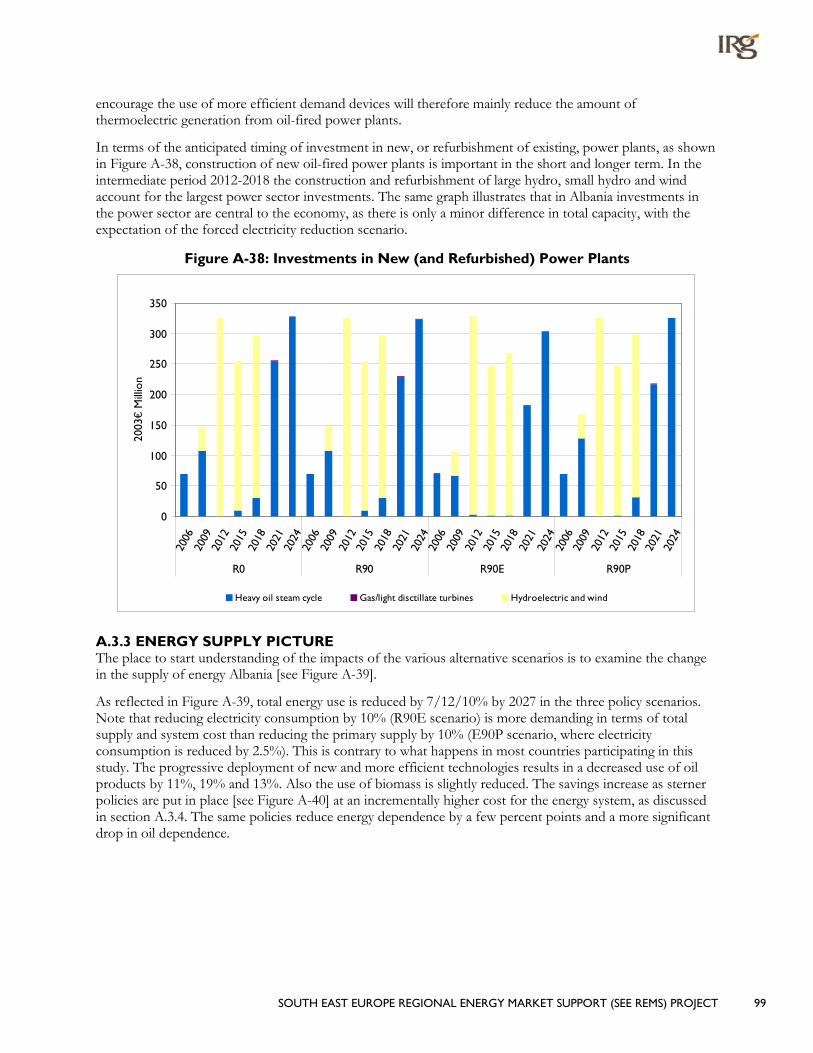

A.3 Scenario Analysis RESULTS .................................................................................................................... 96 A.3.1 Final Energy Consumption Patterns ........................................................................................... 96 A.3.2 Power Sector Investments and Electricity Generation ......................................................... 97 A.3.3 Energy Supply Picture .................................................................................................................... 99 A.3.4 Costs ............................................................................................................................................... 101

B. Bosnia and Herzegovina ........................................................................................... 102 B.1 Highlights ................................................................................................................................................... 102

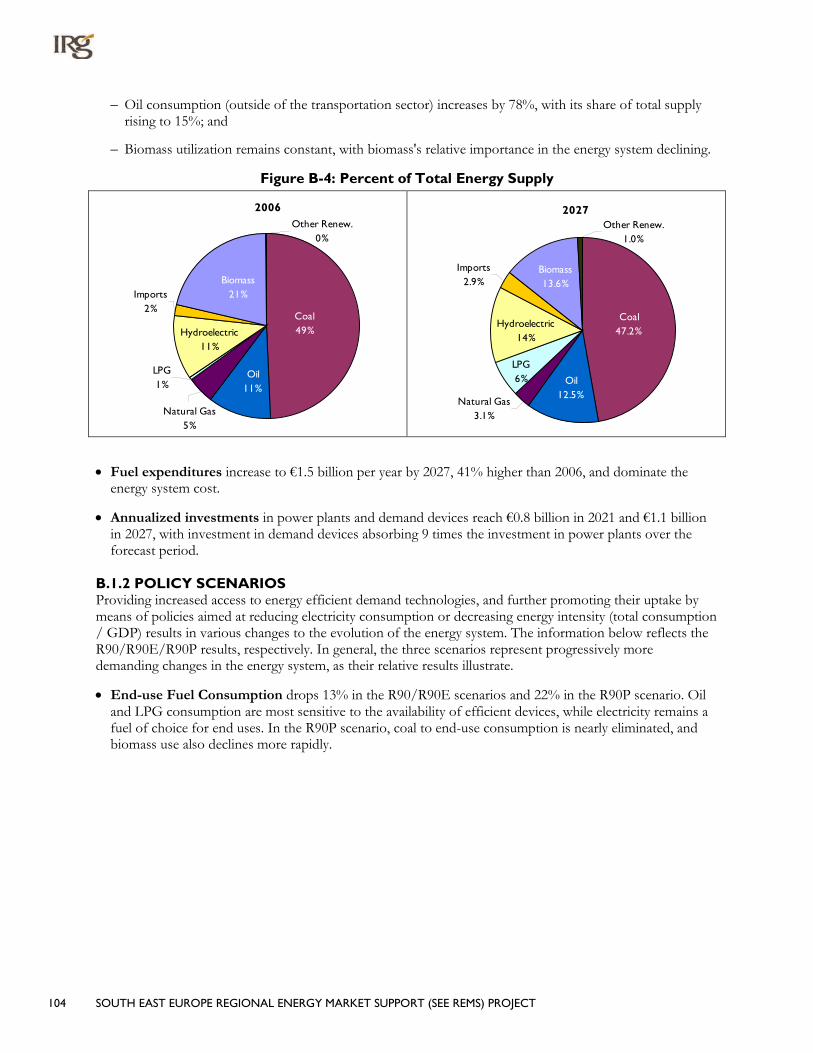

B.1.1 Reference Scenario ....................................................................................................................... 102 B.1.2 Policy Scenarios ............................................................................................................................. 104

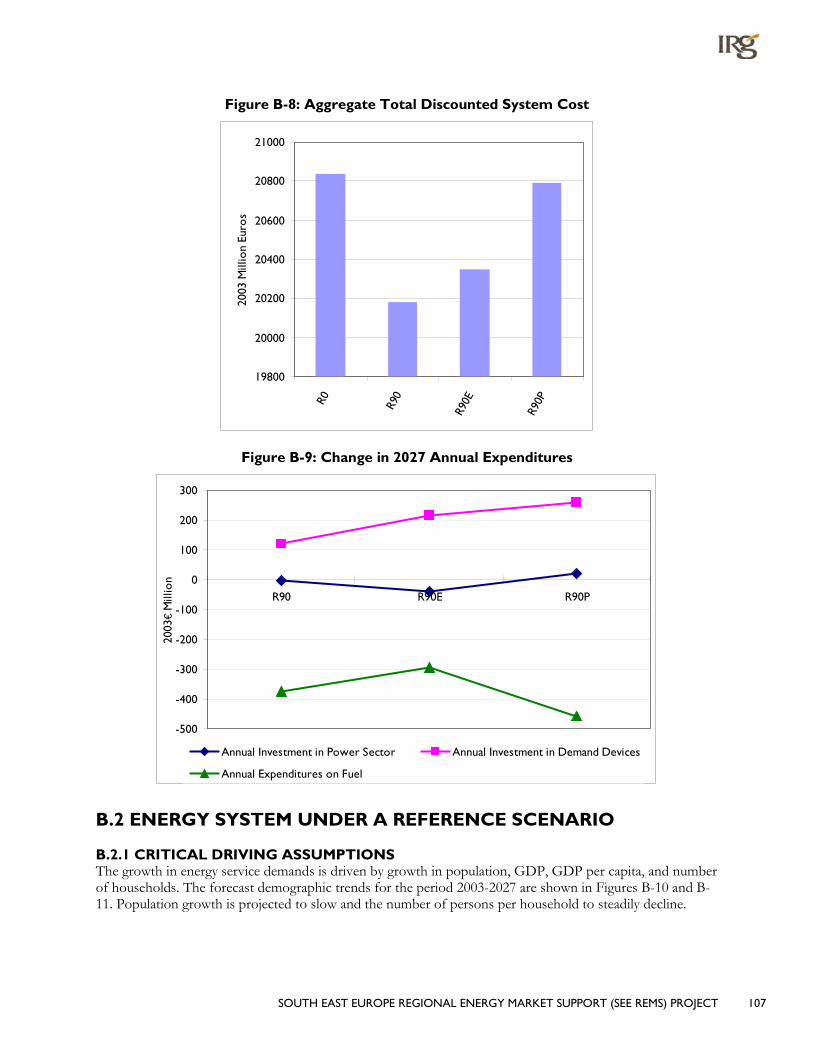

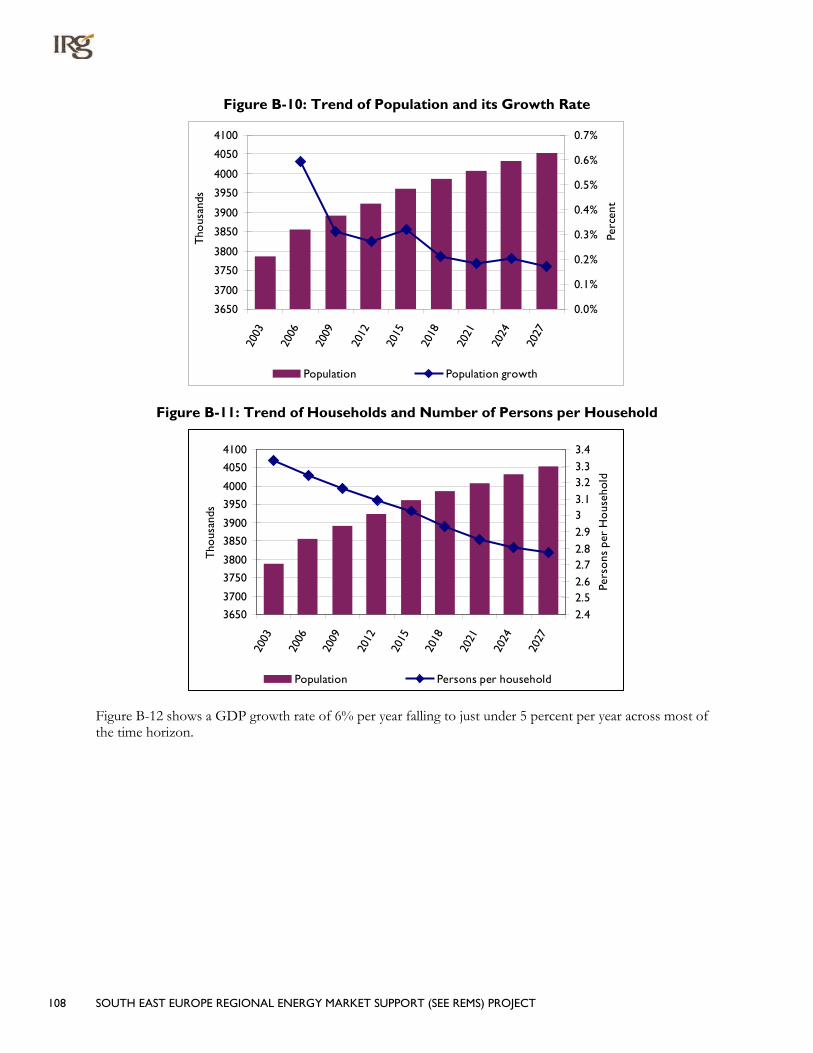

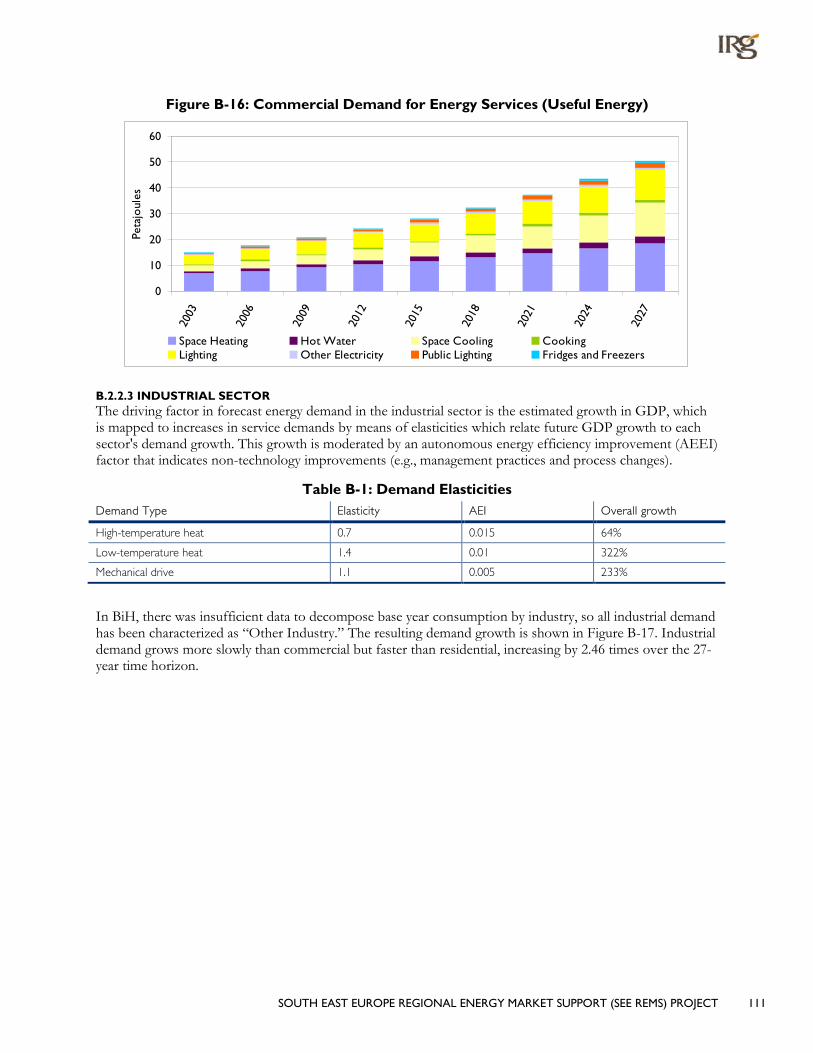

B.2 Energy System Under a Reference Scenario ..................................................................................... 107 B.2.1 Critical Driving Assumptions ..................................................................................................... 107 B.2.2 Energy Service Demand Projections ........................................................................................ 109 B.2.3 Energy Supply and Prices............................................................................................................. 112 B.2.4 Reference Scenario Highlights ................................................................................................... 113

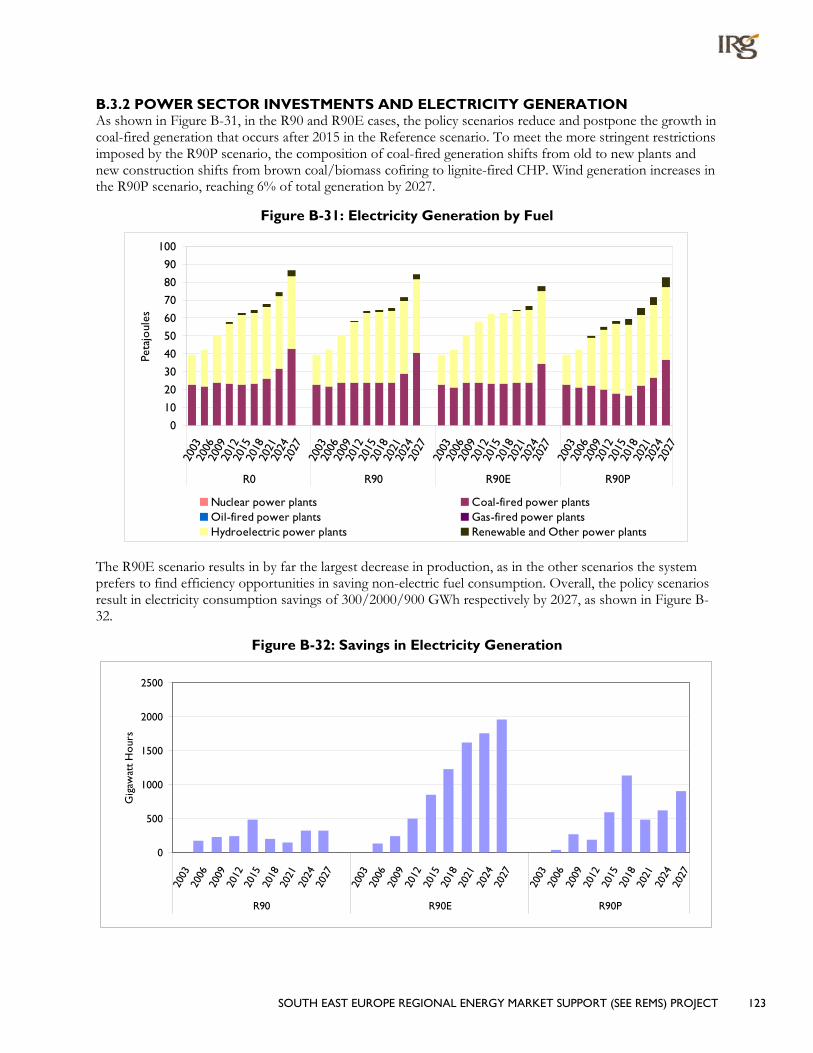

B.3 Scenario Analysis Highlights .................................................................................................................. 121 B.3.1 Final Energy Consumption Patterns ......................................................................................... 122 B.3.2 Power Sector Investments and Electricity Generation ....................................................... 123 B.3.1 Energy Supply Picture .................................................................................................................. 124 B.3.4 Costs ................................................................................................................................................ 126

C. Bulgaria ...................................................................................................................... 128 C.1 Highlights ................................................................................................................................................... 128

C.1.1 Reference Scenario ...................................................................................................................... 128 C.1.2 Policy Scenarios ............................................................................................................................ 130

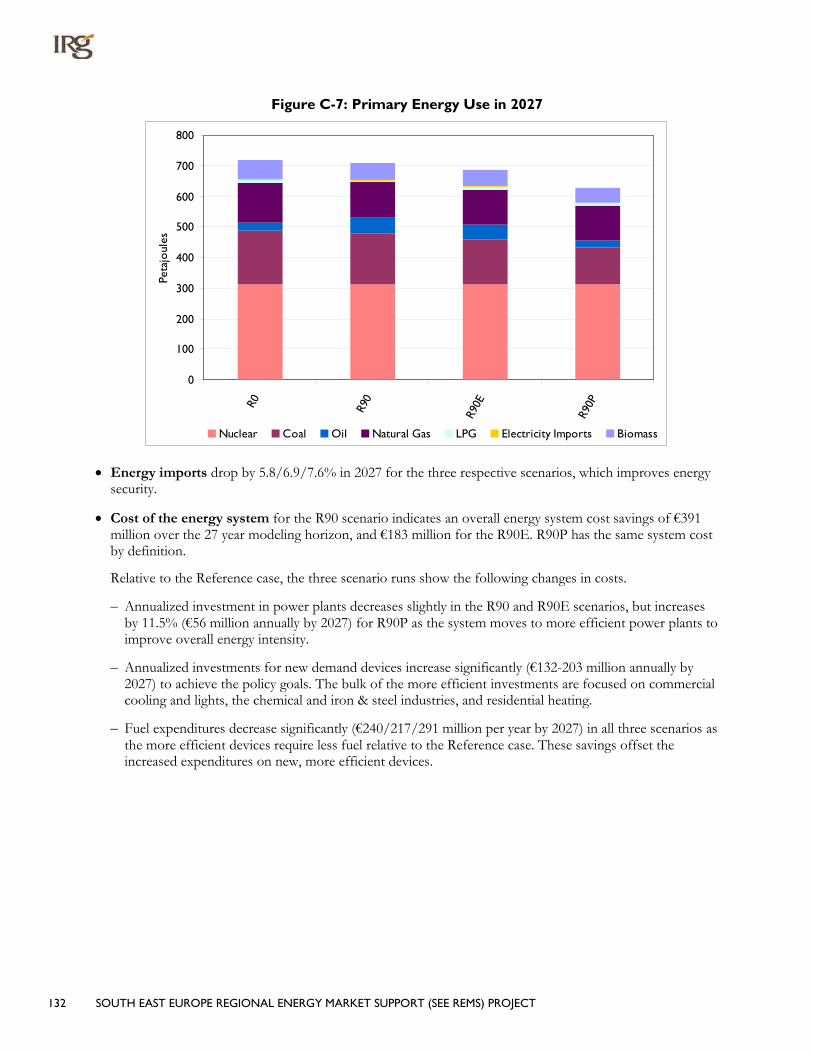

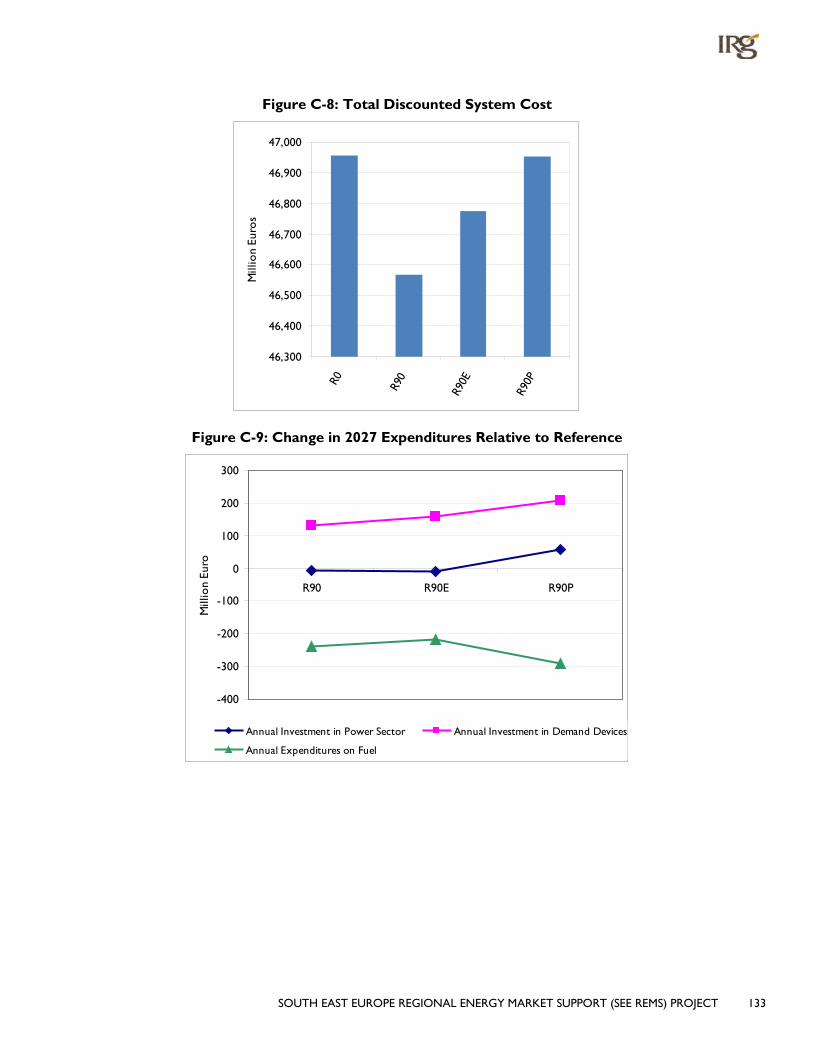

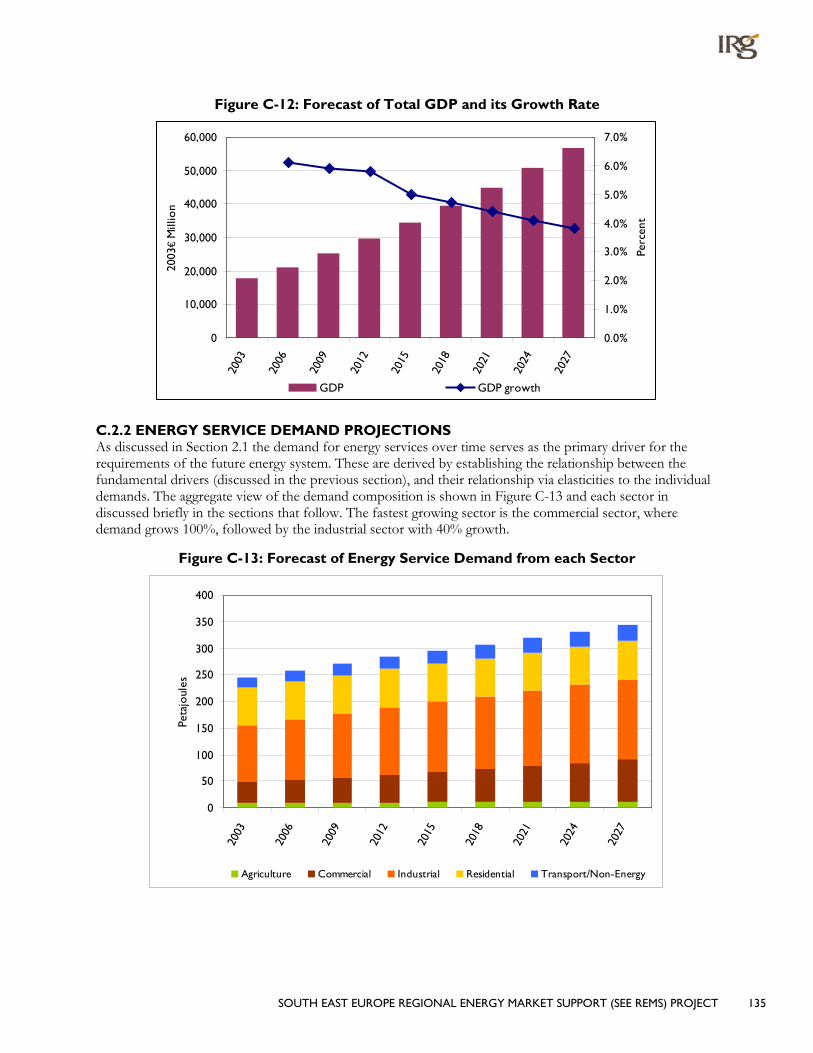

C.2 Energy System Under a Reference Scenario .................................................................................... 134 C.2.1 Critical Driving Assumptions .................................................................................................... 134 C.2.2 Energy Service Demand Projections ....................................................................................... 135 C.2.3 Energy Supply and Prices ............................................................................................................ 138 C.2.4 Reference Scenario Highlights................................................................................................... 139

C.3 Scenario Analysis Highlights ................................................................................................................. 148 C.3.1 Final Energy Consumption Patterns ........................................................................................ 149

SOUTH EAST EUROPE REGIONAL ENERGY MARKET SUPPORT (SEE REMS) PROJECT iii

C.3.2 Power Sector Investments and Electricity Generation ....................................................... 150 C.3.3 Energy Supply Picture .................................................................................................................. 152 C.3.4 Costs ............................................................................................................................................... 154

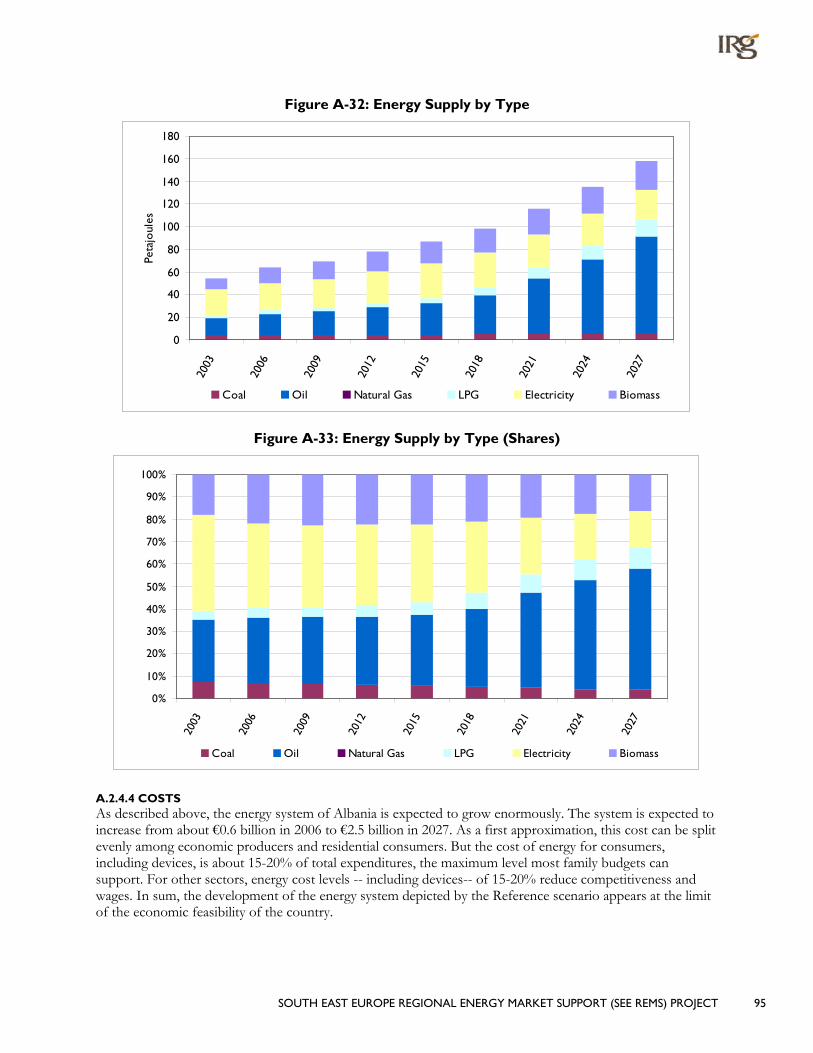

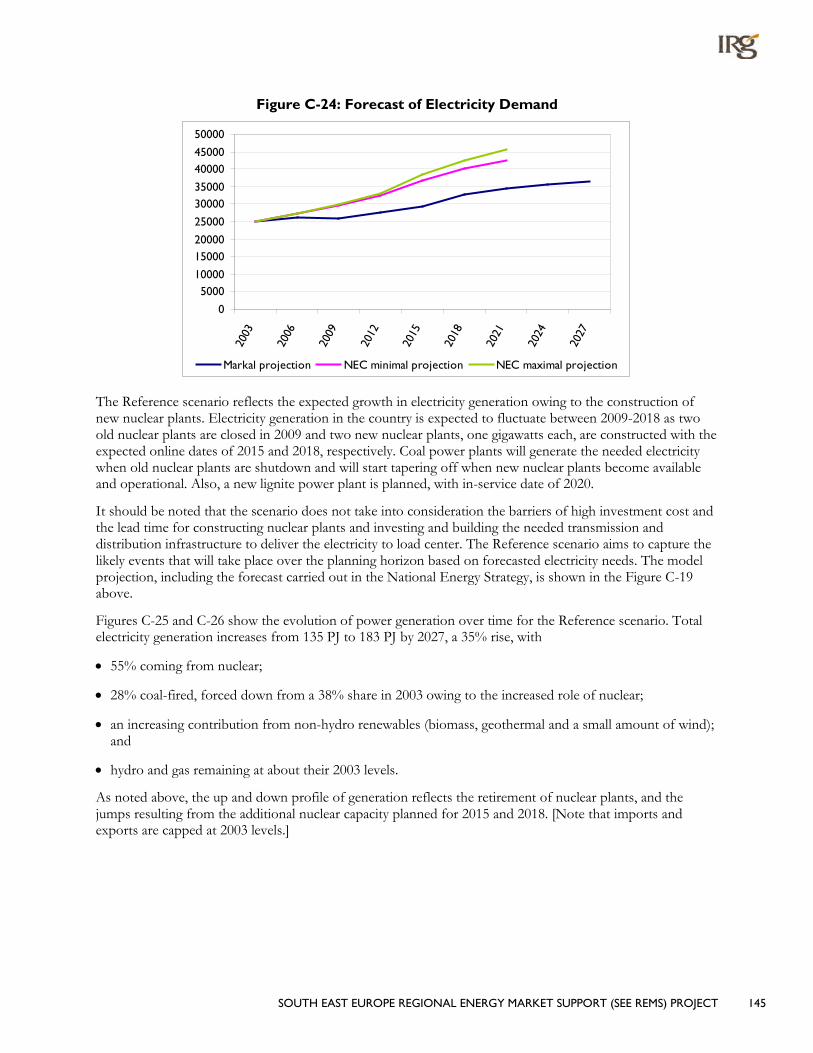

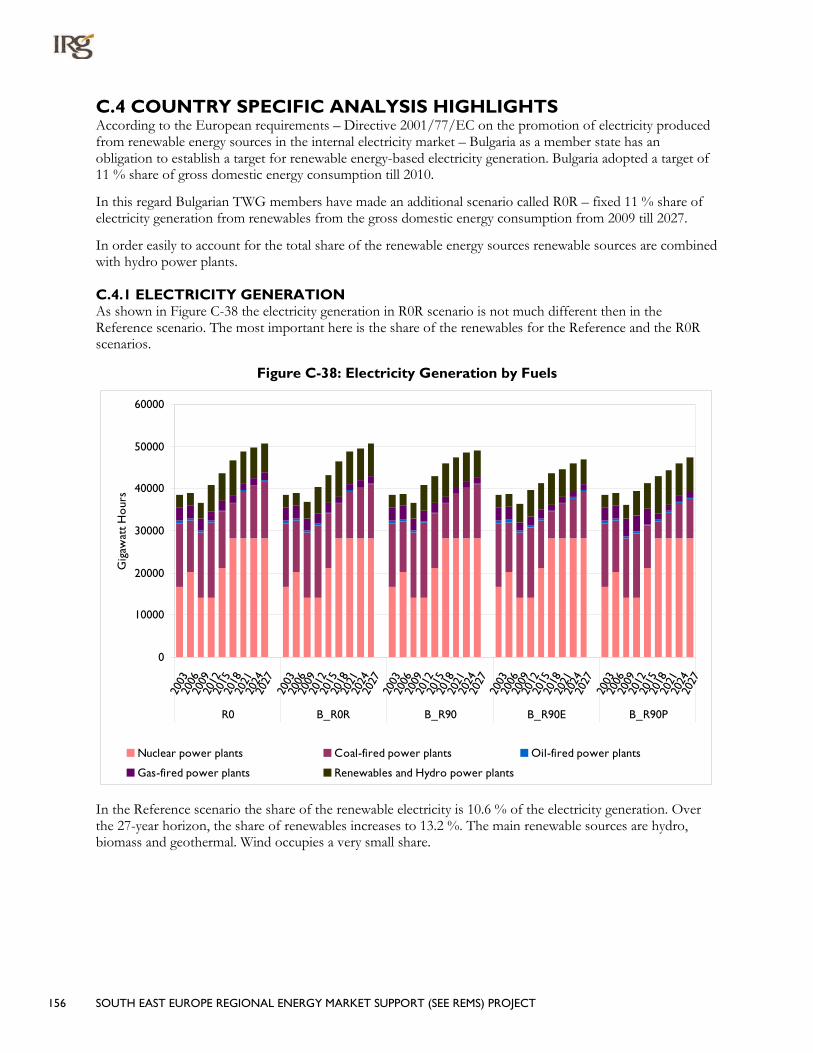

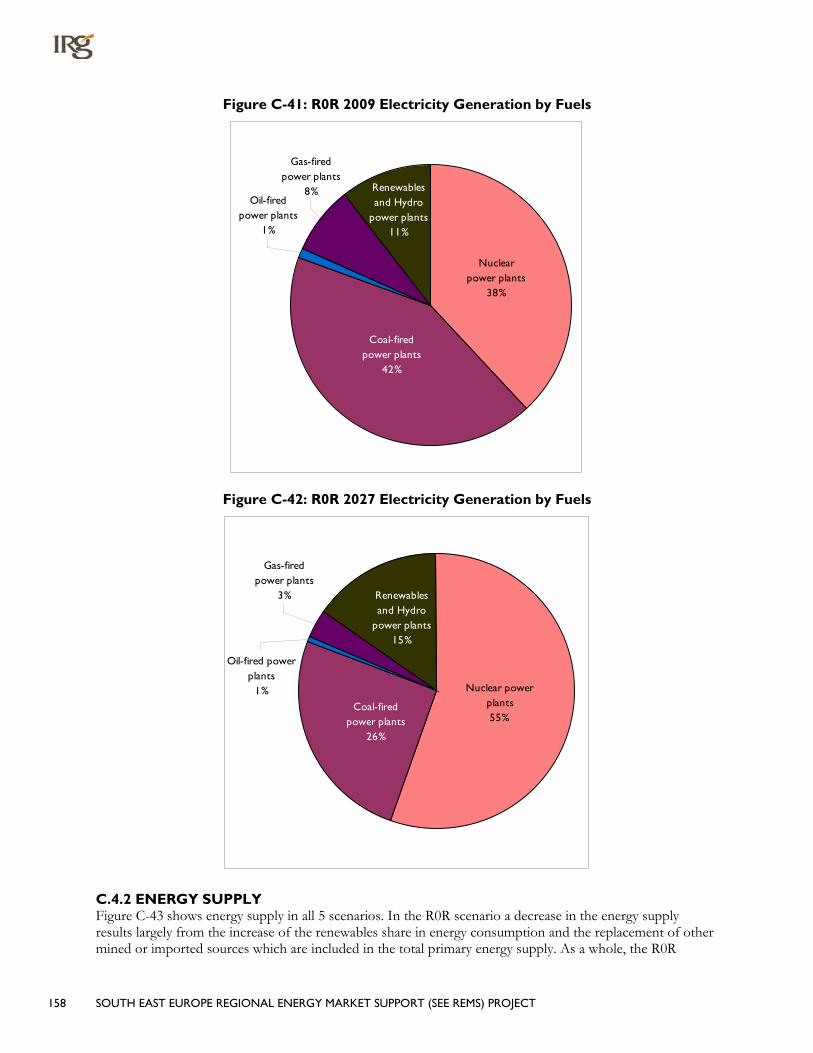

C.4 Country Specific Analysis Highlights .................................................................................................. 156 C.4.1 Electricity generation .................................................................................................................. 156 C.4.2 Energy Supply ................................................................................................................................ 158 C.4.3 Carbon Dioxide Emissions......................................................................................................... 159

D. Croatia ....................................................................................................................... 161 D.1 Highlights .................................................................................................................................................. 161

D.1.1 The Reference Scenario ............................................................................................................. 161 D.1.2 The Policy Scenarios ................................................................................................................... 163

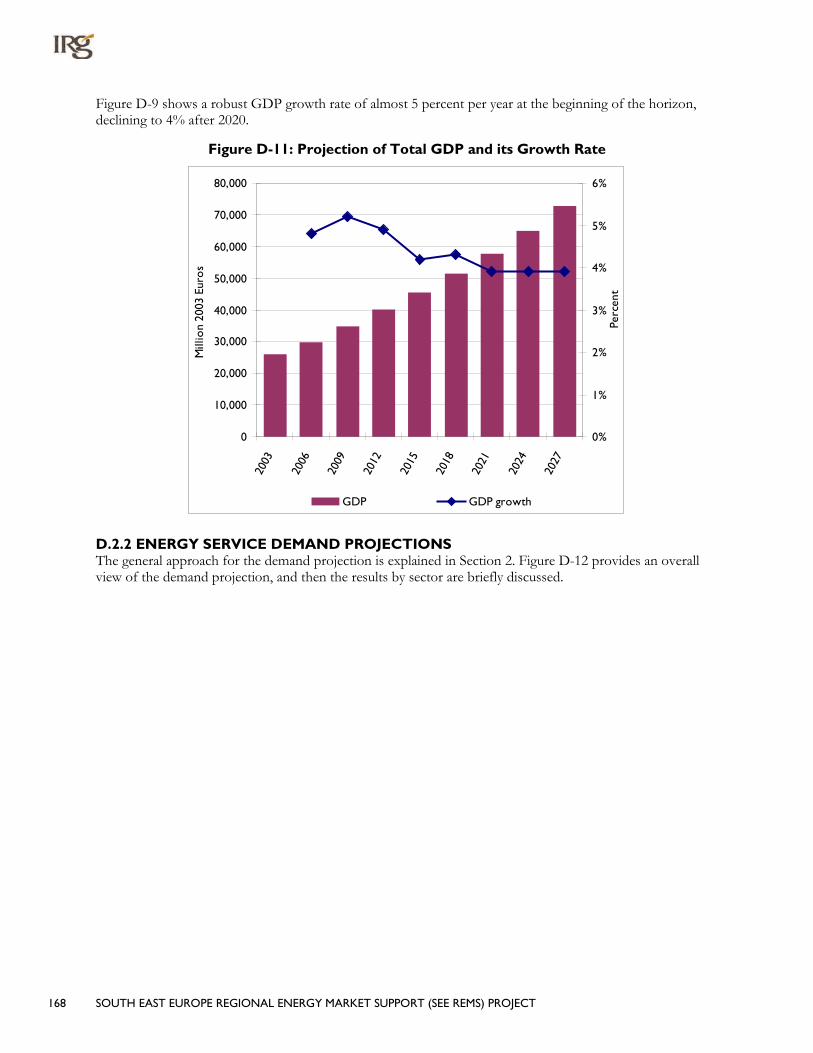

D.2 Assumptions for a Reference Scenario ............................................................................................. 166 D.2.1 Assumptions for the Drivers’ Growth ................................................................................... 166 D.2.2 Energy Service Demand Projections ....................................................................................... 168 D.2.3 Energy Resources and Regional Energy Prices ..................................................................... 172

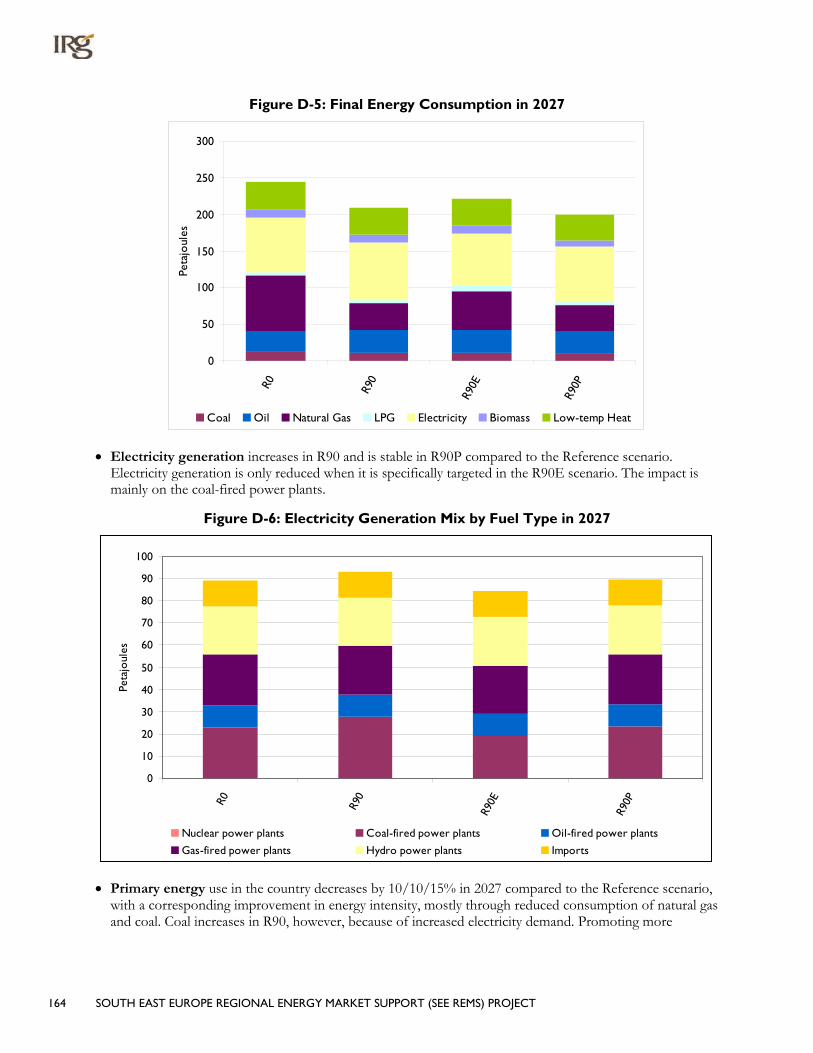

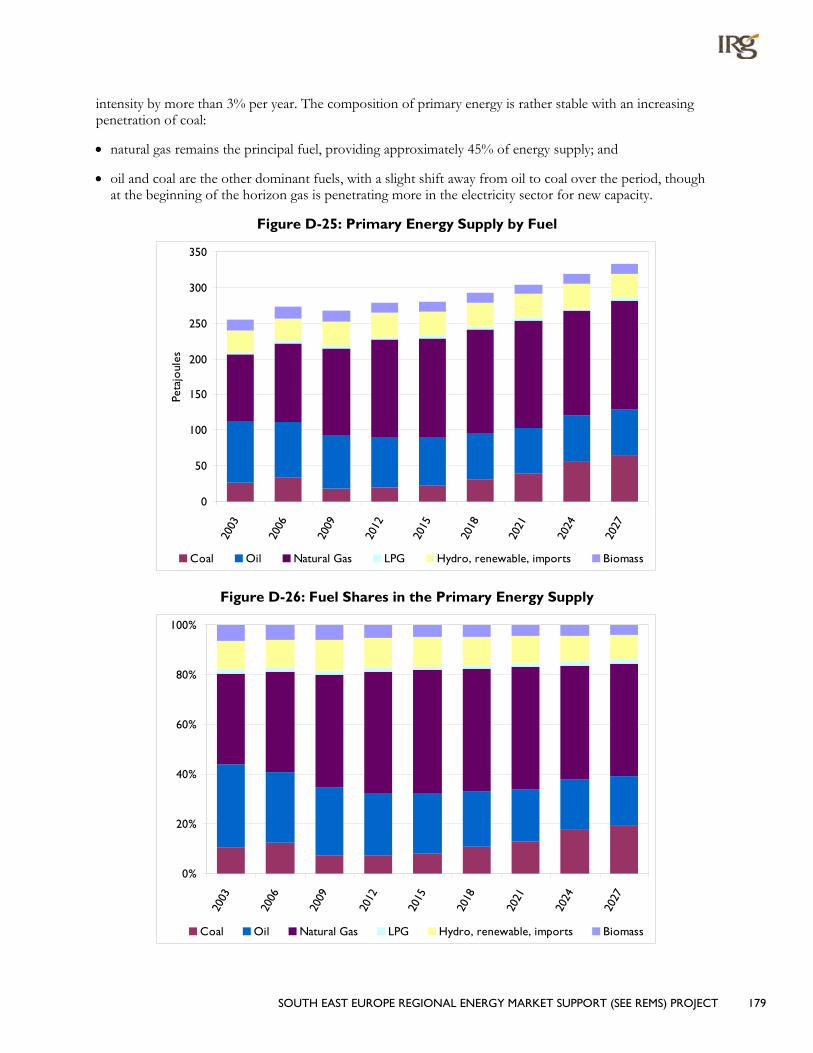

D.3 Reference Scenario Highlights ............................................................................................................. 173 D.3.1 Final Energy Consumption ......................................................................................................... 173 D.3.2 Electricity Generation Requirements ...................................................................................... 177 D.3.3 Primary Energy Supply ................................................................................................................ 178 D.3.4 Costs ............................................................................................................................................... 180

D.4 Scenario Analysis Highlights ................................................................................................................. 180 D.4.1 Final Energy Consumption ......................................................................................................... 180 D.4.2 Electricity Generation and Power Sector Investments ....................................................... 181 D.4.3 Primary Energy Supply ................................................................................................................ 183 D.4.4 Energy System Costs ................................................................................................................... 184

D.5 Country Specific Analyses .................................................................................................................... 186 D.5.1 Country Issues for Future Analyses I – Renewable Case Scenario ................................. 186 D.5.2. Country Issues for Future Analyses II – Nuclear PP Option Case Scenario ................ 187

D.6 Country Issues for Future Analyses ................................................................................................... 188 E. Macedonia .................................................................................................................. 189

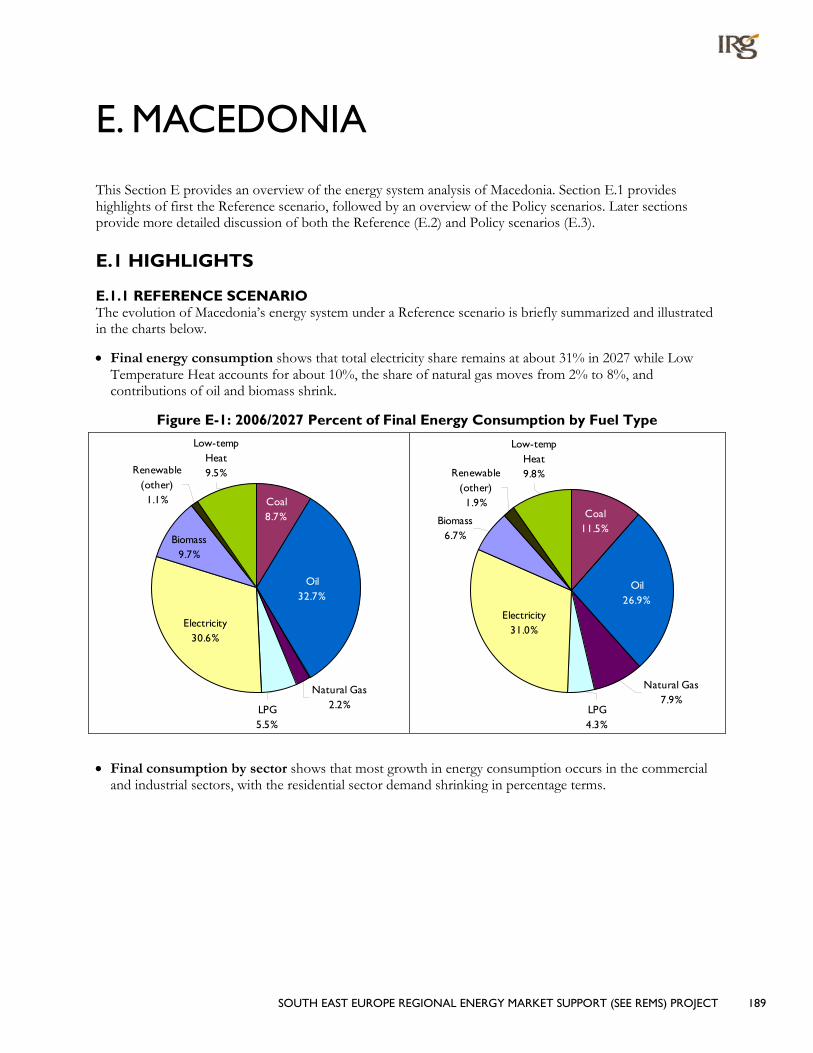

E.1 Highlights.................................................................................................................................................... 189 E.1.1 Reference Scenario ....................................................................................................................... 189 E.1.2 Policy Scenarios ............................................................................................................................. 191

E.2 Energy System Under a Reference Scenario ..................................................................................... 195 E.2.1 Critical Driving Assumptions ..................................................................................................... 195

iv SOUTH EAST EUROPE REGIONAL ENERGY MARKET SUPPORT (SEE REMS) PROJECT

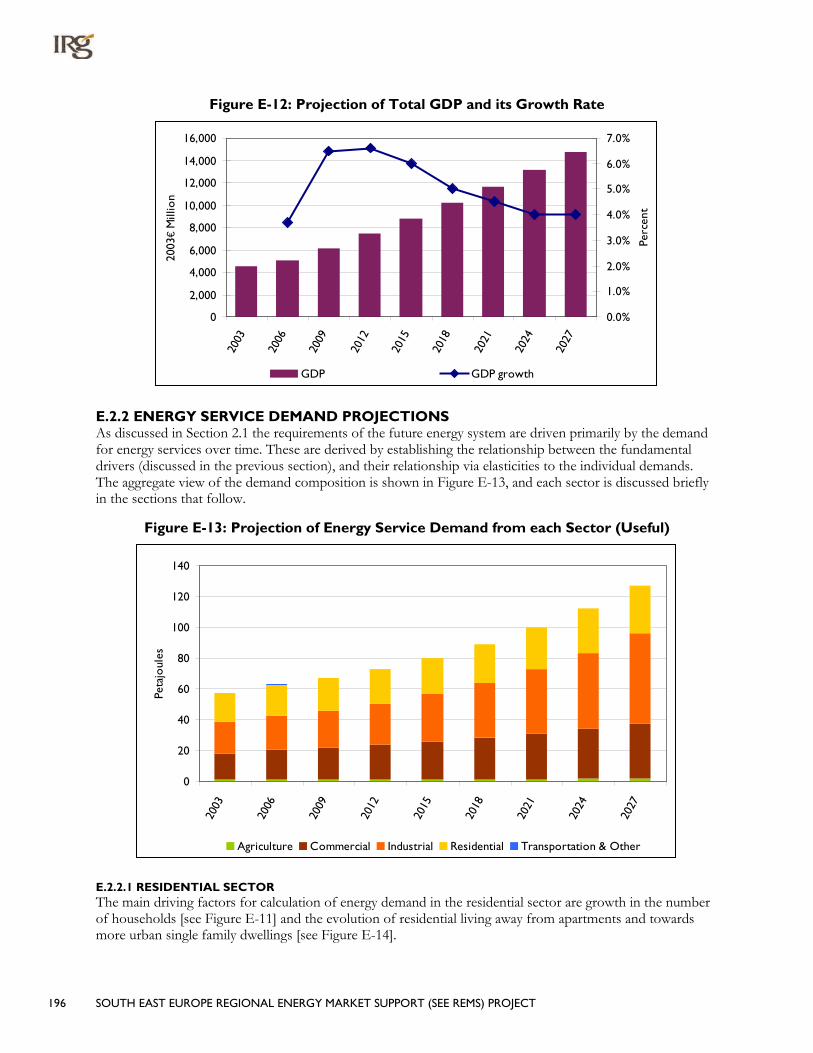

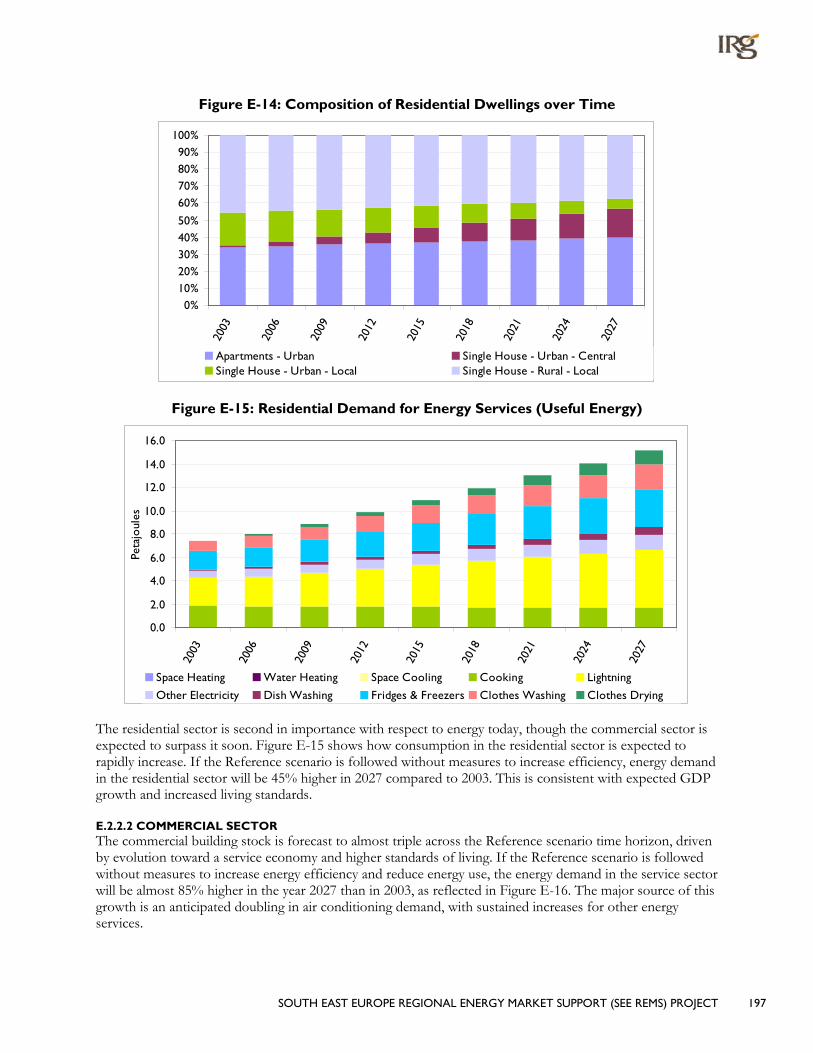

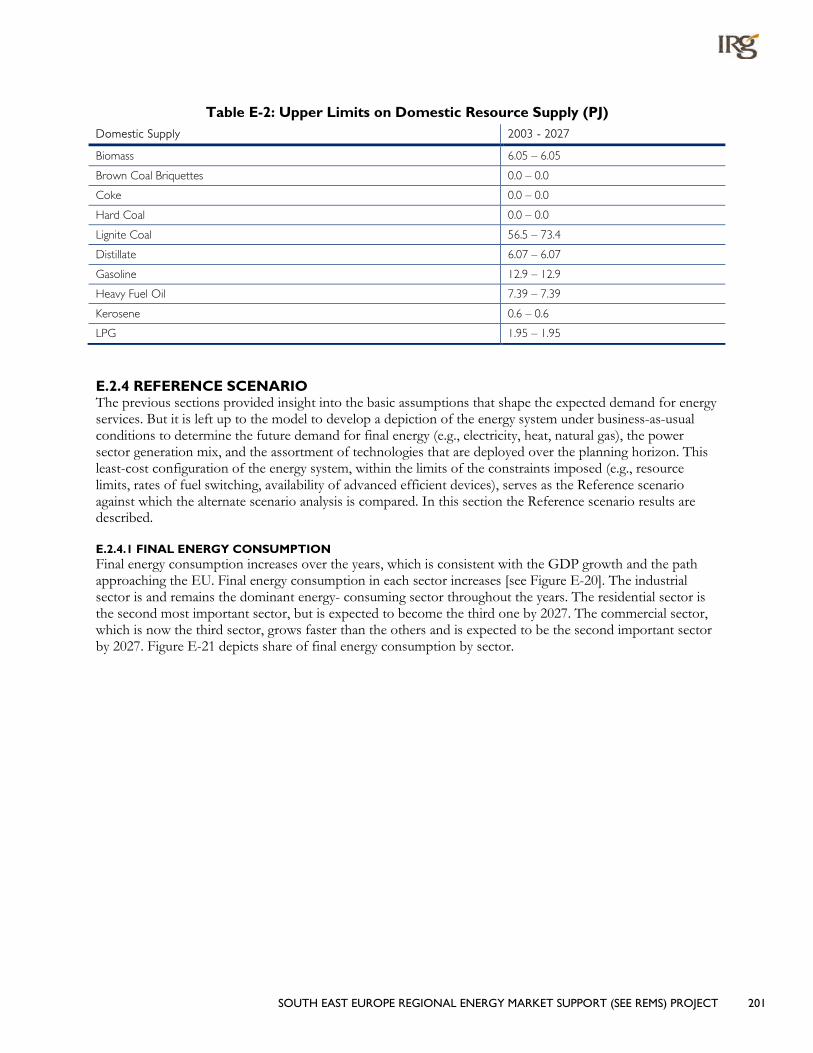

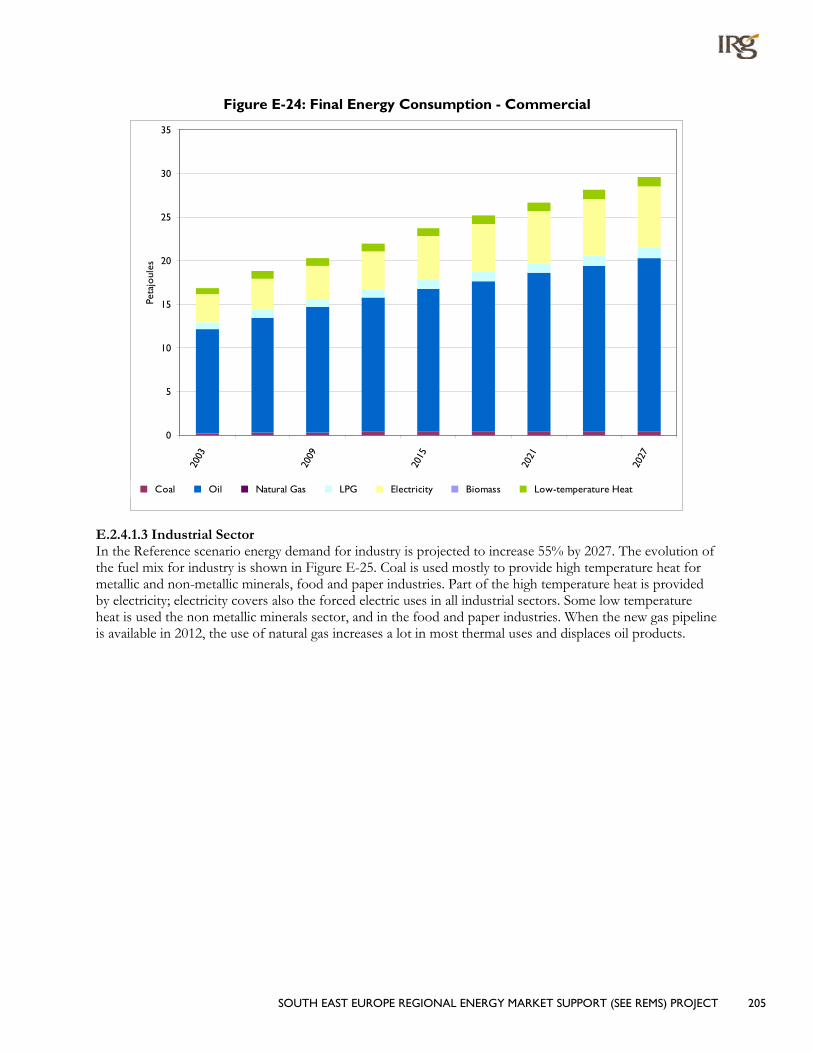

E.2.2 Energy Service Demand Projections ........................................................................................ 196 E.2.3 Energy Supply and Prices ............................................................................................................. 199 E.2.4 Reference Scenario ....................................................................................................................... 201

E.3 Scenario Analysis Results ....................................................................................................................... 210 E.3.1 Final Energy Consumption Patterns ......................................................................................... 210 E.3.2 Power Sector Investments and Electricity Generation ........................................................ 212 E.3.3 Energy Supply Picture ................................................................................................................... 214 E.3.4 Costs ................................................................................................................................................ 216

F. Romania ...................................................................................................................... 218 F.1 Highlights .................................................................................................................................................... 218

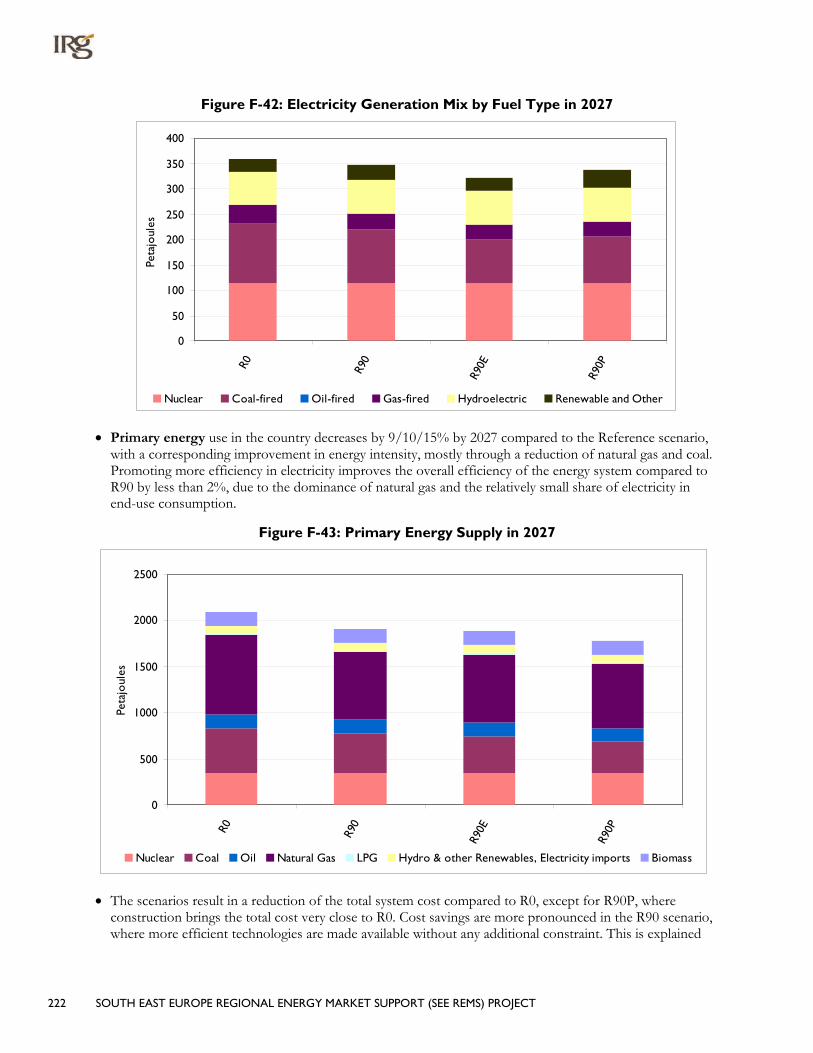

F.1.1 The Reference Scenario .............................................................................................................. 218 F.1.2 Policy Scenarios ............................................................................................................................. 221

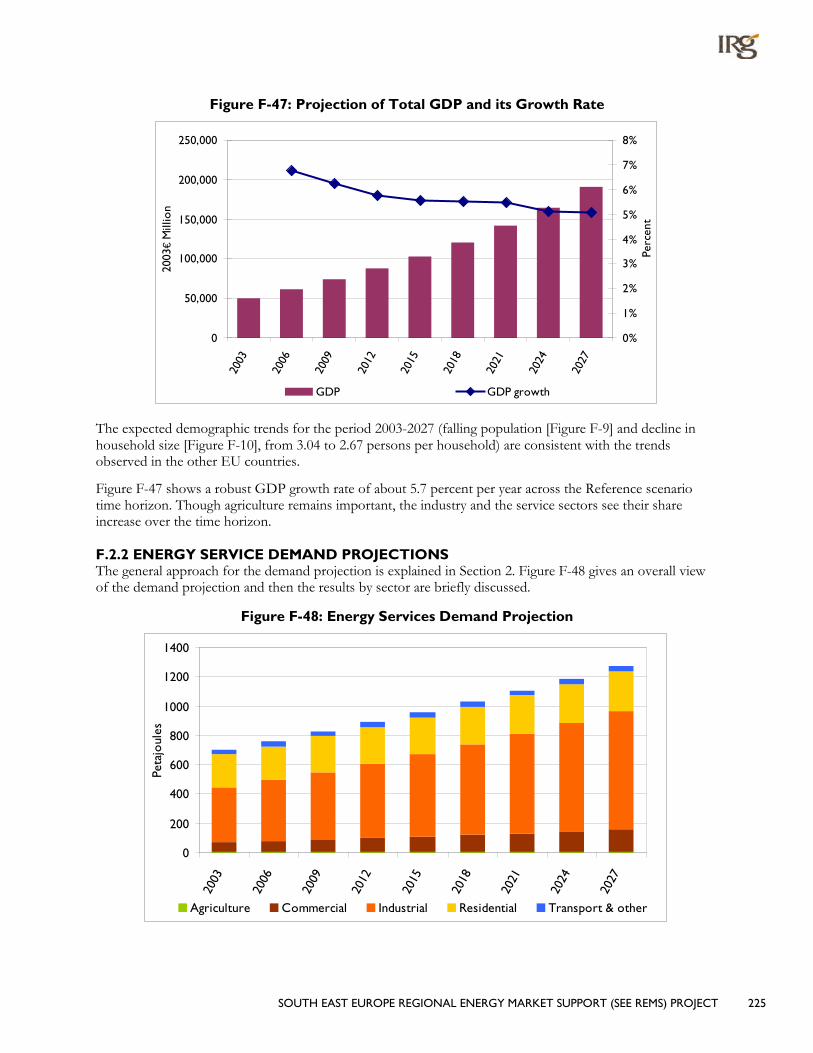

F.2 Assumptions for a Reference Scenario ............................................................................................... 223 F.2.1 Assumptions for the Drivers’ Growth ..................................................................................... 223 F.2.2 Energy Service Demand Projections ......................................................................................... 225 F.2.3 Energy Resources and Regional Energy Prices ....................................................................... 229

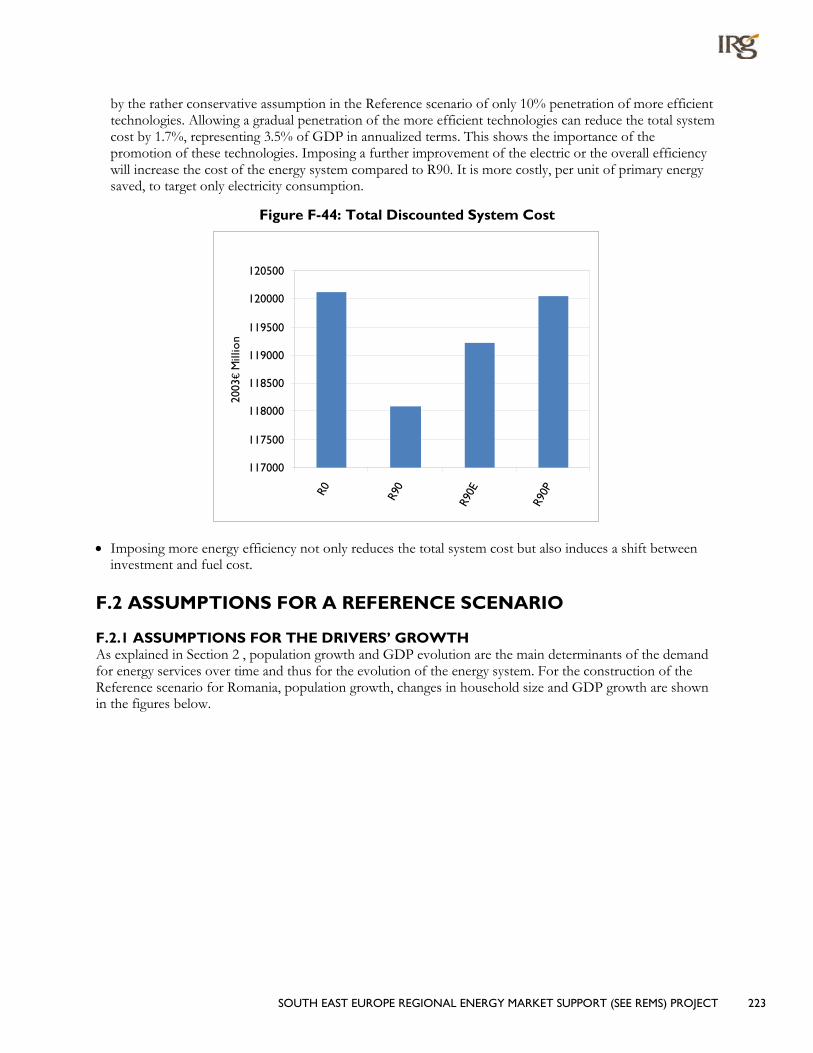

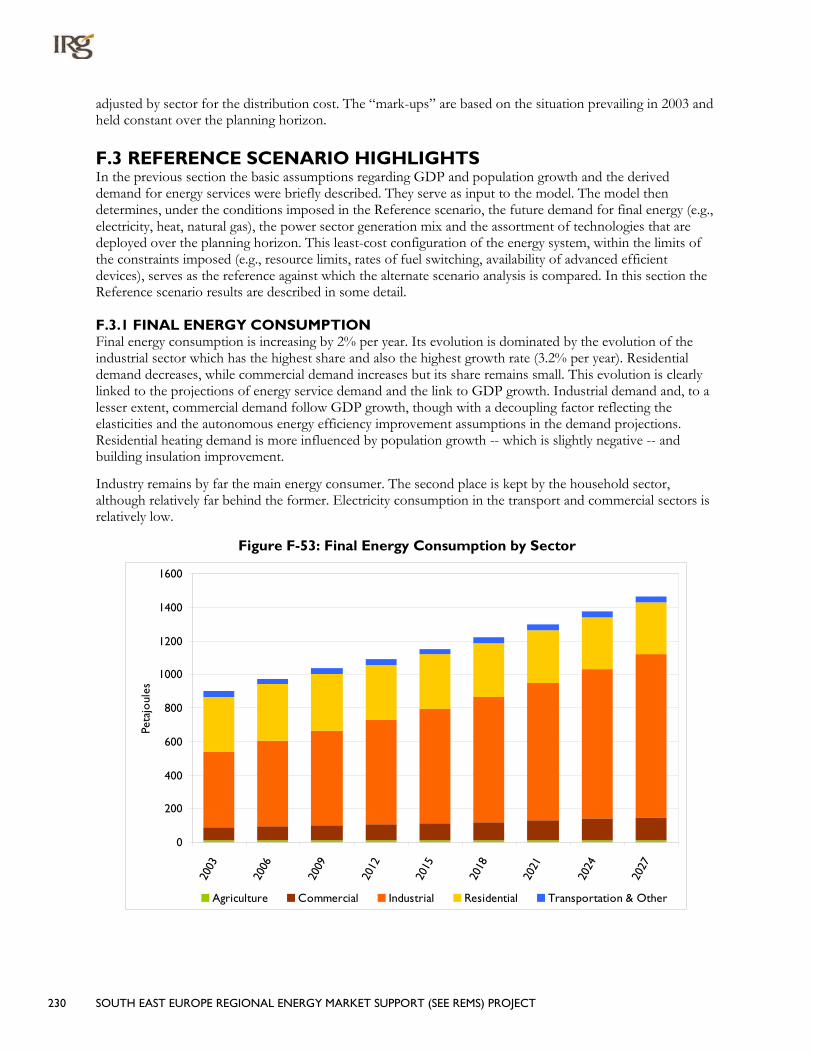

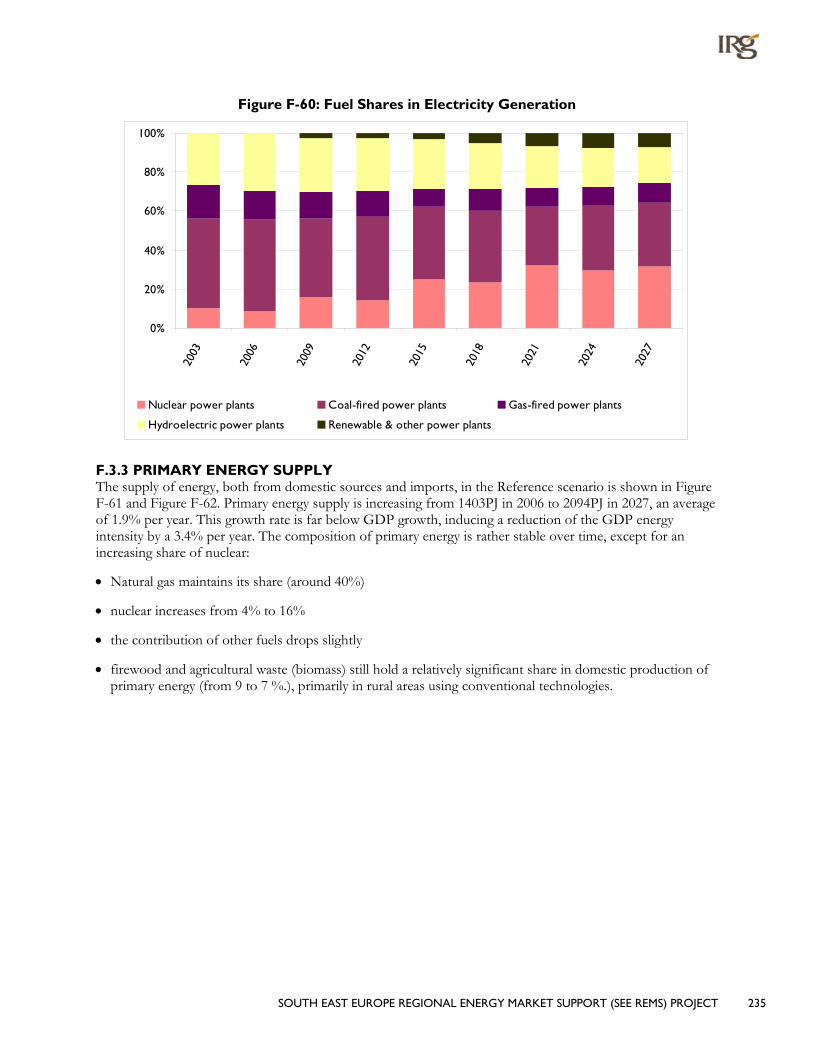

F.3 Reference Scenario Highlights .............................................................................................................. 230 F.3.1 Final Energy Consumption .......................................................................................................... 230 F.3.2 Electricity Generation Requirements ....................................................................................... 234 F.3.3 Primary Energy Supply ................................................................................................................. 235 F.3.4 Costs ................................................................................................................................................ 236

F.4 Scenario Analysis Highlights .................................................................................................................. 237 F.4.1 Final Energy Consumption .......................................................................................................... 237 F.4.2 Electricity Generation and Power Sector Investments ........................................................ 238 F.4.3 Primary Energy Supply ................................................................................................................. 241 F.4.4 Energy System Costs .................................................................................................................... 242

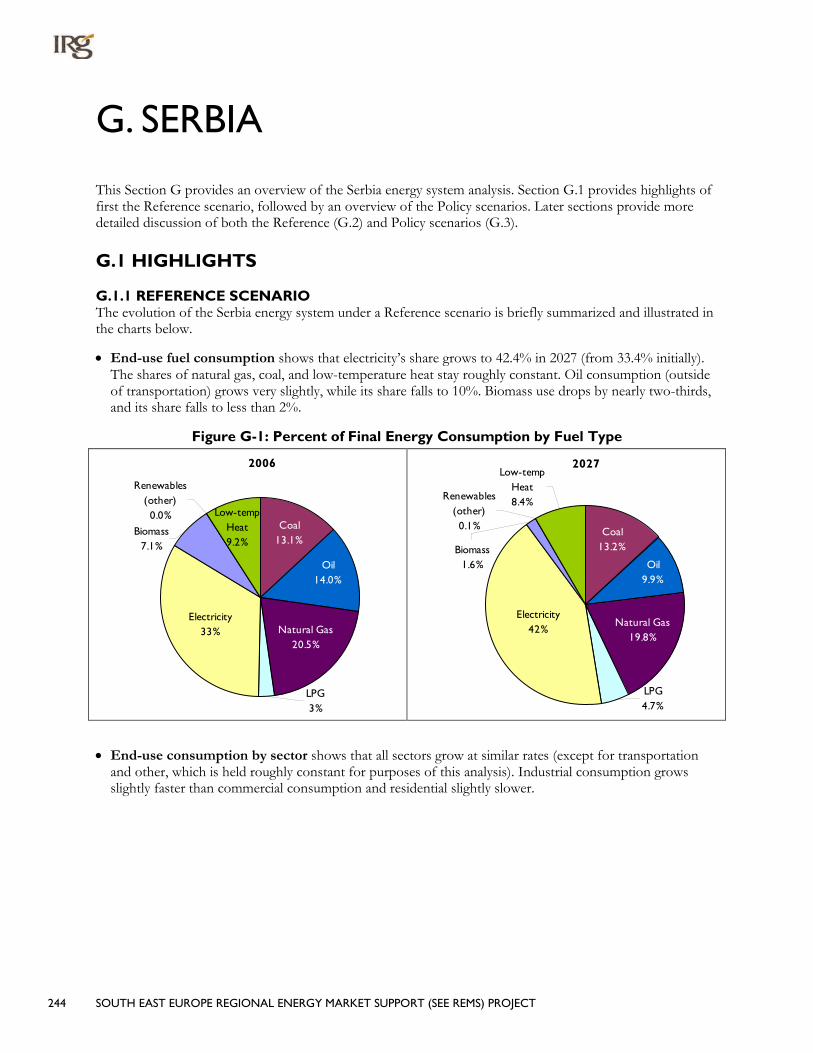

G. Serbia ......................................................................................................................... 244 G.1 Highlights .................................................................................................................................................. 244

G.1.1 Reference Scenario ...................................................................................................................... 244 G.1.2 Policy Scenarios ............................................................................................................................ 246

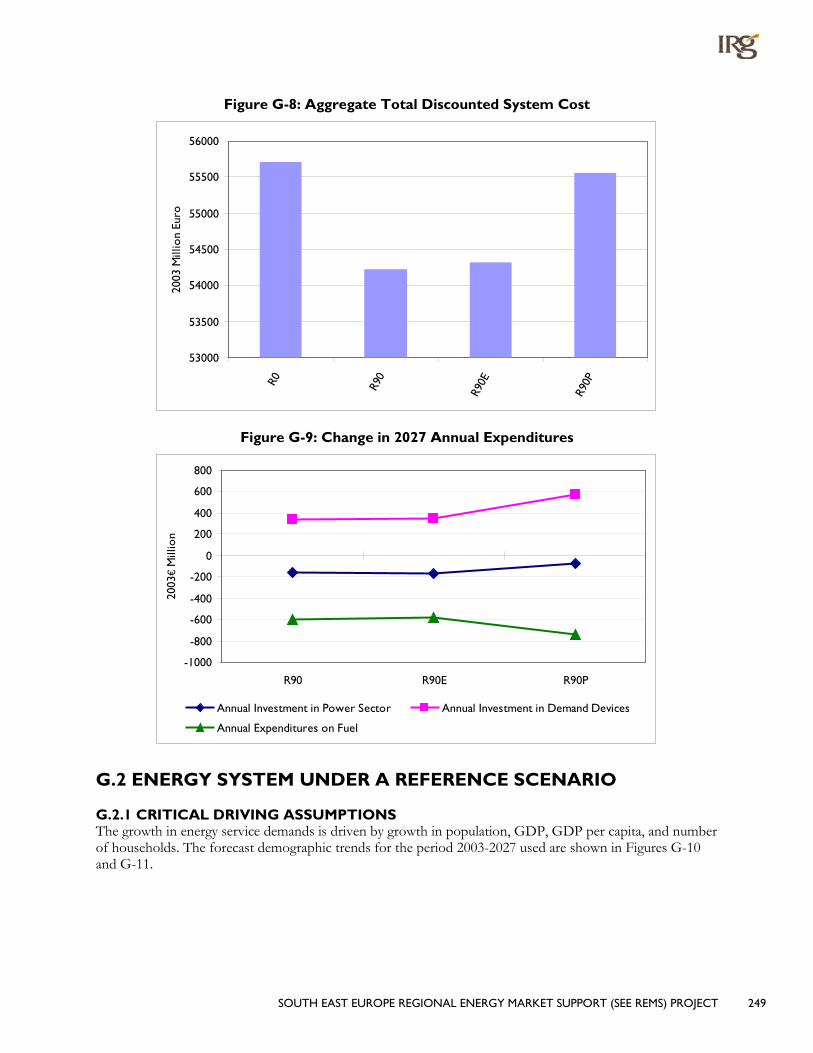

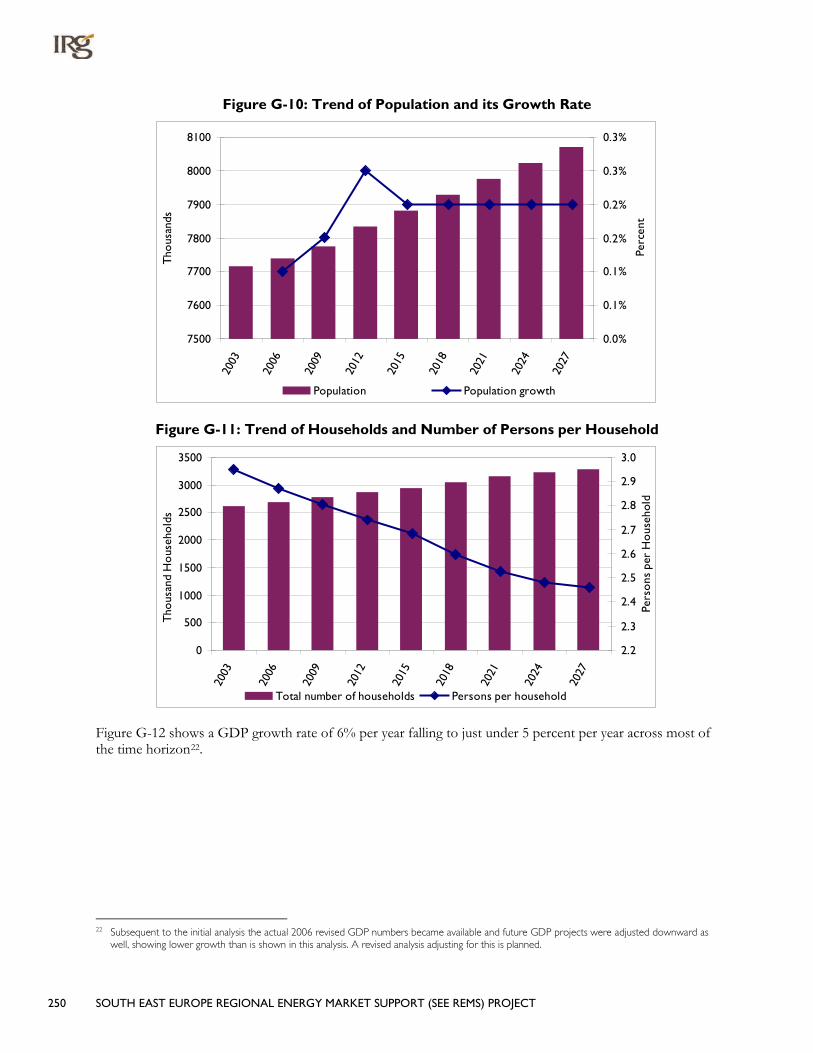

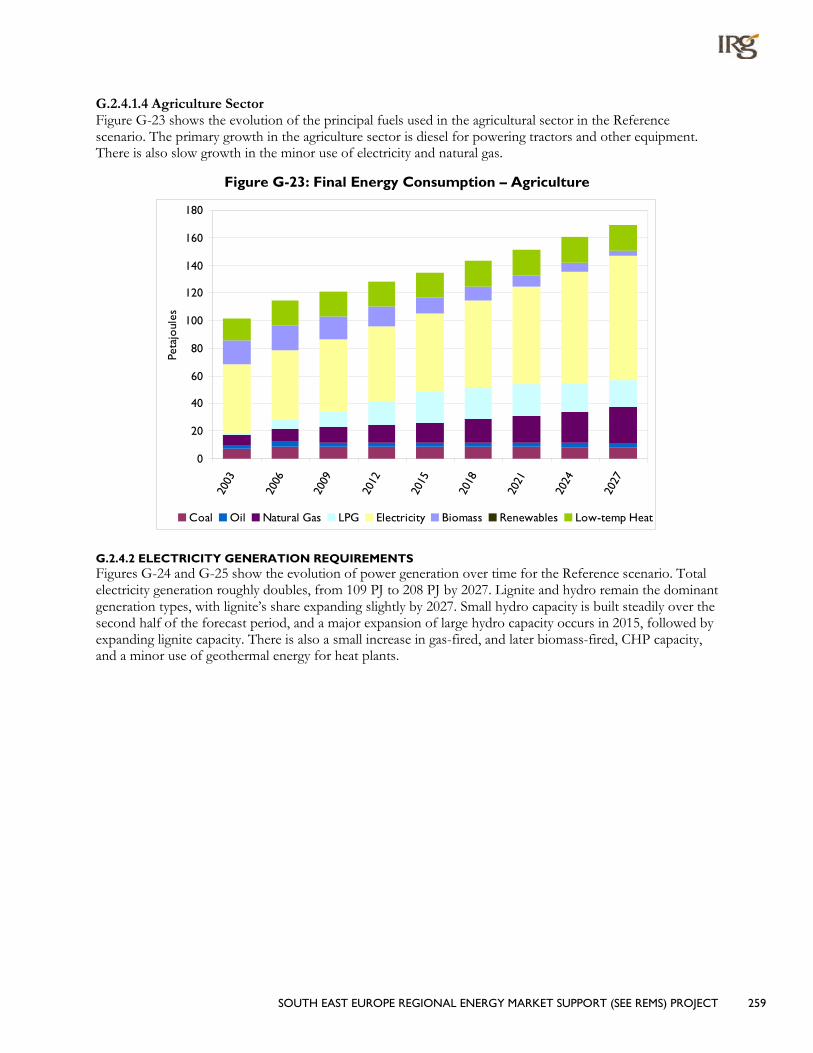

G.2 Energy System Under a Reference Scenario .................................................................................... 249 G.2.1 Critical Driving Assumptions .................................................................................................... 249 G.2.2 Energy Service Demand Projections ....................................................................................... 251 G.2.3 Energy Supply and Prices ............................................................................................................ 254 G.2.4 Reference Scenario Highlights .................................................................................................. 255

SOUTH EAST EUROPE REGIONAL ENERGY MARKET SUPPORT (SEE REMS) PROJECT v

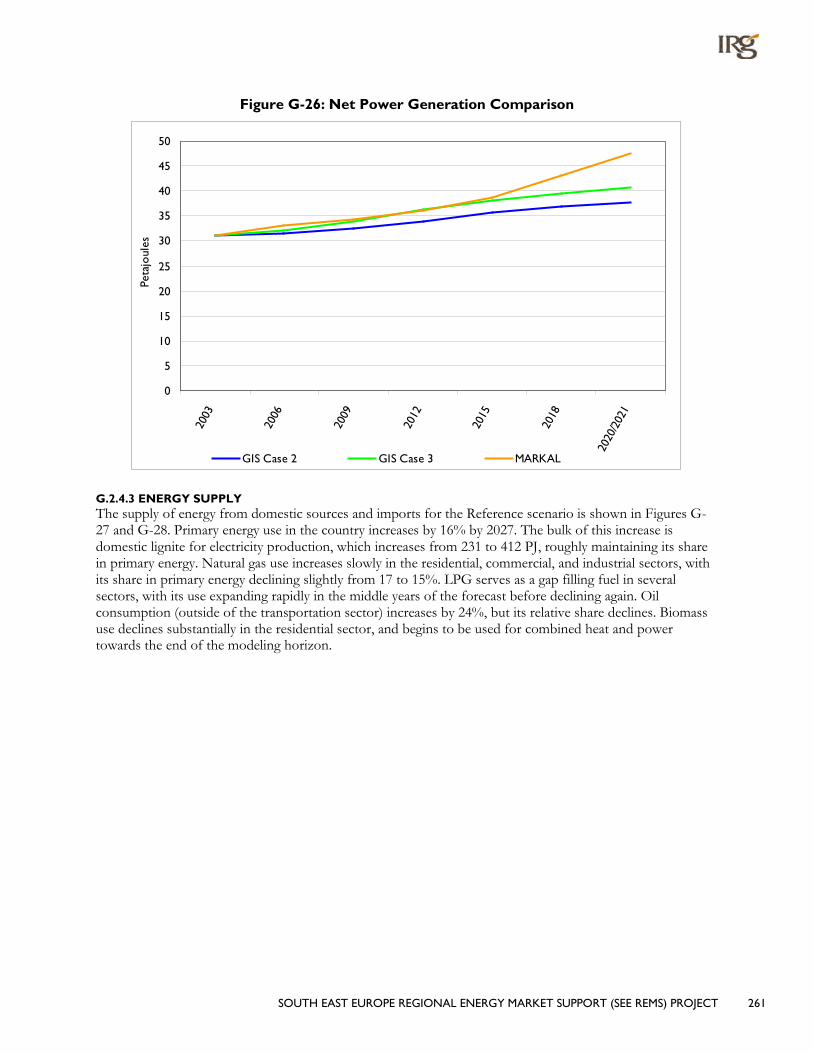

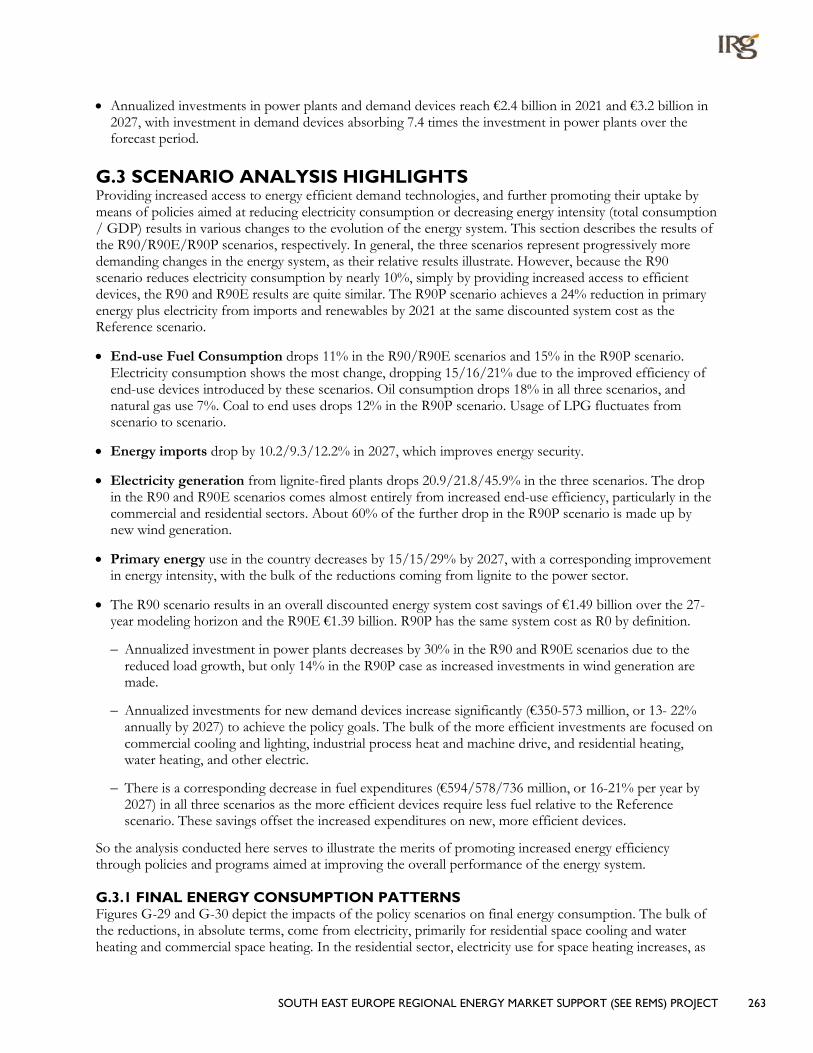

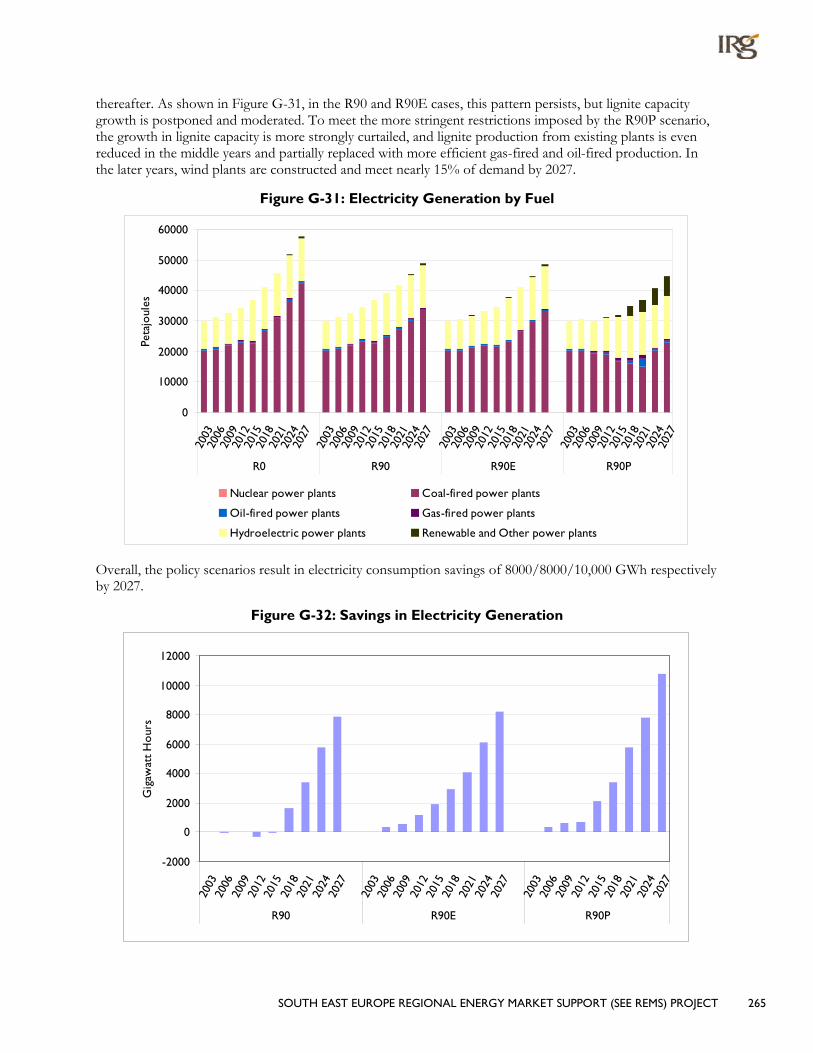

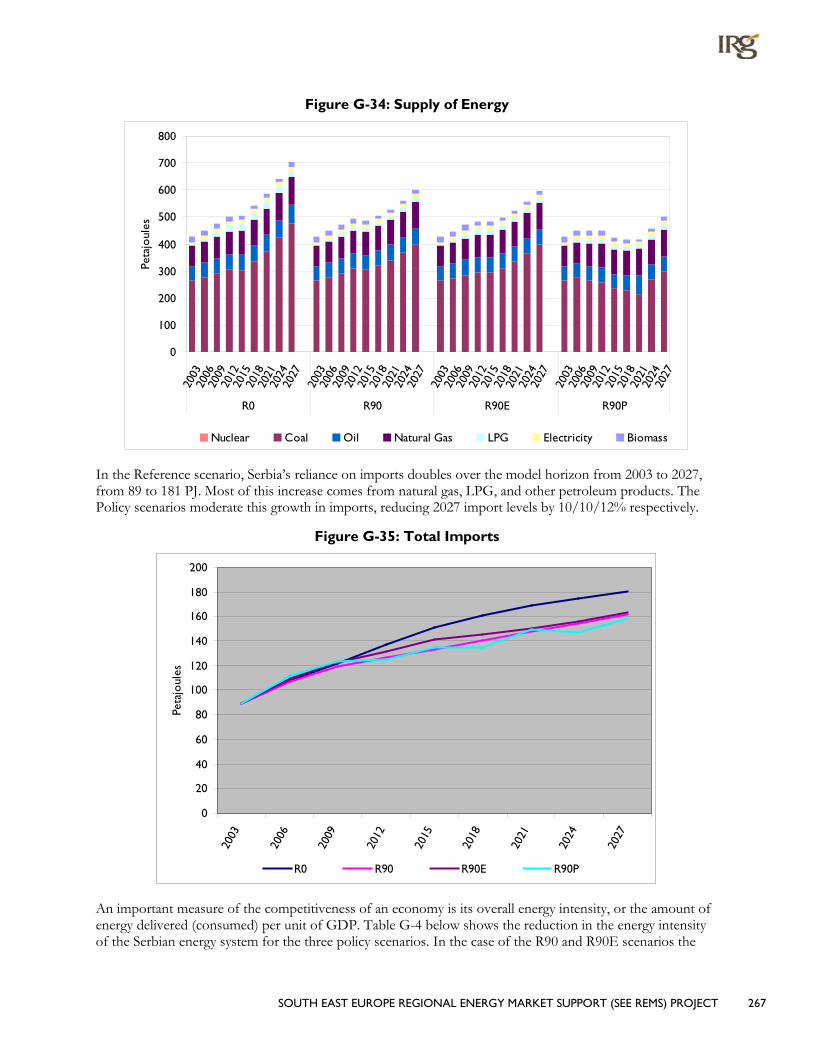

G.3 Scenario Analysis Highlights ................................................................................................................. 263 G.3.1 Final Energy Consumption Patterns ........................................................................................ 263 G.3.2 Power Sector Investments and Electricity Generation ....................................................... 264 G.3.3 Energy Supply Picture ................................................................................................................. 266 G.3.4 Costs ............................................................................................................................................... 268

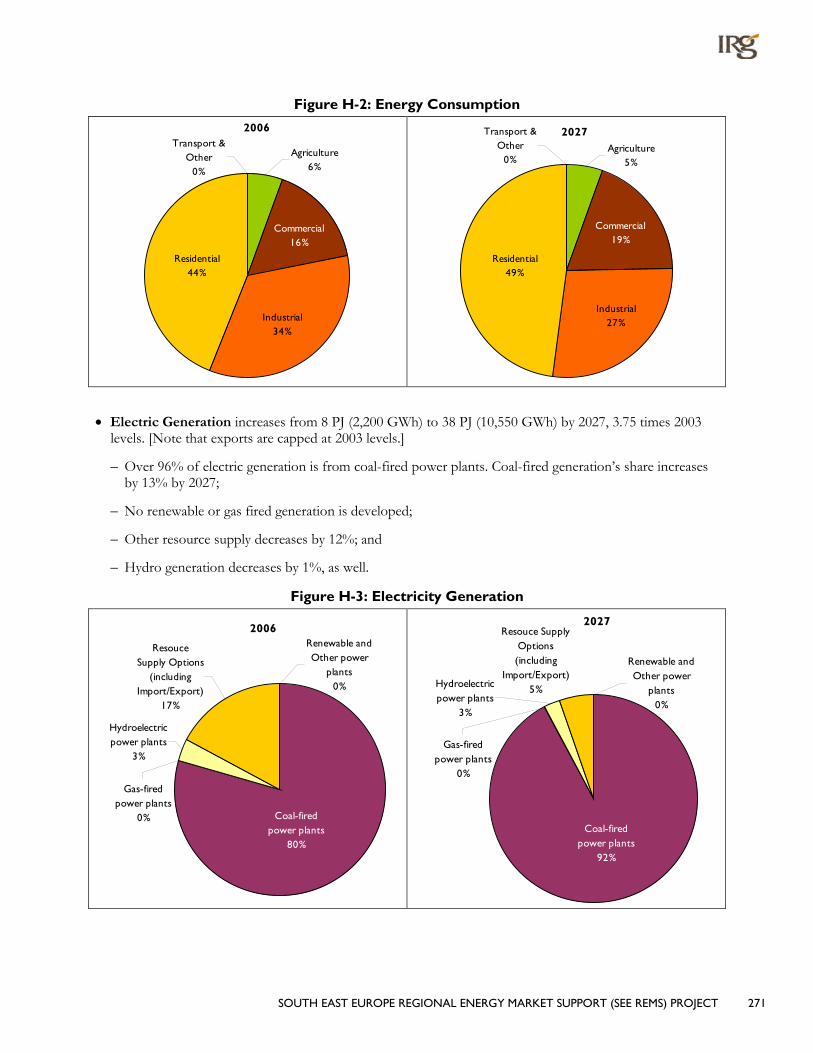

H. UNMIK ....................................................................................................................... 270 H.1 Highlights .................................................................................................................................................. 270

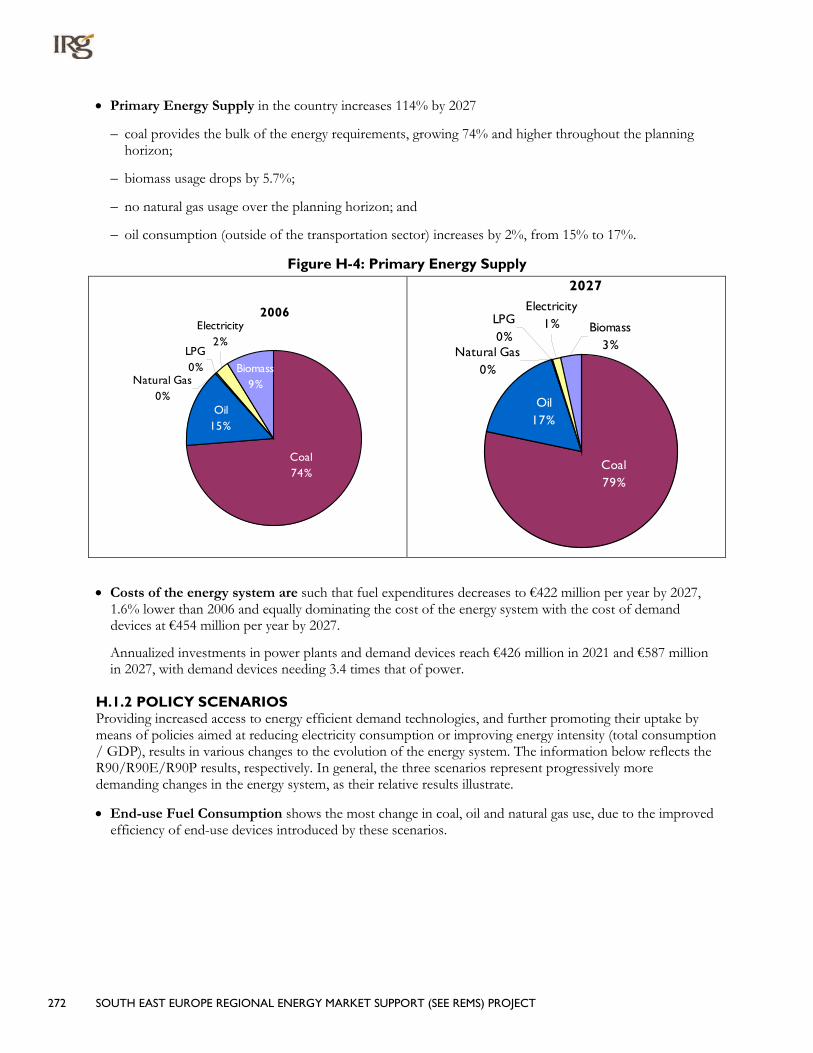

H.1.1 Reference Scenario ...................................................................................................................... 270 H.1.2 Policy Scenarios ............................................................................................................................ 272

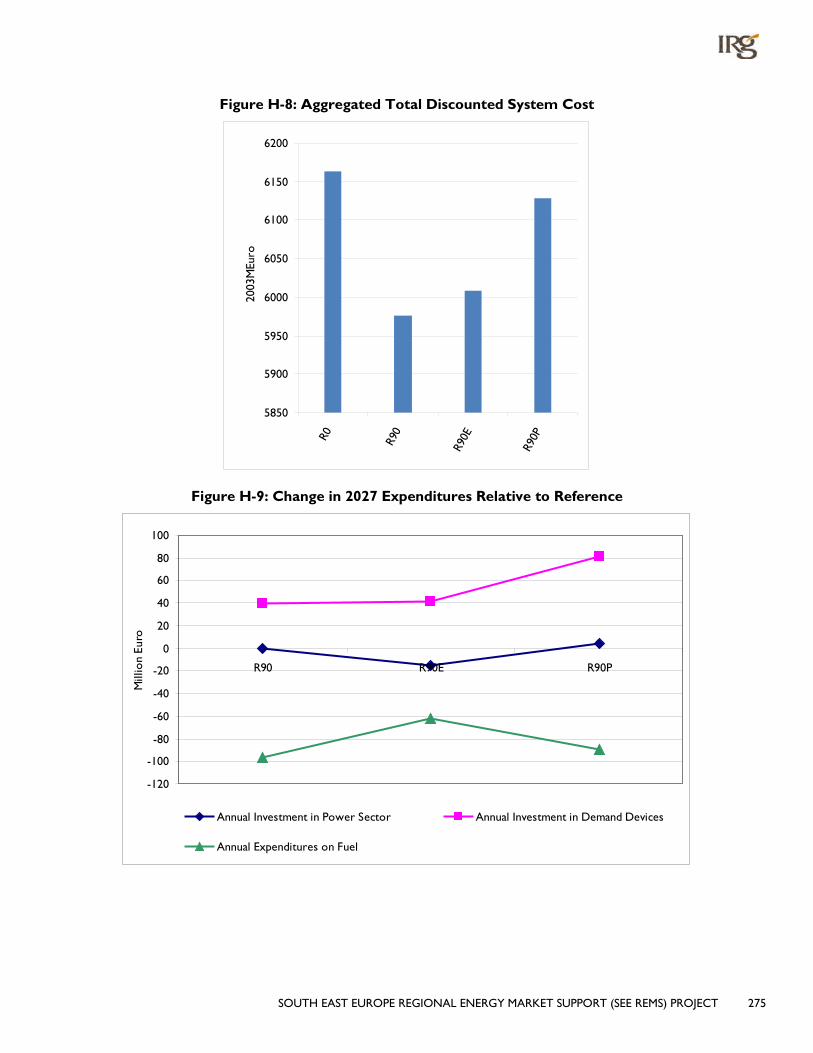

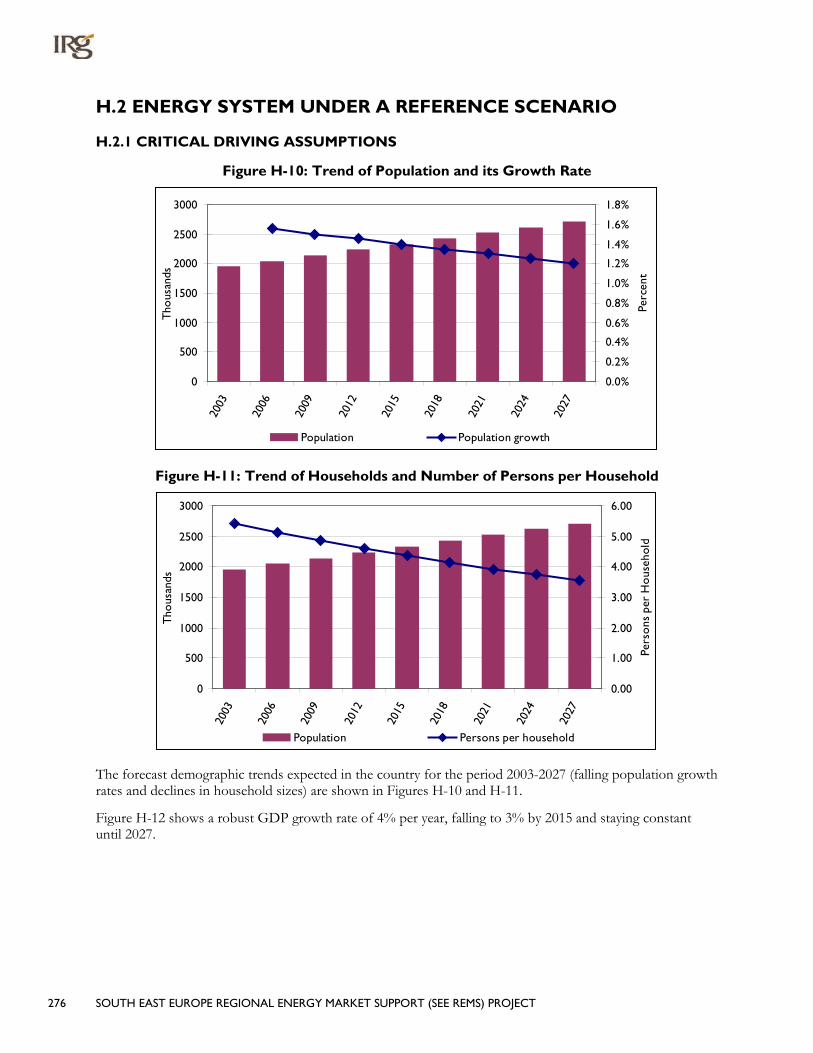

H.2 Energy System Under a Reference Scenario .................................................................................... 276 H.2.1 Critical Driving Assumptions .................................................................................................... 276 H.2.2 Energy Service Demand Projections ....................................................................................... 277 H.2.3 Energy Supply and Prices ............................................................................................................ 280 H.2.4 Reference Scenario Highlights .................................................................................................. 282

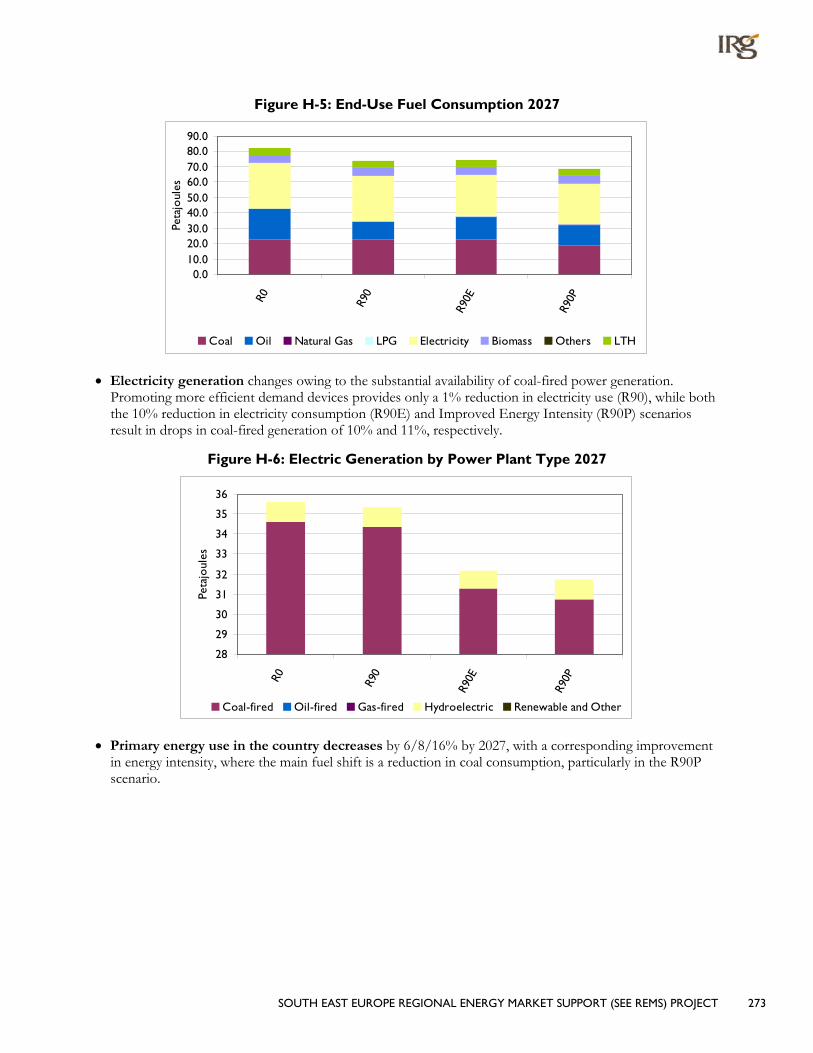

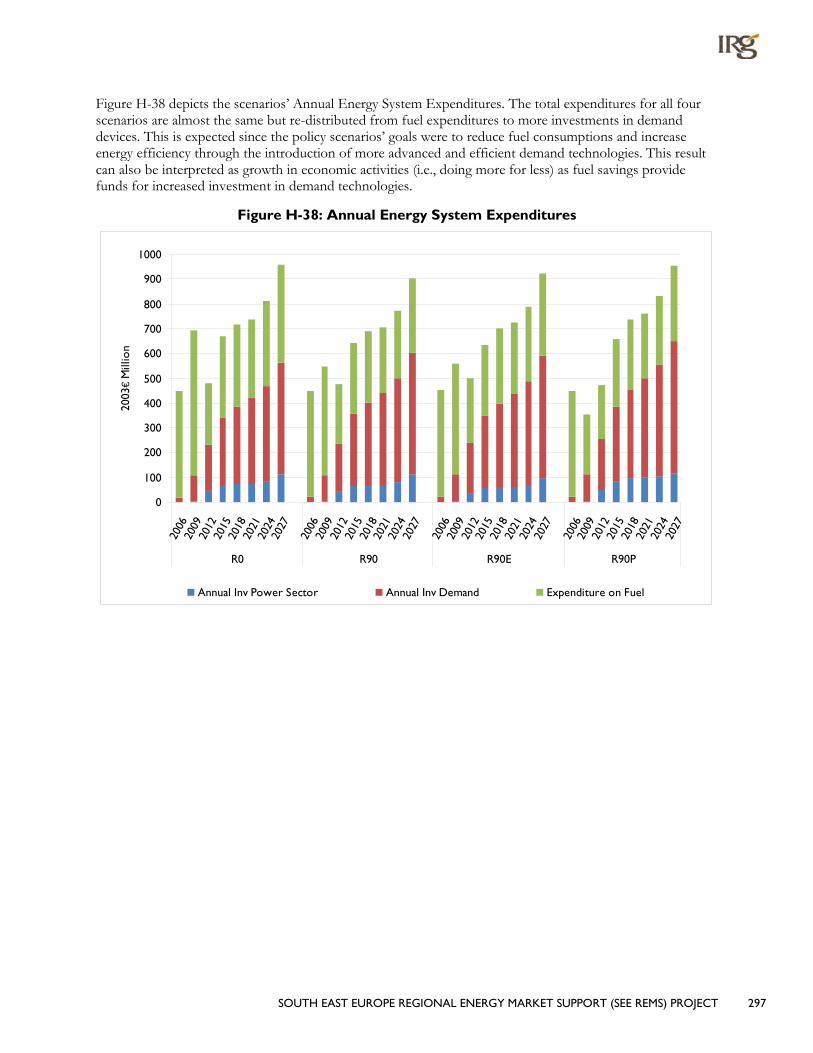

H.3 Scenario Analysis Highlights ................................................................................................................. 290 H.3.1 Final Energy Consumption Patterns ........................................................................................ 290 H.3.2 Power Sector Investments and Electricity Generation ....................................................... 292 H.3.3 Energy Supply Picture.................................................................................................................. 294 H.3.4 Costs ............................................................................................................................................... 296

SOUTH EAST EUROPE REGIONAL ENERGY MARKET SUPPORT (SEE REMS) PROJECT 1

EXECUTIVE SUMMARY

CONTEXT The countries of South East Europe are developing regional approaches to energy cooperation. The Athens Treaty that came into force in July 2006 encourages creating regional electricity and gas markets as steps towards integration into the European Union’s (EU’s) Internal Energy Market. Countries in the region are in varying stages of transition to competitive markets and accession to the European Union. There are several core issues that should be examined as countries transition to liberalized energy markets while simultaneously addressing EU directives and fostering development of globally competitive economies. These issues include: the relationship between economic growth and energy demand, the potential for energy efficiency gains, the increased role for natural gas and renewables, and full integration and harmonization of the regional electricity and natural gas systems.

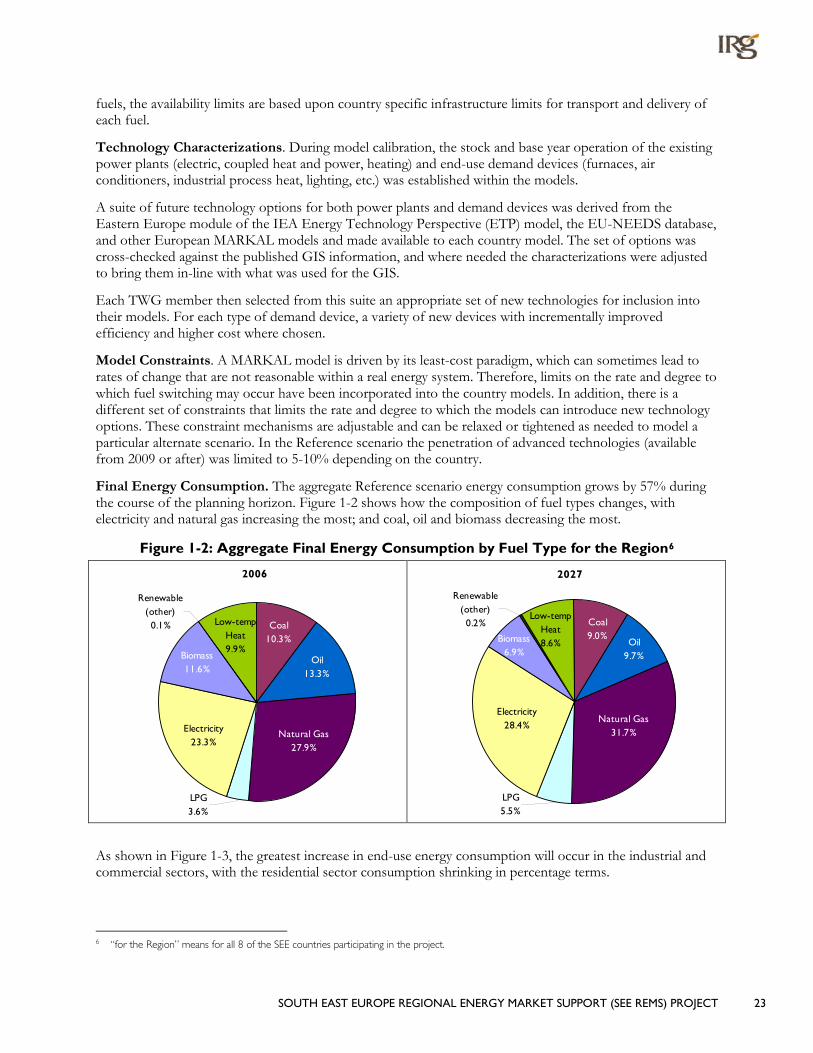

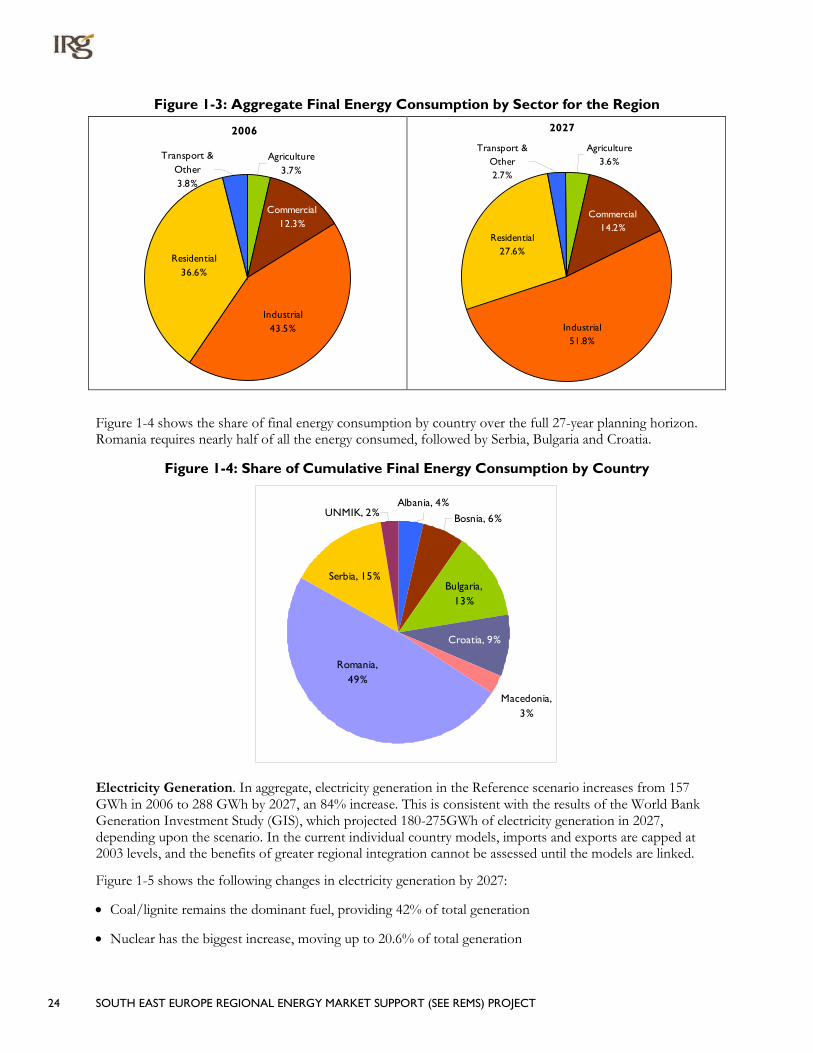

As is detailed in Section 2, the Reference scenario, continuation of current trends in regional energy use, shows aggregate energy use for the region increasing by almost 60 percent [and electricity use rising by over 80 percent] over the next 27 years. Careful planning and the institution of policies to foster more efficient and cost-effective energy technologies could temper this growth, while providing significant environmental and economic benefits. The goal is to lay the foundation for fostering a better understanding of the possible paths for the evolution of the national energy systems by building analytical capacity within the region to inform energy planners and decision-makers and to use these tools to examine the costs and benefits of more efficient alternatives to the current course of energy policy.

This report summarizes the results to date of the United States Agency for International Development (USAID)-supported Regional Energy Demand Planning (REDP) activities under the South East Europe Regional Energy Market Support (SEE REMS) Project (10/1/2004 – 9/30/2008). The original countries directly involved in implementing the planning activities included Albania, Bulgaria, Bosnia and Herzegovina, Croatia, Macedonia, Romania, Serbia and Montenegro and the United Nations Interim Mission in Kosovo (UNMIK pursuant to the UN SCR 1244). Under REDP, USAID sought to complement the work begun under the Generation Investment Study (GIS) 1

ACCOMPLISHMENTS

of the World Bank by conducting a more detailed analysis of the demand for energy and the competing factors and policies that will shape this demand.

The SEE REMS project supported teams from the energy planning ministries of each country in developing National Energy Planning Models using the MARKAL/TIMES framework2

For each country model, the current energy system was depicted and calibrated using 2003 national energy balance data to produce a baseline “snapshot” of the technology stock in place. Forecasts for economic growth were translated into projected future demands for energy services (e.g., heating buildings, lighting houses, providing high-temperature heat to industry) out to 2027. The technical and economic characterizations of existing and advanced energy supply and end-use technologies were incorporated into the models, and each of the country teams used its knowledge and expert judgment to refine the models’

. These national models provide a framework for exploring policy options and investment strategies, integrating supply-side and demand-side options to promote the cost-effective evolution of the energy systems in each country, and in the region as a whole.

1 Development of Power Generation In the South East Europe Update of Generation Investment Study, , Volume 1: Summary Report, Final

Report, prepared by South East Europe Consultants Ltd. for The World Bank, January 9, 2007. 2 A widely applied full-sector energy systems modeling platform that can analyze energy, economic and environmental issues at the global, national

and municipal levels, over several decades; www.etsap.org.

2 SOUTH EAST EUROPE REGIONAL ENERGY MARKET SUPPORT (SEE REMS) PROJECT

projection of a Reference (or continued current dynamics) scenario for each country. This scenario then served as the comparison point for evaluating the benefits, costs, and technology investments that would result from the implementation of possible future government policies, programs, environmental constraints, and various resource supply options.

As part of this USAID project the regional capacity to perform national energy system modeling and analysis has been created by mentoring the country teams through the process of model development and utilization. As this report demonstrates, the teams now have the capacity to perform meaningful analyses with their models. This capacity is a significant first step towards better informed national and regional policy making decisions based on more robust, locally guided, analyses – the ultimate objective of the REDP. With this foundation, policy makers in the region can now collaborate with the country model teams to perform ever changing analyses of various economic and policy scenarios to evaluate the costs and benefits of a range of mechanisms and select the preferred set of actions to effect desired outcomes. The potential benefits are enormous – in terms of more efficient investment, enhanced energy security, increased environmental protection, and more targeted policies with fewer unanticipated impacts.

The analysis in this report focuses largely on potential benefits to be gained from efficiency improvements and examines both supply-side solutions and introduction of programs and policies to encourage investments in demand-side energy efficiency measures and thereby reduce necessary supply-side costs. The indicative policy analyses indicate the resultant benefits in terms of energy security (less imports) and competitiveness (better energy intensity at acceptable cost).

ANALYTICAL RESULTS This report presents the results of a few indicative policy scenario analyses performed using the newly built models and provides insights into regional and national energy system dynamics by:

• Quantifying the energy supply needed to meet future energy demand;

• Comparing the investments (supply-side and end-use) and fuel expenditures required to implement alternate policies relative to the Reference scenario;

• Identifying the impacts of those policies on technology choices and fuel mix in the different demand sectors; and

• Examining the changes in energy system costs, energy security and environmental impacts.

The analysis explores the potential role of policies aimed at encouraging greater energy efficiency throughout the region using three alternatives to the Reference scenario representing progressively stronger implementation of energy efficiency measures:

• Promoting Energy Efficiency (R90) – accelerated adoption of more energy efficient end-use devices

• Reducing Electricity Consumption (R90E) – a “mandated” 10% reduction in electricity consumption from the Reference levels and

• Reducing Energy Intensity (R90P) – a cost-effective (relative to the Reference scenario) reduction in overall energy system intensity achieved by limiting total energy use (supply and end-use).

The primary results of the analysis are summarized in Table ES-1, and Figures ES-1 and ES-2. Table ES-1 shows the range of cost and energy savings provided by the three scenarios relative to the Reference scenario.

SOUTH EAST EUROPE REGIONAL ENERGY MARKET SUPPORT (SEE REMS) PROJECT 3

Table ES-1. Benefits Arising from Increased Energy Efficiency Improvement Benefit Range (in 2027)

Total discounted energy system cost savings 1.5 - 2% (€3.78 - €6.06 billion) over the planning horizon

Change in undiscounted annual costs

Power plant investment Decrease of .2 – 15% (5 - 455€ million)

Demand-side investment Increase of 14 – 28% (1.59 – 3.16€ billion)

Fuel Expenditure Decrease of 13 – 16% (€3.43/3.36/4.04 billion)

Annual energy savings 9 – 18% (417 – 793 PJ)

Annual electricity savings 6 – 11% (17 - 33GWh)

Reduction of imports 16 – 17% (309 – 343 PJ)

Decrease in energy intensity 9.4 – 18%

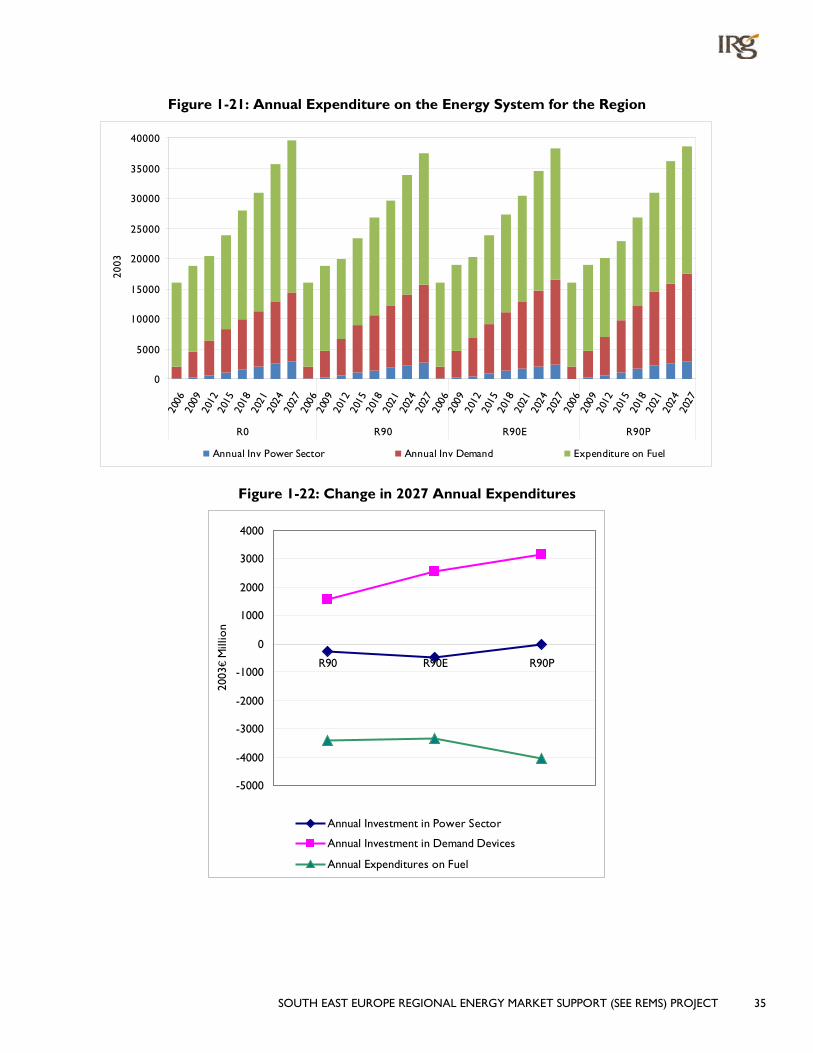

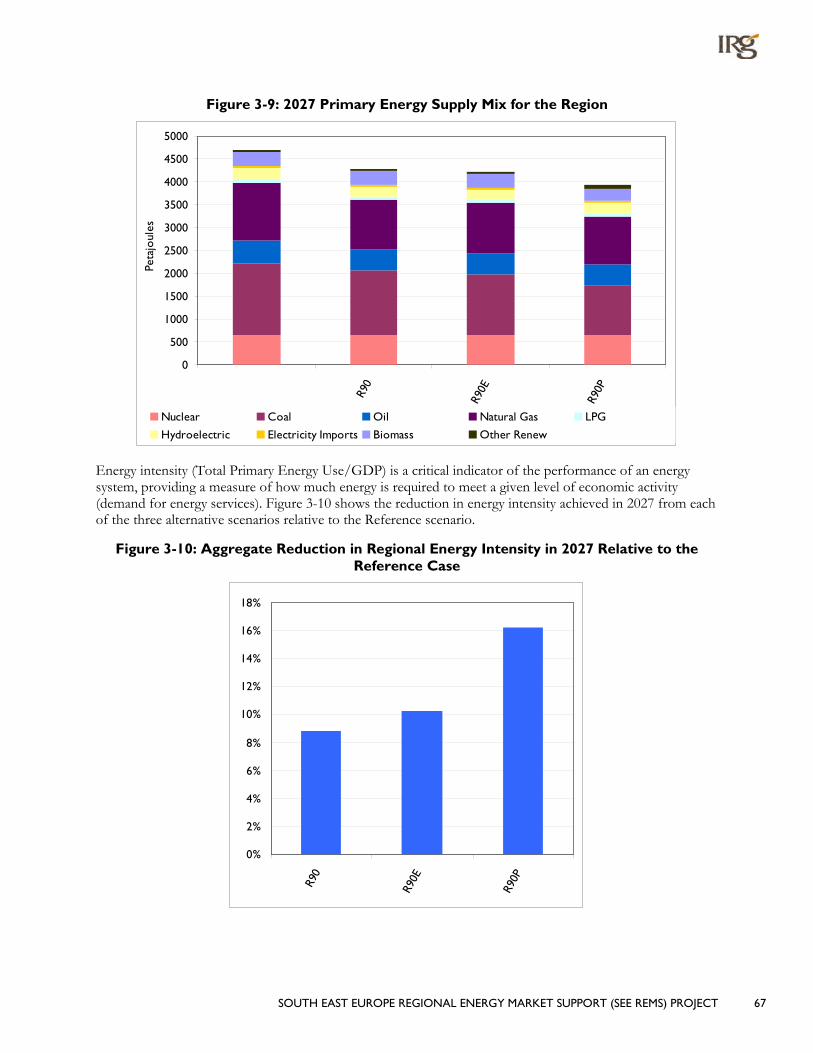

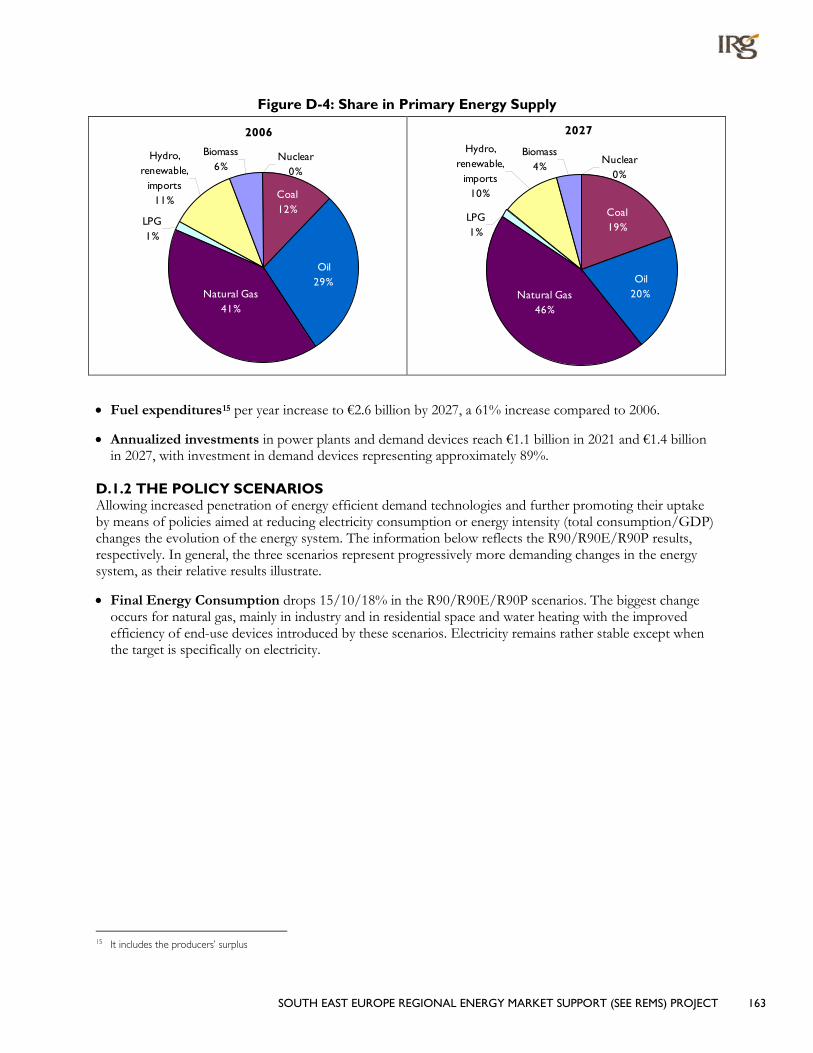

Figure ES-1 shows the decrease in regional energy intensity in 2027 achieved through implementation of the energy efficiency policies described above compared to the Reference case. At the same time, the alternate scenarios lower the total energy system cost (including investments in new capacity and demand devices, expenditure on fuel, transmission and distribution infrastructure, etc., to the extent represented in the models) by almost 2% for the Promoting Energy Efficiency scenario (R90) and by 1.2% for the Reducing Electricity Consumption (R90E) scenario. For the Reducing Energy Intensity (R90P) scenario, the total energy system cost approximates that of the Reference scenario, indicating the level of improvement that can be achieved at costs similar to those of the Reference scenario. Figure ES-2 shows that the overall cost of implementing the energy system improvements represented in these alternate scenarios is relatively small because the increased investments made in more efficient end-use technologies are offset by significant reductions in fuel expenditures and modest reductions in the level of new investments in the power sector. Further details of the assumptions, costs, and benefits of these scenarios are provided in subsequent sections of this report.

Figure ES-1: Aggregate Reduction in Regional Energy Intensity in 2027 Relative to the

Reference Case

Figure ES-2: Change in 2027 Annual Expenditures

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

R90

R90E

R90P

-5000

-4000

-3000

-2000

-1000

0

1000

2000

3000

4000

R90 R90E R90P

2003

€ M

illio

n

Annual Investment in Power Sector

Annual Investment in Demand Devices

Annual Expenditures on Fuel

4 SOUTH EAST EUROPE REGIONAL ENERGY MARKET SUPPORT (SEE REMS) PROJECT

REPORT ORGANIZATION • Section 1 presents the main highlights of the analysis.

• Section 2 summarizes the approach, data and key assumptions used to develop the Reference scenario and presents the aggregate regional results for the 8 national models. Examination of the Reference scenario provides insights into the current dynamics of the region’s national energy systems and lays the foundation for examining the critical resource, technology and end-use demand issues facing the region over the next 25 years.

• Section 3 presents a regional analysis of the alternate scenarios as compared to the Reference scenario, analyzing the aggregate picture arising from promoting energy efficiency in the region in terms of energy and cost savings, investment requirements, and technology changes.

• Appendices 1 through 8 contain the individual country results developed by the national experts and the USAID consultants. Each Section of Appendix 1 provides additional country level details for the Reference and three alternate scenarios, as well as other selected country scenarios.

SOUTH EAST EUROPE REGIONAL ENERGY MARKET SUPPORT (SEE REMS) PROJECT 5

LIST OF TABLES

Table ES-1. Benefits Arising from Increased Energy Efficiency ............................................................................... 3 Table 1-1: SEE-REDP Participating Institutions ......................................................................................................... 19 Table 1-2: Efficiency Promotion Scenarios Examined ............................................................................................. 28 Table 1-3. Benefits Arising from Increased Energy Efficiency ............................................................................... 36 Table 2-1: Key Demand Drivers .................................................................................................................................. 39 Table 2-2: SEE-REDP Example Power Plant Characteristics ................................................................................. 45 Table 2-3: Share of Final Energy in 2027, ordered by % of Total for the Region ............................................ 50 Table 3-1: Efficiency Improvement Scenarios Examined ........................................................................................ 59 Table A-1: Sector Fuel Price “Mark-Ups” (M2003€/PJ) ......................................................................................... 85

Table A-2: Upper Limits on Domestic Resource Supply (PJ)................................................................................ 87 Table A-3: Energy Intensity (PJ/GDP) ....................................................................................................................... 101 Table B-1: Demand Elasticities ................................................................................................................................... 111 Table B-2: Growth Rate of Agricultural Production ............................................................................................. 112 Table B-3: Sector Fuel Price “Mark-Ups” (M2003€/PJ) ........................................................................................ 113

Table B-4: Upper limits on Domestic Resource Supply (PJ) ............................................................................... 113 Table B-5: Energy Intensity (PJ/GDP) ........................................................................................................................ 126 Table C-1: Demand Elasticities ................................................................................................................................... 137 Table C-2: Sector Fuel Price “Mark-Ups” (M2003€/PJ) ....................................................................................... 138

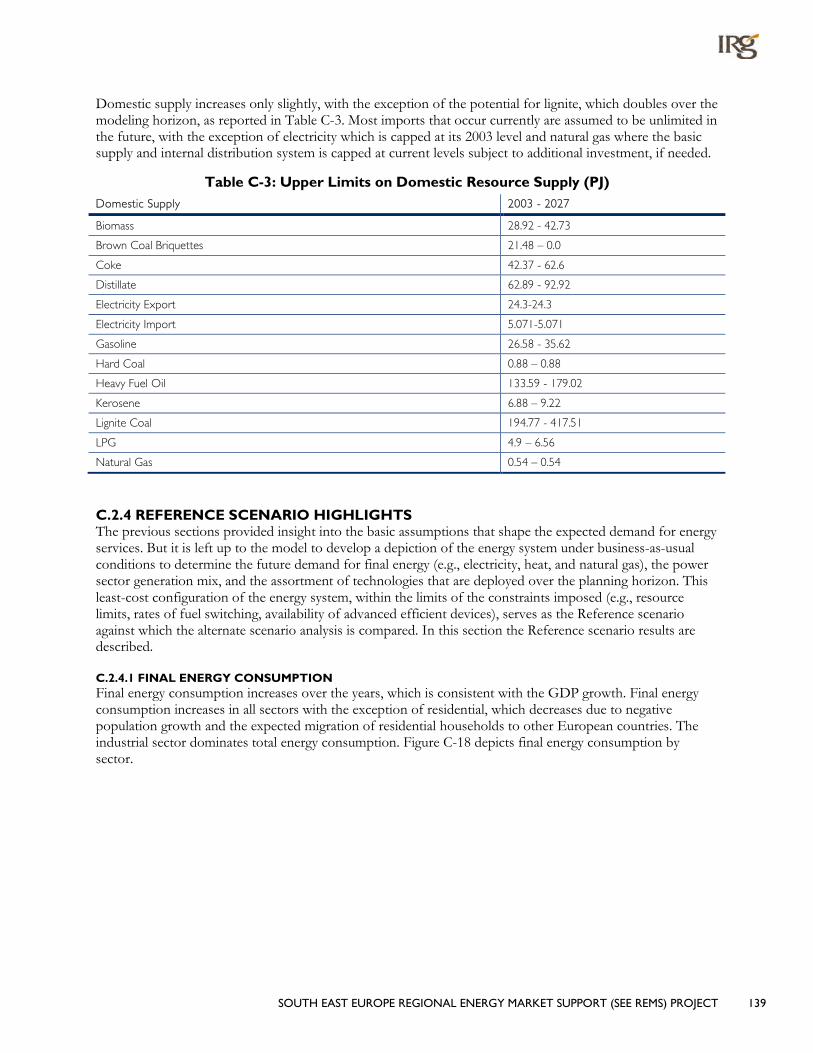

Table C-3: Upper Limits on Domestic Resource Supply (PJ) ............................................................................. 139 Table C-4: Percentage Change from R0 .................................................................................................................. 154 Table D-1: Demand Elasticities .................................................................................................................................. 171 Table D-2: Upper Limits on Domestic Resource .................................................................................................. 172 Table D-3: Sector Fuel Distribution Cost (M2003€/PJ) ....................................................................................... 173 Table D-4: Energy Intensity (PJ/GDP) ....................................................................................................................... 184 Table D-5: New Potential for Renewables in the Electricity Sector (GW) .................................................... 186 Table E-1: Sector Fuel Price “Mark-ups” (M2003€/PJ) ......................................................................................... 200

Table E-2: Upper Limits on Domestic Resource Supply (PJ) .............................................................................. 201 Table E-3: Energy Intensity (PJ/GDP) ........................................................................................................................ 216 Table F-6: Demand Elasticities .................................................................................................................................... 228 Table F-7: Upper Limits on Domestic Resource ................................................................................................... 229 Table F-8: Sector Fuel Distribution Cost (M2003€/PJ) ........................................................................................ 229

6 SOUTH EAST EUROPE REGIONAL ENERGY MARKET SUPPORT (SEE REMS) PROJECT

Table F-9: Energy Intensity (PJ/GDP) ........................................................................................................................ 241 Table G-1: Demand Elasticities................................................................................................................................... 253 Table G-2: Sector Fuel Price “Mark-Ups” (M2003€/PJ) ....................................................................................... 254

Table G-3: Upper Limits on Domestic Resource Supply (PJ) ............................................................................. 255 Table G-4: Energy Intensity (PJ/GDP) ....................................................................................................................... 268 Table H-1: Demand Elasticities ................................................................................................................................... 279 Table H-2: Sector Fuel Price “Mark-Ups” (M2003€/PJ) ....................................................................................... 281

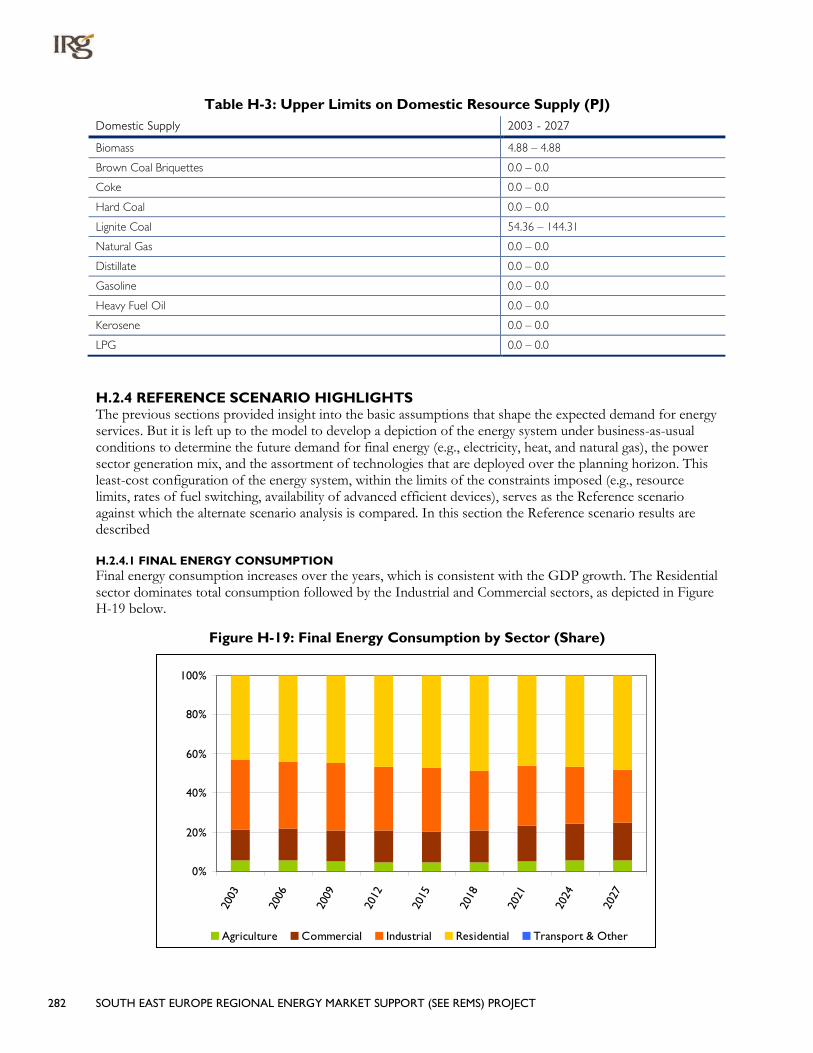

Table H-3: Upper Limits on Domestic Resource Supply (PJ) ............................................................................. 282 Table H-4: Percentage Change from R0 .................................................................................................................. 296

SOUTH EAST EUROPE REGIONAL ENERGY MARKET SUPPORT (SEE REMS) PROJECT 7

LIST OF FIGURES

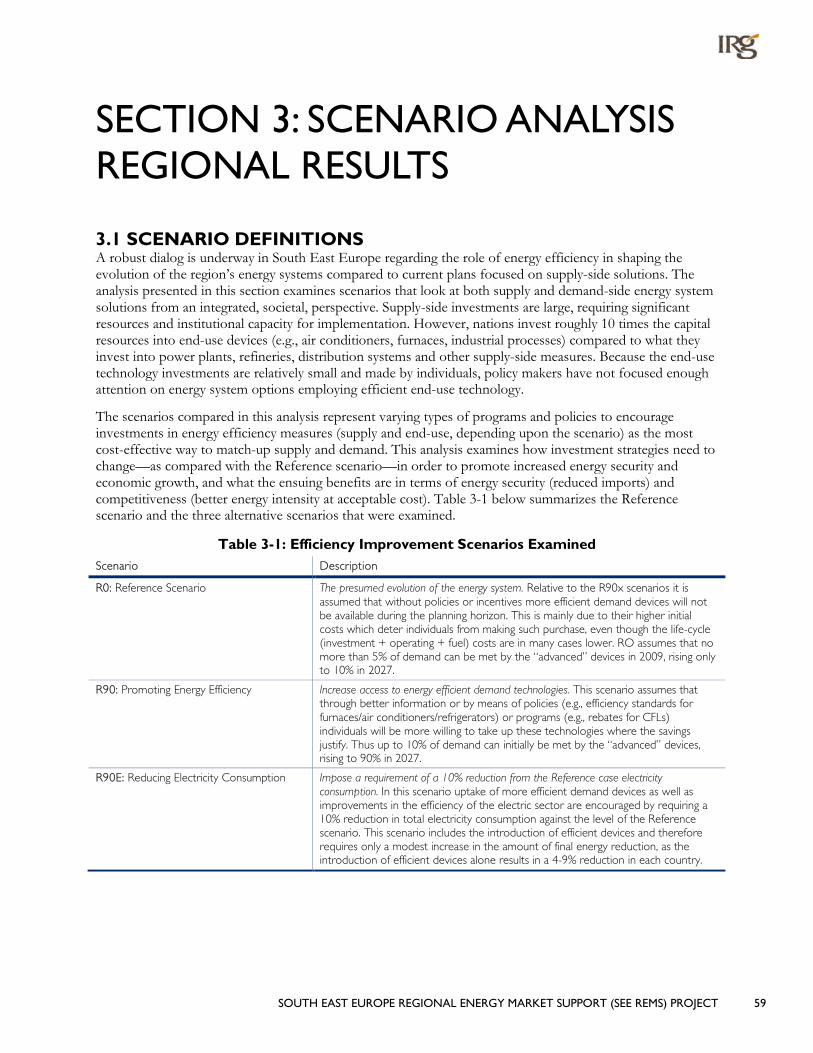

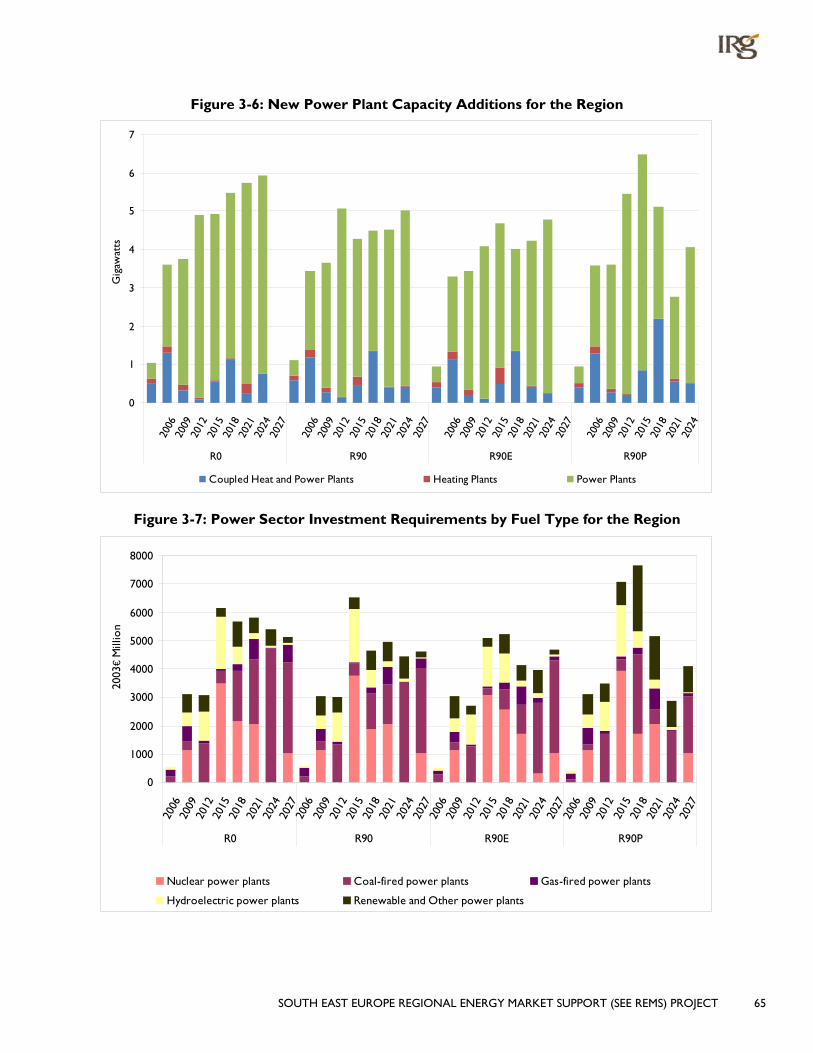

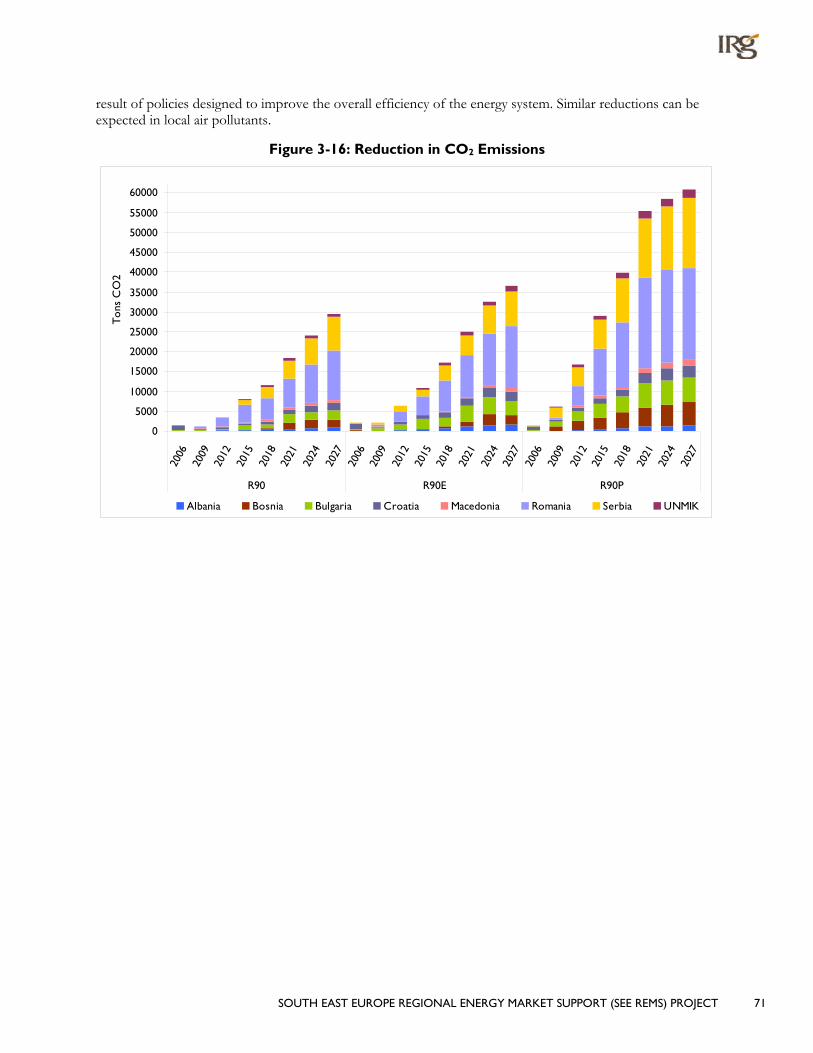

Figure ES-1: Aggregate Reduction in Regional Energy Intensity in 2027 Relative to the Reference Case ... 3 Figure ES-2: Change in 2027 Annual Expenditures .................................................................................................... 3 Figure 1-1: SEE-REDP Organizational Framework .................................................................................................. 18 Figure 1-2: Aggregate Final Energy Consumption by Fuel Type for the Region ............................................... 23 Figure 1-3: Aggregate Final Energy Consumption by Sector for the Region ..................................................... 24 Figure 1-4: Share of Cumulative Final Energy Consumption by Country .......................................................... 24 Figure 1-5: Aggregate Electricity Generation by Fuel Type for the Region ....................................................... 25 Figure 1-6: Electricity Generation for the Region .................................................................................................... 25 Figure 1-7: Aggregate Primary Energy Use for the Region .................................................................................... 26 Figure 1-8: Composition of Energy Supply by Country in 2003 ........................................................................... 27 Figure 1-9: Total Discounted Energy System Cost for the Region ..................................................................... 27 Figure 1-10: Aggregate Annual Energy System Expenditure for the Region ..................................................... 28 Figure 1-11: Aggregate Savings in Total Final Energy Demand by Sector for the Region .............................. 29 Figure 1-12: Aggregate Savings in Total Final Energy Demand by Country....................................................... 30 Figure 1-13: Aggregate Saving in Total Electricity Consumption for the Region ............................................. 30 Figure 1-14: Aggregate Electricity Generation by Fuel Type for the Region .................................................... 31 Figure 1-15: 2027 Electricity Generation Mix by Fuel Type for the Region ...................................................... 31 Figure 1-16: Aggregate Total Primary Energy Supply for the Region .................................................................. 32 Figure 1-17: Reduction in Energy Intensity by Country ......................................................................................... 32 Figure 1-18: Level of Import for the Region ............................................................................................................. 33 Figure 1-19: Drop in Imports’ Share of Total Primary Energy by Country ....................................................... 33 Figure 1-20: Aggregate Total Discounted System Cost for the Region ............................................................. 34 Figure 1-21: Annual Expenditure on the Energy System for the Region ............................................................ 35 Figure 1-22: Change in 2027 Annual Expenditures ................................................................................................. 35 Figure 2-1: Evolution of the Demand for Energy Services by Sector .................................................................. 41 Figure 2-2: NEEDS Import Energy Price Assumptions ........................................................................................... 42 Figure 2-3: Final Energy Demand by Sector .............................................................................................................. 47 Figure 2-4: 2003/2027 Share of Final Energy Demand by Sub-sector ................................................................. 48 Figure 2-5: Final Energy Demand by Fuel Type ........................................................................................................ 51 Figure 2-6: Final Energy Demand by Country ........................................................................................................... 51 Figure 2-7: Electricity Generation by Fuel Form by Country ............................................................................... 52

8 SOUTH EAST EUROPE REGIONAL ENERGY MARKET SUPPORT (SEE REMS) PROJECT

Figure 2-8: Fuel Input to Power Generation ............................................................................................................. 52 Figure 2-9: Electric Generation (plus Imports) by Country .................................................................................. 53 Figure 2-10: Percent 2003 Energy Supply Share by Fuel Type .............................................................................. 54 Figure 2-11: Percent 2003 Energy Supply Share by Country ................................................................................ 54 Figure 2-12: Composition of Energy Supply by Country in 2003 ........................................................................ 55 Figure 2-13: Regional Primary Energy Supply ............................................................................................................ 56 Figure 2-14: Primary Energy Supply by Country ...................................................................................................... 57 Figure 2-15: Annual Investment and Operating Costs (excluding fuel) .............................................................. 57 Figure 2-16: Annual Energy System Costs ................................................................................................................. 58 Figure 3-1: Final Energy Saving by Subsector for the Region ................................................................................ 61 Figure 3-2: Final Energy Savings from “EE” Policy by Demand Sector for the Region .................................... 62 Figure 3-3: Total Electricity Saving from “EE” Policy for the Region .................................................................. 62 Figure 3-4: Electricity Generation by Fuel Type for the Region ........................................................................... 63 Figure 3-5: 2027 Electricity Generation Mix by Fuel Type for the Region ........................................................ 64 Figure 3-6: New Power Plant Capacity Additions for the Region ....................................................................... 65 Figure 3-7: Power Sector Investment Requirements by Fuel Type for the Region ......................................... 65 Figure 3-8: Total Primary Energy Supply for the Region ........................................................................................ 66 Figure 3-9: 2027 Primary Energy Supply Mix for the Region ................................................................................ 67 Figure 3-10: Aggregate Reduction in Regional Energy Intensity in 2027 Relative to the Reference Case . 67 Figure 3-11: Level of Import for the Region ............................................................................................................. 68 Figure 3-12: Reduction of Imports by Fuel for the Region .................................................................................... 68 Figure 3-13: Aggregate Total Discounted System Cost for the Region ............................................................. 69 Figure 3-14: Annual Expenditure on the Energy System for the Region ............................................................ 70 Figure 3-15: Change in 2027 Annual Expenditures ................................................................................................. 70 Figure 3-16: Reduction in CO2 Emissions .................................................................................................................. 71 Figure A-1: Percent of Final Energy Consumption by Fuel Type ......................................................................... 73 Figure A-2: Percent of Final Energy Consumption by Sector ............................................................................... 74 Figure A-3: Percent Electricity Generation by Fuel Type ...................................................................................... 74 Figure A-4: Percent of Total Energy Supply .............................................................................................................. 75 Figure A-5: 2027 Total Energy Supply ........................................................................................................................ 76 Figure A-6: 2027 Electricity Generation Mix by Fuel .............................................................................................. 76 Figure A-7: 2027 Final Energy Consumption ............................................................................................................ 77 Figure A-8: Aggregate Total Discounted System Cost ........................................................................................... 78 Figure A-9: Change in 2027 Annual Expenditures ................................................................................................... 78

SOUTH EAST EUROPE REGIONAL ENERGY MARKET SUPPORT (SEE REMS) PROJECT 9

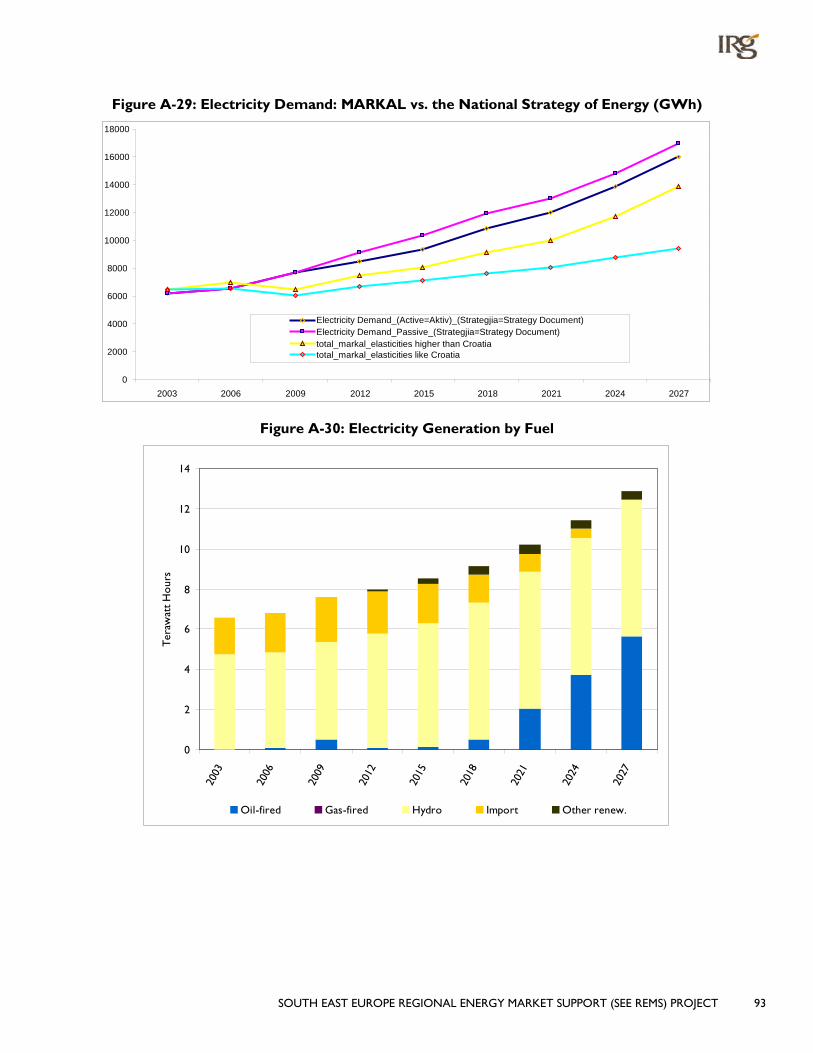

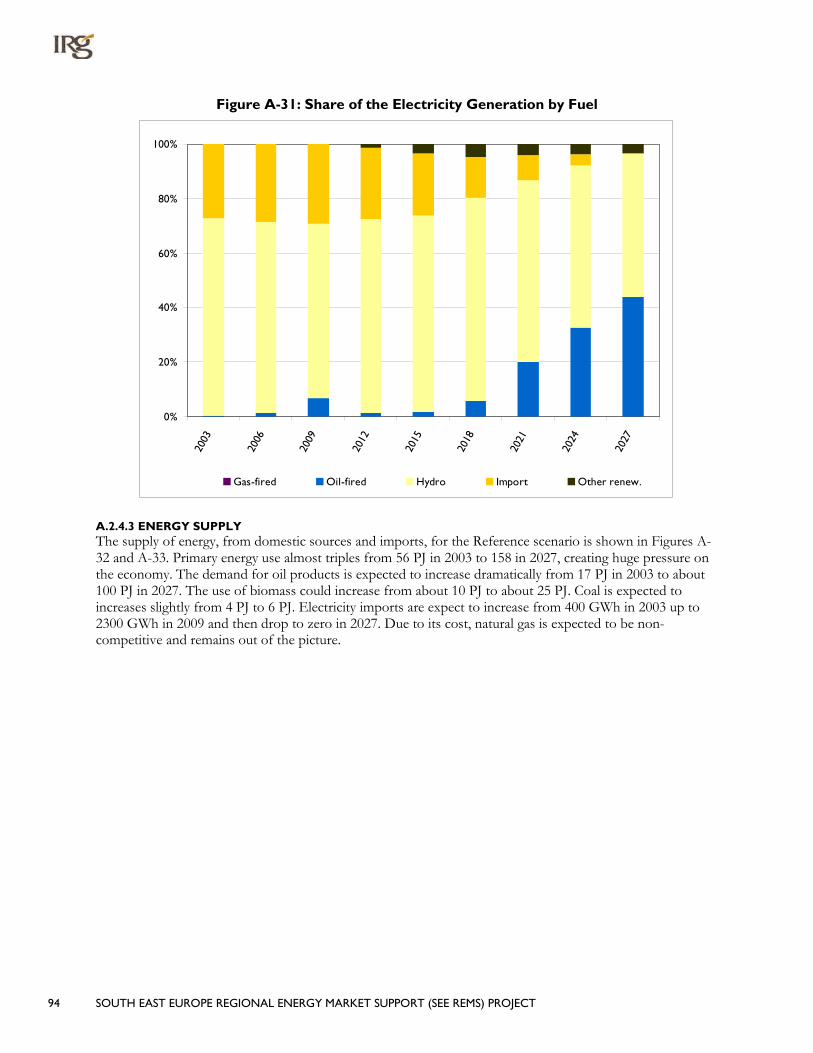

Figure A-10: Trend of Population and its Growth Rate ......................................................................................... 79 Figure A-11: Trend of Households and Number of Persons per Household ................................................... 79 Figure A-12: Projection of Total GDP and its Growth Rate ................................................................................ 80 Figure A-13: Sectoral Contributions to GDP ........................................................................................................... 80 Figure A-14: Projection of Energy Service Demand from Each Sector (Useful Energy)................................. 81 Figure A-15: Composition of Residential Dwellings over Time ........................................................................... 82 Figure A-16: Residential Demand for Energy Services (Useful Energy) .............................................................. 82 Figure A-17: Commercial Demand for Energy Services (Useful Energy) ........................................................... 83 Figure A-18: Present Contribution of Industrial Sub-Sectors to GDP (MEURO - 2003) .............................. 84 Figure A-19: Projections of the Industrial GDP (€2003 million) in 2027 ........................................................... 84 Figure A-20: Industrial Demand for Energy Services (Useful Energy) ................................................................. 85 Figure A-21: Energy Prices Based on the EU NEEDS Project............................................................................... 86 Figure A-22: Final Energy Consumption by Sector .................................................................................................. 88 Figure A-23: Final Energy Consumption by Sector (Share) ................................................................................... 88 Figure A-24: Final Energy Consumption by Fuel ...................................................................................................... 89 Figure A-25: Final Energy Consumption – Residential ............................................................................................ 90 Figure A-26: Final Energy Consumption – Commercial ......................................................................................... 90 Figure A-27: Final Energy Consumption – Industry ................................................................................................. 91 Figure A-28: Final Energy Consumption – Agriculture ........................................................................................... 92 Figure A-29: Electricity Demand: MARKAL vs. the National Strategy of Energy (GWh) .............................. 93 Figure A-30: Electricity Generation by Fuel .............................................................................................................. 93 Figure A-31: Share of the Electricity Generation by Fuel ...................................................................................... 94 Figure A-32: Energy Supply by Type............................................................................................................................ 95 Figure A-33: Energy Supply by Type (Shares) ........................................................................................................... 95 Figure A-34: Final Energy Consumption by Fuel ...................................................................................................... 96 Figure A-35: Savings in Final Energy by Sector ......................................................................................................... 97 Figure A-36: Electricity Generation by Fuel .............................................................................................................. 98 Figure A-37: Savings in Electricity Generation .......................................................................................................... 98 Figure A-38: Investments in New (and Refurbished) Power Plants .................................................................... 99 Figure A-39: Supply of Energy ..................................................................................................................................... 100 Figure A-40: Imports Share of Total Supply ............................................................................................................ 100 Figure A-41: Annual Energy System Expenditures ................................................................................................. 101 Figure B-1: Percent of Final Energy Consumption by Fuel Type ........................................................................ 102 Figure B-2: Percent of Final Energy Consumption by Sector .............................................................................. 103

10 SOUTH EAST EUROPE REGIONAL ENERGY MARKET SUPPORT (SEE REMS) PROJECT

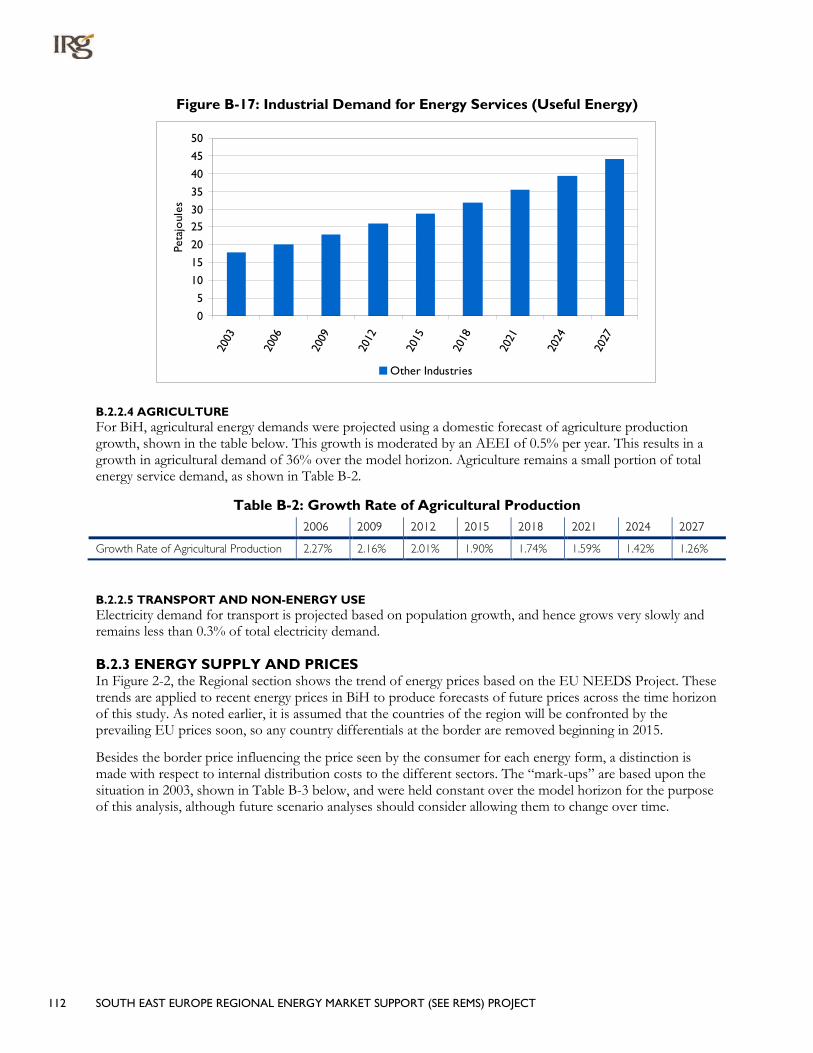

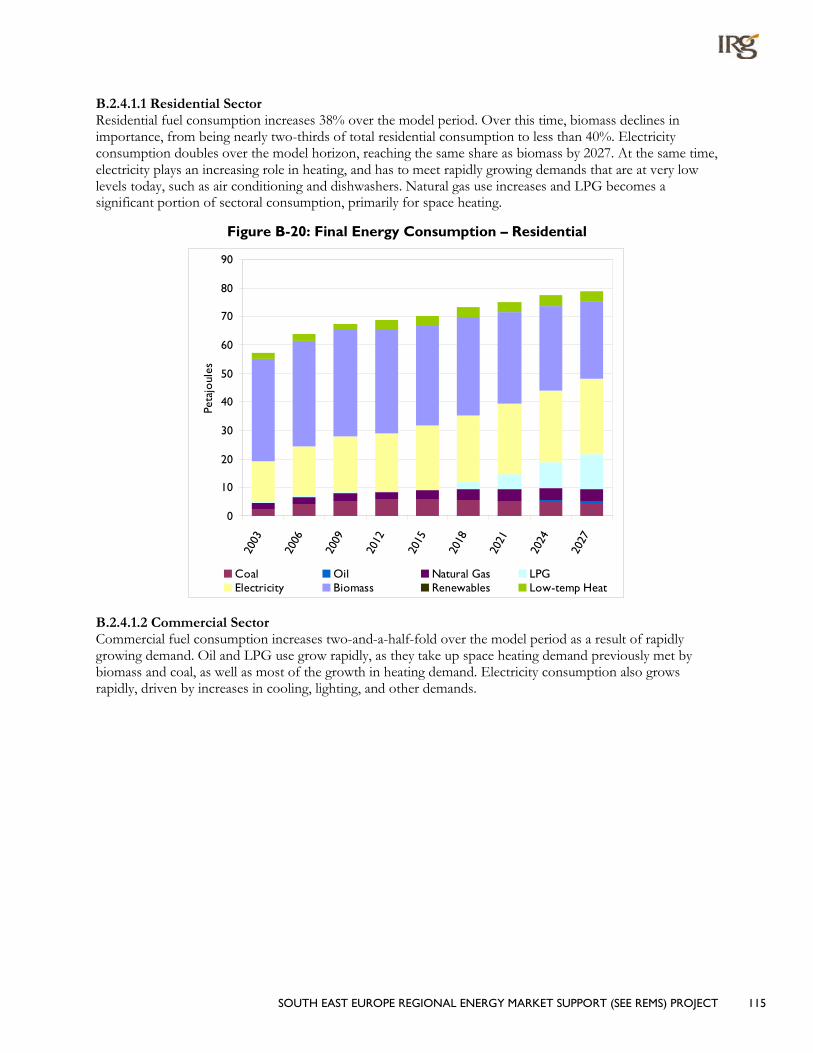

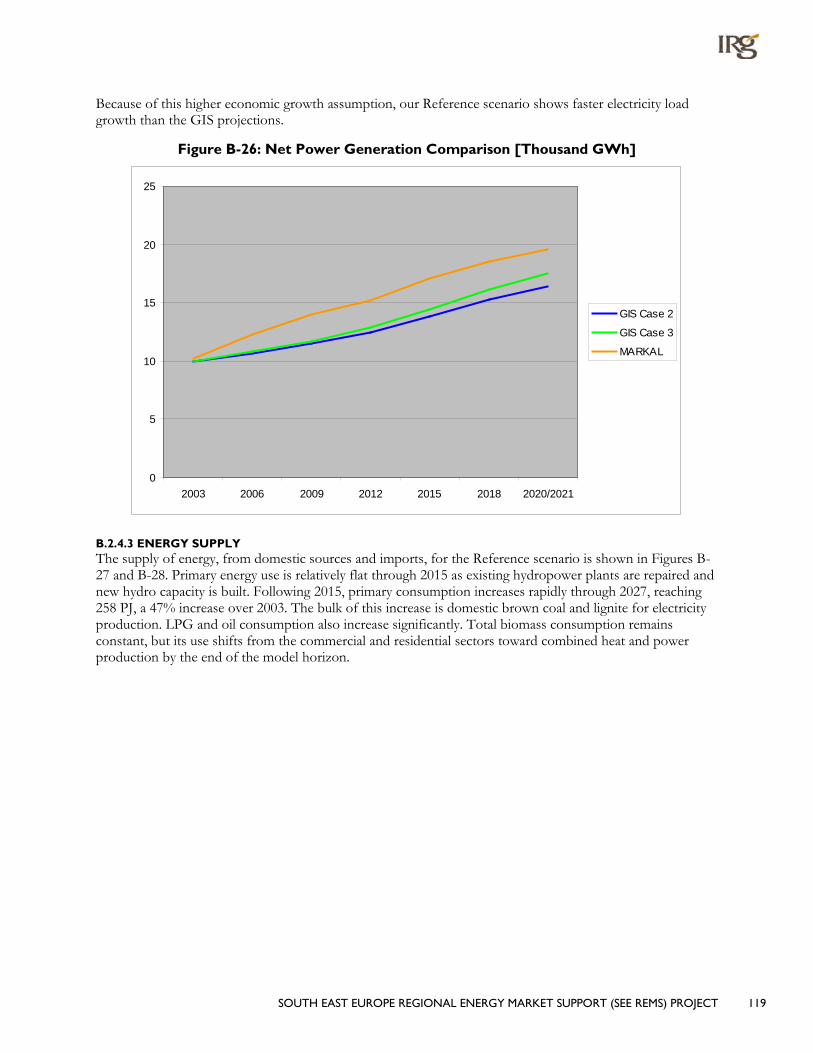

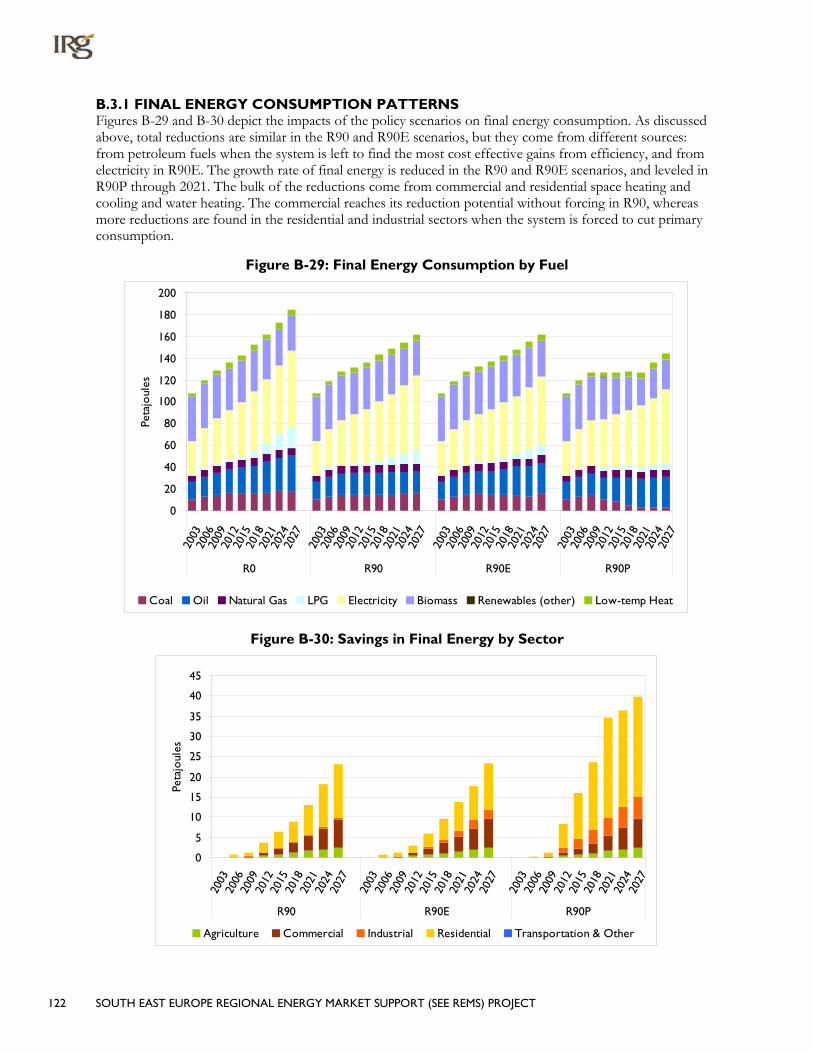

Figure B-3: Percent Electricity Generation by Fuel Type ..................................................................................... 103 Figure B-4: Percent of Total Energy Supply ............................................................................................................. 104 Figure B-5: Final Energy Consumption ..................................................................................................................... 105 Figure B-6: 2027 Electricity Generation Mix by Fuel Type .................................................................................. 105 Figure B-7: Total Energy Supply ................................................................................................................................. 106 Figure B-8: Aggregate Total Discounted System Cost ......................................................................................... 107 Figure B-9: Change in 2027 Annual Expenditures.................................................................................................. 107 Figure B-10: Trend of Population and its Growth Rate ....................................................................................... 108 Figure B-11: Trend of Households and Number of Persons per Household ................................................. 108 Figure B-12: GDP and GDP Growth Rate ............................................................................................................... 109 Figure B-13: Projection of Energy Service Demand for each Sector ................................................................ 109 Figure B-14: Composition of Residential Dwellings over Time.......................................................................... 110 Figure B-15: Residential Demand for Energy Services (Useful Energy) ............................................................ 110 Figure B-16: Commercial Demand for Energy Services (Useful Energy) ......................................................... 111 Figure B-17: Industrial Demand for Energy Services (Useful Energy) ............................................................... 112 Figure B-18: Final Energy Consumption by Fuel ..................................................................................................... 114 Figure B-19: Final Energy Consumption by Sector ................................................................................................ 114 Figure B-20: Final Energy Consumption – Residential .......................................................................................... 115 Figure B-21: Final Energy Consumption – Commercial ....................................................................................... 116 Figure B-22: Final Energy Consumption – Industry ............................................................................................... 116 Figure B-23: Final Energy Consumption – Agriculture ......................................................................................... 117 Figure B-24: Electricity Generation by Fuel ............................................................................................................. 118 Figure B-25: Share of the Electricity Generation by Fuel ..................................................................................... 118 Figure B-26: Net Power Generation Comparison [Thousand GWh] .............................................................. 119 Figure B-27: Energy Supply by Type .......................................................................................................................... 120 Figure B-28: Energy Supply by Type (Shares) .......................................................................................................... 120 Figure B-29: Final Energy Consumption by Fuel ..................................................................................................... 122 Figure B-30: Savings in Final Energy by Sector ........................................................................................................ 122 Figure B-31: Electricity Generation by Fuel ............................................................................................................. 123 Figure B-32: Savings in Electricity Generation ........................................................................................................ 123 Figure B-33: Investments in New (and Refurbished) Power Plants ................................................................... 124 Figure B-34: Supply of Energy ..................................................................................................................................... 125 Figure B-35: Total Imports .......................................................................................................................................... 125 Figure B-36: Total Discounted Energy System ....................................................................................................... 126

SOUTH EAST EUROPE REGIONAL ENERGY MARKET SUPPORT (SEE REMS) PROJECT 11

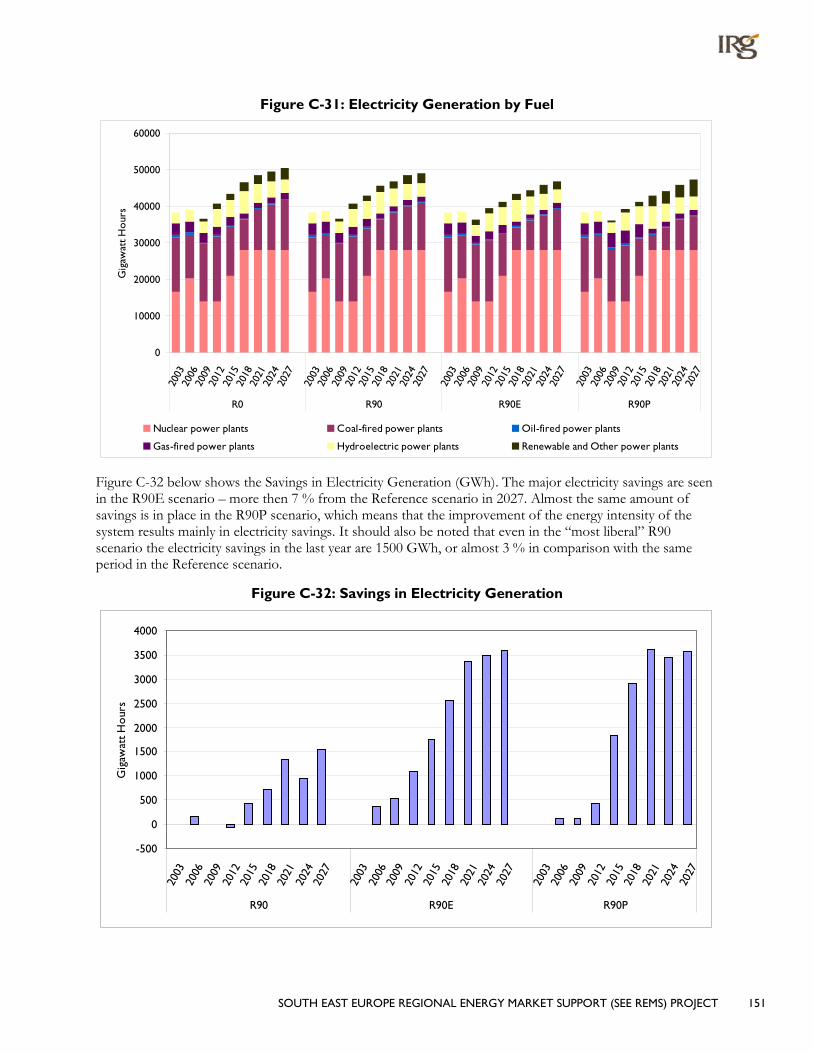

Figure B-37: Annual Energy System Expenditures ................................................................................................. 127 Figure C-1: End-Use Fuel Consumption .................................................................................................................. 128 Figure C-2: Energy Consumption by Sector ........................................................................................................... 129 Figure C-3: Electricity Generation ............................................................................................................................. 129 Figure C-4: Primary Energy Use ................................................................................................................................. 130 Figure C-5: End-Use Fuel Consumption in 2027 ................................................................................................... 131 Figure C-6: Electric Generation by Power Plant Type in 2027 .......................................................................... 131 Figure C-7: Primary Energy Use in 2027 .................................................................................................................. 132 Figure C-8: Total Discounted System Cost ............................................................................................................ 133 Figure C-9: Change in 2027 Expenditures Relative to Reference ...................................................................... 133 Figure C-10: Trend of Population and its Growth Rate ....................................................................................... 134 Figure C-11: Trend of Households and Number of Persons per Household ................................................. 134 Figure C-12: Forecast of Total GDP and its Growth Rate .................................................................................. 135 Figure C-13: Forecast of Energy Service Demand from each Sector ............................................................... 135 Figure C-14: Composition of Residential Dwellings over Time ......................................................................... 136 Figure C-15: Residential Demand for Energy Services (Useful Energy) ........................................................... 136 Figure C-16: Commercial Demand for Energy Services (Useful Energy) ......................................................... 137 Figure C-17: Industrial Demand for Energy Services (Useful Energy) .............................................................. 138 Figure C-18: Final Energy Consumption by Sector Share .................................................................................... 140 Figure C-19: Final Energy Consumption by Fuel .................................................................................................... 141 Figure C-20: Final Energy Consumption - Residential .......................................................................................... 142 Figure C-21: Final Energy Consumption - Commercial ........................................................................................ 143 Figure C-22: Final Energy Consumption - Industry ............................................................................................... 143 Figure C-23: Final Energy Consumption - Agriculture ......................................................................................... 144 Figure C-24: Forecast of Electricity Demand .......................................................................................................... 145 Figure C-25: Electricity Generation by Fuel ............................................................................................................ 146 Figure C-26: Share of the Electricity Generation by Fuel .................................................................................... 146 Figure C-27: Energy Supply by Type ......................................................................................................................... 147 Figure C-28: Energy Supply by Type (Shares) ......................................................................................................... 147 Figure C-29: Final Energy Consumption by Fuel .................................................................................................... 149 Figure C-30: Savings in Final Energy by Sector ....................................................................................................... 150 Figure C-31: Electricity Generation by Fuel ............................................................................................................ 151 Figure C-32: Savings in Electricity Generation ....................................................................................................... 151 Figure C-33: Investments in New (and Refurbished) Power Plants .................................................................. 152

12 SOUTH EAST EUROPE REGIONAL ENERGY MARKET SUPPORT (SEE REMS) PROJECT

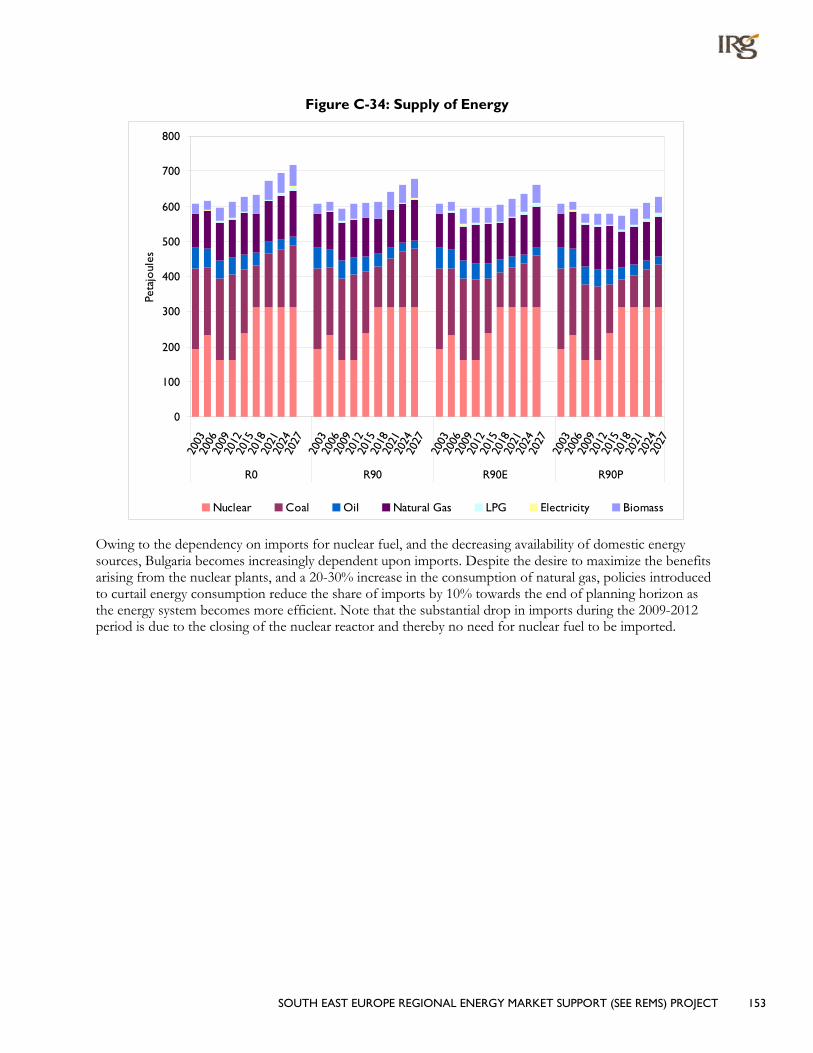

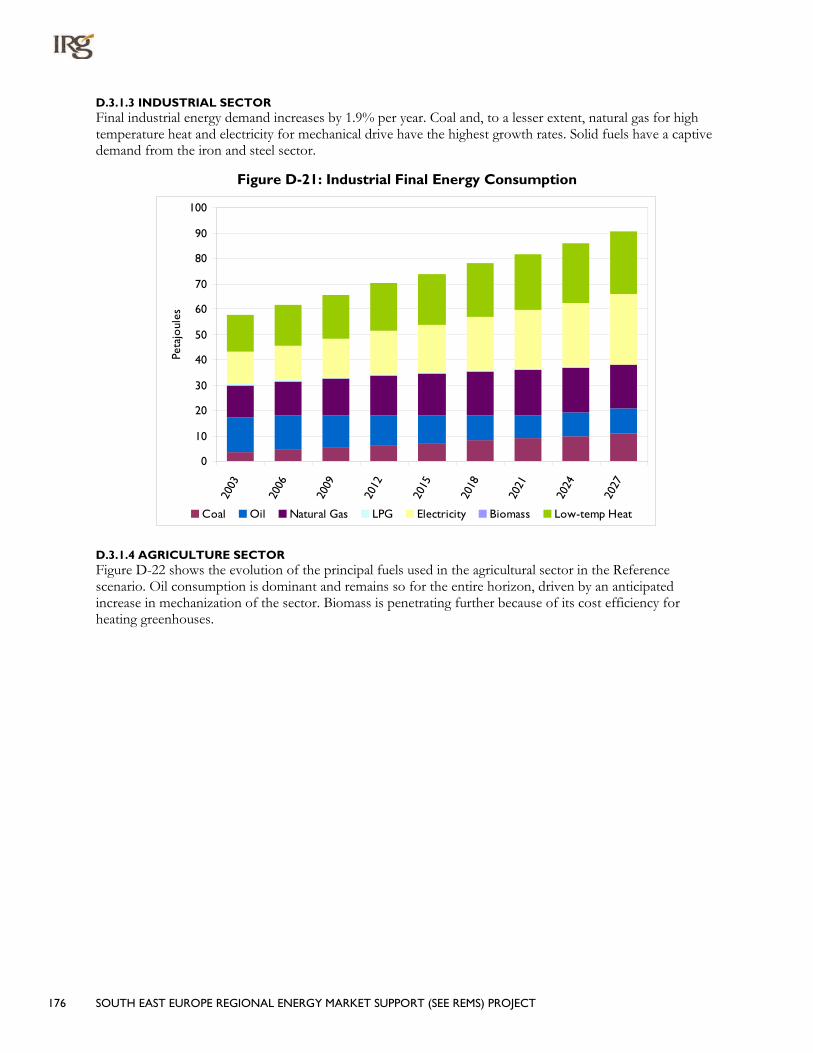

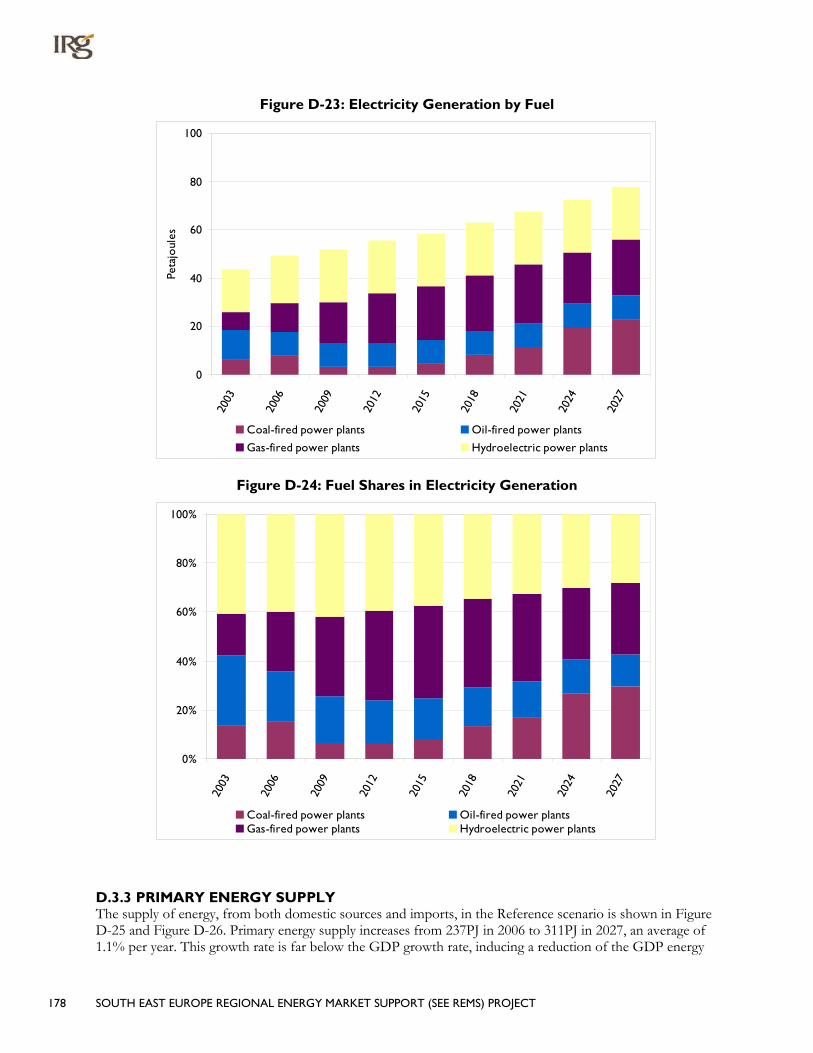

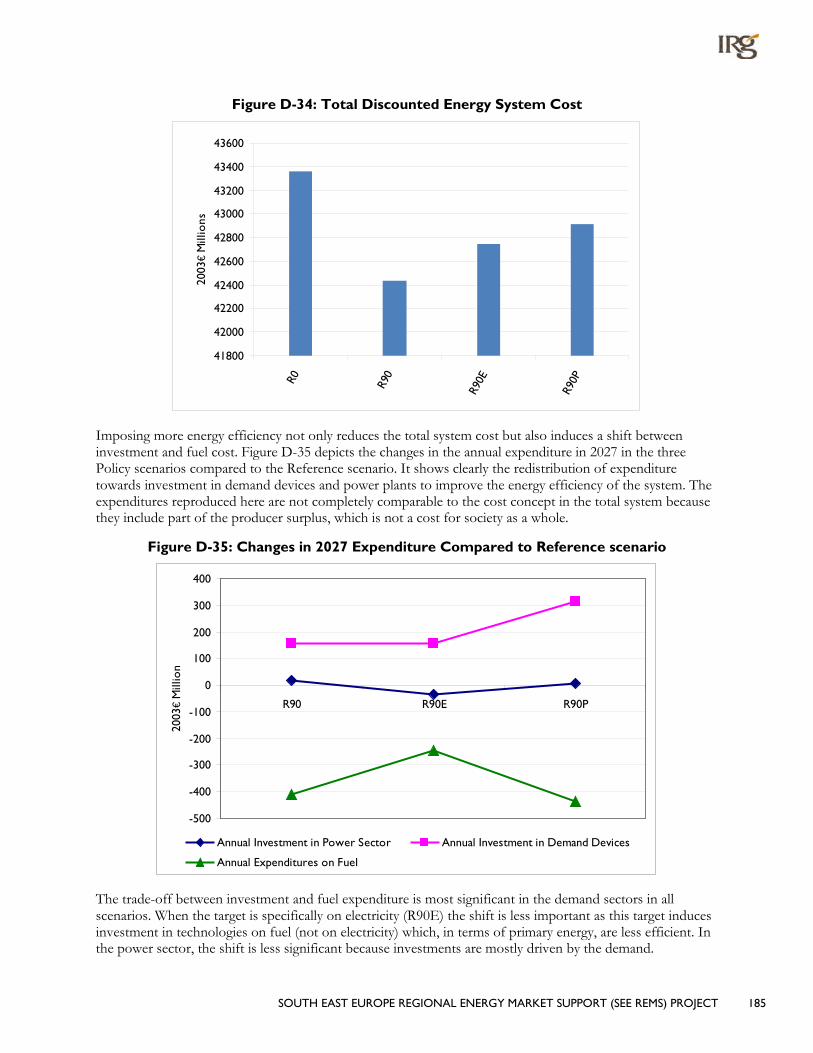

Figure C-34: Supply of Energy .................................................................................................................................... 153 Figure C-35: Total Imports .......................................................................................................................................... 154 Figure C-36: Total Discounted Energy System Cost ............................................................................................ 155 Figure C-37: Annual Energy System Expenditures ................................................................................................. 155 Figure C-38: Electricity Generation by Fuels .......................................................................................................... 156 Figure C-39: R0 2009 Electricity Generation by Fuels ......................................................................................... 157 Figure C-40: R0 2027 Electricity Generation by Fuels ......................................................................................... 157 Figure C-41: R0R 2009 Electricity Generation by Fuels ....................................................................................... 158 Figure C-42: R0R 2027 Electricity Generation by Fuels ....................................................................................... 158 Figure C-43: Primary Energy Supply .......................................................................................................................... 159 Figure C-44: CO2 Emissions ........................................................................................................................................ 160 Figure D-1: Fuel Shares in Final Energy Consumption .......................................................................................... 161 Figure D-2: Sector Shares in Final Energy Consumption ..................................................................................... 161 Figure D-3: Share in Electricity Generation ............................................................................................................ 162 Figure D-4: Share in Primary Energy Supply ............................................................................................................ 163 Figure D-5: Final Energy Consumption in 2027...................................................................................................... 164 Figure D-6: Electricity Generation Mix by Fuel Type in 2027 ............................................................................ 164 Figure D-7: Primary Energy Supply in 2027 ............................................................................................................. 165 Figure D-8: Total Discounted System Cost ............................................................................................................ 166 Figure D-9: Trend of Population and its Growth Rate ......................................................................................... 167 Figure D-10: Trend of Households and Number of Persons per Household ................................................ 167 Figure D-11: Projection of Total GDP and its Growth Rate .............................................................................. 168 Figure D-12: Energy Services Demand Projection ................................................................................................. 169 Figure D-13: Shares of Types of Residential Dwellings Over Time .................................................................. 169 Figure D-14: Residential Energy Service Demand (Useful Energy) .................................................................... 170 Figure D-15: Commercial Energy Service Demand (Useful Energy) ................................................................. 171 Figure D-16: Industrial Energy Service Demand (Useful Energy) ....................................................................... 172 Figure D-17: Final Energy Consumption by Sector ............................................................................................... 174 Figure D-18: Final Energy Consumption by Fuel .................................................................................................... 174 Figure D-19: Residential Final Energy Consumption ............................................................................................. 175 Figure D-20: Commercial Final Energy Consumption .......................................................................................... 175 Figure D-21: Industrial Final Energy Consumption ................................................................................................ 176 Figure D-22: Agriculture Final Energy Consumption ............................................................................................ 177 Figure D-23: Electricity Generation by Fuel ............................................................................................................ 178

SOUTH EAST EUROPE REGIONAL ENERGY MARKET SUPPORT (SEE REMS) PROJECT 13

Figure D-24: Fuel Shares in Electricity Generation ............................................................................................... 178 Figure D-25: Primary Energy Supply by Fuel ........................................................................................................... 179 Figure D-26: Fuel Shares in the Primary Energy Supply ....................................................................................... 179 Figure D-27: Final Energy Consumption by Fuel .................................................................................................... 181 Figure D-28: Savings in Final Energy by Sector ....................................................................................................... 181 Figure D-29: Electricity Generation by Fuel ............................................................................................................ 182 Figure D-30: Investment in Power Plants by Fuel Type ....................................................................................... 182 Figure D-31: Savings in Electricity Consumption ................................................................................................... 183 Figure D-32: Primary Supply of Energy..................................................................................................................... 183 Figure D-33: Change in Imports ................................................................................................................................. 184 Figure D-34: Total Discounted Energy System Cost ............................................................................................ 185 Figure D-35: Changes in 2027 Expenditure Compared to Reference scenario ............................................. 185 Figure D-36: Electricity Generation by Fuel ............................................................................................................ 187 Figure E-1: 2006/2027 Percent of Final Energy Consumption by Fuel Type ................................................... 189 Figure E-2: 2006/2027 Percent of Final Energy Consumption by Sector ......................................................... 190 Figure E-3: 2006/2027 Percent Electricity Generation by Fuel Type ................................................................ 190 Figure E-4: 2006/2027 Percent of Total Energy Supply ........................................................................................ 191 Figure E-5: 2027 Final Energy Consumption ........................................................................................................... 192 Figure E-6: 2027 Electricity Generation Mix by Fuel............................................................................................. 192 Figure E-7: 2027 Total Energy Supply ....................................................................................................................... 193 Figure E-8: Aggregate Total Discounted System Cost ......................................................................................... 194 Figure E-9: Change in 2027 Annual Expenditures .................................................................................................. 194 Figure E-10: Trend of Population and its Growth Rate........................................................................................ 195 Figure E-11: Trend of Households and Number of Persons per Household .................................................. 195 Figure E-12: Projection of Total GDP and its Growth Rate ............................................................................... 196 Figure E-13: Projection of Energy Service Demand from each Sector (Useful) ............................................. 196 Figure E-14: Composition of Residential Dwellings over Time .......................................................................... 197 Figure E-15: Residential Demand for Energy Services (Useful Energy) ............................................................ 197 Figure E-16: Commercial Demand for Energy Services (Useful Energy) .......................................................... 198 Figure E-17: Contribution of Industry Sub-Sectors to Total GDP .................................................................... 198 Figure E-18: Industrial Demand for Energy Services (Useful Energy) ............................................................... 199 Figure E-19: Energy Prices Based on the EU NEEDS Project ............................................................................. 200 Figure E-20: Final Energy Consumption by Sector ................................................................................................ 202 Figure E-21: Final Energy Consumption by Sector (Share) .................................................................................. 202

14 SOUTH EAST EUROPE REGIONAL ENERGY MARKET SUPPORT (SEE REMS) PROJECT