final report mrp nishant

TRANSCRIPT

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 1/29

A REPORT

ON

In-depth analysis and replenishment of supply

chain activities in retail grocery industry.

Submitted by:

Nishant 10bsp0030

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 2/29

A Report on

In-depth analysis and replenishment of supply

chain activities in retail grocery industry.

“The Report is submitted as a partial fulfilment of the

requirement of PGPM program of IBS AHMEDABAD”

Submitted to: Prof: Dhwanika Ahya

(Faculty Guide)

ICFAI Business School, Ahmedabad

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 3/29

Acknowledgment

These works being the imprints of many persons whose valuable assistance and

insightful suggestions have made this project a success.

If words are considered to be signs of gratitude then let these words convey the very

same.

I take this opportunity to thank our faculty guide, Prof. Dhwanika Ahya for encouraging

with her kind words of knowledge & wisdom and also co-operating with me.

I shall remain grateful to her hope her best wishes will guide me to come out with flying

colours on the path of honesty and harmony.

3

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 4/29

Table of Contents

Cover 1

Title Page 2

Acknowledgment 3

1. Introduction 5-17

1.1. Retail In India 5

1.1.1. Major developments and investments 5-6

1.1.2. Present Scenario 6-9

1.2. SWOT Analysis 9-11

2. Main Text 12-28

2.1.Retail Models in India:Current and Emerging 12-17

2.2. Analysis of Food Retail Sector 17-27

2.3. Challenges and Constraints 27

3. Recommendations: 28-29

4. Conclusion 29

4

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 5/29

Introduction:

Retail in India: Brief Overview

Indian retail business values at around US$ 550 billion as of now and about four per

cent of it accounts for the organised sector. A report by Boston Consulting Group (BCG)has revealed that the country's organised retail is estimated at US$ 28 billion with

around 7 per cent penetration. It is projected to become a US$ 260 billion business over

the next decade with around 21 per cent penetration.

Another report by Business Monitor International (BMI) suggests that enhancing middle and

upper class consumer base has set vast opportunities in India's tier-II & tier-III cities. The

greater availability of personal credit, improved mobility, better tourism et al, are all small, but

significant contributors to the growth of Indian retail industry. Also, more and more companies

are willing to invest in India due to significant growth forecasts on gross domestic product (GDP)

(BMI predicts average annual GDP growth of 7.6 per cent through 2015). Luxury Retail Soars High

Without wasting any time to react on the Indian Government's decision of allowing 100

per cent foreign direct investment (FDI) in single-brand retail, luxury brand retailers have

announced their expansion plans in Indian markets. Brands like Vertu, Christian

Loubotin, Armani Junior, among others, will open their exclusive stores at DLF Emporio

in early 2012, while brands like Van Laack and Diesel Black Gold will commence their

operations by January 2012 itself.

A report by CII-AT Kearney revealed that Luxury brands market in India grew at a

healthy 20 per cent during 2010 reaching a size of US$ 5.8 billion. It further stated thatthe Indian luxury market stood at a value of US$ 4.76 billion in 2009 and is anticipated

to be worth US$ 14.7 billion by 2015.

Where on one hand the luxury electronics and car segments registered a growth of over 35

per cent, fine dining grew by almost 40 per cent in 2010. Apparel and accessories, watches

and personal care witnessed a substantial growth rate, between 24-30 per cent.

Similarly, India has surpassed the US to become the third largest men's luxury jewellery

market in the world in 2011, stated the researcher Euromonitor International. The

researcher's study projected Indian men's jewellery market at Rs 954 crore (US$ 183.76

million) in terms of sales and made an anticipation for it to grow 36.4 per cent in 2012

5

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 6/29

Retail: Major Developments and Investments

After the US, Germany has also come up in full support of FDI in retail in India. Metro

AG, one of the prominent German retail chains, has shown intentions to venture in

Indian markets along with US' Wal-Mart and France's Carrefour.

Cumulative FDI inflows in single-brand retail trading during April 2000 to September2011 stood at US$ 44.45 million, according to the Department of Industrial Policy and

Promotion (DIPP). Certain developments and investments that took place on the Indian

retail canvas recently are discussed below-

Real estate major DLF's subsidiary DLF Brands has struck a deal with Chicago-

based Claire's Stores Inc to bring the latter to India and open its 75 stores over

2011-16. Claire's is a specialty retailer which targets young girls through over

3,000 stores globally.

French retail chain, Carrefour is on an expansion spree in India wherein it is

about to finalize lease deals across 10 to 12 sites in the country to open cash-and-carry (wholesale) outlets.

The world's largest retailer Wal-Mart will open an innovation lab in Bengaluru by the

end of 2011. The lab would be tasked to drive the US$ 422-billion company's next

generation innovations that impact shopping behavior among the customers.

US fast moving consumer good (FMCG) giant McCormick, that has recently

formed a joint venture (JV) with Indian basmati rice brand Kohinoor Foods,

intends to tap Indian packaged food industry and achieve sales of US$ 85 million

in the first year of operations in the country.

FMCG firm GSK Consumer Healthcare (GSKCH) has made a debut into Indianbreakfast cereal market by launching oats cereal under its flagship brand ‘Horlicks'. The

breakfast cereal market in India is currently dominated by PepsiCo and Kellogg's.

Oral and dental hygiene products manufacturer Colgate Palmolive has decided

to invest Rs 200 crore (US$ 38.52 million) to establish a greenfield facility at an

upcoming industrial estate in Sanand which is being developed by state-run

Gujarat Industrial Development Corporation (GIDC).

Retailing over Internet

Indian retailers and consumer durables companies are joining the web bandwagon with

India's online shopping industry registering phenomenal growth of almost 100 per centannually. India has more than 100 million internet users, out of which around half of

them are up for online purchases and the statistics is growing every year, says Google.

Furthermore, the Indian online retail industry would register annual growth rate of 35 per

cent to increase from current size of Rs 2, 000 crore (US$ 385 million) to Rs 7,000 crore

(US$ 1.35 billion) by 2015, according to a leading industry body.

6

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 7/29

The US$ 10 billion Indian e-commerce market is expanding exponentially (it grew 47 per

cent in 2011 to reach the present size) as rising internet penetration is making customers

buy more and more stuff online. Investors are also betting high in the industry; they poured

around US$ 200 million into Indian e-commerce start-ups in last couple of years.

Retail brands are expected to bring a great transformation in online space. Women'sapparel retail brand Biba and tyre brand Bridgestone have become available online

recently. Internet and Mobile Association of India (IAMAI) expects online advertising to

increase by 30-40 per cent in 2011-12 on back of increased internet usage by retailers

PRESENT SCENARIO

FDI in Multi-Brand retailing is prohibited in India. FDI in Single-Brand Retailing was, however,

permitted in 2006, to the extent of 51%. Since then, a total of 94 proposals have been received

till May, 2010. Of this, 57 proposals were approved. An FDI inflow of US $ 194.69 million (Rs.901.64 crore) was received between April, 2006 and March, 2010, comprising 0.21% of the total

FDI inflows during the period, under the category of single brand retailing. The proposals

received and approved related to retail trading of sportswear, luxury goods, apparel, fashion

clothing, jewellery, hand bags, life-style products etc., covering high-end items. Single brand

retail outlets with FDI generally pertain to high-end products and cater to the needs of a brand

conscious segment of the population, mainly attracting a brand loyal clientele, which often has a

pre-set positive disposition towards the specific brand. This segment of customers is distinctly

different from one that is catered by the small retailers/ kirana shops.

FDI in cash and carry wholesale trading was first permitted, to the extent of 100%,under the Government approval route, in 1997. It was brought under the automatic

route in 2006. Between April, 2000 to March, 2010, FDI inflows of US $ 1.779 billion

(Rs. 7799 crore) were received in the sector. This comprised 1.54 % of the total FDI

inflows received during the period.

Though the data on volume of turnover by retail is not separately maintained,

commodity composition of private consumption expenditure provides reasonable

estimates of the size of the retail sector

7

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 8/29

Table A: Private Final Consumption Expenditure- Commodity

Composition (Rs. in crore)

item 2004-05 2005-06 2006-07 2007-08 2008-09

Food and Beverages 763,345 852,798 947,856 1,070,794 1,182,211

Clothing & Footwear 127,608 150,633 188,276 202,797 213,344 Rent, Fuel and Power 250,986 277,310 311,915 356,197 415,436

Furniture and Appliances 64,944 76,458 93,401 111,536 121,984

Medical Care 95,560 105,244 115,900 127,648 140,584

Transport and Communication 378,217 418,363 477,521 521,858 608,048

Recreation, Education and 65,327 73,348 82,778 97,962 110,954 Culture

Miscellaneous Goods and 180,871 204,195 259,562 336,564 434,265 Services

‘FDI IN RETAIL- A POLICY PERSPECTIVE’, PREPARED BY FICCI AND ICICI PROPERTY

SERVICES IN FEBRUARY, 2005

i. Competition within the host country sector is a critical driver of improvements in

sector performance as a result of FDI.

ii. However, FDI's potential for impact can be greater because of the combination of

scale, capital, and global capabilities which allow MNCs to close existing large

productivity gaps more aggressively.

iii. FDI can be a powerful catalyst to spur competition in industries characterized by low

competition and poor productivity. Examples include the cases of consumer electronics

in Brazil and India, food retail in Mexico, and auto in China, India, and Brazil.

iv. Competition is also key to diffusing FDI-introduced innovation across an industry.

In Brazilian food retail, high competitive intensity caused by informal players

forced all modern retailers to rapidly increase productivity; in Mexican and

Brazilian auto cases, increasing competition from imports induced foreign players

themselves to increase their productivity.

v. Increasingly, foreign direct investment is integrating developing countries into the global

economy, creating large economic benefits to both the global economy and to the

developing countries themselves. Industry restructuring enables global growth as

companies reduce production costs and create new markets. For the large developing

countries, integrating into the global economy through foreign direct investments

improves standards of living by improving productivity and creating output growth. The

biggest beneficiaries from this transition are consumers - both global consumers that

8

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 9/29

reap the benefits from global industry restructuring, and consumers in the host

countries that see their purchasing power and standards of living improve.

vi. FDI can be a powerful catalyst to spur competition in the retail industry, due to the

current scenario of low competition and poor productivity. It can bring about:

Supply Chain Improvement

Investment in Technology

Manpower and Skill development

Tourism Development

Greater Sourcing From India

Up gradation in Agriculture

Efficient Small and Medium Scale Industries

Growth in market size

Greater Productivity

Benefits to government: through greater GDP, tax income and employmentgeneration

vii The report inter alia made the following recommendations:

Permit FDI in retail

Remove Bottlenecks in the supply chain

Relax SSI Reservation

Remove distribution constraints

Organize market for real estate

Increase land supply

Road Ahead

The BMI India Retail Report for the first quarter of 2012 released forecasts that the total

retail sales will grow from US$ 422.09 billion in 2011 to US$ 825.46 billion by 2015. The

report highlights strong underlying economic growth, population expansion, increasing

disposable income and rapid emergence of organised retail infrastructure as major

factors behind the forecast growth.

The report further predicts that sales through mass grocery retail (MGR) outlets will increase by

219 per cent to reach US$ 28.14 billion by 2015 while automotive sales would swell by almost

44.8 per cent from 3.6 million units in 2011 to 5.21 million units in 2015. Consumer electronic

9

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 10/29

sales are estimated at US$ 29.44 billion in 2011, with over-the-counter (OTC)

pharmaceutical sales at US$ 3.03 billion.

On the similar lines, global consultancy firm PricewaterhouseCoopers expects Indian

retail sector to be worth US$ 900 by 2014 in its report ‘Strong and Steady 2011.

SWOT ANALYSIS Strength:

1) Retailing is a “technology-intensive" industry. It is technology that will help the

organised retailers to score over the unorganized retailers. Successful organised

retailers today work closely with their vendors to predict consumer demand, shorten

lead times, reduce inventory holding and ultimately save cost. Example: Wal-Mart

pioneered the concept of building competitive advantage through distribution &

information systems in the retailing industry. They introduced two innovative logistics

techniques – cross-docking and EDI (electronic data interchange).

2) On an average a super market stocks up to5000 SKU's (Stock keeping Units)against a few hundreds stocked with an average unorganized-retailer.

Weakness:

1) Less Conversion level: Despite high footfalls, the conversion ratio has been very low in

the retail outlets in a mall as compared to the standalone counter parts. It is seen that

actual conversions of footfall into sales for a mall outlet is approximately 20-25 percent.

On the other hand, a high street store of retail chain has an average conversion of about

50-60percent. As a result, a stand-alone store has a ROI (return on investment) of 25-30

percent; in contrast the retail majors are experiencing a ROI of 8-10 percent.

2) Customer Loyalty: Retail chains are yet to settle down with the propermerchandise mix for the mall outlets. Since the stand-alone outlets were

established long time back, sot hey have stabilized in terms of footfalls

&merchandise mix and thus have a higher customer loyalty base.

3) The Indian middle class is already 30 crore &is projected to grow to over 60 crore

by 2010, making India one of the largest consumer markets of the world. The

IMAGES-KSA projections indicate that by 2015 India will have over 55 crore

people under the age of 20 – reflecting the enormous opportunities possible in the

kids and teens retailing segment.

Opportunity:

1) Percolating down: In India it has been found out that the top 6 cities contribute 66

percent of the total organised retailing. While the metros have already been exploited,

the focus has now been shifted towards the tier-II cities. The 'retail boom' of which 85

percent has so far been concentrated in the metros, is beginning to percolate down to

10

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 11/29

these smaller cities and towns. The contribution of these tier-II cities to total

organised retailing sales is expected to grow to 20-25 percent.

2) Rural Retailing: India's huge rural population has caught the eye of the retailers

looking for new areas of growth. ITC launched India's first rural mall "Chaupal

Saga" offering a diverse range of products from FMCG to electronic goods toautomobiles, attempting to provide farmers a one-stop destination for all their

needs. "Hariyali Bazar", started by DCM Sriram group, provides farm-related

inputs & services. The Godrej group has launched the concept of 'agri-stores'

named "Aadhaar" which offers agricultural products such as fertilizers & animal

feed along with the required knowledge for effective use of the same to the

farmers. Pepsi on the other hand is experimenting with the farmers of Punjab for

growing the right quality of tomato for its tomato purees, pastes

Threats:

1) If the unorganised retailers are put together, they are parallel to a largesupermarket with little or no over-heads, a high degree of flexibility in

merchandise, display, prices and turnover.

2) Shopping Culture has not developed in India as yet. Even now malls are just a place to

hang around, largely confined to window-shopping.

Due time limitation and being a large are, the scope will be limited to Ahmedabad city only.

Objective:

1) Tactical level inventory control decisions of the retail grocer seeking to improve

the replenishment process and reduce total inventory cost.

2) Strategic implications of supply chain activities that contribute and enable

sustained firm performance.

Methodology: The data for the research project would be mainly secondary data.

Various sources of secondary data like, newspapers, magazines, internet, budget

reports, and government sites will be used for the successful fulfillment of the project.

11

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 12/29

Scope: The scope of the project will be limited mainly to Ahmedabad city.

One the reason for limiting the research to Ahmedabad is because the city itself is big market

for the secondary data. The other reason for the area confinement is due to the lack of time.

Retail Models in India: Current & Emerging

The Indian food retail market is characterized by several co-existing types and formats.

These are:

1. The road side hawkers and the mobile (pushcart variety) retailers.

2. The kirana stores (the Indian equivalent of the mom-and-pop stores of the US), within

which: a. Open format more organized outlets

b. Small to medium food retail outlets. Modern trade – the organized retailers Within

modern trade, we have:

1. The discounter (Subhiksha, Apna Bazaar, Margin Free)

2. The value-for-money store (Nilgiris)

3. The experience shop (Foodworld, Trinethra)

4. The home delivery (Fabmart)

While the focus of this note is on modern organized retail trade, we hereunder present

insights into the smaller, semi and unorganized retailers.

Hawkers – ‘mobile supermarkets’

The unorganized sector is characterized by the cart vendors (also known as “mobilesupermarket”) seen in every Indian town and city is, therefore, difficult to track, measure

and analyze. But they do know their business – these lowest cost retailers can be found

wherever more than 10 Indians collect – a rural post office, a dusty roadside bus stop or a

village square As far as location is concerned, these retailers have succeeded beyond all

doubt. They have neither village nor city-wide ambitions or plans – their aim is simply a

12

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 13/29

long walk down the end of the next lane. This mode of “mobile retailers” is neither

scalable nor viable over the longer term, but is certainly replicable all over India. Most

retailing of fresh foods in India occurs in Mandis and roadside hawker parks, which are

usually illegal and entrenched. These are highly organized in their own way. Hawking

of food products, cooked food and FMCG products is a very interesting model ofretailing. Much has been written about these roadside “malls” – from social security

issues to their nuisance value. However if you put these hawkers together, they are

akin to a large supermarket with little or no overheads and high degree of flexibility in

merchandise, display, prices and turnover. While shopping ambience and the trust

factor maybe missing, these hawkers sure have a system that works.

Kirana/Mom-and-Pop Stores

Semi-organized retailers like kirana (mom-and-pop stores), grocers and provision

stores are characterized by the more systematic buying – from the mandis or the

farmers and selling – from fixed structures. Economies of scale are not yet realized in

this format, but the front end is already visible changing with the times. These stores

have presented Indian companies with the challenge of servicing them, giving rise to

distribution and cash flow cycles as never seen elsewhere in Asia. The model is very

antithesis of modern retail in terms of the buyer (retailer) - seller (FMCG) equations. Itis not unknown for MNC leaders to link the supply of one line of products to another

slower moving line of products. These retailers are not organized in the manner that

they could challenge the power of the sellers, most protests have been in the form of

boycotts, which really have not hit any company permanently.

Evolution of organized retailing

Retailing, one of the largest sectors in the global economy, is going through a transition

phase in India. For a long time, the corner grocery store was the only choice available tothe consumer, especially in the urban areas. This is slowly giving way to international

formats of retailing. The traditional food and grocery segment has seen the emergence of

supermarkets/grocery chains, convenience stores and fast-food chains.

The traditional grocers, by introducing self-service formats as well as value-

added services such as credit and home delivery, have tried to redefine themselves.

13

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 14/29

However, the boom in retailing has been confined primarily to the urban markets in

the country. Even there, large chunks are yet to feel the impact of organized retailing.

There are two primary reasons for this. First, the modern retailer is yet to feel the

saturation' effect in the urban market and has, therefore, probably not looked at the

other markets as seriously. Second, the modern retailing trend, despite its cost-effectiveness, has come to be identified with lifestyles.

Retail stores necessarily have to identify with different lifestyles. This trend is

already visible with the new stores with an essentially `value for money' image. The

attractiveness of the other stores actually appeals to the existing affluent class as well

as those who aspire to be part of this class. Hence, one can assume that the retailing

revolution is emerging along the lines of the economic evolution of society.

In 2000, the economists put a figure to it: Rs. 400,000 crore, which was expected

to develop to around Rs. 800,000 crore by the year 2005 – an annual increase of 20 per

cent. Retailing in India is unorganized with poor supply chain management perspective.According to a recent survey by some of the retail consulting bodies, an overwhelming

proportion of the Rs. 400,000 crore retail markets is unorganized. In fact, only a Rs.

20,000 crore segment of the market is organized. As much as 96 per cent of the 5 million-

plus outlets are smaller than 500 square feet area. This means that India per capita

retailing space is about 2 square feet (compared to 16 square feet in the United States).

India's per capita retailing space is thus the lowest in the world.

Impact of Organized

Retail

Organized retailing is spreading and making its presence felt in different parts of the

country. The trend in grocery retailing, however, has been slightly different with a growth

concentration in the South. Though there were traditional family owned retail chains in

South India such as Nilgiri’s as early as 1905, the retail revolution happened with the

RPG group starting the Foodworld chain of food retail outlets in South India with focus on

Chennai, Hyderabad and Bangalore markets, preliminarily. The experiment has

reaped rich dividends and the group is now foraying into other territories as well.

Owing to the success of Foodworld model of RPG group, several new models such asTrinethra, Subhiksha, Margin Free and others have made their foray into this sector

albeit at regional levels. Today the food retail sector in India is about Rupees Ten

Lakh Crores (USD 200 billions) of which the organised food retail segment is about 1

per cent and increasing at a pace of over 20% year-to-years.

14

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 15/29

To be successful in food retailing in India essentially means to draw away

shoppers from, the roadside hawkers and kirana stores to supermarkets. This

transition can be achieved to some extent through pricing, so the success of a food

retailer depends on how best he understands and squeezes his supply chain. The

other major factor is that of convenience shopping which the supermarket has theedge over the traditional kinara stores. On an average a supermarket stocks up to

5000 SKU’s against few hundred stocked at an average kirana stores.

Though with excellent potential, India poses a complex situation for a retailer,

as this is a Country where each State is a mini Country by itself. The demography’s of

a region vary quite distinctly from others. In order to appeal to all classes of the

society, retail stores would have to Identify with different lifestyles. Hence we may find

more of regional players and it would take enormously long time before nationwide

successful retail chains emerge. This is the main reason as to why the successful

retail chains in the country today operate at regional segments only and are not

aiming at nationwide presence, at least for the time being.

In the organized retail industry, the gestation periods are long, institutional funding

is difficult, and there is none or little Government support. But the belief among top retailer

chains in the country is that the industry will see large investments coming once the

current ban on foreign direct investment is lifted. But that could be two-three years away.

Food and grocery retailing is a tough business in India with margins being very low, and

consumers not dissatisfied with existing shops where they buy. For example, the next-

door grocery shopkeeper is smart and delivers good customer service, though not value.

As of now, while Chennai has about five organized food and grocery retail chains, other

big cities such as Delhi, Bangalore, and Mumbai average only two-three such chains.

Almost all food retail players have been region-specific as far as geographical presence is

concerned in the country. To illustrate with examples, the RPG Group's Food World,

Nilgiris, Margin Free, Giant, Varkey's and Subhiksha, all of which are more or less spread

in the Southern region; Sabka Bazaar has a presence only in and around Delhi; names

such as Haiko and Radhakrishna Foodland are Mumbai-centric; while Adani is

Ahmedabad-centric. Industry topography in India is such that spreading presence across

cities is a tough call. As pointed out by many experts, organized food and grocery retailing

chains going national requires significant investments Retailing within this sector is not

just about the front end, but involves complex supply chain and logistics issues as well.

The trend and mindset of the present retailer chains in India can be best understood

by studying Food World as an example, which came in first in the food and grocery retailing

sector. The chain has no plans to venture beyond the Southern region just yet. Current plans

15

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 16/29

are to focus on the Southern markets and achieve saturation. The intention is that by 2005,

they could look at the other regions. Subhiksha, a Chennai based discount chain, too wants to

be the principal store of purchase for at least 40 per cent of all consumers living within 500-

750 meters of the store, that is, within walking distance. This makes the point very clear that

the strategy among most existing retail chains of various formats is to completely saturate themarkets where they are already established players and then move on to virtually untouched

areas where the challenge of sourcing resources and extending their supply chain model to

best suit the size and expanse of the market would be a challenging task.

Meanwhile, the RPG group plans to take its new formats such as Giant Hypermarkets

national over the next three years. Grocery is a large component of this format, but not the

only one. To elaborate on the hurdles of going pan-Indian, fundamentally, the way a basic

grocery retailing model works is that the high set-up costs in terms of setting up buying/

distribution infrastructure is gradually amortized over a large number of stores. The back-end

costs without distribution centre costs, or what in retail jargon is called retail administration

costs, should stabilize at around 2.5 per cent to 3 per cent of sales.

It can be explained that the obstacles of looking at a pan-India model for

grocery are several. Given the federal nature of the country, the weak infrastructure

and the major variances in eating habits in different parts of the country, one will have

to replicate the retail administration costs for at least each region and therefore the

gestation period of the project becomes huge. However, if a model is in place where

the upfront store revenues scale very rapidly, then it is possible. Therefore, if one is to

attempt a pan-Indian grocery foray, it will have to be in the hypermarket format with its

attendant investment numbers and risk profile.

If a close look is taken at the nature of the Indian Retail Markets, it can be seen that

there is so much potential to extract from individual regions, that players are in no

tearing hurry to spread out. Based on a recent study by a renowned government

institution in India, in the six major metros, Delhi has the highest per capita

consumption of food and grocery, among supermarkets. Chennai, “the Mecca of

retailing”, comes at fourth place. This shows the high potential the sector presents.

Chennai has some five supermarket chains, and each of these are doing well for

themselves. So there is enough scope to expand even in one single city in India.

It can be observed that the most popular retail format in India is the ‘supermarket’,

beside the corner shop/grocery store ’mom and pop’ store . Hypermarkets have very recently

come into being and are negligible in number though most retail chains do intend to expand

their presence through this format as well very soon. ‘Discount chains’ are also substantial in

number and are growing at a fast pace through the country, predominantly, in the southern

16

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 17/29

region. Given that organized retail has been registering growth rates of approximately 40

per cent over the last three years, it is expected to grow to about Rs 35,000 crore in 2005,

and close to Rs 70,000 crore in 2010. If projections were to be made considering the

current trends in food retailing in India, some years down the line, food and grocery stores

will become dominating trade partners for the food industry, which, in turn, will be forcedto offer special discounts and trade terms for them to get the shelf space in such stores.

Also, once established, in-store label brands will become a real threat to the industry as

manufacturers will have to compete with the store label brands that are generally very

price-competitive. As for the spread geographically, strong chances stand that the major

chains would spread to the next grade of cities in the country over the next 5 years or so

and then progressively start covering every corner of the country. Most chains have

already started developing their own unique supply chains that would suit their needs

precisely. Replicating the success stories of the big names of the Western nations may

still be a distant dream for Indian food and grocery retailers, but at least the winds are

blowing in the direction of growth.

Analysis of food retail

sector

Retailing is a sunrise industry in India with many challenges like exclusion of small

farms, management of processing and distribution chains. Evolution of super markets

and fast food chains is a recent phenomenon in India. Various demand and supply

side factors have contributed towards this growth.

Supply

Side

The liberalization of the economy in the 1990s led to a boom in the “Consumer Goods”

Industry with reductions in custom duties and shift from quota to tariff based system. Entry

barriers on multinationals were largely removed after which Food Industry majors like

Kellogg’s, Heinz, Tropicana, etc., entered the Indian food industry. This gave rise to

tremendous development of sophisticated supply chain and logistics which eventually andgradually has led to the growth in the food processing & packaging industry.

Demand

The increase in the income levels of middle & higher income groups in the 1990s coupled with

the reduction in poverty levels was major factor in contributing to the increase in demand for

17

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 18/29

high quality food retailing services. Changing consumer lifestyles with the steep increase in

time value, wide spread change in the Indian family structure from vast Joint Hindu families

to more manageable nuclear families and increasing level of quality awareness has also

helped the cause of the Food Retailing industry considerably. Another major factor that has

accelerated the growth of the Indian Food Retailing Sector has been the advent of cable television and the increasing Instances of overseas travel by Indians for various reasons.

Retailing is subject to a plethora of laws and regulations at central, state and

Municipal/local levels, some of which have been listed below:

- Restrictive zoning legislation limits availability of land for retail/ commercial purposes

- Restrictions on intense movement of food grains deprive farmers from getting

remunerative Prices.

- Restrictive Labor laws

- Urban land ceiling regulations, restrictions on shop opening timings, requirements for

shops to

Close once a week

- There is no uniform tax structure - multiple layers of taxes.

Food & Grocery from big and better portion of organized retailing these days.

India’s retail sales now account for 44 per cent of its GDP. Food retail sales make up for

close to 63 per cent of total retail sales. In absolute terms, food retail sales have grown

from Rs 3,81,000 crore in 1996, to Rs 7,03,900 crore in 2001. And, just for the record,

non-food retail sales have grown from Rs 2,22,400 crore in 1996, to Rs 4,19,000 crore in

2001. Besides, the food and grocery sector now accounts for 14 % of total organized

retail, after clothing and textiles (36 %) and watches and jeweler (17 %).

Modern, or organized retail, accounts for just about 1.6 per cent of the total

retail sales in the country, estimated at Rs 18,000 crore. The study further analyses

that last year, for the first time in five years, retail shares of grocery dropped, even

though in terms of absolute value, the shares remained stable.

18

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 19/29

According to Mr. .R Subramanian, Director of the Chennai-based discount

retail chain, Subhiksha: "Food and grocery retailing is a tough business. Margins are

low, and consumers are not dissatisfied with existing shops where they buy. For

example, the next door grocery shopkeeper is smart and delivers good customer

service, though not value." As of now, while Chennai has some five organized food and grocery retail chains, other big cities such

as Delhi, Bangalore and Mumbai average only two-three such chains. Also, most food

retail players have been region-specific as far as geographical presence is concerned.

RPG Group's FoodWorld, Nilgiris, Margin Free, Giant, Varkey's and Subhiksha, all of

which are more or less spread in the

Southern region; Sabka Bazaar has a presence only in and around Delhi; names such as Haiko

and Radhakrishna Foodland are Mumbai-centric; while Adani is Ahmedabad-centric. "Organised

food and grocery retailing chains going national requires significant investments. Retailing within

this sector is not just about the front-end, but involves complex supply chain and logistics issues

as well." Says Mr. Arvind Singhal, Chairman KSA Technopak. FoodWorld, which came in first in

the food and grocery retailing sector. The chain has no Plans to venture beyond the Southern

region just yet. Food World has a current sales figure of Rs 350 crore. Subhiksha too is gung-ho

about the future of the discount chain. Given that organised retail has been registering growth

rates of approximately 40 per cent over the last three years, it is expected to grow to about Rs

35,000 crore in 2005, and close to Rs 70,000 crore in 2010.

And as an industry analyst elaborates, "Some years down the line, food and grocery

stores will become dominating trade partners for the food industry, which, in turn, will be

forced to offer special discounts and trade terms for them to get the shelf space in such

stores. Also, once established, in-store label brands will become a real threat to the

industry as manufactures will have to compete with the store label brands which are

generally very price-competitive." In the retail format, hypermarkets are expected to be

the most successful format. Food and grocery and hypermarkets are likely to generate the

best returns in 5 years.. Most of the growth will come from hypermarkets and,

coincidentally, all announcements of expansions by leading players are in this format. In

terms of returns, food and grocery format scores over the apparel one. Although apparel

stores have higher margins, food and grocery stores earn higher returns once the stores

stabilise; this is driven by lower fixed costs and significantly higher stock turnover ratios.

Private labels have yielded higher margins for most large players.

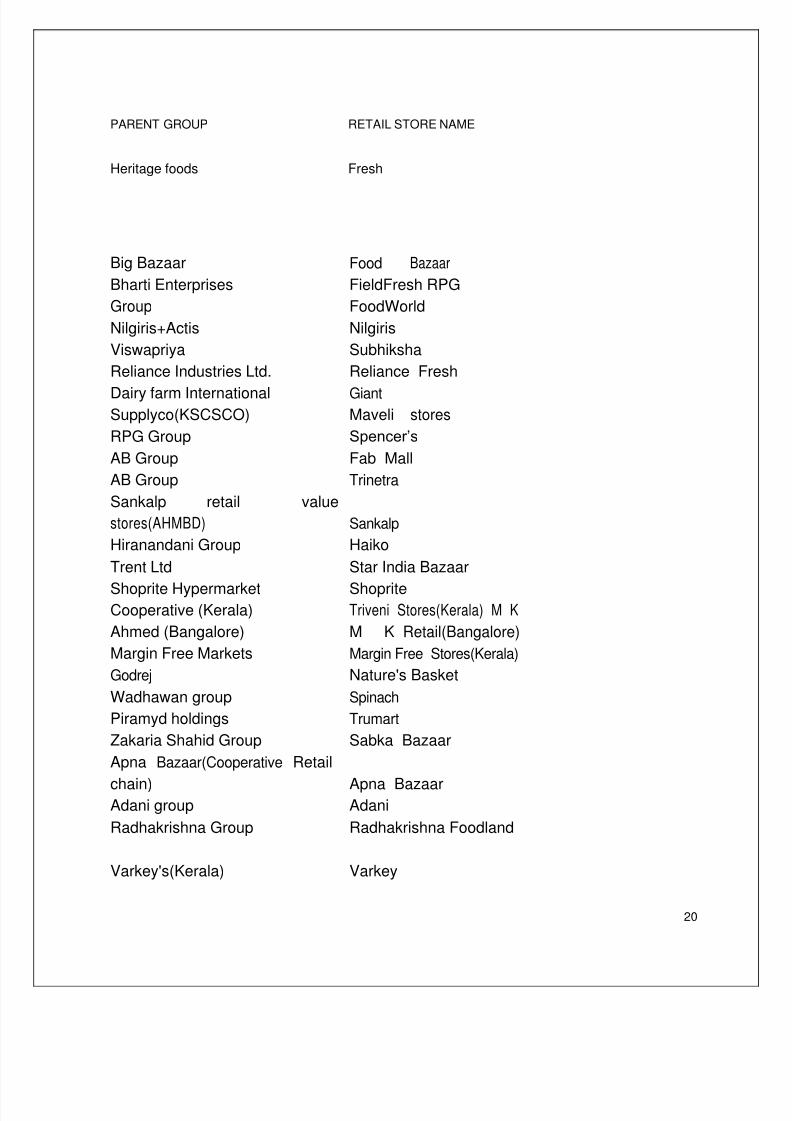

The comprehensive list of Food & Grocery retail in

India are :

19

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 20/29

PARENT GROUP RETAIL STORE NAME

Heritage foods Fresh

Big Bazaar Food Bazaar

Bharti Enterprises FieldFresh RPG

Group FoodWorld

Nilgiris+Actis Nilgiris

Viswapriya Subhiksha

Reliance Industries Ltd. Reliance Fresh

Dairy farm International Giant Supplyco(KSCSCO) Maveli stores

RPG Group Spencer’s

AB Group Fab Mall

AB Group Trinetra

Sankalp retail value

stores(AHMBD) Sankalp

Hiranandani Group Haiko

Trent Ltd Star India Bazaar

Shoprite Hypermarket Shoprite Cooperative (Kerala) Triveni Stores(Kerala) M K

Ahmed (Bangalore) M K Retail(Bangalore)

Margin Free Markets Margin Free Stores(Kerala)

Godrej Nature's Basket

Wadhawan group Spinach

Piramyd holdings Trumart

Zakaria Shahid Group Sabka Bazaar

Apna Bazaar(Cooperative Retail

chain) Apna Bazaar Adani group Adani

Radhakrishna Group Radhakrishna Foodland

Varkey's(Kerala) Varkey

20

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 21/29

Example: Big Bazaar

Organization overview

Big Bazaar is a chain of hypermarket in India. Currently there are 210 stores across 80

cities and towns in India. Big Bazaar is designed as an agglomeration of bazaars or

Indian markets with clusters offering a wide range of merchandise including fashion and

apparels, food products, general merchandise, furniture, electronics, books, fast food

and leisure and entertainment sections.

Store format

There are 93 outlets today across Southern and Western India. Self service

oriented merchandising strategy is followed. Big Bazaar display format follows

functional racking with no fancy accessories. The stores have a very dominant

corporate fascia/signage, with the logo written in yellow on bold red. Typical store

carries about 5000 items. The average ticket size ranges around Rs280-300. Site

strategy is residential high street with minimum 6000 households in two to three km

radius and the Core customer target between one-and-a-half and two kilometers of

the store .Big Bazaar stores consider ground floor properties only- between 3000 to

3500 sq ft with minimum 40 ft frontage. Additional space of approximately

400 sq ft for back office and standby generator is used.

Positing

A “self service neighborhood Grocery" store catering largely to the "monthly"

consumables requirement of households in the immediate vicinity. It offers a complete

range of fresh foods, including Fruits, Vegetables, Bakery etc .Primarily it is a

shopping destination for people staying within one-and-a-half kilometer radius of

21

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 22/29

the store. It provides customers with a wide range of quality products reasonable prices

under one roof, in a convenient location, in a clean, bright and functional ambience.

Product Mix

It consists of seven major groups, namely, staples, processed foods, beverages,

non-food, health & beauty, perishables and hardware and home appliances.

Further divided into 49 categories, such as destination, strategic (routine),

convenience and specialty (occasional) depending upon the importance in the

customers’ purchase basket and frequency of purchase.28 per cent of Big

Bazaar's foods and groceries are private labels -launched more than 150 items

under Big Bazaar Brand Big Bazaar Brands are backed by a 100% No QuestionsAsked Replacement Guarantee- a first of its kind in the market.

Marketing Strategy

Big Bazaar marketing strategy’s focus is to maximize traffic in the store.

Merchandising and display strategy geared toward increasing the size of the bill

value and purchase basket for each customer. Direct mailers and in-store

shopping guides main communicators for the customers for the strategy. In-storeshopping ambience built using bright and prominent displays like posters, large

shelf talkers and bulk merchandising or floor displays.

Distribution Strategy

It follows a strategy of minimum suppliers to take advantage of economies of scale (in

purchasing and supply logistics), reduced overheads and control requirements, and

easier vendor development. Big Bazaar works on the hub-and-spoke model. A hub istypically of 50,000-60,000 sq ft in area and serves about 30-40 stores in a radius of 30

km .Creation of Regional Hubs facilitates over 90% central distribution .The

remaining 10% (mostly perishable items like fruits and vegetables, bakery etc) supplied

direct to store. It consolidates the harvests from Ooty, Kodaikanal, Hosekote,

Venkatagirikota, Bangalore and Hyderabad. It participates in early morning auctions at

22

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 23/29

the major wholesale markets. It has a set of suppliers who grade, clean, pack and

label the fresh products in time for early morning dispatch to the stores.. On an

average, 250 tones of fruits and vegetables a month are supplied from here to all Big

Bazaar stores. Big Bazaar has close to 8,000 SKUs at any given point in time in

the stores. Revenue as of year 2005 was Rs 382 crore. CAGR, in terms ofturnover has been at 30% over the years.

Customized Distribution and

Logistics Supply Chain

Big Bazaar provides Customized Distribution & Logistics services encompassing the entire

supply chain, such as storage, handling and distribution solutions to various clients. The

services are tailor made to suit each client’s requirements, which include organizations such

as McDonalds and Radhakrishna Hospitality Services Pvt. Ltd. (RKHS)

Platter of Services

Supply Chain activities

Inventory Planning and Replenishment Management

Warehouse Management

Customer Order Fulfillment

Logistics-Temperature Control

Third Party Logistics

Key Features:

Dedicated to ‘cold chain’

movement

23

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 24/29

The only logistics solution provider with expertise in handlingagri – produce

Total kilometer run per month is – 6,00,000 km

Perishable tonnage handled per month – 6,000tons

Robust quality systems &processes

First in the country to use multi temperaturevehicles

Use of innovative methods to ensure temperature integrityduring transit

Experienced staff – The BEST in theindustry.

Fresh Rush

Aimed at movement of small volumes of perishable items. Companies loose out revenue due

to non catering few markets due to the inexperience in movement of perishable items.

Fresh Rush is a temperature controlled transportation service addressing the

needs of small volume cargo.

Features: Multi temperature products, such as Frozen(below –18ºC) and Chilled (1ºC to

4ºC) can be transported.

Flexibility of load movement - A minimum of 500 kgs to maximum of 5000 kgscan be transported

24

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 25/29

In transit temperaturetracking

Fixed schedule of pickup anddelivery

Well trained and experiencedmanpower

Adherence to strict hygienestandards

Consignment can be tracked throughGPS system

Advantage Big Bazaar

Big Bazaar’s domain expertise and experience helps customers deriveoptimum efficiency and profitability

Waste reduction, shelf life extension and cost reduction of agri-produce from

hinterlands and upcountry sources supplying to the country’s main markets

Freedom from managing the day-to-day affairs of supply chain management

Major cost saving, coupled with timely management of schedules and deliveries

Dependable and trustworthy services matching global standards of companies like McDonalds

McDonalds:

Full Supply Chain responsibility

Multi Temp. Products - Over 65 % temperature controlled

Stores as far as 500 – 1000 kms

25

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 26/29

Drops per month – Over 700

Movement mainly by road

Regular movement of perishables by air

Routing Challenges

No margin for error – Operations critical client

No Stock Outs at store

On time delivery record – above 97 %

Clean delivery record – above 99 %

Unfailing inbound supply chain

Private Labels

Big Bazaar offers its own private labels, under the ‘Big Bazaar’ brand.

Products

Fruits & Vegetables

Staples

Bakery Items

Non Veg

26

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 27/29

Delicatessen (premium ready-to-eat veg, chicken and pork products)

Features:

Sourcing from reliable vendors who follow stringent Quality Assurance andFood Safety standards

Distribution Centers equipped with multi-temperature zones to store and process

different types of products depending upon their specific requirements.

Extensive training imparted to food-handlers and others involved in thewhole chain to ensure superior output

Hygienic Packaging

Delivery vehicles capable of carrying products across temperature dispositions

Strict Quality Assurance and Food Safety programs to ensure product integrity

Challenges and Constraints

It faces competition from emerging value-based formats and from independent modern

stores providing a better value proposition. No investments made in areas like IT,

Back end administration, and customer relationship management, where returns are

not immediate. Unorganized sector is getting organized -Bombay Bazaar and E-food mart have also been formed which are aggregations of Kirana’s. Challenges in the

area of infrastructure, supply chain, warehousing, and local legislation still lie ahead.

27

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 28/29

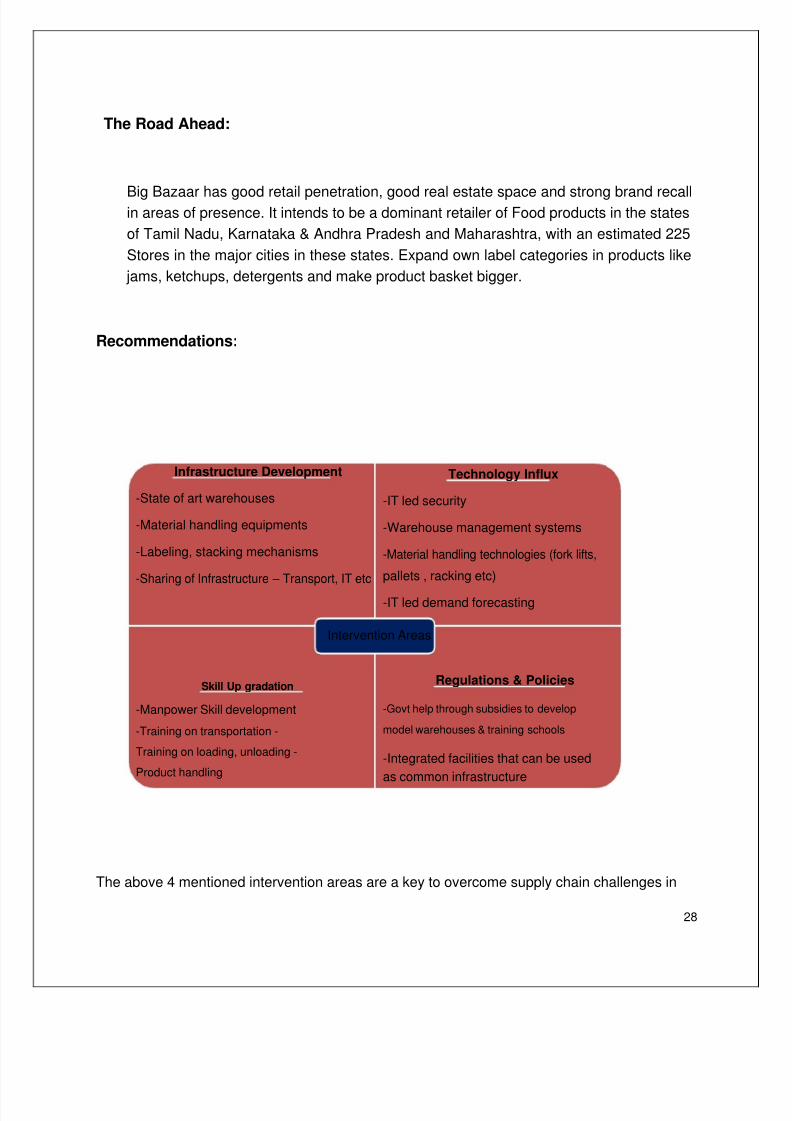

The Road Ahead:

Big Bazaar has good retail penetration, good real estate space and strong brand recallin areas of presence. It intends to be a dominant retailer of Food products in the states

of Tamil Nadu, Karnataka & Andhra Pradesh and Maharashtra, with an estimated 225

Stores in the major cities in these states. Expand own label categories in products like

jams, ketchups, detergents and make product basket bigger.

Recommendations:

Infrastructure Development Technology Influx

-State of art warehouses -IT led security

-Material handling equipments -Warehouse management systems

-Labeling, stacking mechanisms -Material handling technologies (fork lifts,

-Sharing of Infrastructure – Transport, IT etc pallets , racking etc)

-IT led demand forecasting

Skill Up gradation

-Manpower Skill development

-Training on transportation -

Training on loading, unloading -

Product handling

Intervention Areas

Regulations & Policies

-Govt help through subsidies to develop

model warehouses & training schools

-Integrated facilities that can be used

as common infrastructure

The above 4 mentioned intervention areas are a key to overcome supply chain challenges in

28

8/3/2019 Final Report Mrp Nishant

http://slidepdf.com/reader/full/final-report-mrp-nishant 29/29

retail industry. The key to success will be to use these methods in a holistic approach.

A very good example can be of the Future group’s “Mega Food Park concept”. The

company has started to build a cold storage in Tumkur, Karnataka. The cold storage will be

used by many farmers who can store their seasonal vegetables in them, keeping the fresh

and available on request at all times. The rent would be paid by the farmers. Thegovernment has allotted Future Group with 40% of the amount required to build the

infrastructure. This type of initiative will help the retail industry in India to shine n future.

Conclusion: Ideally retail supply chains need to be designed to be lean & defect free prior to

implementation of the processes. However, this is rarely possible in real life given the pace at

which the industry is expanding. Even if this is done & processes designed optimally the rapidly

changing market dynamics soon make them ineffective. Hence there is a need to continuously

review & revive the standard operating practices (SOPs) that are used to document & audit

process implementation. A well designed lean six sigma initiative helps in continuous process

redesign in order to ensure efficiency & accuracy despite changing operating conditions.

References:

1) Indiaretailing.com

2) A.C Nielsen report3) Future Group employees

4) National Seminar on Logistics &Supply Chain Management, IASMS, BANGALORE, INDIA