final project- fiscal decentralization(1)-1

TRANSCRIPT

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 1/95

KWAME NKRUMAH UNIVERSITY OF SCIENCE AND

TECHNOLOGY, KUMASI

COLLEGE OF ART AND SOCIAL SCIENCES

KNUST SCHOOL OF BUSINESS

Challenges and prospects of fiscal decentralization in Ghana:

A case study of the Wa Municipality

BY

BA-INGE MATHIAS

IB-KU ROLAND

KARIMU NASHIRU

SEIDU ABDUL-KUDUS

MAY, 2012

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 2/95

i

KWAME NKRUMAH UNIVERSITY OF SCIENCE AND

TECHNOLOGY, KUMASI

COLLEGE OF ART AND SOCIAL SCIENCES

KNUST SCHOOL OF BUSINESS

Challenges and prospects of fiscal decentralization in Ghana:

A case study of the WA Municipality

A Dissertation

Presented to the KNUST School of Business in Partial Fulfillment of the

Requirements for the award of BSc. Business Administration degree

TITLE PAGE

BY

BA-INGE MATHIAS

IB-KU ROLAND

KARIMU NASHIRU

SEIDU ABDUL-KUDUS

MAY, 2012

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 3/95

ii

DECLARATION

We declare that this long essay is our original work and has not been presented, either

whole or in part, for any purpose anywhere. To the best of our ability, we have duly

acknowledged information from other sources.

NAME INDEX NUMBER SIGNATURE DATE

BA-INGE MATHIAS 2502808 ……………… …................

IB-KU ROLAND 2505108 ……………… …................

KARIMU NASHIRU 2505408 ……………… …................

SEIDU ABDUL-KUDUS 2510008 ……………… …................

SUPERVISED BY:

MR. KWAME MIREKU ……………….. …................

SIGNATURE DATE

CERTIFIED BY:

MR. J. M. FRIMPONG ……………….. …................

SIGNATURE DATE

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 4/95

iii

DEDICATION

We dedicate this work to our beloved parents; Mr. Joseph Ba-inge and his wife Mrs.

Georgina Ba-inge, Mr. Haruna Seidu and his wife Seidu Asana, Mr. Maalu Albanus

and his wife Dery Basilia, Mr. Wadjia Karimu and his wife Adamu Safia with whose

support and encouragement this work has come to reality.

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 5/95

iv

ACKNOWLEDGMENT

All praises and thanks are due to God, the most gracious and the most merciful, who

has given us knowledge, protection and guidance throughout our education.

Our profound gratitude goes to Mr. Kwame Mireku, a lecturer in the KNUST School

of Business, who supervised this work and whose guidance has made this study a

success. To all lecturers of the KNUST School of Business, we thank them for

making our university education a reality.

Also, our sincere thanks go to the staff of the Wa Municipal Assembly especially

Hon. Duogu Yakubu, the Municipal Chief Executive and Mr. Dabuo Julius, the

Municipal budget officer who contributed in diverse ways in assisting us to get data

for this project. We say may God bless them.

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 6/95

v

ABSTRACT

The need for growth and development at the grass-root level has necessitated the concept

of local government and decentralization in Ghana. Under the Local Government Act,

1993, (Act 462), District Assemblies are responsible for the development and the general

needs of the local communities. This has resulted in high expectations towards

development from the local communities. Whiles significant progress has been made

towards the other facets of decentralization; fiscal decentralization seems not to be

progressing. The resources provided by central government to the district assemblies are

not always sufficient to meet the developmental expectations of the people hence, the

need for district assemblies to mobilize revenue from internal sources to supplement the

transfers from the central government. It is however not uncommon to see district

assemblies generating revenue below their revenue needs and targets.

The study covers all the eight towns in the Wa Municipality. Out of this population, a

sample of one hundred and fifty (150) was selected. Quotas of one hundred and twelve

(112), twenty (20) and eighteen (18) were assigned to the general public, revenue

collectors and the assembly’s staff respectively. Purposive sampling was used for the

assembly’s staff, whiles convenience sampling was used for both the general public and

the revenue collectors.

The study identifies several challenges to fiscal decentralization and remedies for

overcoming them. For the fiscal decentralization policy to achieve its intended objectives

the central government and MMDAs in Ghana need to adopt measures such as: an

adequate enabling environment, assignment of an appropriate set of functions to local

governments, assignment of an appropriate set of local own-source revenues to local

governments and the establishment of an adequate intergovernmental fiscal transfer

system.

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 7/95

vi

TABLE OF CONTENTS

TITLE PAGE .................................................................................................................. i

DECLARATION ........................................................................................................... ii

DEDICATION ............................................................................................................. iii

ACKNOWLEDGMENT............................................................................................... iv

ABSTRACT ................................................................................................................... v

TABLE OF CONTENTS .............................................................................................. vi

LIST OF TABLES ....................................................................................................... xii

LIST OF FIGURES ..................................................................................................... xii

LIST OF ABBREVIATIONS AND ACRONYMS .................................................. xiii

CHAPTER ONE ............................................................................................................ 1

INTRODUCTION ......................................................................................................... 1

1.1 Background of the study .......................................................................................... 1

1.2 Problem Statement ................................................................................................... 3

1.3 Research Objectives ................................................................................................. 5

1.4 Research Questions .................................................................................................. 5

1.5 Significance of the study .......................................................................................... 5

1.6 Scope and limitations of the study ........................................................................... 6

1.7 Organization of the study ......................................................................................... 6

CHAPTER TWO ........................................................................................................... 8

LITERATURE REVIEW .............................................................................................. 8

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 8/95

vii

2.1 Introduction .............................................................................................................. 8

2.2 Definition of key concepts ....................................................................................... 9

2.3 Overview of Fiscal Decentralization in Ghana ...................................................... 10

2.4 Objectives and implications of fiscal decentralization in developing countries .... 12

2.5 Arguments for fiscal decentralization .................................................................... 12

2.6 Extent of decentralization of fiscal powers ............................................................ 14

2.7 Effectiveness of fiscal decentralization ................................................................. 16

2.8 Challenges of fiscal decentralization in developing countries ............................... 17

2.8.1 Intergovernmental transfers ................................................................................ 18

2.8.2 Expenditure management and financing ............................................................. 18

2.8.3 Adequacy of local revenues and autonomy ........................................................ 19

2.8.4 Local government borrowing .............................................................................. 19

2.8.5 Budget discretion ................................................................................................ 20

2.9 Prospects of Fiscal Decentralization ...................................................................... 22

2.9.1 An Agenda for Reforming Expenditure Assignment and Management ............. 23

2.9.2 An Agenda for Improving Local Revenue Generation and Autonomy .............. 24

2.9.3 An Agenda for Reforming Intergovernmental Transfers .................................... 24

2.9.4 Local Government Borrowing and Investment Finance ..................................... 25

2.9.5 Better Framing of Institutional Reform .............................................................. 26

2.10 History of decentralization in Ghana ................................................................... 26

CHAPTER THREE ..................................................................................................... 28

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 9/95

viii

METHODOLOGY ...................................................................................................... 28

3.1 Introduction ............................................................................................................ 28

3.2 Research methods .................................................................................................. 28

3.3 Data sources ........................................................................................................... 28

3.3.1 Primary sources of data ....................................................................................... 28

3.3.2 Secondary sources of data ................................................................................... 29

3.4 Sample Population and Sample Size...................................................................... 29

3.5 Sampling techniques .............................................................................................. 29

3.6 Data Collection Instruments .................................................................................. 30

3.6.1 Interview ............................................................................................................. 30

3.6.2 Questionnaires..................................................................................................... 31

3.7 Data Analysis Tools ............................................................................................... 31

3.8 Profile of the Wa Municipal Assembly ................................................................. 32

CHAPTER FOUR ........................................................................................................ 36

DATA PRESENTATION AND ANALYSIS ............................................................. 36

4.1 INTRODUCTION ................................................................................................. 36

4.2 THE EXTENT OF DECENTRALIZATION OF FISCAL POWERS .................. 36

4.2.2 Power to generate and use revenue ..................................................................... 37

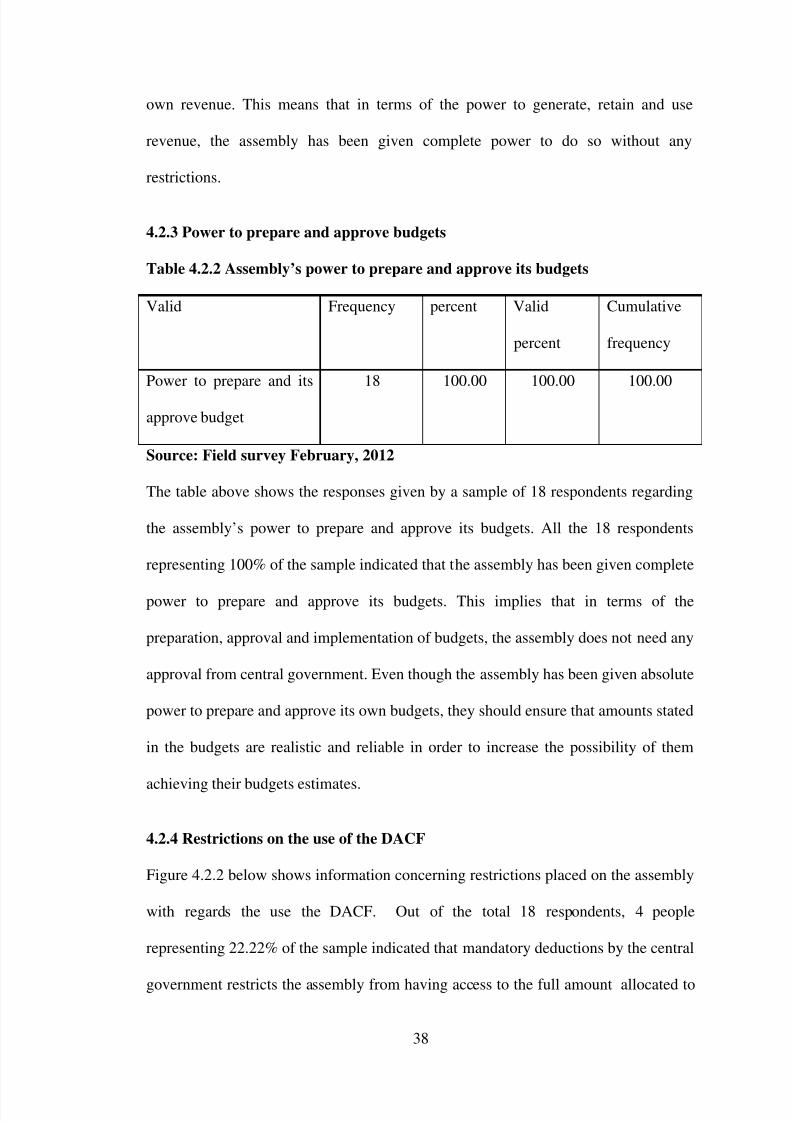

4.2.3 Power to prepare and approve budgets ............................................................... 38

4.2.4 Restrictions on the use of the DACF .................................................................. 38

4.3 EFFECTIVENESS OF FISCAL DECENTRALIZATION ................................... 40

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 10/95

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 11/95

x

CHAPTER FIVE ......................................................................................................... 60

SUMMARY OF FINDINGS, RECOMMENDATIONS AND CONCLUSION ........ 60

5.1 INTRODUCTION ................................................................................................. 60

5.2 SUMMARY OFFINDINGS .................................................................................. 60

5.2.1 The extent of decentralization of fiscal powers .................................................. 60

5.2.2 Effectiveness of fiscal decentralization .............................................................. 61

5.2.3 The challenges of fiscal decentralization ............................................................ 61

5.2.4 Remedies to the challenges of fiscal decentralization ........................................ 62

5.2.5 Prospects of fiscal decentralization ..................................................................... 64

5.3. Recommendations ................................................................................................. 65

5.4 Recommendation for further research ................................................................... 66

5.5 Conclusion ............................................................................................................. 66

REFERENCES ............................................................................................................ 68

APPENDIX .................................................................................................................. 72

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 12/95

xi

LIST OF TABLES

Table 4.2.1 The assembly’s power to borrow and its restrictions .............................. 36

Table 4.2.2 Assembly’s power to prepare and approve its budgets ............................. 38

Table 4.3.1 Budgeted and actual revenue for 2009 and 2010 ..................................... 40

Table 4.3.2 Level of education of revenue collectors .................................................. 43

Table 4.4.1 Challenges The Assembly Faces In Mobilizing Revenue ........................ 46

Table 4.4.2 challenges faced by tax payers in paying taxes ........................................ 48

Table 4.5.1 Measures to overcome assembly’s challenges in borrowing funds .......... 50

Table 4.5.2 Measures to overcome the challenges revenue collectors face................ 53

Table 4.5.3 Measures to overcome the challenges the assembly encounter in preparing

its budgets .................................................................................................................... 55

Table 4.5.4 Measures to overcome challenges faced by taxpayers in paying taxes .... 56

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 13/95

xii

LIST OF FIGURES

Figure 4.2.1 Apart from borrowing, does the assembly have power to generate and

use its own revenue? .............................................................................. 37

Figure 4.2.2 Restriction placed on the use of the DACF ........................................... 39

Figure 4.3.1 Does the assembly always meet its budget plans? ................................ 41

Figure 4.4.1 Challenges the assembly encounters in acquiring loans ....................... 43

Figure 4.4.2 Challenges the assembly face in preparing its budgets ......................... 45

Figure 4.4.3 Challenges faced by revenue collectors in collecting revenue .............. 49

Figure 4.5.1 Measures to be put in place to ensure effective revenue generation ..... 52

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 14/95

xiii

LIST OF ABBREVIATIONS AND ACRONYMS

BoG Bank of Ghana

CPP Convention People’s Party

DACF District Assemblies Common Fund

DAs District Assemblies

DDF District Development Facility

DPs Development Partners

FAD Financial Administration Decree

GTV Ghana’s Television

IRS Internal Revenue Service

L.I Legislative Instrument

MCE Municipal Chief Executive

MMDAs Metropolitan, Municipal and District Assemblies

MTDPs Medium-Term Development Plans

PNDC Provisional National Defense Council

PNDCL Provisional National Defense Council Legislation

SMCD Supreme Military Council Decree

SNGs Sub-National Governments (SNGs)

SPSS Statistical Package for Social Sciences

T-Z Tuo–Zaafi

USAID United States Agency for International Development

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 15/95

1

CHAPTER ONE

INTRODUCTION

1.1 Background of the study

The decentralization of authority and responsibility for public services provision to

local government is an essential part of the overall governance and development

strategy in many developed and developing countries around the world. Some

countries, organizations and institutions have recognized the need for decentralization

as a tool to enhance the effectiveness and efficiency of their operations. Development

partners, district assembly functionaries, donors, academia and the local communities

have stressed the need for decentralization. This will increase economic efficiency

and allow greater differentiation in the provision of public services due to improved

preference matching and government accountability (Bardhan and Mookherjee 2006;

Lockwood 2006). This thus reflects the belief that because local governments are

closer to the people than the central government, they will be better informed about

the preferences and circumstances of the residents; therefore, decentralization can

improve allocation efficiency in the sense that the services provided by local

governments will be better matched with the preferences of their populace; and local

people might be better informed about the actions of local government; therefore, they

will be in a better position to hold their government more accountable.

The idea of decentralization in Ghana started during the colonial era. The colonial

masters (the British) adopted indirect rule to govern the Gold Coast colony through

local authorities. These local councils or authorities were responsible for the

oversight of public health, peace and order and the imposition of taxes and levies for

development at the grass root or local level.

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 16/95

2

Since independence, succeeding governments in Ghana have regarded

decentralization as a necessary condition not only for socio-economic development,

but also to achieve political objectives such as legitimacy and (paradoxically)

recentralization of power (Ayee 1994; 2004; 2008a). This is evidenced by over ten

(10) commissions and committees of enquiry established to look at decentralization

reforms. The introduction of the assembly system of local government in 1988 with

the passage of the Local Government Law, PNDCL 207 and its successor Local

Government Act, 1993 (Act 462) brought into being local authorities known as

Metropolitan, Municipal and District Assemblies (MMDAs) with legislating,

executing, budgeting, planning and rating powers.

In trying to carry out their duties, MMDAs encounter certain problems and challenges

including little fiscal autonomy and greater control by central government among

others. The then Upper West Regional Minister, Alhaji Isahaku Salia in his speech at

the launch of a four day public hearing of composite budgets for the various

Municipal and district assemblies in the Region, targeting coordinating directors,

planning officers and municipal and district finance officers which was published

on14th

October, 2011, observed that though Ghana’s decentralization programme

started in 1988, its fiscal component, which is a prime facilitator of the entire

decentralization policy, has been rather slow in changing. He said fiscal

decentralization involves a level of resource allocation to local government which

would allow it to perform decentralized functions, that is why according to him: “The

composite budget approach has been adopted to facilitate the transfer of resources to

the metropolitan, municipal and district assemblies”.Dr. Esther Ofei Aboagye, the

director of the institute for local government studies in her words at the Brong Ahafo

regional consultative forum for decentralization, indicated that several improvements

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 17/95

3

have been made in almost all areas of decentralization except fiscal decentralization.

This was resounded by the GTV’s regional diary on December 12, 2009. Ahwoi

(2000) and Nuama (2003) noted this earlier in their works. The decentralization

programme of Ghana has been anchored on four main inter-related pillars including:

Political Decentralization, Administrative Decentralization, Decentralized Planning

and Fiscal Decentralization. A widely cited World Bank report states that an effective

public sector in a modern developing country depends on the ability of the central

government to harness the resources of lower levels of government (Cochrane, 1983).

The over-reliance of local governments on central government transfers, which are

usually not predictable in terms of timing and magnitude, raises issues of concern.

Central government, development partners, district assembly functionaries, and the

local communities have become increasingly disturbed by the current state of fiscal

decentralization in Ghana. Whilst Ghana has made tremendous progresses towards

political, administrative and decentralized planning, a lot of problems and challenges

still need to be addressed especially in the area of fiscal decentralization. Fiscal

decentralization is defined as the ceding of expenditure and revenue mobilization

functions by the central government to MMDAs. Decisions about revenue generation

and expenditure are transferred from the central government to the local level. The

local units prepare tax collection models (Ahwoi 2009). This study thus, seeks to

examine the prospects and challenges of fiscal decentralization in Ghana using the Wa

Municipality as a case study.

1.2 Problem Statement

Fiscal decentralization is seen all over the world as an effective tool for good

governance and development. Since independence, succeeding governments in Ghana

have tried to exploit this tool by advancing the fiscal decentralization programme. The

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 18/95

4

introduction of the local government structure was therefore to transfer authority and

power to the MMDAs to enhance effective and efficient governance.

It is however interesting to note that most MMDAs in Ghana are unable to meet their

revenue generation targets because of central government’s restrictions and other

internal factors. This problem is more serious among the municipal and district

assemblies of which Wa Municipality is no exception. The Municipality’s inability to

generate enough funds from its internal sources makes it depend more on external

sources like the District Assemblies Common Fund (DACF) and donations for

development. The main problem with this issue is that, as the needs of the populace

are on the increase, the resources needed to fulfill these needs are not sufficient. As a

result the Municipality mostly depends on central government for funds to carry out

its developmental projects. However, the amount and timing of these inflows from the

central government is unpredictable and this retards the rate of development in the

Municipality. Though Ghana’s decentralization program started in 1988, its fiscal

component, which is a prime facilitator of the entire decentralization policy, has been

rather slow in changing. This is because MMDAs in Ghana are not completely

fiscally independent from the central government and their financing do not

commensurate with their responsibilities. The revenue raising powers given to

MMDAs are inadequate and as a result, local authorities depend mostly on central

government for funds to carry out their developmental projects and also the

responsibility for budgets preparation, administration and control of budgetary

allocations to the various departments is impeded hence the need for this research.

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 19/95

5

1.3 Research Objectives

The general objective of this research is to examine the challenges and prospects of

fiscal decentralization in Ghana. From the general objective, the following specific

objectives have been formed:

1. To find out the extent to which fiscal powers have been decentralized in the Wa

Municipality.

2. To assess the effectiveness of fiscal decentralization in the Wa Municipality.

3. To examine the challenges of fiscal decentralization within the Wa

Municipality.

4. To examine the prospects of fiscal decentralization in Ghana.

1.4 Research Questions

1. What is the extent of decentralization of fiscal powers in the Wa Municipality?

2. How effective is fiscal decentralization in the Wa Municipality?

3.

What are the challenges of fiscal decentralization within the Wa Municipality?

4. What are the prospects of fiscal decentralization in Ghana?

1.5 Significance of the study

The study is aimed at bringing to bare the challenges and prospects of fiscal

decentralization. This stems from the fact that little attention has been given to fiscal

decentralization as compared to all the other forms of decentralization. This study

seeks to identify the challenges of fiscal decentralization in the Wa Municipality and

ways of overcoming them. The study also seeks to bring on board development

partners and central government to undertake an effective economic planning in

promoting adequate development. It will also enable them to perform effectively

despite changing international economic conditions and structural adjustment

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 20/95

6

programmes designed to improve public sector performance which have created

serious fiscal difficulties for developing countries of which Ghana is no exception.

Also, the study will emphasize the need for fiscal autonomy in Ghana (the transfer of

fiscal powers from central government to MMDAs). This study also seeks to provide

some of the measures that can be put in place in order to ensure effective fiscal

decentralization in Ghana.

1.6 Scope and limitations of the study

The study area includes the Wa regional administration, the area councils of the

municipality, the eight main markets and selected communities within the

municipality.

As a result of the scattered nature of the geographical area, the study was limited by

the inability to cover all towns and villages. The study was as well limited by the

unwillingness of some citizens to provide information on their activities as it hammers

on revenue and tax activities. Coupled with this was the difficulty in administering of

the questionnaires due to inability of some citizens to respond to the questionnaires

especially the traders, businessmen and women owing to the busy nature of their

activities.

1.7 Organization of the study

The study is organized into five chapters which are summarized as follows: Chapter

one is made up of the background of the study, problem statement, research

objectives, research questions, significance of the study, scope and limitations of the

study and the organization of the study. Chapter two highlights on the literature

review related to the topic of the research. This covers the introduction, the definition

of key terms, history of fiscal decentralization in Ghana, overview of fiscal

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 21/95

7

decentralization in Ghana, Prospects of Fiscal Decentralization, Objectives and

implications of fiscal decentralization in developing countries, arguments for fiscal

decentralization, and challenges of fiscal decentralization. Chapter three deals with

the method of the research which covers the sources of data, the population and

sample of the study, methods of data collection and analysis, and the background to

the study. Chapter four is concerned with data analysis to achieve the objectives of the

study. It covers the analysis of secondary data, the primary data and the qualitative

analysis. Chapter five encompasses the summary of the findings of the research,

recommendations and finally, conclusion.

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 22/95

8

CHAPTER TWO

LITERATURE REVIEW

2.1 Introduction

This chapter deals with a review of information with regard to the topic of study. It

brings to bare already existing knowledge that has been published by other writers

and researchers on fiscal decentralization. It also provides a general overview of

decentralization and the challenges and prospects of fiscal decentralization.

Public service delivery by sub-national governments (SNGs) in many African

countries is tightly linked to subventions from central government. Inflexible transfer

systems that are rarely well defined often constrain the ability of local governments to

plan and to efficiently deliver basic public services, especially education and health.

Meanwhile, on-going political reforms on the continent will inevitably involve more

decentralization, where local governments are assigned greater responsibilities of

delivering key development projects and public services. This process should include

legal and administrative reforms that facilitate planning at the local government level,

in terms of identification of opportunities and mobilization of local as well as external

resources, including private savings, to meet the development goals of the local

community (Adam, 2007).

Prof J E A Mills the then vice president of the Republic of Ghana in his opening

address on the forum; “a decade of decentralization in Ghana retrospect and

prospects” in 2000, states; “Global trends in governance present many challenges for

governments and the governed alike. The demands of the governed are clearly for

satisfaction of their basic needs and rights and responsibilities for participation and

self-realization. Those who govern, on the other hand are constrained by what is

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 23/95

9

possible within the limitations of available resources and competing demands of

interest groups. The best way to reconcile these two viewpoints is to make the people

part of the decision making process through decentralization”.

2.2 Definition of key concepts

According to Rondinelli (1983), decentralization is defined as “the transfer or

delegation of legal and political authority to plan, make decisions and manage public

functions, from the central government and its agencies to field organizations of those

agencies”.

Ayee (2003) stated that, “decentralization is the transfer of responsibility (authority)

and resources (human and financial) and accountability from central government to

local self- governing entity. This involves long process of political, fiscal and

administrative decentralization. When only responsibility or authority is transferred

but not resources-there is de-concentration. When responsibility and resources are

transferred, there is delegation. When there is transfer of responsibility, resources and

accountability (partially or completely) there is devolution or democratic

decentralization”. According to Ayee, (1992) decentralization can be seen in the

following perspectives;

a. Devolution: “the legal conferment of powers upon formally constituted local

authorities to discharge specific or residual functions. Authority for making

decisions on certain issues is vested in sub-regional units of government and

central government”.

b. De-concentration: “a minimal transfer of power that is needed for decision

making on the spot although some latitude is given for routine decision

making. Field staff remained employees of the center and the center sets broad

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 24/95

10

guidelines within which the field is administered. Other names for de-

concentration are administrative decentralization, field decentralization and

bureaucratic decentralization”.

c. Privatization: “the transfer of activities formally performed by state agencies

to private sector thereby reducing the role of government. Privatization also

involves the market provision of goods and services”.

Atakora, (2006) defined decentralization as “the transfer of power and authority from

the central government to sub-units either by political, administrative, economic and

fiscal means.”

Fiscal decentralization is defined as the ceding of expenditure and revenue

mobilization functions by the central government to MMDAs. Decisions about

revenue generation and expenditure are transferred from the central government to the

local level. The local units prepare tax collection models, Ahwoi (2009).

According to Ahmed et al (2005: 6), fiscal decentralization has four major

components:

(1) Allocation of expenditure responsibilities by central and local governments;

(2) Assignment of taxes by government tiers;

(3) The design of an intergovernmental grant system; and

(4) The budgeting and monitoring of fiscal flows between different government tiers.

2.3 Overview of Fiscal Decentralization in Ghana

Fiscal decentralization entails entrusting local government units with the authority and

capacity to generate, allocate and utilize financial resources to promote socio-

economic development. According to Kokor and Kroes (2000), the objectives of

Ghana’s decentralization programme are to increase local revenue mobilization,

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 25/95

11

restructure allocation of resources to meet local needs and empower MMDAs to make

allocation decisions at the local level over both locally generated funds and those

transferred from the central government.

In furtherance of these objectives, the District Assemblies Common Fund was

established and has been in operation for over a decade. The allocations to each

MMDA are based on a formula approved by Parliament. Disbursements are made on

a quarterly basis and a quarter in arrears. The DACF is available to MMDAs only for

investment expenditure. In 2008, the proportion of total government revenue allocated

to the DACF was reviewed from 5% to 7.5 %. All MMDAs can only receive their

allocations upon the submission of their Annual Action Plans and Annual Budgets to

the Administrator of the DACF. MMDAs have also been mandated under section 245

of the 1992 Constitution and Act 462 to collect fees, fines, rates, tolls and licenses in

order to support socio-economic development in their areas. Further to this, several

legal instruments have been enacted to ensure transparency and accountability in the

use of financial resources at the local level. These include:

• Financial Administration Act, 2003 (Act 654, amendment to FAD, 1979,

SMCD 221)

• Financial Administration Regulations, 2004 (L.I. 1802, revoking the Financial

Administration Regulations, 1979, L.I. 1234)

• Public Procurement Act, 2003 (Act 663)

• Ghana Audit Service Act, 2000, (Act 658)

• Internal Audit Agency Act, 2004 (Act 656),

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 26/95

12

2.4 Objectives and implications of fiscal decentralization in developing countries

Literature indicates that only a few developing countries have adopted comprehensive

political, fiscal and administrative decentralization. Fiscal decentralization has four

major components:

i. Allocation of expenditure responsibilities by central and local governments;

ii. Assignment of taxes by government tiers;

iii. The design of an intergovernmental grant system; and

iv. The budgeting and monitoring of fiscal flows between different governments

tiers (Ahmed et al 2005: 6).

It should be noted that lack of meaningful political and administrative decentralization

often renders fiscal decentralization ineffective and hence complicates the analysis

(Guimaraes 1997). Instead of genuine political decentralization, central governments

in many countries appoint officials of sub-national governments, replacing

administrative decentralization with administrative deconcentration (where decision

making is shifted to regional or local officials of the central government) or

administrative delegation (where local governments undertake activities on behalf of

central government).The inability of central government to meet increasing demand

for local services underpins moves towards decentralization in developing countries.

Decentralization of fiscal responsibilities is envisaged to increase efficiency in service

delivery and reduce information and transaction costs associated with the provision of

public services (De Mello 2000b).

2.5 Arguments for fiscal decentralization

Accordingly, De Mello (2000b: 365) summarizes the arguments for fiscal

decentralization as follows:

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 27/95

13

i. Fiscal decentralization enables sub-national governments to take account of

local differences in culture, environment, endowment of natural resources,

and economic and social institutions.

ii. Information on local preferences and needs can be extracted more cheaply

and accurately by local governments, which are closer to the people hence

more identified with local causes.

iii. Bringing expenditure assignments closer to revenue sources can enhance

accountability and transparency in government actions.

iv.

Fiscal decentralization can help promote streamlining public sector activities

and the development of local democratic traditions.

v. By promoting allocation efficiency, fiscal decentralization can influence

macro-economic governance, promote local growth and poverty alleviation

directly as well as through spillovers.

Smoke (2001) also identifies three main reasons for the relevance of fiscal

decentralization in developing countries. These are:

i. The failure of economic planning by central governments in promoting

adequate development.

ii. Changing international economic conditions and structural adjustment

programmes designed to improve public sector performance which have

created serious fiscal difficulties for developing countries.

iii. Encouragement of the development of financial autonomy in developing

countries by changing of political climates. Thus, fiscal decentralization can

be considered relevant for effective governance, macroeconomic stability and

growth.

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 28/95

14

2.6 Extent of decentralization of fiscal powers

A particularly significant means of restricting local government autonomy is through

central government control of the purse strings. To what degree is local government

fiscally independent? To what extent is local government financing commensurate

with its responsibilities? How dependent are district authorities on central government

for their financing? How adequate are their own revenue raising powers?

District authorities have three sources of revenue: the District Assemblies’ Common

Fund, ceded revenue, and their own revenue-raising powers through local taxation.

The DACF is the main source, providing a constitutionally guaranteed minimum

share of government revenue, and thus some financial independence. Yet evidence of

its workings is somewhat mixed. On the one hand, annual monies distributed by the

DACF have increased quite significantly from 38.5 billion cedis in 1994 to 165 billion

cedis in 1999 in actual amounts, that is without taking inflation into account

(Nkrumah 2000: 63). On the other hand, it is disputed whether district authorities

have received the full five per cent, with annual allocations based on projections of

annual revenue, and invariably underestimated. A report for USAID states that DACF

disbursements have averaged about 4.3 per cent of actual annual revenue, though no

source is cited (USAID 2003: 15).A further argument is that the five per cent

minimum of national revenue is insufficient, given the broad range of responsibilities

devolved to district authorities. A second source of finance is ‘ceded revenue’. This is

revenue from a number of lesser tax fields that central government has ceded to the

DAs. Ceded revenue is still collected by the Ghanaian Internal Revenue Service

(IRS), but then transferred to DAs via the Ministry of Local Government and Rural

Development. Again, there is mixed evidence of its workings. Nkrumah (2000: 62)

suggests that ceded revenue has contributed quite substantial sums to local

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 29/95

15

governments, yet Ayee (2000: 32) cites evidence from his three case-study districts

that none had actually received such disbursements from central government. Local

authorities are not completely dependent on central government and do themselves

have some revenue-raising powers. Such local taxation is limited, however, with

Nkrumah (2000: 61) commenting that the “lucrative tax fields” (for example, income

tax, sales tax, import and export duties) all belong to the center, while local

government has access only to “low yielding taxes such as basic rates and market

tolls”.

Given the extensive responsibilities decentralized to district authorities, outlined

above, it is generally recognized that their financial position is weak. Local

government has little fiscal independence, remaining overwhelmingly dependent on

central government for its financial resources, with limited revenue raising ability.

Oyugi (2000: 12-3) suggests that the dependence of local authorities on central

government funding leads to a loss of ‘operational autonomy’, with local initiatives

undermined. The establishment of the DACF is certainly an advance in this respect,

providing a constitutionally guaranteed minimum, though the figure of five per cent

would seem inadequate. Yet we are also reminded that central government directives

determine 75 per cent of expenditure. Greater autonomy still would stem from the

ceding of greater revenue-raising powers, but the likelihood of such fiscal reforms is

slim. Overall, it appears that central government has been more willing to share its

responsibilities with local government than to share its revenue. The consequence of a

fiscal crisis for local government, perhaps generated by central government, would be

an inability to deliver public services in line with new responsibilities, in turn

undermining the DA’s legitimacy in the eyes of the local electorate. Any notion of

popular control is undermined by the truism that ‘he who pays the piper, call the

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 30/95

16

tune’, with DAs responding less to local taxpayers and more to the requirements of

central government.

Despite the constitutional provisions that implied an autonomous and lead role for

local government in initiating and coordinating local development policies (Article

240[2][b]), the evidence of the degree of central government control and the lack of

local government autonomy undermines any notion of ‘domains of discretionary

power’. It is further weakened by the discussion of powers and functions, noting the

extensive range of 86 functions decentralized to local government, yet the non-

existent or limited discretionary power in the majority of those areas. Full power and

responsibility only resides with district authorities for the minority of devolved public

services, estimated at 25 per cent of DACF expenditure. Where public services are

deconcentrated or delegated, DAs merely act as agencies for the central state or have

tasks delegated to them by central government ministries, with little or no

discretionary powers. There is little to suggest that DAs have become the principle

authority, providing direction and supervision to all other authorities in the district,

including central government departments and agencies, as outlined in constitutional

and legislative provisions. On the contrary, central government appears to remain

dominant at district level, in terms of top-down policy direction and guidance from

the Ministry of Local Government and Rural Development, the National

Development Planning Commission and the Ministry of Finance, and in terms of

policy implementation by central government agencies.

2.7 Effectiveness of fiscal decentralization

Significant progress has been made towards achieving fiscal and macro-economic

stabilization since the transition in most countries – progress which has importantly

changed the environment in which the decentralization process is taking place. There

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 31/95

17

has, however, been substantial variation in the nature and pace of reforms across

countries. In general, the Eastern European and Baltic countries, the most advanced

reformers, have made rapid progress. The intermediate reformers – the South-Eastern

European countries of Albania, Bulgaria, and the slow reformers – Armenia,

Azerbaijan, Belarus, Georgia, Tajikistan, Turkmenistan, Uzbekistan have been less

successful in establishing fiscal institutions, controlling fiscal imbalances, and

redefining the role of the state ( EBRD, 1998; Valdivieso, 1998).

2.8 Challenges of fiscal decentralization in developing countries

It has to be acknowledged that some modest gains have been achieved since the

process of fiscal decentralization was set in motion in Ghana. According to Kunfaa

(2002), despite the many negative stories about misappropriation of funds in

MMDAs, a significant number of development projects have been carried out on the

initiative of almost every MMDA throughout the country, which would not have been

the case if development was initiated from only the central government. A number of

bottlenecks towards fully institutionalizing fiscal decentralization in Ghana however

still remain. These include the following:

• Substantial authority has been given to MMDAs without accompanying

resources to fulfill the mandates;

•

Composite budget system has not been fully operationalized;

• MDAs continue to prepare budget estimates and account for expenditure on

sectoral basis at the district and regional levels;

• Limited discretionary authority of MMDAs over funds from DACF;

• Weak local revenue generation and mobilization capacity of MMDAs

• Untimely disbursement of funds from DACF; and

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 32/95

18

• Substantial deduction in the quarterly DACF allocation to the MMDAs to

finance national level programme, for example National Youth Employment

Programme, Fumigation among others.

• Variances in the amounts allocated, disbursed and actually received by

MMDAs from the DACF. The variations were as a result of the fact that

certain expenditures were incurred on behalf of MMDAs and the cost

deducted at source.

According to De Mello (2000b), some of the challenges of fiscal decentralization

include the following:

2.8.1 Intergovernmental transfers

The failure to adequately address the question of how to manage intergovernmental

fiscal relations in order to meet the growing needs for public services at the local level

while preserving fiscal discipline nationally and sub-nationally. This requires

institutional clarity and transparency to avoid coordination failures that lead to

inefficient spending by local governments manifested in deficit bias and higher

borrowing costs that can aggravate macro-economic imbalances and instability. To

avoid such undesirable outcomes, there is a need for incentives and capacity building

on top of institutional checks and balances to ensure prudence in sub-national fiscal

management.

2.8.2 Expenditure management and financing

Assignment of expenditure and financing responsibilities to sub-national

governments can adversely affect service delivery in different ways. For example

decentralization of water and sanitation services to small local governments in Latin

America have led to a loss of economies of scale in service delivery. Many

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 33/95

19

governments in Latin America and Africa keep the financing of health and education

at national level because the spillover effects from health and education outcomes and

their impact on equity are national. Assignment of certain business taxes to local

levels in the United States have led to inefficient tax competition, constraining the

ability of municipalities to generate revenue and deliver services.

2.8.3 Adequacy of local revenues and autonomy

The lack of clearly defined, stable and uniform revenue assignments between the

center and sub-national governments inherent in this approach has weakened

budgetary management at the sub-national level and created perverse incentives for

sub-national governments to either hide locally mobilized revenue sources in extra-

budgetary funds or to simply reduce their efforts to mobilize revenues locally.

Punitive “extractions” by higher level governments in the form of clawing back any

additional revenues raised by lower level governments through reduced sharing rates

have also created perverse incentives for revenue mobilization, at the local levels in

many countries. This led to surplus funds being trapped in the treasury system and

captured by the central government by the end of the year. The resultant non-

uniformity in revenue sharing and the absence of stability undermined sound fiscal

management at the local level (Banks and Pigey 1988).

Some of the provisions in the Local Government Service Act, 2003 also pose some

challenges for MMDAs which include the following:

2.8.4 Local government borrowing

Subject to article 181 of the Constitution and to subsection (2), a District Assembly

may raise loans or obtain overdrafts within the Republic of the amounts, from the

sources, in the manner, for the purposes and on the conditions approved by the

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 34/95

20

Minister in consultation with the Minister responsible for Finance. An approval is not

required where the loan or overdraft does not exceed twenty million cedis and the

loan or overdraft does not require a guarantee by the Government. This poses a

challenge to local government (local government Services act, 2003 Act 656).

2.8.5 Budget discretion

Subject to section 3(a) (ii) of the Local Government Act, 2003, MMDAs are to

prepare the budget of the district related to the approved plans to the Minister

responsible for Finance for approval. Most often, not all the estimates in the budget

are usually approved by the Minister of Finance and this constitutes a challenge for

MMDAs. The ability of central authorities to pursue fiscal consolidation at the

expense of sub-national budgets by unilaterally transferring financial obligations for

politically sensitive social protection programmes, without providing a compensatory

increase in sub-national revenues demonstrates that in many countries expenditure

assignments continue to lack integrity, clarity and stability. The infringement on sub-

national budget autonomy is further extended by the fact that while transferring the

financial responsibility, central authorities retain control over key cost parameters

such as allowable rental charges for housing, administered prices for utilities,

minimum wages and benefit rates. Typically, the transfer of social protection

spending to local governments is an unfunded mandate. The persistence of such

unfunded mandates constrains sub-national budgetary autonomy and undermines

fiscal accountability by preventing a clear distinction between central and sub-

national responsibilities.

The adverse effects of decentralization on service delivery arise due to a number of

common factors. These factors include: first, lack of capacity at sub-national

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 35/95

21

government level, which restricts local service delivery, because local authorities lack

the ability to manage public finances and keep proper accounting procedures, second,

misalignment of responsibilities owing to incomplete decentralization or political

factors, for example, while local authorities may be responsible for education, higher

levels of government pay teachers, third, political capture by local elites when civic

participation in local government is low, finally, other problems including a soft

budget constraint that leads to over borrowing by sub-national governments. To

overcome these challenges, optimal assignment of expenditure and tax responsibilities

should be based on such criteria as economies of scale, spillover benefits, and cost of

administering taxes, tax efficiency, and equity. In practice, however, fiscal

decentralization often depends on political realities expediencies and historical

legacies (Ahmed et al 2005).

Recent studies suggest that the design and implementation of a multi-tier system of

government can significantly affect overall resource allocation in the economy and,

hence, economic efficiency, growth, and welfare (Davoodi and Zou, 1998; Martinez-

Vazquez and McNab, 2003; Akai and Sakata, 2002). A central argument for fiscal

decentralization leading to improved resource allocation rests on the assumption that

fiscal decentralization increases local influence over the public sector. However, in

theory, there is an equal possibility that fiscal decentralization simply transfers power

from national to local elites and that improved access of local elites to public

resources increases opportunities for corruption (Bardhan and Mookherjee, 2000).In

light of the possible effects – that depend on the institutional design – of fiscal

decentralization on economic growth, macro-economic management and corruption, a

key challenge for many transition economies has been to reap the economic benefits

of decentralization while maintaining control over public expenditures and borrowing,

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 36/95

22

restoring growth and improving accountability of local governments and officials to

limit corruption.

2.9 Prospects of Fiscal Decentralization

To address the related challenges with fiscal decentralization in Ghana, a number of

initiatives are being implemented. An inter-governmental fiscal framework that

clearly assigns service responsibilities between the central government and the sub-

national level has been developed and is being implemented. A Municipal Finance

Bill to assist local governments to source funds from the open capital market is being

considered by Parliament. In a bid to further strengthen the fiscal capacity of

MMDAs, the Ghana government and Development Partners (DPs) have introduced

the District Development Facility (DDF). This facility exists to provide additional

financial resources to MMDAs through an annual performance assessment to enable

them implement programmes and projects in their Medium-Term Development Plans

(MTDPs). The Ministry of Local Government and Rural Development also intends to

introduce the concept and practice of “municipal contracts” whereby Metropolitan

and Municipal Assemblies would be assessed at the technical/urban, financial and

organizational levels with a view to granting them additional financial assistance to

implement projects identified in a Priority Investment Programme prepared after the

assessment (Kunfaa, 2002).

In ensuring effective implementation of a good fiscal decentralization programme,

Smoke (2001) identifies five critical elements. These elements are:

• An adequate enabling environment;

• Assignment of an appropriate set of functions to local governments;

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 37/95

23

• Assignment of an appropriate set of local own-source revenues to local

governments;

• The establishment of an adequate intergovernmental fiscal transfer system;

and

• The establishment of adequate access of local governments to development

capital.

According to Jorge (2011) different countries are at different levels of development

and refinement of their decentralized fiscal frameworks. Furthermore, the following

measures can be put in place in order to address the challenges of fiscal

decentralization in developing countries:

2.9.1 An Agenda for Reforming Expenditure Assignment and Management

A clear assignment of expenditure responsibilities should be at the top of national

reform agenda for local government finance. The following topics must be addressed:

i. Exclusive responsibilities must be identified.

ii. For concurrent competencies, specific responsibilities for various aspects—

regulation, financing, and implementation—must be assigned.

iii. Higher level controls on local expenditures must be appropriately limited.

iv. With limited administrative capacity, asymmetric assignments between central

and local governments should be considered.

v. Methods to translate responsibilities into expenditure needs and financing

requirements should be developed.

vi. Unfunded mandates must be avoided.

vii. Funding and staffing of deconcentrated offices of line ministries should be

downscaled or eliminated if services are devolved.

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 38/95

24

viii. Implementation of expenditure decentralization needs to be strategic (capacity

building and technical assistance).

2.9.2 An Agenda for Improving Local Revenue Generation and Autonomy

The overarching goal should be to increase reliance on own revenues with meaningful

discretion.

In addition:

i. Reforming and modernizing property tax administration must be a priority;

and

ii. Diversifying sub-national tax bases:

a) Avoiding nuisance taxes and economic distortions;

b) Creating a shortlist of other good local taxes: vehicle taxes, business

license taxes, and betterment levies on real estate;

c) Implementing business taxes which offer opportunities (using sales

turnover as a proxy, but avoiding conflict with national value-added

taxes);

d) Furthering local tax autonomy through introduction of a local

“piggyback” personal income tax with a flat rate and possibly

payroll taxes; and

e)

Implementing “green” taxes related to waste management, water and

air-polluting activities, and the production of energy.

2.9.3 An Agenda for Reforming Intergovernmental Transfers

Reforming intergovernmental transfers has several requirements. Among them are the

following:

i.

Assuring predictable, regular, and transparent transfer mechanisms;

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 39/95

25

ii. Securing an appropriate balance among the various types of transfers (using

separate instruments for separate goals);

iii. Expanding and improving the use of equalization transfers based on a formula

using measures of expenditure needs and fiscal capacity and introducing an

explicit rule for the pool of funds to be distributed determining the source in

origin (fraternal—or contributions by richer jurisdictions versus vertical—or

contributions by the central government, and in the latter case, also

determining the amount as a percentage of central government revenues);

iv.

Reviewing and improving mechanisms for allocating resources under

conditional grants (rule based as opposed to discretionary);

v. Consolidating specific grants where large numbers of poorly coordinated

programmes exist into fewer “block” grants—providing larger but still

conditional discretion to sub-national governments;

vi. Implementing performance-based grants for encouraging budget process

reforms and improvements in service delivery; and

vii. Rationalizing capital grants (what is being pursued) and coordinating with

borrowing policies.

2.9.4 Local Government Borrowing and Investment Finance

To varying degrees, many countries in Asia and Africa, such as Indonesia,

Philippines, Ghana, and Nigeria allow for local government borrowing within a

regulated framework. Prudent, fiscally responsible local government borrowing needs

to be promoted in many countries in these regions. Legal and regulatory frameworks

for local government borrowing need to be strengthened. Options and support

mechanisms for local government borrowing must be expanded, including support,

where appropriate, to intermediate financial institutions or municipal development

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 40/95

26

funds (such as in the Philippines). Given the needs for public infrastructure, other

financing mechanisms should have wider adoption [tax increment financing,

betterment levies (valorization), and public–private partnerships].

2.9.5 Better Framing of Institutional Reform

The reforms above should be reinforced by other measures of an institutional nature:

i. Strengthen regular and systematic dialogue between sub-national

governments and the central government on intergovernmental financial

policy.

ii. Where deconcentrated units coexist with decentralized governments, identify

the right roles for and interactions between deconcentrated and devolved

government entities.

iii. Rethink the role of parallel institutions (social funds, etc.) to sub-national

units and try to limit them and incorporate them into the main sub-national

government stream.

2.10 History of decentralization in Ghana

Since independence, succeeding governments in Ghana have regarded

decentralization as a necessary condition not only for socio-economic development,

but also to achieve political objectives such as legitimacy and (paradoxically)

recentralization of power (Ayee 1994; 2004; 2008a). These political objectives

explain in part why the progress of decentralization has been slow and has often

resulted in recentralization, despite over 10 commissions and committees of enquiry

established to look at decentralization reforms. For instance, the post-colonial

government of the Convention People’s Party (CPP) under Kwame Nkrumah (1957–

1966) fearing that decentralization would promote divisive tendencies, encouraged

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 41/95

27

centralization of power in the nation’s capital, particularly the Office of the President.

The government also at times has fragmented the decentralized units as a way of

weakening them (Ayee 1994). In addition to these, charges of corruption and

ineptitude particularly in the CPP era have tainted their effectiveness. The local

government service was also hampered by the insecurity local government workers

felt in relation to their conditions of service, pay equity, and general well-being; a

unified civil service was considered desirable to enhance local administration. These

weaknesses, as well as other shortcomings (such as the dual hierarchy structure in

which the central and local government institutions operated, a lack of political and

bureaucratic commitment to decentralization, and inadequate financial and human

resources) continued up to the passage of local government reforms in 1988 (Ayee

2004a, b).

Under the Provisional National Defense Council (PNDC) from 1981 up to the

elections of 1992, Ghana undertook a range of efforts to extend governance at the

local level, and some of these were later incorporated into the present-day system.

This included the creation of local cells initially called “Committees for the Defense

of the Revolution,” along with Unit Committees. In 1988, the PNDC established the

District Assembly system with the passage of Law 207. The 1992 Constitution, along

with subsequent statutes and enabling legislation, superseded the pre-existing local

governance system and reorganized it to constitute a new framework. This

Constitution was the origin of the current arrangement, and was elaborated upon in

1993 with the Local Government Act, and with subsequent legislation. Ghana’s

decentralization sequence moved from administrative decentralization (beginning in

the 1980s) to political decentralization (with elections in 1988 and the Constitution of

1992) and then to fiscal decentralization (after 1994).

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 42/95

28

CHAPTER THREE

METHODOLOGY

3.1 Introduction

This chapter explains the methodology employed by the researcher to carry out the

research work. The chapter also outlines how the researcher gathered information

from a wide range of approaches and analytical techniques which were used as the

basis for interpretations, explanations, inferences and predictions. It also highlights

the population of the study, the sample size, and the sampling technique, sources of

data, method of data collection as well as data analysis.

3.2 Research methods

This research adopts both qualitative and quantitative approaches. Qualitative

approach often categorizes data into patterns as the primary basis for organizing and

reporting results. The qualitative approach typically would use the following methods

for gathering information: observation, interview, open-ended questions and analysis

of documents and materials in order to gather non-numerical data. The quantitative

approach on the other hand would use highly structured methods such as close-ended

questions in gathering numerical data.

3.3 Data sources

The sources from which data was gathered for this research has been grouped into

two, namely primary and secondary data sources.

3.3.1 Primary sources of data

The primary sources from which data was collected were, administering of

questionnaires to the officials of the Municipality comprising the municipal finance

officer, the accountant, municipal planner, budget officer, the municipal chief

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 43/95

29

executive, the municipal coordinating director, who are better placed to provide first-

hand information on fiscal decentralization of the municipal assembly. Some

questionnaires were also administered to the revenue collectors and ordinary citizens

of the eight towns in the Wa municipality including ,Wa township, Busa, Charia, Boli,

Kpongu, Kperisi/Mengwe, Goripie, Kolkpong, to obtain first-hand information from

them to compare with that of those in the offices.

3.3.2 Secondary sources of data

The secondary sources from which data was collected were; rates fixing resolutions,

annual budgets and management reports on the comparison of budgets against actual,

Municipal Chief Executive (MCE) session reports, journal reports, newspaper

articles, the World Wide Web (internet),and books among others.

3.4 Sample Population and Sample Size

The population of this research covered all the eight towns within the Wa

Municipality. However, because of the dispersed nature of the geographical area and

large size of the population of 221,905 (2000 population and Housing census), there

search could not cover the entire population and hence a sample population was

drawn. The sample population for this research was made up of the entire population

out of which 150 was selected as the sample size.

3.5 Sampling techniques

Due to the dispersed nature of the population and the diversity of stakeholders in the

municipality, quota sampling which is a non-probability sampling technique was used

to assign quotas to the various sub-groups where the data was collected from in order

to ensure that views of the different stakeholders were captured and data collected is a

representation of the entire municipality. For the officials of the municipality,

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 44/95

30

purposive sampling which is a non-probability sampling technique was used to select

respondents who fell within the quota. For the revenue collectors of the eight towns,

respondents who fell within the quota were selected using convenience sampling,

which is a non-probability sampling technique. For the general public, a non-

probability sampling technique known as convenience sampling was used to select the

respondents who fell within the quota.

In line with the research objectives and the nature of fiscal decentralization in the

municipality, a quota of fourteen (18) people was given to the officials of the

municipal assembly, twenty-four (20) people to revenue collectors of the eight towns

with two or three people assigned to each town and one hundred and twelve (112)

people to the ordinary citizen who were further divided into fourteen (14) people each

to the eight towns.

3.6 Data Collection Instruments

The use of questionnaires and interview guides were the main data collection

instruments for the research.

3.6.1 Interview

For the purposes of this research, a semi-structured interview was employed. With

this, a set of questions based on the objectives of the study were prepared but other

questions were also asked emanating from responses given by the respondents. Group

interviews as well as face to face interviews were conducted for the ordinary citizens

in the eight towns. This form of data collection was used as a result of the following

reasons.

1. It afforded the researchers the opportunity to escape any issue of restriction

created by strictly going by predesigned questions.

8/11/2019 Final Project- Fiscal Decentralization(1)-1

http://slidepdf.com/reader/full/final-project-fiscal-decentralization1-1 45/95

31

2. It gave the opportunity for the researchers to ask follow up questions to answers

given by respondents. Misunderstandings were cleared up immediately during the

interview.

3. The researchers were also able to reword and reorder the questions as and when it

became necessary.

3.6.2 Questionnaires

Both closed and open ended questionnaires were used in the data collection exercise.

The closed ended questions were followed with options from which respondents

could choose. Some of the questions were closed because of the inhabitants’ level of

understanding of issues concerning fiscal decentralization in the municipality. For

respondents who could not understand the English Language, the questions were

explained to them in their local dialect by the researchers. The questionnaires totaling

one hundred and fifty (150) were interviewer-administered and respondents who had

difficulties in answering were assisted to answer the questions and all answered

questionnaires were submitted on the spot. This was done because it was envisaged

that many would not return the questionnaires when allowed to take them home to