final project 1

DESCRIPTION

final project report on axis bankTRANSCRIPT

Report of Summer Training Conducted at

Axis Bank

Submitted in partial fulfillment of the requirements

for the award of the degree of

Master of Business Administration (MBA)

To

Guru Gobind Singh Indraprastha University, Delhi

Guide: Submitted by:

Guide Name: Ms. Gayatri Chopra Student Name: Preeti Saini

Roll No.:19619103913

Gitarattan International Business School

New Delhi -110085

Batch 2013-15

CERTIFICATE

I, Ms. Preeti Saini, Roll No -19619103913 certify that the summer training report (Paper

Code MS-201) entitled “Axis Bank” is done by me and it is an authentic work carried out

by me at Axis Bank. The matter embodied in this Report has not been submitted earlier

for the award of any degree or diploma to the best of my knowledge and belief.

Signature of the student

Date:

Certifies that the Summer Training Report (Paper Code MS-201) entitled Axis Bank

done by Ms. Preeti Saini, 1919103913 is completed under my guidance.

Signature of the Guide

Date:

Countersigned

Director/Project Co-ordinate

ACKNOWLEDGEMENT

On the very outset of this report, I would like to extend my sincere & heartfelt obligation

towards all the personages who have helped me in this endeavour. Without their active

guidance, help, cooperation & encouragement, I would not have made headway in the

project.

I wish to express my indebted gratitude and special thanks to Mr Arun Bahri, Branch

Head, AXIS BANK" who in spite of being extraordinarily busy with his duties, took time

out to hear, guide and keep me on the correct path and allowing me to carry out my

industrial project work at their esteemed organization and extending during the training.

I express my sincere gratitude to our Director, Dr. D. S. Chaturvedi who has been my

source of inspiration. And also I am thankful to our Project Coordinator Ms Uma Gulati

for her immense support and guidance.

I am extremely thankful to my faculty Ms Gayatri Chopra for her valuable guidance and

support on completion of this project.

Preeti Saini

CONTENTS

S. No Topic Page no.

1 Certificate (s)

2 Acknowledgements

3 List of Tables

4 List of Figures

5 Executive Summary

6 Chapter-1: Profile of the Firm/Company

7 Chapter-2: SWOT Analysis of the Company

8 Chapter-3: Data Collection & Presentation

9 Chapter-4: Functional Analysis of the Company

10 Chapter-5: Summary & Conclusions

11 References/Bibliography

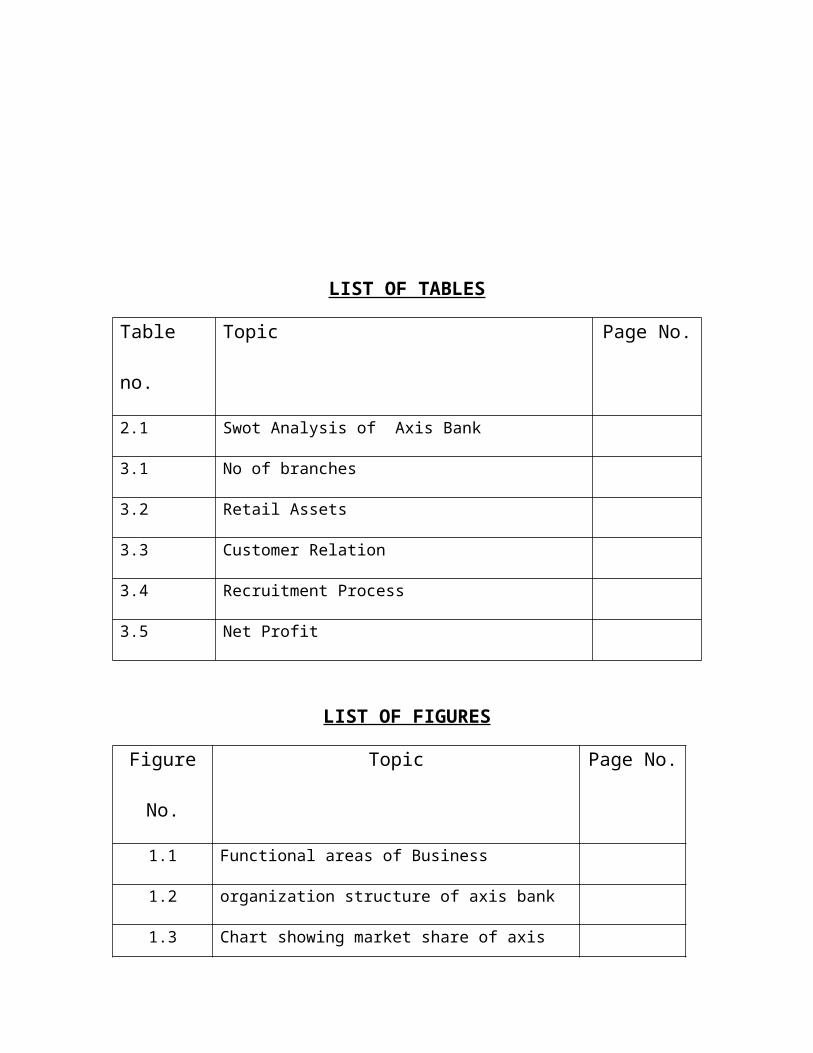

LIST OF TABLES

Table no. Topic Page No.

2.1 Swot Analysis of Axis Bank

3.1 No of branches

3.2 Retail Assets

3.3 Customer Relation

3.4 Recruitment Process

3.5 Net Profit

LIST OF FIGURES

Figure No. Topic Page No.

1.1 Functional areas of Business

1.2 organization structure of axis bank

1.3 Chart showing market share of axis bank

1.4 Present Leaders of axis bank

2.1 SWOT Analysis

3.1 No. of branches

3.2 Retail Assets

3.3 Customer Relation

3.4 Net Profit

4.1 Porter’s model

Executive Summary

There has been a rapid growth in the banking industry in the past few years. In the

residential sector, a growing middle class is enjoying rising income levels. Combined

with smaller household sizes, this demographic change has boosted demand for more

modern housing and home loans. Meanwhile, increasing consumer spending power has

encouraged growth in organized retailing – both feeding off and contributing to the spear

of ‘mall culture’ and the popularity of other large-scale retail property developments.

In the commercial property segment, strong growth in the services sector – particularly in

the IT and ITES sectors – and corporate growing scale of operations have led to greater

demand for commercial space, including modern offices, warehouses and lodging space.

Many Developers have substantial plans to increase both their size and geographical

spread. They are also expanding into different kinds of properties, which can boost the

firms’ franchise values and reduce concentration risks. However, managing and financing

such activities can be a challenge, and puts a premium on financial flexibility, capital

access and operational infrastructure.

The project assigned to me has an objective to find and analyze the current scenario of

Axis bank, covering the preferences of current as well as prospective customers. The

major part of the project also analyses the size of investment in various states and mind

set of the customers regarding this as well as the perceptions of customers towards major

leading Axis Bank players.

Once the data was collected, this data was analyzed and various conclusions were drawn.

Researchers’ viewpoints on various issues were also taken in order to get a more insight

into the Axis Bank.

They can provide the introduction All About the axis bank. All information related to the

Branch or the various leaders of Axis bank or the Structure of Axis Bank. what is the

mission and vision of bank also define the products.

They are related with SWOT of the Axis bank. In which they can explain the strengths,

weakness, opportunities and the threats of Axis bank

They are explain the functional area like marketing, HR, finance and production and

operation. They can also be present through the graphical presentation. In the marketing

they can explain the product, advertisement, promotional strategies etc in the HR they

can explain the about the recruitment and selection process of Axis bank. And finance

can provide the balance sheet and profit and loss account.

They can provide the analysis of all functional areas and they are- Marketing, HR,

finance, It Technology, production & operation.

It can include the conclusion, suggestion which can be done on the basic of fact and

figure which can provide by p roject report. lesson that have learn during the intership.

Chapter-1

PROFILE OF THE COMPANY

1.1

Name of The Firm : Axis Bank

Address : Ground floor and basement plot no. 104,

pocket-27,sector 24,rohini,New Delhi

TeleFax : 011-27042808

Telephone : 011-27042805

Website : http://www.axisbank.com

E-Mail : [email protected]

Type : Multinational company

Industry : Banking services

Headquarters : Hyderabad, India

Registered office : NPCI,5th floor, “gigaplex”,

Plot no I.T.5,MIDC,Airoli

Knowledge park, Mumbai 400708

1.2Nature of axis bank

It was incorporated in the year 1993 as ‘UTI Bank Ltd’ which provided corporate and retail

banking products and was the first private bank to have begun operations in 1994,after the

government of India allowed new private banks to be established. The bank was promoted jointly by

the Administrator of the Specified Undertaking of the Unit Trust of India (UTI), Life Insurance

Corporation of India (LIC), General Insurance Corporation Ltd.,National Insurance Company Ltd.,

The New India Assurance Company, The Oriental Insurance Corporation and United India

Insurance Company. UTI holds a special position in the Indian capital markets and has promoted

many leading financial institutions in the country. The bank changed its name to Axis Bank in April

2007 to avoid confusion with other unrelated entities with similar name. After the retirement of Mr.

P. J. Nayak, Shikha Sharma was named as the bank's managing director and CEO on 20 April 2009.

The bank has strength in both retail and corporate banking and is committed to adopting the best

industry practices internationally in order to achieve excellence.

The recommendation for name change to Axis Bank has arisen from the existence of several

shareholder-unrelated entities using the UTI brand, and the consequent brand confusion that this

generates.The name UTI bank was changed to AXIS bank as UTI gave a look of government sector

bank. They had to change the name to have own brand and identity. The name was taken into effect

consequent to the approval of shareholders, Reserve Bank of India and the central government

(Registrar of Companies). The UTI brand is owned by UTI Asset Management Company. The bank

change the logo and colour of logo the bank was likely spent around Rs 50 crore in the re-branding

exercise.REBRANDING has retained the burgundy color, but has changed the logo.The bank

acquired the services of Ogilvy & Mather (O&M) to design and implement the rebranding

campaign. The new name ‘AXIS’was chosen considering the bank’s pan-Indian as well as

international presence. The first time that a bank has dropped an established brand for an unknown

name.The name Axis is chosen as it is simple and it conveys a sense of solidity and a sense of

maturity. It also has a universal appeal. The New Logo depicts a strong growth path for the bank

supported by a strong base, indicating that the bank is moving on from a position of strength.

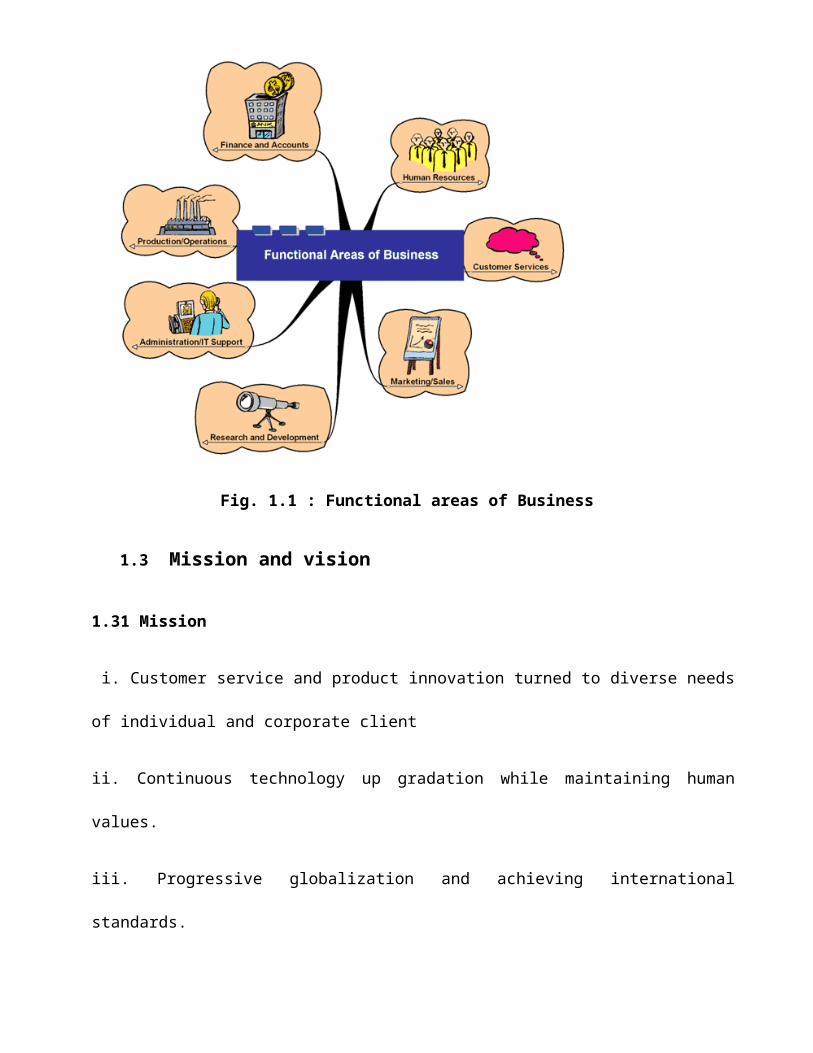

Functional Areas

Functional areas can be defined as grouping of individuals on the basis of their functions, each

performs in the organisation such as financing, marketing, manufacturing, customer services, R&D,

IT, HR & operations.

Fig. 1.1 : Functional areas of Business

1.3 Mission and vision

1.31 Mission

i. Customer service and product innovation turned to diverse needs of individual and corporate

client

ii. Continuous technology up gradation while maintaining human values.

iii. Progressive globalization and achieving international standards.

iv. Efficiency and effectiveness built on ethical practices.

v. Customer Service and Product Innovation tuned to diverse needs of individual and corporate clientele.

1.32 Vision

To be preferred financial solutions provider excelling in customer delivery through insight,

empowered employees and smart use of technology.

1.33 CORE VALUES

Customer Centricity

Transparency

Teamwork

Ownership

Ethics

1.4 Product range of axis bank

1.41 Savings Account

i. Easy Access Savings Account

ii. Prime plus savings Account

iii. Pension Savings Account

iv. Insurance Agent Account

v. Small Savings Account

vi. Prime Savings Account

vii. Women’s savings Account

1.42 Salary Account

i. Prime Salary Account

ii. Priority Salary Account

iii. Defense Salary Account (Power Salute)

iv. Wealth Salary Account

v. Easy Access Salary account

1.43 Current account

i. Resident Foreign Currency(Domestic) Account

ii. Regular Current Accounts

iii. Exclusive Current Account

iv. Current Accounts by Industry

1.44 Insurance

i. Life Insurance

ii. General Insurance

iii. Health Insurance

iv. Motor Insurance

v. Jewellery Insurance

vi. Home Insurance

vii. Travel Insurance

1.44 Loans

i. Home loans

ii. Car Loans

iii. Personal Loans

iv. Loans Against Property

v. Loans Against Share

vi. Loans Against Securities

vii. Loan Against Gold

viii. Education Loan

ix. Loan against Fixed Deposit

1.45Cards

i. Titanium Smart Credit Card

ii. Platinum Advantage Credit Card

iii. Visa Signature Credit Card

iv. Visa Infinite Credit Card

a. Business Banking

The Bank offers a wide range of current account product and cash management solutions for

corporate, institutional, central and state government departments as well as small business

customers.

b. Small & Medium Enterprises

At Axis Bank we understand that timely availability of credit is an integral ingredient to success.

With this in mind our ongoing endeavour is to be a financial partner that lets businesses focus on

business while their financing needs are in safe hands with the bank.

1.47 Agri Business Loans

i. Kisan Power

ii. Power Gold

iii. Arthia Power

iv. Agro Power

c. Corporate Credit Card

Axis Bank Corporate/Purchase Card Solution offers best-in-class customizable product features,

comprehensive reporting and expense management tools as well as round-the-clock service. It helps

your corporate save time and money by simplifying your purchase, bill payment and expense

management processes. To facilitate the above, the Bank also appoints a dedicated Relationship

Manager to ensure prompt response to all service related queries.

d. Treasury

Axis Bank has built a strong integrated Treasury book across domestic and global

markets by effectively managing liquidity and maximizing income by trading in financial

markets

Infrastructure Business

The Bank has consulted, financed and executed a wide range of projects ranging across roads,

highways, bridges and other large scale Infrastructure projects. Our expertise covers risk

management and mitigation, financial planning and sourcing of funds, project advisory and

negotiations.

1.48 Foreign Exchange

i. Travel Card

ii. Outward Remittances

iii. Foreign Currency Demand Drafts

iv. Foreign Currency Cash

v. Foreign Currency Travellers’ Cheques

vi. India Travel Card

e. Travel Currency Card

Axis Bank is the first Indian Bank to launch Travel Currency Card. This is a secure, convenient and

hassle-free way to carry money and make payments when on foreign shores and aims to make

travelling abroad a truly memorable experience. Axis Bank is the first Bank in India to achieve a

loading of US Dollar One Billion. The Card is accepted worldwide and is available in nine currency

options.

f. Salary Product

At Axis Bank we provide tailor-made privileges to our Salary Account holders with a range of

banking, investment and lending solutions under one roof. It is a unique offering wherein we offer

not just the best products but also the choice of how you want to give them to your employees.While

the same salary account variant can be offered to all employees, you can also give them the freedom

to choose a higher salary account variant and the associated privileges, as per their net salary

eligibility.

Prepaid Cards

i. My Money Card

ii. Gift Cards

g. Syndication

The bank is a leading provider of debt solutions in the form of bond or debenture issuances and loan

syndication and has successfully managed various debt issuances of mid and large sizes. The bank is

the largest bond house in the country and has been ranked first in terms of various domestic and

international league tables in terms of domestic debt insurances. Its clientele includes leading public as

well as private sector corporate.

h. Online Trading

TRADING ACCOUNT

Axis Direct’s 3-in-1 Online Trading Account offers seamless integration between your

Savings, Demat& Trading accounts, all three of which are required to trade online. The

Savings and Demat accounts are offered by Axis Bank while the trading account is held

with Axis Securities and Sales Ltd. This arrangement allows hassle free and seamless

direct debit/credit of funds/shares, to and from the customer’s account.

i. Inward Remittances

AXISREMIT Online

AXISREMIT Direct

Money Transfer Operators - (Money Gram, Easy Remit, Express Money )

Wire Transfers

1.5 Size of Organization

Size of Manpower

The Bank has branches in over 36 states covering a wide varoius area of the country.

Employees come from varied cultural, social.

Employees are Bank’s greatest assets. As of 31 March 2014, 42,420 employees were part

of the AXIS Bank. The follow a non-discrimination policy with regards to employment

and have employees with varied degrees of disabilities in certain functions of the bank.

Turnover and Financials (Over 34034.78 Crores)

Profit and Loss Account: Year ended March 31, 2014

For the year ended March 31, 2014, the Bank earned total income of `11951.64’ crores.

The Banks Net Profit for the year ended March 31, 2014 was `6217.67’ crores, up

27.92%, over the year 2013

Balance Sheet: As of March 31, 2014

The Bank’s total balance sheet size increased to Rs 3,83,244.89crores as of March 31,

2014 from Rs 3,40,560.66crores as of March 31, 2013. Total net advances as of March

31, 2014 were Rs 2,30,066.76crores, as increased March 31, 2013. Total Deposits were

Rs 2,80,944.56crores, an increase March 31, 2013

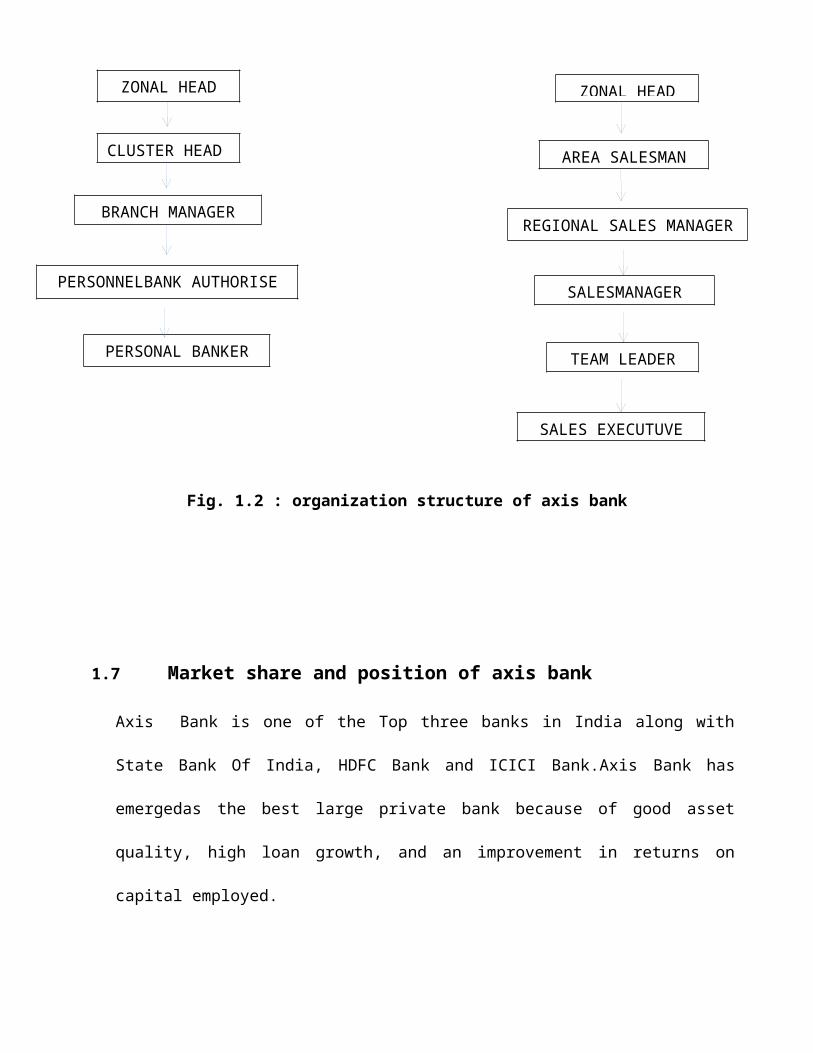

1.6 Organization structure of axis bank

Fig. 1.2 : organization structure of axis bank

MANGING DIRECTOR

DIRECTOR

EXECUTIVE DIIRECTOR

ZONAL HEAD

REGIONAL HEAD

CLUSTER HEAD

SALESMANAGER

PERSONAL BANKER

NATIONAL HEAD

ZONAL HEAD

RETAIL AND BRANCH BANKING HEAD

PERSONNELBANK AUTHORISE

BRANCH MANAGER

TEAM LEADER

AREA SALESMAN

REGIONAL SALES MANAGER

SALES EXECUTUVE

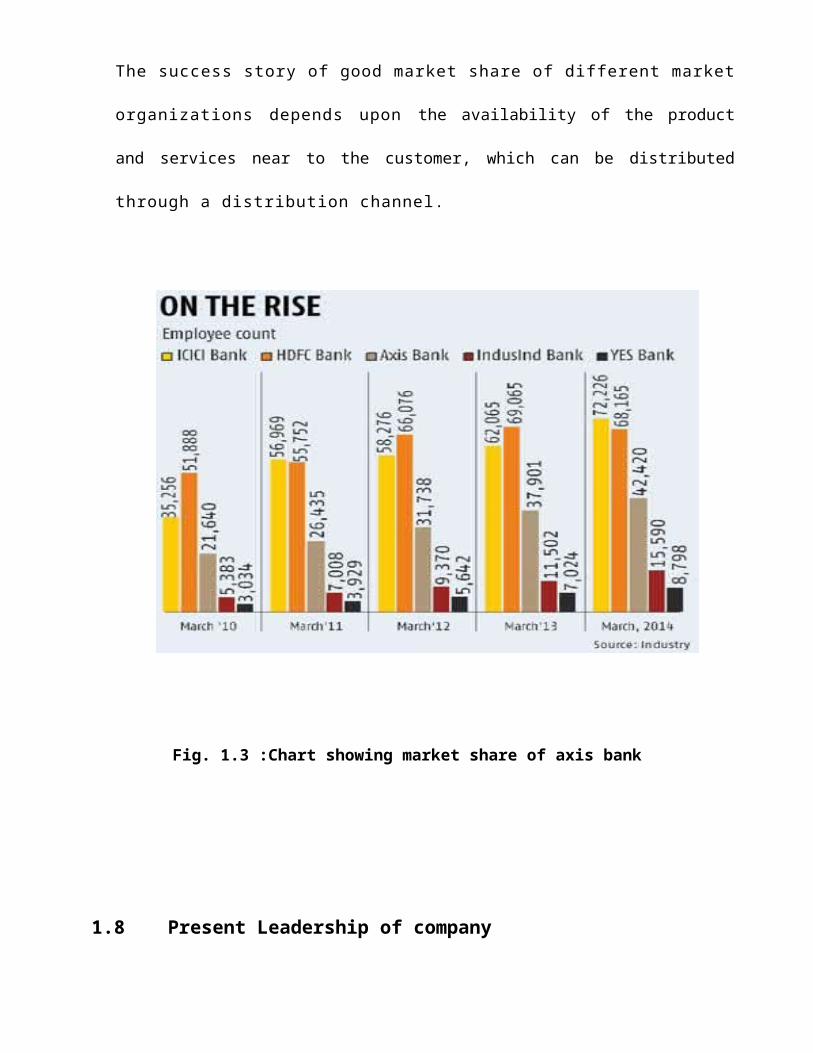

1.7 Market share and position of axis bank

Axis Bank is one of the Top three banks in India along with State Bank Of India, HDFC Bank

and ICICI Bank.Axis Bank has emergedas the best large private bank because of good asset

quality, high loan growth, and an improvement in returns on capital employed.

The success story of good market share of different market organizations depends

upon the availability of the product and services near to the customer, which can be distributed

through a distribution channel.

Fig. 1.3 :Chart showing market share of axis bank

1.8Present Leadership of company

Name Designation

Dr. SanjivMisra Chairman

Mrs. Shikha Sharma Managing Director & Chief Executive Officer

Mr. K.N. Prithviraj Director

Mr. V.R. Kaundinya Director

Mr. S.B. Mathur Director

Mr. Prasad Menon Director

Mr. Rabindranath Bhattacharya Director

Prof. Samir K. Barua Director

Mr. Som Mittal Director

Mrs. IreenaVittal Director

Mr. RohitBaghat Director

Smt. UshaSangwan Director

Mr. V. Srinivasan Executive Director, Corporate Banking

Mr. SomnathSengupta Executive Director, Corporate Center

Mr. R.K. Bammi Executive Director, Retail Banking

Fig. 1.4 :Present Leaders of axis bank

Present leader of axis bank

Mr. ArunBahri. (Branch Head)

Mrs. ShaliniAggarwal (Operation Head)

Mr. TarunRehan (Branch Sales Manager)

Mr. Rahul Kumar (Assistant Sales Manager)

Mr. Sunil kumar (operation Manager)

Mr. Amit Kumar (Assistant Sales Manager)

Mr. Deepak Jaiprakash (Assistant Manager Operations)

1.9Source of Data Collection

The data which is provided has been drawn from various sources ,so that we are able to

complete the report with correct information. The information has been drawn from various

sources as :

Primary Data :

A well structuredquestionaire was personally administered to the selected sample to collect

the primary data.

Secondary Data :

Secondary data are those which have already been collected by some other person for their

purpose & published. Secondary data are usually in shape of finised products.

Chapter- 2

SWOT ANALYSIS

2.1 SWOT Analysis

Table No-2.1: SWOT Analysis

STRENGTH

i. Unique products

ii. Brand name

iii. Customer loyalty

iv. Good services

v. Technology

WEAKNESS

i. Less advertisement

ii. Online presence.

iii. Weak management.

iv. Investment in research and

development

v. Tax structure.

THREAT

i. Competition from HDFC,

ICICI.

ii. Competition from public

banks.

iii. New markets and technology.

iv. International expansion.

v. Loosening regulations

OPPORTUNITY

i. Intense competitor.

ii. By providing proper schemes

axis can increase its

customers.

iii. Political risk.

iv. Substitute products

SWOT analysis is a tool for auditing an organization and its environment. It is the first

stage of planning and helps marketers to focus on key issues. SWOT stands for strengths,

weaknesses, opportunities, and threats. Strengths and weaknesses are internal factors.

Opportunities and threats are external factors.

The SWOT Matrix

A firm should not necessarily pursue the more lucrative opportunities. Rather, it may

have a better chance at developing a competitive advantage by identifying a fit between

the firm's strengths and upcoming opportunities. In some cases, the firm can overcome a

weakness in order to prepare itself to pursue a compelling opportunity.

To develop strategies that take into account the SWOT profile, a matrix of these factors

can be constructed. The SWOT matrix (also known as a TOWS Matrix) is shown below:

SWOT / TOWS Matrix

Strengths Weaknesses

Opportunities S-O strategies W-O strategies

Threats S-T strategies W-T strategies

S-O strategies pursue opportunities that are a good fit to the company's strengths.

W-O strategies overcome weaknesses to pursue opportunities.

S-T strategies identify ways that the firm can use its strengths to reduce its vulnerability

to external threats.

W-T strategies establish a defensive plan to prevent the firm's weaknesses from making it

highly susceptible to external threats.

2.11 Strengths

a. Axis bank has been given rating as one of the top three position in terms of fastest growth in

private sector banks.

b. Financial express has given number two position and BT-KPMG has rated Axis bank as the

best bank with some 26 parameters.

c. The bank has a network of 1.787 domestic branches and 10.363 ATMs

d. The bank has its presence in 971 cities and towns.

e. The bank financial positions grows at a rate of 20% every year which is a major positive

sign for any bank.

f. The company’s net profit is Q3FY12 is 1,102.27 which has a increase of 25.19%growth

compared to 2011.

2.12Weakness

a. Gaps- majority they concentrated in cooperate, wholesale banking, treasury service, retail

banking.

b. Foreign branches constitute only 8% of total assets.

c. Very recently the bank started focusing its attention towards personal banking and rural areas.

d. There share rates of Axis bank is constantly fluctuating in higher margins which makes

investors in an uncomfortable positions most of the time.

e.There are lot of financial product gaps in terms of performance as well as reaching out of the

customers.

2.13 Opportunities

a. Acquisitions to fill gap.

b. 2009, alliance with motilaloswal for online trading for 10 million customers.

c. In 2010,acquiredEnam securities Pvt ltd – broking and investment banking.

d. In sep 2009, SEBI approval axis assets management co. for mutual fund business.

e. No. of e-transactions increased from 0.7 million to around 2 million.

f. Geographical expansion to rural market-80% of them have no access to formal lending.

g. 46% use informal lending channels.

h. 24% unregulated money lenders.

i. Now number of branches increased to 1787.

j. Last quarter there were 48 new branches opened across the nation.

k.The assets in their international operations are growing at a very faster pace with a growth

rate of 9%.

l. The concept of ETM (everywhere teller machine)by axis bank had a good response in terms

of attracting new customers in personal segment.

2.14 Threats

a. Since 2009, RBI has increased CRR by 100 basic points.

b. Increased repo rate reverse repo rate by 50 points-11 times of late.

c. Increasing popularity of QIPs due to ease in fund raising.

d. RBI allowed foreign bank to invest up to 74% in indian banking.

e. Government schemes are most often serviced only by govern banks like SBI, Indian banks,

Punjab national bank etc.

f. ICICI and HDFC are imposing strong threats in terms of their expansion in customers basic

by their aggressive marketing strategies.

2.2 Best Practices in various Fields

2.21 HR Practices

Employees at axis bank believe that a fun filled and friendly work environment helps

reduce stress and creates a healthy bond between colleagues. We strive to ensure that our

employees unwind themselves from time to time, have a hearty laugh amidst the work-

pressure which is always a great reliever in stress and a motivator in challenging

conditions.

Axis bank care about their employees and keenly collect feedback to learn first-hand

about their daily experience at work. We aim to be a preferred employer, and hence we

have transparent processes in place to ensure that our employees can have their say.

To achieve this we have periodic employee satisfaction surveys requesting for feedback

and input from our employees to find out whether we're delivering a work experience that

optimizes employee performance and engagement.

It is also important to motivate employees to focus on customer success; profitable

growth and the company well-being. Axis bankprovide all those benefits to their

employees for their motivation. Axis bank listen to employees and making them feel

involved will create loyalty, in turn reducing turnover allowing for growth

2.22 Marketing Practices

Work with Companies

By partnering with companies, you will have access to an audience of employees who

might be interested in your product. Speak with local companies and schedule a time to

hold a seminar about life insurance where you can explain the benefits, costs and

complexities in a relaxed setting with people who have opted to be there. As you search

for companies, look for businesses who have older executives in industries with high

compensation rates; employees in this type of business will be more likely to be able to

afford life insurance, as opposed to a younger, lower-income people. Older, wealthier

professionals may also be more concerned with protecting their wealth and their families

in case of death or emergency.

Chapter-3

DATA COLLECTION & PRESENTATION

3.1 Marketing

3.11. Product Planning Process

Axis bank plans and improves its product:

a. Conducting initial survey of the product (plan and price) to check on the acceptability of the

product.

b. It insisted on minimum no. of lives to be covered as pricing to be based on the same and to

make the product sustainable

3.12 Pricing Policies/Strategies

Axis bank is using the competitive pricing strategies with respect to other banker. It gives

the best services to its customers at every facility so as to get the competitive edge over the

other banks.

3.13 Channel Planning and Management

Channel is the term used for the various approaches a company uses to tap its customers.

Axis bank uses a multi channel approach to ensure the service and other allied activities are

carried out in the most effective manner. The channels used by axis bank can be broadly

stated as under:

Retail: The Retail channel consists of sales executives, sales officers and agents. They are the

one who are in direct contact with the customers.

Online banking: axis bank has developed a web-based system to meet all the saving and

current account transaction. The Internet provides a secure medium for transferring funds

electronically between bank accounts, and also for making banking transaction over the

Internet. Credit cards transactions are a form of Internet Banking. banking is one form of

Home Banking.. With the do-it-yourself architecture, the online channel is fast,

convenient, and easy to understand and operate.

Table:3.1-No of branches

Name of bank No. of Branch

SBI 18324

HDFC 2564

ICICI 2760

AXIS 2160

Fig: 3.1- No. of branches

Year Reatil Amount

2009-10 20821

2010-11 27759

2011-12 37570

2012-13 53960

2013-14 74491

Table: 3.2-Reatil Assets

SBI HDFC ICICI AXIS0

2000400060008000

100001200014000160001800020000 18324

2564 27602160

No of Branches

No of Branches

Fig:3.2 Reatil Assets

3.14 Promotional Policies and their Effects on Sale

All areas and aspects involved with promoting a bank and product. Promotional policy is

sometimes equated with advertising, however advertising is only one part of a

promotional policy. Other important aspects of a promotional policy may include public

relations, consumer promotions, and any other area which increases awareness and

spreads the word about the item. Axis bank is focusing on all of the above promotional

activities. Axis bank is providing the Advertisement to promote its accounts and also

provide their customers a better Service which is another way to promote the activities.

3.15 CRM Policies

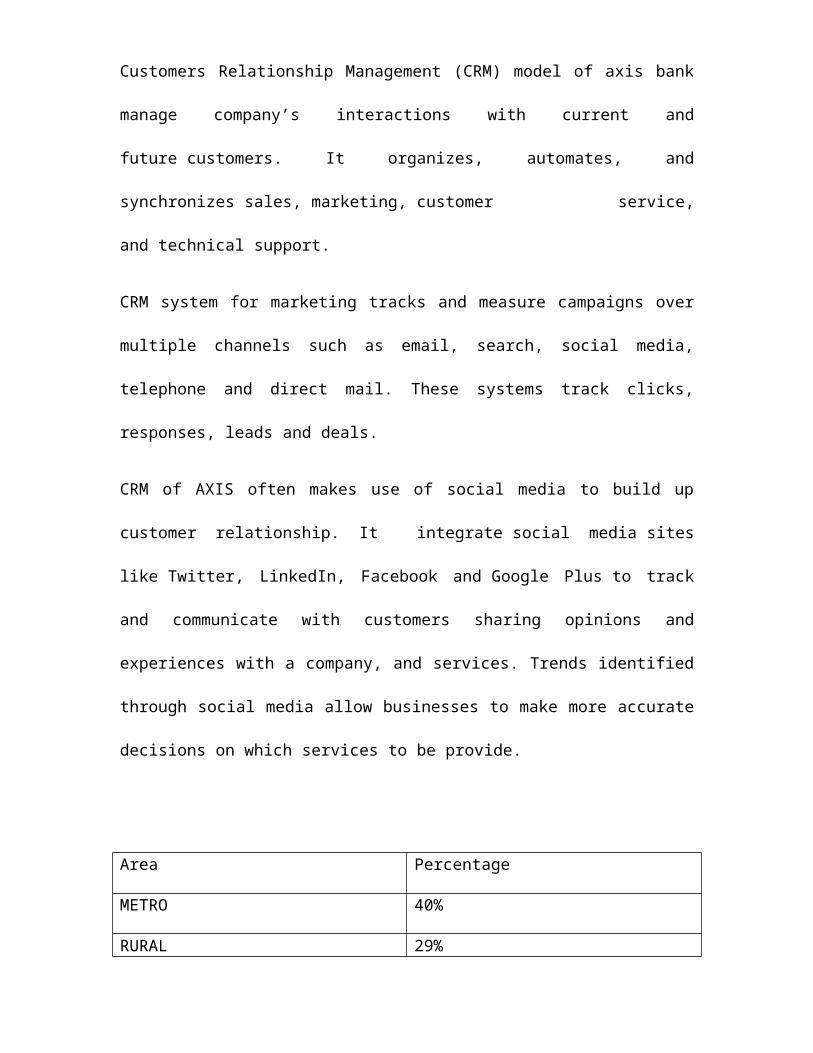

Customers Relationship Management (CRM) model of axis bank manage company’s

interactions with current and future customers. It organizes, automates, and

synchronizes sales, marketing, customer service, and technical support.

CRM system for marketing tracks and measure campaigns over multiple channels such as

email, search, social media, telephone and direct mail. These systems track clicks,

responses, leads and deals.

CRM of AXIS often makes use of social media to build up customer relationship. It

integrate social media sites like Twitter, LinkedIn, Facebook and Google Plus to track

and communicate with customers sharing opinions and experiences with a company, and

services. Trends identified through social media allow businesses to make more accurate

decisions on which services to be provide.

Area Percentage

METRO 40%

RURAL 29%

SEMI URBAN 13%

URBAN 18%

Table:3.3-Customer Relation

Rural29%

Semi Urban13%

Urban18%

Metro39%

Customer Relation

Fig:3.3 Customer Relation

3.17 Advertisement Process

An integral part of marketing, advertisements are public notices designed to inform and

motivate. Their objective is to change the thinking pattern (or buying behaviour) of the

recipient, so that he or she is persuaded to take the action desired by the advertiser. When

aired on radio or television, an advertisement is called a commercial. According to the

Canadian-US advertising pioneer, John E. Kennedy (1864-1928), an advertisement is

“salesmanship in print.”

Axis Bank,a private sector bank, has announced the launch of the third phase of its

advertising campaign around its brand philosophy of ‘Badhtikanaamzindagi…’ or

‘Progress On’. The campaign conceptualised by Lowe Lintas and Partners features the

bank’s brand ambassador DeepikaPaudukone.

The film opens at a press conference. Padukone walks into the room and the journalists

try to gain her attention to ask her questions. She takes a seat on the stage and points put

to a particular reporter to ask a question. The reporter asks her how she felt about her

association with Axis Bank. She replies that she feels that she is progressing in life. She

then looks on to the Axis Bank branding on the stage and mentions

‘Badhtikanaamzindagi’. She then asks for the reporters to ask another question and the

TVC ends with a super saying- ‘To be continued...’

On the campaign, Rajiv Anand, president, retail banking, Axis Bank, said, “The new film

takes our brand positioning of Badhtikanaamzindagi ahead. The campaign is based on the

insight that Progress means different things to different people and can also be defined

differently for the same individual at different times. This insight is captured in our new

communication which brings to life the ubiquitous and multidimensional nature of

progress.”

ArunIyer, national creative director, Lowe Lintas and Partners, said,

‘BadhtikaNaamZindagi’ or 'Progress on' is the essence of brand Axis. In our earlier

campaigns we have explored this philosophy from various angles, be it an individual’s

progress or the progress of the collective. The objective this year was to explore a new

dimension of progress while showcasing the range of products, which brings us to the

idea behind the campaign ‘Progress has many meanings’. It is not just material but also

emotional and personal. While growing monetarily is important but it is also important to

have value-system in place and that’s the whole thinking behind the philosophy of

‘BadhtikaNaamZindagi’.”

3.2. Human Resource Management

3.21 HR Planning

Human resources planning of AXIS bank follows the process of assessing the manpower

requirement for future period of time. It attempts to provide sufficient manpower required

to perform organizational activities. HR planning is a continuous process in axis bank

which starts with identification of HR objectives, move through analysis of manpower

resources and ends at appraisal of HR planning. Following are the major steps involved

in human resource planning

a. Assessing Human Resource: The assessment of HR in axis bank begins with

environmental analysis, under which the external (PEST) and internal (objectives,

resources and structure) are analysed to assess the currently available HR inventory level.

After the analysis of external and internal forces of the organization, HR manager of axis

bank find out the internal strengths as well as weakness of the organization in one hand

and opportunities and threats on the other.

b. Demand Forecasting: The HR manager of axis bank firstly determines the future

needs of HR in terms of quantity & quality. This is performed to determine the future

needs this is determined by analysing the future needs by the current number of

manpower present with the organization.

c. Supply Forecasting: After analysing the demand at axis bank the HR department

focuses on fulfilling these demand by internal sources like as promotion, transfer, job

enlargement and enrichment and also from external sources including recruitment of

fresh candidates who are capable of performing well in the organization.

3.22 Recruitment & Selection

a. Recruitment: Recruitment is the process of finding and hiring the best-qualified

candidate (from within or outside of an organization) for a job opening, in a timely and

cost effective manner.

Sources of recruitment in AXIS bank

Before axis actively begins to recruit applicants it should consider the mostly likely

source of the type of employee it needs. Some companies try to develop new sources

while most try to tackle the existing sources they have. These sources accordingly may be

termed as internal and external.

1Internal Sources – This is one of the important sources of recruitment. The employees

who are already working in the outside.

Internal sources consist of the following :-

a. Present Employees

Promotions and transfers among the present employees can be a good source of internal

recruitment

b. Employee Referrals

In an organization with a large number of employees referrals can provide quite a large

pool of potential organizational members.

c . Former Employee

These are another internal source of recruitment. Some retired employees may be willing

to come back to work.

Previous Employee

Those who have previously applied for jobs can be contacted by mail.

2 External Sources: These are as follows –

a. Advertisement

b. . Professional Organization

c. Data Bank

d. Walk in

e. Recruiting Agencies

f. Competitor

g. Displaced Person

h. E-recruitment

b. Selection:AXIS bank undergoes selection process by interviewing and evaluating

candidates for a specific job and selecting an individual for employment based on certain

criteria. Employee selection can range from a very simple process to a very complicated

process depending on the firm hiring and the position. Certain employment laws such as

anti-discrimination laws are obeyed during employee selection.

Steps in Scientific Selection Procedure of AXIS bank:

1. Job analysis: The worth of job is analyzed acc. to its priority.

2. Recruitment : In this the candidates are invited to present their details.

3. Application form : The information of candidate is duly filled.

4. Written examination : A written exam is conducted.

5. Preliminary interview : Interviews about conducted of shortlisted candidates.

6. Tests : The final test for job is decided.

7. Medical examination: Medical fitness of candidate is checked thorougly.

8. Reference checks : The reference given are cross checked to remove falsified

information.

9. Line managers decision: The line manager lately decide to recruit.

Table: 3.4 Recruitment process of axis bank

3.23 Training, Performance Appraisal

a. Training and Development: axis bank believes in adding value to its human capital

through various programs, viz. induction program, product training, e-learning modules

and other functional training programs. The aim of these trainings is to enhance the skills

axis bank induction schedule for all new joiners. Talent identification and grooming

programs.Grooming and etiquettes programs.Role change programs and executive

5. Job Offer

4. Reply Letter

3. Capability Based Interviews

2. Ability Test

Recruitment Process

1. CV Submission

development programs. Formal classes are organized to train the employees. The

development programs are also organized like on job training, off job training &

improvement chances provided to the employees.

b. Performance Appraisal: Performance appraisals serve as an opportunity for two-way

discussion between managers and employees as well as a chance to review

accomplishments and set business objectives and goals.

Methods of Performance Appraisal at axis bank:

1. Assessment center :In this individual from departments are brought to spend two

or three days working on an individual or group observers rank the performance

of each and every participant in order of merit.

2. .Human Resource Accounting :

Human resource accounting deals with the cost of contribution of human resources to the

organization. Organization cost of the employees includes costs of manpower planning,

recruitment, selection induction, placement, training development, ages and benefits etc.

employee contribution is the money value of employee service, which can be measured

by labor productivity or value added by human resources.

c. Internal Career Opportunities: The Company believes in flexibility and having the right

person for the right job. An employee can apply for other positions within the company

internally thereby having an opportunity to grow in the field he is best suited.

3.24 HR Policies and Practice

Axis bank believes in a progressive human resource philosophy that turns human capital

into a key source of competitive advantage. The capability and motivation level of

employees is a key determinant in success of any service-oriented organization. The bank

has people from diverse backgrounds including banking, financial services, consumer

goods, telecom, automotive engineering etc.

3.25 HR Philosophy:

Quality is an integral part of axis bank well-defined and dynamic Human Resource (HR)

policy. The company follows a strong value system which is driven by result orientation,

adaptability to change, humility and respect for colleagues and peers. It believes that

investment in human capital is the key source of competitive advantage and sustained

growth. Its constant endeavor is to create and maintain a performance driven work culture

focusing on employee satisfaction and retention. With attractive compensation packages,

positive and productive work environment and challenging assignments and opportunities

across the world, axis bank is committed to being the employer of choice wherever it

operates. The company not only wants to attract and retain the very best of professionals,

but also wants them to be partners in progressive growth.

3.3 Production & Operations

3.31 Planning the Story:

In this, the bank focuses on the potential customers who are seeking to have investment in any

form or willing to save their money for a long period of time. Firstly those peoples are

approached by agents those main motive for investing.

3.32 Gathering the Information:

In this, the information about the Clint is gathered & then focus about the future aspects,

in this the repayment capacity of the client & the Potential plans about the consumer is

analyzed and the platform for opening account is prepared.

3.33 Setting up the Platform:

In this, the whole platform is prepared by making client clear about the account

information plan & giving him information's about various kind of account.

3.34 Quality Control:

The quality of whole process is maintained by the organization by making a fair promise

with its consumers, to maintain the trust of the potential customers as well as current

customers. In this the grievances among the company & customer is resolved out. The

various aspects are also used to resolve out the problems of employees as well as

consumers by providing values to them.

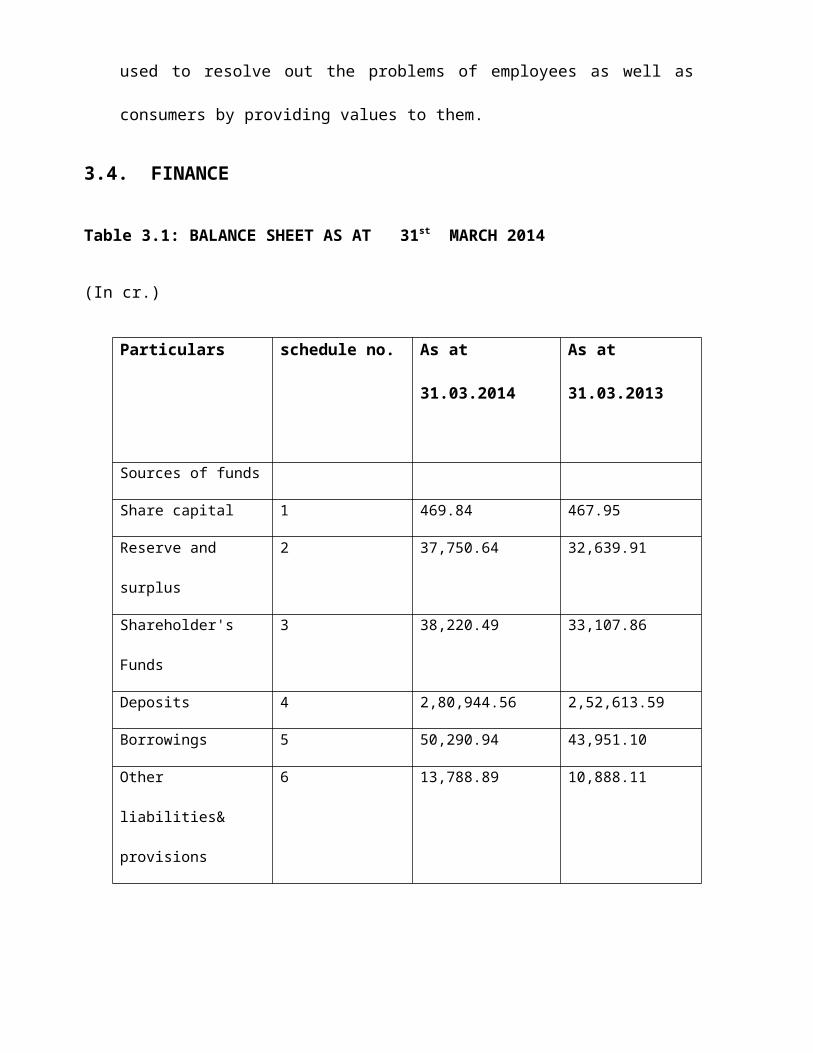

3.4. FINANCE

Table 3.1: BALANCE SHEET AS AT 31st MARCH 2014

(In cr.)

Particulars schedule no. As at 31.03.2014 As at 31.03.2013

Sources of funds

Share capital 1 469.84 467.95

Reserve and surplus 2 37,750.64 32,639.91

Shareholder's Funds 3 38,220.49 33,107.86

Deposits 4 2,80,944.56 2,52,613.59

Borrowings 5 50,290.94 43,951.10

Other liabilities& 6 13,788.89 10,888.11

provisions

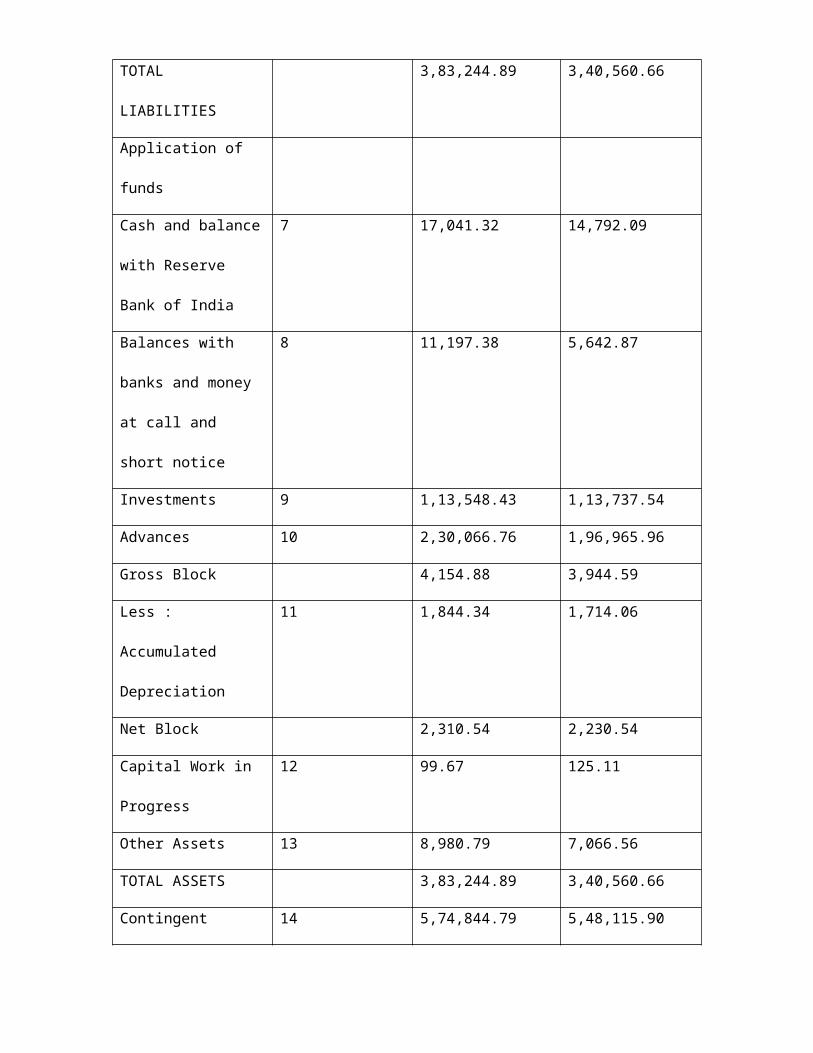

TOTAL LIABILITIES 3,83,244.89 3,40,560.66

Application of funds

Cash and balance with

Reserve Bank of India

7 17,041.32 14,792.09

Balances with banks and

money at call and short

notice

8 11,197.38 5,642.87

Investments 9 1,13,548.43 1,13,737.54

Advances 10 2,30,066.76 1,96,965.96

Gross Block 4,154.88 3,944.59

Less : Accumulated

Depreciation

11 1,844.34 1,714.06

Net Block 2,310.54 2,230.54

Capital Work in

Progress

12 99.67 125.11

Other Assets 13 8,980.79 7,066.56

TOTAL ASSETS 3,83,244.89 3,40,560.66

Contingent Liability 14 5,74,844.79 5,48,115.90

Bills for collection 15 36,601.58 27,894.88

Table 3.2: Profit & Loss Account:

(IN CRORES)

PARTICULARS YEAR ENDED

31.03.2014

YEAR ENDED

31.03.2013

Income

Interest Earned 30,641.16 27,182.57

Other Income 7,405.22 6,551.11

Total Income 38,046.38 33,733.68

Expenditure

Interest expended 18,689.52 17,516.31

Employee Cost 2,601.35 2,376.98

Selling and Admin Expenses 0.00 0.00

Depreciation 363.93 351.73

Miscellaneous Expenses 10,173.91 8,309.22

Preoperative ExpCapitalised 0.00 0.00

Operating Expenses 7,900.77 6,914.23

Provisions & Contingencies 5,238.42 4,123.70

Total Expenses 31,828.71 28,554.24

Net Profit for the Year 6,217.67 5,179.43

Extraordionary Items 0.00 0.00

Profit brought forward 10,029.26 7,329.45

Total 16,246.93 12,508.88

Preference Dividend 0.00 0.00

Equity Dividend 939.69 843.86

Corporate Dividend Tax 161.44 143.37

Per share data (annualized)

Earning Per Share (Rs) 132.33 110.68

Equity Dividend (%) 200.00 180.00

Book Value (Rs) 813.47 707.50

Appropriations

Transfer to Statutory Reserves 1,644.36 1,392.38

Transfer to Other Reserves -0.01 0.01

Proposed Dividend/Transfer to

Govt

1,101.13 987.23

Balance c/f to Balance Sheet 13,501.45 10,029

Total 16,246.93 12,508.88

Table 3.3 CASH FLOW STATEMENT

(In thousand)

PARTICULARS YEAR ENDED

31.03.2014

YEAR ENDED

31.03.2013

CASH FLOW FROM

OPERATING

ACTIVITIES

NET PROFIT BEFORE

TAX

93,486,266 75,526,929

ADJUSTMENTS FOR:

Depreciation on fixed assets 3,639,307 3,517,343

Depreciation on investments (1,002,934) (1,039,359)

Amortisation of premium on

Held to Maturity

investments

741,629 674,599

Provision for Non

Performing Assets

(including bad debts)

12,959,797 11,792,245

Provision on standard assets 2,902,257 1,966,686

Provision for wealth tax 4,200 3,800

(Profit)/Loss on sale of fixed

assets (net)

142,344 44,662

Provision for country risk - (96,300)

Provision for restructured

assets

1,947,624 1,039,492

Provision for other

contingencies

4,263,632 3,837,828

119,084,122 97,267,925

Adjustments for

(Increase)/Decrease in

investments

139,416,485 (95,527,142)

(Increase)/Decrease in

advances

(344,886,856) (284,769,149)

Increase/(Decrease) in

deposits

283,309,768 325,092,849

(Increase)/Decrease in other

assets

(15,824,833) (3,340,140)

increase/(Decrease) in other

liabilities & provisions

20,351,130 14,760,950

Direct taxes paid (34,424,254) (26,294,900)

Net cash flow from

operating activities

167,025,562 27,190,393

Cash flow from investing

activities

Purchase of fixed assets (5,894,258) (4,718,705)

(Increase)/Decrease in Held

to Maturity investments

(131,899,049) (109,099,212)

(Increase)/Decrease in

Investment in Subsidiaries

(6,378,202) (718,875)

Proceeds from sale of fixed

assets

1,686,699 193,531

Proceeds from transfer of net

assets acquired under

demerger to subsidiary

- 2,741,502

Net cash used in investing

activities

(142,474,810) (111,601,759)

Cash flow from financing

activities

Proceeds from issue of

subordinated debt, perpetual

debt & upper Tier II

instruments (net of

repayment)

(1,341,919) 19,654,731

Increase/(Decrease) in

borrowings (excluding

subordinated debt,

perpetual debt & upper Tier

II instruments)

64,740,359 79,139,533

Proceeds from issue of share

capital

18,901 426,605

Proceeds from share

premium (net of share issue

expenses)

1,356,819 56,227,263

Payment of dividend (9,872,689) (7,702,164)

Net cash generated from

financing activities

54,901,471 147,745,968

Effect of exchange

fluctuation translation

(1,414,876) 1,675,840

reserve

Net increase in cash and cash

equivalents

78,037,347 65,010,442

Cash and cash equivalents at

the beginning of the year

204,349,599 139,339,157

Cash and cash equivalents at

the end of the year

282,386,946 204,349,599

Notes to the Cash Flow

Statement

Cash and cash equivalents

includes the following

Cash and Balances with

Reserve Bank of India

170, 413,196 147,920,883

Balances with Banks and

Money at Call and Short

Notice

111,973,750 56,428,716

Cash and cash equivalents at

the end of the year

282,386,946 204,349,599

Name of Bank Net Profit(%)

ICICI 51%

Axis 20%

HDFC 19%

CITI 10%

Table: 3.5 Net Profit

51%

20%

19%

10%

NET PROFITICICI Axis HDFC CITI

Fig: 3.4 Net Profit

3.5 USES OF IT & INFRASTRUCTURE

3.51 Technology: Growth without technological advancement is not possible. axis is

incorporating new technology within the organization to help the organization grow. It is

integrating technology with business processes and trying to create a business process

which is totally integrated so that they can handle any amount of work.

Axis bank has effectively used Information Technology to meet growing customer needs

while improving operational efficiency and profitability. The Company’s IT strategy,

architecture and successful deployment form the backbone of its business.

a. Staying ahead in IT infrastructure through:

1. Online Manager: A web-based interface that allows a customer to update with their

account, transfer of money, payment of various bills.

2. Using SMS technology to deliver timely alerts and reminders to keep customers

informed of various transactions.

3. Using intranet effectively to enhance employee productivity and simplify human

resource functions.

4. The only bank to provide digitally signed documents through the online interface.

3.52 Mobile Application: Driven by its customer centric approach, axis bank launched

mobile application - “axis”. The application is an extremely interactive and useful tool for

customers to transfer money, transaction purpose.

\

Chapter-4

FUNCTIONAL ANALYSIS

4.1 Marketing

a. Axis Bank inducts Schroders as a 25% partner in Axis AMC.

b. Axis bank ranked no. 1bank in india in both primary and secondary market of

cooperate bonds.The asset benchmark research.

c. Axis bank ranked No.1 in Asia in the IT Biz Award- large enterprises category by

express IT awards.

d. Axis bank voted for most trusted private sector bank in the country in the trusted

brands survey.

e. To deliver a great customer experience consistently across all touch points a service

transformation initiative.

4.2 Human Resources Management

a. Axis bank adopted innovative strategies to dig deeper into the market’s alternate talent

pools and make them insurance-ready.

b. The Company’s T&D team designs and conducts different types of programs.

Such as induction, product training, insurance training, and regulatory training, to

employees at all levels in the company and distributors as well.

c. Axis bank aims to contribute to improving and enhancing the quality of life of

communities in which the company operates thereby helping to create an equitable

society.

d .Axis bank, to acknowledge the employees timely for imbibing the organization’s

values, excelling in performance and putting in extra efforts to help achieve the

Company’s goals.

e. They communicate internally through platforms, like CEO Confluence, CEO Blogs,

Coffee with Leadership and so on. Use of different modes helps foster a culture of open

communication

4.3 Information & Technology

a. This online form, with its dynamic questions, helps to gather all relevant customer

information in one go in a hassle-free manner.

b. This information is processed real-time by an intelligent rule engine-enabling virtual

underwriting decisions within minutes in the customer’s living room

c. To improve work environment flexibility, virtual desktops have been deployed in top

80 branches.

4.4 Finance

a. The Bank continued to deliver a steady growth in both business and earnings, in the

midst of a moderation in economic growth and intensifying competitive financial

landscape. The Bank reported a net profit of `6,217.67 crores for the year ended

31st March 2014, registering a growth of 20.05% over the net profit of `5,179.43 crores

last year.

b. The Bank’s total income increased by 12.78% to reach `38,046.38 crores as compared

to `33,733.68 crores last year.

c.Operating revenue over the same period increased by 19.36% to `19,356.86 crores while

operating profit increased by 23.14% to `11,456.09 crores

d. The growth in earnings wasmainly due to a strong growth in net interest income

e.The operating expenses grew at a slower pace by 14.27% to `7,900.77 crores from

`6,914.24 crores last year.

4.5 Porter’s Model

Fig:4.1-Porter’s model

Compared to many other industries, the intensity of rivalry among developers in

residential development is relatively low. The area where it is felt most is in competition

for development land. When it comes to selling end units, developers typically try to

avoid competing directly by:

a. Developing products in different markets\locations

b. Launching products at different time periods

c. Differentiating product types

Threats of New Entrants

When industry has over 60,000 registered participants, it is hard to conclude that barriers

to entry are high. Although the number of entrants varies over time and according to

market conditions, they are sufficiently low relative to other industries that new entrants

can continue to enter and eventually push above average returns back to historical means.

The potential barriers to entry for any industry fall into several broad categories :

a. Capital

b. Technology

c. Legal Authorization

d. Expertise and Know-How

Legal Authorization is necessary for certain types of industries such as telecoms and

utilities. The number of participants in this industry is limited due to the nature of the

businesses or the return profiles.

The technological and expertise\know-how component of this industry is not particularly

high. Designs, names and concepts can all be copied as there is less ability to protect

these through patents or copyrights. Large value supply chains such as agents,

consultants, property managers and employees of rivals can all be hired or co-opted.

Capital can be considered as a barrier but mostly to larger scale projects. The gross

amount of capital needed to “enter” the industry is paltry compared to the likes of steel

mills or chip fabs.

Real estate development involves different types of products: residential, office, retail

and industrial being the most common. Economies of scale mean larger firms can

produce at lower cost per unit. This tends to lower the number of firms in the industry

and reduce competition. Proprietary product differences are the characteristics that make

a product appeal to a large market segment. But only those characteristics that cannot be

copied at low cost by competitors (“proprietary”) will be a barrier to entry. Brand identity

is the extent to which buyers take the brand name into account when making purchase

decisions. Capital requirements are the total cost of acquiring the plant and equipment

necessary to begin operating in the industry.

Bargaining Power of Suppliers

Overall, developers are in a favorable bargaining position relative to the key suppliers in

the industry. The 3 key suppliers to any residential developer are :

a. Land sellers

b. Construction contractors

c. Building materials and home furnishing

d. Capital providers

A typical developer’s bargaining position relative to a land seller varies according to :

e. Nature of seller

f. Location of sale

Developers typically prefer to buy land through direct bilateral negotiations with the

government or 3rd party rather than be involved in a multi-party bidding ware. Auctions

are the least desired channel for land acquisition but sometimes a necessity.

Differentiation of inputs means that different suppliers provide different input

characteristics for inputs that basically do the same job. The greater the degrees of

differentiation among suppliers the more bargaining power suppliers have. Presence [and

availability] of substitute inputs means the extent to which it is possible to switch to

another supplier for an input (or a close substitute). The greater the number and closeness

of substitute inputs the lower the bargaining power of suppliers.

Supplier concentration is the degree of competition among suppliers. Usually the more

concentrated the industry, the fewer suppliers and the more control suppliers have over

the prices they charge. Greater supplier concentration often means greater supplier

bargaining power.

Cost relative to total purchases in the industry refers to the amount your firm spends on

inputs from a particular supplier compared to the total revenue of all firms in the

supplier’s industry. Lower expenditure usually implies more bargaining power for the

supplier. The buyer’s bargaining power falls as spending with a particular firm falls

simply because the buyer’s business isn’t as important to the supplier.

Bargaining Power of Customers

If the bargaining power of customers is high, they influence the profitability of the

market by imposing their requirements in terms of price, service, and quality. Choosing

clients is crucial because a firm should avoid being in a situation of dependence. The

level of concentration of customers gives them more or less power. Generally their

bargaining power tends to be inversely proportional to that of the suppliers.

Buyer concentration versus firm concentration refers to the extent of concentration in the

buyer’s industry compared to the extent of concentration in your industry. The more

concentrated the buyer’s industry relative to your industry the greater the bargaining

power of buyers. Buyer volume is the number of units of your product the buyer

purchases from all sources. The greater buyer volume compared to the quantity

purchased from you, the greater the bargaining power of buyers.

Buyer information is the state of information buyers have about your industry. The more

information buyers have about your industry the more bargaining power buyers have.

Substitute products mean the number and closeness of substitutes available for your

product. The greater the number of available substitutes the more bargaining power

buyers has.

Chapter -5

SUMMARY AND CONCLUSIONS

5.1 Findings/Results

The Findings/Results of the study are:

a. Bank is having 853 branches all over the country.

b. The number of branches should be increased.

c. 50 % customer’s give the higher rating to AXIS Ban

d. Less no. of customers use mobile banking and net banking

e. The accounts of axis bank (both salary and saving) provide great flexibility in

terms of offering the accounts.

f. The accounts of axis band don’t have much difference in terms of features to

other bank but when it comes to service providing the axis bank gets an edge

because of their great customer service.

g. The bank has good relations with its customers. The customers are very satisfied

with the relationship manager service provided by bank.

h. The bank and its customers have a long term relationship. Axis bank has the

tendency to retain its customers at any cost. They believe that the old customer is

more profitable instead of a new one that’s why they try to maintain good and long

term relations to their customers

5.2 Lesson Learnt

My Internship in axis bank started on 12th June 2014. I grabbed the opportunity to meet

different people from diverse backgrounds and occupations to discuss on bank related

topics. Working in axis bank has helped me to gain lots of experience in the each field.

The main contribution of an employee to its organization is to perform its responsibilities

given with 100% effort and honesty.

My major responsibility was to sell the product and analyze the performance of the

investment team by comparing the portfolio performance for the organization. For the

goodwill of the company I was always honest to tell all the facts and benefits of the

product to the customer and convince them for the right product that best suited them.

After login their forms I called them and do a formal call that whether they received their

documents or not and if some complication occurred with the document.

Investment department is performing very well and company is able to provide good

returns to the customers. I am very much satisfied with the level of work; I have done for

the company.

I have also flab information about how to deal with superiors & customers. This will help

me through our my professional carrier ahead. Various functional areas are also seen by

me and how they work accordingly.

5.2Suggestions

a. Number of Branches should be increased covering a wider area in various states.

b. A wide publicity to be given about the organization and its products through

various means of communications to keep growth moments.

c. More number of training and educational programmers should be included in Banks

schedule.

d. Developing a learning culture through continuous learning process.

e. axis bank is normally not using properly for the current account so its popularity

ratio is quite down. This bank normally using for the long term planning like saving

and FD.

a)

BIBLIOGRAPHY

Websites-

http:// www.google.co.in

http:// www.wikipedia.org

http://www.axisbank.com

http:// www.we-connect.axisb.com (Intranet site of Axis Bank)

http:// www.rbi.gov.in

Books-

Marketing Management –Philip Kotler,Keller,Koshy & Jha

Research Methodology-Dr. Deepak Chawla

Banking & You –Magazine

Inputs from my industry mentor Mr.Lav Kumar Mishra

Inputs from my faculty mentor Prof.Gajendra Sharma