final ppt ifp

TRANSCRIPT

8/3/2019 Final Ppt Ifp

http://slidepdf.com/reader/full/final-ppt-ifp 1/14

Presented By:Megha Moonka (10DF053)Preeti Singh (10DF054)Shilpa Duttaroy (10DF055)

8/3/2019 Final Ppt Ifp

http://slidepdf.com/reader/full/final-ppt-ifp 2/14

HEALTH CARE FINANCING IN INDIAHEALTH CARE FINANCING IN INDIA

The share of public financing in totalhealth care is just about 1% of GDP

compared to 2.8% in other developing

countries.Beneficiaries are both poor a/ w/ a well-

fed section of society.

Over 80% of the total health financing isprivate financing,much of which is out-of-

pocket payments (i.e. User charges) and

not any prepayment schemes.

8/3/2019 Final Ppt Ifp

http://slidepdf.com/reader/full/final-ppt-ifp 3/14

2004 US UK Mexico Brazil China IndiaLife expectancy

(avg. # of years)

77.4 78.3 72.6 71.4 72.5 64.0

# of Physicians

per 1,000 people

2.7 1.9 1.7 1.2 1.7 0.4

Healthcare spend

(USD per capita)

5,365 3,036 336 236 62 32

Healthcare spend

(% of GDP)

13.2 8.4 5.5 7.5 5.0 5.3

Health care spend in India is considerablyHealth care spend in India is considerably

lower than that in other countrieslower than that in other countries

8/3/2019 Final Ppt Ifp

http://slidepdf.com/reader/full/final-ppt-ifp 4/14

The proportion of insurance in health careThe proportion of insurance in health care

financing in India is extremely lowfinancing in India is extremely low

0%

100%

Source of finance Means of finance

86% from

out-of-

expenses

83% from

private

sector

spending

Health care financing in India 2002, %

8/3/2019 Final Ppt Ifp

http://slidepdf.com/reader/full/final-ppt-ifp 5/14

WHAT IS HEALTH INSURANCE?WHAT IS HEALTH INSURANCE?

SYSTEM OF ASSURANCE TO MAKECONTINGENCIES OF HEALTH CAREEXPENSES.

TO PROVIDE PROTECTION AGAINSTFINANCIAL LOSS BY UNFORSEENSICKNESS.

TO MEET COST OF GOOD MEDICALCARE.

RELIEVES ANXIETY AND TENSION.

8/3/2019 Final Ppt Ifp

http://slidepdf.com/reader/full/final-ppt-ifp 6/14

Origin of Health Insurance:Origin of Health Insurance:

International

1883 Bismarck- sickness benefit to workers.

1911 Lloyd George- National Health

Insurance Scheme to cover sickness

expense, medical relief, drugs &

compensation of wages lost, to improve

quality of life and improve industrialproduction.

J.F.Kimball: prepayment system of health

care.

8/3/2019 Final Ppt Ifp

http://slidepdf.com/reader/full/final-ppt-ifp 7/14

8/3/2019 Final Ppt Ifp

http://slidepdf.com/reader/full/final-ppt-ifp 8/14

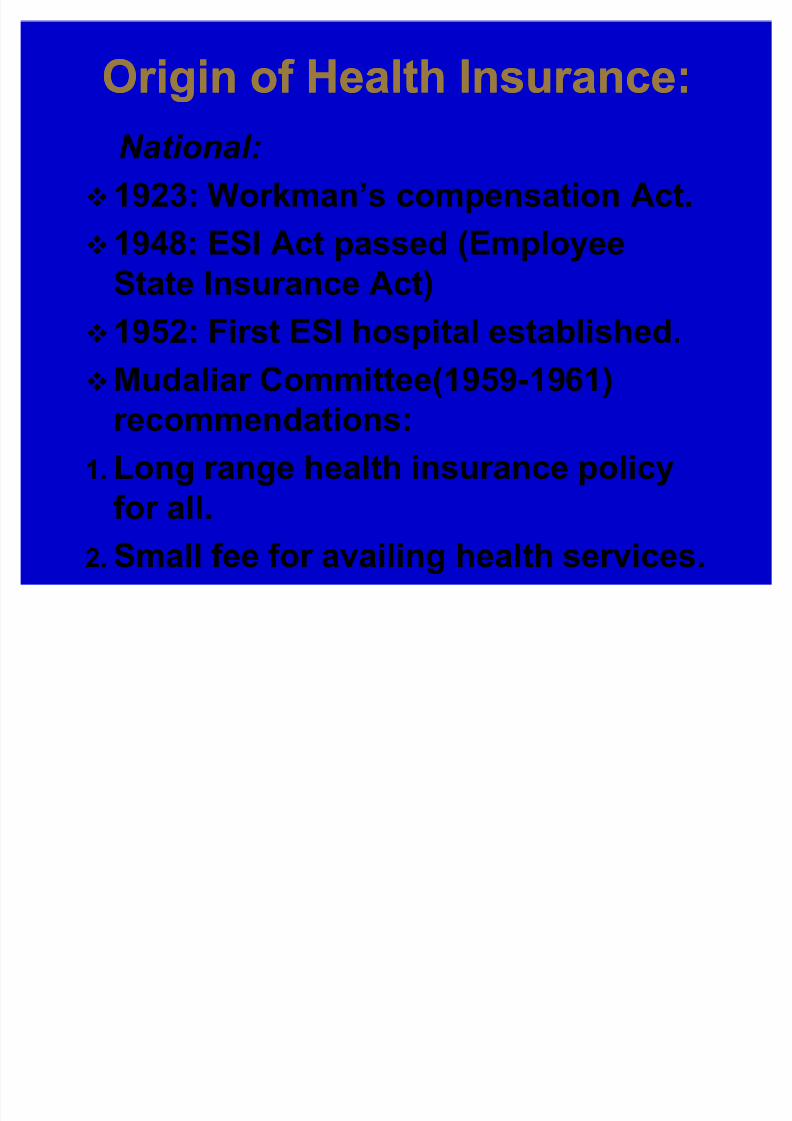

Origin of Health Insurance«contdOrigin of Health Insurance«contd

N ational:

1999: IRDA act passed. 2001: Insurance amendment Act:

Emphasis on TPAs.

8/3/2019 Final Ppt Ifp

http://slidepdf.com/reader/full/final-ppt-ifp 9/14

Forms of Insurance AvailableForms of Insurance Available

Indemnity Insurance: where theinsurer first pay to the hospital and

claim is made. E.g. Jeevan Asha II,

Asha Deep II, Mediclaim. Cashless Claim Facility:TPAs who

bear the expenses on behalf of

insurance company. Patients neednot to pay directly as a rule e.g.

Bajaj Alliance.

8/3/2019 Final Ppt Ifp

http://slidepdf.com/reader/full/final-ppt-ifp 10/14

The key issue related to financing of healthThe key issue related to financing of health

care in India revolves around the lack of care in India revolves around the lack of

adequate insurance . .adequate insurance . . ..

Limited coverage

± Only around 10% of the population is coveredthrough health financing schemes

± Geographic spread in terms of health carefacilities and financing awareness is limited

± Selection criteria by suppliers often restricts thepoor (and more likely to be ill) from affordablepre-payment schemes

M oral hazard and Adverse selection

± Claims ratios for Mediclaim and Jan Arogyapolicies have been in the range of 120 ± 130%.

8/3/2019 Final Ppt Ifp

http://slidepdf.com/reader/full/final-ppt-ifp 11/14

The key issue related to financing of healthThe key issue related to financing of health

care in India revolves around the lack of care in India revolves around the lack of

adequate insurance «adequate insurance « contdcontd

Sy stem leakages

± Provider malpractices leading to over-

charging or pre-selection / selectiverecommendation

Lack of universal schemes

± Limitations in terms of coverage of illnesses

as well as treatment options

± Alternative therapies often not considered /included under insurance

8/3/2019 Final Ppt Ifp

http://slidepdf.com/reader/full/final-ppt-ifp 12/14

Suggestions for the Growth of HealthSuggestions for the Growth of Health

Insurance in IndiaInsurance in India

Appropriate market segmentation, awareness

initiatives, product innovation, and incentives

Easing of entry norms for specialist health

insurance companies

Provider rating and credentialing

Centralized database for health insuranceexperience statistics

Efficient back-office support for underwriting

and claims processing

8/3/2019 Final Ppt Ifp

http://slidepdf.com/reader/full/final-ppt-ifp 13/14

ConclusionConclusion

Health insurance is an emerging important

financial tool in meeting health care needs

of the people of INDIA. CBHI is to be further explored so that the disadvantaged section

get maximum benefit.

In India at present no Pan-India Model of HI.All different forms need to be explored.

8/3/2019 Final Ppt Ifp

http://slidepdf.com/reader/full/final-ppt-ifp 14/14

THANK YOU !!!

14